Embed Size (px)

Citation preview

CLICK ON EACH FILE IN THE LEFT HAND COLUMN TO SEE INDIVIDUAL PRESENTATIONS.

If no column is present: click Bookmarks or Pages on the left side of the window.

If no icons are present: Click View, select Navigational Panels, and chose either Bookmarks or Pages.

If you need assistance or to register for the audio portion, please call Strafford customer service at 800-926-7926 ext. 10

D&O Duty of Oversight Amid the Economic CrisisAvoiding and Defending Breach of Fiduciary Duty Lawsuits

presents

Today's panel features:

Michael E. Foreman, Partner, Dorsey & Whitney, New York

Susan Webster, Partner, Cravath Swaine & Moore, New York

Lisa A. Fontenot, Partner, Gibson Dunn & Crutcher, Palo Alto, Calif.

Thursday, June 11, 2009

The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific

The audio portion of this conference will be accessible by telephone only. Please refer to the dial in instructions emailed to registrants to access the audio portion of the conference.

A Live 90-Minute Audio Conference with Interactive Q&A

Directors and Officers’ Duties Amid the Economic Crisis Strafford Publications Teleconference Program – June 11, 2009

Michael Foreman, Esq. Dorsey & Whitney LLP

In the midst of the current economic crisis, directors and officers of companies

that appeared relatively healthy only a short time ago may find themselves facing serious second-

guessing on decisions made in the months prior to the onset of the crisis, or in the first few

months of the economic crisis as its severity started to become apparent. These times bring with

them issues of fiduciary duties and responsibilities that many may not have seen before. They

also bring with them the propensity for Monday morning quarterbacks to challenge board

decisions with the benefit of hindsight, and the desire of those most injured by the corporate

losses incurred during the economic crisis – shareholders and creditors – to seek redress against

the decision-makers. Yet, the Delaware Chancery court’s February 24, 2009 decision in In re

Citigroup Inc. Shareholder Deriv. Litig.1issued a sobering instruction to potential plaintiff’s

looking to recover lost value by imposing liability on corporate directors:

It is understandable that investors, and others, want to find someone to hold responsible for these losses, and it is often difficult to distinguish between a desire to blame someone and a desire to force those responsible to account for their wrongdoing …. we must not let out desire to blame someone for our losses make us lose sight of the purpose of our law. Ultimately, the discretion granted directors and managers allows them to maximize shareholder value in the long term by taking risks without the debilitating fear that they will be held personally liable if the company experiences losses. this doctrine also means, however, that when the company suffers losses, shareholders may not be able to hold the directors personally liable.2

1 C.A. No. 3338-CC (Del. Ch. Feb. 24, 2009).

2 Id. at 58.

-2-

Recent cases out of the Delaware and Third Circuit courts have indicated that, in

bankruptcy, creditor and trustee plaintiffs continue to have an arsenal of potent weapons in

seeking redress against officers and directors for losses resulting from their company’s failure.

Historically, two concepts have dominated restructuring practice and commentary on the duties

of directors and officers of a company facing financial distress – the “zone of insolvency” (as

discussed herein, the period in which a company’s financial performance is near but not quite at

insolvency) and “deepening insolvency” (as discussed herein, the worsening of an insolvent

company’s financial condition) – to suggest an expansion of director and officer duties, as a

company approaches or operates in insolvency, for the benefit of the company’s creditors. Then,

in 2006 and 2007, case law, particularly in the Delaware state courts and Third Circuit

bankruptcy courts, appeared to signal a retreat from the expansion of duties suggested by the

“zone of insolvency” and “deepening insolvency “ models for fiduciary duties and liability,

signaling that the prospect for exposure may not be as great as directors and officers regularly

had been counseled. However, the zone of insolvency analysis continues to be relevant in light

of uncertainties in determining with real-time precision the point when a company becomes

insolvent. Plaintiffs have sought to navigate around case law discrediting “deepening

insolvency” as an independent cause of action by linking their allegations to more traditional

breach of fiduciary duty claims.

Accordingly, as an increasing number of companies find themselves facing

difficult financial, transactional and operational options, their directors must be ever mindful of

their duty to monitor and oversee the business, and the need to implement corporate processes

that enable directors to advance the corporate interests and assess business risk. Moreover, as a

company enters a phase of financial and operational restructuring, directors must keep a watchful

-3-

eye on the solvency of the corporation and take great care to act in good faith and exercise

reasonable business judgment appropriate for the circumstances notwithstanding the exigencies

of the moment. Their fiduciary duties may be shifting right before their eyes.

I. Directors’ Fiduciary Duties and Caremark and Revlon Obligations

Generally, directors owe duties of care and loyalty to the corporation. Officers

also owe the same fiduciary duties of care and loyalty as directors.3 These fiduciary duties have

been explained further under Delaware law as creating obligations in two significant areas –the

oversight of the corporation and obtaining the best available price in selling the company or its

significant assets – which flesh out the framework for guidelines to be considered by directors

acting in the current economic climate.

The “duty of care” requires directors both to use that amount of care which

ordinarily careful and prudent persons would use in similar circumstances, and to consider all

material information reasonably available.4 Duty of care liability can arise in two contexts: (i)

where liability may be said to follow from a board decision that results in a loss because that

decision was ill advised, or negligent; or (ii) where liability for a loss arises from an

unconsidered failure of the board to act in circumstances in which due attention would, arguably,

have prevented the loss.5

3 Gantler v. Stephens, Case No. 132, 2008, C.A. No. 2392 (De. January 27, 2009).

4 In Re Walt Disney Co. Deriv. Litig., 907 A.2d 693, 749 (Del. Ch. 2005); See also Smith v. Van Gorkom, 488 A.2d 858 (Del. 1985); Robert Clark, Corporate Law Section 3.4, 123 (Aspen Publishers, Inc. 1986).

5 In re Caremark Int’l Inc. v. Deriv. Litig., 698 A.2d 959, 967 (Del. Ch. 1996)

-4-

Directors generally will not be held liable for the consequences of their exercise

of business judgment -- even for judgments that appear to have been clear mistakes – unless

certain exceptions apply, such as fraud, conflict of interest, or gross negligence.6 Gross

negligence is the proper standard for determining whether a business judgment reached by a

board of directors was an informed one.7 However, the business judgment rule protections do

not apply where a loss results from director inaction.8

The mere fact that a company assumes business risk and suffers losses does not

evidence misconduct, and is not a basis for director liability in and of itself. In the Caremark

case, the Delaware Supreme Court noted that “compliance with a director’s duty of care can

never appropriately be judicially determined by reference to the content of the board decision

that leads to corporate loss, apart from consideration of the good faith or rationality of the

process employed.”(emphasis in original)9 As a result, the Court articulated a standard for

liability that is sometimes referred to as the “duty of oversight,” stating that directors could be

found liable for a failure to monitor upon evidence of a lack of good faith upon “only a sustained

or systematic failure of the board to exercise oversight – such as an utter failure to attempt to

assure a reasonable information and reporting system exists.”10

In Citigroup, the Delaware Chancery Court further explained that a director’s

oversight duties under Delaware law are not designed to subject directors to personal liability for 6 Id. 7 Smith V. Van Gorkom, 488 A.2d 858, 873 (Del. 1986). 8 In Re Walt Disney Co. Deriv. Litig., 907 A.2d at 748. 9 In re Caremark Int’l Inc. v. Deriv. Litig., 698 A.2d at 967-68.

10 Id. at 971.

-5-

failure to predict the future and to properly evaluate business risk.11 The Chancery Court

declared that

“[b]usiness decision-makers must operate in the real world, with imperfect information, limited resources, and an uncertain future. To impose liability on directors for making a “wrong” business decision would cripple their ability to earn returns for investors by taking business risks. Indeed, this kind of judicial second guessing is what the business judgment rule was designed to prevent, and even if a complaint is framed under a Caremark theory, this Court will not abandon such bedrock principles of Delaware fiduciary duty law.”12

The Court explained that “the mere fact that a company takes on business risk and suffers losses

– even catastrophic losses – does not evidence misconduct, and, without more, is not a basis for

personal director liability.”13

In contrast, the “duty of loyalty“ identifies director misconduct when fiduciaries

take advantage of their beneficiaries by means of fraudulent or unfair transactions.14 Fiduciaries

may breach their duty of loyalty by intentionally failing to act in the face of a known duty to act,

demonstrating a conscious disregard for their duties.15 The distinction between breach of duty of

care and breach of loyalty claims are significant, because Delaware Corporate law permits a

Delaware corporation to eliminate or limit, in its certificate of incorporation, the personal

11 In re Citigroup Inc. Shareholder Deriv. Litig. at 41.

12 Id. at 31.

13 Id. at 38-39.

14 Robert Clark, Section 4.1 at 141. See also Lewis v. Vogelstein, 699 A.2d 327 (Del. Ch. 327); Weinberger v. UOP, Inc., 457 A.2d 701 (Del. 1983).

15 In re Bridgeport Holdings, Inc., 388 B.R. 548, 564 (Bankr. D. Del. May 30, 2008, B. J. Walsh), citing Stone, 911

A.2d at 369.

-6-

liability of a director to the corporation or its stockholders for monetary damages for breach of

fiduciary duty of care (with certain exceptions), but not for a breach of the duty of loyalty.16

In Stone v. Ritter,17 the Delaware Supreme Court held that a breach of loyalty

claim may be premised upon the failure of a fiduciary to act in good faith, while a claim for

breach of the duty of care does not implicate a director’s bad faith.18 Bad faith encompasses not

only an intent to harm but also intentional dereliction of duty, falling between subjective bad

faith – i.e., fiduciary conduct motivated by an actual intent to do harm – and a lack of due care –

i.e., action taken solely by reason of gross negligence without any malevolent intent. As a result,

no comprehensive or exclusive definition of “bad faith” has been articulated by the Delaware

courts.19

Accordingly, the Delaware Supreme Court in Stone v. Ritter determined that a

director’s oversight obligations were “embedded in the fiduciary duty of loyalty, a breach of

which implicates a director’s bad faith.20 Those oversight obligations do not constitute a

freestanding fiduciary duty that could independently give rise to liability.21 Rather, oversight

liability will be established if a plaintiff proves that the directors knew they were not discharging

16 8 Del. C. § 107(b)(7). Lyondell Chem. Co., 2009 Del. LEXIS 152.

17 911 A.2d 362, 370 (Del. 2006). 18 “[W]here a claim of directorial liability for corporate loss is predicated upon ignorance of liability creating

activities within the corporation … only a sustained or systematic failure of the board to exercise oversight – such as an utter failure to attempt to assure a reasonable information and reporting system exists – will establish the lack of good faith that is a necessary condition to liability.” Lyondell Chem. Co. v. Ryan, 2009 Del. LEXIS 152 at *11 (March 25, 2009) (quoting In re Caremark Int’l Deriv. Litig., 698 A.2d at 971).

19 In Re Walt Disney Co. Deriv. Litig., 907 A.2d at 64 – 66.

20 Stone v. Ritter, 911 A.2d at 370.

21 In re Citigroup Inc. Shareholder Deriv. Litig. at 23.

-7-

their fiduciary obligations or that the directors demonstrated a conscious disregard for their

responsibilities such as by failing to act in the face of a known duty to act. As the Chancery

Court explained in Citigroup, “a showing of bad faith is a necessary condition to director

oversight liability.” (emphasis in original, footnotes omitted)22

Similarly, when the Delaware Supreme Court declared in Revlon v. MacAndrews

& Forbes Holdings, Inc.23that directors were obligated to obtain the best available price in

selling a company, no new fiduciary duties were created for directors. Rather, under Delaware

law, directors’ duties of care and loyalty require that a board deciding to proceed with a change-

of-control transaction must perform its fiduciary duties by taking reasonable measures to obtain

the best available price in selling the company.24

Where directors have been exculpated from personal liability for breaches of the

duty of care, and the board is found to have been independent and not motivated by self-interest

or ill will, the sole issue under a Revlon claim is whether the directors breached their duty of

loyalty by failing to act in good faith.25 In its decision of March 25, 2009 in Lyondell Chem. Co.

v. Ryan, the Delaware Supreme Court re-affirmed the broad protections afforded disinterested

directors from personal liability for damages in the face of Revlon claims of breach of fiduciary

duties. Where directors have been exculpated by corporate charter provision from personal

22 Id. at 24.

23 506 A.2d 173, 182 (Del. 1986).

24 Revlon v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 182 (Del. 1986).

25 Lyondell Chem. Co., 2009 Del. LEXIS 152 at *10.

-8- 4851-3352-3971\1 10/13/2008 9:20 AM

liability for duty of care claims, plaintiffs claim a non-exculpable breach of good faith must

demonstrate that the directors “utterly failed” to attempt to obtain the best sale price.26

The Court determined that Revlon duties do not arise when a third party puts the

company “in play,” but, rather, apply only once the company embarks on a change-of-control

transaction on its own initiative or in response to an unsolicited offer.27 No single blueprint or

set of enumerated requirements exist for satisfying a directors Revlon duties. As a result,

directors are able to tailor their actions to the unique circumstances they face.28 An imperfect

attempt to comply to a board’s Revlon duties does not equate to a conscious disregards of those

duties so as to constitute a breach of the duty of loyalty.29

If directors breach either of the fiduciary duties of care or loyalty, a derivative suit

– for an injury to the corporation – may be brought against the corporation by its shareholders on

the corporation’s behalf. If the alleged wrong is not to the corporation, but to its shareholder(s),

a direct suit (such as a suit to inspect a corporation’s books, to enforce voting rights or to compel

the declaration of dividends)30 may be brought against individual directors.

26 Lyondell Chem. Co., 2009 Del. LEXIS 152 at *18-19.

27 Id. at *14.

28Id. at *16.

29 Id. at *19.

30 Robert Clark, Section 15.9 at 662.

-9-

Whether a derivative action against directors may be asserted by creditors or

shareholders is determined by a corporation’s solvency.31 “When a corporation is solvent,

[shareholders] have standing to bring derivative actions on behalf of the corporation because

they are the ultimate beneficiaries of the corporation’s growth and increased value… When a

corporation is insolvent, however, its creditors [come before] shareholders as the…principal

constituency injured by any fiduciary breaches that diminish the firm’s value.”32

II. Additional Considerations In Times of Financial Distress

For a company in financial distress, directors need to be mindful of three different

circumstances in which a company’s financial distress may manifest: insolvency, the zone of

insolvency and deepening insolvency.

Under Delaware law, a corporation is insolvent if it “has either: 1) a deficiency of

assets below liabilities with no reasonable prospect that the business can be successfully

continued in the face thereof, or 2) an inability to meet maturing obligations as they fall due in

the ordinary course of business.”33 The U.S. Bankruptcy Code defines the term “insolvent” with

reference to an entity other than a partnership or municipality as a financial condition such that

the sum of the entity’s debts is greater than all of the entity’s property, at a fair valuation,

exclusive of property transferred, concealed or removed with intent to hinder, delay or defraud

the entity’s creditors. 11 U.S.C. § 101(32)(A). Debt” means liability on a claim. 11 U.S.C. §

31 According to recent case law, it appears that creditors may assert direct claims against directors only on very rare

occasions, if such directors show a “marked degree of animus toward a particular creditor.” Prod. Res. Group, L.L.C., 863 A.2d at 798 (Del. Ch. 2004).

32 North Am. Catholic Educ. Programming Found., Inc. v. Gheewalla, 930 A.2d 92, 101-02, ((Del. 2007) (citations omitted) (emphasis in original).

33 Prod. Res. Group, L.L.C. v. NCT Group, Inc., 863 A.2d 772, 782 (Del. Ch. 2004).

-10-

101(12). “Claim” means (A) right to payment, whether or not such right is reduced to judgment,

liquidated, unliquidated, fixed, contingent, matured, unmatured, disputed, undisputed, legal,

equitable, secured, or unsecured; or (B) right to an equitable remedy for breach of performance if

such breach gives rise to a right to payment, whether or not such right to an equitable remedy is

reduced to judgment, fixed, contingent, matured, unmatured, disputed, undisputed, secured, or

unsecured. 11 U.S.C. § 101(5).

The concept of a “zone of insolvency” arose from the decisions of certain courts

finding that directors may owe fiduciary duties to creditors just before a company reaches

insolvency: i.e., when it is in the zone of insolvency.34 However, courts generally have avoided

developing a hard and fast definition for the “zone of insolvency.”35

The “zone of insolvency” analysis likely started with a footnote to the Delaware

Court of Chancery Credit Lyonnais Bank Nederland, N.V. v. Pathe Communications Corp. case,

which stated:

Such directors will recognize that in managing the business affairs of a solvent corporation in the vicinity of insolvency, circumstances may arise when the right (both the efficient and the fair) course to follow for the corporation may diverge from the choice that the stockholders (or the creditors, or the employees, or any single group interested in the corporation) would make if given the opportunity to act. 36

34 See, e.g., Weaver v. Kellogg, 216 B.R. 563, 582-84 (S.D.Tex.1997); Official Comm. Of Unsecured Creditors of

Buckhead Am. Corp. v. Reliance Capital Group, Inc. (In re Buckhead Am. Corp.), 178 B.R. 956, 968-69 (D.Del.1994); Credit Lyonnais Bank Nederland, N.V. v. Pathe Communications Corp., 1991 WL 277613 (Del. Ch. 1991).

35 For a discussion on the difficulties of defining the concept of “zone of insolvency, see Prod. Res. Group, L.L.C.,

863 A.2d at 790-91(Del. Ch. 2004).

36 Credit Lyonnais Bank Nederland, N.V., 1991 WL 277613, at *34 n. 55.

-11-

In Prod. Res. Group, L.L.C. v. NCT Group, Inc,. the Delaware Court of Chancery

noted that Credit Lyonnais Bank Nederland, N.V footnote 55 “was read more expansively by

some, not to create a shield for directors from stockholder claims, but to expose directors to a

new set of fiduciary duty claims, this time by creditors. To the extent that a firm is in the zone of

insolvency, some read this case as authorizing creditors to challenge directors’ business

judgments as breaches of a fiduciary duty owed to them.”37

However, in North American Catholic Educational Programming Foundation,

Inc. v. Gheewalla,38 the Delaware Supreme Court put to rest the notion that, in Delaware,

directors of a not-yet-insolvent company owed a duty both to shareholders and creditors. The

Court determined that,. as a matter of law, a corporation’s creditors may not assert direct claims

against directors for breach of fiduciary duties when the corporation is either insolvent or in the

zone of insolvency.” They may only assert derivative claims.39 When a company is operating in

the “zone of insolvency” but is not yet insolvent, directors owe their fiduciary duties to a

corporation and its shareholders and not to creditors.40 Thus, under current Delaware law, if a

corporation is approaching insolvency,41 the fiduciary duties of directors do not shift from

shareholders to creditors. Directors must continue to make decisions of business judgment based

37 Prod. Res. Group, L.L.C., 863 A.2d at 789. 38 930 A.2d 92 (Del. 2007). 39Gheewalla, 930 A.2d at 97. 40 Id. at 101. 41 The definitions of insolvency are discussed above.

-12-

on what is best for the corporation and its shareholders and not necessarily what is best for the

creditors.42

The concept of “deepening insolvency” refers to a situation where an already

insolvent company becomes more insolvent as a result of actions taken or not taken by the

company, or the impact of commercial industry, or economic conditions. Some courts have

concluded or suggested that once a company is insolvent, acts or inaction causing a company to

assume greater debt and become more insolvent (or entering “deepening insolvency”) are

justification for a derivative suit on behalf and for the benefit of all creditors.43

The concept of “deepening insolvency” – “an injury to the Debtors’ corporate

property from the fraudulent expansion of corporate debt and prolongation of corporate life”44 –

as a viable source of litigation recoveries for a company’s creditors took root upon the Third

Circuit’s holding in Official Committee of Unsecured Creditors v. R.F. Lafferty & Co., Inc. that

deepening insolvency constituted a valid cause of action under Pennsylvania law. The Third

Circuit noted that deepening insolvency could harm a corporation in several ways: the incurrence

of additional debt could force a company into bankruptcy, thereby creating additional

administrative costs; bankruptcy stemming from deepening insolvency could harm a

corporation’s ability to conduct business in a profitable manner; it could harm relationships with

and credibility with customers, suppliers, employees; and lastly, “prolonging an insolvent

42 See discussion below on recent case law developments regarding the application of the Business Judgment Rule

when a company is insolvent. 43 See, e.g., Official Committee of Unsecured Creditors v. R.F. Lafferty & Co., Inc., 267 F.3d 340 (3d Cir. 2001). 44 267 F.3d at 374.

-13-

corporation’s life through bad debt may simply cause the dissipation of corporate assets.”45 The

Third Circuit explained that the “harms [stemming from deepening insolvency] can be averted,

and the value within an insolvent corporation salvaged, if the corporation is dissolved in a timely

manner, rather than kept afloat with spurious debt.”46

In Seitz v. Detweiler, Hersey & Assocs., P.C. (In re CitX Corp.),47 the Third

Circuit further explained that “deepening insolvency” could be a valid cause of action48 but

“should not be interpreted to create a novel theory of damages for an independent cause of action

like malpractice.”49 Deepening insolvency beyond the Lafferty holding was determined to be

limited, and would not sustain a claim of negligence or support an independent deepening-

insolvency cause of action.50 The Third Circuit did note that its holding in Lafferty did not

extend the concept of deepening insolvency beyond Pennsylvania.51

However, in Trenwick America Litigation Trust v. Ernst & Young, L.L.P.,52 the

Third Circuit held that Delaware law does not recognize an “independent cause of action for

deepening insolvency.” The Third Circuit declared that the board of even an insolvent company

45 Id. at 349-50. 46 Id. at 350. 47 448 F.3d 672 (3d Cir. 2006). 48 Id. at 681. 49 Id. at 677. 50 Id. at 681. 51 Id. at 680 n. 11. 52 906 A.2d 168, 205 (Del. Ch. 2006).

-14-

“may pursue, in good faith, strategies to maximize the value of the firm.”53 It explained that

when an insolvent corporation’s board acts with due diligence and good faith in the pursuit of a

“business strategy that it believes will increase the corporation’s value, [even if the strategy]

involves the incurrence of additional debt[,]... [t]hat the strategy results in continued insolvency

and an even more insolvent entity does not in itself give rise to a cause of action.”54 In such

circumstances, the directors will be protected by the business judgment rule because the “fact of

insolvency does not render the concept of ‘deepening insolvency’ a more logical one than the

concept of ‘shallowing profitability.’55 Rather, the “proper role of insolvency [is] to act as an

important contextual fact in the fiduciary duty matrix.”56 Significantly, deepening insolvency

has been challenged outside of the Third Circuit as a valid cause of action.57

Consequently, where a creditors’ committee was found to have tried claims of

recharacterization and breach of fiduciary duty as if it were a “deepening insolvency” case, the 53 Id . 54 Id. 55 Id. 56 Id. 57 See, e.g., In re SI Restructuring, Inc., 532 F.3d 355, 362-64 (5th Cir. June 20, 2008) (agreeing in dicta with the

Third Circuit’s Trenwick decision, while finding that the trustee’s deepening insolvency theory was not supported by the court’s findings); Fehribach v. Ernst & Young LLP, 493 F.3d 905, 909 (7th Cir. 2007) (refusing to accept plaintiff’s deepening insolvency theory and stating that “the theory makes no sense when invoked to create a substantive duty of prompt liquidation that would punish corporate management for trying in the exercise of its business judgment to stave off a declaration of bankruptcy, even if there were no indication of fraud, breach of fiduciary duty, or other conventional wrongdoing.”); In re Parmalat Sec. Litig., 501 F.Supp.2d 560 (S.D.N.Y. 2007).

Federal and state courts often follow Delaware’s lead on such creditor issues, suggesting that it is likely that

deepening insolvency will no longer be a credible alternative for plaintiffs elsewhere. See, e.g., In re I.G. Services, Ltd., 2007 WL 2229650, at *3 (Bkrtcy.W.D.Tex. July 31, 2007) (“The Delaware courts’ decisions have proved to be immensely influential in the national debate over the shape of causes of action that have their genesis in breach of fiduciary duties on the part of officers and directors….It seems fair to say…that both state and federal courts within this jurisdiction are likely to give weight to the court from whence creditor-initiated actions for breach of fiduciary duties have emerged.”) (citation omitted).

-15-

bankruptcy court held, in In re Radnor Holdings Corp.,58 that, in light of Trenwick, “simply

calling a discredited deepening insolvency cause of action by some other name does not make it

a claim that passes muster.”59 The court explained that, under Delaware law, a board is not

required to wind down operations simply because a company is insolvent, but rather may

conclude to take on additional debt in the hopes of turning operations around.60 The court also

noted that the making of a loan does not increase insolvency, but, rather, “increases liabilities

(the amount of the loan) and assets (the cash provided by the loan) in the same amount.”61 The

court also found that “[a]s a matter of law, there is no per se breach of fiduciary duty for an

insider making a bid to purchase a company or its assets.”62

No bright-line “real-time” methods exist of determining when a company may be

approaching insolvency or actually is insolvent, based on an insolvency test that aggregates all of

a company’s known and potential liabilities and is based on the fair market value of a company’s

assets. Similarly, a company’s reasonable prospects for successfully continuing a business

cannot be assessed by an objective test. In addition, a company may be unable to pay its most

significant debts as they mature, such as loans and public or private bond debt, while it continues

to pay its obligations arising in the ordinary course of business to trade vendors and service

providers. Accordingly, the “zone of insolvency” and “deepening insolvency” concepts continue

to be relevant in guiding directors along the slippery slope of corporate financial distress.

58 353 B.R. 820 (Bankr. D.Del. 2006).

59 Id. at 842.

60 Id.

61 Id.

62 Id. at 845.

-16-

III. Significant Recent Developments

The most recent trend in Delaware and Third Circuit case law suggests that

directors should be less concerned with whether the company is almost insolvent or may become

more insolvent, and more concerned with whether they are taking actions that reflect their

reasonable business judgment, without regard for their personal interests, in good faith and in the

best interests of all stakeholders in the company – shareholders, creditors, employees, suppliers.

In In re Bridgeport Holdings, Inc., the Debtor sold a substantial portion of its

assets one day prior to filing its Chapter 11 petition. The Debtor’s liquidating trust asserted a

claim for breach of fiduciary duties based on. among other claims, the board’s abdication of

responsibility to the restructuring professional it hired, the board’s failure to supervise the

restructuring professional, and the board’s acquiescence in the restructuring professional’s

decision to sell the assets in an allegedly rushed and uninformed manner.63 The court determined

that where a breach of the duty of loyalty and lack of good faith is alleged as well as a breach of

duty of care, an exculpatory provision in the company’s articles of incorporation cannot justify a

dismissal of the duty of care claims.64

First, the court examined the board’s Caremark obligations of oversight. The

lawsuit against the debtor’s board of directors alleged that the directors had ignored their

responsibilities by failing to hire a restructuring advisor early on in the restructuring process,

disregarded the financial “red flags and painted an unjustifiably rosy picture of the company’s

63 388 B.R. at 554-61.

64 Id. at 568.

-17-

future.”65 The plaintiffs also alleged that, once the directors actually did hire a restructuring

advisor, they abdicated their duties and responsibilities to him.66

Within 72 hours of commencing his work, the restructuring advisor determined to

sell the company’s assets, and started negotiations with a party identified by a director only a few

days before, instead of instituting a competitive bidding process.67 Looking at the directors’

Revlon obligations, the court found that, in the sale context, a board’s failure to obtain a

valuation of the company’s assets and to adequately market those assets constituted breaches of

the duty of care.68 The business judgment rule otherwise protecting the directors would be

rebutted if the plaintiff showed that the directors failed to exercise due care in informing

themselves before making their decision.69

In In re Troll Communications, LLC.,70 the Chapter 7 trustee alleged breach of

fiduciary duties claims based on the directors’ decision to use proceeds of an equity buy-in to

pay debts owed to an equity holder of the company. The trustee also asserted that the directors

failed to take reasonable actions to prevent the “ever-deepening insolvency” of the debtor

entities.71 The court found that where the trustee pled facts sufficient to question the

disinterestedness of a majority of the board of directors, the business judgment rule presumption

65 Id. at 555.

66 Id. at 556.

67 Id. at 556 – 57.

68 Id. at 570.

69 Id. at 572.

70 385 B.R. 110 (Bankr. D. Del. April 2, 2008, B.J. Carey).

71 Id. at 117.

-18-

may not be used as a basis to dismiss a breach of loyalty claim.72 However, the court determined

that where the trustee’s cause of action was not explicitly asserted as a “deepening insolvency”

cause of action but was, in substance, a claim of deepening insolvency, the claim was dismissed

as both a cause of action and a theory of damages.73

In In re The Brown Schools,74 the Chapter 7 trustee asserted against debtor’s

former majority equity holder and its affiliates (as well as former directors of the debtor and the

former law firm representing the debtor) claims for breach of fiduciary duty, aiding and abetting

breach of fiduciary duty, corporate waste and civil conspiracy, as well as a cause of action for

deepening insolvency. The court held that while Trenwick mandated the dismissal of the claim

for deepening insolvency, it did not require dismissal of the other causes of action.75 The court

further explained that duty of care violations may resemble causes of action for deepening

insolvency, because the alleged injury in both is the result of the board of directors’ poor

business decision, claims for breach of the fiduciary duty of loyalty in the form of self-dealing

are not deepening insolvency claims in disguise.76 The court then determined that the CitX

decision only held that deepening insolvency was not a viable theory of damages for the

particular malpractice claim before the Third Circuit in that case, and was not a broad

invalidation of deepening insolvency as a valid theory of damages for all independent causes of

72 Id. at 119-20.

73 Id. at 122.

74 386 B.R. 37 (Bankr. D. Del. April 24, 2008, B.J. Walrath).

75 Id. at 46.

76 Id. at 47.

-19-

action. Accordingly, deepening insolvency was found to be a valid theory of damages for the

trustee’s breach of fiduciary duty claim.77

IV. Guidelines for Directors of Companies in Financial Crisis

Because the test for insolvency lies in a fairly gray area absent the requisite

intensive review of a company’s financial position, directors addressing their company’s

financial crisis should be mindful of creditors and all other stakeholders of the company when

they think a company is approaching insolvency but may not yet be insolvent. Once a company

reaches the point of insolvency, however measured, directors’ fiduciary duties transfer from the

corporation’s shareholders to its creditors: “The directors continue to have the task of attempting

to maximize the economic value of the firm. That much of their job does not change. But the

fact of insolvency does necessarily affect the constituency on whose behalf the directors are

pursuing that end. By definition, the fact of insolvency places the creditors in the shoes normally

occupied by the shareholders – that of residual risk-bearers.”78

Creditors are placed in the shoes of shareholders once the firm is insolvent. In

theory, they may assert any of the same claims that previously belonged to shareholders, but

such suits are generally limited to derivative suits. Creditors may not be able to assert direct

claims against a corporation’s directors at all, but if they are, such claims could only arise in very

narrow and unique circumstances if such directors “display such a marked degree of animus

77 Id. at 48.

78 See also Production Resources Group, 863 A.2d at 790-91.

-20-

towards a particular creditor with a proven entitlement to payment that they expose themselves to

a direct fiduciary duty claim by that creditor.”79

Even though directors may not simultaneously owe duties to creditors and

shareholders, both groups, in theory, could bring simultaneous suits (although not both

successfully). Moreover, the question of whether a company is insolvent may be litigated within

the context of a derivative suit, and the test for insolvency is more complicated than liabilities

exceeding assets. For example, a finding of insolvency under certain definitions must also

include a finding that the company has “no reasonable prospect that the business can be

successfully continued.”80 Accordingly, the period when a corporation approaches insolvency or

right after it enters insolvency is dangerous because it is a time when creditors and shareholders

may take different positions on whether the corporation is solvent, and both groups may bring

suits. Although only one suit, at most, could stand, in order to avoid needless litigation, directors

should take heed of potential duties to both groups.

79 Id. at 798. 80 Id. at 782 (citations and quotation marks omitted).

-21-

Once a company does reach the point of insolvency, directors may not be fearful

of making good faith decisions for the company which result in the company accumulating

greater corporate debt, or other decisions which may turn out to deepen the company’s

insolvency. Nonetheless, directors must continue to be mindful that they continue to exert the

degree of “skill, diligence, and care” that their constituents reasonably may demand. Directors

are cautioned to establish decision-making processes which permit the review and analysis of

restructuring alternatives as best as possible under a range of exigencies. Directors also will be

well-advised to adhere to those processes during the course of the financial crisis.

Michael Foreman Dorsey & Whitney LLP [email protected] 212-415-9243

CRAVATH, SWAINE & MOORE LLP

SEC 2009 Agenda

Susan WebsterCravath, Swaine & Moore LLPPractice Leader, General Corporate and Corporate Governance and Board Advisory Group

June 11, 2009

CRAVATH, SWAINE & MOORE LLP1

Warning

● The material discussed in these slides is for training and illustrative purposes only and does not purport to reflect appropriate or inappropriate procedures or disclosure that should be followed or inquiries that should be made, if any, in any particular situation.

CRAVATH, SWAINE & MOORE LLP2

SEC 2009 Agenda● Schapiro Commission

● Enhanced enforcement

● Shareholder empowerment

● Corporate governance and risk management

● Executive compensation

CRAVATH, SWAINE & MOORE LLP3

Schapiro Commission● New leadership

– Mary Schapiro new Chairman in January 2009

● Other new faces– Kayla Gillan, Senior Advisor to the Chairman– Rob Khuzami, Director of the Division of Enforcement– Meredith Cross, Director of the Division of Corporation Finance

● Shift in decision-making philosophy

– Consensus required v. willingness to proceed with a 3-2 vote

CRAVATH, SWAINE & MOORE LLP4

Enhanced Enforcement● New Director, Robert Khuzami

– Background● Federal Prosecutor with the U.S. Attorney’s Office for the Southern District

of New York● General Counsel for the Americas, Deutsche Bank AG

– Reorganization of enforcement division – specialized teams

● Immediate actions– Increased staffing– End to “pilot penalties program”– Easier process for formal orders and subpoenas– New whistleblower procedures

● Increase in FCPA actions

CRAVATH, SWAINE & MOORE LLP5

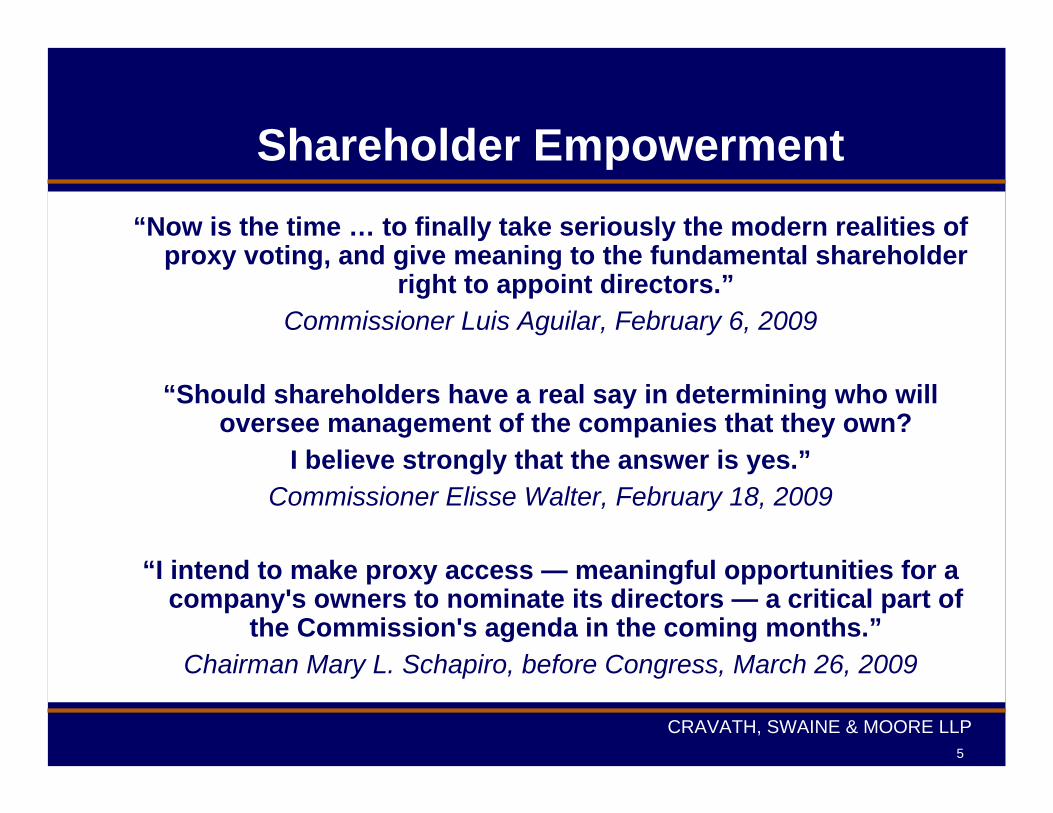

Shareholder Empowerment“Now is the time … to finally take seriously the modern realities of

proxy voting, and give meaning to the fundamental shareholder right to appoint directors.”

Commissioner Luis Aguilar, February 6, 2009

“Should shareholders have a real say in determining who will oversee management of the companies that they own?

I believe strongly that the answer is yes.” Commissioner Elisse Walter, February 18, 2009

“I intend to make proxy access — meaningful opportunities for a company's owners to nominate its directors — a critical part of

the Commission's agenda in the coming months.” Chairman Mary L. Schapiro, before Congress, March 26, 2009

CRAVATH, SWAINE & MOORE LLP6

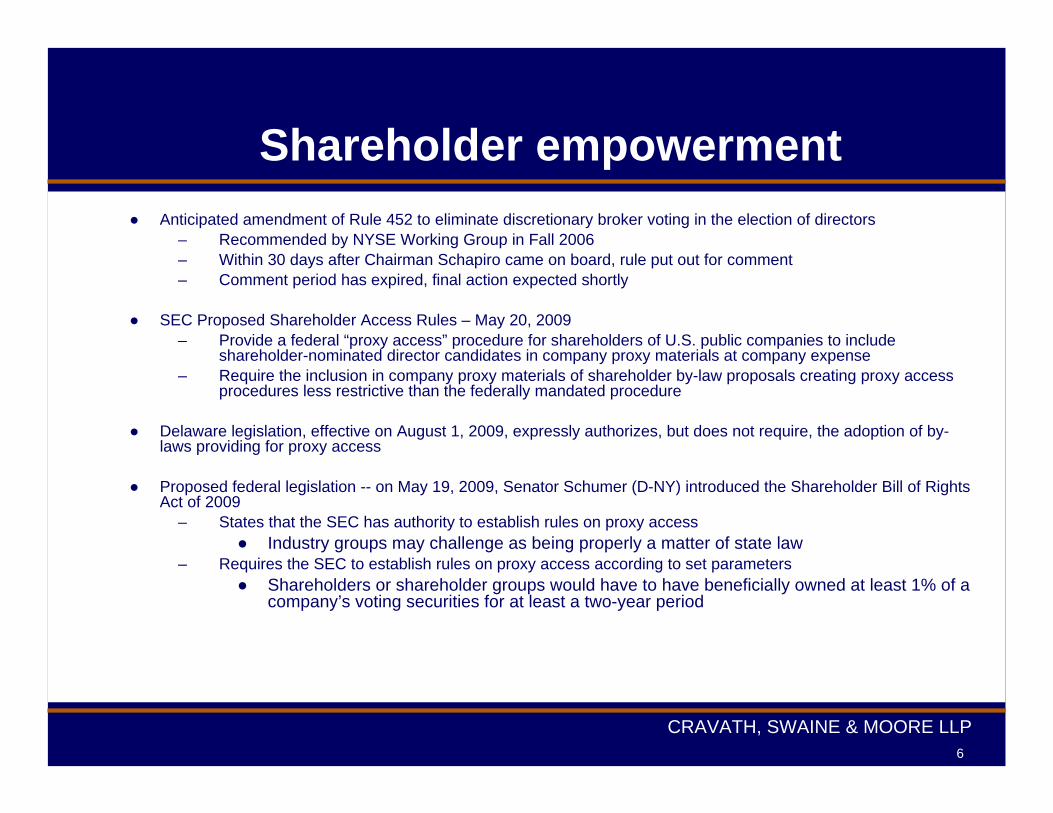

Shareholder empowerment● Anticipated amendment of Rule 452 to eliminate discretionary broker voting in the election of directors

– Recommended by NYSE Working Group in Fall 2006– Within 30 days after Chairman Schapiro came on board, rule put out for comment– Comment period has expired, final action expected shortly

● SEC Proposed Shareholder Access Rules – May 20, 2009– Provide a federal “proxy access” procedure for shareholders of U.S. public companies to include

shareholder-nominated director candidates in company proxy materials at company expense– Require the inclusion in company proxy materials of shareholder by-law proposals creating proxy access

procedures less restrictive than the federally mandated procedure

● Delaware legislation, effective on August 1, 2009, expressly authorizes, but does not require, the adoption of by-laws providing for proxy access

● Proposed federal legislation -- on May 19, 2009, Senator Schumer (D-NY) introduced the Shareholder Bill of Rights Act of 2009

– States that the SEC has authority to establish rules on proxy access● Industry groups may challenge as being properly a matter of state law

– Requires the SEC to establish rules on proxy access according to set parameters● Shareholders or shareholder groups would have to have beneficially owned at least 1% of a

company’s voting securities for at least a two-year period

CRAVATH, SWAINE & MOORE LLP7

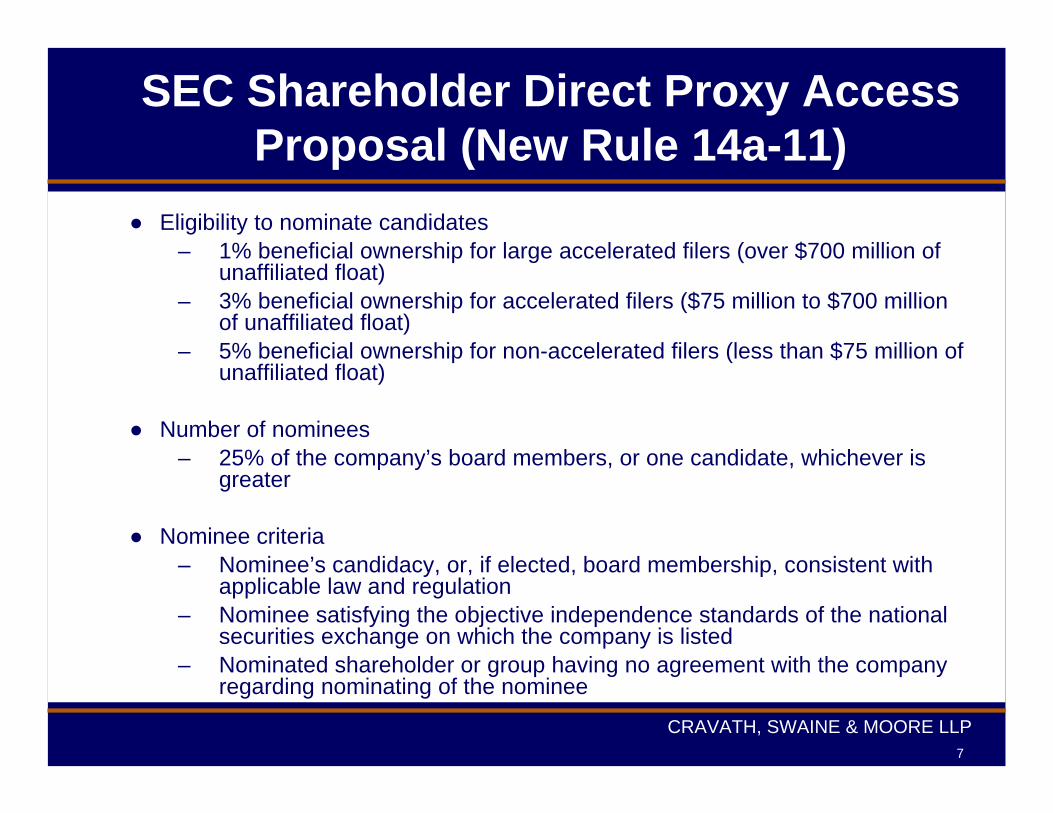

SEC Shareholder Direct Proxy Access Proposal (New Rule 14a-11)

● Eligibility to nominate candidates– 1% beneficial ownership for large accelerated filers (over $700 million of

unaffiliated float)– 3% beneficial ownership for accelerated filers ($75 million to $700 million

of unaffiliated float)– 5% beneficial ownership for non-accelerated filers (less than $75 million of

unaffiliated float)

● Number of nominees– 25% of the company’s board members, or one candidate, whichever is

greater

● Nominee criteria– Nominee’s candidacy, or, if elected, board membership, consistent with

applicable law and regulation– Nominee satisfying the objective independence standards of the national

securities exchange on which the company is listed– Nominated shareholder or group having no agreement with the company

regarding nominating of the nominee

CRAVATH, SWAINE & MOORE LLP8

SEC Shareholder Direct Proxy Access Proposal (New Rule 14a-11)

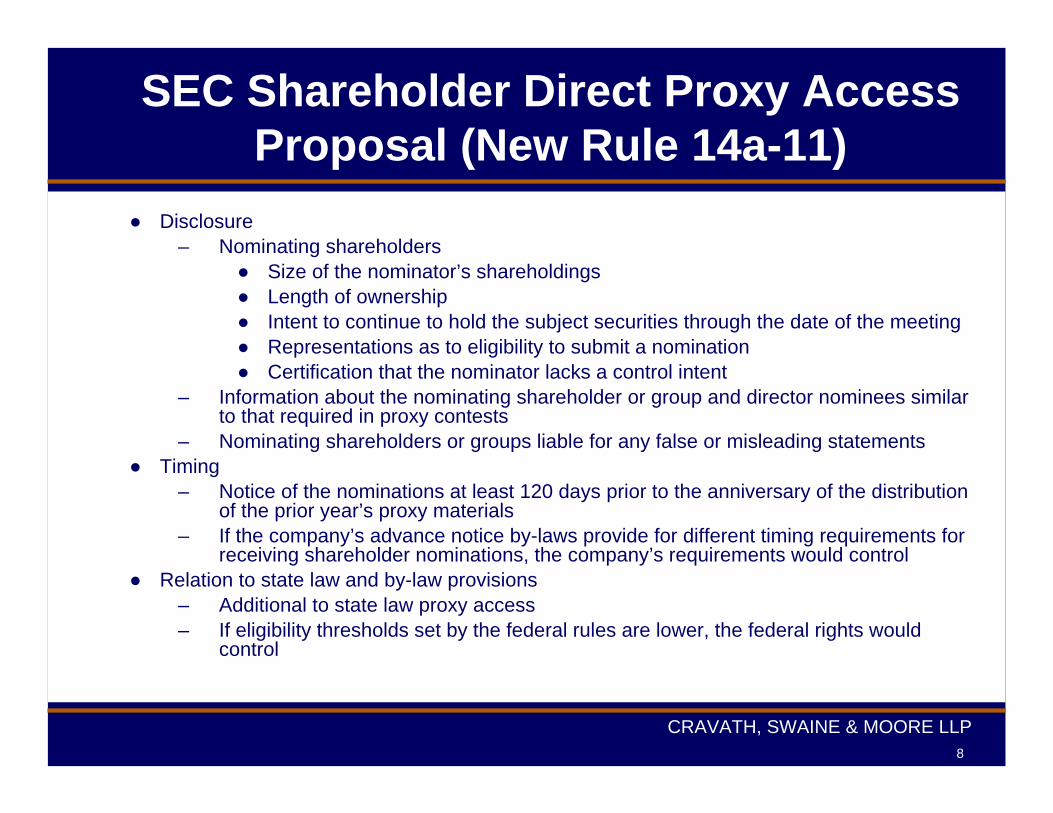

● Disclosure– Nominating shareholders

● Size of the nominator’s shareholdings● Length of ownership● Intent to continue to hold the subject securities through the date of the meeting● Representations as to eligibility to submit a nomination● Certification that the nominator lacks a control intent

– Information about the nominating shareholder or group and director nominees similar to that required in proxy contests

– Nominating shareholders or groups liable for any false or misleading statements● Timing

– Notice of the nominations at least 120 days prior to the anniversary of the distribution of the prior year’s proxy materials

– If the company’s advance notice by-laws provide for different timing requirements for receiving shareholder nominations, the company’s requirements would control

● Relation to state law and by-law provisions– Additional to state law proxy access– If eligibility thresholds set by the federal rules are lower, the federal rights would

control

CRAVATH, SWAINE & MOORE LLP9

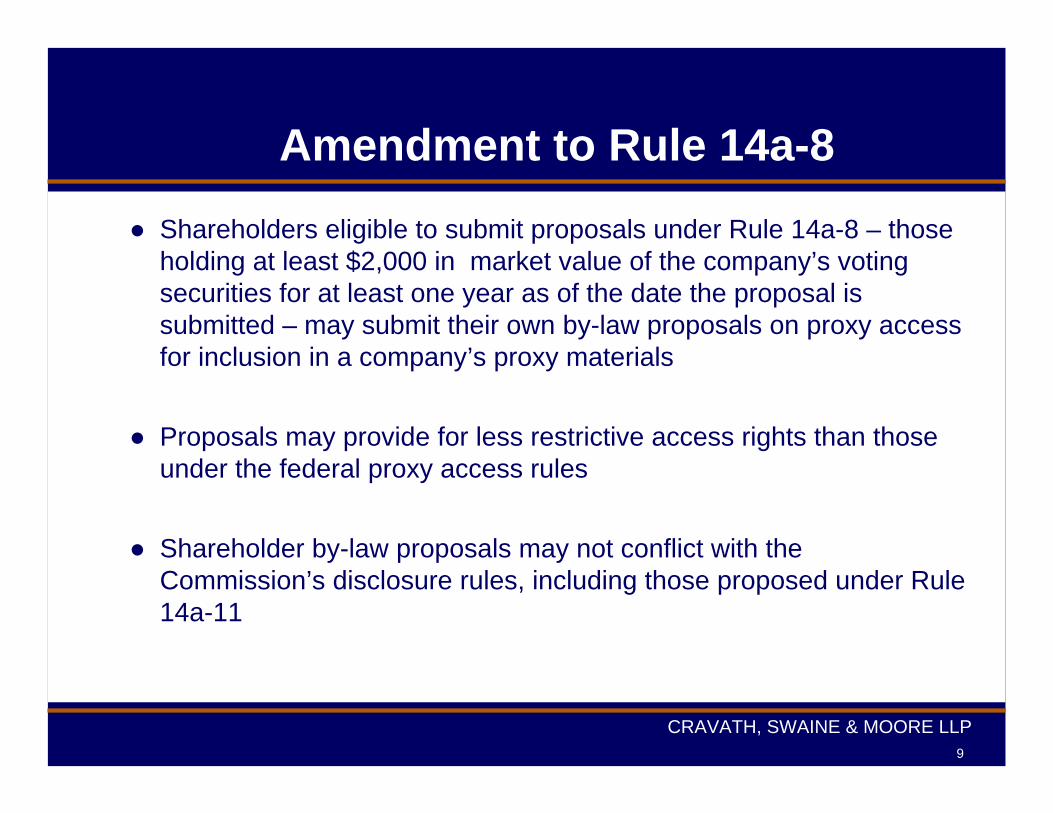

Amendment to Rule 14a-8● Shareholders eligible to submit proposals under Rule 14a-8 – those

holding at least $2,000 in market value of the company’s votingsecurities for at least one year as of the date the proposal is submitted – may submit their own by-law proposals on proxy access for inclusion in a company’s proxy materials

● Proposals may provide for less restrictive access rights than those under the federal proxy access rules

● Shareholder by-law proposals may not conflict with the Commission’s disclosure rules, including those proposed under Rule 14a-11

CRAVATH, SWAINE & MOORE LLP10

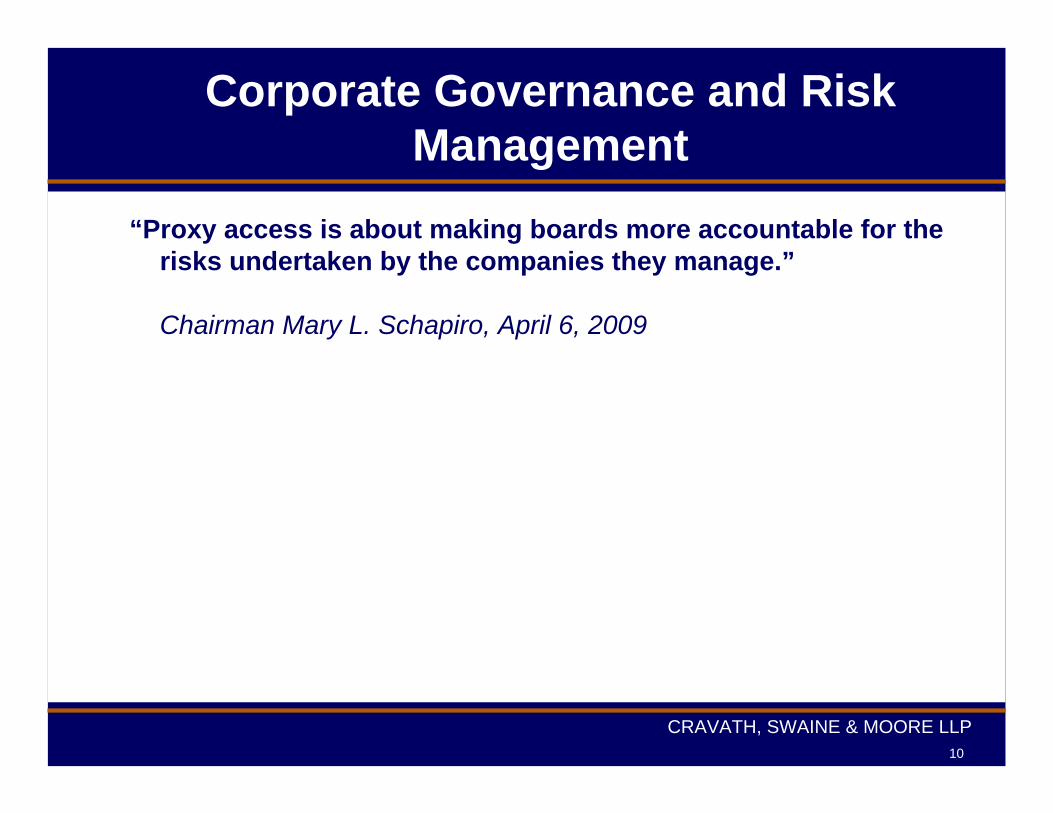

Corporate Governance and Risk Management

“Proxy access is about making boards more accountable for the risks undertaken by the companies they manage.”

Chairman Mary L. Schapiro, April 6, 2009

CRAVATH, SWAINE & MOORE LLP11

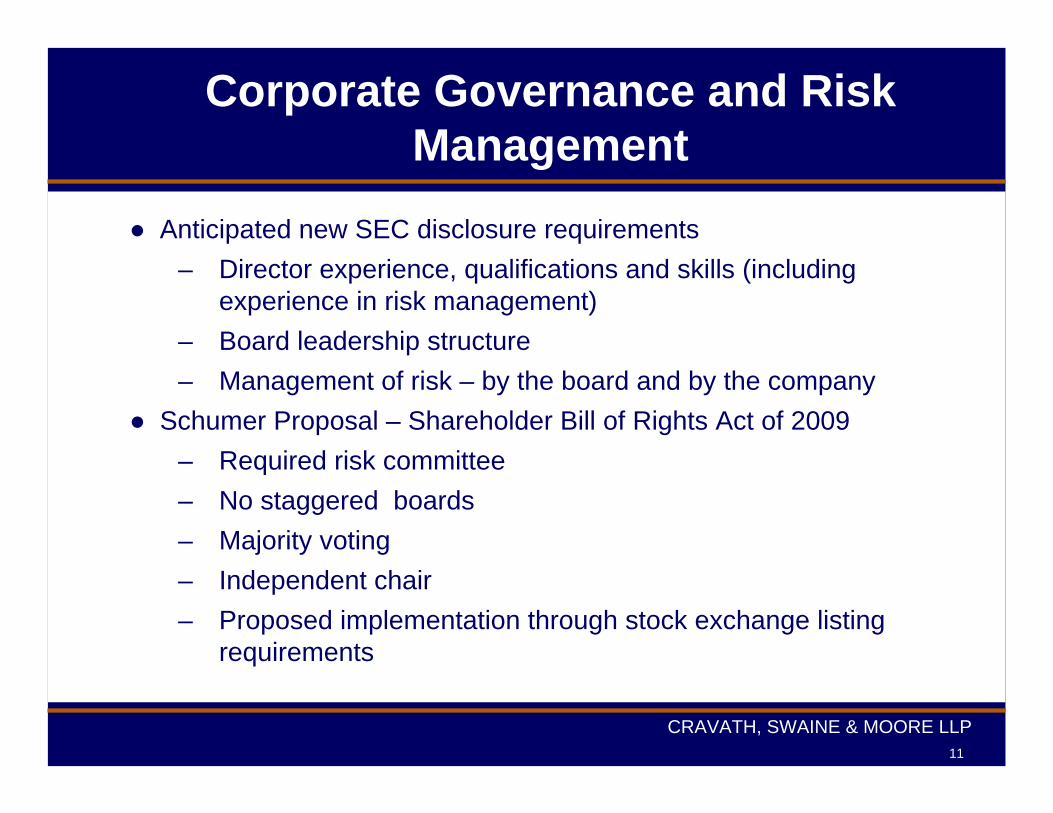

Corporate Governance and Risk Management

● Anticipated new SEC disclosure requirements– Director experience, qualifications and skills (including

experience in risk management)– Board leadership structure– Management of risk – by the board and by the company

● Schumer Proposal – Shareholder Bill of Rights Act of 2009– Required risk committee– No staggered boards– Majority voting– Independent chair– Proposed implementation through stock exchange listing

requirements

CRAVATH, SWAINE & MOORE LLP12

Executive compensation“Compensation disclosure is letting a company's owners know

how their managers and directors ensure that compensation does not drive inappropriate risk-taking.”

Chairman Mary L. Schapiro, April 4, 2009

CRAVATH, SWAINE & MOORE LLP13

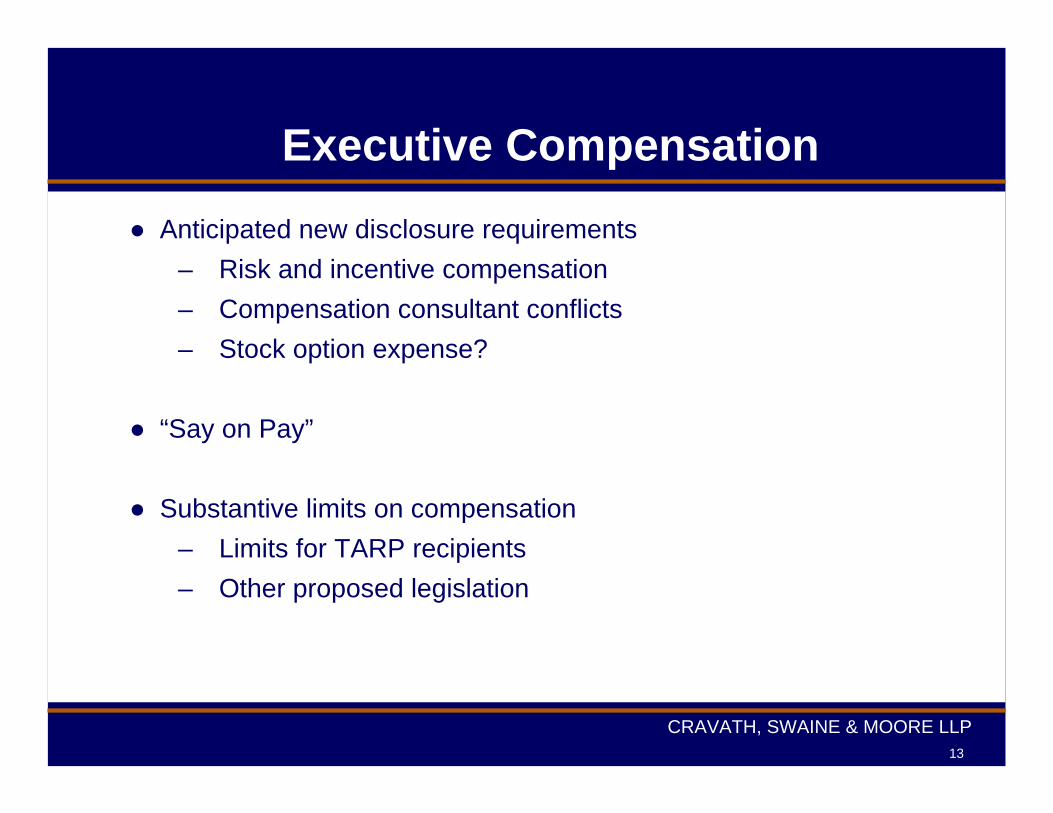

Executive Compensation● Anticipated new disclosure requirements

– Risk and incentive compensation– Compensation consultant conflicts– Stock option expense?

● “Say on Pay”

● Substantive limits on compensation– Limits for TARP recipients– Other proposed legislation

Board Oversight and

Risk Management

Lisa A. FontenotJune 11, 2009

2

Risk Management: Current Environment

• Sharply increased attention as to how companies address risk assessment and management arising from the general perception that undue risk-taking led to the financial crisis.

• Management implementation/review of Enterprise Risk Management programs and appointment of CROs.

• Boards seeking to effectively fulfill their oversight duties.

• Stockholder proposals regarding risk management.

• Legislative proposals seeking additional independence, oversight and transparency.

• Increased regulatory enforcement efforts.

3

Thinking about Risk Management

“A process applied in strategy-setting and across the enterprise, designed to identify events that may affect the entity, and manage risk within its risk appetite...to provide reasonable assurance regarding the achievement of entity objectives.”

- COSO

In short, a business management function that the Board oversees.

4

Risk Management and the Board: Current Frameworks

• State Law Fiduciary Duties

• U.S. and Foreign Laws

Sarbanes-Oxley, Foreign Corrupt Practices Act, TARP Requirements, Federal Sentencing Guidelines

• Stock Exchange Listing Requirements (NYSE)

• Reputation (Ratings agencies, media, regulatory scrutiny)

5

Board Structure for Risk Oversight:Overview

• The appropriate structure for risk oversight by the Board is company-specific - not “one size fits all”.

• Audit Committee: Many companies address risk through the audit committee, including almost all of the Dow 30.NYSE rules require the audit committee to discuss

guidelines and policies to govern the process by which risk assessment and management is undertaken.

The audit committee may delegate oversight of certain risks to other Board committees, provided the audit committee remains responsible for discussing general policies regarding risk management and risk assessment.

6

Board Structure for Risk Oversight

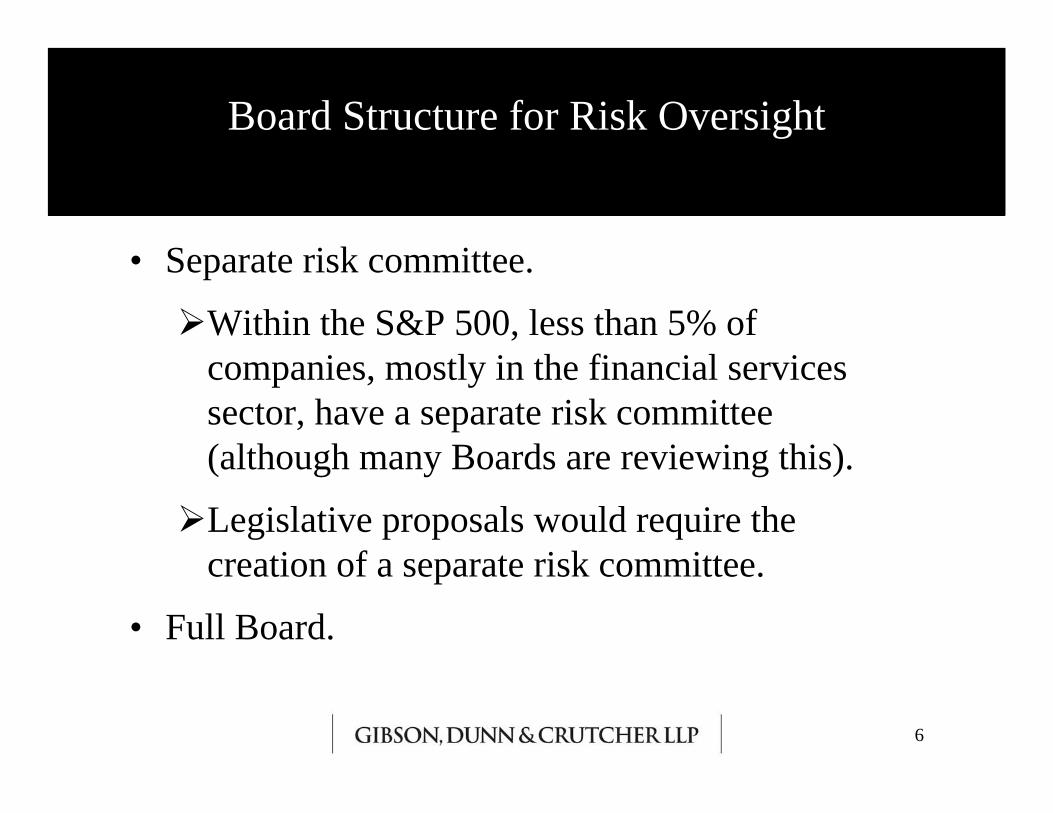

• Separate risk committee.

Within the S&P 500, less than 5% of companies, mostly in the financial services sector, have a separate risk committee (although many Boards are reviewing this).

Legislative proposals would require the creation of a separate risk committee.

• Full Board.

7

• The audit committee is focused on Sarbanes-Oxley compliance, audit and disclosure matters, and financial risk.

• Ask: What is the nature of the significant risks facing the company? Does the audit committee have the ability (time, experience) to

focus on all types of risk? How does risk oversight fit in the overall governance structure? Is oversight sufficiently visible to management & shareholders?

• Ultimately, the full Board needs to understand the risks facing the company and how management addresses them on a firm-wide basis.

Board Structure for Risk Oversight

8

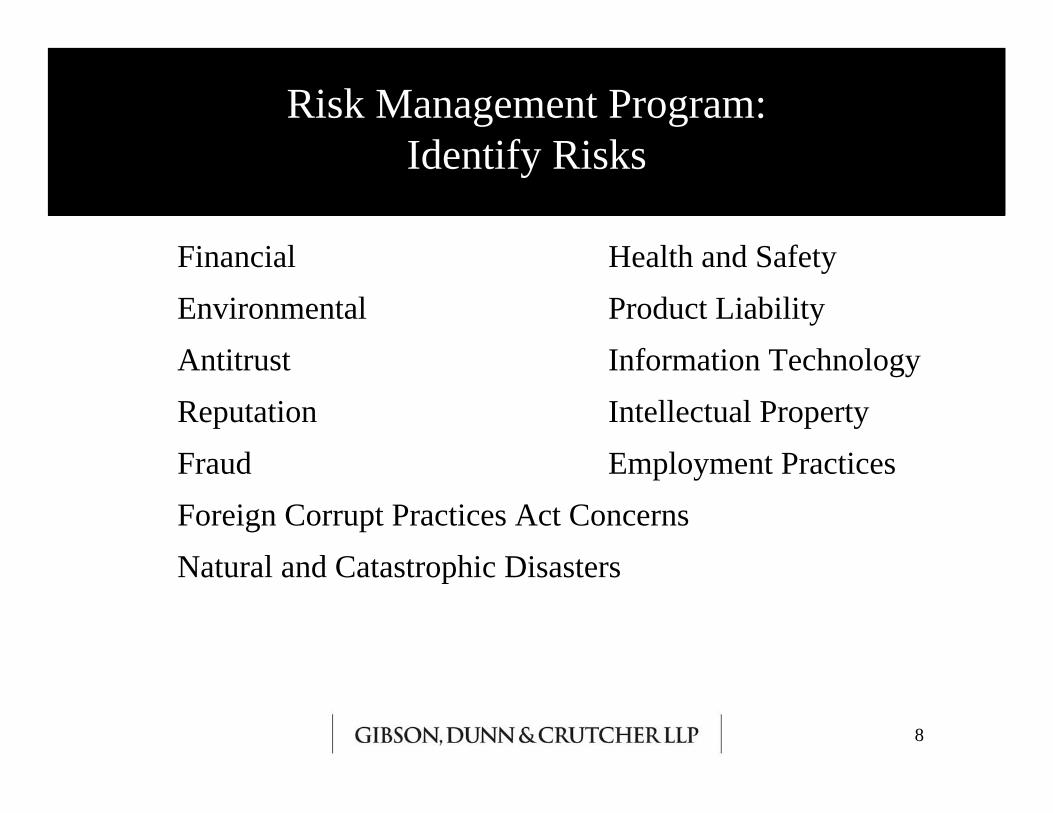

Risk Management Program:Identify Risks

Financial Health and Safety Environmental Product LiabilityAntitrust Information TechnologyReputation Intellectual PropertyFraud Employment PracticesForeign Corrupt Practices Act ConcernsNatural and Catastrophic Disasters

9

Risk Management Program:Evaluate and Manage the Risks

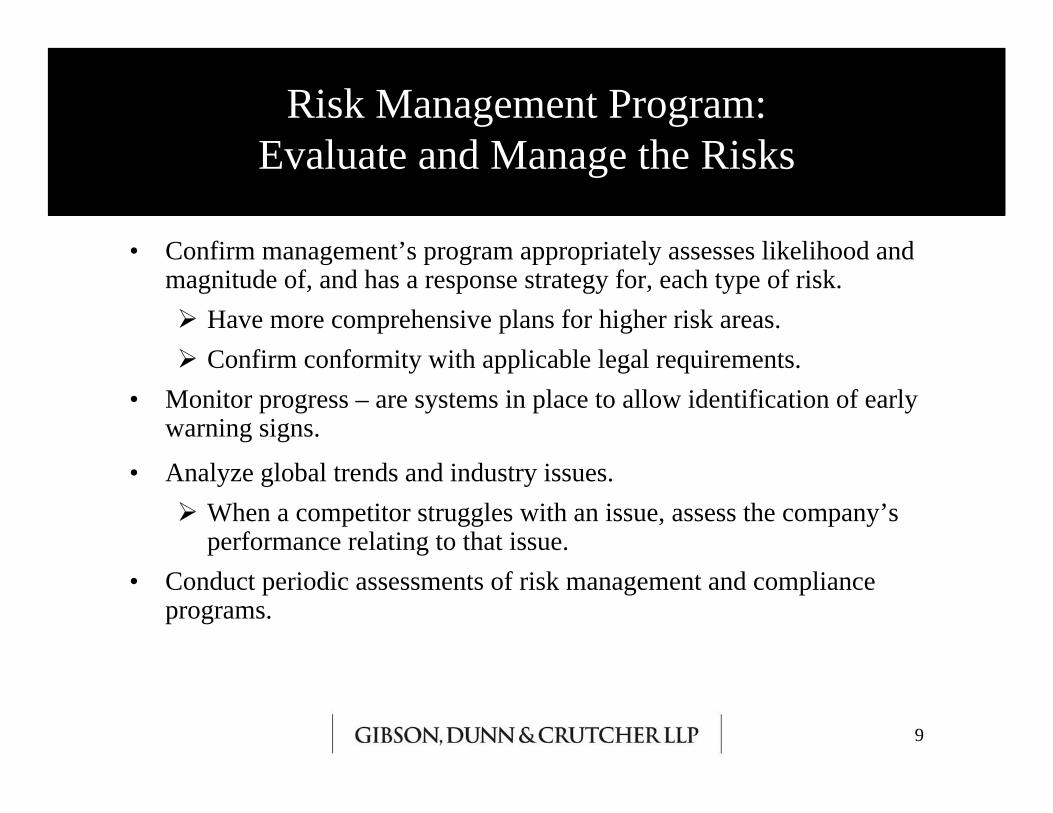

• Confirm management’s program appropriately assesses likelihood and magnitude of, and has a response strategy for, each type of risk. Have more comprehensive plans for higher risk areas. Confirm conformity with applicable legal requirements.

• Monitor progress – are systems in place to allow identification of early warning signs.

• Analyze global trends and industry issues. When a competitor struggles with an issue, assess the company’s

performance relating to that issue.• Conduct periodic assessments of risk management and compliance

programs.

10

Corporate Governance and Risk Management: Set the Tone & Infrastructure

• Assess risks of corporate strategies and business environment.• Determine the company’s tolerance for risk.• Review Board membership to determine qualification to oversee risk

management and management’s ability to manage risk.• Review Code of Conduct and establish procedures to discourage fraud

and non-compliance.• Confirm sufficient budgeting for active and ongoing risk management.• Conduct new and continuing director education/training.• Keep risk discussions on the agenda for Board meetings.• Take prompt action when issues arise.

11

Corporate Governance and Risk Management: Execution

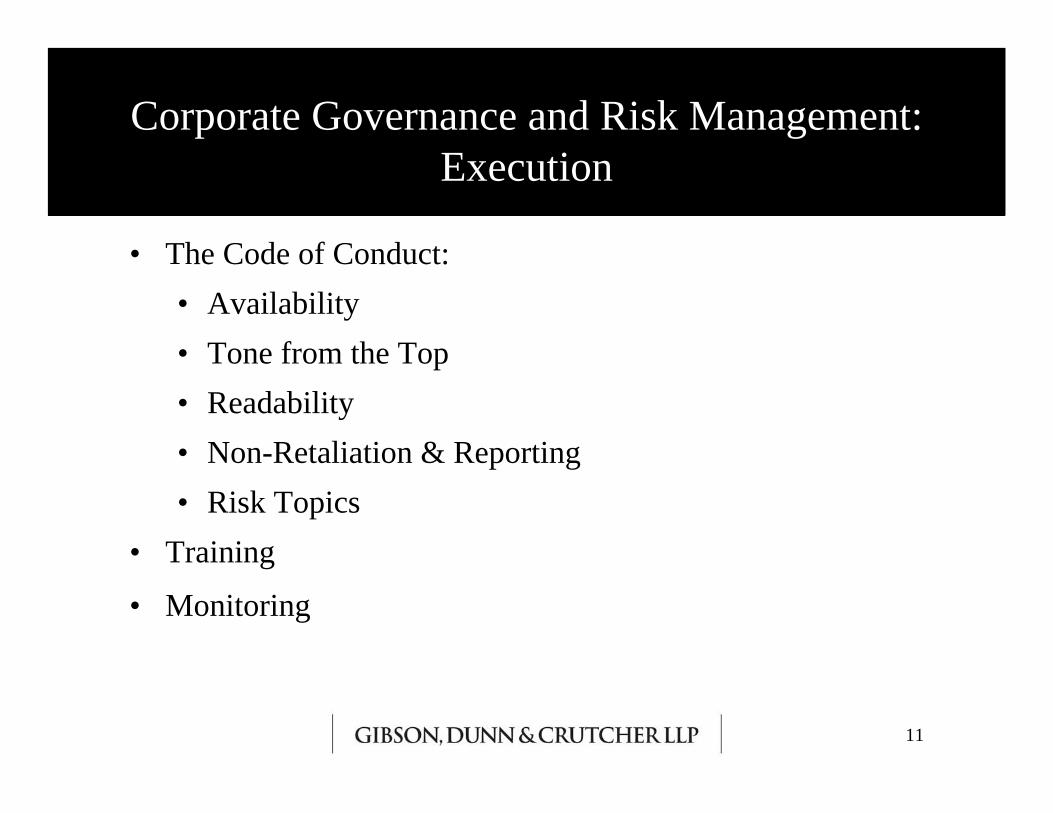

• The Code of Conduct:• Availability• Tone from the Top• Readability• Non-Retaliation & Reporting• Risk Topics

• Training

• Monitoring

12

Corporate Governance and Risk Management:Execution

• Demand adequate flow of accurate, timely information between the Board and management.

• Keep Board guidance to management aligned with corporate strategy and risk appetite.

• Meet privately with compliance and risk officers.• Review controls and reporting practices and processes.• Understand and inquire about disclosures (risk factors,

MD&A, CD&A).• Require a risk evaluation from management of all major

business decisions and transactions.• Address succession planning.

13

Corporate Governance and Risk Management:Execution

• Consider communications with auditors, counsel and other advisors – their perspective is useful.

• Be aware of external commentary on the company, industry, counterparties and overall economy affecting the company.

• Pay particular attention with increased reporting re: credit, counterparty and liquidity risks in the current climate.

• Give attention to violations or realized risks and remediation – may later be viewed as red flags.

14

Oversight and Executive Compensation:Interaction of Compensation & Risk

• TARP implications for standard setting - “Ensure that incentive compensation for senior executives does not encourage unnecessary and excessive risks that threaten the value of the institution.”

• Understand the effects of each pay package component – focus on the ends and means in the CD&A.• What is the link between pay, performance and accountability?• How does the company reward or penalize risk-taking? • Is the company rewarding short vs. long-term results?

• Include risk management as a component of senior executive evaluations.

• Consider features countering short-termism: Claw-backs, equity retention.

• Review comp tally sheets. • Consider ratio between CEO, management and other employee pay.

15

Prepare for Corporate Governance Regulation and Activism

• Continually recognize the importance of transparency and responsiveness to shareholder interests.

• Consider the corporate governance structure and whether action should be taken in light of legislative proposals and rule-making:

• Majority voting• Separating the Chairman and CEO roles• Declassifying the Board• “Say on Pay”• Establishment of separate Risk Committee• Proxy Access

16

Indemnification and Insurance

• Conduct periodic review of D&O insurance to understand coverage and confirm adequacy.

• Confirm charter provisions and indemnification agreements are in place and sufficiently protective.

• Remember the state law fiduciary standards –breach of duty of loyalty is not subject to exculpation or indemnification.

17

Closing

• Risk assessment is not static.

• To maximize shareholder value - embed in strategic thinking and culture this important, ongoing process for management to conduct and for directors to oversee.

18

Find Us

Los Angeles333 South Grand AvenueLos Angeles, California 90071-3197(213) 229-7000

*Peter Wardle – (213) 229-7242*Candice Choh – (213) 229-7793

Orange County3161 Michelson DriveIrvine, California 92612-4412(949) 451-3800

Century City2029 Century Park EastLos Angeles, California 90067-3026(310) 552-8500

New York200 Park AvenueNew York, New York 10166-0193(212) 351-4000

San Francisco555 Mission Street, Suite 3000San Francisco, California 94105-2933(415) 393-8200

Dallas2100 McKinney Avenue, Suite 1100Dallas, Texas 75201-6911(214) 698-3100

MunichWidenmayerstraße 1080538 Munich, Germany49-89-189-33-0

SingaporeOne Raffles QuayLevel# 37-01, North TowerSingapore 04858365-6507-3600

Domestic Offices: Washington, D.C.1050 Connecticut Avenue, N. W.Washington, D. C. 20036-5306(202) 955-8500

Palo Alto1881 Page Mill RoadPalo Alto, California 94304-1125(650) 849-5300

Denver1801 California Street, Suite 4200Denver, Colorado 80202-2641(303) 298-5700

LondonTelephone House2-4 Temple AvenueLondon EC4Y 0HB, United Kingdom44-20-7071-4000

BrusselsAvenue Louise 480 1050 Brussels, Belgium32-2-554-70-00

Paris166 rue du Faubourg Saint Honoré75008 Paris, France33-1-56-43-13-00

DubaiLevel 12, The GateDubai International Finance CentrePO Box 506654, DubaiUnited Arab Emirates971-4-365-0470

International Offices:

Link to Gibson, Dunn & Crutcher article:http://www.gibsondunn.com/Publications/Pages/Treasury‐CongressExpandGovtOversight‐ExecCompensation.aspx

![INSOLVENCY REGULATIONS [ ]](https://img.pdfslide.net/doc/110x75/61570418a097e25c765020e9/insolvency-regulations-.jpg)