Embed Size (px)

Citation preview

A report from The Economist Intelligence Unit

PART OF THE GROWTH CROSSINGS SERIES

Commissioned by

Shorter, smarter and more sustainable?

Rebooting supply chains

© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

1. Executive summary 42. Confidence, commodities and costs 83. Strategic innovation and supply chains 124. A future with shorter supply chains 165. Treasury: Supply-chain leader 206. Conclusion 24Appendix – Survey results 26

CONTENTS

4 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

EXECUTIVE SUMMARY1company executives are focused on keeping down operating costs over the next year and increasing operational transparency through technological innovation. Over the next five years, companies envision bigger changes: sourcing networks will be simpler, smarter and ideally more sustainable.

Key findings from the research include:

Most companies are confident about being able to deal with supply-chain disruptions over the next year, but they are very sensitive about costs.

The survey found that those who are better prepared are more confident about dealing with challenges and disruptions. There was substantial agreement on another point: lowering costs in the supply chain.

Innovation is seen as a crucial part of strategic supply-chain management because it will help create full visibility across production networks and thereby support sustainability.

Commitment to technological innovation is extraordinarily widespread in supply chain management. More than nine-in-ten (93%) executives surveyed have identified it as important. Companies that believe innovation is very important are also more confident they can address external disruptions.

Concerns about geopolitical and economic risks have grown among those who oversee company supply chains. Both Brexit in 2016 and the seeming arrival in 2017 of a new era in US trade policy under the presidency of Donald Trump have created new uncertainties. For example, factory managers in Asia, whose operations are vital links in many companies’ global supply chains, may read nationalistic rhetoric from the West and logically wonder whether some of their supplier relationships have become politically inexpedient. Senior executives at multinational companies with complex sourcing networks spanning the globe may worry that populist pressure could force them to re-shore jobs or to rethink how their products are made and where they come from. These are not necessarily unfounded fears, as this Economist Intelligence Unit (EIU) report concludes.

The rules of global trade are shifting and companies will need to make sure their supply chains have the agility and resourcefulness to deal with potential challenges and disruptions that may lie ahead. Questions remain about whether the pace of globalisation will slow considerably, shift its direction or possibly reverse

A survey about the future of supply chains, conducted by The EIU and commissioned by Standard Chartered Bank, found that

5© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

Global supply chains are expected to shorten, but depending on the industry may not necessarily become less complex.

More companies (49%) expect supply chains to become shorter and simpler in the next five years than those (33%) who expect them to grow longer and more complex. Even so, some companies that expect to shorten their supply chains may increase their complexity in response to consumer preferences. Shortening and simplifying are seen as ways to reduce the vulnerability of the supply chain to external disruptions, as well as to lower costs and improve effectiveness.

Treasury may yet emerge as a leader of strategic supply-management efforts. Are treasurers ready for the challenge?

Companies rate core skills of the treasury function highly when it comes to managing supply chains in the future. But most companies still see treasurers in a governance role, rather than having a strategically important role for supply chains. Treasury will have to be enabled, and some industries, such as IT, energy and industrials, are more likely to thrust treasury into a leadership role. This begs the question: are treasurers ready to embrace the challenge of leading a supply chain?

6 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

C-level or board positions, while the rest are senior executives and other senior managers.

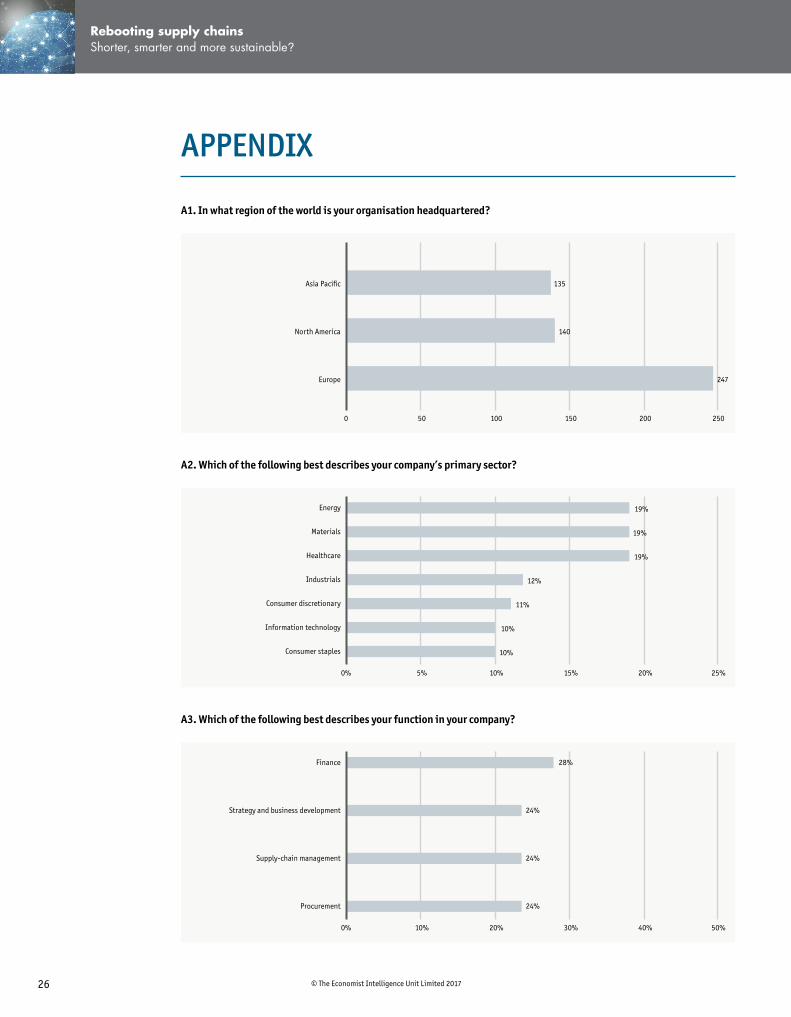

n In terms of corporate functions, financial executives and managers represent 28% of the sample. The remaining three categories of respondents each represent 24% of the sample: strategy and business development, procurement, and supply-chain management.

Survey respondents are distributed across seven types of businesses. Three of them – energy, materials and healthcare – each represent 19%. Industrials are the next largest segment at 12%, followed by consumer discretionary at 11%, and information technology and consumer staples both at 10%.

About the study Rebooting supply chains: Shorter, smarter

and more sustainable? is an EIU report, sponsored by Standard Chartered Bank. It is part of the Growth Crossings series. The report explores the objectives, challenges and potential disruptions facing companies with global supply chains and how they are preparing to deal with them in the future.

The report draws on two strands of research for its findings:

n In February 2017, The EIU surveyed 522 business leaders in 13 countries. Six of the nations represented are in Asia Pacific, five in Europe, and two in North America. Nearly half (48%) of the respondents hold

Respondents participating in The EIU survey are spread around the world in countries from North America to Europe to Asia Pacific.

NORTH AMERICA

140

ASIA PACIFIC

135

EUROPE

247

7© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

In-depth interviews were conducted with the following individuals (in alphabetical order by their surname):

• Deborah Elms, founder and executive director, Asian Trade Centre

• John Hayduk, chief operating officer, Tata Communications

• Tom Linton, chief procurement and supply chain officer, Flex

• Ernest Mui, director of treasury and tax, Asia Pacific, Knorr-Bremse

• Corrado Snaiderbaur, supply chain manager, Chiesi Farmaceutici

• Sander de Vries, manager, Zanders

• Roy Williams, managing director, Vendigital

We would like to thank all interviewees and survey respondents for their time and insight.

The EIU bears sole responsibility for the content of this report. The findings do not necessarily reflect the views of the sponsor. n

8 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

CONFIDENCE, COMMODITIES AND COSTS2

report, we will see how these factors may be driving a focus over the next twelve months on reducing supply-chain-related costs.

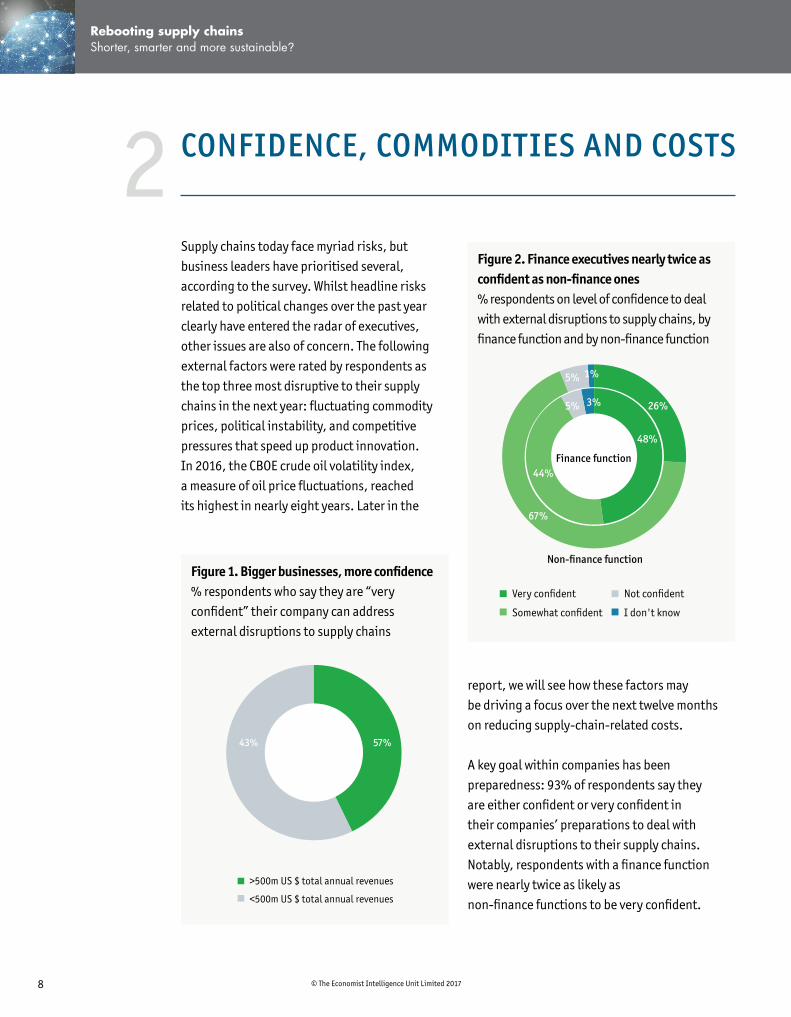

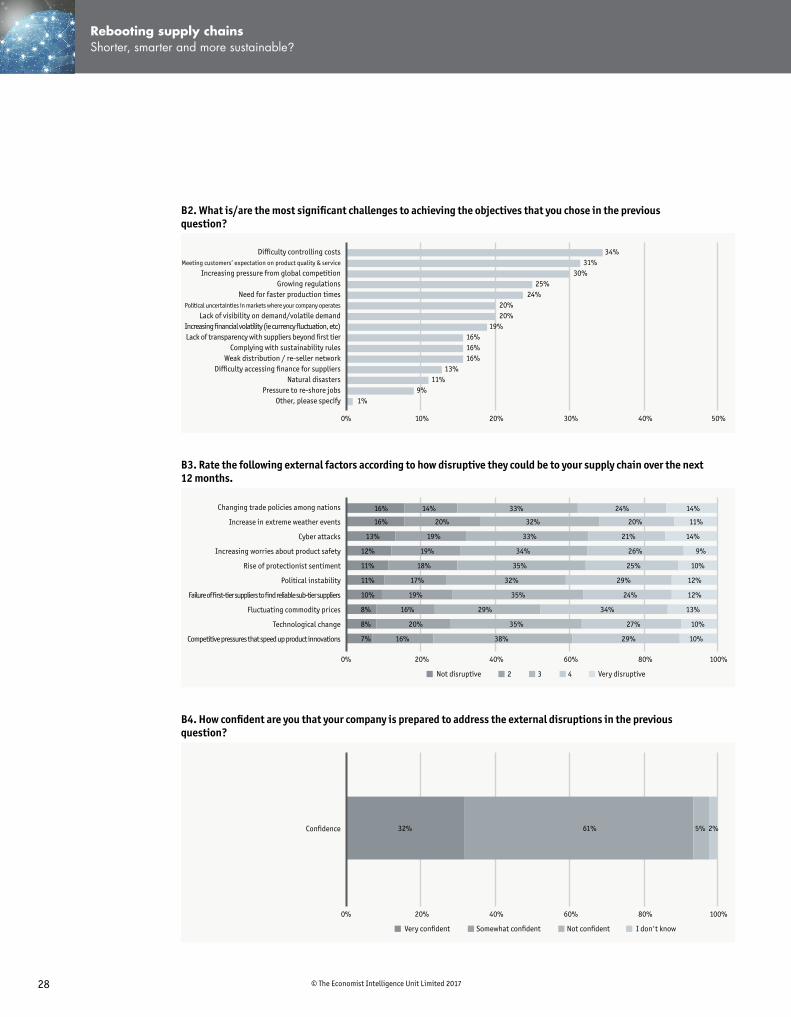

A key goal within companies has been preparedness: 93% of respondents say they are either confident or very confident in their companies’ preparations to deal with external disruptions to their supply chains. Notably, respondents with a finance function were nearly twice as likely as non-finance functions to be very confident.

Supply chains today face myriad risks, but business leaders have prioritised several, according to the survey. Whilst headline risks related to political changes over the past year clearly have entered the radar of executives, other issues are also of concern. The following external factors were rated by respondents as the top three most disruptive to their supply chains in the next year: fluctuating commodity prices, political instability, and competitive pressures that speed up product innovation. In 2016, the CBOE crude oil volatility index, a measure of oil price fluctuations, reached its highest in nearly eight years. Later in the

>500m US $ total annual revenues

<500m US $ total annual revenues

57%43%

Finance function

Non-�nance function

1%

44%

5%

5%

3%

48%

26%

67%

Very con�dent

Somewhat con�dent

Not con�dent

I don't know

Figure 1. Bigger businesses, more confidence % respondents who say they are “very confident” their company can address external disruptions to supply chains

Figure 2. Finance executives nearly twice as confident as non-finance ones % respondents on level of confidence to deal with external disruptions to supply chains, by finance function and by non-finance function

9© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

Overall, collaboration between internal teams, including finance and risk management, is the top action that 42% of respondents said they

Collaboration between internal

teams, including finance

and risk management, is

the top action that 42% of

respondents said they were

taking to reduce fallout from

supply-chain disruptions.

This report will make the case that whilst internal collaboration between operations and finance is taking place to manage supply chains, much more needs to be done to achieve strategic objectives.

Size matters, but also preparation

Among the respondents who said they were very confident about their company’s ability to deal with external supply-chain disruptions, 57% came from firms with more than US$500m in annual revenues. This suggests the size of the principal in a supply chain matters when it comes to provision of resources to deal with disruptions. But this is only one factor.

42%

29%

28%

28%

25%

23%

22%

21%

21%

Collaboration among internal teams

Mitigation plans for disruptions

Demand planning for new products

Product portfolio review for resilience

Scenario planning

Online analytical tools to mitigate risk

Insurance against speci�c events

Internal unit to study disruptions

Secured more lines of credit

Hired risk management specialists

0% 10% 20% 30% 40% 50%

42%

Figure 3. Internal collaboration tops action plans % respondents by action taken to limit fallout from external disruptions

10 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

(28%) respondents say their companies have also engaged in scenario planning.

Scenario planning is particularly handy during a time of geopolitical uncertainty, and should also include disruptions in trade policy, such as fallout from Brexit, says Deborah Elms, executive director of the Asian Trade Centre in Singapore. “It will take a while for companies to grasp how damaging this will be,” she says because clarity about the new rules governing trade flows in Europe will not be known for quite some time.

A closer look at the cohort of respondents who said they were very confident about dealing with supply-chain disruptions reveals a simple rule: those who are very confident are more likely to have taken steps to limit supply-chain disruptions. Among the actions taken to reduce

were taking to reduce fallout from supply-chain disruptions. A third of those surveyed report their companies have then taken the next logical step and developed plans to mitigate the fallout from disruptions. Being prepared to mitigate or hedge potential disruptions allows companies to be more flexible with their responses, says Roy Williams, managing director at Vendigital, a consultancy focused on supply-chain management. “If your supply chain is more agile, you can adjust to changing trade policy and other challenges,” he says.

Given that the pace of new product innovation can be a significant challenge to supply chains, 29% of respondents in the survey also report their companies are conducting demand planning for new products to mitigate fallout from disruptions. And nearly three-in-ten

0%

10%

20%

30%

40%

Very con�dent in addressing external disruptions

Internal unit tostudy disruptions

Insurance againstspeci�c events

Hired riskmanagement specialists

Added linesof credit

Less con�dent in addressing external disruptions

31%

18%

30%

20%

29%

18%

28%

17%

Figure 4. Virtuous circle of confidence and preparedness % cohort, by actions taken to reduce fallout from supply-chain disruptions

11© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

fallout, the very-confident cohort was more likely than the less-or-not-confident cohort to set up internal units to study disruptions, buy insurance against specific events, hire supply-chain management specialists and secure additional lines of credit.

There is no silver bullet for supply-chain risks however. A significant majority of respondents take multiple actions to prepare against potential disruptions.

Delivering value, or slash and burn?

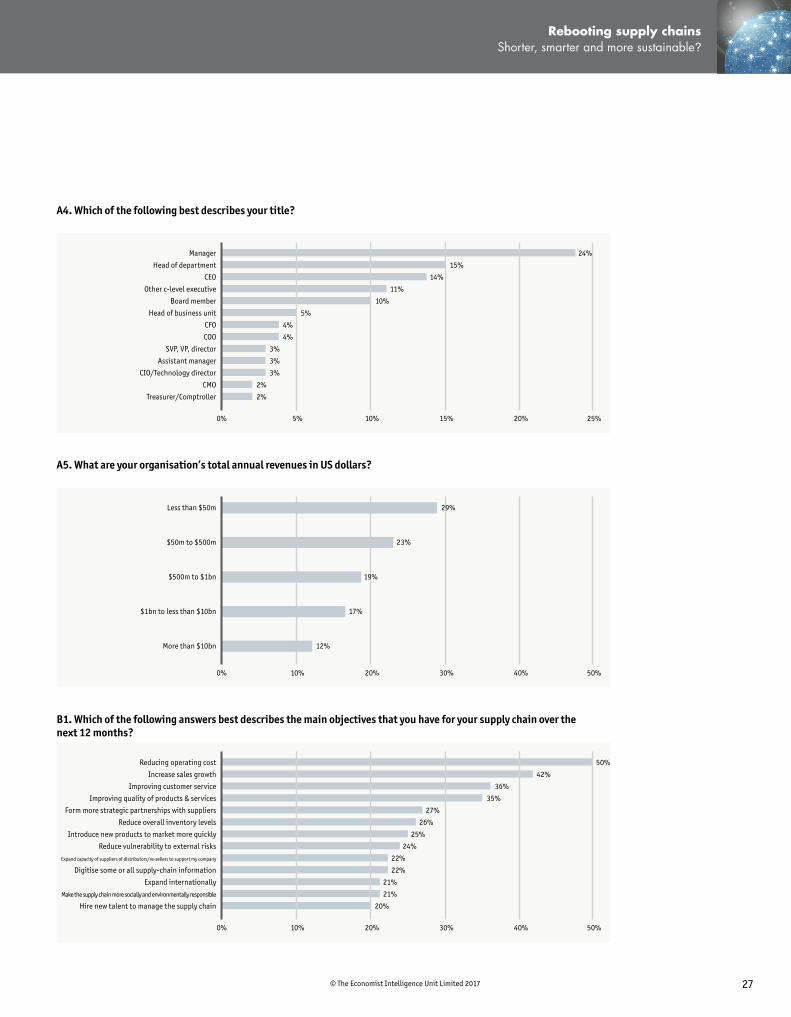

Supply-chain-related costs are a top concern among businesses globally, particularly as customer expectations for product quality increase. Reducing costs in the supply chain over the next twelve months is the most-cited objective, with 50% of respondents identifying it as a focus. Respondents are also keen on increasing sales (42%), improving customer service (36%) and improving the quality of products and services (35%).

Controlling costs is important because companies have to provide a return on their investment earlier and earlier in product cycles, according to Corrado Snaiderbaur, supply chain manager at Chiesi Farmaceutici in Parma, Italy. Even patents, which offer protection for new pharmaceutical products, do not provide a long term safe harbour like they used to do. “If you are not able to earn a return on investment in the shortest possible period, you may be exposed to risk from competitors who may put a better drug on the market,” he says.

Cutting costs is a logical reaction to higher levels of market uncertainty, but businesses should be focused on delivering value to customers rather than getting caught in relentless drives to reduce expenditure.

Boosting profitability and competitive position undoubtedly gives companies a better chance of dealing with disruptions. The survey found that difficulty controlling costs in the supply chain is the most significant challenge, a view cited by half of respondents. However, there is often a lack of clarity around what is really driving costs within an organization. Later in the report we will explore how achieving complete transparency in supply-chain operations isa major strategic goal.

Vendigital’s Mr Williams adds that it is important that business leaders avoid a “slash and burn approach” to cutting costs. Indeed, there are good costs and bad costs. Bad costs may be more associated with fixed legacy costs in a part of the business where margins are eroding, and these should be the focus of cost reduction drives. “Good costs are things that help the business grow,” he says. These are usually variable costs that, when they are rising, translate into higher revenue and profit growth. The next section of this report will focus on what may be one of the most important “good costs” when it comes to strategic management of supply chains: innovation. n

12 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

STRATEGIC INNOVATION AND SUPPLY CHAINS3

“We know how our materials move in different areas of the world and how finished products reach our customer’s door step,” says Mr Linton. “In times of crisis and disasters, we can quickly react to it because the system allows us to run ‘what-if’ scenarios and hypotheses in a very detailed manner.”

Strengthening data reliability

The need for better information to make business decisions lies at the heart of data reliability issues. Supply chains can generate huge amounts of valuable data, such as delivery times, shipment locations, inventories, new orders, payments and the list goes on. But before a company can process and analyse this information, it needs to know the data is clean and reliable.

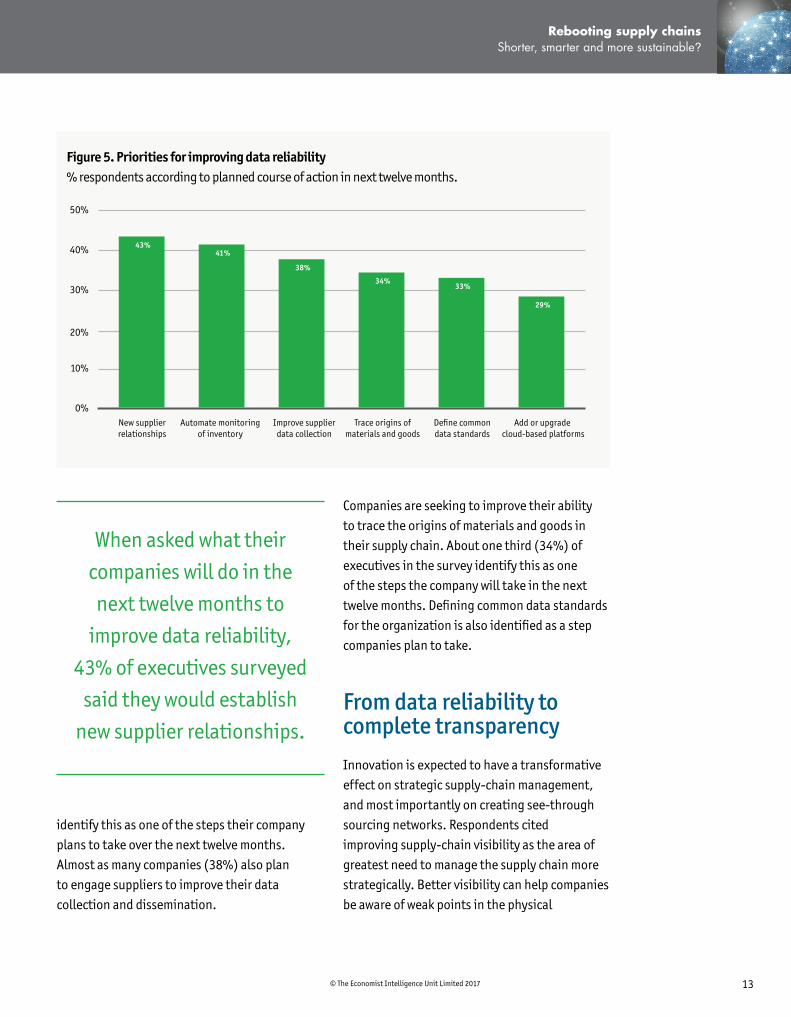

When asked what their companies will do in the next twelve months to improve data reliability, 43% of executives surveyed said they would establish new supplier relationships. This strongly suggests suppliers themselves will need to improve their data management capabilities or face the risk of being replaced. Companies plan to automate processes in the supply chain to improve their ability to monitor inventory. More than four in ten (41%) in the survey

Innovation, especially through the use of digital technologies, will likely transform supply-chain management over the next five years. This study found that business leaders are focused on using innovative technologies to increase efficiency and ultimately to achieve much greater transparency about operations.

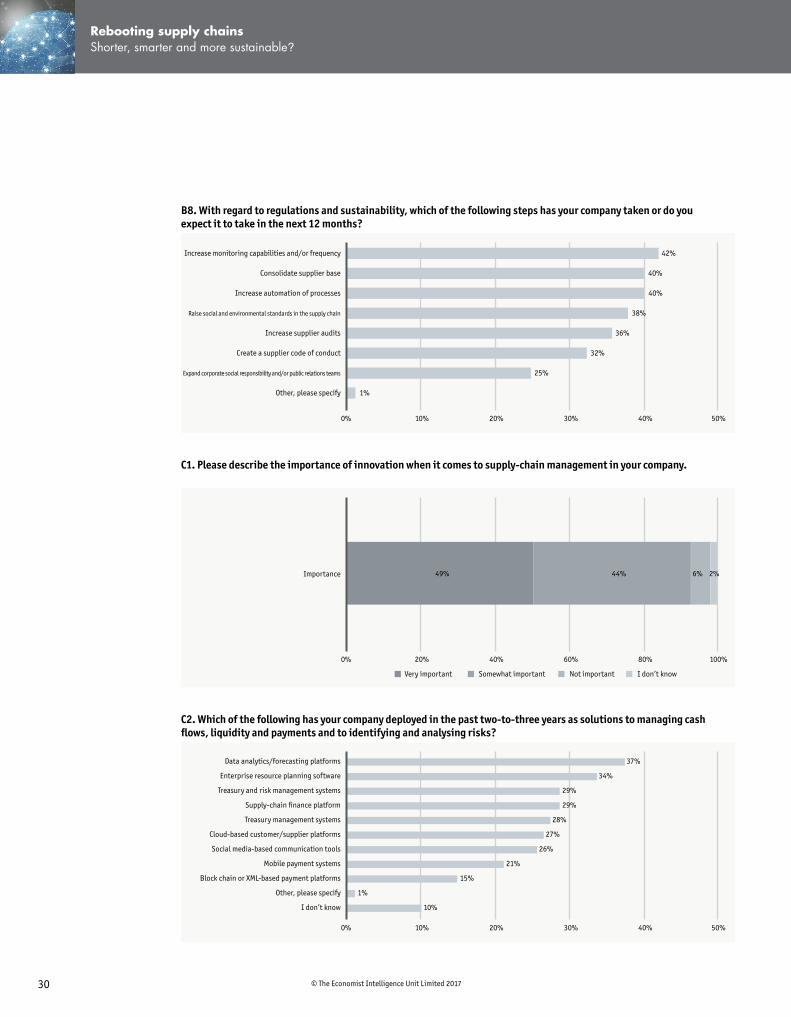

Nine-out-of-ten (93%) respondents say innovation is important when it comes to supply-chain management. Nearly half (49%) rated innovation very important, with 44% rating it somewhat important.

Companies clearly are embracing an innovation ethos when it comes to their supply chains, and over the next five years they will be focused on improving two related aspects of supply-chain management: data analytics and visibility. For senior executives, this will likely mean that the kind of skills and capabilities needed to manage supply chains will evolve and may require much more collaboration with hitherto unrelated functions, such as treasury and IT systems management.

Technology improvements that enhance visibility can also improve productivity, says Tom Linton, chief procurement and supply chain officer at Flex in San Jose, California. He cites as an example the company’s creation of a cloud-based platform that allows it to be better informed in near real-time about the functioning of the supply chain.

13© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

identify this as one of the steps their company plans to take over the next twelve months. Almost as many companies (38%) also plan to engage suppliers to improve their data collection and dissemination.

Companies are seeking to improve their ability to trace the origins of materials and goods in their supply chain. About one third (34%) of executives in the survey identify this as one of the steps the company will take in the next twelve months. Defining common data standards for the organization is also identified as a step companies plan to take.

From data reliability to complete transparency

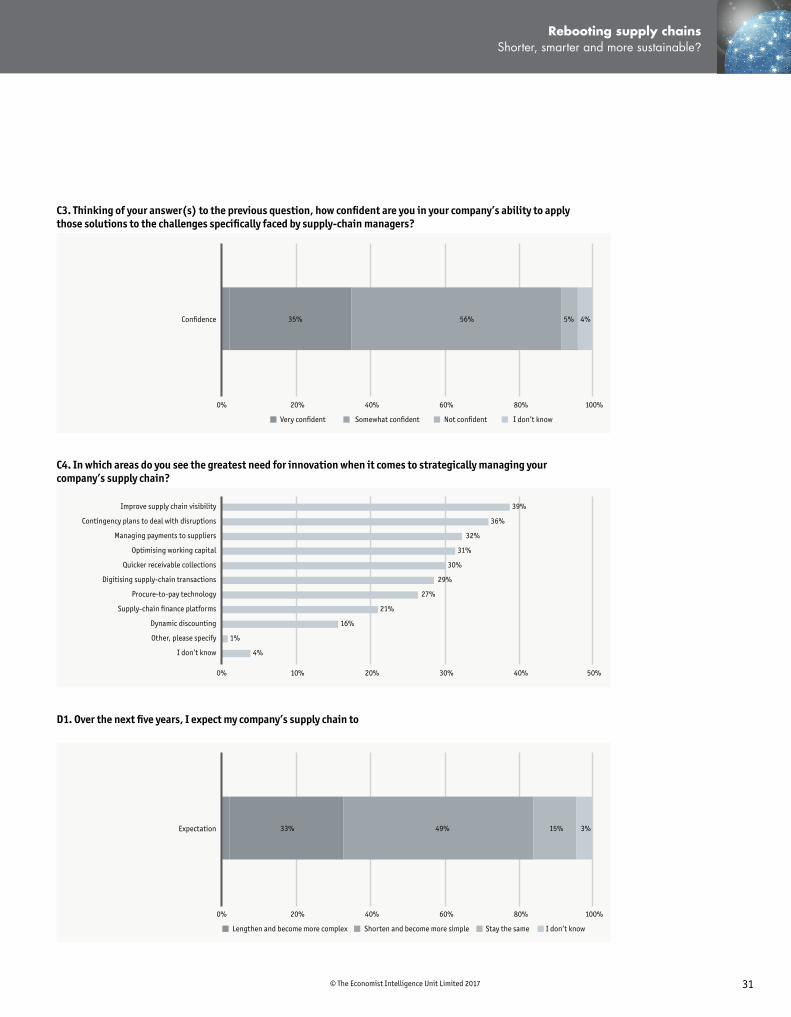

Innovation is expected to have a transformative effect on strategic supply-chain management, and most importantly on creating see-through sourcing networks. Respondents cited improving supply-chain visibility as the area of greatest need to manage the supply chain more strategically. Better visibility can help companies be aware of weak points in the physical

41%

38%

34%33%

29%

0%

10%

20%

30%

40%

50%

New supplierrelationships

Automate monitoringof inventory

Improve supplierdata collection

Trace origins ofmaterials and goods

De�ne commondata standards

Add or upgrade cloud-based platforms

43%

Figure 5. Priorities for improving data reliability % respondents according to planned course of action in next twelve months.

When asked what their

companies will do in the

next twelve months to

improve data reliability,

43% of executives surveyed

said they would establish

new supplier relationships.

14 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

Better visibility can help companies decide where in distribution they need to send new product shipments, according to Mr Snaiderbaur, who implemented a supply -chain planning tool for group affiliates when he came to Chiesi twelve years ago. In 2012, the company implemented an enterprise resource planning (ERP) platform to monitor data from affiliates. “Having clear visibility of data across the supply chain from the corporate position allows you to make a common decision with the affiliates based on data and not based on a negotiation basis, which is always better,” says Mr Snaiderbaur. Such decisions involve where Chiesi will ship new products so that the company can be sure they are sent to where they are needed and not to where inventory may be too high.

production process or in financing that could lead to slowdowns in deliveries or disruptions. By knowing where these weak points are, supply-chain leadership can take steps to mitigate or hedge those risks.

Improve supply chain visibility

Contingency plans for disruptions

Managing supplier payments

Optimising working capital

Quicker receivable collections

Digitising supply-chain transactions

Procure-to-pay technology

Supply-chain �nance platforms

Dynamic discounting

0% 10% 20% 30% 40% 50%

39%

36%

32%

31%

30%

29%

27%

21%

16%

Figure 6. Supply-chain visibility in need of innovation % repondents, according to areas in greatest need of innovation to manage supply chains

Innovation is expected to

have a transformative effect

on strategic supply-chain

management, and most

importantly on creating

see-through sourcing networks.

15© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

Companies also see a need for contingency plans to deal with disruptions. More than a third (36%) of executives in the survey identify this as an area of greatest need for innovation. Nearly a third (31%) of respondents identify optimising working capital as an area of greatest need, while 30% also named quicker receivable collections.

Digitising supply-chain transactions was cited by nearly one-in-three (29%) respondents as an area of greatest need for innovation. Why is digitisation so important? It automatically identifies and records which part of a supply chain is involved in a particular event or issue, according to Vendigital’s Mr Williams. When transactions are digitised, it frees up resources than can be applied toward reducing costs and improving the effectiveness of the supply chain.

Improving financial flows can reduce delays in the financial supply system that can slow down movement in the physical supply chain. Thus, it should not be a surprise that companies also identify as areas of greatest need several innovations designed to streamline the flow

of funds in the financial supply chain. These include procure-to-pay technology, cited by 27%, supply-chain finance platforms (21%) and dynamic discounting (16%). n

Improving financial flows

can reduce delays in the

financial supply system that

can slow down movement in

the physical supply chain.

16 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

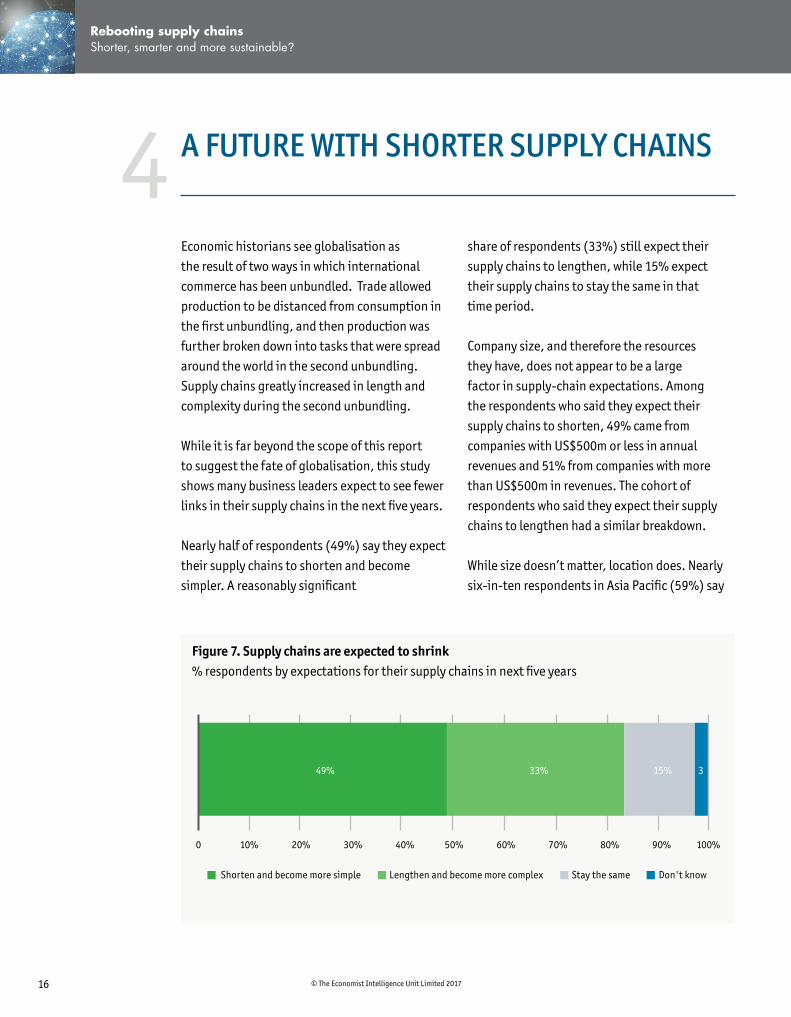

A FUTURE WITH SHORTER SUPPLY CHAINS4share of respondents (33%) still expect their supply chains to lengthen, while 15% expect their supply chains to stay the same in that time period.

Company size, and therefore the resources they have, does not appear to be a large factor in supply-chain expectations. Among the respondents who said they expect their supply chains to shorten, 49% came from companies with US$500m or less in annual revenues and 51% from companies with more than US$500m in revenues. The cohort of respondents who said they expect their supply chains to lengthen had a similar breakdown.

While size doesn’t matter, location does. Nearly six-in-ten respondents in Asia Pacific (59%) say

Economic historians see globalisation as the result of two ways in which international commerce has been unbundled. Trade allowed production to be distanced from consumption in the first unbundling, and then production was further broken down into tasks that were spread around the world in the second unbundling. Supply chains greatly increased in length and complexity during the second unbundling.

While it is far beyond the scope of this report to suggest the fate of globalisation, this study shows many business leaders expect to see fewer links in their supply chains in the next five years.

Nearly half of respondents (49%) say they expect their supply chains to shorten and become simpler. A reasonably significant

100%40%20% 30%10% 80%60% 70% 90%50%0

Shorten and become more simple Lengthen and become more complex Stay the same Don't know

49% 33% 15% 3

Figure 7. Supply chains are expected to shrink % respondents by expectations for their supply chains in next five years

17© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

they expect shorter supply chains versus 46% in Europe and 45% in North America. Businesses in Asia Pacific may be keen on keeping their supply chains closer to end customers in the region, where intraregional trade has been rising.

At Knorr-Bremse, a maker of braking systems for trains and commercial vehicles, the general rule is that “we always want to have a shorter and simpler supply chain,” says Ernest Mui, the company’s Hong Kong-based director of treasury and tax for Asia Pacific. The company faces a challenge in achieving that desirable goal. Mr Mui is concerned that in the coming year, the political environment in some countries raises the possibility those nations may not remain committed to free trade and keeping their market open. “For the United States, there is already a bit of uncertainty,” he says. “If some important markets become less open, the supply chain would obviously become longer.”

Shorter is not always simpler

Shortening supply chains, of course, does not necessarily make them less complex. More than a third of respondents (36%) say they agree with the statement that a rising regulatory burden will add cost and complexity to managing their supply chains.

Furthermore, consumer preferences for innovation and products that are tailored to their needs will tend to drive complexity, while also making it more important that supply chains are shorter to speed product innovations. Food

service companies have been shortening their supply chains in the UK but they have also been adding more local ingredients into their food supply because of a strong demand by consumers for local content. Thus, consumer preferences and demands can act to add complexity even when supply chains are shortening.

Not surprisingly for most industry sectors, high levels of confidence about the ability to deal with external disruptions is accompanied by expectations that supply chains will be shorter and simpler over the next five years. This is true of the consumer staples, consumer discretionary, healthcare, materials, industrials and IT sectors. The energy sector is the exception: respondents from this segment have very high levels of confidence their companies can address disruptions and also generally expect longer supply chains. This is understandable given the nature of extractive industries, where production happens where resources lie.

Consumer preferences for

innovation and products that

are tailored to their needs will

tend to drive complexity, while

also making it more important

that supply chains are shorter

to speed product innovations.

18 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

services to end customers. “On the supply side, getting our partners to digitise operations so they can provide services they offer today and not have a human and not have a manual process to execute against, will bring consistency, speed on the transaction, and a higher level of availability, making it possible for a machine to run more than one eight-hour shift,” John Hayduk, chief operating officer at Tata Communications, says.

Tata Communications has taken steps to automate parts of its business it controls internally. “Now the company is taking a bigger step to bring those same benefits to the company as a whole,” according to Mr Hayduk. Achieving that goal requires creating an automated flow with its partners employing standardised software. The company has completed the model for how it will accomplish this goal with its partners and will begin execution next year. Mr Hayduk expects that major partners will be able to complete the digitisation project within the next two years.

Enhancing sustainability Improving supply-chain sustainability also strengthens it against challenges and disruptions. To deal with regulations and sustainability, more than four-in-ten (42%) respondents report their companies are increasing their monitoring capabilities or the frequency of monitoring. By a similar margin (40%) companies plan to consolidate their supplier base and increase automation. Such actions would tend to shorten the length of the supply chain and reduce its complexity.

Important clues about why many respondents expect to see shorter and simpler supply chains are found in their strategic objectives over the next five years. They suggest businesses are seeking greater, more centralised control over their supply chains.

Digitise, digitise, digitise! American writer Henry David Thoreau once said famously: “Our life is frittered away by detail. Simplify, simplify, simplify!” Today’s supply-chain operator would agree but would probably suggest replacing simplify with digitise.

When respondents were asked to rank the objectives that are likely to be the most important over the next five years, more than half of respondents (55%) said digitising most aspects of supply-chain management. Nearly as many (54%) cited achieving complete transparency about where and how all products are sourced.

The strategic future of supply chains, at least over the next five years, entails not only making supply chains shorter to reduce complexity, but also digitising the information generated to enhance understanding about production across the supplier network. Doing this would make them transparent.

Digitisation and automation are critical to the future of the supply chain that delivers services to customers at Tata Communications, a global provider of telecommunication services. The company would like to extend digitisation to major partners who deliver

19© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

Therefore, it should be no surprise that more than a third (36%) of companies identify supply-chain sustainability as a strategic focus. This is the case, in part, because more than one third (36%) also see regulations governing sustainability adding to the cost and complexity of the company’s supply chain management.

A substantial share of respondents (38%) report that the companies plan to take steps to raise social and environmental standards in the supply chain. Similarly, more than a third (36%) plan to increase supplier audits and 32% plan to create a supplier code of conduct.

More than a third (35%) say that social and environmental impact of the supply chain is just as important as compliance with standards. A similar share (35%) say that regulations will improve social and environmental standards for their company’s supply chain.

Improving sustainability, however, faces challenges. A significant share of respondents (28%) agree or strongly agree that complexity is preventing their company’s supply chain from becoming more sustainable. Respondents also see a downside to complying with regulations. Nearly a third (32%) strongly agree with the statement that regulations will make it more difficult for their company to achieve greater supply-chain efficiency. n

20 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

TREASURY: SUPPLY-CHAIN LEADER5their companies have developed mitigation plans to deal with disruptions. Risk management, in fact, is identified by 68% of executives in the survey as an important skill for managing their supply chain over the next five years, more than any other factor. In addition, 63% say monitoring corporate cash flow will be important for strategic supply-chain management in five years.

So, business leaders are encouraging collaboration between operations and finance teams to reduce the impact of near-term supply-chain disruptions, and they see strategic needs for more risk management and cash and liquidity management skills in the future.

Can treasury lead the way? However, when respondents were asked about treasury’s role in managing supply chains more strategically over the next five years, the top three choices were traditional in scope: oversee cost management (47%), optimise working capital (47%) and monitor liquidity and risk management (43%).

Less than a third of respondents (31%) thought treasury would be regularly collaborating with business heads, despite the importance of its skill sets. Also, only 28% of executives thought treasury would be leading a financial supply chain team in the organisation and 19%

The future needs of supply-chain managers will require a much more cross-functional approach. The days of supply chains being run only by the COO’s office or by engineers and logisticians appear to be fading. Instead a highly collaborative model is emerging.

Yet, business leaders need to enable the role of treasury when it comes to supply-chain management and think beyond the traditional role that treasurers play in the organisation. Treasury may even need to lead some supply chains.

To reduce the fallout from disruptions, 42% of respondents say that their companies have increased collaboration among internal teams, such as finance and risk management. In addition, one third of executives surveyed say

The days of supply chains

being run only by the COO’s

office or by engineers and

logisticians appear to be fading.

Instead a highly collaborative

model is emerging.

21© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

thought treasury would be a part of an executive committee or equivalent.

Business leaders clearly see a growing need for the expertise of treasury when it comes to the future of supply chains, but their vision of treasury’s role seems limited and stricken with unrealised potential.

Looking more closely at the data and some industries are more likely than others to empower the treasury function. For example, 41% of respondents in the energy industry say in five years treasurers will be collaborating with

business heads on supply-chain management, compared with 31% of overall respondents. A third of respondents in the IT industry see treasury joining executive committees in five years, a much greater share than the 19% of overall respondents.

Furthermore, respondents who described innovation as being “very important” to their company’s supply-chain management were much more likely to be empowering their treasury function vs the overall pool of respondents. According to this cohort, in five years, treasury would be collaborating with business heads (40%

47%

31%

47%

43%

28%

19%

Oversee costmanagement

Optimise workingcapital

Monitor liquidityand risk

Collaborate withbusiness heads

Lead a �nancialsupply team

Member ofexecutive committee

Figure 8. Treasurers seen handling cost controls, working capital in future of supply chains % respondents, expectations for treasurer’s role in supply-chain management over next five years

22 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

that data analytics and systems management – traditionally a role of IT departments – is an important skill for strategic management of sourcing networks.

Many companies have been upgrading legacy data management systems and consolidating platforms over the past several years. The survey showed that over the past 2-3 years, more than a third of businesses (37%) have deployed data analytics platforms to manage cash flows, liquidity and payments. Given that this is a critical strategic area for supply-chain management, it is surprising that more businesses have not already introduced these solutions.

Fewer respondents have deployed other technologies, including supply chain finance platforms (29%), cloud-based customer and supplier platforms (27%), social media-based communication tools (26%), mobile payment systems (21%) and blockchain or XML-based payment platforms (15%).

Businesses see the importance of liquidity and risk management in the future, but they have not yet deployed a solution to monitor areas such as cash flows, payments and risk exposures, and they may need to play catchup. n

vs 24% overall), leading financial supply chain teams (36% vs 30% overall) and serving on an executive committee (25% vs 19% overall).

Some businesses are ready to enable their treasurers to take a leadership role when it comes to supply chains. Are treasurers ready for the role?

Sander de Vries, manager at Zanders, Treasury and Finance Solutions in The Netherlands, believes so. Treasury can play a leading role in the implementation of financial supply chain management strategies that work hand in glove with the physical supply chain management, he says. Treasury’s value-add would be to reduce the overall financing cost for the supply chain, at a time when reducing costs are paramount, according to the survey findings.

The treasury department can manage risks and increase efficiencies. For example, treasury can streamline purchase-to-pay, as well as order-to-cash processes. Such steps can both improve the functioning of the supply chain and reduce its overall costs. “The treasury department has expertise and knowledge on the dynamics between operational risk and financial risk. It also knows how to quantify different kinds of risk and to handle those risks,” Mr de Vries says.

Skills for the future In addition to risk management and cash and liquidity management, respondents also see data management increasing in importance for supply chains. Overall, 62% of respondents think

23© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

24 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

CONCLUSION6This study has argued that the future of supply chains will entail shorter though not always simpler production links. The future will require a varied collection of skills that include risk management, cash and liquidity management, data analytics and systems management among others. It will require transparency to meet demands of regulators and senior executives, and digitisation of information across the supply chain.

The stakes are high. The role of treasurers and others on company financial and risk management teams are likely to become important to the management of the supply chain, and being able to conceive of these roles in an innovative way will be a competitive advantage. Ultimately collaboration and innovation will make supply chains efficient, more reliable, more flexible and more durable. n

Donald Rumsfeld, former US secretary of defense, in a moment of obfuscation once said to the media: “There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.” It’s the unknown unknowns that have businesses encouraging greater internal collaboration between teams to reduce the risk to their supply chains.

Geopolitical uncertainty and political risk are rising and supply chains could be in for some shocks. However, companies have been stepping up their ability to mitigate disruptions and meet ever-intensifying competitive pressures from consumers and customers demanding greater levels of product differentiation.

Managing a supply chain is a never-ending, constantly changing, demanding challenge that requires clear thinking and sharp vision. One needs to be prepared even for the unthinkable, at least on some level. It is a network that, when necessary, can hum with more activity and intensity than even the busiest bee hives. With so many moving parts and each so vulnerable to so many unexpected disruptions, it is amazing supply chains work relatively well for so many companies.

26 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

APPENDIX

A1. In what region of the world is your organisation headquartered?

A2. Which of the following best describes your company’s primary sector?

A3. Which of the following best describes your function in your company?

0 50 100 150 200 250

Asia Paci�c

North America

Europe

135

140

247

0% 5% 10% 15% 20% 25%

Energy

Materials

Healthcare

Industrials

Consumer discretionary

Information technology

Consumer staples

19%

19%

19%

12%

11%

10%

10%

0% 10% 20% 30% 40% 50%

Finance

Strategy and business development

Supply-chain management

Procurement

28%

24%

24%

24%

27© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

A4. Which of the following best describes your title?

0% 5% 10% 15% 20% 25%

24%

15%

14%

11%

10%

5%

4%

4%

3%

3%

3%

2%

2%

Manager

Head of department

CEO

Other c-level executive

Board member

Head of business unit

CFO

COO

SVP, VP, director

Assistant manager

CIO/Technology director

CMO

Treasurer/Comptroller

0% 10% 20% 30% 40% 50%

50%

42%

36%

35%

27%

26%

25%

24%

22%

22%

21%

21%

20%

Reducing operating cost

Increase sales growth

Improving customer service

Improving quality of products & services

Form more strategic partnerships with suppliers

Reduce overall inventory levels

Introduce new products to market more quickly

Reduce vulnerability to external risks

Expand capacity of suppliers of distributors/re-sellers to support my company

Digitise some or all supply-chain information

Expand internationally

Make the supply chain more socially and environmentally responsible

Hire new talent to manage the supply chain

0% 10% 20% 30% 40% 50%

Less than $50m

$50m to $500m

$500m to $1bn

$1bn to less than $10bn

More than $10bn

29%

23%

19%

17%

12%

A5. What are your organisation’s total annual revenues in US dollars?

B1. Which of the following answers best describes the main objectives that you have for your supply chain over the next 12 months?

28 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

B2. What is/are the most significant challenges to achieving the objectives that you chose in the previous question?

B3. Rate the following external factors according to how disruptive they could be to your supply chain over the next 12 months.

B4. How confident are you that your company is prepared to address the external disruptions in the previous question?

0% 10% 20% 30% 40% 50%

Difficulty controlling costsMeeting customers’ expectation on product quality & service

Increasing pressure from global competitionGrowing regulations

Need for faster production timesPolitical uncertainties in markets where your company operates

Lack of visibility on demand/volatile demandIncreasing financial volatility (ie currency fluctuation, etc)Lack of transparency with suppliers beyond first tier

Complying with sustainability rulesWeak distribution / re-seller network

Difficulty accessing finance for suppliersNatural disasters

Pressure to re-shore jobsOther, please specify

34% 31% 30% 25% 24% 20% 20% 19% 16% 16% 16% 13% 11% 9% 1%

Changing trade policies among nations

Increase in extreme weather events

Cyber attacks

Increasing worries about product safety

Rise of protectionist sentiment

Political instability

Failure of �rst-tier suppliers to �nd reliable sub-tier suppliers

Fluctuating commodity prices

Technological change

Competitive pressures that speed up product innovations

0% 20% 40% 60% 80% 100%

Not disruptive 2 3 4 Very disruptive

7% 16% 38% 29% 10%

8% 20% 35% 27% 10%

8% 16% 29% 34% 13%

10% 19% 35% 24% 12%

11% 17% 32% 29% 12%

11% 18% 35% 25% 10%

12% 19% 34% 26% 9%

13% 19% 33% 21% 14%

16% 20% 32% 20% 11%

16% 14% 33% 24% 14%

Con�dence

0% 20% 40% 60% 80% 100%

32% 61% 5% 2%

Very con�dent Somewhat con�dent Not con�dent I don't know

29© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

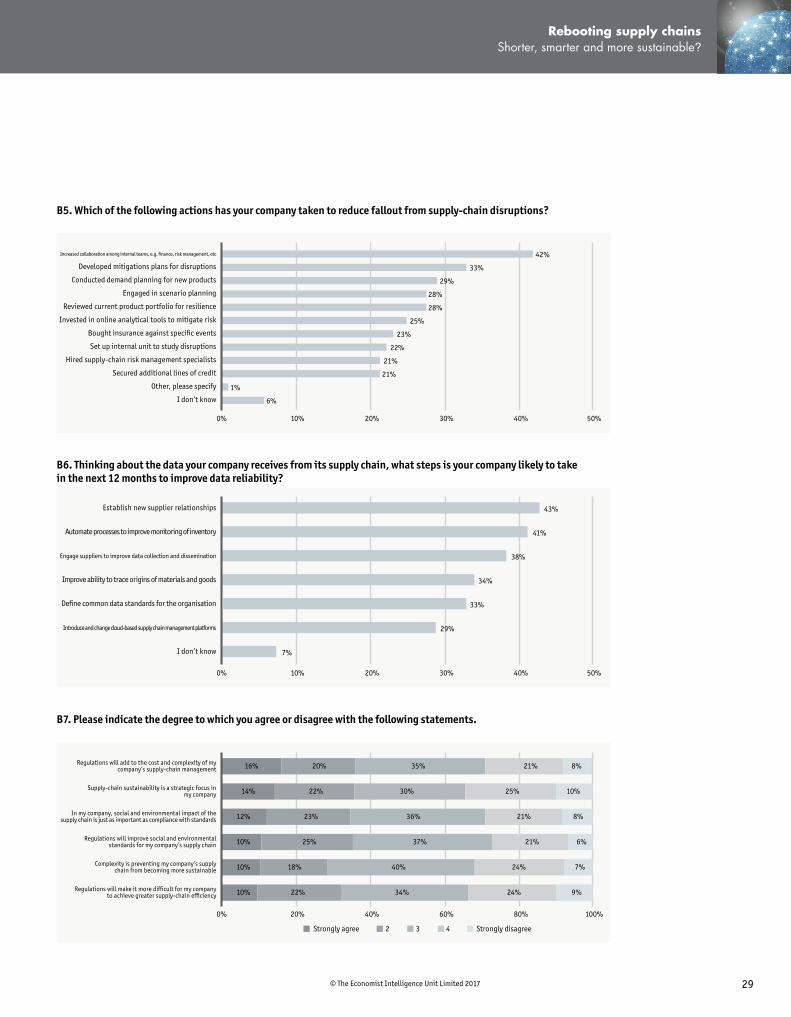

B5. Which of the following actions has your company taken to reduce fallout from supply-chain disruptions?

42%

33%

29%

28%

28%

25%

23%

22%

21%

21%

1%

6%

0% 10% 20% 30% 40% 50%

Increased collaboration among internal teams, e.g. �nance, risk management, etc

Developed mitigations plans for disruptions

Conducted demand planning for new products

Engaged in scenario planning

Reviewed current product portfolio for resilience

Invested in online analytical tools to mitigate risk

Bought insurance against speci�c events

Set up internal unit to study disruptions

Hired supply-chain risk management specialists

Secured additional lines of credit

Other, please specify

I don’t know

0% 20% 40% 60% 80% 100%

Strongly agree 2 3 4 Strongly disagree

Regulations will add to the cost and complexity of mycompany’s supply-chain management

Supply-chain sustainability is a strategic focus inmy company

In my company, social and environmental impact of thesupply chain is just as important as compliance with standards

Regulations will improve social and environmentalstandards for my company’s supply chain

Complexity is preventing my company’s supplychain from becoming more sustainable

Regulations will make it more dif�cult for my companyto achieve greater supply-chain ef�ciency

16% 20% 35% 21% 8%

14% 22% 30% 25% 10%

12% 23% 36% 21% 8%

10% 25% 37% 21% 6%

10% 18% 40% 24% 7%

10% 22% 34% 24% 9%

0% 10% 20% 30% 40% 50%

Establish new supplier relationships

Automate processes to improve monitoring of inventory

Engage suppliers to improve data collection and dissemination

Improve ability to trace origins of materials and goods

De�ne common data standards for the organisation

Introduce and change cloud-based supply chain management platforms

I don’t know

43%

41%

38%

34%

33%

29%

7%

B6. Thinking about the data your company receives from its supply chain, what steps is your company likely to take in the next 12 months to improve data reliability?

B7. Please indicate the degree to which you agree or disagree with the following statements.

30 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

B8. With regard to regulations and sustainability, which of the following steps has your company taken or do you expect it to take in the next 12 months?

C1. Please describe the importance of innovation when it comes to supply-chain management in your company.

C2. Which of the following has your company deployed in the past two-to-three years as solutions to managing cash flows, liquidity and payments and to identifying and analysing risks?

0% 10% 20% 30% 40% 50%

Increase monitoring capabilities and/or frequency

Consolidate supplier base

Increase automation of processes

Raise social and environmental standards in the supply chain

Increase supplier audits

Create a supplier code of conduct

Expand corporate social responsibility and/or public relations teams

Other, please specify

42%

40%

40%

38%

36%

32%

25%

1%

Very important Somewhat important Not important I don’t know

Importance

0% 20% 40% 60% 80% 100%

49% 44% 6% 2%

0% 10% 20% 30% 40% 50%

Data analytics/forecasting platforms

Enterprise resource planning software

Treasury and risk management systems

Supply-chain �nance platform

Treasury management systems

Cloud-based customer/supplier platforms

Social media-based communication tools

Mobile payment systems

Block chain or XML-based payment platforms

Other, please specify

I don’t know

37%

34%

29%

29%

28%

27%

26%

21%

15%

1%

10%

31© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

C3. Thinking of your answer(s) to the previous question, how confident are you in your company’s ability to apply those solutions to the challenges specifically faced by supply-chain managers?

Very con�dent Somewhat con�dent Not con�dent I don’t know

Con�dence

0% 20% 40% 60% 80% 100%

35% 56% 5% 4%

Expectation

0% 20% 40% 60% 80% 100%

33% 49% 15% 3%

Lengthen and become more complex Shorten and become more simple Stay the same I don’t know

0% 10% 20% 30% 40% 50%

Improve supply chain visibility

Contingency plans to deal with disruptions

Managing payments to suppliers

Optimising working capital

Quicker receivable collections

Digitising supply-chain transactions

Procure-to-pay technology

Supply-chain �nance platforms

Dynamic discounting

Other, please specify

I don’t know

39%

36%

32%

31%

30%

29%

27%

21%

16%

1%

4%

C4. In which areas do you see the greatest need for innovation when it comes to strategically managing your company’s supply chain?

D1. Over the next five years, I expect my company’s supply chain to

32 © The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

D2. Looking at the next five years, rank the following objectives based on how important they will be for your company?

D3. In the previous question, you answered that improving social and cultural diversity in first-tier suppliers will not be an important objective for your company over the next five years. Choose the most relevant reasons why among the choices below.

D4. Thinking of managing both physical and financial supply chains more strategically, what roles do you anticipate treasury will play over the next five years?

Not important 2 3 4 Very important

0% 20% 40% 60% 80% 100%

Co-create products with suppliers

Establish �nancial incentive programmes with suppliersto improve quality standards

Improve social and cultural diversity in �rst-tier suppliers

Reduce the environmental impact of my company’ssupply chain

Holistically manage physical and �nancial supply chains

Achieve complete transparency about where and howall products are sourced

Digitise most aspects of supply-chain management

7% 11% 34% 34% 14%

6% 13% 34% 32% 14%

4% 14% 35% 31% 16%

4% 16% 34% 32% 14%

4% 9% 38% 33% 16%

3% 11% 32% 34% 20%

2% 8% 35% 34% 21%

0% 10% 20% 30% 40% 50%

My company's executive leadership is focused onother priorities

My company has already focused a lot on socialand cultural diversity in its supply chain

Social and cultural diversity is too dif�cult tomonitor in our supply chain

Other, please specify

44%

42%

12%

2%

0% 10% 20% 30% 40% 50%

Oversee cost management

Optimise working capital

Monitor liquidity and risk management

Regularly collaborate with heads of businesses

Lead a �nancial supply chain team

Become member of the executive committee or equivalent

I don’t know

47%

47%

43%

31%

28%

19%

8%

33© The Economist Intelligence Unit Limited 2017

Rebooting supply chains Shorter, smarter and more sustainable?

D5. Rank the following skills by how important they will be in five years to managing your company’s supply chain more strategically.

Not important 2 3 4 Very important

0% 20% 40% 60% 80% 100%

Ability to collaborate with finance teams

Product innovation

Leadership on social and environmental standards

Risk management

Data analytics and systems management

Ability to form and direct corporate strategy

Monitor corporate cash flow and liquidity

3% 7% 30% 39% 20%

3% 11% 24% 38% 24%

2% 11% 37% 30% 20%

2% 8% 33% 36% 21%

1% 6% 29% 38% 25%

2% 5% 25% 42% 26%

2% 7% 29% 36% 26%

LONDON 20 Cabot Square London E14 4QW United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

NEW YORK 750 Third Avenue 5th Floor New York, NY 10017, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected] HONG KONG 1301 Cityplaza Four 12 Taikoo Wan Road Taikoo Shing Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

SINGAPORE 8 Cross Street #23-01 PWC Building Singapore 048424 Tel: (65) 6534 5177 Fax: (65) 6428 2630 E-mail: [email protected]

GENEVA Rue de l’Athénée 32 1206 Geneva Switzerland Tel: (41) 22 566 2470 Fax: (41) 22 346 9347 E-mail: [email protected]

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out herein.