Embed Size (px)

Citation preview

Looking Ahead 103

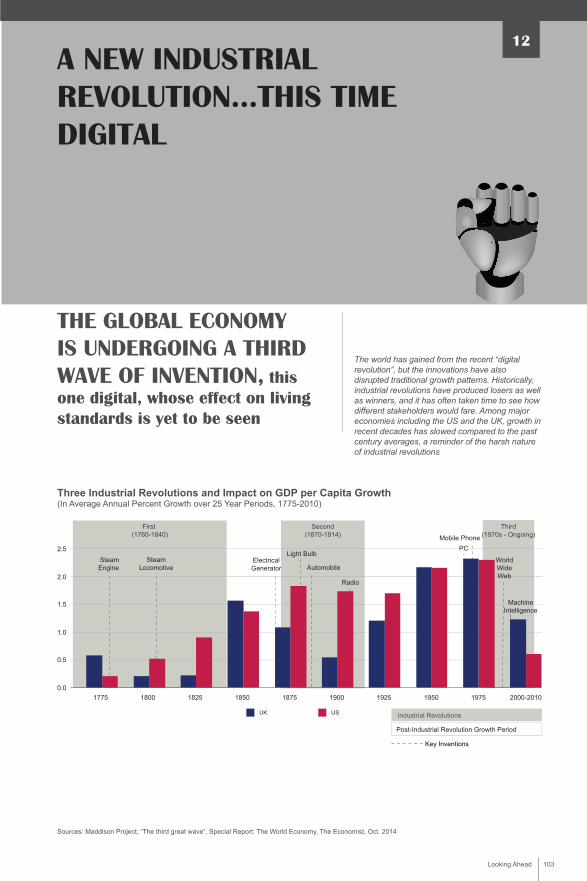

Three Industrial Revolutions and Impact on GDP per Capita Growth(In Average Annual Percent Growth over 25 Year Periods, 1775-2010)

A NEW INDUSTRIAL REVOLUTION…THIS TIME DIGITAL

12

THE GLOBAL ECONOMY IS UNDERGOING A THIRD WAVE OF INVENTION, this one digital, whose effect on living standards is yet to be seen

The world has gained from the recent “digital revolution”, but the innovations have also disrupted traditional growth patterns. Historically, industrial revolutions have produced losers as well as winners, and it has often taken time to see how different stakeholders would fare. Among major economies including the US and the UK, growth in recent decades has slowed compared to the past century averages, a reminder of the harsh nature of industrial revolutions

Sources: Maddison Project; “The third great wave”, Special Report: The World Economy, The Economist, Oct. 2014

1825 1850 18751775 1800 1900 1925 1950 1975 2000-2010

SteamEngine

SteamLocomotive

ElectricalGenerator Automobile

WorldWideWeb

Radio

Mobile Phone

MachineIntelligence

PCLight Bulb

First (1760-1840)

Second(1870-1914)

Third(1970s - Ongoing)

0.0

0.5

1.0

1.5

2.0

2.5

USUK Industrial Revolutions

Post-Industrial Revolution Growth Period

Key Inventions

LA_PublicVersion(Bleed3175)_ENG_V22.indd 103 10/28/15 1:28 PM

Looking Ahead 104

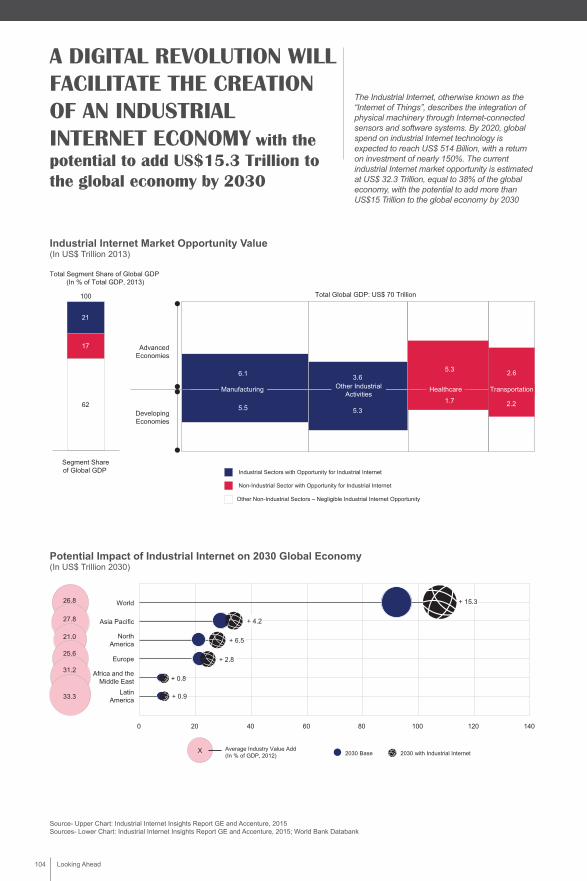

A DIGITAL REVOLUTION WILL FACILITATE THE CREATION OF AN INDUSTRIAL INTERNET ECONOMY with the potential to add US$15.3 Trillion to the global economy by 2030

The Industrial Internet, otherwise known as the “Internet of Things”, describes the integration of physical machinery through Internet-connected sensors and software systems. By 2020, global spend on industrial Internet technology is expected to reach US$ 514 Billion, with a return on investment of nearly 150%. The current industrial Internet market opportunity is estimated at US$ 32.3 Trillion, equal to 38% of the global economy, with the potential to add more than US$15 Trillion to the global economy by 2030

Source- Upper Chart: Industrial Internet Insights Report GE and Accenture, 2015Sources- Lower Chart: Industrial Internet Insights Report GE and Accenture, 2015; World Bank Databank

Industrial Internet Market Opportunity Value (In US$ Trillion 2013)

Potential Impact of Industrial Internet on 2030 Global Economy(In US$ Trillion 2030)

Industrial Sectors with Opportunity for Industrial Internet

Non-Industrial Sector with Opportunity for Industrial Internet

Other Non-Industrial Sectors – Negligible Industrial Internet Opportunity

6.1 3.6 2.65.3

2.21.75.5 5.3Developing

Economies

AdvancedEconomies

Manufacturing Other IndustrialActivities

Healthcare Transportation

Total Global GDP: US$ 70 Trillion

Total Segment Share of Global GDP (In % of Total GDP, 2013)

62

17

21

Segment Shareof Global GDP

100

0 20 40 60 80 100 120 140

+ 15.3

+ 4.2

+ 6.5

+ 2.8

+ 0.8

+ 0.9

World

Asia Pacific

Europe

Africa and theMiddle East

NorthAmerica

LatinAmerica

26.8

33.3

27.8

21.0

25.6

31.2

2030 with Industrial Internet2030 BaseAverage Industry Value Add (In % of GDP, 2012)

X

LA_PublicVersion(Bleed3175)_ENG_V22.indd 104 10/28/15 1:28 PM

Looking Ahead 105

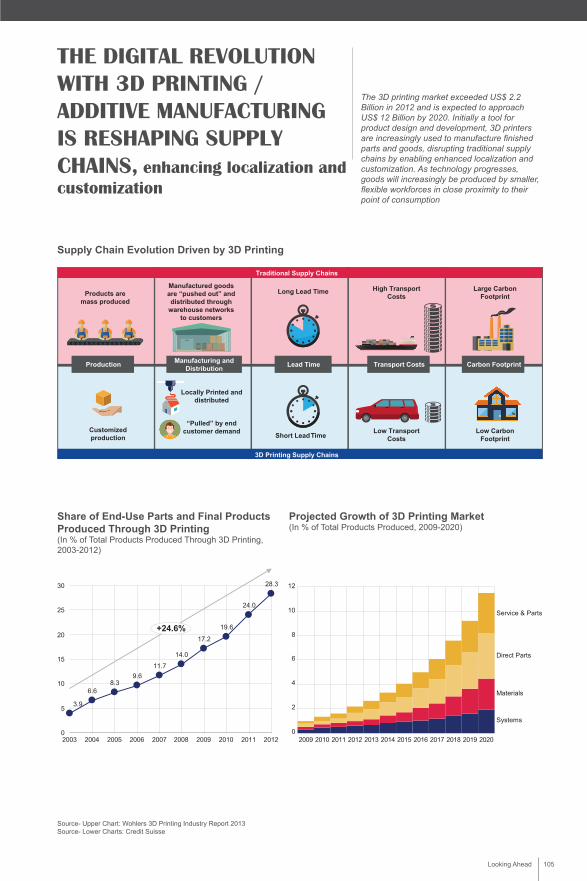

THE DIGITAL REVOLUTION WITH 3D PRINTING / ADDITIVE MANUFACTURING IS RESHAPING SUPPLY CHAINS, enhancing localization and customization

The 3D printing market exceeded US$ 2.2 Billion in 2012 and is expected to approach US$ 12 Billion by 2020. Initially a tool for product design and development, 3D printers are increasingly used to manufacture finished parts and goods, disrupting traditional supply chains by enabling enhanced localization and customization. As technology progresses, goods will increasingly be produced by smaller, flexible workforces in close proximity to their point of consumption

Supply Chain Evolution Driven by 3D Printing

Share of End-Use Parts and Final Products Produced Through 3D Printing(In % of Total Products Produced Through 3D Printing, 2003-2012)

Projected Growth of 3D Printing Market(In % of Total Products Produced, 2009-2020)

Source- Upper Chart: Wohlers 3D Printing Industry Report 2013Source- Lower Charts: Credit Suisse

Long Lead Time

Short Lead Time

Lead Time

High TransportCosts

Low TransportCosts

Transport Costs

Large CarbonFootprint

Low CarbonFootprint

Carbon Footprint

Products aremass produced

Customizedproduction

Production

Manufactured goodsare “pushed out” anddistributed through

warehouse networksto customers

Locally Printed anddistributed

“Pulled” by endcustomer demand

Manufacturing andDistribution

Traditional Supply Chains

3D Printing Supply Chains

0

5

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

+24.6%

28.3

24.0

19.6

17.2

14.0

11.79.6

8.36.6

3.9

0

2

4

8

10

6

12

20192018201720162015201420132012201120102009 2020

Service & Parts

Direct Parts

Materials

Systems

LA_PublicVersion(Bleed3175)_ENG_V22.indd 105 10/28/15 1:28 PM

Looking Ahead 106

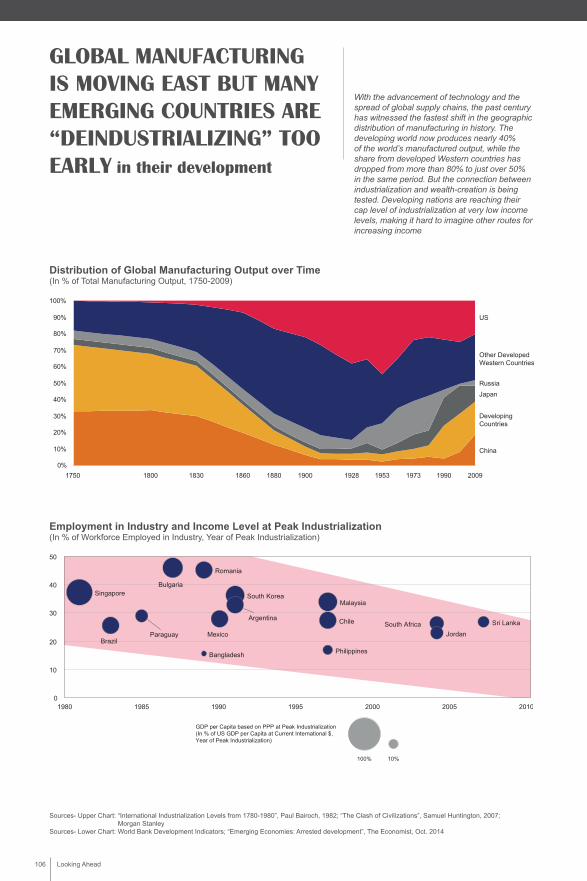

GLOBAL MANUFACTURING IS MOVING EAST BUT MANY EMERGING COUNTRIES ARE “DEINDUSTRIALIZING” TOO EARLY in their development

With the advancement of technology and the spread of global supply chains, the past century has witnessed the fastest shift in the geographic distribution of manufacturing in history. The developing world now produces nearly 40% of the world’s manufactured output, while the share from developed Western countries has dropped from more than 80% to just over 50% in the same period. But the connection between industrialization and wealth-creation is being tested. Developing nations are reaching their cap level of industrialization at very low income levels, making it hard to imagine other routes for increasing income

Distribution of Global Manufacturing Output over Time(In % of Total Manufacturing Output, 1750-2009)

Employment in Industry and Income Level at Peak Industrialization(In % of Workforce Employed in Industry, Year of Peak Industrialization)

Sources- Upper Chart: “International Industrialization Levels from 1780-1980”, Paul Bairoch, 1982; “The Clash of Civilizations”, Samuel Huntington, 2007; Morgan Stanley

Sources- Lower Chart: World Bank Development Indicators; “Emerging Economies: Arrested development”, The Economist, Oct. 2014

1980 1990 20102000 200519951985

100% 10%

GDP per Capita based on PPP at Peak Industrialization(In % of US GDP per Capita at Current International $,Year of Peak Industrialization)

0

10

20

30

40

50

South Africa

Singapore

Romania

Paraguay

Philippines

Malaysia

Mexico

Sri Lanka

South Korea

Jordan

Chile

Brazil

Bulgaria

Bangladesh

Argentina

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China

Japan

Russia

US

20091990197319531928190018801860183018001750

Other DevelopedWestern Countries

DevelopingCountries

LA_PublicVersion(Bleed3175)_ENG_V22.indd 106 10/28/15 1:28 PM

Looking Ahead 107

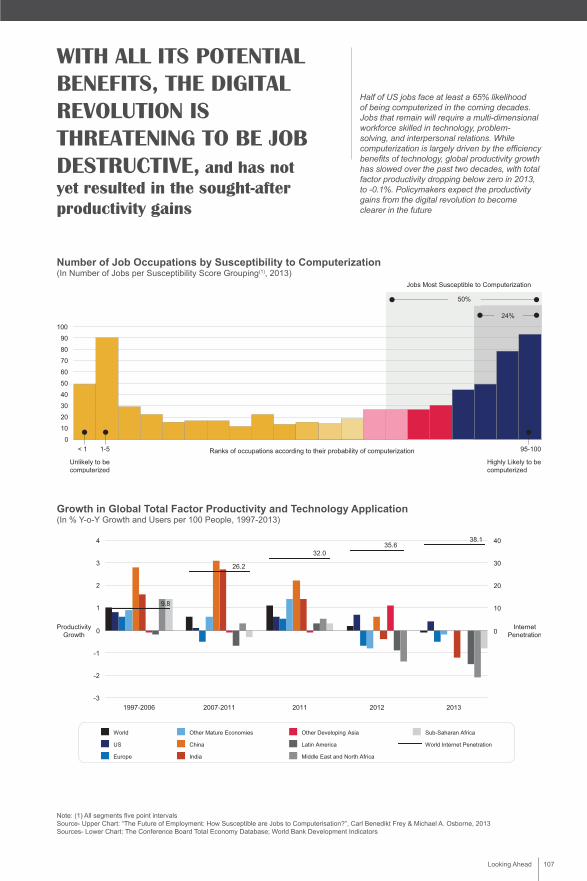

WITH ALL ITS POTENTIAL BENEFITS, THE DIGITAL REVOLUTION IS THREATENING TO BE JOB DESTRUCTIVE, and has not yet resulted in the sought-after productivity gains

Half of US jobs face at least a 65% likelihood of being computerized in the coming decades. Jobs that remain will require a multi-dimensional workforce skilled in technology, problem-solving, and interpersonal relations. While computerization is largely driven by the efficiency benefits of technology, global productivity growth has slowed over the past two decades, with total factor productivity dropping below zero in 2013, to -0.1%. Policymakers expect the productivity gains from the digital revolution to become clearer in the future

Number of Job Occupations by Susceptibility to Computerization(In Number of Jobs per Susceptibility Score Grouping(1), 2013)

Growth in Global Total Factor Productivity and Technology Application(In % Y-o-Y Growth and Users per 100 People, 1997-2013)

Note: (1) All segments five point intervalsSource- Upper Chart: “The Future of Employment: How Susceptible are Jobs to Computerisation?”, Carl Benedikt Frey & Michael A. Osborne, 2013Sources- Lower Chart: The Conference Board Total Economy Database; World Bank Development Indicators

0

10

20

30

40

50

60

70

80

90

100

50%

24%

Jobs Most Susceptible to Computerization

< 1 95-1001-5 Ranks of occupations according to their probability of computerization

Unlikely to becomputerized

Highly Likely to becomputerized

ProductivityGrowth

InternetPenetration

-3

-2

-1

0

1

2

3

4 40

30

20

10

0

2013201220112007-20111997-2006

9.8

26.2

32.035.6

38.1

World Internet Penetration

Sub-Saharan Africa

Middle East and North Africa

Latin America

Other Developing Asia

India

China

Other Mature Economies

Europe

US

World

LA_PublicVersion(Bleed3175)_ENG_V22.indd 107 10/28/15 1:28 PM

![From Industrial Revolution to Digital Innovation [Poster]](https://img.pdfslide.net/doc/110x75/61e4e41f2e642854c5653fe3/from-industrial-revolution-to-digital-innovation-poster.jpg)