Embed Size (px)

Citation preview

co -2:=!: >< >< .. w w 0 -

A GUIDE TO CONSUMER CREDIT IN FIVE COUNTRIES OF THE EUROPEAN UNION :

GERMANY, BELGIUM, SPAIN, FRANCE AND THE UNITED KINGDOM

The guide has been compiled by Science Practique SA (France) thanks to the financial support of:

the European Commission, Cetelem (France),

the Association Franyaise des Societes Financieres (ASF), the Association Franyaise des Banques (AFB)

and the Secretariat General ofthe Conseil National du Credit et du Titre (France). This guide was exclusively compiled and written by his own author.

Contributions to the guide were also made by the Confederation of Family Associations of the European Community (COF ACE), L'Association d'Education et d'Information du consommateur de la Federation de !'Education Nationale (ADEIC-FEN) of France and those who agreed to be

surveyed within the framework of the study which preceeded the writing of the guide. We would like to thank them all. - 1999-

2

{ CJ. '1ft fl(t

TABLE OF CONTENTS 1. EUROPEAN STATUTORY FRAMEWORK : DIFFERENT NATIONAL LAWS

2. THE QUESTIONS TO ASK AND TO ASK ONESELF Is credit necessary ? What type of credit? Stages of a credit agreement

1. The information stage 2. The offer and its examination 3 Acceptance of the contract 4. The hfe of a contract

3. TAKING OUT CREDIT IN A COUNTRY Prior information Contractual offer The contract Life of the contract

4. GOING FROM ONE COUNTRY TO ANOTHER If you come from Germany : If you come from Belgium : If you come from Spain : If you come from France : If you come from United Kingdom:

5. DEALING WITH PROBLEMS Who to contact in Germany Who to contact in Belgium ? Who to contact in Spain ? Who to contact in France ? Who to contact in United Kingdom

3

4

6 6 6 7 8

10 12 13

15 16 18 20 22

24 25 26 27 28 29

30 32 33 34 35 36

1. European statutory framework : different national laws

The single European market came into existence on January 1, 1993. To achieve this, legislation had to be drawn up to allow for the opening up of the countries. All the Member States have legislation based on common principles and rules governing the workings of the new economic area. The provisions in the area of finance are particularly precise and, as a result, credit institutions are able to offer financial services throughout the whole of the European Union through a variety of means.

European regulations operate under the form of texts called directives, which the Member States are under the obligation to transpose to their national law within a given period of time. According to the domain, such directives are more or less precise and restrictive.

In the case of consumer credit, given that it is an activity which involves consumers, private individuals, European regulations only establish minimal provisions, each State remaining at liberty to formulate more specific rules.

The Treaty of Rome, the founding treaty of the European Union, actually states in article 3 that the consumer should be covered by specific measures of protection : " the action of the Community consists in (0) s) a contribution to the strengthening of consumer protection"

stipulates in article 1 OOA " the Commission, in its proposals (0) concerning health, environmental and consumer protection, will take as a base a high level of protection"

and article 129A establishes that protection be provided for by specific measures but that such "actions shall not prevent a Member State from maintaining or establishing stricter measures (0) compatible with the (0) Treaty "

Consequently, in the domain of consumer credit

each country has proceeded to draw up specific legislation on the basis of minimal common rules, the result being disparate sets of regulations

4

Yet, until present, each of us has lived in our own country, in the main. We have acquired habits developed on the basis of our day-to-day experiences with our various suppliers of goods and services. It is on the basis of such habits that we make decisions, such as the decision to borrow on certain terms.

Consumer credit is not something to be entered into lightly as it implies future financial consequences affecting the whole family.

It therefore essential to find out all the often tacit ins and outs of a credit agreement, to be sure to master such an operation .

The present guide sets out to achieve just that within a European context, by looking into the situation of a consumer who comes from one country in which he has acquired certain habits and intends to examine or obtain credit facilities ffered by an organisation based in another country.

Consumer credit, which has generally become a straightforward operation and is readily available, is tied to a very precise legislative framework seeking to protect the consumer. The latter is, in fact, considered to have less powers of analysis and understanding than a professional. Furthermore, there are a number of international texts which govern the application of contract law. Diversity among national laws may lead to confusion which may cloud the reality of the commitment being entered into by both the lender and the borrower. It should also be borne in mind that an operation which may be considered as very simple in one's own country, ceases to be so when going beyond one's own borders, whether physically or virtually, insofar as the necessary experience and habits have not been acquired.

The legislation in the various countries covers a number of different areas, ranging from publicity and overindebtedness to interest free credit and redemption before due date.

The method proposed in this guide consists in drawing attention to the various aspects or the various stages of a credit agreement, to serve as a reminder to the consumer, as well as the person he is dealing with, that questions have to be asked and that one must ask oneself questions :

good credit is well mastered credit.

5

2. The questions to ask and to ask oneself

amount eammgs

Is credit necessary ?

A purchase can be made in cash, payment by credit is not obligatory.

What are the advantages and disadvantages of buying cash and on credit ? Can I postpone this purchase ? Can I include this new credit facility in my monthly budget calculated as follows, without upsetting the balance ?

amount fixed expenses

amount amount variable expenses monthly payments

available budget

I am certain of the obligations I will be taking on as a result of the credit obtained ? What would be the consequences of such a commitment were my situation unexpectedly to change. The larger the amounts involved the more important it is to be fully aware of the potential consequences.

What type of credit?

We do not pay for a car in the same way as we pay for a television or a holiday. It is therefore important to ensure that the product and its durability concurs with the credit facilities for that product and the restrictions that the borrower accepts.

The following possibilities exist in almost each country under different names :

( overdraft with a bank, operated by forms of payment such as charge cards or personal credit granted by the credit institution of the current account.

( personal line of credit granted by the credit institution to someone for a certain amount and defined repayments (credit or installment plan).

( renewable credit granted for a maximal amount and to be repaid at settled dates or chosen ones, called also permanent credit or revolving credit or credit opening. Can be used either directly or with a card. Renewal modalities or closure of the contract changes from one country to another.

6

• credit to finance a specific purchase, granted either by the seller or by a credit institution. Such contracts are most often drawn up at the place where the purchase is made or specifically arranged to finance the purchase in a shop. We can also talk about hire-purchase sales.

• lease-purchase agreement or leasing , which consist in the payment of rentals until a buying option allows for the purchase of the good at a previously arranged residual value.

The cost, the methods of use of such credit, the risks and the guarantees provided for by law vary in accordance with the amounts involved, the type of credit and its duration.

Each country has specific regulations governing consumer credit, however the definitions vary as to the operations which are and are not covered by legal provisions. It is wiser to be protected by the law. These elements are covered below in the pages devoted to the countries.

Later in the guide you will find information on :

Germany, Belgium, Spain, France and the United Kingdom, set out country by country,

coming from one country and seeking credit in one of the other four countries

Stages of a credit agreement

There are several stages in the conclusion of a credit agreement, though they may vary according to the circumstances : if you take out credit to cover a purchase made in a shop, you will not be subjected to the same demand or waiting period that apply when credit is used for a planned purchase or takes the form of a cash advance. In the first instance the two initial stages tend to be associated with one another while in the second no link is made.

The process of acquiring credit can be divided 4 main stages :

1. Prior information, the stage during which you yourself and the credit grantor will collect the information required to make a decision

2. The formalisation of the credit grantor's offer and your study of it

3. The conclusion of the contract

4. The life of the contract

7

1. The information stage

This is essential in coming to a clear decision. It depends on the form the offer takes. It may be made through an advertisement, a door-to-door sales person, the media, or may be made in response to the direct request of a consumer made to a credit grantor .

You have the right to the minimum level of information required to know, to understand, to examine and to choose:

- The identity of the credit grantor

- the product being considered

? the overall effective rate, expressed in tem1s of a percentage, includmg the debt interest (or the way in which it is set, for example in the case of a permanent credit at a variable rate of interest) and the various charges linked to the operation. This rate is expressed either in yearly or monthly terms. The methods of calculation vary from country to country, it is therefore necessary to ensure that you are given all the details of what the rate includes and how it is calculated in the case of your operation.

? The effective rates are not capped everywhere by usurious rates. There are fixed ceilings which are determined by the law in the case of Belgium and France. The rates are determined by the legal definitions of the courts in a more (Germany) or less (Spain, UK) precise way.

? The duration and the amount of the repayments or failing that their method of calculation

But you can get more :

- by asking the credit grantor, for example, about the charges that are linked but not obligatory and may be waived, the other products available, other insurance policies, etc.

- by contacting a consumer advice bureau or by consulting a magazine which specialises in comparing the offers made by credit institutions, or brochures, guides, or books on the subject

- by contacting several credit grantors at the same time or an intermediary who is familiar with several lenders

-by contacting the administrative services in certain countries

The better informed you the more chance you have, first of all, of using the competition in your favour and, secondly, of mastering all there is to know about credit facilities, which include technical aspects which may be offputting at first glance.

8

The credit grantor, for its part, requires information to decide whether to grant you credit. It wishes to assess your ability to honour your commitment to repay the amounts foreseen on the due dates, given that the money loaned to you does not belong to it : Either it has borrowed it itself, or is using the savings entrusted with it by its depositors.

The credit grantor will ask you for information which will aid it in making its decision. It also has access to data included in the files on you.

The decision of credit grantors depends on the amount and the duration of the operation and on the other hand on the way in which they organise the decision making process for granting credit facilities, as in many instances credit decisions are decentralised, bemg left in the hands of thousands of commercial representatives : the decision making process ought to be the same from place to place, in other words standardised.

The larger the amount and the duration the greater the risk for the credit grantor, thus more information, documents or guarantees will be requested. The smaller the amount and the duration, the simpler the requirements will be.

Credit grantors are making increasing use of what is known as credit scoring, based on the comparison of the data collected from you with the statistics on repayment and non repayment corresponding to similar data on the clientele as a whole who have requested credit facilities. Depending on the country, the criteria used in this method of selection may or may not be submitted for examination to an agency for the protection of private data.

The decision of the credit grantor is final, you do not have an automatic right to credit.

It is difficult to make generalisations about the information requested as it varies according to the system used by the lenders. You will, however, in addition to your name and address at least be asked about :

your earnings, your expenditure and costs, questions regarding your : marital status, length of service in employment, the length of time living in one place, and various other questions.

There are two kinds of files to which the credit grantors have access :

- their own files, or those of the organisations with which they have links such as credit insurers in the country where they are based, which contain a record of any previous dealings you may have had with them

- and those of external organisations, be they private or public. Depending on the country in question, such files may contain positive data (all your credit operations in addition to any defaults where applicable : credit reference agencies) or simply the negative data (defaults on payments, legal proceedings or overindebtedness)

9

Legislation exists with regard to these files and provision is made in all instances for the right to have access to the data contained in them and to rectify such data.

You may have received an offer directly from a credit grantor, or you may have contacted the institution yourself, in which case, following an assessment of your situation, the credit grantor will prepare to make you an offer.

But you may have contacted an intermediary because you live far out of town or because you are not sure of the outcome of a request made directly to the lender, or maybe because you hope that an expert will provide you with the best offer available and will take charge of playing the competition off against each other in your stead.

The situation varies greatly from country to country, it is therefore difficult to generalise, but under no circumstances may an intermediary ask you for money for an operation which is not executed.

In the event that you have to pay commission, the intermediary must make it clear in advance and give you a detailed receipt distinguishing the commission from the possible costs incurred by him.

Furthermore, along with the offers made by the lenders he must also provide you with the minimum information that the lender would be obliged to give you if dealing with you directly.

2. The offer and its examination

To enable you to examine the offer and its consequences, the laws provide for a period of reflection or renunciation.

In order to give you the time to reflect on, study and understand the operation that you are committing yourself to, the credit grantor is under the obligation to submit you a written offer which includes either a period for decision (France), for validity (Belgium), or a cancellation deadline (France) or a renunciation (Belgium) (see the pages dealing with the countries).

If, for example, you take out a credit facility to finance a purchase, you should be aware that the legal provisions on this matter stipulate a legal link between the two operations when they are initially undertaken, in order that :

( you are left with the opportunity to cancel the credit agreement if you return the good or the service, or if the purchase fails to correspond to the purpose for which it was intended

( you are under no obligation to purchase the good or service if for one reason or another credit has not been granted.

10

However, once the two operations have been approved and the legal deadlines expired, they become the object of separate contracts which are independent of each other, each having their rules and obligations, which means that you are obliged to repay the amounts on the due dates established.

During this period, the credit grantor has submitted you a firm offer and is bound by the latter within the limits of the legal deadline established.

That means that it has set aside a loan opportunity for you which it could use for other clients, because its overall credit activity is controlled.

Furthermore, although interests rates may undergo significant variations, the credit grantor is bound to stand by its offer if it comprises a fixed rate. Such proviswns serve to protect you, while in its own way the credit mstitution takes a risk.

The submission of a written offer is obligatory : you must demand one, even if certain institutions may be reticent to submit it to you.

The period of reflection provides you with an opportunity to read and study the contractual clauses since the offer generally covers the terms of the contract.

Take the time to read the text and maybe have it explained to you, by the lender or an organisation providing assistance to consumers, because the contract contains provisions which concern you.

Take the time to study the guarantees demanded or those that you personally are providing if you are standing surety or if you are a co-debtor. That is, if you are affixing your signature to a commitment on behalf of a third party which commits you, under certain conditions and with a certain degree of protection, as if you personally were the debtor.

The more time you dedicate to studying the contract, the less surprises you will be faced with if difficulties were to arise.

Nevertheless, one does not always have time to study the offers.

The guarantees most commonly demanded by credit establishments m exchange for giving you credit, are the following:

- assignment of wages. Very common practice in certain countries, while very rare in others. In the former case, a documents is presented as an integral part of the contract and means that the borrowers agrees to a portion of his wages being seized by the lender in case of a default on payments.

11

- co-signature by a third party, spouse or other, who becomes a co-debtor and is able to take action against you, in the event of payment made in your place.

- surety demanded from a third person. In most of the countries, the legal provisions apply to and protect both the person standing surety and the borrower. The person standing surety has the right to receive the offer or the contract and benefits from specific protection.

- a pledge on good, for example when purchasing a car. The provisions in this matter stipulate the signing and depositing of legal certificates. More often demanded and stipulated is access to the credit balances or assets (savings accounts, shares, etc.) on the balance sheets of the bank.

In general terms, you should be aware that when in debt liability for repayment covers the whole of your earnings and belongings and possibly those of your spouse, depending on the marriage contract, within the limits of the goods and earnings threshold deemed unseizable and defined by the law. At the same time, certain countries have introduced specific provisions into their legislation for people who are no longer able, for whatever reason, to honour their debts.

3. Acceptance of the contract.

The text must contain certain references in compliance with the law, stating the presumption that the borrower possesses all the information required to understand and manage the commitment undertaken.

The contract must, in particular, make reference to the effective rate ofthe loan :this rate which varies in name and in content from one country to the next must enable you to make a comparison within the same territory of the offers of different organisations. Be aware of the aspects to determine such.

Most credit institutions in the majority of countries ask for hand written references which precede your signature. Such references are established by the law, and are aimed at drawing your attention to the commitment that you are undertaking. Nevertheless, it is in your interest to ask for an explanation of the purpose of each of the signatures which you are asked to give, especially to fully distinguish between that which relates to the credit agreement and another undertaking, such as an assignment of wages, for example.

The law establishes a period of cancellation (France) or renunciation (Belgium) of the contract. Be aware of how it works, particularly if you are required to act, you should know what to do and how to do it.

12

You should also be aware that credit institutions in certain countries transfer the funds before the above period has expired. If you want to renounce the debt, you must ensure that you are able to repay it in full, and within the briefest time span possible.

4. The life of a contract

a) information provided during the life of the contract

Legal provisions generally only cover information on changes in the debt interest in the case of overdrafts, credit arrangements or variable rate credit. A rate may not applied before you are informed of it : you have the right to contest it.

In practice most institutions provide you with a depreciation table in the case of loans with known rates and due dates, then send you account statements on a regular basis.

Do not hesitate to ask for an explanation of the permanent credit statements and the methods of calculating the rates, costs and charges.

b) redemption before due date

The law in every country provides for the possibility of redeeming a debt before the due date. This possibility is systematic and cost free in the case of overdrafts and permanent or revolving credit, but is more restrictive in the case of other products. The costs and the methods vary considerable from one country to the other (see tables dedicated to the countries).

c) dealing with temporary difficulties

Financial difficulties can affect anyone and it is in the interest of the credit grantor itself to help you to resolve them, as debt collection proceedings taken out against you, whether settled in court or amiably, cost it dearly and it also runs the risk of losing your custom.

Take the initiative and contact you credit grantor !

All the institutions are organised in such a way as to find negotiated solutions to problems. Their representatives will offer you solutions. Taking the initiative could save you from the deduction of charges (follow-up charges, interest on arrears) and the unpleasantness of receiving a follow-up letter of varying severity.

13

You should be aware that if you do not do anything, and let a due date go by without payment you will receive a follow-up letter anything between one week and one month later, claiming the arrears on the interest built up over that period calculated at a different, higher rate than the normal interest on the operation. Furthermore, in the case of monthly payments, you will not only be asked for the overdue payment and the charged on it, but also the next due payment, which mean that there is every chance of worsening your financial situation.

It is often common practice for certain lenders to provide the opportunity of putting off a due payment without costs or consequences during the life of a credit agreement. Ask for the details !

d) dealing with a longer-term difficulty

• Debt collection and legal proceedings in the case of disputes take on different forms. It can happen to anyone, however, to find oneself no longer able to repay one's debts.

• Some countries have adopted provisions to assist overindebted people, but the conditions vary enormously.

• All the countries have different organisations which can help you to understand and compare offers, as well as assisting you when faced with difficulties. Do not hesitate to contact them. Certain consumer organisations are particularly well equipped and specialised in these areas and may provide you with legal services and will either ask you to pay a fee or will invoice you for the aid provided. In certain countries other organisations providing specialist help in the area of debt exist alongside such consumer organisations.

14

3. Taking out credit in a country

The principle data regarding the information, the offers, the agreements and the life of contracts in each of the countries

15

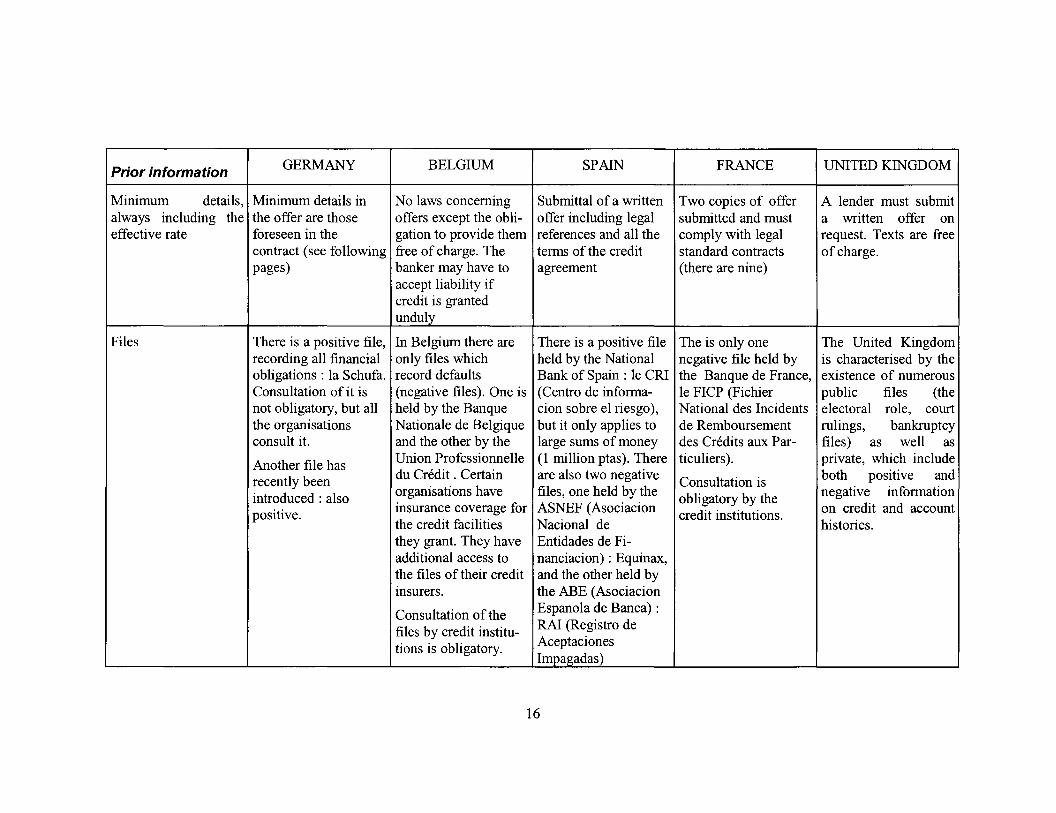

Prior information GERMANY BELGIUM SPAIN FRANCE UNITED KINGDOM

Minimum details, Minimum details in No laws concerning Submittalofavrritten Two copies of offer A lender must submit always including the the offer are those offers except the obli- offer including legal submitted and must a written offer on effective rate foreseen in the gation to provide them references and all the comply with legal request. Texts are free

contract (see following free of charge. The terms of the credit standard contracts of charge. pages) banker may have to agreement (there are nine)

accept liability if credit is granted unduly

Files There is a positive file, In Belgium there are There is a positive file The is only one The United Kingdom recording all financial only files which held by the National negative file held by is characterised by the obligations : Ia Schufa. record defaults Bank of Spain : le CRI the Banque de France, existence of numerous Consultation of it is (negative files). One is (Centro de informa- le FICP (Fichier public files (the not obligatory, but all held by the Banque cion sabre el riesgo ), National des Incidents electoral role, court the organisations Nationale de Belgique but it only applies to de Remboursement rulings, bankruptcy consult it. and the other by the large sums of money des Credits aux Par- files) as well as

Another file has Union Professionnelle (1 million ptas). There ticuliers). private, which include

recently been du Credit . Certain are also two negative Consultation is both positive and

introduced : also organisations have files, one held by the obligatory by the negative information

positive. insurance coverage for ASNEF (Asociacion credit institutions. on credit and account the credit facilities Nacional de histories. they grant. They have Entidades de Fi-additional access to nanciacion): Equinax, the files of their credit and the other held by insurers. the ABE (Asociacion

Consultation of the Espanola de Banca):

files by credit institu- RAl (Registro de

tions is obligatory. Aceptaciones Impagadas)

16

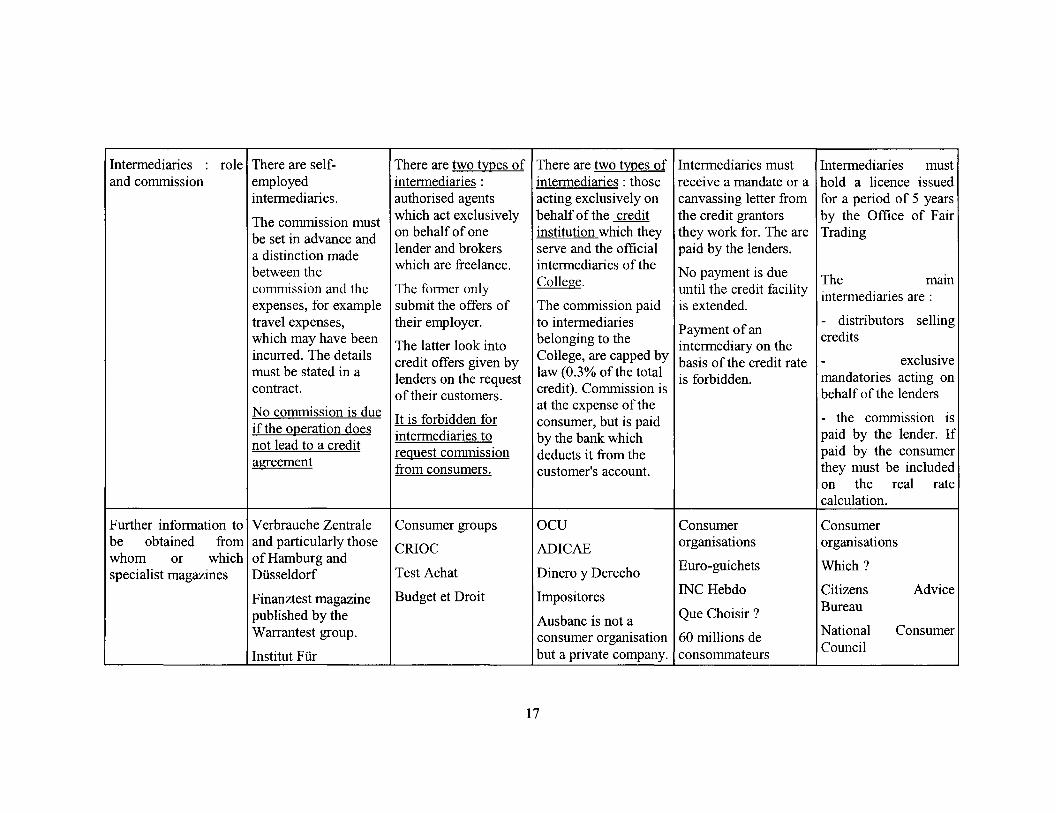

Intermediaries and commission

role There are selfemployed intermediaries.

The commission must be set in advance and a distinction made between the commission and the expenses, for example travel expenses, which may have been incurred. The details must be stated in a contract.

No commission is due if the operation does not lead to a credit agreement

Further information to V erbrauche Zentrale be obtained from and particularly those whom or which of Hamburg and specialist magazines Dusseldorf

Finanztest magazine published by the Warrantest group.

Institut Fiir

There are two types of intermediaries : authorised agents which act exclusively on behalf of one lender and brokers which are freelance.

The former only submit the offers of their employer.

The latter look into credit offers given by lenders on the request of their customers.

It is forbidden for intermediaries to request commission from consumers.

Consumer groups

CRIOC

Test Achat

Budget et Droit

There are two types of Intermediaries must receive a mandate or a canvassing letter from the credit grantors they work for. The are paid by the lenders.

Intermediaries must hold a licence issued for a period of 5 years by the Office of Fair Trading

intermediaries : those acting exclusively on behalf of the credit institution which they serve and the official intermediaries ofthe College.

No payment is due The mam until the credit facility intermediaries are : is extended.

Payment of an intermediary on the

- distributors selling credits

The commission paid to intermediaries belonging to the College, are capped by law (0.3% of the total credit). Commission is at the expense of the consumer, but is paid by the bank which deducts it from the customer's account.

basis of the credit rate - exclusive

ocu AD I CAE

Dinero y Derecho

Impositores

Ausbanc is not a

is forbidden.

Consumer organisations

Euro-guichets

INCHebdo

Que Choisir ?

consumer organisation 60 millions de but a private company. consommateurs

17

mandatories acting on behalf of the lenders

- the comm1ss1on 1s paid by the lender. If paid by the consumer they must be included on the real rate calculation.

Consumer organisations

Which?

Citizens Bureau

Advice

National Council

Consumer

Finanzdienstleistungen Budget et Droit Money Advice e. V. (IFF) Scotland Euro-Info- National Debt Line V erbraucher e. V.

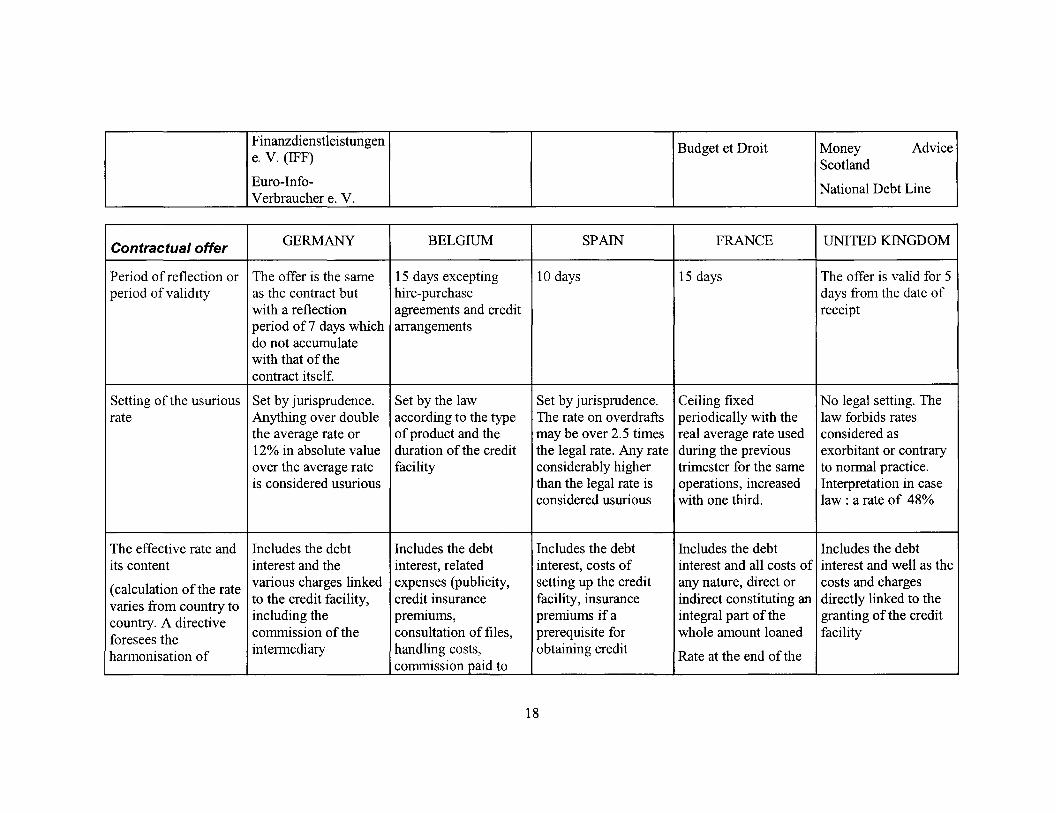

Contractual offer GERMANY BELGIUM SPAIN FRANCE UNITED KINGDOM

Period of reflection or The offer is the same 15 days excepting 10 days 15 days The offer is valid for 5 period of validity as the contract but hire-purchase days from the date of

with a reflection agreements and credit receipt period of 7 days which arrangements do not accumulate with that of the contract itself.

Setting of the usurious Set by jurisprudence. Set by the law Set by jurisprudence. Ceiling fixed No legal setting. The rate Anything over double according to the type The rate on overdrafts periodically with the law forbids rates

the average rate or of product and the may be over 2.5 times real average rate used considered as 12% in absolute value duration ofthe credit the legal rate. Any rate during the previous exorbitant or contrary over the average rate facility considerably higher trimester for the same to normal practice. is considered usurious than the legal rate is operations, increased Interpretation in case

considered usurious with one third. law : a rate of 48%

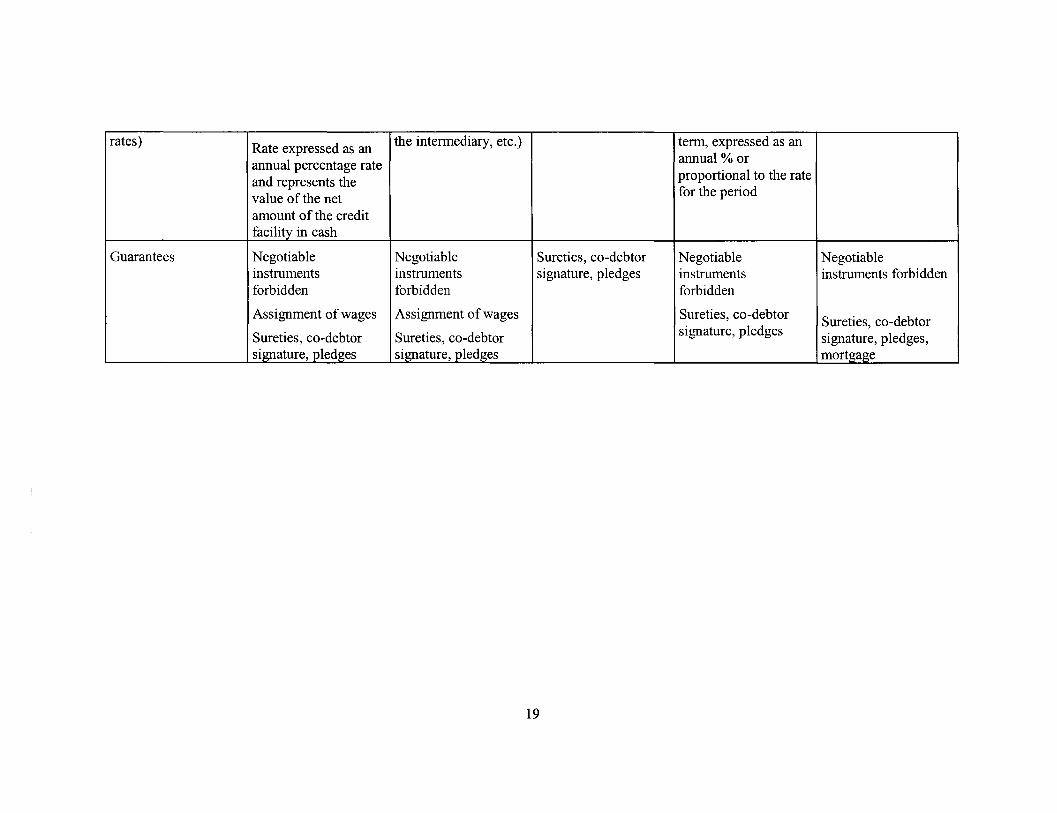

The effective rate and Includes the debt Includes the debt Includes the debt Includes the debt Includes the debt its content interest and the interest, related interest, costs of interest and all costs of interest and well as the

(calculation of the rate various charges linked expenses (publicity, setting up the credit any nature, direct or costs and charges

varies from country to to the credit facility, credit insurance facility, insurance indirect constituting an directly linked to the

country. A directive including the premiums, premiums if a integral part ofthe granting of the credit

foresees the commission of the consultation of files, prerequisite for whole amount loaned facility

harmonisation of intermediary handling costs, obtaining credit Rate at the end of the commissionpaid to

18

rates) Rate expressed as an the intermediary, etc.) term, expressed as an

annual percentage rate annual% or

and represents the proportional to the rate

value of the net for the period

amount of the credit facility in cash

Guarantees Negotiable Negotiable Sureties, co-debtor Negotiable Negotiable instruments instruments signature, pledges instruments instruments forbidden forbidden forbidden forbidden

Assignment of wages Assignment of wages Sureties, co-debtor Sureties, co-debtor Sureties, co-debtor Sureties, co-debtor signature, pledges signature, pledges, signature, pledges signature, pledges mortgage

19

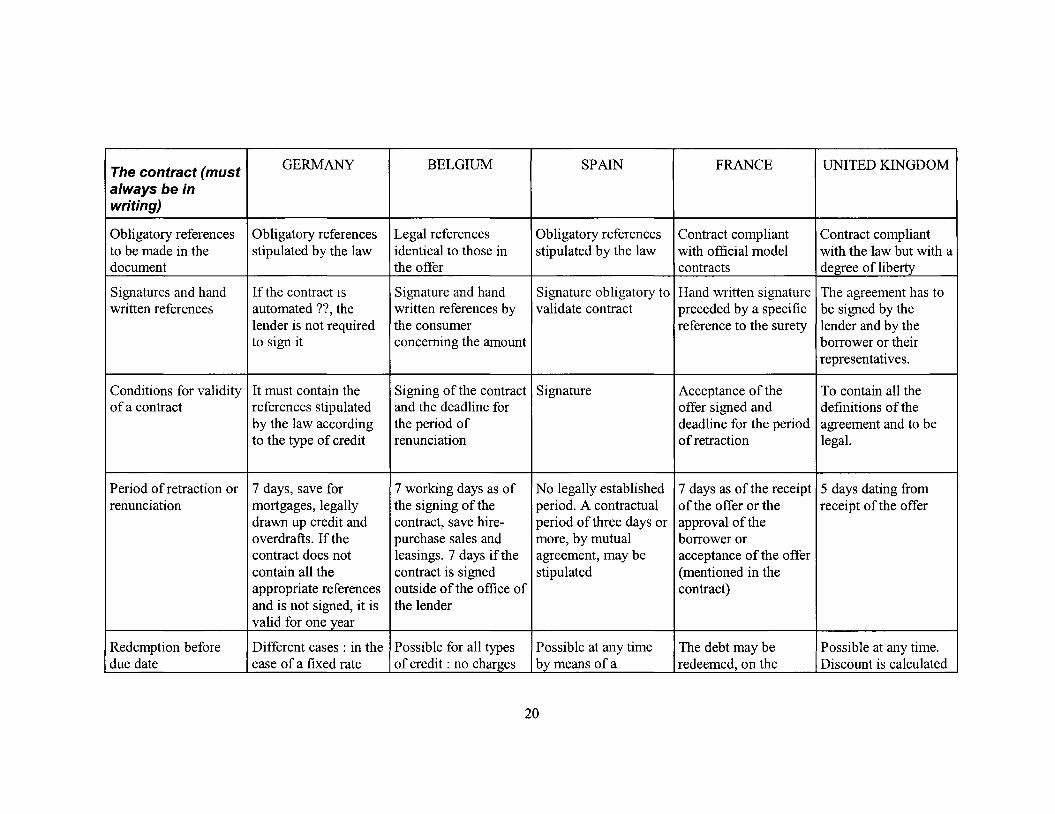

The contract (must GERMANY BELGIUM SPAIN FRANCE UNITED KINGDOM

always be in writing)

Obligatory references Obligatory references Legal references Obligatory references Contract compliant Contract compliant to be made in the stipulated by the law identical to those in stipulated by the law with official model with the law but with a document the offer contracts degree of liberty

Signatures and hand If the contract 1s Signature and hand Signature obligatory to Hand written signature The agreement has to written references automated ?? , the written references by validate contract preceded by a specific be signed by the

lender is not required the consumer reference to the surety lender and by the to sign it concerning the amount borrower or their

representatives.

Conditions for validity It must contain the Signing of the contract Signature Acceptance of the To contain all the of a contract references stipulated and the deadline for offer signed and definitions of the

by the law according the period of deadline for the period agreement and to be to the type of credit renunciation of retraction legal.

Period of retraction or 7 days, save for 7 working days as of No legally established 7 days as of the receipt 5 days dating from renunciation mortgages, legally the signing of the period. A contractual of the offer or the receipt ofthe offer

drawn up credit and contract, save hire- period of three days or approval of the overdrafts. If the purchase sales and more, by mutual borrower or contract does not leasings. 7 days ifthe agreement, may be acceptance of the offer contain all the contract is signed stipulated (mentioned in the appropriate references outside ofthe office of contract) and is not signed, it is the lender valid for one year

Redemption before Different cases : in the Possible for all types Possible at any time The debt may be Possible at any time. due date case of a fixed rate of credit : no charges by means of a redeemed, on the Discount is calculated

20

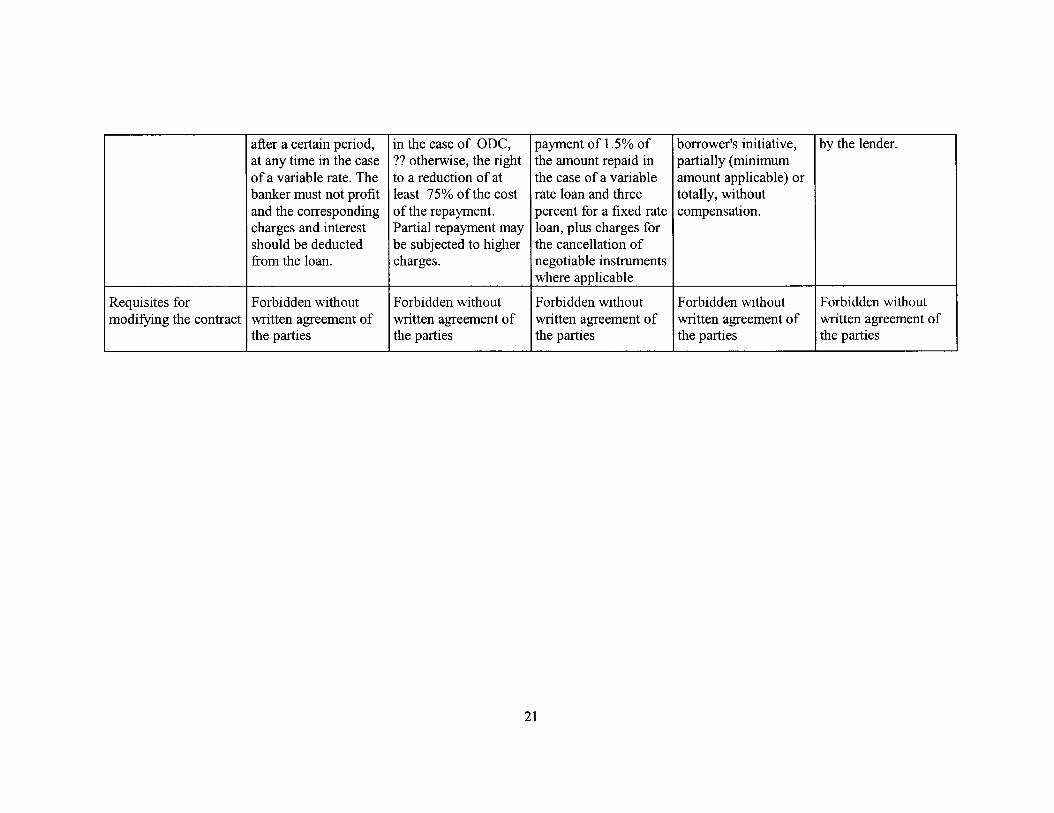

after a certain period, in the case of ODC, payment of 1.5% of borrower's initiative, by the lender. at any time in the case ?? otherwise, the right the amount repaid in partially (minimum of a variable rate. The to a reduction of at the case of a variable amount applicable) or banker must not profit least 75% ofthe cost rate loan and three totally, without and the corresponding of the repayment. percent for a fixed rate compensation. charges and interest Partial repayment may loan, plus charges for should be deducted be subjected to higher the cancellation of from the loan. charges. negotiable instruments

where applicable

Requisites for Forbidden without Forbidden without Forbidden without Forbidden without Forbidden without modifying the contract written agreement of written agreement of written agreement of written agreement of written agreement of

the parties the parties the parties the parties the parties

21

Life of the contract GERMANY BELGIUM SPAIN FRANCE UNITED KINGDOM

Information Account statement Account statement Account statement Monthly account Regular statements throughout the including credit Modification of statement including Response to all duration of the credit deducted, payments charges credit deducted, requests for facility made, interest and payments made, information by the

charges due interest and charges customer due

Modification of charges

The modification of Announced in writing Announced in writing Announced in writing Announced in writing Announced in writing rates on variable rate and the new rate can and the new rate and the new rate and the new rate and the new rate loans not be applied before cannot be applied cannot be applied cannot be applied cannot be applied

it ahs been reported to before it has been before it has been before it has been before it has been the customer reported to the reported to the reported to the reported to the

customer customer customer and accepted customer by the borrower

Dealing with Contact the lender to Contact the lender to Contact the lender to Contact the lender to Contact the lender to temporary difficulties seek an amiable seek an amiable seek an amiable seek an amiable seek an amiable

solution solution solution solution solution

If the lender reacts to a If the lender reacts to a If the lender reacts to a If the lender reacts to a The law gives free default on a payment, default on a payment, default on a payment, default on a payment, reign to clauses charges will be charges will be charges will be charges will be regarding default. applied. An amiable applied. An amiable applied. An amiable applied. An amiable Certain contracts solution is always solution is always solution is always solution is always stipulate that a single sought sought sought sought late payment is suffice

There are products to constitute a breach of the contract. Take which make explicit urgent measures in

22

provisions for case of temporary postponing a due date difficulties at the end of the contract

23

4. Going from one country to another

The single market provides credit institutions based in one country the possibility of offering their services throughout all the countries of the Union, within the framework of a provision known as the "free movement of services", established by European law.

Furthermore, the conventions of private international law, namely the Brussels Convention and the Rome Convention, govern the question of determining the law enforceable in the case of contracts entered into with consumers, that is, people acting outside the realm of professional activity.

Determining the law to be enforced in the case of a dispute arising from a credit agreement is of prime importance since, as we have just seen, legislation varies from country and country and the consumer is generally most familiar with the normal practice in his own country.

Accordingly, the two conventions mentioned above stipulate that if the contract entered into is preceded by a proposal or an advertisement received at the residence of the consumer, then the law which applies is that of the consumer's habitual residence, unless otherwise agreed by the parties. This situation is, as a general rule, the most favourable.

Given these conditions, if you sign a contract with a credit institution in another country keep all traces of such advertisements or proposals until the termination of the credit agreement.

It may also arise, however, that it is you who have taken the initiative and that you have chosen to contact a lender in another country. It would be wise in this case to pay special attention to the chief differences between your country of residence and that with which you are carrying out the credit operation.

24

Ifyoucome and go to BELGIUM SPAIN FRANCE UNITED KINGDOM from: =>

You will find more formalities, You will find less protectiOn m You will find more formalities, You will find that there is greater

GERMANY including in the case of a legal certain areas : negotiable including in the case of a legal freedom in the practices of the dispute instruments to guarantee credit, dispute lender or the intermediaries

Your rights are guaranteed by contracts which cannot be pulled

Your rights are guaranteed by The lenders consult a large out of, obscure contracts, link

The method of calculating longer periods (validity and

between credit and purchase, longer periods. Documents are number of positive public and

renunciatwn) and more precise more precise. Several consumer pnvate files provisiOns and informatiOn.

wh1le you will find more m organisations spec1ahse in credit

the effective rate is specific others : longer period of validity,

and you will find euro-guichets Credit mstltutwns are bound by

There are only negative files more ease in redemption before codes of good conduct rather

You may be faced with due date There are only negative files than restrictive legislation

to Germany and cannot be intermediaries who omit to give You may be advised by official Dealings with intermediaries are You will obtain credit more you or ask you for information, intermediaries. The commission rare easily even 1f you have financial

directly compared with the but under no circumstances is at your expense but paid by the You will not be able to make a

difficulties, but it may be at a should you pay them lender and deducted from the

direct comparison between the very high cost as there is no strict

other countries You will not be surprised by the loan granted.

effective rate in your country and defimtion of exorbitant rates

request regarding the assignment In the case of hire purchase you Germany, the methods of Redemption before due date is of wages as a guarantee are less protected in the event of calculation are different. possible at any time by means of

You will be offered credit legal actwn Usurious rates are capped by the a discount

facilities with greater ease, but Consumer organisations law.

overdrafts equal to three month's specialising in financial services You will not be asked to approve wages are less systematic, like are generally less well equipped the assignment of your wage to the depositing organisations and less efficient. secure credit

The rates are capped by the law Fmanc1al organisations are most You will find it easier to redeem often available at the point of your debt before the due date sale which is without compensation

There are only negative files and can be done at any time

save when the operation exceeds 1 million pesetas

25

lfyoucome and go to GERMANY SPAIN FRANCE UNITED KINGDOM from: =>

There is a positive file consulted You will find official There are generally many You will find that there is greater

BELGIUM before the making of an offer intermediaries offering more similarities in practices between freedom in the practices of the

The validity and renunciation guarantees and advice France and Belgium, however, lender or the mtermediaries

consumer credit is even more period is shorter The validity periods are shorter

codified in France. Standard The lenders consult a large

Credit insurers are specific Consumer organisations keep a and the contract may not offer

contracts are set out by the number of positive public and

close check on credit mstitutwns any possibility of cancellatiOn.

administration. pnvate files

to Belgium and are not and have powerful and efficient The texts are more obscure Lending organisations will not

Credit institutions are bound by means of exerting pressure codes of good conduct rather

You will not be asked for access ask for the assignment of your than restrictive legislation

found in any of the They are independent, subsidised to your wages as a guarantee but wage to guarantee a loan. by the States and will invoice may be asked for negotiable

You will not find intermediaries You will obtain credit more

you for their advice instruments easily even if you have financial countries opposite

You will find intermediaries with You will also find Test Achat but Consumer organisations are difficulties, but it may be at a

whom a written contract must be consumer organisations are greater in number and several very high cost as there is no legal

drawn up generally less specialised in specialise in financial services. cap on rates.

You only have to pay them if financial services and less You will also find local editions Lending orgamsations will not

you have obtained credit but equipped to advise you or defend of Test Achat ask for the assignment of your

may have to reimburse their you wage to guarantee a loan.

expenses There are less financial The period of reflection is

You will find it less easy to organisations lending direct, they slightly shorter are more often found in sales

redeem your debt before the due outlets As a general rule the legal date ; it may cost you less provisions provide less direct

Lenders are less inclined to offer You are less protected in the case protection.

you credit arrangements and of hire purchase

The consumer organisations are offer more overdrafts competent as to the financial and

credit matters

26

lfyoucome and go to GERMANY BELGIUM FRANCE UNITED KINGDOM from: =>

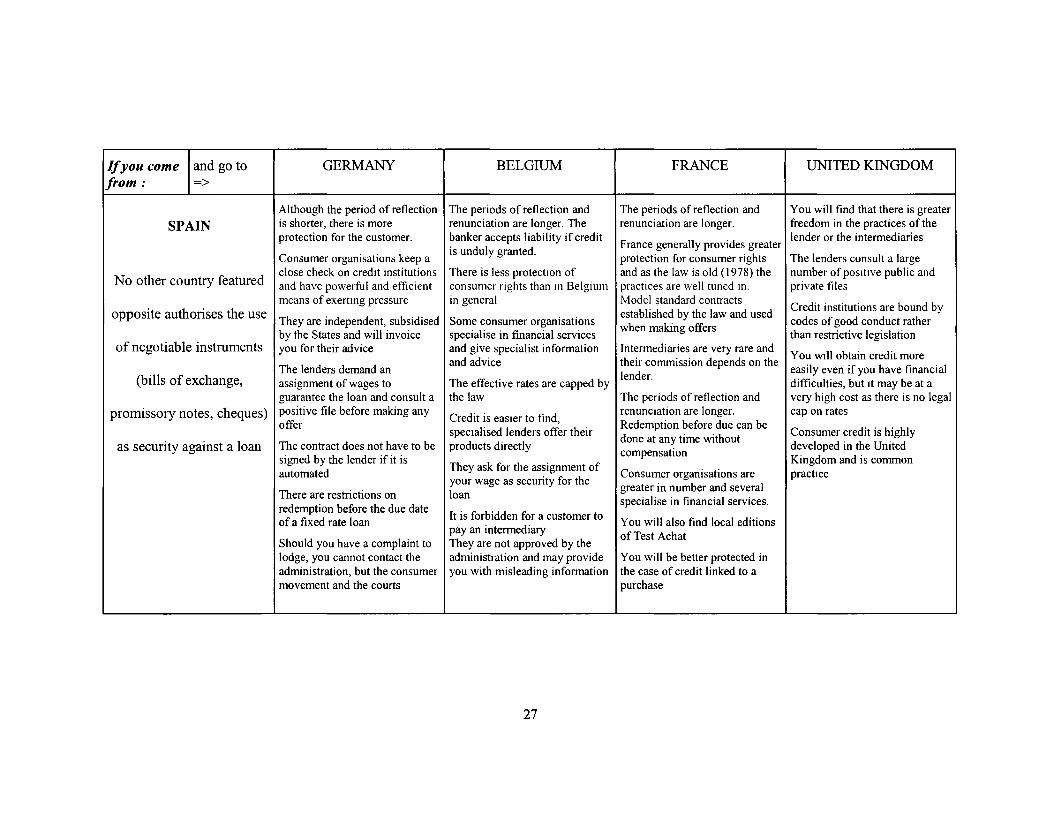

Although the period of reflection The periods of reflection and The periods of reflection and You will find that there is greater

SPAIN is shorter, there is more renunciation are longer. The renunciation are longer. freedom in the practices of the protection for the customer. banker accepts liability if credit

France generally provides greater lender or the intermediaries

Consumer organisations keep a is unduly granted.

protection for consumer rights The lenders consult a large

No other country featured close check on credit mstitutions There is less protectiOn of and as the law is old (1978) the number of positive public and and have powerful and efficient consumer rights than m Belgium practices are well tuned m. private files means of exertmg pressure in general Model standard contracts

Credit institutions are bound by opposite authorises the use They are independent, subsidised Some consumer organisations

established by the law and used codes of good conduct rather

by the States and will invoice specialise in financial services when making offers

than restrictive legislation of negotiable instruments you for their advice and give specialist information Intermediaries are very rare and

You will obtain credit more The lenders demand an

and advice their commission depends on the easily even if you have financial

(bills of exchange, assignment of wages to The effective rates are capped by lender.

difficulties, but It may be at a guarantee the loan and consult a the law The periods of reflection and very high cost as there is no legal

promissory notes, cheques) positive file before making any Credit is easier to find,

renunciation are longer. cap on rates offer

specialised lenders offer their Redemption before due can be

Consumer credit is highly as security against a loan The contract does not have to be products directly

done at any time without developed in the United compensation

signed by the lender if it is They ask for the assignment of

Kingdom and is common automated Consumer organisations are practice

your wage as security for the greater in number and several

There are restrictions on loan redemption before the due date

specialise in financial services. It is forbidden for a customer to of a fixed rate loan pay an intermediary

You will also find local editions

Should you have a complaint to They are not approved by the of Test Achat

lodge, you cannot contact the administration and may provide You will be better protected in administration, but the consumer you with misleading information the case of credit linked to a movement and the courts purchase

27

lfyou come and go to GERMANY BELGIUM SPAIN UNITED KINGDOM from: =>

There is less legislatiOn and the The situation is very similar in The use of credit IS less codified, You will find that there is greater

FRANCE period of reflection and Belgium, but there is slightly the penods of reflection shorter, freedom in the practices of the renunciation is shorter less codification of practises and no period of renunciation. lender or the intermediaries

All lenders first consult a The lenders ask for the The practices are much more

The lenders consult a large recent than in France and

The method of calculatmg positive file and ask for the assignment of your wage as recourse to credit less developed. number ofpostt1ve public and assignment of your wage as security for the loan pnvate files security for the loan

There are intermediaries which Lenders can ask for negotiable

Credit mst1tutions are bound by the effective rate is very There are intermediaries who are the client is forbidden to pay.

instruments as security for the codes of good conduct rather

paid by the customer, subject to They are not approved by the loans

than restrictive legislation different in France and the signing of a credit agreement. administration and may provide You may be efficiently advised

You will obtam credit more The commission only has to be you with misleading information by the official intermediaries.

easily even if you have financial cannot be compared paid if credit is extended Their payment is at your expense

Redemption before due date is (included m the credit) difficulties, but it may be at a more costly in Belgium and may very high cost as there is no legal

directly with all the Consumer organisations keep a pose problems if it is a partial You are less protected in the case cap on rates. close check on credit institutions redemption of hire purchase

The period of reflection is and have powerful and efficient

countries means of exerting pressure There is less consumer slightly shorter protection.

They are independent, subsidised As a general rule the legal

by the States and w1ll invoice Consumer organisations provisions provide less direct

Redemption before due you for serviced provided specialising in financial services protection are generally less well equipped

There is no administration with and less efficient. date without compensation which you can lodge complaints

Financial organisations are most There are more restrictions on often available at the point of

is specific to France redemption before the due date sale of a fixed rate loan

28

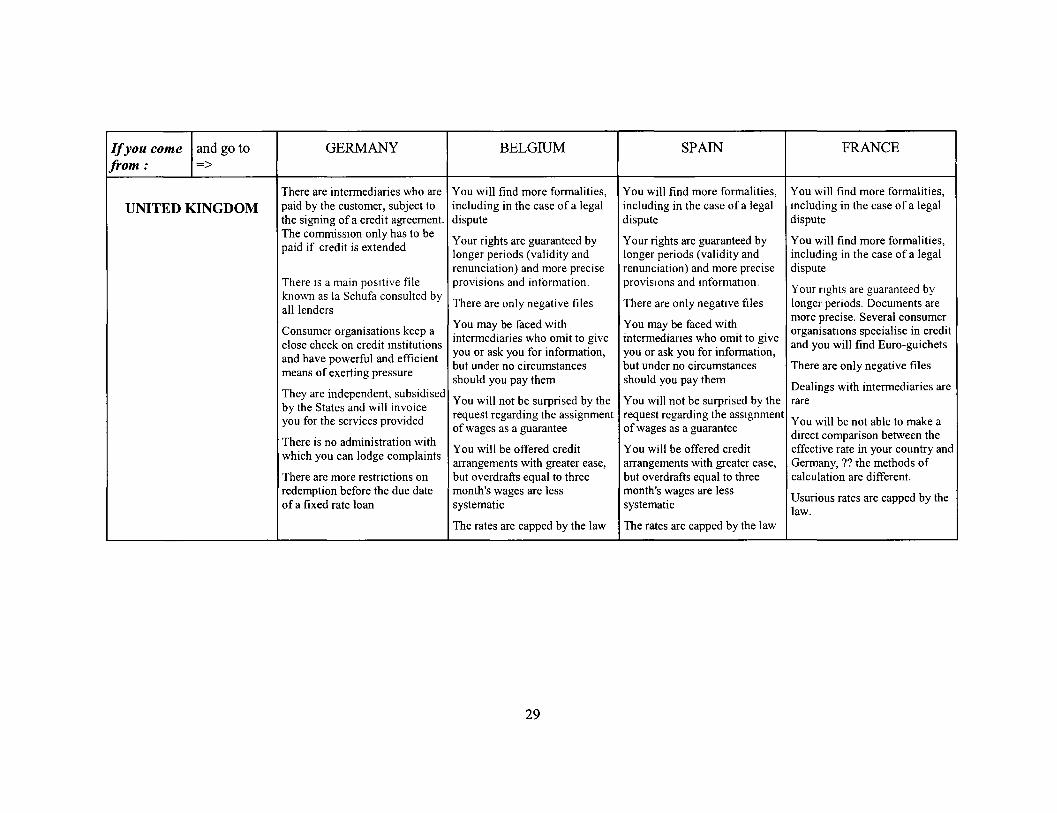

lfyou come and go to GERMANY BELGIUM SPAIN FRANCE from: =>

There are intermediaries who are You will find more formalities, You will find more formalities, You will find more formalities,

UNITED KINGDOM paid by the customer, subject to including in the case of a legal including in the case of a legal mcluding in the case of a legal the signing of a credit agreement. dispute dispute dispute The commissiOn only has to be

Your rights are guaranteed by Your rights are guaranteed by You will find more formalities, paid if credit is extended

longer periods (validity and longer periods (validity and including in the case of a legal renunciation) and more precise renunciation) and more precise dispute

There IS a main positive file provisions and information. provisiOns and informatiOn. Your nghts are guaranteed by

known as Ia Schufa consulted by all lenders

There are only negative files There are only negative files longer periods. Documents are

You may be faced with You may be faced with more precise. Several consumer

Consumer organisations keep a organisatiOns specialise in credit close check on credit mstitutions

intermediaries who omit to give intermedianes who omit to give and you will find Euro-guichets and have powerful and efficient

you or ask you for information, you or ask you for information, but under no circumstances but under no circumstances There are only negative files

means of exerting pressure should you pay them should you pay them

They are independent, subsidised Dealings with intermediaries are

by the States and will invoice You will not be surprised by the You will not be surprised by the rare

you for the services provided request regarding the assignment request regarding the assignment

You will be not able to make a of wages as a guarantee of wages as a guarantee direct comparison between the

There is no administration with which you can lodge complaints

You will be offered credit You will be offered credit effective rate in your country and arrangements with greater ease, arrangements with greater ease, Germany, ?? the methods of

There are more restrictions on but overdrafts equal to three but overdrafts equal to three calculation are different. redemption before the due date month's wages are less month's wages are less

Usurious rates are capped by the of a fixed rate loan systematic systematic

law. The rates are capped by the law The rates are capped by the law

29

5. Dealing with problems

There are several stages to dealing with problems.

The first, as we have seen, is to contact the credit grantor and seek an amiable solution with a commercial representative. Most problems are resolved in this way.

Yet, it may be that this does not suffice. Several options are open to you which make up a number of stages.

The first step is to take the case to the customer service department of the credit institution.

If that does not suffice or you require a more detailed decision, you may contact the establishment's arbitration board or the arbitration board linked to the profession, that is, the organisation representing the profession.

In France, the establishments bearing the certificate of quality are bound by the related convention which foresees recourse to a specific arbitrator, the decision of which they undertake to respect.

In certain countries public administration services receive and deal with complaints or requests for information. Such services are generally to be found in the Ministry of Finance (Belgium), at the DGCCRF (in France) or at the Central Bank (Spain).

There are consumer organisations in all the countries, which provide information, advice, and legal assistance in case of difficulties. Some are entirely free of charge, others simply ask for a subscription fee, while others only provide services against payment. In certain countries such associations may assist consumers fighting court cases or may guide them towards such assistance. Organisations specialising specifically in the assistance of indebted people can also be found in certain countries.

Some countries have arranged legal recourse to enable the parties to reach an out-of-court settlement with a magistrate.

In the event that all of the above solutions fail, the judicial stage remains, in which event the case is taken to court or submitted to the provisions for overindebtedness. People in great difficulty may have access tdegal aid.

30

Provisions to deal with overindebtedness exist in Germany (introduced in 1999), Belgium (introduced in 1999), France (introduced in 1989) and the United Kingdom (introduced in 1986).

The legal procedures and the ways of dealing withoverindebtedness differ from country to country. It is not the purpose of this guide to give specific details but to point out the existence of these differences.

In each country there are provisions to get access to the legal system that can be called upon by the magistrates, organisations or persons asked for assistance.

The legislation protects people by guaranteeing a minimum of persona-properties and income that is considered to be undistrainable.

The easing up on the access to credit and the economic difficulties have contributed to the fact that thousands of people in each and every country face excessive indebtedness.

31

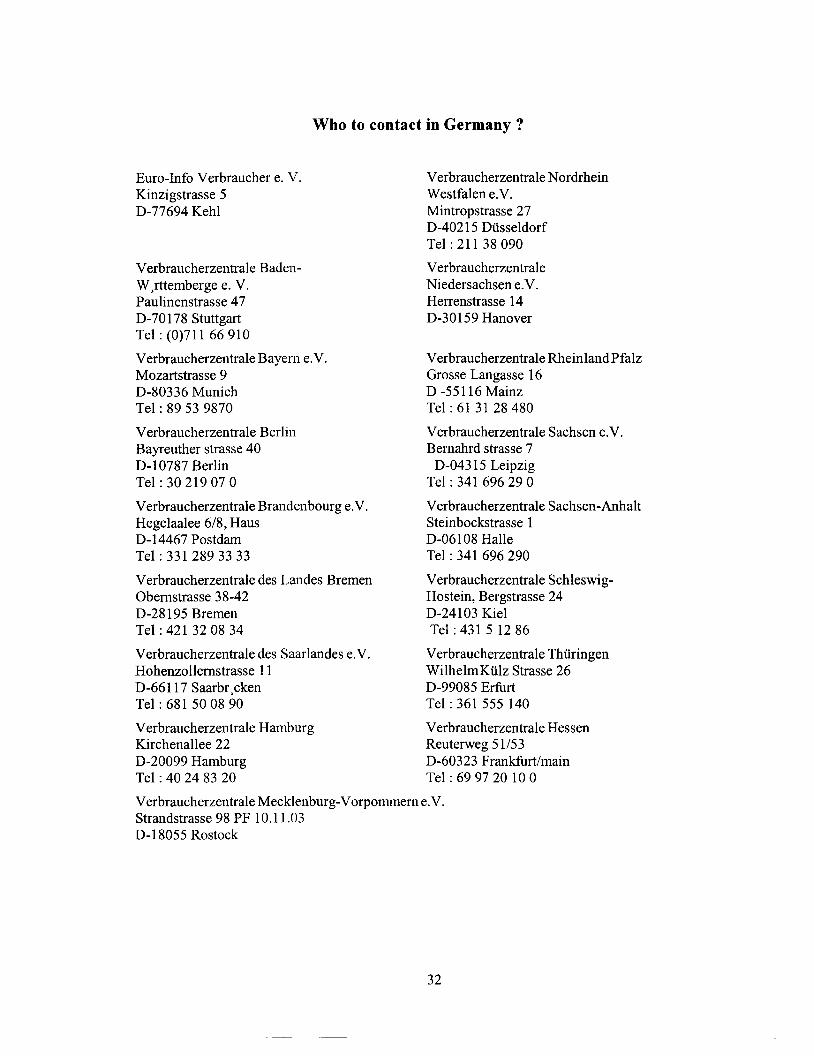

Who to contact in Germany ?

Euro-Info Verbraucher e. V. Kinzigstrasse 5 D-77694 Kehl

V erbraucherzentrale BadenW,rttemberge e. V. Paulinenstrasse 4 7 D-70 178 Stuttgart Tel: (0)711 66 910

V erbraucherzentrale Bay ern e. V. Mozartstrasse 9 D-80336 Munich Tel : 89 53 9870

Verbraucherzentrale Berlin Bayreuther strasse 40 D-1 0787 Berlin Tel:30219070

Verbraucherzentrale Branden bourg e.V. Hegelaalee 6/8, Haus D-14467 Postdam Tel: 331 289 33 33

V erbraucherzentrale des Landes Bremen Obernstrasse 38-42 D-28195 Bremen Tel: 421 32 08 34

Verbraucherzentrale des Saarlandes e.V. Hohenzollernstrasse 11 D-6611 7 Saarbr, cken Tel: 681 50 08 90

V erbraucherzentrale Hamburg Kirchenallee 22 D-20099 Hamburg Tel : 40 24 83 20

Verbraucherzentrale Nordrhein Westfalen e.V. Mintropstrasse 27 D-40215 Dusseldorf Tel: 21138 090

V erbraucherzentrale Niedersachsen e.V. Herrenstrasse 14 D-30159 Hanover

V erbraucherzentrale Rheinland Pfalz Grosse Langasse 16 D -55116 Mainz Tel: 61 31 28 480

Verbraucherzentrale Sachsen e.V. Bernahrd strasse 7

D-04315 Leipzig Tel: 341 696 29 0

V erbraucherzentrale Sachsen-Anhalt Steinbockstrasse 1 D-061 08 Halle Tel : 341 696 290

Verbraucherzentrale SchleswigHostein, Bergstrasse 24 D-24103 Kiel Tel:43151286

V erbraucherzentrale Thtiringen WilhelmKtilz Strasse 26 D-99085 Erfurt Tel: 361 555 140

V erbraucherzentrale Hessen Reuterweg 51153 D-60323 Frankfurt/main Tel : 69 97 20 10 0

Verbraucherzentrale Mecklenburg-Vorpommern e. V. Strandstrasse 98 PF 10.11.03 D-18055 Rostock

32

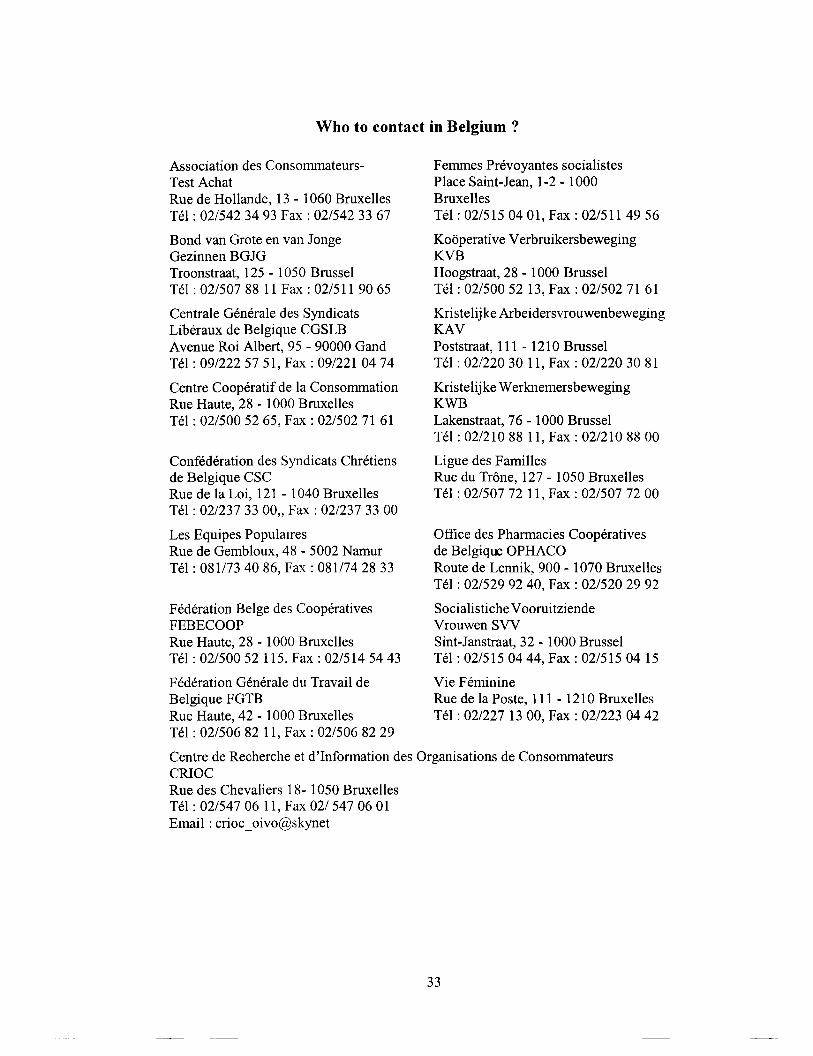

Who to contact in Belgium ?

Association des ConsommateursTest Achat Rue de Hollande, 13 - 1060 Bruxelles Tel : 02/542 34 93 Fax : 02/542 33 67

Bond van Grote en van Jonge Gezinnen BGJG Troonstraat, 125- 1050 Brussel Tel : 02/507 88 11 Fax : 02/511 90 65

Centrale Generale des Syndicats Liberaux de Belgique CGSLB Avenue Roi Albert, 95-90000 Gand Tel: 09/222 57 51, Fax: 09/221 04 74

Centre Cooperatif de la Consommation Rue Haute, 28 - 1000 Bruxelles Tel : 02/500 52 65, Fax : 02/502 71 61

Confederation des Syndicats Chretiens de Belgique CSC Rue de la Loi, 121 - 1 040 Bruxelles Tel : 02/237 33 00, Fax : 02/237 33 oo Les Equipes Populmres Rue de Gembloux, 48 - 5002 Namur Tel: 081/73 40 86, Fax: 081/74 28 33

Federation Belge des Cooperatives FEBECOOP Rue Haute, 28 - 1000 Bruxelles Tel: 02/500 52 115, Fax: 02/514 54 43

Federation Generale du Travail de Belgique FGTB Rue Haute, 42 - 1000 Bruxelles Tel: 02/506 82 11, Fax: 02/506 82 29

Femmes Prevoyantes socialistes Place Saint-Jean, 1-2- 1000 Bruxelles Tel: 02/515 04 01, Fax: 02/511 49 56

Kooperative Verbruikersbeweging KVB Hoogstraat, 28 - 1000 Brussel Tel: 02/500 52 13, Fax: 02/502 71 61

Kristelijke Arbeidersvrouwenbeweging KAV Poststraat, 111 - 1210 Brussel Tel : 02/220 30 11, Fax : 02/220 30 81

Kristelijke Werknemersbeweging KWB Lakenstraat, 76- 1000 Brussel Tel: 02/210 88 11, Fax: 02/210 88 oo Ligue des Families Rue du Trone, 127- 1050 Bruxelles Tel : 02/507 72 11, Fax : 02/507 72 00

Office des Pharmacies Cooperatives de Belgique OPHACO Route de Lennik, 900 - 1070 Bruxelles Tel : 02/529 92 40, Fax : 02/520 29 92

Socialistiche Vooruitziende Vrouwen SVV Sint-Janstraat, 32- 1000 Brussel Tel: 02/515 04 44, Fax: 02/515 04 15

Vie Feminine Rue de la Poste, 111 - 1210 Bruxelles Tel : 02/227 13 oo, Fax : 02/223 04 42

Centre de Recherche et d 'Information des Organisations de Consommateurs CRIOC Rue des Chevaliers 18- 1050 Bruxelles Tel: 02/547 06 11, Fax 02/ 547 06 01 Email : crioc _ oivo@skynet

33

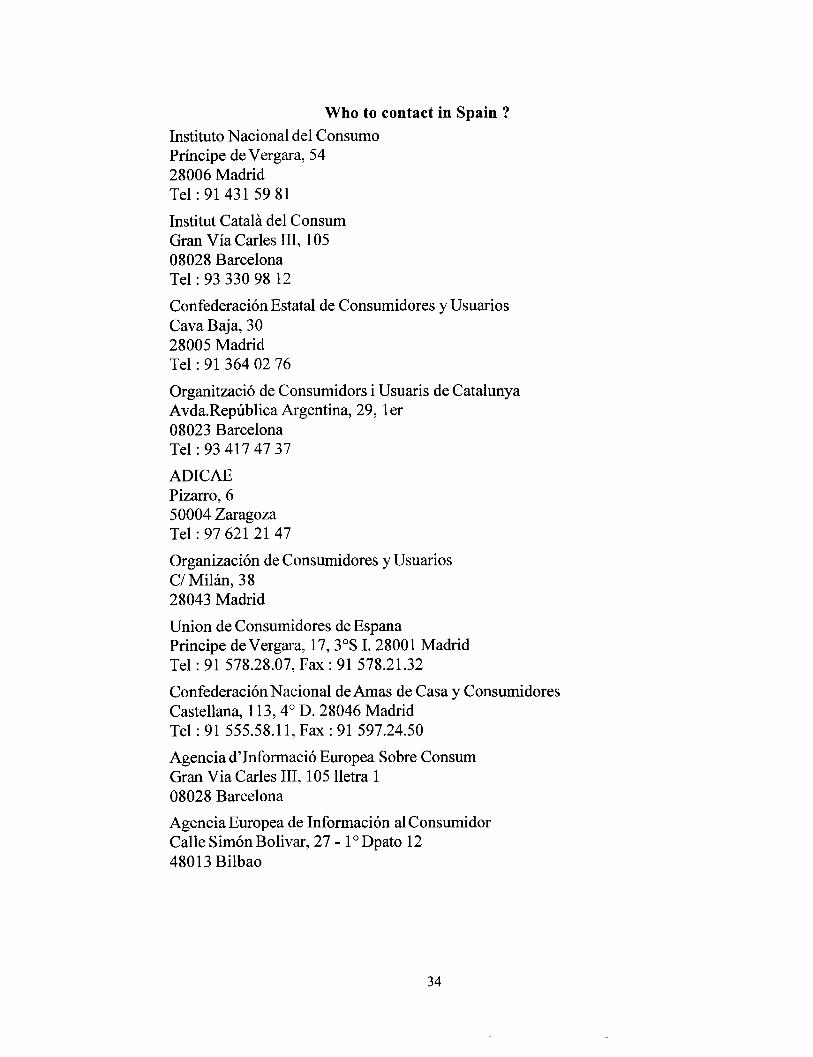

Who to contact in Spain ?

Instituto Nacional del Consumo Principe de Vergara, 54 28006 Madrid Tel: 91 431 59 81

Institut Catala del Consum Gran Via Carles III, 105 08028 Barcelona Tel: 93 330 98 12

Confederacion Estatal de Consumidores y Usuarios Cava Baja, 30 28005 Madrid Tel: 91 364 02 76

Organitzacio de Consumidors i Usuaris de Catalunya Avda.Republica Argentina, 29, 1er 08023 Barcelona Tel: 93 417 47 37

AD I CAE Pizarro, 6 50004 Zaragoza Tel: 97 621 21 47

Organizacion de Consumidores y Usuarios C/Mihin, 38 28043 Madrid

Union de Consumidores de Espana Principe de Vergara, 1 7, 3 os I. 2800 1 Madrid Tel: 91 578.28.07, Fax: 91 578.21.32

ConfederacionNacional deAmas de Casa y Consumidores Castellana, 113, 4° D. 28046 Madrid Tel: 91 555.58.11, Fax: 91 597.24.50

Agencia d'Informacio Europea Sobre Consum Gran Via Carles III, 105 lletra 1 08028 Barcelona

Agencia Europea de Informacion al Consumidor Calle Simon Bolivar, 27- 1 o Dpato 12 48013 Bilbao

34

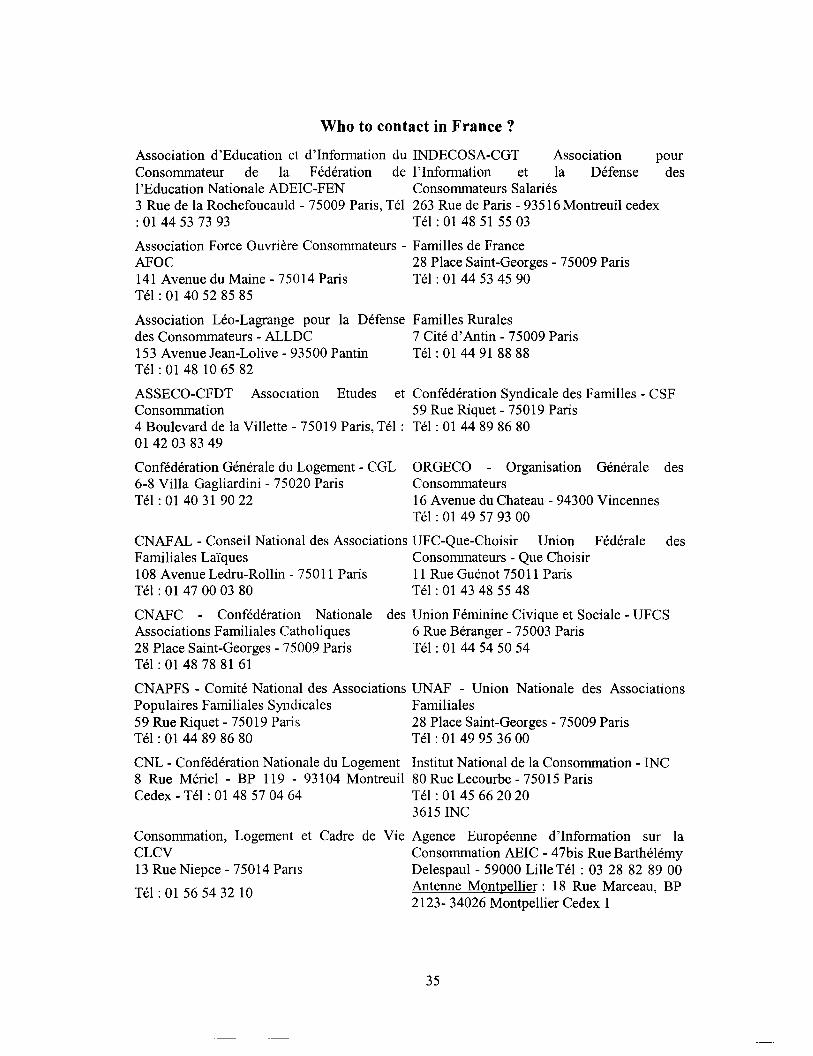

Who to contact in France ?

Association d'Education et d'lnformation du INDECOSA-CGT Association pour Consommateur de la Federation de !'Information et la Defense des !'Education Nationale ADEIC-FEN Consommateurs Salaries 3 Rue de la Rochefoucauld- 75009 Paris, Tel 263 Rue de Paris- 93516Montreuil cedex : 01 44 53 73 93 Tel: 01 48 51 55 03

Association Force Ouvriere Consommateurs - Families de France AFOC 28 Place Saint-Georges - 75009 Paris 141 Avenue du Maine- 75014 Paris Tel: 01 44 53 45 90 Tel : 01 40 52 85 85

Association Leo-Lagrange pour la des Consommateurs - ALLDC

Defense Families Rurales

153 Avenue Jean-Lolive- 93500 Pantin Tel: 01 48 10 65 82

7 Cite d'Antin -75009 Paris Tel : 01 44 91 88 88

ASSECO-CFDT Assoctation Etudes et Confederation Syndicale des Families - CSF Consommation 59 Rue Riquet- 75019 Paris 4 Boulevard de la Villette- 75019 Paris, Tel : Tel: 01 44 89 86 80 0142 03 83 49

Confederation Generale du Logement - COL 6-8 Villa Gagliardini- 75020 Paris Tel : 01 40 31 90 22

ORGECO - Organisation Generale des Consommateurs 16 Avenue du Chateau - 94300 Vincennes Tel: 01 49 57 93 oo

CNAF AL - Conseil National des Associations UFC-Que-Choisir Union Federale des Familiales Laiques Consommateurs - Que Choisir 108 Avenue Ledru-Rollin- 75011 Paris 11 Rue Guenot 75011 Paris Tel : 01 47 oo 03 80 Tel : 01 43 48 55 48

CNAFC - Confederation Nationale des Union Feminine Civique et Sociale - UFCS Associations Familiales Catholiques 6 Rue Beranger- 75003 Paris 28 Place Saint-Georges- 75009 Paris Tel : 01 44 54 50 54 Tel: 01 48 78 81 61

CNAPFS - Cornite National des Associations UNAF - Union Nationale des Associations Populaires Familiales Syndicales 59 Rue Riquet- 75019 Paris Tel: 01 44 89 86 80

Familiales 28 Place Saint-Georges- 75009 Paris Tel: 01 49 95 36 oo

CNL- Confederation Nationale du Logement 8 Rue Meriel - BP 119 - 93104 Montreuil Cedex- Tel: 01 48 57 04 64

Institut National de la Consommation- INC 80 Rue Lecourbe- 75015 Paris Tel: 01 45 66 20 20

Consommation, Logement et Cadre de CLCV 13 Rue Niepce- 75014 Pans

Tel : 01 56 54 32 10

3615 INC

Vie Agence Europeenne d'Information sur la Consommation AEIC - 4 7bis Rue Barthelemy Delespaul - 59000 Lille Tel : 03 28 82 89 00 Antenne Montpellier : 18 Rue Marceau, BP 2123-34026 Montpellier Cedex 1

35

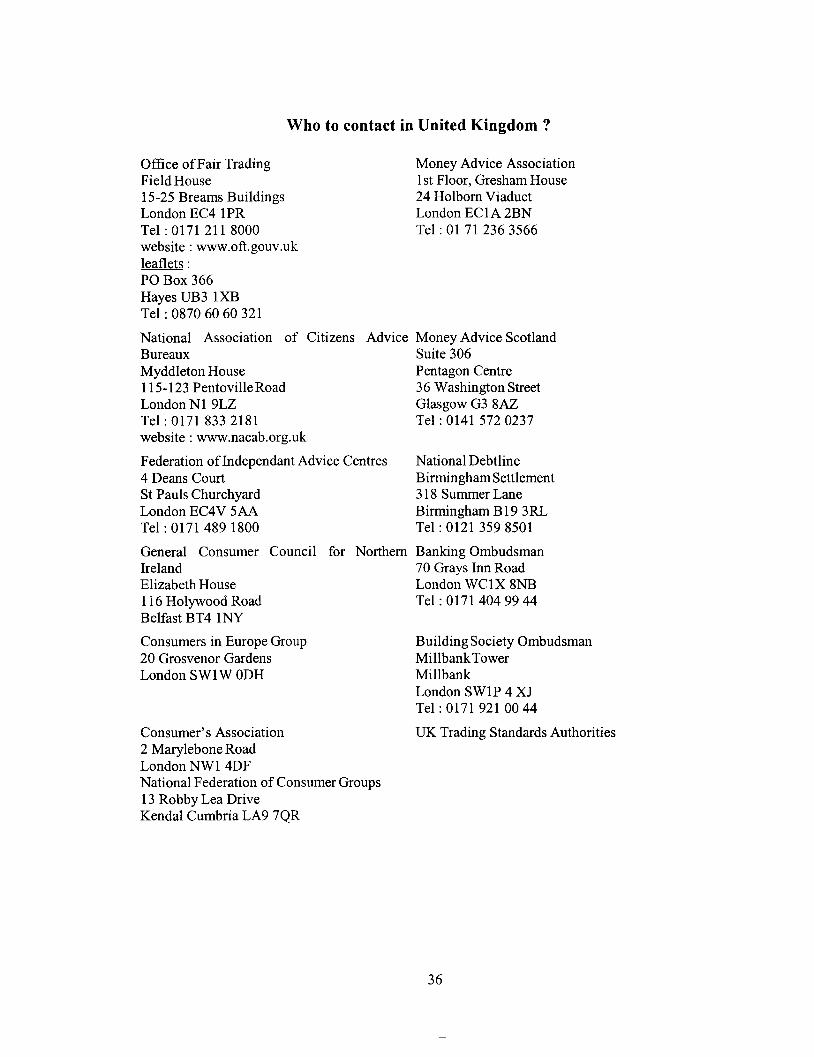

Who to contact in United Kingdom?

Office ofF air Trading FieldHouse 15-25 Breams Buildings London EC4 1PR Tel : 0171 211 8000 website : www.oft.gouv.uk leaflets: PO Box 366 Hayes UB3 lXB Tel: 0870 60 60 321

Money Advice Association 1st Floor, Gresham House 24 Holborn Viaduct London EC 1 A 2BN Tel : 01 71 236 3566

National Association of Citizens Advice Money Advice Scotland Bureaux Suite 306 Myddleton House Pentagon Centre 115-123 PentovilleRoad 36 Washington Street London Nl 9LZ Glasgow G3 8AZ Tel: 0171 833 2181 Tel: 0141 572 0237 website: www.nacab.org.uk

Federation oflndependant Advice Centres 4 Deans Court St Pauls Churchyard London EC4V 5AA Tel : 0171 489 1800

General Consumer Council for Northern Ireland Elizabeth House 116 Holywood Road Belfast BT4 1NY

Consumers in Europe Group 20 Grosvenor Gardens London SWl W ODH

Consumer's Association 2 Marylebone Road London NWl 4DF National Federation of Consumer Groups 13 Robby Lea Drive Kendal Cumbria LA9 7QR

National Debtline Birmingham Settlement 318 Summer Lane Birmingham B19 3RL Tel: 0121 359 8501

Banking Ombudsman 70 Grays Inn Road London WClX 8NB Tel: 0171 404 99 44

Building Society Ombudsman MillbankTower Mill bank London SWlP 4 XJ Tel: 0171 921 00 44

UK Trading Standards Authorities

36