Embed Size (px)

Citation preview

GCEAS and A Level Specification

Accounting For exams from June 2014 onwards

For certification from June 2014 onwards

1

GCE Accounting for exams from June 2014 onwards (version 1.3)

Contents

1 Introduction 2 1.1 Why choose AQA? 2

1.2 Why choose Accounting? 2

1.3 HowdoIstartusingthisspecification? 3

1.4 HowcanIfindoutmore? 3

2 SpecificationataGlance 4

3 Subject Content 63.1 Unit1–ACCN1 IntroductiontoFinancialAccounting 6

3.2 Unit2–ACCN2 FinancialandManagementAccounting 8

3.3 Unit3–ACCN3 FurtherAspectsofFinancialAccounting 10

3.4 Unit4–ACCN4 FurtherAspectsofManagementAccounting 12

4 Scheme of Assessment 144.1 Aims 14

4.2 Assessment objectives 14

4.3 Nationalcriteria 15

4.4 Priorlearning 15

4.5 SynopticAssessmentandStretchandChallenge 15

4.6 AccesstoAssessmentforDisabledStudents 16

5 Administration 175.1 AvailabilityofAssessmentUnitsandCertification 17

5.2 Entries 17

5.3 PrivateCandidates 17

5.4 AccessArrangementsandSpecialConsideration 17

5.5 LanguageofExaminations 18

5.6 QualificationTitles 18

5.7 AwardingGradesandReportingResults 18

5.8 Re-sitsandShelf-lifeofUnitResults 18

Appendices 19A Performance Descriptions 19

B Spiritual,Moral,Ethical,SocialandotherIssues 23

C OverlapswithotherQualifications 24

D KeySkills 25

ThisspecificationwillbepublishedannuallyontheAQAWebsite(www.aqa.org.uk).IfthereareanychangestothespecificationcentreswillbenotifiedinprintaswellasontheWebsite.TheversionontheWebsiteisthedefinitiveversionofthespecification.

Verticalblacklinesindicateasignificantchangeoradditiontothepreviousversionofthisspecification.

2

GCE Accounting for exams from June 2014 onwards (version 1.3)

1 Introduction

1

1.1 Why choose AQA?It’s a fact that AQA is the UK’s favourite exam board and more students receive their academic qualificationsfromAQAthanfromanyotherboard.ButwhydoesAQAcontinuetobesopopular?

• SpecificationsOursaredesignedtothehigheststandards,so teachers,studentsandtheirparentscanbeconfidentthatanAQAawardprovidesanaccurate measure of a student’s achievements. And the assessment structures have been designedtoachieveabalancebetweenrigour,reliabilityanddemandsoncandidates.

• SupportAQA runs the most extensive programme of supportmeetings;freeofchargeinthefirstyearsofanewspecificationandataveryreasonablecostthereafter.Thesesupportmeetingsexplainthespecificationandsuggestpracticalteachingstrategiesandapproachesthatreallywork.

• ServiceWearecommittedtoprovidinganefficientandeffective service and we are at the end of the phone when you need to speak to a person about animportantissue.Wewillalwaystrytoresolveissuesthefirsttimeyoucontactusbut,shouldthatnotbepossible,wewillalwayscomebacktoyou(bytelephone,emailorletter)andkeepworkingwithyoutofindthesolution.

• EthicsAQA is a registered charity. We have no shareholderstopay.WeexistsolelyforthegoodofeducationintheUK.Anysurplusincomeisploughedbackintoeducationalresearchandourservicetoyou,ourcustomers.Wedon’tprofitfromeducation,youdo.

If you are an existing customer then we thank you for your support. If you are thinking of moving to AQA thenwelookforwardtowelcomingyou.

1.2 Why choose Accounting?• Alargedegreeofcontinuity with the previous

specification

• Astudyofbothfinancial accounting and management accounting at both AS and A2

• Accessiblequestionswithinthewrittenpapersenablingcandidatestodemonstratethefullextentof their achievements

• Arangeofquestiontypeswithinwrittenpapersinvolvingbothcomputationalandproseanswers,withtheemphasisonthecomputational

• AnAccountingspecificationwhichcanbeofferedasacoherent,self-standingAScourseand which alsoprovidesalogicalprogressiontoA2intermsofknowledge,understandingandskills.

3

GCE Accounting for exams from June 2014 onwards (version 1.3)

1

1.3 HowdoIstartusingthisspecification?Already using the existing AQA GCE Accounting specification? • Registertoreceivefurtherinformation,suchas

markschemes,pastquestionpapers,detailsofteachersupportmeetings,etc,at http://www.aqa.org.uk/rn/askaqa.php Informationwillbeavailableelectronicallyorinprint,foryourconvenience.

• Tellusthatyouintendtoentercandidates.Wecan thenmakesurethatyoureceiveallthematerialyouneedfortheexaminations.Thisisparticularlyimportantwhereexaminationmaterialisissuedbeforethefinalentrydeadline.YoucanletusknowbycompletingtheappropriateIntentiontoEnterandEstimatedEntryforms.WewillsendcopiestoyourExamsOfficerandtheyarealsoavailableonourwebsite http://www.aqa.org.uk/admin/p_entries.html

Not using the AQA specification currently?• AlmostallcentresinEnglandandWalesuseAQA

or have used AQA in the past and are approved AQAcentres.Asmallminorityarenot.IfyourcentreisnewtoAQA,pleasecontactourcentreapprovalteamat [email protected]

Ask AQA Youhave24-houraccesstousefulinformationandanswerstothemostcommonlyaskedquestionsathttp://www.aqa.org.uk/rn/askaqa.php

Iftheanswertoyourquestionisnotavailable,you cansubmitaqueryforourteam.Ourtargetresponse time is one day.

Teacher SupportDetailsofthefullrangeofcurrentTeacherSupportmeetingsareavailableonourwebsiteat http://www.aqa.org.uk/support/teachers.html

ThereisalsoalinktoourfastandconvenientonlinebookingsystemforTeacherSupportmeetingsathttp://events.aqa.org.uk/ebooking

IfyouneedtocontacttheTeacherSupportteam,[email protected]

1.4 HowcanIfindoutmore?

4

GCE Accounting for exams from June 2014 onwards (version 1.3)

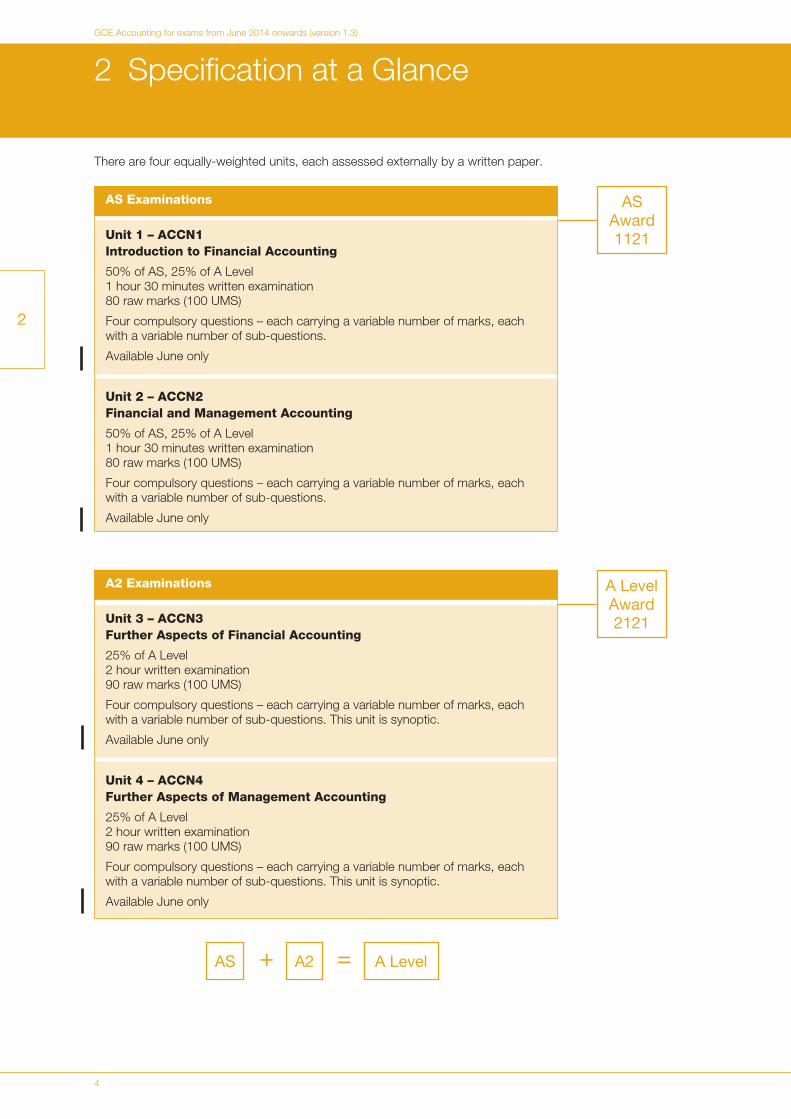

2 SpecificationataGlance

2

AS Examinations

Unit 1 – ACCN1Introduction to Financial Accounting

50%ofAS,25%ofALevel 1 hour 30 minutes written examination 80rawmarks(100UMS)

Fourcompulsoryquestions–eachcarryingavariablenumberofmarks,eachwithavariablenumberofsub-questions.

AvailableJuneonly

Unit 2 – ACCN2Financial and Management Accounting

50%ofAS,25%ofALevel 1 hour 30 minutes written examination 80rawmarks(100UMS)

Fourcompulsoryquestions–eachcarryingavariablenumberofmarks,eachwithavariablenumberofsub-questions.

AvailableJuneonly

AS Award 1121

A2 Examinations

Unit 3 – ACCN3 Further Aspects of Financial Accounting

25%ofALevel 2 hour written examination 90rawmarks(100UMS)

Fourcompulsoryquestions–eachcarryingavariablenumberofmarks,eachwithavariablenumberofsub-questions.Thisunitissynoptic.

AvailableJuneonly

Unit 4 – ACCN4 Further Aspects of Management Accounting

25%ofALevel 2 hour written examination 90rawmarks(100UMS)

Fourcompulsoryquestions–eachcarryingavariablenumberofmarks,eachwithavariablenumberofsub-questions.Thisunitissynoptic.

AvailableJuneonly

A Level Award 2121

Therearefourequally-weightedunits,eachassessedexternallybyawrittenpaper.

+AS A2 = A Level

5

GCE Accounting for exams from June 2014 onwards (version 1.3)

2

ChangesrequiredbyQCA’ssubjectcriteriainclude:

• movingfromsixunitstofourunits

• providinggreater‘stretchandchallenge’forcandidates,particularlythemostable.

Other changesinclude:

• bringingthesubjectcontentuptodatewiththecurrent accounting environment

• movingcertainaspectsofthesubjectcontentbetweenunitsforgreaterbalanceandcoherence

• discontinuingModule2fromthepreviousspecificationwhichhadbeenavailableasanalternativetoModule1,butretainingitscontentwithin other units

• reducingtheoverallcontenttoensuremanageability

• providingcandidateswithamoregeneroustimeallocationintheexaminationsothatanswerscanbe more considered.

Candidatestakingthisspecificationshould:

• developknowledgeandunderstandingofthepurposesofaccounting,itsconcepts,techniquesand procedures

• applythisknowledgeandunderstandingtoavarietyofaccountingproblems

• developanappreciationoftheroleandlimitationsofaccountingindecision-making

• analyse,interpretandevaluateaccountinginformation,assessalternativecoursesofactionand make reasoned judgements taking into considerationeconomic,legal,technologicalandsocialfactors.

Thespecificationalsoencouragescandidatestoacquirearangeofimportant and transferable skills:

• dataskills:candidateswillbeexpectedtomanipulatedatainavarietyofformsandtointerprettheirresults

• presentingargumentsandmakingjudgementsandjustifiedrecommendationsonthebasisoftheavailableevidence

• recognisingthenatureofproblems,solvingproblemsandmakingdecisionsusingappropriateaccountingtoolsandmethods

• planningwork,takingintoaccountthedemandsofthetaskandthetimeavailabletocompleteit.

6

GCE Accounting for exams from June 2014 onwards (version 1.3)

3 Subject Content

3

3.1 ASUnit1ACCN1IntroductiontoFinancialAccounting

Thisunitisdesignedasafoundationforthecourseandcoversdouble-entryproceduresasappliedtotheaccountingsystemsofsoletraders.

Candidatesshoulddevelopanunderstandingofhowthedouble-entrysystemoperatesanddevelopskillsinkeepingaccurateaccountingrecords.Candidatesshouldbeabletorecordavarietyoftransactions,workingfromoriginaldocumentsandusingtheappropriatebooksoforiginalentry.

Candidatesshouldbeabletoverifytheaccuracyofaccountingrecords,explainthepurposeandlimitations ofverificationtechniquesandbeabletoassesstheconsequencesoferrorsonprofitcalculationsand balancesheets.

Candidatesshouldbeabletodemonstrateanunderstandingofthecompletedouble-entryprocessbytransferringrelevantaccountstotheincomestatement(tradingandprofitandlossaccount),balancingaccountsandpreparingabalancesheetsetoutingoodform.Candidatesshouldbeabletomakestraightforwardadjustmentstoexpensesinthefinancialstatementsincludingtherecordingofdepreciationbasedonthestraight-linemethod.

Purposesofaccounting Candidatesshouldbeableto:

know and understand the reasons for keeping accounting records andthebenefitswhicharisefortheownerofabusinessandotherstakeholders.

Accountingrecords:subsidiarybooks Candidatesshouldbeableto:andledgeraccounts prepare and understand accounting records based on source documentsandusethemainsubsidiarybooksandledgeraccounts.

Note: Sourcedocumentsincludeinvoices,creditnotes,cheque

counterfoils,paying-inslipcounterfoils,cashreceipts,tillrolls,informationfrombankstatementssuchasstandingorders,directdebits,BACS,credittransfers,bankcharges.

Thesubsidiarybooksare:generaljournal,fourdaybooks,maincashbook.

Ledgeraccountsmaybesubdividedintothesales,purchaseandgeneralledgers.

CandidateswillnotberequiredtounderstandtheVATsystemormakeaccountingrecordsofVAT.Candidateswillnot be asked to prepare petty cash books.

The purpose of this statement is to clarify the position regarding the application of new International Accounting Standards (IAS) terminology.

• ThisSpecificationincludesthenewIAStermsfollowedbytheoldUKtermsinbrackets(i.e.itadoptsdualterminology).

• June 2010 onwards: the question papers and mark schemeswillincorporatedualterminologyinthefollowingstyle;New term (Old term).

• BothnewIAStermsandoldUKtermswillbeacceptedbyexaminerswhenmarkingthecandidateresponses.

7

GCE Accounting for exams from June 2014 onwards (version 1.3)

Text

3

Verificationofaccountingrecords Candidatesshouldbeableto:

verifytheaccuracyofthedouble-entryrecordsbythepreparationof trialbalances,bankreconciliationstatements,andsalesandpurchasesledgercontrolaccounts;

make entries to correct errors;

assesstheeffectoferrorsonprofitcalculationsandbalancesheets;

understandthelimitationsoftrialbalancesandcontrolaccounts.

Note: Theprocessoferrorcorrectionmayinvolvetheuseofasuspense

account.Controlaccountswillbememorandumrecordsonly.

IncomeStatements(tradingandprofit Candidatesshouldbeableto:andlossaccounts)andbalancesheets prepareincomestatements(tradingandprofitandlossaccounts)includingsimpleadjustments andbalancesheetsbytransferringrelevantaccountstotheincome

statements(tradingandprofitandlossaccounts),identifyinggrossprofitandprofit(netprofit)fortheyear;

prepareincomestatements(tradingandprofitandlossaccounts)andbalancesheetsworkingfromtrialbalancesandadditionalinformation;

preparebalancesheetswithsubheadingsfornon-current(fixed)andcurrentassets,capital,non-current(long-term)andcurrentliabilities;

makeentriesforsimpleadjustmentsforexpenseprepaymentsandaccrualsinledgeraccountsandintheincomestatements(tradingandprofitandlossaccounts)andbalancesheet;

makeentriesforbaddebtsinthesalesledgerandfinancialstatements;

make entries for depreciation in the income statement (trading and profitandlossaccount)andbalancesheetusingthestraight-linemethod.

Note: Candidateswillnotberequiredtomakeentriesforbaddebts

recoveredorprovisionsfordoubtfuldebts.Candidateswillnot be requiredtomakeledgeraccountentriesfordepreciation.

8

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

3.2 ASUnit2ACCN2FinancialandManagementAccounting

Thisunitprovidescandidateswiththeopportunitytodeveloptheirknowledgeandunderstandingoffinancialaccountingandintroducesthecandidatetosomeofthewaysinwhichfinancialaccountingcanprovidevaluableinformationformeasuringandmonitoringbusinessperformanceandforplanningfuturebusinessoperations.

Candidateswilldeveloptheirabilitytoproducefinancialstatements(finalaccounts)forsoletradersaswellaslimitedcompanies.Candidatesshouldbeabletomakemorecomplexadjustmentstofinancialstatements.Inaddition,candidatesshouldbeabletodemonstrateanunderstandingoftheconceptswhichunderliethepreparationoffinancialstatementsandtoexplainhowtheseareappliedtoavarietyofsituations.

Candidatesareexpectedtounderstandhowthefinancialstructureofalimitedcompanydiffersfromthatofasoletraderandapartnership,andhowownershipandcontrolareseparated.Candidatesshouldappreciatewhy these forms of ownership are appropriate in certain circumstances.

Candidatesshouldbeabletoreportontheperformanceofsoletradersandlimitedcompaniesbyevaluatingtheirfinancialstrengthsandweaknesses.Candidatesshouldbeabletosupporttheircommentswithevidencebasedonratioanalysisfocusingonissuesofprofitabilityandliquidity.Candidatesshouldbeabletorecommendcoursesofactionwhichwillbenefitthebusinessandexplaintheconsequencesoffailingtotakeremedialaction.

Candidatesshouldbeabletodemonstrateanunderstandingofthepurposesofbudgetingandbeabletoprepare cash budgets.

Note:Candidateswillnot be expected to prepare manufacturing accounts (this topic is covered in Unit 4).

Typesofbusinessorganisation Candidatesshouldbeableto:

compare the advantages and disadvantages of different types of ownership.

Note: Typesofownershipincludesoletraders,partnershipsandlimited

companies.However,candidateswillnot be expected to prepare the accounts of partnerships (this topic is covered in Unit 3).

Accountingconcepts Candidatesshouldbeableto:

demonstrateanunderstandingofgenerallyappliedaccountingconcepts;

explainhowaccountingconceptsareappliedtoavarietyofsituationsincludingthepreparationoffinancialstatements,assetvaluation,depreciationofnon-current(fixed)assets,inventories(stock)usingcostornetrealisablevalueasthebasisofvaluation.

Note: Theconceptstobecoveredare:cost,goingconcern,accruals,

consistency,prudence,materiality,realisation,businessentityandobjectivity.

Furtheraspectsofthepreparationof Candidatesshouldbeableto:thefinancialstatementsandbalance preparethefinancialstatementsandbalancesheetsofsoletraders, sheetsofsoletraders makingadjustmentsforbaddebtsrecovered,incomedueand receivedinadvance,provisionsfordoubtfuldebts;

demonstrate an understanding of the reasons for providing for depreciationandofreducingbalanceaswellasstraight-linemethodsof depreciation;

makeappropriateentriesinledgeraccountsforadjustmentsincludingtheuseofaccountsforprovisionsfordepreciation,andaccountforthedisposalofnon-current(fixed)assets;

distinguishbetweencapitalandrevenueexpenditureandincome.

9

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

Financialstatementsoflimited Candidatesshouldbeableto:companies explainthemeaningoflimitedliability,authorisedcapital,issued

capital,ordinaryandpreferenceshares,capitalandrevenuereserves,shareholders’funds,loancapital;

evaluatesharesandloancapitalassourcesoffinance;

preparetheinternalfinancialstatementsoflimitedcompanies,identifyingprofitfromoperations,makingentriesfordividends,sharepremiums,provisionfortaxation;

accountfortherevaluationofnon-current(fixed)assets;

explainthedifferencebetweenarightsissueandabonusissueofshares,andrecordtheeffectofsuchtransactionsonthefinancialstatement.

Note: Candidateswillnotbeexpectedtoprepareanappropriationaccount

butcouldbeaskedtoprepareastatementshowingall changes in equity.

Candidateswillnotbeexpectedtomaketaxcalculations.Candidateswillnotberequiredtomakeledgerentriesfortheissueofshares.

Ratioanalysisandtheassessmentof Candidatesshouldbeableto:business performance calculateandexplainthesignificanceofgrossprofitmargin,mark-up,

rateofinventory(stock)turnover,overheadsinrelationtorevenue(turnover),profitinrelationtorevenue(turnover),returnoncapitalemployed,netcurrentasset(current)ratio,liquidcapital(acidtest)ratio,receivabledays(debtorcollectionperiod)andpayabledays(creditorpaymentperiod),gearing;

analysethefinancialstatementsofsoletradersandlimitedcompanies,andcommentontheperformanceofbusinessesmakingcomparisonswithotherbusinesses,ofoneaccountingperiodwithanotherandwithcompetitorsfocusingontheissuesofprofitability,liquidityandcapitalstructure;

developanunderstandingofthedifferencebetweencashandprofitsandtheeffectoftransactionsonprofitabilityandliquidity;

explainthelimitationsoffinancialstatementsandratioanalysiswhenassessing business performance.

Introductiontobudgetingand Candidatesshouldbeableto:budgetarycontrol understand the need for budgeting in business organisations and be

abletoexplainthebenefitsofbudgetarycontrol,butalsobeawareofitslimitations;

prepare cash budgets.

Note: OtherbudgetswillbecoveredinUnit4.

TheimpactofICTinaccounting Candidatesshouldbeableto:

demonstrateanawarenessofthemainapplicationsofICTinaccounting,forexampleindouble-entryrecordkeeping,inventory(stock)records,receivables(debtor)analysis,preparationofbudgets;

explaintheadvantagesanddisadvantagesofICTinaccounting.

Note: CandidateswillnotbeexpectedtouseICTintheexamination,nor

aretheyexpectedtohaveaknowledgeofanyspecificspreadsheetoraccountingpackage,buttheyshouldhaveageneralunderstandingof what can be achieved with various types of software.

3.3 A2Unit3ACCN3FurtherAspectsofFinancialAccounting

Inthisunit,candidateswillhavetheopportunitytodeveloptheirunderstandingoffinancialaccountingtechniqueswhichcanbeappliedwhereabusinessdoesnotmaintainacompleteaccountingsystem.Candidateswillalsohavetheopportunitytodevelopanunderstandingofthetechniquesandprocedureswhicharerelevanttopartnerships.Candidateswillalsodevelopfurthertheirunderstandingoffinancialaccountinginrelationtolimitedcompaniesbydevelopinganunderstandingofthecontentofpublishedaccountsandtheirimportancetovarioususergroups.Candidateswillbeabletoextendtheirrangeofadvancedtechniquesandknowledgeofaccountingbythestudyofstatementsofcashflowandinternationalaccountingstandards.

Note:Candidateswillnotberequiredtoprepareorcommentonfinancialstatementsfornot-for-profitorganisations.

Sources offinance Candidatesshouldbeableto:

assessdifferenttypesofbusinessfinanceincludinginternalfinance,shares,debentures,bankloansandoverdrafts,andmortgages.

Note: Candidateswillnotbeexpectedtoassesshirepurchaseorleasing

asformsoffinance.

Incompleterecords Candidatesshouldbeableto:

prepareastatementofaffairsandcalculateprofitorlossfromchangesincapitalovertime;

calculatecreditsalesandpurchasesusingtotalaccounts;

calculatemissingfiguresusingmarkupormargin;

preparefinancialstatements(finalaccounts)basedonincompleterecords;

assessthedrawbacksofmaintaininglimitedaccountingrecords;

commentonendofyearfinancialstatementsbasedonincompleterecords.

Partnershipaccounts Candidatesshouldbeableto:

prepareandcommentontheendofyearfinancialstatementsforpartnerships,includingappropriationaccounts;

preparecapitalandcurrentaccountsofpartners;

accountforchangesinapartnership,includingchangesinprofit-sharing,revaluationofassetsincludinggoodwill,retirementofapartner,admissionofapartneranddissolutionofapartnership(includingtherulinginGarnerv.Murray).

Note: Candidatesshouldunderstandthecircumstancesunderwhich

partnersmaychoosetohaveonlycapitalaccountstorecordtheirrelationshipwiththefirm,andbeabletopreparetheseaccounts;candidatesshouldknowandbeabletoapplythetermsofthePartnershipAct1890inrelationtosharingprofitsandlosses;candidatesshouldbeabletodistinguishbetweenapartner’sloanandcapital,andaccountforthese.Questionswillnot be set on piecemealdissolutionofpartnershipsnor the conversion of a partnershiptoalimitedcompany.

10

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

11

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

Publishedaccountsoflimitedcompanies Candidatesshouldbeableto:

identifythemainelementsofpublishedreportsandexplainwhylimitedcompaniesarerequiredtopublishtheiraccounts;

demonstrateaknowledgeofthecorporatereportrequirementsofdifferentusergroupsandexplainthevalueofpublishedaccountstothese groups;

demonstrateanawarenessofthelimitationsofpublishedfinancialstatements;

prepareschedulesofnon-current(fixed)assets;

prepareastatementofcashflows;

commentoncashflowstatementsandexplaintheirvaluetopotentialuser groups;

explainthedifferencebetweenthedutiesofthedirectorsandauditors with regard to the accounts.

Note: Candidateswillnotbeexpectedtopreparefinancialstatements

inaformsuitableforpublication,ornotestotheaccountsotherthanschedulesofnon-current(fixed)assets,norhaveadetailedknowledgeofformats.

Usergroupsincludeshareholders,loanstockholders,creditors,employees,potentialinvestors,analysts,etc.

StatementsofcashflowsshouldbepreparedusingtheindirectmethodfollowingtheformatgiveninIAS7.

Candidateswillnotberequiredtocalculateorcommentondividendspershare,dividendyield,dividendcoverandprice/earningsratios.

Questionswillnotbesetrequiringaknowledgeofgroupaccounts.

InternationalAccountingStandards Candidatesshouldbeableto:

explainandcommentonthepurposeandimportanceofthefollowinginternationalaccountingstandards:

IAS1 Presentationoffinancialstatements IAS 2 Inventories IAS7 Statementofcashflows IAS8 Accountingpolices,changesinaccountingestimates

and errors IAS 10 Events after the reporting period IAS16 Property,plantandequipment IAS18 Revenue IAS 36 Impairment of assets IAS37 Provisions,contingentliabilitiesandcontingentassets IAS38 Intangibleassets.

Note: Candidateswillnotbeexpectedtohaveadetailedknowledgeofany

particularaccountingstandard(otherthanIAS7).

FurtherinformationaboutthistopicisgivenintheTeachers’Guide.

Inventory(Stock)valuation Candidatesshouldbeableto:

usetheFIFOandAVCOmethodsofdetermininginventoryvaluesandexplainwhydifferentinventoryvaluationmethodsproducedifferentprofitfiguresintheshortterm;

reconcileinventoryvalueswithactualinventories.

Note: CandidateswillnotbeexpectedtousetheLIFOmethodofinventory

valuation.

3.4 A2Unit4ACCN4FurtherAspectsofManagementAccounting

Thisunitprovidesanopportunityforcandidatestodevelopfurtherthewaysinwhichaccountingtechniquescanbeusedtoaidthemanagementofabusinessandcontributetoeffectivedecision-making.

Candidateswilldevelopanunderstandingofmanufacturingaccountsandcertaincostconcepts,includingcontribution,overheadabsorption,activitybasedcosting,standardcostingandvarianceanalysis.

Theunitprovidesanopportunitytodeveloptwotechniquesformakingcapitalinvestmentdecisionsanddevelopfurthertheirunderstandingofsourcesoffinance.

Candidateswilldevelopfurthertheirunderstandingofbudgetingandbudgetarycontrol.

Candidateswillbeexpectedtoconsidersocialaccountingfactorswhenmakingdecisions.

Manufacturingaccounts Candidatesshouldbeableto:

prepareandcommentonthefinancialstatements(finalaccountsandbalancesheet)ofmanufacturingorganisations,calculateprimecosts,overheadcost,factorycostoffinishedgoods,profitonmanufacture,andmakeprovisionsforunrealisedprofit.

Marginal,absorptionandactivity Candidatesshouldbeableto:based costing explainthetermsdirectcosts,indirectcosts,variablecosts,

semi-variablecosts,fixedcosts,marginalcost,contributionandbreak-even;

calculatethebreak-evenpointbyuseofformulae,andexplainthelimitationsofbreak-evenanalysisbyformulaandgraph;

explainthetermabsorptioncostingandbeabletocompareabsorptionandmarginalcosting,identifyingtheirusesandlimitations;calculateprofitusingmarginalcostingandabsorptioncosting;

explainthetermcostcentre,andhowtoallocateandapportioncostsincludingthoseforservicecostcentresbyeliminationmethodonly;

explainthetermactivitybasedcosting;explainandidentifycostpoolsandcostdrivers;compareabsorption,marginalandactivitybasedcosting,identifyingtheirusesandlimitations;

calculateoverheadabsorptionratesandapplythemusingthemachinehourandlabourhourmethods;

applycostconceptstopricingpolicyandbeabletocostasimpleproject;

selectandapplyrelevanttechniquesfordecision-making,includingmakeorbuy,acceptanceofadditionalwork,pricesetting,optimumuse of scarce resources.

Note: Further information about activity based costing is given in the

Teachers’Guide.

Standardcostingandvarianceanalysis Candidatesshouldbeableto:

explainthepurpose,advantagesanddisadvantagesofasystemofstandard costing;

calculateandinterpretthefollowingvariances:sales(volumeandprice);material(usageandprice);labour(efficiencyandrate);

demonstrateanunderstandingoftheinterrelationshipofvariances;

preparestatementsreconcilingbudgetedandactualfigures.

12

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

13

GCE Accounting for exams from June 2014 onwards (version 1.3)

3

Capitalinvestmentappraisal Candidatesshouldbeableto:

demonstrateanunderstandingofpaybackandnetpresentvalue(discountedcashflow)methodsofcapitalinvestmentappraisal;

calculateestimatedcashflows,andusetheseinappraisingprojectsusingeitherorbothofthemethodsspecified;

makerecommendationsastowhichprojectshouldbechosenandsupporttherecommendationwithappropriatefinancialanalysis;

assessthemethodsusedforcapitalinvestmentappraisalandtheirlimitations.

Budgeting:furtherconsiderations Candidatesshouldbeableto:

demonstrateanunderstandingofthepurposesandapplicationsofasystemofbudgetarycontrol;

prepareandcommentonpurchases,sales,production,labour,receivables(debtor)andpayables(creditor)budgetsandtheirrelationshipwiththemasterbudget;

prepareandcommentonforecastoperatingstatementsandbalancesheets.

Otherfactorsaffectingdecision-making: Candidatesshouldbeableto:socialaccounting demonstrateanawarenessofotherfactors,includingsocial

accountingfactors,tobeconsideredinmakingdecisions;

considerfactorsbeyondthefinancialrequirementsofabusiness,includingethicalfactors,andmakeacriticalassessmentofanyrecommendationsaffectingstakeholdersincludingemployees,thelocalandnationaleconomyandtheenvironment.

14

GCE Accounting for exams from June 2014 onwards (version 1.3)

4 Scheme of Assessment

4

4.1 AimsASandALevelcoursesbasedonthisspecificationshouldencouragecandidatestodevelop:

• anunderstandingoftheimportanceofeffectiveaccounting information systems and an awarenessoftheirlimitationsthroughacriticalconsiderationofcurrentfinancialissuesandmodern business practices

• anunderstandingofthepurposes,principles,conceptsandtechniquesofaccounting

• thetransferableskillsofnumeracy,communication,ICT,application,presentation,interpretation,analysisandevaluationinanaccountingcontext

• anappreciationoftheeffectsofeconomic,legal,ethical,social,environmentalandtechnologicalinfluencesonaccountingdecisions

• acapacityformethodicalandcriticalthoughtwhichwouldserveasanendinitself,aswellasabasisfor further study of accounting and other subjects.

4.2 Assessment Objectives (AOs)TheAssessmentObjectivesarecommontoASandALevel.TheassessmentunitswillassessthefollowingAssessment Objectives in the context of the content andskillssetoutinSection3(SubjectContent).

AO1 Knowledge and UnderstandingDemonstrateknowledgeandunderstandingofaccountingprinciples,conceptsandtechniques.

AO2 ApplicationSelectandapplyknowledgeandunderstandingofaccountingprinciples,conceptsandtechniquestofamiliarandunfamiliarsituations.

AO3 Analysis and EvaluationOrder,interpretandanalyseaccountinginformationinanappropriateformat.Evaluateaccountinginformation,takingintoconsiderationinternalandexternalfactorstomakereasonedjudgements,decisionsandrecommendations,andassessalternativecoursesofactionusinganappropriateformandstyleofwriting.

Quality of Written Communication (QWC)InGCEspecificationswhichrequirecandidatestoproducewrittenmaterialinEnglish,candidatesmust:

• ensurethattextislegibleandthatspelling,punctuation and grammar are accurate so that meaningisclear

• selectanduseaformandstyleofwritingappropriatetopurposeandtocomplexsubjectmatter

• organiseinformationclearlyandcoherently,usingspecialistvocabularywhenappropriate.

Inthisspecification,QWCwillbeassessedinall units. Oneachpaper,twoofthemarksforproseanswerswillbeallocatedto‘qualityofwrittencommunication’,andtwoofthemarksfornumericalanswerswillbeallocatedto‘qualityofpresentation’.Thesub-questionsconcernedwillbeidentifiedonthequestionpapers.

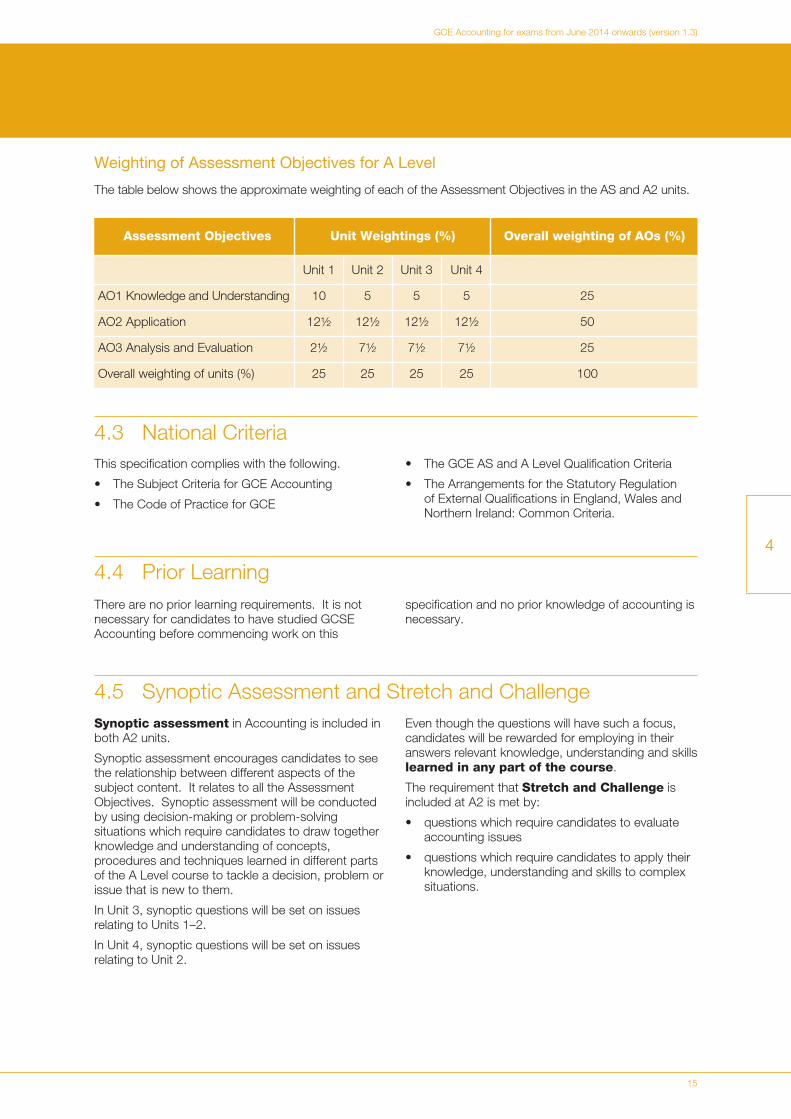

Weighting of Assessment Objectives for ASThetablebelowshowstheapproximateweightingofeachoftheAssessmentObjectivesintheASunits.

Assessment Objectives Unit Weightings (%) Overall weighting of AOs (%)

Unit 1 Unit 2

AO1KnowledgeandUnderstanding 20 10 30

AO2Application 25 25 50

AO3AnalysisandEvaluation 5 15 20

Overallweightingofunits(%) 50 50 100

15

GCE Accounting for exams from June 2014 onwards (version 1.3)

4

4.3 NationalCriteriaThisspecificationcomplieswiththefollowing.

• TheSubjectCriteriaforGCEAccounting

• TheCodeofPracticeforGCE

• TheGCEASandALevelQualificationCriteria

• TheArrangementsfortheStatutoryRegulationofExternalQualificationsinEngland,WalesandNorthernIreland:CommonCriteria.

4.4 PriorLearningTherearenopriorlearningrequirements.Itisnotnecessary for candidates to have studied GCSE Accounting before commencing work on this

specificationandnopriorknowledgeofaccountingisnecessary.

4.5 SynopticAssessmentandStretchandChallengeSynoptic assessmentinAccountingisincludedinboth A2 units.

Synoptic assessment encourages candidates to see therelationshipbetweendifferentaspectsofthesubjectcontent.ItrelatestoalltheAssessmentObjectives.Synopticassessmentwillbeconductedbyusingdecision-makingorproblem-solvingsituationswhichrequirecandidatestodrawtogetherknowledgeandunderstandingofconcepts,proceduresandtechniqueslearnedindifferentpartsoftheALevelcoursetotackleadecision,problemorissue that is new to them.

InUnit3,synopticquestionswillbesetonissuesrelatingtoUnits1–2.

InUnit4,synopticquestionswillbesetonissuesrelatingtoUnit2.

Eventhoughthequestionswillhavesuchafocus,candidateswillberewardedforemployingintheiranswersrelevantknowledge,understandingandskillslearned in any part of the course.

TherequirementthatStretch and Challenge is includedatA2ismetby:

• questionswhichrequirecandidatestoevaluateaccounting issues

• questionswhichrequirecandidatestoapplytheirknowledge,understandingandskillstocomplexsituations.

Weighting of Assessment Objectives for A Level

ThetablebelowshowstheapproximateweightingofeachoftheAssessmentObjectivesintheASandA2units.

Assessment Objectives Unit Weightings (%) Overall weighting of AOs (%)

Unit 1 Unit 2 Unit 3 Unit 4

AO1KnowledgeandUnderstanding 10 5 5 5 25

AO2Application 12½ 12½ 12½ 12½ 50

AO3AnalysisandEvaluation 2½ 7½ 7½ 7½ 25

Overallweightingofunits(%) 25 25 25 25 100

16

GCE Accounting for exams from June 2014 onwards (version 1.3)

4

4.6 AccesstoAssessmentforDisabledStudentsAS/ALevelsoftenrequireassessmentofabroaderrangeofcompetences.Thisisbecausetheyare generalqualificationsand,assuch,preparecandidates for a wide range of occupations and higherlevelcourses.

TherevisedAS/ALevelqualificationandsubjectcriteria were reviewed to identify whether any of the competencesrequiredbythesubjectpresentedapotentialbarriertoanydisabledcandidates.Ifthiswasthecase,thesituationwasreviewedagaintoensurethatsuchcompetenceswereincludedonlywhereessentialtothesubject.Thefindingsofthisprocesswerediscussedwithdisabilitygroupsandwithdisabledpeople.

Reasonableadjustmentsaremadefordisabledcandidatesinordertoenablethemtoaccesstheassessments.Forthisreason,veryfewcandidateswillhaveacompletebarriertoanypartoftheassessment.

Candidateswhoarestillunabletoaccessa significantpartoftheassessment,evenafterexploringallpossibilitiesthroughreasonableadjustments,maystillbeabletoreceiveanaward.Theywouldbegivenagradeonthepartsoftheassessmenttheyhavetakenandtherewouldbeanindicationontheircertificatethatnotallthecompetenceshadbeenaddressed.Thiswillbekeptunder review and may be amended in the future.

17

GCE Accounting for exams from June 2014 onwards (version 1.3)

5 Administration

5

5.3 PrivateCandidatesThisspecificationisavailabletoprivatecandidates.Aswewillnolongerbeprovidingsupplementaryguidanceinhardcopy,seeourwebsiteforguidanceand information on taking exams and assessments as aprivatecandidate:

www.aqa.org.uk/exams-administration/entries/private-candidates

5.2 EntriesPleaserefertothecurrentversionofEntry Procedures and Codes for up to date entry procedures.Youshouldusethefollowingentrycodesfortheunitsandforcertification.

Unit 1 – ACCN1

Unit 2 – ACCN2

Unit 3 – ACCN3

Unit 4 – ACCN4

AScertification–1121

ALevelcertification–2121

5.1 AvailabilityofAssessmentUnitsandCertification

AfterJune2013,examinationsandcertificationfor thisspecificationareavailableinJuneonly.

5.4 AccessArrangementsandSpecialConsiderationWehavetakennoteofequalityanddiscriminationlegislationandtheinterestsofminoritygroupsindevelopingandadministeringthisspecification.

WefollowtheguidelinesintheJointCouncilforQualifications(JCQ)document:Access Arrangements, Reasonable Adjustments and Special Consideration: General and Vocational Qualifications.ThisispublishedontheJCQwebsite(http://www.jcq.org.uk)oryoucanfollowthelinkfrom our website (http://www.aqa.org.uk).

Access ArrangementsWe can make arrangements so that candidates with disabilitiescanaccesstheassessment.Thesearrangements must be made before the examination.Forexample,wecanproduceaBraillepaperforacandidatewithavisualimpairment.

Special ConsiderationWecangivespecialconsiderationtocandidateswhohavehadatemporaryillness,injuryorindispositionatthetimeoftheexamination.Wherewedothis,itisgiven after the examination.

ApplicationsforaccessarrangementsandspecialconsiderationshouldbesubmittedtoAQAbytheExaminationsOfficeratthecentre.

18

GCE Accounting for exams from June 2014 onwards (version 1.3)

5

5.8 Re-sitsandShelf-lifeofUnitResultsUnitresultsremainavailabletocounttowardscertification,whetherornottheyhavealreadybeenused,aslongasthespecificationisstillvalid.

EachassessmentisavailableinJuneonly.Candidatesmayre-sitaunitanynumberoftimeswithintheshelf-lifeofthespecification.Thebestresultforeachunitwillcounttowardsthefinal

qualification.Candidateswhowishtorepeataqualificationmaydosobyre-takingoneormoreunits.Theappropriatesubjectawardentry,aswellastheunitentry/entries,mustbesubmittedinorderto be awarded a new subject grade.

Candidateswillbegradedonthebasisoftheworksubmitted for assessment.

5.5 LanguageofExaminationsWewillprovideunitsforthisspecificationinEnglishonly.

5.6 QualificationTitlesQualificationsbasedonthisspecificationare:

• AQAAdvancedSubsidiaryGCEinAccountingand

• AQAAdvancedLevelGCEinAccounting.

5.7 AwardingGradesandReportingResultsTheASqualificationwillbegradedonafive-pointscale:A,B,C,DandE.ThefullALevelqualificationwillbegradedonasix-pointscale:A*,A,B,C,DandE.TobeawardedanA*candidateswillneedtoachieveagradeAonthefullALevelqualificationandanA*ontheaggregateoftheA2units.

ForASandALevel,candidateswhofailtoreach theminimumstandardforgradeEwillberecorded asU(unclassified)andwillnotreceiveaqualificationcertificate.Individualassessmentunitresultswillbecertificated.

19

GCE Accounting for exams from June 2014 onwards (version 1.3)

Appendices

A

A Performance Descriptions

Theseperformancedescriptionsshowthelevelofattainment characteristic of the grade boundaries at ALevel.TheygiveageneralindicationoftherequiredlearningoutcomesattheA/BandE/UboundariesatASandA2.Thedescriptionsshouldbeinterpretedinrelationtothecontentoutlinedinthespecification;

theyarenotdesignedtodefinethatcontent.

Thegradeawardedwilldependinpracticeuponthe extent to which the candidate has met the AssessmentObjectives(seeSection4)overall.Shortcomings in some aspects of the examination maybebalancedbybetterperformancesinothers.

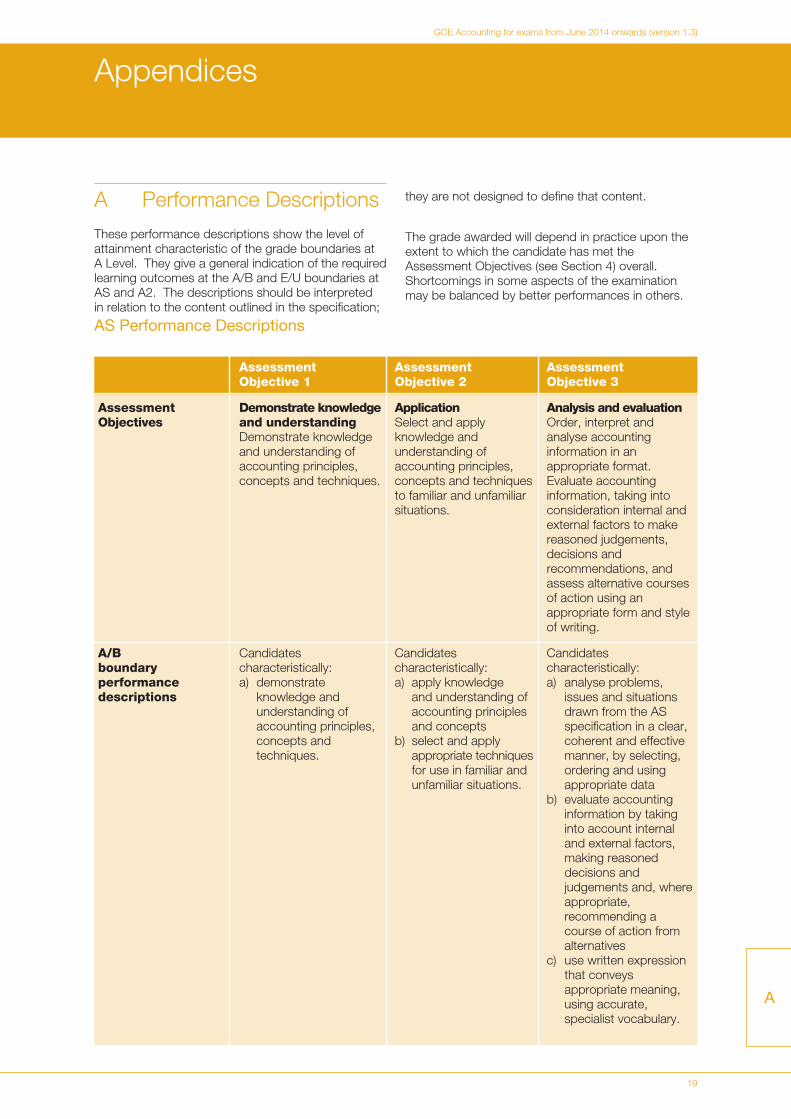

AS Performance Descriptions

Assessment Assessment Assessment Objective 1 Objective 2 Objective 3

Assessment Demonstrate knowledge Application Analysis and evaluation Objectives and understanding Selectandapply Order,interpretand Demonstrateknowledge knowledgeand analyseaccounting and understanding of understanding of information in an accountingprinciples, accountingprinciples, appropriateformat. conceptsandtechniques. conceptsandtechniques Evaluateaccounting tofamiliarandunfamiliar information,takinginto situations. considerationinternaland externalfactorstomake reasonedjudgements, decisions and recommendations,and assessalternativecourses of action using an appropriateformandstyle of writing.

A/B Candidates Candidates Candidates boundary characteristically: characteristically: characteristically: performance a) demonstrate a) applyknowledge a) analyseproblems, descriptions knowledgeand andunderstandingof issuesandsituations understandingof accountingprinciples drawnfromtheAS accountingprinciples, andconcepts specificationinaclear, conceptsand b) selectandapply coherentandeffective techniques. appropriatetechniques manner,byselecting, foruseinfamiliarand orderingandusing unfamiliarsituations. appropriatedata b) evaluateaccounting information by taking intoaccountinternal andexternalfactors, making reasoned decisions and judgementsand,where appropriate, recommending a course of action from alternatives c) use written expression that conveys appropriatemeaning, usingaccurate, specialistvocabulary.

20

GCE Accounting for exams from June 2014 onwards (version 1.3)

A

AS Performance Descriptions, continued

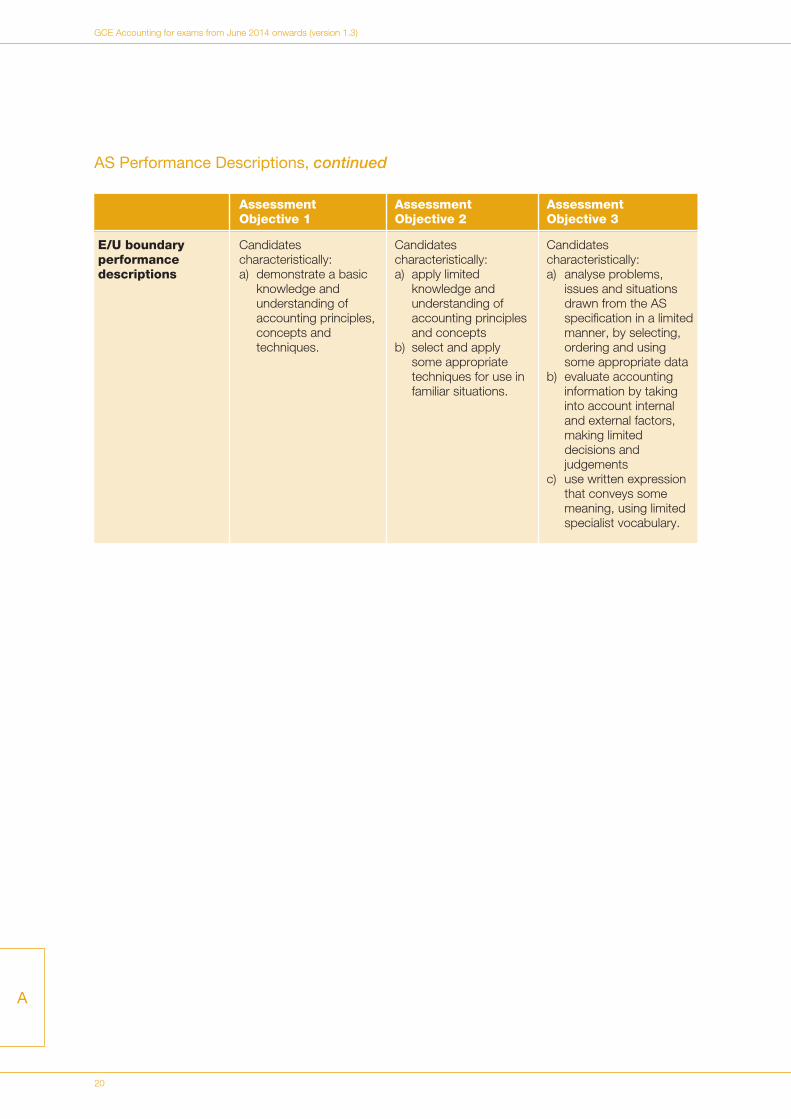

Assessment Assessment Assessment Objective 1 Objective 2 Objective 3

E/U boundary Candidates Candidates Candidates performance characteristically: characteristically: characteristically: descriptions a) demonstrateabasic a) applylimited a) analyseproblems, knowledgeand knowledgeand issuesandsituations understanding of understanding of drawn from the AS accountingprinciples, accountingprinciples specificationinalimited conceptsand andconcepts manner,byselecting, techniques. b) selectandapply orderingandusing some appropriate some appropriate data techniquesforusein b) evaluateaccounting familiarsituations. informationbytaking intoaccountinternal andexternalfactors, makinglimited decisions and judgements c) use written expression that conveys some meaning,usinglimited specialistvocabulary.

21

GCE Accounting for exams from June 2014 onwards (version 1.3)

A

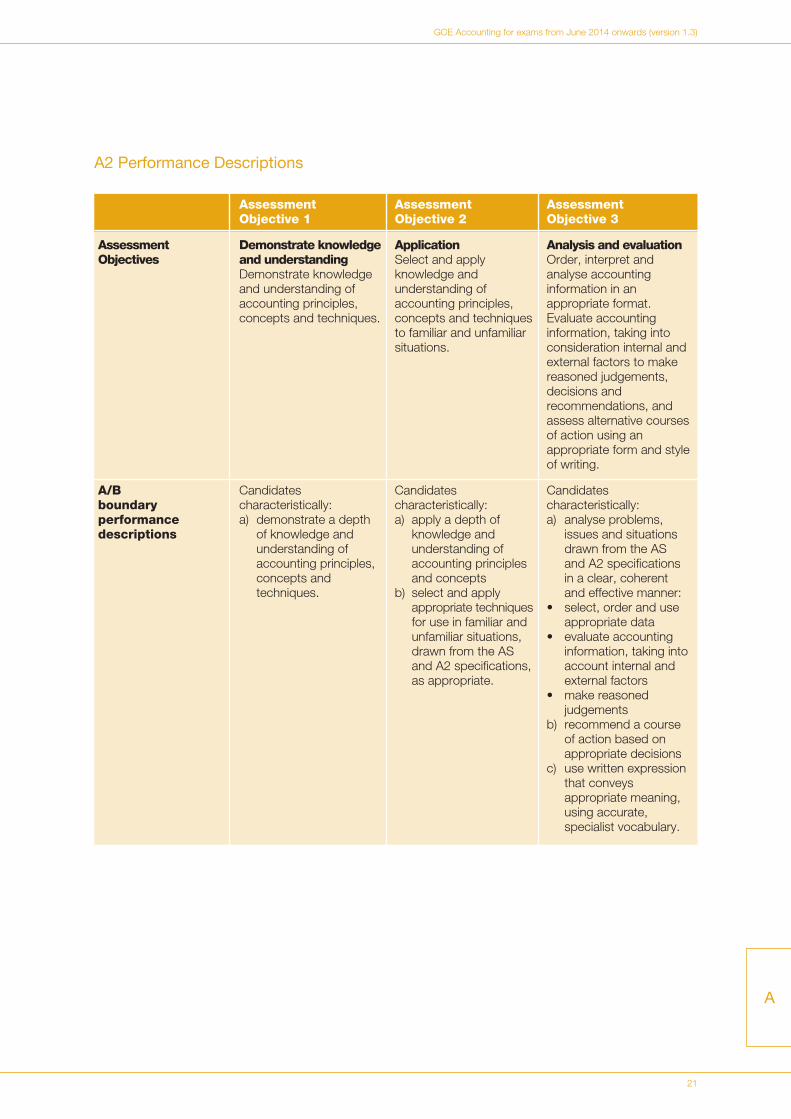

A2 Performance Descriptions

Assessment Assessment Assessment Objective 1 Objective 2 Objective 3

Assessment Demonstrate knowledge Application Analysis and evaluation Objectives and understanding Selectandapply Order,interpretand Demonstrateknowledge knowledgeand analyseaccounting and understanding of understanding of information in an accountingprinciples, accountingprinciples, appropriateformat. conceptsandtechniques. conceptsandtechniques Evaluateaccounting tofamiliarandunfamiliar information,takinginto situations. considerationinternaland externalfactorstomake reasonedjudgements, decisions and recommendations,and assessalternativecourses of action using an appropriateformandstyle of writing.

A/B Candidates Candidates Candidates boundary characteristically: characteristically: characteristically: performance a) demonstrateadepth a) applyadepthof a) analyseproblems, descriptions ofknowledgeand knowledgeand issuesandsituations understanding of understanding of drawn from the AS accountingprinciples, accountingprinciples andA2specifications conceptsand andconcepts inaclear,coherent techniques. b) selectandapply andeffectivemanner: appropriatetechniques • select,orderanduse foruseinfamiliarand appropriatedata unfamiliarsituations, • evaluateaccounting drawnfromtheAS information,takinginto andA2specifications, accountinternaland asappropriate. externalfactors • makereasoned judgements b) recommend a course of action based on appropriate decisions c) use written expression that conveys appropriatemeaning, usingaccurate, specialistvocabulary.

22

GCE Accounting for exams from June 2014 onwards (version 1.3)

A

A2 Performance Descriptions, continued

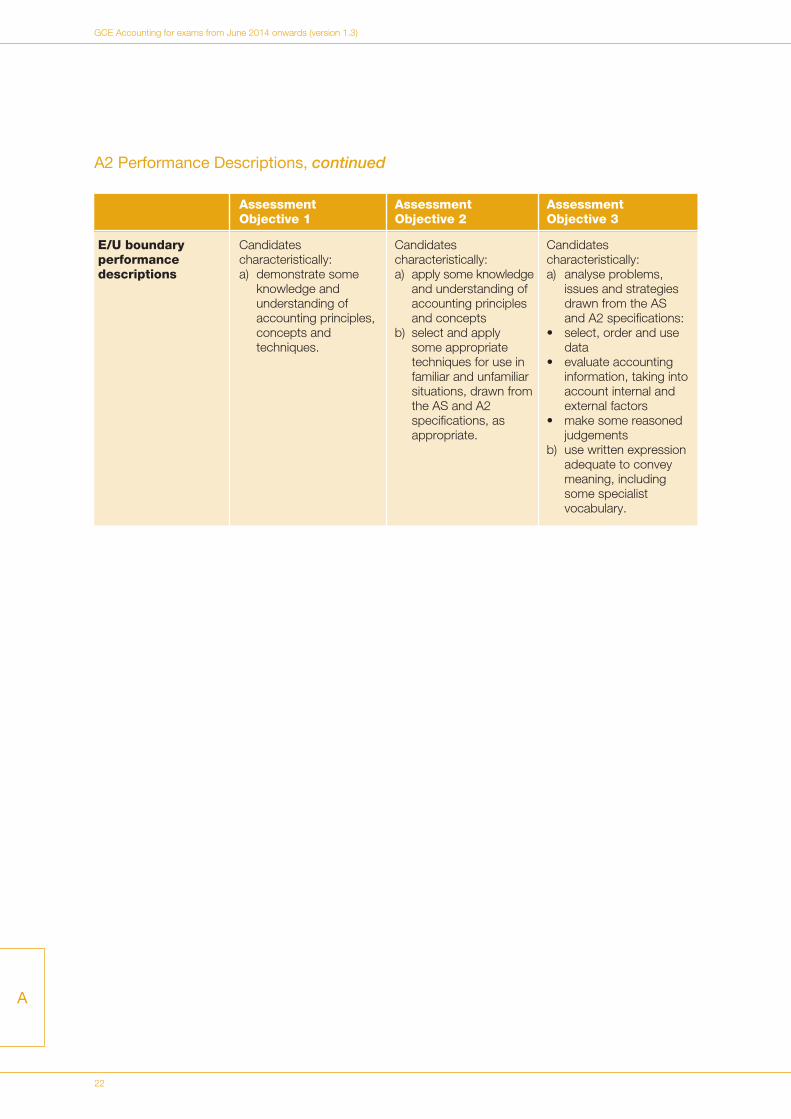

Assessment Assessment Assessment Objective 1 Objective 2 Objective 3

E/U boundary Candidates Candidates Candidates performance characteristically: characteristically: characteristically: descriptions a) demonstratesome a) applysomeknowledge a) analyseproblems, knowledgeand andunderstandingof issuesandstrategies understandingof accountingprinciples drawnfromtheAS accountingprinciples, andconcepts andA2specifications: conceptsand b) selectandapply • select,orderanduse techniques. someappropriate data techniquesforusein • evaluateaccounting familiarandunfamiliar information,takinginto situations,drawnfrom accountinternaland theASandA2 externalfactors specifications,as • makesomereasoned appropriate. judgements b) use written expression adequatetoconvey meaning,including somespecialist vocabulary.

23

GCE Accounting for exams from June 2014 onwards (version 1.3)

B

B Spiritual,Moral,Ethical,SocialandOtherIssuesWhilstfinancialandlegislativeconsiderationsareof majorimportanceinanystudyofaccounting,the subjectcanalsocontributetocandidates’understandingofspiritual,moral,ethical,socialandculturalissues.Candidatesareencouragedtoconsiderthenon-financialaspectsofaccountingwhichquestionprofitabilityasthesoleormaindeterminantofpolicy.Forexample,inUnit4,thesocialaspectsofaccountingcanbeexploredinavarietyofsituations,suchastheclosureofanunprofitablebusinessinadeprivedarea,thereplacementoflabourbyadvancedtechnology,theeffectsofredundancyandearlyretirementonthelabourforce,theeffectsofusingnon-renewableresourcesordangerousmaterialsontheenvironment,tradingwhichhaspoliticaland/orethicalimplications(e.g.tobacco,arms),andexcessivecostsavingwhichaffectsadverselyhealthandsafetyatwork.

European DimensionAQAhastakenaccountofthe1988ResolutionoftheCounciloftheEuropeanCommunityinpreparingthisspecificationandassociatedspecimenunits.

Environmental EducationAQAhastakenaccountofthe1988Resolutionof theCounciloftheEuropeanCommunityandthe1993 report “Environmental Responsibility: An Agenda for Further and Higher Education” in preparing this specificationandassociatedspecimenunits.

Inparticular,Unit4providesopportunitiesforcandidates to consider the effects on the environment whendecisionsrelatingtocostingandcapitalinvestment are made.

Avoidance of BiasAQA has taken great care in the preparation of this specificationandspecimenunitstoavoidbiasofanykind.

24

GCE Accounting for exams from June 2014 onwards (version 1.3)

C

C OverlapswithotherQualificationsThereisapotentialoverlapbetweenaspectsofGCEAccounting and GCE Business Studies.

25

GCE Accounting for exams from June 2014 onwards (version 1.3)

D

D KeySkillsKeySkillsqualificationshavebeenphasedoutandreplacedbyFunctionalSkillsqualificationsinEnglish,MathematicsandICTfromSeptember2010.

GCE Accounting (2120) For exams from June 2014 onwardsQualification Accreditation Number: AS 500/2325/1 - A Level 500/2329/9

For updates and further information on any of our specifications, to find answers or to ask a question:

Copyright © 20 AQA and its licensors. All rights reserved.13 AQA Education (AQA), is a company limited by guarantee registered in England and Wales (company number 3644723),and a registered charity . 1073334Registered address: AQA, Devas Street, Manchester M15 6EX.

http://www.aqa.org.uk/professional-developmentFor information on courses and events please visit:

register with ASK AQA at:http://www.aqa.org.uk/help-and-contacts/ask-aqa

Every specification is assigned a discounting code indicating the subject area to which it belongsfor performance measure purposes.The discount codes for this specification are:AS AK6A Level 7410

The definitive version of our specification will always be the one on our website,this may differ from printed versions.

![Qualification Specification for: ATI Level 5 Diploma for ... · [Type text] [Type text] [Type text] Qualification Specification for: ATI Level 5 Diploma for Accounting Technicians](https://img.pdfslide.net/doc/110x75/5b0cb0697f8b9a6a6b8cbb07/qualification-specification-for-ati-level-5-diploma-for-type-text-type-text.jpg)