Embed Size (px)

Citation preview

CORPORATE STRATEGY 2014 & FINANCIAL

PERFORMANCE AS AT DEC 2013 By: Hizamuddin Jamalluddin Head, Strategic Management & Managing Director’s Office

Strictly Private & Confidential

TABLE OF CONTENTS

Managing Director’s Office Page 2

Corporate Profiles

Business Operations

Financial Highlights

Corporate Strategic Plan

Sec 1

Sec 2

Sec 3

Sec 4

Managing Director’s Office Page 3

BANK ISLAM AT GLANCE

Managing Director’s Office Page 4

Malaysia’s 1st

Islamic bank Incorporated on 1 March

1983

134 branches nationwide with more than

1,200 self-service

terminals

Universal

licence able to offer commercial

and investment banking

activities all under one roof

>4,000 staff Top 50 Malaysia’s Most

Preferred Employers

Primarily a

retail bank with more than 70%

financing driven by

Consumer banking

Voted

Islamic Bank

of the Year by

The Banker in 2013

CORPORATE VISION

Managing Director’s Office Page 5

Value-Based Organization

TO BE A GLOBAL LEADER IN ISLAMIC BANKING

“Global Leader” is defined as being the ultimate

guidance and source of reference for innovative

Shariah-based products and services

MISSION STATEMENT

Managing Director’s Office Page 6

To continually develop and innovate universally

accepted financial solutions in line with Shariah principles

To provide a reasonable and sustainable return to shareholders

To provide a conducive working environment and to become an Employer of Choice for top talents in the market

To deliver comprehensive financial solutions of

global standards using state-of-the-art technology

To be a responsible and prudent corporate citizen

In carrying out this corporate mission, Bank Islam shall

be guided by its corporate brand values by being: A Leader, Dynamic, Professional, Caring and Trustworthy

CORPORATE VALUES

Managing Director’s Office Page 7

•Our Islamic products are the benchmark. Reputed as the pioneer in Islamic banking. Built the Islamic banking industry in Malaysia

Leader

•Progressive and innovative - constantly moving ahead, technologically advanced, with new products & services

Dynamic

•Fast, efficient and responsive service. Knowledgeable and equipped staff to handle global business challenges

Professional

•A supportive partner who is approachable, ever ready to provide solutions to your financial problems

Caring

•100% Shariah-based products, services and principles

Trustworthy

54.4% 9.98% 5.11% 5.05%

CORPORATE STRUCTURE @ MARCH 2014

Managing Director’s Office Page 8

100%

14.4%

GOVERNANCE STRUCTURE

Managing Director’s Office Page 9

BOARD OF DIRECTORS

Managing Director’s Office Page 10

SHARIAH SUPERVISORY COUNCIL ("SSC")

Managing Director’s Office Page 11

• Dr. Ahmad Shahbari

@ Sobri Salamon

Chairman • Datuk Mohd Bakir Mansor

• Assistant Professor Dr. Uzaimah Ibrahim

• Professor Dr. Ahmad Hidayat Buang

• Dr. Muhammad Syafii Antonio

• Mohd Nazri Chik

Secretary to SSC

SHARIAH GOVERNANCE FRAMEWORK

Managing Director’s Office Page 12

SHARIAH AS OVERARCHING PRINCIPLE IN BANK ISLAM

SHARIAH

SUPERVISORY COUNCIL (SSC) • Oversight accountability on Shariah related

matters.

BOARD OF

DIRECTORS (Overall oversight on Shariah governance structure & Shariah

compliance)

BOARD RISK COMMITTEE

AUDIT &

EXAMINATION COMMITTEE (AEC)

MANAGEMENT • Ensure execution of business & operations are in accordance with Shariah principles. • Provide necessary resources, infrastructure, enablers to the SSC.

Shariah Risk Management Control Function: Identify, measure, monitor, report & control Shariah non-compliance risk

Shariah Review Function: Review business operation on regular basis to ensure Shariah compliance.

Shariah Research Function: (under Product Development) Conduct in-depth Shariah research prior to submission to Shariah Committee.

Shariah Audit Function: Provide independent assessment & objective assurance designed to value add & improve Bank Islam adherence to Shariah

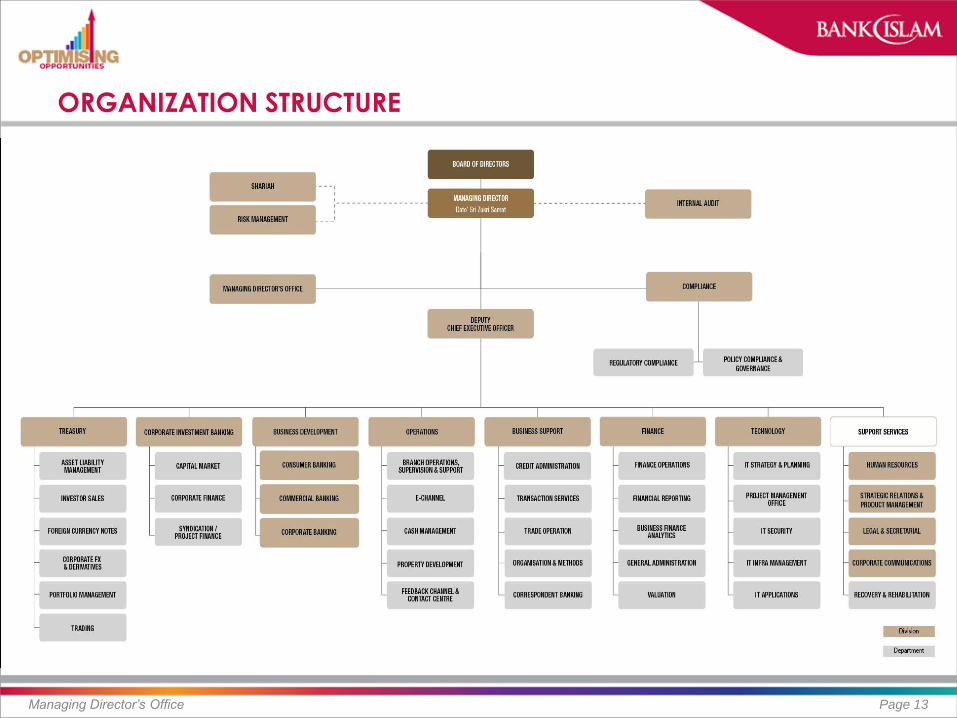

ORGANIZATION STRUCTURE

Managing Director’s Office Page 13

SENIOR MANAGEMENT

Managing Director’s Office Page 14

SENIOR MANAGEMENT

Managing Director’s Office Page 15

• Dato’ Sri Zukri Samat

Managing Director

• Hizamuddin Jamalluddin

General Manager /Head

Strategic Management &

Managing Director’s Office

• Maria Mat Said

General Manager/Head

Legal & Secretarial

cum Company Secretary

• Nik Azmir Nik Anis

Assistant General Manager/Head

Compliance

• Mohd Nazri Chik

General Manager/Head

Shariah

• Jeroen P.M.M. Thijs

Chief Risk Officer

• Mohamed Iran Moriff Mohd Shariff

Chief Internal Audit

SENIOR MANAGEMENT - BUSINESS

Managing Director’s Office Page 16

• Khairul Kamarudin

Director

Business Development

• Abdul Rashid Abdul Hamid

General Manager/Head

Commercial Banking

• Mujibburrahman Abd Rashid

General Manager/Head

Consumer Banking

• Norashikin Mohd Kassim

Director

Treasury

• Mashitah Osman

Director

Corporate Investment Banking

• Zaharin Mohd Ali

Assistant General Manager /Acting Head

Corporate Banking

SENIOR MANAGEMENT – OPERATION & SERVICES

Managing Director’s Office Page 17

• Wahid Ali Mohd Khalil

Chief Operating Officer

Business Support

• Dato’ Norasni Ayob

Chief Operating Officer

Operation

• Ryan Liew Choon Ching

Chief Technology Officer

• Malkit Singh Maan

Chief Financial Officer

• Jamilah Abdul Sallam

General Manager/Head

Human Resource

• Azmir Abdul Malik

Assistant General Manager/Head

Corporate Communication

• Dato’ Wan Ismail Wan Yusoh

General Manager/Head

Strategic Relations &

Product Management

• Mizan Masram

Assistant General Manager/Head

Recovery & Rehabilitation

Managing Director’s Office Page 18

BUSINESS

OPERATIONS

BUSINESS ACTIVITIES

Managing Director’s Office Page 19

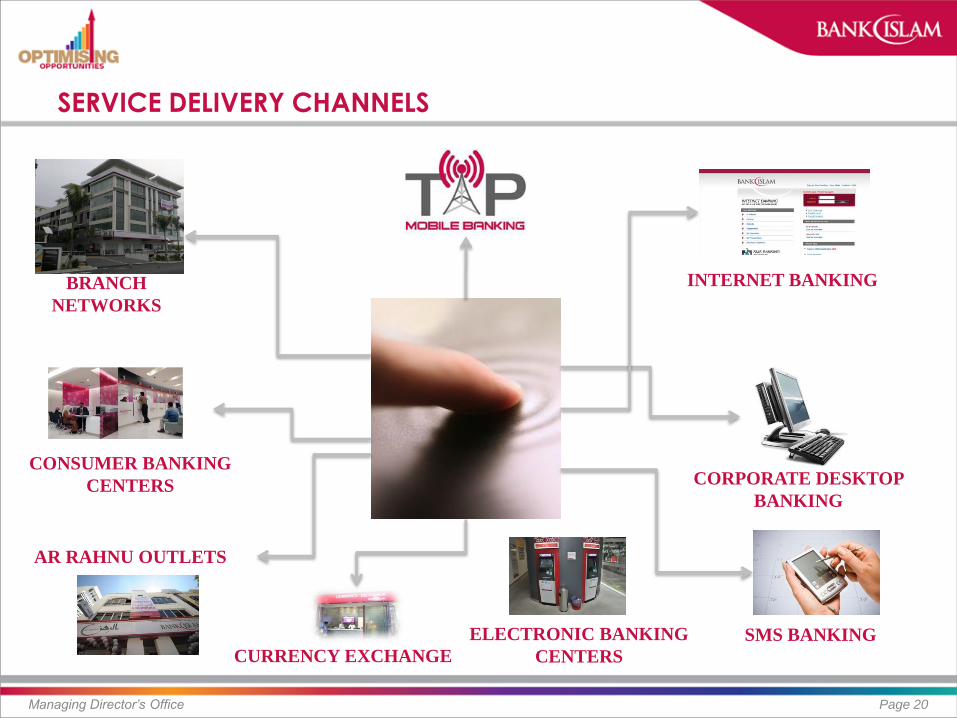

SERVICE DELIVERY CHANNELS

Managing Director’s Office Page 20

BRANCH

NETWORKS

INTERNET BANKING

CONSUMER BANKING

CENTERS

AR RAHNU OUTLETS

CURRENCY EXCHANGE

SMS BANKING

CORPORATE DESKTOP

BANKING

ELECTRONIC BANKING

CENTERS

BRANCH NETWORKS

Managing Director’s Office Page 21

Perlis - 1

Kedah - 11

Kelantan - 13

Pulau Pinang - 5

Perak - 9

Pahang - 9

Terengganu - 5

Selangor – 26 Kuala Lumpur - 18

Negeri

Sembilan -6

Melaka - 4 Johor - 15

Sarawak - 6

Sabah - 5 Labuan- 1

Region Total

Central 44

Northern 26

Eastern 27

Southern 25

East Malaysia 12

Total @ 31 Dec 2013 134

SELF SERVICE TERMINALS

Managing Director’s Office Page 22

ATM – 8 CDM – 4

CQM – 1 SP - 1

ATM – 36 CDM – 14

CQM – 7 SP -1

ATM – 30 CDM – 16

CQM – 7 SP -3

ATM – 2 CDM – 1

CQM – 1 SP - 1

ATM – 58 CDM – 27

CQM – 14 SP -4

ATM – 56 CDM –31

CQM – 11 SP - 4

ATM – 32 CDM – 13

CQM – 3 SP - 1

ATM – 39 CDM – 22

CQM – 7 SP - 2

ATM – 55 CDM – 20

CQM – 12 SP - 7

COIN - 1

ATM -158 CDM – 57

CQM – 28 SP - 10

ATM – 31 CDM – 14

CQM – 6 SP -2

ATM – 78 CDM - 36

CQM – 14 SP – 7

ATM – 33 CDM – 16

CQM – 6 SP - 4

ATM – Automated Teller Machine CDM – Cash Deposit Machine CQM – Cheque Deposit Machine SP – Statement Printer COIN – Coin Deposit Machine

ATM – 39 CDM – 17

CQM – 5 SP - 0

COIN - 1

ATM – 67 CDM – 36

CQM – 11 SP - 4

COIN - 1

Location type ATM CDM CQM SP Coin Total

Branches 291 211 116 43 3 664

IPTA/IPTS 119 19 4 4 0 146

Shopping Centres 92 9 1 2 0 104

Corporate Offices 67 23 7 1 0 98

TH Branches 40 29 0 0 0 69

Petrol Stations 34 2 0 0 0 36

Hospitals 21 0 1 0 0 22

Mosques 15 10 0 0 0 25

Others 43 21 4 1 0 69

Total 722 324 133 51 3 1,233

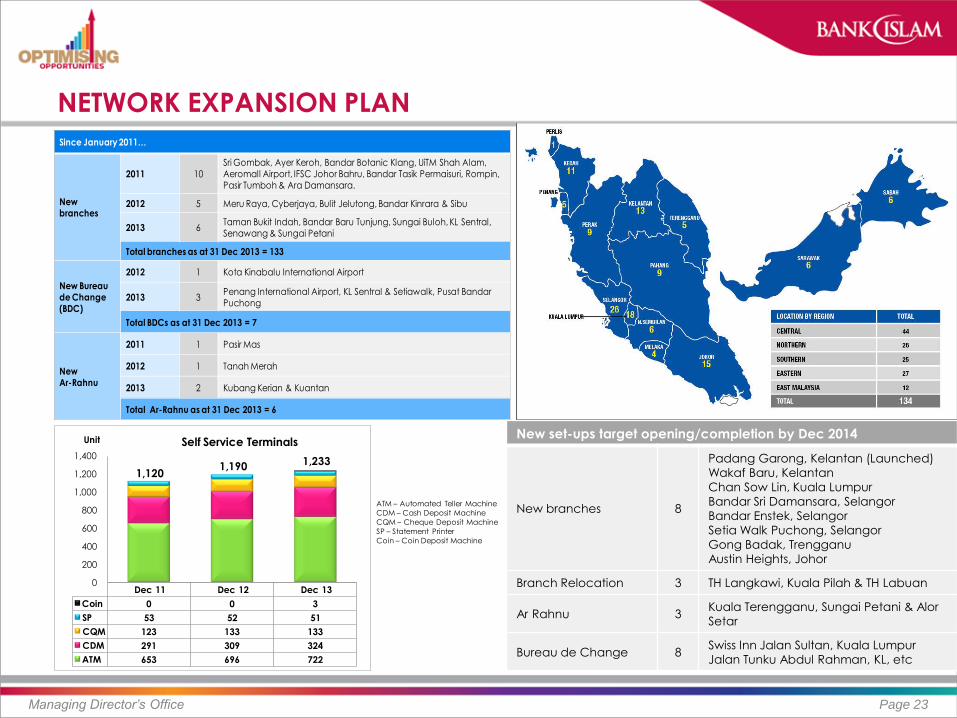

NETWORK EXPANSION PLAN

Managing Director’s Office Page 23

Dec 11 Dec 12 Dec 13

Coin 0 0 3

SP 53 52 51

CQM 123 133 133

CDM 291 309 324

ATM 653 696 722

0

200

400

600

800

1,000

1,200

1,400

Unit Self Service Terminals

1,1201,190 1,233

ATM – Automated Teller Machine

CDM – Cash Deposit Machine

CQM – Cheque Deposit Machine

SP – Statement Printer

Coin – Coin Deposit Machine

Since January 2011…

New branches

2011 10

Sri Gombak, Ayer Keroh, Bandar Botanic Klang, UiTM Shah Alam, Aeromall Airport, IFSC Johor Bahru, Bandar Tasik Permaisuri, Rompin, Pasir Tumboh & Ara Damansara.

2012 5 Meru Raya, Cyberjaya, Bulit Jelutong, Bandar Kinrara & Sibu

2013 6Taman Bukit Indah, Bandar Baru Tunjung, Sungai Buloh, KL Sentral, Senawang & Sungai Petani

Total branches as at 31 Dec 2013 = 133

New Bureaude Change (BDC)

2012 1 Kota Kinabalu International Airport

2013 3Penang International Airport, KL Sentral & Setiawalk, Pusat Bandar Puchong

Total BDCs as at 31 Dec 2013 = 7

New Ar-Rahnu

2011 1 Pasir Mas

2012 1 Tanah Merah

2013 2 Kubang Kerian & Kuantan

Total Ar-Rahnu as at 31 Dec 2013 = 6

New set-ups target opening/completion by Dec 2014

New branches 8

Padang Garong, Kelantan (Launched)

Wakaf Baru, Kelantan

Chan Sow Lin, Kuala Lumpur

Bandar Sri Damansara, Selangor

Bandar Enstek, Selangor

Setia Walk Puchong, Selangor

Gong Badak, Trengganu

Austin Heights, Johor

Branch Relocation 3 TH Langkawi, Kuala Pilah & TH Labuan

Ar Rahnu 3 Kuala Terengganu, Sungai Petani & Alor

Setar

Bureau de Change 8 Swiss Inn Jalan Sultan, Kuala Lumpur

Jalan Tunku Abdul Rahman, KL, etc

CONSUMER BANKING

Managing Director’s Office Page 24

AR RAHNU OUTLETS

Managing Director’s Office Page 25

Kota Bharu Outlet

Pasir Puteh Outlet

Pasir Mas Outlet

Tanah Merah Outlet

…6 Ar Rahnu Outlets

…another outlet in Kuala

Trengganu by end of Dec 2013

No. Location State Day 1

1 Kota Bahru KLN 10 Jun 2010

2 Pasir Puteh KLN 15 Jul 2010

3 Pasir Mas KLN 29 Jul 2011

4 Tanah Merah KLN 28 Jun 2012

5 Kubang Kerian KLN 11 Jul 2013

6 Kuantan PHG 24 Aug 2013

Kubang Kerian Outlet

CORPORATE INVESTMENT BANKING

Managing Director’s Office Page 26

RM5.311 billion

Islamic Securities

Programme

Turus Pesawat Sdn Bhd

Joint Lead Manager

RM8.0 billion

Government Guaranteed

Islamic CPs/MTNs

Programme

DANAINFRA

N A S I O N A L

DanaInfra Nasional Berhad

Joint Lead Manager

Runner

RM10.0 billion

Islamic Medium Term

Notes Programme

Aman Sukuk Berhad

Joint Lead Manager &

Shariah Adviser

RM5.0 billion**

Islamic Securities

Programme

Manjung Island Energy

Berhad

Joint Principal Advisers,

Joint Lead Arrangers, Joint

Lead Managers & Joint Shariah Advisers

RM1.66 billion

Sukuk Murabahah

BIMB Holdings Berhad

Lead Aranger

RM500.0 million

Bank Guaranteed

Sukuk Ijarah

Aras Sejagat Sdn Bhd

Joint Lead Arranger &

Joint Lead Manager

RM4.0 billion

Sukuk Musyarakah

Plus SPV Berhad

Joint Book Runner

RM1.5 billion

Islamic Medium Term

Notes Programme

Malaysia Debt Ventures

Berhad

Joint Lead Manager

CORPORATE INVESTMENT BANKING…CONT

Managing Director’s Office Page 27

RM1.0 billion

Istisna’

Projek Usahasama

Transit Aliran Ringan

Joint Arranger & Shariah

Adviser

RM2.2 billion

BaIDS

KL International Airport

Berhad

Sole Lead Arranger

RM1.5 billion

Al-Ijarah Muntahiyah

Bit-Tamlik

Kumpulan Guthrie Berhad

Structuring & Shariah

Adviser

USD150.0 million

Sukuk Al Ijarah

First Global Sukuk Inc

Sole Lead Arranger

USD600.0 million

Sukuk Al Ijarah

Malaysia Global Sukuk Inc

Co-Arranger

RM1.28 billion

BaIDS

SAJ Holdings Sdn Bhd

Joint Lead Arranger/Lead Manager & Shariah

Adviser

RM752.2 million

Mudharabah Sukuk

Manfaat Tetap Sdn Bhd

Shariah Adviser

RM200.0 million BBA CPs

RM3.0 billion BBA MTNs

Syarikat Bekalan Air

Selangor Sdn Bhd

Joint Lead Arranger & Shariah Adviser

RM4.0 billion

Ijarah Medium Term Notes

Programme

Syarikat Prasarana

Negara Berhad

Co-Manager

RM200.0 million

Bai’ Murabahah Medium

Term Notes Programme

TH Plantations Berhad

Joint Lead Arranger &

Shariah Adviser

CORPORATE FINANCE

Managing Director’s Office Page 28

Listing of APFT Berhad

on the Main Market of

Bursa Malaysia

Securities Berhad

Main Adviser

APFT Berhad

Listing of Focus Lumber

Berhad on the Main

Market of Bursa Malaysia

Securities Berhad

Main Adviser

Focus Lumber Berhad

Listing of PESTECH

International Berhad

on the Main Market of

Bursa Malaysia

Securities Berhad

Main Adviser

Exemption from the

obligation to undertake

Mandatory Take-over Offer

arising from the acquisition of

Syarikat Sabaco Sdn Bhd

from TH Ladang (Sabah &

Sarawak) Sdn Bhd

Main Adviser

Lembaga Tabung Haji

Akarmas Sdn Bhd

Conditional Mandatory

Take-over Offer by Akarmas

Sdn Bhd to acquire all the

remaining ordinary shares

of RM1.00 each in PK

Resources Berhad for a

cash consideration of

RM0.60 per share

Main Adviser

Acquisitions by BIMB

Holdings Berhad of the

remaining 49% equity

interest in Bank Islam

Malaysia Berhad for a total

purchase consideration of

USD884.6 million

Main Adviser

TH Plantations Berhad

•Acquisitions of Syarikat

Sabaco Sdn Bhd and Ladang

Bukit Belian Sdn Bhd from TH

Ladang (Sabah & Sarawak)

Sdn Bhd for a total purchase

consideration of RM199 million

•Bonus Issue

•Employees’ Share Option

Scheme

Main Adviser

Renounceable rights Issue of

426,715,958 new ordinary

shares of RM1.00 each in BIMB

Holdings Berhad together with

426,715,958 free detachable

warrants to raise gross

proceeds of

RM1.814 billion

Main Adviser *

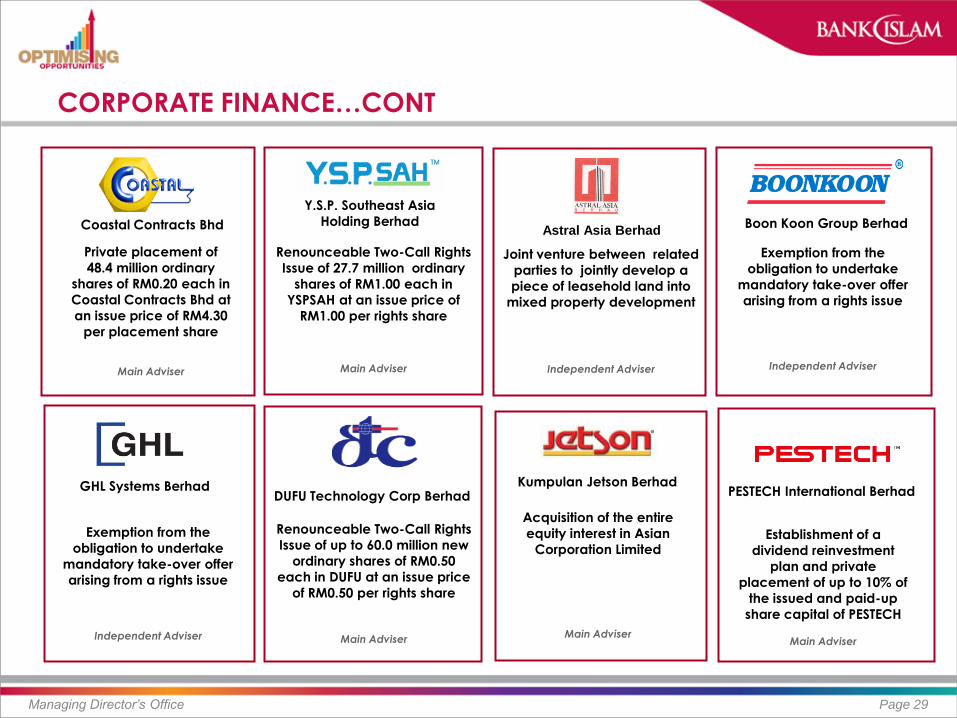

CORPORATE FINANCE…CONT

Managing Director’s Office Page 29

Boon Koon Group Berhad

Exemption from the

obligation to undertake

mandatory take-over offer

arising from a rights issue

Independent Adviser

GHL Systems Berhad

Exemption from the

obligation to undertake

mandatory take-over offer

arising from a rights issue

Independent Adviser

Astral Asia Berhad

Joint venture between related

parties to jointly develop a

piece of leasehold land into

mixed property development

Independent Adviser

Y.S.P. Southeast Asia

Holding Berhad

Renounceable Two-Call Rights

Issue of 27.7 million ordinary

shares of RM1.00 each in

YSPSAH at an issue price of

RM1.00 per rights share

Main Adviser

Acquisition of the entire

equity interest in Asian

Corporation Limited

Main Adviser

Kumpulan Jetson Berhad PESTECH International Berhad

Establishment of a

dividend reinvestment

plan and private

placement of up to 10% of

the issued and paid-up

share capital of PESTECH

Main Adviser

Coastal Contracts Bhd

Private placement of

48.4 million ordinary

shares of RM0.20 each in

Coastal Contracts Bhd at

an issue price of RM4.30

per placement share

Main Adviser

DUFU Technology Corp Berhad

Renounceable Two-Call Rights

Issue of up to 60.0 million new

ordinary shares of RM0.50

each in DUFU at an issue price

of RM0.50 per rights share

Main Adviser

BUREAU DE CHANGE

Managing Director’s Office Page 30

Kota Kinabalu International Airport

Contact Pier,

Kuala Lumpur International Airport

KLIA - LCCT

Penang International Airport*

Bukit Bintang

BDC

No. Location State Day 1

1 LCCT, Sepang SGR 15 Dec 2008

2 Contact Pier International, KLIA SGR 01 Oct 2010

3 Bukit Bintang KL 03 Dec 2010

4 Kota Kinabalu International Airport SBH 26 Jul 2012

5 Penang International Airport PNG 1 Feb 2013

6 KL Sentral KL 13 Sep 2013

7 Setiawalk, Puchong SGR 21 Nov 2013

8 Swiss Inn, Kuala Lumpur KL 22 April 2014

KL Sentral

BEST ISLAMIC BANK

Managing Director’s Office Page 31

Managing Director’s Office Page 32

CORPORATE

STRATEGIC PLAN

STRATEGIC MANAGEMENT PYRAMID

Managing Director’s Office Page 33

Vision, Mission & Corporate Values

3-year Corporate Plan

Annual Corporate/Business Plan - Resource Allocation

Divisional/Tactical Plan

Key Performance Indicators Framework

Accountability & Reporting Regime

…Strategic management process - The full set of commitments, decisions, and actions required for a firm to

create value and earn above-average returns

STRATEGY DOCUMENTATION

Page 34

Divisional Business Plan & Roadmap

Tactical Plan Divisional KPIs

Framework Product Plan

Divisional Policy, Manuals & SOP

Annual Business Plan & Budget

Corporate Plan Risk Appetite

Statement Budget & Financial

Projections Corporate KPIs

Corporate Master Plan

Managing Director’s Office

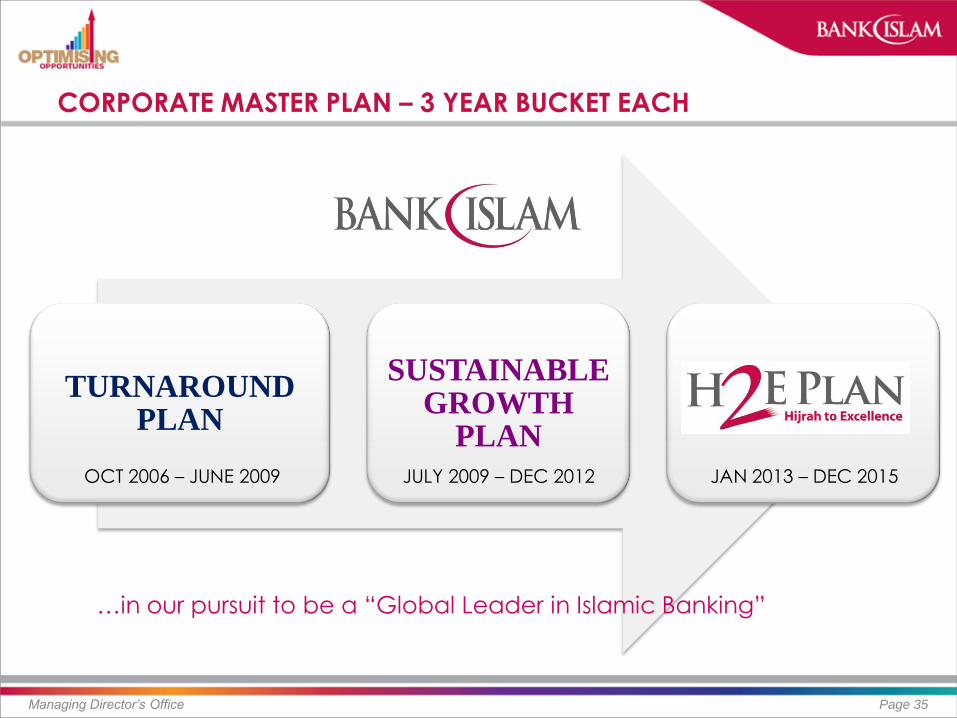

CORPORATE MASTER PLAN – 3 YEAR BUCKET EACH

Page 35

TURNAROUND PLAN

SUSTAINABLE GROWTH

PLAN

OCT 2006 – JUNE 2009 JULY 2009 – DEC 2012

…in our pursuit to be a “Global Leader in Islamic Banking”

JAN 2013 – DEC 2015

Managing Director’s Office

TURNAROUND PLAN (OCT 2006- JUNE 2009)

Page 36

Recapitalization & Balance Sheet Restructuring

Transformation Programme

IT Infrastructure

Revamp

Cost Rationalization

Human Capital Development

Managing Director’s Office

BRAND POSITIONING

Managing Director’s Office Page 37

“Banking for Muslims”

“Banking for All”

… growing recognition that the inherent tenets of Islamic finance are aligned to sustainable dimensions of ethical banking and responsible financing.

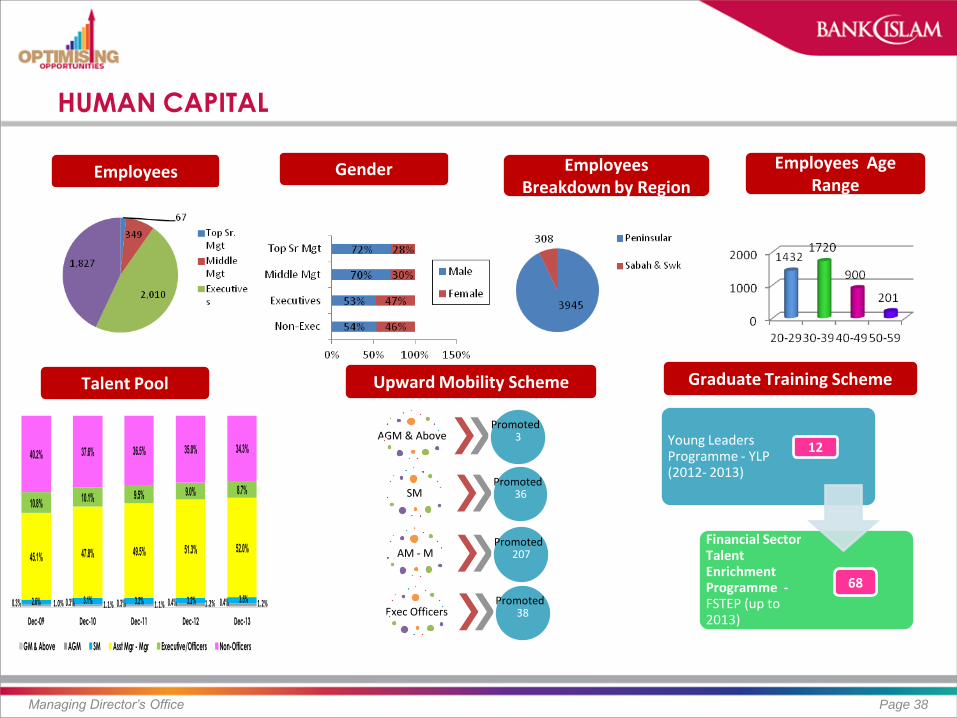

HUMAN CAPITAL

Managing Director’s Office Page 38

Employees Employees Breakdown by Region

Employees Age Range

Gender

Total Spent:

RM1.5 bil Total Spent:

RM1.5 bil

Graduate Training Scheme Talent Pool

0.3% 0.3% 0.3% 0.4% 0.4%1.0% 1.1% 1.1% 1.2% 1.2%2.6% 3.1% 3.2% 3.2% 3.5%

45.1% 47.8% 49.5% 51.3% 52.0%

10.8%10.1% 9.5% 9.0% 8.7%

40.2% 37.6% 36.5% 35.0% 34.3%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

GM & Above AGM SM Asst Mgr - Mgr Executive/Officers Non-Officers

Upward Mobility Scheme

AGM & Above 3 Promoted

SM 36 Promoted

AM - M 207 Promoted

Exec Officers 38 Promoted

Young Leaders Programme - YLP (2012- 2013)

Financial Sector Talent Enrichment Programme - FSTEP (up to 2013)

12

68

Business Innovation

Robust Risk Management

Strengthening Enabling

Infrastructure

Building Capability & Capacity

Franchise Develop-

ment

In-organic

Growth & Corporate Expansion

SUSTAINABLE GROWTH PLAN… ENDED DEC 2012

Page 39 Managing Director’s Office

BUSINESS INNOVATION

Managing Director’s Office Page 40

2009 2010 2011 2012 2013

ROBUST RISK MANAGEMENT

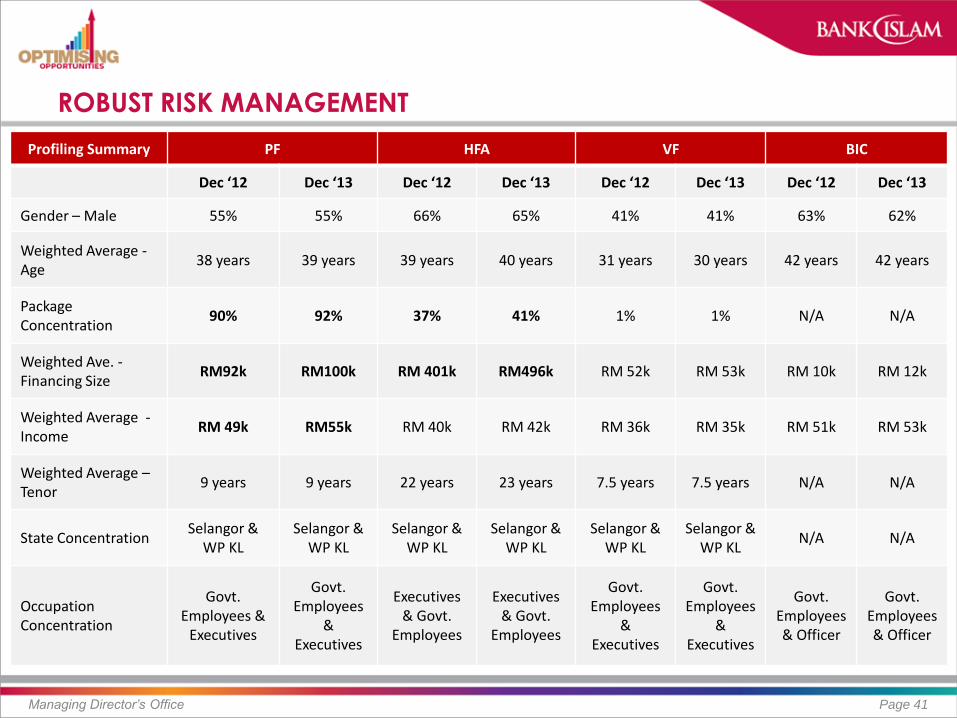

Managing Director’s Office Page 41

Profiling Summary PF HFA VF BIC

Dec ‘12 Dec ‘13 Dec ‘12 Dec ‘13 Dec ‘12 Dec ‘13 Dec ‘12 Dec ‘13

Gender – Male 55% 55% 66% 65% 41% 41% 63% 62%

Weighted Average - Age

38 years 39 years 39 years 40 years 31 years 30 years 42 years 42 years

Package Concentration

90% 92% 37% 41% 1% 1% N/A N/A

Weighted Ave. - Financing Size

RM92k RM100k RM 401k RM496k RM 52k RM 53k RM 10k RM 12k

Weighted Average - Income

RM 49k RM55k RM 40k RM 42k RM 36k RM 35k RM 51k RM 53k

Weighted Average – Tenor

9 years 9 years 22 years 23 years 7.5 years 7.5 years N/A N/A

State Concentration Selangor &

WP KL Selangor &

WP KL Selangor &

WP KL Selangor &

WP KL Selangor &

WP KL Selangor &

WP KL N/A N/A

Occupation Concentration

Govt. Employees &

Executives

Govt. Employees

& Executives

Executives & Govt.

Employees

Executives & Govt.

Employees

Govt. Employees

& Executives

Govt. Employees

& Executives

Govt. Employees & Officer

Govt. Employees & Officer

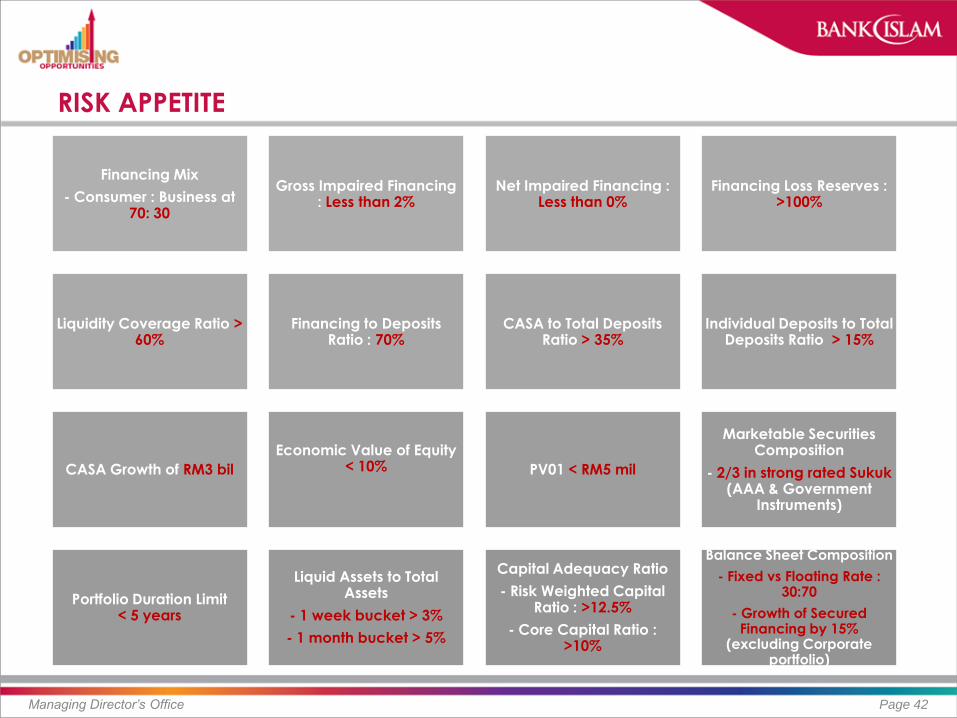

RISK APPETITE

Managing Director’s Office Page 42

Financing Mix

- Consumer : Business at 70: 30

Gross Impaired Financing : Less than 2%

Net Impaired Financing : Less than 0%

Financing Loss Reserves : >100%

Liquidity Coverage Ratio > 60%

Financing to Deposits Ratio : 70%

CASA to Total Deposits Ratio > 35%

Individual Deposits to Total Deposits Ratio > 15%

CASA Growth of RM3 bil

Economic Value of Equity < 10%

PV01 < RM5 mil

Marketable Securities Composition

- 2/3 in strong rated Sukuk (AAA & Government

Instruments)

Portfolio Duration Limit < 5 years

Liquid Assets to Total Assets

- 1 week bucket > 3%

- 1 month bucket > 5%

Capital Adequacy Ratio

- Risk Weighted Capital Ratio : >12.5%

- Core Capital Ratio : >10%

Balance Sheet Composition

- Fixed vs Floating Rate : 30:70

- Growth of Secured Financing by 15%

(excluding Corporate portfolio)

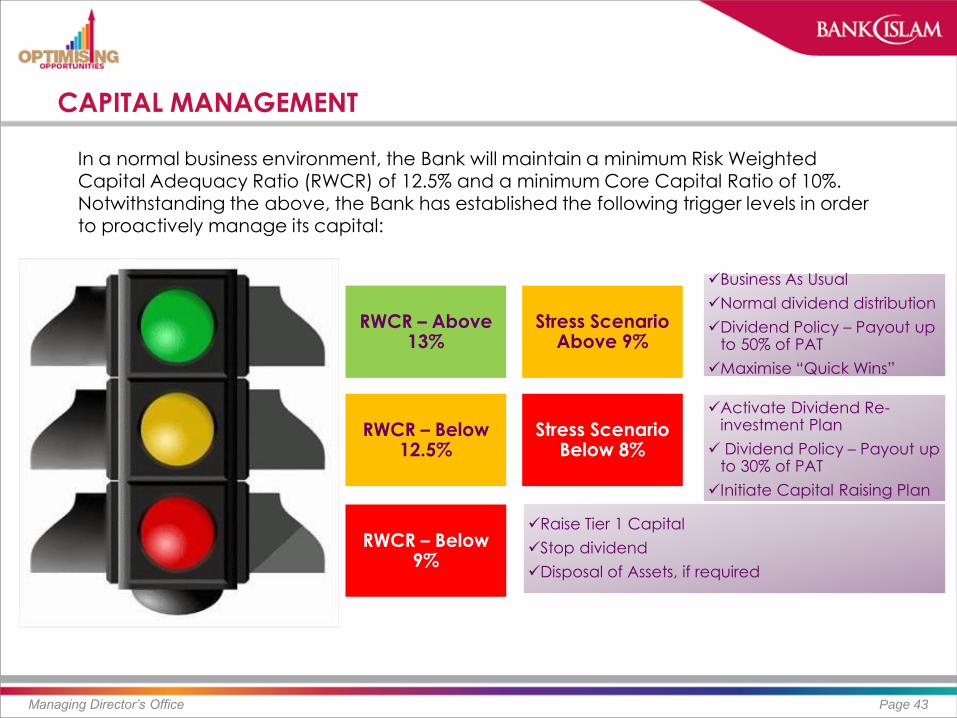

CAPITAL MANAGEMENT

Managing Director’s Office Page 43

In a normal business environment, the Bank will maintain a minimum Risk Weighted Capital Adequacy Ratio (RWCR) of 12.5% and a minimum Core Capital Ratio of 10%. Notwithstanding the above, the Bank has established the following trigger levels in order to proactively manage its capital:

RWCR – Above 13%

RWCR – Below 12.5%

RWCR – Below 9%

Stress Scenario Below 8%

Stress Scenario Above 9%

Business As Usual

Normal dividend distribution

Dividend Policy – Payout up to 50% of PAT

Maximise “Quick Wins”

Activate Dividend Re-investment Plan

Dividend Policy – Payout up to 30% of PAT

Initiate Capital Raising Plan

Raise Tier 1 Capital

Stop dividend

Disposal of Assets, if required

FRANCHISE DEVELOPMENTS

Managing Director’s Office Page 44

2010 2011 2012 2013

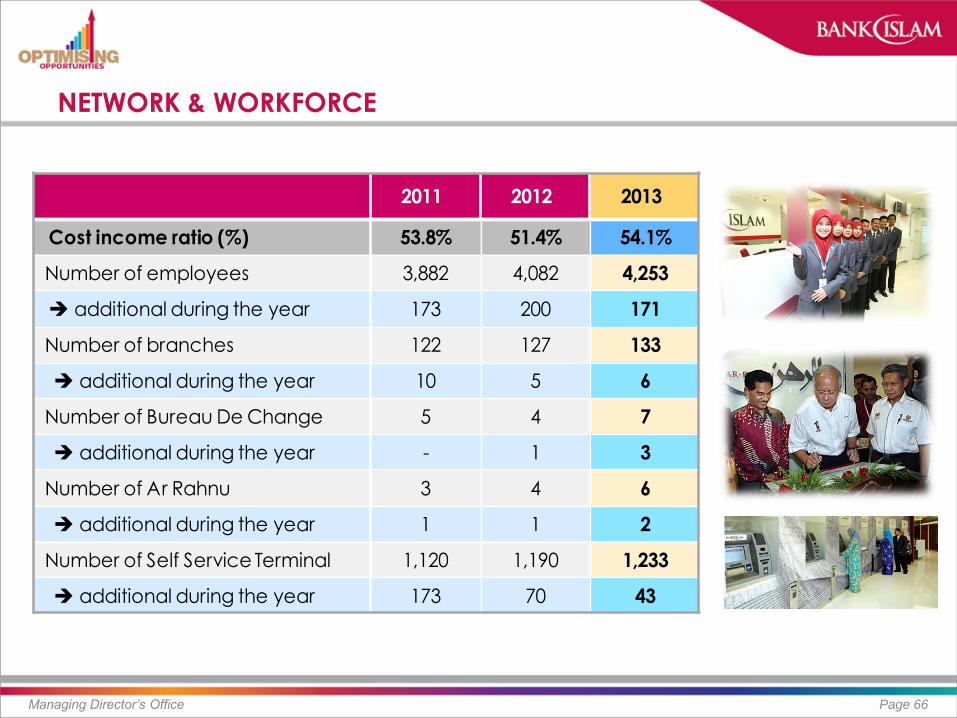

NETWORK & WORKFORCE

Managing Director’s Office Page 45

2011 2012 2013

Cost income ratio (%) 53.8% 51.4% 54.1%

Number of employees 3,882 4,082 4,253

additional during the year 173 200 171

Number of branches 122 127 133

additional during the year 10 5 6

Number of Bureau De Change 5 4 7

additional during the year - 1 3

Number of Ar Rahnu 3 4 6

additional during the year 1 1 2

Number of Self Service Terminal 1,120 1,190 1,233

additional during the year 173 70 43

HIJRAH TO EXCELLENCE PLAN – H2E (2013 TO 2015)

Page 46

Robust Organic Growth

Service Excellence

Shariah-led Innovation

Resource Optimisation

Employer of Choice

Regional-isation

Managing Director’s Office

KEY COMPONENTS OF H2E

Page 47

Robust Organic Growth

Asset Growth of 15% p.a.

Financing Growth between 20% to 25% p.a.

Financing-to-Deposit Ratio of 75% by 2015

Non-fund Base Income of 15% by 2015

Gross Profit Growth of 15% p.a.

Service Excellence

Customer Centric – Client Driven Model

Service Transformation – Service Culture

Operational Excellence

Product Attractiveness & Competitiveness

Technology as Key Enabler

Shariah-led Innovation

Shariah Centre of Excellence

Aspire Pioneering

World Class Shariah Product/Contracts

Innovation-based Incentives – “Idea

Bank”

Cost Effective Product Structure

Resource Optimisation

Harnessing Share of Wallet – “Cross

Selling & Up Selling”

Process Improvement &

Optimization

Shared Services

Cost Efficiency & High Productivity

Re-energise Brand Equity

Employer of Choice

Inspired Employees – Mindset of Excellence

Passionate Leadership

People Engagement & Shared Values

High Performance & Knowledge -

based Workplace

Work-life Balance –”Community Connection”

Regionalisation

“Close to Home” – ASEAN region

Fit Our Franchise

Right Local Partner

Business Synergistics

Strong Domestic Presence &

Delivery Networks

Managing Director’s Office

OPTIMISING OPPORTUNITIES – STRATEGIC PRIORITIES

Managing Director’s Office Page 48

Optimising Returns Accelerating CASA Growth

Delivering Superior Banking Experience

Optimising Resources

Cross Marketing for Fee-Based

Income

(FOREX, Cash Mgmt, etc)

Financing-to-Deposit Ratio of

70%

Sustaining Net Income Margin

Focus on Retail CASA

(Salary a/c)

Individual Deposit -15% of Total

Deposit

First-time Resolution at

Contact Centre

Expanding Footprint &

Optimising Cross Marketing at

Branches

Refinement of Turnaround

Time& Customer Service Charter

Seamless customer service across all customer touch points

(Greetings/Welcoming environment, Interaction with

customers, Service level, Product knowledge, etc)

Service/Channel Differentiation (i.e. Bulk Opening accounts at site for universities,

factories, etc)

Channel Productivity &

Efficiency

Reinforcing Performance

Culture

Proactive Capital

Management

Rightsizing of Operating Environment &

Redeployment of Human Capital

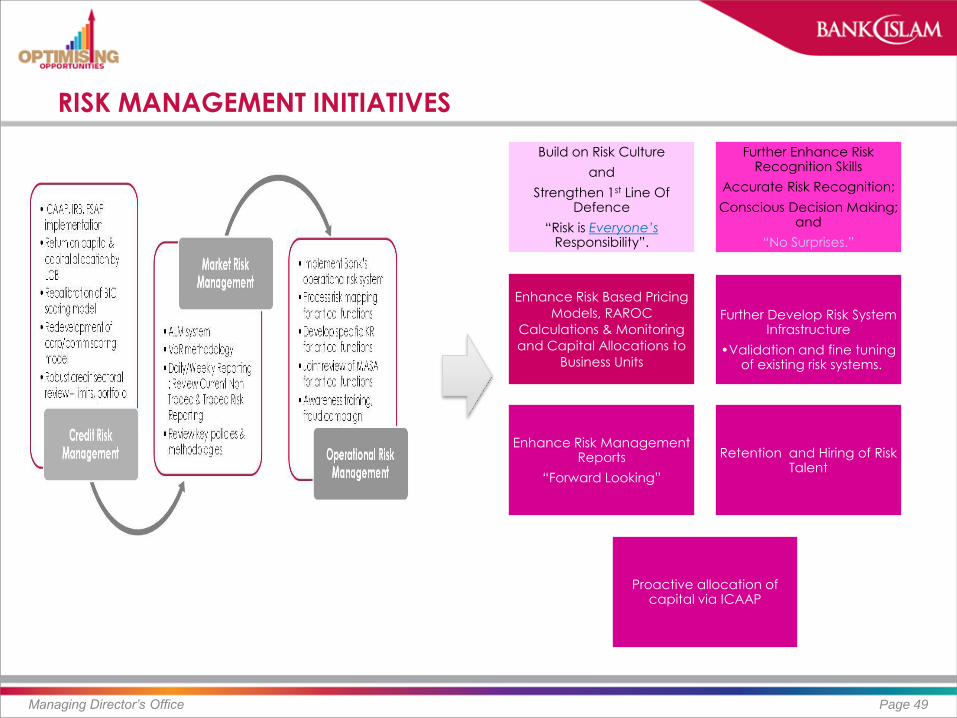

RISK MANAGEMENT INITIATIVES

Managing Director’s Office Page 49

Build on Risk Culture

and

Strengthen 1st Line Of Defence

“Risk is Everyone’s Responsibility”.

Further Enhance Risk Recognition Skills

Accurate Risk Recognition;

Conscious Decision Making; and

“No Surprises.”

Enhance Risk Based Pricing

Models, RAROC

Calculations & Monitoring

and Capital Allocations to

Business Units

Further Develop Risk System Infrastructure

•Validation and fine tuning of existing risk systems.

Enhance Risk Management Reports

“Forward Looking”

Retention and Hiring of Risk Talent

Proactive allocation of capital via ICAAP

Managing Director’s Office Page 50

BUSINESS

MODALITY

ASSETS & REVENUE COMPOSITION AS AT DEC 2013

Managing Director’s Office Page 51

42.6%

7.5% 6.1%

40.7%

0.4%

2.7% Consumer

Commercial

Corporate

Treasury

BILOB

Others*

Asset Composition Revenue Composition Revenue Mix

53.8%

7.8% 6.1%

31.2%

0.3%

0.7% Consumer

Commercial

Corporate

Treasury

BILOB

Others 87.4%

12.6%

Fund-based Income

Non-fund based Income

…primarily a retail bank…

CONSUMER BANKING – TARGET MARKET

Managing Director’s Office Page 52

Product Target Market Minimum

Salary

Debt Service Ratio Others

House

Financing

Owner-occupied

Ticket size >RM250K for Klang Valley & State Capital

Matured locations/ Well established – refinancing market –

reputable development/ developer

Existing customer base with good credit record

Shorten Financing tenure up to 35 years

Focus on preferred customer

Package customer

>5k Outside Klang Valley

Income 3k & below - ≤ 60%

Income RM3001- RM7k - ≤ 70%

Income RM7,001 and above - ≤ 75%

Klang Valley

Income 5k & below - ≤ 60%

Income RM5001- RM7k - ≤ 70%

Income RM7,001 and above - ≤ 75%

-MOF ≤ 80%

Personal

Financing

Package employers (salary deduction from source)

Secured financing (Gold, TH savings, GIA, SIA)

Shorten financing up to 10 years

Larger ticket items >RM50k

Special programme financing to: (i) Mass affluent professionals

(ii) Medical practitioners

(iii) Engineers

(iv) Accountants

-Package

RM2,000

-Non

Package RM3,000

Outside Klang Valley

Income 3k & below - ≤ 60%

Income RM3001- RM7k - ≤ 70%

Income RM7,001 and above - ≤ 75%

Klang Valley Income 5k & below - ≤ 60%

Income RM5001- RM7k - ≤ 70%

Income RM7,001 and above - ≤ 75%

-Fin amount

capped at 30x

salary

-Ticket size >50k

-Fin >10 yrs with min income

RM3,000 p.m.

-Fin >RM150k min

income RM120k

p.a.

Vehicle

Financing

Package Customers

New Nationall

Gradhitz Package Risk Based Pricing for VF

Murabahah Purchase Orderer (MPO) product for VF

Motorbikes financing initiatives for selected customers

Min RM1,500

pm

Subject to

loan amt &

DSR

With house 70%

Without house 50%

Net Take Home Pay: Klang Valley RM1,000

Outside Klang Valley RM750

-Tenure not

exceed 9 years

B.I Card Senior management & owner of reputable Corp/Comm

customers (i.e.GLCs & MNCs)

Packaged employers

Government Servant

Mass affluent and middle income earners

Loyalty Program

Balance Transfer

Increase POS Terminal

RM2,000 70%

Net Take Home Pay

Klang Valley RM1,000

Outside Klang Valley RM750

-New customer

with Balance

Transfer

KEY CUSTOMERS – PACKAGE EMPLOYERS

Managing Director’s Office Page 53

KEY CUSTOMERS – NON GOVERNMENT AGENCIES

Managing Director’s Office Page 54

… salary deduction from source/Employers

NEW TARGET SEGMENTS

Managing Director’s Office Page 55

EXPOSURE TO ETP PROJECTS

Managing Director’s Office Page 56

Oil, Gas & Energy

Education

Palm Oil

Healthcare

Greater Kuala Lumpur

About RM360 million About RM4.7 billion

About RM4.7 billion

About RM515 million

..out of RM219.3 billion worth of committed ETP projects, only RM20.5 billion were realised by end-Sept 2013. The balance will flow through from 2014 onwards

GAME CHANGING INITIATIVES

Managing Director’s Office Page 57

Total

Spent:

RM1.5 bil

Total

Spent:

RM1.5 bil

1. ENABLING E-PAYMENT SERVICES FOR SMEs AND MICRO ENTERPRISES

Agenda: Promoting Electronic Banking Transactions Introduced the country’s first low-cost Mobile Point of Sales (MPOS) to allow small business entrepreneurs

and petty traders to benefit from electronic payment

Facilitate usage of online banking via eBanker and internet banking by SMEs – achieved 39.4% growth

from April 2013 to March 2014

Deployed self-service Internet (SSI) kiosks at branches - 48 SSIs were deployed in 2013

Deployment of POS Terminals and Acceptance of Payment Cards at Government Agencies

Internet Banking Fund Transfer and Interbank Giro for SME at Internet Banking and Ebanker

National Bill Payment System Project – ePayment standardisation

eDebit card and EDCPOS – for retail driven by Credit Card business (BICC)

2. MOBILE BANKING

Agenda: Attaining Excellence in Service Delivery to Customers Launched the first mobile banking service without internet access known as TAP Mobile Banking-i, where

account owners can perform banking transactions anywhere and anytime

In partnership with Amanah Ikhtiar Malaysia (AIM) to facilitate collection of micro financing via mobile

banking

Gained 447K subscribers within three years, mainly from Generation X and Y.

To cater for the younger segment of the demographics that appreciate the value of technology and

hassle-free transactions

Digital Malaysia

Programme

Digital

Malaysia Programme

Rural Transformation

Programme

GAME CHANGING INITIATIVES…CONT

Managing Director’s Office Page 58

Total

Spent:

RM1.5 bil

Total

Spent:

RM1.5 bil

3. AR RAHNU (ISLAMIC PAWN-BROKING)

Agenda: Promoting Financial Inclusion and Microfinancing Pawn broking services, providing access to capital to the underserved community hence facilitating social

uplift

5 Ar Rahnu Outlets in Kelantan

1 Ar Rahnu Outlet in Kuantan, Pahang

Total Financing outstanding of RM85m as at Q1 2014

No of customers grew by 34% from 10,896 in 2012 to 14,597 as at Mar 2014.

4. UNIDEBIT CARD

Agenda: Promoting Cashless Ecosystem to the University Community Providing infrastructure and enabler to social uplift, in support of Rural Transformation Programme and

Digital Malaysia Programme

Corporate Card and University student COMBO card with total active UniDebit Cards of more than 6,500

in UMK, UMP and UPSI and more than RM1.5m in terms of total transaction amounts.

Digital Malaysia

Programme

Digital Malaysia

Programme

Rural Transformation

Programme

Rural Transformation

Programme

Managing Director’s Office Page 59

FINANCIAL

HIGHLIGHTS

ROBUST ORGANIC GROWTH

Managing Director’s Office Page 60

+13.8% PBZT Growth

+14.4% Total Assets Growth

+21.7% Financing Growth

65% Financing-to-deposits ratio

1.2% Gross Impaired Ratio

236.7 308.3

233.1 342.5

493.0 600.3

683.0

Jun 07 Jun 08 Jun 09 Dec 10 Dec 11 Dec 12 Dec 13

19,091.2 23,559.4

27,497.5 30,397.9 32,226.5 37,450.8

42,836.5

June 07 June 08 June 09 Dec 10 Dec 11 Dec 12 Dec 13

8,472.1 9,061.3 9,661.9 11,857.1

14,160.3

19,508.7

23,740.9

June 07 June 08 June 09 Dec 10 Dec 11 Dec 12 Dec 13 -0.9% Net Impaired Ratio

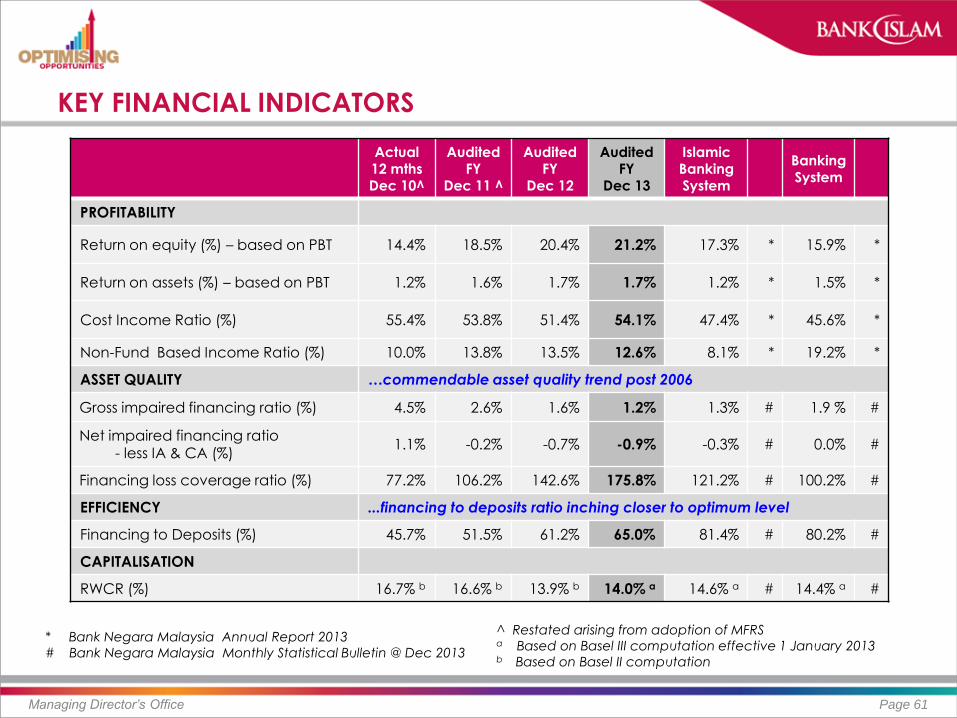

KEY FINANCIAL INDICATORS

Managing Director’s Office Page 61

Actual 12 mths Dec 10^

Audited FY

Dec 11 ^

Audited FY

Dec 12

Audited FY

Dec 13

Islamic Banking System

Banking System

PROFITABILITY

Return on equity (%) – based on PBT 14.4% 18.5% 20.4% 21.2% 17.3% * 15.9% *

Return on assets (%) – based on PBT 1.2% 1.6% 1.7% 1.7% 1.2% * 1.5% *

Cost Income Ratio (%) 55.4% 53.8% 51.4% 54.1% 47.4% * 45.6% *

Non-Fund Based Income Ratio (%) 10.0% 13.8% 13.5% 12.6% 8.1% * 19.2% *

ASSET QUALITY …commendable asset quality trend post 2006

Gross impaired financing ratio (%) 4.5% 2.6% 1.6% 1.2% 1.3% # 1.9 % #

Net impaired financing ratio - less IA & CA (%)

1.1% -0.2% -0.7% -0.9% -0.3% # 0.0% #

Financing loss coverage ratio (%) 77.2% 106.2% 142.6% 175.8% 121.2% # 100.2% #

EFFICIENCY ...financing to deposits ratio inching closer to optimum level

Financing to Deposits (%) 45.7% 51.5% 61.2% 65.0% 81.4% # 80.2% #

CAPITALISATION

RWCR (%) 16.7% b 16.6% b 13.9% b 14.0% a 14.6% a # 14.4% a #

* Bank Negara Malaysia Annual Report 2013

# Bank Negara Malaysia Monthly Statistical Bulletin @ Dec 2013

^ Restated arising from adoption of MFRS a Based on Basel III computation effective 1 January 2013 b Based on Basel II computation

INCOME STATEMENT

Managing Director’s Office Page 62

FYE Dec 13

FYE Dec 12

Variance

RM million Amount %

Total income 2,244.3 1,987.4 256.9 12.9%

Profit to depositors (780.3) (593.4) (186.9) -31.5%

Net income 1,464.0 1,394.0 70.0 5.0%

Total overheads (792.3) (716.8) (75.5) -10.5%

Profit before allowance for impairment 671.7 677.2 (5.5) -0.8%

Allowance for impairment on financing and advances 15.0 (66.1) 81.1 -122.7%

Allowance for impairment on investments (9.2) 0.6 (9.8) -1,696.4%

Reversal on allowance for impairment on other assets 5.5 3.4 2.1 63.2%

Provision for contingent liability - (14.8) 14.8 -100.0%

Profit before zakat and tax 683.0 600.3 82.7 13.8%

Zakat (12.6) (9.2) (3.4) -35.9%

Tax (178.8) (160.3) (18.5) -11.6%

Profit for the period 491.6 430.8 60.8 14.1%

RETURN ON EQUITY – DEC 2013 VS DEC 2012

Managing Director’s Office Page 63

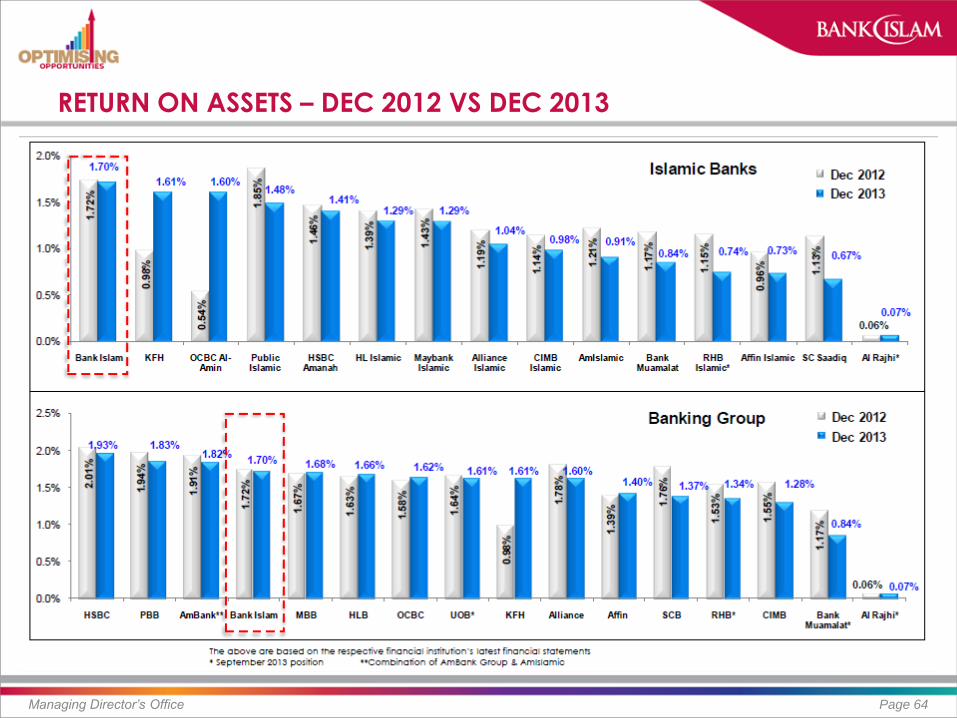

RETURN ON ASSETS – DEC 2012 VS DEC 2013

Managing Director’s Office Page 64

NET INCOME SPREAD

Managing Director’s Office Page 65

NETWORK & WORKFORCE

Managing Director’s Office Page 66

2011 2012 2013

Cost income ratio (%) 53.8% 51.4% 54.1%

Number of employees 3,882 4,082 4,253

additional during the year 173 200 171

Number of branches 122 127 133

additional during the year 10 5 6

Number of Bureau De Change 5 4 7

additional during the year - 1 3

Number of Ar Rahnu 3 4 6

additional during the year 1 1 2

Number of Self Service Terminal 1,120 1,190 1,233

additional during the year 173 70 43

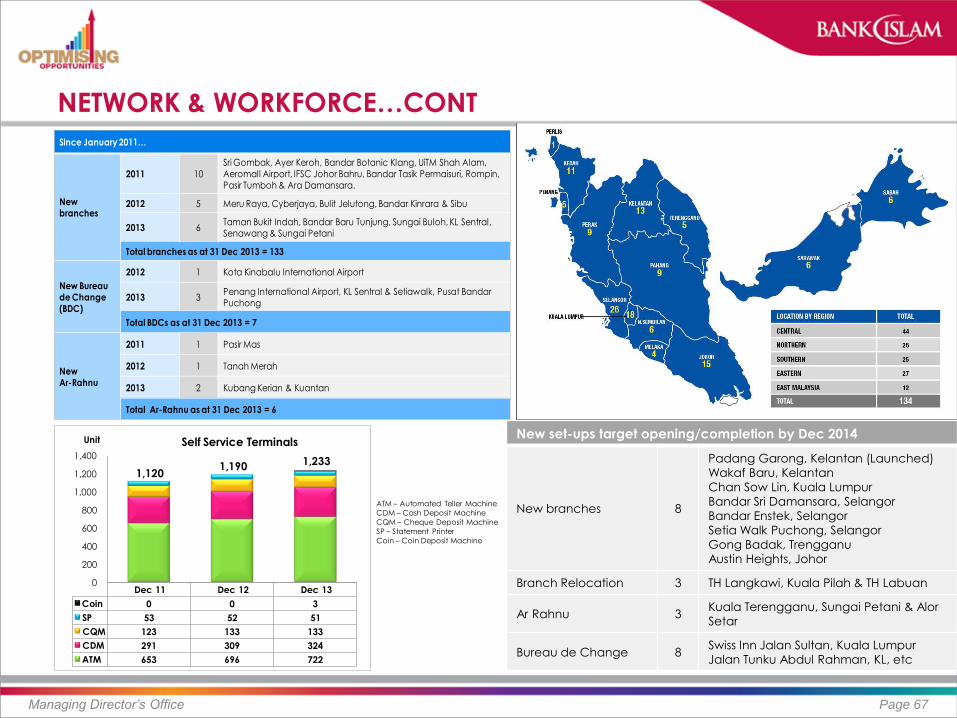

NETWORK & WORKFORCE…CONT

Managing Director’s Office Page 67

Dec 11 Dec 12 Dec 13

Coin 0 0 3

SP 53 52 51

CQM 123 133 133

CDM 291 309 324

ATM 653 696 722

0

200

400

600

800

1,000

1,200

1,400

Unit Self Service Terminals

1,1201,190 1,233

ATM – Automated Teller Machine

CDM – Cash Deposit Machine

CQM – Cheque Deposit Machine

SP – Statement Printer

Coin – Coin Deposit Machine

Since January 2011…

New branches

2011 10

Sri Gombak, Ayer Keroh, Bandar Botanic Klang, UiTM Shah Alam, Aeromall Airport, IFSC Johor Bahru, Bandar Tasik Permaisuri, Rompin, Pasir Tumboh & Ara Damansara.

2012 5 Meru Raya, Cyberjaya, Bulit Jelutong, Bandar Kinrara & Sibu

2013 6Taman Bukit Indah, Bandar Baru Tunjung, Sungai Buloh, KL Sentral, Senawang & Sungai Petani

Total branches as at 31 Dec 2013 = 133

New Bureaude Change (BDC)

2012 1 Kota Kinabalu International Airport

2013 3Penang International Airport, KL Sentral & Setiawalk, Pusat Bandar Puchong

Total BDCs as at 31 Dec 2013 = 7

New Ar-Rahnu

2011 1 Pasir Mas

2012 1 Tanah Merah

2013 2 Kubang Kerian & Kuantan

Total Ar-Rahnu as at 31 Dec 2013 = 6

New set-ups target opening/completion by Dec 2014

New branches 8

Padang Garong, Kelantan (Launched)

Wakaf Baru, Kelantan

Chan Sow Lin, Kuala Lumpur

Bandar Sri Damansara, Selangor

Bandar Enstek, Selangor

Setia Walk Puchong, Selangor

Gong Badak, Trengganu

Austin Heights, Johor

Branch Relocation 3 TH Langkawi, Kuala Pilah & TH Labuan

Ar Rahnu 3 Kuala Terengganu, Sungai Petani & Alor

Setar

Bureau de Change 8 Swiss Inn Jalan Sultan, Kuala Lumpur

Jalan Tunku Abdul Rahman, KL, etc

KEY BALANCE SHEET ITEMS

Managing Director’s Office Page 68

RM million Actual Dec 13

Actual Dec 12

Growth

Amount %

Total assets 42,836.5 37,450.8 5,385.7 14.4%

Net financing, advances and others 23,740.9 19,508.7 4,232.2 21.7%

Gross impaired financing 285.3 308.7 (23.4) -7.6%

Net impaired financing (216.3) (131.6) (84.7) 64.3%

Deposits from customers 37,272.4 32,583.2 4,689.2 14.4%

Equity 3,329.4 3,099.6 229.8 7.4%

TOTAL ASSETS & MARKET SHARE TRENDS

Managing Director’s Office Page 69

TOTAL ASSET

Managing Director’s Office Page 70

GROSS FINANCING & MARKET SHARE TRENDS

Managing Director’s Office Page 71

GROSS FINANCING BY BUSINESS UNITS

Managing Director’s Office Page 72

% growth Dec 13 vs

Dec 12

Business units mix (%) Dec 10 Dec 11 Dec 12 Dec 13

Consumer 75.9% 75.5% 73.7% 75.2%

Commercial 12.2% 12.5% 12.3% 13.2%

Corporate 9.9% 10.3% 13.1% 10.9%

BILOB 2.0% 1.7% 0.9% 0.7%

CONSUMER FINANCING PORTFOLIO

Managing Director’s Office Page 73

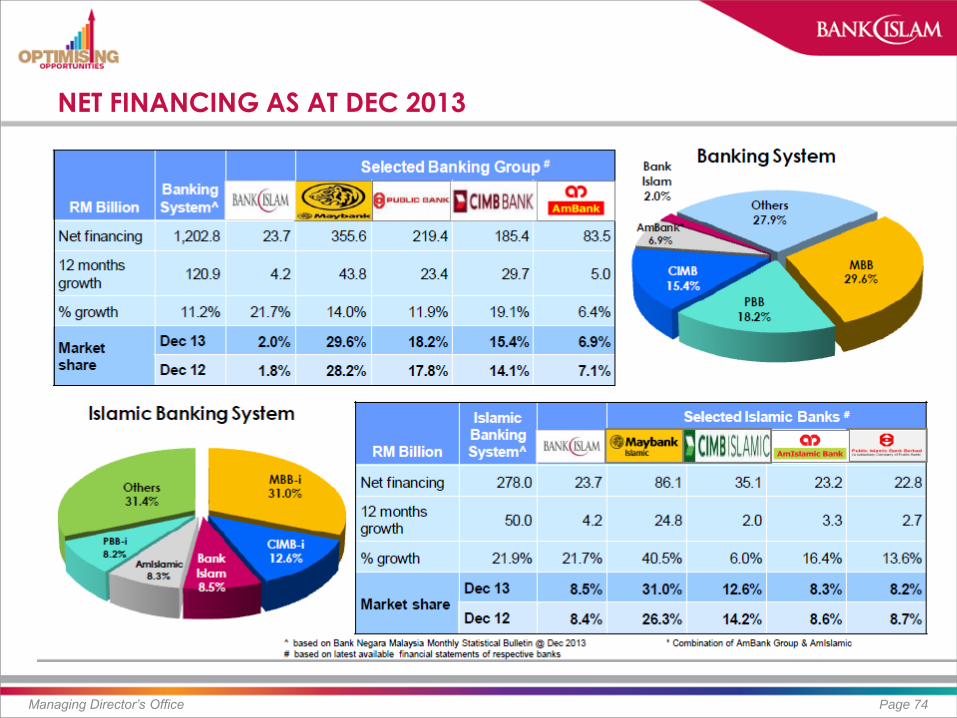

NET FINANCING AS AT DEC 2013

Managing Director’s Office Page 74

CUSTOMER DEPOSITS

Managing Director’s Office Page 75

Growth 14.4%

Financing to Deposits %

45.7% 51.5% 61.2% 65.0%

CUSTOMER DEPOSITS & MARKET SHARE TREND

Managing Director’s Office Page 76

DEPOSIT MARKET SHARE

Managing Director’s Office Page 77

CASA MARKET SHARE

Managing Director’s Office Page 78

CREDIT QUALITY TREND

Managing Director’s Office Page 79

ASSET QUALITY

Managing Director’s Office Page 80

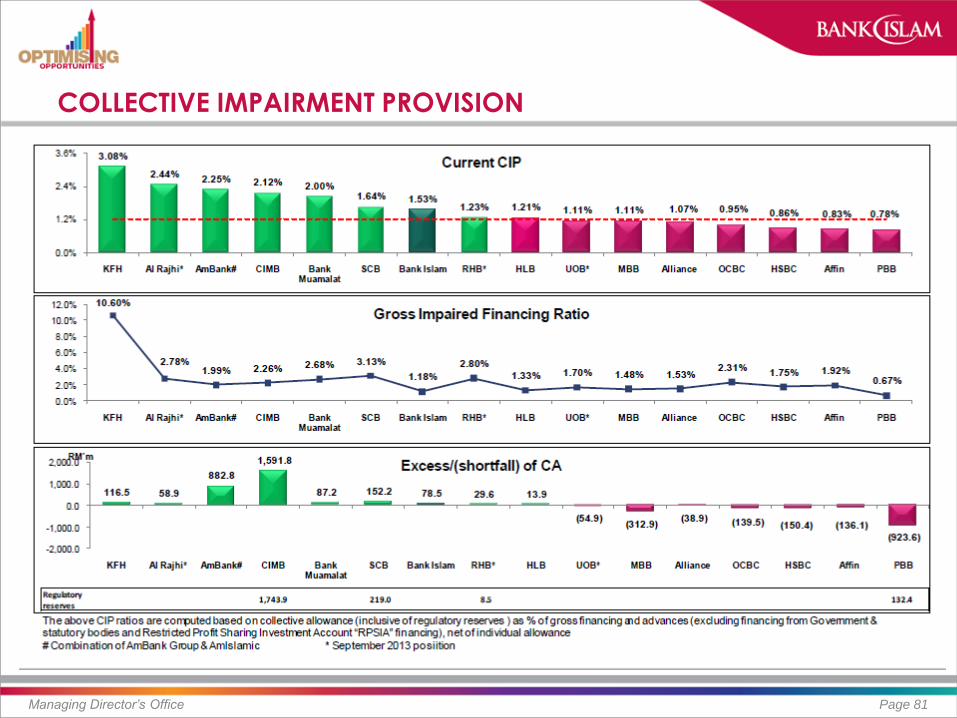

COLLECTIVE IMPAIRMENT PROVISION

Managing Director’s Office Page 81

COLLECTIVE IMPAIRMENT PROVISION FOR ISLAMIC BANKS

Managing Director’s Office Page 82

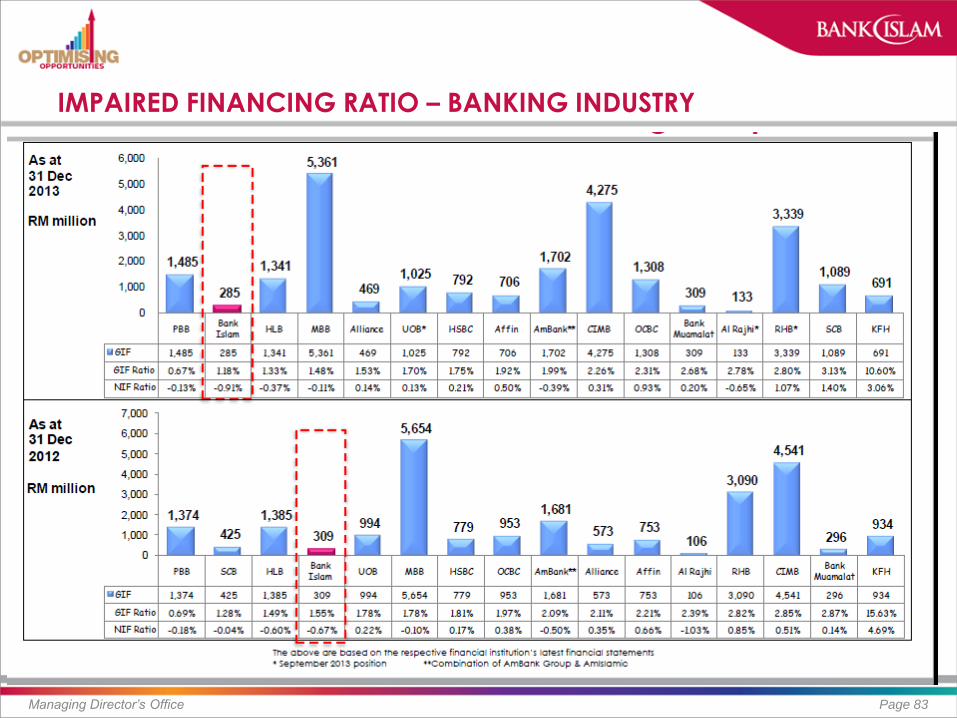

IMPAIRED FINANCING RATIO – BANKING INDUSTRY

Managing Director’s Office Page 83

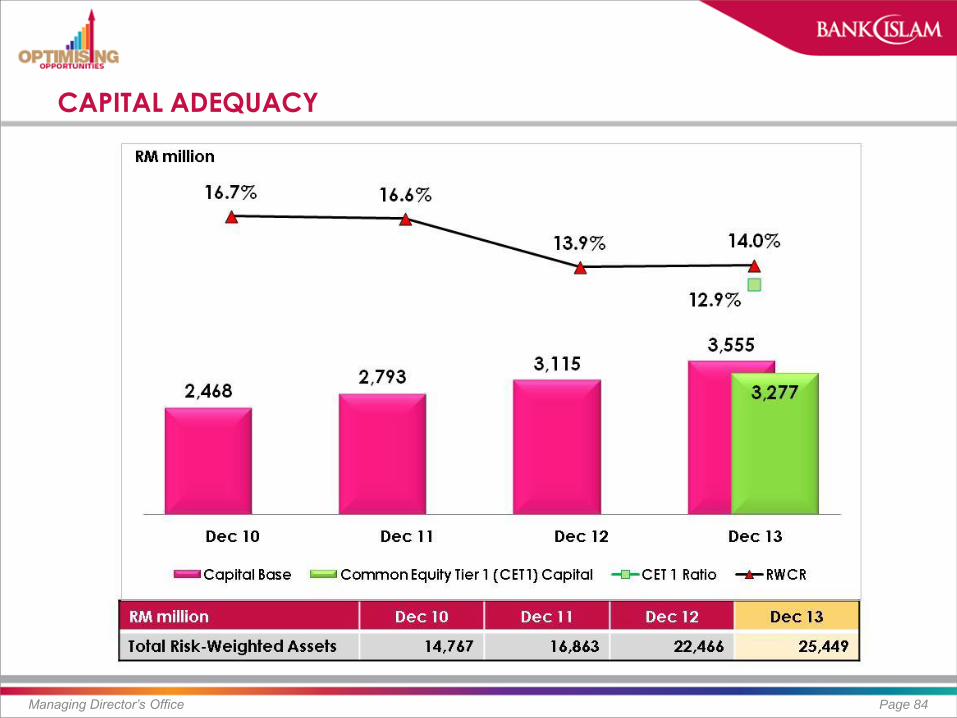

CAPITAL ADEQUACY

Managing Director’s Office Page 84

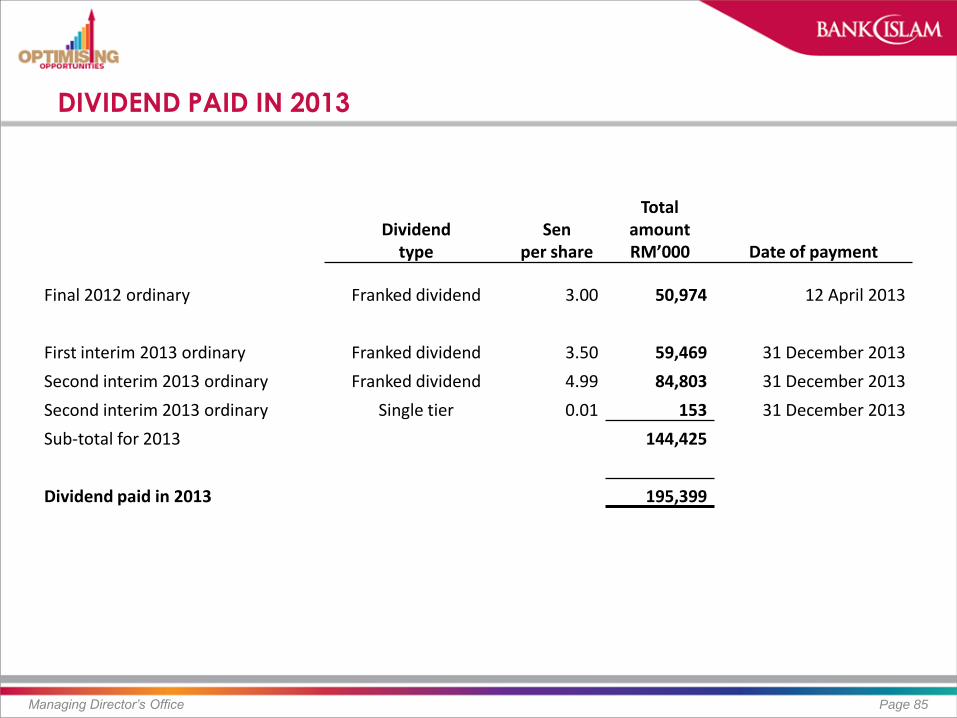

DIVIDEND PAID IN 2013

Managing Director’s Office Page 85

Dividend type

Sen per share

Total amount RM’000 Date of payment

Final 2012 ordinary Franked dividend 3.00 50,974 12 April 2013

First interim 2013 ordinary Franked dividend 3.50 59,469 31 December 2013

Second interim 2013 ordinary Franked dividend 4.99 84,803 31 December 2013

Second interim 2013 ordinary Single tier 0.01 153 31 December 2013

Sub-total for 2013 144,425

Dividend paid in 2013 195,399

ZAKAT

Managing Director’s Office Page 86

Figu

res

in R

M ‘0

00

4,885

8,934

11,575

8,081

9,251

12,584

FY2008 FY2009 FY2010* FY2011 FY2012 FY2013

* Amount for 2010 is for a period of 18 months due to change of our

financial year from 30 June to 31 December

Managing Director’s Office Page 87

ISLAMIC BANKING

LANDSCAPE

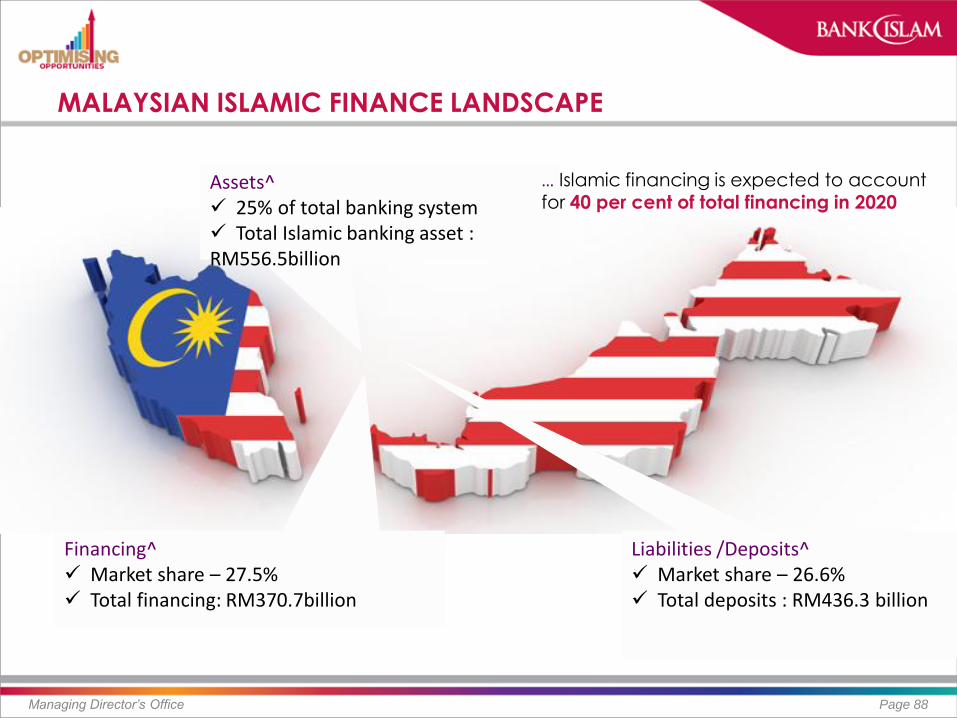

MALAYSIAN ISLAMIC FINANCE LANDSCAPE

Managing Director’s Office Page 88

Assets^ 25% of total banking system Total Islamic banking asset : RM556.5billion

Financing^ Market share – 27.5% Total financing: RM370.7billion

Liabilities /Deposits^ Market share – 26.6% Total deposits : RM436.3 billion

… Islamic financing is expected to account for 40 per cent of total financing in 2020

KEY STATISTICS OF ISLAMIC BANKING

Managing Director’s Office Page 89

Source: BNM

Chart 1: % of total banking system

19.6

20.7

22.4

23.8

25.0

21.6

22.7

24.3

25.8

27.5

20.7

22.6

24.4 25.6

26.6

15.0

17.0

19.0

21.0

23.0

25.0

27.0

29.0

2009 2010 2011 2012 2013

Total assets

Total financing

Total deposits 2.2

2.1

1.6

1.2

1.0

1.3 1.3

1.0

1.3

1.2

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2009 2010 2011 2012 2013

Net impaired

financing ratio (RHS)

Return on asset

Chart 2: ROA vs. net impaired ratio

KEY STATISTICS OF ISLAMIC BANKING…CONT

Managing Director’s Office Page 90

Chart 3: Income composition in 2013 Chart 4: Return on Equity

Fund-based income 89.3%

Fee-based income 10.7%

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013

5-yr average @ 15.7

KEY STATISTICS OF ISLAMIC BANKING…CONT

Managing Director’s Office Page 91

Source: BNM

Chart 5: Cost-to-income ratio Chart 6: # of Employee vs. Office Network

45.3%

46.7%

47.4%

50.9%

50.2%

44.0%

45.0%

46.0%

47.0%

48.0%

49.0%

50.0%

51.0%

52.0%

2009 2010 2011 2012 2013

7,829

8,515

9,214

9,751

10,205

0

500

1,000

1,500

2,000

2,500

7,500

8,000

8,500

9,000

9,500

10,000

10,500

2009 2010 2011 2012 2013

Number of employee

Office network (RHS)

GLOBAL SUKUK MARKET SHARE AS AT END OF DECEMBER 2012

Managing Director’s Office Page 92

About 58.8% of the

global outstanding

Sukuk

or RM512 billion or

USD160 bil were

originated from

Malaysia

Total global outstanding

Sukuk was worth about

US$272.1 bil

… continues to be the world largest Sukuk market

Managing Director’s Office Page 93

DEPOSIT

TRANSITION PLAN

ISLAMIC BANKING BUSINESS REFLECTIVE OF SHARIAH CONTRACTS

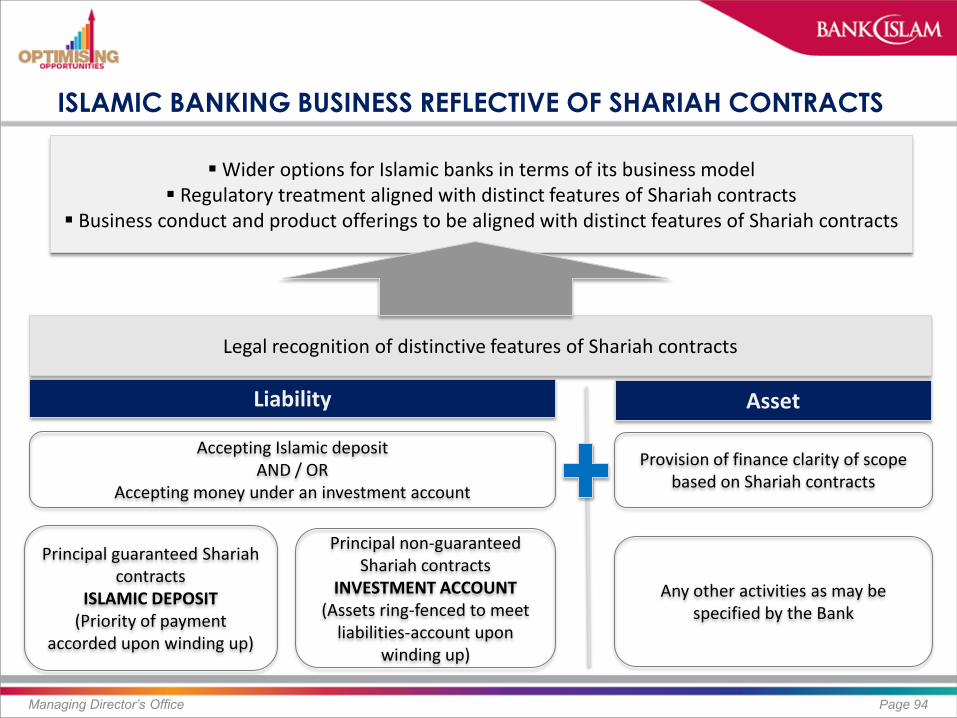

Managing Director’s Office Page 94

Wider options for Islamic banks in terms of its business model Regulatory treatment aligned with distinct features of Shariah contracts

Business conduct and product offerings to be aligned with distinct features of Shariah contracts

Liability Asset

Accepting Islamic deposit AND / OR

Accepting money under an investment account

Provision of finance clarity of scope based on Shariah contracts

Principal guaranteed Shariah contracts

ISLAMIC DEPOSIT (Priority of payment

accorded upon winding up)

Principal non-guaranteed Shariah contracts

INVESTMENT ACCOUNT (Assets ring-fenced to meet

liabilities-account upon winding up)

Any other activities as may be specified by the Bank

Legal recognition of distinctive features of Shariah contracts

RECLASSIFYING OF FUNDS

Managing Director’s Office Page 95

30 June 2013 - IFSA is effective, distinguishing Islamic deposit and Islamic investment accounts as follows:

The new IA guideline was released take effect from 14 March 2013 while the transition policy for IA will take effect commencing from 1 June 2015

Existing customers who hold Mudarabah and Wakalah based demand deposit and investment products are effected by transition plan

Islamic Deposit

Sum of money paid or accepted in accordance with Shariah

Principal is Guaranteed With or without any consideration Repayment on demand or at a certain

time

Investment Account (IA)

Money paid or accepted for purposes of investment in accordance with Shariah

Principal Non-Guaranteed With any consideration Repayment at certain time

OVERVIEW OF DEPOSIT ACCOUNTS

Managing Director’s Office Page 96

Deposit Account

Wadiah/Qard Tawarruq Bai Inah

Wadiah/Qard

No returns Marketing on services/features

i.e.: debit-card facility, access to TH account, TAP mobile banking, MEPS IBFT, etc

Tawarruq

Similar to fixed/term deposit Returns are fixed upfront as part

of murabaha structure Brokerage fees to be borne by

the Bank

OVERVIEW OF INVESTMENT ACCOUNTS (IA)

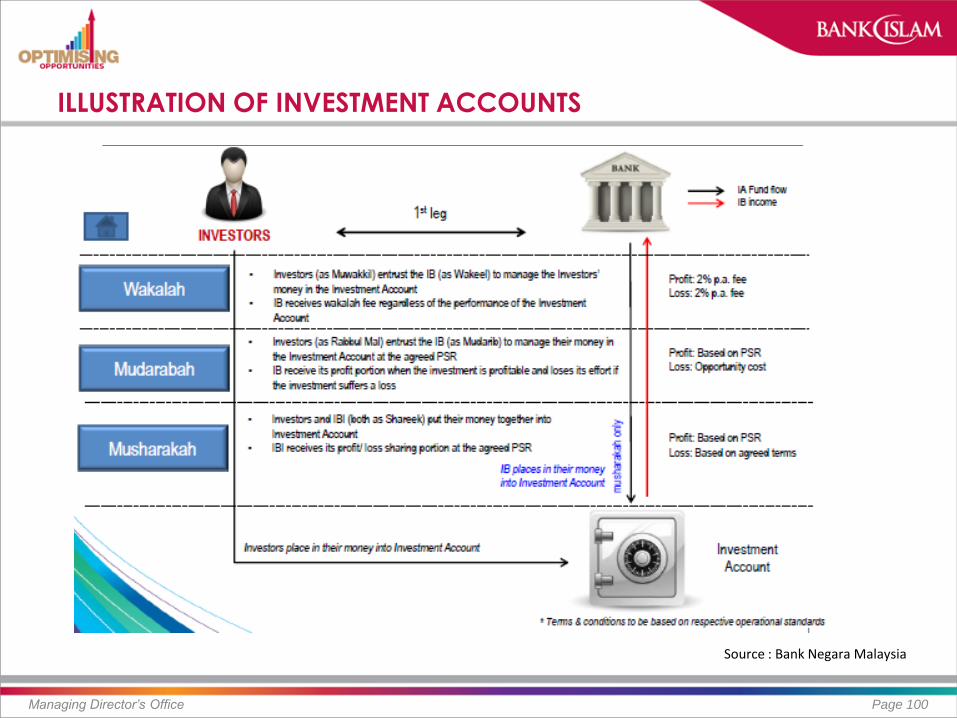

Managing Director’s Office Page 97

Investors Bank As Agent (Wakalah); or As Entrepreneur (Mudarabah); or As Business Partner (Musharakah)

Venture

1st Leg 2nd Leg

Contract under IA : Wakalah Mudarabah Musharakah

Contract between Bank and business owner Equity financing (Musharakah,

Mudarabah) Lease-based financing (Ijarah) Sale-based (Murabahah, Istisna’,

Inah) Fee based (Wakalah , Ujra’)) Guarantee (Kafalah)

Principal non-guaranteed Shariah contracts

INVESTMENT ACCOUNT (Assets ring-fenced to meet liabilities-

account upon winding up)

IA RELATIONS

Managing Director’s Office Page 98

Islamic Banking Institutions

(IBIs)

IBIs to play significant role in structuring RIA to

match investors & ventures

KEEN INVESTORS GOOD VENTURES

Retail Investors

Institutional Investors

Small Business

Established Business

Source : Bank Negara Malaysia

TYPE OF SHARIAH CONTRACTS FOR INVESTMENT ACCOUNTS

Page 99

Shariah Contract Definitions

Mudarabah

“Mudarabah”, means a contract between capital provider (rabbul mal) and an entrepreneur (mudarib) under which the rabbul mal provides capital to be managed by the mudarib based on any profit generated from the capital is shared between the rabbul mal and the mudarib according to mutually agreed profit sharing ratio (PSR) whilst financial losses are borne by the rabbul mal provided that such losses are not due to the mudarib’s misconduct (ta’adi), negligence (taqsir) or breach of specified terms (mukhafalah al-shurut).

Musharakah

“Musharakah”, means a partnership between two or more parties which may take effect through contractual relationship (‘aqd) or by operation of Islamic law, whereby all contracting parties will share the profit and bear loss from partnership.

Wakalah

“Wakalah”, means a contract in which a party (muwakkil) authorizes another party as his agent (wakil) to perform a particular task, in matters that may be delegated, either voluntarily or with imposition of fee.

Managing Director’s Office

ILLUSTRATION OF INVESTMENT ACCOUNTS

Managing Director’s Office Page 100

Source : Bank Negara Malaysia

ILLUSTRATION ON APPLICATION OF IA

Managing Director’s Office Page 101

Source : Bank Negara Malaysia

IMPACT OF INVESTMENT ACCOUNTS

Managing Director’s Office Page 102

Bank

Benefits: Cost savings from capital management - Credit and market risk

weighted assets funded by investment account (URIA or RIA) shall be excluded from the calculation of capital adequacy ratio. Zero capital charges.

All investment accounts are excluded from Eligible Liabilities (EL) base for the purposes of statutory reserve requirement (SRR) computation

Cost avoidance - Zero takaful premium for Deposit Insurance Scheme - PIDM

Drawbacks: Expected higher cost of funding Incur incidental administrative/prudential cost

IMPACT TO EXISTING CUSTOMERS

Customers whose Islamic deposit account are structured based on Shariah contract with non-principal guaranteed feature (i.e. Mudharabah Savings Account or Wakalah Deposit) will be dully informed of the alternative products and provided with sufficient information/ transparency to make an informed decision.

Customers would have a choice to either maintain their funds with Islamic deposit or change to investment account product depending on the customers’ risk appetite.

Customers will be accorded sufficient time to inform the Islamic banks of their decision by June 2014.

During the transition period, all the Islamic deposits based on Shariah contract with non-principal guarantee feature will remain status quo and continue to be eligible for PIDM protection (up to RM250K) until the completion of the transition plan.

Page 103 Managing Director’s Office

ACCOUNTING TREATMENT

Managing Director’s Office Page 104

Bank

Investors

BNM is currently facilitating the discussion with Malaysia Institute of Accountant and Malaysia Accounting Standard Board with regards to the following accounting treatment: URIA – On vs Off balance sheet Consolidation Financial Ratios Notes to the Account

Disclosure in the Account Valuation / Mark-to-market accounting

Managing Director’s Office Page 105

BUSINESS

ENVIRONMENT

THE 5 WAVES

Managing Director’s Office Page 106

Intensified Competition

Price War

Eroding Margin

War for Deposits

- Pricing of CASA

- Reclassifying Deposit & Investment

- Liquidity Management

Cost of Regulatory Compliance

New Shariah Standards, Deposit Transition Plan, PDPA, FATCA,

etc

Macro Prudential Measures

- Responsible Financing Guidelines - New Measures for Property Fin. - Stringent Provision Requirement

Scarce Capital

- BASEL III

- ICAAP

Managing Director’s Office Page 107

ECONOMIC

UPDATE

Managing Director’s Office Page 108

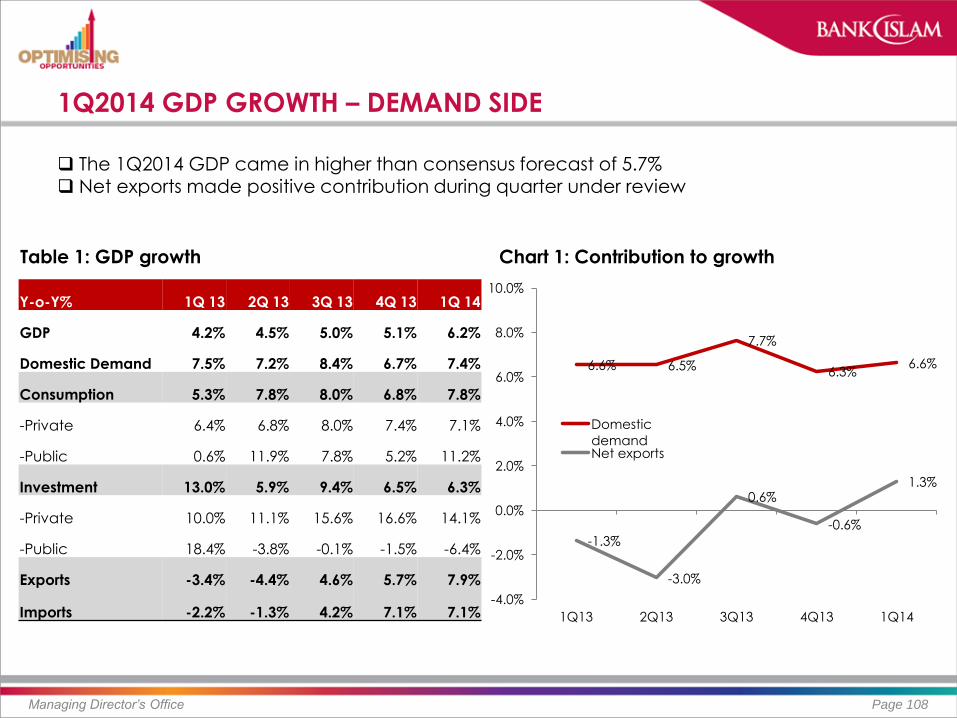

1Q2014 GDP GROWTH – DEMAND SIDE

Y-o-Y% 1Q 13 2Q 13 3Q 13 4Q 13 1Q 14

GDP 4.2% 4.5% 5.0% 5.1% 6.2%

Domestic Demand 7.5% 7.2% 8.4% 6.7% 7.4%

Consumption 5.3% 7.8% 8.0% 6.8% 7.8%

-Private 6.4% 6.8% 8.0% 7.4% 7.1%

-Public 0.6% 11.9% 7.8% 5.2% 11.2%

Investment 13.0% 5.9% 9.4% 6.5% 6.3%

-Private 10.0% 11.1% 15.6% 16.6% 14.1%

-Public 18.4% -3.8% -0.1% -1.5% -6.4%

Exports -3.4% -4.4% 4.6% 5.7% 7.9%

Imports -2.2% -1.3% 4.2% 7.1% 7.1%

6.6% 6.5%

7.7%

6.3% 6.6%

-1.3%

-3.0%

0.6%

-0.6%

1.3%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1Q13 2Q13 3Q13 4Q13 1Q14

Domestic

demand Net exports

Table 1: GDP growth Chart 1: Contribution to growth

The 1Q2014 GDP came in higher than consensus forecast of 5.7%

Net exports made positive contribution during quarter under review

1Q2014 GDP GROWTH – SUPPLY SIDE

Managing Director’s Office Page 109

YoY% 1Q 13 2Q 13 3Q 13 4Q 13 1Q 14

GDP 4.2% 4.5% 5.0% 5.1% 6.2%

Agriculture 6.2% 0.3% 2.0% 0.2% 2.3%

Mining and

Quarrying -1.4% 4.4% 1.4% -1.2% -0.8%

Manufacturing 0.4% 3.8% 4.3% 5.2% 6.8%

Construction 14.2% 10.0% 10.2% 9.8% 18.9%

Services 6.1% 5.0% 6.0% 6.4% 6.6%

-0.1%

0.0%

0.4%

1.3%

3.5%

-0.1%

0.2%

0.7%

1.7%

3.6%

-1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

Mining and Quarrying

Agriculture

Construction

Manufacturing

Services

1Q 14

4Q 13

Chart 1: Contribution to growth Table 1: GDP growth – by industry

On the supply side, growth was largely underpinned by services and manufacturing

sector

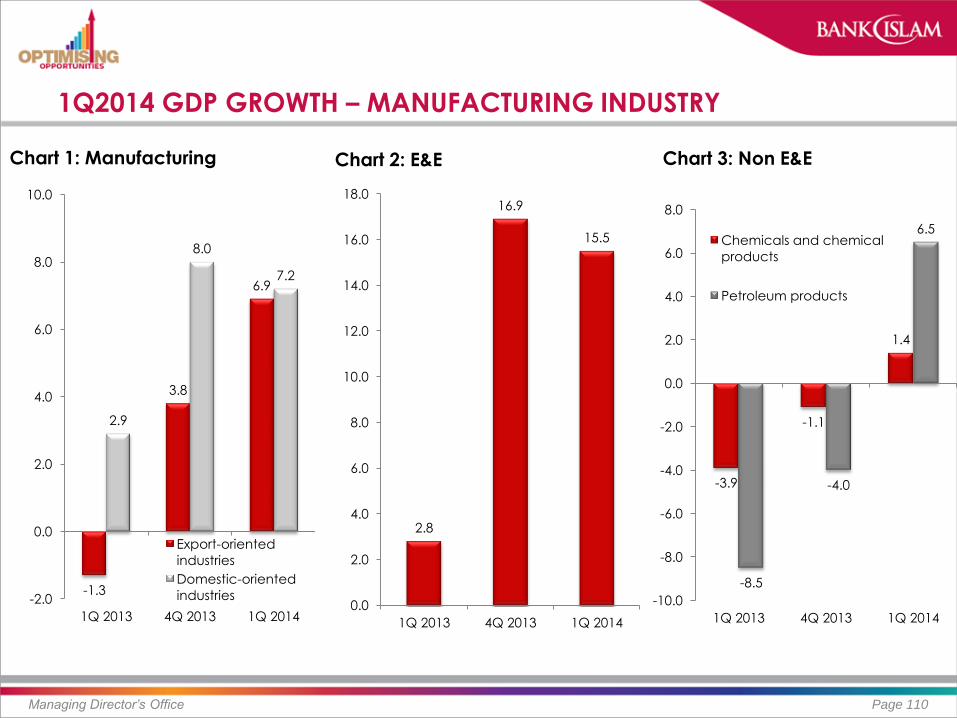

1Q2014 GDP GROWTH – MANUFACTURING INDUSTRY

Managing Director’s Office Page 110

Chart 1: Manufacturing

-1.3

3.8

6.9

2.9

8.0

7.2

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

1Q 2013 4Q 2013 1Q 2014

Export-oriented

industries

Domestic-oriented

industries

2.8

16.9

15.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1Q 2013 4Q 2013 1Q 2014

Chart 2: E&E

-3.9

-1.1

1.4

-8.5

-4.0

6.5

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

1Q 2013 4Q 2013 1Q 2014

Chemicals and chemical

products

Petroleum products

Chart 3: Non E&E

Managing Director’s Office Page 111

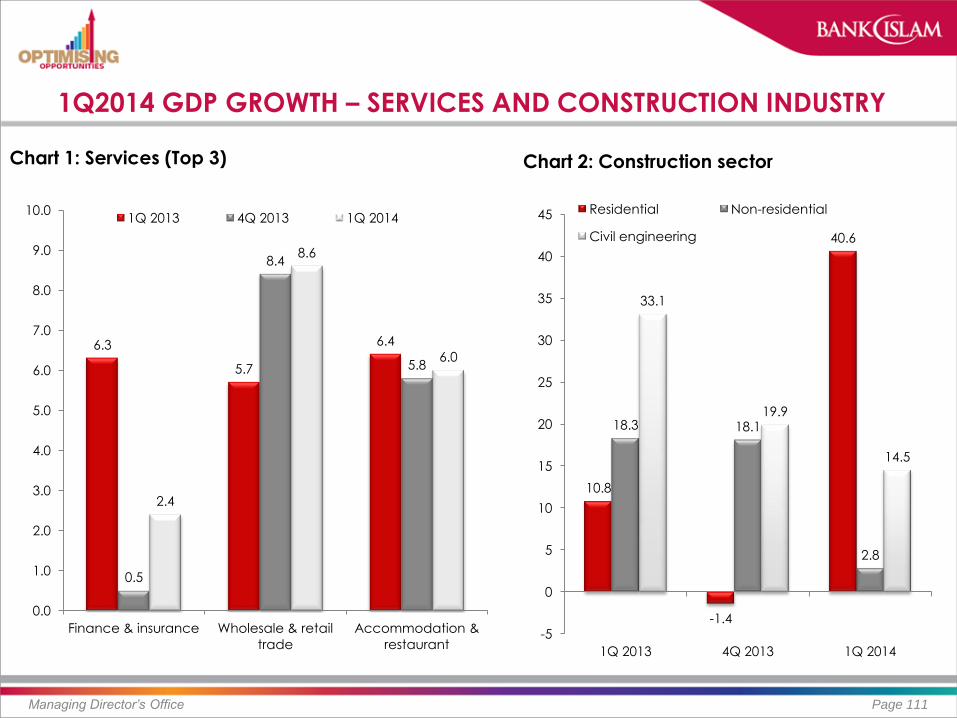

1Q2014 GDP GROWTH – SERVICES AND CONSTRUCTION INDUSTRY

Chart 1: Services (Top 3) Chart 2: Construction sector

6.3

5.7

6.4

0.5

8.4

5.8

2.4

8.6

6.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Finance & insurance Wholesale & retail

trade

Accommodation &

restaurant

1Q 2013 4Q 2013 1Q 2014

10.8

-1.4

40.6

18.3 18.1

2.8

33.1

19.9

14.5

-5

0

5

10

15

20

25

30

35

40

45

1Q 2013 4Q 2013 1Q 2014

Residential Non-residential

Civil engineering

OTHER INDICATORS

Managing Director’s Office Page 112

1Q2013 4Q2013 1Q2014

Current Account 13.2 14.8 19.8

(% of GNI) 5.8 5.8 7.9

Goods 28.0 33.3 33.6

Services -2.6 -4.1 -2.7

Primary income -8.0 -10.0 -6.4

Secondary income -4.2 -4.4 -4.6

Financial Account 1.2 -9.7 -37.6

Direct investment -2.8 -4.0 -14.6

-Assets -11.6 -6.5 -20.4

-Liabilities 8.8 10.4 5.8

Portfolio investment 3.9 -0.8 -13.4

-Assets -5.3 -5.4 -7.6

-Liabilities 9.2 4.6 -5.8

Financial derivatives 0.2 0.4 -1.5

Other investment -0.2 -13.3 -8.1

Errors & omissions -10.3 -7.8 0.4

Overall Balance 4.0 -2.7 -17.3

1Q2013 4Q2013 1Q2014

Revenue 43.8 61.1 49.2

% annual growth -8.6 6.8 12.4

Operating expenditure 49.9 58.8 55.2

% annual growth 9.4 -4.6 10.6

Current account -6.1 2.3 -6.0

% of GDP -2.6 0.9 -2.3

Net development expenditure 8.8 16.0 7.0

% annual growth 8.3 -3.4 -20.9

Overall balance -14.9 -13.8 -13.0

% of GDP -6.4 -5.2 -5.1

Total Federal Government debt

(as at end-period) 508.9 539.9 560.6

% of GDP 51.6 54.7 52.2

Domestic debt 352.2 381.5 398.5

% of GDP 35.7 38.7 37.1

External debt 156.7 158.4 162.1

% of GDP 15.9 16.1 15.1

Balance of payment (RM bn) Federal government finance (RM bn)

CAPITAL FLOWS IN MALAYSIA

Managing Director’s Office Page 113

-3.0

0.9 0.6

-6.3

-2.8

-5.6 -3.4

0.4

2.8

-10.0

-5.0

0.0

5.0

1H Dec 13 2H Dec 13 1H Jan 14 2H Jan 14 1H Feb 14 2H Feb 14 1H Mar 14 2H Mar 14 1H April 14

-1930.1

-989.7

-1653.6

-710.1

668.5 402.4

-2500

-2000

-1500

-1000

-500

0

500

1000

Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14

Chart 1: Fortnightly changes in international reserve assets (RM billion)

Chart 2: Net (sales) or purch. by foreign investors in equities market (RM Mil)

Sources: CEIC, BNM & MIDF Research

MALAYSIA – HOUSEHOLD LOAN GROWTH REMAINED STEADY

Managing Director’s Office Page 114

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

Total loans

Household Sector

Business loans

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Mar-12 Jul-12 Nov-12 Mar-13 Jul-13 Nov-13 Mar-14

Purchase of residential properties

Purchase of transport vehicle - passenger cars

Credit card

Chart 1: System loan growth y-o-y% Chart 2: Household loan growth

Source: CEIC

The current trend suggests further tightening in lending practices is on the horizon

INCOME PROFILE FOR THE MASS AFFLUENT

Managing Director’s Office Page 115

Source: World Top Income Data Base & DOS

22.53 24.65 24.18

8.18 9.42 9.33

0

5

10

15

20

25

30

Y00 Y05 Y10

Top 10% income share Top 1% income share

3,808 5,545 5,172

6,516 7,444

11,705

18,276 18,793

24,910

28,736

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Y85 Y95 Y00 Y05 Y10

Top 10% Top 1%

Chart 2: Average monthly income

2009 2012 chg

Total 5.9 9.7 3.8

Bumiputera 4.5 7.4 2.9

Chinese 9.3 15.4 6.1

India 6.1 10.2 4.1

Others 7.4 4.9 -2.5

Table 1: % of income distribution for RM 10,000 and above

Chinese remained the at the top spot in

terms of percentage of those who earned RM10,000 and above followed by India and Bumiputera.

Chart 1: Share of income (%)

Q & A SESSION

Managing Director’s Office Page 116

Originating Department Page 117