Embed Size (px)

Citation preview

1

A Comparative View on Financial Transfers in Canada and the EU

Isabella Eiselt Institut d’études européennes (Université de Montréal/McGill University)

Working Paper prepared for the ECSA-C Conference in Edmonton/Alberta September 25-27, 2008

Work in progress – please do not cite without permission

2

1.Introduction The main subject of this paper is a comparison of central governmental budgetary policy in Canada and the EU. Inspired by theories on fiscal federalism it starts from the preposition that financial arrangements between provinces/states and the central government form the heart of intergovernmental relations. In general, it is held that economic considerations of optimal allocation of competencies and resources tend to overlook that politics is at the center of fiscal federalism. As Bruno Théret notes “(l)’approche économique normative est tout particulièrement inadaptée pour traiter du fédéralisme dans la mesure même où celui-ci est un principe d’allocation du pouvoir politique qui précisement nie les présupposés monistes et individualistes de la théorie standard, destiné qu’il est à prendre en charge sous une forme unitaire, mais sans faire table rase de ces différenciations, la diversité des identités individuelles et collectives et la pluralité des rationalités.” (Théret 2002: 62). And: “Federal-provincial fiscal arrangements are much more than an economic issue. How financial and administrative responsibilities are allocated between governments is a central political question. The answer to this question reflects a country’s style, its concerns, and its goals.” (Bird 1990: 109, as cited in: Milne 1994: 175). Decisions on why and how to transfer funds between levels of government are salient issues of intergovernmental cooperation. The major question within the framework of this paper is: How do intergovernmental transfers frame cooperation within the federative structures of Canada and the EU? Thus, the comparative perspective on the role of central governmental budgets is focused on the institutional setting that predisposes and frames intergovernmental relations. It is the general theoretical outlook of this study that formal structures of state power do matter in terms of shaping and even predisposing political cooperation and conflict. Moreover, within federative organizations of power relations, formal institutional settings are, at the same time, source and outcome of a normative discussion of the value of intergovernmental cooperation. As point of departure it has been assumed that institutionalization respectively centralization of budgetary activity at the supranational level of the European Union would lead to strengthened political cooperation and unity in a multicultural environment and eventually promote its federal development. The successful administration of common issues was meant to trigger common values that overhaul the divisive forces inherent in societal and cultural traditions of constituent units of a multinational federation. Furthermore, it was held that the more institutionalized fiscal federal arrangements are, the more stable a federal union is, and the more effective it can work. This theoretical inclination remains valid throughout the paper, although the empirical validation sustains the frequently observed fact that simply equating one specific set of institutional arrangements with specific outcomes in terms of intensity of cooperation and conflict, power relations and normative statements on the value of intergovernmental cooperation is not possible (Bird 1994: 297). The article proceeds as follows: The first chapter presents the basic systemic features of the financial transfer system in Canada and the EU, primarily facts and figures on financial means, institutions and processes. The second chapter opposes the basic characteristics of the two transfer systems: unconditionality versus conditionality of transfers, formula-based calculations versus political

3

bargaining, informal versus formal institutionalization of intergovernmental cooperation. A preliminary conclusion tries to assess the lessons learned from the Canadian experience in intergovernmental cooperation on budgetary policy and financial transfers. 1. Basic Features In most cases, the institutions of intergovernmental fiscal relations in Canada do not have a legal base. However, there are long-lasting mostly centrally administered fiscal arrangements, and fiscal federal politics in general shows an impressive low level of structural conflict. In contrast, in the European Union, intergovernmental relations are strongly institutionalized, and budgetary politics and fiscal federal transfers in particular rely on formal decision-making procedures and strict control mechanisms. The intergovernmental decision-making procedures involve a plurality of actors and the recurrent debates on the multiannual budgetary framework represent particularly high points of intergovernmental battles. Canada is an example for ad hoc and informal arrangements of fiscal federal relations that primarily rely on central initiative. The EU represents a highly institutionalized fiscal federal regime where major decisions are taken by the member states. The examination of the Canadian fiscal federal transfer system revealed not only that institutionalization may not improve an intergovernmental cooperation system that relies on ad hoc meetings, case-by-case arrangements or tacit understandings but it may contrary to theoretical expectations harden conflict lines and worsen the cooperative climate. It is most important to keep in mind that this comparative exercise is focused on features of intergovernmental cooperation on budgetary issues and intergovernmental financial transfers within federal or, in the case of the EU, quasi-federal political structures1. The Canadian federal budget as such is not comparable to the EU budget. But the comparison conducted in this study is not primarily about the quantity and structure of the central governmental budgets but their role in the midst of a framework of intergovernmental relations. Obviously, the political aspect of federal-provincial/state transfers is most interesting in this regard. Whereas the EU budget and its financial transfers rely on more or less direct contributions from its member states, the Canadian budget depends on federal tax incomes. Thus, the central governmental level in Canada is much more independent from provincial interference when it comes to decide on financial transfers and federal budgetary preferences. On the other hand, federal interference into provincial policies has become a particular sensitive issue in federal-provincial relations in recent years and so has intergovernmental cooperation.2 In the EU, intergovernmental cooperation is an essential condition for policy development and administration. As regards budgetary policy, intergovernmental consent is all the more important as the major part of the financial resources depends on the goodwill of the member states’ governments. Compared to the situation in Canada, we see a reversed picture. The central governmental level is dependent on the constituent units when it comes to decide on financial arrangements. Thus, a well functioning intergovernmental cooperative climate is crucial for budgetary development and the design of supranational policy.

1 See for assessments of the federal quality of the European Union inter alia Théret 2002, Nicolaidis/Howse 2001, Menon/Schain 2006. 2 See for developments of intergovernmental relations in Canada Choudry/Gaudreault-DesBiens/Sossin 2006, Lazar 2005, Meekison/Telford/Lazar 2004, Simeon/Papillon 2006, Banting/Brown/Chourchene 1994. Brown/Courchene 1994).

4

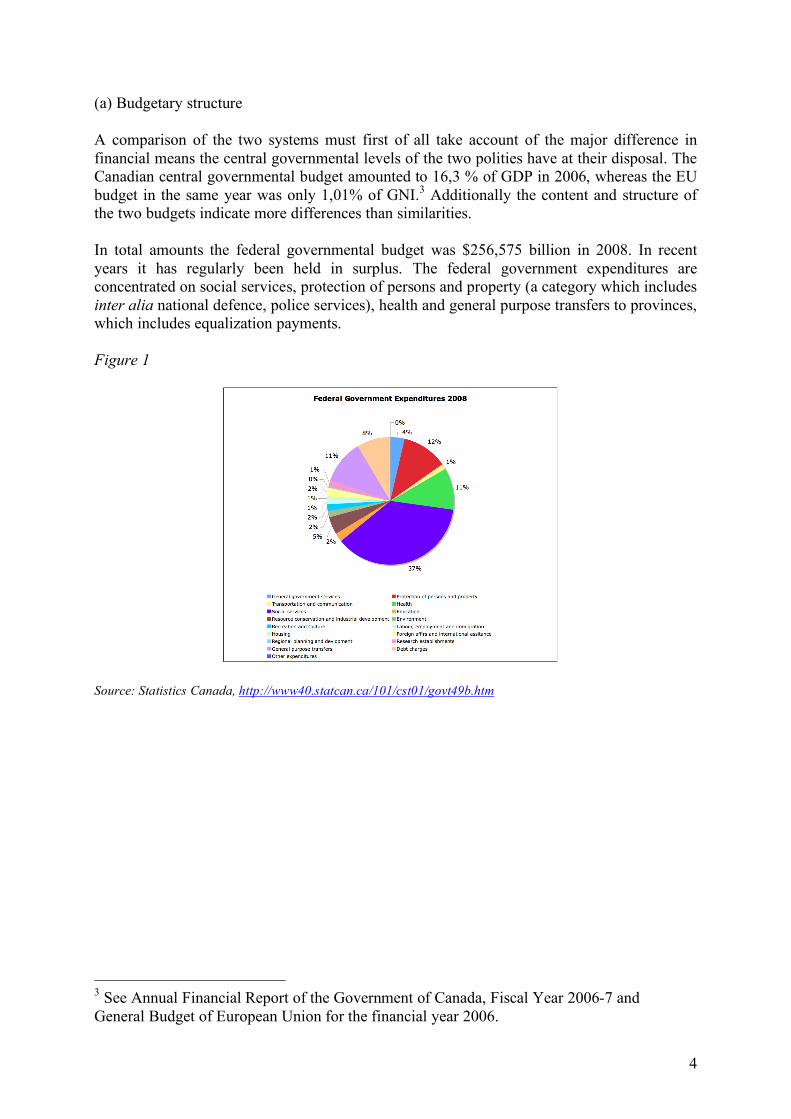

(a) Budgetary structure A comparison of the two systems must first of all take account of the major difference in financial means the central governmental levels of the two polities have at their disposal. The Canadian central governmental budget amounted to 16,3 % of GDP in 2006, whereas the EU budget in the same year was only 1,01% of GNI.3 Additionally the content and structure of the two budgets indicate more differences than similarities. In total amounts the federal governmental budget was $256,575 billion in 2008. In recent years it has regularly been held in surplus. The federal government expenditures are concentrated on social services, protection of persons and property (a category which includes inter alia national defence, police services), health and general purpose transfers to provinces, which includes equalization payments. Figure 1

Source: Statistics Canada, http://www40.statcan.ca/101/cst01/govt49b.htm

3 See Annual Financial Report of the Government of Canada, Fiscal Year 2006-7 and General Budget of European Union for the financial year 2006.

5

Figure 2

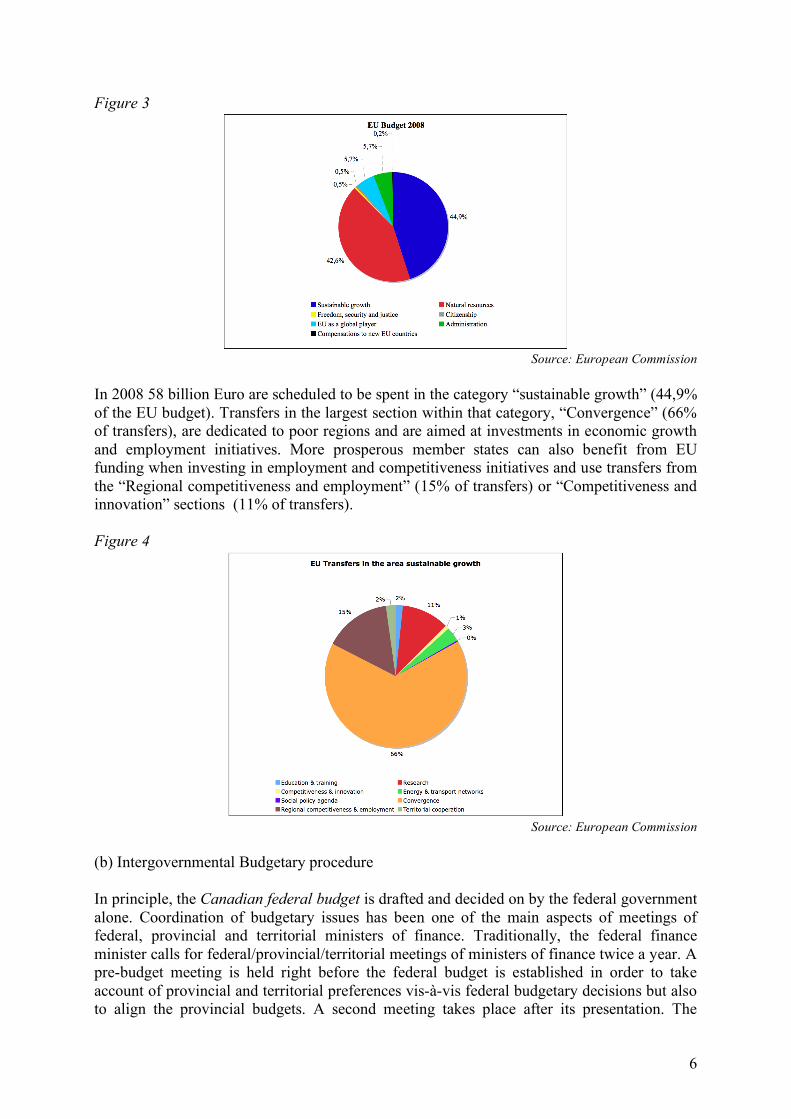

Source: Department of Finance Canada, http://www.fin.gc.ca/FEDPROV/mtpe.html In 2008, the major part of the Canadian federal financial transfers to the provinces was dedicated to the Canada Health and Social Transfer (CHST) (66%). 27% were spent as unconditional equalization payments, 5% entered into the Territorial Formula Financing Programme and 2% were spent under newly installed Offshore Accords. Again for 2008, the actual amounts were $33,2 billion for Canada Health and Social Transfer (CHST), $13,6 billion for Equalization, $2,3 billion for Territorial Formula Financing and $0,8 billion for Offshore Accords. The EU budget may be classified as a total as transfers between the central and the state level, although spending in the section “sustainable growth” comes closest to what can be referred to as federal financial transfers from the central governmental level to the member states. That category will be referred to when comparing institutional features of intergovernmental cooperation in the remainder of the paper. In 2008 the EU budget amounted to 129,1 billion Euro. Budgetary rules laid down in treaty law do not allow a budgetary deficit. The major part of EU central governmental spending (44,9%) is dedicated to projects referred to as promoting “sustainable growth”, i.e. that enhance competitiveness of the European economy and strengthen cohesion measured in terms of economic growth. Supported policy fields are inter alia education and training, research and innovation, energy and transport networks, and social policy issues. As far as cohesion is the objective of spending within that category, projects are concentrated in industrial development, interstate business cooperation and regional economic restructuring. The second most developed EU spending program (“Natural Resources”, 42,6%) supports the agricultural sector and the environment. Spending in the area called “EU as a global player” concerns EU foreign and security policy issues, such as the European neighborhood policy, development cooperation, humanitarian aid, and pre-accession aid. Minor parts of the budget are spent on projects in the realm of internal security and judicial policies (“Freedom, Security and Justice”) and public health, consumer protection and cultural policies (“Citizenship”). 5,7% of the 2008 budget are administration costs.

6

Figure 3

Source: European Commission

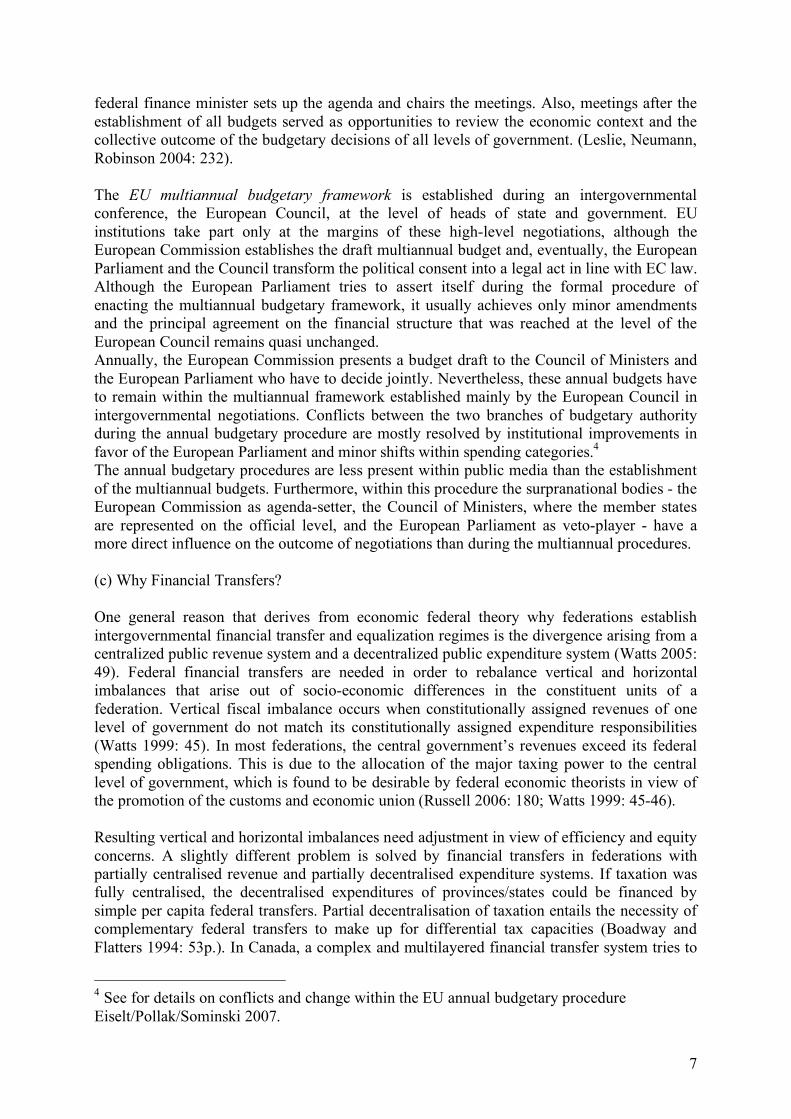

In 2008 58 billion Euro are scheduled to be spent in the category “sustainable growth” (44,9% of the EU budget). Transfers in the largest section within that category, “Convergence” (66% of transfers), are dedicated to poor regions and are aimed at investments in economic growth and employment initiatives. More prosperous member states can also benefit from EU funding when investing in employment and competitiveness initiatives and use transfers from the “Regional competitiveness and employment” (15% of transfers) or “Competitiveness and innovation” sections (11% of transfers). Figure 4

Source: European Commission

(b) Intergovernmental Budgetary procedure In principle, the Canadian federal budget is drafted and decided on by the federal government alone. Coordination of budgetary issues has been one of the main aspects of meetings of federal, provincial and territorial ministers of finance. Traditionally, the federal finance minister calls for federal/provincial/territorial meetings of ministers of finance twice a year. A pre-budget meeting is held right before the federal budget is established in order to take account of provincial and territorial preferences vis-à-vis federal budgetary decisions but also to align the provincial budgets. A second meeting takes place after its presentation. The

7

federal finance minister sets up the agenda and chairs the meetings. Also, meetings after the establishment of all budgets served as opportunities to review the economic context and the collective outcome of the budgetary decisions of all levels of government. (Leslie, Neumann, Robinson 2004: 232). The EU multiannual budgetary framework is established during an intergovernmental conference, the European Council, at the level of heads of state and government. EU institutions take part only at the margins of these high-level negotiations, although the European Commission establishes the draft multiannual budget and, eventually, the European Parliament and the Council transform the political consent into a legal act in line with EC law. Although the European Parliament tries to assert itself during the formal procedure of enacting the multiannual budgetary framework, it usually achieves only minor amendments and the principal agreement on the financial structure that was reached at the level of the European Council remains quasi unchanged. Annually, the European Commission presents a budget draft to the Council of Ministers and the European Parliament who have to decide jointly. Nevertheless, these annual budgets have to remain within the multiannual framework established mainly by the European Council in intergovernmental negotiations. Conflicts between the two branches of budgetary authority during the annual budgetary procedure are mostly resolved by institutional improvements in favor of the European Parliament and minor shifts within spending categories.4 The annual budgetary procedures are less present within public media than the establishment of the multiannual budgets. Furthermore, within this procedure the surpranational bodies - the European Commission as agenda-setter, the Council of Ministers, where the member states are represented on the official level, and the European Parliament as veto-player - have a more direct influence on the outcome of negotiations than during the multiannual procedures. (c) Why Financial Transfers? One general reason that derives from economic federal theory why federations establish intergovernmental financial transfer and equalization regimes is the divergence arising from a centralized public revenue system and a decentralized public expenditure system (Watts 2005: 49). Federal financial transfers are needed in order to rebalance vertical and horizontal imbalances that arise out of socio-economic differences in the constituent units of a federation. Vertical fiscal imbalance occurs when constitutionally assigned revenues of one level of government do not match its constitutionally assigned expenditure responsibilities (Watts 1999: 45). In most federations, the central government’s revenues exceed its federal spending obligations. This is due to the allocation of the major taxing power to the central level of government, which is found to be desirable by federal economic theorists in view of the promotion of the customs and economic union (Russell 2006: 180; Watts 1999: 45-46). Resulting vertical and horizontal imbalances need adjustment in view of efficiency and equity concerns. A slightly different problem is solved by financial transfers in federations with partially centralised revenue and partially decentralised expenditure systems. If taxation was fully centralised, the decentralised expenditures of provinces/states could be financed by simple per capita federal transfers. Partial decentralisation of taxation entails the necessity of complementary federal transfers to make up for differential tax capacities (Boadway and Flatters 1994: 53p.). In Canada, a complex and multilayered financial transfer system tries to

4 See for details on conflicts and change within the EU annual budgetary procedure Eiselt/Pollak/Sominski 2007.

8

compensate for these imbalances arising from differential provincial/state tax capacities in a federation with decentralised taxation. The Canadian system of unconditional equalization payments can be viewed as interpersonal redistribution measures or as compensatory payments that take account of differing revenue situation of provinces within the decentralised taxation system in the federation. In terms of efficiency fiscal transfers may be particularly important in ensuring efficient allocation. Allocative inefficiencies are caused when people/tax payers/human resources leave or enter a federative unit only because of expected net fiscal benefits arising from different provincial/state fiscal capacities. Net fiscal benefits occur due to variations of provincial activities in providing public goods. They may be positive, if residents benefit from provincially provided public goods whose costs exceed their contributions through provincial taxes. They are negative if the province taxes more than it gives back in public goods. In order to avoid fiscally induced migration that would disturb the efficient allocation of resources, net fiscal benefits should be equalized across provinces (Coucherne 1984: 94). However, in order to offset differences in individual net fiscal benefits, transfer payments would have to be dispersed ad personam. These explanations for financial transfers and equalizing payments are less of concern to the EU, which does not dispose of central taxing powers. Only its “own resources”, i.e. some indirect taxes (custom duties and agricultural levies and duties) that make up a minor part of the EU revenues are levied centrally. Another share of the EU budget revenue is levied on the basis of member states’ value-added tax (VAT). The member states transfer part of their VAT revenue (calculated from a standardised VAT base) to the central level. Other revenue is provided directly by the member states on the basis of their GNI. The latter makes up for the majority of funds available to the EU budget. The “Lamassoure report” on the future of EU own resources proposed inter alia a tax rental system for the EU. The member states should authorize the EU to raise part of their tax money for itself (Lamassoure report 2006: 14). Taxes that were considered as possible EU own resources are VAT, energy taxes (gasoline and others), consumption taxes on tobacco and alcohol, corporate profit taxes. Various other sources are under discussion. However, the maintenance of fiscal autonomy is in the special interest of the more affluent member states, and actually none of the member states seems to be prepared to cede tax authority to the supranational level in the EU. Additional to economic considerations there are political reasons for financial transfers and equalization payments that are also valid for the EU. Further integration or enlargement of the Community has always been accompanied by compensation payments to poorer member states. The deepening of integration would not have been possible without financial transfers. It is however not the supranational level, the Commission, the EP and the Council, that provides the financial resources for that compensation. It is more an interstate transfer system than a federal transfer system considered that, although the central level distributes the funds, the decision about what amount and how the money will be spent lies with the member states5.

5 This may be on the verge of changing in the near future: Only recently the EP has asserted itself as the second branch of the EU budgetary authority. In the course of the debate on budgetary reform taking place 2008/09 it may be on the forefront of a more federal/central

9

2. Institutional Characteristics Federal-provincial transfers in Canada

• are mostly unconditional or only loosely conditioned. • mainly aim at a comparable level of public services as opposed to an equal standard of

public goods. • are mostly decided on at the level of the federal government without significant

influence by the provincial governments. EU transfers

• are mostly strictly conditional • mainly aim at economic development and growth • are decided in intergovernmental negotiations.

The rationale for intergovernmental transfers is set out in the 1982 Constitution Act of Canada (Boadway and Flatters 1994: 60) where equalization as a constitutional obligation of the federal parliament and government is enshrined in Section 36: (1) Without altering the legislative authority of Parliament or of the provincial legislatures, or the rights of any of them with respect to the exercise of their legislative authority, Parliament and the legislatures, together with the government of Canada and the provincial governments, are committed to

a. promoting equal opportunities for the well-being of all Canadians; b. furthering economic development to reduce disparity in opportunities; an c. providing essential public services of reasonable quality to all Canadians.

(2) Parliament and the government of Canada are committed to the principle of making equalization payments to ensure that provincial governments have sufficient revenues to provide reasonably comparable levels of public services at reasonably comparable levels of taxation. As it has been mentioned above, the most important part of the Canadian federal financial transfers is the Canadian Health and Social Transfers (CHST) that makes up 66% of all transfers. However, since the EU has not yet established a significant financially equipped health and social policy at the supranational level, the comparative exercise executed here will primarily focus on the Canadian equalization system. The cohesion funds or transfers committed in the category “sustainable growth” are the comparative counterparts within the EU system of financial transfers. A basic feature of the Canadian equalization program is its focus on the equality of revenue capacity without taking account of variations in expenditure needs (Watts 1999: 118). In contrast, the EU transfer system is strategically oriented towards expenditure needs that cannot or otherwise would not be fulfilled by a member state. The focus on expenditure needs adds complexity to a transfer system in many ways. It has to be decided what a necessity is and who is able to decide on what a necessity is. Common measures of expenditure need have to be found, and most importantly the “common interest” of these expenditure needs must be visible and justifiable as far as not everyone will benefit directly from these transfers.

development of EU budgetary politics (“Report on the future of the European Union’s own resources” (2006/2205 (INI)), PE 382.623, hereinafter Lamassoure report 2006).

10

The EU financial transfers find its basis in Art. 158 of the Treaty establishing the European Community: In order to promote its overall harmonious development, the Community shall develop and pursue its actions leading to the strengthening of its economic and social cohesion. In particular, the Community shall aim at reducing disparities between the levels of development of the various regions and the backwardness of the least favoured regions or islands, including rural areas. As far as the Canadian transfer system is based on provincial governments’ tax revenues it follows the compensation rationale. In contrast, the EU system of cohesion payments is measured against GDP figures. The payments may not amount to more than 4% of the national GDP of the recipient country. Also, in order to become eligible for cohesion funds payments, the member state must not reach 90% of the average EU GDP. For structural funds payments this threshold applies to regional GDP and is set at 75%. (a) Conditionality versus unconditionality The most important difference between financial transfers in the EU and Canada is conditionality. In principle, Canadian federal-provincial transfers are only loosely conditional. Although the major part of financial transfers, the Canadian Health and Social Transfer, must be invested in provincial health and social policy, the respective conditions are formulated in a general way and focus primarily on the obligation of provincial governments to conform provincial health and social policy to relevant federal law. As far as equalization payments are concerned, the federal transfers are entirely unconditional. The objective of these transfers is the actual adjustment of provincial revenues to a level that guarantees theoretically a comparable level of public service provision across Canada. It neither is specified what kind or quality of public services should be provided by the provincial government using equalization money, nor can or does the federal sponsor control the actual employment of the funds. In contrast to aligning policy outcomes, which is the general objective of health and social transfers, the equalization transfers aim at harmonizing the financial resources of provincial governments. The framework conditions of the CHST conflict in principle with the exclusive provincial competencies in the area of health, welfare and education. However, the federal government was successful in arguing their legal admissibility as far as the condition did not foresee that it engages directly in program provision. Furthermore, as mentioned above, the 1982 Constitution Act, section 36 explicitly provided for federal responsibilities in equalization and regional disparities and, hence, the use of the federal spending power has a legal base (Boadway and Flatters 1994: 43). In contrast, EU financial transfers are 100% conditional and the adherence of the recipients of funding to strictly specified conditions is closely examined ex-ante and ex-post. Most of the spending that occurs as EU-member state transfer is set out as a co-financing scheme, i.e. the receiving state must not only present an appropriate project according to EU financing priorities, but also engage itself into the project by bearing part of the cost. Co-financing of EU transfers is comparable to shared-cost programs in the early period of social policy funding in Canada (since the 1950s). Cost-sharing as a major federal policy instrument in Canada was replaced by block-funding in the form of the Canada Health and Social Transfer (CHST) only in 1995 (Noël 2001:10). Although this meant less money for the provinces and provincial governments faced difficulties in adjusting to less federal financial assistance during times of growing financial needs in social policies, they gained significant autonomy

11

in adjusting social and health programs to provincial needs within the general framework of federal law. While control of the use of the transfers plays a minor role in Canada, in particular as concerns equalization transfers, the EU has engaged in a transparency initiative as regards its financial activities. Recently it has started to publish the actual amounts each member states gets out of the EU budget, and to list the projects that received EU funding. That trend to more transparency may be accompanied by a general move to less detailed conditionality in EU financial transfers. The new programming period that conforms to the multi-annual financial perspective 2007-2013 foresees that member states’ authorities under general supervision of the Commission execute management and control of funds. In general, it was held that unconditional financial transfers may face criticism and needs for justification more likely than conditional transfers, e.g. in the area of health policy (Choudry 2006: 49). Most commonly, arguments against unconditional fiscal transfers are based on financial responsibility and accountability: Control of taxpayers’ money was only ensured if the funds are to be used according to certain conditions. The accountability problem may be solved if provincial/state governments take on the responsibility for the use of the funds (Watts 1999: 49-50). On the other hand, conditional grants are regarded as undermining the autonomy of provincial/state governments by forcing them to execute expenditures possibly not matching their policy priorities. It may be a sign of centralization if a majority of financial transfers are conditional; on the other hand, unconditional transfers may be a characteristic for more decentralised federations (Courchene 1984: 83). The centralizing efforts that may inform conditional funding decisions in the EU may have some significant impact on member state’s policies in selected policy areas, but by now they have been far too minor and restricted in scale to actually steer policy options of the member states’ governments. Furthermore, the conditionality of transfers may also hint at the distribution of power positions within a federation. Where the constituent states enjoy a powerful position, unconditional transfers may be more common than within states where the central government is predominant in the design of policies. To put it another way: a system of unconditional federal transfers may strengthen the power position of recipients, whereas conditional transfers may strengthen the central donor. The Canadian experience shows that the move to predominantly unconditional federal-provincial transfers led to strengthened provincial governments and decentralization. In the EU we may observe the opposite development path, i.e. strengthened centralization, so long as the strict conditionality in EU funding is maintained. However, the theoretical equation of conditionality of funding leading to institutional centralization is to be qualified within the respective institutional environment. In view of the dependence of the EU budget on member states’ contributions and their influential position in policy design, conditional funding can only be one pillar of centralizing efforts that would have to be accompanied by changes on the revenue side of the budget, i.e. tax resources for the supranational level, and power shift within the decision-making procedures. By now, as regards taxing and spending powers, the power relations in the EU are clearly on the side of the constituent parts of the federation, whereas the Canadian central government is in a far better position vis-à-vis the Canadian provinces and territories.

12

(b) Formula-based calculation of transfers versus political bargaining Experts within the Canadian federal ministry of finance determine equalization payments annually. They follow a complex calculation formula that is set out to ensure an objective and fair distribution of transfers. The EU employs in a first step general eligibility criteria for the distribution of financial transfers based on GDP and other macroeconomic characteristics. In a second step, project proposal for funding have to fit into several objective-oriented funding frameworks. The formula-based approach used in Canada’s equalization system determines the overall amount of equalization transfers as well as the distribution of payments among the provinces. The financial resources of the Equalization Programme stem from general federal taxes. The determination of the equalization formula lies with the federal government with no formal inclusion of the provincial governments (Watts 1999: 53). The procedure determining equalization transfers starts with a technical calculation of each provinces’ revenue capacity. The calculation does not take into account the actual revenues of provinces, but their potential revenues from 33 tax sources applying an average national tax rate for each category (representative tax system). Thereby the fiscal capacity per head is established for each province. In a second step the average of provincial fiscal capacity is calculated on the basis of a 10-province standard. In recent years the equalization norm was about $6200 per capita. The provinces that do not reach that standard are equalized up to that amount per head. The total annual payments by way of equalization transfers amount actually to about $10 billion (Defraiteur 2007: 55).6 In the EU the distribution of financial transfers also basically follows a formula-based approach, but the dependence of budgetary decisions on member states goodwill entails that the formulas are more directly subject to political bargaining and simple package deals than it seems to be the case within the Canadian system. Moreover, EU financial transfers are revenue-based, i.e. after the member states have decided on the overall amount available for transfer, the affordable programme framework is established. Treaty law supports most of the funding programmes. The member states governments as signatories to the treaties thereby provide the framework of transfers, whereas the details of project funding are left to the discretion of the European Commission that prepares respective eligibility criteria for transfers and negotiates funding schemes with the member states that meet the objectives set out in the treaties. However strict the eligibility criteria are, every member state is set out to gain from one or the other funding program. A purely calculative approach to equalization payments provides for more or less predictable regular financial transfers, but leaves scarce room for adjustments to changing circumstances. Furthermore, the more complex a formula is the more obscure and unintelligible it is. Only a handful of experts on the federal and provincial official level handle the Canadian equalization system. The general public largely ignores its existence and only a few academic experts comment on that part of the financial transfer system. Coordination between federal provincial levels has been reduced to the small circle of officials with the relevant ministries

6 In 2004 the federal government presented a new approach to equalization and set up a financial limit on total payments amounting to $10 billion adjusted by 3% per year. The financial framework should rest in place until 2010 (Defraiteur 2007: 56). After fierce opposition from provincial governments and academics, the new system was abandoned and the formula-based 5-province standard was reintroduced.

13

of finance, and the federal lead in determining the formula and doing the calculations has remained undisputed. On the one hand, the central authority over the equalization program fulfils a balancing function. Decision-making on the allocation of payments to the provinces necessarily means that gains of one group of provinces come at the expense of other provinces. On the other hand, the legitimacy of the federal program authority relies on the application of established rules and formulas that are beyond doubt of political arbitrariness (MacKinnon 2006: 3). Only recently, the Ontario government has launched a net payer debate during the provincial electoral campaign. As a consequence of rising natural resources revenues in Alberta that raised the equalization standard significantly, the equalization formula has been frequently adjusted and accompanied by side agreements that called the traditional objectivity of the transfer system into question. Choudry (2006: 48) identified the agreement reached between the federal government, Newfoundland and Nova Scotia over the treatment of royalties from offshore oil and gas projects by the equalization program in February 2005 as a turning point in this regard. The agreement excludes royalties from the calculation of equalization payments.7 These recent developments show that even the strictest formula-based approach to financial transfers does not keep politics and political bargaining aside. Formulae can be established in such a way that they result in politically desired outcomes (Bird 1994: 303). Various kinds of exemptions and extra payments provide for equalization measures that are far from having a technical or economic base. In the EU, political bargaining is at the centre of decision-making on the amounts and the distribution of financial transfers. Package deals and side-payments are most common and indispensable within the EU financial transfer system. In fact, the roots of the nowadays most important transfer program (structural and cohesion funds, now relabelled as transfers within the budgetary category “sustainable growth”) go back to a package deal with the United Kingdom on the occasion of its accession in 1973 and to a side-payment to the southern European member states for their acceptance of the accession of Greece in 1981. There have always been formulas and criteria, but they mainly serve as guidelines. After the intergovernmental bargaining on the overall financial framework for transfers is finished, negotiations between the European Commission and each member state guarantee the objective-oriented use of funds. This dense cooperation throughout the process certainly increases its complexity. Negotiations include a plurality of actors and must accommodate diverging interests. Conflicts may arise at various stages of the bargaining procedure and necessary compromises may reduce the effectiveness and efficiency of the outcome of negotiations. (c) Institutionalization of intergovernmental cooperation Depending on initial decisions on federal organization, such as most importantly the distribution of competencies, the design of intergovernmental institutions for cooperation follows more or less conventional rules. As a rule of thumb, decentralized federations are more likely to guarantee institutionalized representation of the interests of the constituent units than federations dominated by central government. Canada seems to depart from that general proposition as its intergovernmental institutions rarely take conventional forms despite its decentralized federal structure. In contrast to most other federative organizations of state, provincial governments lack adequate representation within the federal government.

7 Before the new agreement royalties earned by the provinces reduced equalization payments to that provinces 1:1 or at least 1:0,70 (Choudry 2006: 48).

14

Because of the rather strict separation of competencies between the federal and provincial governments, formal intergovernmental institutions are of minor importance. With regard to the fiscal federal system on the whole, Robin Boadway states that it is non-cooperative in the sense that fiscal decisions are taken independently by the federal and the provincial level (Boadway 2003: 2). Basically, the federal government disposes of the “first-mover” advantage with respect to revenue decisions since the provinces have to accommodate to the level of tax room left by federal decisions and to the amount of transfers issued by the federal level. Although there is no standardized institutional mechanism that allows for the regular involvement of provinces in fiscal federal issues, coordination between intergovernmental affairs offices and the federal/provincial ministries of finance on the provincial as well as on the federal level occurred on a regular basis according to observations made in 2002 (Leslie, Neumann, Robinson 2004: 230p.). Also, coordination of fiscal federal issues use to “happen” as side effects of either First Ministers’ Conferences or Annual Premiers’ Conferences or Regional Premiers’ conferences. With regard to federal budgetary policy there are, however, institutional structures that indicate a cooperative institutional climate at least at an officials’ level. Twice a year the federal minister calls for federal/provincial meetings of ministers of finance in view of coordination of budgetary issues. These meetings usually took place before the federal budget was established in order to take account of provincial preferences vis-à-vis federal budgetary decisions, but also to align the subsequently established provincial budgets. The second meetings were convened after the establishment of all budgets and served as opportunities to review the economic context and the collective outcome of the budgetary decisions of all levels of government (Leslie, Neumann, Robinson 2004: 232). Usually, the federal minister sets up the agenda and chairs the meetings. The federal agenda-setting power has recently been challenged by provinces asking for a system of co-chairs that is used in other federal/provincial settings. Coordination of the provinces’ positions takes place prior to the meetings. A provincial chairperson presents the common position of the provinces/territories on agenda issues. Additionally, federal and provincial finance departments dispose jointly of several technical committees that prepare studies and policy options on fiscal issues (Leslie, Neumann, Robinson 2004: 231). Table 1: Budgetary cycle (as established in the 1980s): November/December

February/March June

pre-budget meeting presentation of federal budget provincial budgets

post-budget meeting

Whereas federal/provincial meetings in general have recently become less frequent, meetings among provincial finance ministers have gained in importance. Provincial coordination without the inclusion of the federal level started in the form of “bloc meetings” where western provinces have met regularly and issued public reports annually. The Atlantic provinces followed the western example and, also, began to assert their interests as a bloc. More recently all provinces joined in formulating consensus positions vis-à-vis the federal level and in coordinating their fiscal policy independently from the federal level (tobacco taxes increase). In 2003, the Council of the Federation has been founded, where the provincial cooperation should find its conventional institutional setting.

15

Due to the strict separation of competencies and the lack of conventional rules, these coordination efforts entirely depend on the goodwill of the federal respectively the provincial governments. After the election of a liberal government in Canada in 1980, accountability and transparency became central to the federal government’s agenda. The cooperative era in Canadian federalism came to an end when the federal government tried to strengthen its power position by raising issues of Canadian unity, efficiency, transparency and accountability. The new Canadian federalism is best characterized by competitive legitimation of the two (or even three) orders of government. Competitive federalism opened up the fora of intergovernmental negotiation. Particularly, the establishment of intergovernmental ministries rendered intergovernmental conflict more public and explicit (Teliszewski/Stoney 2007:30). In an atmosphere of “competitive state-building” (Leibfried/Pierson 1998) intergovernmental cooperation events offered the opportunity for federal and provincial high officials to expose themselves to their constituencies. The federal level began to present cooperative federalism and decentralization as a danger to the unity and strength of the country. Intensive coordination and joint decision-making was regarded as inefficient as concerns the procedure and the lowest common denominator outcome. Furthermore, with regard to federal democratic legitimacy, decentralization would weaken the central government’s ties with the citizens. They would credit their provincial governments for taking actions in important policy areas without considering that the funds financing these actions actually originate from the federal budget. Additionally, in terms of political and financial responsibility, the federal-provincial transfer system reduced direct accountability at the level of provincial governments. At the federal level it could be regarded as irresponsible to the federal taxpayer if federal transfers were distributed to provincial governments without conditions (Simeon/Robinson 1990: 290). The EU coordination of budgetary policy follows a highly institutionalised path of intergovernmental cooperation. Treaty law prescribes dates and deadlines of the procedure on the supranational level, and the regular annual meetings between the heads of state and governments ensure an ongoing coordination process. The European Commission acts as the general intergovernmental secretariat, whereas the basic central government function is assumed by the Council of Ministers and the European Parliament, under clear domination of the former. The European Council is the highest political body in the EU, where the head of state and governments meet twice a year and define the strategic political developments of the Union. Budgetary policy involves all institutions. Recently the fora of negotiation were also opened up to the public by requesting citizen’s opinions on the financial priorities of the EU. In view of a major reform process of the EU budgetary policy, the European Commission established a website where public and private institutions, and individuals can deposit their views on the reform. The Commission is expected to present its proposal for budgetary reform at the end of 2008 or the beginning of 2009. The rather strict timetable and structure underlying the EU budgetary procedure certainly have the advantage of representing a framework for settling conflicts within a highly sensitive policy field. Policy preferences and actors’ strategic interests culminate in decisions on revenues and expenditures. On the one hand continuous negotiations under inclusion of a multitude of actors are of course prone to major conflicts, but on the other hand the outcome may be more legitimate. In contrast, a transparent policy process adds complexity that may not be justified by policy improvement. In this regard, the coordination of Canadian

16

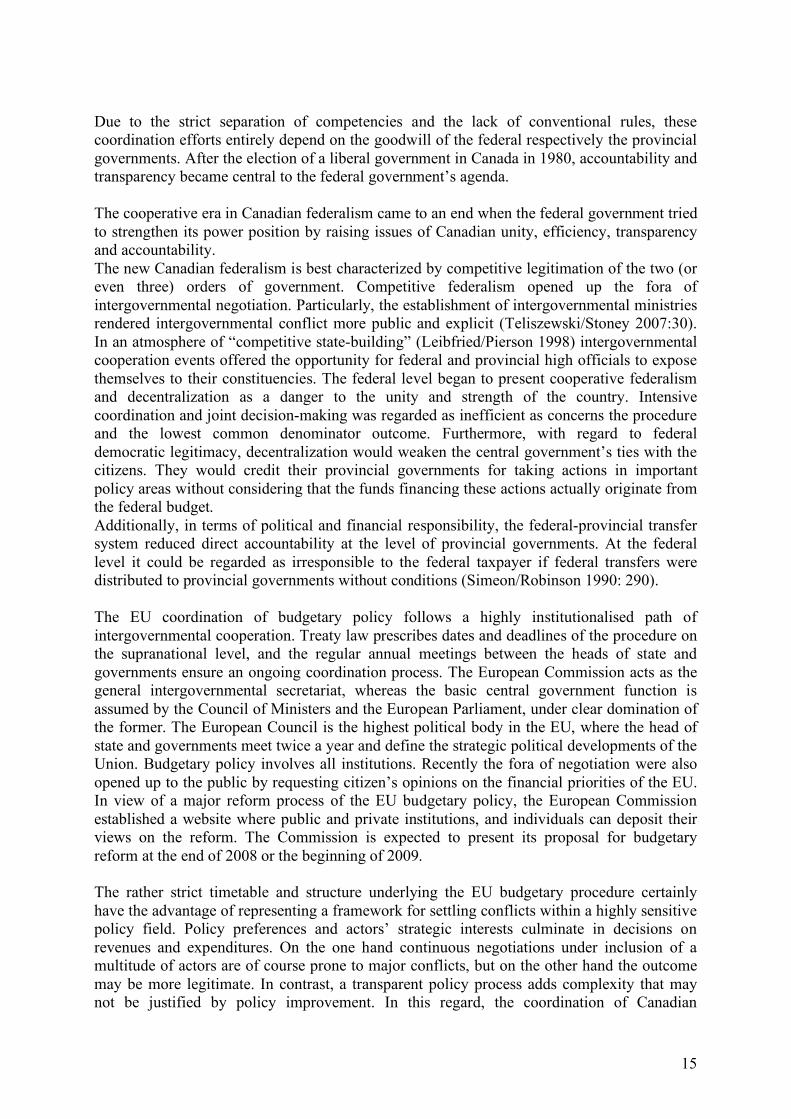

budgetary policy on the officials’ level also proved to be more effective and efficient. Furthermore, the Canadian federal government dominates the system of financial transfers as central decision-maker. It disposes of the agenda-setting power as well as the final decisional power. The mainly informal institutional setting may, however, confine the policy development to a small circle of experts, what may hamper the implementation of necessary reforms. 3. Preliminary Conclusion Despite decentralising tendencies, inter-provincial solidarity seems to be an undisputed asset of the Canadian federation. The Canadian system of equalization payments has been based on a broad national consensus as to its objective of achieving national equity. Simeon and Robinson present two major reasons for that consensus: “[O]n the one hand, the commitment to national equity that was part of the postwar philosophy of the welfare state and, on the other hand, an acceptance of a relatively high degree of decentralization. The equalization program said, in effect, that lack of fiscal capacity should not prevent the provinces from pursuing the priorities which the federal constitution otherwise granted their citizens the right to determine.” (Simeon and Robinson 1990: 198). The main achievement with equalization and other more or less unconditional federal-provincial transfers in Canada is the reconciliation of provincial autonomy with federal equity norms. In 2004, 85% of Canadians supported the transfer of money from richer to poorer provinces. This figure rose by 2% compared to 2001 (Noël 2006: 65). The following figure shows public attitudes vis-à-vis interregional redistribution in Canada8 and reveals high rate of acceptance of assistance to poorer regions over time. Figure 5

Source: Source Canadian Opinion Research Archive (CORA) http://www.queensu.ca/cora/_trends/Spend_PoorReg.htm 8 The question asked was: "Keeping in mind that increasing services could increase taxes, do you think the federal government is spending too much, just the right amount, or should be spending more on each of the following: assistance to poorer regions", in 2003 it has been changed to “Keeping in mind that increasing services could increase taxes, do you think the federal government should spend more, less, or the same on each of the following?”

17

Furthermore, the Canadian principle of equalization rests on the conviction that every Canadian should receive a comparable set of publicly provided social services, i.e. equal treatment of individual citizens. By now, this understanding of equality is not part of EU policy. Social services and redistribution are part of the member states’ undisputed prerogatives. If there is an equality discourse in EU politics it is mainly concerned with economic performance indicators and GNPs. But the general public seems to welcome interregional distribution. A recent Eurobarometer survey revealed that 85,7% of respondents to a Europe-wide survey were in favour of supporting poor regions by means of structural and cohesion funding (Flash Eurobarometer 2008). Central governmental budgetary policy and financial transfers are one means that bind a federation together and asserts the economic as well as political stability of a multilayered polity. Budgetary policy in the European Union is actually under revision. Even if it remains doubtful that major changes will occur in the near future, a comparative view on institutions and structures, achievements and failures within other organisations of intergovernmental relations certainly widens the alternative spectrum of reform options. Lessons learned from the Canadian experience in intergovernmental cooperation on budgetary policy and financial transfers can be summarised as follows:

• Central taxing powers open up the room of manoeuvre for central budgetary policy without necessarily locking in a centralizing development path for the federation.

• Conditionality of financial transfers more likely impacts on the balance of power within a federation in conjunction with a centralized tax revenue system.

• Formula-based calculations of financial transfers strengthen objectivity and regularity of transfers, but lack adequate consideration of changing political and economic circumstances.

• Efficient decision-making within an intergovernmental setting does not rely on a formal institutional framework if the distribution of competencies is clear-cut.

• Furthermore, institutionalization of intergovernmental cooperation does not guarantee less conflict.

18

References Adam, Marc-Antoine (2007) “Federalism and the Spending Power: Section 94 to the Rescue”, in: Policy Options Vol. 28 No. 03, March 2007, 30-34. Banting, Keith G., Brown, Douglas M., Courchene, Thomas J. (eds.) (2004) The Future of Fiscal Federalism (Kingston, Ont.: School of Politics). Bird, Richard M. (1994) “A Comparative Perspective on Federal Finance”, in: Keith G. Banting, Douglas M. Brown, Thomas J. Courchene (eds.), The Future of Fiscal Federalism (Kingston, Ont.: School of Politics), 293-322. Boadway, Robin (2003) “Should the Canadian Federation be Rebalanced? A Memo for Paul Martin”, University of Windsor Faculty of Science Seminar Series. Boadway, Robin and Flatters, Frank, (1994) “Fiscal Federalism: Is the System in Crisis?”, in: Keith G. Banting, Douglas M. Brown, Thomas J. Courchene (eds.), The Future of Fiscal Federalism (Kingston, Ont.: School of Politics), 25-74. Brown, Douglas M., Courchene Thomas J. (eds.) (1994) The Future of Fiscal Federalism (Kingston, Ont.: School of Politics). Choudry, Sujit, Gaudreault-DesBiens, Jean-François, and Sossin, Lorne (2006) Dilemmas of Solidarity: Rethinking Redistribution in the Canadian Federation (Toronto: University of Toronto Press) Choudry, Sujit (2006) “Redistribution in the Canadian Federation: The Impact of the Cities Agenda and the New Canada” in: Sujit Choudry, Jean-François Gaudreault-DesBiens, and Lorne Sossin: Dilemmas of Solidarity: Rethinking Redistribution in the Canadian Federation (Toronto: University of Toronto Press), 45-56. Courchene, Thomas J. (1984) Equalization Payments: Past, Present, Future (Ontario Economic Council). Defraiteur. Vincent (2007) “ Péréquation et déséquilibre fiscal: d’argent, de politique, de technicité…”, in: Policy Options Vol. 28 No. 03, March 2007, 54-57. Eiselt, Isabella, Pollak, Johannes, Slominski, Peter (2007) “Codifying Temporary Stability? The Role of Interinstitutional Agreements in Budgetary Politics”, in: European Law Journal 13/1, 75-91. Flash Eurobarometer (2008) Citizen’s perceptions of EU Regional Policy, Analytical Report, Flash Eurobarometer 234 (The Gallup Organisation), European Commission. Lamassoure report (2006), “Report on the future of the European Union’s own resources” (2006/2205 (INI)), PE 382.623. Lazar, Harvey (ed.) (2005) Canadian Fiscal Arrangements: What Works, What Might Work Better (Kingston: Queen’s University, Institute for Intergovernmental Relations).

19

Leibfried, Stephan, Pierson, Paul (1995) European Social Policy. Between Fragmentation and Integration (Washington D.C.: Brookings Institution). Leslie, Peter, Neumann, Ronald H., Robinson, Russ (2004) “Managing Canadian Fiscal Federalism”, in: J. Peter Meekison, Hamish Telford and Harvey Lazar, Canada: The State of the Federation. Reconsidering the Institutions of Canadian Federalism (Kingston: Institute of Intergovernmental Relations), 213-248. Leslie, Peter (1993) “The Fiscal Crisis of Canadian Federalism” in: P.M. Leslie, K. Norrie and I.Ip (eds.), A Partnership in Trouble: Renegotiating Fiscal Federalism (Toronto: C.D. Howe Institute). MacKinnon, Janice (2006) “Is Equalization Broken? Can Equalization Be Fixed?” in: Fiscal Federalism and the Future of Canada, Selected Proceedings from the Conference, September 28-29, 2006, Folio 3, Institute of Intergovernmental Relations. Meekison, J. Peter, Telford, Hamish and Lazar, Harvey (eds.) (2004) Canada: The State of the Federation. Reconsidering the Institutions of Canadian Federalism (Kingston: Institute of Intergovernmental Relations). Menon, Anand, Schain, Martin A. (eds.) (2006) Comparative Federalism, The European Union and the United States in Comparative Perspective (Oxford: Oxford University Press). Milne, David (1994) “Comment: Political Constraints on Fiscal Federalism”, in: Douglas M. Brown and Thomas J. Courchene (eds.), The Future of Fiscal Federalism (Kingston, Ont.: School of Politics), 175-180. Musgrave, R. M. (1959) The Theory of Public Finance (New York: McGraw-Hill). Nicolaidis, Kalypso, Howse Robert (eds.) (2001) The Federal Vision, Legitimacy and Levels of Governance in the United States and the European Union (Oxford: Oxford University Press). Noël, Alain (2006) “Social Justice in Overlapping Sharing Communities” in: Sujit Choudry, Jean-François Gaudreault-DesBiens, and Lorne Sossin: Dilemmas of Solidarity: Rethinking Redistribution in the Canadian Federation (Toronto: University of Toronto Press), 57-72. Noël, Alain (1998) “Le principe fédérale, la solidarité et le partenariat”, in: Guy Laforest and Roger Gibbins, Sortir de l’impasse: les voises de la reconciliation (Montréal: Institut de recherché politiques publiques (IRPP)), 263-295. Norrie, Kenneth (1994) “ Social Policy and Equalization: New Ways to Meet an Old Objective”, in: Keith G. Banting, Douglas M. Brown, Thomas J. Courchene (eds.), The Future of Fiscal Federalism (Kingston, Ont.: School of Politics), 155-174. Simeon, Richard and Papillon, Martin (2006) “Canada”, in: Akthar Majeed, Ronald L. Watts, and Douglas M. Brown (eds.): Distribution of Powers and Responsibilities in Federal Countries (Montreal&Kingston: McGill-Queen’s University Press), 92-122.

20

Simeon, Richard and Robinson, Ian (1990) State, Society, and the Development of Canadian Federalism (Toronto: University of Toronto Press). Oates, W. E. (1999) An Essay on Fiscal Federalism. Journal of Economic Literature 37, 1120-1149. Oates, W. E. (1972) Fiscal Federalism (New York: Harcourt, Brace, Jovanovich). Teliszewsky, Andrew/Stoney, Christopher (2007) “Addressing the Fiscal Imbalance through Asymetrical Federalism: Dangerous Times for the Harper Government and for Canada”, in: How Ottawa Spends 2007-2008 (McGill-Queen’s University Press). Théret, Bruno (2002) Protection social et fédéralisme: L’Europe dans le miroir de l’Amérique du Nord (Bruxelles: P.I.E.-Peter Lang). Watts, Ronald L. (2005) “Autonomy or Dependence: Intergovernmental Financial Relations in Eleven Countries”, Working Paper 2005(5), Institute for Intergovernmental Relations, Queen’s University. Watts, R.L. (1999) Comparing Federal Systems (Kingston: Institute for Intergovernmental Relations, Queen’s University).