Embed Size (px)

Citation preview

A REVIEW OF BUILDING ENERGY EFFICIENCY DEVELOPMENT

IN INDONESIA

By Lee Siew Eang

January 2015

1

1.0 Overview

Indonesia is an archipelago comprising 17,500 islands and lies between latitudes 11°S and 6°N,

and longitudes 95°E and 141°E. It is therefore a tropical countries spreading on the both sides of

the equator. It has a population of 252million, the 4th most populous nation in the world. 58% of

its population lives in Java Island, making it the most populous island in the world.

Indonesia has a mixed economy where both the private and public sectors play significant roles.

It is the largest economy in Southeast Asia and a member of the G-20 major economies.

Indonesia's estimated gross domestic product (nominal), as of 2012 was US$928.274 billion with

estimated nominal per capita GDP was US$3,797, and per capita GDP PPP was US$4,943

(international dollars)[1]. According to World Bank affiliated report based on 2011 data, the

Indonesian economy was the world's 10th largest by nominal GDP (PPP based), with the country

contributing 2.3 percent of global economic output. The industry sector is the economy's largest

and accounts for 46.4% of GDP (2012), this is followed by services (38.6%) and agriculture (14.4%).

According to the South East Asia Energy Outlook 2013[2], a status report prepared by the

International Energy Agency (IEA), Indonesia is South East Asia’s largest energy consumer

consuming 36% of the total primary energy consumed in South East Asia in 2011. Indonesia is a

net importer of oil, but the world’s top exporter of steam coal, and a major supplier of Liquefied

Natural Gas (LNG). As the world largest archipelago and a developing economy, it is indeed a

challenge to provide modern energy infrastructure to the entire country. Hence, 27% of its

population lack access to electricity. This has partly contributed to its low per-capita consumption

of energy, at around 20% of OECD’s average currently.

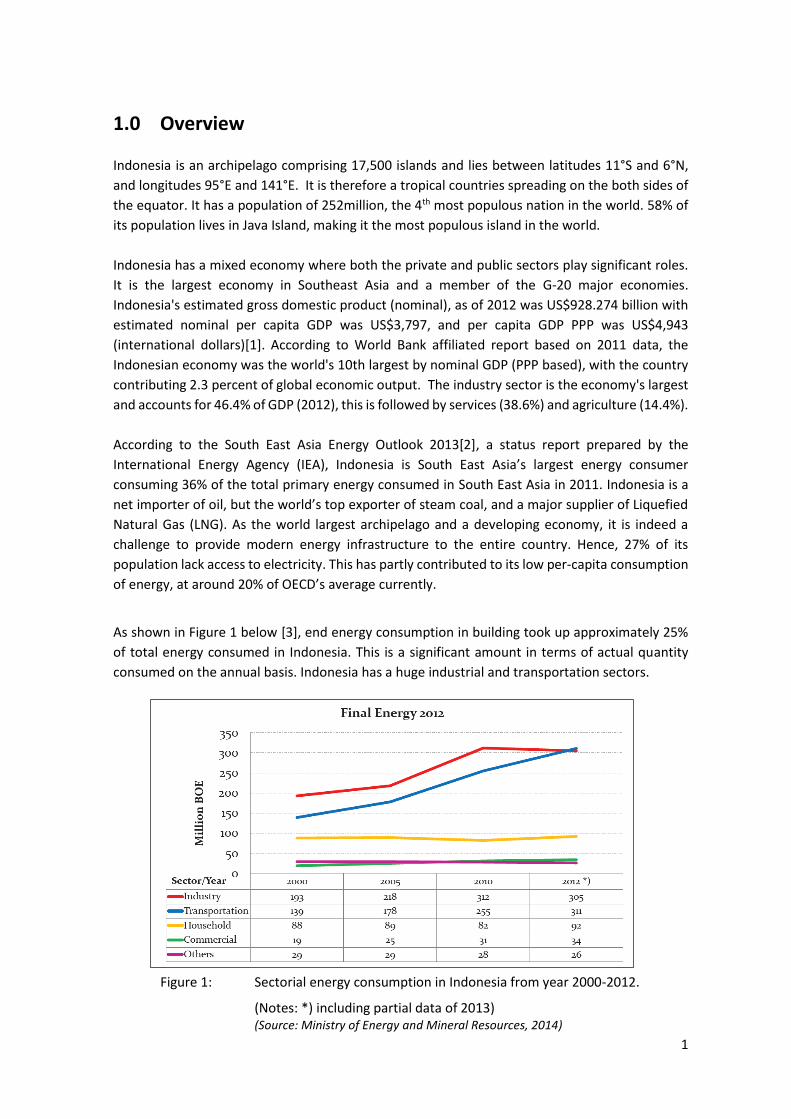

As shown in Figure 1 below [3], end energy consumption in building took up approximately 25%

of total energy consumed in Indonesia. This is a significant amount in terms of actual quantity

consumed on the annual basis. Indonesia has a huge industrial and transportation sectors.

Figure 1: Sectorial energy consumption in Indonesia from year 2000-2012.

(Notes: *) including partial data of 2013) (Source: Ministry of Energy and Mineral Resources, 2014)

2

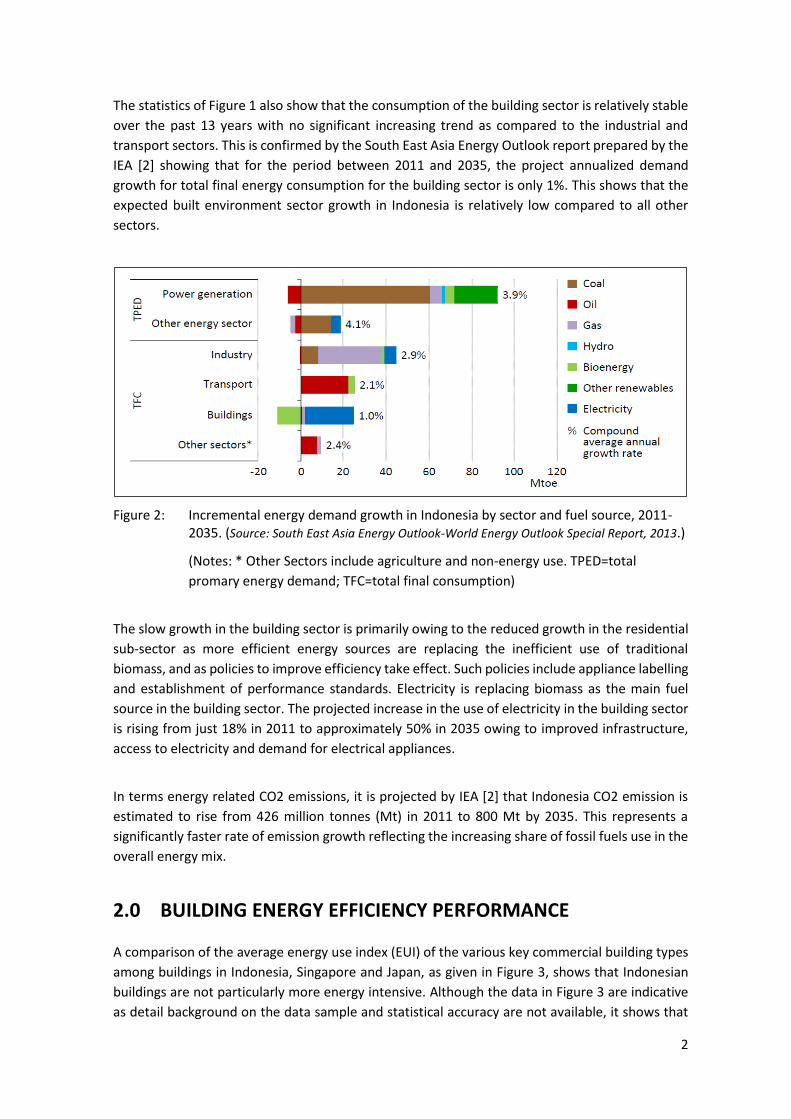

The statistics of Figure 1 also show that the consumption of the building sector is relatively stable

over the past 13 years with no significant increasing trend as compared to the industrial and

transport sectors. This is confirmed by the South East Asia Energy Outlook report prepared by the

IEA [2] showing that for the period between 2011 and 2035, the project annualized demand

growth for total final energy consumption for the building sector is only 1%. This shows that the

expected built environment sector growth in Indonesia is relatively low compared to all other

sectors.

Figure 2: Incremental energy demand growth in Indonesia by sector and fuel source, 2011-2035. (Source: South East Asia Energy Outlook-World Energy Outlook Special Report, 2013.)

(Notes: * Other Sectors include agriculture and non-energy use. TPED=total

promary energy demand; TFC=total final consumption)

The slow growth in the building sector is primarily owing to the reduced growth in the residential

sub-sector as more efficient energy sources are replacing the inefficient use of traditional

biomass, and as policies to improve efficiency take effect. Such policies include appliance labelling

and establishment of performance standards. Electricity is replacing biomass as the main fuel

source in the building sector. The projected increase in the use of electricity in the building sector

is rising from just 18% in 2011 to approximately 50% in 2035 owing to improved infrastructure,

access to electricity and demand for electrical appliances.

In terms energy related CO2 emissions, it is projected by IEA [2] that Indonesia CO2 emission is

estimated to rise from 426 million tonnes (Mt) in 2011 to 800 Mt by 2035. This represents a

significantly faster rate of emission growth reflecting the increasing share of fossil fuels use in the

overall energy mix.

2.0 BUILDING ENERGY EFFICIENCY PERFORMANCE

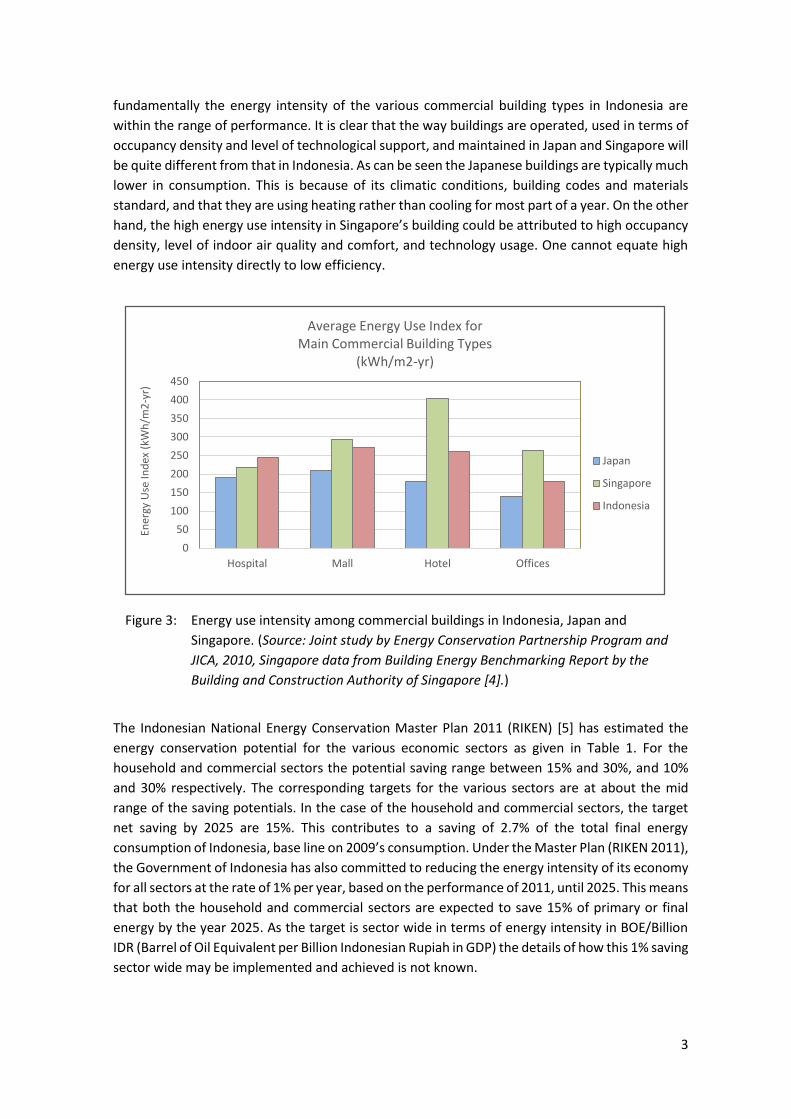

A comparison of the average energy use index (EUI) of the various key commercial building types

among buildings in Indonesia, Singapore and Japan, as given in Figure 3, shows that Indonesian

buildings are not particularly more energy intensive. Although the data in Figure 3 are indicative

as detail background on the data sample and statistical accuracy are not available, it shows that

3

fundamentally the energy intensity of the various commercial building types in Indonesia are

within the range of performance. It is clear that the way buildings are operated, used in terms of

occupancy density and level of technological support, and maintained in Japan and Singapore will

be quite different from that in Indonesia. As can be seen the Japanese buildings are typically much

lower in consumption. This is because of its climatic conditions, building codes and materials

standard, and that they are using heating rather than cooling for most part of a year. On the other

hand, the high energy use intensity in Singapore’s building could be attributed to high occupancy

density, level of indoor air quality and comfort, and technology usage. One cannot equate high

energy use intensity directly to low efficiency.

Figure 3: Energy use intensity among commercial buildings in Indonesia, Japan and

Singapore. (Source: Joint study by Energy Conservation Partnership Program and

JICA, 2010, Singapore data from Building Energy Benchmarking Report by the

Building and Construction Authority of Singapore [4].)

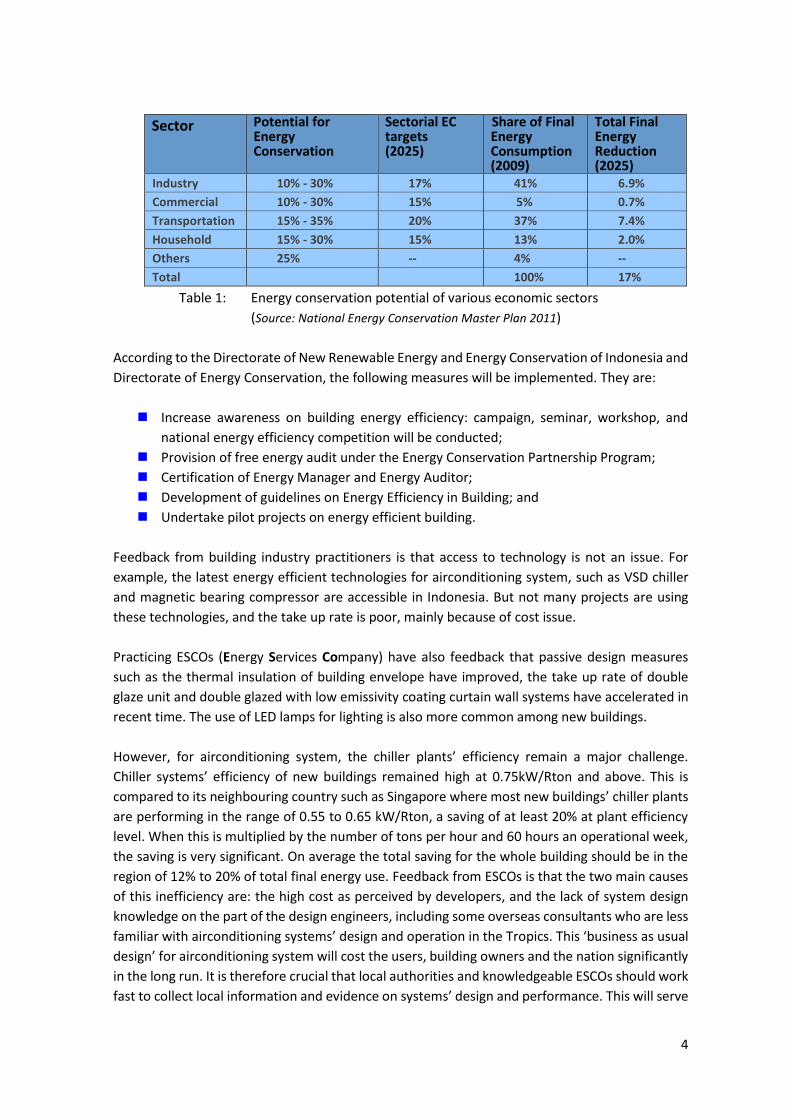

The Indonesian National Energy Conservation Master Plan 2011 (RIKEN) [5] has estimated the

energy conservation potential for the various economic sectors as given in Table 1. For the

household and commercial sectors the potential saving range between 15% and 30%, and 10%

and 30% respectively. The corresponding targets for the various sectors are at about the mid

range of the saving potentials. In the case of the household and commercial sectors, the target

net saving by 2025 are 15%. This contributes to a saving of 2.7% of the total final energy

consumption of Indonesia, base line on 2009’s consumption. Under the Master Plan (RIKEN 2011),

the Government of Indonesia has also committed to reducing the energy intensity of its economy

for all sectors at the rate of 1% per year, based on the performance of 2011, until 2025. This means

that both the household and commercial sectors are expected to save 15% of primary or final

energy by the year 2025. As the target is sector wide in terms of energy intensity in BOE/Billion

IDR (Barrel of Oil Equivalent per Billion Indonesian Rupiah in GDP) the details of how this 1% saving

sector wide may be implemented and achieved is not known.

0

50

100

150

200

250

300

350

400

450

Hospital Mall Hotel Offices

Ener

gy U

se In

dex

(kW

h/m

2-y

r)

Average Energy Use Index for Main Commercial Building Types

(kWh/m2-yr)

Japan

Singapore

Indonesia

4

Sector Potential for Energy Conservation

Sectorial EC targets (2025)

Share of Final Energy Consumption (2009)

Total Final Energy Reduction (2025)

Industry 10% - 30% 17% 41% 6.9%

Commercial 10% - 30% 15% 5% 0.7%

Transportation 15% - 35% 20% 37% 7.4%

Household 15% - 30% 15% 13% 2.0%

Others 25% -- 4% --

Total 100% 17%

Table 1: Energy conservation potential of various economic sectors

(Source: National Energy Conservation Master Plan 2011)

According to the Directorate of New Renewable Energy and Energy Conservation of Indonesia and

Directorate of Energy Conservation, the following measures will be implemented. They are:

Increase awareness on building energy efficiency: campaign, seminar, workshop, and

national energy efficiency competition will be conducted;

Provision of free energy audit under the Energy Conservation Partnership Program;

Certification of Energy Manager and Energy Auditor;

Development of guidelines on Energy Efficiency in Building; and

Undertake pilot projects on energy efficient building.

Feedback from building industry practitioners is that access to technology is not an issue. For

example, the latest energy efficient technologies for airconditioning system, such as VSD chiller

and magnetic bearing compressor are accessible in Indonesia. But not many projects are using

these technologies, and the take up rate is poor, mainly because of cost issue.

Practicing ESCOs (Energy Services Company) have also feedback that passive design measures

such as the thermal insulation of building envelope have improved, the take up rate of double

glaze unit and double glazed with low emissivity coating curtain wall systems have accelerated in

recent time. The use of LED lamps for lighting is also more common among new buildings.

However, for airconditioning system, the chiller plants’ efficiency remain a major challenge.

Chiller systems’ efficiency of new buildings remained high at 0.75kW/Rton and above. This is

compared to its neighbouring country such as Singapore where most new buildings’ chiller plants

are performing in the range of 0.55 to 0.65 kW/Rton, a saving of at least 20% at plant efficiency

level. When this is multiplied by the number of tons per hour and 60 hours an operational week,

the saving is very significant. On average the total saving for the whole building should be in the

region of 12% to 20% of total final energy use. Feedback from ESCOs is that the two main causes

of this inefficiency are: the high cost as perceived by developers, and the lack of system design

knowledge on the part of the design engineers, including some overseas consultants who are less

familiar with airconditioning systems’ design and operation in the Tropics. This ‘business as usual

design’ for airconditioning system will cost the users, building owners and the nation significantly

in the long run. It is therefore crucial that local authorities and knowledgeable ESCOs should work

fast to collect local information and evidence on systems’ design and performance. This will serve

5

to build a business case for justifying an energy efficient airconditioning system, and provide

appropriate training for the local developers and design and professionals.

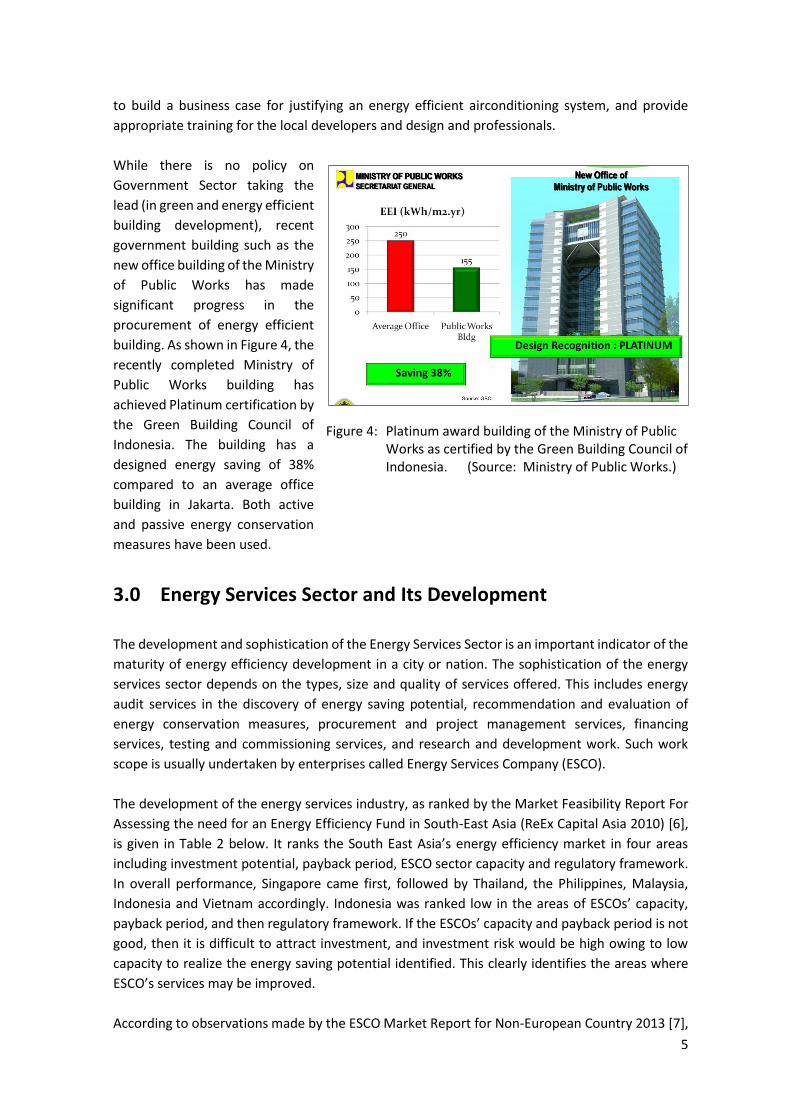

While there is no policy on

Government Sector taking the

lead (in green and energy efficient

building development), recent

government building such as the

new office building of the Ministry

of Public Works has made

significant progress in the

procurement of energy efficient

building. As shown in Figure 4, the

recently completed Ministry of

Public Works building has

achieved Platinum certification by

the Green Building Council of

Indonesia. The building has a

designed energy saving of 38%

compared to an average office

building in Jakarta. Both active

and passive energy conservation

measures have been used.

3.0 Energy Services Sector and Its Development

The development and sophistication of the Energy Services Sector is an important indicator of the

maturity of energy efficiency development in a city or nation. The sophistication of the energy

services sector depends on the types, size and quality of services offered. This includes energy

audit services in the discovery of energy saving potential, recommendation and evaluation of

energy conservation measures, procurement and project management services, financing

services, testing and commissioning services, and research and development work. Such work

scope is usually undertaken by enterprises called Energy Services Company (ESCO).

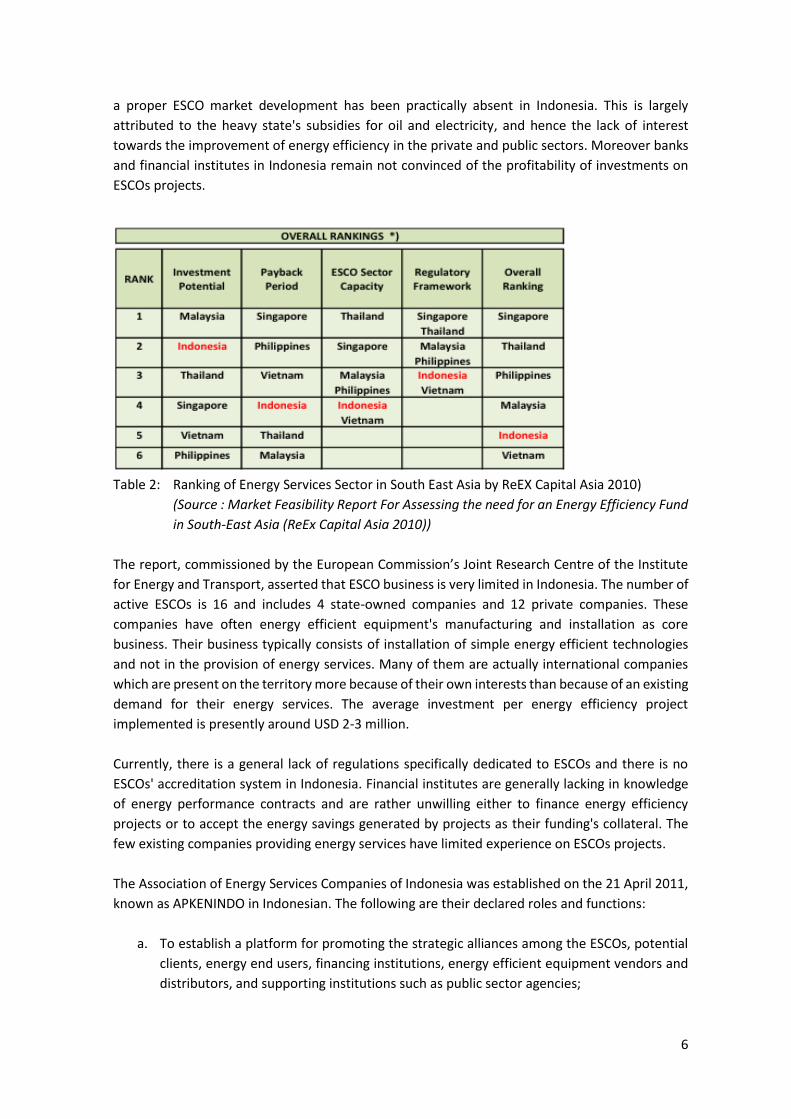

The development of the energy services industry, as ranked by the Market Feasibility Report For

Assessing the need for an Energy Efficiency Fund in South-East Asia (ReEx Capital Asia 2010) [6],

is given in Table 2 below. It ranks the South East Asia’s energy efficiency market in four areas

including investment potential, payback period, ESCO sector capacity and regulatory framework.

In overall performance, Singapore came first, followed by Thailand, the Philippines, Malaysia,

Indonesia and Vietnam accordingly. Indonesia was ranked low in the areas of ESCOs’ capacity,

payback period, and then regulatory framework. If the ESCOs’ capacity and payback period is not

good, then it is difficult to attract investment, and investment risk would be high owing to low

capacity to realize the energy saving potential identified. This clearly identifies the areas where

ESCO’s services may be improved.

According to observations made by the ESCO Market Report for Non-European Country 2013 [7],

Figure 4: Platinum award building of the Ministry of Public Works as certified by the Green Building Council of Indonesia. (Source: Ministry of Public Works.)

6

a proper ESCO market development has been practically absent in Indonesia. This is largely

attributed to the heavy state's subsidies for oil and electricity, and hence the lack of interest

towards the improvement of energy efficiency in the private and public sectors. Moreover banks

and financial institutes in Indonesia remain not convinced of the profitability of investments on

ESCOs projects.

Table 2: Ranking of Energy Services Sector in South East Asia by ReEX Capital Asia 2010)

(Source : Market Feasibility Report For Assessing the need for an Energy Efficiency Fund

in South-East Asia (ReEx Capital Asia 2010))

The report, commissioned by the European Commission’s Joint Research Centre of the Institute

for Energy and Transport, asserted that ESCO business is very limited in Indonesia. The number of

active ESCOs is 16 and includes 4 state-owned companies and 12 private companies. These

companies have often energy efficient equipment's manufacturing and installation as core

business. Their business typically consists of installation of simple energy efficient technologies

and not in the provision of energy services. Many of them are actually international companies

which are present on the territory more because of their own interests than because of an existing

demand for their energy services. The average investment per energy efficiency project

implemented is presently around USD 2-3 million.

Currently, there is a general lack of regulations specifically dedicated to ESCOs and there is no

ESCOs' accreditation system in Indonesia. Financial institutes are generally lacking in knowledge

of energy performance contracts and are rather unwilling either to finance energy efficiency

projects or to accept the energy savings generated by projects as their funding's collateral. The

few existing companies providing energy services have limited experience on ESCOs projects.

The Association of Energy Services Companies of Indonesia was established on the 21 April 2011,

known as APKENINDO in Indonesian. The following are their declared roles and functions:

a. To establish a platform for promoting the strategic alliances among the ESCOs, potential

clients, energy end users, financing institutions, energy efficient equipment vendors and

distributors, and supporting institutions such as public sector agencies;

7

b. Strengthen the offering of ESCOs through the establishment of a special fund serving as a

clean energy financing option; the establishment of a financing mechanism that will allow

ESCOs to bundle several projects and reduce transaction costs;

c. Support members in developing energy efficiency project by: offering technical

assistance; assist in establishing contacts and negotiations; consolidation of projects’

experience and publicize results; build capacity among ESCOs, and provision of training

programme and seminars.

d. APKENINDO serves to support the Regulators in the promotion and development of the

energy efficiency and services sector, and the development of the regulatory frame-

works.

Currently, there are 16 registered members of this association. From the stated roles and

functions, it can be seen that there is still a great deal of work to be done to bring this sectors to

a level where it can serve the energy efficiency sector of Indonesia effectively. As stated by the

APKENINDO, the lack of development and support for the ESCO industry are caused by several

factors as follows:

i. Lack of regulatory frame works for the ESCO Industry, at multi level stages.

ii. No ESCOs accredited body established in Indonesia, hence the absence of ESCO standard model applied.

iii. Existing ESCOs have limited experience with successful ESCO projects (limited published information).

iv. Limited access to financial resources for Energy Efficiency projects under ESCOs’ performance contract approach.

v. Manufacturers or suppliers of energy efficient technologies are advancing their own “ESCO model” for energy efficiency or clean energy projects. MNC ESCOs are also adopting their own model with its own capitals.

vi. Immature ESCO’s Associations (established in Q1 of 2011) resulted low ESCO capacity.

The statements above show that there will be some structural problems in the development of

the ESCO industry. The APKENINDO might have admitted weak members into its midst and is

trying to develop them. In this way, these weak ESCOs might lead to poor delivery of energy

performance contracts and consequently lead to poor reputation and thereby the lack of

confidence in ESCOs. This is an important issue that requires addressing. If the APKENINDO is

hoping for strong support from the industry and the Government, then its members must be doing

good work.

4.0 Energy Policies, Regulations and Programmes

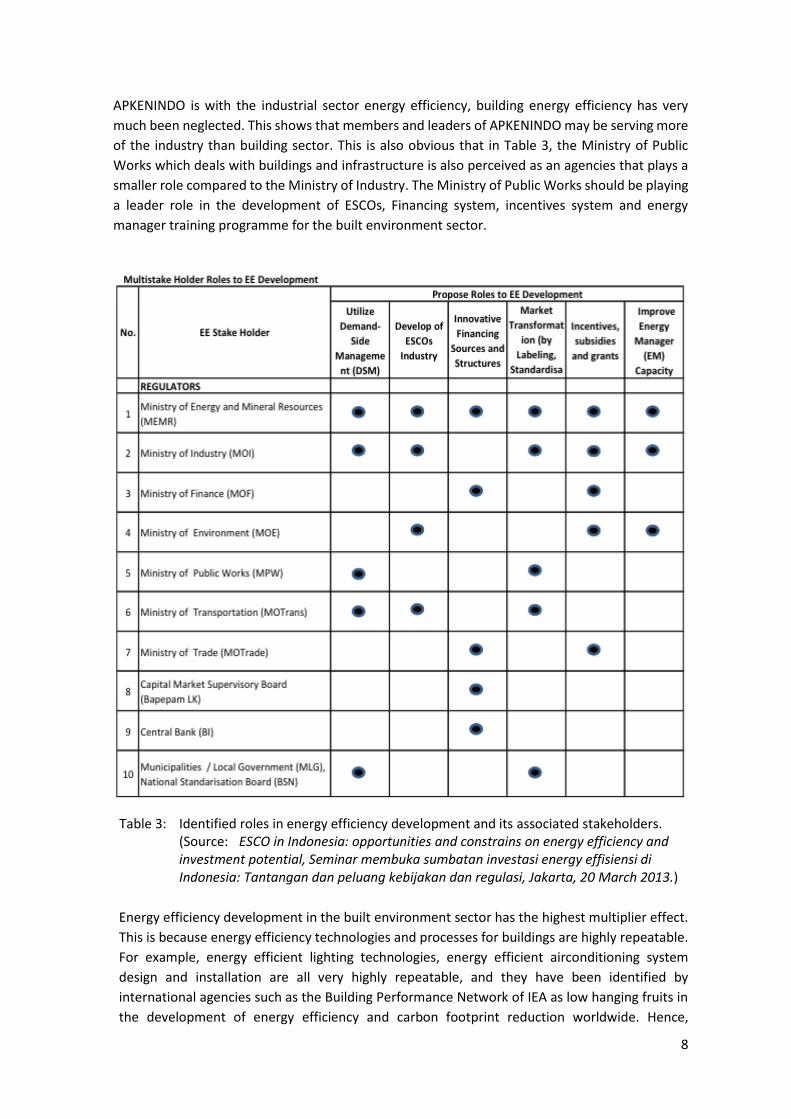

The APKENINDO has identified the various potential programmes for enhancing energy efficiency

development in Indonesia, and the associated stakeholders. This is as shown in Table 3. It can be

seen that the two key agencies as perceived by them are the Ministry for Energy and Mineral

Resources (MEMR), and the Ministry of Industry (MOI). It can be seen that the emphasis of the

8

APKENINDO is with the industrial sector energy efficiency, building energy efficiency has very

much been neglected. This shows that members and leaders of APKENINDO may be serving more

of the industry than building sector. This is also obvious that in Table 3, the Ministry of Public

Works which deals with buildings and infrastructure is also perceived as an agencies that plays a

smaller role compared to the Ministry of Industry. The Ministry of Public Works should be playing

a leader role in the development of ESCOs, Financing system, incentives system and energy

manager training programme for the built environment sector.

Table 3: Identified roles in energy efficiency development and its associated stakeholders. (Source: ESCO in Indonesia: opportunities and constrains on energy efficiency and

investment potential, Seminar membuka sumbatan investasi energy effisiensi di Indonesia: Tantangan dan peluang kebijakan dan regulasi, Jakarta, 20 March 2013.)

Energy efficiency development in the built environment sector has the highest multiplier effect.

This is because energy efficiency technologies and processes for buildings are highly repeatable.

For example, energy efficient lighting technologies, energy efficient airconditioning system

design and installation are all very highly repeatable, and they have been identified by

international agencies such as the Building Performance Network of IEA as low hanging fruits in

the development of energy efficiency and carbon footprint reduction worldwide. Hence,

9

although the built environment sector may just consume 18% (sum of commercial sector and the

household sector) of the total final energy of Indonesia, it remains an important sector because

of the repeatability of technologies, and speed at which energy conservation actions may be

implemented and achieved.

The key policies and regulations governing energy conservation actions among the various

sectors of Indonesian economy are as follows:

Law No. 30 / 2007 Concerning ENERGY: Among other things, this law led to the

establishment of the National Energy Council, and the development of the National Energy

Plan and Regional Energy Plan.

Government Regulation No.70/2009 On Energy Conservation: Among various stipulations,

this regulation stipulates that energy consumers which consume 6000TOE and more are

obliged to implement energy management by setting up energy conservation program,

appoint energy manager and implementing energy audit. It provides for the establishment

of standards and labeling programme, and development of incentive and disincentive for

energy consumer and producer of energy saving technology.

Ministry of EMR Regulation No.13 / 2012 on Electricity Consumption Savings: This

regulation requires all Government Buildings, State owned buildings, official residence

(government and state owned), street lighting, decorative lighting and billboards, are

required to save 20% of energy based on the average consumption of the previous six

months.

Ministry of EMR Regulation No.14 / 2012 on Energy Management: This regulation requires

all consumers consuming 6000TOE per year to implement energy management

programme. This programme must comprise the following actions:

a. Appoint energy managers to assist in the implementation of energy management

programme;

b. Design energy conservation programme;

c. Conduct regular energy audit at the frequency of at least once a year;

d. Implement the recommendations of the energy auditors;

e. Report to the authority on the energy conservation programme implemented.

Ministry of EMR Regulation No. 6/2011 on Affixing Label Energy Saving for Swaballast Lamp:

This regulation stipulates the standards and labeling system for domestic appliances. A list

of key household appliances has been listed as priority for implementation. The design and

reporting information for the label to be affixed to such labeled products have also been

stipulated.

Ministry of EMR Regulation No 13/2010 and No.14/2010 on Competency Standard for

Energy Manager:

i. Ministry of Manpower and Transmigration Regulation No. 321 and

323/MEN/XII/2011 on Standard Work Competence of Indonesia for Energy

Manager (SKKNI Manajer Energi);

ii. Ministry of Manpower and Transmigration Regulation No. 614/MEN/IX/2012 on

Standard Work Competence of Indonesia for Energy Auditor (SKKNI Auditor

10

Energi);

From the leading Laws and Regulations highlighted above, it can be seen that fundamental and

important provisions have been put in place. If the engine of energy efficiency did not take off,

then there are only three possibilities. They are firstly the issues of institutional framework and

capacity to implement all regulatory frameworks effectively; secondly, the issues of manpower

resources and capacity to undertake the various technical and managerial tasks are either

inadequate or not at the right level of competency; thirdly, financial and other resources are not

in place or made available.

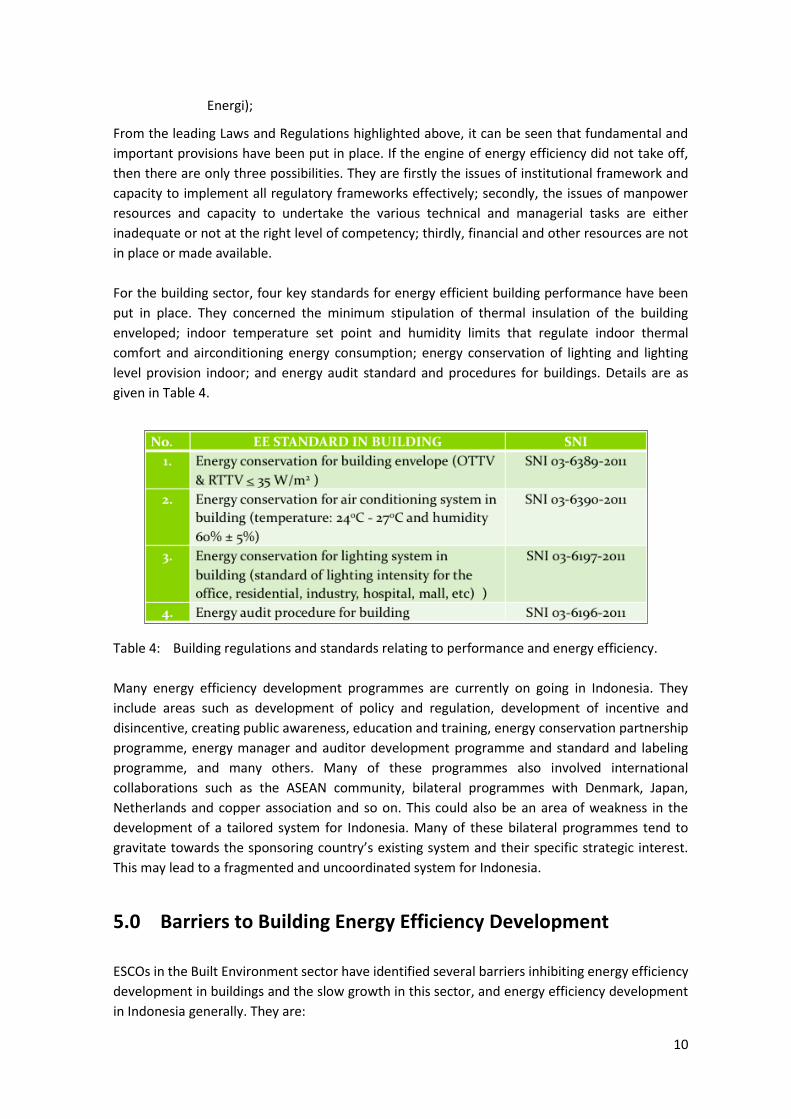

For the building sector, four key standards for energy efficient building performance have been

put in place. They concerned the minimum stipulation of thermal insulation of the building

enveloped; indoor temperature set point and humidity limits that regulate indoor thermal

comfort and airconditioning energy consumption; energy conservation of lighting and lighting

level provision indoor; and energy audit standard and procedures for buildings. Details are as

given in Table 4.

Table 4: Building regulations and standards relating to performance and energy efficiency.

Many energy efficiency development programmes are currently on going in Indonesia. They

include areas such as development of policy and regulation, development of incentive and

disincentive, creating public awareness, education and training, energy conservation partnership

programme, energy manager and auditor development programme and standard and labeling

programme, and many others. Many of these programmes also involved international

collaborations such as the ASEAN community, bilateral programmes with Denmark, Japan,

Netherlands and copper association and so on. This could also be an area of weakness in the

development of a tailored system for Indonesia. Many of these bilateral programmes tend to

gravitate towards the sponsoring country’s existing system and their specific strategic interest.

This may lead to a fragmented and uncoordinated system for Indonesia.

5.0 Barriers to Building Energy Efficiency Development

ESCOs in the Built Environment sector have identified several barriers inhibiting energy efficiency

development in buildings and the slow growth in this sector, and energy efficiency development

in Indonesia generally. They are:

11

a. Fossil fuel subsidy leads to the lack of incentive to implement energy management

programme;

b. Lack of energy saving awareness and available accurate benchmarking database;

c. Lack of knowledge on available energy efficiency options and realizable saving on the

part of building managers and owners;

d. Perceived high initial investment for energy efficiency technology, and the lack of

knowledge on return on investment (ROI);

e. Lack of smart financing mechanism for energy efficiency projects.

On the other hand, the APKENINDO has identified the following as their perceived barrier:

Lack of Know How and Awareness

Lack of energy efficiency development and project financing

Lack of regulatory framework

Lack of customer demand

From the list (a) to (e) and the various bullet points above, it can be seen that the main barrier is

the low energy cost and electricity tariff owing to state subsidies. The lack of awareness, and most

importantly the lack of excellent real life examples of successful energy efficiency retrofit projects

that resulted in significant saving within the private sector are not barrier. They are market

structure weakness, and all markets at its early stage of development share the same problems.

The lack of information and knowledge is not strictly speaking a barrier, as it does not inhibit

development. In the case of Indonesia, since policies such as mandating energy management and

audits are already in place in 2009, and yet not able to create significant demand for energy

efficiency projects, the barrier must then lie with the implementation processes and/or the lack

of critical resources such as financing or technical capacity. To jump-start the system at its early

stage of development, the followings are important:

a. Effective and correct financial incentive to encourage the early ventures to come forward.

b. The early energy efficiency projects must be well managed to give highest successes. All

achievement must be accurately and independently measured and verified. The additional

work scope for such case examples may be borne by public agencies as part of the incentive.

c. For the incentives earned, the beneficiaries must pledge to publicize their results and serve

as energy efficiency advocates.

d. Only certified and qualified ESCOs are allowed to receive incentives on behalf of the

owners/developers. Incentive must be given in the measured ways according to return and

saving, and technological achievements.

Dominating state owned ESCOs may also unknowingly serve as a barrier to healthy private sector

ESCO development if they compete openly with the private sector. Even if they serve only the

public sector enterprises and their facilities, they are likely to cause barrier to the introduction

and development of new small and medium size enterprises.

It is useful to adopt the policy of public sector taking the lead as this may generate many projects

12

for the industry. The successful implementation of such projects serves to demonstrate the

benefits of energy efficiency projects. They will also lower the cost of energy audit services and

technology, such as LED lights and energy efficient airconditioning system.

The practitioners of the energy efficiency industry recommend that urgent actions be taken to

overcome the problems of slow development of the building energy efficiency sector. They

include:

Removing fuel subsidy;

Increasing awareness on energy efficiency;

Improving capacity and knowledge on energy efficiency in building sector;

Strengthening Research and Development on energy efficiency technology;

Accelerate market transformation through smart financing mechanism on energy efficiency projects.

These recommended actions are broad and generic in nature. Detail examinations are required

to establish the appropriate priority for implementation. For example, the removal of fuel subsidy

in a huge country like Indonesia cannot be done over night. It required phasing and the right

quantum of subsidy to be removed at the correct timing to ensure market stability and social

balance. Increasing of awareness of energy efficiency must be directed to the right stake-holders

with the right information in the right quantum with objective and accurate verification. This is to

ensure that the awareness generated translate into actions and projects.

While strengthening R&D on energy efficiency technology is important, it is essential to invest in

projects that are practical and useful at the early stage of development. Useful early stage

development includes the establishment of accurate building energy performance benchmarks at

whole building level and system performance level. Such benchmarking system allows the

building managers to discover the performance ranking of his/her building and the setting of

energy efficiency target, while estimating the quantum of saving and the amount of investment

required. This also allow researchers to identify the best practice buildings and develop suitable

case studies to be shared among the market. It is the most effective means of capacity

development.

6.0 Conclusions This paper reviews the status of building energy efficiency development of Indonesia. Based on a

comprehensive review of literatures and feedback from practitioners, four critical areas of

performance were examined. They include the current status of Building Energy Efficiency

Performance Development, Energy Services Sector and Its Development, Energy Policies

Regulations and Programmes, and Barriers to Building Energy Efficiency Development.

The build environment sector is considered a smaller sector consuming only 18% of the annual

final energy use in Indonesia, after the industry and transportation sectors which consume 41%

and 37% respectively. Owing to this the lead stake-holders in energy efficiency development are

the Ministry of Energy and Mineral Resources and the Ministry of Industry. The Ministry of Public

13

Works, which oversees building and infra-structural development, plays a relatively small role.

This may be a reason building energy efficiency development is slow.

Energy efficiency performance of building is estimated to have a saving potential of 15 to 30%

with a targeted saving of 15% by the 2025. This is translated to 0.7% reduction in the overall

national final energy use.

The building energy efficiency sector is relatively under developed and ESCOs’ capacity is generally

low. The ESCOs Association of Indonesia has only 16 members with a low level of activity. It has

indicated that the low energy cost due to energy subsidy is a major barrier affecting the rapid

development of the industry. Other barriers include the lack of awareness on energy efficiency,

the lack of knowledge and experience on the part of some of the ESCOs, and the lack of innovative

financing mechanism. It is recognized that there is a lot of developmental work to do if the building

energy services sector is to flourish. There is also significant preparation work including careful

planning, setting of priority and targets setting. It is also important that the ESCO Association

admits only qualified and good ESCOs to uphold the high quality services and the good reputation

and prestige of the energy efficiency sector.

From the fact that most of the key policies and regulations are in place, and yet the energy

efficiency sector is having difficulty sustaining a good level of activities with only 16 registered

members of the ESCO Association, and for the huge economic of Indonesia, it only points to the

fact that these policies and regulation implementation processes and rigour is perhaps not

suitably apply. Therefore, it is critical that the institutional framework is strengthened to drive the

development of the energy efficiency sector for the built environment.

Although the built environment sector only takes up a small proportion of the total Indonesia’s

final energy consumption, 18%, this is a sector where energy efficiency technology is matured and

well-practiced all over the world, including that in the tropics. It is also highly repeatable such as

the use of lighting and airconditioning in buildings. Hence it is a sector that is being considered as

the low hanging fruits, and that investment to jump start the building energy efficiency sector can

reap significant benefits and multiplier effect.

References:

1. Asia Pacific Energy Research Centre (APERC): Final Report-Peer Review on Energy

Efficiency in Indonesia, 2012; APEC Energy Working Group; Asia Pacific Energy Research

Centre, Japan 2012.

2. International Energy Agency: South East Asia Energy Outlook (a World Energy Outlook

Special Report); Directorate of Global Energy Economics, IEA, Paris 2013.

3. Andriah Feby Misna: Energy Efficiency in Buildings in Indonesia; Seminar presentation by

Directorate of Energy Conservation, Ministry of Energy and Mineral Resources, Jakarta

2014.

14

4. Building and Construction Authority Singapore: BCA Building Energy Benchmarking

Report 2014; Singapore 2014.

5. Maritje Hutapea: Policies on Energy Efficiency Standards and Labeling in Indonesia; 7th

Lites Asia Meeting, 22-23 April 2013 Jakarta, Indonesia 2013.

6. ReExCapitalAsia: South East Asia Energy Efficiency Market Report 2011; Singapore 2011.

7. Joint Research Centre, Institute for Energy and Transport: ESCO Market Report for Non-

European Countries 2013, Report EUR 26886 EN, European Union 2014.