Embed Size (px)

Citation preview

9-1

CHAPTER The Cost of Capital

Sources of capital Component costs WACC

9-2

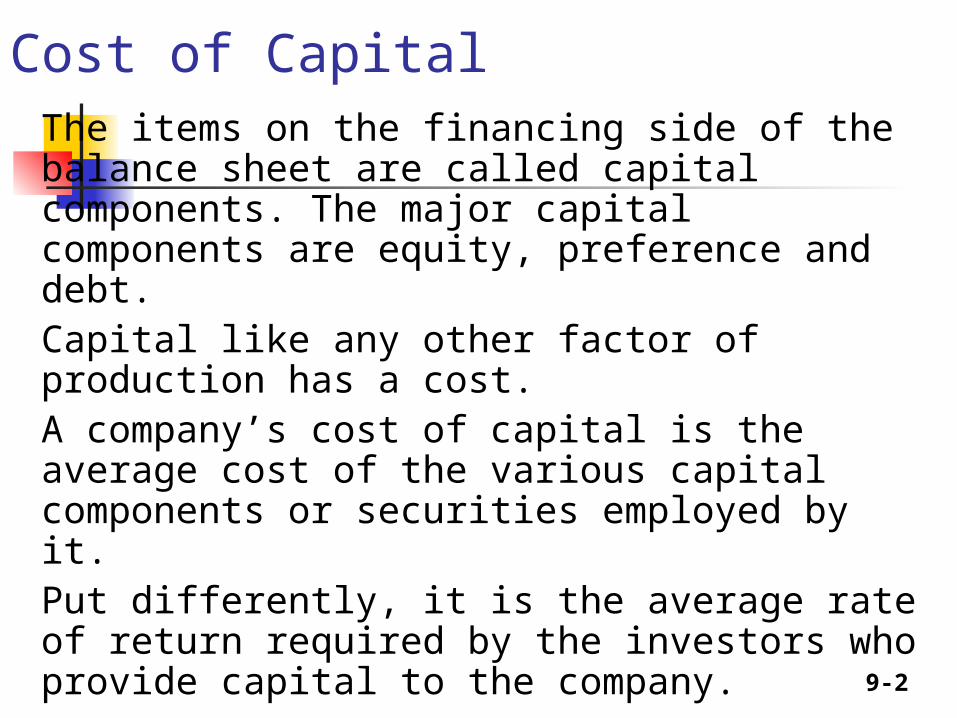

Cost of CapitalThe items on the financing side of the balance sheet are called capital components. The major capital components are equity, preference and debt. Capital like any other factor of production has a cost. A company’s cost of capital is the average cost of the various capital components or securities employed by it. Put differently, it is the average rate of return required by the investors who provide capital to the company.

9-3

Cost of Capital

Cost of the capital is the central concept in financial management. It is used for evaluating investment projects, for determining the capital structure, for assessing leasing proposal etc.

9-4

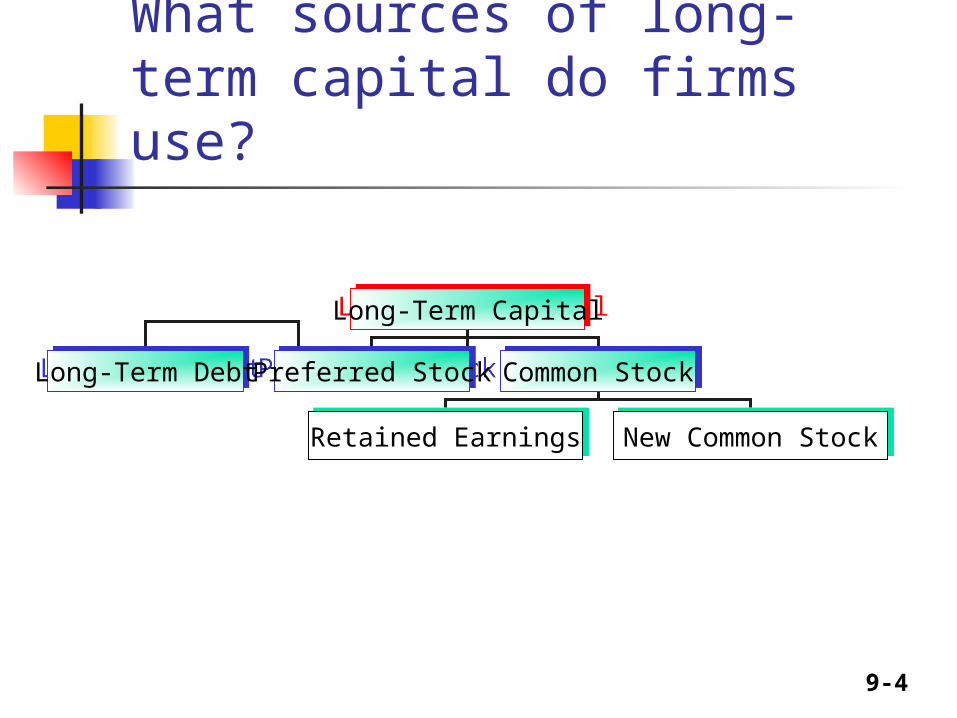

What sources of long-term capital do firms use?

Long-Term CapitalLong-Term Capital

Long-Term DebtLong-Term Debt Preferred StockPreferred Stock Common StockCommon Stock

Retained EarningsRetained Earnings New Common StockNew Common Stock

9-5

Concepts of weighted average cost of capital

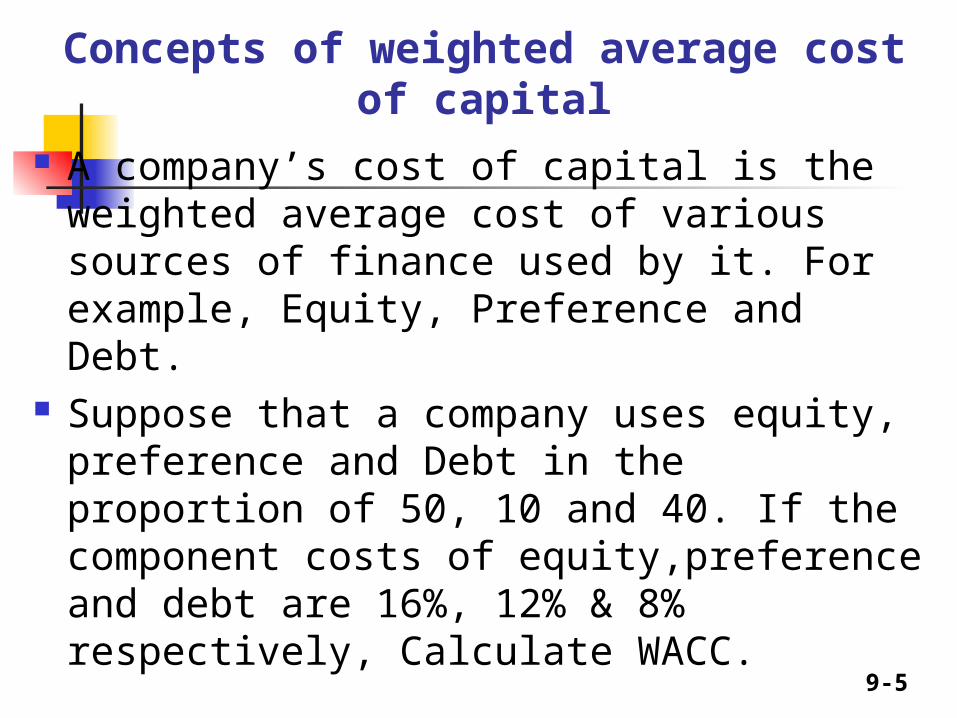

A company’s cost of capital is the weighted average cost of various sources of finance used by it. For example, Equity, Preference and Debt.

Suppose that a company uses equity, preference and Debt in the proportion of 50, 10 and 40. If the component costs of equity,preference and debt are 16%, 12% & 8% respectively, Calculate WACC.

9-6

Concepts of weighted average cost of capital

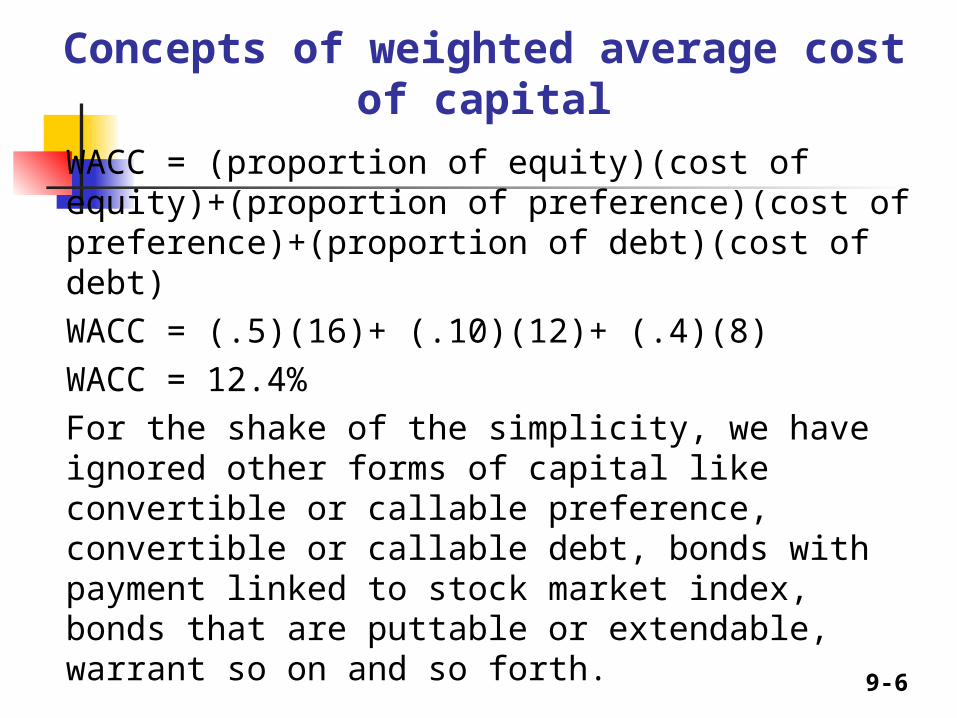

WACC = (proportion of equity)(cost of equity)+(proportion of preference)(cost of preference)+(proportion of debt)(cost of debt)WACC = (.5)(16)+ (.10)(12)+ (.4)(8)WACC = 12.4%For the shake of the simplicity, we have ignored other forms of capital like convertible or callable preference, convertible or callable debt, bonds with payment linked to stock market index, bonds that are puttable or extendable, warrant so on and so forth.

9-7

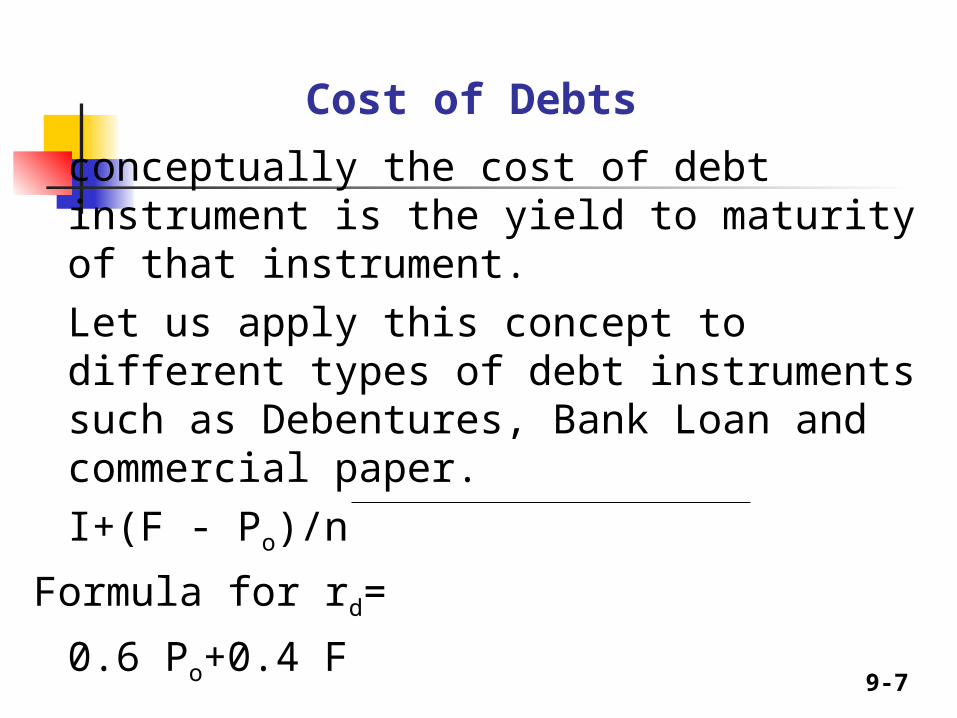

Cost of Debts

conceptually the cost of debt instrument is the yield to maturity of that instrument. Let us apply this concept to different types of debt instruments such as Debentures, Bank Loan and commercial paper.

I+(F - Po)/n

Formula for rd=

0.6 Po+0.4 F

9-8

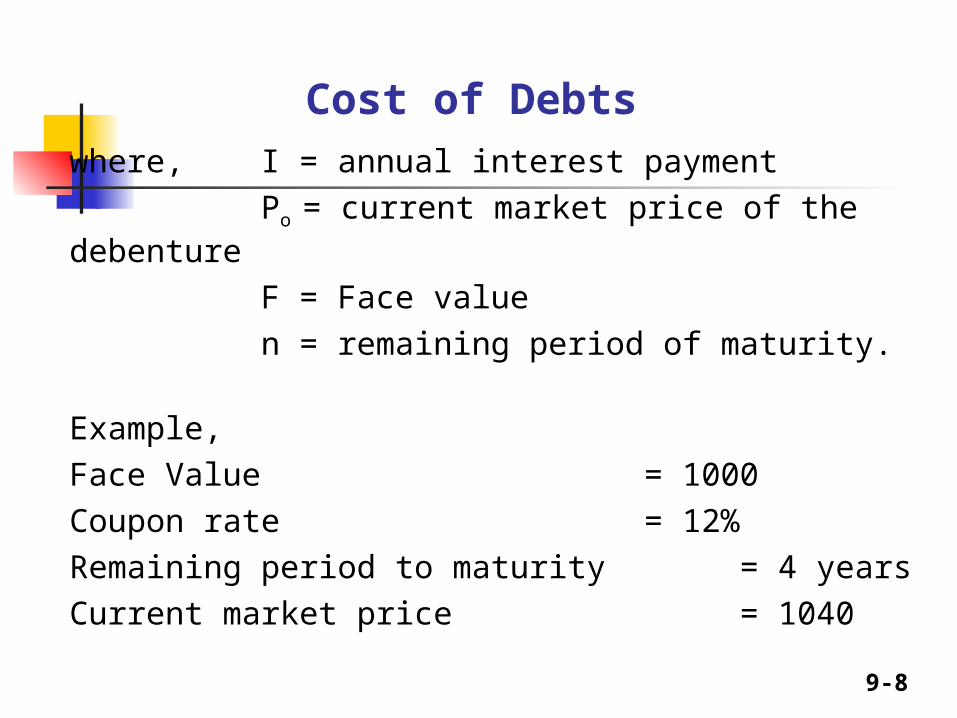

Cost of Debts where, I = annual interest payment

Po = current market price of the debenture

F = Face valuen = remaining period of maturity.

Example,Face Value = 1000Coupon rate = 12%Remaining period to maturity = 4 yearsCurrent market price = 1040

9-9

Cost of Debts

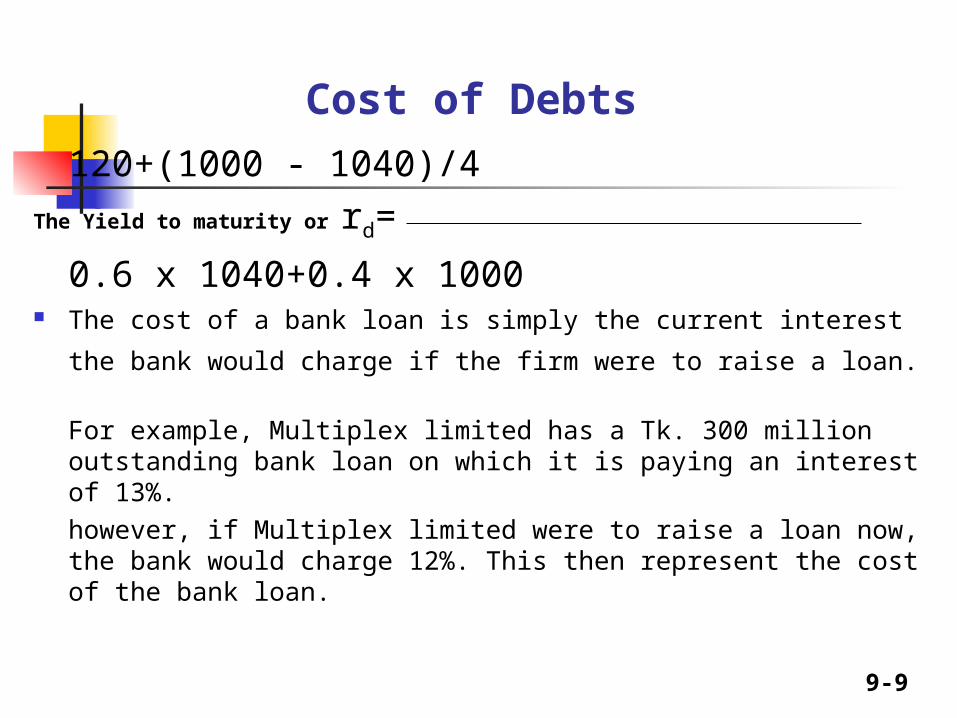

120+(1000 - 1040)/4The Yield to maturity or rd=

0.6 x 1040+0.4 x 1000 The cost of a bank loan is simply the current interest the bank

would charge if the firm were to raise a loan.

For example, Multiplex limited has a Tk. 300 million outstanding bank loan on which it is paying an interest of 13%. however, if Multiplex limited were to raise a loan now, the bank would charge 12%. This then represent the cost of the bank loan.

9-10

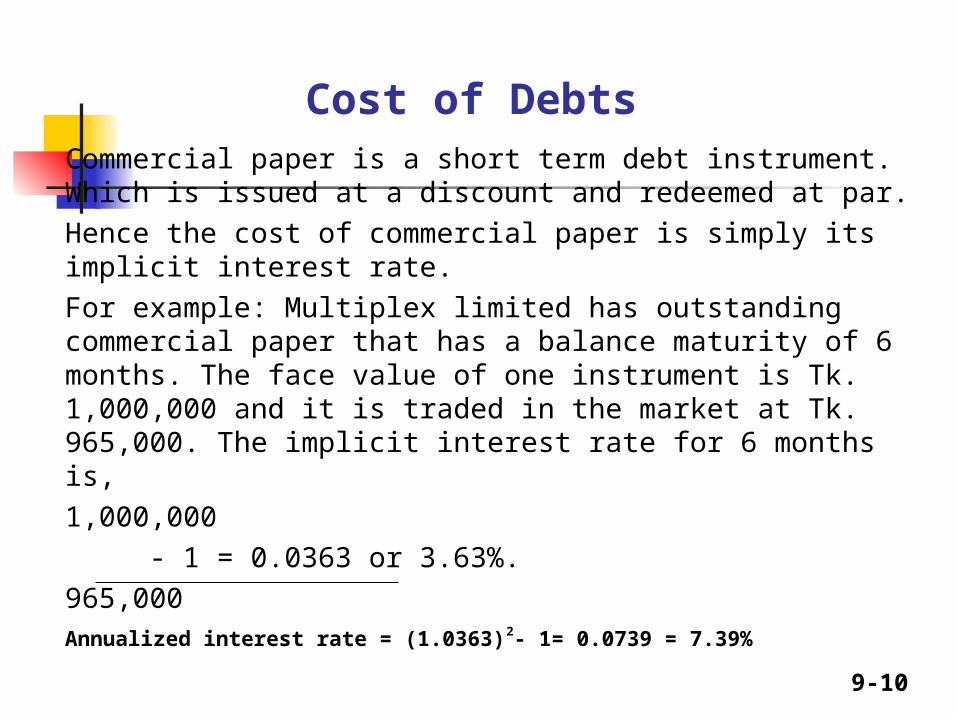

Cost of Debts Commercial paper is a short term debt instrument. Which is issued at a discount and redeemed at par. Hence the cost of commercial paper is simply its implicit interest rate. For example: Multiplex limited has outstanding commercial paper that has a balance maturity of 6 months. The face value of one instrument is Tk. 1,000,000 and it is traded in the market at Tk. 965,000. The implicit interest rate for 6 months is,

1,000,000 - 1 = 0.0363 or 3.63%.

965,000Annualized interest rate = (1.0363)2- 1= 0.0739 = 7.39%

9-11

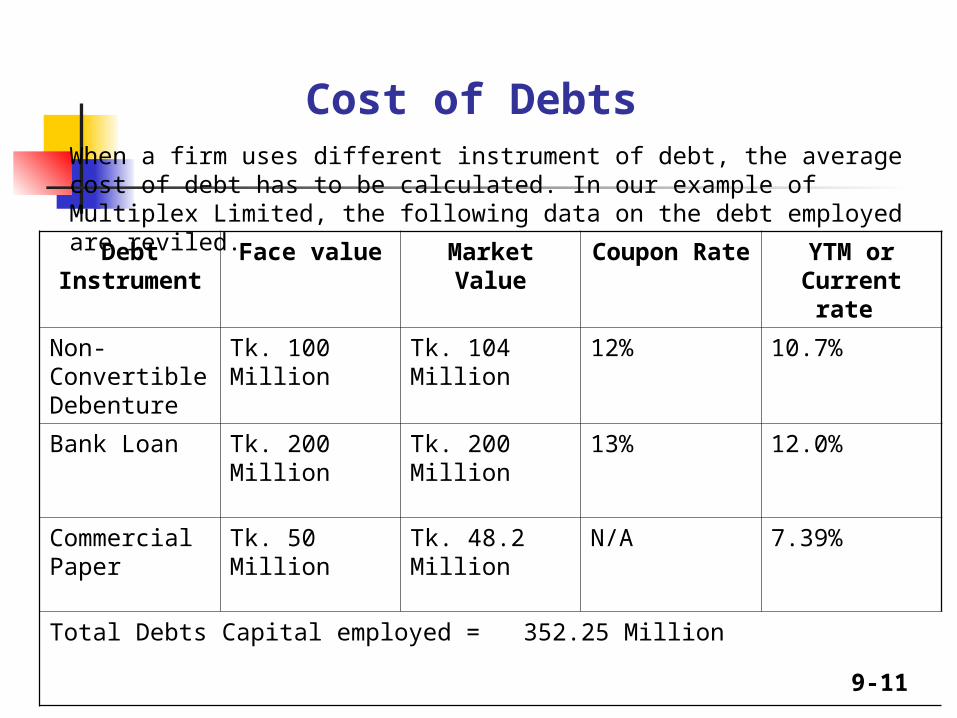

Cost of Debts When a firm uses different instrument of debt, the average cost of debt has to be calculated. In our example of Multiplex Limited, the following data on the debt employed are reviled. Debt

InstrumentFace value Market

ValueCoupon

RateYTM or Current

rate

Non-Convertible Debenture

Tk. 100 Million

Tk. 104 Million

12% 10.7%

Bank Loan Tk. 200 Million

Tk. 200 Million

13% 12.0%

Commercial Paper

Tk. 50 Million Tk. 48.2 Million

N/A 7.39%

Total Debts Capital employed = 352.25 Million

9-12

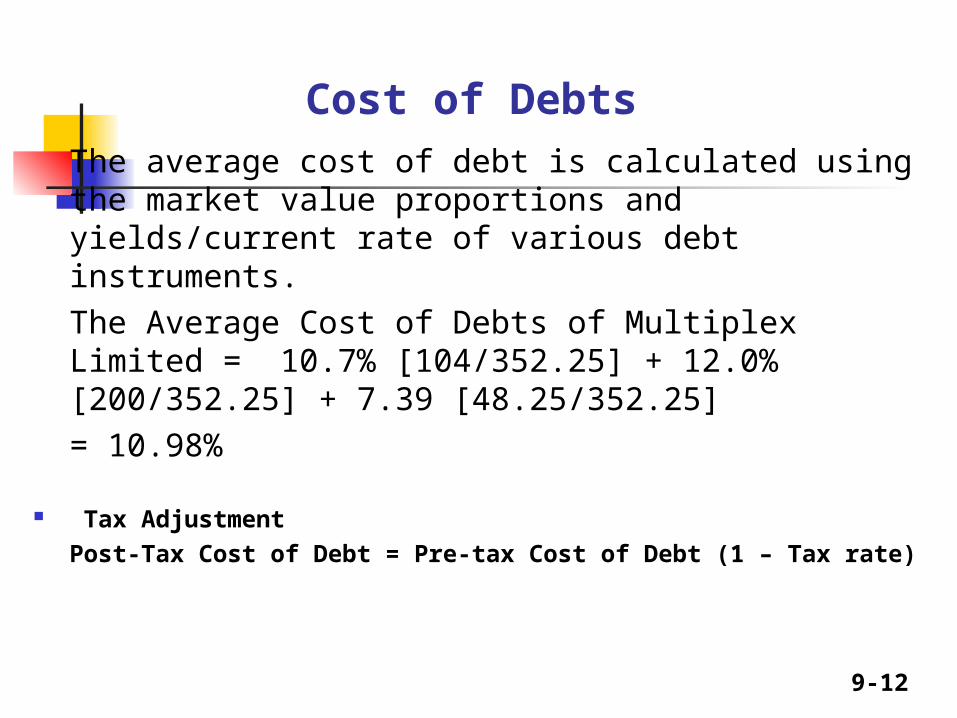

Cost of Debts The average cost of debt is calculated using the market value proportions and yields/current rate of various debt instruments.The Average Cost of Debts of Multiplex Limited = 10.7% [104/352.25] + 12.0% [200/352.25] + 7.39 [48.25/352.25]= 10.98%

Tax Adjustment Post-Tax Cost of Debt = Pre-tax Cost of Debt (1 – Tax rate)

9-13

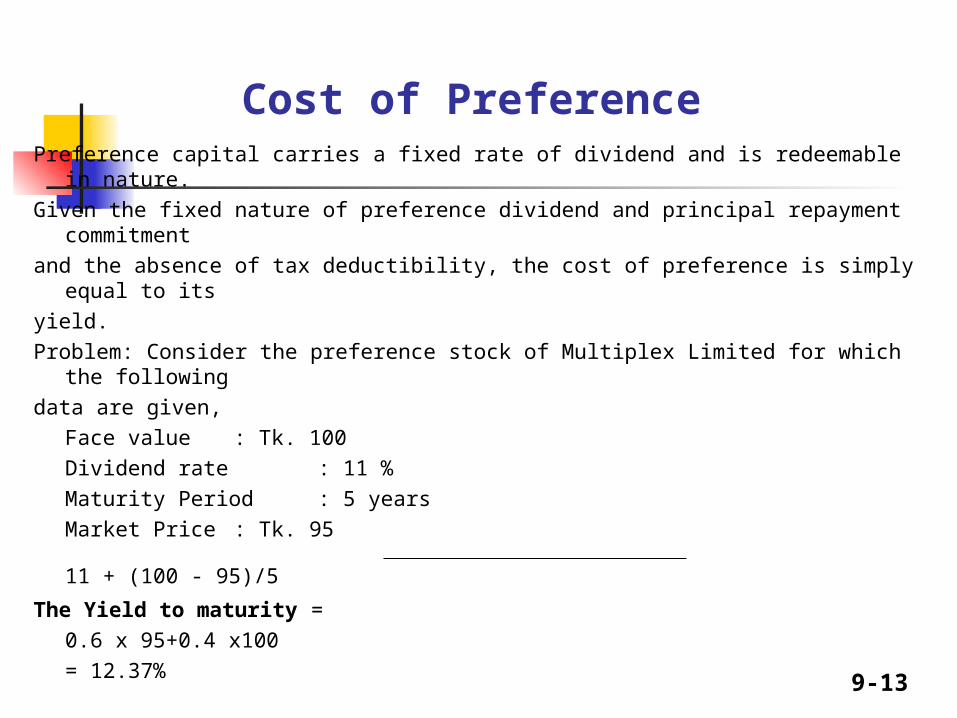

Cost of Preference Preference capital carries a fixed rate of dividend and is redeemable in nature. Given the fixed nature of preference dividend and principal repayment

commitmentand the absence of tax deductibility, the cost of preference is simply equal to

itsyield. Problem: Consider the preference stock of Multiplex Limited for which the

following data are given,

Face value : Tk. 100Dividend rate : 11 %Maturity Period : 5 yearsMarket Price : Tk. 95

11 + (100 - 95)/5

The Yield to maturity = 0.6 x 95+0.4 x100= 12.37%

9-14

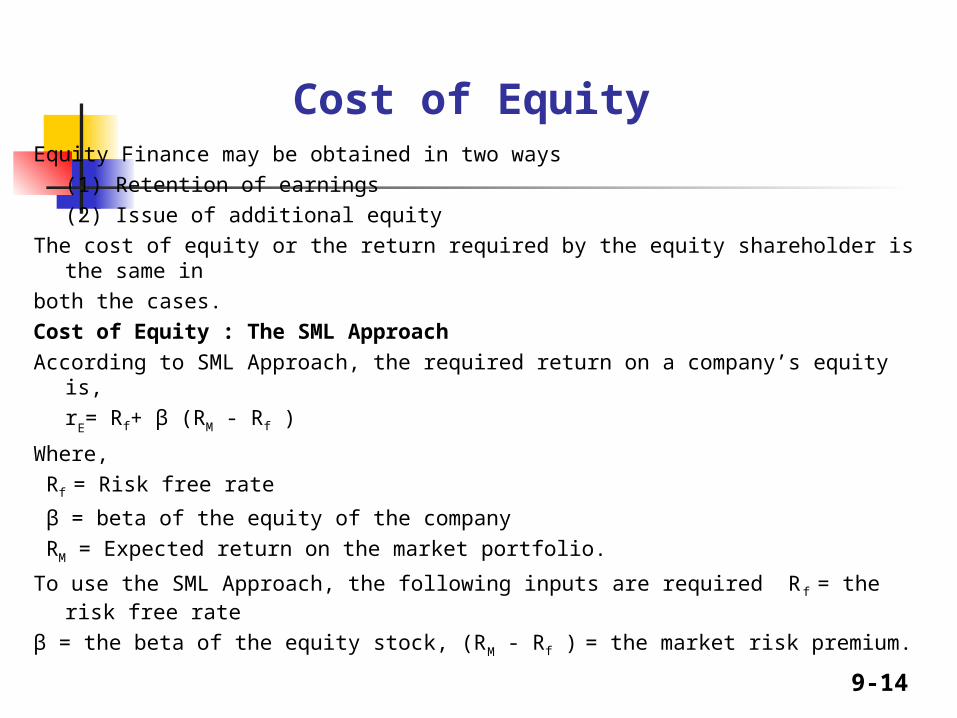

Cost of Equity Equity Finance may be obtained in two ways

(1) Retention of earnings(2) Issue of additional equity

The cost of equity or the return required by the equity shareholder is the same in

both the cases. Cost of Equity : The SML ApproachAccording to SML Approach, the required return on a company’s equity is,

rE= Rf+ β (RM - Rf )

Where, Rf = Risk free rate

β = beta of the equity of the company RM = Expected return on the market portfolio.

To use the SML Approach, the following inputs are required Rf = the risk free rate

β = the beta of the equity stock, (RM - Rf ) = the market risk premium.

9-15

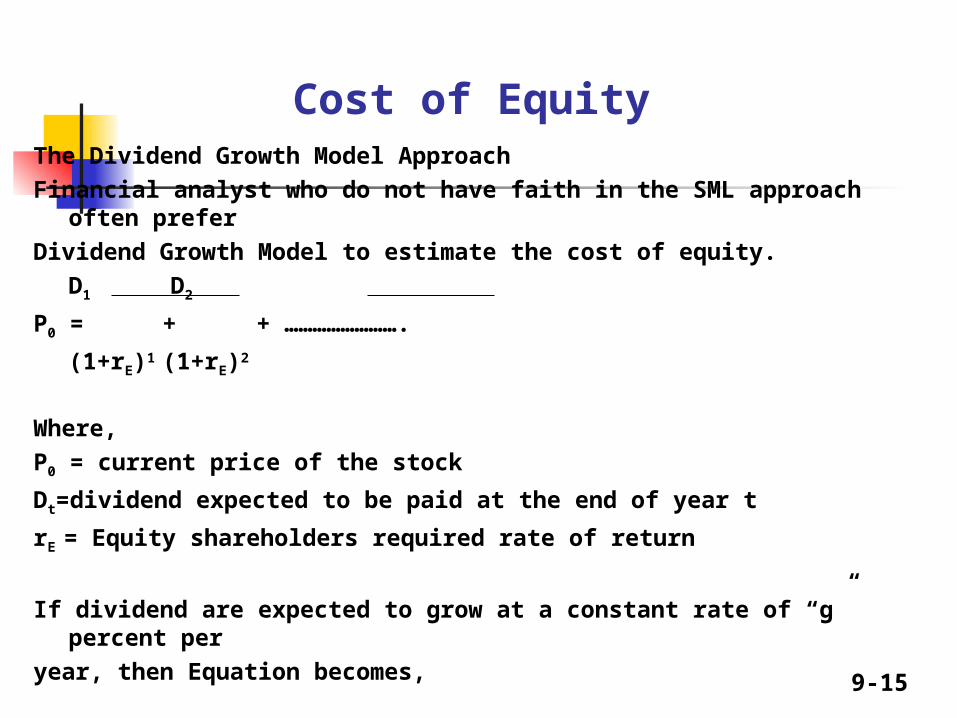

Cost of Equity The Dividend Growth Model ApproachFinancial analyst who do not have faith in the SML approach

often prefer Dividend Growth Model to estimate the cost of equity.

D1 D2

P0 = + + …………………….

(1+rE)1 (1+rE)2

Where, P0 = current price of the stock

Dt=dividend expected to be paid at the end of year t

rE = Equity shareholders required rate of return

If dividend are expected to grow at a constant rate of “g”

percent per year, then Equation becomes,

9-16

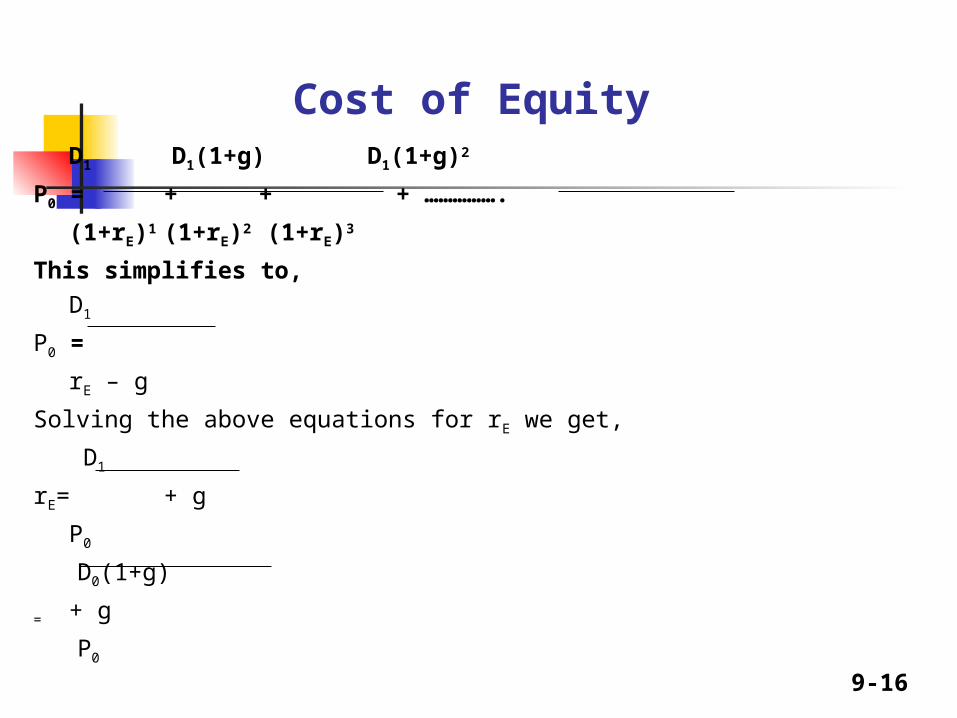

Cost of Equity D1 D1(1+g) D1(1+g)2

P0 = + + + …………….

(1+rE)1 (1+rE)2 (1+rE)3

This simplifies to,D1

P0 =

rE – g

Solving the above equations for rE we get,

D1

rE= + g

P0

D0(1+g)

= + g

P0

9-17

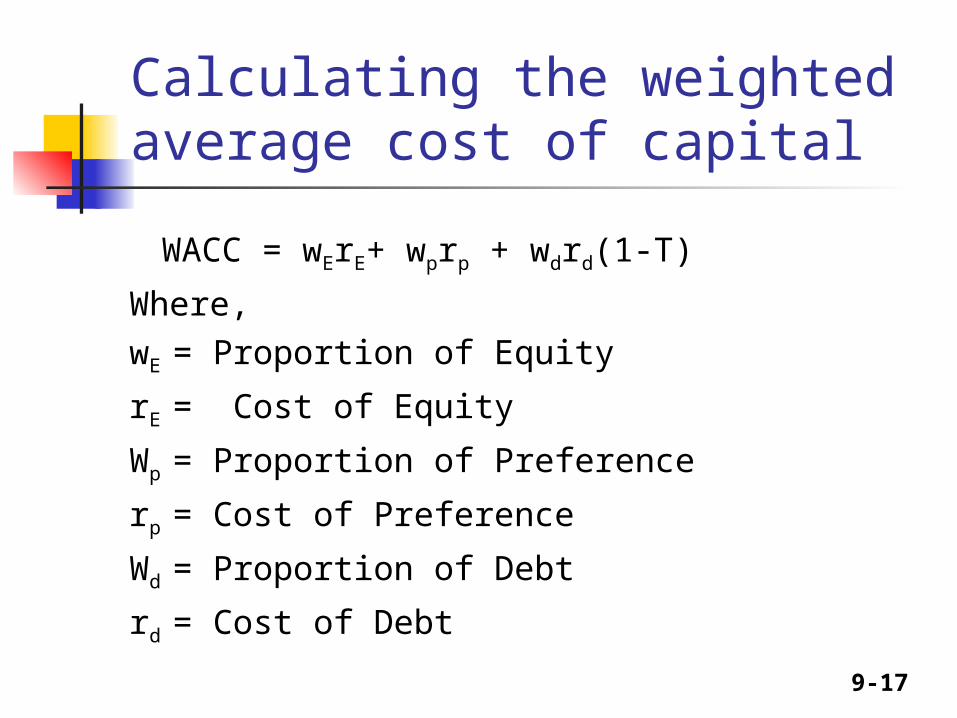

Calculating the weighted average cost of capital

WACC = wErE+ wprp + wdrd(1-T)

Where,wE = Proportion of Equity

rE = Cost of Equity

Wp = Proportion of Preference

rp = Cost of Preference

Wd = Proportion of Debt

rd = Cost of Debt

9-18

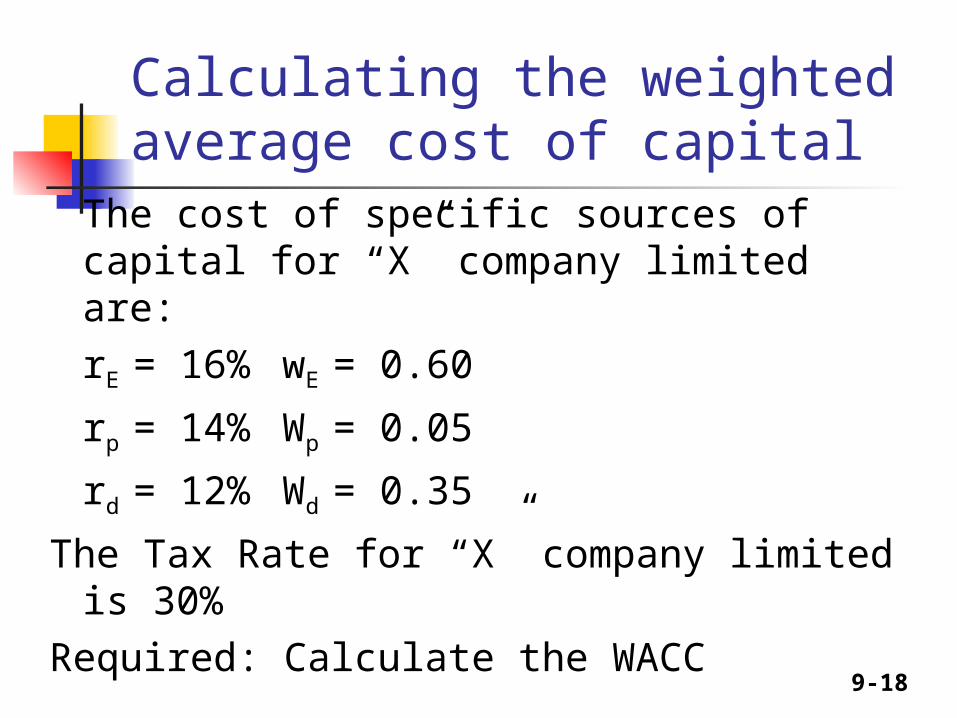

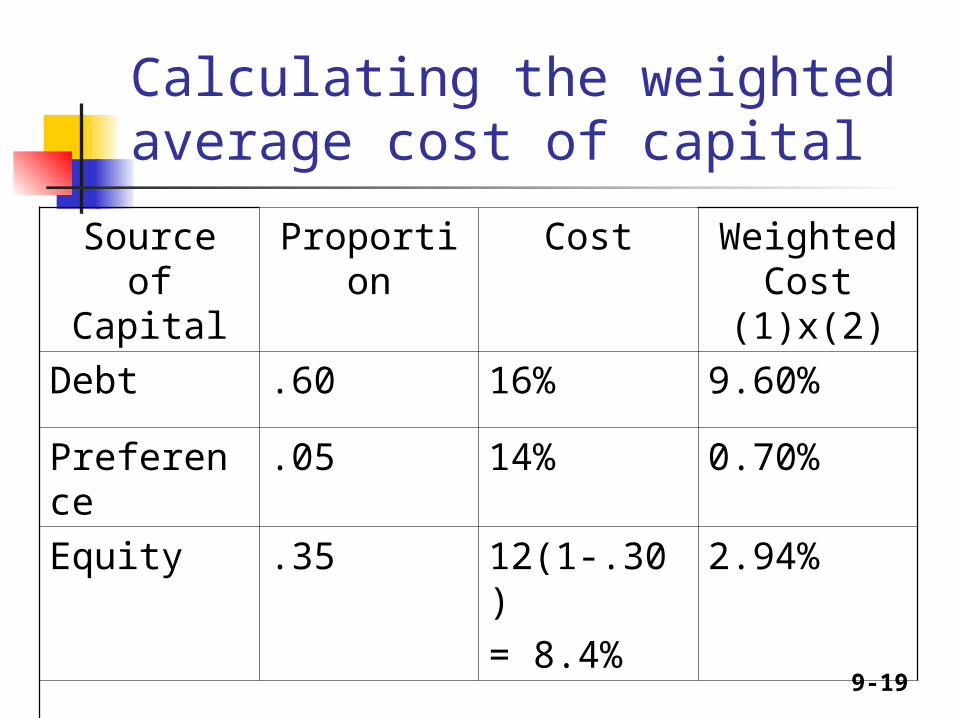

Calculating the weighted average cost of capital

The cost of specific sources of capital for “X” company limited are: rE = 16% wE = 0.60

rp = 14% Wp = 0.05

rd = 12% Wd = 0.35

The Tax Rate for “X” company limited is 30%

Required: Calculate the WACC

9-19

Calculating the weighted average cost of capital

Source of Capital

Proportion Cost Weighted Cost

(1)x(2)

Debt .60 16% 9.60%

Preference

.05 14% 0.70%

Equity .35 12(1-.30)= 8.4%

2.94%

WACC = 13.24%

9-20

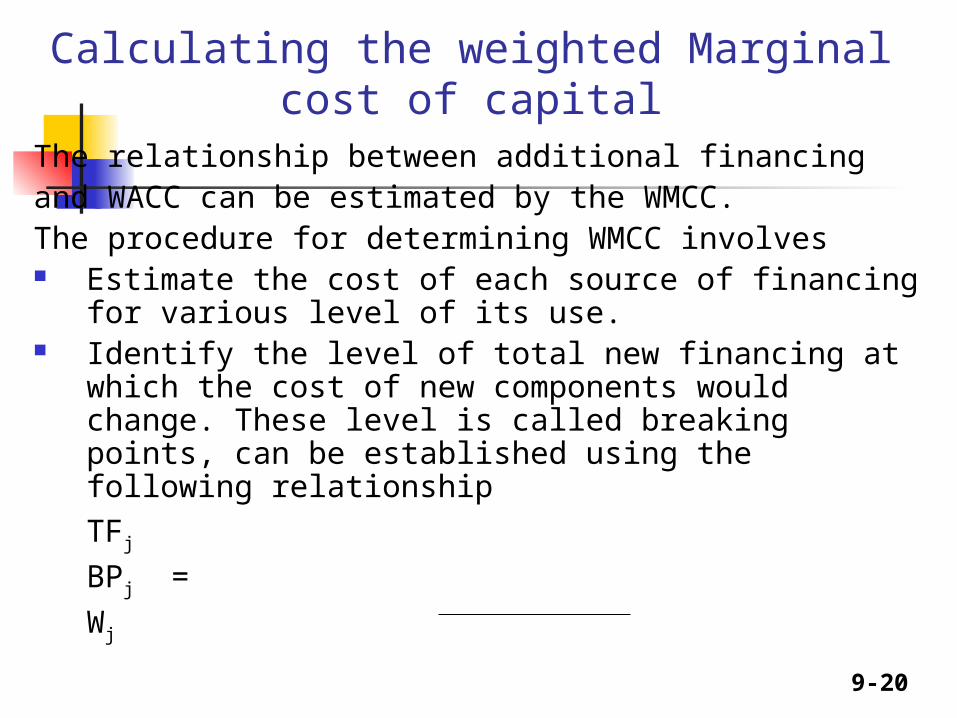

Calculating the weighted Marginal cost of capital

The relationship between additional financing and WACC can be estimated by the WMCC. The procedure for determining WMCC involves Estimate the cost of each source of financing for

various level of its use. Identify the level of total new financing at which

the cost of new components would change. These level is called breaking points, can be established using the following relationship

TFj

BPj =

Wj

9-21

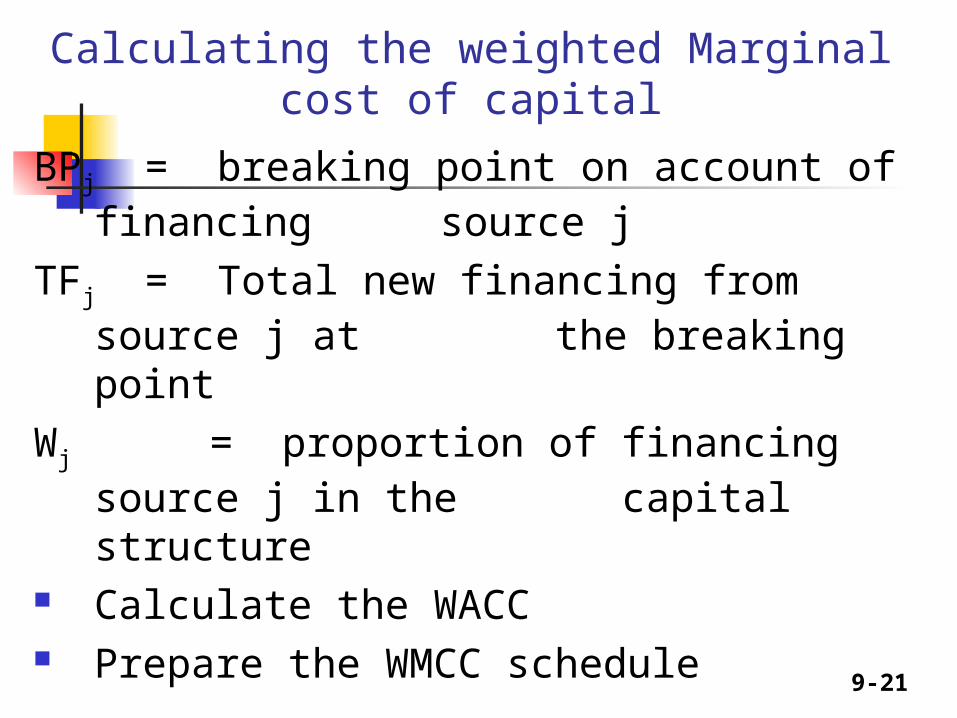

Calculating the weighted Marginal cost of capital

BPj = breaking point on account of financing source j

TFj = Total new financing from source j at the breaking point

Wj = proportion of financing source j in the capital structure

Calculate the WACC Prepare the WMCC schedule

9-22

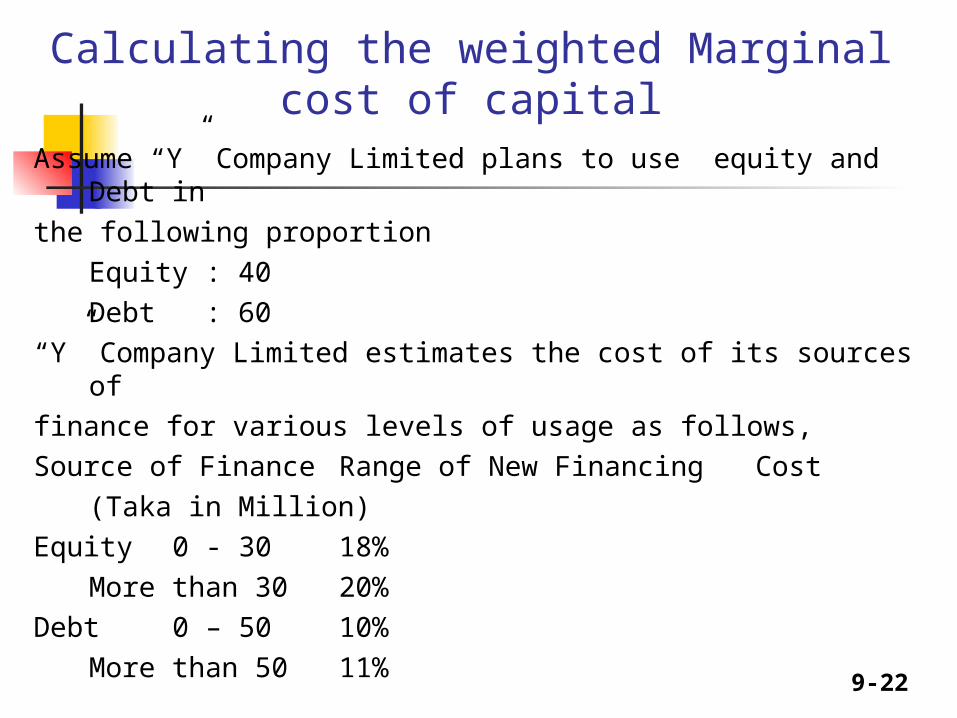

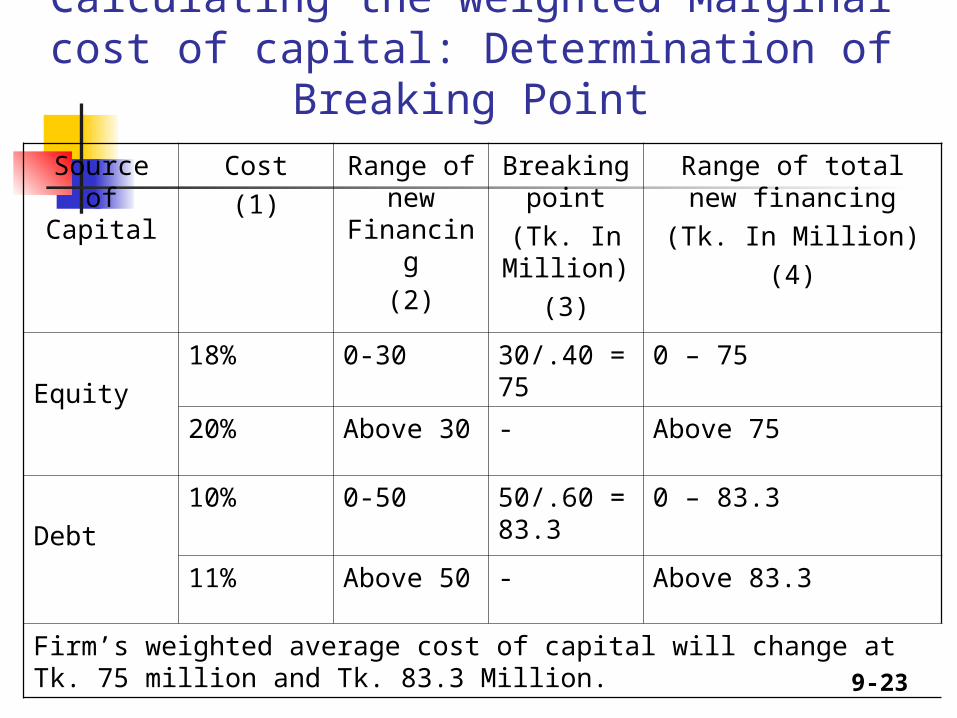

Calculating the weighted Marginal cost of capital

Assume “Y” Company Limited plans to use equity and Debt in the following proportion

Equity : 40Debt : 60

“Y” Company Limited estimates the cost of its sources of finance for various levels of usage as follows, Source of Finance Range of New Financing Cost

(Taka in Million)Equity 0 - 3018%

More than 30 20%Debt 0 – 50 10%

More than 50 11%

9-23

Calculating the weighted Marginal cost of capital: Determination of Breaking

PointSource of Capital

Cost(1)

Range of new

Financing(2)

Breaking point(Tk. In Million)

(3)

Range of total new financing

(Tk. In Million)(4)

Equity 18% 0-30 30/.40 =

750 – 75

20% Above 30 - Above 75

Debt10% 0-50 50/.60 =

83.30 – 83.3

11% Above 50 - Above 83.3

Firm’s weighted average cost of capital will change at Tk. 75 million and Tk. 83.3 Million.

9-24

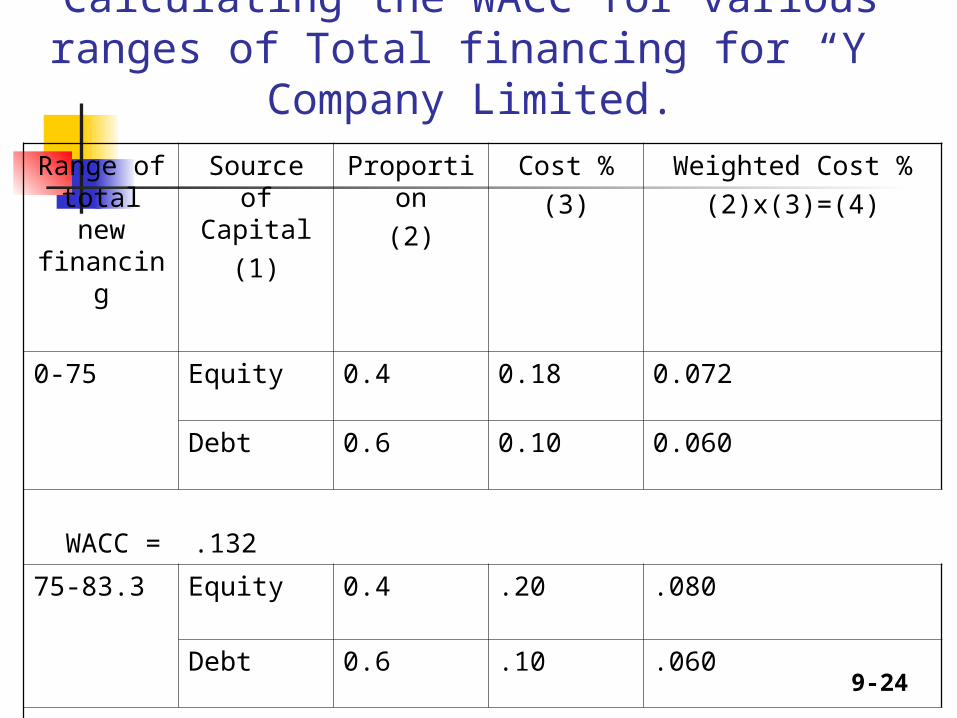

Calculating the WACC for various ranges of Total financing for “Y”

Company Limited.Range of total new financing

Source of Capital

(1)

Proportion

(2)

Cost %(3)

Weighted Cost %(2)x(3)=(4)

0-75 Equity 0.4 0.18 0.072

Debt 0.6 0.10 0.060

WACC = .132

75-83.3 Equity 0.4 .20 .080

Debt 0.6 .10 .060

WACC = .140

9-25

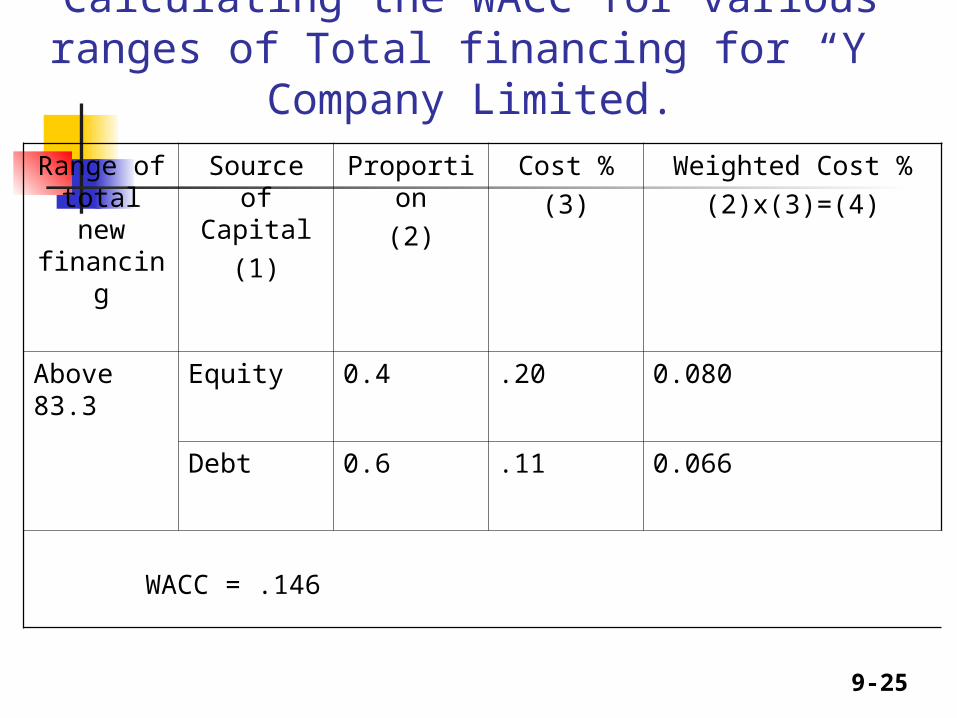

Calculating the WACC for various ranges of Total financing for “Y”

Company Limited.Range of total new financing

Source of Capital

(1)

Proportion

(2)

Cost %(3)

Weighted Cost %(2)x(3)=(4)

Above 83.3

Equity 0.4 .20 0.080

Debt 0.6 .11 0.066

WACC = .146

9-26

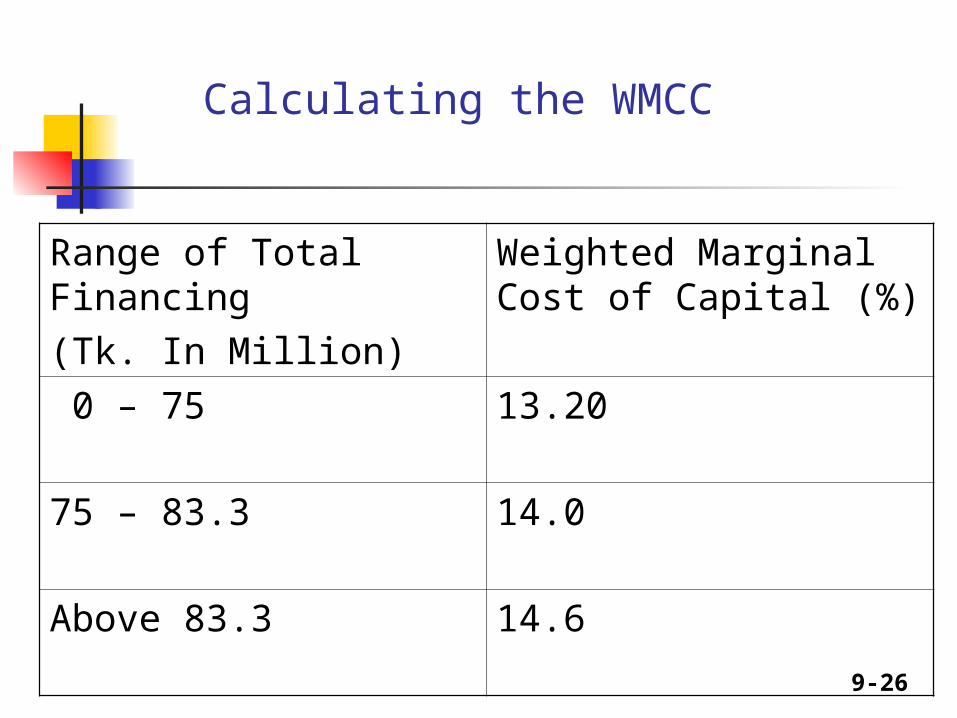

Calculating the WMCC

Range of Total Financing(Tk. In Million)

Weighted Marginal Cost of Capital (%)

0 – 75 13.20

75 – 83.3 14.0

Above 83.3 14.6

9-27

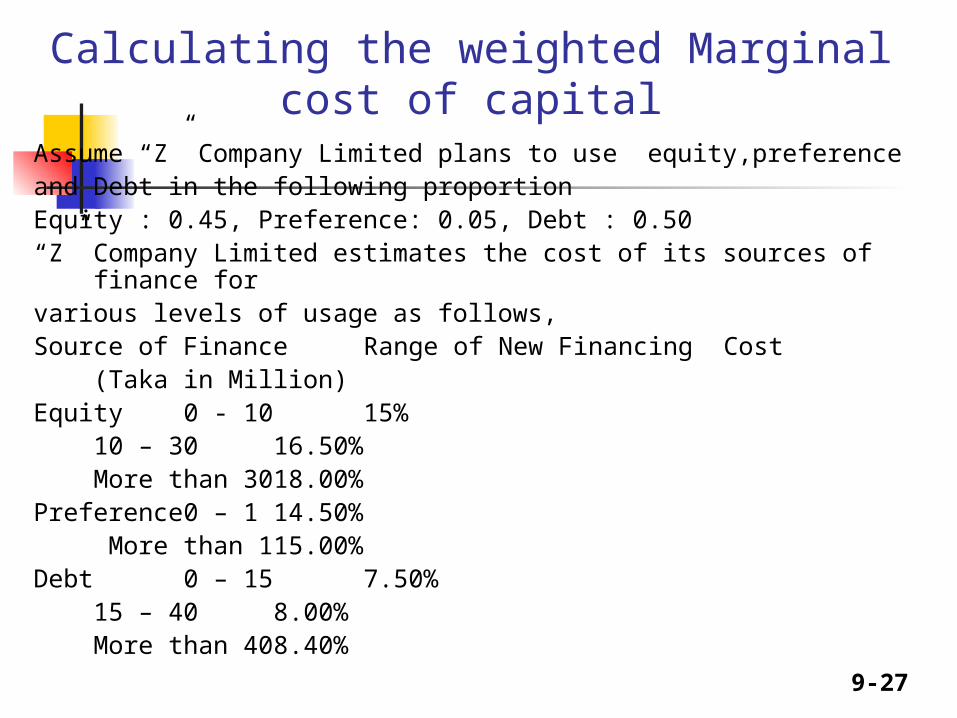

Calculating the weighted Marginal cost of capital

Assume “Z” Company Limited plans to use equity,preference and Debt in the following proportionEquity : 0.45, Preference: 0.05, Debt : 0.50“Z” Company Limited estimates the cost of its sources of finance for various levels of usage as follows, Source of Finance Range of New Financing Cost

(Taka in Million)Equity 0 - 10 15%

10 – 3016.50%

More than 30 18.00%Preference 0 – 1 14.50%

More than 1 15.00%

Debt 0 – 15 7.50%15 – 40 8.00%More than 40 8.40%

9-28

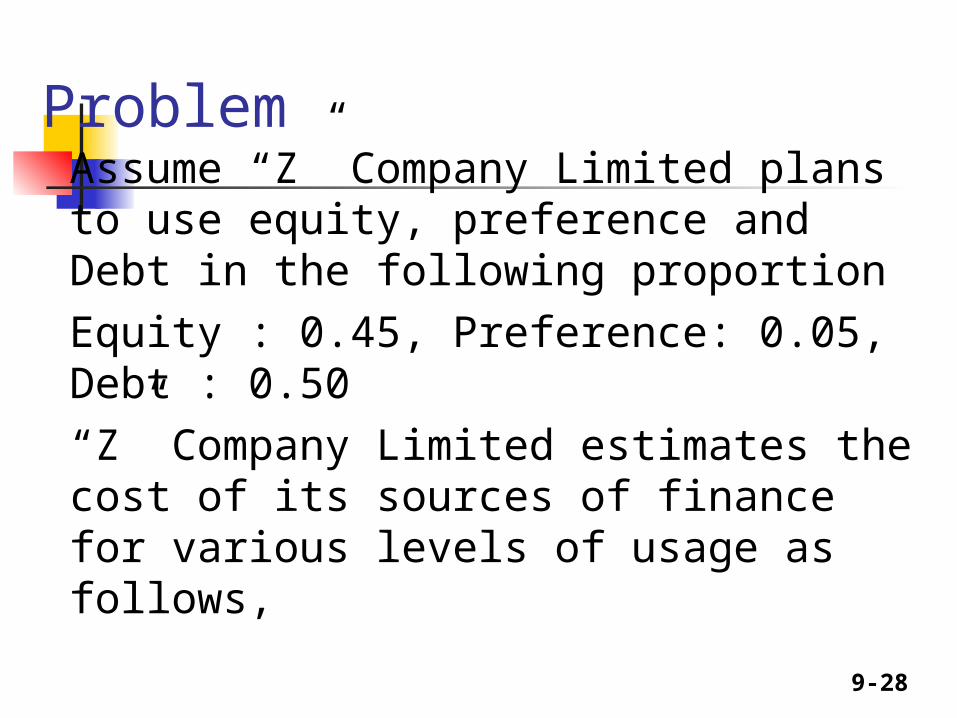

ProblemAssume “Z” Company Limited plans to use equity, preference and Debt in the following proportionEquity : 0.45, Preference: 0.05, Debt : 0.50“Z” Company Limited estimates the cost of its sources of finance for various levels of usage as follows,

9-29

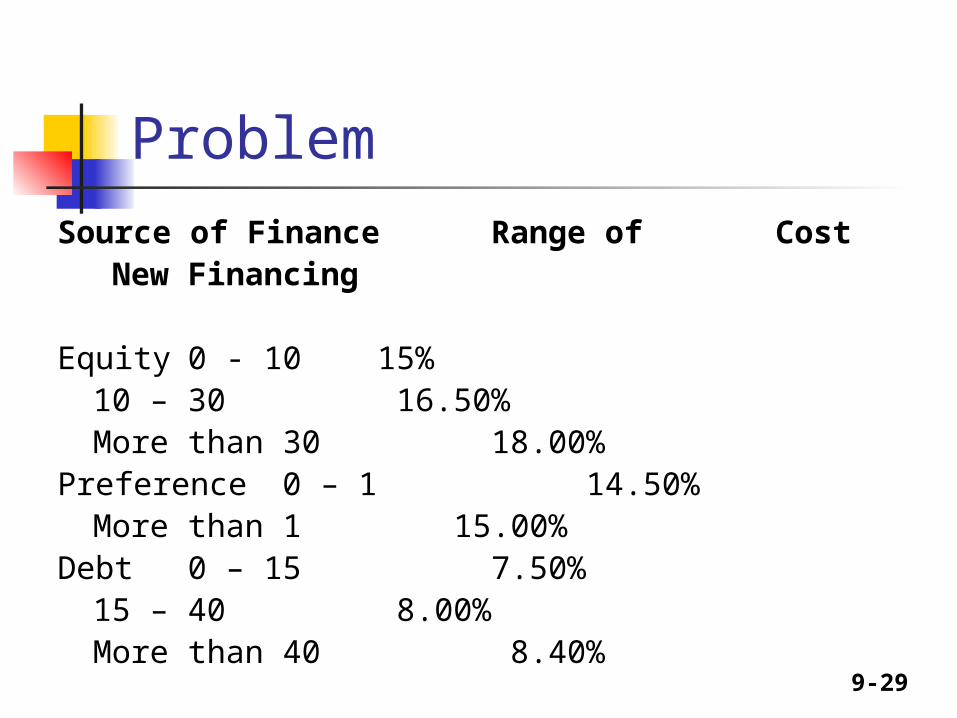

ProblemSource of Finance Range of Cost

New Financing

Equity 0 - 10 15%10 – 30 16.50%More than 30 18.00%

Preference 0 – 1 14.50%More than 1 15.00%

Debt 0 – 15 7.50%15 – 40 8.00%More than 40 8.40%

9-30

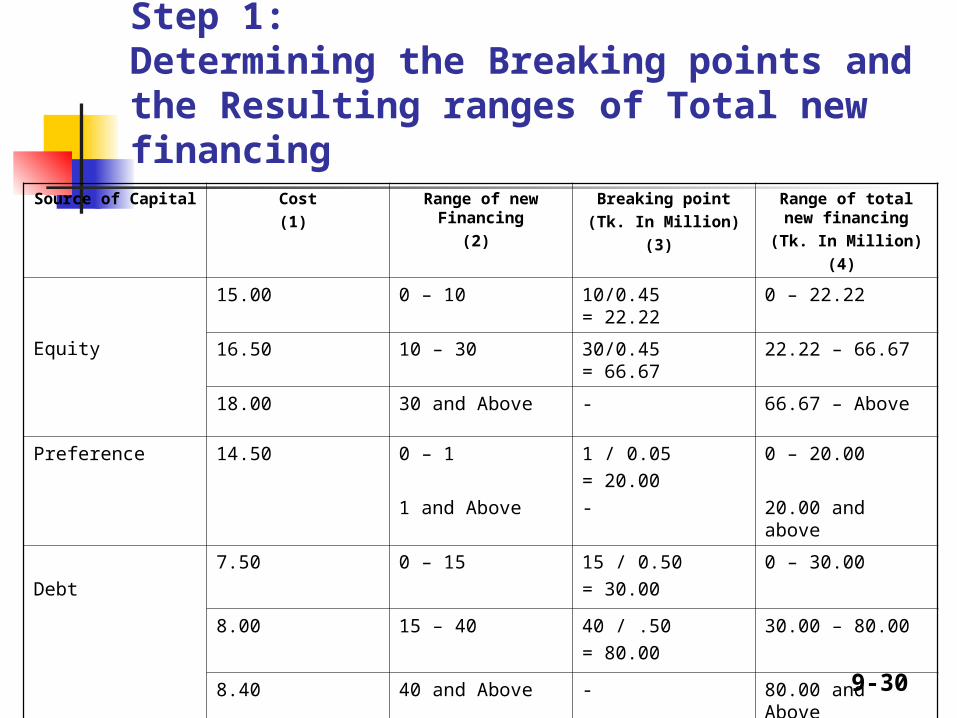

Step 1: Determining the Breaking points and the Resulting ranges of Total new financing

Source of Capital Cost(1)

Range of new Financing

(2)

Breaking point(Tk. In Million)

(3)

Range of total new financing(Tk. In Million)

(4)

Equity

15.00 0 – 10 10/0.45 = 22.22 0 – 22.22

16.50 10 – 30 30/0.45 = 66.67 22.22 – 66.67

18.00 30 and Above - 66.67 – Above

Preference 14.50 0 – 1

1 and Above

1 / 0.05

= 20.00

-

0 – 20.00

20.00 and above

Debt 7.50 0 – 15 15 / 0.50

= 30.00 0 – 30.00

8.00 15 – 40 40 / .50= 80.00

30.00 – 80.00

8.40 40 and Above - 80.00 and Above

9-31

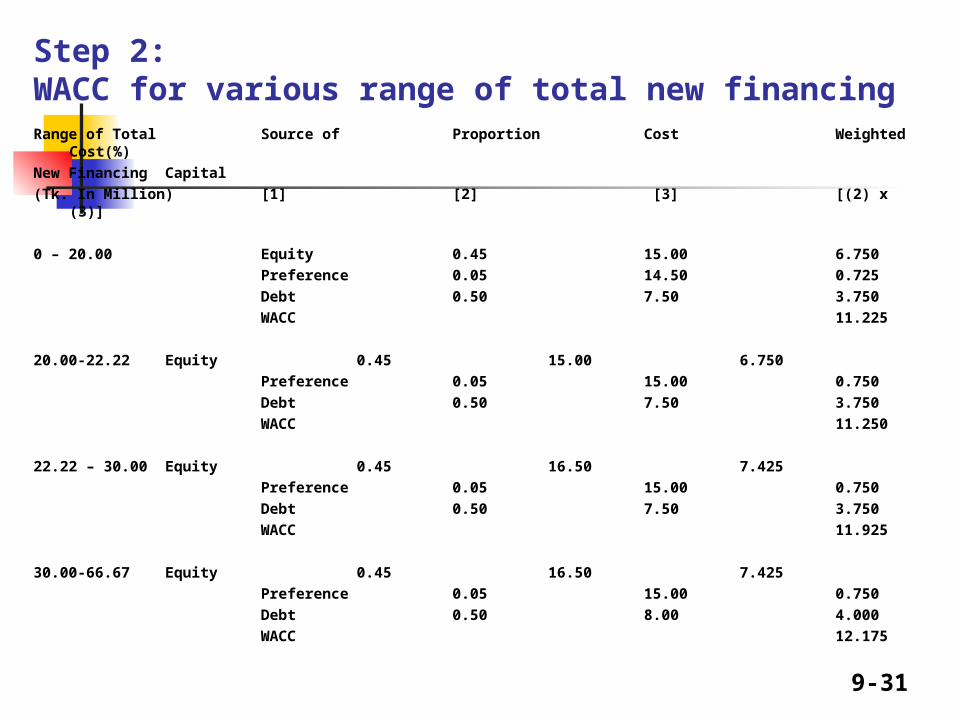

Step 2: WACC for various range of total new financingRange of Total Source of Proportion Cost Weighted Cost(%)New Financing Capital (Tk. In Million) [1] [2] [3] [(2) x (3)]

0 – 20.00 Equity 0.45 15.00 6.750Preference 0.05 14.50 0.725Debt 0.50 7.50 3.750WACC 11.225

20.00-22.22 Equity 0.45 15.00 6.750Preference 0.05 15.00 0.750Debt 0.50 7.50 3.750WACC 11.250

22.22 – 30.00 Equity 0.45 16.50 7.425Preference 0.05 15.00 0.750Debt 0.50 7.50 3.750WACC 11.925

30.00-66.67 Equity 0.45 16.50 7.425Preference 0.05 15.00 0.750Debt 0.50 8.00 4.000WACC 12.175

9-32

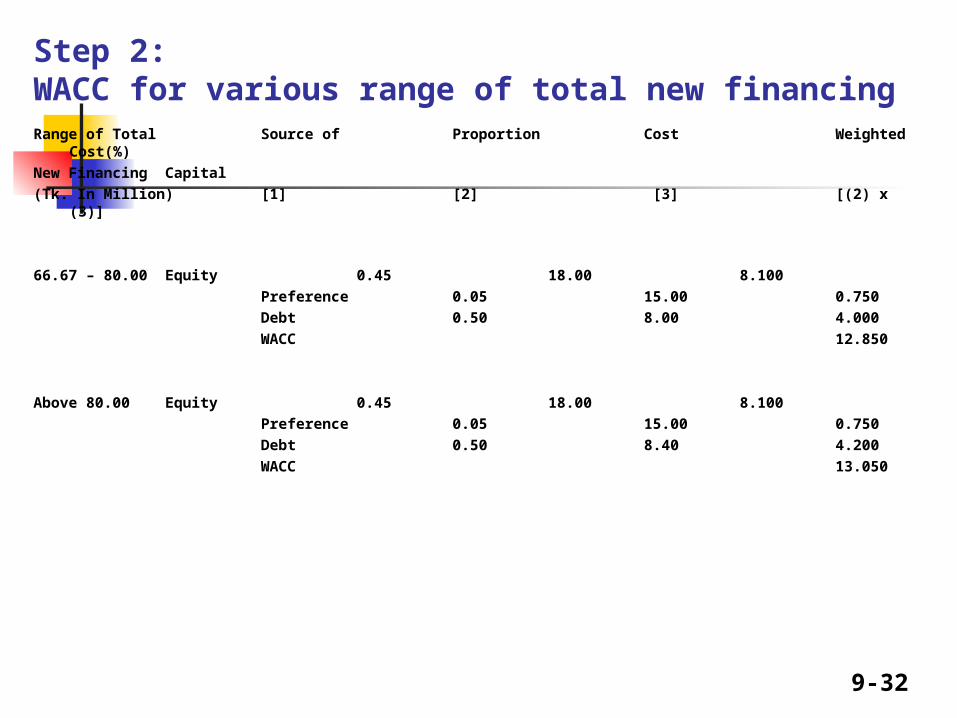

Step 2: WACC for various range of total new financingRange of Total Source of Proportion Cost Weighted Cost(%)New Financing Capital (Tk. In Million) [1] [2] [3] [(2) x (3)]

66.67 – 80.00 Equity 0.45 18.00 8.100Preference 0.05 15.00 0.750Debt 0.50 8.00 4.000WACC 12.850

Above 80.00 Equity 0.45 18.00 8.100Preference 0.05 15.00 0.750Debt 0.50 8.40 4.200WACC 13.050

9-33

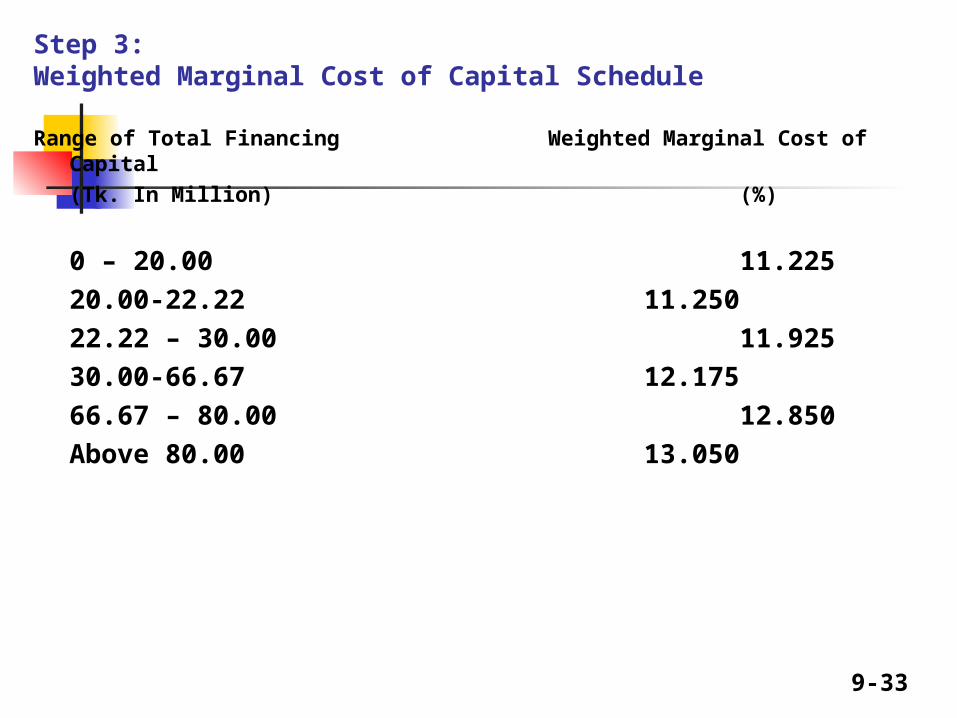

Step 3:Weighted Marginal Cost of Capital Schedule

Range of Total Financing Weighted Marginal Cost of Capital(Tk. In Million) (%)

0 – 20.00 11.22520.00-22.22 11.25022.22 – 30.00 11.92530.00-66.67 12.17566.67 – 80.00 12.850Above 80.00 13.050

9-34

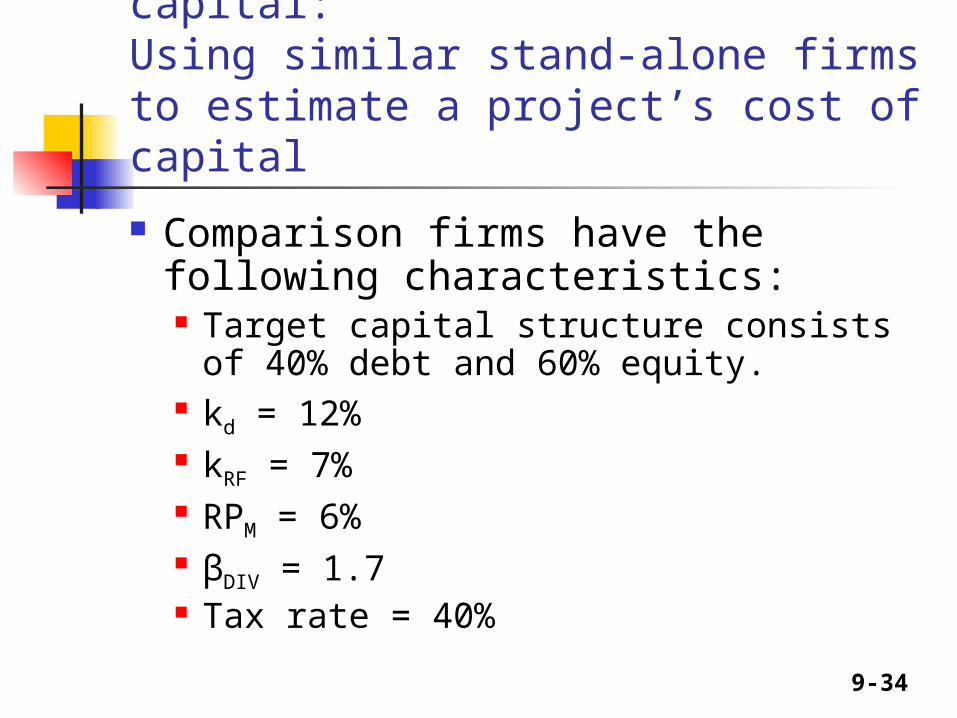

Finding a divisional cost of capital:Using similar stand-alone firms to estimate a project’s cost of capital

Comparison firms have the following characteristics: Target capital structure consists of

40% debt and 60% equity. kd = 12% kRF = 7% RPM = 6% βDIV = 1.7 Tax rate = 40%

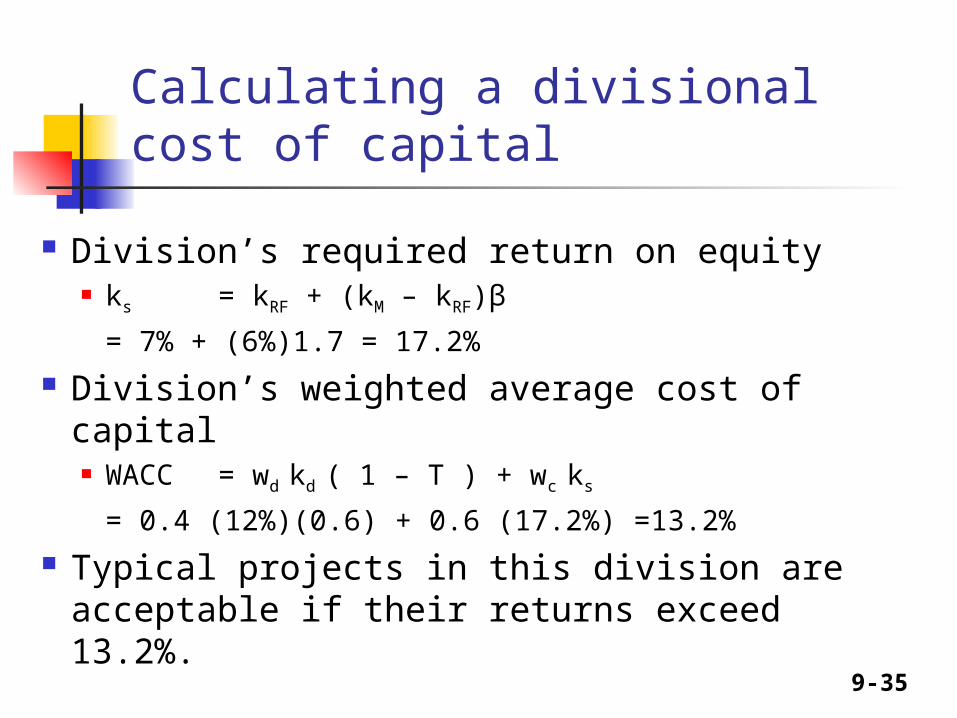

9-35

Calculating a divisional cost of capital

Division’s required return on equity ks = kRF + (kM – kRF)β

= 7% + (6%)1.7 = 17.2% Division’s weighted average cost of capital

WACC = wd kd ( 1 – T ) + wc ks

= 0.4 (12%)(0.6) + 0.6 (17.2%) =13.2% Typical projects in this division are

acceptable if their returns exceed 13.2%.