Embed Size (px)

Citation preview

한국 M&A 및 PE 시장 현황 및 당면과제

강사: 김 수 민

강사 소개

경력: • Procter & Gamble Korea 근무

• Goldman Sachs 홍콩 오피스 IBD (Investment Banking Division)의 M&A 및 기업금융 부서 근무

• Bain & Company 서울 및 싱가포르 오피스 근무

• 2006년 Bain & Company 글로벌 파트너(부사장) 선임

• 2006-2011년 Bain & Company 서울 오피스의 Private Equity 및 M&A Group 대표 역임

학력: • 학사, 서울대학교 경영학과

• MBA, Columbia Business School

220110929-The Bell Academy-M&A Market-Hand Out_v01SEO

주요 경험:

• Procter & Gamble Korea 근무

• Goldman Sachs 홍콩 오피스 IBD (Investment Banking Division)의 M&A 및 기업금융 부서 근무

• Bain & Company 서울 및 싱가포르 오피스 근무

• 2006년 Bain & Company 글로벌 파트너(부사장) 선임

• 2006-2011년 Bain & Company 서울 오피스의 Private Equity 및 M&A Group 대표 역임

• 베인의 사모펀드 및 M&A 컨설팅 부문 한국 대표로서 국내외사모펀드 및 대기업들을 대상으로 M&A 대상 기업의 선정, 전략적 실사, 기업가치 평가, 인수 후 가치창출 및 기업 매각에대한 자문을 제공해왔음

• 그 외에도 은행, 보험, 자산운용, 캐피탈 등의 각종 금융기관 및건설, 화학, 중장비, 헬쓰케어, 방송 등의 다양한 산업에 걸쳐서전사전략, 성장전략, 성과향상, 영업력 강화 등의 프로젝트 수행

• 현재 해외 유수의 사모펀드와 국내 사모펀드의 한국내 합작운용사 설립을 추진 중

김 수 민

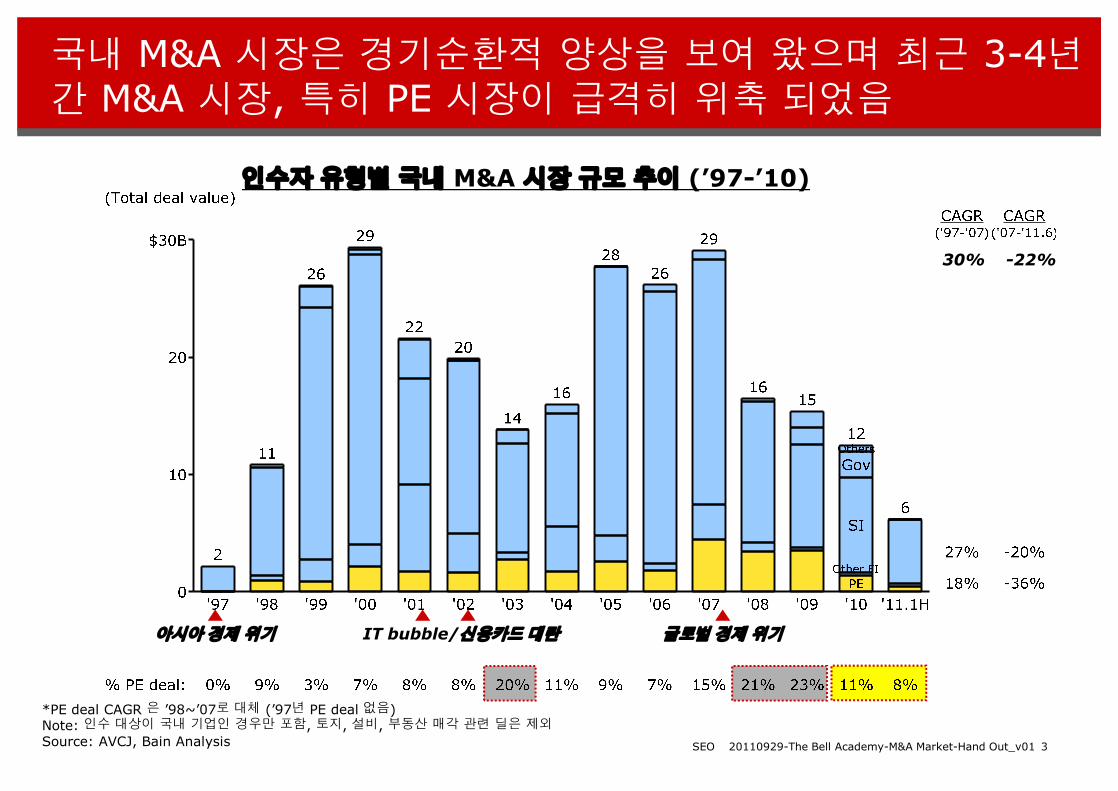

국내 M&A 시장은 경기순환적 양상을 보여 왔으며 최근 3-4년간 M&A 시장, 특히 PE 시장이 급격히 위축 되었음

인수자 유형별 국내 M&A 시장 규모 추이 (’97-’10)

30% -22%

320110929-The Bell Academy-M&A Market-Hand Out_v01SEO

*PE deal CAGR 은 ’98~’07로 대체 (’97년 PE deal 없음)Note: 인수 대상이 국내 기업인 경우만 포함, 토지, 설비, 부동산 매각 관련 딜은 제외

Source: AVCJ, Bain Analysis

IT bubble/신용카드 대란아시아 경제 위기 글로벌 경제 위기

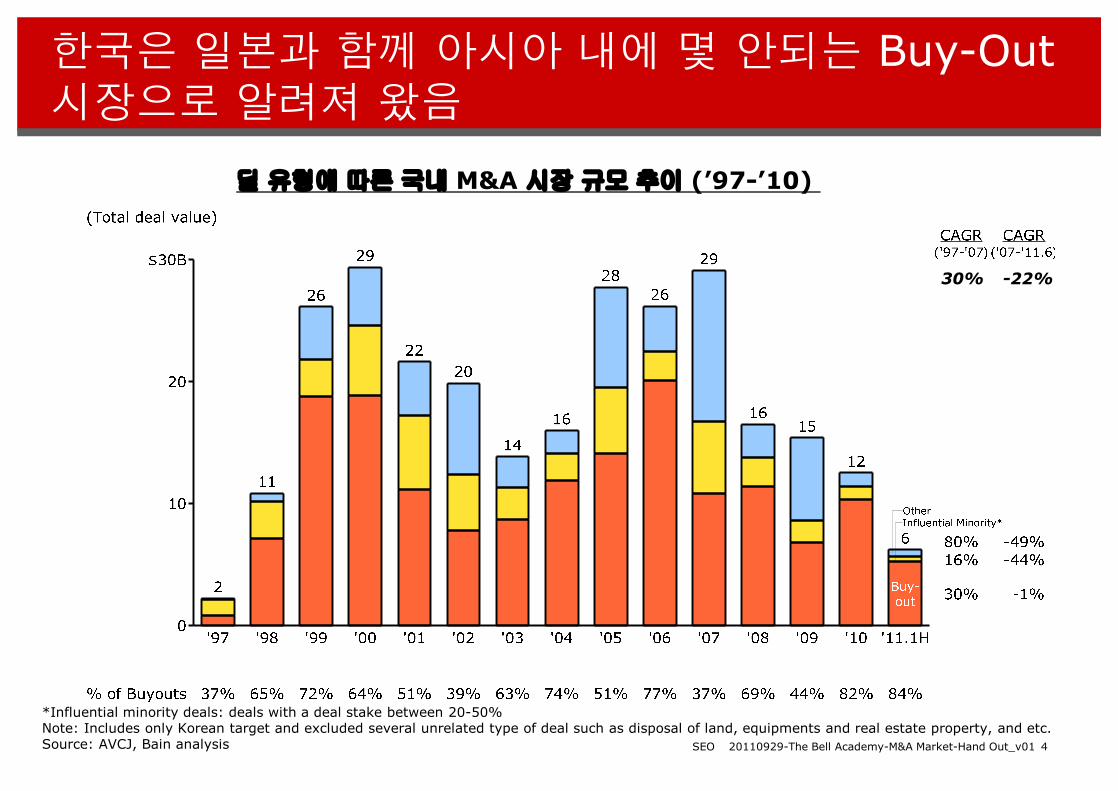

한국은 일본과 함께 아시아 내에 몇 안되는 Buy-Out 시장으로 알려져 왔음

딜 유형에따른 국내 M&A 시장 규모추이 (’97-’10)

30% -22%

420110929-The Bell Academy-M&A Market-Hand Out_v01SEO

*Influential minority deals: deals with a deal stake between 20-50%Note: Includes only Korean target and excluded several unrelated type of deal such as disposal of land, equipments and real estate property, and etc.Source: AVCJ, Bain analysis

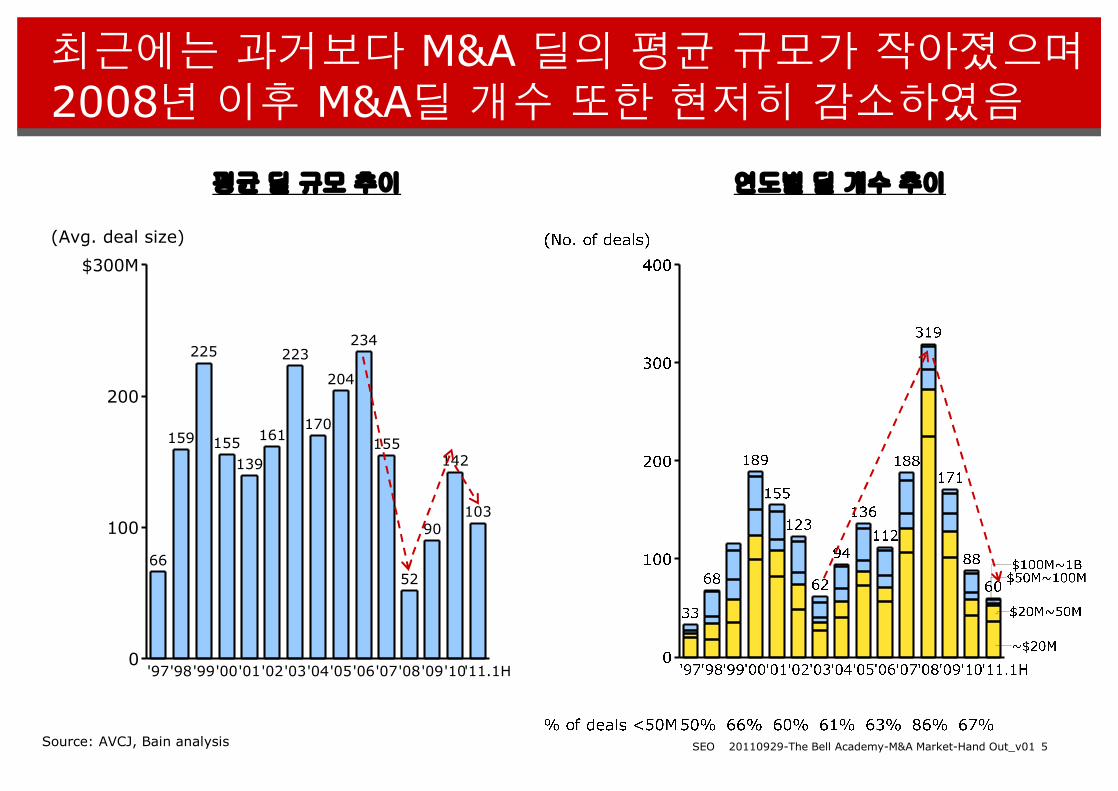

최근에는 과거보다 M&A 딜의 평균 규모가 작아졌으며2008년 이후 M&A딜 개수 또한 현저히 감소하였음

평균 딜 규모 추이 연도별딜 개수 추이

200

$300M

225 223

204

234

(Avg. deal size)

520110929-The Bell Academy-M&A Market-Hand Out_v01SEOSource: AVCJ, Bain analysis

0

100

200

'97

66

'98

159

'99'00

155

'01

139

'02

161

'03'04

170

'05'06'07

155

'08

52

'09

90

'10

142

103

'11.1H

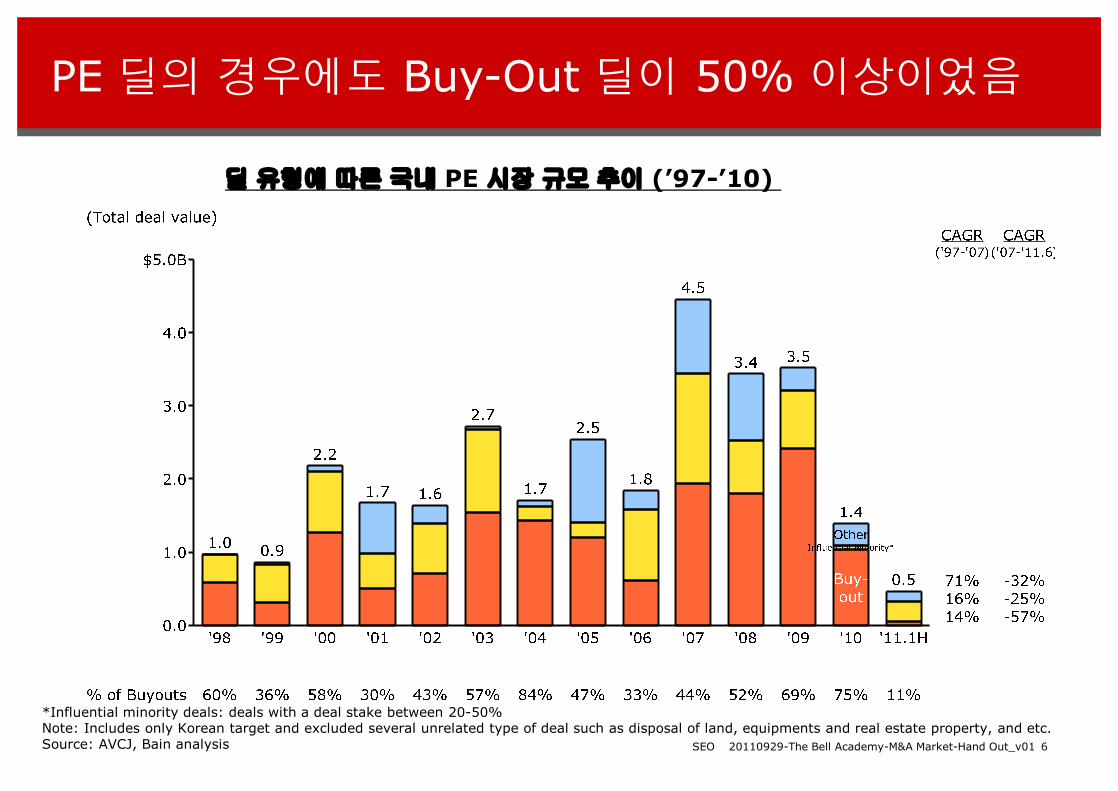

PE 딜의 경우에도 Buy-Out 딜이 50% 이상이었음

딜 유형에따른 국내 PE 시장 규모추이 (’97-’10)

620110929-The Bell Academy-M&A Market-Hand Out_v01SEO

*Influential minority deals: deals with a deal stake between 20-50%Note: Includes only Korean target and excluded several unrelated type of deal such as disposal of land, equipments and real estate property, and etc.Source: AVCJ, Bain analysis

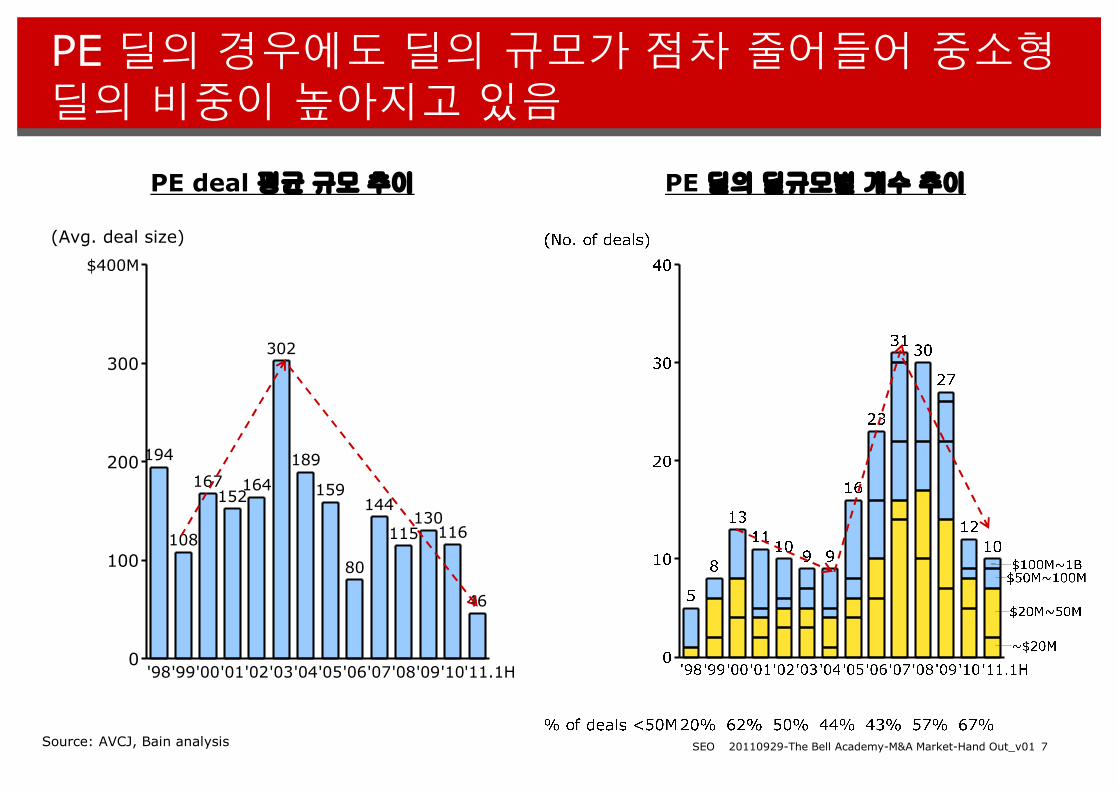

PE 딜의 경우에도 딜의 규모가 점차 줄어들어 중소형딜의 비중이 높아지고 있음

PE deal 평균 규모 추이 PE 딜의 딜규모별개수 추이

300

$400M

302

(Avg. deal size)

720110929-The Bell Academy-M&A Market-Hand Out_v01SEOSource: AVCJ, Bain analysis

0

100

200

'98

194

'99

108

'00

167

'01

152

'02

164

'03'04

189

'05

159

'06

80

'07

144

'08

115

'09

130

'10

116

46

'11.1H

누가 왜 매각하는가

설명 매각주체

• 비효율적인 경영/경기침체로 인해 발생한 부실상황을 개선을위한 기업 또는 기업 자산의 매각

강제 구조조정(“Distressed”)

• 여러 사업을영위하는 대기업

• (주로 재벌) 핵심부문 강화, M&A, 신규 사업 진출 등을 위한자본 조달을 위한 비핵심 사업부문 매각자발적 구조조정

(“Non-core”)

• 여러 사업을영위하는 대기업

• (주로 중형 기업) 오너가 경영에서 손을 떼고 현금화 하기위해서거나 사업을 가족에 승계하기 위한 기업 매각

대주주의 캐시-아웃(“Cash-out”)

• 개인(대주주)

820110929-The Bell Academy-M&A Market-Hand Out_v01SEO

Growth capital 및소수지분 투자

• 투자, 사업 확장, 인수 등을 위한 자본을 조달하기 위한 기업의소액지분 매각

• 대기업/중견기업• 중소기업

• (주로 중형 기업) 오너가 경영에서 손을 떼고 현금화 하기위해서거나 사업을 가족에 승계하기 위한 기업 매각

대주주의 캐시-아웃(“Cash-out”)

• 2000년대 중Ÿ후반 글로벌 및 국내 PE가 투자한 포트폴리오회사를 매각 정리

투자회수를 위한 매각(“Secondary”)

• PEF• 투자자

• 금융위기 동안 부실화되어 정부 및 채권단이 인수하였으나구조조정을 통한 회복 후 매각

공적 자금 회수를 위한정부의 재매각

• 정부

공기업의 민영화• 유틸리티, 공항, 금융기관 등 국유기업의 민영화를 위한 딜 • 정부

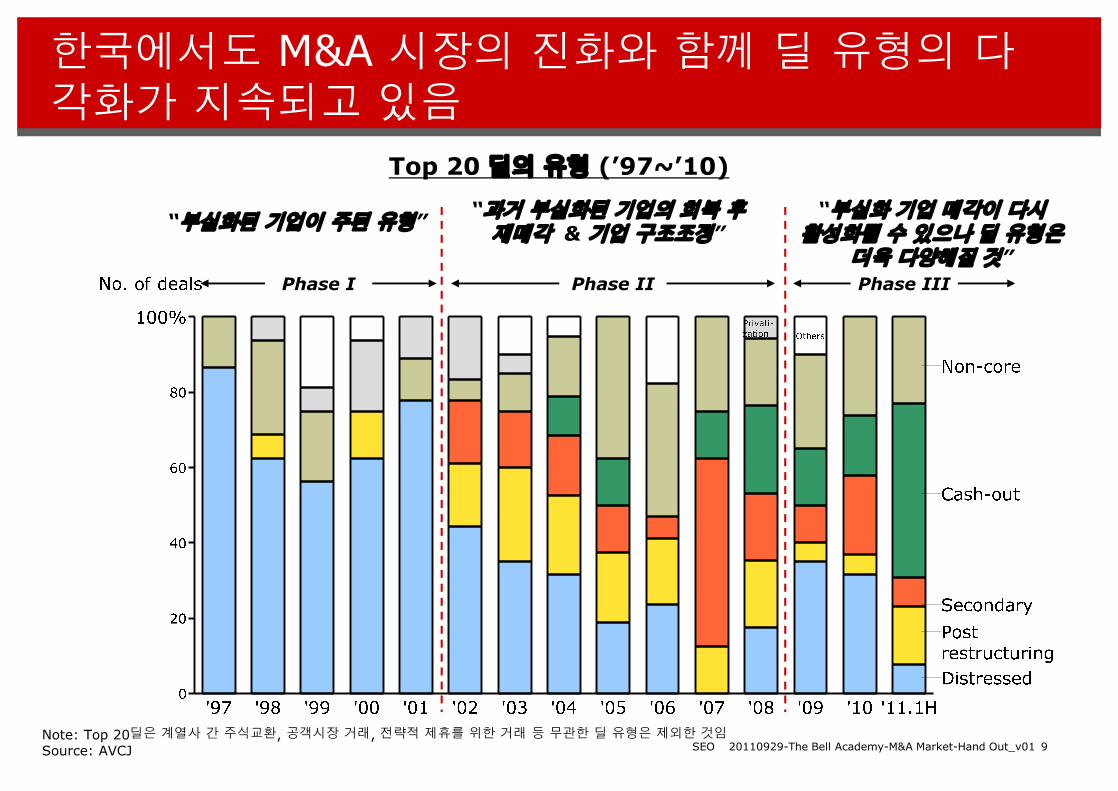

Top 20 딜의 유형 (’97~’10)

한국에서도 M&A 시장의 진화와 함께 딜 유형의 다각화가 지속되고 있음

“부실화된 기업이 주된 유형” “과거 부실화된 기업의 회복 후재매각 & 기업 구조조정”

“부실화 기업 매각이 다시활성화될 수 있으나 딜 유형은

더욱 다양해질 것”Phase III Phase I Phase II

920110929-The Bell Academy-M&A Market-Hand Out_v01SEONote: Top 20딜은 계열사 간 주식교환, 공객시장 거래, 전략적 제휴를 위한 거래 등 무관한 딜 유형은 제외한 것임

Source: AVCJ

매수자 유형별 비중은 시기에 따라 큰 변화를 보여왔으며 2006 – 2008년 사이에 SI들의 대몰락이 있었음

인수자 유형에 따른 Top 20 M&A 딜 (’97-’10)

80

100%

Top 20 deals (in $B)

2.2 8.2 17.7 11.3 15.3 9.8 12.0 12.1 18.3 22.8 15.4 11.6 6.1 8.3 5.8

1020110929-The Bell Academy-M&A Market-Hand Out_v01SEO

* 거래공시가 되지 않은 딜에 참여한 투자자들도 포함 됨 (개인투자자 & 기관투자자)Note: Top 20 딜에서 계열사간의 지분교환, 공개시장거래, 전략적 제휴 등의 관계없는 딜 종류는 제외 되었음.Source: AVCJ; Lit. Search; Bain Analysis

0

20

40

60

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11.1H

Korean SIForeign SIPEGov'tOther *

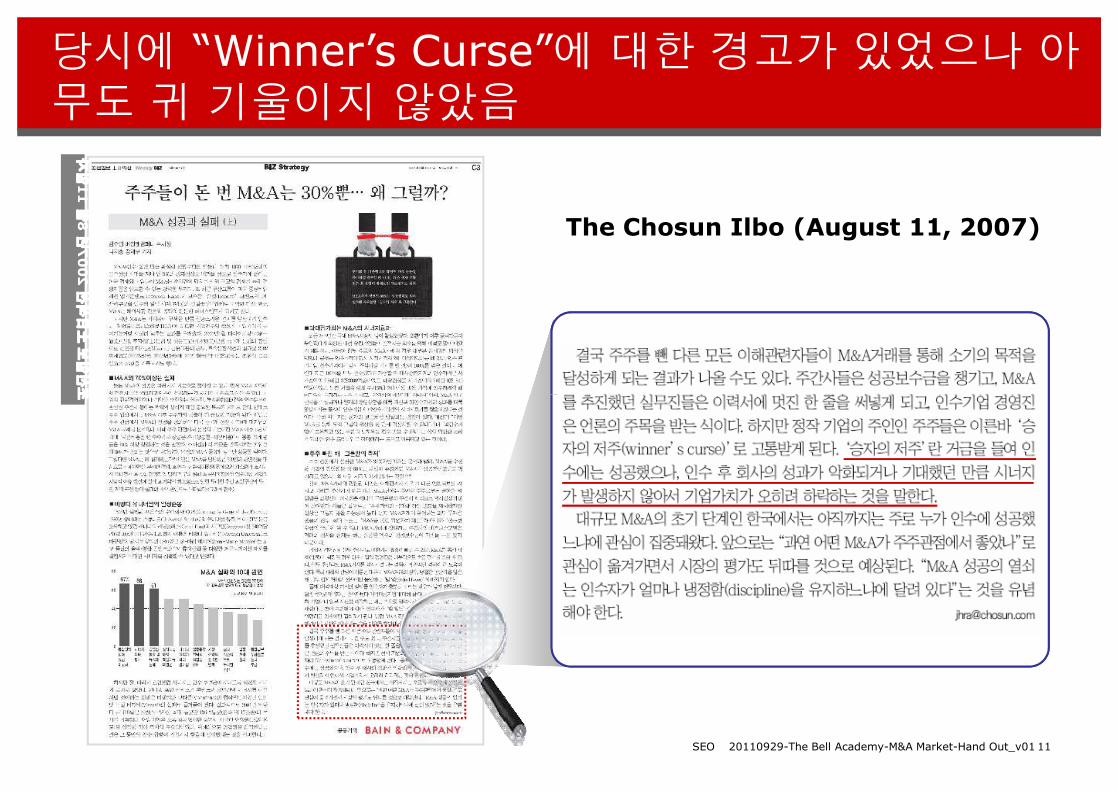

당시에 “Winner’s Curse”에 대한 경고가 있었으나 아무도 귀 기울이지 않았음

조선일보

土日

섹션

2007

년

8

월

11

일자

The Chosun Ilbo (August 11, 2007)

1120110929-The Bell Academy-M&A Market-Hand Out_v01SEO

조선일보

土日

섹션

2007

년

8

월

11

일자

2009년까지만 해도 국내 M&A 시장에서 PEF가 활발한 인수 활동을 보였으나…

Doosan group deal* Distressed

6

Non-coreOriental Brewery1

Yangpoong Mutual Savings Bank Distressed

5

Doosan Soju

Gmarket Non-core

Non-core2

4 TheFaceShop Secondary

3

7

8

On media Non-core

Hana card

49%

100%

86%

29%

100%

90%

55%

49%

308

1,800

323

353

398

362

365

333 Other

Doosan group

Anheuser-Busch InBev

Yangpoong Mutual Savings Bank

InterPark

Doosan Corp

Affinity & Woon-Ho Jung

Owner

Hana Financial Holdings

IMM PE & Mirae Asset MAPS

Affinity & KKR

Tomato Mutual Savings Bank

eBay

Lotte Group

LG Household and Healthcare

CJ O shopping

SK Telecom

Category Target Deal

stake Deal Size(M USD) Seller Buyer

Top 20 M&A deals in 2009

1220110929-The Bell Academy-M&A Market-Hand Out_v01SEONote: *IMM, 미래 에셋은 공동으로 두산 그룹 계열 4개 사에 투자 (Doosan DST, Samhwa Crown & Closure, SRS Korea, Korea Aerospace Industry) Source: AVCJ, Bain analysis

Doosan group deal* Distressed

Kumho Rent-A-Car Distressed

Qrix Holdings Cash-out

10

Jinro

Seoul Express Bus Terminal

Distressed

Distressed

8

9

19

20

BC Card Non-core

11

Daesan Combined Cycle Power Plant Non-core

12

Young Hwa Engineering Cash-out

16

First Fire & Marine Insurance Cash-out

15

Ssangyong Secondary

14

17

18

Novelis Korea Distressed

13

49%

100%

70%

13%

39%

31%

100%

100%

25%

70%

14%

308

250

187

228

232

156

99

84

89

96

97

Doosan group

Kumho Asiana Group

Qrix Holdings

Hite Brewery

Kumho Asiana Group

Hana Bank; SC First Bank

Hyundai Heavy Industries

IMM, I.H. Kim & I.S. Kim

First Fire & Marine Insurance

MSPE

Taihan Electric Wire

IMM PE & Mirae Asset MAPS

KT & MBK

TBroad Holdings

NCUF (National Credit Union Federation Korea)

Core Financial Advisors Group

Vogo Investment

Meiya Power

MBK

Hanwha

GS Holdings

IMM PE

Post restrABCturingHyundai Heavy Industries consortiumKDB,woori bank,creditors50%235Hyundai Corp.

DistressedHotel lotteARD holdings81%237AK global

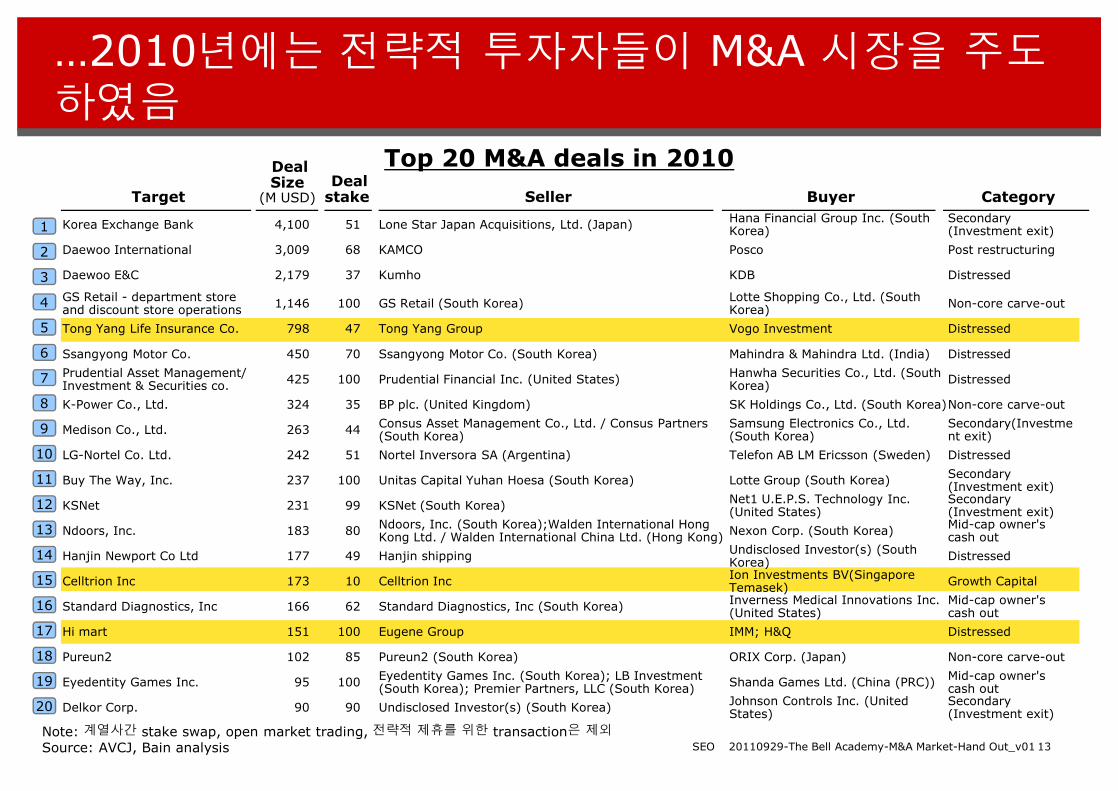

…2010년에는 전략적 투자자들이 M&A 시장을 주도하였음

Top 20 M&A deals in 2010Target

Deal Size

(M USD)Deal

stake Seller Buyer Category

8

7

6

5

3

2

1

4

Non-core carve-outSK Holdings Co., Ltd. (South Korea)BP plc. (United Kingdom)35 324 K-Power Co., Ltd.

DistressedHanwha Securities Co., Ltd. (South Korea)Prudential Financial Inc. (United States)100 425 Prudential Asset Management/

Investment & Securities co.

DistressedMahindra & Mahindra Ltd. (India)Ssangyong Motor Co. (South Korea)70 450 Ssangyong Motor Co.

Non-core carve-outLotte Shopping Co., Ltd. (South Korea)GS Retail (South Korea)100 1,146 GS Retail - department store

and discount store operations

Post restructuringPoscoKAMCO68 3,009 Daewoo International

Secondary (Investment exit)

Hana Financial Group Inc. (South Korea)Lone Star Japan Acquisitions, Ltd. (Japan)51 4,100 Korea Exchange Bank

DistressedKDBKumho372,179Daewoo E&C

DistressedVogo Investment Tong Yang Group47798Tong Yang Life Insurance Co.

1320110929-The Bell Academy-M&A Market-Hand Out_v01SEONote: 계열사간 stake swap, open market trading, 전략적 제휴를 위한 transaction은 제외

Source: AVCJ, Bain analysis

16

14

13

9

8

17

20

10

11

12

15

19

18

Secondary (Investment exit)

Johnson Controls Inc. (United States)Undisclosed Investor(s) (South Korea)90 90 Delkor Corp.

Mid-cap owner's cash outShanda Games Ltd. (China (PRC))Eyedentity Games Inc. (South Korea); LB Investment

(South Korea); Premier Partners, LLC (South Korea)100 95 Eyedentity Games Inc.

Non-core carve-outORIX Corp. (Japan)Pureun2 (South Korea)85 102 Pureun2

DistressedIMM; H&QEugene Group100 151 Hi mart

Mid-cap owner's cash out

Inverness Medical Innovations Inc. (United States)Standard Diagnostics, Inc (South Korea)62 166 Standard Diagnostics, Inc

Growth CapitalIon Investments BV(Singapore Temasek)Celltrion Inc10 173 Celltrion Inc

DistressedUndisclosed Investor(s) (South Korea)Hanjin shipping49 177 Hanjin Newport Co Ltd

Mid-cap owner's cash outNexon Corp. (South Korea)Ndoors, Inc. (South Korea);Walden International Hong

Kong Ltd. / Walden International China Ltd. (Hong Kong)80 183 Ndoors, Inc.

Secondary (Investment exit)

Net1 U.E.P.S. Technology Inc. (United States)KSNet (South Korea)99 231 KSNet

Secondary (Investment exit)Lotte Group (South Korea)Unitas Capital Yuhan Hoesa (South Korea)100 237 Buy The Way, Inc.

DistressedTelefon AB LM Ericsson (Sweden)Nortel Inversora SA (Argentina)51 242 LG-Nortel Co. Ltd.

Secondary(Investment exit)

Samsung Electronics Co., Ltd. (South Korea)

Consus Asset Management Co., Ltd. / Consus Partners (South Korea)44 263 Medison Co., Ltd.

Non-core carve-outSK Holdings Co., Ltd. (South Korea)BP plc. (United Kingdom)35 324 K-Power Co., Ltd.

Top 20 M&A deals in 2011.1HDeal Size

(M USD)Deal

stake Seller Buyer Target Category

7

6

5

3

2

1

4

Hyundai E&C 4,440 35Hana Bank; Hyundai Securities; Kookmin Bank;Korea Exchange Bank; Korea Finance Corporation;NACF; Shinhan Bank; Woori Bank

Hyundai Mobis; Hyundai Motor;Kia Motors Post restructuring

Korea Digital Satellite Broadcasting(SkyLife) 222 14 Affinity Equity Partners KT Corp. Investment exit

BC Card Co., Ltd. 209 34 Shinhan Bank; Woori Bank KT Capital Non-core carve-out

Samsung Medison Co., Ltd. 145 22 Korea Credit Guarantee Fund Samsung Electronics Post restructuring

Doosan Industrial Vehicle 111 49 Doosan Infracore Co., Ltd. Standard Chartered PE Non-core carve-out

Hyundai Logiem Co. Ltd. 90 33 Hyundai Logiem Co. Ltd. Woori Blackstone PEF Growth Capital

Ymir Entertainment Co. Ltd. 69 100 Ymir Entertainment Co. Ltd. Webzen Inc. Mid-cap owner's cash out

2011년 상반기에는 현대건설 매각 딜 한건이 전체M&A시장 규모의 70%이상을 차지하였음

1420110929-The Bell Academy-M&A Market-Hand Out_v01SEO

16

14

13

9

8

7

17

20

10

11

12

15

19

18

Ymir Entertainment Co. Ltd. 69 100 Ymir Entertainment Co. Ltd. Webzen Inc. Mid-cap owner's cash out

Techno Semichem Co. Ltd. 53 N/A Techno Semichem Co. Ltd. STIC Investments Growth capital

KT Telecop Corp. 48 24 KT Telecop Corp. KB Investment Growth Capital

Seil Seres Co. Ltd. 47 100 Undisclosed Seller(s) KSB AG (Germany) Mid-cap owner's cash out

Daehan Paper Tech Co. Ltd. 44 100 Daehan Paper Tech Co. Ltd. Hansol Paper Co Ltd Mid-cap owner's cash out

Doosan Capital Co., Ltd. 44 29 Doosan Capital Co., Ltd. Hana Daetoo IB - PE; IMM;Mirae Asset PE Growth Capital

Hana Micron Inc. 42 17 Hana Micron Inc. H&Q Asia Pacific Growth capital

Unison HiTech Co., Ltd. 40 100 Unison Co., Ltd. (South Korea) Headland Capital Partners Non-core carve-out

Nexolon Co., Ltd. 36 N/A Nexolon Co., Ltd. IBK Capital; Korea Finance Corp. Growth capital

Indilinx, Inc. 35 100 Indilinx, Inc. (South Korea) OCZ Technology Group, Inc. Mid-cap owner's cash out

Leenos Corp. 35 32 Wok-kyu Lee KTB Securities Mid-cap owner's cash out

Korea Rental Corp. 35 13 Korea Rental Corp. (South Korea) Is Dongseo Co. Ltd. Distressed

Chungbuk Soju Co., Ltd. 31 100 Chungbuk Soju Co., Ltd. (South Korea) Lotte Chilsung Beverage Mid-cap owner's cash out

KG Eco Services Korea 28 40 KG Eco Services Korea Eugene Asset Management Growth capital

Note: Excluded stake swap among affiliates, open market trading, transaction for strategic partnershipSource: AVCJ, Bain analysis

4

₩6T

4.1 4.0

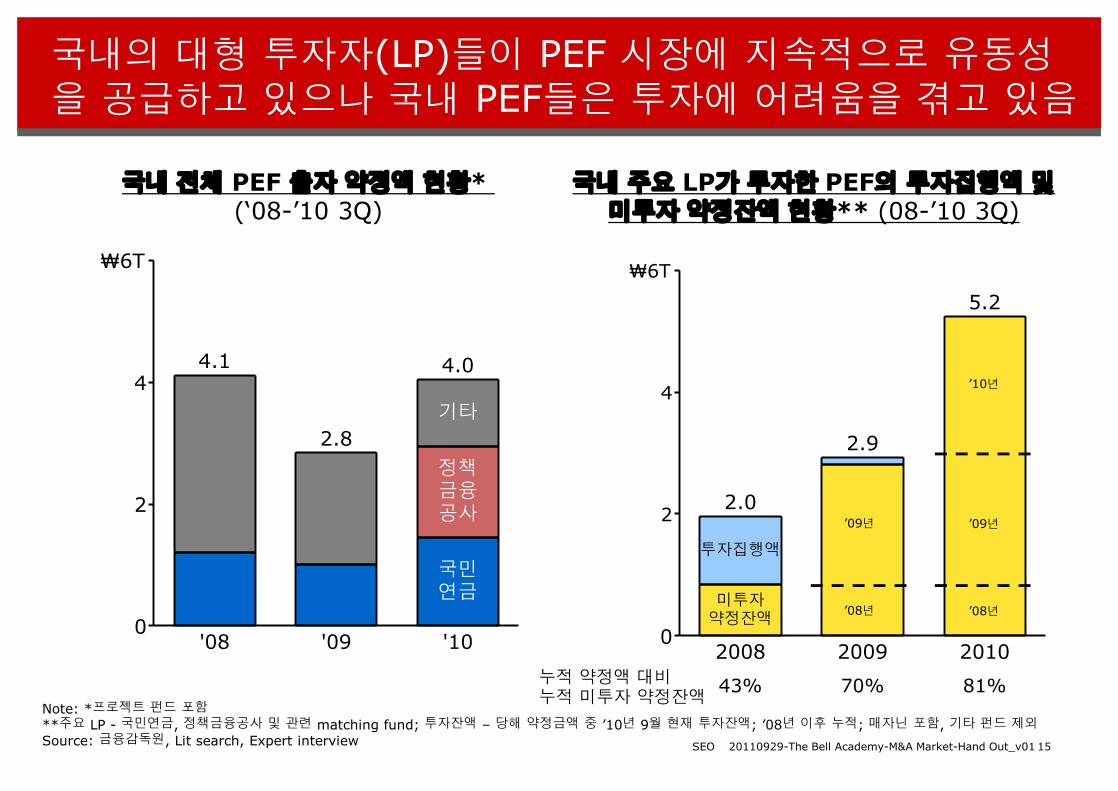

국내의 대형 투자자(LP)들이 PEF 시장에 지속적으로 유동성을 공급하고 있으나 국내 PEF들은 투자에 어려움을 겪고 있음

4

₩6T

5.2

국내 전체 PEF 출자 약정액 현황*(‘08-’10 3Q)

국내 주요 LP가 투자한 PEF의 투자집행액 및미투자 약정잔액 현황** (08-’10 3Q)

’10년

1520110929-The Bell Academy-M&A Market-Hand Out_v01SEO

0

2

'08 '09

2.8

'10

기타

정책금융공사

국민연금

0

2

4

2008

투자집행액

미투자약정잔액

2.0

2009

2.9

2010

43% 70% 81%누적 약정액 대비누적 미투자 약정잔액

Note: *프로젝트 펀드 포함

**주요 LP - 국민연금, 정책금융공사 및 관련 matching fund; 투자잔액 – 당해 약정금액 중 ’10년 9월 현재 투자잔액; ’08년 이후 누적; 매자닌 포함, 기타 펀드 제외

Source: 금융감독원, Lit search, Expert interview

’08년

’09년

’08년

’09년

향후, PE capital overhang 현상을 고려시, 재무투자자와의 인수 경쟁도 다시 심화될 것으로 전망됨

사모 펀드가 인수한 국내 M&A 시장 규모 (’97-’10)

’10년 capital overhang약 7조 원*

PE 딜 갯수

글로벌 PEF국내 PEF

5

6

7

30

40

4.5

PE 딜 규모 (조원) PE 딜 갯수 (개)

1620110929-The Bell Academy-M&A Market-Hand Out_v01SEO

* 주요 LP의 ‘08-’10 출자 약정액 (전체 출자 약정액의 약 75% 차지) 중 누적 dry powder 규모를 통해 capital overhang 추산

Note: 인수 대상이 국내 기업인 경우만 포함, 토지, 설비, 부동산 매각 관련 딜은 제외

Source: AVCJ, Bain Analysis

‘08~’10년 PEF 출자약정액 총계:

약 11조 원0

1

2

3

4

0

10

20

'97 '98

1.0

'99

0.9

'00

2.2

'01

1.7

'02

1.6

'03

2.7

'04

1.7

'05

2.5

'06

1.8

'07 '08

3.4

'09

3.5

'10

1.5

0.00 0.47 1.67 1.56 1.23 1.210.01 0.00 0.05 0.13 0.02 0.02 0.58 0.30국내 PEF deal 규모

0 8 23 21 20 81 0 2 3 2 2 5 7국내 PEF deal 갯수

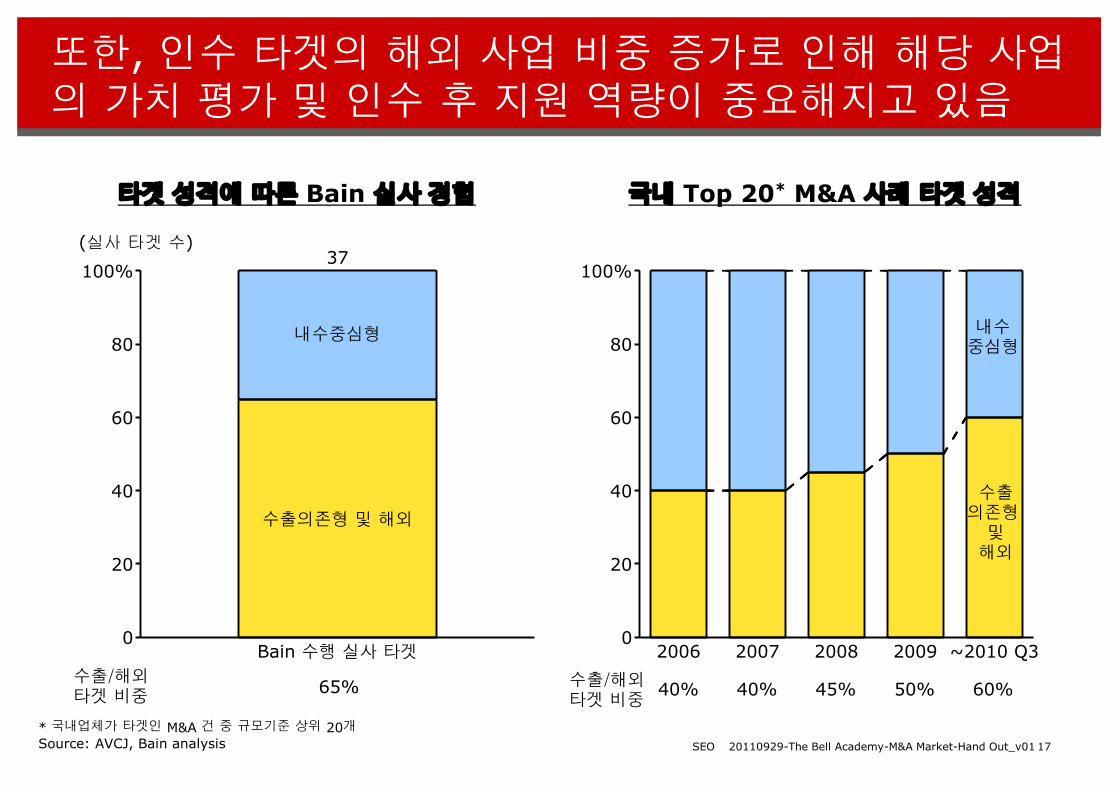

또한, 인수 타겟의 해외 사업 비중 증가로 인해 해당 사업의 가치 평가 및 인수 후 지원 역량이 중요해지고 있음

80

100%

내수중심형

37(실사 타겟 수)

타겟 성격에 따른 Bain 실사 경험

80

100%

내수중심형

국내 Top 20* M&A 사례 타겟 성격

1720110929-The Bell Academy-M&A Market-Hand Out_v01SEO

0

20

40

60

Bain 수행 실사 타겟

수출의존형 및 해외

65%수출/해외타겟 비중

0

20

40

60

2006 2007 2008 2009 ~2010 Q3

수출의존형

및해외

40% 40% 45% 50% 60%수출/해외타겟 비중

* 국내업체가 타겟인 M&A 건 중 규모기준 상위 20개

Source: AVCJ, Bain analysis

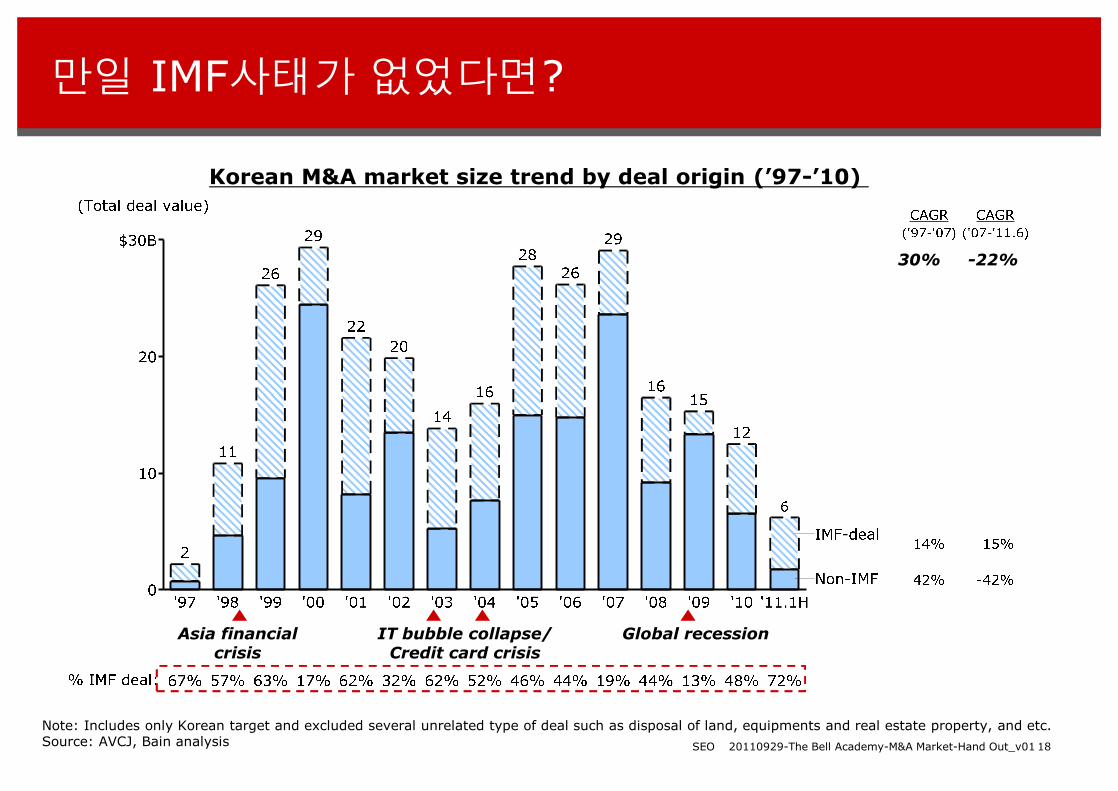

만일 IMF사태가 없었다면?

Korean M&A market size trend by deal origin (’97-’10)

30% -22%

1820110929-The Bell Academy-M&A Market-Hand Out_v01SEO

IT bubble collapse/Credit card crisis

Note: Includes only Korean target and excluded several unrelated type of deal such as disposal of land, equipments and real estate property, and etc.Source: AVCJ, Bain analysis

Asia financial crisis

Global recession

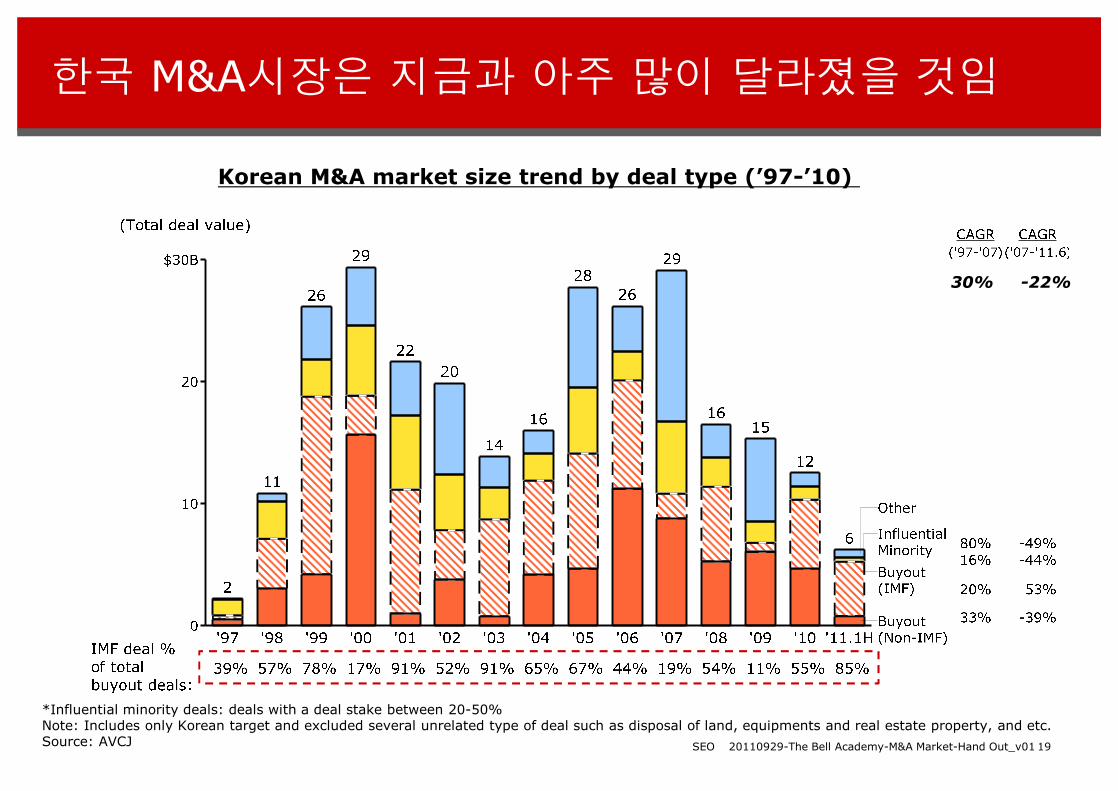

한국 M&A시장은 지금과 아주 많이 달라졌을 것임

Korean M&A market size trend by deal type (’97-’10)

30% -22%

1920110929-The Bell Academy-M&A Market-Hand Out_v01SEO

*Influential minority deals: deals with a deal stake between 20-50%Note: Includes only Korean target and excluded several unrelated type of deal such as disposal of land, equipments and real estate property, and etc.Source: AVCJ

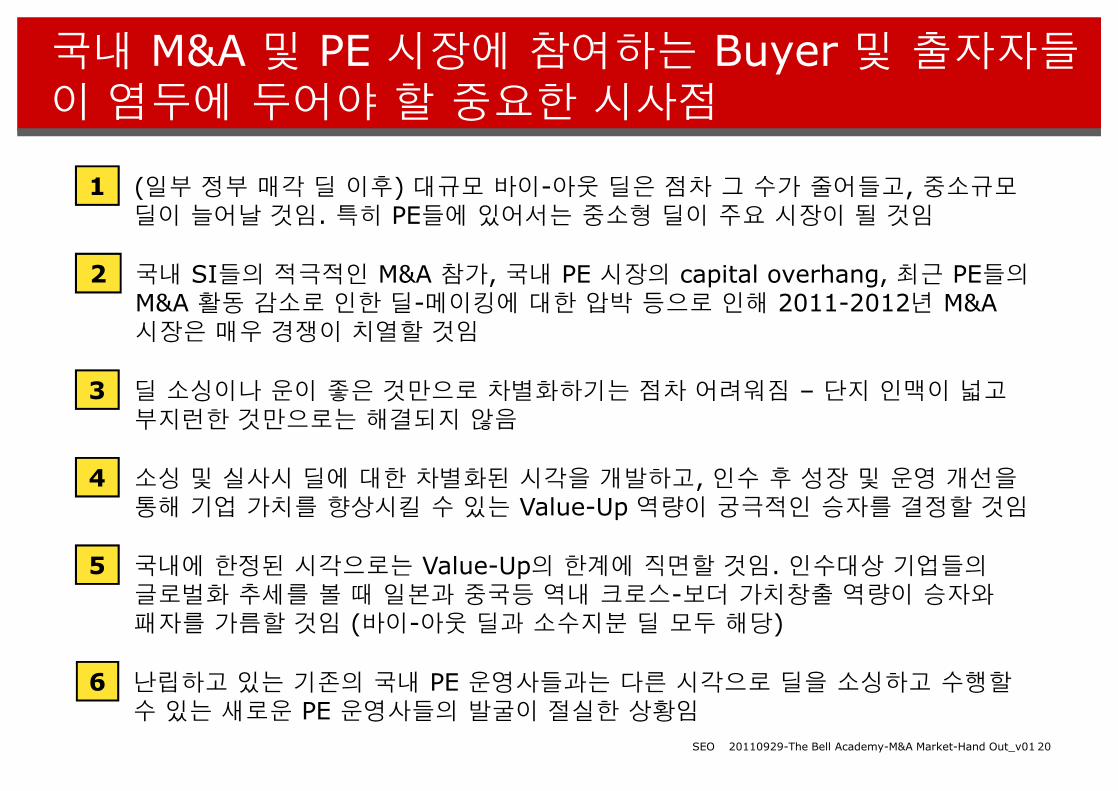

국내 M&A 및 PE 시장에 참여하는 Buyer 및 출자자들이 염두에 두어야 할 중요한 시사점

• (일부 정부 매각 딜 이후) 대규모 바이-아웃 딜은 점차 그 수가 줄어들고, 중소규모딜이 늘어날 것임. 특히 PE들에 있어서는 중소형 딜이 주요 시장이 될 것임

1

• 국내 SI들의 적극적인 M&A 참가, 국내 PE 시장의 capital overhang, 최근 PE들의M&A 활동 감소로 인한 딜-메이킹에 대한 압박 등으로 인해 2011-2012년 M&A 시장은 매우 경쟁이 치열할 것임

2

• 딜 소싱이나 운이 좋은 것만으로 차별화하기는 점차 어려워짐 – 단지 인맥이 넓고부지런한 것만으로는 해결되지 않음

3

2020110929-The Bell Academy-M&A Market-Hand Out_v01SEO

• 딜 소싱이나 운이 좋은 것만으로 차별화하기는 점차 어려워짐 – 단지 인맥이 넓고부지런한 것만으로는 해결되지 않음

3

• 소싱 및 실사시 딜에 대한 차별화된 시각을 개발하고, 인수 후 성장 및 운영 개선을통해 기업 가치를 향상시킬 수 있는 Value-Up 역량이 궁극적인 승자를 결정할 것임

4

• 국내에 한정된 시각으로는 Value-Up의 한계에 직면할 것임. 인수대상 기업들의글로벌화 추세를 볼 때 일본과 중국등 역내 크로스-보더 가치창출 역량이 승자와패자를 가름할 것임 (바이-아웃 딜과 소수지분 딜 모두 해당)

5

난립하고 있는 기존의 국내 PE 운영사들과는 다른 시각으로 딜을 소싱하고 수행할수 있는 새로운 PE 운영사들의 발굴이 절실한 상황임

6

![[기아워캠9기] 김수민 활동결과보고_독일 IJGD14238](https://img.pdfslide.net/doc/110x75/55b63997bb61ebe60f8b46d7/9-ijgd14238.jpg)