Embed Size (px)

Citation preview

A growing asset class in difficult times

LIUC

April 2009

1

Investing in High Yield and Distressed Debt

AGENDA

Basics of Credit Investing

Investing in HY and Distress

Strategies and Trading Technicals

Current situation

Appendix

2

Basics of Credit Investing

A Focus on High Yield Bonds and

Leverage Loans

3

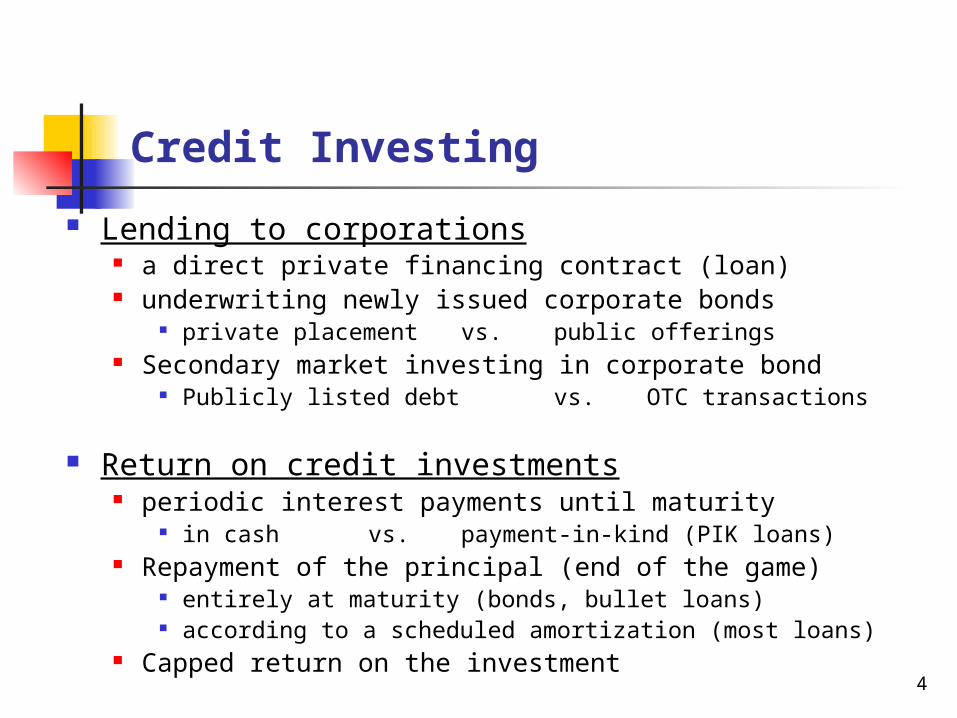

Credit Investing

Lending to corporations a direct private financing contract (loan) underwriting newly issued corporate bonds

private placement vs. public offerings Secondary market investing in corporate bond

Publicly listed debt vs. OTC transactions

Return on credit investments periodic interest payments until maturity

in cash vs. payment-in-kind (PIK loans) Repayment of the principal (end of the game)

entirely at maturity (bonds, bullet loans) according to a scheduled amortization (most loans)

Capped return on the investment 4

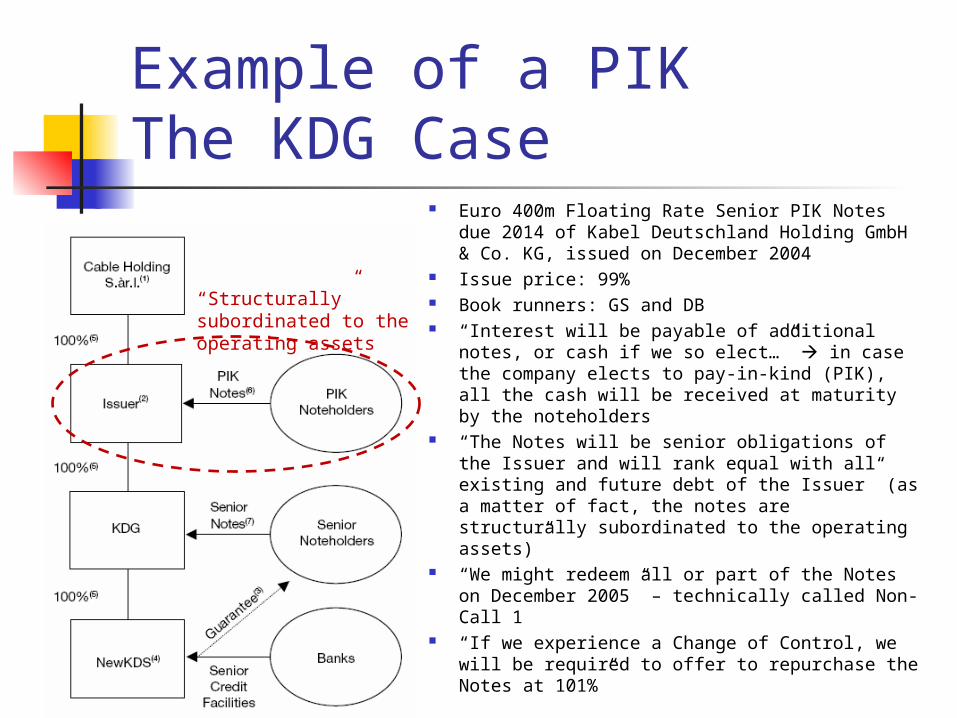

Example of a PIK The KDG Case

Euro 400m Floating Rate Senior PIK Notes due 2014 of Kabel Deutschland Holding GmbH & Co. KG, issued on December 2004

Issue price: 99% Book runners: GS and DB “Interest will be payable of additional notes, or

cash if we so elect…” in case the company elects to pay-in-kind (PIK), all the cash will be received at maturity by the noteholders

“The Notes will be senior obligations of the Issuer and will rank equal with all existing and future debt of the Issuer” (as a matter of fact, the notes are structurally subordinated to the operating assets)”

“We might redeem all or part of the Notes on December 2005” – technically called Non-Call 1

“If we experience a Change of Control, we will be required to offer to repurchase the Notes at 101%”

“Structurally” subordinated to the operating assets

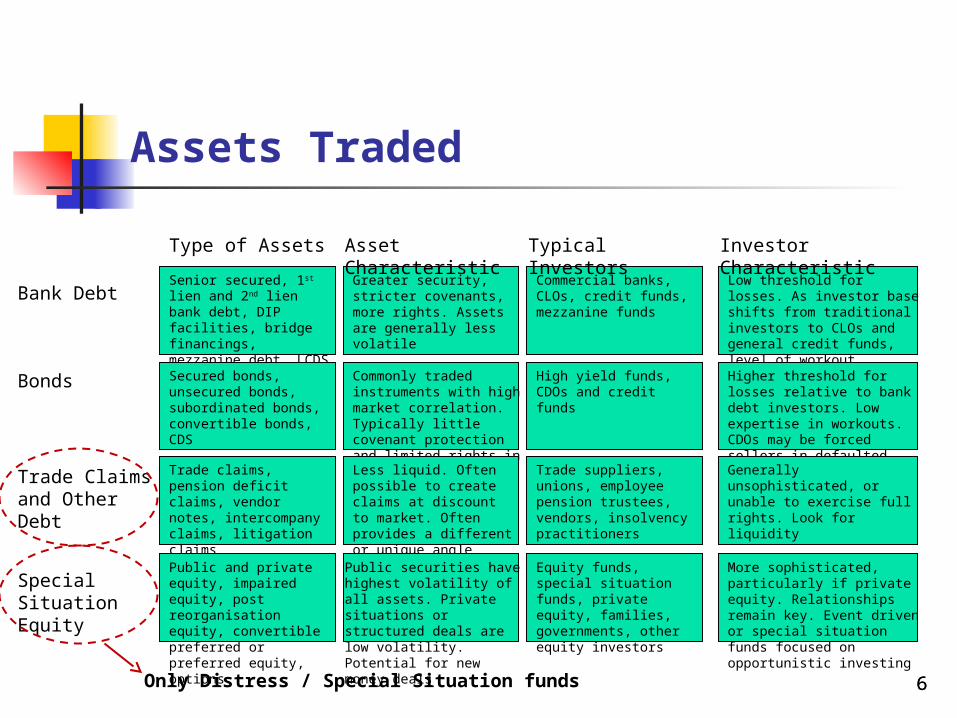

Assets Traded

Senior secured, 1st lien and 2nd lien bank debt, DIP facilities, bridge financings, mezzanine debt, LCDS

Greater security, stricter covenants, more rights. Assets are generally less volatile

Commercial banks, CLOs, credit funds, mezzanine funds

Low threshold for losses. As investor base shifts from traditional investors to CLOs and general credit funds, level of workout expertise is decreasing

Secured bonds, unsecured bonds, subordinated bonds, convertible bonds, CDS

Commonly traded instruments with high market correlation. Typically little covenant protection and limited rights in a workout

High yield funds, CDOs and credit funds

Higher threshold for losses relative to bank debt investors. Low expertise in workouts. CDOs may be forced sellers in defaulted situations

Trade claims, pension deficit claims, vendor notes, intercompany claims, litigation claims

Less liquid. Often possible to create claims at discount to market. Often provides a different or unique angle

Trade suppliers, unions, employee pension trustees, vendors, insolvency practitioners

Generally unsophisticated, or unable to exercise full rights. Look for liquidity

Public and private equity, impaired equity, post reorganisation equity, convertible preferred or preferred equity, options

Public securities have highest volatility of all assets. Private situations or structured deals are low volatility. Potential for new money deals

Equity funds, special situation funds, private equity, families, governments, other equity investors

More sophisticated, particularly if private equity. Relationships remain key. Event driven or special situation funds focused on opportunistic investing

Type of Assets Asset CharacteristicTypical Investors Investor Characteristic

Bank Debt

Bonds

Trade Claims and Other Debt

Special Situation Equity

6Only Distress / Special Situation funds 6

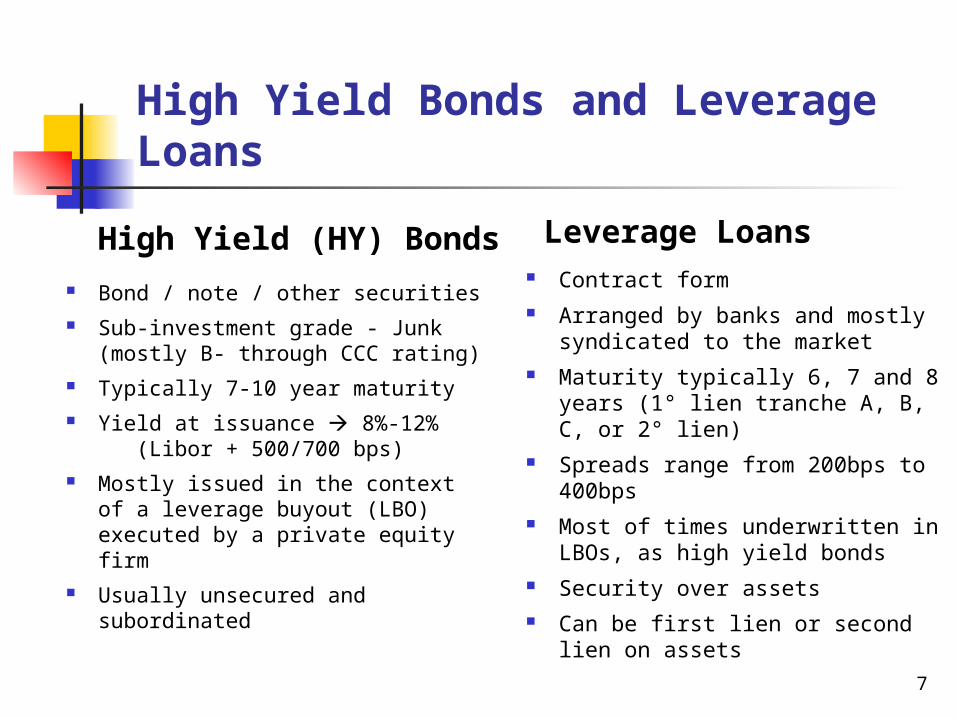

High Yield Bonds and Leverage Loans

High Yield (HY) Bonds

Bond / note / other securities Sub-investment grade - Junk

(mostly B- through CCC rating) Typically 7-10 year maturity Yield at issuance 8%-12%

(Libor + 500/700 bps) Mostly issued in the context of

a leverage buyout (LBO) executed by a private equity firm

Usually unsecured and subordinated

Leverage Loans Contract form Arranged by banks and mostly

syndicated to the market Maturity typically 6, 7 and 8

years (1° lien tranche A, B, C, or 2° lien)

Spreads range from 200bps to 400bps

Most of times underwritten in LBOs, as high yield bonds

Security over assets Can be first lien or second lien

on assets7

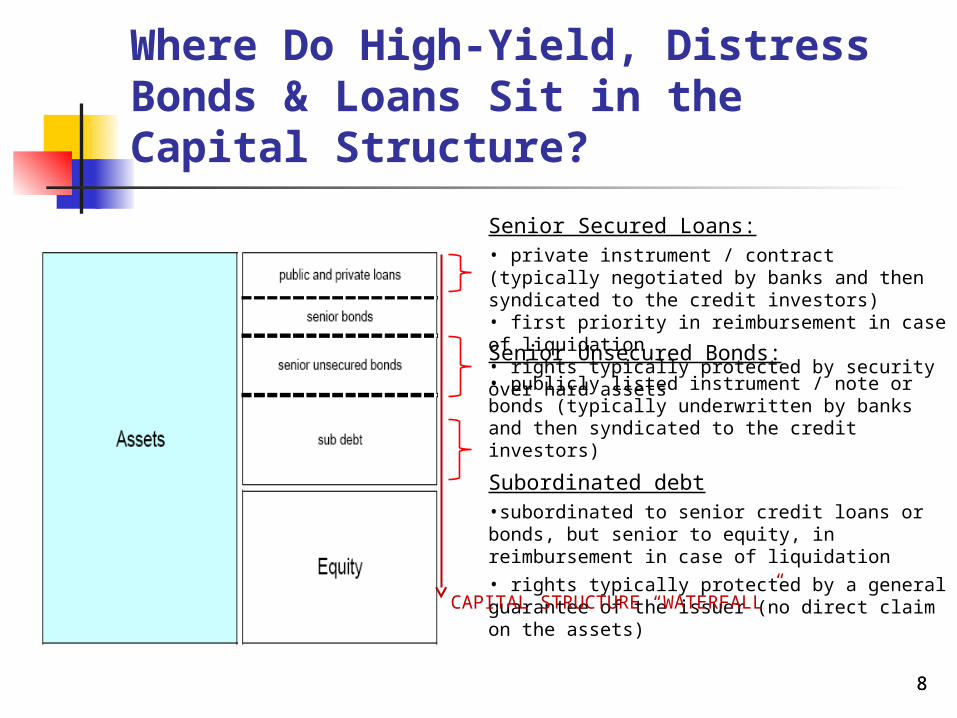

Where Do High-Yield, Distress Bonds & Loans Sit in the Capital Structure?

• private instrument / contract (typically negotiated by banks and then syndicated to the credit investors)• first priority in reimbursement in case of liquidation• rights typically protected by security over hard assets• publicly listed instrument / note or bonds (typically underwritten by banks and then syndicated to the credit investors)

Subordinated debt•subordinated to senior credit loans or bonds, but senior to equity, in reimbursement in case of liquidation

• rights typically protected by a general guarantee of the issuer (no direct claim on the assets)

Senior Secured Loans:

Senior Unsecured Bonds:

8

CAPITAL STRUCTURE “WATERFALL”

8

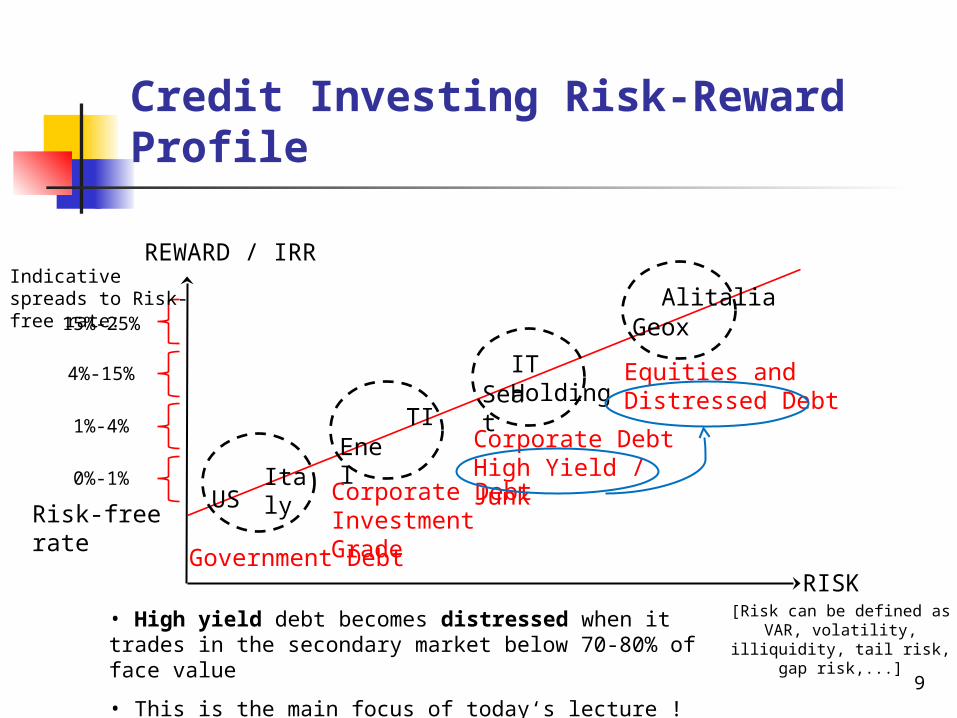

Credit Investing Risk-Reward Profile

RISK

REWARD / IRR

Risk-free rate

USItaly

Government Debt

Enel

TI

Corporate DebtInvestment Grade

Seat

IT Holding

Corporate DebtHigh Yield / Junk

GeoxAlitalia

Equities andDistressed Debt

Indicative spreads to Risk-free rate:

15%-25%

4%-15%

1%-4%

0%-1%

• High yield debt becomes distressed when it trades in the secondary market below 70-80% of face value

• This is the main focus of today‘s lecture !

[Risk can be defined as VAR, volatility, illiquidity,

tail risk, gap risk,...]

9

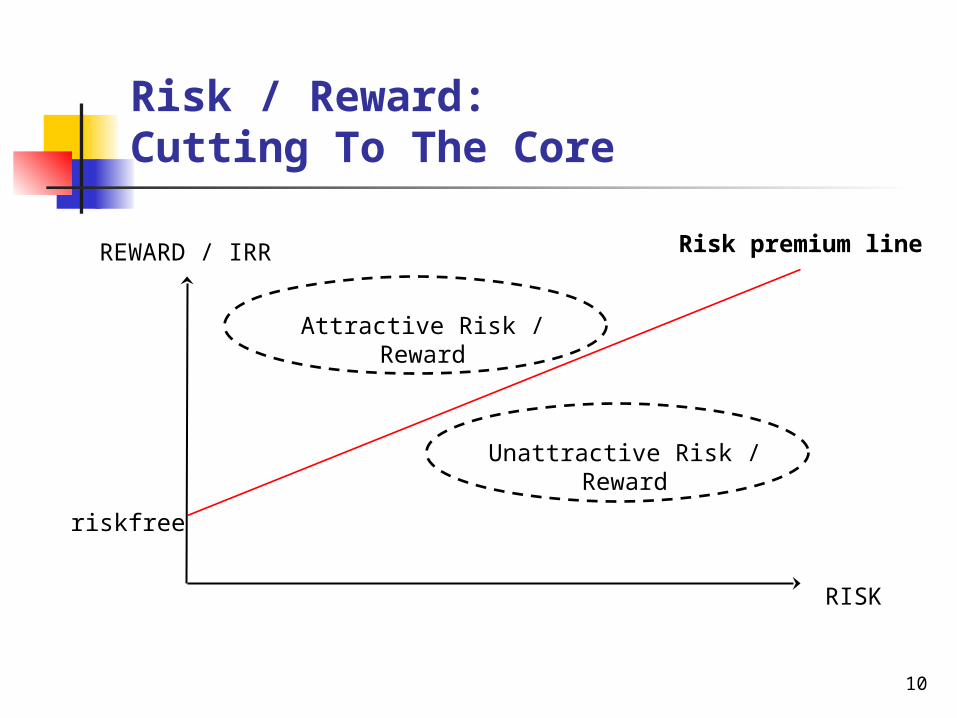

Risk / Reward: Cutting To The Core

RISK

REWARD / IRR

Attractive Risk / Reward

Unattractive Risk / Reward

10

Risk premium line

riskfree

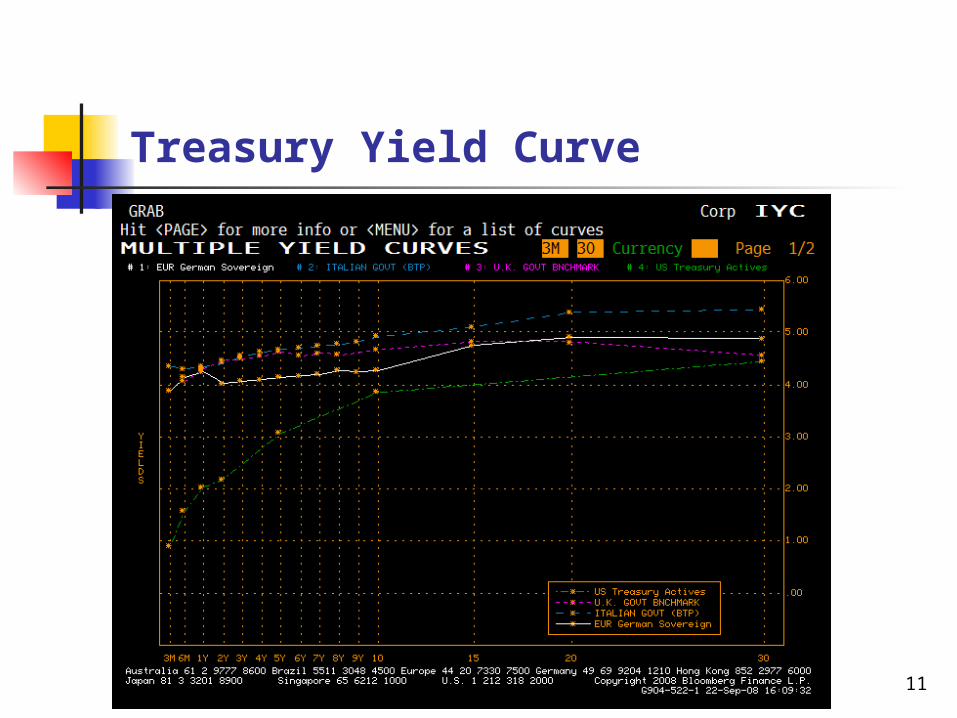

Treasury Yield Curve

11

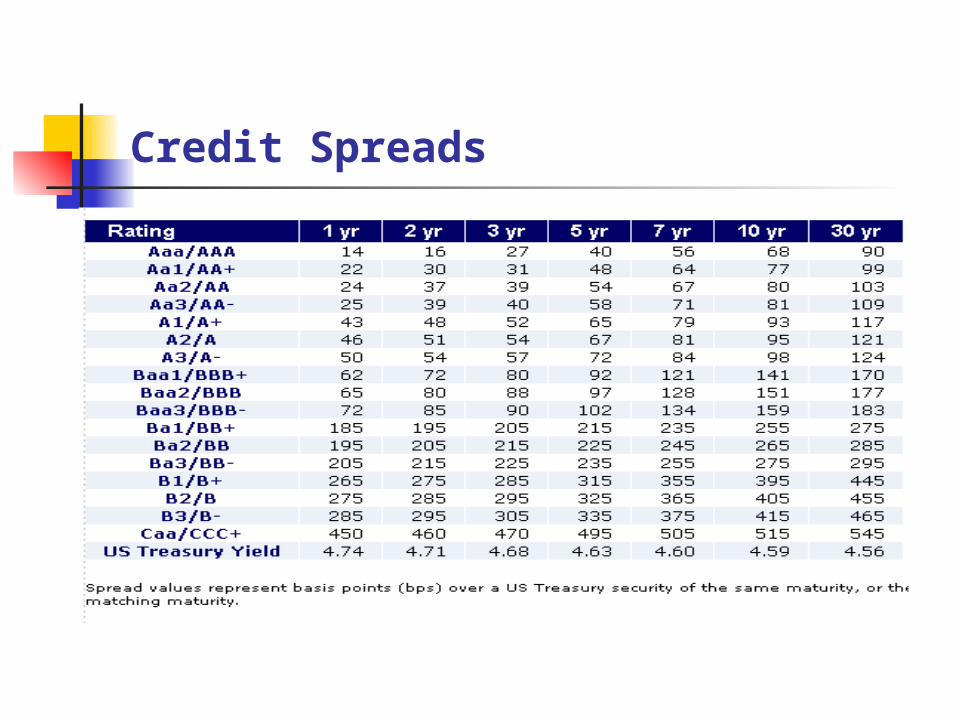

Credit Spreads

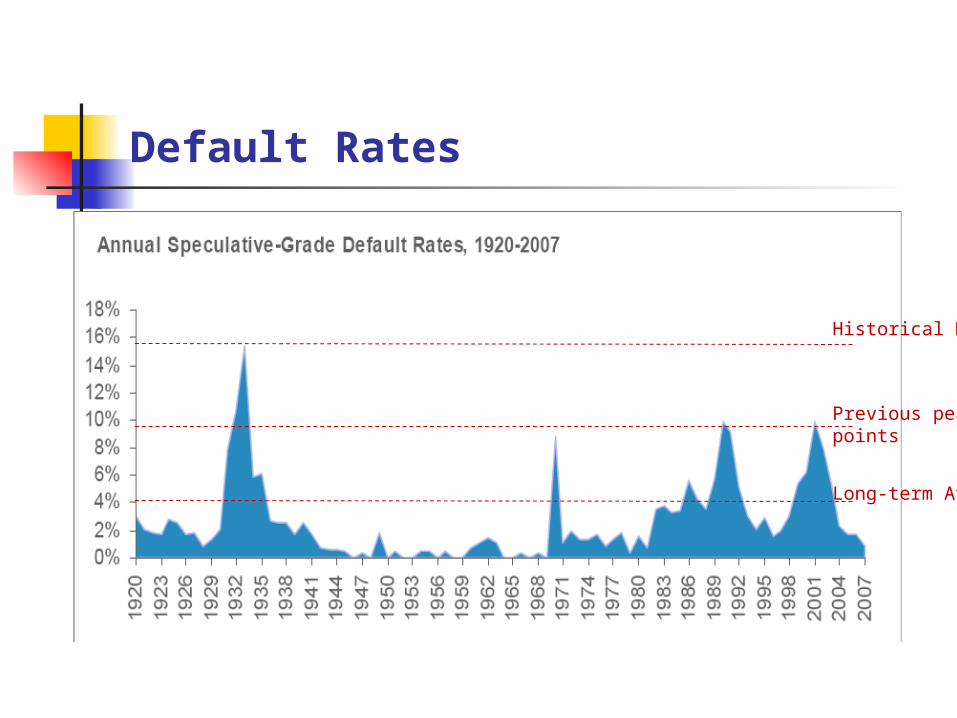

Default Rates

Long-term Avg

Previous peakpoints

Historical Max

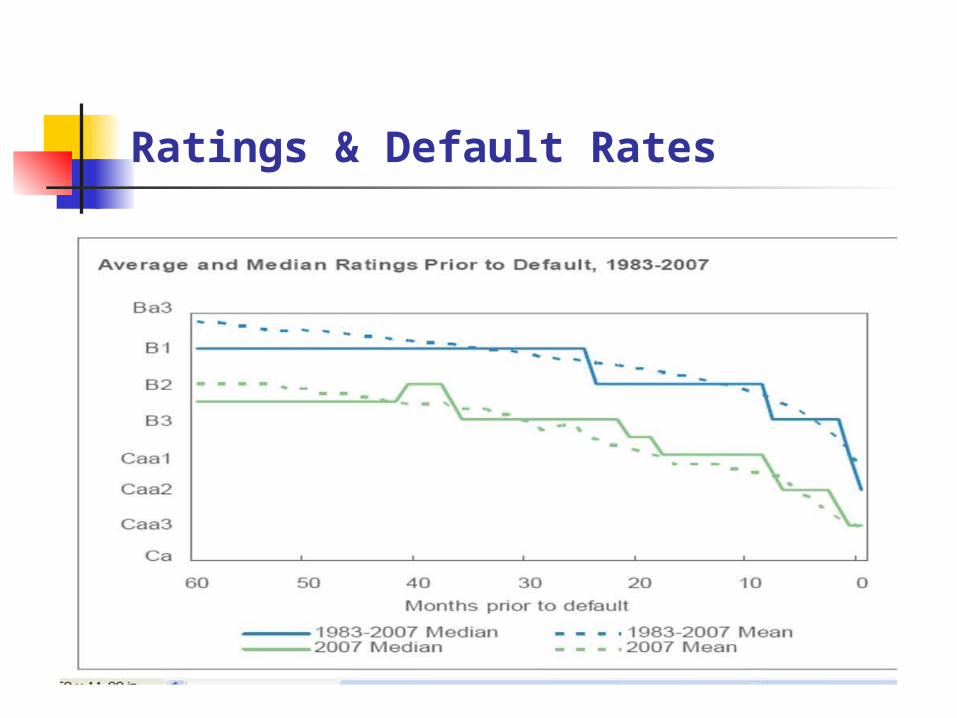

Ratings & Default Rates

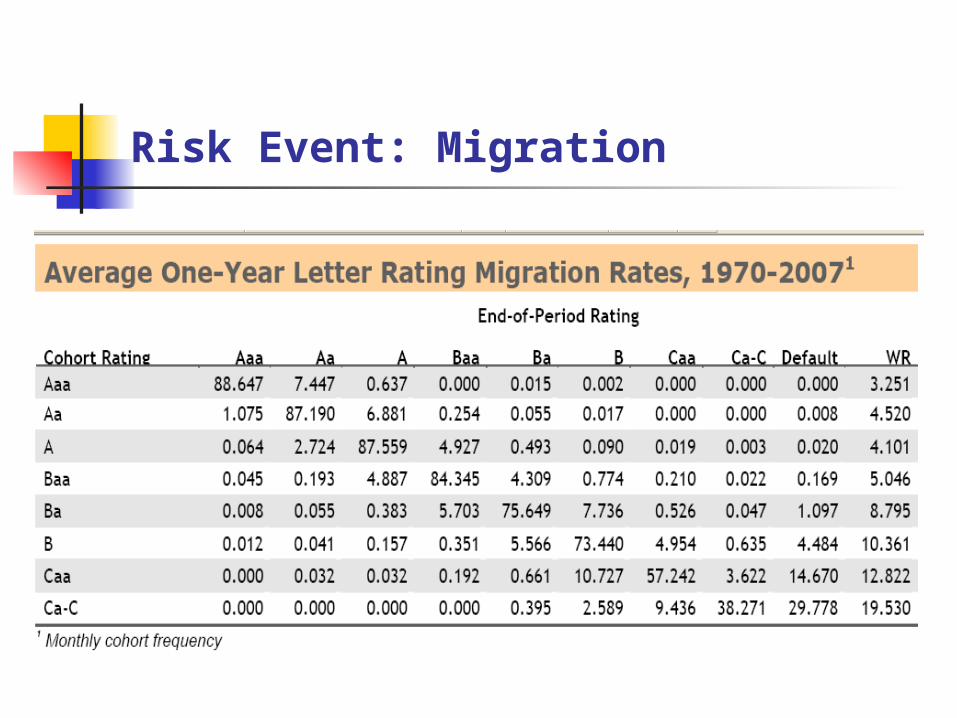

Risk Event: Migration

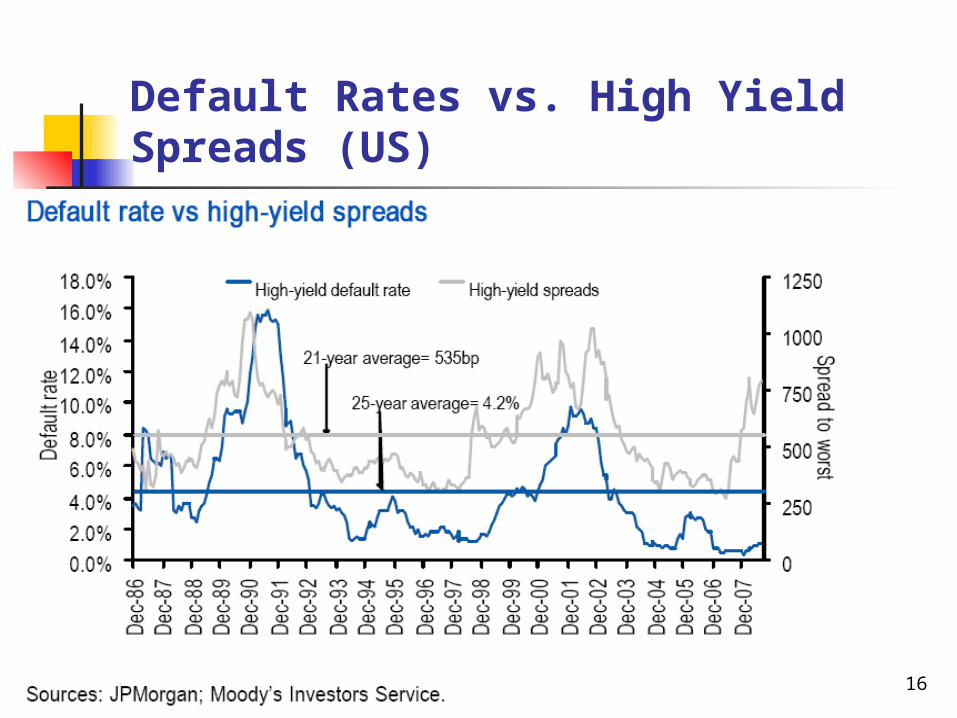

Default Rates vs. High Yield Spreads (US)

16

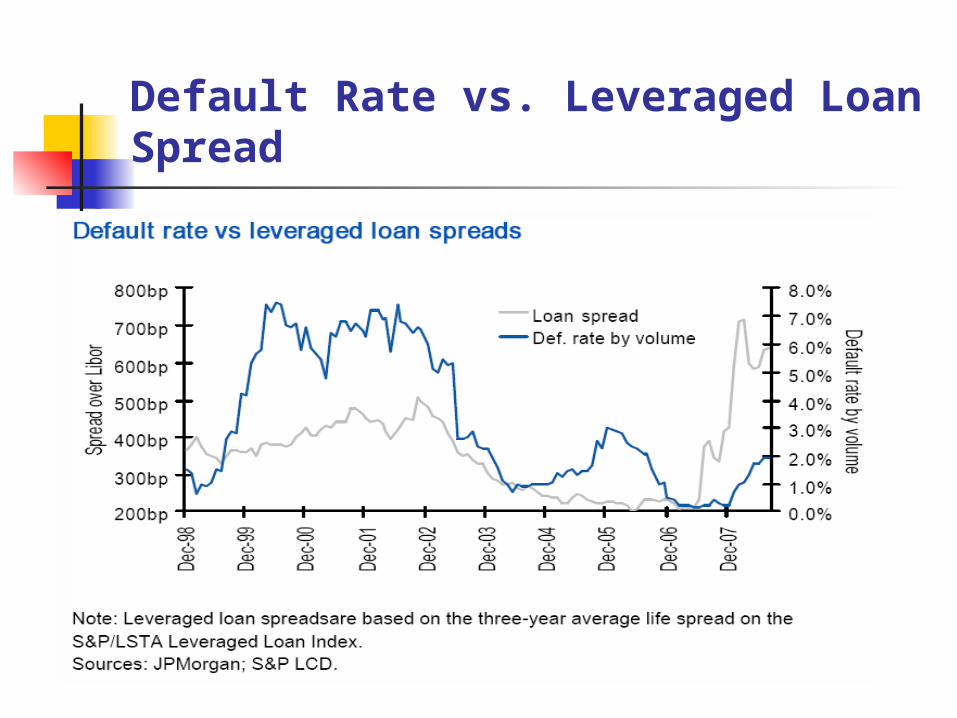

Default Rate vs. Leveraged Loan Spread

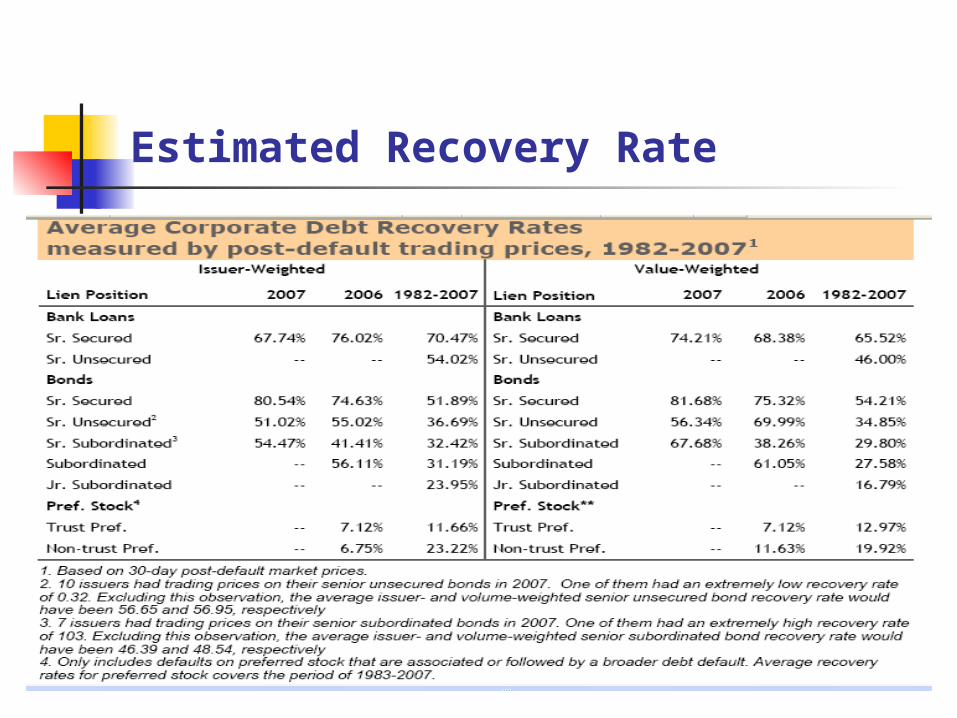

Estimated Recovery Rate

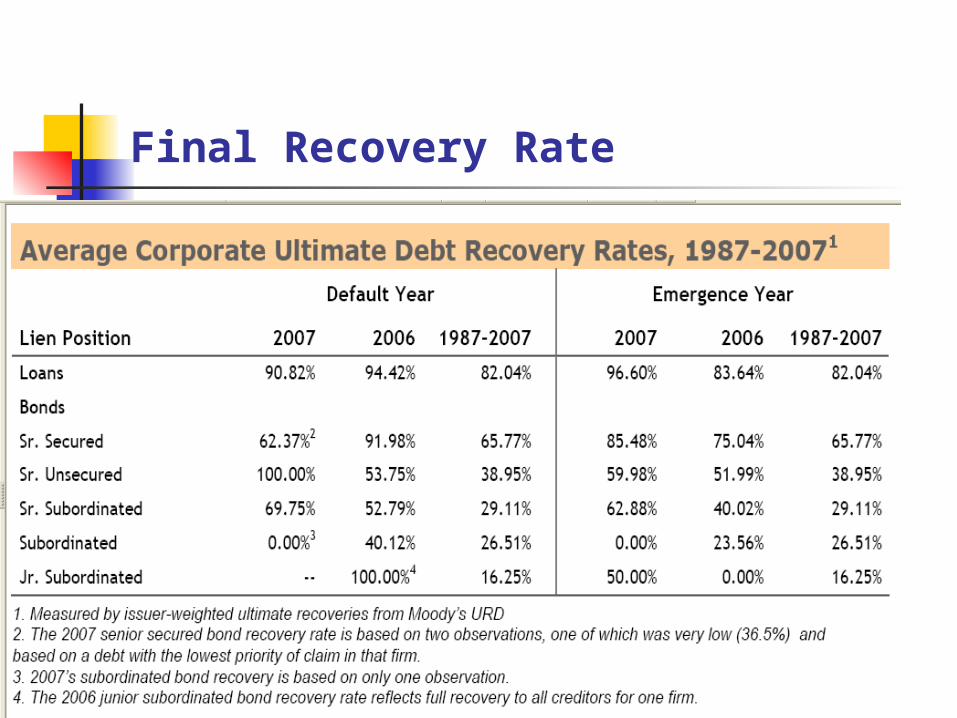

Final Recovery Rate

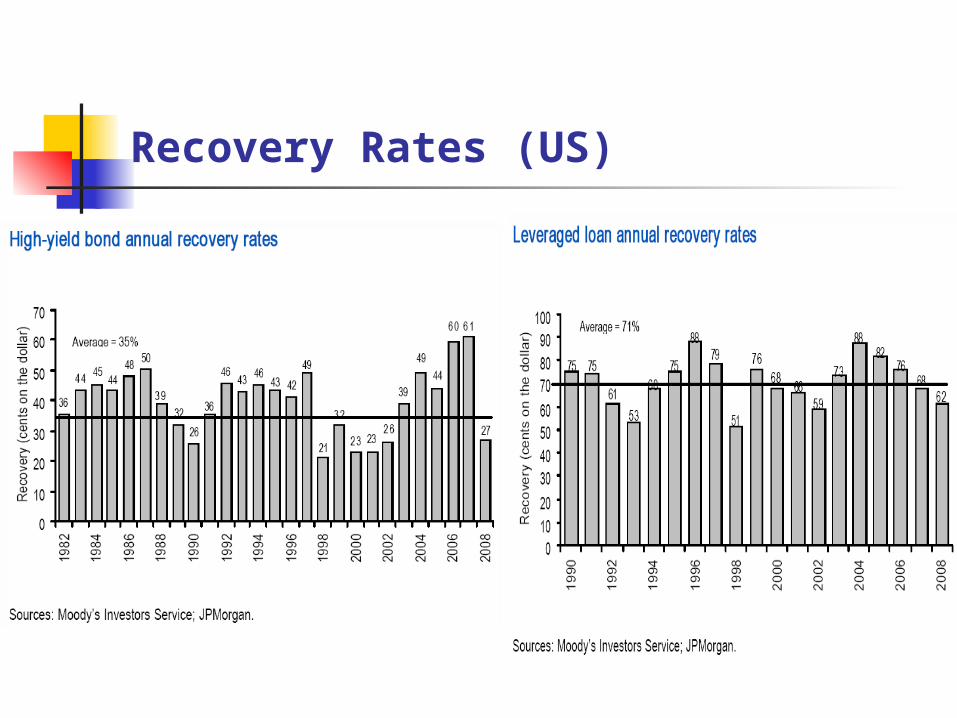

Recovery Rates (US)

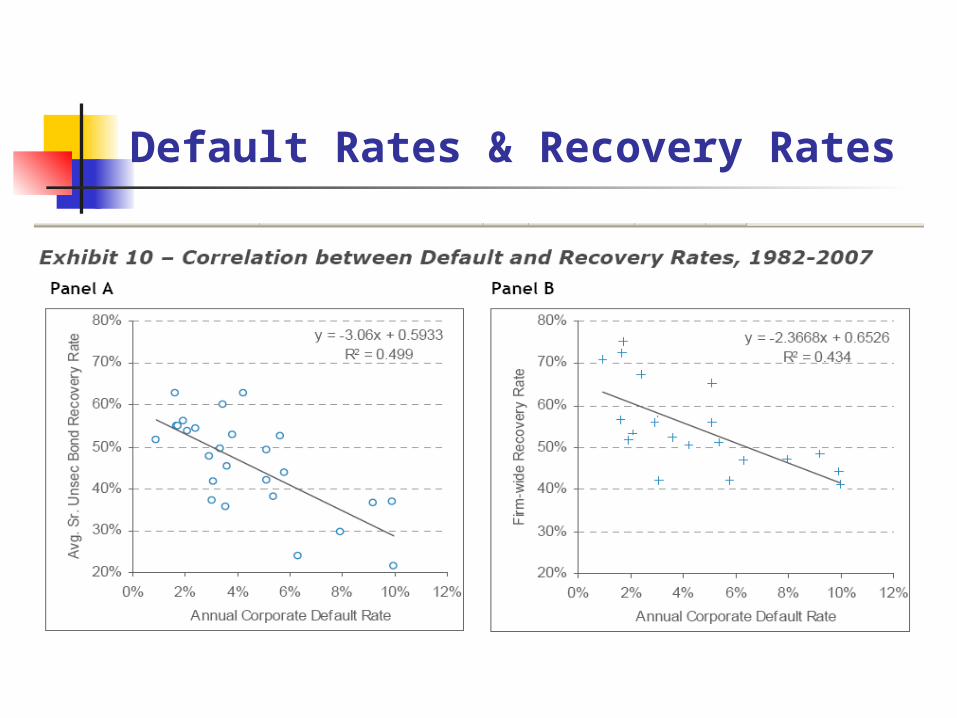

Default Rates & Recovery Rates

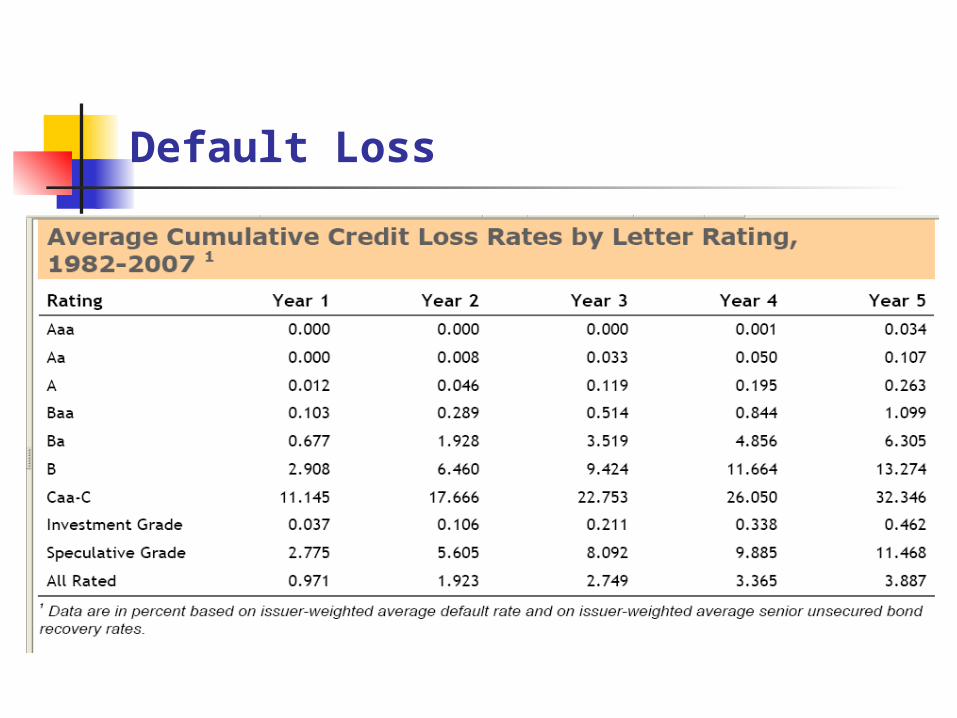

Default Loss

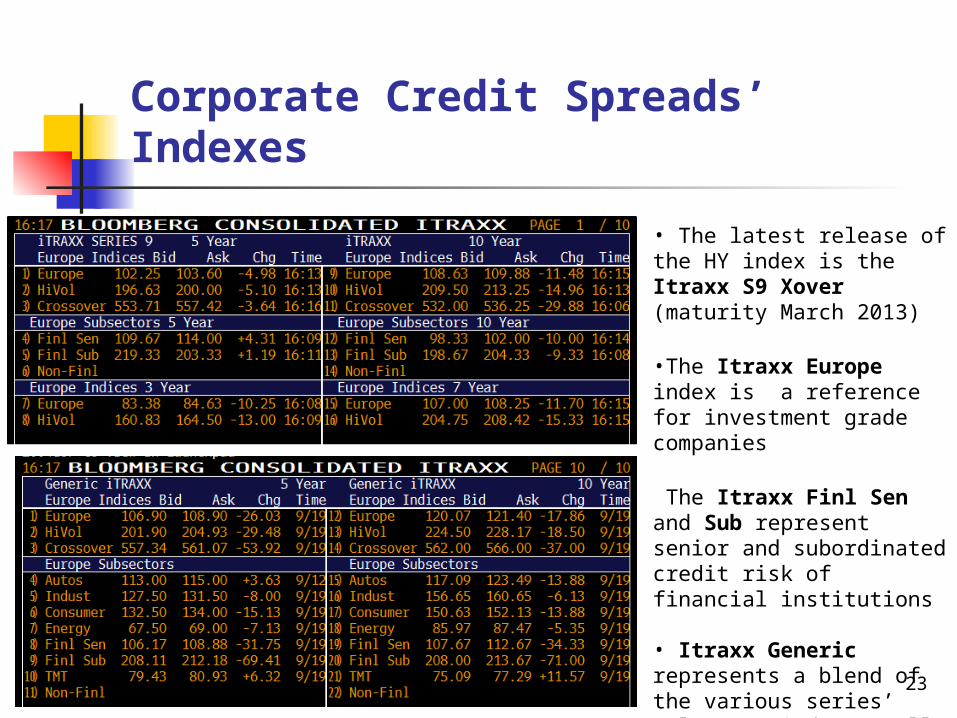

Corporate Credit Spreads’ Indexes

• The latest release of the HY index is the Itraxx S9 Xover (maturity March 2013)

•The Itraxx Europe index is a reference for investment grade companies

The Itraxx Finl Sen and Sub represent senior and subordinated credit risk of financial institutions

• Itraxx Generic represents a blend of the various series’ releases (indexes roll every 6 months into a new release with new constituents)

23

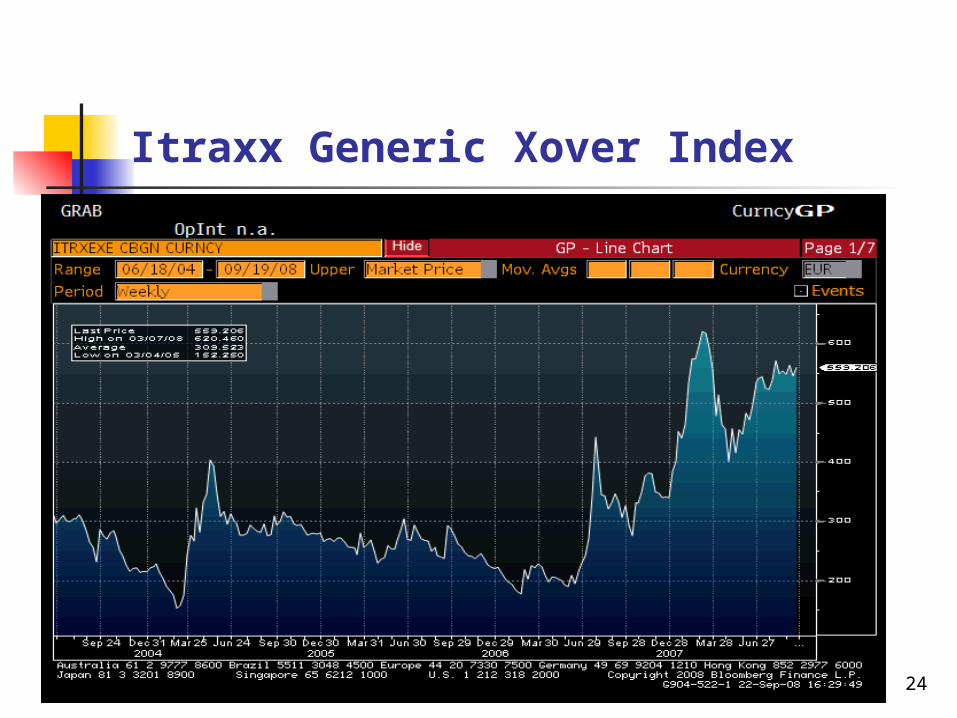

Itraxx Generic Xover Index

24

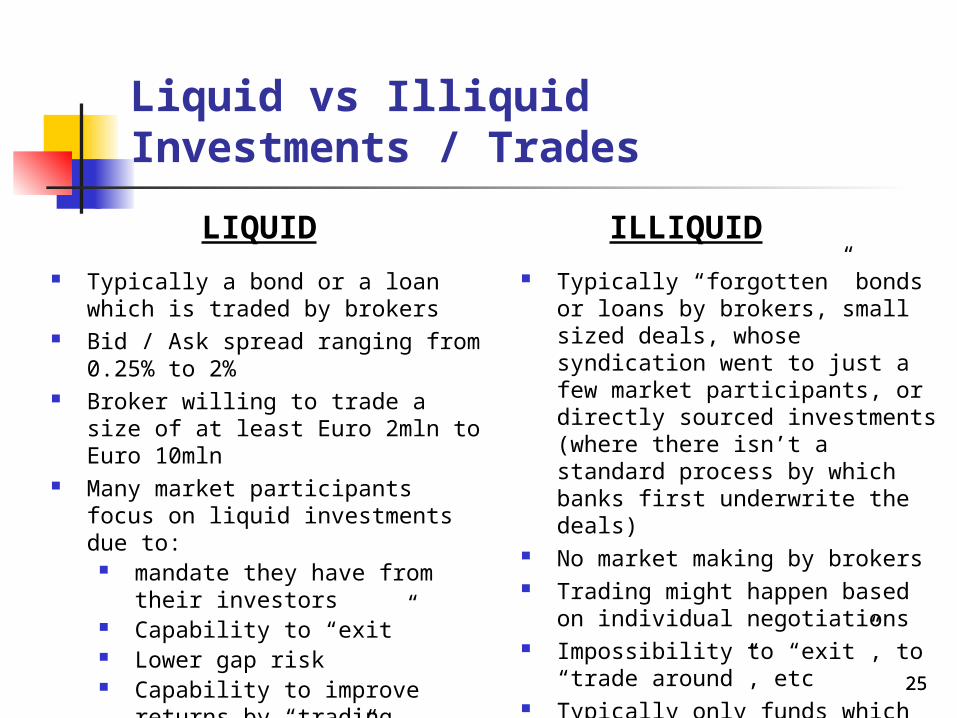

Liquid vs Illiquid Investments / Trades

Typically a bond or a loan which is traded by brokers

Bid / Ask spread ranging from 0.25% to 2%

Broker willing to trade a size of at least Euro 2mln to Euro 10mln

Many market participants focus on liquid investments due to:

mandate they have from their investors

Capability to “exit” Lower gap risk Capability to improve returns

by “trading around positions”, hence benefitting from volatility

Typically “forgotten” bonds or loans by brokers, small sized deals, whose syndication went to just a few market participants, or directly sourced investments (where there isn’t a standard process by which banks first underwrite the deals)

No market making by brokers Trading might happen based on

individual negotiations Impossibility to “exit”, to “trade

around”, etc Typically only funds which have a

lock-up period and who target a return premium for the illiquidity

LIQUID ILLIQUID

2525

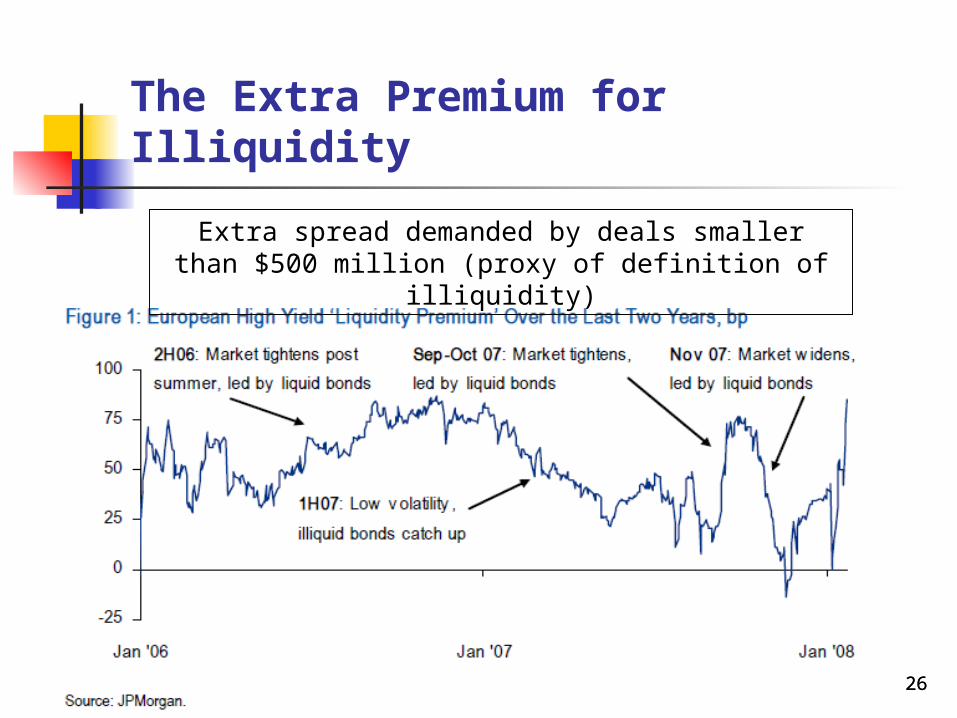

The Extra Premium for Illiquidity

Extra spread demanded by deals smaller than $500 million (proxy of definition of illiquidity)

2626

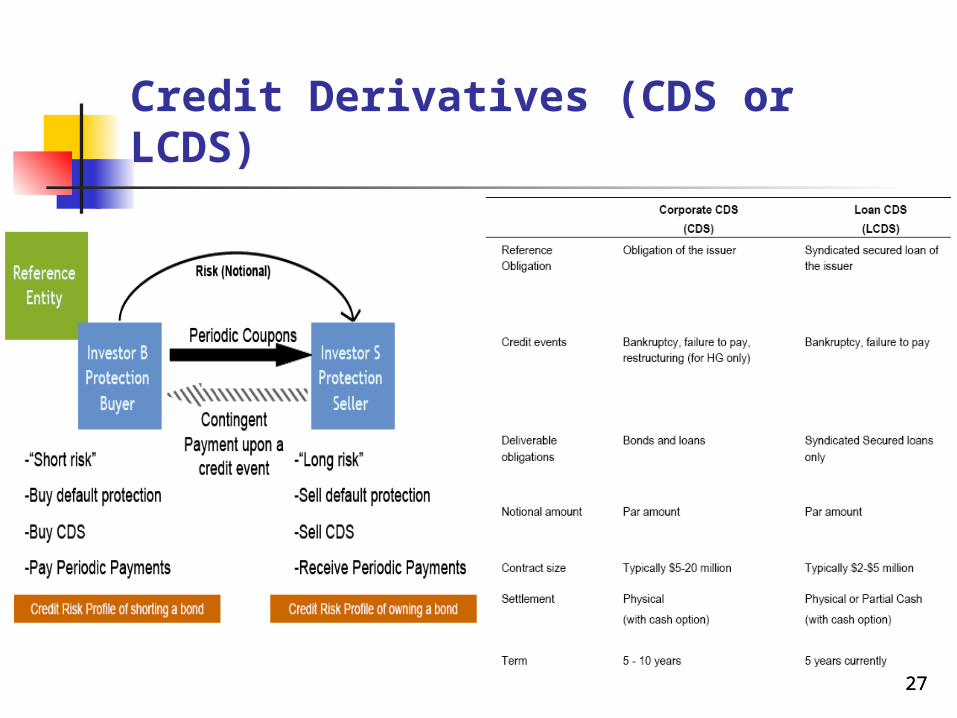

Credit Derivatives (CDS or LCDS)

2727

Importance of Derivatives for the Asset Class

Hedging If you are “long” a single name credit risk, you can hedge

the trade without going through the process of selling the underlying cash asset buying a CDS on that name

If you are “long” market credit risk, you may buy credit index protection to hedge the exposure to the market (i.e. Itraxx)

Capability to have additional liquidity in the market

Capability to deploy curve and basis trades relative value market neutral

2828

Invest in HY and Distress

Evolving Asset Class by the Day

2929

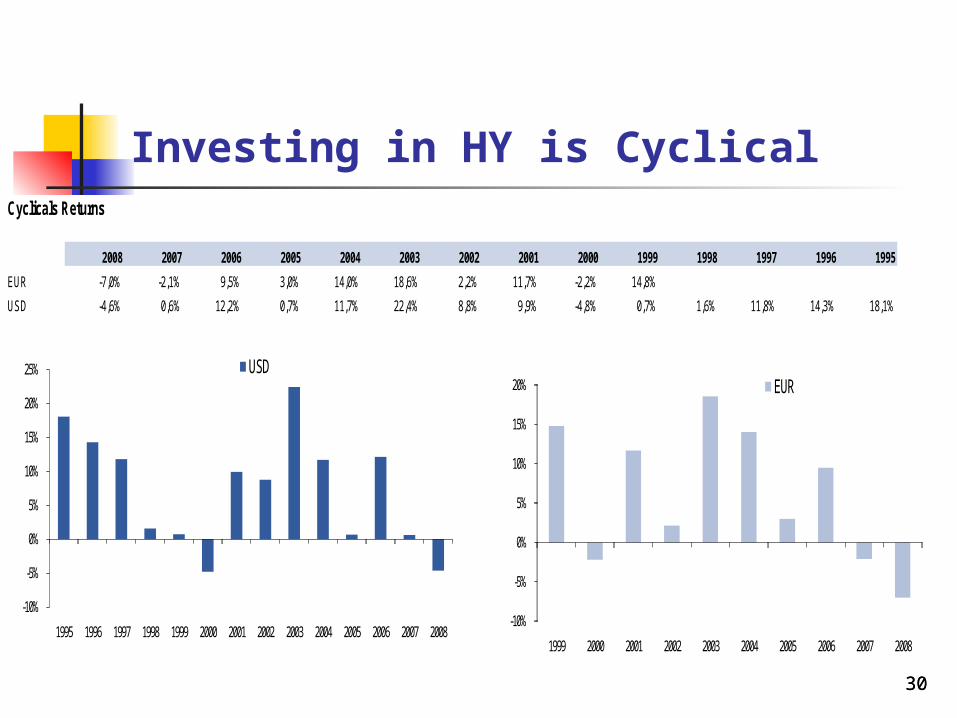

Investing in HY is CyclicalCyclicals Returns

2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995

EUR -7,0% -2,1% 9,5% 3,0% 14,0% 18,6% 2,2% 11,7% -2,2% 14,8%

USD -4,6% 0,6% 12,2% 0,7% 11,7% 22,4% 8,8% 9,9% -4,8% 0,7% 1,6% 11,8% 14,3% 18,1%

-10%

-5%

0%

5%

10%

15%

20%

25%

20082007200620052004200320022001200019991998199719961995

USD

-10%

-5%

0%

5%

10%

15%

20%

2008200720062005200420032002200120001999

EUR

3030

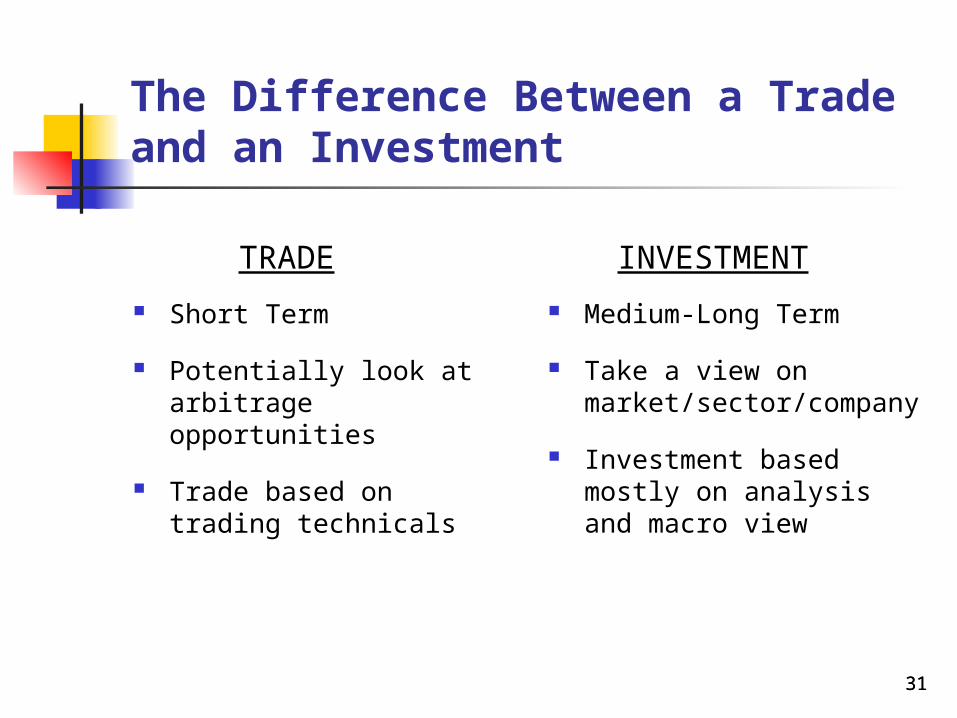

The Difference Between a Trade and an Investment

Short Term

Potentially look at arbitrage opportunities

Trade based on trading technicals

Medium-Long Term

Take a view on market/sector/company

Investment based mostly on analysis and macro view

TRADE INVESTMENT

3131

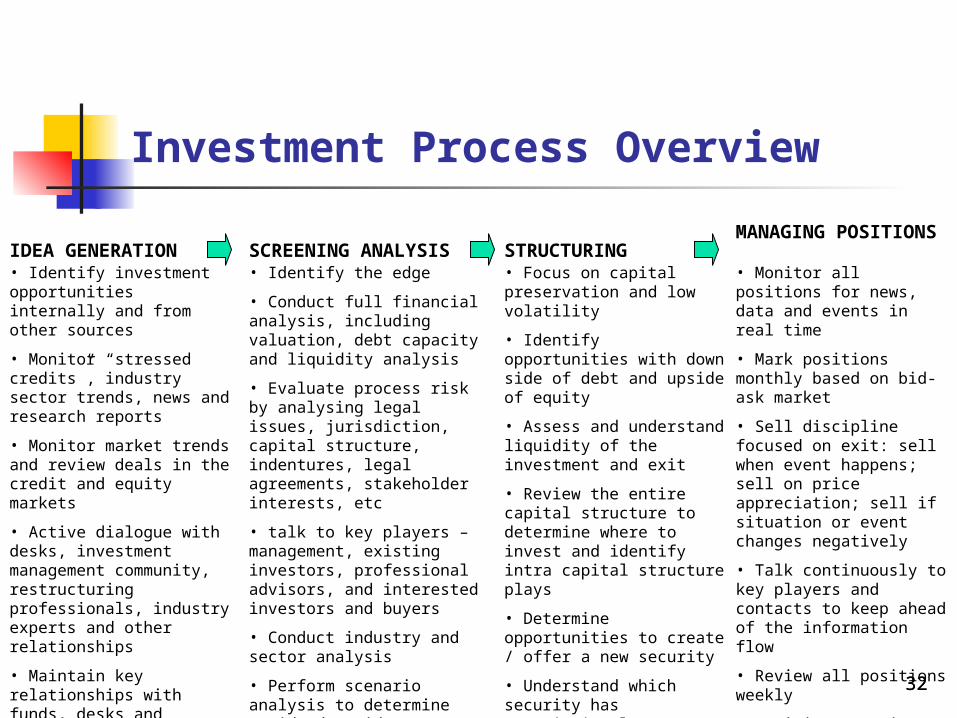

Investment Process Overview

• Identify investment opportunities internally and from other sources

• Monitor “stressed credits”, industry sector trends, news and research reports

• Monitor market trends and review deals in the credit and equity markets

• Active dialogue with desks, investment management community, restructuring professionals, industry experts and other relationships

• Maintain key relationships with funds, desks and professionals and industrial players

• Identify the edge

• Conduct full financial analysis, including valuation, debt capacity and liquidity analysis

• Evaluate process risk by analysing legal issues, jurisdiction, capital structure, indentures, legal agreements, stakeholder interests, etc

• talk to key players – management, existing investors, professional advisors, and interested investors and buyers

• Conduct industry and sector analysis

• Perform scenario analysis to determine upside/downside cases

• Identify events and timing to events

• Focus on capital preservation and low volatility

• Identify opportunities with down side of debt and upside of equity

• Assess and understand liquidity of the investment and exit

• Review the entire capital structure to determine where to invest and identify intra capital structure plays

• Determine opportunities to create / offer a new security

• Understand which security has negotiating leverage, and assess stakeholder interests

• Determine size, liquidity and overall fit with portfolio

• Monitor all positions for news, data and events in real time

• Mark positions monthly based on bid-ask market

• Sell discipline focused on exit: sell when event happens; sell on price appreciation; sell if situation or event changes negatively

• Talk continuously to key players and contacts to keep ahead of the information flow

• Review all positions weekly

• Revisit scenarios constantly

• Advisory panel input during portfolio review process

• Structure hedges

IDEA GENERATION SCREENING ANALYSIS

STRUCTURINGMANAGING POSITIONS

3232

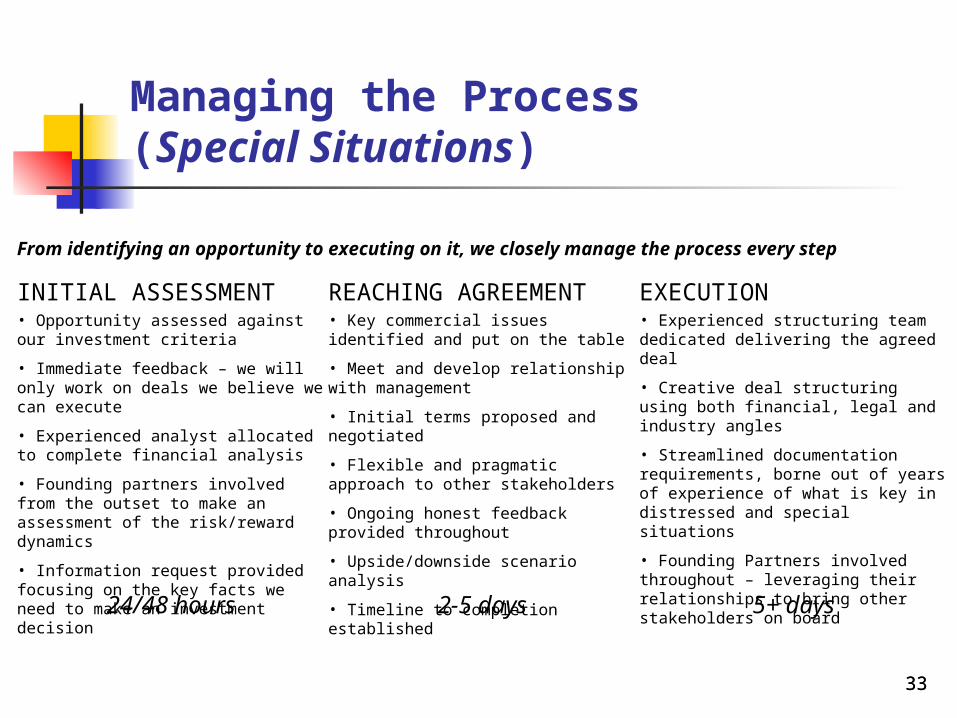

Managing the Process (Special Situations)

INITIAL ASSESSMENT• Opportunity assessed against our investment criteria

• Immediate feedback – we will only work on deals we believe we can execute

• Experienced analyst allocated to complete financial analysis

• Founding partners involved from the outset to make an assessment of the risk/reward dynamics

• Information request provided focusing on the key facts we need to make an investment decision

24/48 hours

REACHING AGREEMENT• Key commercial issues identified and put on the table

• Meet and develop relationship with management

• Initial terms proposed and negotiated

• Flexible and pragmatic approach to other stakeholders

• Ongoing honest feedback provided throughout

• Upside/downside scenario analysis

• Timeline to completion established2-5 days

EXECUTION• Experienced structuring team dedicated delivering the agreed deal

• Creative deal structuring using both financial, legal and industry angles

• Streamlined documentation requirements, borne out of years of experience of what is key in distressed and special situations

• Founding Partners involved throughout – leveraging their relationships to bring other stakeholders on board

5+ days

From identifying an opportunity to executing on it, we closely manage the process every step

3333

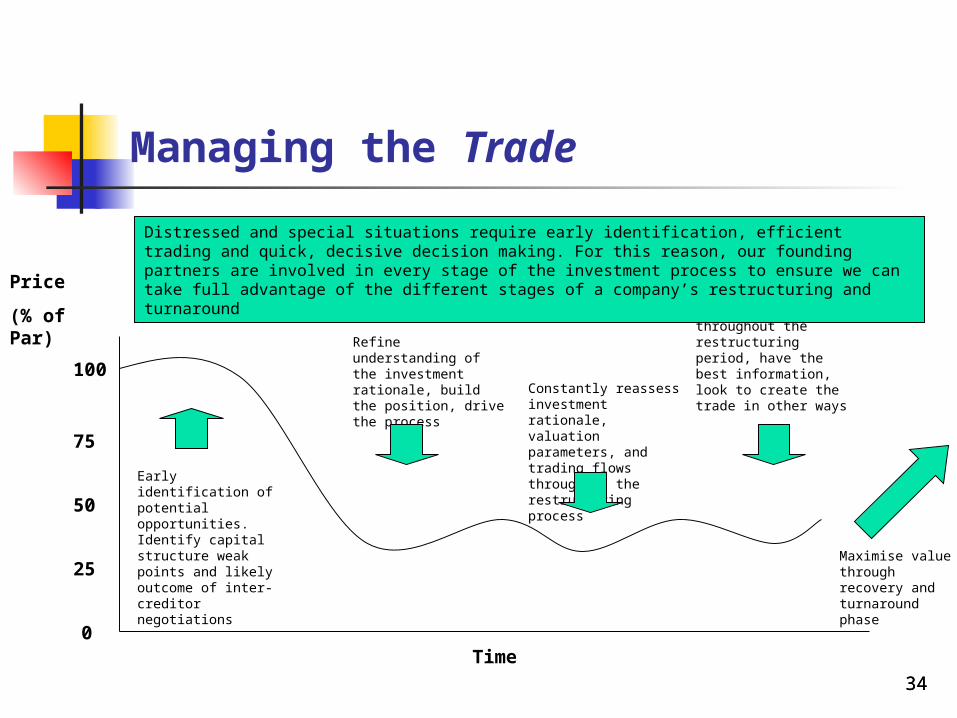

Managing the Trade

Price

(% of Par)

100

75

25

0

50

Time

Early identification of potential opportunities. Identify capital structure weak points and likely outcome of inter-creditor negotiations

Refine understanding of the investment rationale, build the position, drive the process

Constantly reassess investment rationale, valuation parameters, and trading flows throughout the restructuring process

Efficiently trade throughout the restructuring period, have the best information, look to create the trade in other ways

Maximise value through recovery and turnaround phase

Distressed and special situations require early identification, efficient trading and quick, decisive decision making. For this reason, our founding partners are involved in every stage of the investment process to ensure we can take full advantage of the different stages of a company’s restructuring and turnaround

3434

Risk return profile for an HY manager

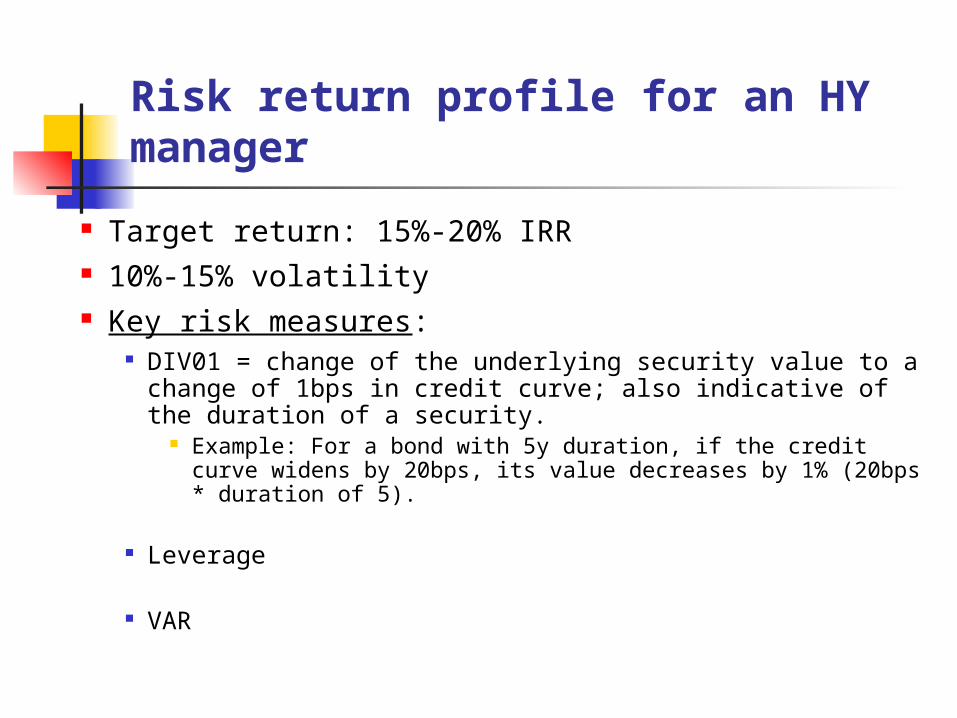

Target return: 15%-20% IRR 10%-15% volatility Key risk measures:

DIV01 = change of the underlying security value to a change of 1bps in credit curve; also indicative of the duration of a security.

Example: For a bond with 5y duration, if the credit curve widens by 20bps, its value decreases by 1% (20bps * duration of 5).

Leverage

VAR

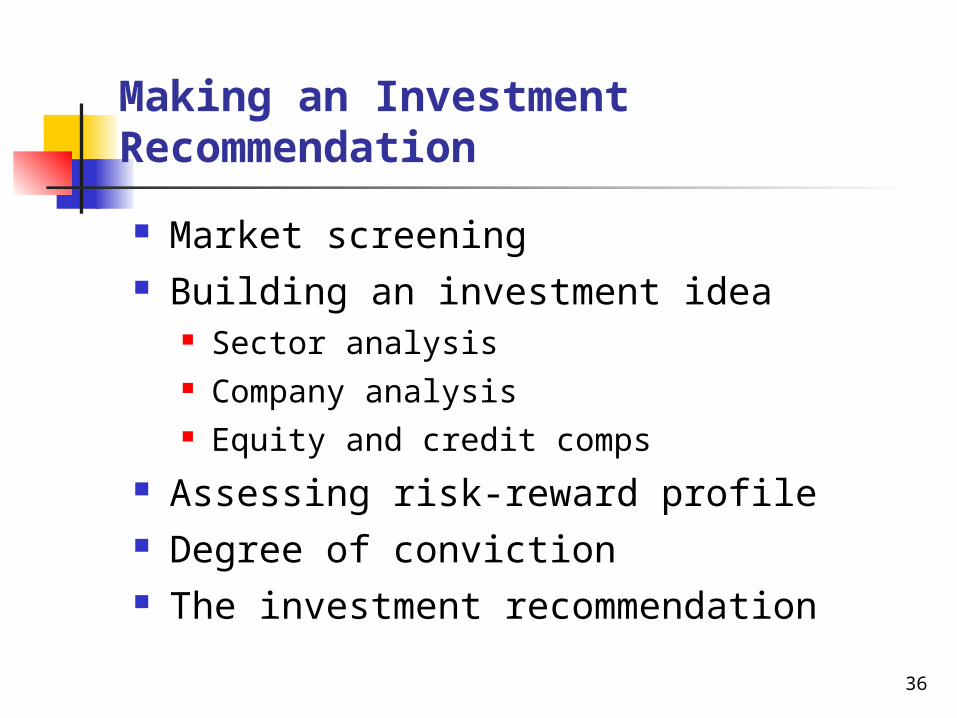

Making an Investment Recommendation

Market screening Building an investment idea

Sector analysis Company analysis Equity and credit comps

Assessing risk-reward profile Degree of conviction The investment recommendation

36

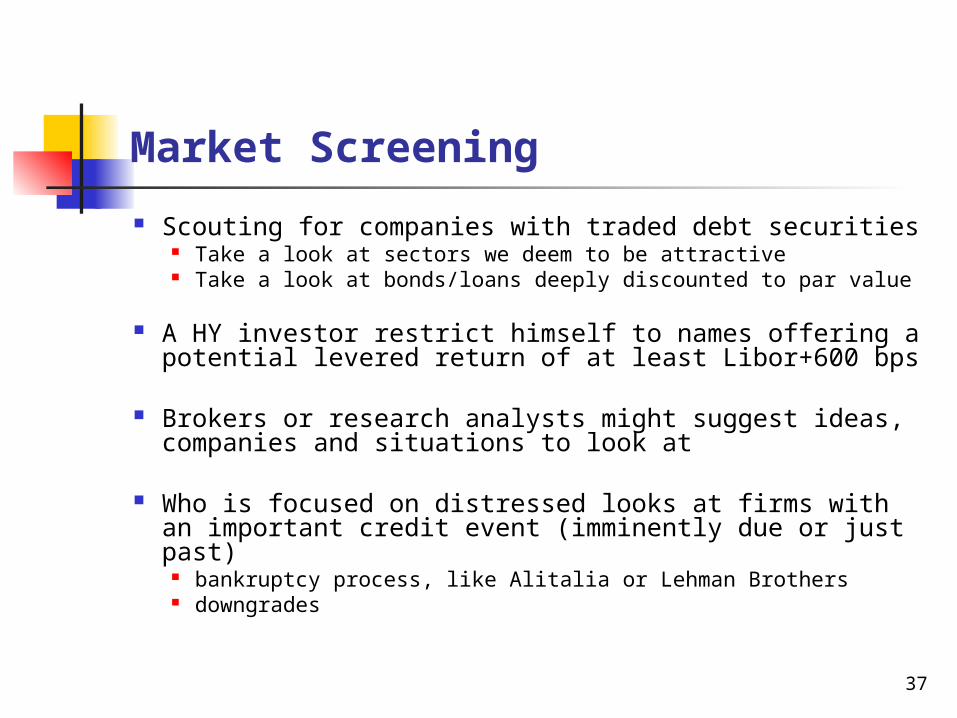

Market Screening

Scouting for companies with traded debt securities Take a look at sectors we deem to be attractive Take a look at bonds/loans deeply discounted to par value

A HY investor restrict himself to names offering a potential levered return of at least Libor+600 bps

Brokers or research analysts might suggest ideas, companies and situations to look at

Who is focused on distressed looks at firms with an important credit event (imminently due or just past)

bankruptcy process, like Alitalia or Lehman Brothers downgrades

37

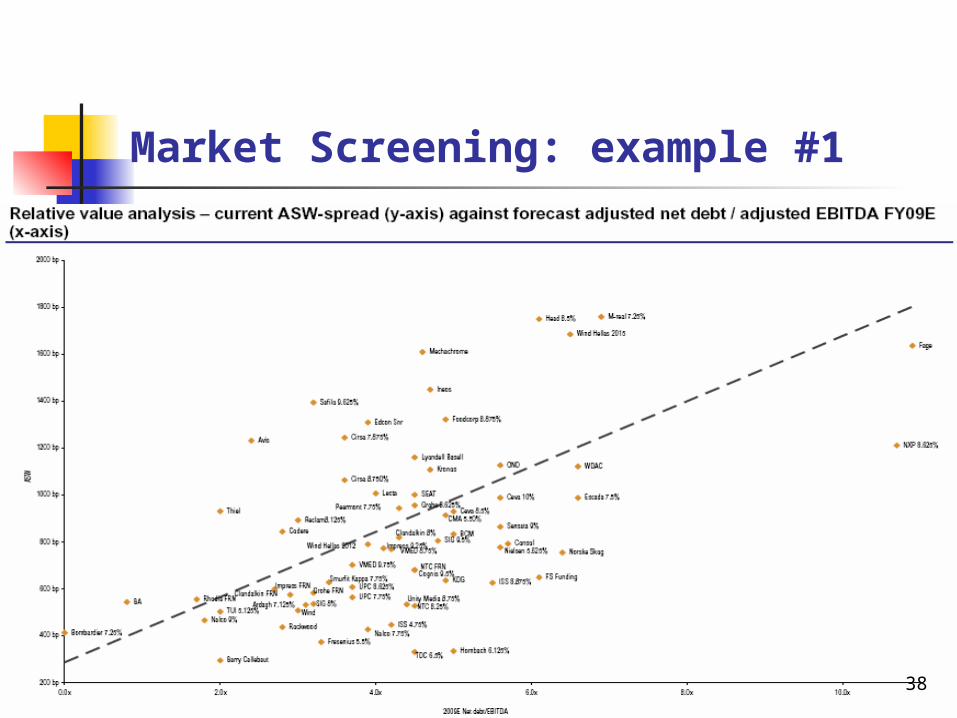

Market Screening: example #1

38

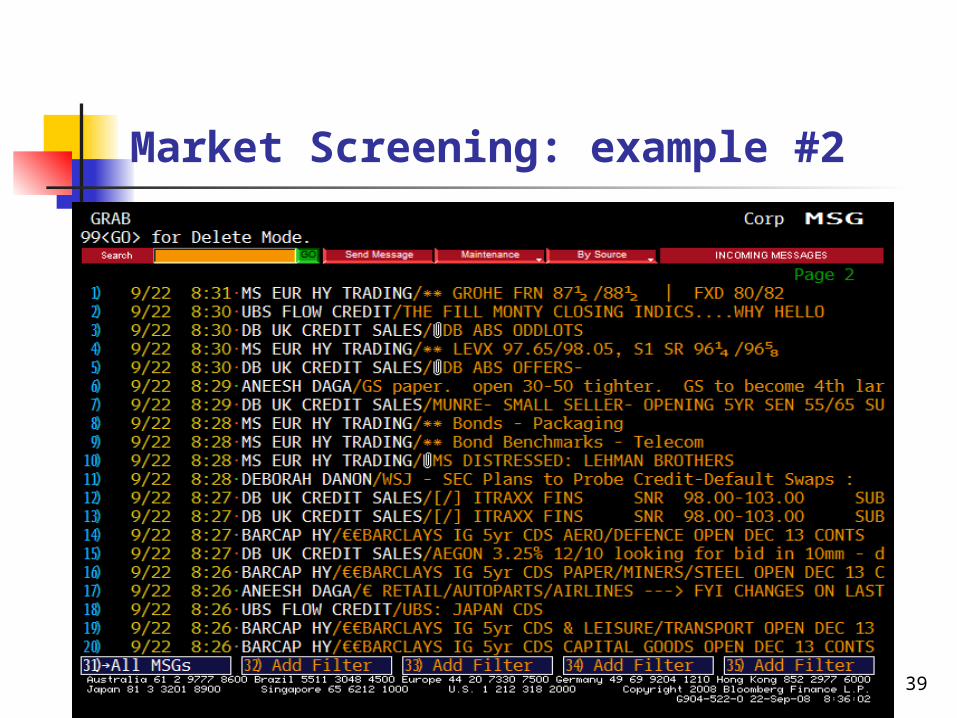

Market Screening: example #2

39

Building an Investment Idea

Choose the right sector

Choose a company with a very good management team in that sector

Pick cheap debt securities of that company in relative value terms

40

(1) Sector Analysis Most of our actual return on capital depends on the sector we invest

in

A deep understanding of all the challenges faced by the companies in the sector are facing is then of paramount importance

e.g. raw material price increases, price pressure, intense competition,…

To gain an educated view on the company sector condition and outlook

look at the competitors/peers in terms of their operating and financial stats (sales growth, EBITDA margin, leverage, cashflow conversion, etc)

when a listed competitor / peer reports its quarterly numbers, we might find a lot of information from its reports and subsequent brokers’ analysis

In the current context (recession) we favor sectors like utilities, telecom, healthcare, aerospace, niche

technologies (“defensive” sectors, uncorrelated with economic cycles) avoid retail, fashion and luxury, financials, automotive and related,

airlines, consumer goods (“cyclical” sector, highly correlated with the economic environment) 41

(2) Company Analysis

Review of Financial accounts (annual reports, quarterly financials statements) Sell side research (equity and credit analyst research)

Interviews to suppliers, customers, peers, etc.

Aim to gain a deep knowledge of: firm’s business model and business plan firm’s financial structure firm’s traded debt securities or loans

The end product is an excel-based output, including a granular operating and financial model of the company

42

(3) Equity and Credit Comps

Need to understand if the debt securities we are considering investing in are “cheap” or “expensive” - compared to the securities of other companies in the same sector or with similar leverage

Especially true if we are trying to deploy a relative value investment strategy to isolate the “ALFA”

One of the key features to make money over time is to invest in cheap securities

Often we find better investment opportunities (better risk/reward and better companies) in comps/peers we look at

By analyzing comps’ securities as well, we might find a better way to express our views by combining together various trades

43

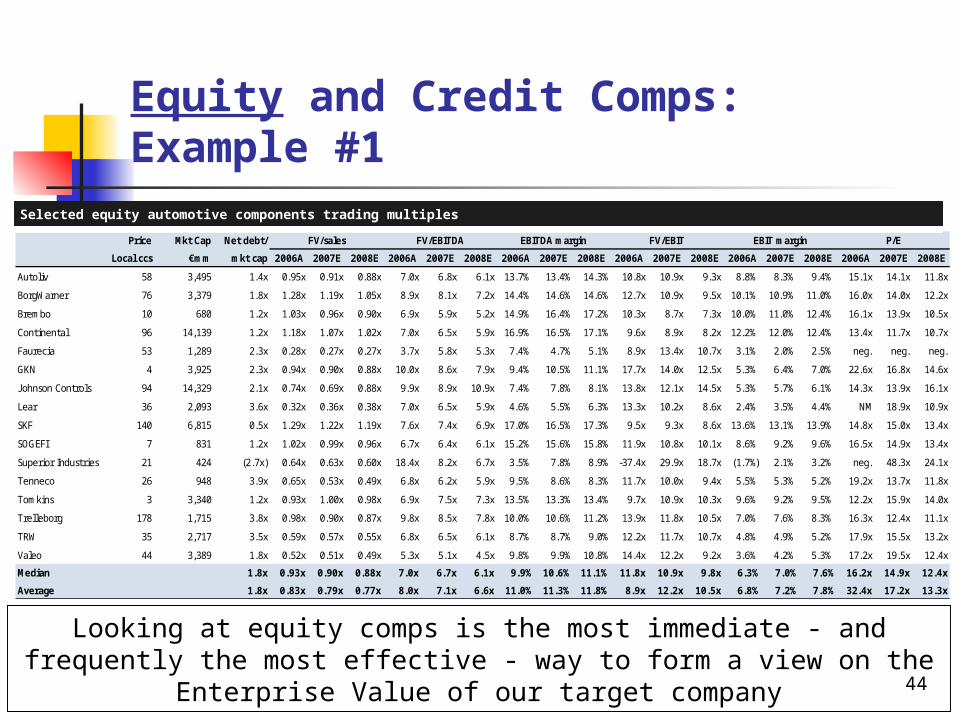

Equity and Credit Comps: Example #1

Price Mkt Cap Net debt/ FV/sales FV/EBITDA EBITDA margin FV/EBIT EBIT margin P/E

Local ccs €mm mkt cap 2006A 2007E 2008E 2006A 2007E 2008E 2006A 2007E 2008E 2006A 2007E 2008E 2006A 2007E 2008E 2006A 2007E 2008E

Autoliv 58 3,495 1.4x 0.95x 0.91x 0.88x 7.0x 6.8x 6.1x 13.7% 13.4% 14.3% 10.8x 10.9x 9.3x 8.8% 8.3% 9.4% 15.1x 14.1x 11.8x

BorgWarner 76 3,379 1.8x 1.28x 1.19x 1.05x 8.9x 8.1x 7.2x 14.4% 14.6% 14.6% 12.7x 10.9x 9.5x 10.1% 10.9% 11.0% 16.0x 14.0x 12.2x

Brembo 10 680 1.2x 1.03x 0.96x 0.90x 6.9x 5.9x 5.2x 14.9% 16.4% 17.2% 10.3x 8.7x 7.3x 10.0% 11.0% 12.4% 16.1x 13.9x 10.5x

Continental 96 14,139 1.2x 1.18x 1.07x 1.02x 7.0x 6.5x 5.9x 16.9% 16.5% 17.1% 9.6x 8.9x 8.2x 12.2% 12.0% 12.4% 13.4x 11.7x 10.7x

Faurecia 53 1,289 2.3x 0.28x 0.27x 0.27x 3.7x 5.8x 5.3x 7.4% 4.7% 5.1% 8.9x 13.4x 10.7x 3.1% 2.0% 2.5% neg. neg. neg.

GKN 4 3,925 2.3x 0.94x 0.90x 0.88x 10.0x 8.6x 7.9x 9.4% 10.5% 11.1% 17.7x 14.0x 12.5x 5.3% 6.4% 7.0% 22.6x 16.8x 14.6x

J ohnson Controls 94 14,329 2.1x 0.74x 0.69x 0.88x 9.9x 8.9x 10.9x 7.4% 7.8% 8.1% 13.8x 12.1x 14.5x 5.3% 5.7% 6.1% 14.3x 13.9x 16.1x

Lear 36 2,093 3.6x 0.32x 0.36x 0.38x 7.0x 6.5x 5.9x 4.6% 5.5% 6.3% 13.3x 10.2x 8.6x 2.4% 3.5% 4.4% NM 18.9x 10.9x

SKF 140 6,815 0.5x 1.29x 1.22x 1.19x 7.6x 7.4x 6.9x 17.0% 16.5% 17.3% 9.5x 9.3x 8.6x 13.6% 13.1% 13.9% 14.8x 15.0x 13.4x

SOGEFI 7 831 1.2x 1.02x 0.99x 0.96x 6.7x 6.4x 6.1x 15.2% 15.6% 15.8% 11.9x 10.8x 10.1x 8.6% 9.2% 9.6% 16.5x 14.9x 13.4x

Superior Industries 21 424 (2.7x) 0.64x 0.63x 0.60x 18.4x 8.2x 6.7x 3.5% 7.8% 8.9% -37.4x 29.9x 18.7x (1.7%) 2.1% 3.2% neg. 48.3x 24.1x

Tenneco 26 948 3.9x 0.65x 0.53x 0.49x 6.8x 6.2x 5.9x 9.5% 8.6% 8.3% 11.7x 10.0x 9.4x 5.5% 5.3% 5.2% 19.2x 13.7x 11.8x

Tomkins 3 3,340 1.2x 0.93x 1.00x 0.98x 6.9x 7.5x 7.3x 13.5% 13.3% 13.4% 9.7x 10.9x 10.3x 9.6% 9.2% 9.5% 12.2x 15.9x 14.0x

Trelleborg 178 1,715 3.8x 0.98x 0.90x 0.87x 9.8x 8.5x 7.8x 10.0% 10.6% 11.2% 13.9x 11.8x 10.5x 7.0% 7.6% 8.3% 16.3x 12.4x 11.1x

TRW 35 2,717 3.5x 0.59x 0.57x 0.55x 6.8x 6.5x 6.1x 8.7% 8.7% 9.0% 12.2x 11.7x 10.7x 4.8% 4.9% 5.2% 17.9x 15.5x 13.2x

Valeo 44 3,389 1.8x 0.52x 0.51x 0.49x 5.3x 5.1x 4.5x 9.8% 9.9% 10.8% 14.4x 12.2x 9.2x 3.6% 4.2% 5.3% 17.2x 19.5x 12.4x

Median 1.8x 0.93x 0.90x 0.88x 7.0x 6.7x 6.1x 9.9% 10.6% 11.1% 11.8x 10.9x 9.8x 6.3% 7.0% 7.6% 16.2x 14.9x 12.4x

Average 1.8x 0.83x 0.79x 0.77x 8.0x 7.1x 6.6x 11.0% 11.3% 11.8% 8.9x 12.2x 10.5x 6.8% 7.2% 7.8% 32.4x 17.2x 13.3x

Selected equity automotive components trading multiplesSelected equity automotive components trading multiples

44

Looking at equity comps is the most immediate - and frequently the most effective - way to form a view on the Enterprise Value of our

target company

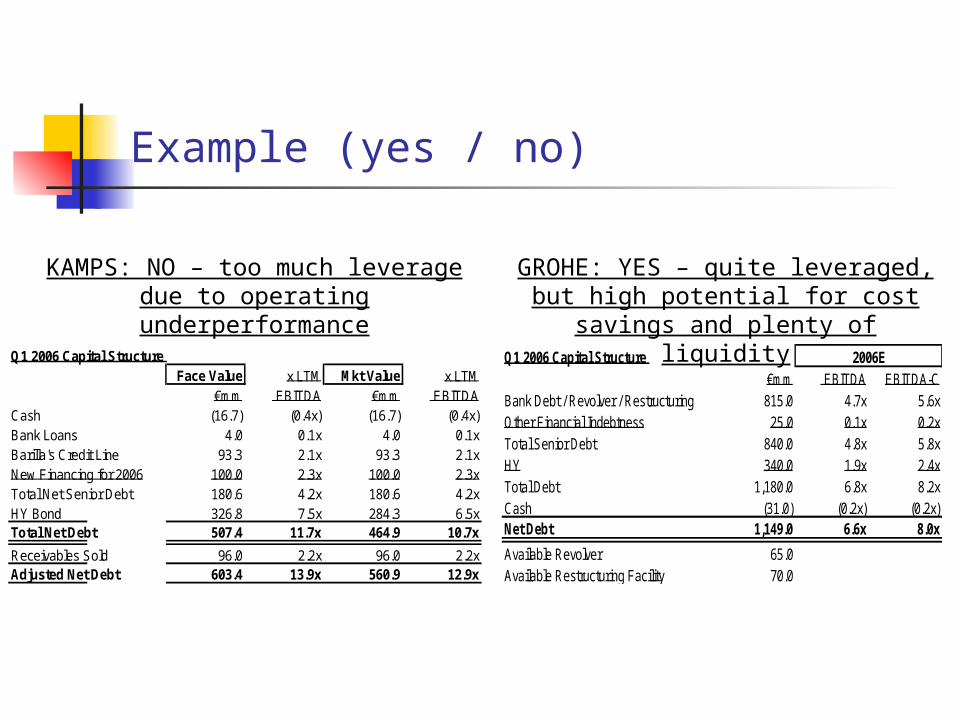

Example (yes / no)

Q1 2006 Capital Structure Face Value x LTM Mkt Value x LTM

€mm EBITDA €mm EBITDACash (16.7) (0.4x) (16.7) (0.4x)Bank Loans 4.0 0.1x 4.0 0.1xBarilla's Credit Line 93.3 2.1x 93.3 2.1xNew Financing for 2006 100.0 2.3x 100.0 2.3xTotal Net Senior Debt 180.6 4.2x 180.6 4.2xHY Bond 326.8 7.5x 284.3 6.5xTotal Net Debt 507.4 11.7x 464.9 10.7x

Receivables Sold 96.0 2.2x 96.0 2.2xAdjusted Net Debt 603.4 13.9x 560.9 12.9x

KAMPS: NO – too much leverage due to operating

underperformance

GROHE: YES – quite leveraged, but high potential for cost savings and

plenty of liquidityQ1 2006 Capital Structure 2006E

€mm EBITDA EBITDA-CBank Debt / Revolver / Restructuring 815.0 4.7x 5.6xOther Financial Indebtness 25.0 0.1x 0.2xTotal Senior Debt 840.0 4.8x 5.8xHY 340.0 1.9x 2.4xTotal Debt 1,180.0 6.8x 8.2xCash (31.0) (0.2x) (0.2x)Net Debt 1,149.0 6.6x 8.0x

Available Revolver 65.0Available Restructuring Facility 70.0

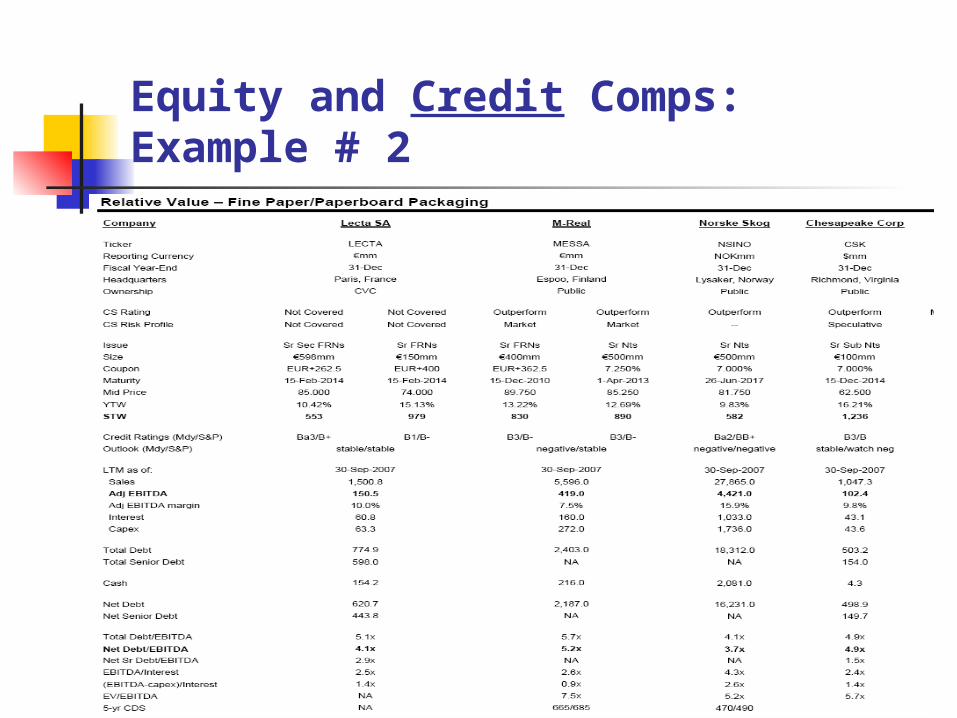

Equity and Credit Comps: Example # 2

46

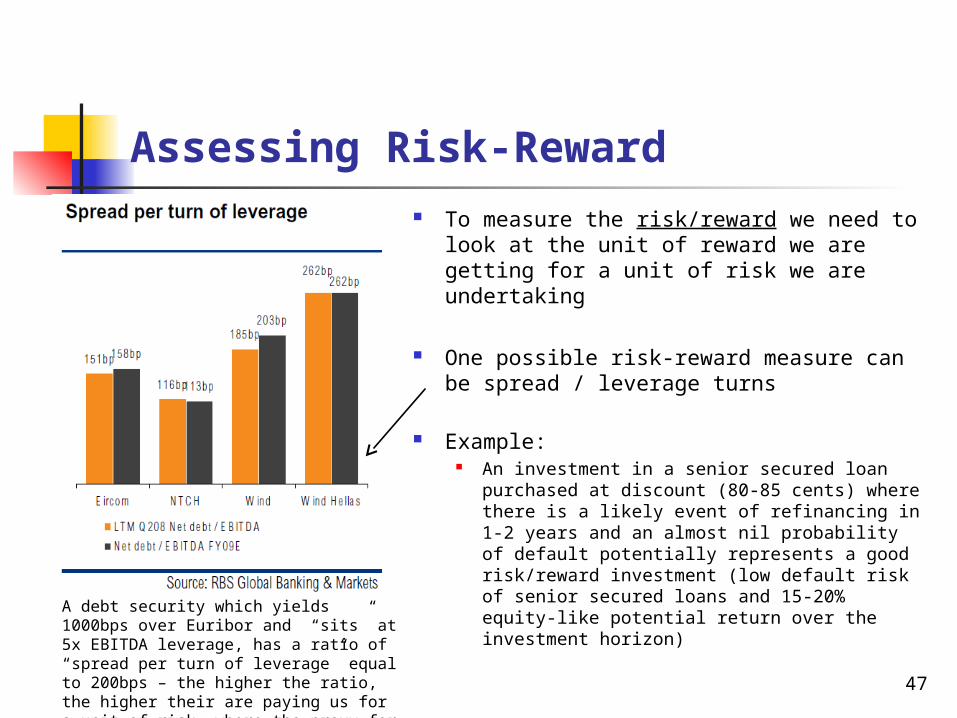

Assessing Risk-Reward To measure the risk/reward we need to

look at the unit of reward we are getting for a unit of risk we are undertaking

One possible risk-reward measure can be spread / leverage turns

Example: An investment in a senior secured loan

purchased at discount (80-85 cents) where there is a likely event of refinancing in 1-2 years and an almost nil probability of default potentially represents a good risk/reward investment (low default risk of senior secured loans and 15-20% equity-like potential return over the investment horizon)

47

A debt security which yields 1000bps over Euribor and “sits” at 5x EBITDA leverage, has a ratio of “spread per turn of leverage” equal to 200bps – the higher the ratio, the higher their are paying us for a unit of risk, where the proxy for the unit of risk is the EBITDA leverage

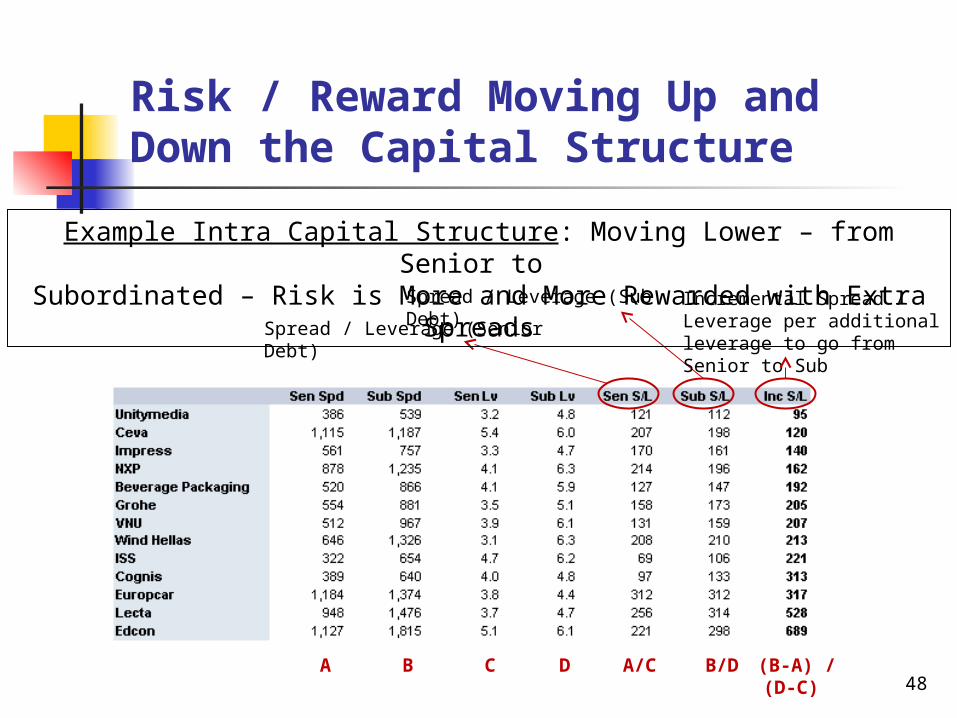

Risk / Reward Moving Up and Down the Capital Structure

Spread / Leverage (Senior Debt)

Spread / Leverage (Sub Debt)Incremental Spread / Leverage per additional leverage to go from Senior to Sub

A B C D A/C B/D (B-A) / (D-C) 48

Example Intra Capital Structure: Moving Lower – from Senior to Subordinated – Risk is More and More Rewarded with Extra Spreads

Degree of Conviction

The degree of conviction represents how comfortable we are in the numbers and in the judgment calls at the basis of our analysis

Having a high degree of conviction in high yield and distress investing is of paramount importance since the loss can be huge Exit may be difficult

49

Degree of Conviction: Examples

50

Situations where we might have a high degree of conviction:

We have been studying the company for a long time and we have had the chance to verify that our financial model works well in terms of forecasting

We have a good relationship with the CEO or CFO of the target company and we feel we have a better understanding of their body language

We know the sector well because we have been investing in it for a long time

We have already invested in the company

Situations where we might NOT have a high degree of conviction:

It is the first time we are looking at the sector of our target company We have little historical financial information on the target company Earnings have historically proven to be very volatile The sector is going through a transformational period

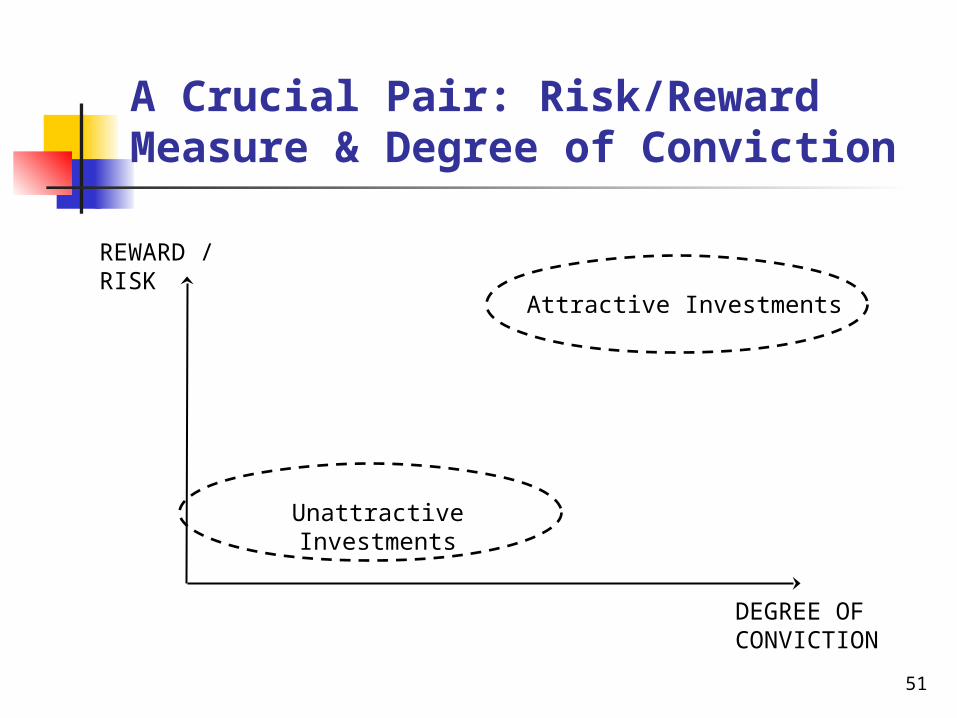

A Crucial Pair: Risk/Reward Measure & Degree of Conviction

REWARD / RISK

Attractive Investments

Unattractive Investments

DEGREE OF CONVICTION

51

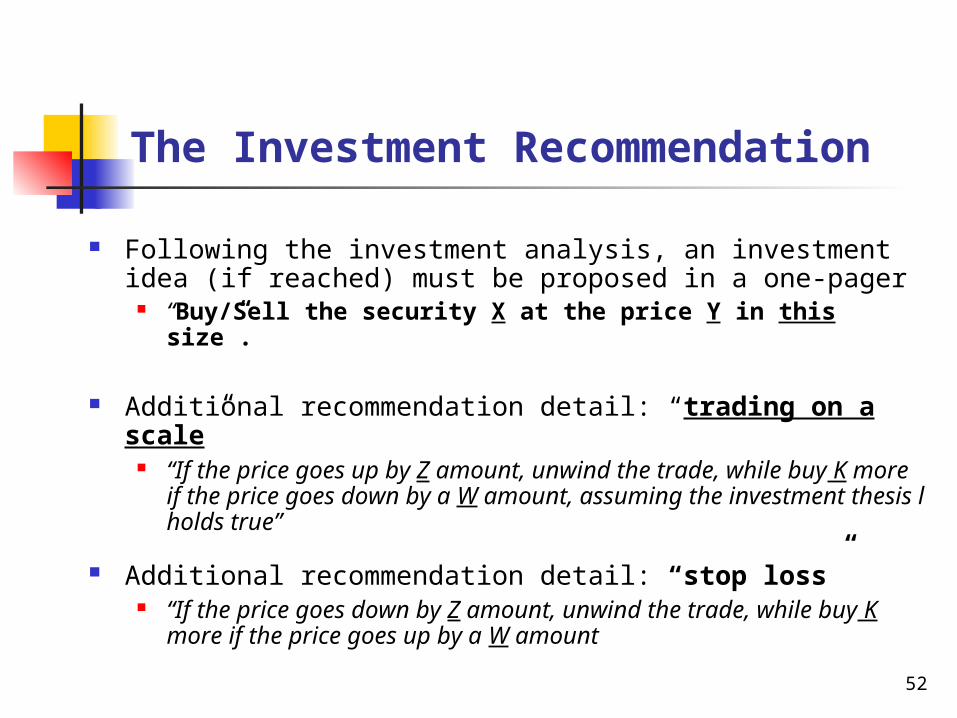

The Investment Recommendation

Following the investment analysis, an investment idea (if reached) must be proposed in a one-pager

“Buy/Sell the security X at the price Y in this size”.

Additional recommendation detail: “trading on a scale” “If the price goes up by Z amount, unwind the trade, while buy

K more if the price goes down by a W amount, assuming the investment thesis l holds true”

Additional recommendation detail: “stop loss” “If the price goes down by Z amount, unwind the trade, while

buy K more if the price goes up by a W amount

52

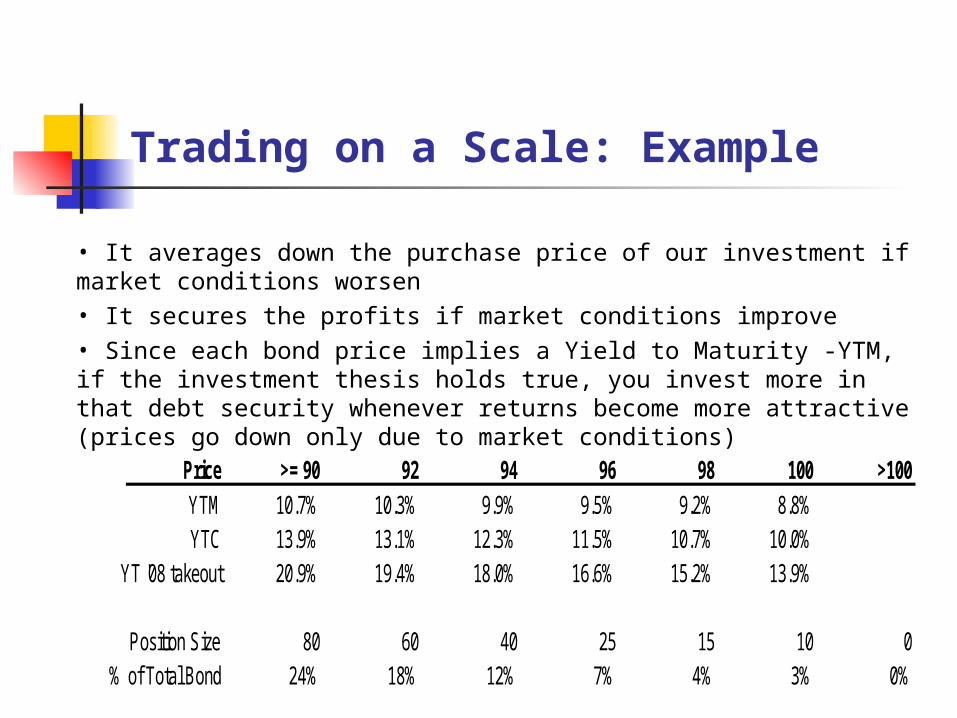

Trading on a Scale: Example

Price >= 90 92 94 96 98 100 >100YTM 10.7% 10.3% 9.9% 9.5% 9.2% 8.8%YTC 13.9% 13.1% 12.3% 11.5% 10.7% 10.0%

YT '08 takeout 20.9% 19.4% 18.0% 16.6% 15.2% 13.9%

Position Size 80 60 40 25 15 10 0% of Total Bond 24% 18% 12% 7% 4% 3% 0%

• It averages down the purchase price of our investment if market conditions worsen• It secures the profits if market conditions improve• Since each bond price implies a Yield to Maturity -YTM, if the investment thesis holds true, you invest more in that debt security whenever returns become more attractive (prices go down only due to market conditions)

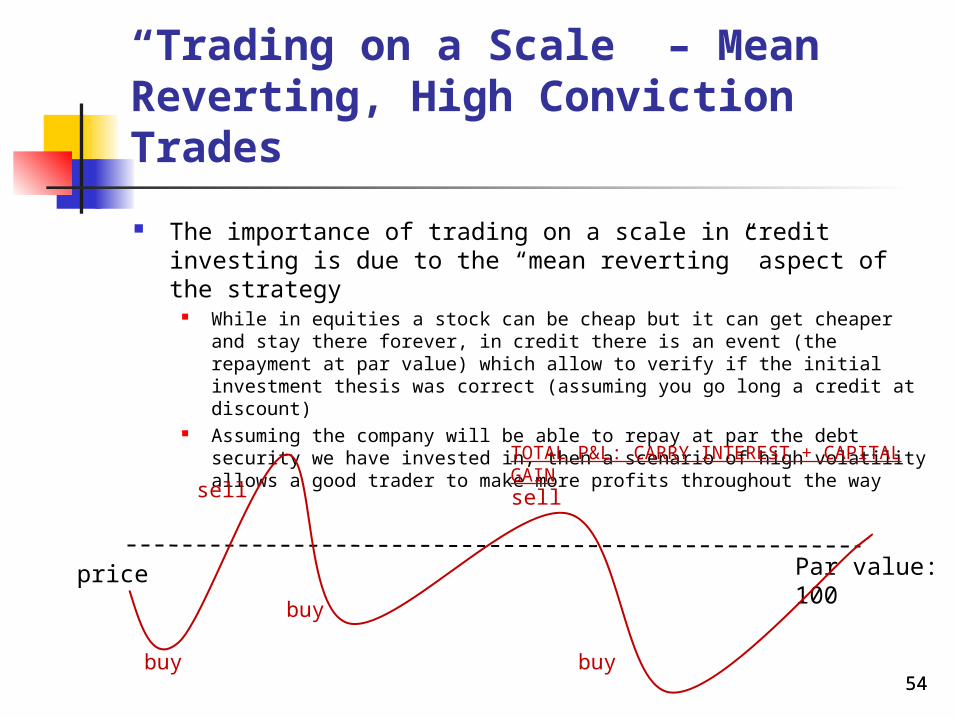

“Trading on a Scale” – Mean Reverting, High Conviction Trades

The importance of trading on a scale in credit investing is due to the “mean reverting” aspect of the strategy

While in equities a stock can be cheap but it can get cheaper and stay there forever, in credit there is an event (the repayment at par value) which allow to verify if the initial investment thesis was correct (assuming you go long a credit at discount)

Assuming the company will be able to repay at par the debt security we have invested in, then a scenario of high volatility allows a good trader to make more profits throughout the way

Par value: 100price

buy

sell

buy

sell

buy

TOTAL P&L: CARRY INTEREST + CAPITAL GAIN

5454

Strategies and Trading Technicals

The Devil is in the Detail

5555

Detailed Company Fundamentals Having a bottom-up granular operating and financial model allows to

forecast quarterly developments of the financials of the company,

You can potentially understand if covenants will be triggered or other events will unfold and act immediately on this expectations

should prices of raw materials price increase, you may immediately run your model to assess changes in the profitability (i.e. EBITDA) of the company without the need to wait for the next quarterly financial release to understand what the numbers are

we can act sooner on our investment (exiting or adding more) before the vast majority of investors who lack a precise and detailed operating and financial model

Credit investors have a much more sophisticated bottom-up approach than equity investors since forecasting cashflows in detail is their core business

in equity investing you will very rarely find people who have detailed operating and financial models on companies under analysis

56

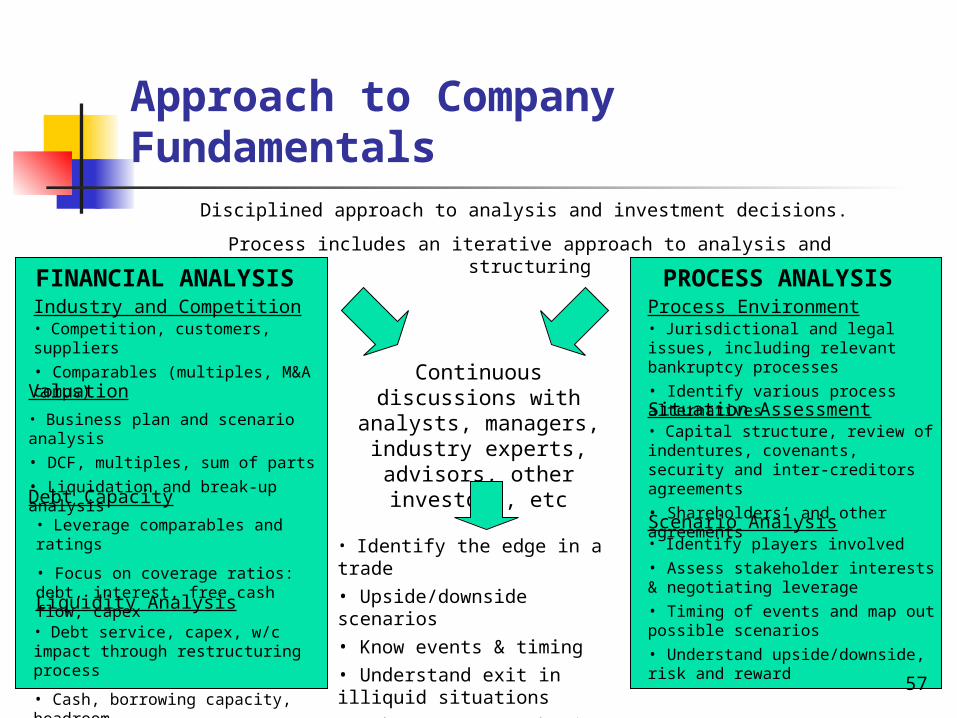

Approach to Company Fundamentals

FINANCIAL ANALYSISIndustry and Competition

• Competition, customers, suppliers

• Comparables (multiples, M&A comps)Valuation• Business plan and scenario analysis

• DCF, multiples, sum of parts

• Liquidation and break-up analysis

Debt Capacity• Leverage comparables and ratings

• Focus on coverage ratios: debt, interest, free cash flow, capex

Liquidity Analysis

• Debt service, capex, w/c impact through restructuring process

• Cash, borrowing capacity, headroom

PROCESS ANALYSISProcess Environment• Jurisdictional and legal issues, including relevant bankruptcy processes

• Identify various process alternativesSituation Assessment• Capital structure, review of indentures, covenants, security and inter-creditors agreements

• Shareholders’ and other agreementsScenario Analysis• Identify players involved

• Assess stakeholder interests & negotiating leverage

• Timing of events and map out possible scenarios

• Understand upside/downside, risk and reward

Disciplined approach to analysis and investment decisions.

Process includes an iterative approach to analysis and structuring

Continuous discussions with analysts,

managers, industry experts, advisors, other

investors, etc

• Identify the edge in a trade

• Upside/downside scenarios

• Know events & timing

• Understand exit in illiquid situations

• Take process or business risk

(not both)

57

58

Company Fundamentals: Example I/IV

[SEE ATTACHMENT]

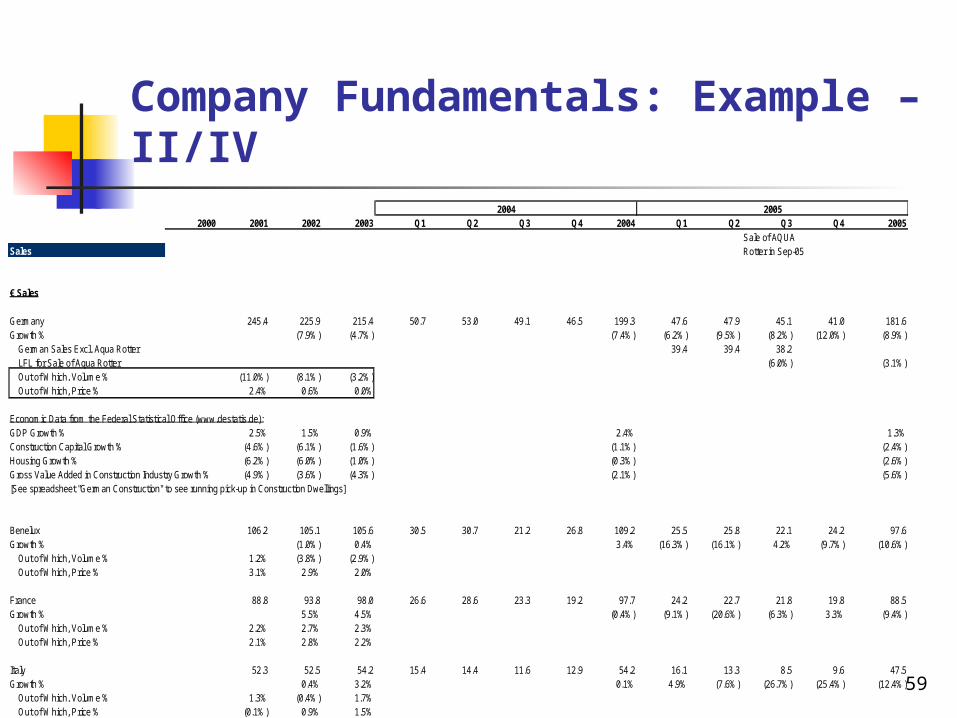

Company Fundamentals: Example – II/IV

59

2004 20052000 2001 2002 2003 Q1 Q2 Q3 Q4 2004 Q1 Q2 Q3 Q4 2005

Sale of AQUASales Rotter in Sep-05

€ Sales

Germany 245.4 225.9 215.4 50.7 53.0 49.1 46.5 199.3 47.6 47.9 45.1 41.0 181.6Growth % (7.9%) (4.7%) (7.4%) (6.2%) (9.5%) (8.2%) (12.0%) (8.9%)

German Sales Excl. Aqua Rotter 39.4 39.4 38.2LFL for Sale of Aqua Rotter (6.0%) (3.1%)Out of Which, Volume % (11.0%) (8.1%) (3.2%)Out of Which, Price % 2.4% 0.6% 0.0%

Economic Data from the Federal Statistical Office (www.destatis.de):GDP Growth % 2.5% 1.5% 0.9% 2.4% 1.3%Construction Capital Growth % (4.6%) (6.1%) (1.6%) (1.1%) (2.4%)Housing Growth % (6.2%) (6.0%) (1.0%) (0.3%) (2.6%)Gross Value Added in Construction Industry Growth % (4.9%) (3.6%) (4.3%) (2.1%) (5.6%)[See spreadsheet "German Construction" to see running pick-up in Construction Dwellings]

Benelux 106.2 105.1 105.6 30.5 30.7 21.2 26.8 109.2 25.5 25.8 22.1 24.2 97.6Growth % (1.0%) 0.4% 3.4% (16.3%) (16.1%) 4.2% (9.7%) (10.6%)

Out of Which, Volume % 1.2% (3.8%) (2.9%)Out of Which, Price % 3.1% 2.9% 2.0%

France 88.8 93.8 98.0 26.6 28.6 23.3 19.2 97.7 24.2 22.7 21.8 19.8 88.5Growth % 5.5% 4.5% (0.4%) (9.1%) (20.6%) (6.3%) 3.3% (9.4%)

Out of Which, Volume % 2.2% 2.7% 2.3%Out of Which, Price % 2.1% 2.8% 2.2%

Italy 52.3 52.5 54.2 15.4 14.4 11.6 12.9 54.2 16.1 13.3 8.5 9.6 47.5Growth % 0.4% 3.2% 0.1% 4.9% (7.6%) (26.7%) (25.4%) (12.4%)

Out of Which, Volume % 1.3% (0.4%) 1.7%Out of Which, Price % (0.1%) 0.9% 1.5%

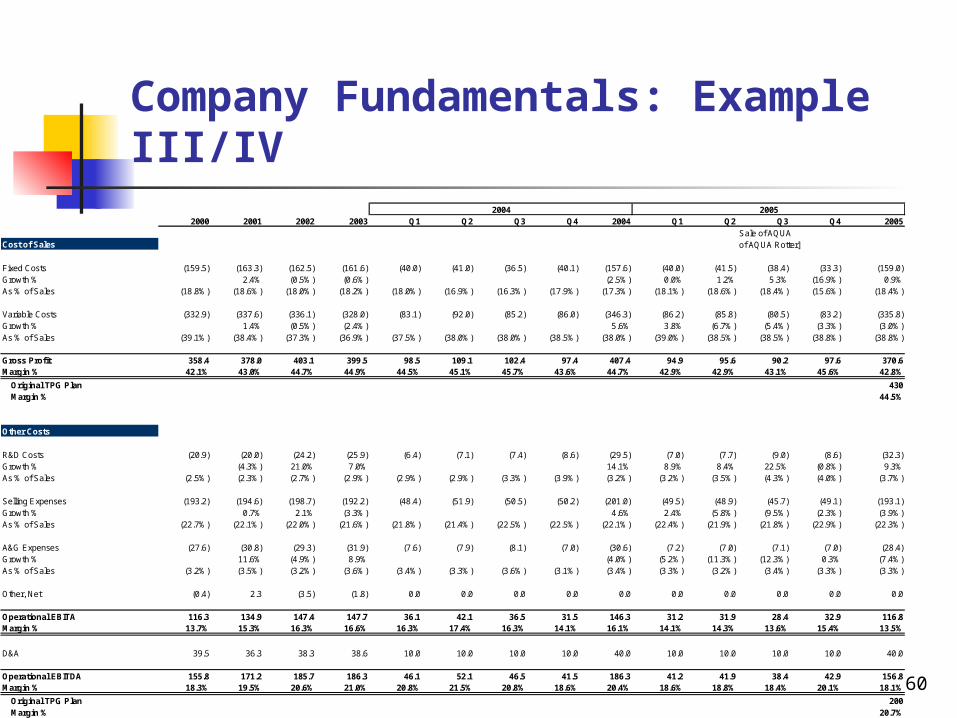

Company Fundamentals: Example III/IV

60

2004 20052000 2001 2002 2003 Q1 Q2 Q3 Q4 2004 Q1 Q2 Q3 Q4 2005

Sale of AQUACost of Sales of AQUA Rotter]

Fixed Costs (159.5) (163.3) (162.5) (161.6) (40.0) (41.0) (36.5) (40.1) (157.6) (40.0) (41.5) (38.4) (33.3) (159.0)Growth % 2.4% (0.5%) (0.6%) (2.5%) 0.0% 1.2% 5.3% (16.9%) 0.9%As % of Sales (18.8%) (18.6%) (18.0%) (18.2%) (18.0%) (16.9%) (16.3%) (17.9%) (17.3%) (18.1%) (18.6%) (18.4%) (15.6%) (18.4%)

Variable Costs (332.9) (337.6) (336.1) (328.0) (83.1) (92.0) (85.2) (86.0) (346.3) (86.2) (85.8) (80.5) (83.2) (335.8)Growth % 1.4% (0.5%) (2.4%) 5.6% 3.8% (6.7%) (5.4%) (3.3%) (3.0%)As % of Sales (39.1%) (38.4%) (37.3%) (36.9%) (37.5%) (38.0%) (38.0%) (38.5%) (38.0%) (39.0%) (38.5%) (38.5%) (38.8%) (38.8%)

Gross Profit 358.4 378.0 403.1 399.5 98.5 109.1 102.4 97.4 407.4 94.9 95.6 90.2 97.6 370.6Margin % 42.1% 43.0% 44.7% 44.9% 44.5% 45.1% 45.7% 43.6% 44.7% 42.9% 42.9% 43.1% 45.6% 42.8%

Original TPG Plan 430Margin % 44.5%

Other Costs

R&D Costs (20.9) (20.0) (24.2) (25.9) (6.4) (7.1) (7.4) (8.6) (29.5) (7.0) (7.7) (9.0) (8.6) (32.3)Growth % (4.3%) 21.0% 7.0% 14.1% 8.9% 8.4% 22.5% (0.8%) 9.3%As % of Sales (2.5%) (2.3%) (2.7%) (2.9%) (2.9%) (2.9%) (3.3%) (3.9%) (3.2%) (3.2%) (3.5%) (4.3%) (4.0%) (3.7%)

Selling Expenses (193.2) (194.6) (198.7) (192.2) (48.4) (51.9) (50.5) (50.2) (201.0) (49.5) (48.9) (45.7) (49.1) (193.1)Growth % 0.7% 2.1% (3.3%) 4.6% 2.4% (5.8%) (9.5%) (2.3%) (3.9%)As % of Sales (22.7%) (22.1%) (22.0%) (21.6%) (21.8%) (21.4%) (22.5%) (22.5%) (22.1%) (22.4%) (21.9%) (21.8%) (22.9%) (22.3%)

A&G Expenses (27.6) (30.8) (29.3) (31.9) (7.6) (7.9) (8.1) (7.0) (30.6) (7.2) (7.0) (7.1) (7.0) (28.4)Growth % 11.6% (4.9%) 8.9% (4.0%) (5.2%) (11.3%) (12.3%) 0.3% (7.4%)As % of Sales (3.2%) (3.5%) (3.2%) (3.6%) (3.4%) (3.3%) (3.6%) (3.1%) (3.4%) (3.3%) (3.2%) (3.4%) (3.3%) (3.3%)

Other, Net (0.4) 2.3 (3.5) (1.8) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Operational EBITA 116.3 134.9 147.4 147.7 36.1 42.1 36.5 31.5 146.3 31.2 31.9 28.4 32.9 116.8Margin % 13.7% 15.3% 16.3% 16.6% 16.3% 17.4% 16.3% 14.1% 16.1% 14.1% 14.3% 13.6% 15.4% 13.5%

D&A 39.5 36.3 38.3 38.6 10.0 10.0 10.0 10.0 40.0 10.0 10.0 10.0 10.0 40.0

Operational EBITDA 155.8 171.2 185.7 186.3 46.1 52.1 46.5 41.5 186.3 41.2 41.9 38.4 42.9 156.8Margin % 18.3% 19.5% 20.6% 21.0% 20.8% 21.5% 20.8% 18.6% 20.4% 18.6% 18.8% 18.4% 20.1% 18.1%

Original TPG Plan 200Margin % 20.7%

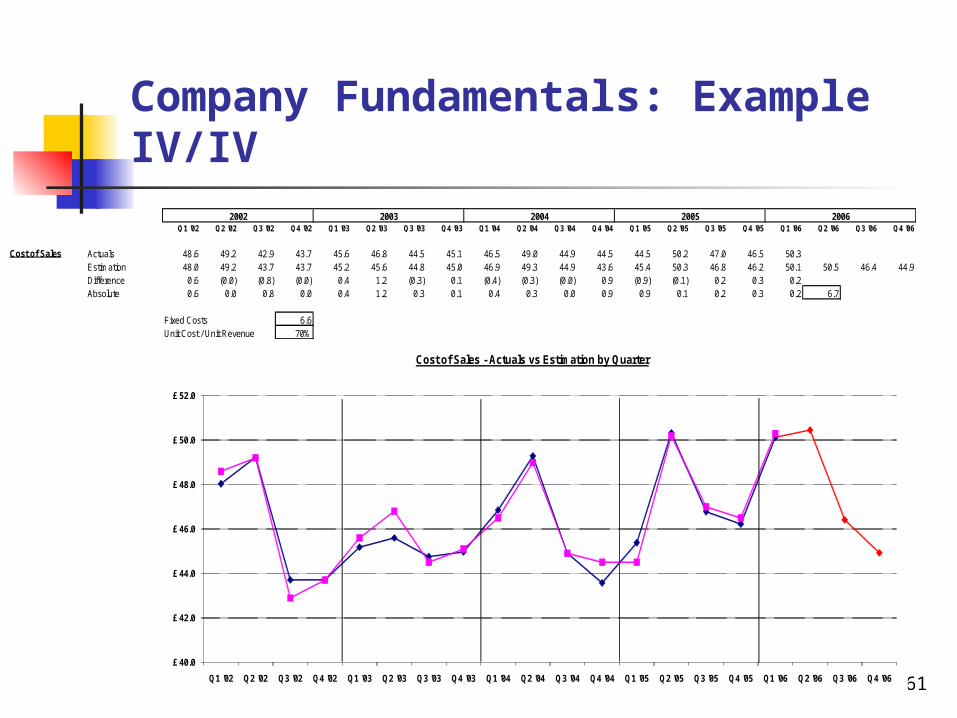

Company Fundamentals: Example IV/IV

61

2002 2003 2004 2005 2006Q1 '02 Q2 '02 Q3 '02 Q4 '02 Q1 '03 Q2 '03 Q3 '03 Q4 '03 Q1 '04 Q2 '04 Q3 '04 Q4 '04 Q1 '05 Q2 '05 Q3 '05 Q4 '05 Q1 '06 Q2 '06 Q3 '06 Q4 '06

Cost of Sales Actuals 48.6 49.2 42.9 43.7 45.6 46.8 44.5 45.1 46.5 49.0 44.9 44.5 44.5 50.2 47.0 46.5 50.3Estimation 48.0 49.2 43.7 43.7 45.2 45.6 44.8 45.0 46.9 49.3 44.9 43.6 45.4 50.3 46.8 46.2 50.1 50.5 46.4 44.9Difference 0.6 (0.0) (0.8) (0.0) 0.4 1.2 (0.3) 0.1 (0.4) (0.3) (0.0) 0.9 (0.9) (0.1) 0.2 0.3 0.2Absolute 0.6 0.0 0.8 0.0 0.4 1.2 0.3 0.1 0.4 0.3 0.0 0.9 0.9 0.1 0.2 0.3 0.2 6.7

Fixed Costs 6.6Unit Cost / Unit Revenue 70%

£ 40.0

£ 42.0

£ 44.0

£ 46.0

£ 48.0

£ 50.0

£ 52.0

Q1 '02 Q2 '02 Q3 '02 Q4 '02 Q1 '03 Q2 '03 Q3 '03 Q4 '03 Q1 '04 Q2 '04 Q3 '04 Q4 '04 Q1 '05 Q2 '05 Q3 '05 Q4 '05 Q1 '06 Q2 '06 Q3 '06 Q4 '06

Cost of Sales - Actuals vs Estimation by Quarter

£ 6.0

£ 6.5

£ 7.0

£ 7.5

£ 8.0

£ 8.5

£ 9.0

Other Net Operating Expenses - Actuals vs Estimation by Quarter

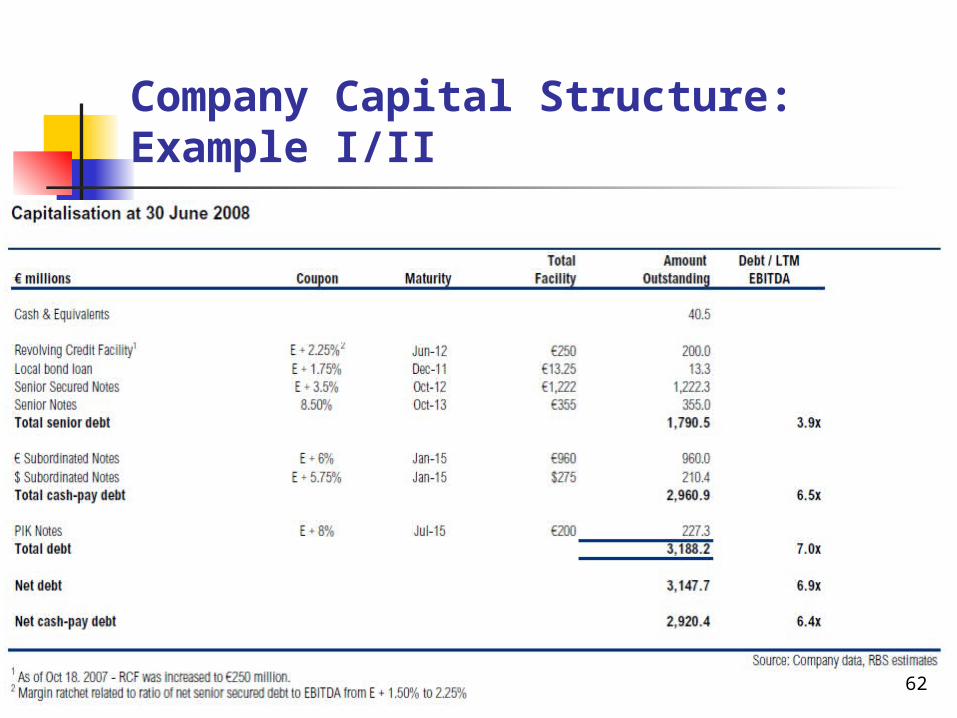

Company Capital Structure: Example I/II

62

Company Capital Structure: Example II/II

63

Combining capital structure analysis with the equity and credit comps’ analysis, we are effectively able to “price” the distress securities

Previous example of Wind Hellas, the Greek telecom operator: from equity comps’ analysis we have that similar type of assets trade between 6x and

7x a 6.5x value would then “break through” Wind Hellas’ capital structure, allowing to

recover par value on the subordinated notes (which sit at 6.5x leverage) and nil on the PIK notes (which sit at 7x leverage)

Among Wind Hellas’ securities, subordinated notes currently trade in the 70s while the PIK notes trade in the 50s implying a return of approx 15-20% on the subordinated notes and of approx 35-40% on the PIK notes

The market is not pricing the subordinated notes at par while the PIK notes at zero The company in two to three years might or might not improve its profitability, hence

the PIK notes might get or do not get value The price of the subordinated notes and the PIK notes tell us that the market on one

hand is pricing the possibility that the company might lower its EBITDA/Valuation (that’s why the subordinated notes are trading at discount) and on the other hand is pricing the possibility that the company might improve its EBITDA/Valuation (that’s why the PIK notes have some value)

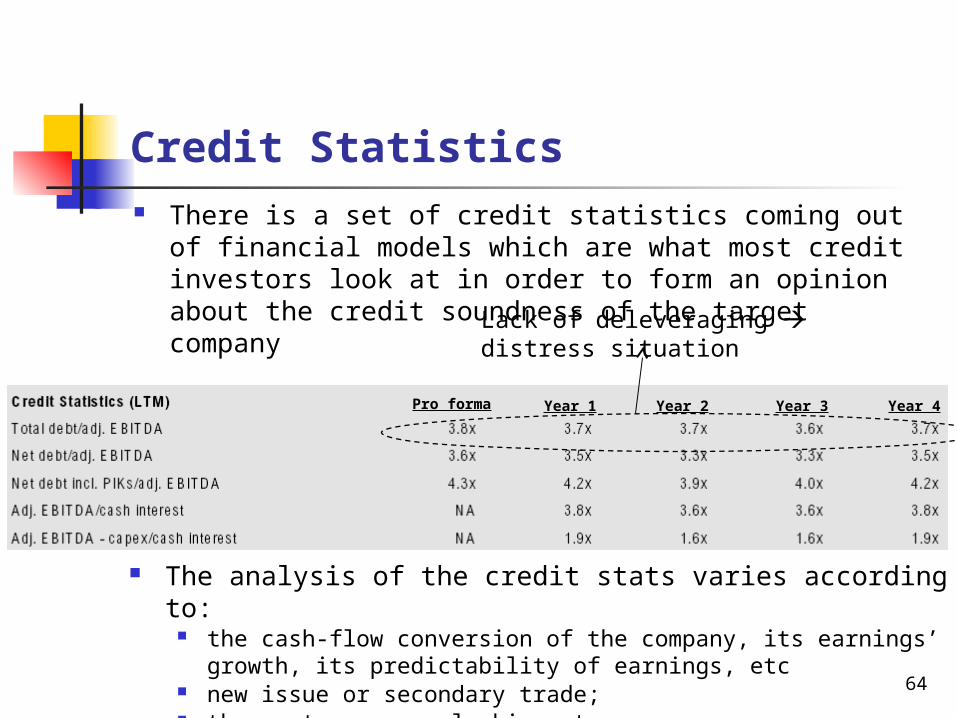

Credit Statistics There is a set of credit statistics coming out of financial

models which are what most credit investors look at in order to form an opinion about the credit soundness of the target company

Pro forma Year 1 Year 2 Year 3 Year 4

Lack of deleveraging distress situation

64

The analysis of the credit stats varies according to: the cash-flow conversion of the company, its earnings’ growth,

its predictability of earnings, etc new issue or secondary trade; the sector we are looking at

Legal and Structure Analysis Investing in credit offers a variety of legal rights as outlined

in legal norms and either loan provisions or bond indenture Basic one: priority be reimbursed vs equity in case of liquidation That’s why credit return is capped

Being able to identify our own rights as creditor is an important step of the investment decision process

the priority in the capital structure, covenants’ protection, majority clauses to change the contract if loan or the bond

indenture if bond, etc The legal and structure analysis becomes more and more

important the more distress the situation we are looking at is When investing in high yield, hopefully we will not get to the

point where we have to worry about liquidation priorities, etc In distress, instead, the legal and structure analysis is

paramount 65

Legal and Structure Analysis When investing in debt securities, the legal

documentation analysis and the understanding of our own and other creditors’ rights rights is of paramount importance

Security / collateral (mainly in case of loans, but also bonds sometimes) Seniority in the capital structure (structural and contractual) Change of control clause Super majority clauses (specifically in case of loans) Covenants and events of default Application of excess cashflow ….. …… …..

66

Liquidation Analysis

High yield and distress investors must understand: the bankruptcy regime of the country where the

default would take place (Center of Main Interest)

Privileged creditors Concordato Preventivo vs Fallimento vs Legge Marzano

etc …..

Understanding of treatment of each class of creditors & waterfall mechanics 67

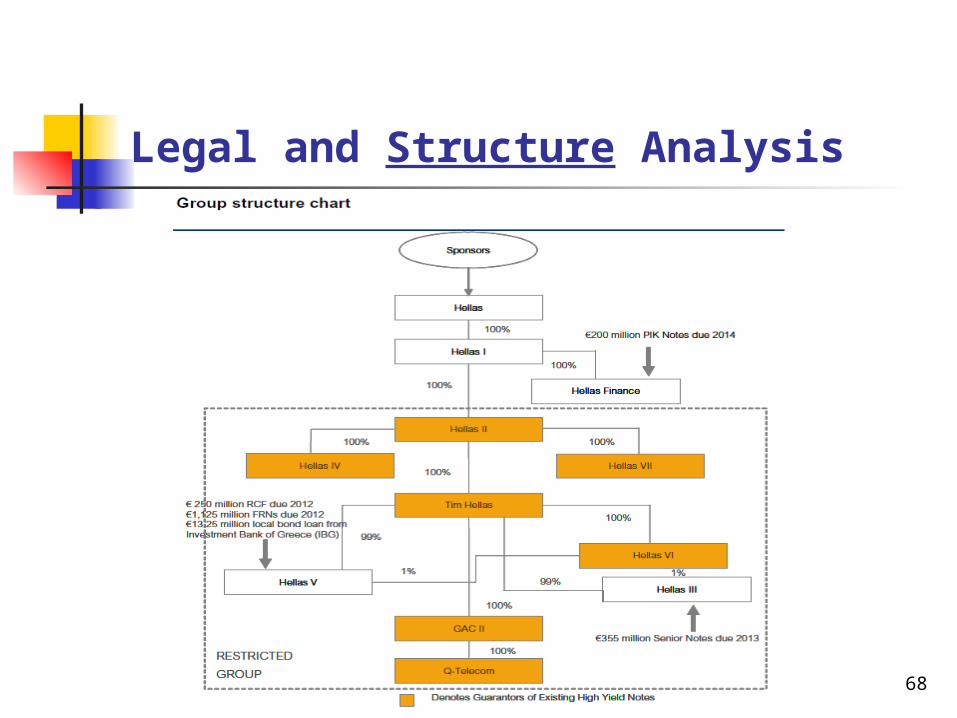

Legal and Structure Analysis

68

Trading Dynamics and Scale Given the illiquidity of the product, being able to rightly

identify which broker to deal with in order to build up a position, which timing to use, etc is a key aspect of investing in high yield and distress bonds/loans

While stocks can be cheap/expensive but can always get cheaper/more expansive, credit investing is mean reverting, i.e. the company will pay you back par value unless it defaults

This feature makes the trading scale strategy crucial

When prices deteriorate because of market conditions, usually high yield and distress investors who have a high degree of conviction would tend to add to their positions (technically called “double down”)

69

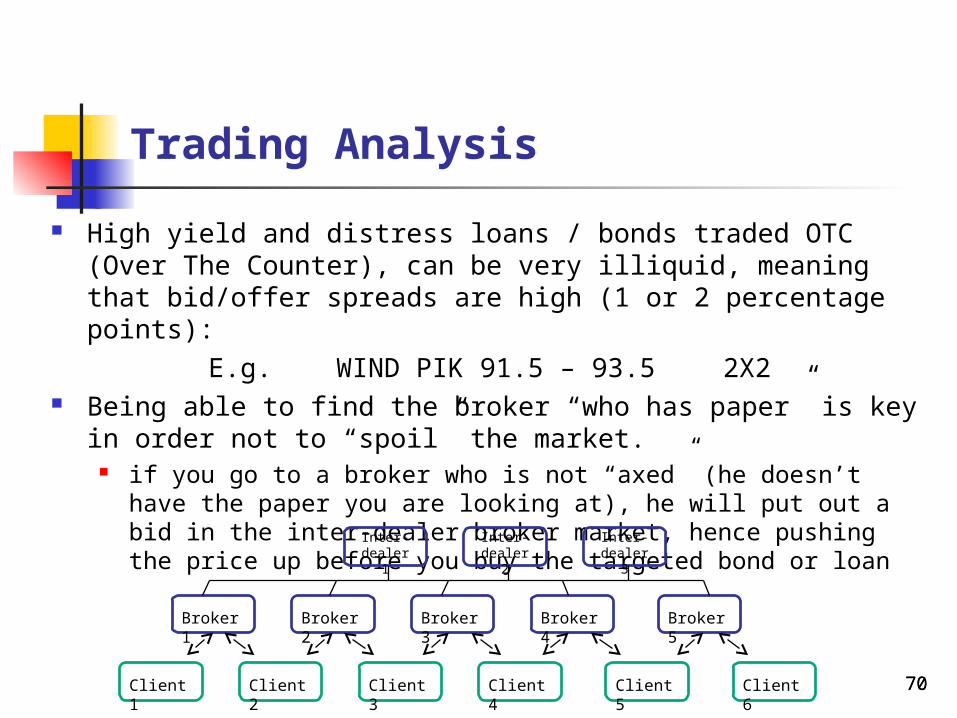

Trading Analysis High yield and distress loans / bonds traded OTC (Over The

Counter), can be very illiquid, meaning that bid/offer spreads are high (1 or 2 percentage points):

E.g. WIND PIK 91.5 – 93.5 2X2 Being able to find the broker “who has paper” is key in order

not to “spoil” the market. if you go to a broker who is not “axed” (he doesn’t have the

paper you are looking at), he will put out a bid in the inter-dealer broker market, hence pushing the price up before you buy the targeted bond or loan

Client 1 Client 2 Client 3 Client 4 Client 5 Client 6

Broker 1

Broker 2

Broker 3

Broker 4

Broker 5

Inter-dealer 1

Inter-dealer 2

Inter-dealer 3

7070

Which Investments to Place in the Portfolio?

In a Portfolio Manager’s perspective, it is key to evaluate where an investment opportunity stands compared to others when added to his portfolio

Each new investment should fit at the “margin” with the existing portfolio when considering risk/reward, degree of conviction and other diversification profiles

This “marginal investment opportunity” needs to be one where the manager think he has a particular edge (competitive advantage)

Investments can be: market directional (beta exposure, both positive or negative) market neutral (long/short credit, curve trades, basis trades,

market-hedged trades, etc)

71

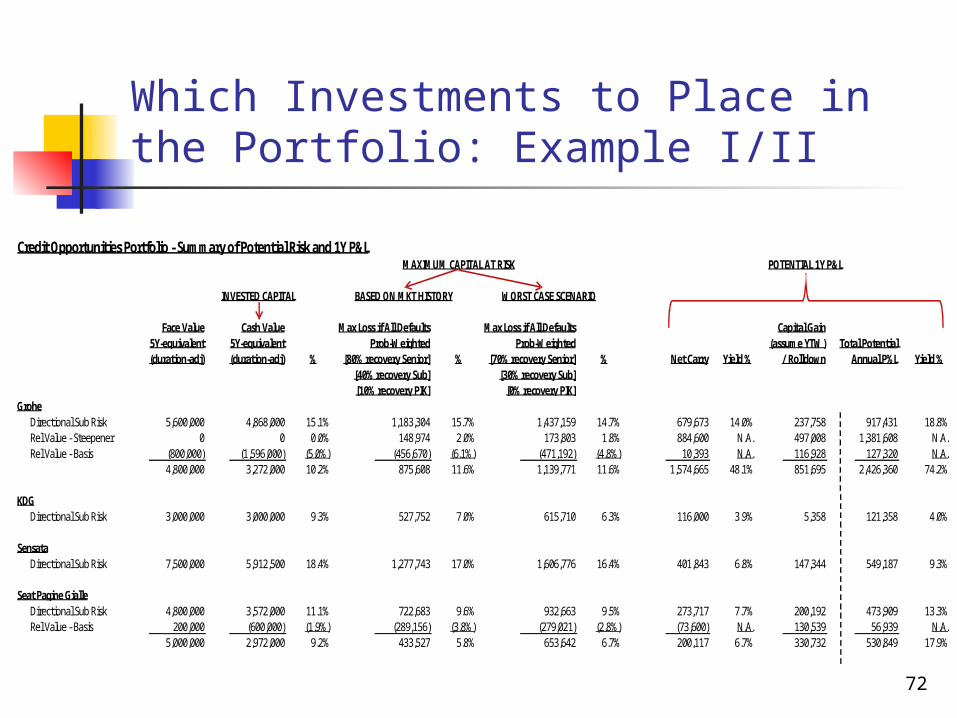

Which Investments to Place in the Portfolio: Example I/II

72

Credit Opportunities Portfolio - Summary of Potential Risk and 1Y P&LMAXIMUM CAPITAL AT RISK POTENTIAL 1Y P&L

INVESTED CAPITAL BASED ON MKT HISTORY WORST CASE SCENARIO

Face Value Cash Value Max Loss if All Defaults Max Loss if All Defaults Capital Gain5Y-equivalent 5Y-equivalent Prob-Weighted Prob-Weighted (assume YTW) Total Potential(duration-adj) (duration-adj) % [80% recovery Senior] % [70% recovery Senior] % Net Carry Yield % / Rolldown Annual P%L Yield %

[40% recovery Sub] [30% recovery Sub][10% recovery PIK] [0% recovery PIK]

GroheDirectional Sub Risk 5,600,000 4,868,000 15.1% 1,183,304 15.7% 1,437,159 14.7% 679,673 14.0% 237,758 917,431 18.8%Rel Value - Steepener 0 0 0.0% 148,974 2.0% 173,803 1.8% 884,600 N.A. 497,008 1,381,608 N.A.Rel Value - Basis (800,000) (1,596,000) (5.0%) (456,670) (6.1%) (471,192) (4.8%) 10,393 N.A. 116,928 127,320 N.A.

4,800,000 3,272,000 10.2% 875,608 11.6% 1,139,771 11.6% 1,574,665 48.1% 851,695 2,426,360 74.2%

KDGDirectional Sub Risk 3,000,000 3,000,000 9.3% 527,752 7.0% 615,710 6.3% 116,000 3.9% 5,358 121,358 4.0%

SensataDirectional Sub Risk 7,500,000 5,912,500 18.4% 1,277,743 17.0% 1,606,776 16.4% 401,843 6.8% 147,344 549,187 9.3%

Seat Pagine GialleDirectional Sub Risk 4,800,000 3,572,000 11.1% 722,683 9.6% 932,663 9.5% 273,717 7.7% 200,192 473,909 13.3%Rel Value - Basis 200,000 (600,000) (1.9%) (289,156) (3.8%) (279,021) (2.8%) (73,600) N.A. 130,539 56,939 N.A.

5,000,000 2,972,000 9.2% 433,527 5.8% 653,642 6.7% 200,117 6.7% 330,732 530,849 17.9%

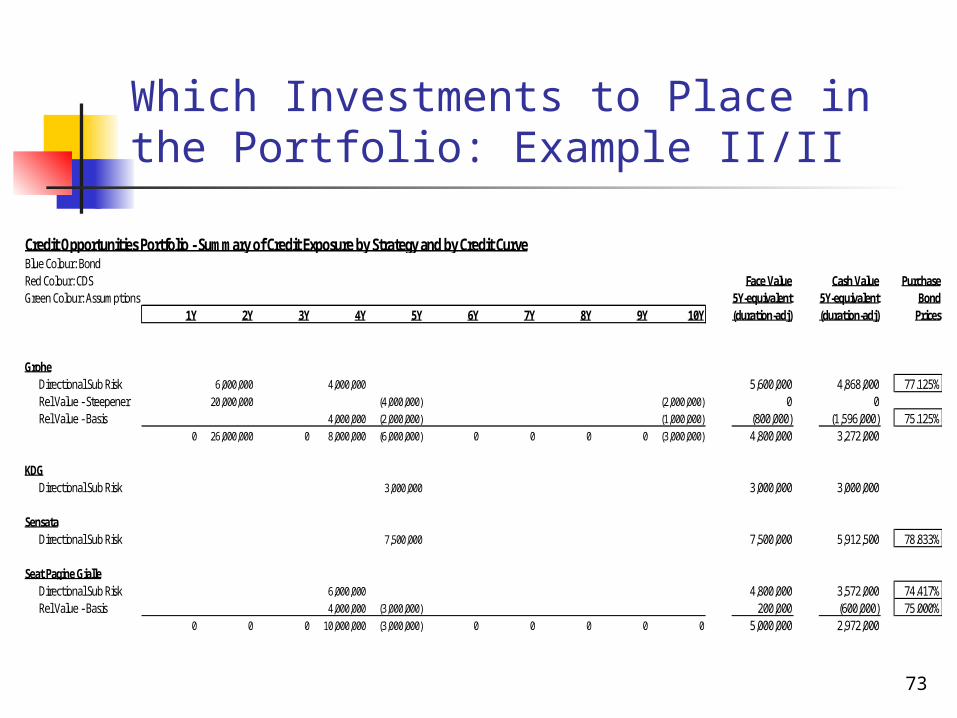

Which Investments to Place in the Portfolio: Example II/II

73

Credit Opportunities Portfolio - Summary of Credit Exposure by Strategy and by Credit CurveBlue Colour: BondRed Colour: CDS Face Value Cash Value PurchaseGreen Colour: Assumptions 5Y-equivalent 5Y-equivalent Bond

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y (duration-adj) (duration-adj) Prices

GroheDirectional Sub Risk 6,000,000 4,000,000 5,600,000 4,868,000 77.125%Rel Value - Steepener 20,000,000 (4,000,000) (2,000,000) 0 0Rel Value - Basis 4,000,000 (2,000,000) (1,000,000) (800,000) (1,596,000) 75.125%

0 26,000,000 0 8,000,000 (6,000,000) 0 0 0 0 (3,000,000) 4,800,000 3,272,000

KDGDirectional Sub Risk 3,000,000 3,000,000 3,000,000

SensataDirectional Sub Risk 7,500,000 7,500,000 5,912,500 78.833%

Seat Pagine GialleDirectional Sub Risk 6,000,000 4,800,000 3,572,000 74.417%Rel Value - Basis 4,000,000 (3,000,000) 200,000 (600,000) 75.000%

0 0 0 10,000,000 (3,000,000) 0 0 0 0 0 5,000,000 2,972,000

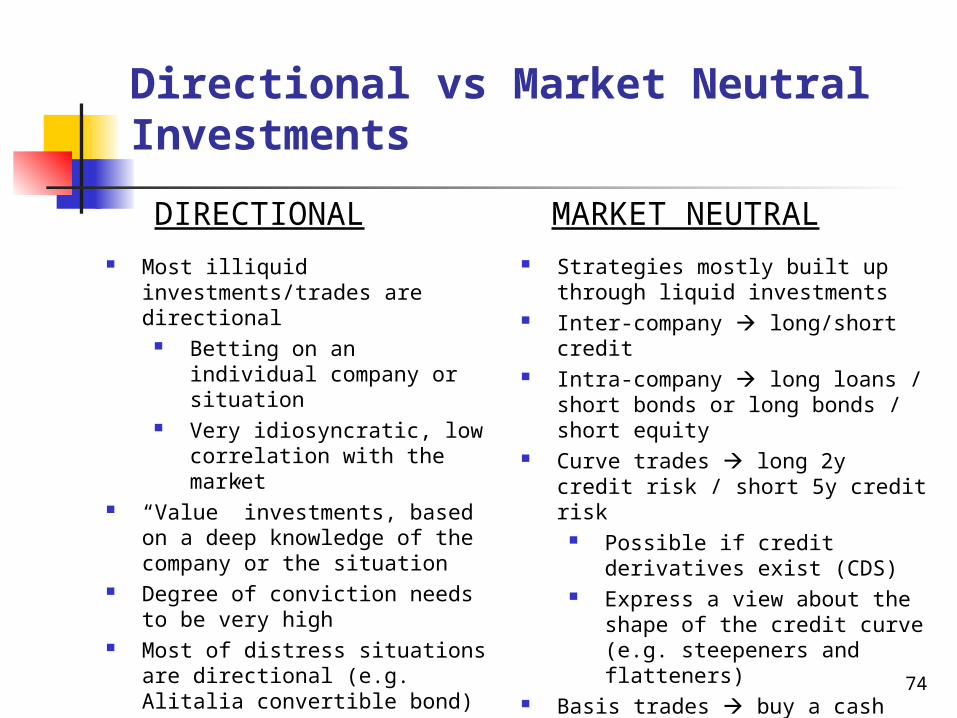

Directional vs Market Neutral Investments

Most illiquid investments/trades are directional

Betting on an individual company or situation

Very idiosyncratic, low correlation with the market

“Value” investments, based on a deep knowledge of the company or the situation

Degree of conviction needs to be very high

Most of distress situations are directional (e.g. Alitalia convertible bond)

Strategies mostly built up through liquid investments

Inter-company long/short credit Intra-company long loans /

short bonds or long bonds / short equity

Curve trades long 2y credit risk / short 5y credit risk

Possible if credit derivatives exist (CDS)

Express a view about the shape of the credit curve (e.g. steepeners and flatteners)

Basis trades buy a cash bond and buy CDS protection, yielding a net interest income (virtually risk free)

DIRECTIONAL MARKET NEUTRAL

74

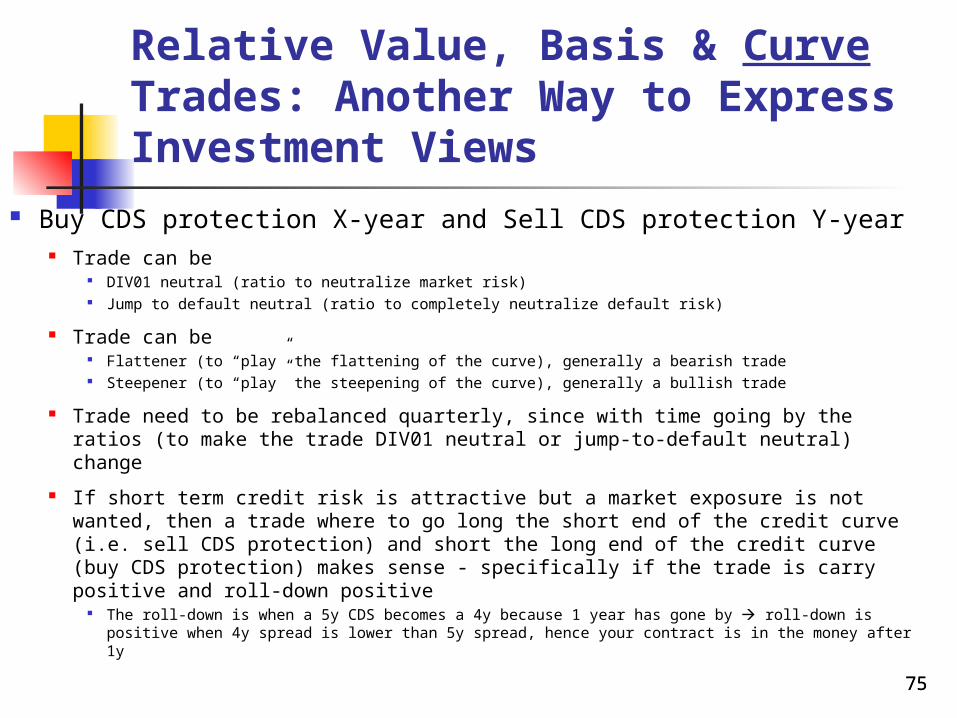

Relative Value, Basis & Curve Trades: Another Way to Express Investment Views

Buy CDS protection X-year and Sell CDS protection Y-year Trade can be

DIV01 neutral (ratio to neutralize market risk) Jump to default neutral (ratio to completely neutralize default risk)

Trade can be Flattener (to “play” the flattening of the curve), generally a bearish trade Steepener (to “play” the steepening of the curve), generally a bullish trade

Trade need to be rebalanced quarterly, since with time going by the ratios (to make the trade DIV01 neutral or jump-to-default neutral) change

If short term credit risk is attractive but a market exposure is not wanted, then a trade where to go long the short end of the credit curve (i.e. sell CDS protection) and short the long end of the credit curve (buy CDS protection) makes sense - specifically if the trade is carry positive and roll-down positive

The roll-down is when a 5y CDS becomes a 4y because 1 year has gone by roll-down is positive when 4y spread is lower than 5y spread, hence your contract is in the money after 1y

7575

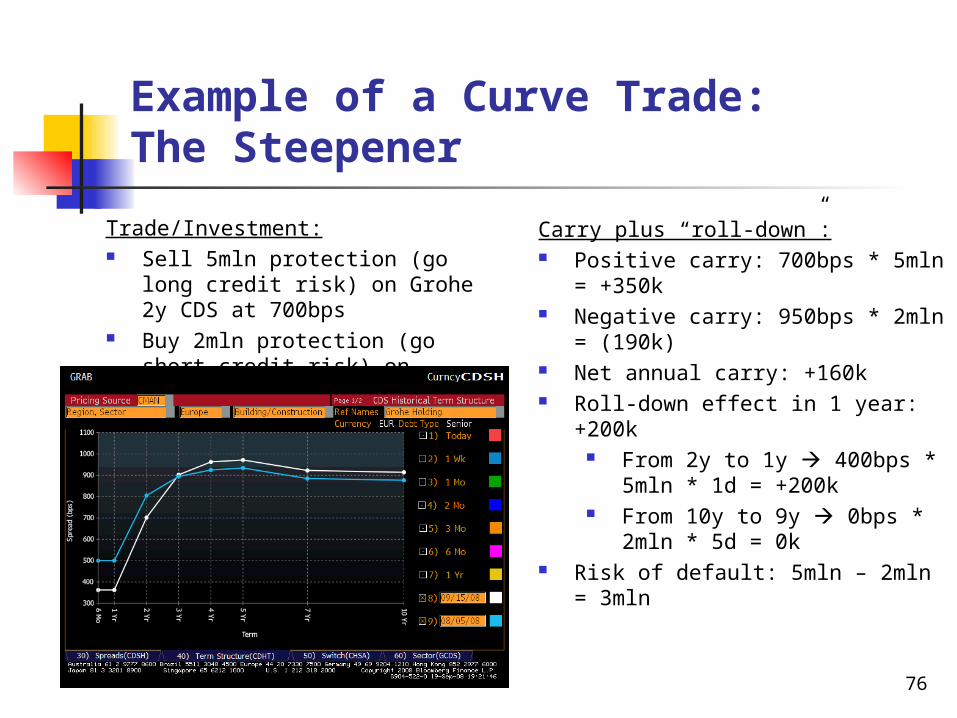

Example of a Curve Trade: The Steepener

Trade/Investment: Sell 5mln protection (go long

credit risk) on Grohe 2y CDS at 700bps

Buy 2mln protection (go short credit risk) on Grohe 10y CDS at 950bps

Carry plus “roll-down”: Positive carry: 700bps * 5mln =

+350k Negative carry: 950bps * 2mln =

(190k) Net annual carry: +160k Roll-down effect in 1 year: +200k

From 2y to 1y 400bps * 5mln * 1d = +200k

From 10y to 9y 0bps * 2mln * 5d = 0k

Risk of default: 5mln – 2mln = 3mln

76

Liquidating a Position

Liquidating a position in high yield can be very expensive (in distress is virtually impossible)

Bid / Ask spread can be up to 5 points in the less liquid names, and most likely would work in max 2mln size

Once you hit a bid of a broker in 2mln, the next “market” the broker might offer you can be 1 or 2 points lower

In a market where there is lack of liquidity, e.g. the days after the Lehman bankruptcy, there is literally no bid for the higher yielding products

The CDS is much more liquid, however not all the cash bonds do have CDS protection outstanding (only the more traded and liquid names)

77

Monitoring Risk

Risk monitoring is done through a portfolio management tool

Interest rate or currency risk exposure Breakdown of exposure by sector Breakdown of exposure by seniority of securities in the capital structure Analysis of carry interest vs accrual of principal (PIK or capital

appreciation when securities purchased at discount) Analysis of liquidity of the instruments Analysis of volatility by instruments Analysis of estimated tail risk (capital at risk in case of financial shocks)

Risk management performed daily with update of prices Risk management need to be put into the overall hedge

fund context

78

Hedging Strategies: Which Risks to Hedge?

Market risk Hedged through shorting the reference index (Itraxx Xover 5y in high yield) Hedged through shorting basket of comps Capital structure trades (long loan, short bond) Curve or basis trades

Tail / Shock market risk Buying out of the money put options on the reference index Buying out of the money put options on the listed public equity of the

company, assuming the company is listed

Operating risks Assuming the company is highly exposed to a raw material, then short the

best proxy of such raw material or buy out of the money call options Assuming the company has significant portion of EBITDA in US$, then

hedge the currency risk

Financial risks Assuming we want to buy a long dated fixed coupon bond, then probably a

good idea would be to hedge the interest rate risk 79

Why is Information so Important?

To refine the company fundamentals analysis Better operating and financial modeling Better knowledge of suppliers’ and customers’ opinion of

company’s products

To forecast events that the market is not aware of

M&A or extraordinary finance transactions which might have an impact on bonds and loans

From a strictly trading perspective, better execution on buying and selling

Knowing who has the paper Knowing how many buyers and sellers there are in the market

80

Current Market Conditions

Are You Ready for Distress?

81

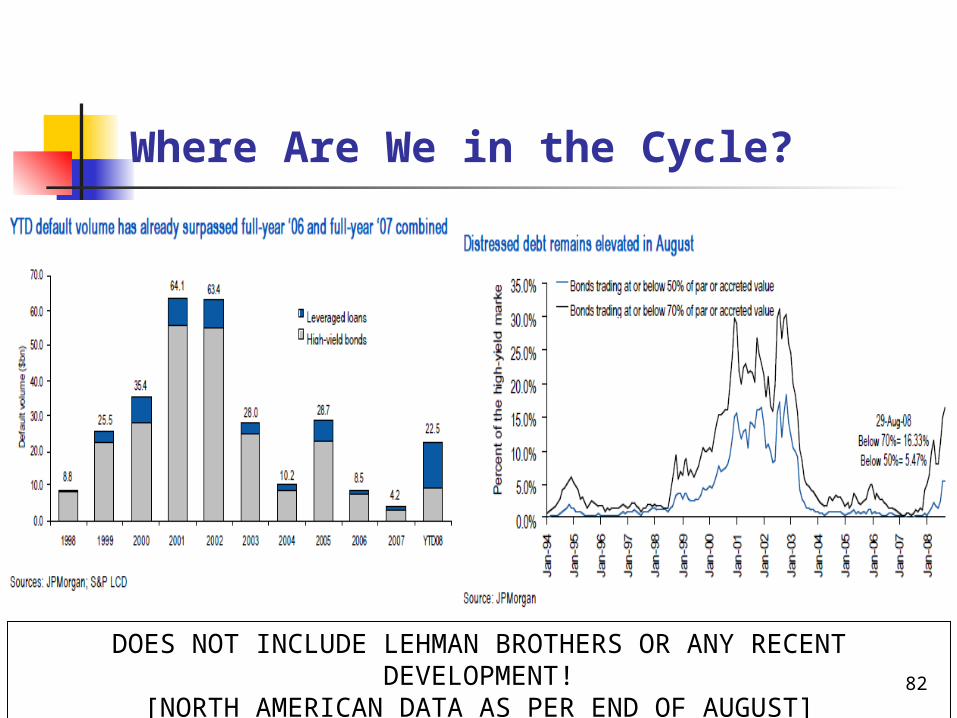

Where Are We in the Cycle?

82

DOES NOT INCLUDE LEHMAN BROTHERS OR ANY RECENT DEVELOPMENT!

[NORTH AMERICAN DATA AS PER END OF AUGUST]

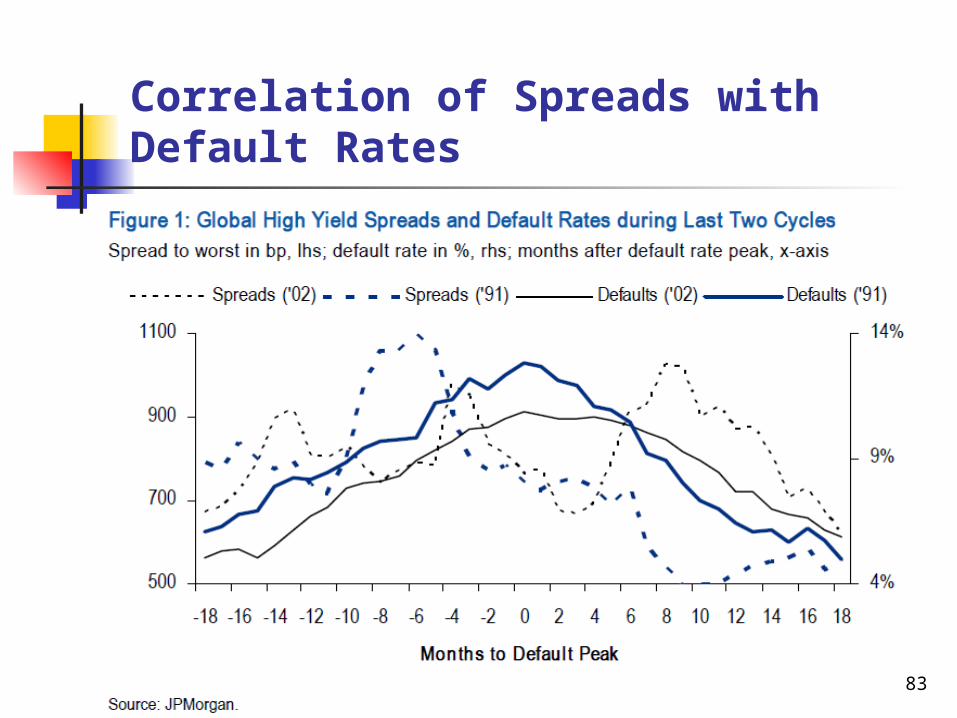

Correlation of Spreads with Default Rates

83

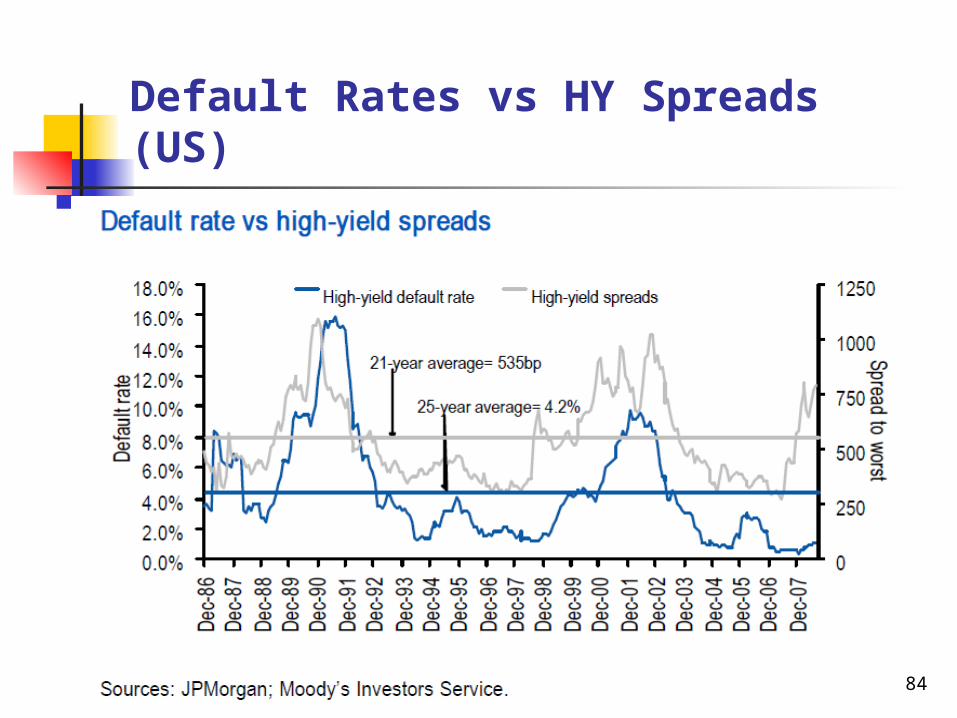

Default Rates vs HY Spreads (US)

84

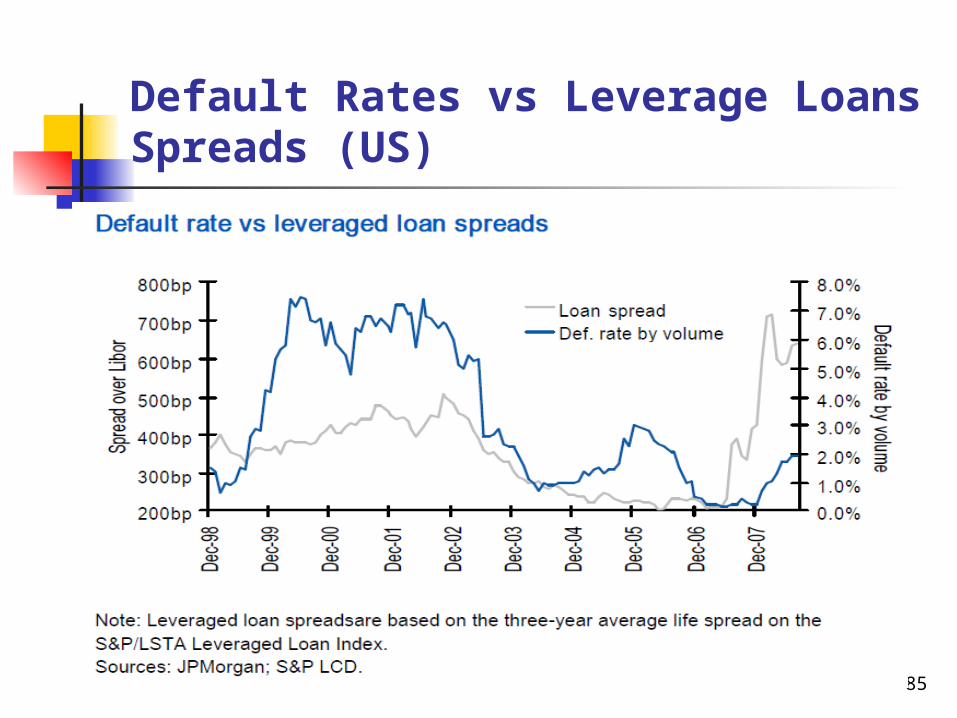

Default Rates vs Leverage Loans Spreads (US)

85

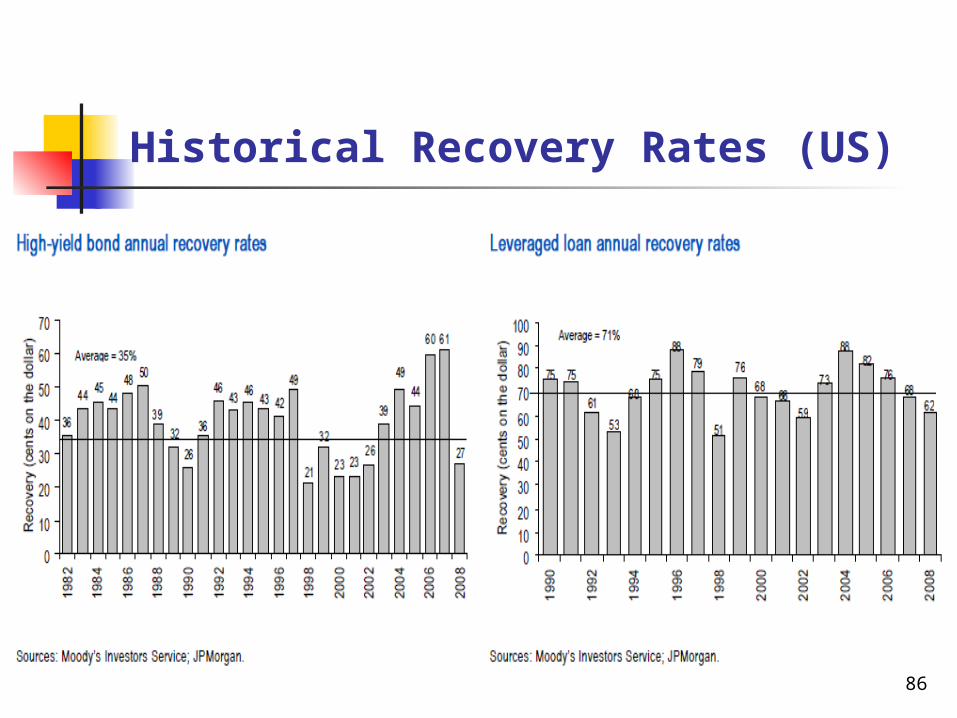

Historical Recovery Rates (US)

86

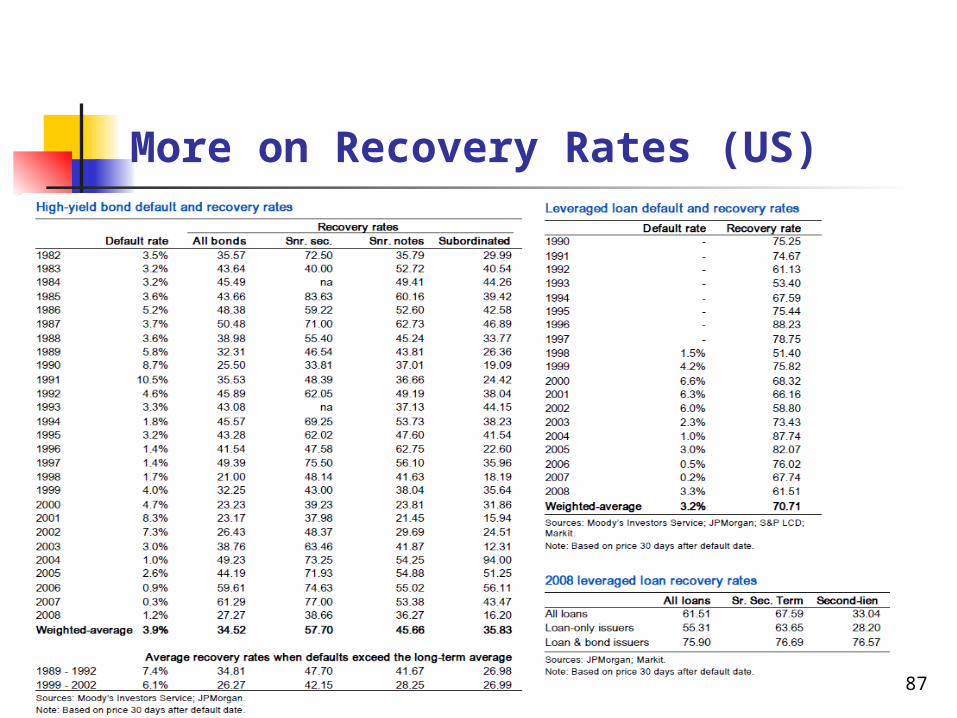

More on Recovery Rates (US)

87

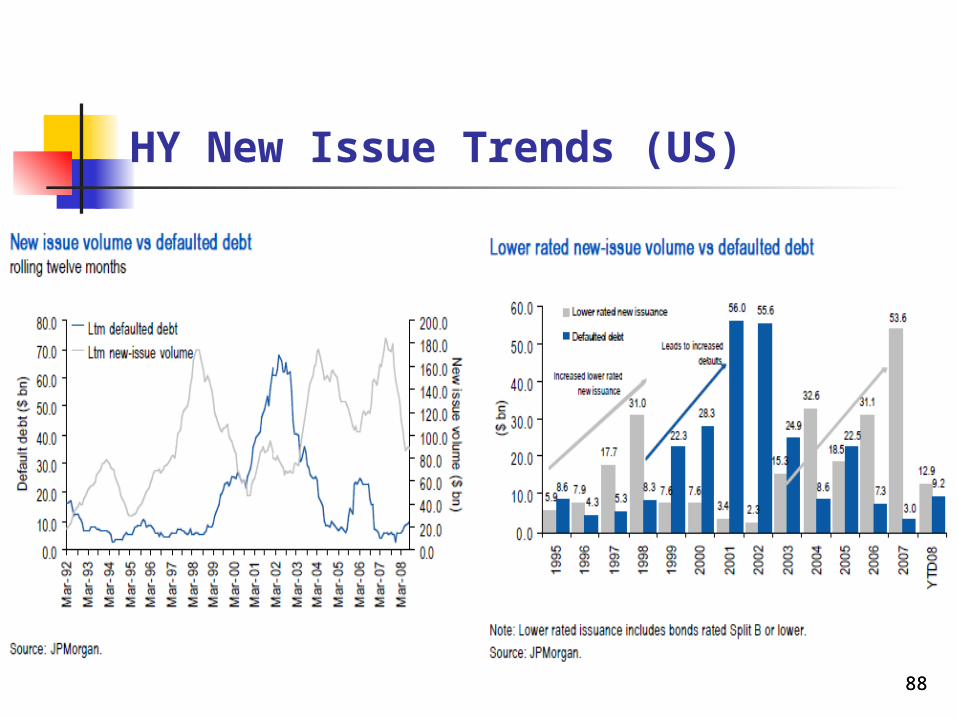

HY New Issue Trends (US)

8888

Conclusions

Distressed debt is already out there Many private equity funds and other institutional funds

are setting up more and more dedicated funds to this asset class

Spreads are currently on the rise, and there to stay for 12-24 months

Carry interest is currently high, looking at historical average, which makes the asset class already attractive

Default rates will peak in the next 12-24 months Market prices (hence spreads) anticipate default rates

89