Embed Size (px)

DESCRIPTION

A Note to the User of This File Visit http://facpub.stjohns.edu/~kwonw/Blackwell.html to check updates for this chapter. - PowerPoint PPT Presentation

Citation preview

1

A Note to the User of This FileA Note to the User of This File

Visit http://facpub.stjohns.edu/~kwonw/Blackwell.html to check updates for this chapter.

This file as well as all other Power Point files for the book, “Risk Management and Insurance: Perspectives in a Global Economy” authored by Skipper and Kwon and published by Blackwell (2007), has been created solely for classes where the book is used as a text. Use or reproduction of the file by

any means, known or to be known, is prohibited without prior written permission by the authors who can be

contacted at [email protected].

2

All the slides in this file are done with a single master All the slides in this file are done with a single master slide format. To change the background, style or bothslide format. To change the background, style or both

Click the drop-down folders of the program:

[View] [Master] [Slide/Handout Master]

Once you close the pop-up menu, all slides will change Once you close the pop-up menu, all slides will change automatically. Of course, you may change a single slide automatically. Of course, you may change a single slide

manually.manually.

Risk Management and Insurance: Perspectives in a Global EconomyRisk Management and Insurance: Perspectives in a Global Economy

15. Risk Management for 15. Risk Management for CatastrophesCatastrophes

Click Here to Add Professor and Course Information

4

Points to PonderPoints to Ponder

Risk analysis

Risk control

Risk financing

Risk Analysis

6

Risk AnalysisRisk Analysis

The analysis for events that hold a catastrophic potential are largely identical to those for non-catastrophic event, except:

Risk managers devote greater time and effort to exploring the susceptibility of the firm’s physical structure to damage.

Such corporations commonly rely more heavily on modeling to estimate the probable effects of natural catastrophes on their businesses.

Scenario planning can play a significant role.

7

Susceptibility to DamageSusceptibility to Damage

Design features and construction qualityThe tradeoff between cost and quality

Causes of damage

Natural

Human-made (e.g., terrorists or disgruntled employees)

Age of structuresThe Great Hanshin (Kobe) Earthquake in Japan in 1995

InfrastructureTransportation and communication facilities of the affected area

Critical to a prompt and orderly recovery

Hurricane Katrina in New Orleans in 2005 in the U.S.

8

Catastrophe ModelingCatastrophe Modeling

The use of computer-assisted mathematical techniques to estimate possible losses associated with catastrophic events

Use of site and specific property characteristics (the so-called “exposure data”)

Primarily for natural catastrophes such as hurricanes, earthquakes, storms, floods

Some for terrorism (e.g., AIR modeling)

Widely used by insurers, reinsurers and intermediariesFigure 15.1 for a natural catastrophe model

9

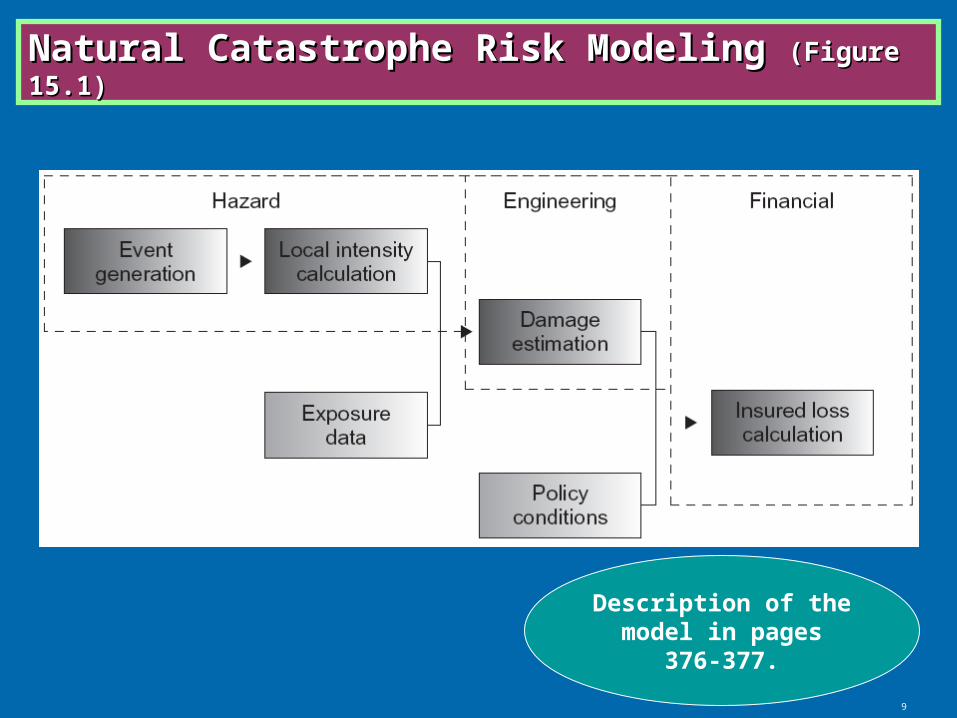

Natural Catastrophe Risk Modeling Natural Catastrophe Risk Modeling (Figure 15.1)(Figure 15.1)

Description of the model in pages 376-

377.

10

Scenario PlanningScenario Planning

A strategic planning method in which analysts generate simulation games that are used by management to consider and develop plans to deal with alternative futures

Scenarios should bring forth decisions by those who are ultimately responsible for making them.

Subsumes elements that are difficult and often impossible to formalize, let alone quantify

It is intended to cause decision-makers to realize that they consciously or unconsciously likely have a preconceived notion of what the “official future” will hold.

Insight 15.1Figure 15.2

11

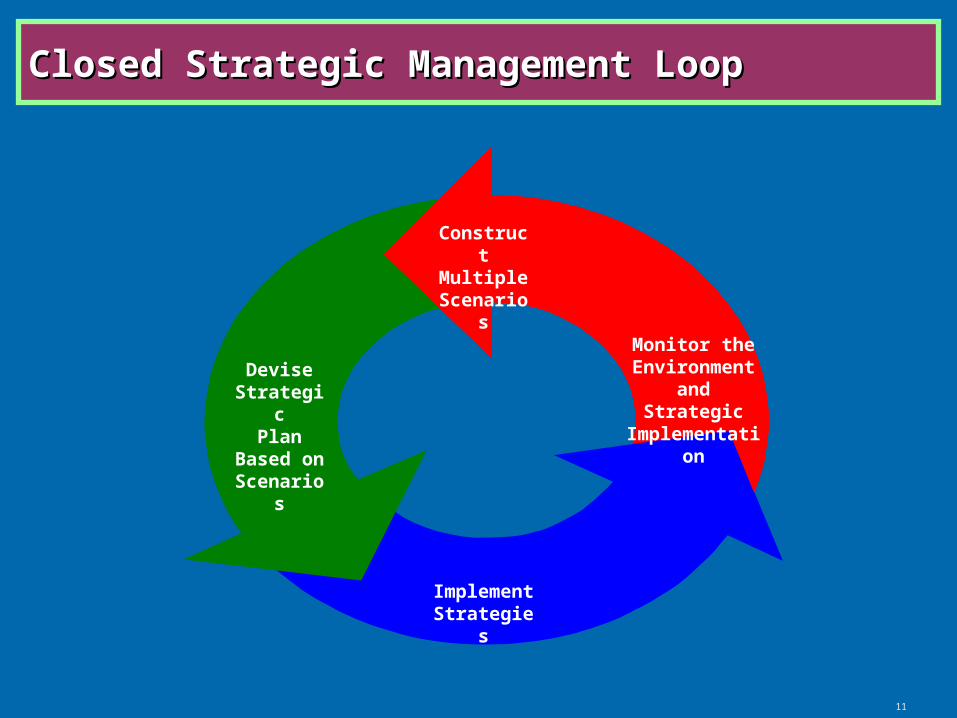

Closed Strategic Management LoopClosed Strategic Management Loop

ConstructMultiple

Scenarios

DeviseStrategic

Plan Based on Scenarios

ImplementStrategies

Monitor theEnvironment and Strategic

Implementation

12

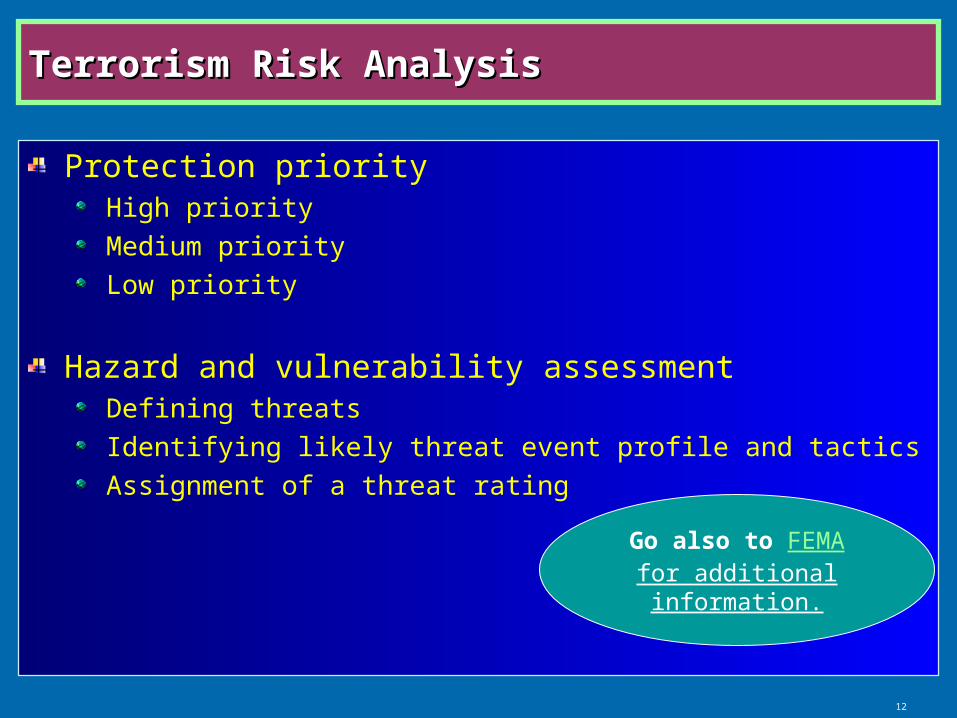

Terrorism Risk AnalysisTerrorism Risk Analysis

Protection priorityHigh priority

Medium priority

Low priority

Hazard and vulnerability assessmentDefining threats

Identifying likely threat event profile and tactics

Assignment of a threat rating

Go also to FEMA for additional information.

Risk Control

14

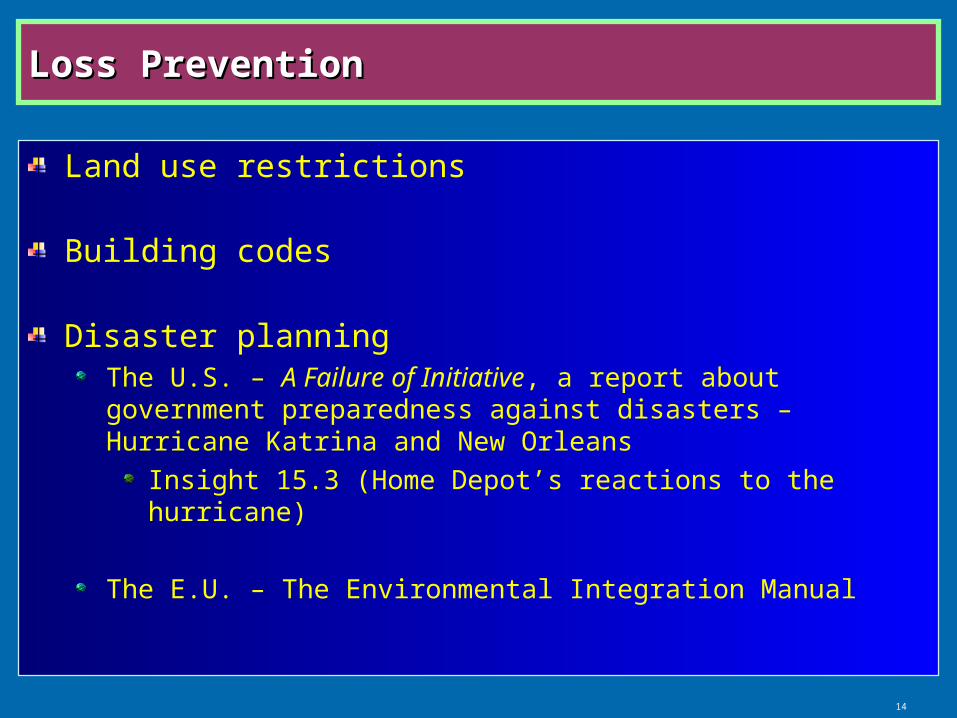

Loss PreventionLoss Prevention

Land use restrictions

Building codes

Disaster planningThe U.S. – A Failure of Initiative, a report about government preparedness against disasters – Hurricane Katrina and New Orleans

Insight 15.3 (Home Depot’s reactions to the hurricane)

The E.U. – The Environmental Integration Manual

15

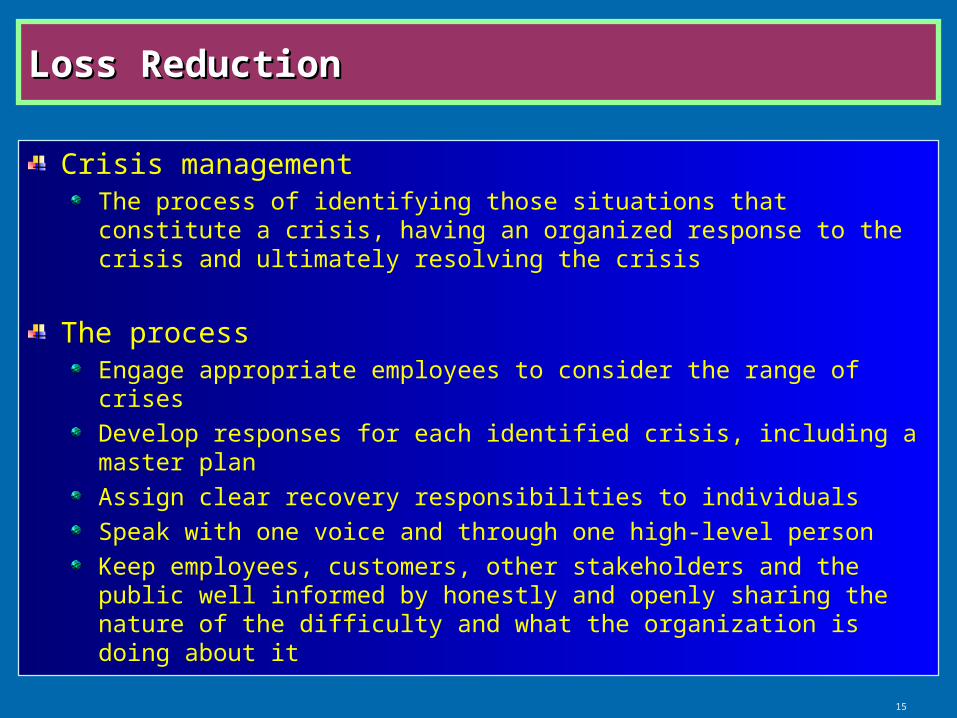

Loss ReductionLoss Reduction

Crisis managementThe process of identifying those situations that constitute a crisis, having an organized response to the crisis and ultimately resolving the crisis

The processEngage appropriate employees to consider the range of crises

Develop responses for each identified crisis, including a master plan

Assign clear recovery responsibilities to individuals

Speak with one voice and through one high-level person

Keep employees, customers, other stakeholders and the public well informed by honestly and openly sharing the nature of the difficulty and what the organization is doing about it

16

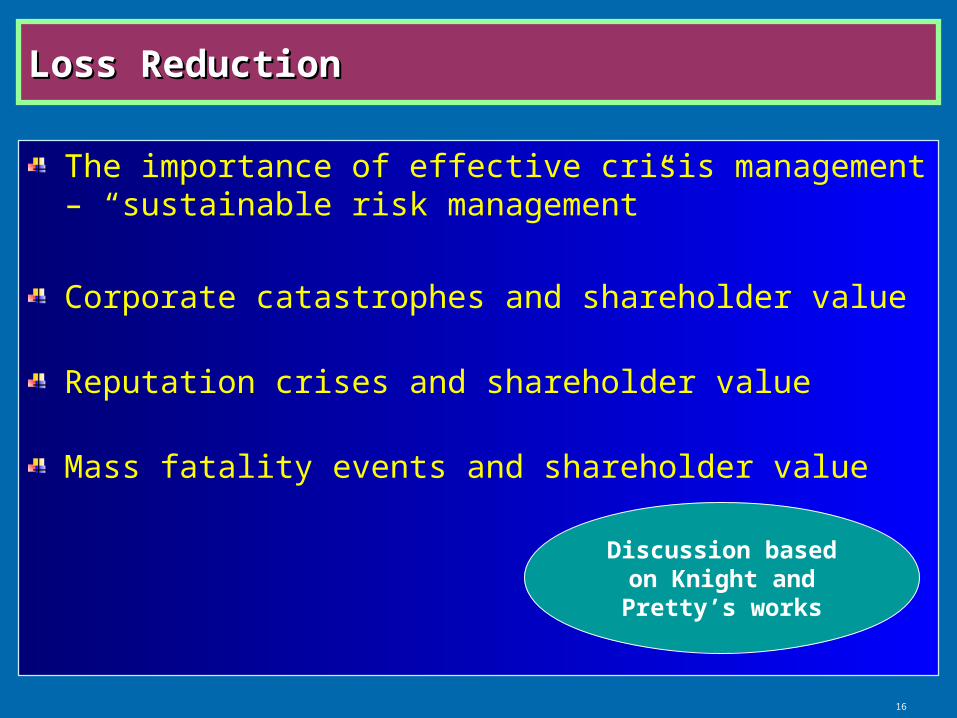

Loss ReductionLoss Reduction

The importance of effective crisis management – “sustainable risk management”

Corporate catastrophes and shareholder value

Reputation crises and shareholder value

Mass fatality events and shareholder value

Discussion based on Knight and Pretty’s

works

17

Loss ReductionLoss Reduction

Insight 15.4 (Tylenol case)

Insight 15.5 (Boycott)

Insight 15.6 (Reputation loss)

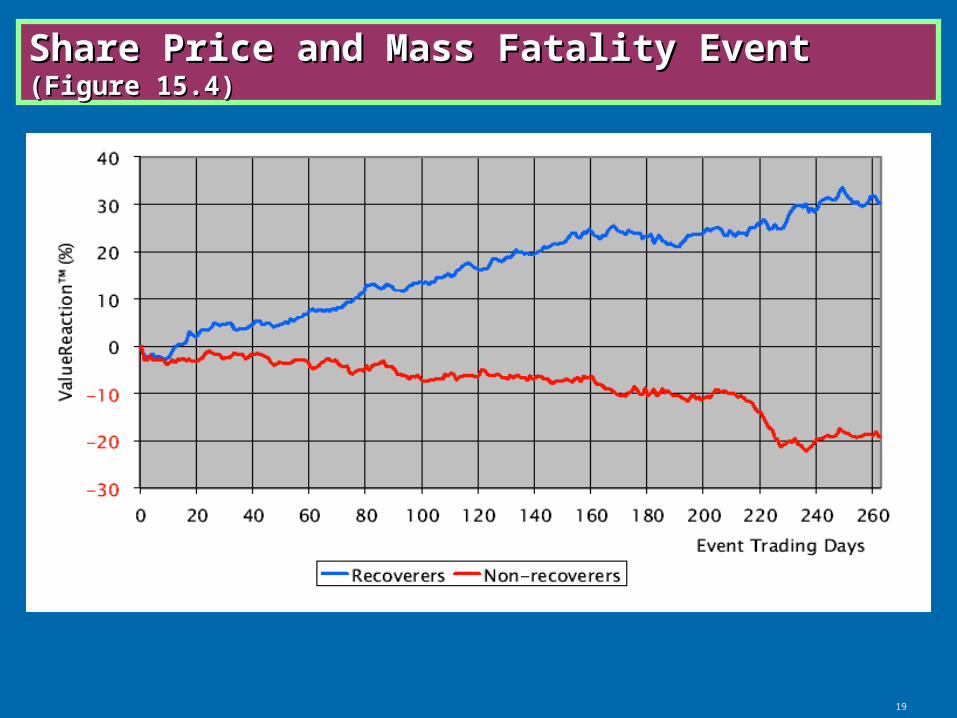

Figure 15.4 (Reaction of Share Prices to Mass Fatality Events)

18

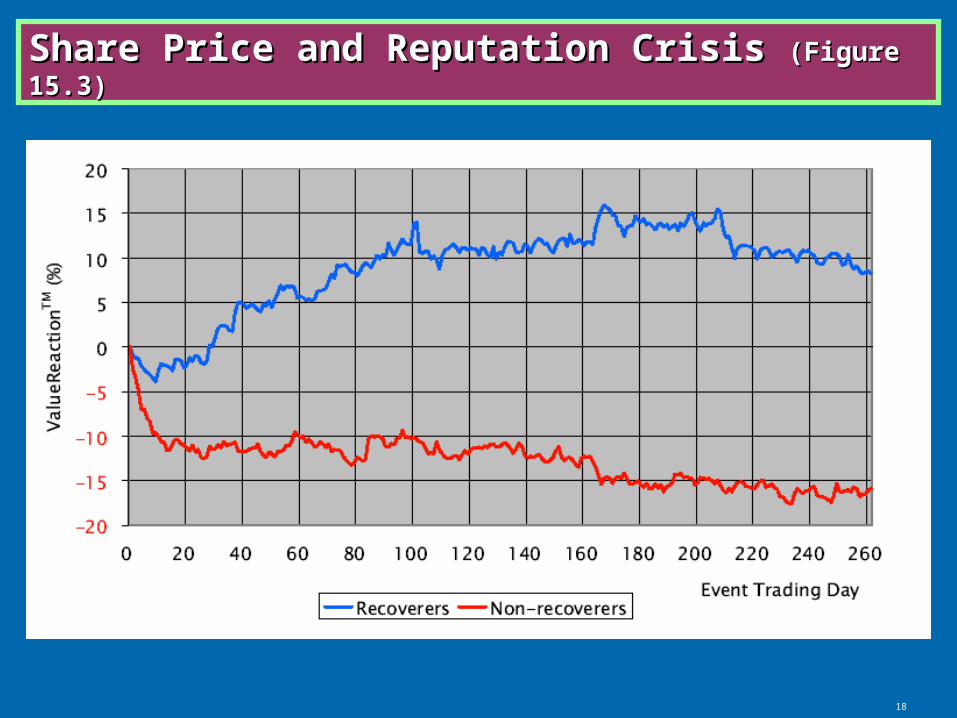

Share Price and Reputation Crisis Share Price and Reputation Crisis (Figure 15.3)(Figure 15.3)

19

Share Price and Mass Fatality Event Share Price and Mass Fatality Event (Figure 15.4)(Figure 15.4)

Risk Financing

21

RetentionRetention

Recommended whenInsurance is unavailable or unaffordable

Property owners have the capability of financing losses internally

Retention is often used along with other risk financing options.

For example, excess insurance on top of large retention

The problems with retention are vividly demonstrated when a catastrophe occurs.

Especially in developing countries

22

InsuranceInsurance

Risk financing capacity for catastrophic loss exposures remains a major concern for the insurance industry internationally

Insurance policies often exclude coverage for many catastrophic events.

Nuclear-related events

Flood damages

Earth movement

Terrorist act

Countrywide variations exist.

23

Insurance – Catastrophe ReinsuranceInsurance – Catastrophe Reinsurance

Often a risk-financing and loss-sharing arrangement between insurance firms

Several reinsurers that specialize in catastrophe reinsuranceThe Caribbean

The London market

24

Insurance – Private Risk PoolsInsurance – Private Risk Pools

A wide array of uses by insurance companiesResidual markets for nonstandard drivers in automobile insurance or employers in workers’ compensation

A case of catastrophic loss exposure – nuclear activityThe World Nuclear Association

OECD’s Paris Convention on Third Party Liability in the Field

of Nuclear Energy of 1960 (amended in 2004)

The Price-Anderson Act in 1957 (U.S.)

Insight 15.7

25

Nuclear Insurance Coverage Nuclear Insurance Coverage (Insight 15.7)(Insight 15.7)

Facility form (liability) policy

Secondary financial protection policy

Master worker policy

Suppliers and transporters policy

26

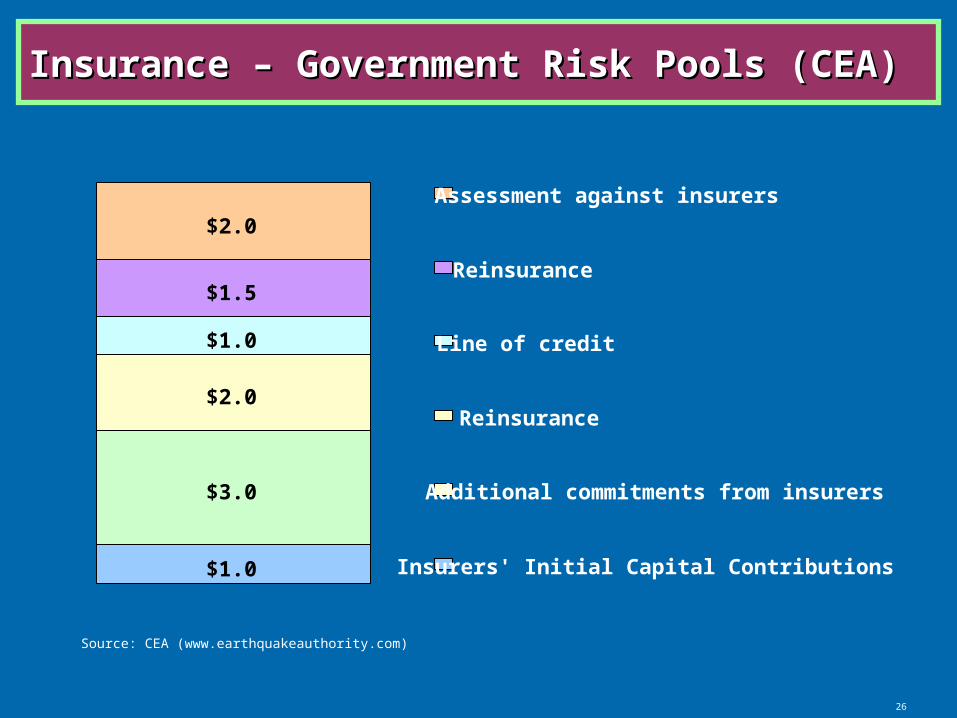

Insurance – Government Risk Pools (CEA)Insurance – Government Risk Pools (CEA)

$1.0

$3.0

$2.0

$1.0

$1.5

$2.0

Assessment against insurers

Reinsurance

Line of credit

Reinsurance

Additional commitments from insurers

Insurers' Initial Capital Contributions

Source: CEA (www.earthquakeauthority.com)

27

Insurance – Terrorism Risk Insurance – Terrorism Risk

Australia – Australian Reinsurance Pool

Austria – Terrorpool Austria

France – GAREAT

Germany – Extremus

Israel – The Property and Tax Compensation Fund

The Netherlands – NHT

Spain – CCS

South Africa – SASRIA

The U.K. – Pool Re

The U.S. – Terrorism Risk and Insurance Act

Table 15.1

28

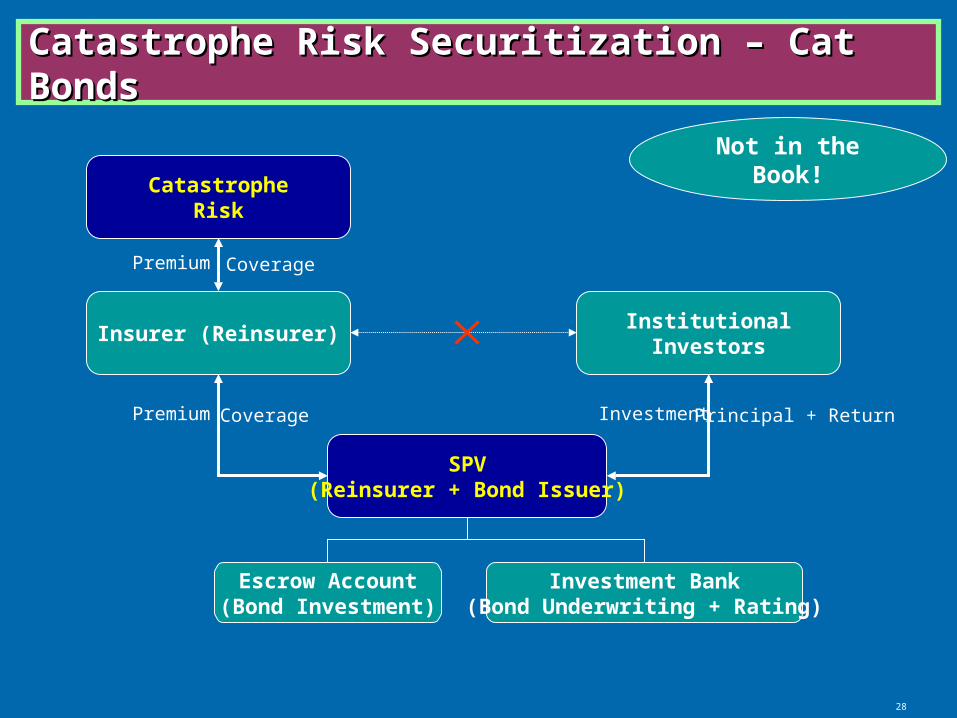

Catastrophe Risk Securitization – Cat BondsCatastrophe Risk Securitization – Cat Bonds

InstitutionalInvestors

CatastropheRisk

SPV(Reinsurer + Bond Issuer)

Premium Coverage Investment Principal + Return

Insurer (Reinsurer)

Premium Coverage

Investment Bank(Bond Underwriting + Rating)

Escrow Account(Bond Investment)

Not in the Book!

Discussion Questions

30

Discussion Question 1Discussion Question 1

Older facilities often are more susceptible to damage than newer ones. Explain why this is so and make a case for why the government should not require that the owners of such older facilities to upgrade them to contemporary structural standards?

31

Discussion Question 2Discussion Question 2

Loss mitigation is a fundamental factor in better managing the physical environment risk. What aspects of loss mitigation do you believe offer the most promise for the future?

32

Discussion Question 3Discussion Question 3

Develop at least two “alternative futures” for how risk management might change for operators of nuclear power plants.

33

Discussion Question 4Discussion Question 4

If sound crisis management is as important as suggested in this chapter, why do major corporations seem to accord it so little attention?

34

Discussion Question 5Discussion Question 5

We have described terrorism risk pools in selected countries.

Find the reasons why some governments listed in the table acted upon creation of a terrorism insurance scheme before September 11, 2001.

Do you find any other governments offering similar programs? (Hint: Examine Brazil, Finland, Hong Kong and Japan for possible programs.)