Embed Size (px)

Citation preview

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

1

A STUDY ON SERVICE QUALITY MEASUREMENT AND ITS IMPACT

IN OPTING INSURANCE COMPANIES

DR. D.H. MALINI*

*Assistant Professor,

Department of Management,

Pondicherry University,

P.K. College of Education Campus

Nehru Nagar, Karaikal Campus-609605.

ABSTRACT

Insurance is a policy from a large financial institution that offers a person, company, or other

entity reimbursement or financial protection against possible future losses or damages. The

meaning of insurance is important to understand for anybody that is considering buying an

insurance policy or simply understanding the basics of finance. Insurance is a hedging instrument

used as a precautionary measure against future contingent losses. This instrument is used for

managing the possible risks of the future. Insurance is bought in order to hedge the possible risks

of the future which may or may not take place. This is a mode of financially insuring that if such

an incident happens then the loss does not affect the present well-being of the person or the

property insured.

The purpose of this study is to evaluate customers‘ general expectation and perception of insurers

in terms of Services offered at the insurance service measurement and its impact. Thus, results of

this study underscore the need for insurance providers to gear customer service and quality

improvement efforts towards components of reliability. The study intends to promote a better

theoretical understanding and recognition of the complexities to service quality and its

measurement. Today, insurance companies in India competing each other by providing exclusive

services. But the challenges for insurance sector in India remains the same that is to bring

innovative services to clients while making them realize the value of those services provided.

When clients realize that quality is something that cannot be compromised, an organization has to

survive in the competitive market while managing high value service.

KEYWORDS: Insurance, Service, Broking.

______________________________________________________________________________

INTRODUCTION

The insurance industry faces numbers of challenge and a unique roadblock to build loyal and

quality customer relationships. The biggest challenge in the insurance industry face is meeting

customer expectations for faster, better service in the face of rising loss cost and increasing price

competition. According to Benchmark Portal, customer service operations in the insurance are a

liability to their organizations, operating neither efficiently nor effectively. Bad experience with a

customer service counter employee lead to public terminates their relationship with the company.

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

2

According to any reports about services, increasing self-service capabilities in the insurance

industry leads to an increase in customer service counter activity. There is a statistical link

between employee behaviour and customer satisfaction. These facts are beginning to resonate

with insurance companies, who are investing in customer relationship management and self-

technologies designed to build customer loyalty and customer centricity.

The term quality is difficult to define impartially. In service there is a humanistic quality

approach, at the one extreme stressing customers, personnel, leadership and culture, whereas at

the other end lies a technical approach concerning operations management, statistics and methods

of measurement. (Gummerson, 1992)

They quality is divided into input and output Lehtinen and Lehtinen (1991). The output consists

of total service offering in terms of quality, and the input includes both tangibles and intangibles

elements. The output in the form of quality is what the customer in fact pays for, which is to a

large extent intangible and may be difficult to quantify (Adam et al., 1995). Service quality is not

the slippery, mystical, or amorphous concept it is often thought to be.

Customers will give an institution high mark for its service when it meets or exceeds their service

desires. The five dimensions of service performance (tangibles, reliability, responsiveness,

assurance and empathy) give direction to the service quality journey. Although these dimensions

will be differently important to various market segments, on an overall basis, they all are

important. As a group, they frame the essence of the service quality mandate to be excellent in

service, seek to be excellent in tangibles, reliability, responsiveness, assurance and empathy

(Berry et al., 1989).

Service quality is generally defined as customer perceived quality which stresses the individual‘s

assessment of the value of the total service offering (Gummesson, 1992). Practically, Gronroos

(1998) described perceived service quality as the difference between expected service quality and

experienced service quality. This has a link to the gap model

(Parasuraman et al., 1985) and other service quality models (e.g. Bitner 1990). On the other hand,

Berry et al (1985) divided service quality into two types: regular services, and handling of

exceptions or problems to ensure that appropriate procedures are taken to deal with inevitable

failures. As regards to service quality, the individual‘s experience of a service forms the basis of

an assessment of its quality. It is great to listen to customers and study their reactions. When

purchasing services, customers‘ attention is often limited to a small number of tangible inputs

(Zeithaml, 1984). Physical environment include buildings, offices and interior design affects

customer beliefs, attitudes and satisfaction Zeithaml and Bitner, 2000), and provides an

opportunity to tell the ‗right‘ story about a given service (Berry et al., 1989). Matters such as how

contact personnel dresses, articulates, writes, designs and presents proposals are likewise not

without meaning (Levitt, 1981). Tangibilising the intangibles is important, because customers do

not usually know what they are getting until they do not get it (Levitt, 1981). As tangible input,

the service personnel represent the service, the organization and the marketers in the customers‘

eyes (Zeithmal and Bitner, 1996). The quality management of personnel includes such things as

motivating, managing information, training, career planning and recruiting and retaining of right

people (Normann, 1991); Zeithaml and Britner, 1996). It is true that service business is

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

3

personnelintensive, meaning that quality supplied to the customer is essentially a result of the way

personnel perform (Normann, 1991). Schneider (1990) showed that both employees and

customers will experience more positive outcomes when the organization operates with a

customer service orientation and management supports it.

OBJECTIVES

The project was conducted after taking into consideration the changing face of the Insurance

sector. The objective for conducting this project was

To understand the market expectations on Insurance companies.

To learn Insurance and Insurance Broking in India.

To identify the service parameters of Insurance Brokers.

To know the preference of Insurance products in related to clients‘ category wise and

products category wise.

To identify the satisfaction level of clients with regard to claim services of Insurance

Brokers.

NEED OF THE STUDY

In India at present there are 23 general Insurance companies which are registered under IRDA

Regulations. The present market prevails tough competition between these Insurance companies

to increase the sales growth. Insurance companies generate moreover 80% of their sales through

insurance brokers. Therefore, there is a need to study what aspects and norms do an Insurance

broker consider from an Insurance company before suggesting Insurance policies for their clients.

SCOPE OF THE STUDY

The study is aimed to understand and analyze the preference of Regional Insurance Brokers in

selecting an Insurance company for their clients. The study is confined to elicit the opinion of

these groups in Chennai City only.

LIMITATIONS

A real time survey in Chennai city with the total sample size of 32 brokers has been taken but

the study would have been much better if the data was collected throughout India from the

total sample size of 255 Insurance Brokers in India.

Tough to fix appointments with Insurance Brokers because of their tight schedule as many

Insurance policies are renewed at the financial year ending.

Getting accurate responses from the respondents due to their inherent problems is difficult.

They may be partial or refuse to co-operate.

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

4

RESEARCH METHODOLOGY

RESEARCH DESIGN

The research method adopted for this study is Descriptive. Descriptive research includes surveys

and fact finding of different types of research problems. The objective of the study is to

understand the preference on Insurer among regional brokers and to suggest the Insurance

companies to gain more market share. Quantitative research was employed in the present study.

In the present study the research steps applied were in accordance with scientific research design

Bodgan and Biklen (1982). According to his study the data collected was based on a

predetermined instrument and the objectives developed prior research. The purpose of this

research project is to determine the importance quality of service provided by the insurance

brokers in selecting insurance companies from the customer viewpoints.

SOURCES OF DATA

The data is a collected through primary and secondary data in the field. It examines perception

and expectations in terms of service. The variables under study are neither controlled nor

manipulated.

PRIMARY DATA

Primary data have been collected from the people in two ways:

Personal Interview

Questionnaire Method

SECONDARY DATA

Secondary data have been collected from the previous researchers and studies in the related study

area. In this study several sources of external data, including periodicals and government

publications of economic indicators. The company‘s websites, books, journals and published

reports printed.

SAMPLE SIZE

Sample sizes of 32 respondents were taken to analyze the Insurance sector and to understand the

changing phase of the Insurance companies.

SAMPLING TECHNIQUE USED

Convenient Sampling

STATISTICAL TOOLS

Percentage analysis

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

5

Chi-square Method

Weighted Average Method

Correlation analysis

Ranking Method

Insurance is a system of spreading the risk of one onto the shoulders of many. While it becomes

somewhat impossible for a man to bear by himself 100% loss to his own property or interest

arising out of an unforeseen contingency, insurance is a method or process which distributes the

burden of the loss on a number of persons within the group formed for this particular purpose.

Basic Human trait is to be averse to the idea of risk taking. In Insurance whether life or non-life, it

provides people with a reasonable degree of security and assurance that they will be protected in

the event of a calamity or failure of any sort. Insurance may be described as a social device to

reduce or eliminate risk of loss to life and property. Under the plan of insurance, a large number

of people associate themselves by sharing risks attached to individuals. The risks, which can be

insured against, include fire, the perils of sea, death and accidents and burglary. Any risk

contingent upon these, may be insured against at a premium commensurate with the risk involved.

Thus collective bearing of risk is insurance.

WHY INSURANCE BROKERS WERE BROUGHT INTO THE INDIAN INSURANCE

Govt. of India decided to embark on economic reforms in the 1990s. The command and control

economy gradually gave way to market economy in sector after sector, including the financial

sector which comprised ―Insurance‖ sector. Various reforms were initiated in the financial sector.

The economy responded positively to the reforms. Competition in the manufacturing sector

geared it up to invest in technology, restructure its operations, reduce cost, achieve improved

productivity, and bring quality of products to international standards. Newspaper Articles started

highlighting the success stories of several enterprises in the Open Market Indian Economy to

demonstrate what could be achieved in a liberalized market economy.

Along with financial sector reforms, there were many reform measures by the Govt. for the

insurance sector. Insurance Sector Reform Measures initiated by the Government were based on

the Report of the Malhotra Committee, which submitted its Report in 1994.

ACCEPTABILITY OF INSURANCE BROKERS IN THE INDIAN MARKET

Brokers as intermediaries are still not wholly acceptable for the corporate or individual clients in

India. Unhealthy competition in the market has also affected the professional image of brokers.

Most of the brokers still do not have professional expertise and their ostrich like attitudes of not

owning up their deficiencies in their mindset and the poor morale of the staff would act as huge

barriers to their perceived strategic strengths at the market place.

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

6

SWOT ANALYSIS

A scan of the internal and external environment is an important part of the strategic planning

process. Environmental factors internal to the firm usually can be classified as strengths (S) or

weaknesses (W), and those external to the firm can be classified as opportunities (O) or threats

(T). Such an analysis of the strategic environment is referred to as a SWOT analysis.

PEST ANALYSIS

A scan of the external macro-environment in which the firm operates can be expressed in terms of

the following factors:

Political

Economic

Social

Technological

The acronym PEST (or sometimes rearranged as "STEP") is used to describe a framework for the

analysis of these macro environmental factors.

4 I’S OF INSURANCE SERVICE:

The 4 I‟ s refers to the different dimensions/ characteristics of any service. Unlike pure

product, services have its own characteristics and its related problems. So the service provider

needs to deal with these problems accordingly. The service provider has to design different

strategies according the varying feature of the service. These 4 I‟ s not only represent the

characteristics of different services but also the problems and advantages attached to it.

These 4 I‟ s can be broadly classified as:

• Intangibility

• Inconsistency

• Inseparability

• Inventory

DATA ANALYSIS

PREFERENCE ON INSURER AMONG REGIONAL BROKERS

INSURANCE BROKERS

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

7

The first set of broking licenses were issued in January 2003 and expectations were naturally high

as stakeholders in the industry anticipated a paradigm shift in the way Insurance was being bought

and sold. While analyzing the role of insurance brokers, the following details furnishes the

preference on Insurer among regional Brokers

Indian Broking Industry – Some quick statistics - Growth in numbers

If we look at the statistics pertaining to the growth of insurance brokers in India, we find that as

against forty brokers as on 31st March, 2003 (when the broking industry was born), we now have

255 insurance brokers (as on April 2011).

A real time survey has been taken with the total Sample size of 32 Insurance Brokers in the

Chennai city to analyze the Preference on Insurer among Regional Brokers. Data analysis of my

report is as follows:-

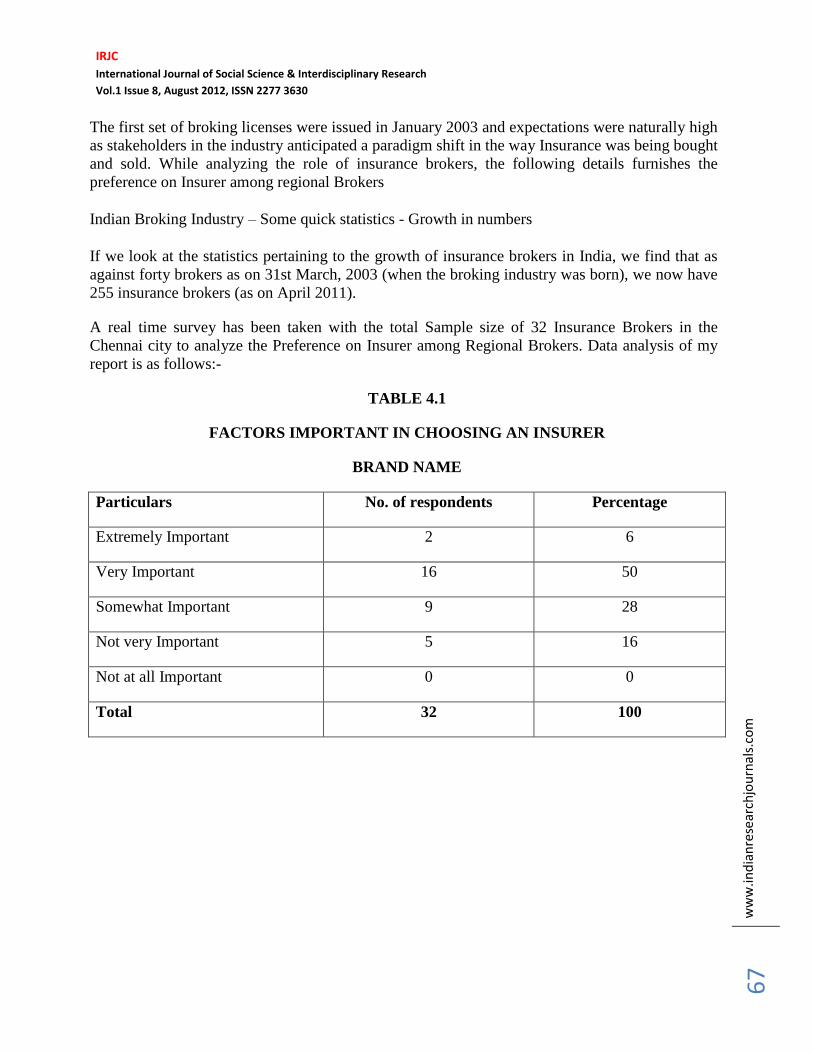

TABLE 4.1

FACTORS IMPORTANT IN CHOOSING AN INSURER

BRAND NAME

Particulars No. of respondents Percentage

Extremely Important 2 6

Very Important 16 50

Somewhat Important 9 28

Not very Important 5 16

Not at all Important 0 0

Total 32 100

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

8

INFERENCE

From the above table, the majority (50%) of the respondents expressed as the brand of the

Insurer is very important and only 6% tells as its extremely important. From this it is evident that

Brokers are not considering the brand name as most to suggest their clients.

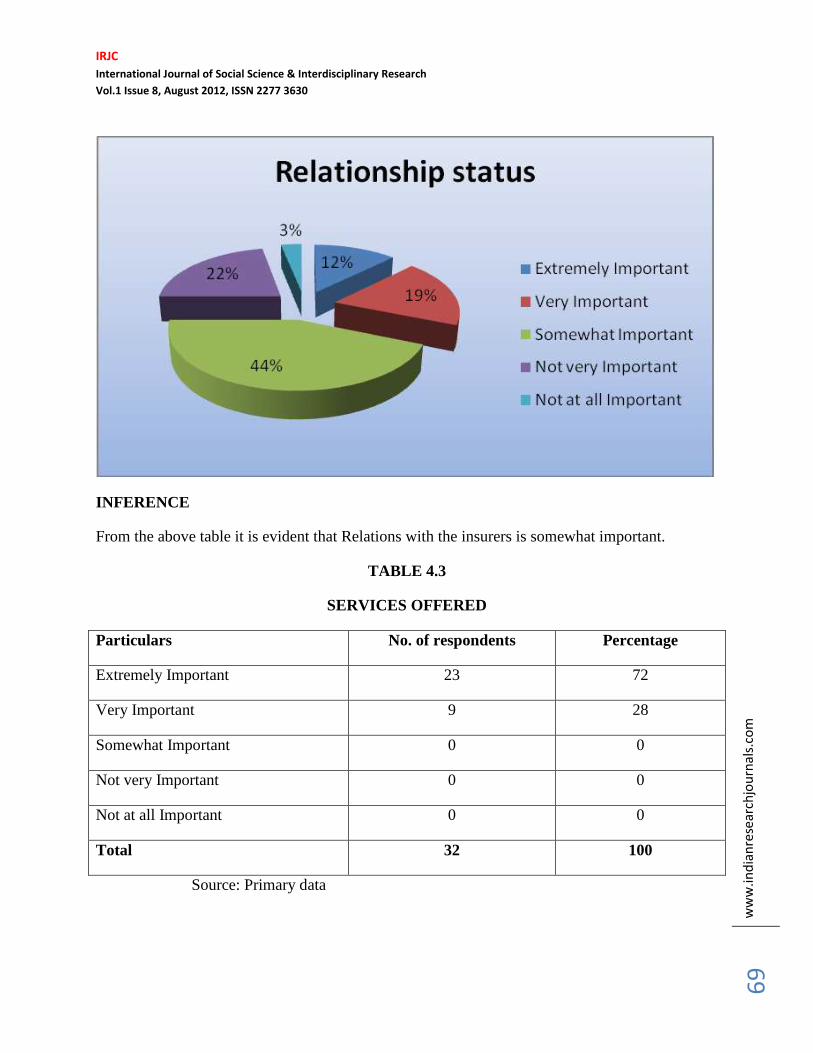

TABLE 4.2

RELATIONSHIP STATUS

Particulars No. of respondents Percentage

Extremely Important 4 13

Very Important 6 19

Somewhat Important 14 44

Not very Important 7 22

Not at all Important 1 3

Total 32 100

Source: Primary Data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

6

9

INFERENCE

From the above table it is evident that Relations with the insurers is somewhat important.

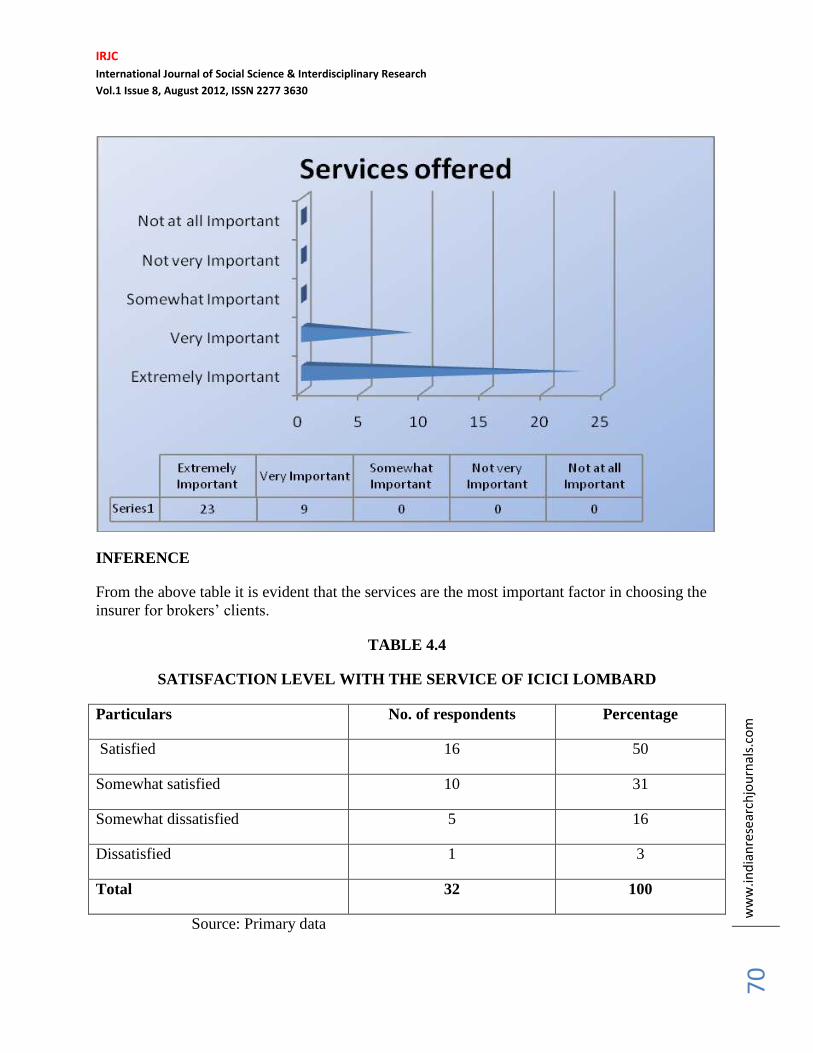

TABLE 4.3

SERVICES OFFERED

Particulars No. of respondents Percentage

Extremely Important 23 72

Very Important 9 28

Somewhat Important 0 0

Not very Important 0 0

Not at all Important 0 0

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

0

INFERENCE

From the above table it is evident that the services are the most important factor in choosing the

insurer for brokers‘ clients.

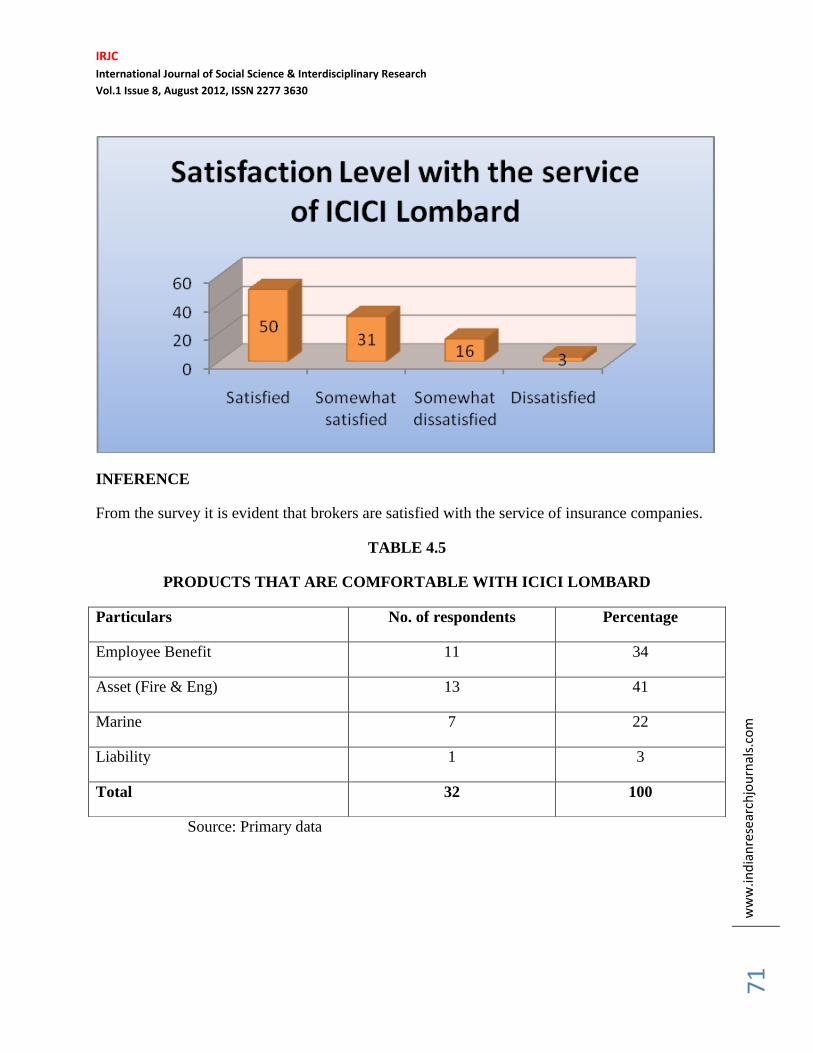

TABLE 4.4

SATISFACTION LEVEL WITH THE SERVICE OF ICICI LOMBARD

Particulars No. of respondents Percentage

Satisfied 16 50

Somewhat satisfied 10 31

Somewhat dissatisfied 5 16

Dissatisfied 1 3

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

1

INFERENCE

From the survey it is evident that brokers are satisfied with the service of insurance companies.

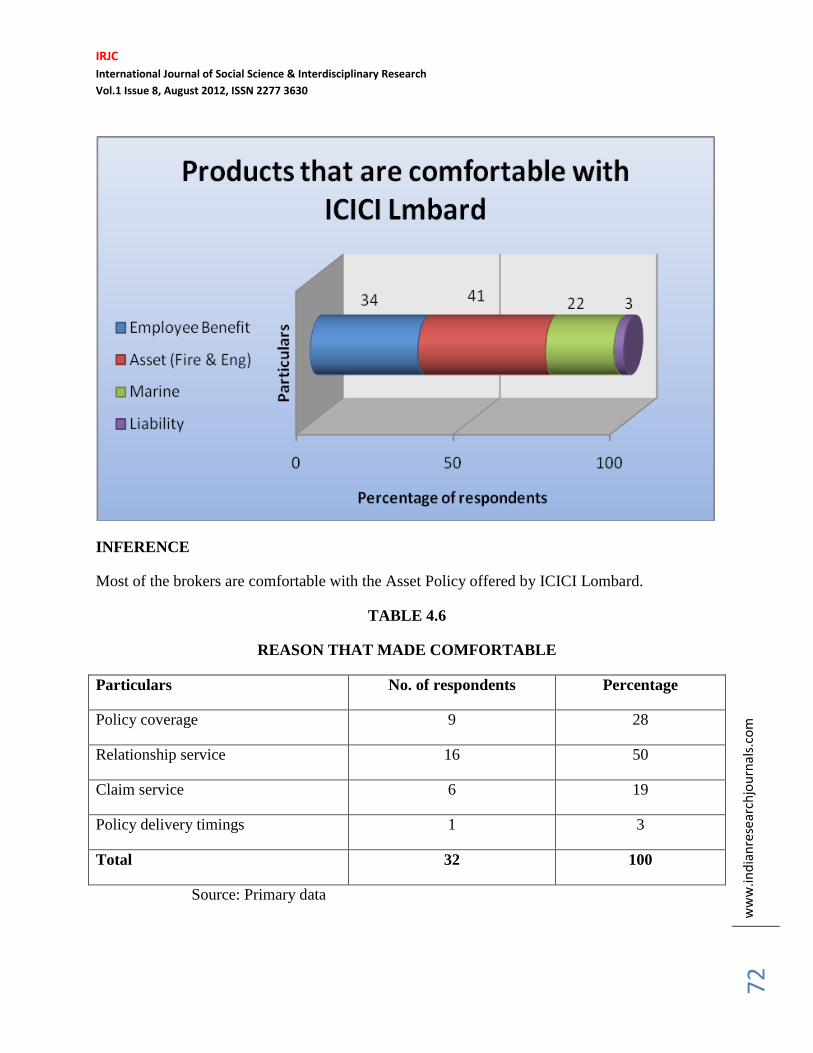

TABLE 4.5

PRODUCTS THAT ARE COMFORTABLE WITH ICICI LOMBARD

Source: Primary data

Particulars No. of respondents Percentage

Employee Benefit 11 34

Asset (Fire & Eng) 13 41

Marine 7 22

Liability 1 3

Total 32 100

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

2

INFERENCE

Most of the brokers are comfortable with the Asset Policy offered by ICICI Lombard.

TABLE 4.6

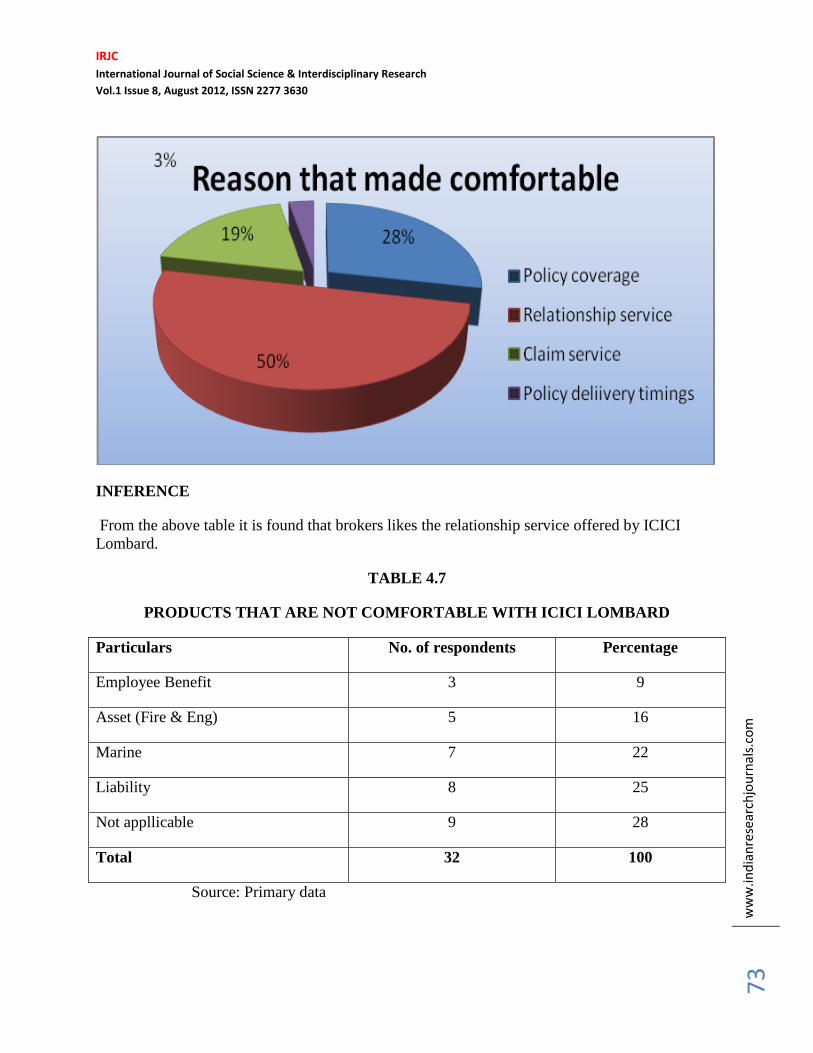

REASON THAT MADE COMFORTABLE

Particulars No. of respondents Percentage

Policy coverage 9 28

Relationship service 16 50

Claim service 6 19

Policy delivery timings 1 3

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

3

INFERENCE

From the above table it is found that brokers likes the relationship service offered by ICICI

Lombard.

TABLE 4.7

PRODUCTS THAT ARE NOT COMFORTABLE WITH ICICI LOMBARD

Particulars No. of respondents Percentage

Employee Benefit 3 9

Asset (Fire & Eng) 5 16

Marine 7 22

Liability 8 25

Not appllicable 9 28

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

4

INFERENCE

Majority of the respondents told that they are comfortable with all products of ICICI Lombard

and 23% of respondents told that they are uncomfortable with the Liability policy offered by

ICICI Lombard as it takes more policy delivery timing.

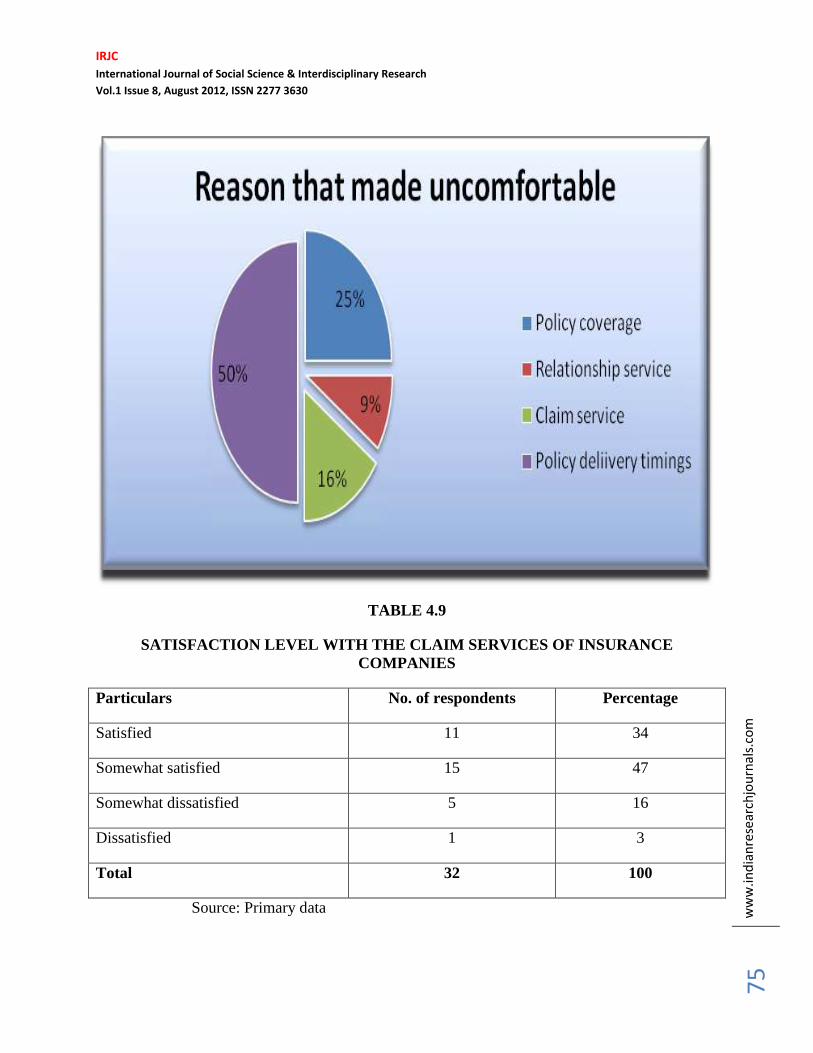

TABLE 4.8

REASON THAT MADE UNCOMFORTABLE

Particulars No. of respondents Percentage

Policy coverage 8 25

Relationship service 3 9

Claim service 5 16

Policy delivery timings 16 50

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

5

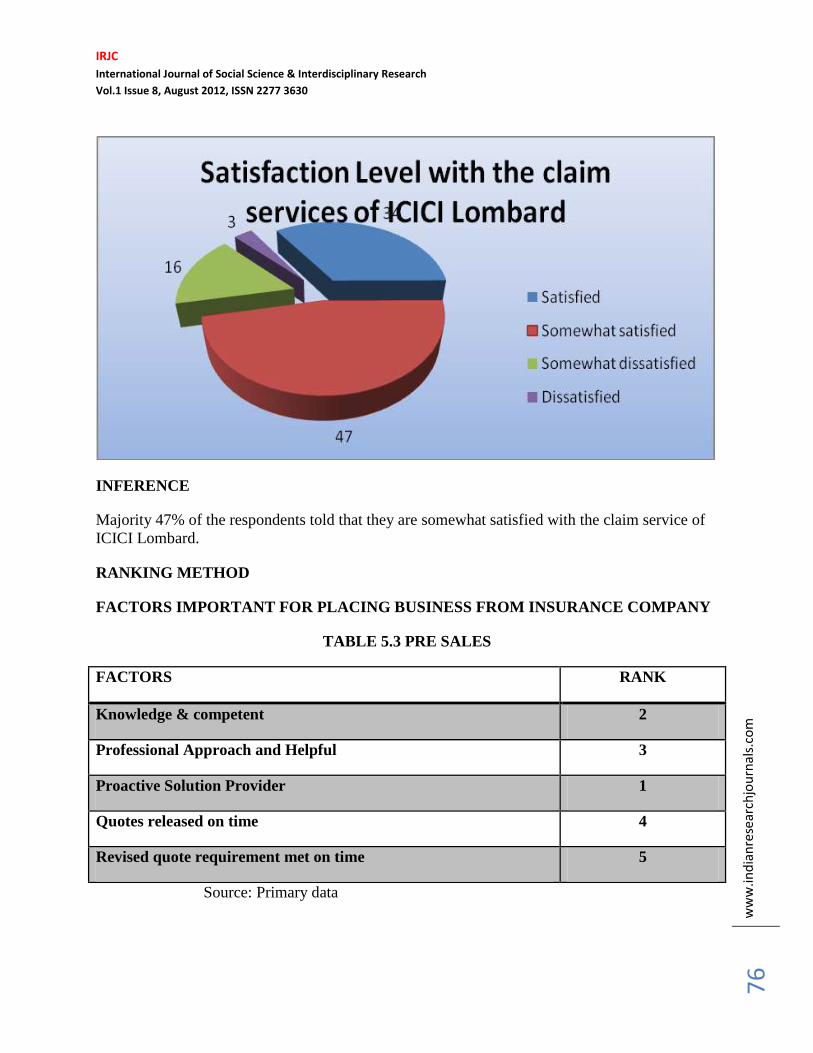

TABLE 4.9

SATISFACTION LEVEL WITH THE CLAIM SERVICES OF INSURANCE

COMPANIES

Particulars No. of respondents Percentage

Satisfied 11 34

Somewhat satisfied 15 47

Somewhat dissatisfied 5 16

Dissatisfied 1 3

Total 32 100

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

6

INFERENCE

Majority 47% of the respondents told that they are somewhat satisfied with the claim service of

ICICI Lombard.

RANKING METHOD

FACTORS IMPORTANT FOR PLACING BUSINESS FROM INSURANCE COMPANY

TABLE 5.3 PRE SALES

FACTORS RANK

Knowledge & competent 2

Professional Approach and Helpful 3

Proactive Solution Provider 1

Quotes released on time 4

Revised quote requirement met on time 5

Source: Primary data

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

7

INFERNCE

From the analysis it is evident that Proactive solution provider is mostly preferable from

respondents from an insurance company to place their business with them.

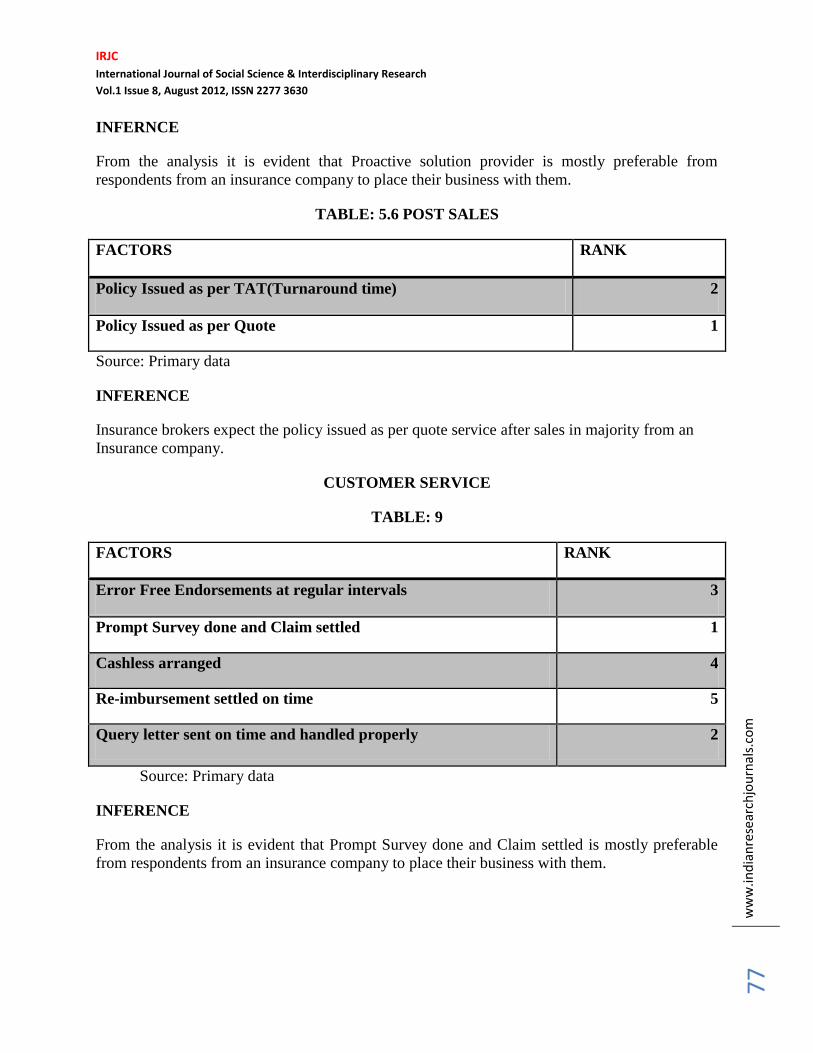

TABLE: 5.6 POST SALES

FACTORS RANK

Policy Issued as per TAT(Turnaround time) 2

Policy Issued as per Quote 1

Source: Primary data

INFERENCE

Insurance brokers expect the policy issued as per quote service after sales in majority from an

Insurance company.

CUSTOMER SERVICE

TABLE: 9

FACTORS RANK

Error Free Endorsements at regular intervals 3

Prompt Survey done and Claim settled 1

Cashless arranged 4

Re-imbursement settled on time 5

Query letter sent on time and handled properly 2

Source: Primary data

INFERENCE

From the analysis it is evident that Prompt Survey done and Claim settled is mostly preferable

from respondents from an insurance company to place their business with them.

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

8

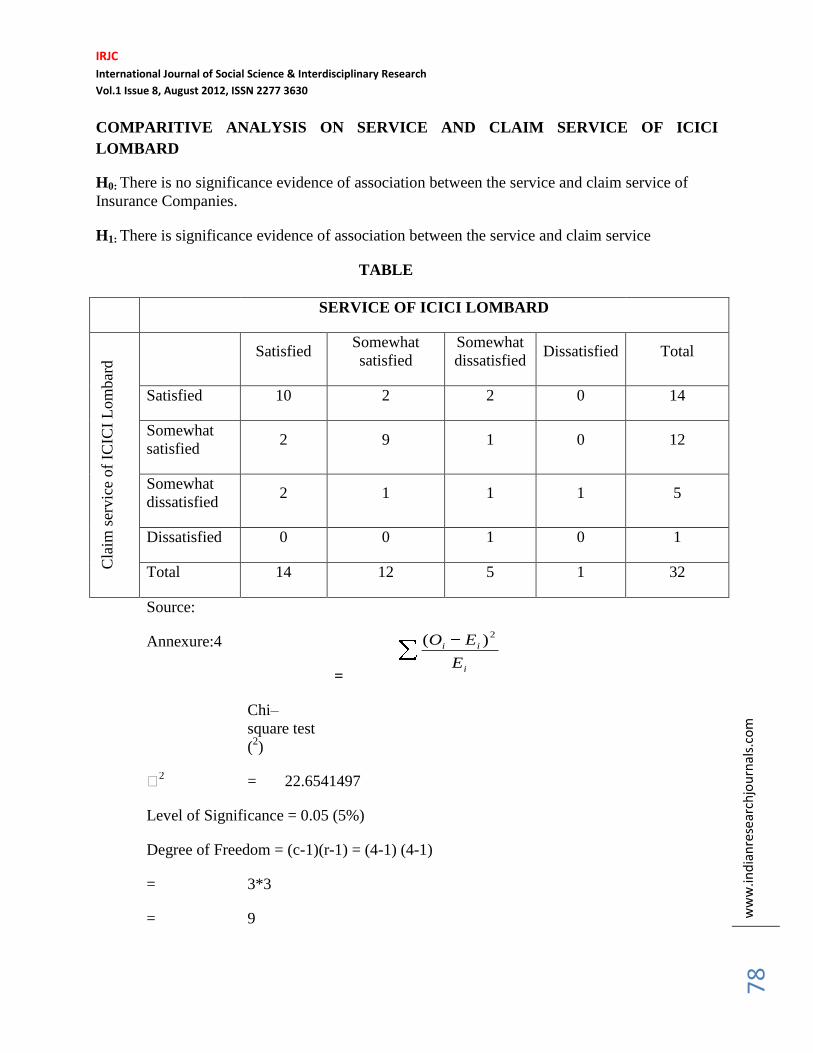

COMPARITIVE ANALYSIS ON SERVICE AND CLAIM SERVICE OF ICICI

LOMBARD

H0: There is no significance evidence of association between the service and claim service of

Insurance Companies.

H1: There is significance evidence of association between the service and claim service

TABLE

SERVICE OF ICICI LOMBARD

Cla

im s

ervic

e of

ICIC

I L

om

bar

d

Satisfied Somewhat

satisfied

Somewhat

dissatisfied Dissatisfied Total

Satisfied 10 2 2 0 14

Somewhat

satisfied 2 9 1 0 12

Somewhat

dissatisfied 2 1 1 1 5

Dissatisfied 0 0 1 0 1

Total 14 12 5 1 32

Source:

Annexure:4

Chi–

square test

(2)

=

2 = 22.6541497

Level of Significance = 0.05 (5%)

Degree of Freedom = (c-1)(r-1) = (4-1) (4-1)

= 3*3

= 9

i

ii

E

EO2

)(

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

7

9

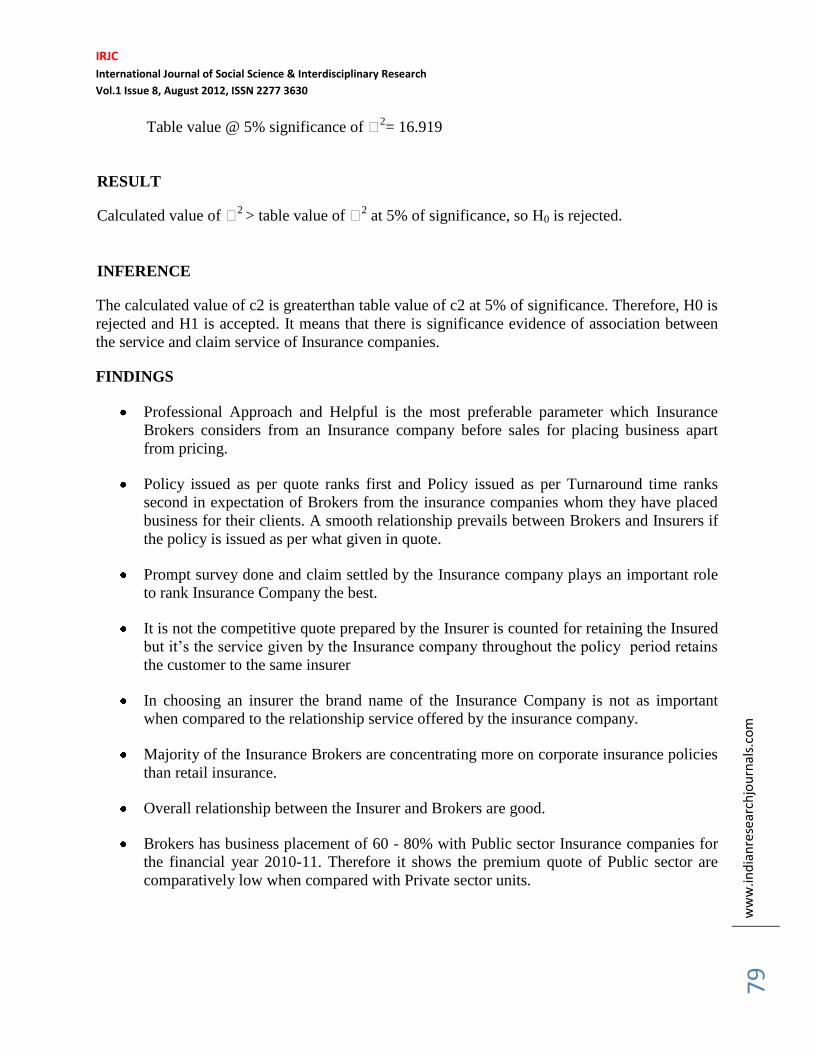

Table value @ 5% significance of 2= 16.919

RESULT

Calculated value of 2

> table value of 2 at 5% of significance, so H0 is rejected.

INFERENCE

The calculated value of c2 is greaterthan table value of c2 at 5% of significance. Therefore, H0 is

rejected and H1 is accepted. It means that there is significance evidence of association between

the service and claim service of Insurance companies.

FINDINGS

Professional Approach and Helpful is the most preferable parameter which Insurance

Brokers considers from an Insurance company before sales for placing business apart

from pricing.

Policy issued as per quote ranks first and Policy issued as per Turnaround time ranks

second in expectation of Brokers from the insurance companies whom they have placed

business for their clients. A smooth relationship prevails between Brokers and Insurers if

the policy is issued as per what given in quote.

Prompt survey done and claim settled by the Insurance company plays an important role

to rank Insurance Company the best.

It is not the competitive quote prepared by the Insurer is counted for retaining the Insured

but it‘s the service given by the Insurance company throughout the policy period retains

the customer to the same insurer

In choosing an insurer the brand name of the Insurance Company is not as important

when compared to the relationship service offered by the insurance company.

Majority of the Insurance Brokers are concentrating more on corporate insurance policies

than retail insurance.

Overall relationship between the Insurer and Brokers are good.

Brokers has business placement of 60 - 80% with Public sector Insurance companies for

the financial year 2010-11. Therefore it shows the premium quote of Public sector are

comparatively low when compared with Private sector units.

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

8

0

Majority 76% of the respondents are comfortable with Employee benefit products offered

by ICICI Lombard. The reason is they like the policy coverage and relationship service of

the company.

25% of the brokers responded that they are not comfortable with Liability policy of ICICI

Lombard as it takes more turnaround time for the delivery of policy and claim settlement.

It is because ICICI Lombard has tie up with only GIC for its reinsurance.

50% of the respondents are satisfied with the service of ICICI Lombard.

47% of the respondents are somewhat satisfied with the claim service of ICICI Lombard.

SUGGESTIONS

Quote participation should be there between Insurance Company and Insurance brokers.

For better relationship with brokers the Insurance Company should route the policy

documents through brokers.

Interaction after quote is necessary for Insurance Company to get more business through

Brokers.

Frequent change of employees should be made less in Insurance companies as the

brokers are finding difficult to maintain relationship with Insurers during claims period.

Private players should provide more coverage with competitive premium to get more

market share compared with public sector units.

CONCLUSION

Competition will surely cause the market to grow beyond current rates, create a bigger "pie," and

offer additional consumer choices through the introduction of new products, services, and price

options. Yet, at the same time, public and private sector companies will be working together to

ensure healthy growth and development of the sector. Challenges such as developing a common

industry code of conduct, contributing to a common catastrophe reserve fund, and chalking out

agreements between insurers to settle claims to the benefit of the consumer will require

concerted effort from both sectors.

The market is now in an evolving phase where one can expect a lot of actions in coming days.

The current impediments for foreign participation – like 26% equity cap on foreign partner, ill

defined regulatory role of IRDA (Insurance Regulatory development Authority the watchdog of

the industry) in pension business etc.—are expected to be removed in near future. The early-

adopters will then have a clear advantage compared to laggards in gaining the market share and

market leadership. The will need to make sure right now that their entire infrastructure is in place

so that they can reap the benefit of an "unlimited potential."

IRJC

International Journal of Social Science & Interdisciplinary Research

Vol.1 Issue 8, August 2012, ISSN 2277 3630

ww

w.in

dia

nre

sear

chjo

urn

als.

com

8

1

REFERENCES

Grace, Martin and Julie Hotchkiss, ―External Impacts on the Property-Liability Insurance

Cycle‖, Journal of Risk and Insurance 62, 738-754.

Harrington, Scott E., 1988, ―Prices and Profits in The Liability Insurance Market‖, in Robert

Litan and Clifford Winston, eds,. Liability: Perspectives and Policy, Washington, D.C.: The

Brookings Institution.

Froot, Kenneth and Jeremy Stein, 1998, ―Risk Management, Capital Budgeting, and Capital

Structure Policy for Financial Institutions: An Integrated Approach‖, Journal of Financial

Economics 47, 55-82.

Doherty, Neil A. and James Garven. 1995, ―Insurance Cycles: Interest Rates and the Capacity

Constraint Model‖, Journal of Business 68, 383-404.

Myers, Stewart C., and Richard A. Cohn, 1986, ―A Discounted Cash Flow Approach To

Property-Liability Insurance Rate Regulation,‖ in J. David Cummins and Scott E. Harrington ,

eds. Fair Rate Of Return In Property-Liability Insurance. Boston: Kluwer.

Tort Policy Working Group,1986, Report of the Tort Policy Working Group on the Causes,

Extent, and Policy Implications of the Current Crisis in Insurance Availability and Affordability,

Washington, D.C.: U.S. Department Of Justice.

Smith, Michael, 1989, ―Investment Returns and Yields To Holders Of Insurance‖, Journal Of

Business 62:81-98.

Winter, Ralph A., 1991b, Solvency Regulation and the Property-Liability ―Insurance Cycle,‖

Economic Inquiry 29, 458-471.