Embed Size (px)

Citation preview

A holistic approach to NPL resolution

FinSAC workshop “How to resolve NPLs at banks – international experiences”

Karlis Bauze

Senior Financial Sector Specialist, FinSAC, World Bank Group

Kiev, Ukraine, September 11-12, 2018

A holistic approach

2

NPL resolution needs a holistic approach

• Only a coordinated work of private and public sector stakeholders could bring meaningful results in NPL reduction

• Banks have the primary responsibility in NPL resolution at individual level and should ensure time bound and efficient NPL workout

• Public sector authorities should set a comprehensive and clear framework for NPL reduction (workout) in the system in order to remove impediments for financial stability and economic growth

3

NPL resolution is a complicated task with many institutions involved

NPLs

Regulator

MoF

MoJ

MoE

Bank 1

Bank 2NPL

investors

Tax authorities

Others

External auditors

Accounting standard setters

• Regulator: regulation on credit risk, loan provisioning, migration of loans from NPL to performing category, income recognition on NPLs, NPL resolution targets per bank, collateral valuation

• MoF: usually a lead institution for the financial crisis resolution, tax legislation (CIT, PIT, VAT), other initiatives

• MoJ: corporate and personal insolvency laws, out-of-court resolution, bailiffs regulation, improvements in judicial system

• MoE: foreign investors, economic growth, SME loans

• Bank 1 and 2: provisioning of NPLs, internal NPL resolution (workout) units, multi-lender cases, financial statements are prepared in accordance with the applicable financial reporting framework

• NPL investors: access to market, availability of NPL servicing platforms, licensing, NPL pricing gap

• Others: the regulation of appraisers and methodology for the appraisal of immovable assets

• Tax authorities: tax debts, super-priority of claims

• External auditors: deliver quality bank audits which foster market confidence in banks’ financial statements and provide audited statements of corporations

• Accounting standard setters: deliver a set of accounting policies, valuation norms and disclosure requirements, based on which financial statements should be prepared

4

Different experiences with NPL resolution

5

• The economic and financial crisis hit many EU countries in 2008

• Latvia, Ireland, and Greece had IMF, EC, and ECB programs

• The countries chose to apply different crisis and economic resolution methods:• one of the most successful was in Latvia – quick

and decisive decisions with substantial short term“economic pain” (internal adjustment);

• Ireland started decisively but structural problems were deeper;

• Greece had substantial structural problems and opted for a slow reform process leading to protracted economic and financial difficulties.

• A holisctic approach to NPL resolution and ownership of reforms matter Source: IMF, Financial Soundness Indicators

NPL workout at the bank

6

How to organize an NPL workout at the bank

7

1. Developing and implementing a strategy for NPL reduction

2. Structuring the workout unit:

Centralized vs. decentralized

Hybrid

Bad bank

3. Staffing the unit:

Skills

Remuneration

Outsourcing

Workload

4. Written policy manual

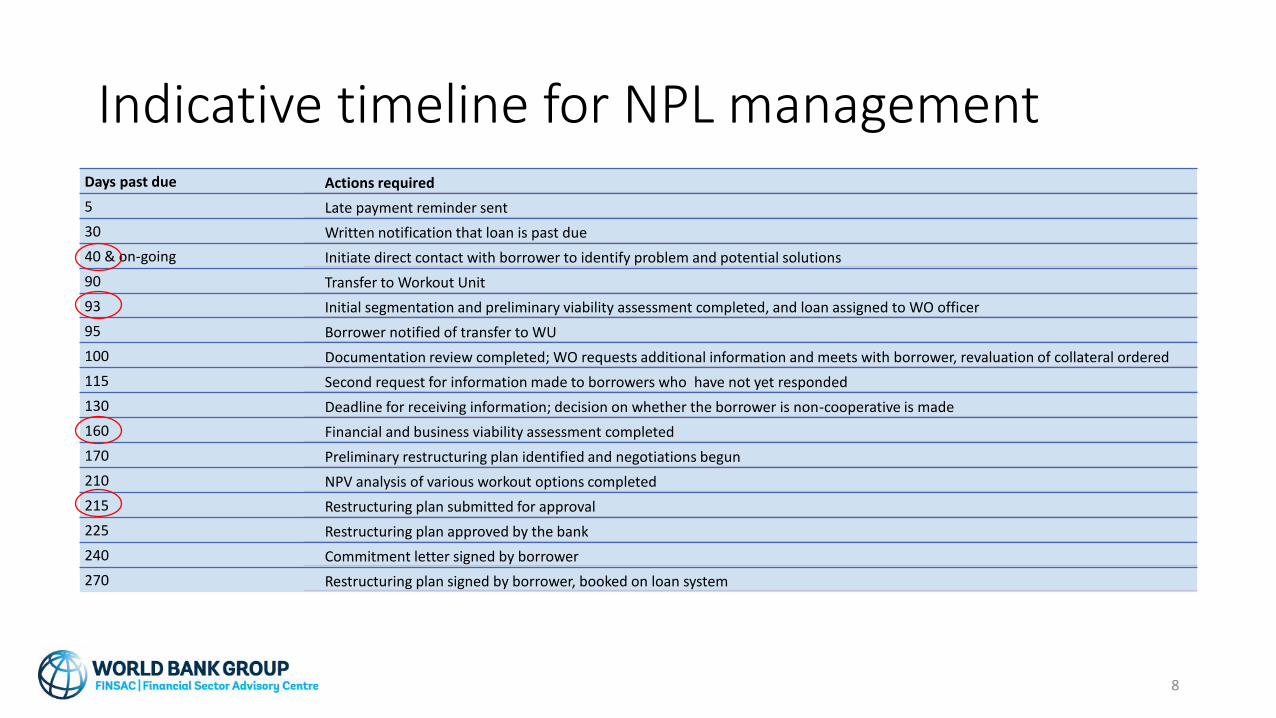

Indicative timeline for NPL managementDays past due Actions required

5 Late payment reminder sent

30 Written notification that loan is past due

40 & on-going Initiate direct contact with borrower to identify problem and potential solutions

90 Transfer to Workout Unit

93 Initial segmentation and preliminary viability assessment completed, and loan assigned to WO officer

95 Borrower notified of transfer to WU

100 Documentation review completed; WO requests additional information and meets with borrower, revaluation of collateral ordered

115 Second request for information made to borrowers who have not yet responded

130 Deadline for receiving information; decision on whether the borrower is non-cooperative is made

160 Financial and business viability assessment completed

170 Preliminary restructuring plan identified and negotiations begun

210 NPV analysis of various workout options completed

215 Restructuring plan submitted for approval

225 Restructuring plan approved by the bank

240 Commitment letter signed by borrower

270 Restructuring plan signed by borrower, booked on loan system

8

Stages of NPL resolution

9

Stages of NPL resolution

Timely recognition

Adequate provisioning

Segmentation

Targeted action

• Four basic NPL resolution blocs are essential for a successful tackling of impaired assets

• All of them require serious consideration

• Banks and regulators play crucial role in the resolution process

• The proper recognition and valuation of NPLs is bank’s primary responsibility

• Regulators should set an unambiguous framework for NPL resolution

• More prescriptive and intrisuve regulation is justified in case of a systemic NPL problem

10

Stages of NPL resolution – timely recognition

Timely recognition

Adequate provisioning

Segmentation

Targeted action

• The timely NPL recognition is done with the implementation of an early warning system (EWS) in banks

• The EWS aims to identify potential credit risks at an early stage (ex-ante, not ex-post) in order to apply pre-emptive remedial solutions as soon as possible

• Indicators: i) economic environment, ii) financial, iii) collateral and behavioral, iv) third party information, v) operational.

• IFRS 9 sets out a rebuttable presumption that the credit risk on a financial asset has increased significantly since initial recognition and requires the recording of lifetime expected credit losses for loans that are past due 30 days or more (stage 2). EWS should identify potential impaired loans, ideally substantially, before 30 days past due

• Identified potential problem clients should be channeled to pre-arrears or early-arrears units in banks and calls should be made to clarify for payment delay reasons

• Maximum time the borrower can remain on a watch list is six months

• The earlier difficulties are identified, the higher are chances that a mutually acceptable solution can be found

11

Stages of NPL resolution – adequate provisioning

Timely recognition

Adequate provisioning

Segmentation

Targeted action

• Loan loss provision is an expense set aside as an allowance for uncollected loans and loan payments

• Provisioning can be complex, with different interpretations in prudential regulation, local, and international accounting standards

• Provisioning should be timely and according to regulation, with realistic repayment and recovery expectations

• The calculation of loss given default (LGD) and assumptions about probability of deault (PD) should be based on historic performance (adjusted for the economic cycle)

• Appropriate provisioning has a significant influence on the development of an NPL market

• Insufficient provisioning is one substantial reason for pricing gaps (bid-ask spreads) in the NPL market

• A regulation on NPL write-offs helps addressing NPLs stock

12

Source: SEACEN Financial Stability Journal, Volume 7, published in December 2016

Stages of NPL resolution – segmentation (triage)

Timely recognition

Adequate provisioning

Segmentation (triage)

Targeted actions

• At the stage when problematic loans are transferred to bank’s internal or external workout unit, segmentation of loans according to specific criteria should be done in order to identify the most appropriate and cost efficient resolution strategy

• The most important segmentation criteria is viability (e.g., debt/EBITDA < 3; interest coverage ratio > 1.1)

• Additional segmentation criteria: i) days-past-due, ii) collateral type, iii) legal actions initiated, iv) regional distribution, iv) FX loans, and v) cooperative, non-cooperative borrower

13

Stages of NPL resolution – targeted action

Timely recognition

Adequate provisioning

Segmentation

Targeted action

• Depending on the materiality of impairment, loan resolution process includes six main actions: (i) forbearance, (ii) restructuring implementation in court, (iii) out-of-court settlement, (iv) collateral enforcement, (v) write-off, and (vi) sale

• To select the most cost efficient options, an NPV calculation should be done for all available options. The calculation must include all costs associated with the selected option, including the costs of the internal or external workout unit (e.g., internal - human resources, IT, legal expenses- or external – asset storage costs, advisory or other services)

• Depending on the bank’s NPL resolution strategy, it might conduct NPL workouts (i) internally; (ii) create external SPV; or (iii) outsource the process to a third party (with pre-determined profit sharing plan or investment contribution) or decide to sell all or part of its NPL portfolio

• Loan forbearance includes – interest only payment, reduced payments, balloon payments, conditional debt forgiveness

• Out-of-court settlement is reached among lender(s) and borrower without lengthy and costly judicial process

• Collateral enforcement envisages full or partial realization of the loan collateral

• As a consequence of write-off bank recognizes unrecoverability of a loan (IFRS 9 is silent about write-off rules)

• Credit files should be in good order and in digital format for the investors to be able to analyze them

14

Collateral valuation

15

Collateral valuation framework

16

• European Regulation No 575/2013 sets a minimum requirement for the European financial institutions

• Para 3 (a) of Article 208 states: “institutions monitor the value of the property on a frequent basis and at a minimum once every year for commercial immovable property and once every three years for residential real estate. Institutions carry out more frequent monitoring where the market is subject to significant changes in conditions”

• Para 1 of Article 229 states: “for immovable property collateral, the collateral shall be valued by an independent valuer at or at less than the market value. An institution shall require the independent valuer to document the market value in a transparent and clear manner”

• The definition of market value, according to TEGOVA, is: “The estimated amount for which the property should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without being under compulsion”

• IFRS 9 establishes the framework for valuation of financial instruments for accounting purposes. The standard requires that: “At initial recognition, an entity measures a financial asset or a financial liability at its fair value plus or minus, in the case of a financial asset or a financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset or the financial liability”

Collateral valuation approaches

17

• The latest EU regulation requires the recognition of NPL in full amount without accounting for collateral

• ECB supervisory expectations require a phase out of the amount of collateral used for provisioning purposes after a certain time

• ECB Guidance on NPLs explicitly forbids the use of the discounted replacement cost method for real estate valuation purposes

• Appraisal experts warn against different interpretations and uncertainty in the use of the term «yield» – it can be i) initial yield, ii) gross yield, iii) net yield, iv) all risks yield, v) equivalent yield, vi) equated yield

Market approach

Income approach

Cost approach

• Comparative method

• Capitalization method

• Discounting method

• Accounts of the current or a theoretical occupier

• Depreciated replacement cost method

• Residual method

Specifics of NPL resolution in Ukraine

18

Real case NPL resolution – Ukraine and Slovenia

19

• Options for NPL resolution should be considered on NPV basis

• In countries with high interest rates, time value is very important

• Insolvency is almost not an option in Ukraine• The calibration of discount rate is a very sensitive issue

Option Slovenia Ukraine

Restructure 81,215 80,673

Loan Sale 82,500 73,500

Enforcement 54,881 34,673

Insolvency 61,955 8,584

Source: FinSAC calculations, based on the World Bank Doing Business index data 2017

Enabling environment for NPLs matter

20

Source: FinSAC calculations, based on the World Bank Doing Business index data 2018

POL

HUN

CZK

SLO

SLOVENEST

LAT

LIT

CRO

ROM

BUL

SER

BiH

MAC

KOS

MON

ALB

RUS

UKR

BEL

MOL

GEO

ARM AZE

GRE

CYPTRK

ECA

OECD

R² = 0.1442

0

5

10

15

20

25

30

35

40

45

0 20 40 60 80 100

Co

st (

% o

f e

stat

e)

Recovery rate

Recovery rate and cost of insolvency

POLHUN CZKSLO

SLOVEN

EST

LAT

LIT

CRO

ROM

BUL SERBiHMAC

KOS

MON

ALB

RUS

UKR

BEL

MOL

GEO

ARM

AZE

GRE

CYP

TRK

ECA

OECD

R² = 0.1148

0

300

600

900

1200

1500

1800

10 20 30 40 50

Tim

e (d

ays)

Cost (% of claim)

Time and cost of collateral enforcement

NPL framework assessment in Ukraine

▪ The assessment was based on the 3 pillar approach and 17 areas were analysed

▪ In this specific case, 11 areas were identified with negative scores above 3.5 (circled with red)

▪ Priority status of recommended improvements was assigned to these areas

Source: ECB Stocktake of national supervisory practices and legal frameworks related to NPLs, WB estimatesCharts interpretation: score 5 stands for the worst NPL framework, whereas 0 score stands the best practice NPL framework

21

Ukraine