Embed Size (px)

Citation preview

A P R I L 2 0 0 6

Po t e n t i a l I m p a c t o f t h eC e n t r a l A m e r i c a f r e e

t r a d e A g r e e m e n t( C A F T A )

w i t h t h e U n i t e dS t a t e s o n C e n t r a l

A m e r i c a n O r g a n i cA g r i c u l t u r e B u s i n e s s

Produced by: And Executed by:

cooperation

inters e c oSecretaría de Estado de economíaSegretariato di Stato dell’economiaSecrétariat d’Etat á l’économieState Secretariat for Economic A�airs

SWITZE

R LAND

+

A Project Commissioned by:

� Enhancing Organic and Fair Trade !

This study has been developed for the project ECOMERCADOS, which is financed by SECO (Swiss State Secretariat for Economic Affairs) and carried out by INTERCOOPERATION (Swiss Foundation for Development and International Cooperation). Ecomercados started its operation in January 2005 in the area of Central America, with emphasis on Costa Rica and Nicaragua.

The main objective of the project is to promote and increase the trade of organic and fairtrade products in the export, regional and local markets, aiming at fostering the markets access for the small and medium producers and thus increasing employment and income for them.This study has been prepared by Lawrence Pratt, CEO; Bernard Kilian, Production and Research manager and Luis Rivera, Associate researcher of CIMS (Sustainable Markets Intelligence Center). Alajuela, Costa Rica.

For more information, please contact:

[email protected]: (506) 437 2200 Website: www.cims-la.com

The authors have compiled all statements, results and materials contained in this publication, to the best of their knowledge. The material has also been verified by CIMS and partners. However, the possibility of errors cannot be ruled out and the authors and/or publisher do not accept any responsibility or liability for any such error that might be contained in the publication.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of ECOMERCADOS.

April 2006

ABOUT THIS STUDY

�Enhancing Organic and Fair Trade !

EXECUTIVE SUMMARY

he United States-Central American Free Trade Agreement (CAFTA) is expected to entry into force in 2006. The main results from CAFTA are the consolidation of CBI trade preferences and the creation of clear market rules for the parties. Regarding agriculture, CAFTA opens the US and Central American markets widely, with the elimination of almost 100 percent of import tariffs. Still, the sensitive agricultural products of Central America obtained additional protection with long tariff phase-out periods. Expected effects of the agreement will depend on the implementation of complementary policies to improve the region’s competitiveness. Within this scenario, organic agriculture in Central America still faces historical traditional sector challenges: low value added, limited access to infrastructure, technology and financial resources, less competitive quality standards, certification problems, and incipient value chain positioning. Still, organic business in the

region has been growing, and US market dynamism offers significant opportunities for further business development. At the same time, stricter US market regulations and more demanding consumer preferences pose additional challenges to Central American organic producers. Therefore, CAFTA´s possible impact would be directly related to the consolidation of national and regional efforts to enhance the agricultural sector conditions in order to compete successfully. The main lesson from NAFTA is that a trade agreement is not enough to modernize an economy and create development opportunities for all. The main challenge for the traditional and organic agriculture of Central America remains the same: develop stronger entrepreneurship, increase private investment, achieve higher competitiveness levels, and promote a closer integration with international high value added chains.

T

� Enhancing Organic and Fair Trade !

ABBREVIATIONS

APHIS Animal and Plant Health Inspection Service

CA Central America

CAFTA Central America Free Trade Agreement with the United States

CBI Caribbean Basin Initiative

CBTPA Caribbean Basin Trade Partnership Act

CGE Computable General Equilibrium

CIMS Sustainable Trade Intelligence Center

EU European Union

FDI Foreign Direct Investment

GDP Gross Domestic Product

GNP Gross National Product

GSP Generalized System of Preferences

GTAP Global Trade Analysis Project

HACCP Hazard Analysis and Critical Control Point

MFN Most Favored Nation

NGO Non-governmental Organization

SPS Sanitary and Phytosanitary Measures

US United States

USITC United States International Trade Commission

5Enhancing Organic and Fair Trade !

TABLE OF CONTENTS

1. INTRODUCTION.........................................................................................................................................................62. AGRICULTURAL TRADE BETWEEN CENTRAL AMERICA AND THE US:

A GOOD TRADITIONAL BUSINESS............................................................................................................................73. CAFTA RESULTS FOR THE CENTRAL AMERICAN AGRICULTURAL SECTOR:

MARKET ACCESS IS THE KEY...................................................................................................................................104. POTENTIAL IMPACTS OF CAFTA FOR THE ECONOMY AND THE

AGRICULTURAL SECTOR IN CENTRAL AMERICA:A GENERAL EQUILIBRIUM ANALYSIS......................................................................................................................14

4.1. ASSESSMENT OF STATIC EFFECTS...............................................................................................................15 4.2. ASSESSMENT OF DYNAMIC EFFECTS.........................................................................................................165. POTENTIAL IMPACTS OF CAFTA FOR ORGANIC AGRICULTURE IN CENTRAL AMERICA:

THE CHALLENGE REMAINS THE SAME....................................................................................................................19 5.1. AGRICULTURE COMPETITIVENESS IN CENTRAL AMERICA: A LONG ROAD AHEAD...............................19 5.2. THE ORGANIC AGRICULTURAL SECTOR IN CENTRAL AMERICA ............................................................20 5.3. THE ORGANIC AGRICULTURE MARKET IN THE UNITED STATES.................................................................23 5.4. POSSIBLE IMPLICATIONS FOR ORGANIC AGRICULTURAL TRADE WITH THE UNITED STATES..................24 5.4.1. Growth Markets............................................................................................................................24 5.4.2. Standards and Technology.........................................................................................................24 5.4.3. Adjustments in the Sector to Meet Demand Trends.................................................................25 5.4.4. Processing and Value Added.....................................................................................................26 5.4.5. Environmental Rules in Conventional Markets..........................................................................27 5.4.6. Promising Products.......................................................................................................................28 5.5. LESSONS LEARNED FROM NAFTA..............................................................................................................296. CONCLUSIONS........................................................................................................................................................337. REFERENCES.............................................................................................................................................................358. ANNEX..................................................................................................................................................................... 37

ANNEX 1. MODEL ESTIMATION RESULTS................................................................................................................ 37ANNEX 2. EVOLUTION OF AGRICULTURAL EXPORTS FROM CENTRAL AMERICAN COUNTRIES TO THE US.......40

6 Enhancing Organic and Fair Trade !

�. INTRODUCTION

he United States and five Central American countries, El Salvador, Guatemala, Honduras, Nicaragua and Costa Rica, concluded negotiations on the US-Central American Free Trade Agreement (CAFTA) in January 2004.1 The agreement was signed on May 2004, and ratified by the US House of Representatives on July 27, 2005. The agreement has also been ratified by El Salvador, Dominican Republic, Guatemala, Honduras and Nicaragua. In Costa Rica the agreement is waiting for discussion in the Parliament.2

Under the US Caribbean Basin Trade Partnership Act (CBTPA),3 and the Generalized System of Preferences (GSP), many exports from Central America already enter the United States duty-free. CAFTA will consolidate these benefits and make them permanent. More than 80 percent of US tariff codes (consumer and industrial products) exported to Central America will be duty-free immediately upon ratification of the agreement, and 85 percent will be duty free within five years. All remaining tariffs will be eliminated within ten years. Close to 98 percent of all goods produced in Central America will enter the US market duty-free immediately. The Central American countries also accorded substantial market access across their entire services regime (i.e. banking, insurance, telecommunications), subject to very few exceptions.

Regarding agriculture, CAFTA opens the market widely, with the elimination of almost 100 percent of import tariffs. The only excluded products are sugar in the US, white corn in all Central American countries, potatoes and onions in Costa Rica. The sensitive agricultural products of Central America (rice, beans, poultry, beef and pork meat, dairy products) obtained protection with long tariff phase-out periods.

Agriculture has been a central issue for CAFTA, mainly because of the asymmetries between the US and Central America in terms of production, protection levels (both subsidies and import tariffs), productivity, degree of sector development and competitiveness. Currently, Central America is a net exporter of agricultural goods to the US. In recent years the agricultural supply has been diversified. Today, although coffee, bananas and sugar remain as leading export products, fruits, vegetables, meat and processed goods have gained market positioning in the US. In addition, the production and exports of organic agricultural goods to the US have increased significantly.

The markets for organic and Fair Trade agricultural products have grown in recent years, with North America, and particularly the US, as one of the leading markets. Sales volumes in the US achieved more than US$10 billion in year 2004.4 At the same time, the organic business in Central America has been developing, with thousands of small farmers transforming their traditional activities to certified organic farms.

Within this scenario, what could be expected from CAFTA for the organic agriculture of Central America? The answer is directly related to the possible implications of the agreement for the agricultural sector, the economy, and the future of agricultural competitiveness. It depends on the impact of CAFTA on poverty and development opportunities as well. Organic production is seen as a promising option for agricultural development in the region, with high expectations from its growth potential and possible impacts on sustainable rural development.

This document offers insights about the potential impacts of CAFTA for the organic agricultural business in Central America. First, it describes the evolution of agricultural trade between Central America and the US. Then, it makes a brief evaluation of agricultural competitiveness in the region. In a fourth section, a general equilibrium analysis is conducted to assess the economic implications of the agreement for the Central American region, with emphasis on agriculture. The fifth section discusses possible impacts and perspectives for the organic agricultural sector. The final section concludes.

1 The Dominican Republic was included into the Agreement on August 2004, named afterwards DR-CAFTA.2. CAFTA is expected to entry into force on January 1, 2006. However, there would be delays be-cause of lack of legal and regulatory framework harmonization between the US and the rest of DR-CAFTA countries. Partner countries must approve a DR-CAFTA implementation law, in order to “level the playing field for everyone.” The political discussion has been intense in all Central American countries with this and other regards. During the negotiation process, ratification pro-cess discussions, and future implementation strategy planning, DR-CAFTA has been and will be controversial. In general, those in favor of the agreement hope that the Agreement can be part of a policy foundation supportive of growing trade and investment, and long-term social, political, and economic development. On the other hand, there are strong concerns over the potential negative effects of DR-CAFTA on certain Central American productive sectors, workers, small farmers, and other groups. Most opposition to the DR-CAFTA before and after its ratification has emerged from well organized civil society groups (unions, agricultural organizations, environmental groups, aca-demic institutions, political parties, religious organizations, among others). At this point in Central America’s economic and political development, DR-CAFTA risks becoming a referendum on the entire trade integration and “globalization” goals pursued by the region in general. This means that much of the risk is political, relating to ideology and perceptions of who are the “winners” and the “losers.” See Condo, Colburn and Rivera (2005) for a broader analysis.3 Enacted in May 2000 as part of the Trade and Development Act. The CBTPA enhanced the 1984 Caribbean Basin Initiative (CBI) benefits.

T

4 CIMS (2005a).

7Enhancing Organic and Fair Trade !

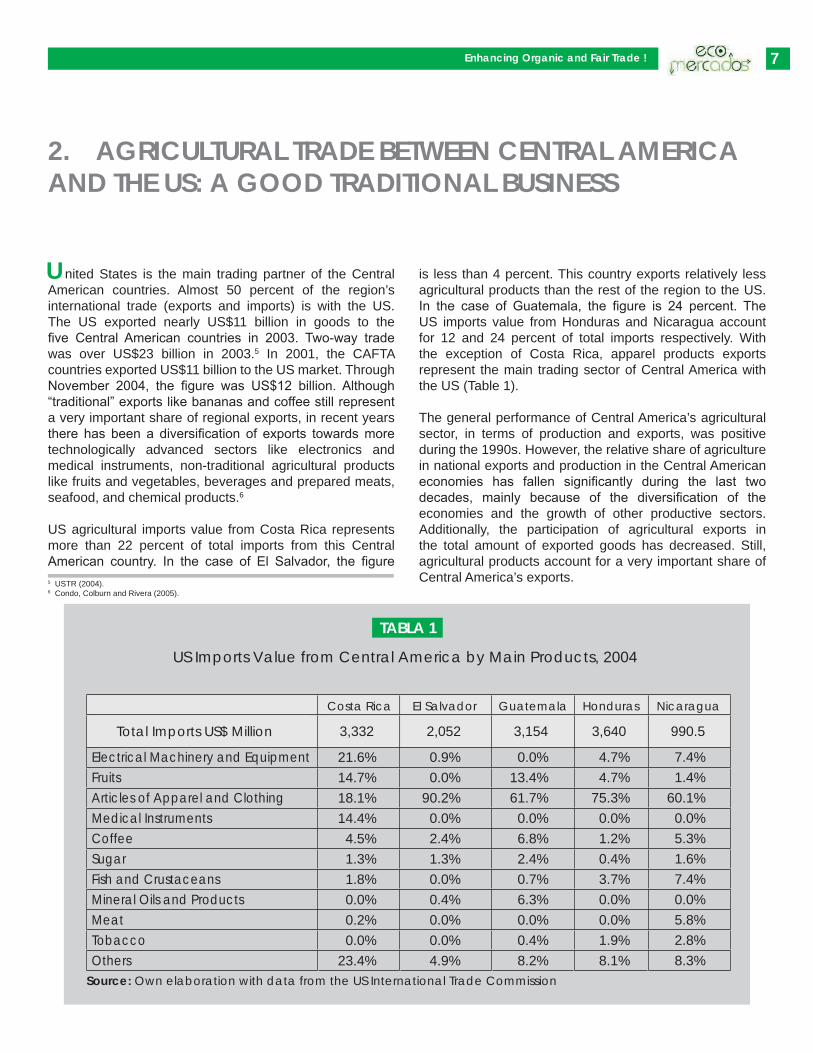

nited States is the main trading partner of the Central American countries. Almost 50 percent of the region’s international trade (exports and imports) is with the US. The US exported nearly US$11 billion in goods to the five Central American countries in 2003. Two-way trade was over US$23 billion in 2003.5 In 2001, the CAFTA countries exported US$11 billion to the US market. Through November 2004, the figure was US$12 billion. Although “traditional” exports like bananas and coffee still represent a very important share of regional exports, in recent years there has been a diversification of exports towards more technologically advanced sectors like electronics and medical instruments, non-traditional agricultural products like fruits and vegetables, beverages and prepared meats, seafood, and chemical products.6

US agricultural imports value from Costa Rica represents more than 22 percent of total imports from this Central American country. In the case of El Salvador, the figure

is less than 4 percent. This country exports relatively less agricultural products than the rest of the region to the US. In the case of Guatemala, the figure is 24 percent. The US imports value from Honduras and Nicaragua account for 12 and 24 percent of total imports respectively. With the exception of Costa Rica, apparel products exports represent the main trading sector of Central America with the US (Table 1).

The general performance of Central America’s agricultural sector, in terms of production and exports, was positive during the 1990s. However, the relative share of agriculture in national exports and production in the Central American economies has fallen significantly during the last two decades, mainly because of the diversification of the economies and the growth of other productive sectors. Additionally, the participation of agricultural exports in the total amount of exported goods has decreased. Still, agricultural products account for a very important share of Central America’s exports.

�. AGRICULTURAL TRADE BETWEEN CENTRAL AMERICA AND THE US: A GOOD TRADITIONAL BUSINESS

U

US Imports Value from Central America by Main Products, 2004

Costa Rica El Salvador Guatemala Honduras Nicaragua

3,332 2,052 3,154 3,640 990.5

Electrical Machinery and EquipmentFruitsArticles of Apparel and ClothingMedical InstrumentsCoffeeSugarFish and CrustaceansMineral Oils and ProductsMeatTobaccoOthers

Source: Own elaboration with data from the US International Trade Commission

TABLA �

7.4%1.4%

60.1%0.0%5.3%1.6%7.4%0.0%5.8%2.8%8.3%

4.7%4.7%

75.3%0.0%1.2%0.4%3.7%0.0%0.0%1.9%8.1%

0.0%13.4%61.7%0.0%6.8%2.4%0.7%6.3%0.0%0.4%8.2%

0.9%0.0%

90.2%0.0%2.4%1.3%0.0%0.4%0.0%0.0%4.9%

21.6%14.7%18.1%14.4%4.5%1.3%1.8%0.0%0.2%0.0%

23.4%

Total Imports US$ Million

5 USTR (2004).6 Condo, Colburn and Rivera (2005).

8 Enhancing Organic and Fair Trade !

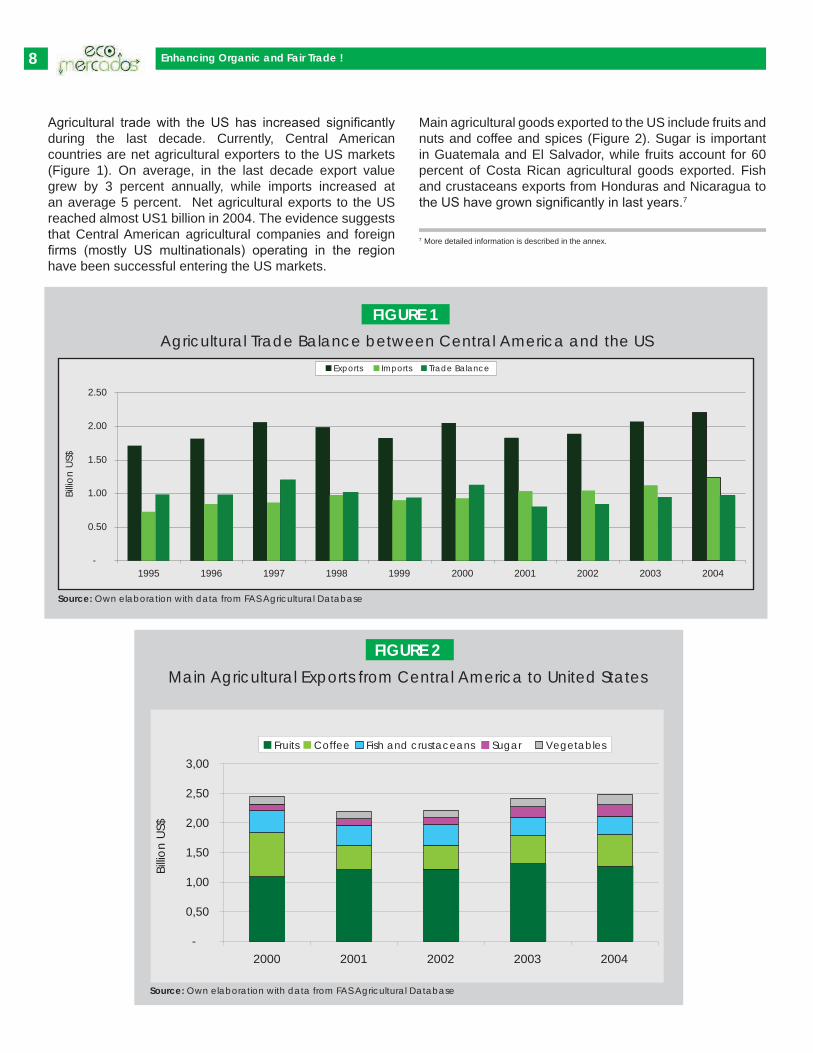

Agricultural trade with the US has increased significantly during the last decade. Currently, Central American countries are net agricultural exporters to the US markets (Figure 1). On average, in the last decade export value grew by 3 percent annually, while imports increased at an average 5 percent. Net agricultural exports to the US reached almost US1 billion in 2004. The evidence suggests that Central American agricultural companies and foreign firms (mostly US multinationals) operating in the region have been successful entering the US markets.

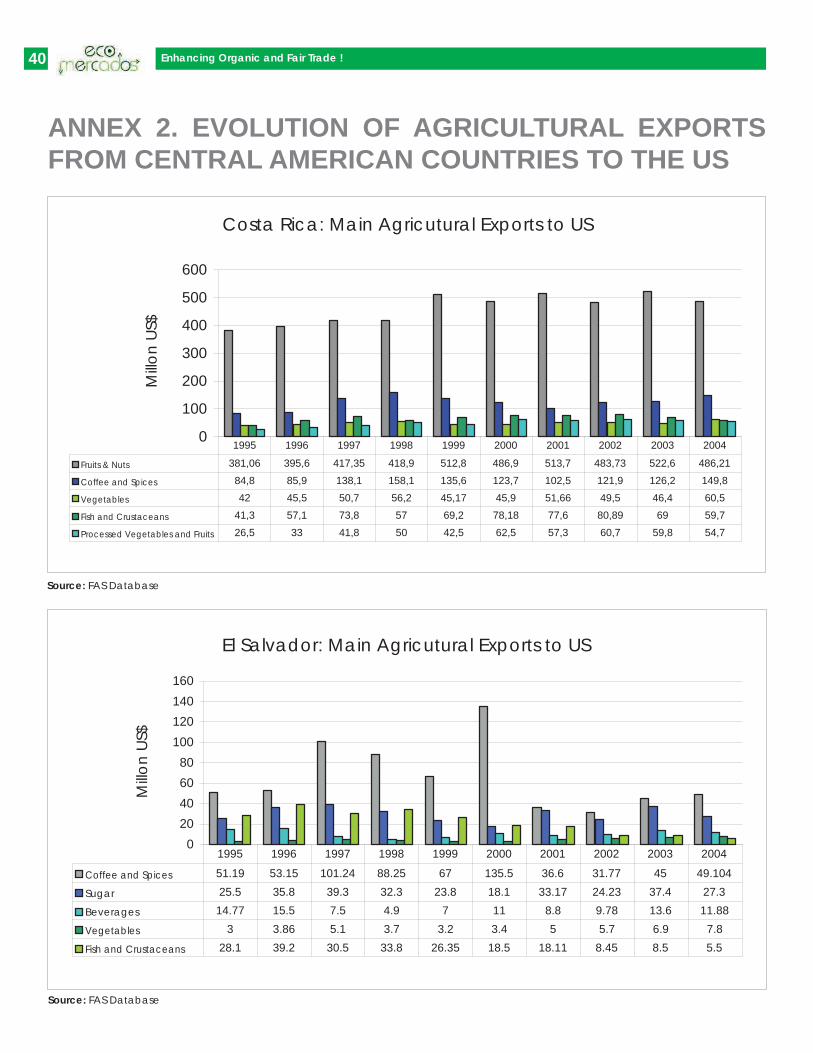

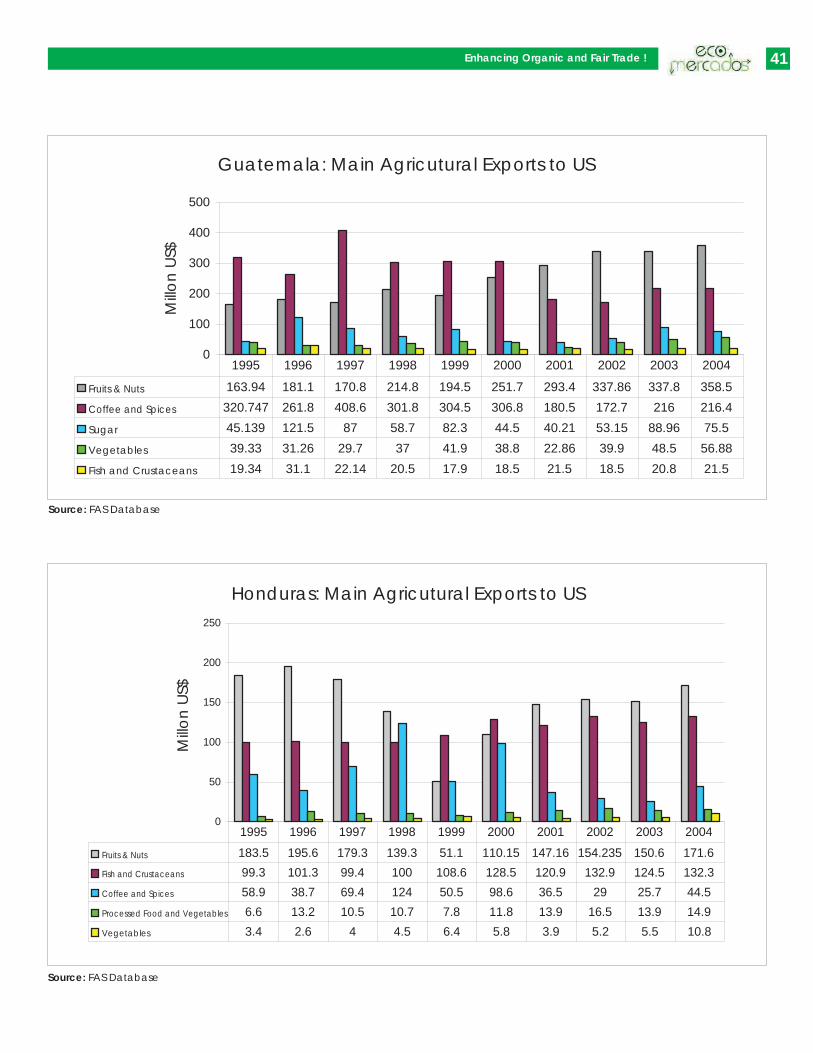

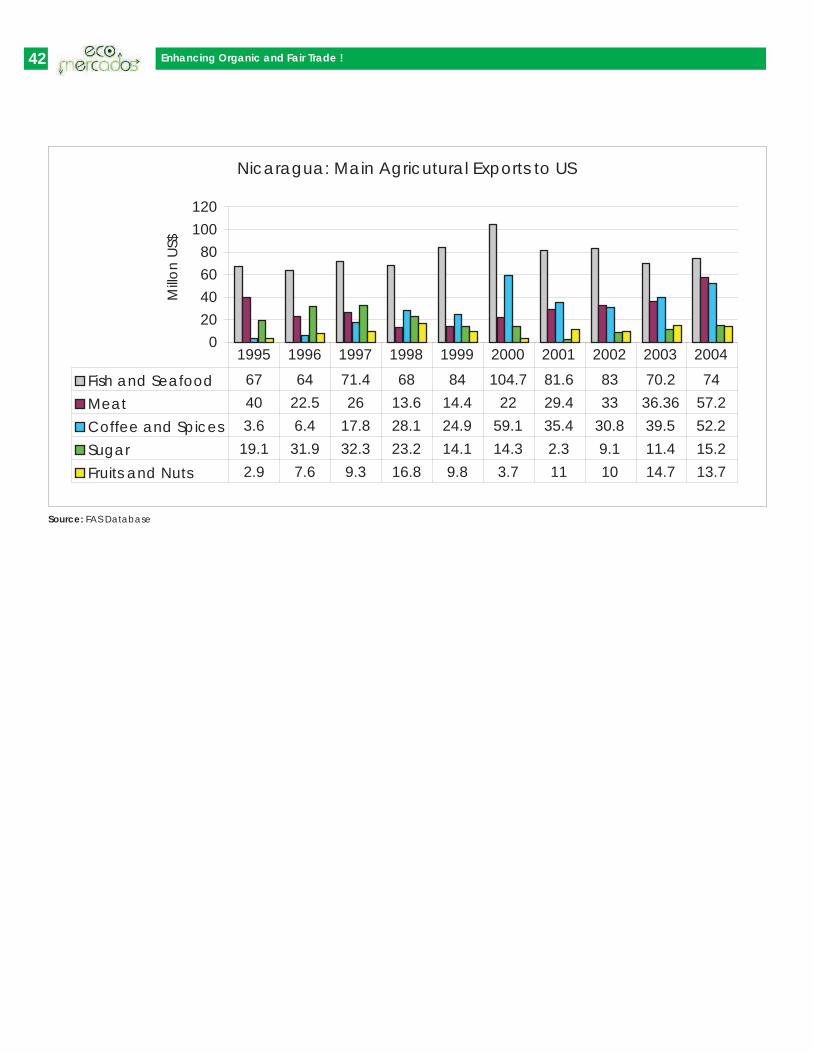

Main agricultural goods exported to the US include fruits and nuts and coffee and spices (Figure 2). Sugar is important in Guatemala and El Salvador, while fruits account for 60 percent of Costa Rican agricultural goods exported. Fish and crustaceans exports from Honduras and Nicaragua to the US have grown significantly in last years.7

-

0.50

1.00

1.50

2.00

2.50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Billio

n US

$

Exports Imports Trade Balance

Source: Own elaboration with data from FAS Agricultural Database

Agricultural Trade Balance between Central America and the US FIGURE �

7 More detailed information is described in the annex.

Main Agricultural Exports from Central America to United States FIGURE �

-

0,50

1,00

1,50

2,00

2,50

3,00

2000 2001 2002 2003 2004

Billio

n US

$

Fruits Coffee Fish and crustaceans Sugar Vegetables

Source: Own elaboration with data from FAS Agricultural Database

9Enhancing Organic and Fair Trade !

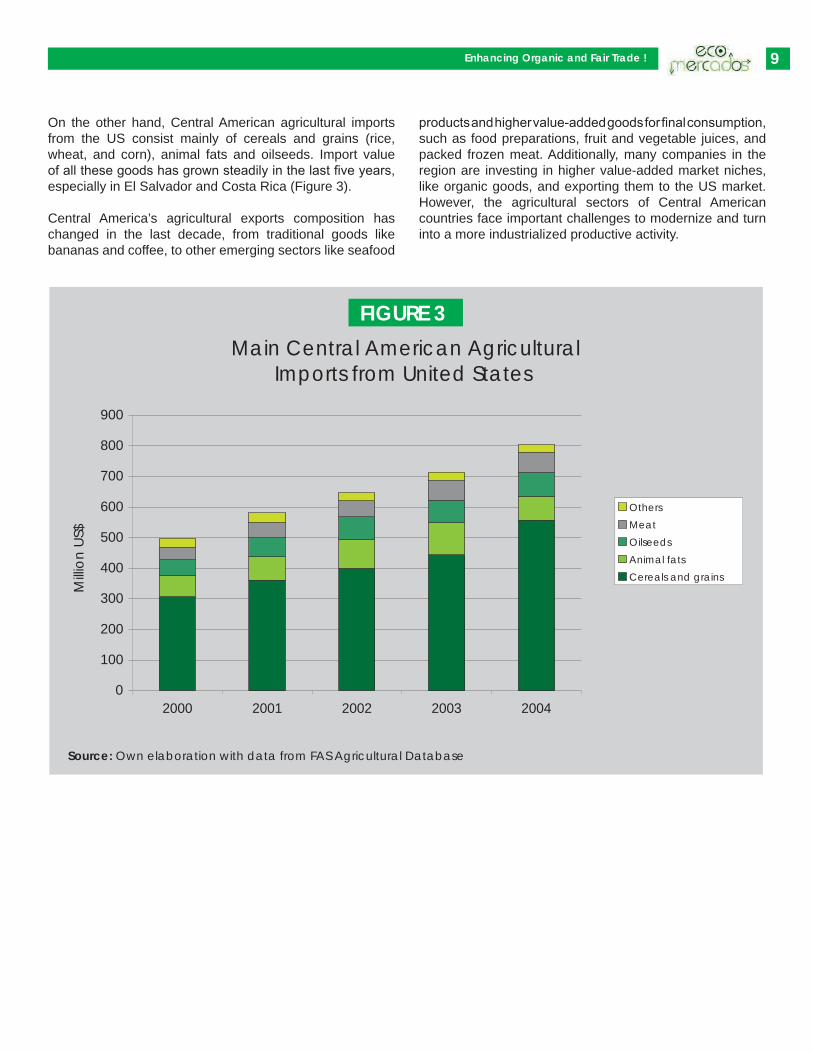

On the other hand, Central American agricultural imports from the US consist mainly of cereals and grains (rice, wheat, and corn), animal fats and oilseeds. Import value of all these goods has grown steadily in the last five years, especially in El Salvador and Costa Rica (Figure 3).

Central America’s agricultural exports composition has changed in the last decade, from traditional goods like bananas and coffee, to other emerging sectors like seafood

products and higher value-added goods for final consumption, such as food preparations, fruit and vegetable juices, and packed frozen meat. Additionally, many companies in the region are investing in higher value-added market niches, like organic goods, and exporting them to the US market. However, the agricultural sectors of Central American countries face important challenges to modernize and turn into a more industrialized productive activity.

Main Central American AgriculturalImports from United States

FIGURE �

Source: Own elaboration with data from FAS Agricultural Database

0

100

200

300

400

500

600

700

800

900

2000 2001 2002 2003 2004

Milli

on U

S$

OthersMeatOilseedsAnimal fatsCereals and grains

10 Enhancing Organic and Fair Trade !

fter nine rounds of negotiation, plus an additional round between Costa Rica and the US, CAFTA was signed. The long-term benefits of the agreement for Central America appear to outweigh the long-term costs.8 However, how much Central America benefits will depend on how effectively the countries can manage the process of transforming their agriculture productive capacity.

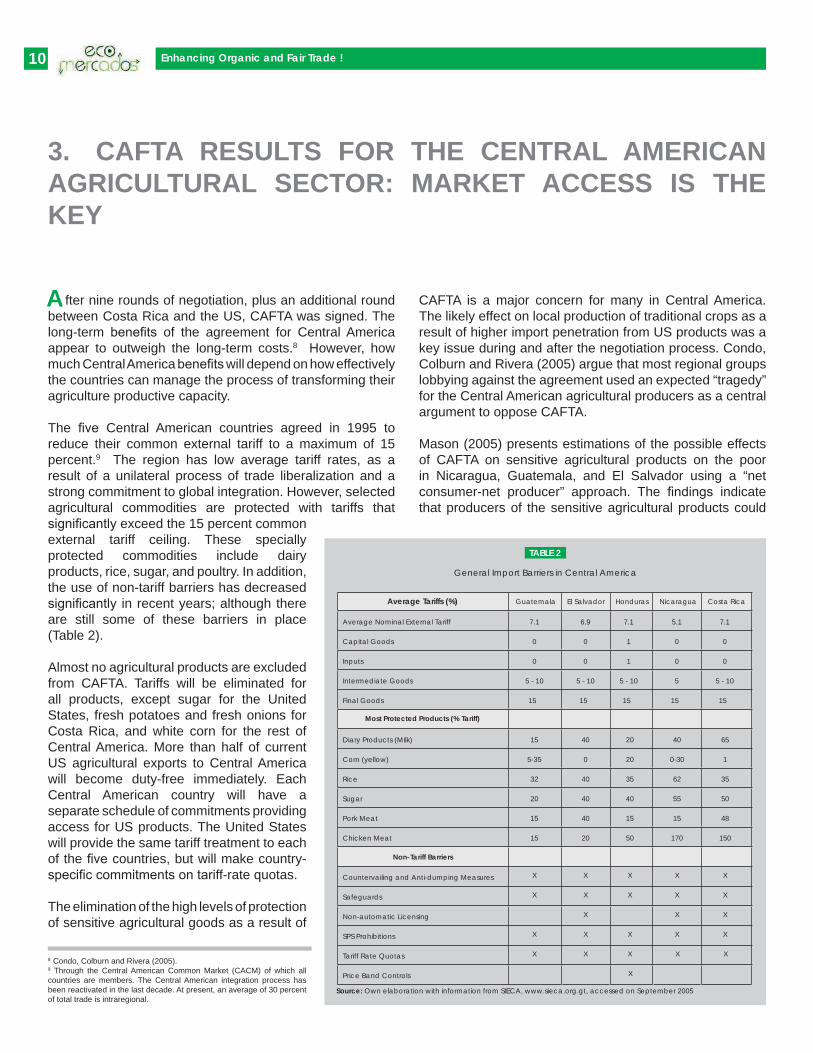

The five Central American countries agreed in 1995 to reduce their common external tariff to a maximum of 15 percent.9 The region has low average tariff rates, as a result of a unilateral process of trade liberalization and a strong commitment to global integration. However, selected agricultural commodities are protected with tariffs that significantly exceed the 15 percent common external tariff ceiling. These specially protected commodities include dairy products, rice, sugar, and poultry. In addition, the use of non-tariff barriers has decreased significantly in recent years; although there are still some of these barriers in place (Table 2).

Almost no agricultural products are excluded from CAFTA. Tariffs will be eliminated for all products, except sugar for the United States, fresh potatoes and fresh onions for Costa Rica, and white corn for the rest of Central America. More than half of current US agricultural exports to Central America will become duty-free immediately. Each Central American country will have a separate schedule of commitments providing access for US products. The United States will provide the same tariff treatment to each of the five countries, but will make country-specific commitments on tariff-rate quotas.

The elimination of the high levels of protection of sensitive agricultural goods as a result of

CAFTA is a major concern for many in Central America. The likely effect on local production of traditional crops as a result of higher import penetration from US products was a key issue during and after the negotiation process. Condo, Colburn and Rivera (2005) argue that most regional groups lobbying against the agreement used an expected “tragedy” for the Central American agricultural producers as a central argument to oppose CAFTA.

Mason (2005) presents estimations of the possible effects of CAFTA on sensitive agricultural products on the poor in Nicaragua, Guatemala, and El Salvador using a “net consumer-net producer” approach. The findings indicate that producers of the sensitive agricultural products could

3. CAFTA RESULTS FOR THE CENTRAL AMERICAN AGRICULTURAL SECTOR: MARKET ACCESS IS THE KEY

A

8 Condo, Colburn and Rivera (2005).9 Through the Central American Common Market (CACM) of which all countries are members. The Central American integration process has been reactivated in the last decade. At present, an average of 30 percent of total trade is intraregional.

General Import Barriers in Central America

Source: Own elaboration with information from SIECA, www.sieca.org.gt, accessed on September 2005

TABLE 2

Average Tariffs (%) Guatemala El Salvador Honduras Nicaragua Costa Rica

7.1

0

0

5 - 10

15

15

5-35

32

20

15

15

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

40

0

40

40

40

20

20

20

35

40

15

50

40

0-30

62

55

15

170

65

1

35

50

48

150

7.1

0

0

5 - 10

15

6.9

0

0

5 - 10

15

7.1

1

1

5 - 10

15

5.1

0

0

5

15

Average Nominal External Tariff

Capital Goods

Inputs

Intermediate Goods

Final Goods

Diary Products (Milk)

Corn (yellow)

Rice

Sugar

Pork Meat

Chicken Meat

Countervailing and Anti-dumping Measures

Safeguards

Non-automatic Licensing

SPS Prohibitions

Tariff Rate Quotas

Price Band Controls

Most Protected Products (% Tariff)

Non-Tariff Barriers

��Enhancing Organic and Fair Trade !

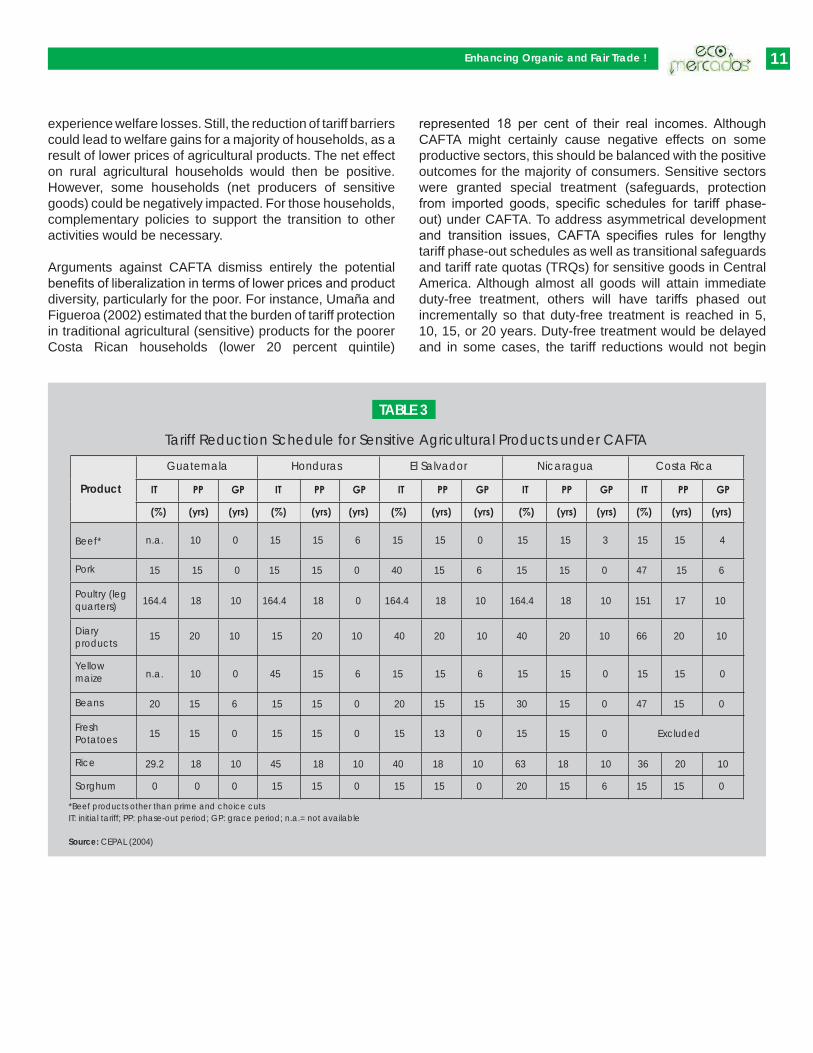

experience welfare losses. Still, the reduction of tariff barriers could lead to welfare gains for a majority of households, as a result of lower prices of agricultural products. The net effect on rural agricultural households would then be positive. However, some households (net producers of sensitive goods) could be negatively impacted. For those households, complementary policies to support the transition to other activities would be necessary.

Arguments against CAFTA dismiss entirely the potential benefits of liberalization in terms of lower prices and product diversity, particularly for the poor. For instance, Umaña and Figueroa (2002) estimated that the burden of tariff protection in traditional agricultural (sensitive) products for the poorer Costa Rican households (lower 20 percent quintile)

represented 18 per cent of their real incomes. Although CAFTA might certainly cause negative effects on some productive sectors, this should be balanced with the positive outcomes for the majority of consumers. Sensitive sectors were granted special treatment (safeguards, protection from imported goods, specific schedules for tariff phase-out) under CAFTA. To address asymmetrical development and transition issues, CAFTA specifies rules for lengthy tariff phase-out schedules as well as transitional safeguards and tariff rate quotas (TRQs) for sensitive goods in Central America. Although almost all goods will attain immediate duty-free treatment, others will have tariffs phased out incrementally so that duty-free treatment is reached in 5, 10, 15, or 20 years. Duty-free treatment would be delayed and in some cases, the tariff reductions would not begin

Tariff Reduction Schedule for Sensitive Agricultural Products under CAFTA

Guatemala Honduras El Salvador Nicaragua Costa Rica

Product

Beef* n.a. 10 0 15 15 6 15 15 0 15 15 3 15 15 4

Pork

Poultry (leg quarters)

Diary products

Yellow maize

Beans

Fresh Potatoes

Rice

Sorghum

15 15 0 15 15 0 40 15 6 15 15 0 47 15 6

164.4 18 10 164.4 18 0 164.4 18 10 164.4 18 10 151 17 10

15 20 10 15 20 10 40 20 10 40 20 10 66 20 10

n.a. 10 0 45 15 6 15 15 6 15 15 0 15 15 0

20 15 6 15 15 0 20 15 15 30 15 0 47 15 0

15 15 0 15 15 0 15 13 0 15 15 0 Excluded

29.2 18 10 45 18 10 40 18 10 63 18 10 36 20 10

0 0 0 15 15 0 15 15 0 20 15 6 15 15 0

*Beef products other than prime and choice cutsIT: initial tariff; PP: phase-out period; GP: grace period; n.a.= not available

Source: CEPAL (2004)

TABLE �

�� Enhancing Organic and Fair Trade !

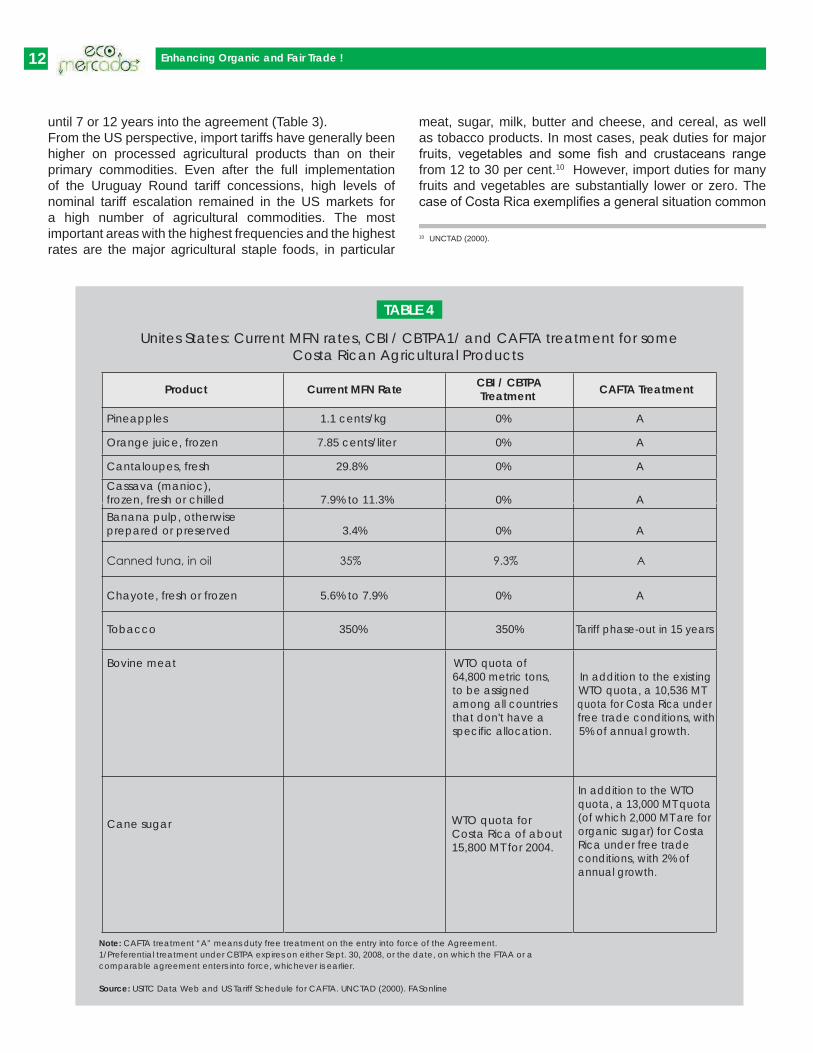

until 7 or 12 years into the agreement (Table 3).From the US perspective, import tariffs have generally been higher on processed agricultural products than on their primary commodities. Even after the full implementation of the Uruguay Round tariff concessions, high levels of nominal tariff escalation remained in the US markets for a high number of agricultural commodities. The most important areas with the highest frequencies and the highest rates are the major agricultural staple foods, in particular

meat, sugar, milk, butter and cheese, and cereal, as well as tobacco products. In most cases, peak duties for major fruits, vegetables and some fish and crustaceans range from 12 to 30 per cent.10 However, import duties for many fruits and vegetables are substantially lower or zero. The case of Costa Rica exemplifies a general situation common

10 UNCTAD (2000).

Unites States: Current MFN rates, CBI / CBTPA1/ and CAFTA treatment for someCosta Rican Agricultural Products

Note: CAFTA treatment “A” means duty free treatment on the entry into force of the Agreement. 1/Preferential treatment under CBTPA expires on either Sept. 30, 2008, or the date, on which the FTAA or acomparable agreement enters into force, whichever is earlier.

Source: USITC Data Web and US Tariff Schedule for CAFTA. UNCTAD (2000). FASonline

TABLE �

Pineapples 1.1 cents/kg 0% A

Orange juice, frozen 7.85 cents/liter 0% A

Cantaloupes, fresh 29.8% 0% A

Cassava (manioc),frozen, fresh or chilled 7.9% to 11.3% 0% ABanana pulp, otherwiseprepared or preserved 3.4% 0% A

Chayote, fresh or frozen 5.6% to 7.9% 0% A

Tobacco 350% 350% Tariff phase-out in 15 years

Bovine meat WTO quota of 64,800 metric tons, In addition to the existing to be assigned WTO quota, a 10,536 MT among all countries quota for Costa Rica under that don't have a free trade conditions, with specific allocation. 5% of annual growth.

Cane sugar WTO quota forCosta Rica of about15,800 MT for 2004.

In addition to the WTOquota, a 13,000 MT quota(of which 2,000 MT are fororganic sugar) for CostaRica under free tradeconditions, with 2% ofannual growth.

Product CAFTA Treatment CBI / CBTPATreatmentCurrent MFN Rate

��Enhancing Organic and Fair Trade !

to all Central American agricultural exporters (Table 4).Under the US Caribbean Basin Trade Partnership Act (CBTPA) and the Generalized System of Preferences (GSP), many agricultural exports from Central America already enter the United States duty-free. However, Monge et al (2003) document that hundreds of Central American agricultural goods with significant revealed comparative advantages have been excluded from US preferential access schemes. Despite CBI preferences, a long list of Central American agricultural products (over one-half of goods exported to the world but not the US) face important barriers in the US market. In addition, tariff escalation could have blocked the exports of many processed higher added-value agricultural goods.

One of the advantages of CAFTA is that almost 100 per cent of all agricultural goods produced in Central America will enter the US market duty-free. CAFTA will make unilateral CBI preferences permanent. As a result, many agricultural goods from the region would have the opportunity to compete in the US market. Goods like fruits and vegetables, forestry products, and processed food have growth potential, particularly if higher value is added with further processing, product differentiation, and quality improvements.

On the other hand, after CAFTA, the relevance of non-tariff barriers for agricultural trade with the US will increase. Incidence of non-tariff barriers has historically been significant, and will gain more importance parallel to agricultural tariffs elimination. As an example, avocado exports from Central American countries to the US are currently prohibited as a result of the outbreak of Mediterranean fly disease. Other agricultural products have faced difficulties entering US markets because of lack of information, weak health and safety standards, technical limitations, packaging restrictions and certification capacities. This is a key competitiveness issue that must be addressed as a high priority.

Central American organic (and conventional) agricultural producers must understand and apply necessary measures to comply with market entry regulations, particularly those related to Sanitary and Phytosanitary (SPS) standards. In addition to the proper organic certifications, compliance

with Hazard Analysis and Critical Control Point (HACCP) regulations, Animal and Plant Health Inspection Service (APHIS) standards, and bioterrorism related laws, are a must. The agricultural business in Central America has bifurcated in two: those sectors that comply with SPS standards and those that do not. The former group will not enter the market.

One implication of CAFTA is the strengthening of SPS regulations.11 At the same time, more transparency and cooperation opportunities emerge from the agreement. For instance, Jaramillo and Lederman (2005) indicate that the US committed to resolve delays in food inspection procedures for meat and poultry products from Central America. Honduras obtained a schedule for the resolution of sanitary issues that affect export of poultry, dairy products, tomatoes and peppers, as well as technical assistance to strengthen institutions in the sanitary and phytosanitary area. Nicaragua is receiving help in solving SPS problems for exports of cheese, papaya, pitahaya, peppers and tomatoes. Costa Rica obtained guaranteed access of ornamental plants over eighteen inches in height, more flexible sanitary treatment for some of its flower exports, and advanced in the recognition of its poultry inspection system.12

CAFTA makes SPS regulations stricter, but at the same time offers new opportunities for Central American countries to catch up with agricultural market requirements. The final outcome will depend on national and regional efforts, on coordinated actions between companies and public organizations, to invest more on technical capacities, laboratories, certification infrastructure, and create an incentives scheme to promote the required adjustments and restructuring of companies. Technical cooperation and technology transfer from the US is an option to take

11 With CAFTA the parties agreed to apply the science-based disciplines of the WTO Agreement on Sanitary and Phytosanitary (SPS) Measures. An SPS working group was established to expedite resolution of technical issues and to contribute to the dissemination of the regulations and procedures applied in the US for key products of interest.12 These changes are expected to have significant impacts, e.g. in the case of Costa Rica’s ornamental plants, producers have estimated that this may increase their export earnings by 50 percent just by exporting taller rather than shorter plants (Jaramillo, 2005).

�� Enhancing Organic and Fair Trade !

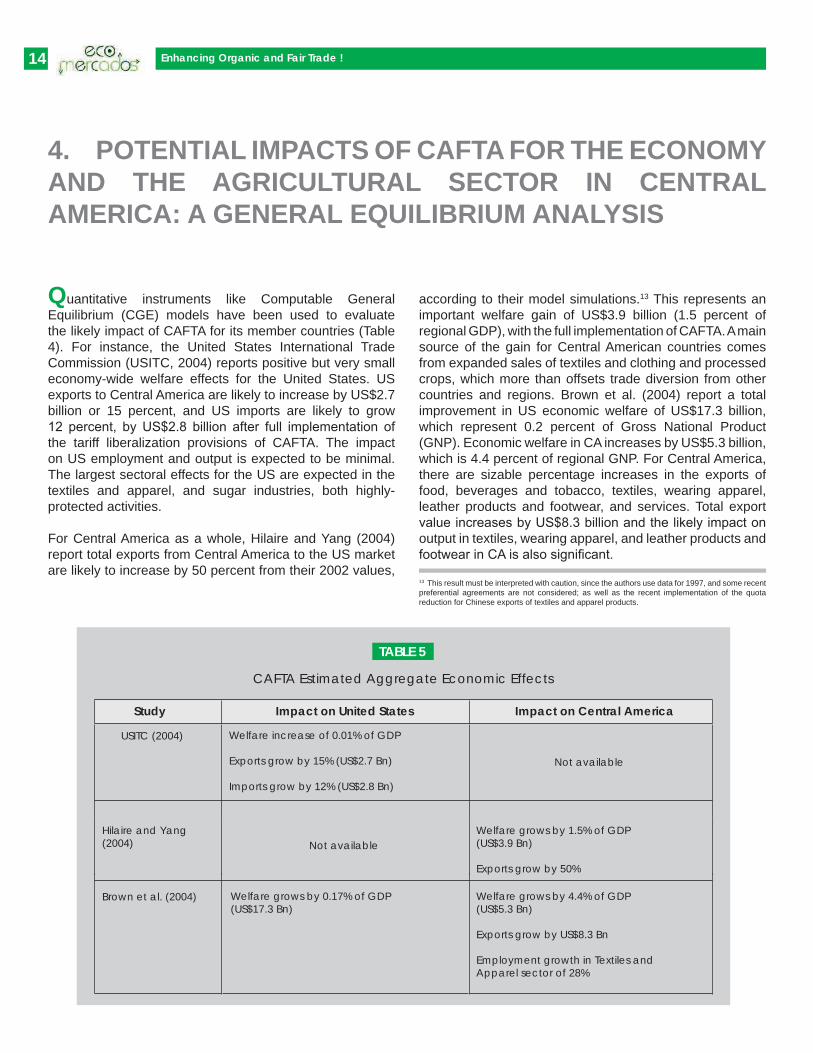

uantitative instruments like Computable General Equilibrium (CGE) models have been used to evaluate the likely impact of CAFTA for its member countries (Table 4). For instance, the United States International Trade Commission (USITC, 2004) reports positive but very small economy-wide welfare effects for the United States. US exports to Central America are likely to increase by US$2.7 billion or 15 percent, and US imports are likely to grow 12 percent, by US$2.8 billion after full implementation of the tariff liberalization provisions of CAFTA. The impact on US employment and output is expected to be minimal. The largest sectoral effects for the US are expected in the textiles and apparel, and sugar industries, both highly-protected activities. For Central America as a whole, Hilaire and Yang (2004) report total exports from Central America to the US market are likely to increase by 50 percent from their 2002 values,

4. POTENTIAL IMPACTS OF CAFTA FOR THE ECONOMY AND THE AGRICULTURAL SECTOR IN CENTRAL AMERICA: A GENERAL EQUILIBRIUM ANALYSIS

Q according to their model simulations.13 This represents an important welfare gain of US$3.9 billion (1.5 percent of regional GDP), with the full implementation of CAFTA. A main source of the gain for Central American countries comes from expanded sales of textiles and clothing and processed crops, which more than offsets trade diversion from other countries and regions. Brown et al. (2004) report a total improvement in US economic welfare of US$17.3 billion, which represent 0.2 percent of Gross National Product (GNP). Economic welfare in CA increases by US$5.3 billion, which is 4.4 percent of regional GNP. For Central America, there are sizable percentage increases in the exports of food, beverages and tobacco, textiles, wearing apparel, leather products and footwear, and services. Total export value increases by US$8.3 billion and the likely impact on output in textiles, wearing apparel, and leather products and footwear in CA is also significant.

13 This result must be interpreted with caution, since the authors use data for 1997, and some recent preferential agreements are not considered; as well as the recent implementation of the quota reduction for Chinese exports of textiles and apparel products.

CAFTA Estimated Aggregate Economic Effects

TABLE �

USITC (2004)

Not available

Hilaire and Yang(2004) Not available

Welfare grows by 1.5% of GDP(US$3.9 Bn)

Exports grow by 50%

Brown et al. (2004) Welfare grows by 4.4% of GDP(US$5.3 Bn)

Exports grow by US$8.3 Bn

Employment growth in Textiles andApparel sector of 28%

Welfare increase of 0.01% of GDP

Exports grow by 15% (US$2.7 Bn)

Imports grow by 12% (US$2.8 Bn)

Welfare grows by 0.17% of GDP(US$17.3 Bn)

Study Impact on United States Impact on Central America

��Enhancing Organic and Fair Trade !

For this paper, the GTAP database and Computable General Equilibrium (CGE) model14 were used to analyze the potential economic implications of CAFTA for Central America, with emphasis on the agricultural sector.15 The GTAP database 6.0 pre-release 3.10 version uses 2001 as its baseline and provides one of the best available bases to analyze current trade policy (USITC, 2004).16

The data was aggregated in 19 sectors and 3 regions: USA, Central America, and the Rest of the World (ROW). The sector aggregation was done considering 17 agricultural sub-sectors plus manufacturing and services.17

First, a standard GTAP static model with different shocks was used to evaluate alternative scenarios under CAFTA.18 Then, some potential dynamic effects were assessed, taking into consideration possible increases in US foreign direct investment flows to Central America and capital accumulation in response to the incentives provided by the bilateral liberalization, the potential impact of trade facilitation strategies, and the reduction of unemployment by labor market adjustments. It is important to stress that the simulation results include the full adjustment of the Central America economy and the agricultural sector to the policy shock and thus, can represent, ceteris paribus, the long-run effect of CAFTA. Therefore, the short-run adjustment and preliminary implications of the trade agreement are not analyzed here.

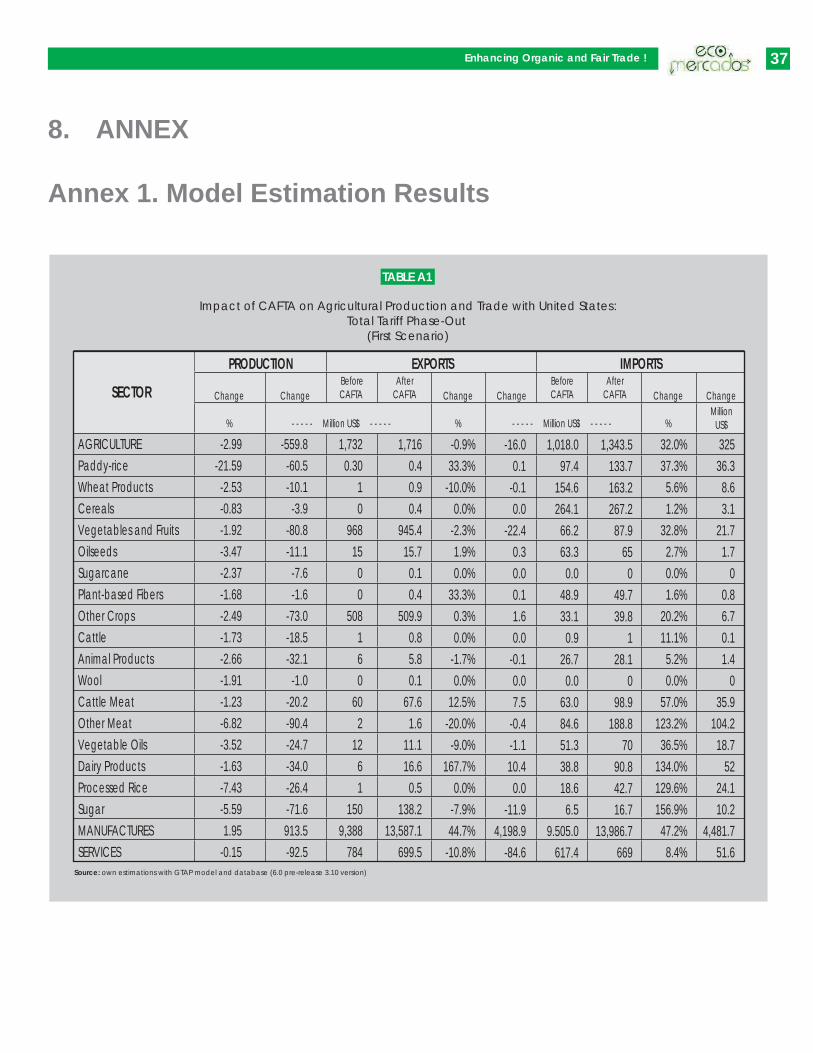

�.�. ASSESSMENT OF STATIC EFFECTS19

In the first scenario, a full liberalization of trade between US and Central America is assumed. Thus, all tariffs between both regions and among Central American countries are reduced to zero, keeping the original tariffs with the ROW. However, tariffs for sugar in the US and for corn in CA are not removed, in accordance to the agricultural exclusions made in the agreement.20 In addition, some minor quotas across both regions and countries were also eliminated (Table 6).

The results for this scenario show that welfare gains are likely to be positive for CA. It increases US$993 million or 1.4 percent of previous GDP, which in turn has a 0.22 percent growth rate. Household incomes rise 4 percent, driven by a significant increase in wages and capital returns. Moreover, CA has positive terms-of-trade effects that also contribute to these welfare gains.21 As expected, the equivalent values for the US are close to zero.22

Manufacturing production in CA increases by 2 percent, drawing a higher specialization into this sector, at the expense of all the rest of the economy, and particularly the agricultural sector production, which falls by 3 percent. Agricultural production in all sectors falls, with rice being the most affected sector. This situation is also reflected in the export performance, were manufacturing exports to US grows 45 percent, while agricultural exports are almost unaltered (-1 percent). In terms of imports change, the simulation results are the expected ones. Import penetration from the US is significant, due to tariff asymmetries between both regions that are eliminated with the agreement. The phase out of sensitive agricultural goods tariff barriers strengthens the imports effect. The imports of rice, meat, dairy products and sugar grow enormously. Vegetables and fruits imports increase significantly as well. Central America’s comparative advantage in these sectors appears to be relatively eroded under a free-trade environment with the US.23

When analyzing factor prices, CA experiences significant increases in wages for unskilled and skilled labor, as well as capital returns. This would contribute to welfare and income increases mentioned before and moreover, promises some relief to poor unskilled workers. In addition, consumer prices

Global Effects of CAFTA for Central America:Total Tariff Phase-Out (First Scenario)

TABLE 6

GDPEconomy WelfareHousehold IncomeFactors of Production PriceLandUnskilled LaborSkilled LaborCapitalNatural Resources

0.22%1.42%

4.0%

-8.18%5.37%5.74%5.97%7.59%

Source: own estimations with GTAP model and database (6.0 pre-release 3.10 version)

14 For a detailed description of the GTAP model theoretical setting see Hertel and Tsigas (1997).15 The Global Trade Analysis Project (GTAP) is an international network of institutions and researchers that facilitates and fosters trade analysis. The main aim of the project is to provide updated datasets of bilateral trade, transport, and import protection data in conjunction with individual-country input-output databases. Moreover, it also provides a modelling framework to conduct CGE static analysis of multi-region and economy-wide scenarios. In particular it can simulate the effects of trade policy and resource-related shocks on the medium-term patterns of global production and trade.16 For this specific application, there are two main limitations. First, the regional aggregation available in the database groups the five Central American participants (Costa Rica, El Salvador, Guatemala, Honduras and Nicaragua) together with Belize and Panama, which are not part of CAFTA (currently, Panama is negotiating an agreement with the US). Secondly, the baseline year is four years apart from the implementation date of the agreement. This implies that the economic environment and data changes that have taken place between 2001 and 2005 are not included in these estimations. Still, the analysis is relevant for regional impact estimations. Further research is necessary to assess the impacts by each country.17 The GTAP database allows for other possible combinations of sectors and regions. 18 In particular, the RunGTAP software version 5 is used.19 Tables A1 and A2 in the annex include the disaggregated results.20 Because of limitations with the aggregation of sectors provided by the GTAP database, the exclusion of white corn is proxied by leaving the tariff of “Cereals” unaltered, even when other products are being included there. For similar reasons, onion and potato tariffs in Costa Rica were not considered, since they were excluded from the negotiated tariff reductions.

21 These positive terms-of-trade effects are present throughout the rest of scenarios, with an average percentage increase between 2 percent and 3 percent.22 US impacts are available by request.23 Manufacturing imports´ growth from the US is also significant, notwithstanding the relatively low import tariffs of this sector.

�6 Enhancing Organic and Fair Trade !

increase less than income. The overall situation of poverty in each country is likely to improve under these conditions. However, land returns are negatively affected because of the negative impact of CAFTA on the agricultural sector. This implies a redistribution of income from rural land-owners to (rural) workers.

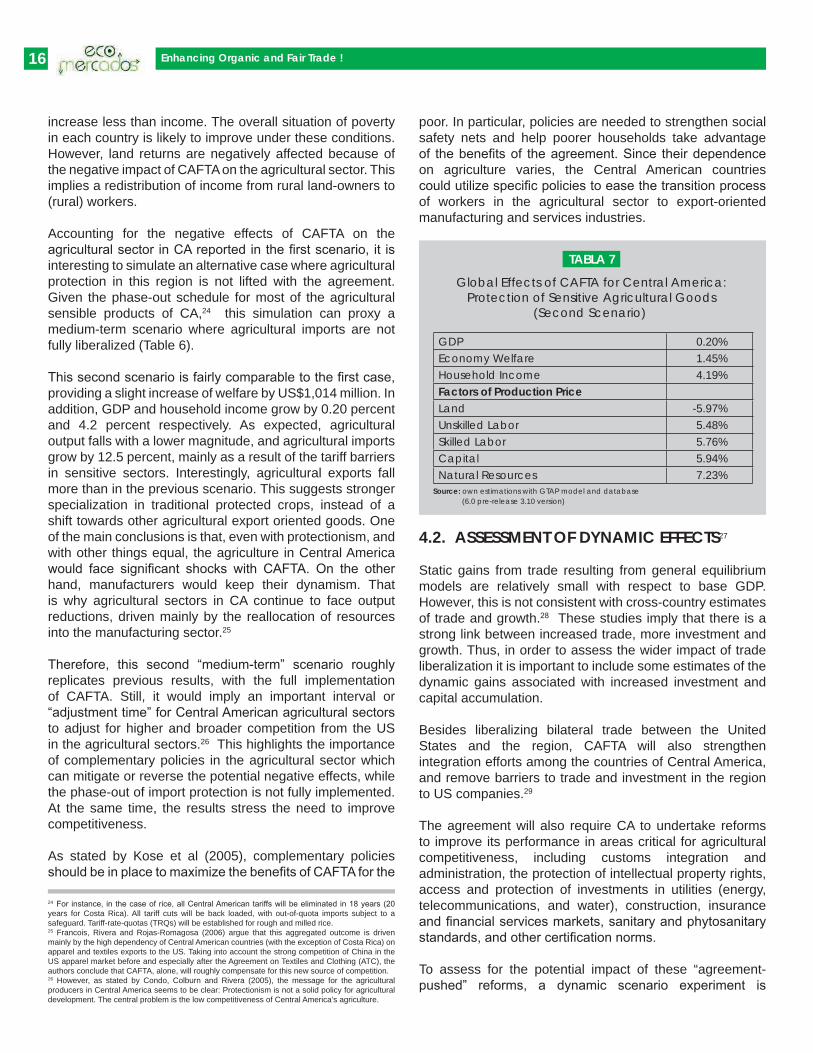

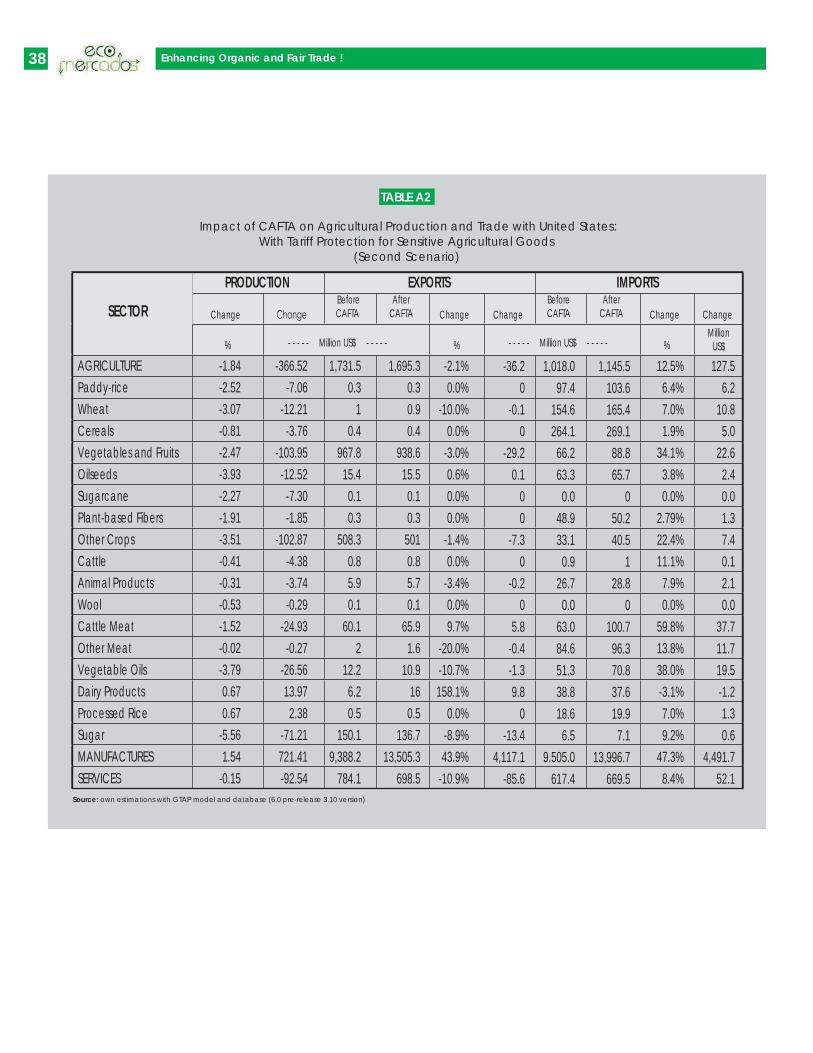

Accounting for the negative effects of CAFTA on the agricultural sector in CA reported in the first scenario, it is interesting to simulate an alternative case where agricultural protection in this region is not lifted with the agreement. Given the phase-out schedule for most of the agricultural sensible products of CA,24 this simulation can proxy a medium-term scenario where agricultural imports are not fully liberalized (Table 6).

This second scenario is fairly comparable to the first case, providing a slight increase of welfare by US$1,014 million. In addition, GDP and household income grow by 0.20 percent and 4.2 percent respectively. As expected, agricultural output falls with a lower magnitude, and agricultural imports grow by 12.5 percent, mainly as a result of the tariff barriers in sensitive sectors. Interestingly, agricultural exports fall more than in the previous scenario. This suggests stronger specialization in traditional protected crops, instead of a shift towards other agricultural export oriented goods. One of the main conclusions is that, even with protectionism, and with other things equal, the agriculture in Central America would face significant shocks with CAFTA. On the other hand, manufacturers would keep their dynamism. That is why agricultural sectors in CA continue to face output reductions, driven mainly by the reallocation of resources into the manufacturing sector.25

Therefore, this second “medium-term” scenario roughly replicates previous results, with the full implementation of CAFTA. Still, it would imply an important interval or “adjustment time” for Central American agricultural sectors to adjust for higher and broader competition from the US in the agricultural sectors.26 This highlights the importance of complementary policies in the agricultural sector which can mitigate or reverse the potential negative effects, while the phase-out of import protection is not fully implemented. At the same time, the results stress the need to improve competitiveness.

As stated by Kose et al (2005), complementary policies should be in place to maximize the benefits of CAFTA for the

Global Effects of CAFTA for Central America:Protection of Sensitive Agricultural Goods

(Second Scenario)

TABLA 7

GDPEconomy WelfareHousehold IncomeFactors of Production PriceLandUnskilled LaborSkilled LaborCapitalNatural Resources

0.20%1.45%4.19%

-5.97%5.48%5.76%5.94%7.23%

Source: own estimations with GTAP model and database (6.0 pre-release 3.10 version)

24 For instance, in the case of rice, all Central American tariffs will be eliminated in 18 years (20 years for Costa Rica). All tariff cuts will be back loaded, with out-of-quota imports subject to a safeguard. Tariff-rate-quotas (TRQs) will be established for rough and milled rice.25 Francois, Rivera and Rojas-Romagosa (2006) argue that this aggregated outcome is driven mainly by the high dependency of Central American countries (with the exception of Costa Rica) on apparel and textiles exports to the US. Taking into account the strong competition of China in the US apparel market before and especially after the Agreement on Textiles and Clothing (ATC), the authors conclude that CAFTA, alone, will roughly compensate for this new source of competition.26 However, as stated by Condo, Colburn and Rivera (2005), the message for the agricultural producers in Central America seems to be clear: Protectionism is not a solid policy for agricultural development. The central problem is the low competitiveness of Central America’s agriculture.

poor. In particular, policies are needed to strengthen social safety nets and help poorer households take advantage of the benefits of the agreement. Since their dependence on agriculture varies, the Central American countries could utilize specific policies to ease the transition process of workers in the agricultural sector to export-oriented manufacturing and services industries.

�.�. ASSESSMENT OF DYNAMIC EFFECTS27

Static gains from trade resulting from general equilibrium models are relatively small with respect to base GDP. However, this is not consistent with cross-country estimates of trade and growth.28 These studies imply that there is a strong link between increased trade, more investment and growth. Thus, in order to assess the wider impact of trade liberalization it is important to include some estimates of the dynamic gains associated with increased investment and capital accumulation.

Besides liberalizing bilateral trade between the United States and the region, CAFTA will also strengthen integration efforts among the countries of Central America, and remove barriers to trade and investment in the region to US companies.29

The agreement will also require CA to undertake reforms to improve its performance in areas critical for agricultural competitiveness, including customs integration and administration, the protection of intellectual property rights, access and protection of investments in utilities (energy, telecommunications, and water), construction, insurance and financial services markets, sanitary and phytosanitary standards, and other certification norms.

To assess for the potential impact of these “agreement-pushed” reforms, a dynamic scenario experiment is

�7Enhancing Organic and Fair Trade !

conducted. In this scenario the effects of Foreign Direct Investment (FDI) and capital accumulation, trade facilitation and the reduction of unskilled labor unemployment are combined. The joint impact of these expected positive outcomes provides an upper-bound or “optimistic scenario” concerning CAFTA.

Foreign direct investment (FDI) inflows to CA have increased significantly in the 1990s. This phenomenon has contributed in a decisive manner to increase export diversity in the region. Moreover, FDI inflows help finance the persistent current account deficits, especially in Costa Rica.30 One of the main issues negotiated in CAFTA was the inclusion of legal and administrative provisions to ease the flow of FDI into the region. Moreover, given that the Caribbean Basin Trade Partnership Act (CBTPA) already grants market access to the US for many Central American products, it is expected that investment will provide the biggest economic impact of the agreement for the region.31

Assuming that CAFTA increases the flow of FDI into the region, the dynamic effects can be estimated by allowing capital to change endogenously.32 The results show an increase in capital stock of 10.4 percent associated with CAFTA. The raise in the capital stock is directly associated with a GDP increase of 4.8 percent. Since terms-of-trade are also improving, then social welfare is further increased by US$ 2,300 million (or 4.7 percent of GDP), with respect to the first scenario (total tariff phase-out).

In addition, trade facilitation mechanisms are modelled as a decrease in the “iceberg” trade costs.33 These efficiency-enhancing trade facilitation mechanisms include customs automatization, improvements in ports and roads infrastructure that reduce transportation costs, and the simplification of custom procedures that serve to reduce the effective import prices.34

A uniform 2 percent decrease in the transportation costs between both regions and within CA, to simulate an improvement in trade facilitation mechanisms, generates significant gains from CAFTA. First, an approximated 10 percent additional increase in trade volumes between both regions is reached. In addition, welfare gains for CA rise by US$726 million with respect to the “static” case, which are motivated by a 3.5 percent increase in terms of trade and additional increases in the price of productive factors in the region.

One of the most anticipated gains from CAFTA for CA is expected to be on increased employment opportunities for the region, which can curb low wages and high under-employment and sub-utilization rates. In turn, these improved labor conditions can help to reduce the high poverty rates of the region. While the previous “static” scenario shows a wage increase of around 5.5 percent for both skilled and unskilled labor, these figures are implicitly assuming full employment.

Despite relatively low unemployment figures, labor sub-utilization is a serious problem in CA. Therefore, a more realistic simulation must take into account these labor market characteristics. To simulate an eventual positive impact of the agreement on employment, the skilled and unskilled workers wages in CA are fixed, to allow for trade shocks to adjust the number of employed workers. As a result, CAFTA increases employment of unskilled workers by 5.1 percent and skilled by 4.7 percent. In addition, GDP presents an increase of 2.6 percent, determined by the use of previously idle productive factors. Thus, even when sub-utilization figures will remain high, CAFTA could be a very positive influence to tackle this problem in the region, while providing a significant increase in production.

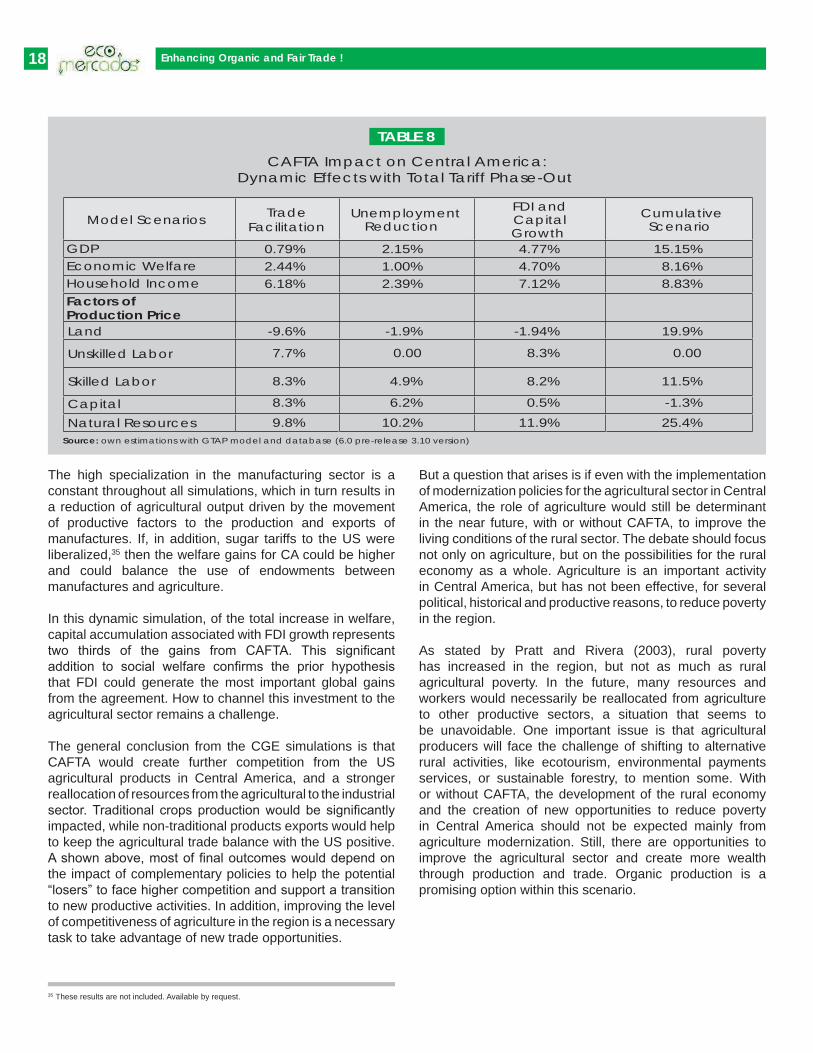

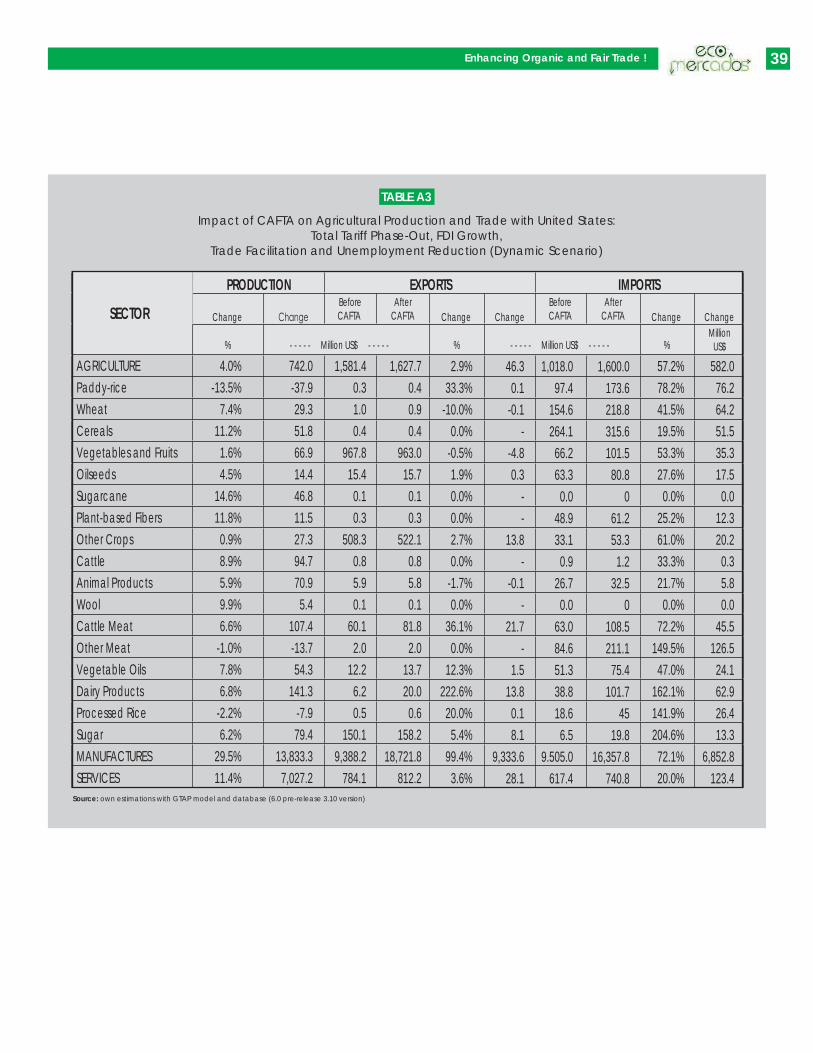

With these previous three shocks combined, an upper-bound or optimistic scenario where welfare is improved the most can be assessed (Table 8). In this scenario, capital stock increases by 21 percent and unskilled labor employment is increased by 13.5 percent. This increase in productive factors is directly associated with an improvement in social welfare by US$ 5,700 million and a GDP growth of 15 percent. This is achieved even when terms-of-trade do not improve as much as in the “static” case. These significant welfare gains reflect the potential and economic possibilities associated with free trade in general. Moreover, the overall reduction in agriculture production and exports from the first scenario is not observed. Even though some specific sectors are affected, some others are now expanding and this reflects the increase in the productive capacity of the region. On the other hand, import penetration remains high. Still, the agricultural trade balance with the US remains positive.

27 Table A3 in the annex includes the disaggregated results.28 See Helpman (2004) for a critical assessment of the literature on the links between trade openness and growth. 29 Pratt and Rivera (2003).30 Francois, Rojas-Romagosa and Rivera (2006).31 The Economist (2005). Many of the economy-wide effects of increased trade openness are dynamic in nature. While an improvement in the allocation of resources is the main static effect of liberalization, most of the expected gains from increased trade are dynamic. These include more and cheaper inputs and final products, pro-competitive effects associated with increasing returns to scale and the erosion of market power. However, the increase in investment flows is generally regarded as the main dynamic effect associated with trade liberalization.32 Following Francois et al. (1996), the impact of increased capital accumulation can de assessed by changing the closure rule of the standard GTAP model. To do this, it is assumed that the savings rate and the initial level of capital are endogenously determined and thus, the increase in capital associated with trade liberalization affects the results of the simulation. In practical terms, GTAP uses the end-of-period capital level, which is associated with the new savings rate and the flow of FDI from regions with lower capital returns, as the initial capital level. Hence, the trade shocks are implicitly considering the capital accumulation associated with the shock itself. In this way, although a dynamic model is not explicitly used, a good proxy of the dynamic effects of FDI and capital accumulation with CAFTA can be estimated. Therefore, FDI flows into the region can be linked with an increase in the amount of capital. With the GTAP model, this effect is assessed by including an additional scenario with a shock in the total tariff phase-out case by changing the closure rule to include capital accumulation and endogenous saving rates.33 In the GTAP setting trade costs are modelled using the “iceberg cost” approach. This implies that no specific international transportation sector is modelled, but instead, there is a mark-up between the effective price of goods and services between importers and exporters. This mark-up is lost (“melted”) and cannot by explained by tariffs or non-tariff barriers (NTBs), nor is it assigned to any region or institution.34 Hertel et al. (2001).

�8 Enhancing Organic and Fair Trade !

The high specialization in the manufacturing sector is a constant throughout all simulations, which in turn results in a reduction of agricultural output driven by the movement of productive factors to the production and exports of manufactures. If, in addition, sugar tariffs to the US were liberalized,35 then the welfare gains for CA could be higher and could balance the use of endowments between manufactures and agriculture.

In this dynamic simulation, of the total increase in welfare, capital accumulation associated with FDI growth represents two thirds of the gains from CAFTA. This significant addition to social welfare confirms the prior hypothesis that FDI could generate the most important global gains from the agreement. How to channel this investment to the agricultural sector remains a challenge.

The general conclusion from the CGE simulations is that CAFTA would create further competition from the US agricultural products in Central America, and a stronger reallocation of resources from the agricultural to the industrial sector. Traditional crops production would be significantly impacted, while non-traditional products exports would help to keep the agricultural trade balance with the US positive. A shown above, most of final outcomes would depend on the impact of complementary policies to help the potential “losers” to face higher competition and support a transition to new productive activities. In addition, improving the level of competitiveness of agriculture in the region is a necessary task to take advantage of new trade opportunities.

But a question that arises is if even with the implementation of modernization policies for the agricultural sector in Central America, the role of agriculture would still be determinant in the near future, with or without CAFTA, to improve the living conditions of the rural sector. The debate should focus not only on agriculture, but on the possibilities for the rural economy as a whole. Agriculture is an important activity in Central America, but has not been effective, for several political, historical and productive reasons, to reduce poverty in the region.

As stated by Pratt and Rivera (2003), rural poverty has increased in the region, but not as much as rural agricultural poverty. In the future, many resources and workers would necessarily be reallocated from agriculture to other productive sectors, a situation that seems to be unavoidable. One important issue is that agricultural producers will face the challenge of shifting to alternative rural activities, like ecotourism, environmental payments services, or sustainable forestry, to mention some. With or without CAFTA, the development of the rural economy and the creation of new opportunities to reduce poverty in Central America should not be expected mainly from agriculture modernization. Still, there are opportunities to improve the agricultural sector and create more wealth through production and trade. Organic production is a promising option within this scenario.

35 These results are not included. Available by request.

CAFTA Impact on Central America:Dynamic Effects with Total Tariff Phase-Out

TABLE 8

Source: own estimations with GTAP model and database (6.0 pre-release 3.10 version)

Model Scenarios

-9.6%

7.7%

TradeFacilitation

UnemploymentReduction

FDI andCapitalGrowth

CumulativeScenario

GDPEconomic WelfareHousehold Income

0.79%2.44%6.18%

2.15%1.00%2.39%

4.77%4.70%7.12%

15.15%8.16%8.83%

-1.9%

0.00

-1.94%

8.3%

19.9%

0.00

8.3%

8.3%9.8%

4.9%

6.2%10.2%

8.2%

0.5%11.9%

11.5%

-1.3%25.4%

Factors ofProduction PriceLand

Unskilled Labor

Skilled Labor

CapitalNatural Resources

�9Enhancing Organic and Fair Trade !

�.� AGRICULTURE COMPETITIVENESS IN CENTRAL AMERICA: A LONG ROAD AHEAD

istorically, the competitiveness of agriculture in Central America has been based on its comparative

advantages in geographical location, climatic variety, and endowments of water, soil, and abundant labor. According to Pratt and Rivera (2003) the experiences of successful companies and countries indicate that a greater agricultural competitiveness depends on at least four basic aspects: i) a more-efficient market functioning; ii) an active support policy for the sector in the short, medium and long terms that promotes product quality and greater value-added for its transformation and exports; iii) large-scale public and private investments in research and development, specialized infrastructure, education, market intelligence and international commercialization; and iv) the creation of world-class agribusiness clusters that allow the development of new and specialized products and services to support competitiveness.

Modern agriculture is an international business. The Central American countries are price- and rules-takers, since their influence on world markets is marginal. The region does not hold market power to be able to change neither global policies nor international agricultural business, both of which are becoming more concentrated among a small group of countries and multinational companies. In addition, there are important barriers in agricultural trade, and high interventionism in the most-developed nations of the world.

The central problem remains at the local level, because of the low levels of competitiveness of Central America’s agriculture. The real, long-term exit to agricultural problems depends on the reorientation of public policies, business strategies, and interrelations between the private, public, civil and multilateral sectors, given that the region has been left behind by the great advances experienced in modern agro-industrial systems worldwide.

Contrary to global tendencies to implement policies and national strategies to create value and develop more-competitive agricultural chains, governmental support for the agricultural sector in Central America stagnated in the

5. POTENTIAL IMPACTS OF CAFTA FOR ORGANIC AGRICULTURE IN CENTRAL AMERICA: THE CHALLENGE REMAINS THE SAME

last decade. The Central American countries have paid little attention to agriculture precisely during the years in which developed countries have intensified their investments in infrastructure, technological development, human capital creation, quality certification systems, environmental technologies, agricultural extension and, in general, clearly-established sector competitiveness policies.

Since agricultural activities are the basis of well-being and development for a large quantity of Central Americans, the impediments and problems that act as obstacles to the sector’s growth should be corrected, and there should be further efforts to contribute to a productive transition towards a greater diversification of the rural economy. Rural and agricultural policy formulation should consider the heterogeneity of the actors who form the sector, and be linked to the great challenges of competitiveness, sustainability and the fight against poverty.

What type of agricultural sector should be promoted? One that is efficient and competitive at international prices, based on companies´ capabilities, with their technical, social and environmental attributes, and in the conditions created by a competitive business climate. Additionally, the use of support instruments that have been successful on a world level, based on the provision of knowledge, infrastructure, the transfer of technology and trade intelligence, should be promoted.

After CAFTA, the Central American countries should redouble their efforts to continue promoting agricultural competitiveness policies that take advantage of existing comparative advantages, and further advance the creation of competitive advantages based on productivity, product differentiations and high value-added, to create more and better jobs, and new opportunities for Central America’s development. Within this scenario, organic agriculture would have a better environment to develop and position competitively in the US and other international markets. Or seen from another perspective, it is not likely that Central America will experience great success in organic exports in a region that is not competitive in agriculture in general – the changes that make conventional agriculture successful are a necessary (but not sufficient) condition for organic agriculture to be successful.

H

�0 Enhancing Organic and Fair Trade !

�.� THE ORGANIC AGRICULTURAL SECTOR IN CENTRAL AMERICA

The Organic agricultural production in Central America is driven by thousands of small farmers, organized in cooperatives and associations. Many producers sell their products through intermediaries and foreign buyers that process and export the agricultural organic goods. It is estimated that, on average, organic farms have an extension of 5 hectares. Currently, more than 79,000 hectares of land in the region are organic certified. The main characteristics of Central American organic markets, from the supply perspective, are:,36

● Most production is export oriented, although local and regional markets are increasing.

● Coffee is the most important product, followed by fruits and seeds.

● There is a high concentration on fresh products, with low levels of value added through processing.

● Produced volumes are low, with the exception of coffee and bananas.

● Organic animal and diary products market are not well developed, although organic meat has gained relevance in Nicaragua.

● Some personal care and processed food products are sold as “organic” without proper certifications.

Organic farms in Central America can be categorized in five groups: i) highly diversified farms with almost no use of synthetic inputs (i.e. coffee farms), ii) farms historically managed with indigenous sustainable practices, currently certified (i.e. raspberries), iii) organic transformed farms, iv) very small farms (less than one hectare) operated without chemicals due to budgetary restrictions, and v) conventional farms in transition to organic certification. Currently, the main incentive to transform conventional practices into organic agriculture practices has been the emerging market opportunities. On the other hand, many producers have seen organic production as an alternative to traditional sectors crisis, like the decreasing international prices of coffee.

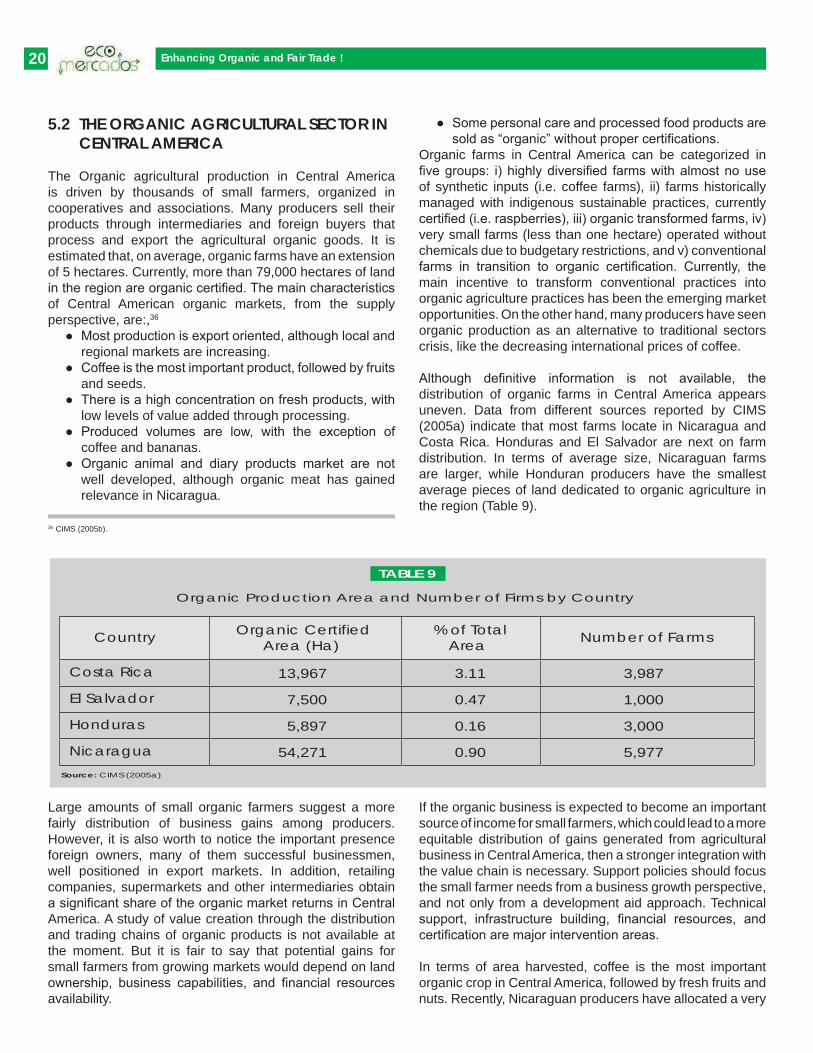

Although definitive information is not available, the distribution of organic farms in Central America appears uneven. Data from different sources reported by CIMS (2005a) indicate that most farms locate in Nicaragua and Costa Rica. Honduras and El Salvador are next on farm distribution. In terms of average size, Nicaraguan farms are larger, while Honduran producers have the smallest average pieces of land dedicated to organic agriculture in the region (Table 9).

TABLE 9

Country % of TotalArea

Number of Farms

Costa Rica

El Salvador

Honduras

Nicaragua

Organic CertifiedArea (Ha)

13,967

7,500

5,897

54,271

3,987

1,000

3,000

5,977

3.11

0.47

0.16

0.90

Organic Production Area and Number of Firms by Country

Source: CIMS (2005a)

Large amounts of small organic farmers suggest a more fairly distribution of business gains among producers. However, it is also worth to notice the important presence foreign owners, many of them successful businessmen, well positioned in export markets. In addition, retailing companies, supermarkets and other intermediaries obtain a significant share of the organic market returns in Central America. A study of value creation through the distribution and trading chains of organic products is not available at the moment. But it is fair to say that potential gains for small farmers from growing markets would depend on land ownership, business capabilities, and financial resources availability.

If the organic business is expected to become an important source of income for small farmers, which could lead to a more equitable distribution of gains generated from agricultural business in Central America, then a stronger integration with the value chain is necessary. Support policies should focus the small farmer needs from a business growth perspective, and not only from a development aid approach. Technical support, infrastructure building, financial resources, and certification are major intervention areas.

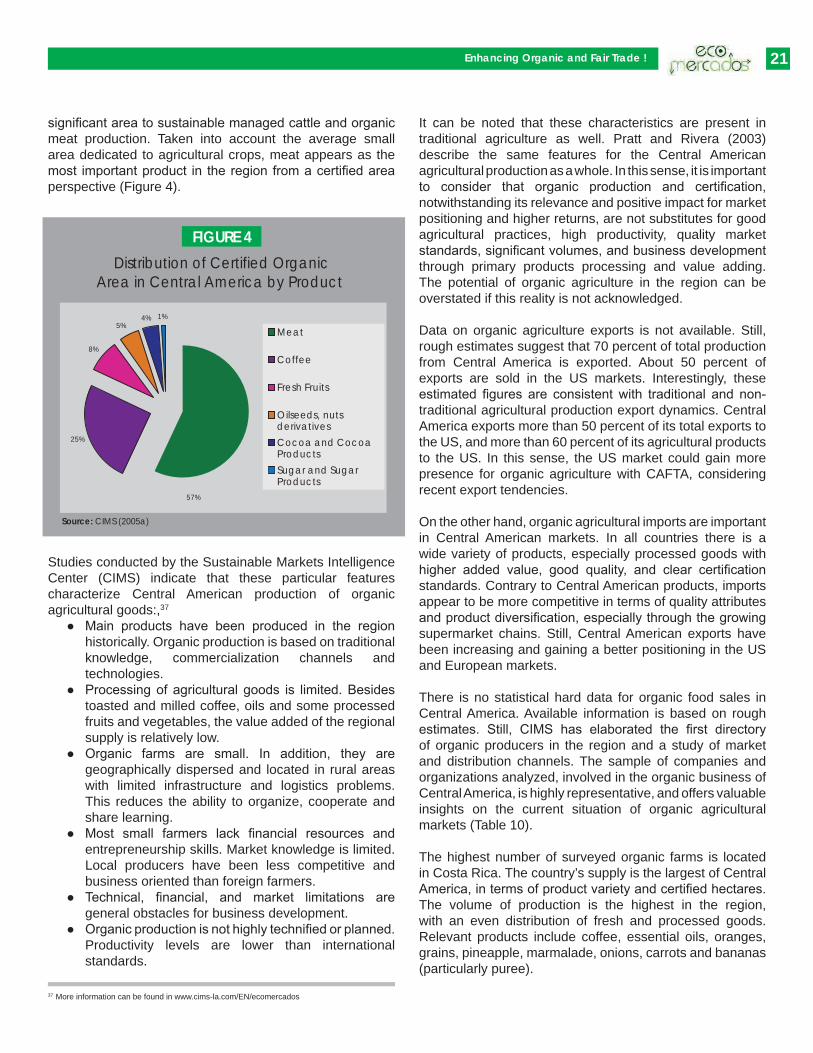

In terms of area harvested, coffee is the most important organic crop in Central America, followed by fresh fruits and nuts. Recently, Nicaraguan producers have allocated a very

36 CIMS (2005b).

��Enhancing Organic and Fair Trade !

Distribution of Certified OrganicArea in Central America by Product

FIGURE �

Source: CIMS (2005a)

25%

8%

5%4% 1%

57%

Meat

Coffee

Fresh Fruits

Oilseeds, nutsderivativesCocoa and CocoaProductsSugar and SugarProducts

significant area to sustainable managed cattle and organic meat production. Taken into account the average small area dedicated to agricultural crops, meat appears as the most important product in the region from a certified area perspective (Figure 4).

Studies conducted by the Sustainable Markets Intelligence Center (CIMS) indicate that these particular features characterize Central American production of organic agricultural goods:,37

● Main products have been produced in the region historically. Organic production is based on traditional knowledge, commercialization channels and technologies.

● Processing of agricultural goods is limited. Besides toasted and milled coffee, oils and some processed fruits and vegetables, the value added of the regional supply is relatively low.

● Organic farms are small. In addition, they are geographically dispersed and located in rural areas with limited infrastructure and logistics problems. This reduces the ability to organize, cooperate and share learning.

● Most small farmers lack financial resources and entrepreneurship skills. Market knowledge is limited. Local producers have been less competitive and business oriented than foreign farmers.

● Technical, financial, and market limitations are general obstacles for business development.

● Organic production is not highly technified or planned. Productivity levels are lower than international standards.

It can be noted that these characteristics are present in traditional agriculture as well. Pratt and Rivera (2003) describe the same features for the Central American agricultural production as a whole. In this sense, it is important to consider that organic production and certification, notwithstanding its relevance and positive impact for market positioning and higher returns, are not substitutes for good agricultural practices, high productivity, quality market standards, significant volumes, and business development through primary products processing and value adding. The potential of organic agriculture in the region can be overstated if this reality is not acknowledged.

Data on organic agriculture exports is not available. Still, rough estimates suggest that 70 percent of total production from Central America is exported. About 50 percent of exports are sold in the US markets. Interestingly, these estimated figures are consistent with traditional and non-traditional agricultural production export dynamics. Central America exports more than 50 percent of its total exports to the US, and more than 60 percent of its agricultural products to the US. In this sense, the US market could gain more presence for organic agriculture with CAFTA, considering recent export tendencies.

On the other hand, organic agricultural imports are important in Central American markets. In all countries there is a wide variety of products, especially processed goods with higher added value, good quality, and clear certification standards. Contrary to Central American products, imports appear to be more competitive in terms of quality attributes and product diversification, especially through the growing supermarket chains. Still, Central American exports have been increasing and gaining a better positioning in the US and European markets.

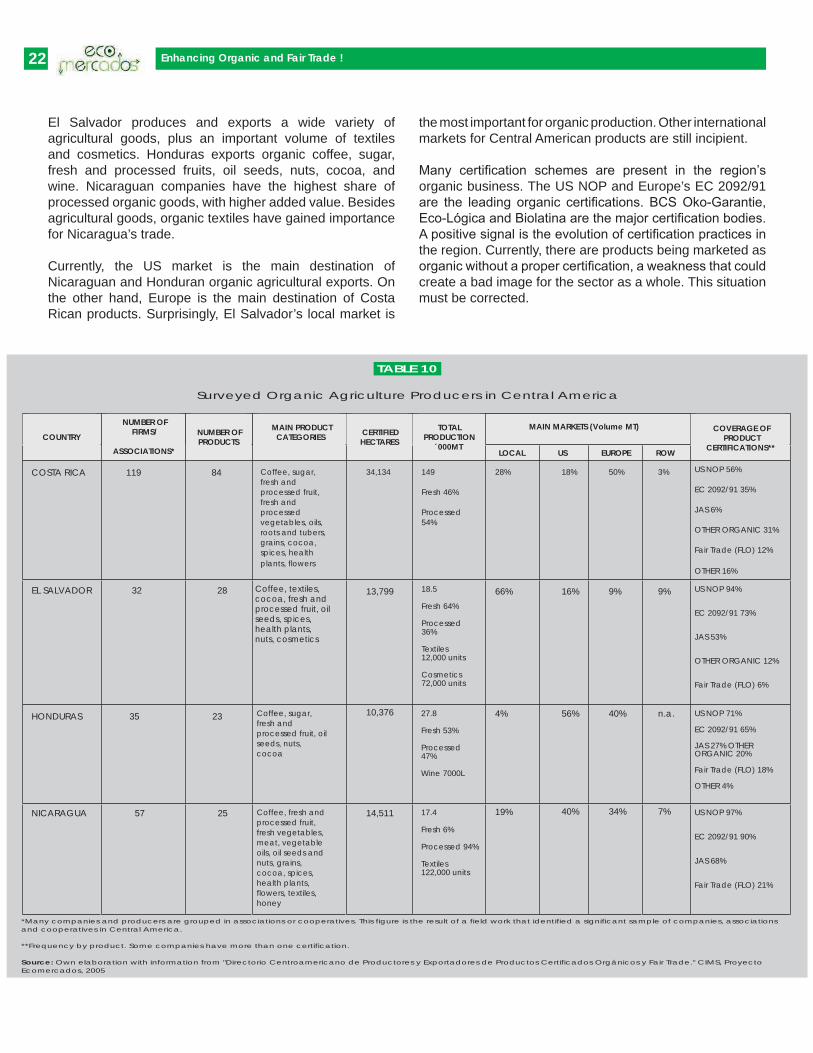

There is no statistical hard data for organic food sales in Central America. Available information is based on rough estimates. Still, CIMS has elaborated the first directory of organic producers in the region and a study of market and distribution channels. The sample of companies and organizations analyzed, involved in the organic business of Central America, is highly representative, and offers valuable insights on the current situation of organic agricultural markets (Table 10).

The highest number of surveyed organic farms is located in Costa Rica. The country’s supply is the largest of Central America, in terms of product variety and certified hectares. The volume of production is the highest in the region, with an even distribution of fresh and processed goods. Relevant products include coffee, essential oils, oranges, grains, pineapple, marmalade, onions, carrots and bananas (particularly puree).

37 More information can be found in www.cims-la.com/EN/ecomercados

�� Enhancing Organic and Fair Trade !

El Salvador produces and exports a wide variety of agricultural goods, plus an important volume of textiles and cosmetics. Honduras exports organic coffee, sugar, fresh and processed fruits, oil seeds, nuts, cocoa, and wine. Nicaraguan companies have the highest share of processed organic goods, with higher added value. Besides agricultural goods, organic textiles have gained importance for Nicaragua’s trade.

Currently, the US market is the main destination of Nicaraguan and Honduran organic agricultural exports. On the other hand, Europe is the main destination of Costa Rican products. Surprisingly, El Salvador’s local market is

the most important for organic production. Other international markets for Central American products are still incipient.

Many certification schemes are present in the region’s organic business. The US NOP and Europe’s EC 2092/91 are the leading organic certifications. BCS Oko-Garantie, Eco-Lógica and Biolatina are the major certification bodies. A positive signal is the evolution of certification practices in the region. Currently, there are products being marketed as organic without a proper certification, a weakness that could create a bad image for the sector as a whole. This situation must be corrected.

TABLE �0

Surveyed Organic Agriculture Producers in Central America

COUNTRYCOVERAGE OF

PRODUCTCERTIFICATIONS**

Coffee, sugar,fresh andprocessed fruit,fresh andprocessedvegetables, oils,roots and tubers,grains, cocoa,spices, healthplants, flowers

US NOP 56%

EC 2092/91 35%

JAS 6%

OTHER ORGANIC 31%

Fair Trade (FLO) 12%

OTHER 16%

US NOP 94%

EC 2092/91 73%

JAS 53%

OTHER ORGANIC 12%

Fair Trade (FLO) 6%

US NOP 71%

EC 2092/91 65%

JAS 27% OTHERORGANIC 20%

Fair Trade (FLO) 18%

OTHER 4%

US NOP 97%

EC 2092/91 90%

JAS 68%

Fair Trade (FLO) 21%

34,134

13,799

10,376

14,511

28%

66%

4%

19%

18%

16%

56%

40%

50%

9%

40%

34%

3%

9%

n.a.

7%

149

Fresh 46%

Processed54%

18.5

Fresh 64%

Processed36%

Textiles12,000 units

Cosmetics72,000 units

27.8

Fresh 53%

Processed47%

Wine 7000L

17.4

Fresh 6%

Processed 94%

Textiles122,000 units

NUMBER OFFIRMS/

ASSOCIATIONS*

NUMBER OFPRODUCTS

MAIN PRODUCTCATEGORIES CERTIFIED

HECTARES

TOTALPRODUCTION

´000MT

MAIN MARKETS (Volume MT)

COSTA RICA 119 84

EL SALVADOR 32 28

HONDURAS 35 23

NICARAGUA 57 25

Coffee, textiles,cocoa, fresh andprocessed fruit, oilseeds, spices,health plants,nuts, cosmetics

Coffee, sugar,fresh andprocessed fruit, oilseeds, nuts,cocoa

Coffee, fresh andprocessed fruit,fresh vegetables,meat, vegetableoils, oil seeds andnuts, grains,cocoa, spices,health plants,flowers, textiles,honey

*Many companies and producers are grouped in associations or cooperatives. This figure is the result of a field work that identified a significant sample of companies, associationsand cooperatives in Central America.

**Frequency by product. Some companies have more than one certification.

Source: Own elaboration with information from "Directorio Centroamericano de Productores y Exportadores de Productos Certificados Orgánicos y Fair Trade." CIMS, ProyectoEcomercados, 2005

LOCAL US EUROPE ROW

23Enhancing Organic and Fair Trade !

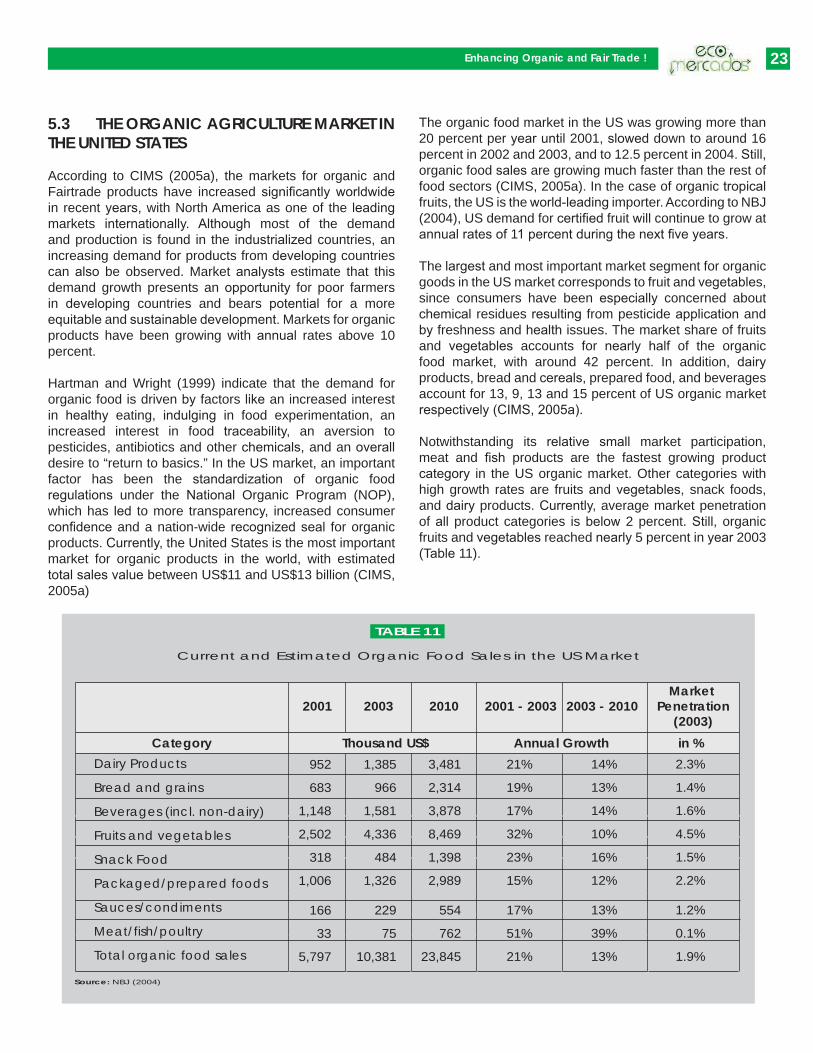

5.3 THE ORGANIC AGRICULTURE MARKET IN THE UNITED STATES

According to CIMS (2005a), the markets for organic and Fairtrade products have increased significantly worldwide in recent years, with North America as one of the leading markets internationally. Although most of the demand and production is found in the industrialized countries, an increasing demand for products from developing countries can also be observed. Market analysts estimate that this demand growth presents an opportunity for poor farmers in developing countries and bears potential for a more equitable and sustainable development. Markets for organic products have been growing with annual rates above 10 percent.

Hartman and Wright (1999) indicate that the demand for organic food is driven by factors like an increased interest in healthy eating, indulging in food experimentation, an increased interest in food traceability, an aversion to pesticides, antibiotics and other chemicals, and an overall desire to “return to basics.” In the US market, an important factor has been the standardization of organic food regulations under the National Organic Program (NOP), which has led to more transparency, increased consumer confidence and a nation-wide recognized seal for organic products. Currently, the United States is the most important market for organic products in the world, with estimated total sales value between US$11 and US$13 billion (CIMS, 2005a)