Embed Size (px)

Citation preview

1

The elephant: a symbol of our 100 years of strength and longevity.

A Few Tax Concepts Associated With Certain Insurance Products

March 2013

2

Topics covered

> Some life insurance transfer rules

> Life insurance held by a corporation

> Shared ownership critical illness insurance

3

Life insurance transfer rules

TRANSFER = Disposition of a life insurance policy Examples of disposition:

> Surrender

> Policy loan

> Dissolution by reason of maturity

> Significant changes to the policy (depending on the facts): Change of ownership (change of name on the policy) Substitution of insured Policy conversion Etc.

4

Life insurance transfer rules

General rule – Consequences of disposition > For the policyholder (seller):

Amount received for the policy - ACB = 100% taxable

> For the recipient of the transfer (buyer): Amount paid = their ACB

5

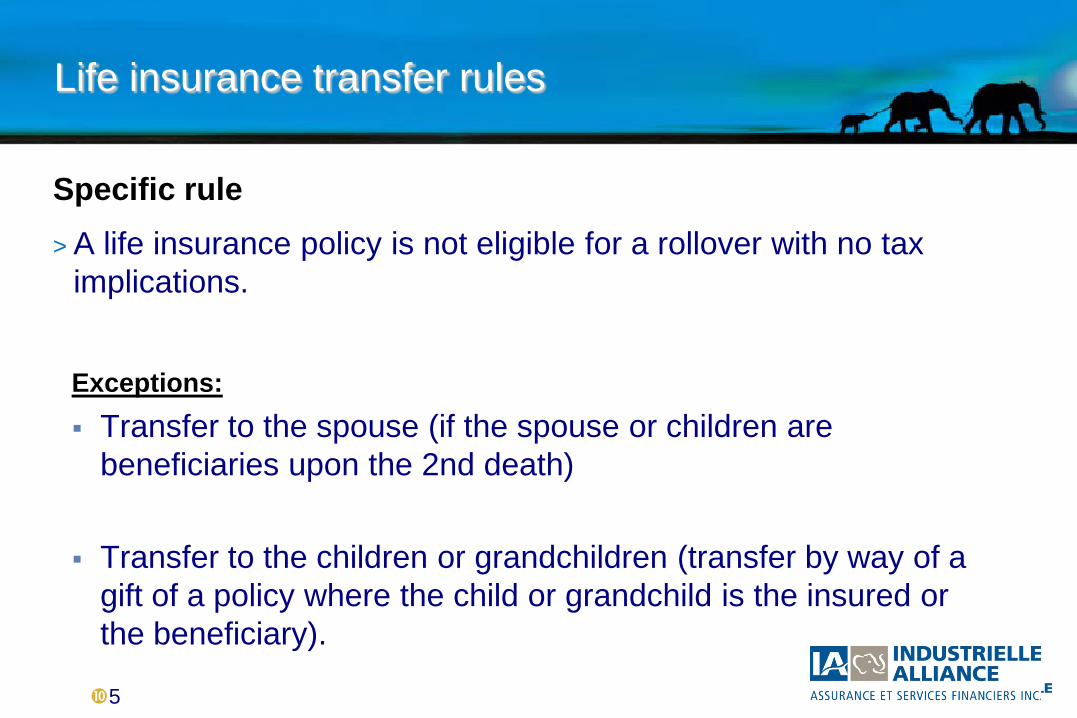

Life insurance transfer rules

Specific rule > A life insurance policy is not eligible for a rollover with no tax

implications.

Exceptions: Transfer to the spouse (if the spouse or children are

beneficiaries upon the 2nd death)

Transfer to the children or grandchildren (transfer by way of a gift of a policy where the child or grandchild is the insured or the beneficiary).

6

Life insurance transfer rules

Specific rules – Donation or distribution at non-arm's length > Subsection 148(7) ITA: Where an interest in a life insurance policy is disposed of (…) by way of a

gift (during the policyholder's lifetime or by the policyholder's will), by distribution from a corporation (…) to any person OR in any manner whatever to any person with whom the policyholder was not dealing at arm's length, the policyholder shall be deemed thereupon to become entitled to receive proceeds of the disposition equal to the value of the interest (…) and the person who acquires the interest by virtue of the disposition shall be deemed to acquire it at a cost equal to that value.

> Subsection 148(9) ITA: "Value": The value of an interest in a life insurance policy means:

a) where the interest includes an interest in the cash surrender value of the policy, the amount in respect thereof (…)

b) in any other case, nil Exceptions: Transfer to the spouse Transfer to an insured child

7

Life insurance transfer rules

Specific rules – Donation, distribution and disposition at non-arm's length

> For the policyholder (seller):

CSV – ACB = 100% taxable

> For the recipient of the transfer (buyer): CSV = their ACB

"Without regard for the fair market value (FMV)"

8

Fair market value

The CRA's position on the fair market value of a life insurance policy

>The FMV of a policy may be different from the CSV

>Information Circular IC89-3 / Interpretation Bulletin IT- 416

A life insurance policy must be valued in accordance with normal valuation

practices, taking into consideration all facts such as life expectancy and the insured's state of health.

9

Fair market value

Indicators of a high FMV > Type of insurance

Permanent vs. term, paid-up policy > Policy issued some time ago > Deterioration in insured's health > Change in economic environment > Cash surrender value > Additional riders

Conversion privilege Guaranteed insurability Increase in sum insured Exercise of options

10

Transfer of a life insurance policy by an individual to a corporation

"Opco / Holdco"

(non arm's-length relationship)

Mr. Client

11

Transfer of a life insurance policy by an individual to a corporation

Specific rules – Donation or distribution at non-arm's length > For the policyholder (Mr. Client) CSV – ACB = 100% taxable

> For the recipient of the transfer (Opco/Holdco): CSV = their ACB

"Without regard for the fair market value (FMV)"

12

Transfer of a life insurance policy by an individual to a corporation

> If the FMV > the CSV at the time of the transfer, a sale for valuable consideration will enable the assignor (shareholder), in some cases, to receive the value of the policy over and above the CSV, tax free.

The CRA already confirmed that there was no taxable benefit for the shareholder (assignor).

However, this situation has been under observation by the federal Department of Finance… since 2002…

13

Transfer of a life insurance policy by an individual to a corporation

> If the corporation keeps the policy until the insured's death, the funds received by the shareholder over and above the CSV will never be taxed since the sum insured will mostly go through the CDA ( > ACB):

To do this, the corporation must be the beneficiary of the policy. Otherwise, there will be a taxable benefit for the shareholder.

14

Transfer of a life insurance policy by an individual to a corporation

If the ACB > the CSV at the time of the transfer:

> The policyholder realizes a non-deductible loss.

> Since the corporation is deemed to have acquired the policy at the CSV, its ACB will be smaller:

Therefore, there's a potential upward impact on the CDA.

15

Transfer of a life insurance policy by an individual to a corporation

"Corporation" (non arm's-length

relationship)

Mr. Client

Example:

Policy features:

ACB $50,000 CSV $125,000 FMV $250,000

Scenarios:

1) The shareholder gives the policy to the corporation 2) The corporation pays the shareholder an amount equal to the ACB 3) The corporation pays an amount equal to the CSV 4) The corporation pays an amount equal to the FMV

16

Transfer of a life insurance policy by an individual to a corporation

Assignor: Shareholder Assignee: Corporation

Deemed Policy Amount Taxable New

disposition ACB gain paid benefit ACB

[148(7)] [148(1)] [148(7)]

Scenario 1 125,000 50,000 75,000 0 N/A 125,000

Scenario 2 125,000 50,000 75,000 50,000 N/A 125,000

Scenario 3 125,000 50,000 75,000 125,000 N/A 125,000

Scenario 4 125,000 50,000 75,000 250,000 N/A 125,000

No sections of the ITA allow for a benefit to the corporation, which is neither a shareholder nor an employee.

Summary...

17

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

"Opco"

(non arm's-length relationship)

Mr. Client

18

> Circumstances:

Sale of the corporation's shares owned by the shareholder

Life insured leaves the company (key employee)

Retirement, etc.

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

19

> The transfer produces tax implications Disposition for the assignor (the corporation) Acquisition for the assignee (the shareholder or the

employee)

> Considerations Potential benefit for the assignee Impact of this benefit on the ACB

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

20

Tax considerations for the transferring corporation > Under the specific transfer rules defined in 148(7) of the ITA, the

assignor is deemed to have received the value of the interest in the policy, i.e. the CSV.

The corporation will therefore have to be taxed on the amount over and above the CSV minus the policy's ACB.

This income is defined as investment income from property and will therefore be taxed at the federal and provincial combined rate of 46.57%.

The Refundable Dividend Tax on Hand (RDTOH) rules will apply (26.67%).

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

21

> Under the specific transfer rules defined in 148(7) of the ITA, the assignee is deemed to have acquired the policy at the CSV.

Possibility of a taxable benefit for the shareholder or the employee.

The taxable benefit is added to the shareholder's or employee's ACB.

In all cases, the ACB is limited to the FMV.

Tax considerations for the individual assignee (employee or shareholder)

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

22

Taxable benefit: > A taxable benefit may be conferred if the policy's FMV at the time of

the transfer exceeds the amount paid by the assignee.

> Refer to the indicated criteria for the policy's FMV.

Tax considerations for the individual (employee or shareholder)

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

23

Example:

Policy features: ACB $50,000 CSV $125,000 FMV $250,000

Scenarios: 1) The corporation gives the policy to the shareholder 2) The shareholder pays the corporation an amount equal to the ACB 3) The shareholder pays the corporation an amount equal to the CSV 4) The shareholder pays the corporation an amount equal to the FMV

"Opco"

(non arm's-length relationship)

Mr. Client

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

24

Deemed Policy Amount Taxable Newdisposition ACB gain paid benefit ACB

[148(7)] [148(1)] [15(1)] [148(7 and 9)]

Scenario 1 125,000 50,000 75,000 0 250,000 250,000Scenario 2 125,000 50,000 75,000 50,000 200,000 250,000Scenario 3 125,000 50,000 75,000 125,000 125,000 250,000Scenario 4 125,000 50,000 75,000 250,000 0 125,000

Assignor: Corporation Assignee: Shareholder

Evaluating the real cost of a taxable benefit may be advantageous from a financial standpoint.

The higher the taxable benefit, the less the employee or shareholder will have to pay to acquire the policy (amount paid + tax on the taxable benefit).

Summary...

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

25

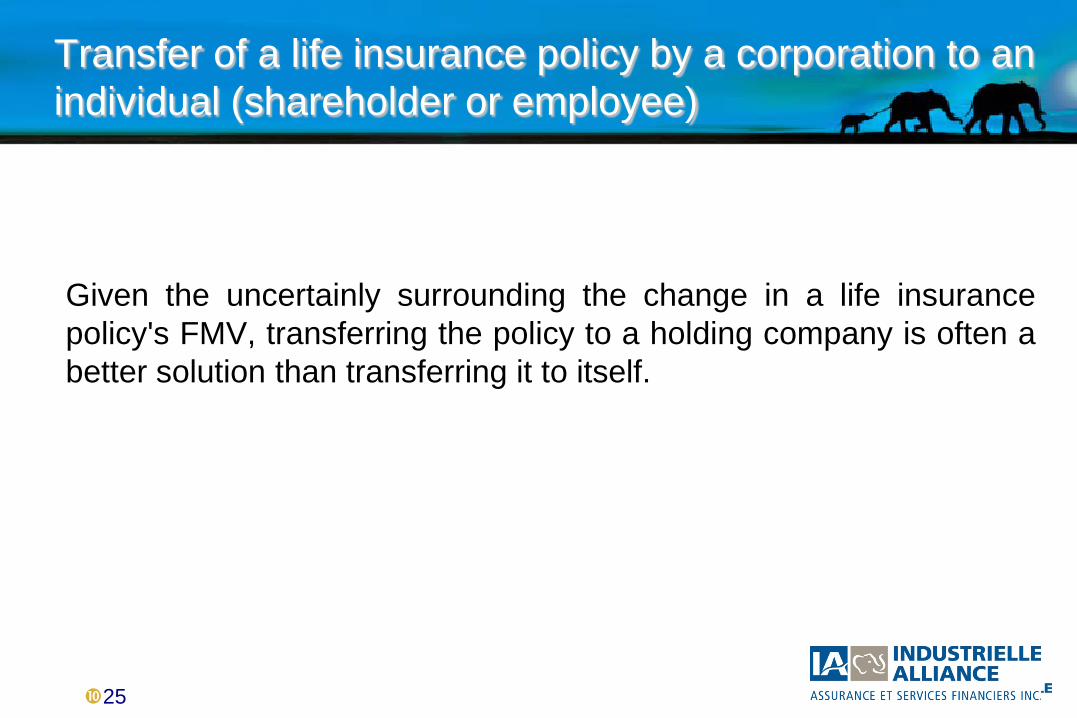

Given the uncertainly surrounding the change in a life insurance policy's FMV, transferring the policy to a holding company is often a better solution than transferring it to itself.

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

26

> Options:

Cancel the old policy and purchase a new one.

• Check the insured's health and the costs associated with a new policy.

Transfer the existing policy.

• Find out the tax implications of the transfer.

Transfer of a life insurance policy by a corporation to an individual (shareholder or employee)

27

Transfer of a life insurance policy by an operating company to a holding company

"Holdco"

"Opco"

28

> Scenario:

OPCO holds an interest in a life insurance policy which it transfers to HOLDCO via a dividend in kind.

If HOLDCO controls OPCO or a taxable Canadian corporation, the dividend in kind will not be taxable because it's an intercorporate dividend.

Important: If an RDTOH is created for OPCO upon disposition of the policy

(CSV > ACB), HOLDCO could be subject to dividend tax under Part IV of the ITA if OPCO requests a dividend refund.

Transfer of a life insurance policy by an operating company to a holding company

29

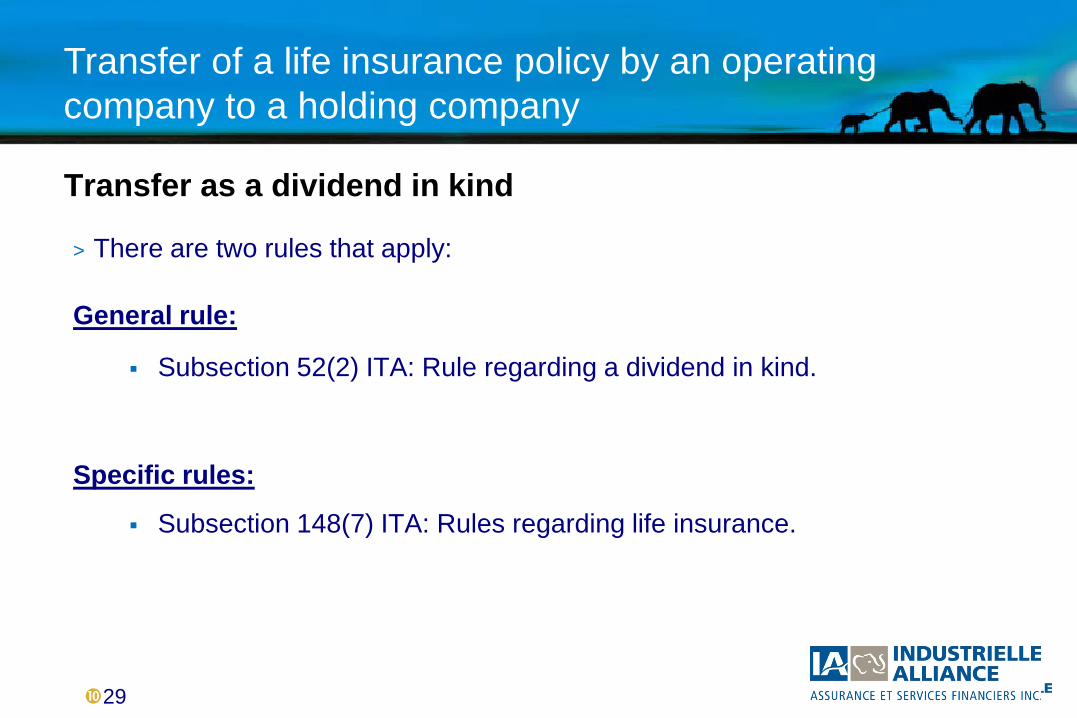

Transfer as a dividend in kind

> There are two rules that apply:

General rule:

Subsection 52(2) ITA: Rule regarding a dividend in kind.

Specific rules:

Subsection 148(7) ITA: Rules regarding life insurance.

Transfer of a life insurance policy by an operating company to a holding company

30

> Any corporation (OPCO) that transfers property as payment of a dividend is deemed to have disposed of the property at its FMV at that time.

> Any shareholder (HOLDCO) that receives property as payment of a dividend is deemed to have acquired the property at its FMV at that time.

General rule

Under subsection 52(2) of the ITA.

Transfer of a life insurance policy by an operating company to a holding company

31

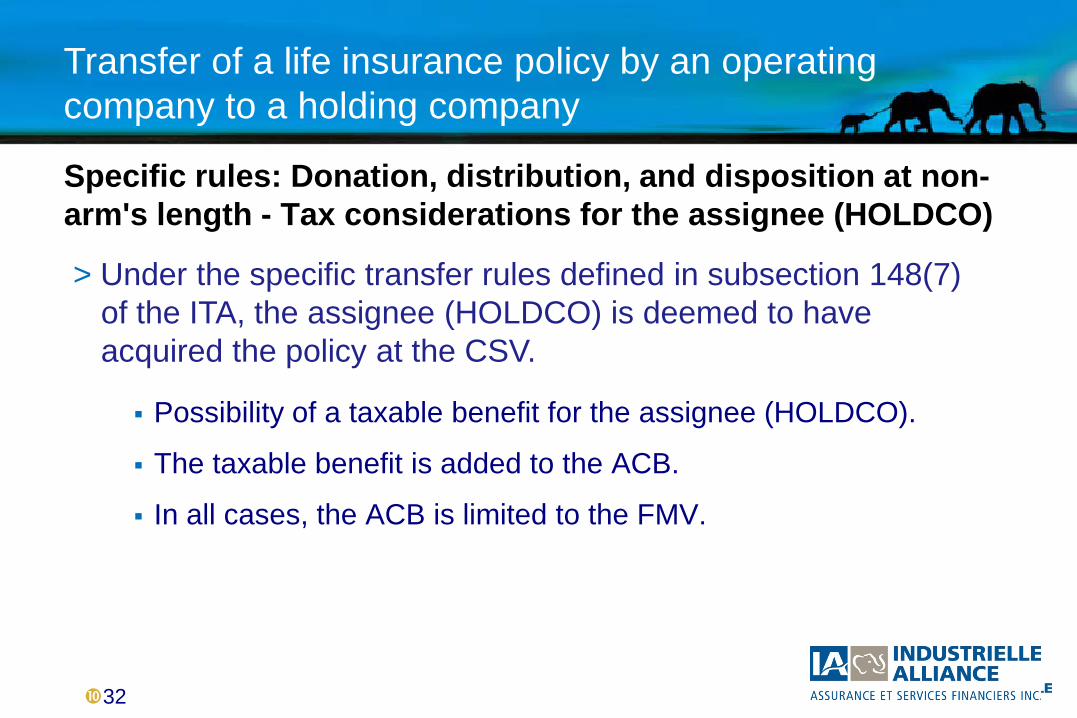

Specific rules: Donation or distribution at non-arm's length - Tax considerations for the assignor (OPCO)

> Under the specific transfer rules defined in subsection 148(7) of the ITA, the assignor (OPCO) is deemed to have received the value of the interest in the policy following the disposition, i.e. the CSV.

The corporation will therefore have to be taxed on the amount by which the CSV exceeds the policy's ACB.

This income is defined as investment income from property and will therefore be taxed at the federal and provincial combined rate of 46.57%.

The RDTOH rules will apply (26.67%).

Transfer of a life insurance policy by an operating company to a holding company

32

> Under the specific transfer rules defined in subsection 148(7) of the ITA, the assignee (HOLDCO) is deemed to have acquired the policy at the CSV.

Specific rules: Donation, distribution, and disposition at non-arm's length - Tax considerations for the assignee (HOLDCO)

Possibility of a taxable benefit for the assignee (HOLDCO).

The taxable benefit is added to the ACB.

In all cases, the ACB is limited to the FMV.

Transfer of a life insurance policy by an operating company to a holding company

33

A taxable benefit may be conferred if the policy's FMV at the time of the transfer exceeds the amount paid by the assignee.

Refer to the criteria indicated earlier for the policy's FMV.

> Taxable benefit:

Tax considerations for the assignee (HOLDCO)

Transfer of a life insurance policy by an operating company to a holding company

34

Example: Policy features: ACB $50,000 CSV $125,000 FMV $250,000

Scenarios:

1) OPCO gives the policy to HOLDCO

2) OPCO pays a dividend equal to the ACB to HOLDCO

3) OPCO pays a dividend equal to the CSV to HOLDCO

4) OPCO pays a dividend equal to the FMV to HOLDCO

"Holdco"

"Opco"

Transfer of a life insurance policy by an operating company to a holding company

35

Deemed Policy Dividend Taxable New disposition ACB gain received benefit ACB

[148(7)] [148(1)] [15(1)] 148(7 and 9)

Scenario 1 125,000 50,000 75,000 0 250,000 250,000Scenario 2 125,000 50,000 75,000 50,000 200,000 250,000Scenario 3 125,000 50,000 75,000 125,000 125,000 250,000Situation 4 125,000 50,000 75,000 250,000 n/a 125,000

Assignor: OPCO Assignee: HOLDCO

According to the CRA, scenario 4 does not allow an increase in the ACB since the taxation of HOLCO is caused by the receipt of a dividend, whereas only an amount included as a shareholder's benefit will be eligible for an increase in the ACB, for an amount equal to the amount by which the FMV exceeds the CSV.

(Ref: Tech. Interpretation # 2003-0035655)

Summary...

Transfer of a life insurance policy by an operating company to a holding company

36

"Subsidiary 1"

"Subsidiary 2"

Client

Transfer between sister corporations (two subsidiaries) (non arm's-length relationship)

37

Tax considerations for the transferring corporation

> Under the specific transfer rules defined in 148(7) of the ITA, the assignor is deemed to have received the value of the interest in the policy, i.e. the CSV.

The assignor will therefore have to be taxed on the amount by which the CSV exceeds the policy's ACB.

This income is defined as investment income from property and will therefore be taxed at the federal and provincial combined rate of 46.57%.

Transfer between sister corporations (two subsidiaries)

38

Under the specific transfer rules defined in 148(7) of the ITA, the assignee is deemed to have acquired the policy at the CSV.

No taxable benefit.

Tax considerations for the assignee

Transfer between sister corporations (two subsidiaries)

39

Example: Policy features: ACB $50,000 CSV $125,000 FMV $250,000

Scenarios:

1) Subsidiary 2 gives the policy to Subsidiary 1

2) Subsidiary 1 pays Subsidiary 2 an amount equal to the ACB

3) Subsidiary 1 pays Subsidiary 2 an amount equal to the CSV

4) Subsidiary 1 pays Subsidiary 2 an amount equal to the FMV

"Subsidiary 1"

"Subsidiary 2"

Transfer between sister corporations (two subsidiaries)

Client

40

Deemed Policy Amount Taxable Newdisposition ACB gain paid benefit ACB

[148(7)] [148(1)] [148(7 and 9)

Scenario 1 125,000 50,000 75,000 0 n/a 125,000Scenario 2 125,000 50,000 75,000 50,000 n/a 125,000Scenario 3 125,000 50,000 75,000 125,000 n/a 125,000Scenario 4 125,000 50,000 75,000 250,000 n/a 125,000

Assignor: Subsidiary 2 Assignee: Subsidiary 1

Once again, no sections of the ITA allow for a benefit to the corporation for a transfer between two sister corporations. They are not shareholders of one another.

Summary...

Transfer between sister corporations (two subsidiaries)

41

Benefits of holding life insurance through a corporation > Funding of the buy/sell agreement > Funding for a share buyback > Key person insurance > Wealth creation > Payment of taxes at death > Business loan protection > Tax room for savings

42

Benefits of holding life insurance through a corporation

> Lower cost of premiums after taxes Premium "normally" non-deductible Insurance costs are much lower when the corporation's income is

eligible for the small business deduction (49.97% vs. 38.54% vs. 19%) To pay an annual premium of $10,000, the employer would have to pay a salary of

$19,988 to the employee. To pay an annual premium of $10,000, the corporation would have to pay a taxable

dividend of $16,271 to the shareholder. To pay an annual premium of $10,000, a corporation that's eligible for the small

business deduction would have to generate income of $12,345 (if the corporation is the policyholder and the beneficiary).

43

Benefits of holding life insurance through a corporation

> Financial reasons: Several shareholders Age differences among the shareholders Evens out the insurance cost for each person by paying dividends

in the context of funding the shareholders' agreement

> Psychological reason: Expenses paid by the corporation, not personally

44

Benefits of holding life insurance through a corporation

> Tax planning options with a shareholders' agreement:

Purchase of shares, buyback of shares or a combination of the

two, which minimizes the tax impact of the deemed disposition upon death

45

Disadvantages of holding life insurance through a corporation

> Accumulated amounts and the death benefit are not sheltered

from company creditors > The cash surrender value of the life insurance policy is a

company asset that must be included as such For valuing the shares For eligibility for the $750,000 capital gains exemption

46

Disadvantages of holding life insurance through a corporation

> The amount eligible for the CDA is reduced by the ACB

However, there are insurance contracts that have an increasing sum insured that will reflect the changes in the ACB

> The death benefit, once the corporation has received it, may

lose its qualified small business corporation (QSBC) status in certain situations

47

Tax implications for the corporation

> Deductibility of annual premiums

Generally speaking, premiums are not deductible. They may be deductible in two cases:

Policy used as collateral for a loan When the premium is considered a taxable employment

benefit (corporation not the beneficiary).

48

Tax implications for the corporation

> Payment of the life insurance proceeds upon death

Not considered taxable income The death benefit over and above the policy's ACB is paid into the

CDA. This excess amount will be paid tax-free to the shareholders and the amount corresponding to the ACB will be paid as a taxable dividend.

49

Tax implications for the corporation

> If the corporation named as the beneficiary of the policy is not the corporation that pays the premiums (policyholder), the CRA is of the opinion that it could invoke the General Anti-Avoidance Rule (GAAR)…

IMPORTANT!

This could happen if it considers that the reason for this kind of arrangement is for the sole purpose of receiving a tax benefit (Ref: Technical Interpretation 9824465).

50

Tax implications for the corporation

"HOLDCO"

"OPCO"

Mr. Client

Payment of premiums

Beneficiary

51

Tax implications for the corporation

> Tax implications: Benefit to the shareholder (Holdco) The holding company will have to include the value of the

premiums paid by the operating company in its income, and pay tax on that income. The GAAR could be applied if the holding of the life insurance

was structured to increase the value of the CDA credit (with the ACB being in the OPCO).

52

Tax implications for the corporation

"HOLDCO"

"OPCO"

Mr. Client

Payment of premiums

Beneficiary

53

Tax implications for the corporation

> Tax implications: No taxable benefit. The GAAR could be applied if the holding of the life insurance

was structured to increase the value of the CDA credit (with the ACB being in the Holdco).

54

Tax implications for the corporation

Solution?

Transfer the policy depending on its tax characteristics The Holdco pays the premium from an inter-corporate

dividend paid by the Opco

55

Tax implications for the shareholder or the employee

> If the beneficiary of the life insurance policy is an individual in their capacity as an employee: Benefit for the employee Deductible for the employer

> If the beneficiary of the life insurance policy is an individual in

their capacity as a shareholder: Benefit for the shareholder Non-deductible for the employer

56

Corporate ownership - Example 1

Mr. Client

Insurance

57

Corporate ownership - Example 1

"OPCO"

Mr. Client

Insurance

58

Corporate ownership - Example 1

"HOLDCO"

"OPCO"

Mr. Client

Insurance

59

Corporate ownership - Example 1

"HOLDCO"

Insurance

"OPCO"

Mr. Client

60

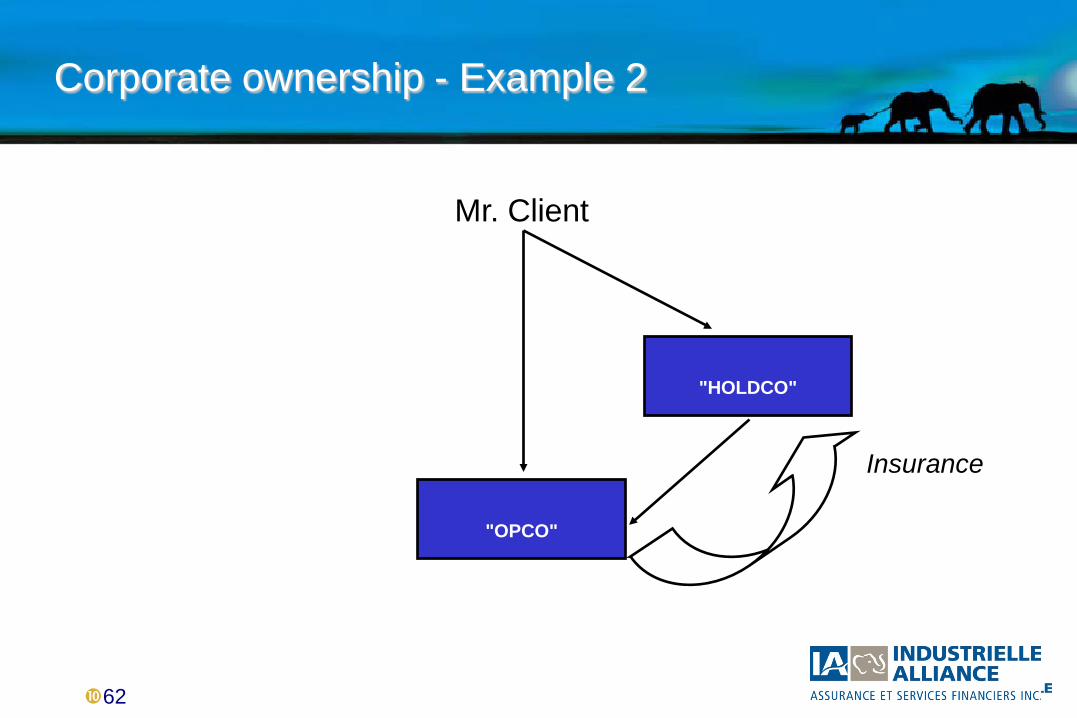

Corporate ownership - Example 2

"OPCO"

Mr. Client

Insurance

61

Corporate ownership - Example 2

"HOLDCO"

Mr. Client

Insurance

"OPCO"

62

Corporate ownership - Example 2

"HOLDCO"

Mr. Client

Insurance

"OPCO"

63

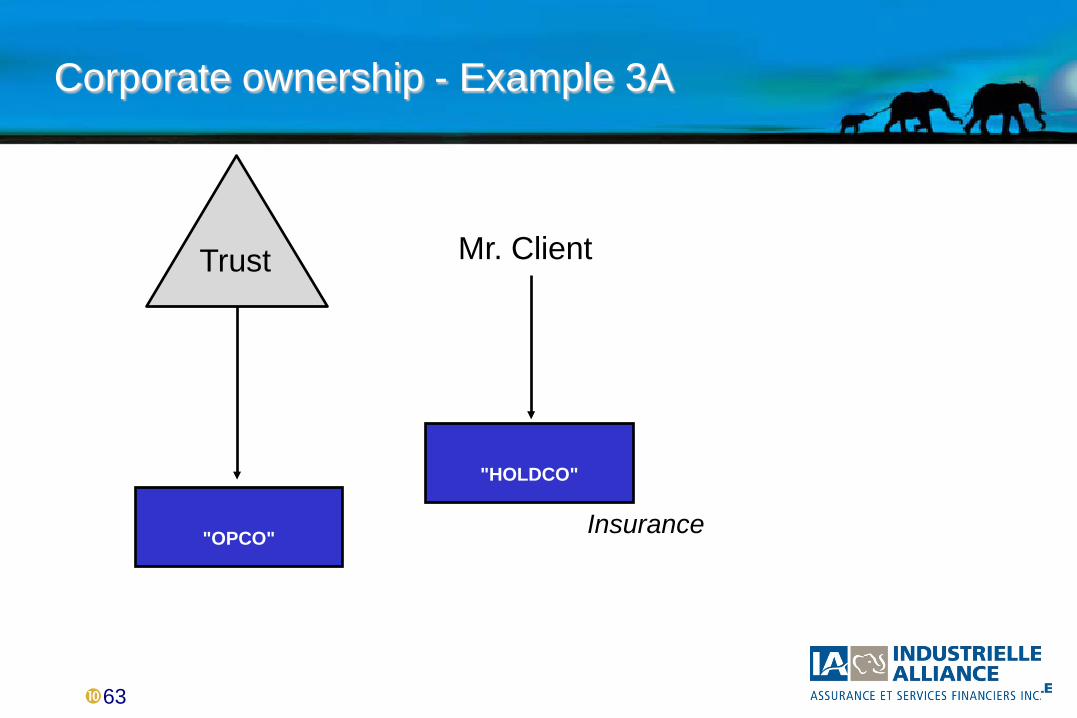

Corporate ownership - Example 3A

"HOLDCO"

Mr. Client

Insurance "OPCO"

Trust

64

Corporate ownership - Example 3B

"HOLDCO"

Mr. Client

Insurance "OPCO"

Trust

65

The elephant: a symbol of our 100 years of strength and longevity.

SHARED OWNERSHIP CRITICAL ILLNESS INSURANCE

66

Shared ownership critical illness insurance - Principle

> Purchasing critical illness insurance

> Designating the beneficiary of the benefit

> Designating the beneficiary of the return of premiums

> Signing a shared ownership agreement

67

Shared ownership critical illness insurance - Principle

> Parties involved:

Corporation

Key person (shareholder or employee)

Other people...

68

Shared ownership critical illness insurance - Principle

> Premium sharing: The corporation pays the premium for the critical illness coverage. The key person pays the premium for the return of premium rider.

69

Shared ownership critical illness insurance - Principle

> Beneficiaries The corporation is the beneficiary of the critical illness benefit. The key person is the beneficiary of the return of premiums.

70

Shared ownership critical illness insurance - Principle

> The shared ownership agreement must be drawn up by an

independent legal advisor.

71

Shared ownership critical illness insurance - Principle

> Shared ownership agreement Parties clearly identified Premium paid by each party Identification of beneficiaries Obligations of each party

Payment of premiums Keeping the policy in force Change of beneficiary Transfer Etc.

72

Shared ownership critical illness insurance - Principle

> Shared ownership agreement Conditions that apply in the following cases:

Financial difficulties and keeping the policy in force Sale of shares in the corporation Disability of the key person Retirement Resignation Etc.

73

Shared ownership critical illness insurance - Taxation

Critical illness insurance doesn't exist

in its own right under the Income Tax Act.

74

Shared ownership critical illness insurance - Taxation

Corporation Key person

Deductibility of premiums Non-deductible Non-deductible

Taxable benefit n/a No taxable benefit*

Critical illness insurance benefit Non-taxable (no CDA)

n/a

Return of premiums at death Non-taxable (no CDA)

Non-taxable No taxable benefit*

Return of premiums upon surrender n/a Non-taxable No taxable benefit*

75

Shared ownership critical illness insurance - Advantages

> The premiums are largely paid by the corporation and the money is taxed at a lower rate.

> The return of premiums includes the premiums paid by the corporation.

76

Shared ownership critical illness insurance - Disadvantages

> Benefit not included in the CDA

> In the event of critical illness: No return of premiums A taxable dividend must be paid to the shareholder in order for

him or her to receive the benefit.

77

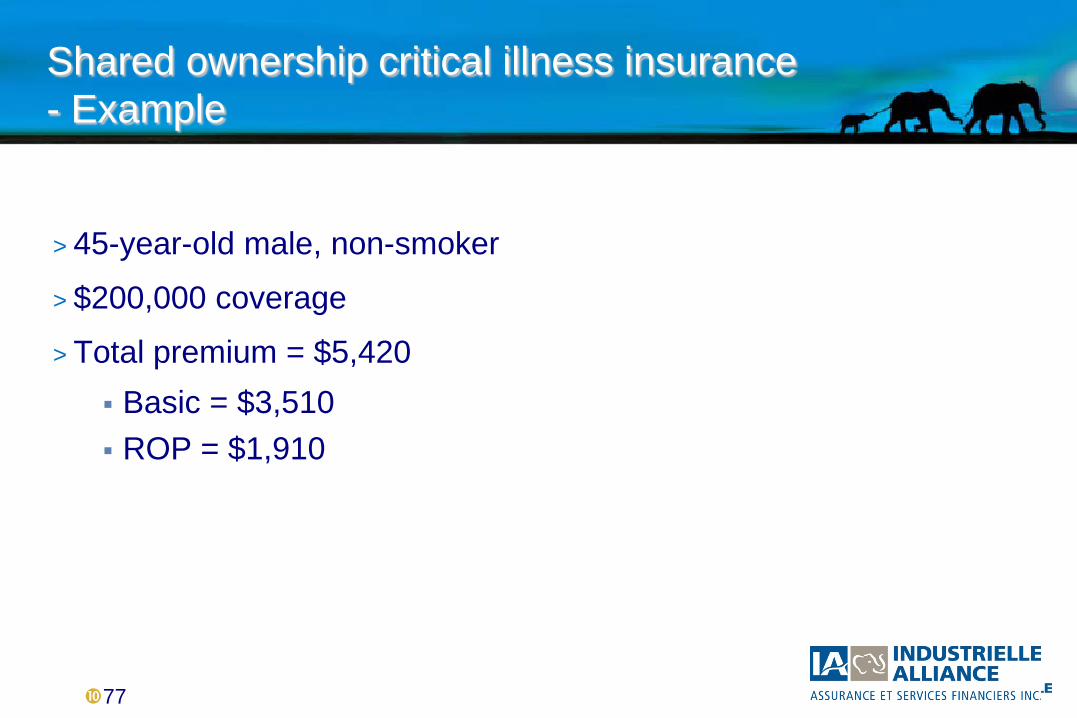

Shared ownership critical illness insurance - Example

> 45-year-old male, non-smoker

> $200,000 coverage

> Total premium = $5,420 Basic = $3,510 ROP = $1,910

78

Shared ownership critical illness insurance - Example

> Individual purchase:

Dividend paid: $8,818 Dividend tax (shareholder): ($3,398)

Premium payment by shareholder: ($5,420)

79

Shared ownership critical illness insurance - Example

> Individual purchase

> The benefit or return of premiums is paid directly to the shareholder

Benefit: $200,000 ROP: $81,300

80

Shared ownership critical illness insurance - Example

> Shared ownership purchase

Basic premium payment $3,510 ROP payment $1,910 Shareholder's taxable benefit $1,910 Tax paid (shareholder) ($736)

* The corporation must pay a dividend of $1,198 to the shareholder in order for him or

her to pay the tax of $736.

81

Shared ownership critical illness insurance - Example

> Shared ownership purchase

> Actual cost for the corporation: Basic premium payment $3,510 ROP payment $1,910 Dividend payment for tax $1,198

Total $6,618

82

Shared ownership critical illness insurance - Example

> Shared ownership purchase

Critical illness benefit $200,000 Dividend to the shareholder Dividend tax ($77,080)

Balance for the shareholder $122,920

83

Shared ownership critical illness insurance

It's essential to properly determine the need for and volume of insurance!

84

2003-0035385 - Critical illness insurance policy

Scenario where a corporation is the owner of a critical illness insurance policy on a single shareholder.

Questions asked:

>"Are the premiums paid by the corporation deductible?"

Answer: No. The premiums are not incurred to earn an income.

>"Does the payment of premiums by the corporation represent a taxable benefit for the shareholder?"

Answer: Yes, if the shareholder is the beneficiary of the policy.

>"Are the benefits received taxable?"

Answer: No, the benefits are not taxable.

85

2003-0182875 Insurance policy transfer

Question asked: "Does a shareholder have to include a benefit in the calculation of his or her

income if a corporation transfers a critical insurance policy to him without consideration?"

Answer: > Although it's not an insurance contract, the tax authorities are of the opinion that a

shareholder who acquires this kind of policy from a corporation for consideration equal to less than its FMV will have to include in his or her income an amount equal to the amount by which the FMV exceeds the consideration received.

> FMV: Age, insured's state of health, the amount of premiums refundable and the amount of premiums paid on the transfer date are aspects to consider.

86

2004-0090181E5 Critical Illness Insurance

Questions asked:

"Is the premium paid by a corporation on a critical illness policy that covers the shareholder and the premium associated with the return of premium rider tax deductible?"

> Answer: No. The premiums are not incurred to earn an income.

"Are the benefits received by the corporation if the shareholder contracts a critical illness and the return of premiums received in the opposite case taxable?"

> Answer: No.

87

2004-0090181E5 Critical Illness Insurance

Question asked: "Does a benefit conferred on a shareholder under subsection 15(1) of the Act have to be recognized for the shareholder, and if so, when?"

Answers: If the corporation owns a critical illness insurance policy whose benefit is payable to the corporation, the premiums paid generally don't generate any taxable benefits. In the opposite case, the tax authorities are of the opinion that there could be a taxable benefit even if the shareholder personally pays for the return of premium rider (depending on the facts).

88

2006-0178561E5 Taxable benefit - CI insurance

Question asked:

"How is the taxable benefit determined for a shareholder with regard to a critical illness insurance policy where one portion of the premiums is paid by the shareholder and another portion is paid by the corporation?"

Answer:

> The value of the benefit could correspond to the amount the shareholder should pay in similar circumstances to obtain the same benefit resulting from the transaction in question from a person who deals at arm's length.

> Is the corporation impoverished in some way? (The notion of the corporation's impoverishment is not clearly determined.)

![TAX ON PRESUMPTIVE BASIS IN CASE OF CERTAIN …. Tax on presumptive basis in... · [As amended by Finance Act, 2017] TAX ON PRESUMPTIVE BASIS IN CASE OF CERTAIN ELIGIBLE BUSINESSES](https://img.pdfslide.net/doc/110x75/5a9bb3667f8b9a9c5b8e309f/tax-on-presumptive-basis-in-case-of-certain-tax-on-presumptive-basis-inas.jpg)

![TAX ON PRESUMPTIVE BASIS IN CASE OF CERTAIN …. tax on presumptive... · [As amended by Finance Act, 2018] TAX ON PRESUMPTIVE BASIS IN CASE OF CERTAIN ELIGIBLE BUSINESSES OR PROFESSIONS](https://img.pdfslide.net/doc/110x75/5b157fac7f8b9ae7348cc755/tax-on-presumptive-basis-in-case-of-certain-tax-on-presumptive-as-amended.jpg)