Embed Size (px)

Citation preview

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 1 See last pages for disclaimer.

A summer break with no breakthrough Fixed Income

■ FI Strategizer: Next week, US data confirming the slowdown in the economic recovery should be supportive for Treasuries. In the EMU, solid figures on German IP and orders should keep investors moderately optimistic, with Bunds suffering slightly. We do not expect major surprises from the ECB meeting.

■ EU Portfolio Strategy: We would return to a minor long duration stance of +0.5 years. We keep our positive view on Italy and we increase moderately our exposure on Spain, closing further the gap with EFFAS weightings. We remain moderately overweight on France.

■ Trade Idea: Over the last week, Spain tightened sharply vs. Italy, especially at the front end and at the extra long end. We prefer Italy, due to its sounder macroeconomic fundamentals and we thus suggest switching from Spain into Italy at the 3Y maturity.

■ MM: This week, results of the 3M auction sent a reassuring signal, confirming that the EU banking system is sound. Next week, only the 1W MRO is scheduled, with EUR 190bn expiring. In line with this week, we expect demand to be slightly lower than the amount expiring, leading to another modest drop in liquidity.

■ Supply Corner: Next week, primary market activity will slow down. There will be no redemptions or coupons in the EMU, while gross supply should be a modest EUR 4bn, coming from Austria and Spain. Activity should focus on the short end, with little action on the extra long end.

Forex

■ FX Strategizer: The USD took the full impact of soft US news, but we do not expect the current market scenario to improve sharply. Investors are likely to scale back their risk exposure, which should provide USD, JPY and CHF some relief and put AUD, NZD and EUR under pressure.

■ EUR: The EMU growth prospects will not be strong enough to completely offset the outstanding budget crisis. The EUR-USD strength should ease and the next key resistance level at 1.3125 won’t be broken easily.

■ JPY: The latent downward pressure in USD-JPY and the modest upside potential for EUR-USD will limit any EUR-JPY rebound. EUR-JPY is thus unlikely to break through, while USD-JPY should stay in the 86/88 band.

■ CHF: As feared, the EUR-CHF recovery proved to be quite capped above 1.38: as risk aversion might spark more demand for safe-haven currencies, a full break of the 1.36 base may prompt a further sell-off.

■ GBP: Sterling should stay firm also in August with risks that our medium-term target for cable at 1.60 may be hit rapidly. EUR-GBP should offer a more constrained picture, as a full break towards 0.80 might require time.

■ Pacific Rim & CAD: Commodity units are now less supported by tighter monetary policy at home. The AUD, NZD and CAD should hold the line vs. the USD, but their recent rally is likely to stay frozen in August.

■ Nordics: A more pronounced plunge of EUR-SEK and EUR-NOK below 9.40 and 7.95 appears quite ambitious at this stage. The two Nordic units should thus struggle in the “land of nowhere” in the coming weeks too.

More insight in our monitors: Swap Curve – Money Market – FX Monitor - FX PPP – IMM Monitor – Beta analysis - FX Hit Parade - FX Correlation – Calendar - Forecasts Table

MARKET PRICES & FORECASTS Actual Sep10 Dec10 Mar11 Jun11

US FedFunds 0.25 0.25 0.25 0.75 1.25 2Y UST 0.55 0.85 1.30 2.00 2.40 10Y UST 2.91 3.40 3.80 4.20 4.30 EUROZONE Refi 1.00 1.00 1.00 1.00 1.00 2Y Bund 0.79 0.85 1.05 1.15 1.30 10Y Bund 2.67 3.00 3.25 3.45 3.50 UK Base rate 0.50 0.50 0.50 0.75 1.50 2Y Gilt 0.76 0.90 1.20 1.60 2.20 10Y Gilt 3.33 3.55 3.70 3.90 4.00 (10Y, bp) US - EU 24 40 55 75 80 US - UK -42 -15 10 30 30 UK - EU 66 55 45 45 50 Swap Spread (10Y, bp) US -3 10 15 20 20 EUROZONE 28 25 25 25 20 UK 5 0 10 10 20

Currencies EUR-USD 1.31 1.24 1.22 1.20 1.18 USD-JPY 86 91 95 100 106 GBP-USD 1.56 1.52 1.57 1.60 1.63 EUR-CHF 1.35 1.29 1.27 1.30 1.33

EGB: CURRENT ASW AND 1W CHANGE (BP)

5Y 10Y 30Y Today 1W Today 1W Today 1W DE -42 -1 -26 -4 4 -2 FR -21 0 5 -5 35 -2 AT -5 0 17 3 41 5 NL -25 1 -4 -2 15 -2 ES 86 -26 116 -13 163 -9 BE 13 -6 35 -6 74 -4 PT 183 -36 214 -30 182 -20 IT 60 -3 98 -5 156 -8 GR 742 -27 599 -6 342 -10 US -24 -1 1 3 29 7 UK -28 -5 2 -6 36 -2 SZ -29 4 -42 3 -37 4

Source: Bloomberg, UniCredit Research

Chief Economist – UniCredit Group Head of Global Economics & FI/FX Research Marco Annunziata +44 20 7826-1770 [email protected] Head of Global FI & FX Research Michael Rottmann +49 89 378-15121 [email protected]

Editor Luca Cazzulani +39 02 8862-0640 [email protected]

Editorial deadline Friday, July 30, 2010 15:30 Prices as of Friday, July 30, 2010, 15:00 Bloomberg: UCGR Internet: www.research.unicreditgroup.eu

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 2 See last pages for disclaimer.

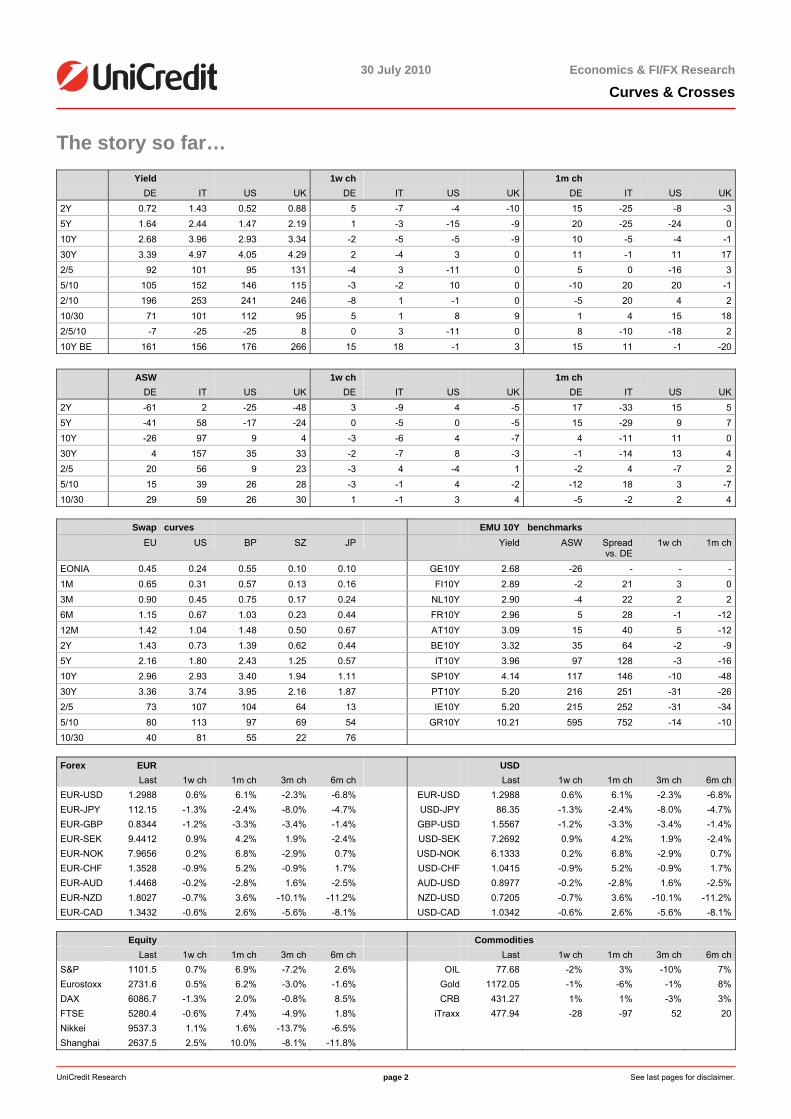

The story so far… Yield 1w ch 1m ch DE IT US UK DE IT US UK DE IT US UK2Y 0.72 1.43 0.52 0.88 5 -7 -4 -10 15 -25 -8 -35Y 1.64 2.44 1.47 2.19 1 -3 -15 -9 20 -25 -24 010Y 2.68 3.96 2.93 3.34 -2 -5 -5 -9 10 -5 -4 -130Y 3.39 4.97 4.05 4.29 2 -4 3 0 11 -1 11 172/5 92 101 95 131 -4 3 -11 0 5 0 -16 35/10 105 152 146 115 -3 -2 10 0 -10 20 20 -12/10 196 253 241 246 -8 1 -1 0 -5 20 4 210/30 71 101 112 95 5 1 8 9 1 4 15 182/5/10 -7 -25 -25 8 0 3 -11 0 8 -10 -18 210Y BE 161 156 176 266 15 18 -1 3 15 11 -1 -20 ASW 1w ch 1m ch DE IT US UK DE IT US UK DE IT US UK2Y -61 2 -25 -48 3 -9 4 -5 17 -33 15 55Y -41 58 -17 -24 0 -5 0 -5 15 -29 9 710Y -26 97 9 4 -3 -6 4 -7 4 -11 11 030Y 4 157 35 33 -2 -7 8 -3 -1 -14 13 42/5 20 56 9 23 -3 4 -4 1 -2 4 -7 25/10 15 39 26 28 -3 -1 4 -2 -12 18 3 -710/30 29 59 26 30 1 -1 3 4 -5 -2 2 4

Swap curves EMU 10Y benchmarks EU US BP SZ JP Yield ASW Spread

vs. DE 1w ch 1m ch

EONIA 0.45 0.24 0.55 0.10 0.10 GE10Y 2.68 -26 - - -1M 0.65 0.31 0.57 0.13 0.16 FI10Y 2.89 -2 21 3 03M 0.90 0.45 0.75 0.17 0.24 NL10Y 2.90 -4 22 2 26M 1.15 0.67 1.03 0.23 0.44 FR10Y 2.96 5 28 -1 -1212M 1.42 1.04 1.48 0.50 0.67 AT10Y 3.09 15 40 5 -122Y 1.43 0.73 1.39 0.62 0.44 BE10Y 3.32 35 64 -2 -95Y 2.16 1.80 2.43 1.25 0.57 IT10Y 3.96 97 128 -3 -1610Y 2.96 2.93 3.40 1.94 1.11 SP10Y 4.14 117 146 -10 -4830Y 3.36 3.74 3.95 2.16 1.87 PT10Y 5.20 216 251 -31 -262/5 73 107 104 64 13 IE10Y 5.20 215 252 -31 -345/10 80 113 97 69 54 GR10Y 10.21 595 752 -14 -1010/30 40 81 55 22 76

Forex EUR USD Last 1w ch 1m ch 3m ch 6m ch Last 1w ch 1m ch 3m ch 6m chEUR-USD 1.2988 0.6% 6.1% -2.3% -6.8% EUR-USD 1.2988 0.6% 6.1% -2.3% -6.8%EUR-JPY 112.15 -1.3% -2.4% -8.0% -4.7% USD-JPY 86.35 -1.3% -2.4% -8.0% -4.7%EUR-GBP 0.8344 -1.2% -3.3% -3.4% -1.4% GBP-USD 1.5567 -1.2% -3.3% -3.4% -1.4%EUR-SEK 9.4412 0.9% 4.2% 1.9% -2.4% USD-SEK 7.2692 0.9% 4.2% 1.9% -2.4%EUR-NOK 7.9656 0.2% 6.8% -2.9% 0.7% USD-NOK 6.1333 0.2% 6.8% -2.9% 0.7%EUR-CHF 1.3528 -0.9% 5.2% -0.9% 1.7% USD-CHF 1.0415 -0.9% 5.2% -0.9% 1.7%EUR-AUD 1.4468 -0.2% -2.8% 1.6% -2.5% AUD-USD 0.8977 -0.2% -2.8% 1.6% -2.5%EUR-NZD 1.8027 -0.7% 3.6% -10.1% -11.2% NZD-USD 0.7205 -0.7% 3.6% -10.1% -11.2%EUR-CAD 1.3432 -0.6% 2.6% -5.6% -8.1% USD-CAD 1.0342 -0.6% 2.6% -5.6% -8.1%

Equity Commodities Last 1w ch 1m ch 3m ch 6m ch Last 1w ch 1m ch 3m ch 6m chS&P 1101.5 0.7% 6.9% -7.2% 2.6% OIL 77.68 -2% 3% -10% 7%Eurostoxx 2731.6 0.5% 6.2% -3.0% -1.6% Gold 1172.05 -1% -6% -1% 8%DAX 6086.7 -1.3% 2.0% -0.8% 8.5% CRB 431.27 1% 1% -3% 3%FTSE 5280.4 -0.6% 7.4% -4.9% 1.8% iTraxx 477.94 -28 -97 52 20Nikkei 9537.3 1.1% 1.6% -13.7% -6.5% Shanghai 2637.5 2.5% 10.0% -8.1% -11.8%

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 3 See last pages for disclaimer.

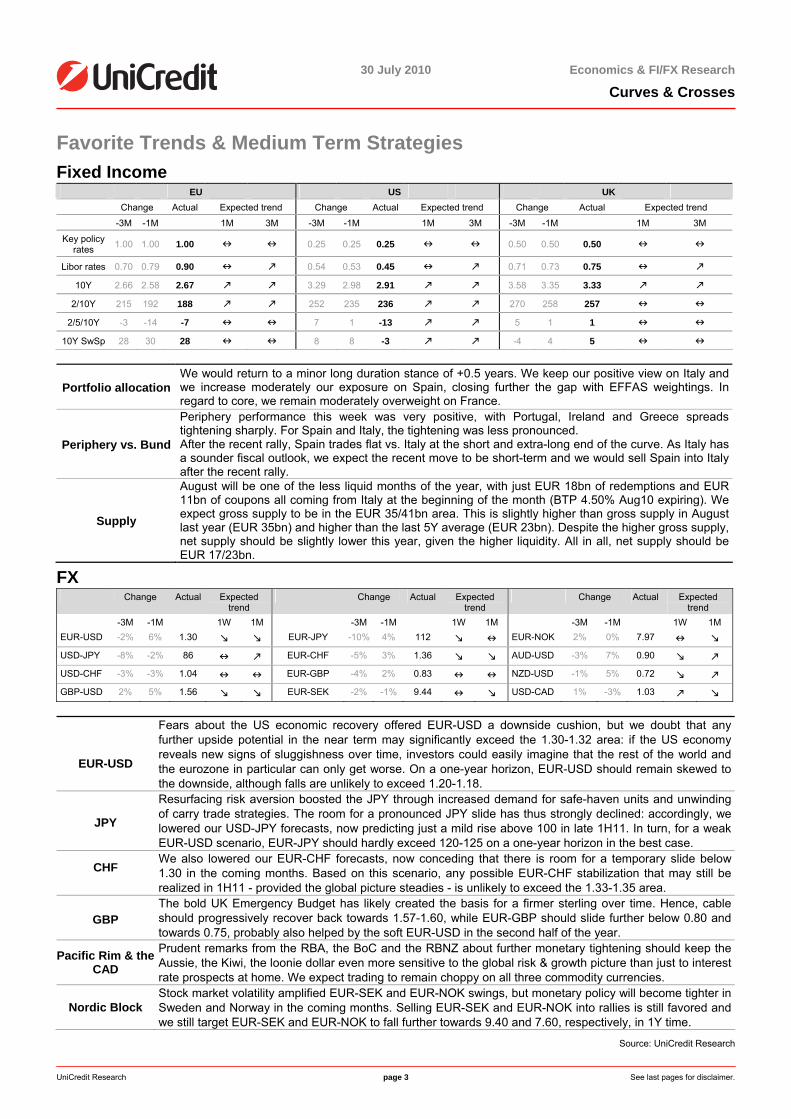

Favorite Trends & Medium Term Strategies Fixed Income EU US UK Change Actual Expected trend Change Actual Expected trend Change Actual Expected trend

-3M -1M 1M 3M -3M -1M 1M 3M -3M -1M 1M 3M

Key policy rates 1.00 1.00 1.00 0.25 0.25 0.25 0.50 0.50 0.50

Libor rates 0.70 0.79 0.90 0.54 0.53 0.45 0.71 0.73 0.75

10Y 2.66 2.58 2.67 3.29 2.98 2.91 3.58 3.35 3.33

2/10Y 215 192 188 252 235 236 270 258 257

2/5/10Y -3 -14 -7 7 1 -13 5 1 1

10Y SwSp 28 30 28 8 8 -3 -4 4 5

Portfolio allocation We would return to a minor long duration stance of +0.5 years. We keep our positive view on Italy and we increase moderately our exposure on Spain, closing further the gap with EFFAS weightings. In regard to core, we remain moderately overweight on France.

Periphery vs. Bund

Periphery performance this week was very positive, with Portugal, Ireland and Greece spreads tightening sharply. For Spain and Italy, the tightening was less pronounced. After the recent rally, Spain trades flat vs. Italy at the short and extra-long end of the curve. As Italy has a sounder fiscal outlook, we expect the recent move to be short-term and we would sell Spain into Italy after the recent rally.

Supply

August will be one of the less liquid months of the year, with just EUR 18bn of redemptions and EUR 11bn of coupons all coming from Italy at the beginning of the month (BTP 4.50% Aug10 expiring). We expect gross supply to be in the EUR 35/41bn area. This is slightly higher than gross supply in August last year (EUR 35bn) and higher than the last 5Y average (EUR 23bn). Despite the higher gross supply, net supply should be slightly lower this year, given the higher liquidity. All in all, net supply should be EUR 17/23bn.

FX Change Actual Expected

trend Change Actual Expected

trend Change Actual Expected

trend -3M -1M 1W 1M -3M -1M 1W 1M -3M -1M 1W 1M EUR-USD -2% 6% 1.30 EUR-JPY -10% 4% 112 EUR-NOK 2% 0% 7.97 USD-JPY -8% -2% 86 EUR-CHF -5% 3% 1.36 AUD-USD -3% 7% 0.90 USD-CHF -3% -3% 1.04 EUR-GBP -4% 2% 0.83 NZD-USD -1% 5% 0.72 GBP-USD 2% 5% 1.56 EUR-SEK -2% -1% 9.44 USD-CAD 1% -3% 1.03

EUR-USD

Fears about the US economic recovery offered EUR-USD a downside cushion, but we doubt that any further upside potential in the near term may significantly exceed the 1.30-1.32 area: if the US economy reveals new signs of sluggishness over time, investors could easily imagine that the rest of the world and the eurozone in particular can only get worse. On a one-year horizon, EUR-USD should remain skewed to the downside, although falls are unlikely to exceed 1.20-1.18.

JPY

Resurfacing risk aversion boosted the JPY through increased demand for safe-haven units and unwinding of carry trade strategies. The room for a pronounced JPY slide has thus strongly declined: accordingly, we lowered our USD-JPY forecasts, now predicting just a mild rise above 100 in late 1H11. In turn, for a weak EUR-USD scenario, EUR-JPY should hardly exceed 120-125 on a one-year horizon in the best case.

CHF

We also lowered our EUR-CHF forecasts, now conceding that there is room for a temporary slide below 1.30 in the coming months. Based on this scenario, any possible EUR-CHF stabilization that may still be realized in 1H11 - provided the global picture steadies - is unlikely to exceed the 1.33-1.35 area.

GBP The bold UK Emergency Budget has likely created the basis for a firmer sterling over time. Hence, cable should progressively recover back towards 1.57-1.60, while EUR-GBP should slide further below 0.80 and towards 0.75, probably also helped by the soft EUR-USD in the second half of the year.

Pacific Rim & the CAD

Prudent remarks from the RBA, the BoC and the RBNZ about further monetary tightening should keep the Aussie, the Kiwi, the loonie dollar even more sensitive to the global risk & growth picture than just to interest rate prospects at home. We expect trading to remain choppy on all three commodity currencies.

Nordic Block Stock market volatility amplified EUR-SEK and EUR-NOK swings, but monetary policy will become tighter in Sweden and Norway in the coming months. Selling EUR-SEK and EUR-NOK into rallies is still favored and we still target EUR-SEK and EUR-NOK to fall further towards 9.40 and 7.60, respectively, in 1Y time.

Source: UniCredit Research

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 4 See last pages for disclaimer.

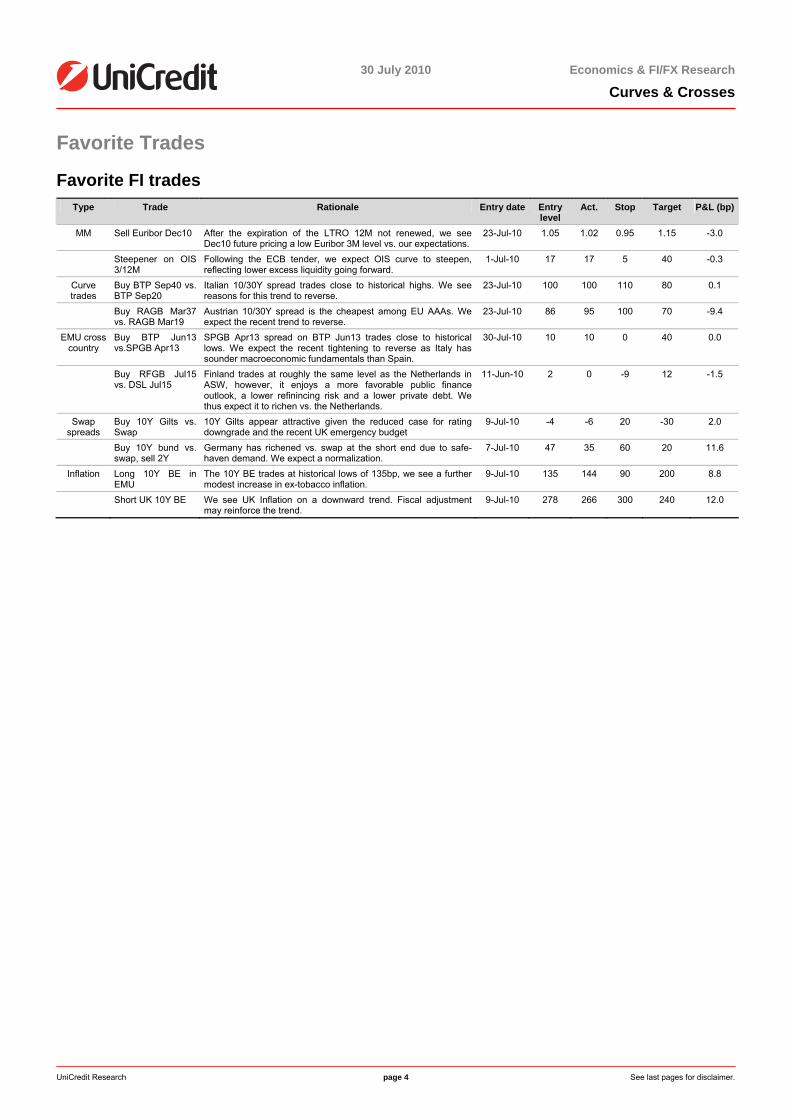

Favorite Trades

Favorite FI trades Type Trade Rationale Entry date Entry

level Act. Stop Target P&L (bp)

MM Sell Euribor Dec10 After the expiration of the LTRO 12M not renewed, we see Dec10 future pricing a low Euribor 3M level vs. our expectations.

23-Jul-10 1.05 1.02 0.95 1.15 -3.0

Steepener on OIS 3/12M

Following the ECB tender, we expect OIS curve to steepen, reflecting lower excess liquidity going forward.

1-Jul-10 17 17 5 40 -0.3

Curve trades

Buy BTP Sep40 vs. BTP Sep20

Italian 10/30Y spread trades close to historical highs. We see reasons for this trend to reverse.

23-Jul-10 100 100 110 80 0.1

Buy RAGB Mar37 vs. RAGB Mar19

Austrian 10/30Y spread is the cheapest among EU AAAs. We expect the recent trend to reverse.

23-Jul-10 86 95 100 70 -9.4

EMU cross country

Buy BTP Jun13 vs.SPGB Apr13

SPGB Apr13 spread on BTP Jun13 trades close to historical lows. We expect the recent tightening to reverse as Italy has sounder macroeconomic fundamentals than Spain.

30-Jul-10 10 10 0 40 0.0

Buy RFGB Jul15 vs. DSL Jul15

Finland trades at roughly the same level as the Netherlands in ASW, however, it enjoys a more favorable public finance outlook, a lower refinincing risk and a lower private debt. We thus expect it to richen vs. the Netherlands.

11-Jun-10 2 0 -9 12 -1.5

Swap spreads

Buy 10Y Gilts vs. Swap

10Y Gilts appear attractive given the reduced case for rating downgrade and the recent UK emergency budget

9-Jul-10 -4 -6 20 -30 2.0

Buy 10Y bund vs. swap, sell 2Y

Germany has richened vs. swap at the short end due to safe-haven demand. We expect a normalization.

7-Jul-10 47 35 60 20 11.6

Inflation Long 10Y BE in EMU

The 10Y BE trades at historical lows of 135bp, we see a further modest increase in ex-tobacco inflation.

9-Jul-10 135 144 90 200 8.8

Short UK 10Y BE We see UK Inflation on a downward trend. Fiscal adjustment may reinforce the trend.

9-Jul-10 278 266 300 240 12.0

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 5 See last pages for disclaimer.

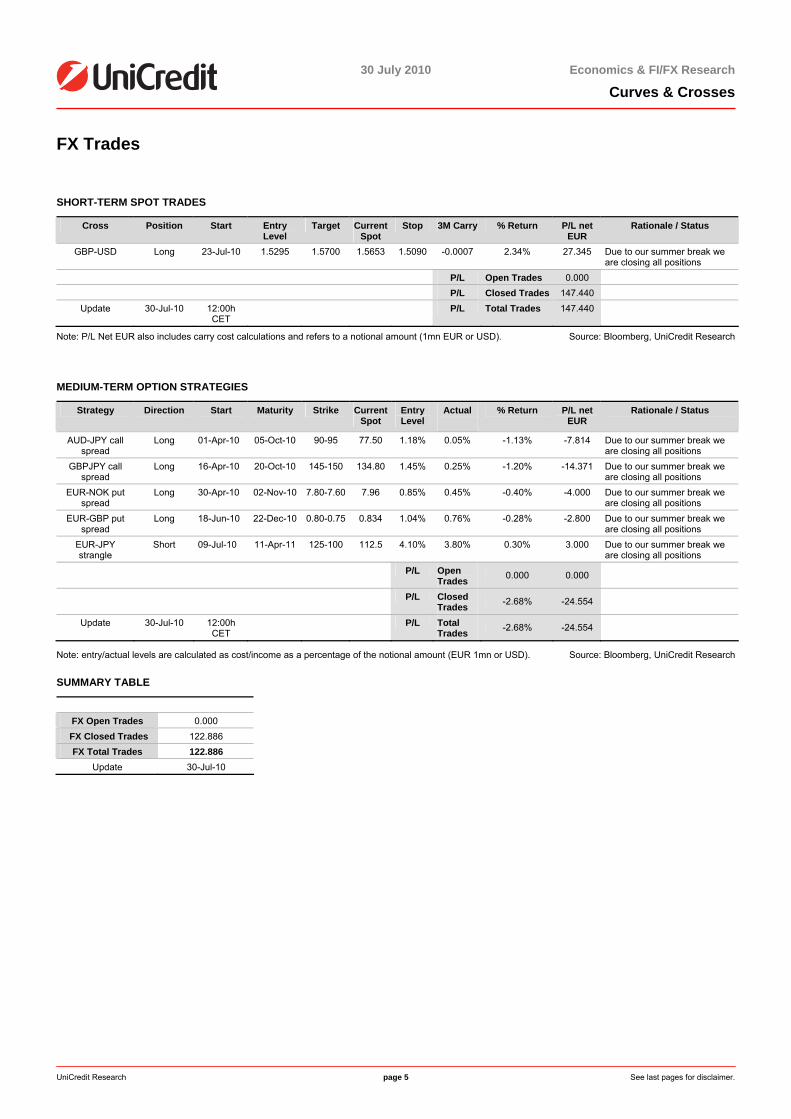

FX Trades

SHORT-TERM SPOT TRADES

Cross Position Start Entry Level

Target Current Spot

Stop 3M Carry % Return P/L net EUR

Rationale / Status

GBP-USD Long 23-Jul-10 1.5295 1.5700 1.5653 1.5090 -0.0007 2.34% 27.345 Due to our summer break we are closing all positions

P/L Open Trades 0.000 P/L Closed Trades 147.440

Update 30-Jul-10 12:00h CET

P/L Total Trades 147.440

Note: P/L Net EUR also includes carry cost calculations and refers to a notional amount (1mn EUR or USD). Source: Bloomberg, UniCredit Research

MEDIUM-TERM OPTION STRATEGIES

Strategy Direction Start Maturity Strike Current Spot

Entry Level

Actual

% Return P/L net EUR

Rationale / Status

AUD-JPY call spread

Long 01-Apr-10 05-Oct-10 90-95 77.50 1.18% 0.05% -1.13% -7.814 Due to our summer break we are closing all positions

GBPJPY call spread

Long 16-Apr-10 20-Oct-10 145-150 134.80 1.45% 0.25% -1.20% -14.371 Due to our summer break we are closing all positions

EUR-NOK put spread

Long 30-Apr-10 02-Nov-10 7.80-7.60 7.96 0.85% 0.45% -0.40% -4.000 Due to our summer break we are closing all positions

EUR-GBP put spread

Long 18-Jun-10 22-Dec-10 0.80-0.75 0.834 1.04% 0.76% -0.28% -2.800 Due to our summer break we are closing all positions

EUR-JPY strangle

Short 09-Jul-10 11-Apr-11 125-100 112.5 4.10% 3.80% 0.30% 3.000 Due to our summer break we are closing all positions

P/L Open Trades 0.000 0.000

P/L Closed Trades -2.68% -24.554

Update 30-Jul-10 12:00h CET

P/L Total Trades -2.68% -24.554

Note: entry/actual levels are calculated as cost/income as a percentage of the notional amount (EUR 1mn or USD). Source: Bloomberg, UniCredit Research

SUMMARY TABLE

FX Open Trades 0.000

FX Closed Trades 122.886 FX Total Trades 122.886

Update 30-Jul-10

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 6 See last pages for disclaimer.

FI Strategizer

Cautiousness to prevail in the summer break Chiara Cremonesi (UniCredit Bank London) +44 207 826 1771 [email protected] Investors have adopted a constructive approach vs. the stress test results publication this week… …while in the US they concentrate on the dovish message coming from macroeconomic data and Fed’s officials

Investors showed a constructive approach after the publication of the stress test results last week. While a few critical issues have been highlighted this week, (for example, the use of the Tier 1 ratio biased the results on the positive side; on the assumption side, the exclusion ofthe hypothesis of default was rather optimistic, as well as the fact that haircuts on sovereign bonds have been applied only to the trading book), the market preferred to concentrate on the increase in transparency in the system brought about by the stress test publication. Indeed, expectations were rather low ahead of the publication, so therather detailed assumptions were a positive surprise. Data wise, in the eurozone, the EMU economic sentiment was up strongly in July (from 99 to 101.3) and the flash estimate for EMU CPI came in at 1.7%, rising from the previous 1.4% In the US, while housing data (new home sales and the S&P CaseShiller) came in above expectations, consumer confidence and durable goods orders were quite disappointing. The advanced release of 2Q GDP came in at 2.4%, slightly below expectations, with a rather weakconsumption component. The Fed’s Beige Book delivered a soft message. Finally, Fed’s Bullard underlined the risks of deflation in the Fed’s Minutes. While market sentiment has remained mildly positive in the EMU, in the US investorsconcentrated on the dovish messages coming from macroeconomic data and Fed’s officials.

All in all, after a positive start of the week for risky assets, risk aversion resurfaced slightly.Stocks were moderately down with the DAX decreasing 1.2% and the S&P decreasing 0.1%. In the EMU, a mild optimism weighed on Bunds, especially at the short end, while in the US,Treasuries were supported by further signs of an economic slowdown. US Treasuries outperformed Bunds at the short end.

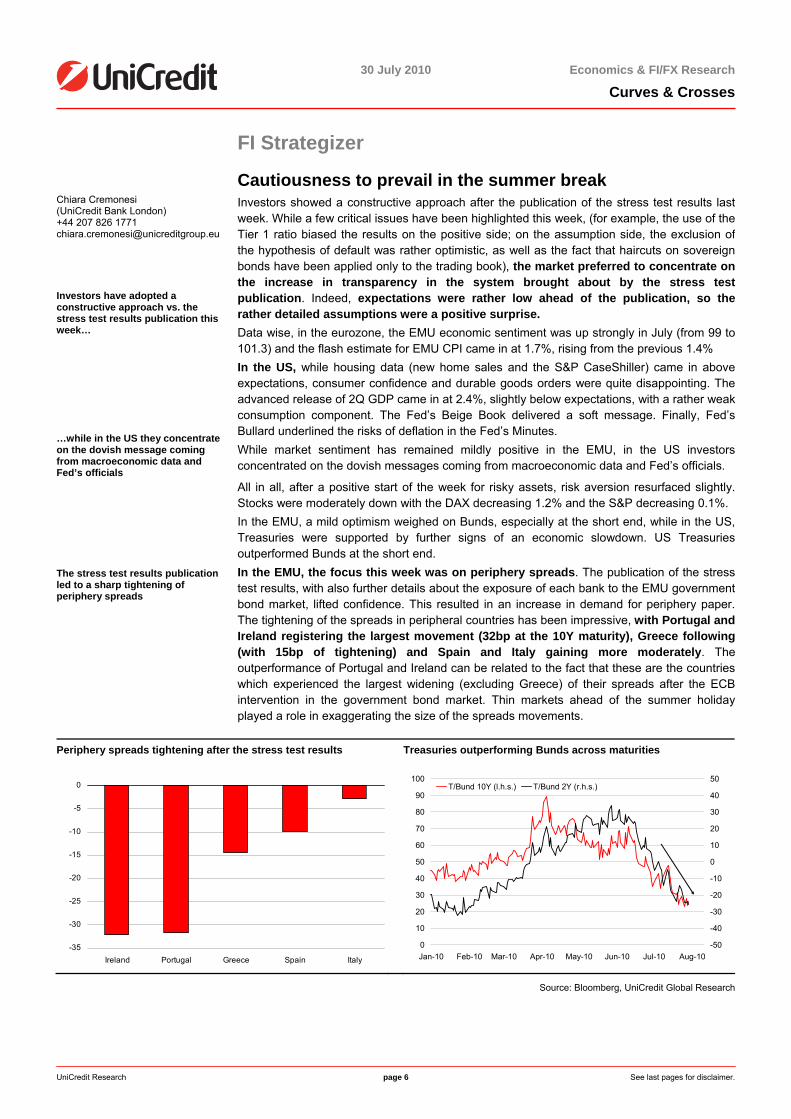

The stress test results publication led to a sharp tightening of periphery spreads

In the EMU, the focus this week was on periphery spreads. The publication of the stress test results, with also further details about the exposure of each bank to the EMU governmentbond market, lifted confidence. This resulted in an increase in demand for periphery paper.The tightening of the spreads in peripheral countries has been impressive, with Portugal and Ireland registering the largest movement (32bp at the 10Y maturity), Greece following (with 15bp of tightening) and Spain and Italy gaining more moderately. The outperformance of Portugal and Ireland can be related to the fact that these are the countrieswhich experienced the largest widening (excluding Greece) of their spreads after the ECBintervention in the government bond market. Thin markets ahead of the summer holiday played a role in exaggerating the size of the spreads movements.

Periphery spreads tightening after the stress test results Treasuries outperforming Bunds across maturities

-35

-30

-25

-20

-15

-10

-5

0

Ireland Portugal Greece Spain Italy

0

10

20

30

40

50

60

70

80

90

100

Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10-50

-40

-30

-20

-10

0

10

20

30

40

50T/Bund 10Y (l.h.s.) T/Bund 2Y (r.h.s.)

Source: Bloomberg, UniCredit Global Research

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 7 See last pages for disclaimer.

3M ECB auction delivered a positive message

The constructive market reaction after the stress test publication is also consistent with the outcome of the ECB 3M auction this week. Demand was EUR 23.16bn, vs. EUR 4.8bn expiring, leading to a EUR 18bn increase in liquidity. As the increase in liquidity wasmodest (EUR 18.3bn), we interpret it as an adjustment after the sizeable decrease in liquidityover the last few weeks. The number of banks participating was 70, which compares favorably with the 171 banksparticipating at the end of June 3M, even taking into account the different environment. Backin June the number of banks was especially high because market participants were rollingover the expiry of the 12M LTRO. All in all, the 3M auction result was reassuring as it seems to confirm that the EU banking system is sound. MM rates put on another 1.5bp during the week. While the trendof increase remains intact, the pace has slightly decreased over the last week.

Next week's data calendar in the US…

Next week, the data calendar will be rather heavy, with ISM and non farm payrolls in the US and the ECB meeting in the EMU.

In the US, ISM Manufacturing should post another decrease, reflecting the fading away of the inventory cycle support and signs of a slowdown in the global economy. We expect the non farm payrolls to come in at -75K, improving from -125K registered in June. The unemployment rate should fall slightly to 9.5% from the previous 9.6%, however, the decline should have been caused again by a decrease in the labor force rather than by an improvement in employment. Data in the US next week should again confirm the currentslowdown in the economic cycle. Bernanke’s speech on Monday should not add any newelement to the recent Fed’s rhetoric.

…and in the EMU In the EMU, the focus should be on the ECB meeting. We do not expect any major surprise here. Trichet will likely welcome the stress test results as a major step towards a higher degree of transparency and coordination of the EU banking system. As far as themacroeconomic outlook is concerned, even though the most recent set of growth indicatorsvindicate the ECB's view that higher short term rates won't jeopardize the recovery, Trichet onThursday will continue to sound cautious on future growth prospects, not least because the lending cycle has not yet turned. Aside from this, June factory orders and industrial productionfigures will be released in Germany. We expect a strong reading for factory orders and IP topost another positive reading in line with the scenario of acceleration in the economic recovery in Germany.

Bond-friendly supply in the EMU and no supply in the US

Supply in the EMU should be friendly, as there should be only EUR 4bn of gross supplycoming from Austria and Spain. In the US, no supply is scheduled.

Macroeconomic data and the absence of supply pressure to support Treasuries next week

All in all, another round of soft data in the US and the absence of supply should favorbonds next week. Over the last few days, the 2Y has come back to trade in the 0.55% area, at its record lows, so we see little room here for a further rally. We see the 2Y Treasury likely to trade in the 0.55/0.60% range, while the 10Y yield should trade in the 2.90/2.95% range.

Optimism should lose momentum in the EMU, but strong data in Germany could support risk appetite

In the EMU, the impact of the optimism observed after the stress test results should lose some steam. However, strong data in Germany could provide some support to risk appetite.This should hit Bunds, with the 2Y yields rising again towards 0.85% and the 10Y towards 2.75%.

In regard to periphery spreads, the stress test has surely been a major trigger to install someconfidence, as shown by the fact that the tightening of periphery spreads following the publication of the stress test results has been very relevant. However, the positive reactionmay be similar to that observed after the ECB intervention in the government bonds marketand after the announcement of the fiscal consolidation programs by the EMU countries, basically short lived. Indeed, market mood on periphery remains fragile and vulnerable to bad news, as also confirmed by the widening or Irish spreads yesterday on Fitch worries on theIrish banking system and this morning on Moody’s remarks about a possible downgrade ofSpain.

A glance at the UK… Finally, in the UK next week, the July manufacturing and service PMIs and the June industrial production figures will be released, while the BoE will hold its meeting.

The PMIs should keep signaling a slowdown in economic activity from the very strongperformance recorded in 2Q, while June factory output might have increased less than in the

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 8 See last pages for disclaimer.

previous month (we expect 0.2% mom).

We do not expect major surprises at the BoE meeting. We do not expect major surprises atthe BoE meeting. Gilts are actually trading at their record low levels. Mixed data next weekshould keep Gilt yields in the current trading range.

August trends in the FI market For the rest of August, investors should continue to lean on the cautious side. More evidence that the US economy is slowing down should continue to support the US Treasuries. In the eurozone, investors should remain slightly more positive, after that a few measures have been put in place in order to restore some confidence in the market following the burst of the sovereign debt crisis. However, also in the EMU uncertainty remains highon periphery and this should keep investors on the prudent side.

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 9 See last pages for disclaimer.

Real Money Section: Euroland Portfolio Strategy

Back to a minor long duration stance Michael Rottmann (UniCredit Bank) +49 89 378-15121 [email protected]

The only thing booming these days is prophecies of doom. Anyone trying to catch a headline has to predict at least a sovereign default, a double-dip recession or deflation. In this regard, financial market commentators responded to the stress test as is their wont: missedopportunity, stress scenario too lax, markdowns on government bonds should have related not only to the exposure in the prop book, and the list goes on and on …

However, investors were deaf to these arguments. In a world dominated by numbers,psychology is apparently to some extent more important. Despite several hundred pages of critical research material immediately before and after the publication of the European stresstest results, the simulation we discussed over the last two weeks was spot on in terms of thedevelopment of currencies and fixed income markets. The EUR-USD exchange rate, the trade-weighted USD, and even yield movements in the euro zone reacted as suggested bythe experience of the US stress test - almost to the decimal place.

Psychology outperformed interpretation

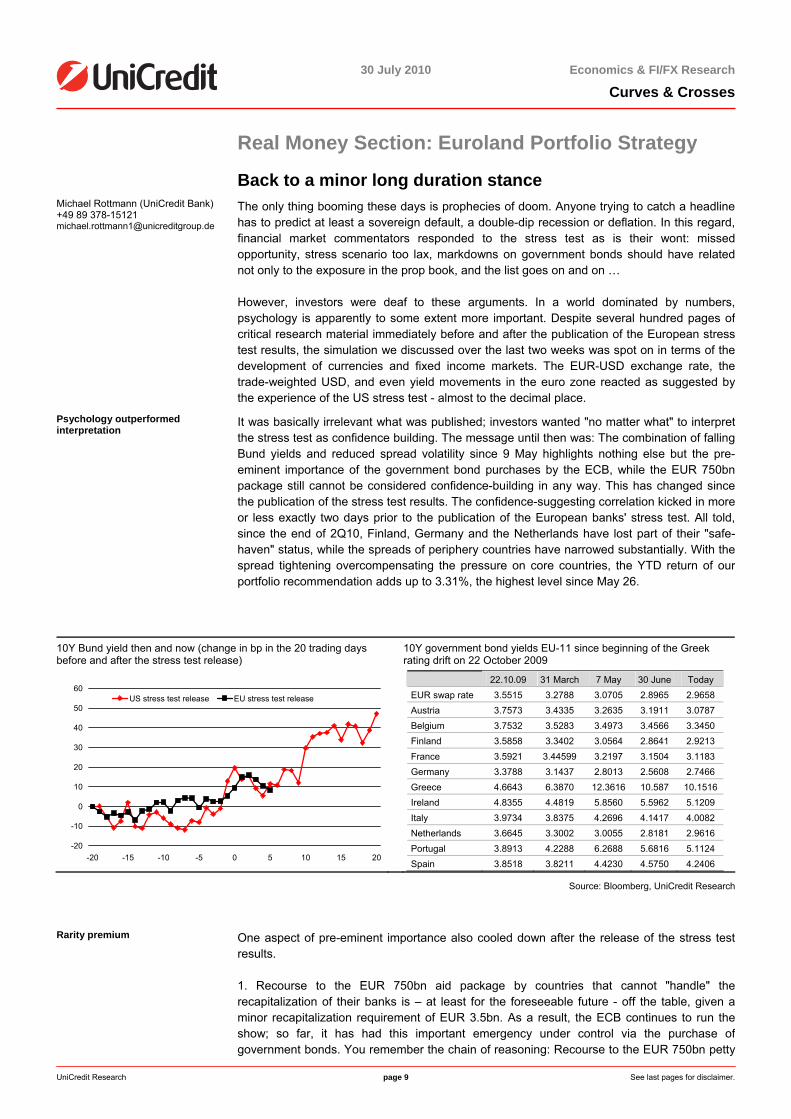

It was basically irrelevant what was published; investors wanted "no matter what" to interpretthe stress test as confidence building. The message until then was: The combination of fallingBund yields and reduced spread volatility since 9 May highlights nothing else but the pre-eminent importance of the government bond purchases by the ECB, while the EUR 750bnpackage still cannot be considered confidence-building in any way. This has changed since the publication of the stress test results. The confidence-suggesting correlation kicked in more or less exactly two days prior to the publication of the European banks' stress test. All told,since the end of 2Q10, Finland, Germany and the Netherlands have lost part of their "safe-haven" status, while the spreads of periphery countries have narrowed substantially. With the spread tightening overcompensating the pressure on core countries, the YTD return of ourportfolio recommendation adds up to 3.31%, the highest level since May 26.

10Y Bund yield then and now (change in bp in the 20 trading days before and after the stress test release)

10Y government bond yields EU-11 since beginning of the Greek rating drift on 22 October 2009

-20

-10

0

10

20

30

40

50

60

-20 -15 -10 -5 0 5 10 15 20

US stress test release EU stress test release 22.10.09 31 March 7 May 30 June Today

EUR swap rate 3.5515 3.2788 3.0705 2.8965 2.9658 Austria 3.7573 3.4335 3.2635 3.1911 3.0787 Belgium 3.7532 3.5283 3.4973 3.4566 3.3450 Finland 3.5858 3.3402 3.0564 2.8641 2.9213 France 3.5921 3.44599 3.2197 3.1504 3.1183 Germany 3.3788 3.1437 2.8013 2.5608 2.7466 Greece 4.6643 6.3870 12.3616 10.587 10.1516 Ireland 4.8355 4.4819 5.8560 5.5962 5.1209 Italy 3.9734 3.8375 4.2696 4.1417 4.0082 Netherlands 3.6645 3.3002 3.0055 2.8181 2.9616 Portugal 3.8913 4.2288 6.2688 5.6816 5.1124 Spain 3.8518 3.8211 4.4230 4.5750 4.2406

Source: Bloomberg, UniCredit Research

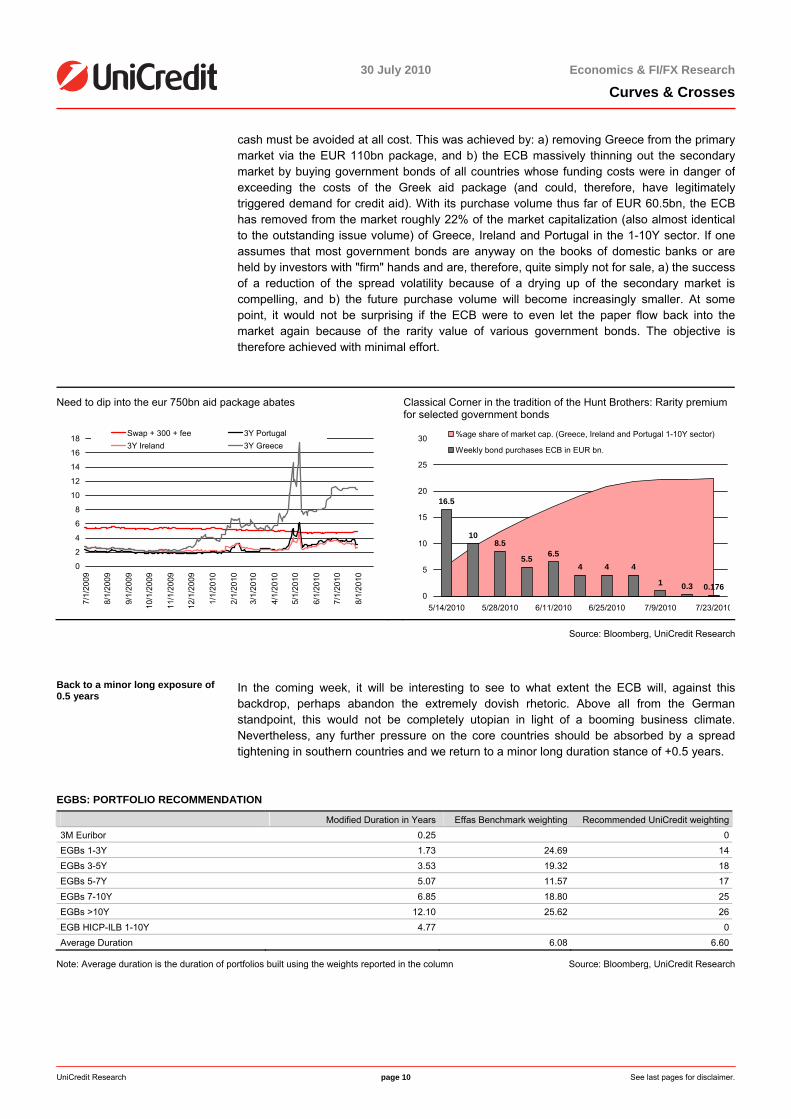

Rarity premium One aspect of pre-eminent importance also cooled down after the release of the stress test

results.

1. Recourse to the EUR 750bn aid package by countries that cannot "handle" therecapitalization of their banks is – at least for the foreseeable future - off the table, given a minor recapitalization requirement of EUR 3.5bn. As a result, the ECB continues to run theshow; so far, it has had this important emergency under control via the purchase ofgovernment bonds. You remember the chain of reasoning: Recourse to the EUR 750bn petty

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 10 See last pages for disclaimer.

cash must be avoided at all cost. This was achieved by: a) removing Greece from the primarymarket via the EUR 110bn package, and b) the ECB massively thinning out the secondarymarket by buying government bonds of all countries whose funding costs were in danger ofexceeding the costs of the Greek aid package (and could, therefore, have legitimatelytriggered demand for credit aid). With its purchase volume thus far of EUR 60.5bn, the ECBhas removed from the market roughly 22% of the market capitalization (also almost identicalto the outstanding issue volume) of Greece, Ireland and Portugal in the 1-10Y sector. If one assumes that most government bonds are anyway on the books of domestic banks or are held by investors with "firm" hands and are, therefore, quite simply not for sale, a) the successof a reduction of the spread volatility because of a drying up of the secondary market iscompelling, and b) the future purchase volume will become increasingly smaller. At some point, it would not be surprising if the ECB were to even let the paper flow back into themarket again because of the rarity value of various government bonds. The objective istherefore achieved with minimal effort.

Need to dip into the eur 750bn aid package abates Classical Corner in the tradition of the Hunt Brothers: Rarity premium for selected government bonds

0

2

4

6

8

10

12

14

16

18

7/1/

2009

8/1/

2009

9/1/

2009

10/1

/200

9

11/1

/200

9

12/1

/200

9

1/1/

2010

2/1/

2010

3/1/

2010

4/1/

2010

5/1/

2010

6/1/

2010

7/1/

2010

8/1/

2010

Swap + 300 + fee 3Y Portugal3Y Ireland 3Y Greece

16.5

108.5

5.5 6.54 4 4

1 0.3 0.1760

5

10

15

20

25

30

5/14/2010 5/28/2010 6/11/2010 6/25/2010 7/9/2010 7/23/2010

%age share of market cap. (Greece, Ireland and Portugal 1-10Y sector)

Weekly bond purchases ECB in EUR bn.

Source: Bloomberg, UniCredit Research

Back to a minor long exposure of 0.5 years

In the coming week, it will be interesting to see to what extent the ECB will, against thisbackdrop, perhaps abandon the extremely dovish rhetoric. Above all from the Germanstandpoint, this would not be completely utopian in light of a booming business climate.Nevertheless, any further pressure on the core countries should be absorbed by a spreadtightening in southern countries and we return to a minor long duration stance of +0.5 years.

EGBS: PORTFOLIO RECOMMENDATION

Modified Duration in Years Effas Benchmark weighting Recommended UniCredit weighting3M Euribor 0.25 0EGBs 1-3Y 1.73 24.69 14EGBs 3-5Y 3.53 19.32 18EGBs 5-7Y 5.07 11.57 17EGBs 7-10Y 6.85 18.80 25EGBs >10Y 12.10 25.62 26EGB HICP-ILB 1-10Y 4.77 0Average Duration 6.08 6.60

Note: Average duration is the duration of portfolios built using the weights reported in the column Source: Bloomberg, UniCredit Research

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 11 See last pages for disclaimer.

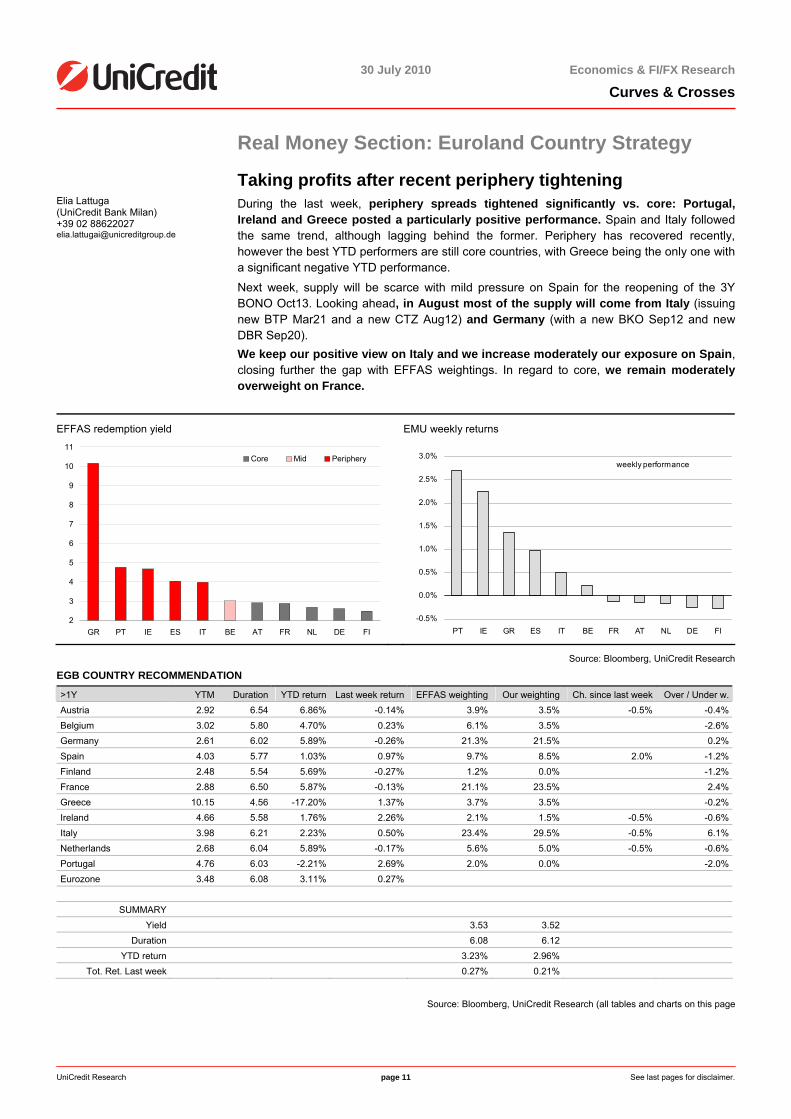

Real Money Section: Euroland Country Strategy

Taking profits after recent periphery tightening Elia Lattuga (UniCredit Bank Milan) +39 02 88622027 [email protected]

During the last week, periphery spreads tightened significantly vs. core: Portugal,Ireland and Greece posted a particularly positive performance. Spain and Italy followed the same trend, although lagging behind the former. Periphery has recovered recently, however the best YTD performers are still core countries, with Greece being the only one witha significant negative YTD performance.

Next week, supply will be scarce with mild pressure on Spain for the reopening of the 3Y BONO Oct13. Looking ahead, in August most of the supply will come from Italy (issuing new BTP Mar21 and a new CTZ Aug12) and Germany (with a new BKO Sep12 and new DBR Sep20). We keep our positive view on Italy and we increase moderately our exposure on Spain, closing further the gap with EFFAS weightings. In regard to core, we remain moderately overweight on France.

EFFAS redemption yield EMU weekly returns

2

3

4

5

6

7

8

9

10

11

GR PT IE ES IT BE AT FR NL DE FI

Core Mid Periphery

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

PT IE GR ES IT BE FR AT NL DE FI

weekly performance

Source: Bloomberg, UniCredit Research

EGB COUNTRY RECOMMENDATION

>1Y YTM Duration YTD return Last week return EFFAS weighting Our weighting Ch. since last week Over / Under w.Austria 2.92 6.54 6.86% -0.14% 3.9% 3.5% -0.5% -0.4%Belgium 3.02 5.80 4.70% 0.23% 6.1% 3.5% -2.6%Germany 2.61 6.02 5.89% -0.26% 21.3% 21.5% 0.2%Spain 4.03 5.77 1.03% 0.97% 9.7% 8.5% 2.0% -1.2%Finland 2.48 5.54 5.69% -0.27% 1.2% 0.0% -1.2%France 2.88 6.50 5.87% -0.13% 21.1% 23.5% 2.4%Greece 10.15 4.56 -17.20% 1.37% 3.7% 3.5% -0.2%Ireland 4.66 5.58 1.76% 2.26% 2.1% 1.5% -0.5% -0.6%Italy 3.98 6.21 2.23% 0.50% 23.4% 29.5% -0.5% 6.1%Netherlands 2.68 6.04 5.89% -0.17% 5.6% 5.0% -0.5% -0.6%Portugal 4.76 6.03 -2.21% 2.69% 2.0% 0.0% -2.0%Eurozone 3.48 6.08 3.11% 0.27%

SUMMARY

Yield 3.53 3.52 Duration 6.08 6.12

YTD return 3.23% 2.96% Tot. Ret. Last week 0.27% 0.21%

Source: Bloomberg, UniCredit Research (all tables and charts on this page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 12 See last pages for disclaimer.

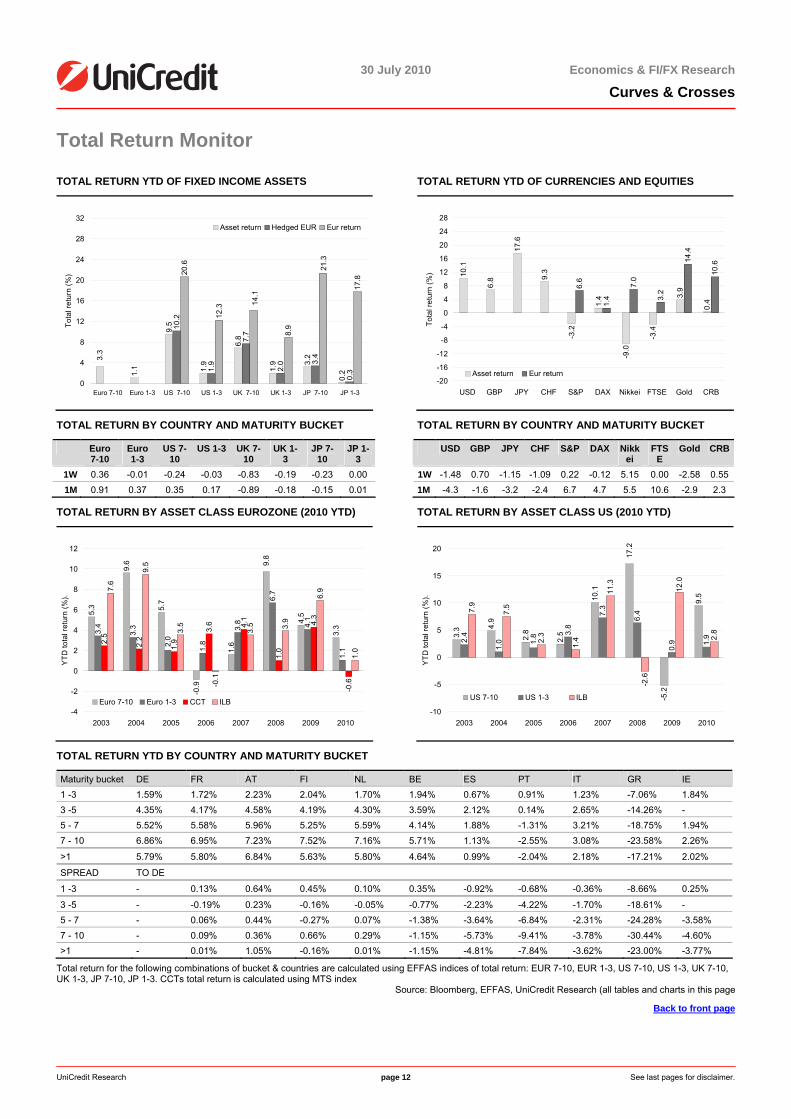

Total Return Monitor

TOTAL RETURN YTD OF FIXED INCOME ASSETS

1.1

9.5

1.9

6.8

1.9 3.

2

0.2

10.2

1.9

7.7

2.0 3.

4

0.3

20.6

12.3

8.9

17.8

3.3

14.1

21.3

0

4

8

12

16

20

24

28

32

Euro 7-10 Euro 1-3 US 7-10 US 1-3 UK 7-10 UK 1-3 JP 7-10 JP 1-3

Tota

l ret

urn

(%)

Asset return Hedged EUR Eur return

TOTAL RETURN YTD OF CURRENCIES AND EQUITIES

10.1

6.8

17.6

9.3

-3.2

1.4

-9.0

-3.4

3.9

0.4

6.6

1.4

7.0

3.2

14.4

10.6

-20

-16

-12

-8

-4

0

4

8

12

16

20

24

28

USD GBP JPY CHF S&P DAX Nikkei FTSE Gold CRB

Tota

l ret

urn

(%)

Asset return Eur return

TOTAL RETURN BY COUNTRY AND MATURITY BUCKET

Euro 7-10

Euro 1-3

US 7-10

US 1-3 UK 7-10

UK 1-3

JP 7-10

JP 1-3

1W 0.36 -0.01 -0.24 -0.03 -0.83 -0.19 -0.23 0.00 1M 0.91 0.37 0.35 0.17 -0.89 -0.18 -0.15 0.01

TOTAL RETURN BY ASSET CLASS EUROZONE (2010 YTD)

5.3

9.6

5.7

-0.9

1.6

4.5

3.33.4

3.3

1.8

3.8

6.7

4.1

1.1

2.5

2.2

1.9

3.6 4.

1

1.0

4.3

-0.6

7.6

9.5

3.5

-0.1

3.5 3.9

6.9

1.0

9.8

2.0

-4

-2

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010

YTD

tota

l ret

urn

(%).

Euro 7-10 Euro 1-3 CCT ILB

TOTAL RETURN BY COUNTRY AND MATURITY BUCKET

USD GBP JPY CHF S&P DAX Nikkei

FTSE

Gold CRB

1W -1.48 0.70 -1.15 -1.09 0.22 -0.12 5.15 0.00 -2.58 0.55 1M -4.3 -1.6 -3.2 -2.4 6.7 4.7 5.5 10.6 -2.9 2.3

TOTAL RETURN BY ASSET CLASS US (2010 YTD)

3.3 4.

9

2.8

2.5

10.1

-5.2

9.5

2.4

1.0

3.8

7.3

6.4

0.9 1.

9

7.9

7.5

2.3

1.4

11.3

-2.6

2.8

17.2

1.8

12.0

-10

-5

0

5

10

15

20

2003 2004 2005 2006 2007 2008 2009 2010

YTD

tota

l ret

urn

(%).

US 7-10 US 1-3 ILB

TOTAL RETURN YTD BY COUNTRY AND MATURITY BUCKET

Maturity bucket DE FR AT FI NL BE ES PT IT GR IE 1 -3 1.59% 1.72% 2.23% 2.04% 1.70% 1.94% 0.67% 0.91% 1.23% -7.06% 1.84% 3 -5 4.35% 4.17% 4.58% 4.19% 4.30% 3.59% 2.12% 0.14% 2.65% -14.26% - 5 - 7 5.52% 5.58% 5.96% 5.25% 5.59% 4.14% 1.88% -1.31% 3.21% -18.75% 1.94% 7 - 10 6.86% 6.95% 7.23% 7.52% 7.16% 5.71% 1.13% -2.55% 3.08% -23.58% 2.26%

>1 5.79% 5.80% 6.84% 5.63% 5.80% 4.64% 0.99% -2.04% 2.18% -17.21% 2.02%

SPREAD TO DE

1 -3 - 0.13% 0.64% 0.45% 0.10% 0.35% -0.92% -0.68% -0.36% -8.66% 0.25%

3 -5 - -0.19% 0.23% -0.16% -0.05% -0.77% -2.23% -4.22% -1.70% -18.61% - 5 - 7 - 0.06% 0.44% -0.27% 0.07% -1.38% -3.64% -6.84% -2.31% -24.28% -3.58% 7 - 10 - 0.09% 0.36% 0.66% 0.29% -1.15% -5.73% -9.41% -3.78% -30.44% -4.60% >1 - 0.01% 1.05% -0.16% 0.01% -1.15% -4.81% -7.84% -3.62% -23.00% -3.77%

Total return for the following combinations of bucket & countries are calculated using EFFAS indices of total return: EUR 7-10, EUR 1-3, US 7-10, US 1-3, UK 7-10, UK 1-3, JP 7-10, JP 1-3. CCTs total return is calculated using MTS index

Source: Bloomberg, EFFAS, UniCredit Research (all tables and charts in this page

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 13 See last pages for disclaimer.

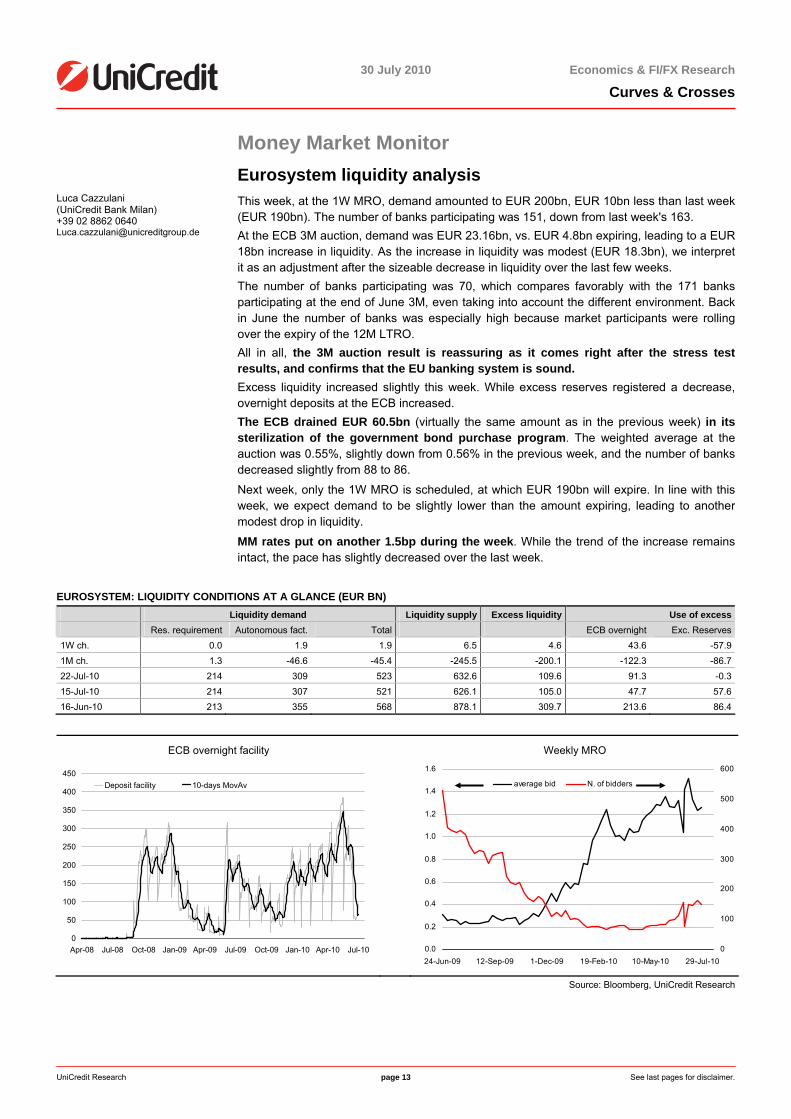

Money Market Monitor Eurosystem liquidity analysis

Luca Cazzulani (UniCredit Bank Milan) +39 02 8862 0640 [email protected]

This week, at the 1W MRO, demand amounted to EUR 200bn, EUR 10bn less than last week (EUR 190bn). The number of banks participating was 151, down from last week's 163. At the ECB 3M auction, demand was EUR 23.16bn, vs. EUR 4.8bn expiring, leading to a EUR18bn increase in liquidity. As the increase in liquidity was modest (EUR 18.3bn), we interpretit as an adjustment after the sizeable decrease in liquidity over the last few weeks. The number of banks participating was 70, which compares favorably with the 171 banksparticipating at the end of June 3M, even taking into account the different environment. Backin June the number of banks was especially high because market participants were rollingover the expiry of the 12M LTRO. All in all, the 3M auction result is reassuring as it comes right after the stress testresults, and confirms that the EU banking system is sound. Excess liquidity increased slightly this week. While excess reserves registered a decrease, overnight deposits at the ECB increased.

The ECB drained EUR 60.5bn (virtually the same amount as in the previous week) in its sterilization of the government bond purchase program. The weighted average at theauction was 0.55%, slightly down from 0.56% in the previous week, and the number of banksdecreased slightly from 88 to 86.

Next week, only the 1W MRO is scheduled, at which EUR 190bn will expire. In line with thisweek, we expect demand to be slightly lower than the amount expiring, leading to anothermodest drop in liquidity.

MM rates put on another 1.5bp during the week. While the trend of the increase remains intact, the pace has slightly decreased over the last week.

EUROSYSTEM: LIQUIDITY CONDITIONS AT A GLANCE (EUR BN) Liquidity demand Liquidity supply Excess liquidity Use of excess Res. requirement Autonomous fact. Total ECB overnight Exc. Reserves1W ch. 0.0 1.9 1.9 6.5 4.6 43.6 -57.91M ch. 1.3 -46.6 -45.4 -245.5 -200.1 -122.3 -86.722-Jul-10 214 309 523 632.6 109.6 91.3 -0.315-Jul-10 214 307 521 626.1 105.0 47.7 57.616-Jun-10 213 355 568 878.1 309.7 213.6 86.4

ECB overnight facility Weekly MRO

0

50

100

150

200

250

300

350

400

450

Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10

Deposit facility 10-days MovAv

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

24-Jun-09 12-Sep-09 1-Dec-09 19-Feb-10 10-May-10 29-Jul-100

100

200

300

400

500

600

average bid N. of bidders

Source: Bloomberg, UniCredit Research

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 14 See last pages for disclaimer.

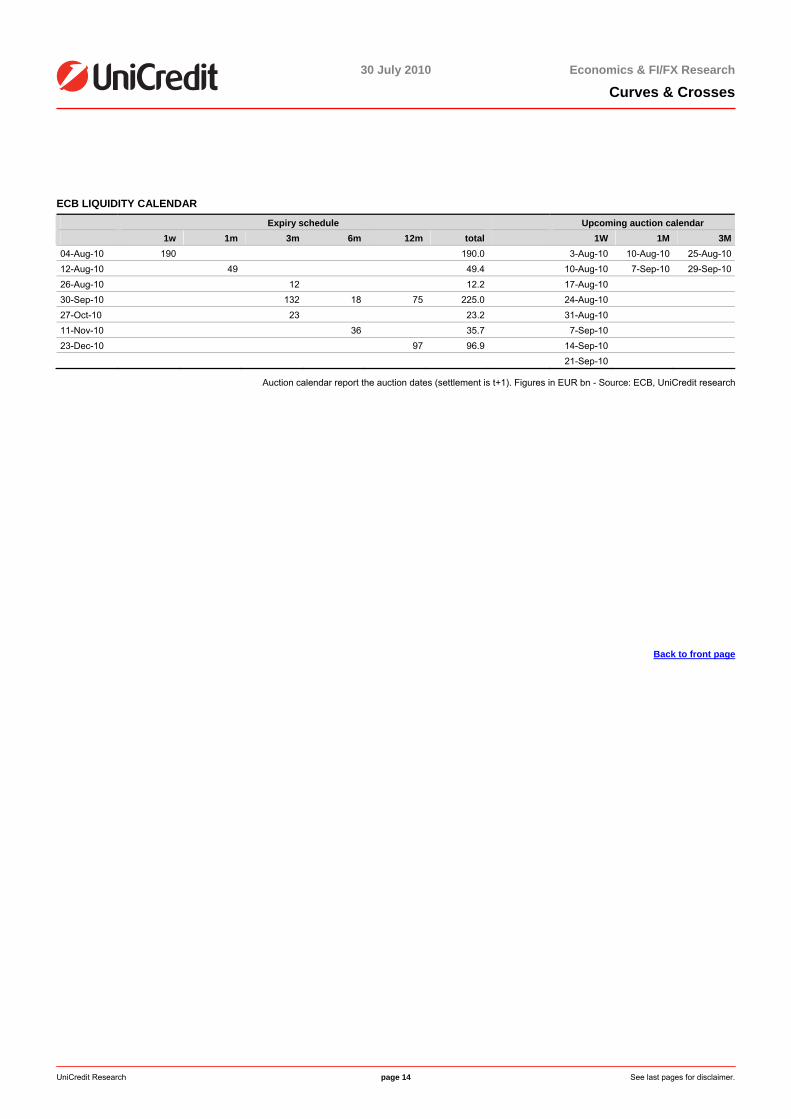

ECB LIQUIDITY CALENDAR

Expiry schedule Upcoming auction calendar 1w 1m 3m 6m 12m total 1W 1M 3M04-Aug-10 190 190.0 3-Aug-10 10-Aug-10 25-Aug-1012-Aug-10 49 49.4 10-Aug-10 7-Sep-10 29-Sep-1026-Aug-10 12 12.2 17-Aug-10 30-Sep-10 132 18 75 225.0 24-Aug-10 27-Oct-10 23 23.2 31-Aug-10 11-Nov-10 36 35.7 7-Sep-10 23-Dec-10 97 96.9 14-Sep-10 21-Sep-10

Auction calendar report the auction dates (settlement is t+1). Figures in EUR bn - Source: ECB, UniCredit research

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 15 See last pages for disclaimer.

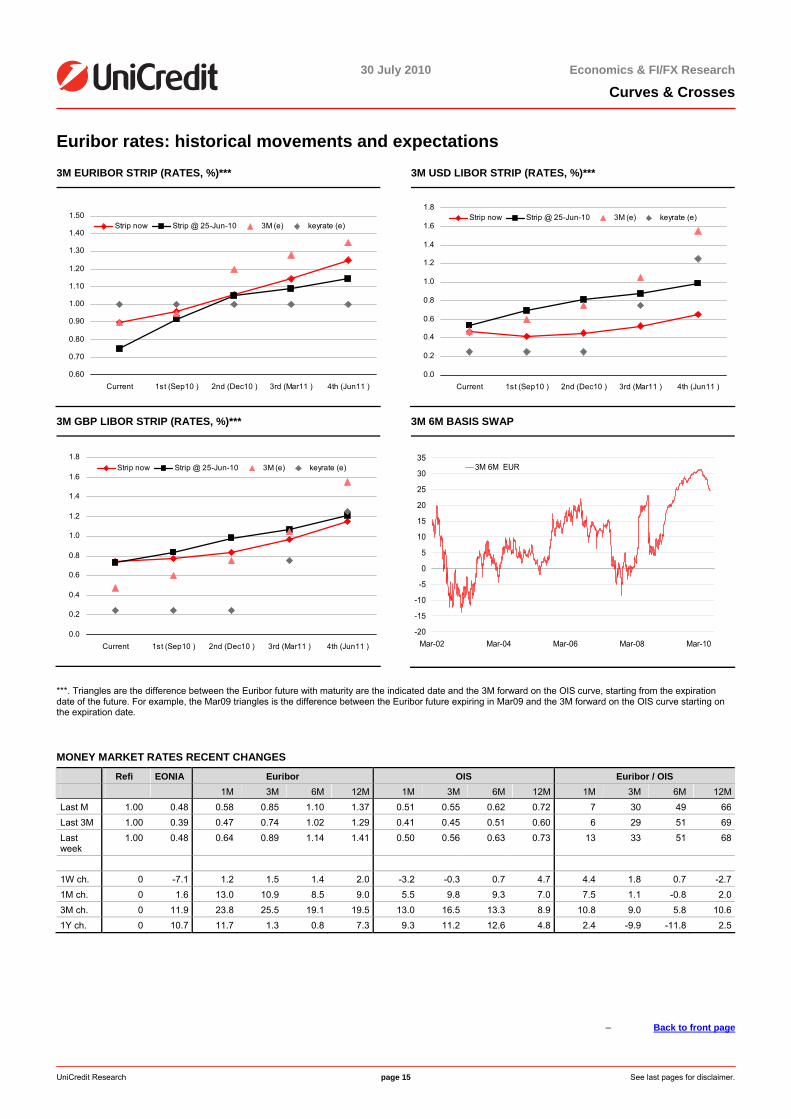

Euribor rates: historical movements and expectations 3M EURIBOR STRIP (RATES, %)***

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

Current 1st (Sep10 ) 2nd (Dec10 ) 3rd (Mar11 ) 4th (Jun11 )

Strip now Strip @ 25-Jun-10 3M (e) keyrate (e)

3M USD LIBOR STRIP (RATES, %)***

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Current 1st (Sep10 ) 2nd (Dec10 ) 3rd (Mar11 ) 4th (Jun11 )

Strip now Strip @ 25-Jun-10 3M (e) keyrate (e)

3M GBP LIBOR STRIP (RATES, %)***

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Current 1st (Sep10 ) 2nd (Dec10 ) 3rd (Mar11 ) 4th (Jun11 )

Strip now Strip @ 25-Jun-10 3M (e) keyrate (e)

3M 6M BASIS SWAP

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Mar-02 Mar-04 Mar-06 Mar-08 Mar-10

3M 6M EUR

***. Triangles are the difference between the Euribor future with maturity are the indicated date and the 3M forward on the OIS curve, starting from the expiration date of the future. For example, the Mar09 triangles is the difference between the Euribor future expiring in Mar09 and the 3M forward on the OIS curve starting on the expiration date.

MONEY MARKET RATES RECENT CHANGES

Refi EONIA Euribor OIS Euribor / OIS 1M 3M 6M 12M 1M 3M 6M 12M 1M 3M 6M 12MLast M 1.00 0.48 0.58 0.85 1.10 1.37 0.51 0.55 0.62 0.72 7 30 49 66Last 3M 1.00 0.39 0.47 0.74 1.02 1.29 0.41 0.45 0.51 0.60 6 29 51 69Last week

1.00 0.48 0.64 0.89 1.14 1.41 0.50 0.56 0.63 0.73 13 33 51 68

1W ch. 0 -7.1 1.2 1.5 1.4 2.0 -3.2 -0.3 0.7 4.7 4.4 1.8 0.7 -2.71M ch. 0 1.6 13.0 10.9 8.5 9.0 5.5 9.8 9.3 7.0 7.5 1.1 -0.8 2.03M ch. 0 11.9 23.8 25.5 19.1 19.5 13.0 16.5 13.3 8.9 10.8 9.0 5.8 10.61Y ch. 0 10.7 11.7 1.3 0.8 7.3 9.3 11.2 12.6 4.8 2.4 -9.9 -11.8 2.5

– Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 16 See last pages for disclaimer.

Swap Monitor SWAP CURVE: PAST, SPOT, 3M FORWARD

1.41.2

6.9

-1.0

2.5

-0.3 3.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0 5 10 15 20 25 30Maturity (years)

30-Jul-10 3 months ago Forward 3M

Numbers denote the 1w bp change in yields

ROLLDOWN &CARRY (3M HORIZON)

0

5

10

15

20

25

30

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30maturity (years)

bp

2 & 5 YEAR SWAP RATE: WHAT FORWARDS TELL US

Cur

rent

: 72

3m: 7

0

6m: 7

2

9m: 7

2

12m

: 71

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

2Y swap rate (%) 5Y swap rate (%) Forward rates

Numbers denote the spread in bp

10 & 30 YEAR SWAP RATE: WHAT FORWARDS TELL US

12m

: 19

9m: 2

5

6m: 3

0

3m: 3

5

Cur

rent

: 40

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

10Y swap rate (%) 30Y swap rate (%) Forward rates

Numbers denote the spread in bp

10&30 AND 2&30 SPREADS: HISTORY AND FORWARD

192

3m 6m 9m 18m

-100

-50

0

50

100

150

200

250

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

10/30Y spread (bp)

2/30Y spread (bp)

2/10Y spread (bp)

Forward spread

SWAP RATES AT A GLANCE

Average Cheap / rich Last Short term

(last 6M) Long term

(Jan99)Short term

(last 6M) Long term

(Jan99)2Y 1.45 1.42 3.42 C EEEE5Y 2.17 2.29 3.93 E EEEE10Y 2.97 3.14 4.43 EE EEEE15Y 3.36 3.52 4.69 E EEEE30Y 3.37 3.51 4.81 E EEEE

Cheap and rich indicators are base on distribution percentiles. EEEE=Very expensive, E= Expensive, CCCC=Very cheap, C=cheap. Valuations are from the investor’s perspective.

5Y SWAP-OPTION VOLA AT 5Y TENOR

18.53

13.4

15.4

8

10

12

14

16

18

20

22

24

Jan-99 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

Swaption vola (5Y) average since 1999 average since Aug07

SWAP CURVE AT A GLANCE

Average Cheap / rich Last Short term

(last 6M)Long term

(Jan99) Short term

(last 6M)Long term

(Jan99)2/5 72 87 50 EEE CC5/10 80 85 49 EEE CCC10/15 39 37 25 CC CCCC15/30 1 -1 11 CC EEE2/5/10 -4 1 1 EEE EE10/15/30 19 19 7 - CCCC

Source: Bloomberg, UniCredit Research

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 17 See last pages for disclaimer.

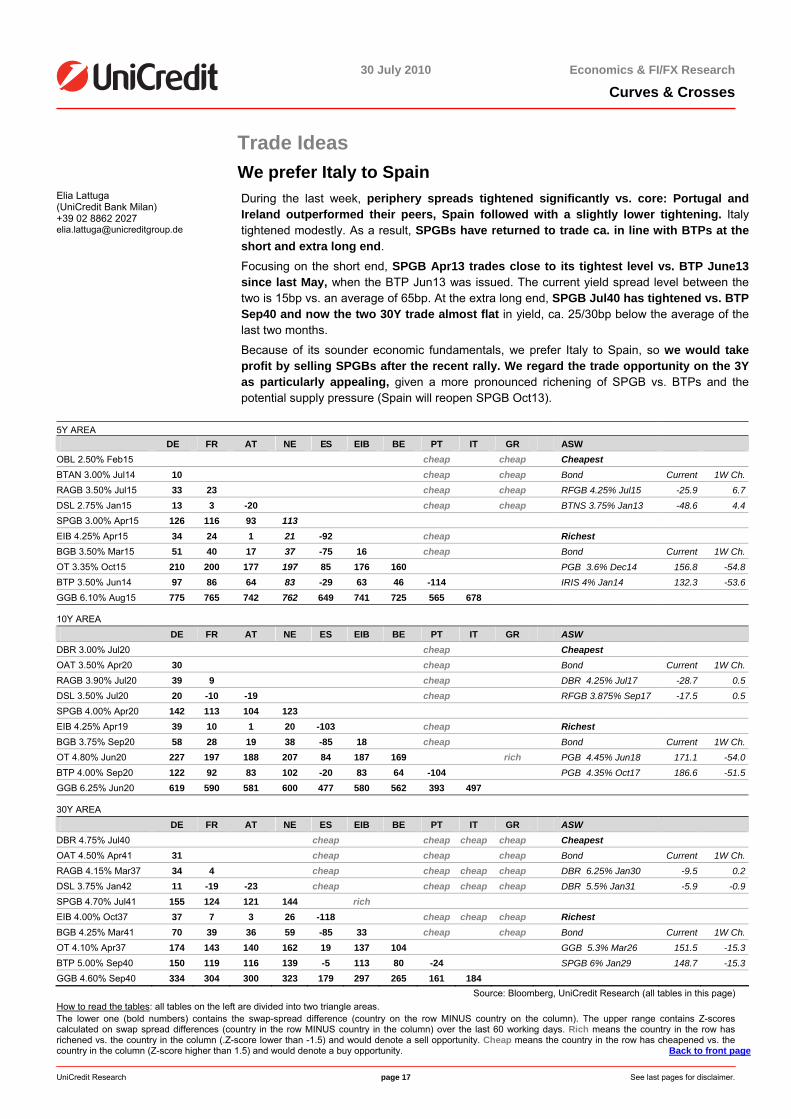

Trade Ideas We prefer Italy to Spain

Elia Lattuga (UniCredit Bank Milan) +39 02 8862 2027 [email protected]

During the last week, periphery spreads tightened significantly vs. core: Portugal and Ireland outperformed their peers, Spain followed with a slightly lower tightening. Italy tightened modestly. As a result, SPGBs have returned to trade ca. in line with BTPs at theshort and extra long end.

Focusing on the short end, SPGB Apr13 trades close to its tightest level vs. BTP June13 since last May, when the BTP Jun13 was issued. The current yield spread level between thetwo is 15bp vs. an average of 65bp. At the extra long end, SPGB Jul40 has tightened vs. BTP Sep40 and now the two 30Y trade almost flat in yield, ca. 25/30bp below the average of the last two months.

Because of its sounder economic fundamentals, we prefer Italy to Spain, so we would take profit by selling SPGBs after the recent rally. We regard the trade opportunity on the 3Y as particularly appealing, given a more pronounced richening of SPGB vs. BTPs and the potential supply pressure (Spain will reopen SPGB Oct13).

5Y AREA

DE FR AT NE ES EIB BE PT IT GR ASW OBL 2.50% Feb15 cheap cheap Cheapest BTAN 3.00% Jul14 10 cheap cheap Bond Current 1W Ch.RAGB 3.50% Jul15 33 23 cheap cheap RFGB 4.25% Jul15 -25.9 6.7DSL 2.75% Jan15 13 3 -20 cheap cheap BTNS 3.75% Jan13 -48.6 4.4SPGB 3.00% Apr15 126 116 93 113 EIB 4.25% Apr15 34 24 1 21 -92 cheap Richest BGB 3.50% Mar15 51 40 17 37 -75 16 cheap Bond Current 1W Ch.OT 3.35% Oct15 210 200 177 197 85 176 160 PGB 3.6% Dec14 156.8 -54.8BTP 3.50% Jun14 97 86 64 83 -29 63 46 -114 IRIS 4% Jan14 132.3 -53.6GGB 6.10% Aug15 775 765 742 762 649 741 725 565 678

10Y AREA DE FR AT NE ES EIB BE PT IT GR ASW DBR 3.00% Jul20 cheap Cheapest OAT 3.50% Apr20 30 cheap Bond Current 1W Ch.RAGB 3.90% Jul20 39 9 cheap DBR 4.25% Jul17 -28.7 0.5DSL 3.50% Jul20 20 -10 -19 cheap RFGB 3.875% Sep17 -17.5 0.5SPGB 4.00% Apr20 142 113 104 123 EIB 4.25% Apr19 39 10 1 20 -103 cheap Richest BGB 3.75% Sep20 58 28 19 38 -85 18 cheap Bond Current 1W Ch.OT 4.80% Jun20 227 197 188 207 84 187 169 rich PGB 4.45% Jun18 171.1 -54.0BTP 4.00% Sep20 122 92 83 102 -20 83 64 -104 PGB 4.35% Oct17 186.6 -51.5GGB 6.25% Jun20 619 590 581 600 477 580 562 393 497

30Y AREA DE FR AT NE ES EIB BE PT IT GR ASW DBR 4.75% Jul40 cheap cheap cheap cheap Cheapest OAT 4.50% Apr41 31 cheap cheap cheap Bond Current 1W Ch.RAGB 4.15% Mar37 34 4 cheap cheap cheap cheap DBR 6.25% Jan30 -9.5 0.2DSL 3.75% Jan42 11 -19 -23 cheap cheap cheap cheap DBR 5.5% Jan31 -5.9 -0.9SPGB 4.70% Jul41 155 124 121 144 rich EIB 4.00% Oct37 37 7 3 26 -118 cheap cheap cheap Richest BGB 4.25% Mar41 70 39 36 59 -85 33 cheap cheap Bond Current 1W Ch.OT 4.10% Apr37 174 143 140 162 19 137 104 GGB 5.3% Mar26 151.5 -15.3BTP 5.00% Sep40 150 119 116 139 -5 113 80 -24 SPGB 6% Jan29 148.7 -15.3GGB 4.60% Sep40 334 304 300 323 179 297 265 161 184

Source: Bloomberg, UniCredit Research (all tables in this page) How to read the tables: all tables on the left are divided into two triangle areas. The lower one (bold numbers) contains the swap-spread difference (country on the row MINUS country on the column). The upper range contains Z-scores calculated on swap spread differences (country in the row MINUS country in the column) over the last 60 working days. Rich means the country in the row has richened vs. the country in the column (.Z-score lower than -1.5) and would denote a sell opportunity. Cheap means the country in the row has cheapened vs. the country in the column (Z-score higher than 1.5) and would denote a buy opportunity. Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 18 See last pages for disclaimer.

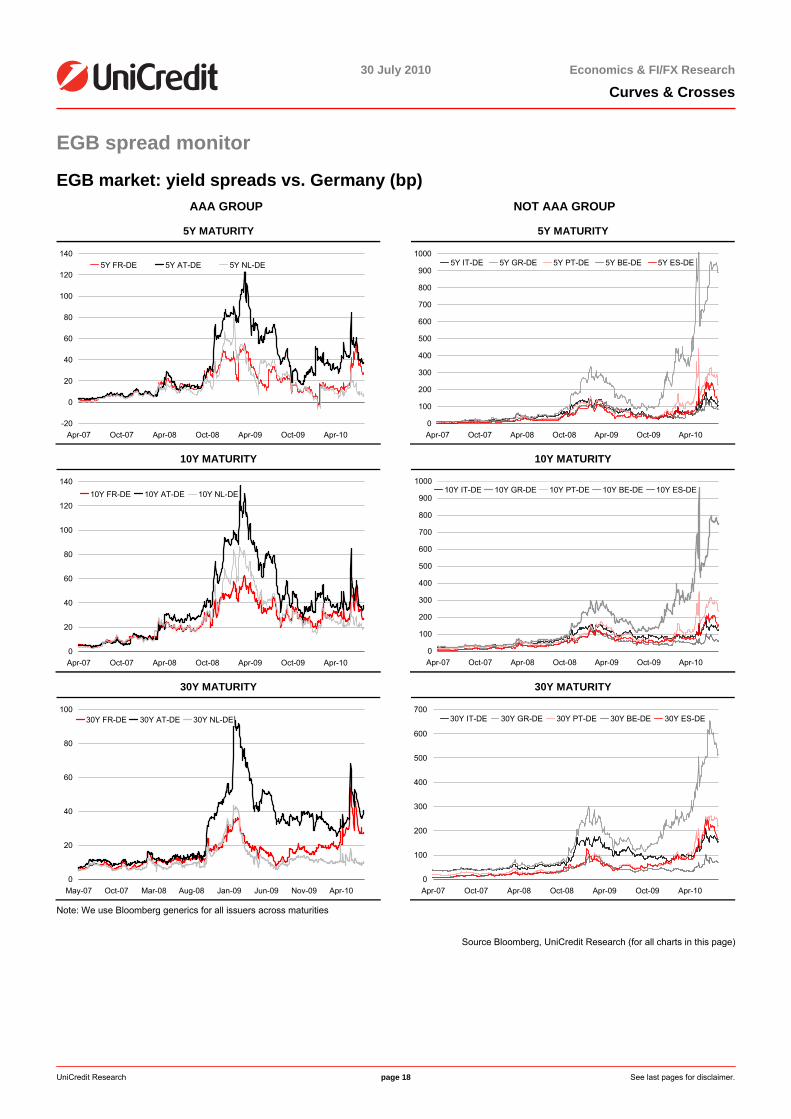

EGB spread monitor

EGB market: yield spreads vs. Germany (bp) AAA GROUP NOT AAA GROUP

5Y MATURITY

-20

0

20

40

60

80

100

120

140

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10

5Y FR-DE 5Y AT-DE 5Y NL-DE

5Y MATURITY

0

100

200

300

400

500

600

700

800

900

1000

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10

5Y IT-DE 5Y GR-DE 5Y PT-DE 5Y BE-DE 5Y ES-DE

10Y MATURITY

0

20

40

60

80

100

120

140

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10

10Y FR-DE 10Y AT-DE 10Y NL-DE

10Y MATURITY

0

100

200

300

400

500

600

700

800

900

1000

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10

10Y IT-DE 10Y GR-DE 10Y PT-DE 10Y BE-DE 10Y ES-DE

30Y MATURITY

0

20

40

60

80

100

May-07 Oct-07 Mar-08 Aug-08 Jan-09 Jun-09 Nov-09 Apr-10

30Y FR-DE 30Y AT-DE 30Y NL-DE

30Y MATURITY

0

100

200

300

400

500

600

700

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10

30Y IT-DE 30Y GR-DE 30Y PT-DE 30Y BE-DE 30Y ES-DE

Note: We use Bloomberg generics for all issuers across maturities

Source Bloomberg, UniCredit Research (for all charts in this page)

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 19 See last pages for disclaimer.

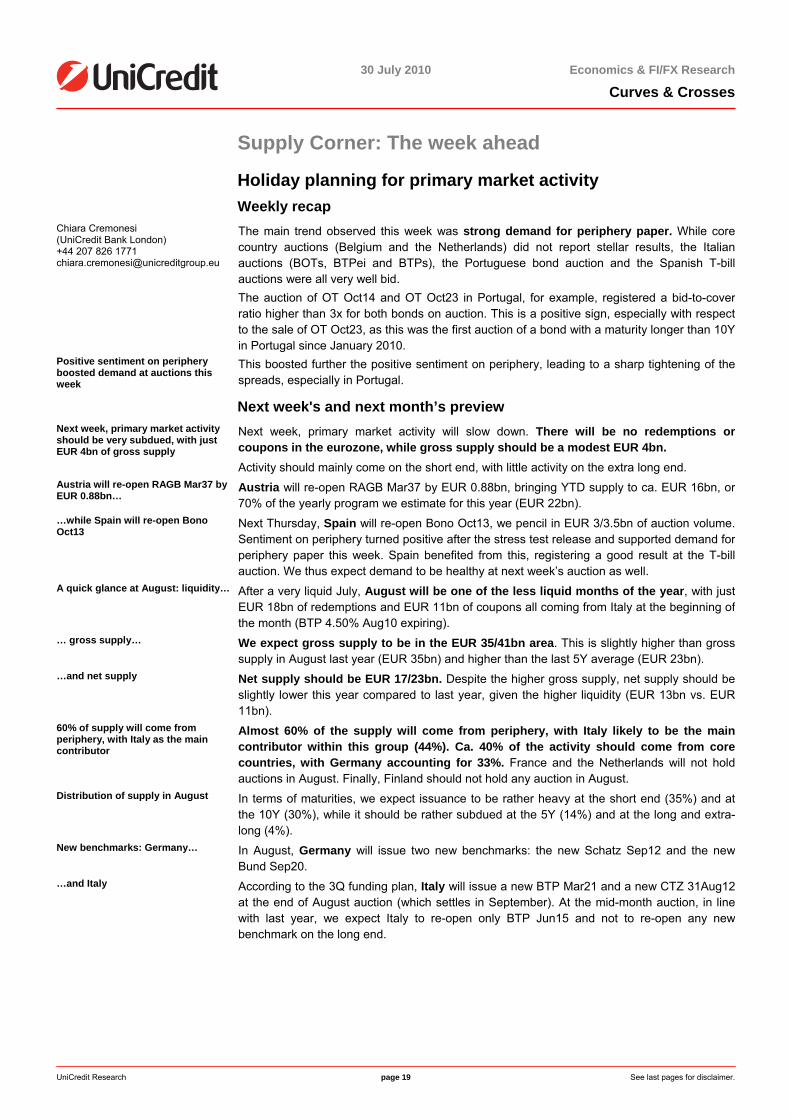

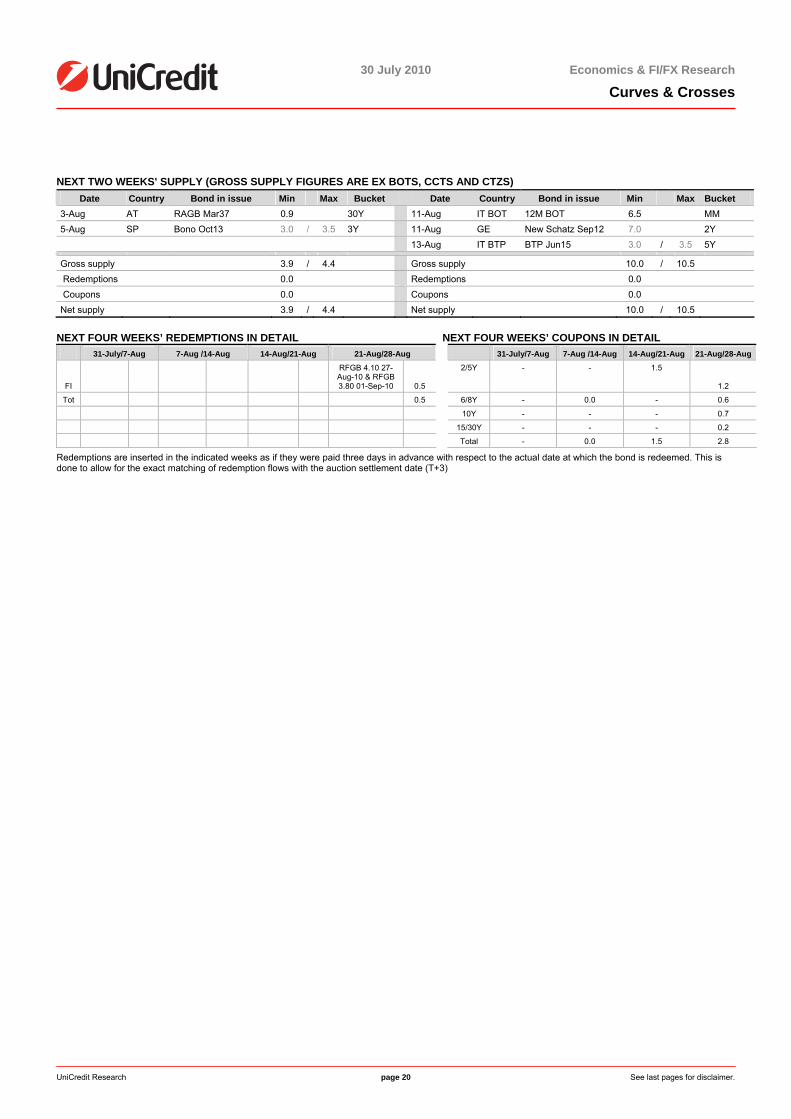

Supply Corner: The week ahead

Holiday planning for primary market activity Weekly recap

Chiara Cremonesi (UniCredit Bank London) +44 207 826 1771 [email protected]

The main trend observed this week was strong demand for periphery paper. While core country auctions (Belgium and the Netherlands) did not report stellar results, the Italianauctions (BOTs, BTPei and BTPs), the Portuguese bond auction and the Spanish T-bill auctions were all very well bid. The auction of OT Oct14 and OT Oct23 in Portugal, for example, registered a bid-to-cover ratio higher than 3x for both bonds on auction. This is a positive sign, especially with respectto the sale of OT Oct23, as this was the first auction of a bond with a maturity longer than 10Y in Portugal since January 2010.

Positive sentiment on periphery boosted demand at auctions this week

This boosted further the positive sentiment on periphery, leading to a sharp tightening of thespreads, especially in Portugal.

Next week's and next month’s preview Next week, primary market activity should be very subdued, with just EUR 4bn of gross supply

Next week, primary market activity will slow down. There will be no redemptions or coupons in the eurozone, while gross supply should be a modest EUR 4bn.

Activity should mainly come on the short end, with little activity on the extra long end. Austria will re-open RAGB Mar37 by EUR 0.88bn…

Austria will re-open RAGB Mar37 by EUR 0.88bn, bringing YTD supply to ca. EUR 16bn, or 70% of the yearly program we estimate for this year (EUR 22bn).

…while Spain will re-open Bono Oct13

Next Thursday, Spain will re-open Bono Oct13, we pencil in EUR 3/3.5bn of auction volume.Sentiment on periphery turned positive after the stress test release and supported demand for periphery paper this week. Spain benefited from this, registering a good result at the T-bill auction. We thus expect demand to be healthy at next week’s auction as well.

A quick glance at August: liquidity… After a very liquid July, August will be one of the less liquid months of the year, with just EUR 18bn of redemptions and EUR 11bn of coupons all coming from Italy at the beginning ofthe month (BTP 4.50% Aug10 expiring).

… gross supply… We expect gross supply to be in the EUR 35/41bn area. This is slightly higher than gross supply in August last year (EUR 35bn) and higher than the last 5Y average (EUR 23bn).

…and net supply Net supply should be EUR 17/23bn. Despite the higher gross supply, net supply should be slightly lower this year compared to last year, given the higher liquidity (EUR 13bn vs. EUR11bn).

60% of supply will come from periphery, with Italy as the main contributor

Almost 60% of the supply will come from periphery, with Italy likely to be the main contributor within this group (44%). Ca. 40% of the activity should come from corecountries, with Germany accounting for 33%. France and the Netherlands will not hold auctions in August. Finally, Finland should not hold any auction in August.

Distribution of supply in August In terms of maturities, we expect issuance to be rather heavy at the short end (35%) and atthe 10Y (30%), while it should be rather subdued at the 5Y (14%) and at the long and extra-long (4%).

New benchmarks: Germany… In August, Germany will issue two new benchmarks: the new Schatz Sep12 and the newBund Sep20.

…and Italy According to the 3Q funding plan, Italy will issue a new BTP Mar21 and a new CTZ 31Aug12 at the end of August auction (which settles in September). At the mid-month auction, in line with last year, we expect Italy to re-open only BTP Jun15 and not to re-open any new benchmark on the long end.

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 20 See last pages for disclaimer.

NEXT TWO WEEKS' SUPPLY (GROSS SUPPLY FIGURES ARE EX BOTS, CCTS AND CTZS)

Date Country Bond in issue Min Max Bucket Date Country Bond in issue Min Max Bucket 3-Aug AT RAGB Mar37 0.9 30Y 11-Aug IT BOT 12M BOT 6.5 MM 5-Aug SP Bono Oct13 3.0 / 3.5 3Y 11-Aug GE New Schatz Sep12 7.0 2Y 13-Aug IT BTP BTP Jun15 3.0 / 3.5 5Y

Gross supply 3.9 / 4.4 Gross supply 10.0 / 10.5 Redemptions 0.0 Redemptions 0.0 Coupons 0.0 Coupons 0.0 Net supply 3.9 / 4.4 Net supply 10.0 / 10.5

NEXT FOUR WEEKS’ REDEMPTIONS IN DETAIL NEXT FOUR WEEKS’ COUPONS IN DETAIL 31-July/7-Aug 7-Aug /14-Aug 14-Aug/21-Aug 21-Aug/28-Aug 31-July/7-Aug 7-Aug /14-Aug 14-Aug/21-Aug 21-Aug/28-Aug

FI

RFGB 4.10 27-Aug-10 & RFGB 3.80 01-Sep-10 0.5

2/5Y - - 1.5

1.2

Tot 0.5 6/8Y - 0.0 - 0.6

10Y - - - 0.7

15/30Y - - - 0.2

Total - 0.0 1.5 2.8

Redemptions are inserted in the indicated weeks as if they were paid three days in advance with respect to the actual date at which the bond is redeemed. This is done to allow for the exact matching of redemption flows with the auction settlement date (T+3)

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 21 See last pages for disclaimer.

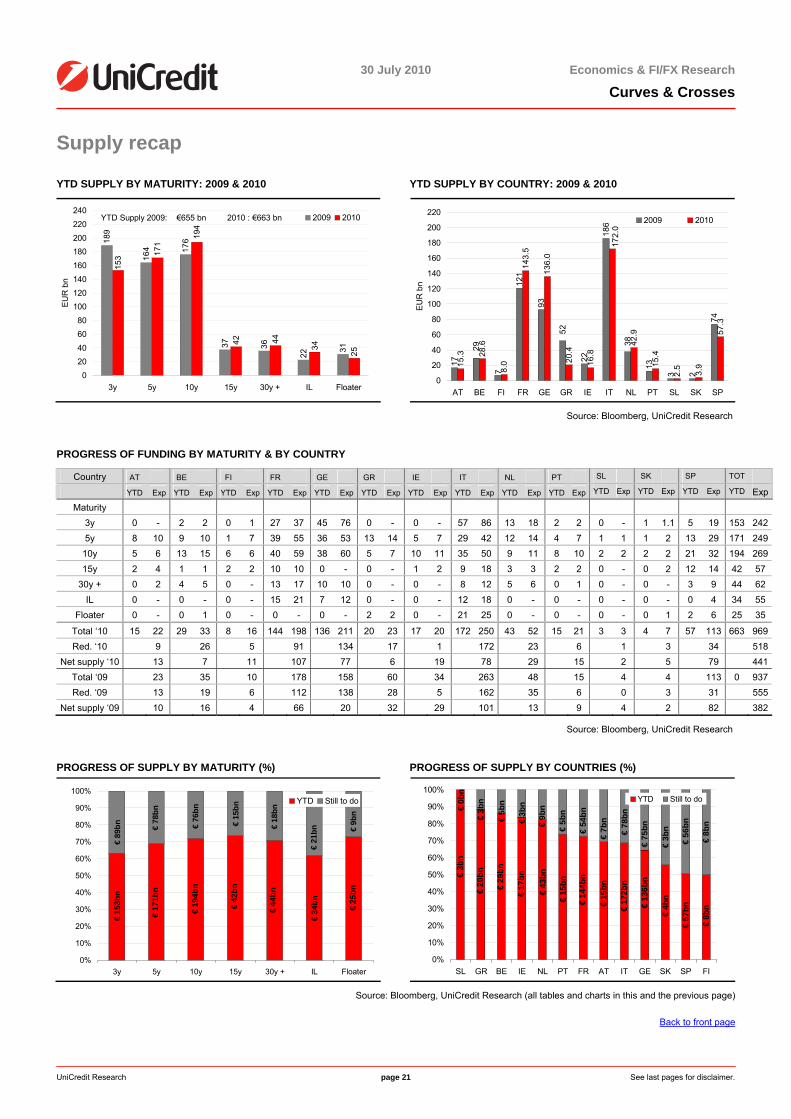

Supply recap

YTD SUPPLY BY MATURITY: 2009 & 2010 YTD SUPPLY BY COUNTRY: 2009 & 2010

189

164 17

6

37 36

22

31

171

42 44

34

25

153

194

02040

6080

100120140

160

180200

220

240

3y 5y 10y 15y 30y + IL Floater

EUR

bn

2009 2010YTD Supply 2009: €655 bn 2010 : €663 bn

17

121

93

22

186

13

3 2

74

15.3 28

.6

8.0

143.

5

136.

0

20.4

16.8

42.9

15.4

2.5

3.9

57.3

7

3829

52

172.

0

0

20

40

60

80

100

120

140

160

180

200

220

AT BE FI FR GE GR IE IT NL PT SL SK SP

EUR

bn

2009 2010

Source: Bloomberg, UniCredit Research

PROGRESS OF FUNDING BY MATURITY & BY COUNTRY

Country AT BE FI FR GE GR IE IT NL PT SL SK SP TOT YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp YTD Exp

Maturity 3y 0 - 2 2 0 1 27 37 45 76 0 - 0 - 57 86 13 18 2 2 0 - 1 1.1 5 19 153 2425y 8 10 9 10 1 7 39 55 36 53 13 14 5 7 29 42 12 14 4 7 1 1 1 2 13 29 171 249

10y 5 6 13 15 6 6 40 59 38 60 5 7 10 11 35 50 9 11 8 10 2 2 2 2 21 32 194 26915y 2 4 1 1 2 2 10 10 0 - 0 - 1 2 9 18 3 3 2 2 0 - 0 2 12 14 42 57

30y + 0 2 4 5 0 - 13 17 10 10 0 - 0 - 8 12 5 6 0 1 0 - 0 - 3 9 44 62 IL 0 - 0 - 0 - 15 21 7 12 0 - 0 - 12 18 0 - 0 - 0 - 0 - 0 4 34 55

Floater 0 - 0 1 0 - 0 - 0 - 2 2 0 - 21 25 0 - 0 - 0 - 0 1 2 6 25 35

Total ‘10 15 22 29 33 8 16 144 198 136 211 20 23 17 20 172 250 43 52 15 21 3 3 4 7 57 113 663 969Red. ‘10 9 26 5 91 134 17 1 172 23 6 1 3 34 518

Net supply ‘10 13 7 11 107 77 6 19 78 29 15 2 5 79 441Total ‘09 23 35 10 178 158 60 34 263 48 15 4 4 113 0 937Red. ‘09 13 19 6 112 138 28 5 162 35 6 0 3 31 555

Net supply ‘09 10 16 4 66 20 32 29 101 13 9 4 2 82 382

Source: Bloomberg, UniCredit Research

PROGRESS OF SUPPLY BY MATURITY (%) PROGRESS OF SUPPLY BY COUNTRIES (%)

€ 25

bn

€ 34

bn

€ 44

bn

€ 42

bn

€ 19

4bn

€ 17

1bn

€ 15

3bn

€ 1

8bn

€ 9

bn

€ 8

9bn

€ 7

8bn

€ 7

6bn

€ 1

5bn

€ 2

1bn

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3y 5y 10y 15y 30y + IL Floater

YTD Still to do

€ 5

7bn

€ 8

bn

€ 56

bn

€ 8b

n

€ 1

72bn

€ 1

5bn

€ 1

44bn

€ 1

5bn

€ 4

3bn

€ 1

7bn

€ 2

9bn

€ 3

bn

€ 1

36bn

€ 2

0bn

€ 4

bn

€ 78

bn

€ 7b

n

€ 54

bn

€ 5b

n

€ 9b

n

€ 3b

n

€ 5b

n

€ 3b

n

€ 0b

n

€ 75

bn

€ 3b

n

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SL GR BE IE NL PT FR AT IT GE SK SP FI

YTD Still to do

Source: Bloomberg, UniCredit Research (all tables and charts in this and the previous page)

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 22 See last pages for disclaimer.

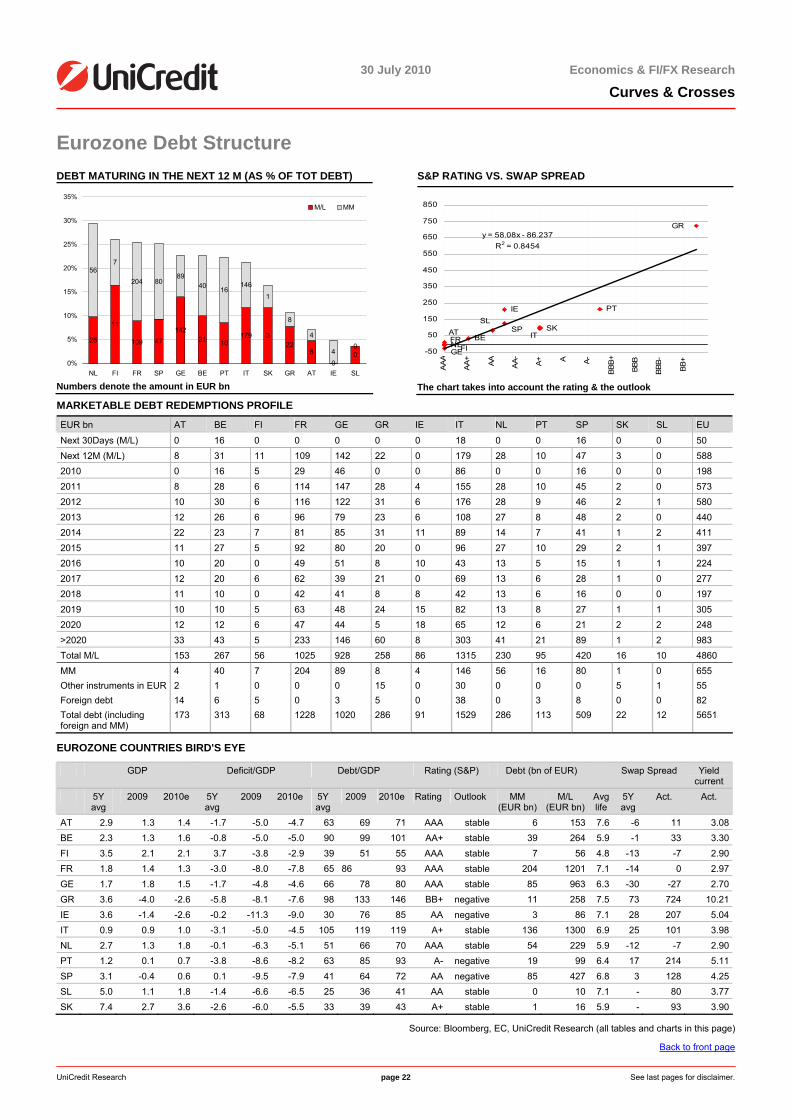

Eurozone Debt Structure DEBT MATURING IN THE NEXT 12 M (AS % OF TOT DEBT)

28

11

109 47142

31 10179 3

228

00

567

204 8089

40 16146

1

8

4

40

0%

5%

10%

15%

20%

25%

30%

35%

NL FI FR SP GE BE PT IT SK GR AT IE SL

M/L MM

Numbers denote the amount in EUR bn

S&P RATING VS. SWAP SPREAD

GR

IE

IT

GE

PT

SPBE

NLFR

FI

ATSL

SK

BB+

AAA

AA+ AA AA- A+ A A-

BBB

+

BBB

BBB

-

y = 58.08x - 86.237R2 = 0.8454

-50

50

150

250

350

450

550

650

750

850

The chart takes into account the rating & the outlook

MARKETABLE DEBT REDEMPTIONS PROFILE

EUR bn AT BE FI FR GE GR IE IT NL PT SP SK SL EU

Next 30Days (M/L) 0 16 0 0 0 0 0 18 0 0 16 0 0 50 Next 12M (M/L) 8 31 11 109 142 22 0 179 28 10 47 3 0 588 2010 0 16 5 29 46 0 0 86 0 0 16 0 0 198 2011 8 28 6 114 147 28 4 155 28 10 45 2 0 573 2012 10 30 6 116 122 31 6 176 28 9 46 2 1 580 2013 12 26 6 96 79 23 6 108 27 8 48 2 0 440 2014 22 23 7 81 85 31 11 89 14 7 41 1 2 411 2015 11 27 5 92 80 20 0 96 27 10 29 2 1 397 2016 10 20 0 49 51 8 10 43 13 5 15 1 1 224 2017 12 20 6 62 39 21 0 69 13 6 28 1 0 277 2018 11 10 0 42 41 8 8 42 13 6 16 0 0 197 2019 10 10 5 63 48 24 15 82 13 8 27 1 1 305 2020 12 12 6 47 44 5 18 65 12 6 21 2 2 248 >2020 33 43 5 233 146 60 8 303 41 21 89 1 2 983 Total M/L 153 267 56 1025 928 258 86 1315 230 95 420 16 10 4860 MM 4 40 7 204 89 8 4 146 56 16 80 1 0 655 Other instruments in EUR 2 1 0 0 0 15 0 30 0 0 0 5 1 55 Foreign debt 14 6 5 0 3 5 0 38 0 3 8 0 0 82 Total debt (including foreign and MM)

173 313 68 1228 1020 286 91 1529 286 113 509 22 12 5651

EUROZONE COUNTRIES BIRD'S EYE

GDP Deficit/GDP Debt/GDP Rating (S&P) Debt (bn of EUR) Swap Spread Yield current

5Y avg

2009 2010e 5Y avg

2009 2010e 5Y avg

2009 2010e Rating Outlook MM (EUR bn)

M/L (EUR bn)

Avg life

5Y avg

Act. Act.

AT 2.9 1.3 1.4 -1.7 -5.0 -4.7 63 69 71 AAA stable 6 153 7.6 -6 11 3.08BE 2.3 1.3 1.6 -0.8 -5.0 -5.0 90 99 101 AA+ stable 39 264 5.9 -1 33 3.30FI 3.5 2.1 2.1 3.7 -3.8 -2.9 39 51 55 AAA stable 7 56 4.8 -13 -7 2.90FR 1.8 1.4 1.3 -3.0 -8.0 -7.8 65 86 93 AAA stable 204 1201 7.1 -14 0 2.97GE 1.7 1.8 1.5 -1.7 -4.8 -4.6 66 78 80 AAA stable 85 963 6.3 -30 -27 2.70GR 3.6 -4.0 -2.6 -5.8 -8.1 -7.6 98 133 146 BB+ negative 11 258 7.5 73 724 10.21IE 3.6 -1.4 -2.6 -0.2 -11.3 -9.0 30 76 85 AA negative 3 86 7.1 28 207 5.04IT 0.9 0.9 1.0 -3.1 -5.0 -4.5 105 119 119 A+ stable 136 1300 6.9 25 101 3.98NL 2.7 1.3 1.8 -0.1 -6.3 -5.1 51 66 70 AAA stable 54 229 5.9 -12 -7 2.90PT 1.2 0.1 0.7 -3.8 -8.6 -8.2 63 85 93 A- negative 19 99 6.4 17 214 5.11SP 3.1 -0.4 0.6 0.1 -9.5 -7.9 41 64 72 AA negative 85 427 6.8 3 128 4.25SL 5.0 1.1 1.8 -1.4 -6.6 -6.5 25 36 41 AA stable 0 10 7.1 - 80 3.77SK 7.4 2.7 3.6 -2.6 -6.0 -5.5 33 39 43 A+ stable 1 16 5.9 - 93 3.90

Source: Bloomberg, EC, UniCredit Research (all tables and charts in this page)

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 23 See last pages for disclaimer.

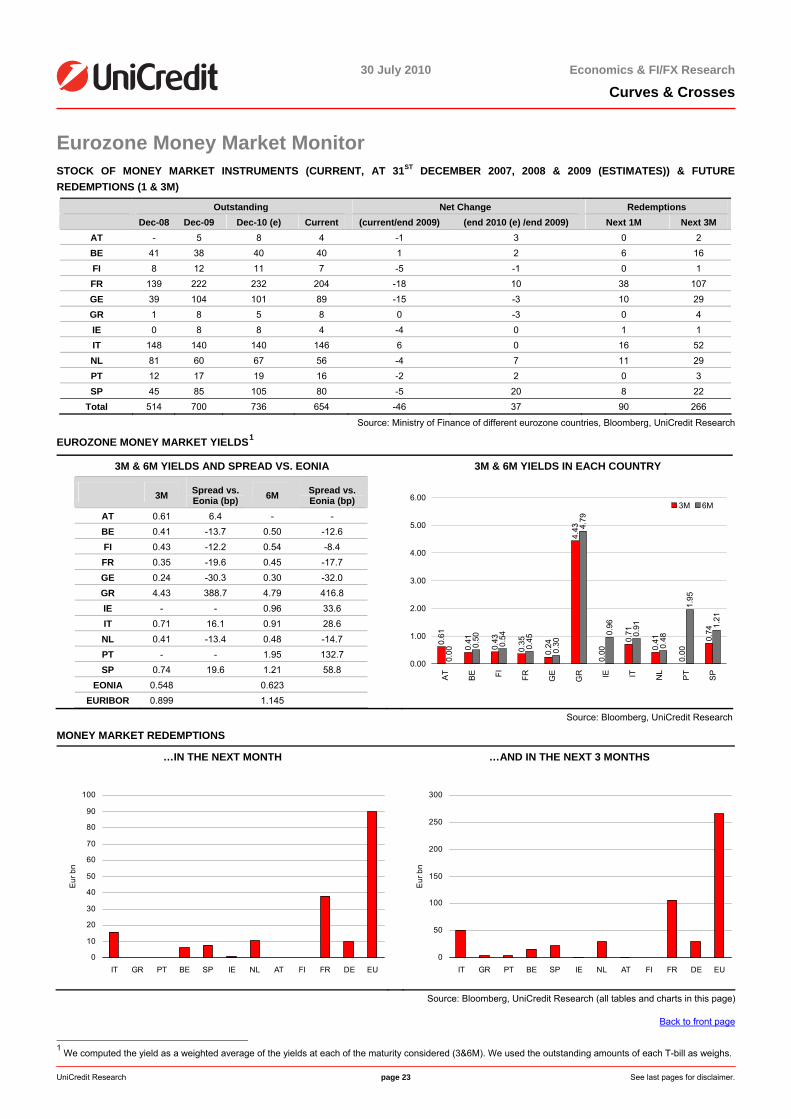

Eurozone Money Market Monitor STOCK OF MONEY MARKET INSTRUMENTS (CURRENT, AT 31ST DECEMBER 2007, 2008 & 2009 (ESTIMATES)) & FUTURE REDEMPTIONS (1 & 3M)

Outstanding Net Change Redemptions Dec-08 Dec-09 Dec-10 (e) Current (current/end 2009) (end 2010 (e) /end 2009) Next 1M Next 3M

AT - 5 8 4 -1 3 0 2 BE 41 38 40 40 1 2 6 16 FI 8 12 11 7 -5 -1 0 1 FR 139 222 232 204 -18 10 38 107 GE 39 104 101 89 -15 -3 10 29 GR 1 8 5 8 0 -3 0 4 IE 0 8 8 4 -4 0 1 1 IT 148 140 140 146 6 0 16 52 NL 81 60 67 56 -4 7 11 29 PT 12 17 19 16 -2 2 0 3 SP 45 85 105 80 -5 20 8 22

Total 514 700 736 654 -46 37 90 266

Source: Ministry of Finance of different eurozone countries, Bloomberg, UniCredit Research

EUROZONE MONEY MARKET YIELDS1

3M & 6M YIELDS AND SPREAD VS. EONIA 3M & 6M YIELDS IN EACH COUNTRY

3M Spread vs. Eonia (bp) 6M Spread vs.

Eonia (bp) AT 0.61 6.4 - - BE 0.41 -13.7 0.50 -12.6 FI 0.43 -12.2 0.54 -8.4 FR 0.35 -19.6 0.45 -17.7 GE 0.24 -30.3 0.30 -32.0 GR 4.43 388.7 4.79 416.8 IE - - 0.96 33.6 IT 0.71 16.1 0.91 28.6 NL 0.41 -13.4 0.48 -14.7 PT - - 1.95 132.7 SP 0.74 19.6 1.21 58.8

EONIA 0.548 0.623 EURIBOR 0.899 1.145

0.61

0.35

0.24

4.43

0.00

0.71

0.41

0.00

0.74

0.00

0.50

0.54

0.45

0.30

4.79

0.96

0.91

0.48

1.95

1.21

0.41

0.43

0.00

1.00

2.00

3.00

4.00

5.00

6.00

AT

BE FI FR GE

GR IE IT NL

PT

SP

3M 6M

Source: Bloomberg, UniCredit Research

MONEY MARKET REDEMPTIONS

…IN THE NEXT MONTH …AND IN THE NEXT 3 MONTHS

0

10

20

30

40

50

60

70

80

90

100

IT GR PT BE SP IE NL AT FI FR DE EU

Eur

bn

0

50

100

150

200

250

300

IT GR PT BE SP IE NL AT FI FR DE EU

Eur

bn

Source: Bloomberg, UniCredit Research (all tables and charts in this page)

Back to front page

1 We computed the yield as a weighted average of the yields at each of the maturity considered (3&6M). We used the outstanding amounts of each T-bill as weighs.

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 24 See last pages for disclaimer.

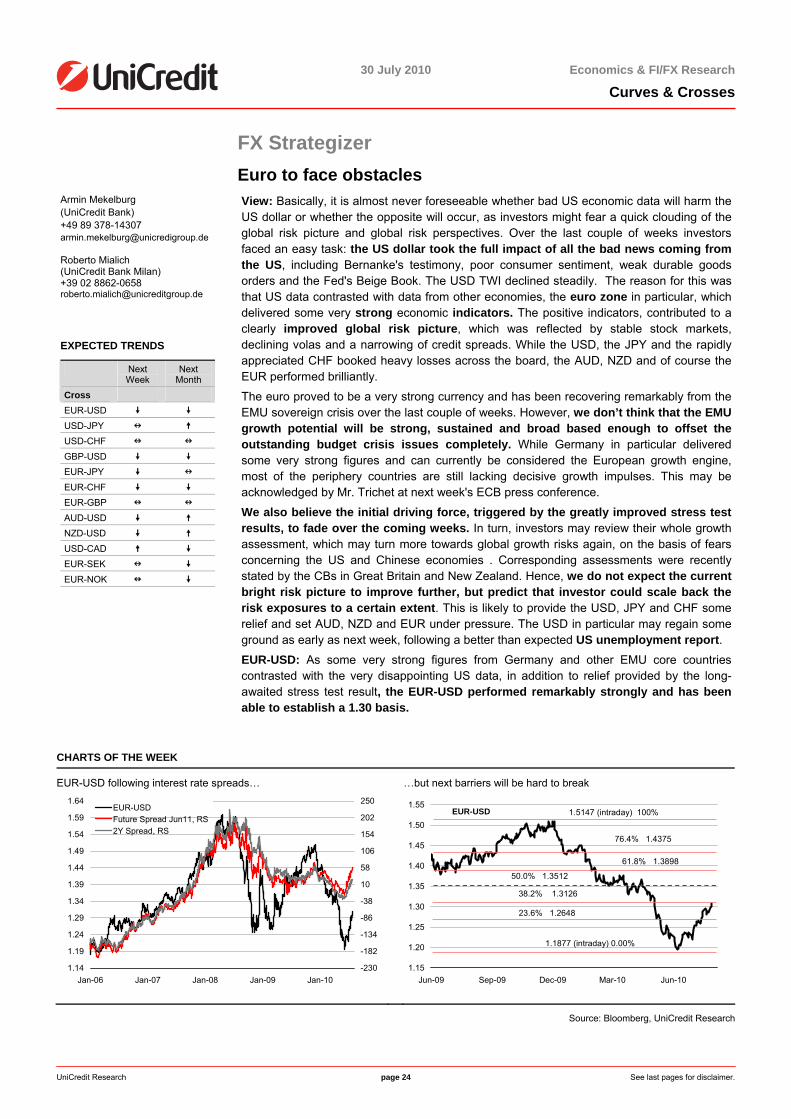

FX Strategizer Euro to face obstacles

Armin Mekelburg (UniCredit Bank) +49 89 378-14307 [email protected] Roberto Mialich (UniCredit Bank Milan) +39 02 8862-0658 [email protected]

EXPECTED TRENDS

Next Week

Next Month

Cross EUR-USD USD-JPY USD-CHF GBP-USD EUR-JPY EUR-CHF EUR-GBP AUD-USD NZD-USD USD-CAD EUR-SEK EUR-NOK

View: Basically, it is almost never foreseeable whether bad US economic data will harm the US dollar or whether the opposite will occur, as investors might fear a quick clouding of the global risk picture and global risk perspectives. Over the last couple of weeks investors faced an easy task: the US dollar took the full impact of all the bad news coming from the US, including Bernanke's testimony, poor consumer sentiment, weak durable goods orders and the Fed's Beige Book. The USD TWI declined steadily. The reason for this was that US data contrasted with data from other economies, the euro zone in particular, which delivered some very strong economic indicators. The positive indicators, contributed to a clearly improved global risk picture, which was reflected by stable stock markets, declining volas and a narrowing of credit spreads. While the USD, the JPY and the rapidly appreciated CHF booked heavy losses across the board, the AUD, NZD and of course the EUR performed brilliantly.

The euro proved to be a very strong currency and has been recovering remarkably from the EMU sovereign crisis over the last couple of weeks. However, we don’t think that the EMU growth potential will be strong, sustained and broad based enough to offset the outstanding budget crisis issues completely. While Germany in particular delivered some very strong figures and can currently be considered the European growth engine, most of the periphery countries are still lacking decisive growth impulses. This may be acknowledged by Mr. Trichet at next week's ECB press conference.

We also believe the initial driving force, triggered by the greatly improved stress test results, to fade over the coming weeks. In turn, investors may review their whole growth assessment, which may turn more towards global growth risks again, on the basis of fears concerning the US and Chinese economies . Corresponding assessments were recently stated by the CBs in Great Britain and New Zealand. Hence, we do not expect the current bright risk picture to improve further, but predict that investor could scale back the risk exposures to a certain extent. This is likely to provide the USD, JPY and CHF some relief and set AUD, NZD and EUR under pressure. The USD in particular may regain some ground as early as next week, following a better than expected US unemployment report. EUR-USD: As some very strong figures from Germany and other EMU core countries contrasted with the very disappointing US data, in addition to relief provided by the long-awaited stress test result, the EUR-USD performed remarkably strongly and has been able to establish a 1.30 basis.

CHARTS OF THE WEEK

EUR-USD following interest rate spreads… …but next barriers will be hard to break

1.14

1.19

1.24

1.29

1.34

1.39

1.44

1.49

1.54

1.59

1.64

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10-230

-182

-134

-86

-38

10

58

106

154

202

250EUR-USDFuture Spread Jun11, RS2Y Spread, RS

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

EUR-USD

1.1877 (intraday) 0.00%

38.2% 1.3126

61.8% 1.3898

1.5147 (intraday) 100%

50.0% 1.3512

23.6% 1.2648

76.4% 1.4375

Source: Bloomberg, UniCredit Research

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 25 See last pages for disclaimer.

EUR: Interest rate spreads with an impact on EUR-USD. But the next technical resistance will be a real challenge for markets

Given the differing economic performance levels of the US and the euro zone, interest rates and money market futures spreads, an almost forgotten driving factor, came to the fore again. It was not the closing of the gap to implied rates of beyond 1.40, but simply the spreadwidening in the euro’s favor. However, as the spreads are already almost exhausted, the upward momentum in EUR-USD should fade strongly, as the next key resistance level of1.3125 is too significant to be simply passed through (see charts previous page).

JPY: EUR-JPY weaker and USD-JPY unchanged

Based on the recently improved market sentiment, the JPY should trade significantly weaker, primarily against the EUR. However, as long as we continue to receive weak US data, the latent downward pressure on the USD-JPY will limit the EUR-JPY's upside potential.Adding the almost exhausted correction potential of the EUR in general, EUR-JPY would even be hard pushed above beyond 115, while the USD-JPY should remain in the 86/88 band.

As expected, EUR-CHF upside proved fairly capped above 1.38, although EUR-USD took advantage from the latest economic data, hinting that the eurozone is apparently “decoupling” from the US. Yet, the EUR-CHF retreat back below 1.36 has been also fostered by talk that the SNB may sell some of its EUR holdings and by excessive speculation about a SNB rate hike after the summer. This reaction was also amplified by incorrect liquidity signals in the Swiss money market rather than any incumbent inflation menace. Any SNB move is unlikely to take place before 1Q11. The CHF may return further on bid in Autumn, when a broad debate of the 2011-2012 budgets across the eurozone may reignite EMU woes and a new demand for safe-haven assets. With USD-CHF also being exposed to a new slide towards parity once 1.04 has gone, a full break below 1.36 may spark a new EUR-CHF sell-off.

GBP: “…and she’s buying a stairway to heaven”

After the UK GDP for 2Q10 revealed a stunning 1.0% qoq growth, sterling was even better positioned for a sustained rally. Hence, cable continued to outperform the other major exchange rates, taking clear advantage of the weaker USD which made breaking through 1.55 easier. This paved then the way for the new target of 1.57. The MPC testimony beforeHM Treasury was basically ignored. Most BoE’s members sound cautious about UK growth,inflation and monetary policy prospects and while next week’s BoE meeting should be a non event, the bank is likely to be prudent in its new Inflation Report on August 11 too. Yet, with new UK data releases likely to be positive again, the pound’s ongoing strength should also continue next month: some profit taking can be expected after the current rally and thisis why we closed our long cable position, however, this would offer a new buying opportunityamid risks that our medium-term target for cable above 1.60 may be reached sooner than we initially predicted. On the other hand, EUR-GBP should reveal a more constrained dynamic: as long as the EUR-USD holds the line, a EUR-GBP break below 0.83 and towards 0.80 might require some time, but this medium-term target remains intact.

The three dollars (AUD, NZD & CAD): a more conservative tone to be expected in August

Commodity currencies are stuck between a rock and a hard place for now: on one hand, they have clearly benefited from a less adverse global risk picture and even more from theweaker USD; on the other hand, monetary policy at home appears less and less helpful:as feared, the RBNZ hiked rates by another 25bp to 3%, but Governor Bollard sounded muchmore cautious about the need for further intense monetary tightening, due to a less benignglobal economic picture that may hurt countries that are sensitive to the world economic cycle,like New Zealand. The RBA will not much differently: the OCR will remain steady at 4.50% on Tuesday and the bank will reaffirm its cautious stance on rates too. The upcoming general elections in Australia on August 21 should favor conservative trading too. Hence, the Aussie, the Kiwi and the loonie dollar should hold the line against the USD, but most of their recent upside potential is likely to remain frozen in August.

Nordics: Still struggling as breaking key levels will look harder

“It can’t shine forever”: a more pronounced appreciation of the two Nordic units appears quite ambitious at this stage. Due also to the firmer EUR-USD, the EUR-SEK and EUR-NOK failed to fall below 9.40 and 7.95 respectively, in turn sparking a pullback towards 9.50 andabove 8.00. Accordingly, both the SEK and the NOK are likely to struggle in the “land of nowhere” in the coming weeks too. The usual external factors (namely, equity markets and swings between risk aversion and risk appetite) should play greater roles here than domesticevents - the Norges Bank’s meeting on 11 August is the only local point of interest.

Back to front page

30 July 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 26 See last pages for disclaimer.

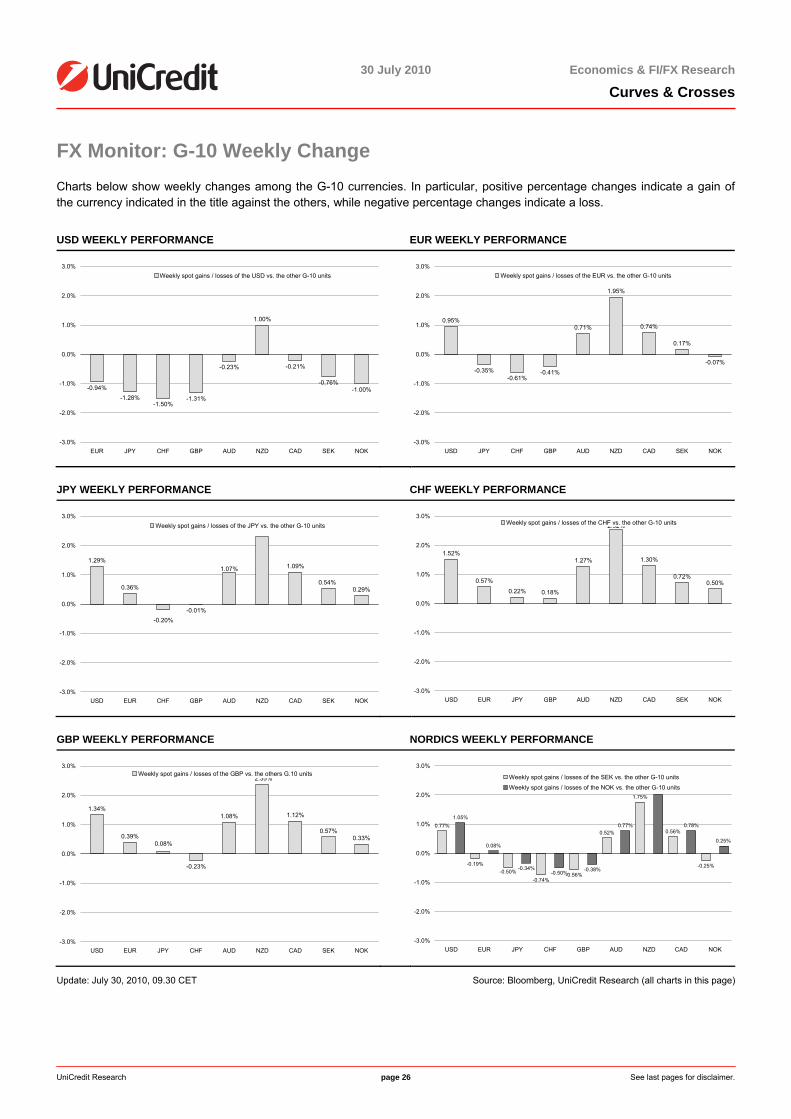

FX Monitor: G-10 Weekly Change Charts below show weekly changes among the G-10 currencies. In particular, positive percentage changes indicate a gain of the currency indicated in the title against the others, while negative percentage changes indicate a loss.

USD WEEKLY PERFORMANCE EUR WEEKLY PERFORMANCE

-0.94%-1.28%

-1.50%-1.31%

-0.23%

1.00%

-0.21%

-0.76%-1.00%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

EUR JPY CHF GBP AUD NZD CAD SEK NOK

Weekly spot gains / losses of the USD vs. the other G-10 units

0.95%

-0.35%-0.61%

-0.41%

0.71%

1.95%

0.74%

0.17%

-0.07%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

USD JPY CHF GBP AUD NZD CAD SEK NOK

Weekly spot gains / losses of the EUR vs. the other G-10 units

JPY WEEKLY PERFORMANCE CHF WEEKLY PERFORMANCE

1.29%

0.36%

-0.01%

1.09%

0.29%

-0.20%

1.07%

0.54%

2.29%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

USD EUR CHF GBP AUD NZD CAD SEK NOK

Weekly spot gains / losses of the JPY vs. the other G-10 units

1.52%

0.57%

0.22% 0.18%

1.30%

0.72%0.50%

1.27%

2.52%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

USD EUR JPY GBP AUD NZD CAD SEK NOK

Weekly spot gains / losses of the CHF vs. the other G-10 units

GBP WEEKLY PERFORMANCE NORDICS WEEKLY PERFORMANCE

1.34%

0.39%

-0.23%

1.12%

0.57%0.33%

2.35%

0.08%

1.08%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

USD EUR JPY CHF AUD NZD CAD SEK NOK

Weekly spot gains / losses of the GBP vs. the others G.10 units

0.77%

-0.19%

-0.74%-0.56%

1.75%

0.56%

-0.25%

1.05%

0.08%

-0.34%-0.50% -0.38%

0.77%