Embed Size (px)

Citation preview

© Copyright FocusROI Inc. 2012 www.focusroi.com

CPEM 2012

Updates to CPEM Forms

Stuart Hartley FCA

© Copyright FocusROI Inc. 2012 www.focusroi.com

Agenda

C·PEM 2012

Letters

NFPO

Form Changes

Issues raised on existing forms

Overview of Key Changes

Questions?

© Copyright FocusROI Inc. 2012 www.focusroi.com

C·PEM 2012

Volume 1 Core concepts

Audits, reviews and compilations

Volume 2 Practical Guidance

Includes 2 integrated case studies

Part A Audits

Part B Reviews

Part C Compilations

Part D Practice Aids

(forms, etc. on a CD)

© Copyright FocusROI Inc. 2012 www.focusroi.com

C·PEM Case Studies

Case Study A Cambridge Furniture Inc.

─ Case Study B Kennedy & Co.

─

Business Furniture manufacturing

$1.5 million $ 230,000

10 2 + owner

Sales

Staff

Furniture manufacturing

Sample audit documentation provided (C-PEM Volume 2)

Primarily standard C-PEM

forms

Primarily memos to file

and condensed C-PEM forms

© Copyright FocusROI Inc. 2012 www.focusroi.com

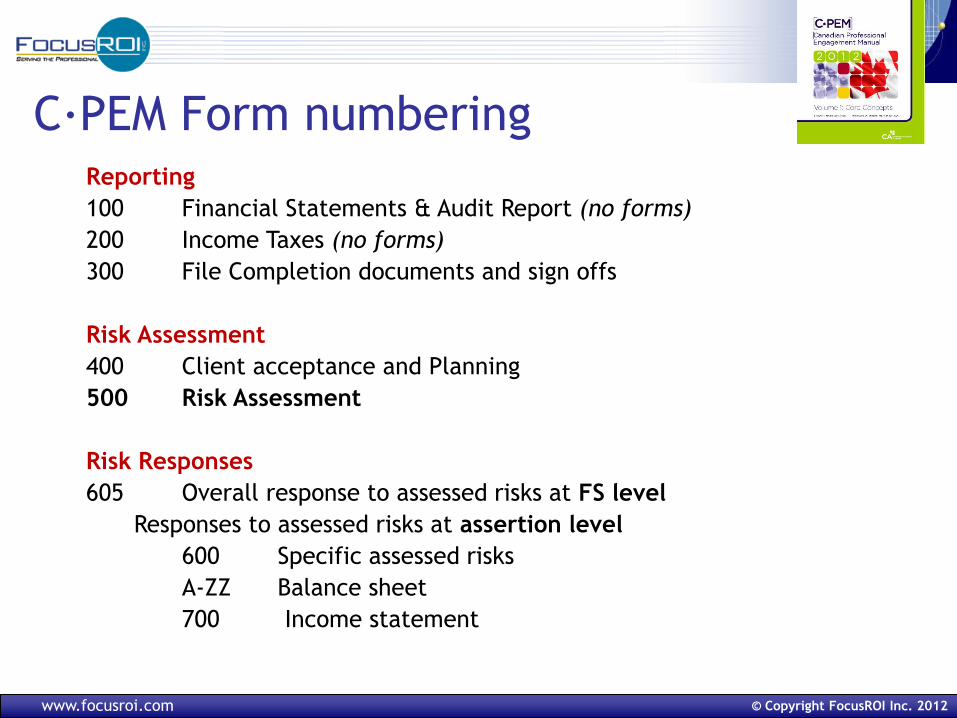

C·PEM Form numbering Reporting

100 Financial Statements & Audit Report (no forms)

200 Income Taxes (no forms)

300 File Completion documents and sign offs

Risk Assessment

400 Client acceptance and Planning

500 Risk Assessment

Risk Responses

605 Overall response to assessed risks at FS level

Responses to assessed risks at assertion level

600 Specific assessed risks

A-ZZ Balance sheet

700 Income statement

© Copyright FocusROI Inc. 2012 www.focusroi.com

C·PEM 2012

The Good News

No substantive changes

made this year to the

CASs

The Bad News

Understanding of certain CAS

requirements still not well

understood

Non compliance with CASs in

key audit areas is still being

identified

© Copyright FocusROI Inc. 2012 www.focusroi.com

Those !!!!!! C·PEM forms

© Copyright FocusROI Inc. 2012 www.focusroi.com

Why so many C·PEM Forms?

© Copyright FocusROI Inc. 2012 www.focusroi.com

Design of C-PEM Forms

FAQ Responses

Purpose ? S tructure for d ocument ing work per formed Assistance in complying with CAS requirements

T r aining required ? Yes . Forms are not a substitute for reading CASs

Ease of use ? Forms have objectives , instructions and consider points to facilitate ease of use

Why d a ta base s instead of checklist s ?

Enables quick and consistent assessments of risk

Enables r e-use of forms (cost saving) by updating the data in subsequent years

How easy t o review? The databases (su ch as risk registers) are structured to facilitate file review

What are CPEM “ Worksheets ” ?

U s e ONLY when applicable

© Copyright FocusROI Inc. 2012 www.focusroi.com

Levels of Audit Documentation

Standard CPEM Forms

Condensed CPEM Forms

StructuredMemos to file

ObjectivesInstructionsCAS requirementsConsider pointsComprehensive

Objectives

SummarizedCAS requirements

Custom

© Copyright FocusROI Inc. 2012 www.focusroi.com

Deciding

What

C·PEM

Forms to

use

© Copyright FocusROI Inc. 2012 www.focusroi.com

Structured Memos

Information captured in the same way (format) for

EVERY firm engagement. Should include:

Objectives and CAS(s) addressed

The work performed

Findings and conclusions

Implications for (and cross references to) other work performed

Need for Structure:

Ensure CAS requirements are not missed

Ease of review by manager/partner

Consider using the relevant C-PEM form for guidance

See the Case Study Examples in CPEM Volume 2

© Copyright FocusROI Inc. 2012 www.focusroi.com

What’s New in C·PEM 2012

1. Updated guidance and illustrations

2. Over 50 New/Revised Sample Letters

3. F/S disclosure checklist for NPO’s

4. New/revised assurance forms addressing

Risk Assessment Procedures

Entity Level Controls

Further Audit Procedures

Review Engagement Procedures

5. Completed Updated forms in case studies

© Copyright FocusROI Inc. 2012 www.focusroi.com

New Audit Process Diagram

Risk Assessment

Preliminary engagement

activities

Materiality for planning and scoping

Team Discussions

Result

Assessed RMM* at..

Assessed RMM* at..

FS** level

FS** level

Assertion level

Assertion level

Design/implement appropriate responses to assessed risks

Overall Responses Further Audit

Procedures

Substantive procedures

Tests of detail

Substantive analytical

Tests of control

Consider: - Professional skepticism

- Level of staff assigned - Extent of staff supervision - Accounting policies used - Unpredictable procedures - Extra further procedures

Sufficient appropriate audit evidence ( to reduce audit risk to an acceptably low level)

Result Result

File assembly and review(s)

Opinion on the FS**

Reporting Risk Response

Identify/assess RMM* in FS** (business and fraud risks) including relevant internal controls

* RMM = Risks of Material Misstatement ** FS = Financial Statements

Pervasive risks Specific risks

Communicate/discuss:

- Significant audit findings/ control deficiencies

- Significant difficulties encountered - Uncorrected Misstatements identifiedt

- Significant conclusions reached - Evaluation of uncorrected misstatements

- Results of final analytical procedures - Basis for forming the audit opinion

Consider:

- Need (if any) for additional procedures - Written representations received

- FS** presentation and disclosures - Adequacy of “two way” communication

Document:

© Copyright FocusROI Inc. 2012 www.focusroi.com

New/Revised Sample Letters

Preliminary Engagement Activities 8

Communications with Component

Auditors 2

Communications with TCWG 4

Management representations etc. 2

Confirmation Letters 14

Requests and Inquiries 14

Review Engagements 7

Compilation Engagements 2

© Copyright FocusROI Inc. 2012 www.focusroi.com

F/S Disclosure Checklists

NEW – FRF971 - Addresses first-time adoption of CICA

Handbook Part III – Accounting Standards for Not-for-

Profit Organizations (ASNFPOs)

NEW – FRF972 – Supplementary checklist to address

disclosures required under Part III, ASNFPOs.

Uses Part II (ASPE) as the base framework

FRF 905-913 (ASPE) to be used as applicable.

Disclosure checklists do NOT address PSAS requirements

© Copyright FocusROI Inc. 2012 www.focusroi.com

2012 C·PEM Form changes

To Address 6 Common Audit Weaknesses

1. Performing Risk Assessment Procedures

2. Evaluating Internal Control

3. Assessing/responding to RMM at the F/S level

4. Use of Assertions

5. Responding to assessed risks at the assertion level

6. Insufficient work on the Income Statement

© Copyright FocusROI Inc. 2012 www.focusroi.com

Preliminary engagement

activities

Materialityfor planning and scoping

Team Discussions

Result

Assessed RMM* at..

FS** level Assertion level

Identify/assess RMM* in FS** (business andfraud risks) including relevant internal controls

Pervasive risks Specific risks

What is

involved

in Risk

Assessment 1. Preliminary

2. Materiality

3. Planning

4. RAPS

5. Internal control

6. Assessing risks at

the two levels

© Copyright FocusROI Inc. 2012 www.focusroi.com

Risk Assessment - Scope

© Copyright FocusROI Inc. 2012 www.focusroi.com

First identify risk source then

identify effects (potential

errors and fraud) in the F/S

The Six Specified Areas of

Understanding Entity

External(economy, industry

and regulatory)

Nature of entity(operations,

financing,structure,

governance)

Selection andapplication of

accountingpolicies

Internal/externalperformance

targets & indicators

Absence of relevant

Internal controls Map Risk Sourcesto Potential

Misstatements (errors/fraud)

in the F/S

Entity objectives &strategies

© Copyright FocusROI Inc. 2012 www.focusroi.com

C-PEM Forms - Planning

Planning - 400 series

Form # Name of form Year 1 Year 2 Year 3 Year 4

405-410

Client acceptance and

continuance Prepare Update Update Prepare

420 Materiality Prepare Update Update Prepare

590 Audit scoping Prepare Update Update Prepare

426 Planning RAPs Prepare Update Update Prepare

430 Overall Audit Strategy Prepare Update Update Prepare

436 Audit Team Discussions Prepare Prepare Prepare Prepare

© Copyright FocusROI Inc. 2012 www.focusroi.com

C-PEM Forms – RAPs and Results Risk Assessment - 500 series

Form # Name of form Year 1 Year 2 Year 3 Year 4

500

Observation and analytical

procedures Prepare Prepare Prepare Prepare

505

Inquiries of management

and others Prepare Prepare Prepare Prepare

510

Identifying risks through

understanding the entity Prepare Update Update Prepare

513

Understanding accounting

estimates Prepare Prepare Prepare Prepare

515

Understanding related

parties Prepare Update Update Prepare

520 Risk register— Business Prepare Update Update Prepare

522 Risk register — Fraud Prepare Update Update Prepare

525 Going concern Prepare Prepare Prepare Prepare

© Copyright FocusROI Inc. 2012 www.focusroi.com

Understanding the Entity - 510c

© Copyright FocusROI Inc. 2012 www.focusroi.com

The 5 step

Top Down

Approach

5. significant deficiencies in controlCommunicate

Understand Internal Control

1. Identify Relevant sRisk

What requireRMMmitigation control ?with s

Document the operation of‘relevant’ internal controls

Do controls identified in step 2exist and are in operation?

What mitigate RMM?controls(pervasive and transactional)

2. Assess Control Design

4. Document Relevant lsContro

3. Assess ControlImplementation

RMM = risks of material mistatement

© Copyright FocusROI Inc. 2012 www.focusroi.com

Significant Risks

The Risk Register

© Copyright FocusROI Inc. 2012 www.focusroi.com

Entity Level Controls Form 530

Additional instructions added to form plus conclusion to each risk factor

© Copyright FocusROI Inc. 2012 www.focusroi.com

Transactional Controls

© Copyright FocusROI Inc. 2012 www.focusroi.com

Assessing Risks at F/S Level 590

© Copyright FocusROI Inc. 2012 www.focusroi.com

Overall Responses Form 605

© Copyright FocusROI Inc. 2012 www.focusroi.com

Using Assertions in Auditing Combined Assertions used in C·PEM

Assertion Classes of

Transactions

Account Balances Presentation &

Disclosure

Completeness Completeness Completeness Completeness

Existence Occurrence Existence Occurrence

Accuracy Accuracy

Cut-off

Classification

Rights and

obligations

Accuracy

Rights and

obligations

Classification and

understandability

Valuation Valuation and

allocation

Valuation

© Copyright FocusROI Inc. 2012 www.focusroi.com

Two Approaches for Designing Procedures

By Over/under statement

Not focused

Can result in both over

and under auditing

Expensive

By Assertion

Highly Focused

Avoids under or over

auditing

Cost effective

© Copyright FocusROI Inc. 2012 www.focusroi.com

Risks at Assertion Level

© Copyright FocusROI Inc. 2012 www.focusroi.com

Design of Audit Response (606)

© Copyright FocusROI Inc. 2012 www.focusroi.com

Basic- (part of general)

© Copyright FocusROI Inc. 2012 www.focusroi.com

Address the First Primary Assertion

© Copyright FocusROI Inc. 2012 www.focusroi.com

Include Your Risk Response Procedures

© Copyright FocusROI Inc. 2012 www.focusroi.com

Then… the Next Primary Assertion etc.

© Copyright FocusROI Inc. 2012 www.focusroi.com

Do not forget the Income Statement

Understand

the

Revenue

and

Expense

streams

© Copyright FocusROI Inc. 2012 www.focusroi.com

Revenues Audit Program

Address

each primary

assertion and

insert your own

custom procedures

© Copyright FocusROI Inc. 2012 www.focusroi.com

Review Engagement Forms

Review forms have been revised to address:

Adoption of Part III, ASNFPOs

Common documentation and file deficiencies:

Management’s procedures for cut-off, inventory observation,

valuation, etc.,

Analytical review and variance analysis for material balances or

class of transactions.

Income statement analysis and assessing plausibility.

Streamline and conform existing forms to the CPEM format.

© Copyright FocusROI Inc. 2012 www.focusroi.com

Extra:

Listing of all the old and new CPEM forms

including:

Form renumbering

Extent of change (if any)

Comments on reasons for changes

© Copyright FocusROI Inc. 2012 www.focusroi.com

Key success factors:

1. A complete understanding of all CASs.

2. Development of a practice specialty

3. Customized checklists

4. Automating the audit practice.

Anatomy of a 12-Hour Audit of Micro-Entities Phil Cowperthwaite, FCA

Closing thought….

© Copyright FocusROI Inc. 2012 www.focusroi.com

Questions Please…

Contact us at

www.focusroi.com

We welcome your feedback (good and

bad) plus any ideas for improvement