Embed Size (px)

Citation preview

A Survey of Recent Empirical Money Demand Studies

SUBRAMANIAN S. SRIRAM*

This paper surveys a selected number of studies that evaluated the demand formoney using the error-correction model approach in the 1990s across a range ofindustrial and developing countries. It briefly presents issues relevant to modelingand estimating the demand for money; and synthesizes information concerningvariables, data period and frequency, unit root and cointegration techniques,stability tests, and findings in a tabular form. In addition, it presents estimatedlong-run income elasticity and elasticities or semi-elasticities for opportunity costand other variables in a comparable framework. It aims to provide a referencetool for future research on demand for money in various countries. [JEL E41]

Demand for money plays a major role in macroeconomic analysis, especiallyin selecting appropriate monetary policy actions. Consequently, a steady

stream of theoretical and empirical research has been carried out worldwide overthe past several decades. The interest has, however, heightened in recent years,triggered primarily by the concern among central banks and researchers on theimpact of the movement toward flexible exchange rate regime, globalization ofcapital markets, ongoing domestic financial liberalization and innovation,advancement in time series econometrics, and country-specific issues.

The extensive literature underscores two major points relevant to modelingand estimating the demand for money: variable selection and representation, and

334

IMF Staff PapersVol. 47, No. 3© 2001 International Monetary Fund

MVPY

=

s

t

−+1

PS

=*

PV

QX

t

t

t+

()

+

+1

yp+ (β

1+( )i

S

*

L Y i( ), *

Y SPP

,

ε+ >*

*This paper was written while the author was with the IMF Research Department; currently he is anEconomist in the IMF Statistics Department. He thanks Michael D. Bradley and Frederick L. Joutz ofGeorge Washington University; Charles Adams, James Boughton, and Timothy D. Lane of the IMF; NeilEricsson of the Board of Governors of the Federal Reserve System, and K.S. Venkatraman, formerly ofthe World Bank, for useful comments.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

335

framework chosen. Failure to provide due consideration to these issues has tendedto yield poor results. For the former, proper specification of opportunity cost vari-ables happens to be the most important factor in getting meaningful results.Regarding the latter, the chosen system should be free of theoretical and estima-tion problems, and should perform well in empirical testing. The error-correctionmodels (ECMs) have shown to meet these criteria.

This paper surveys a selected number of papers that applied the ECMapproach to analyze the demand for money (of various definitions) during the1990s in several industrial and developing countries.1 The objective is to extractrelevant information from these studies and provide it in a readily useable andcomparable framework. In specific, the paper presents details concerning thetechniques followed, variables chosen, periods and frequency selected, and majorfindings. In addition, it summarizes the long-run income elasticities, interest-ratesemi-elasticities (or elasticities), and the coefficients of other relevant variables.It is hoped that the materials presented in this paper provide some reference pointsconcerning the behavior of money demand in various countries, which in turn willhelp the policy makers in designing appropriate monetary policy actions and theresearchers in carrying out further research.2

The paper is organized as follows: Section I briefly specifies the generalframework that usually underlies the empirical formulation in estimating thedemand for money. Section II carries out relevant discussion regarding the vari-ables and estimation techniques, and summarizes information concerning variousstudies including the findings and estimated coefficients. Finally, Section IIIpresents the conclusions.

I. General Framework

There is a diverse spectrum of money demand theories emphasizing the transac-tions, speculative, precautionary or utility considerations.3 These theories implic-itly address a broad range of hypotheses. One significant aspect, however, is thatthey share common important elements (variables) among almost all of them. Ingeneral, they bring forth relationship between the quantity of money demandedand a set of few important economic variables linking money to the real sector ofthe economy (see Judd and Scadding, 1982, p. 993). What sets apart among thesetheories is that although they consider similar variables to explain the demand formoney, they frequently differ in the specific role assigned to each. Consequentlyone consensus that emerges from the literature is that the empirical work is moti-vated by a blend of theories.

The general specification begins with the following functional relationshipfor the long-term demand for money:

1This paper is based on Sriram (1999b, 1999c, and 2000). There have been other survey papers (forexample, Judd and Scadding, 1982; Goldfeld and Sichel, 1990; Boughton, 1992; Laidler, 1993); but none ofthem focused exclusively on ECMs and covering a wide range of both industrial and developing countries.

2Refer to Ericsson (1998) for general issues concerning the empirical modeling of money demand.3See, Laidler (1993) and Sriram (1999c), among others, for a survey of these approaches.

(1)

where the demand for real balances M/P is a function of the chosen scale variable(S) to represent the economic activity and the opportunity cost of holding money(OC). M stands for the selected monetary aggregate in nominal term and P for theprice. Like in theoretical models, the empirical models generally specify themoney demand as a function of real balances (see Laidler, 1993).4

II. Discussion on Variables and Estimation Techniques

Given the above general framework, this section provides a brief overview ofissues concerning selection and representation of variables, modeling, and esti-mation. Sriram (1999c) presents detailed account of these issues, including rele-vant references justifying various approaches undertaken by the researchers. Theliterature shows that money demand has been estimated for various aggregates,their components, or certain combination of these components. As definitions ofmoney differ across countries (see Boughton, 1992, and Kumah, 1989), measuresconsidered, including divisia aggregates, also varied across studies. Scale variableis used in the estimation as a measure of transactions relating to the economicactivity. It is usually represented by variables expressing income, expenditure, orwealth concept (although a host of other variables is discussed in the literature).The price variable is selected to follow closely the chosen scale variable, althoughconsumer price index is the most commonly used measure.

One of the most important aspects of modeling the demand for money is theselection of appropriate opportunity cost variables. The literature has shown thatstudies which paid inadequate attention on this matter produced poor results.There are two major ingredients: (i) own-rate and (ii) alternative return on money.The former happens to be very important, especially if the financial innovation hasbeen taking place in an economy (see Ericsson, 1998). The latter involves yieldson domestic financial and real assets for a closed economy, and additionally onforeign assets for an open economy. A number of instruments are available torepresent the yields on domestic financial assets. The yield on real assets is usuallyproxied by the expected inflation. And, on foreign assets by foreign interest rateor some form of exchange rate variable. Prior to selecting appropriate opportunitycost variables, careful attention should be paid on evaluating macroeconomic situ-ation and developments in the financial system (including institutional details andthe regulatory environment), and degree of openness of the economy.

The economic theory provides some guidance in reference to the relationshipbetween demand for money and its arguments. As the scale variable represents thetransactions or wealth effects, it is positively related to the demand for money. The

MP

f S OC= ( ),

Subramanian S. Sriram

336

4Using the real money balance as the dependent variable will also mean that price homogeneity is explic-itly imposed into the model. Additionally, there are less severe econometric problems associated with usingreal rather than nominal balances as the dependent variable (see Boughton, 1981, and Johansen, 1992b). And,majority of the empirical work does find evidence for the demand being for real balances.

own-rate is expected to be positively related as higher the return on money, lessthe incentive to hold assets alternative for money. Conversely, higher the returnson alternative assets, lower the incentive to hold money, and hence, the coeffi-cients of alternative returns expected to be negative. The expected inflation gener-ally affects the demand for money negatively as agents prefer to hold real assetsas hedges during the periods of rising inflation. The foreign interest rates areexpected to exert negative influence as increase in foreign interest rates potentiallyinduce the domestic residents to increase their holdings of foreign assets whichwill be financed by drawing down domestic money holdings. Similarly, theexpected exchange depreciation will also have a negative relationship. An increasein expected depreciation implies that the expected returns from holding foreignmoney increases, and hence, agents would substitute the domestic currency forforeign currency.5

The economic theory does not provide any rationale as to the correct mathe-matical form of the money demand function. There is consensus, however, that thelog-linear version is the most appropriate functional form (see Zarembka, 1968).While money and scale variables typically enter in logarithms, interest rate vari-ables appear either in levels or in logarithms. Consequently, estimates of the coef-ficient for the scale variable directly provides the measure of income elasticity,and those of interest rates show either elasticities or semi-elasticities depending onthe way they are introduced in the formulation.

The partial adjustment framework was extremely popular in the 1970s.However, it was shown to suffer from specification problem and highly restrictivedynamics (see, for example, Cooley and LeRoy, 1981; Goodfriend, 1985; Hendry,1979 and 1985; Hendry and Mizon, 1978). To counter these problems, two majorsolutions were proposed—modifying the theoretical base and improving thedynamic structure. The former led to buffer-stock models (BSMs), which werebuilt upon the theory of precautionary demand for money (see, for example,Laidler, 1984; Cuthbertson and Taylor, 1987; Milbourne, 1988), and the latter toECMs.6 The BSMs also ran into criticism, especially in their relevance in theempirical estimation (see Milbourne, 1988). Meanwhile, ECMs seem to bepromising. An important aspect of these models is that the data characteristics arethoroughly examined before selecting the appropriate estimation techniques.Furthermore, lag structures are selected based on the data generating process ofthe economic variables and not on a priori based on the economic theory or naivedynamic theory.

The ECM is shown to contain information on both the short- and long-runproperties of the model with disequilibrium as a process of adjustment to the long-run equilibrium. Granger (1983 and 1986) has demonstrated that the concept ofstable long-run equilibrium is the statistical equivalence of cointegration. Whencointegration holds and if there is any shock that causes disequilibrium, thereexists a well-defined short-term dynamic adjustment process such as the error-

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

337

5Refer to Jusoh (1987) and Tan (1997) for reasons to expect positive relationship for expected inflationand expected exchange rate depreciation with the demand for real money respectively.

6In fact, Hendry, Pagan, and Sargan (1984) showed that PAMs and BSMs form the special cases of ECMs.

correction mechanism that will push back the system toward the long-run equilib-rium. In fact, cointegration does imply the existence of a dynamic error-correctionform relating to variables in question (see Engle and Granger, 1987). The majoradvantage of the error-correction modeling is that the economic theory is allowedto specify the long-run equilibrium while the short-run dynamics be defined fromthe data.

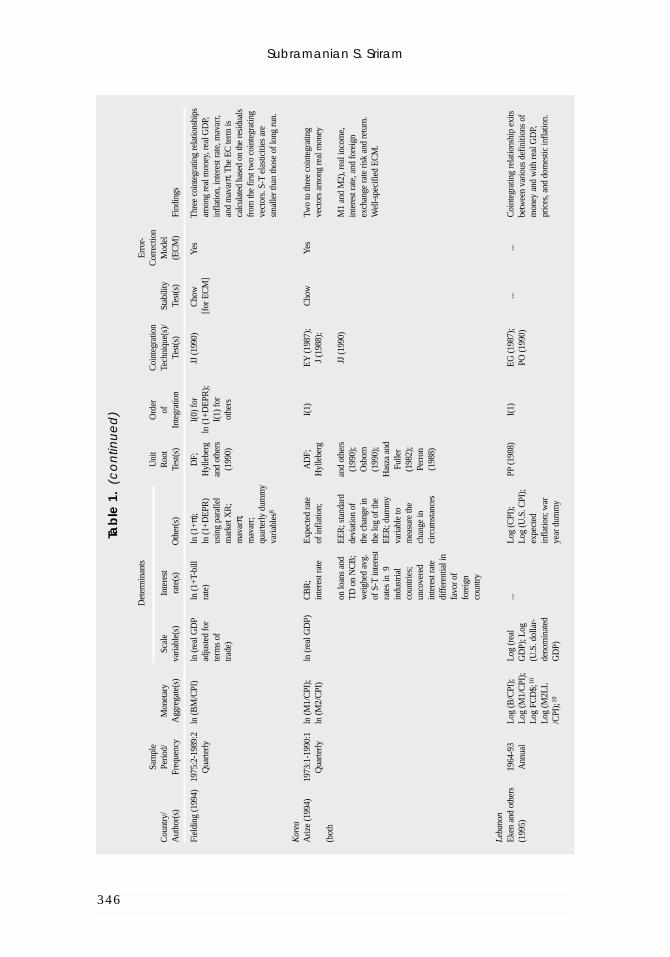

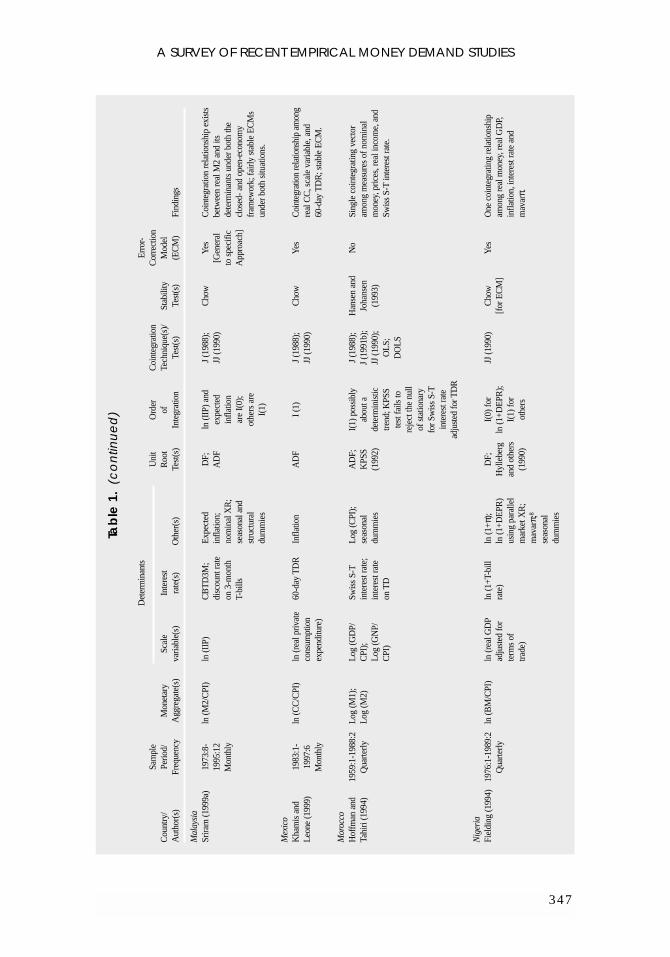

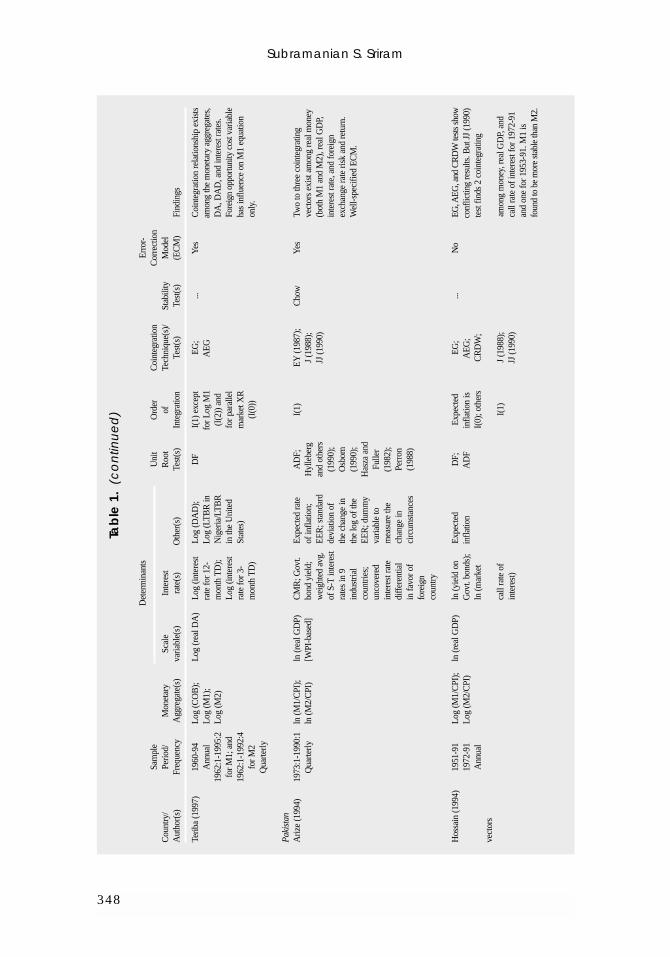

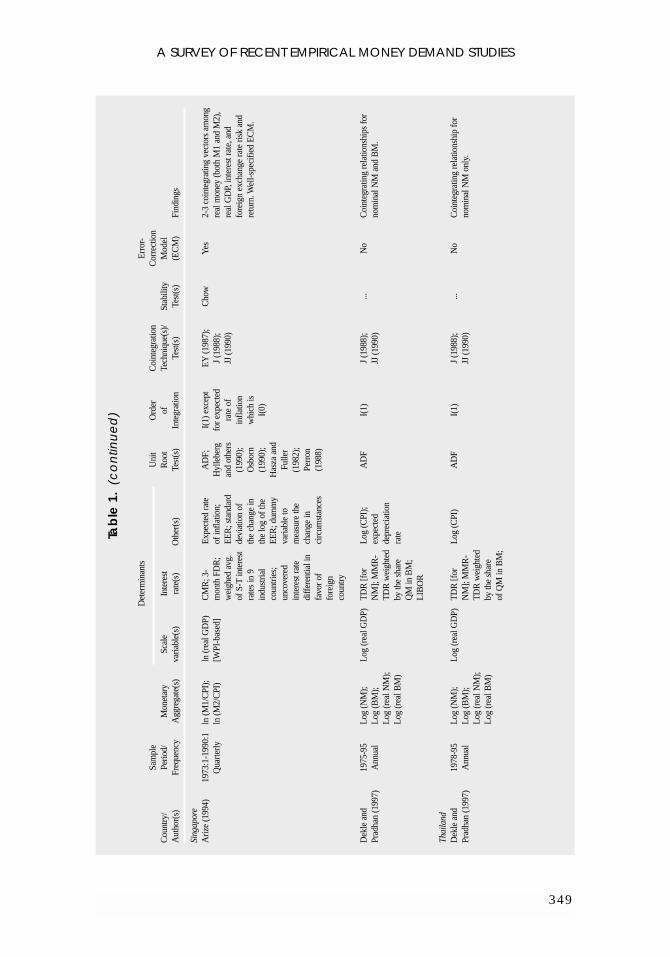

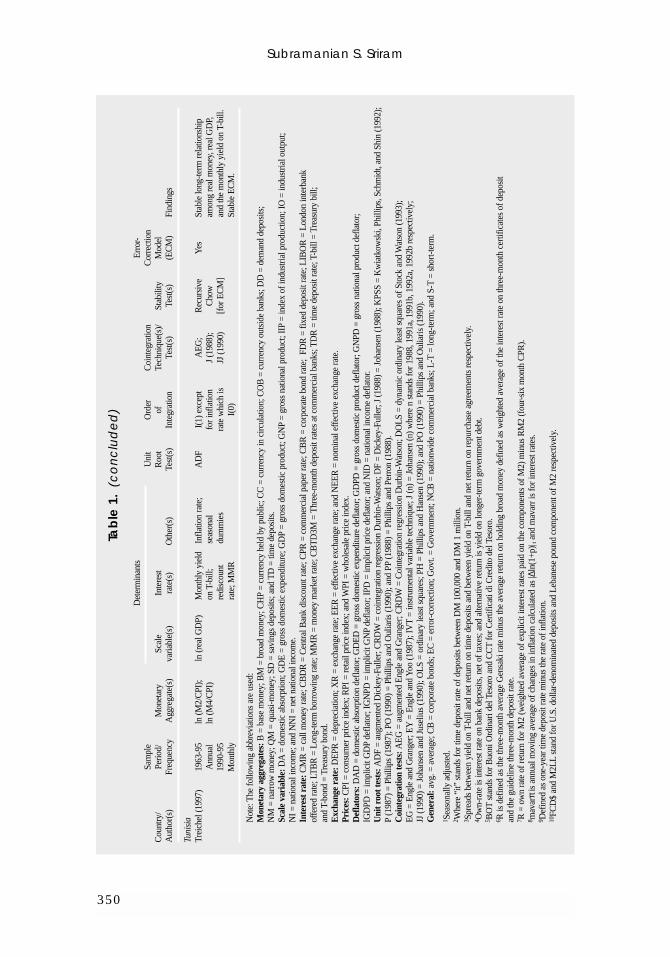

The earlier ECMs on money demand tended to be based on the single equa-tion cointegrating relationship between money and the chosen scale variables asdeveloped by Engle and Granger (1987). However, further research suggested thatmultivariate cointegrating vectors encompassing a broader number of variablesprovided a fuller characterization of the long-run determinants of demand. Thespecification of such multiple cointegrating vectors between nonstationary vari-ables primarily employs the procedures developed by Johansen (1988) andJohansen and Juselius (1990) which make the original Engle-Granger frameworka special case. However, as can be seen from Table 1, a number of other measuresavailable to conduct the cointegration analysis.7

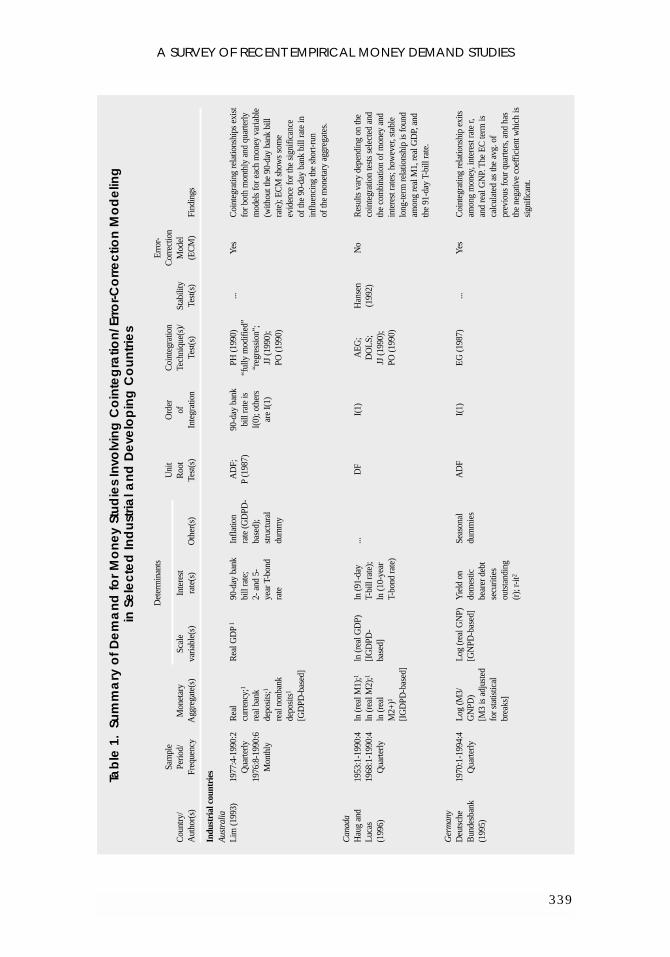

Table 1 also presents details relevant to modeling and estimating the demandfor money from various studies. In specific, it summarizes information for a cross-section of developing and industrial countries, on monetary aggregates (nominalor real), scale variable(s), and the opportunity cost and other variables included;data period and frequency chosen; unit root, cointegration, and stability testsapplied; nature of various time series (such as the order of integration and whetherseasonally adjusted or not). It also presents the findings. The presentation of infor-mation will enable the researchers to draw some insights into the justification ofselecting diverse set of variables and approaches across various countries.

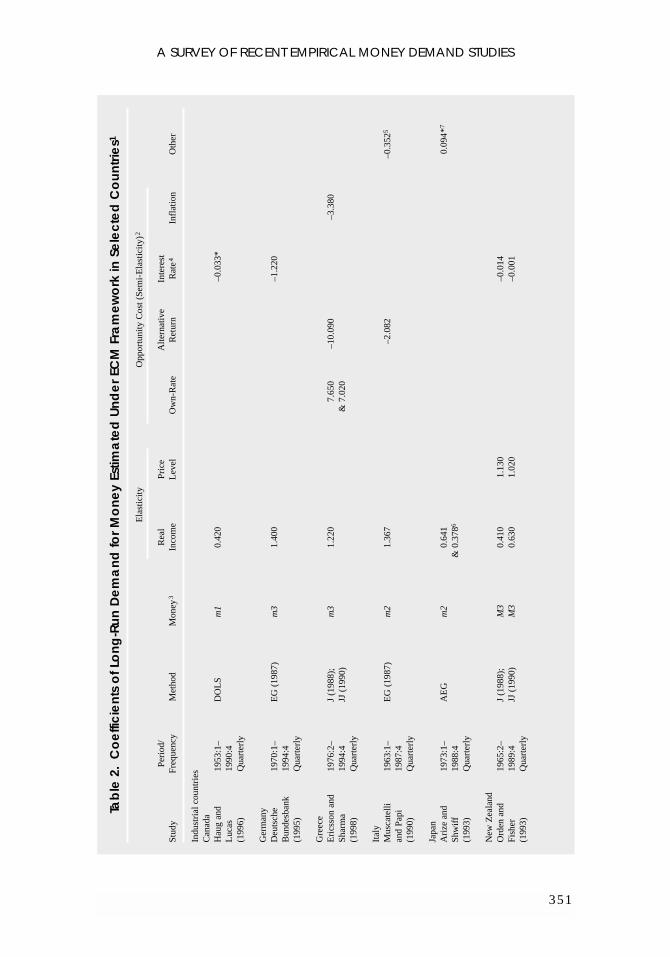

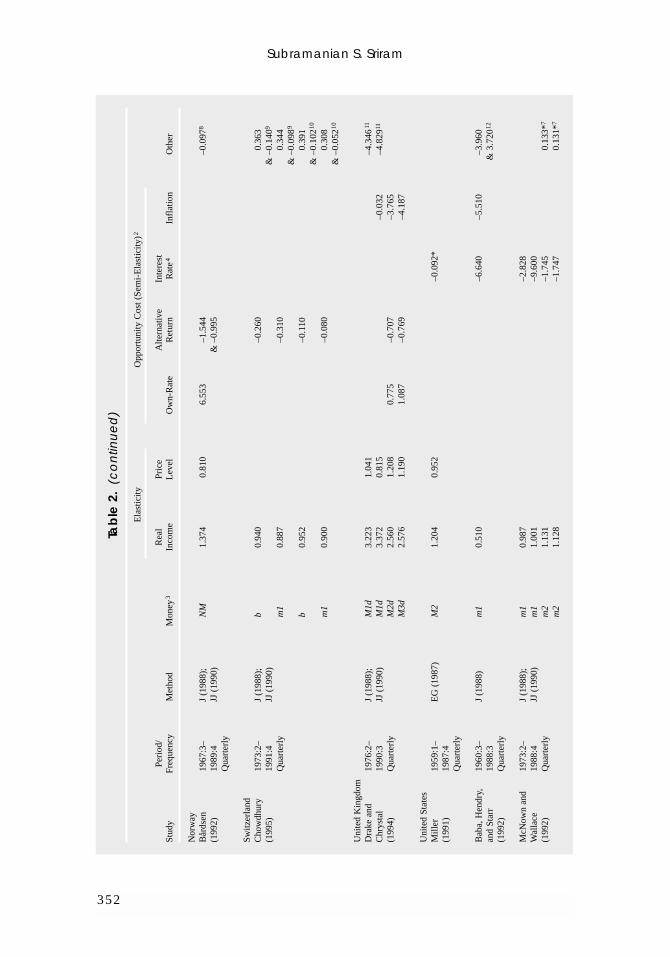

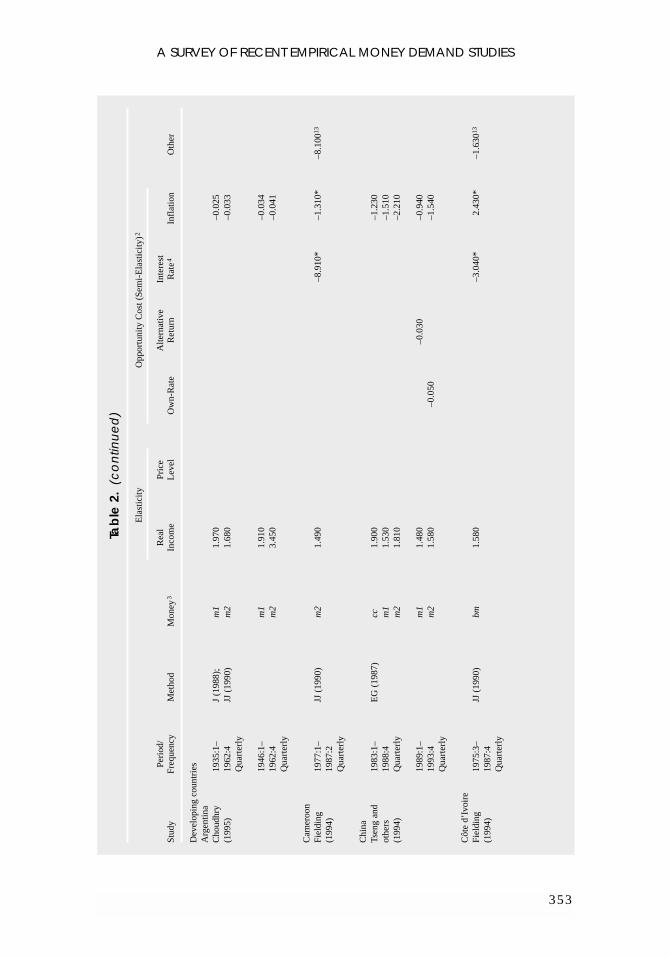

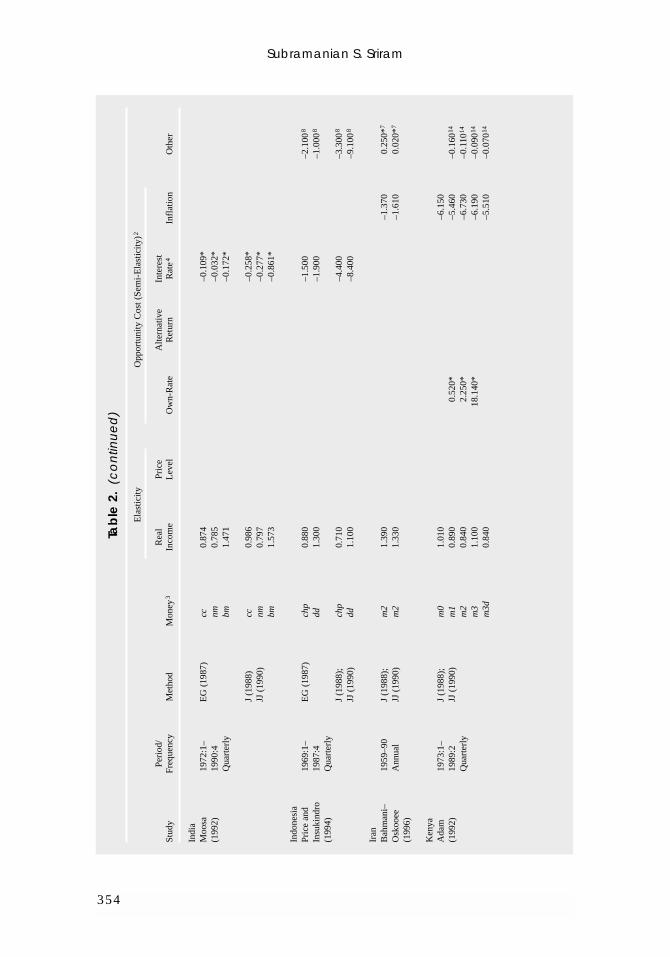

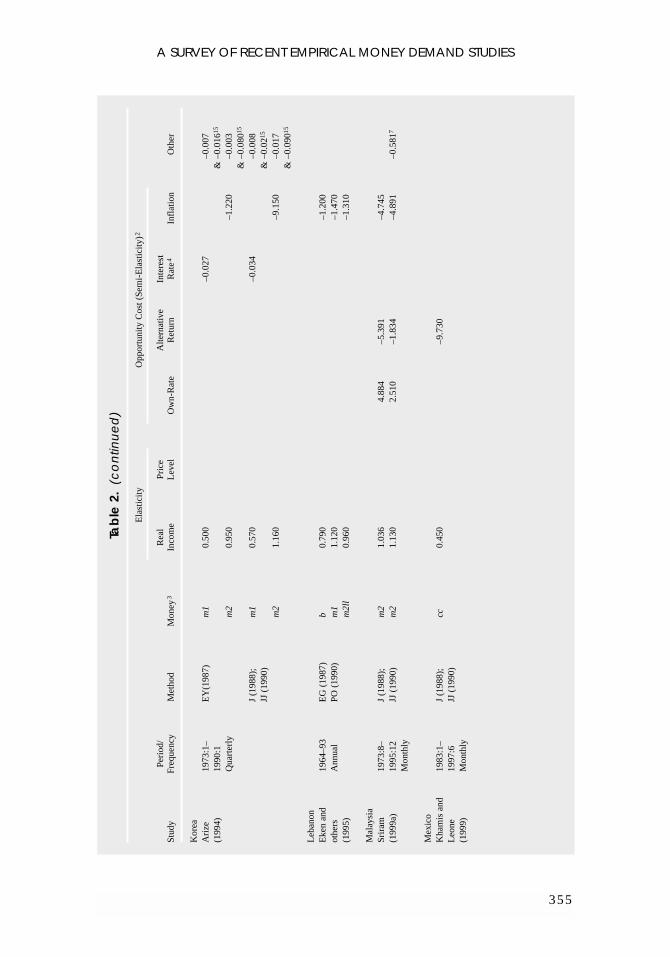

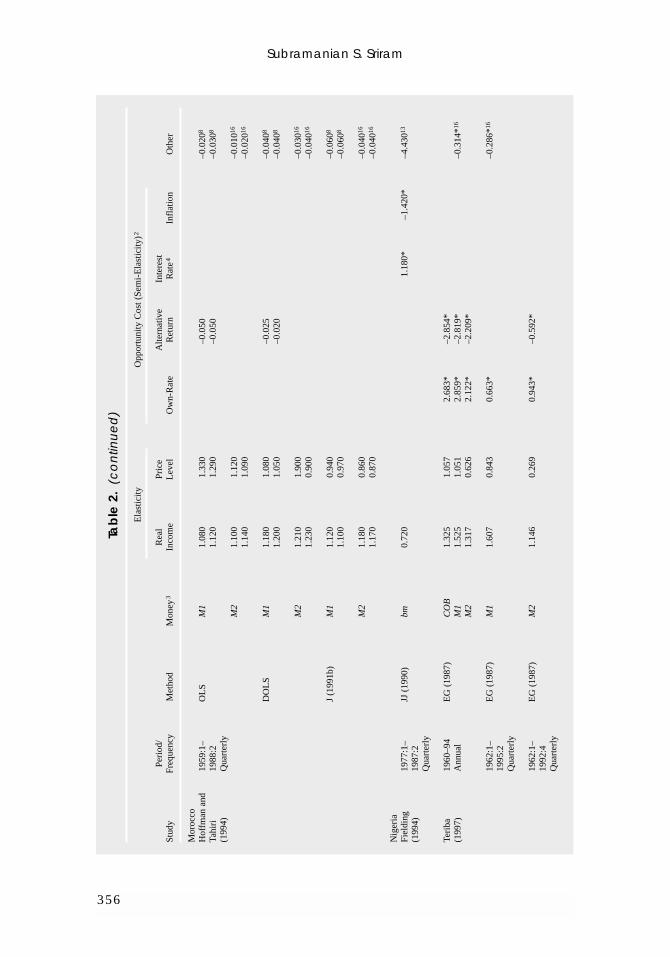

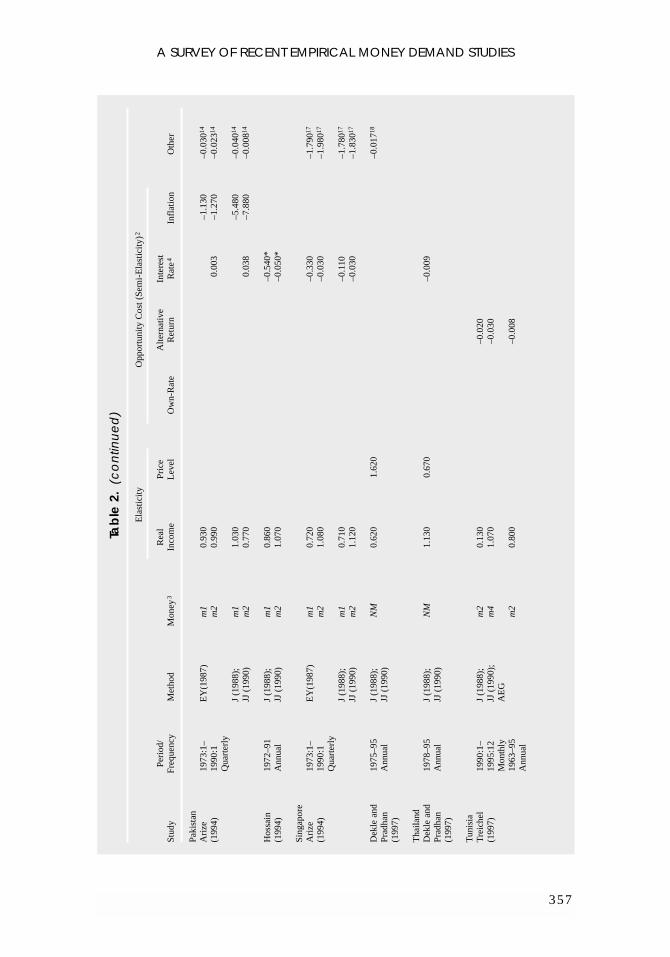

Table 2 summarizes the long-run income elasticities and the semi-elasticities orelasticities of opportunity cost and other variables from those studies listed in Table1. As the short-run dynamics can be potentially complicated, the table concentratesonly on the long-run results. In order to promote comparability, the results are shownonly for those studies which reported the long-term relationship (existence of cointe-gration). If more than one cointegration relationship is found, results are reported onlyfor the preferred cointegration vector(s) as identified by the author(s), which not onlymeet a battery of statistical tests but also economically make sense with correct signsof the variables and meaningful size of coefficients.

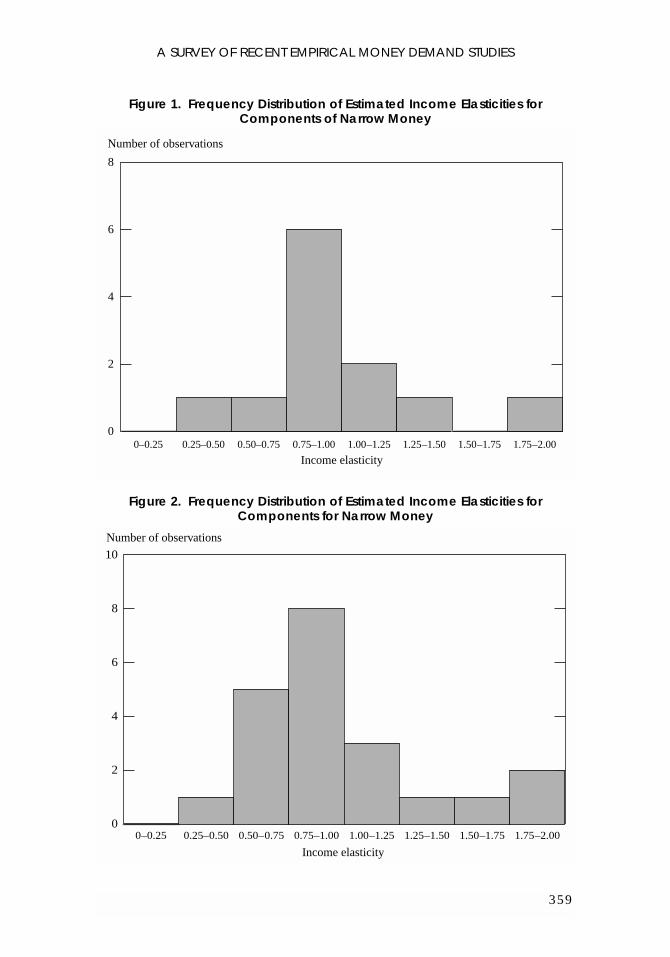

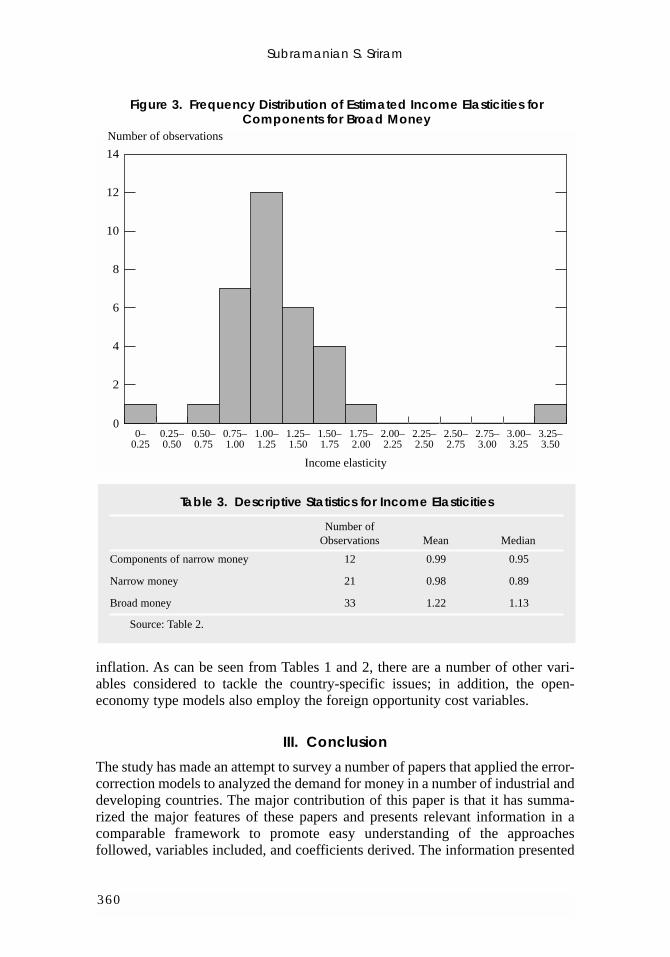

Figures 1–3 show the distribution of income elasticities for real money aspresented in Table 2 for components of narrow money, narrow money, and broadmoney respectively. The relevant descriptive statistics is shown in Table 3. It isclear from the table, the medians for all three groups are closer to one than to 0.5thereby indicating that money does not play the role of transaction measure alone.There is no clear guidance from the theory or empirical studies regarding theacceptable magnitude on elasticities or semi-elasticities of the opportunity costvariables. The most relevant information will be the signs of the coefficients—positive for own-rate and negative for alternative return on money and expected

Subramanian S. Sriram

338

7Refer to Sriram (1999c) for a longer list of studies that applied the ECM framework to analyze thedemand for money in the past two decades.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

339

Tab

le 1

.Su

mm

ary

of D

em

an

d fo

r M

on

ey

Stu

die

s In

volv

ing

Co

inte

gra

tion

/Err

or-C

orr

ec

tion

Mo

de

ling

in

Se

lec

ted

Ind

ust

rial a

nd

De

velo

pin

g C

ou

ntri

es

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Indu

stri

al c

ount

ries

Aus

tral

iaL

im (1

993)

1977

:4-1

990:

2R

eal

Rea

l GD

P1

90-d

ay b

ank

Infla

tion

AD

F;90

-day

ban

kPH

(199

0)...

Yes

Coi

nteg

ratin

g re

latio

nshi

ps e

xist

Qua

rterly

curr

ency

;1bi

ll ra

te;

rate

(GD

PD-

P(1

987)

bill

rate

is“f

ully

mod

ified

” fo

r bot

h m

onth

ly a

nd q

uarte

rly19

76:8

-199

0:6

real

ban

k 2-

and

5-

base

d);

I(0)

; oth

ers

“reg

ress

ion”

;m

odel

s fo

r eac

h m

oney

var

iabl

eM

onth

lyde

posi

ts;1

year

T-b

ond

stru

ctur

alar

e I(

1)JJ

(199

0);

(with

out t

he 9

0-da

y ba

nk b

illre

al n

onba

nkra

tedu

mm

yPO

(199

0)ra

te);

EC

M s

how

s so

me

depo

sits

1ev

iden

ce fo

r the

sig

nific

ance

[GD

PD-b

ased

]of

the

90-d

ay b

ank

bill

rate

in

influ

enci

ng th

e sh

ort-r

un

of th

e m

onet

ary

aggr

egat

es.

Can

ada

Hau

g an

d 19

53:1

-199

0:4

ln (r

eal M

1);1

ln (r

eal G

DP)

ln (9

1-da

y...

DF

I(1)

AE

G;

Han

sen

No

Res

ults

var

y de

pend

ing

on th

eL

ucas

19

68:1

-199

0:4

ln (r

eal M

2);1

[IG

DPD

-T-

bill

rate

);D

OL

S;(1

992)

coin

tegr

atio

n te

sts

sele

cted

and

(199

6)Q

uarte

rlyln

(rea

lba

sed]

ln (1

0-ye

arJJ

(199

0);

the

com

bina

tion

of m

oney

and

M2+

)1T-

bond

rate

)PO

(199

0)in

tere

st ra

tes;

how

ever

, sta

ble

[IG

DPD

-bas

ed]

long

-term

rela

tions

hip

is fo

und

amon

g re

al M

1, re

al G

DP,

and

the

91-d

ay T

-bill

rate

.

Ger

man

yD

euts

che

1970

:1-1

994:

4L

og (M

3/L

og (r

eal G

NP)

Yie

ld o

n Se

ason

al

AD

FI(

1)E

G (1

987)

...Y

esC

oint

egra

ting

rela

tions

hip

exits

Bun

desb

ank

Qua

rterly

GN

PD)

[GN

PD-b

ased

]do

mes

ticdu

mm

ies

amon

g m

oney

, int

eres

t rat

e r,

(199

5)[M

3 is

adj

uste

dbe

arer

deb

tan

d re

al G

NP.

The

EC

term

isfo

r sta

tistic

alse

curit

ies

calc

ulat

ed a

s th

e av

g. o

f br

eaks

]ou

tsta

ndin

g pr

evio

us fo

ur q

uarte

rs, a

nd h

as

(r);

r-it2

the

nega

tive

coef

ficie

nt w

hich

is

sign

ifica

nt.

Subramanian S. Sriram

340

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

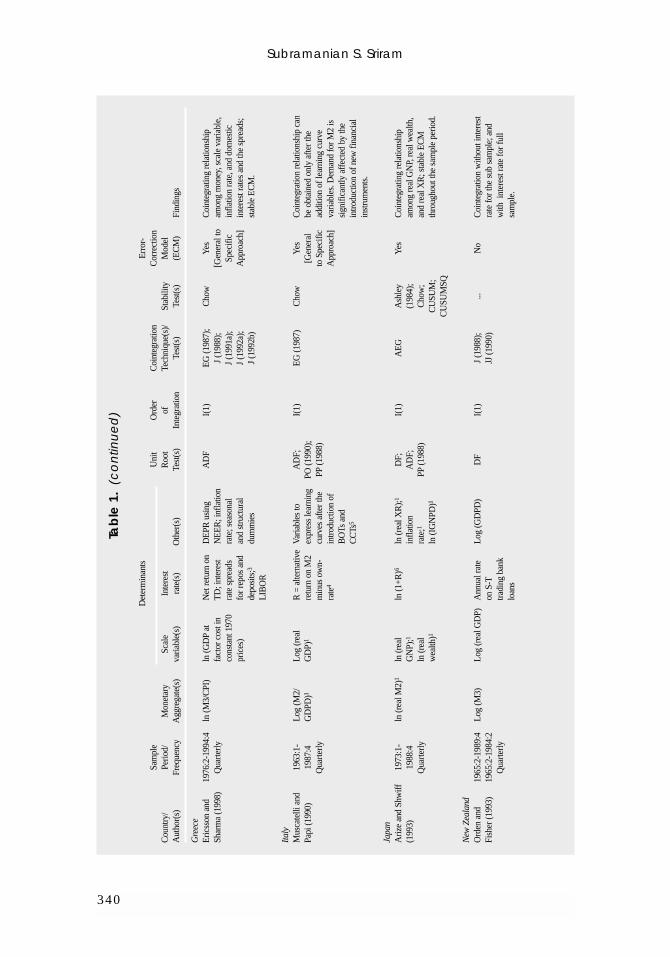

Gre

ece

Eric

sson

and

1976

:2-1

994:

4ln

(M3/

CPI

)ln

(GD

Pat

Net

retu

rn o

nD

EPR

usi

ngA

DF

I(1)

EG

(198

7);

Cho

wY

esC

oint

egra

ting

rela

tions

hip

Shar

ma

(199

8)Q

uarte

rlyfa

ctor

cos

t in

TD

; int

eres

tN

EE

R; i

nfla

tion

J (1

988)

;[G

ener

al to

amon

g m

oney

, sca

le v

aria

ble,

co

nsta

nt 1

970

rate

spr

eads

ra

te; s

easo

nal

J (1

991a

);Sp

ecifi

cin

flatio

n ra

te, a

nd d

omes

tic

pric

es)

for r

epos

and

an

d st

ruct

ural

J (1

992a

);A

ppro

ach]

inte

rest

rate

s an

d th

e sp

read

s;

depo

sits

;3du

mm

ies

J (1

992b

)st

able

EC

M.

LIB

OR

Italy

Mus

cate

lli a

nd19

63:1

-L

og (M

2/L

og (r

eal

R =

alte

rnat

ive

Var

iabl

es to

AD

F;I(

1)E

G (1

987)

Cho

wY

esC

oint

egra

tion

rela

tions

hip

can

Papi

(199

0)19

87:4

GD

PD)1

GD

P)1

retu

rn o

n M

2ex

pres

s le

arni

ngPO

(199

0);

[Gen

eral

be o

btai

ned

only

afte

r the

Q

uarte

rlym

inus

ow

n-cu

rves

afte

r the

PP(1

988)

to S

peci

ficad

ditio

n of

lear

ning

cur

ve

rate

4in

trodu

ctio

n of

App

roac

h]va

riabl

es. D

eman

d fo

r M2

is

BO

Ts a

nd

sign

ifica

ntly

aff

ecte

d by

the

CC

Ts5

intro

duct

ion

of n

ew fi

nanc

ial

inst

rum

ents

.

Japa

nA

rize

and

Shw

iff19

73:1

-ln

(rea

l M2)

1ln

(rea

lln

(1+R

)6ln

(rea

l XR

);1D

F;I(

1)A

EG

Ash

ley

Yes

Coi

nteg

ratin

g re

latio

nshi

p (1

993)

1988

:4

GN

P);1

infla

tion

AD

F;(1

984)

;am

ong

real

GN

P, re

al w

ealth

, Q

uarte

rlyln

(rea

lra

te;1

PP(1

988)

Cho

w;

and

real

XR

; sta

ble

EC

M

wea

lth)1

ln (I

GN

PD)1

CU

SUM

;th

roug

hout

the

sam

ple

perio

d.C

USU

MSQ

New

Zea

land

Ord

en a

nd

1965

:2-1

989:

4L

og (M

3)L

og (r

eal G

DP)

Ann

ual r

ate

Log

(GD

PD)

DF

I(1)

J (1

988)

;...

No

Coi

nteg

ratio

n w

ithou

t int

eres

t Fi

sher

(199

3)19

65:2

-198

4:2

on S

-TJJ

(199

0)ra

te fo

r the

sub

sam

ple;

and

Q

uarte

rlytra

ding

ban

kw

ith i

nter

est r

ate

for f

ull

loan

ssa

mpl

e.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

341

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

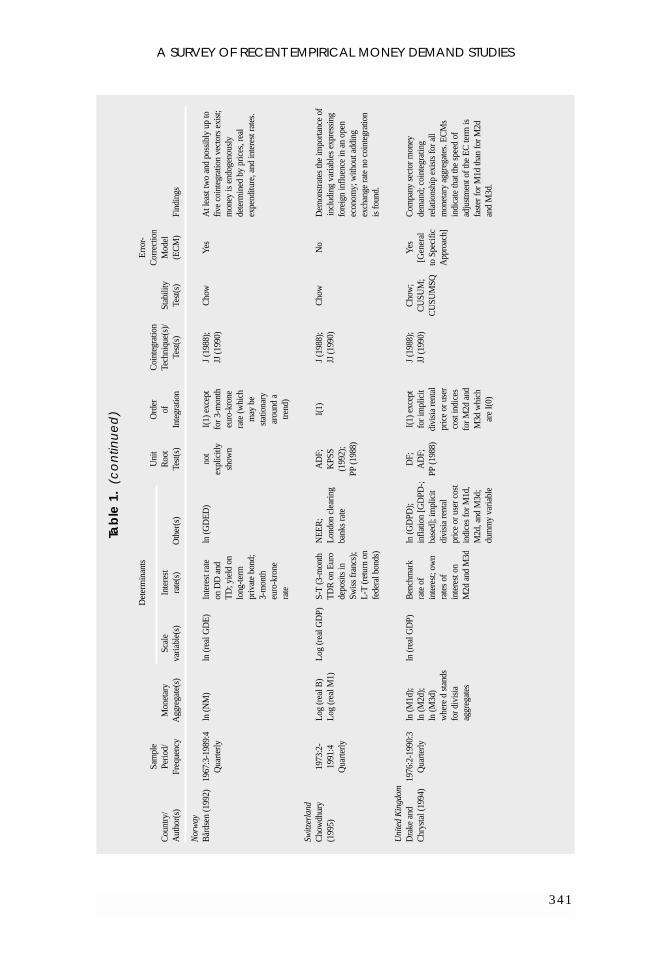

Nor

way

Bår

dsen

(199

2)19

67:3

-198

9:4

ln (N

M)

ln (r

eal G

DE

)In

tere

st ra

teln

(GD

ED

)no

tI(

1) e

xcep

tJ

(198

8);

Cho

w

Yes

At l

east

two

and

poss

ibly

up

toQ

uarte

rlyon

DD

and

expl

icitl

yfo

r 3-m

onth

JJ (1

990)

five

coin

tegr

atio

n ve

ctor

s ex

ist;

TD

; yie

ld o

nsh

own

euro

-kro

nem

oney

is e

ndog

enou

sly

long

-term

rate

(whi

chde

term

ined

by

pric

es, r

eal

priv

ate

bond

;m

ay b

e ex

pend

iture

, and

inte

rest

rate

s.3-

mon

th

stat

iona

ry

euro

-kro

ne

arou

nd a

ra

tetre

nd)

Switz

erla

ndC

how

dhur

y19

73:2

-L

og (r

eal B

)L

og (r

eal G

DP)

S-T

(3-m

onth

NE

ER

;A

DF;

I(1)

J (1

988)

;C

how

No

Dem

onst

rate

s th

e im

porta

nce

of(1

995)

1991

:4L

og (r

eal M

1)T

DR

on

Eur

oL

ondo

n cl

earin

gK

PSS

JJ (1

990)

incl

udin

g va

riabl

es e

xpre

ssin

g Q

uarte

rlyde

posi

ts in

ba

nks

rate

(199

2);

fore

ign

influ

ence

in a

n op

en

Swis

s fr

ancs

);PP

(198

8)ec

onom

y; w

ithou

t add

ing

L-T

(ret

urn

onex

chan

ge ra

te n

o co

inte

grat

ion

fede

ral b

onds

)is

foun

d.

Uni

ted

Kin

gdom

Dra

ke a

nd

1976

:2-1

990:

3ln

(M1d

);ln

(rea

l GD

P)B

ench

mar

kln

(GD

PD);

DF;

I(1)

exc

ept

J (1

988)

;C

how

;Y

esC

ompa

ny s

ecto

r mon

ey

Chr

ysta

l (19

94)

Qua

rterly

ln (M

2d);

rate

of

infla

tion

[GD

PD-;

AD

F;fo

r im

plic

itJJ

(199

0)C

USU

M;

[Gen

eral

dem

and;

coi

nteg

ratin

g ln

(M3d

)in

tere

st; o

wn

base

d]; i

mpl

icit

PP(1

988)

divi

sia

rent

alC

USU

MSQ

to S

peci

fic

rela

tions

hip

exis

ts fo

r all

whe

re d

sta

nds

rate

s of

di

visi

a re

ntal

pric

e or

use

r A

ppro

ach]

mon

etar

y ag

greg

ates

. EC

Ms

for d

ivis

iain

tere

st o

npr

ice

or u

ser c

ost

cost

indi

ces

indi

cate

that

the

spee

d of

ag

greg

ates

M2d

and

M3d

indi

ces

for M

1d,

for M

2d a

ndad

just

men

t of t

he E

C te

rm is

M

2d, a

nd M

3d;

M3d

whi

chfa

ster

for M

1d th

an fo

r M2d

du

mm

y va

riabl

ear

e I(

0)an

d M

3d.

Subramanian S. Sriram

342

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Uni

ted

Stat

esM

iller

(199

1)19

59:1

-198

7:4

ln (a

djus

ted

B);

ln (r

eal G

NP)

ln (4

-6 m

onth

ln (I

PD)

DF;

I(1)

EG

;...

Yes

Coi

nteg

ratio

n re

latio

nshi

p ex

ists

Qua

rterly

ln (M

1);

CPR

);A

DF

AE

Gam

ong

M2,

real

GN

P, IP

D,

ln (M

1A);

ln (d

ivid

end-

and

the

CPR

. EC

M fo

r M2

ln (M

2);

pric

e ra

tio)

sugg

ests

val

id a

nd s

igni

fican

t ln

(M3)

erro

r-co

rrec

tion

term

.

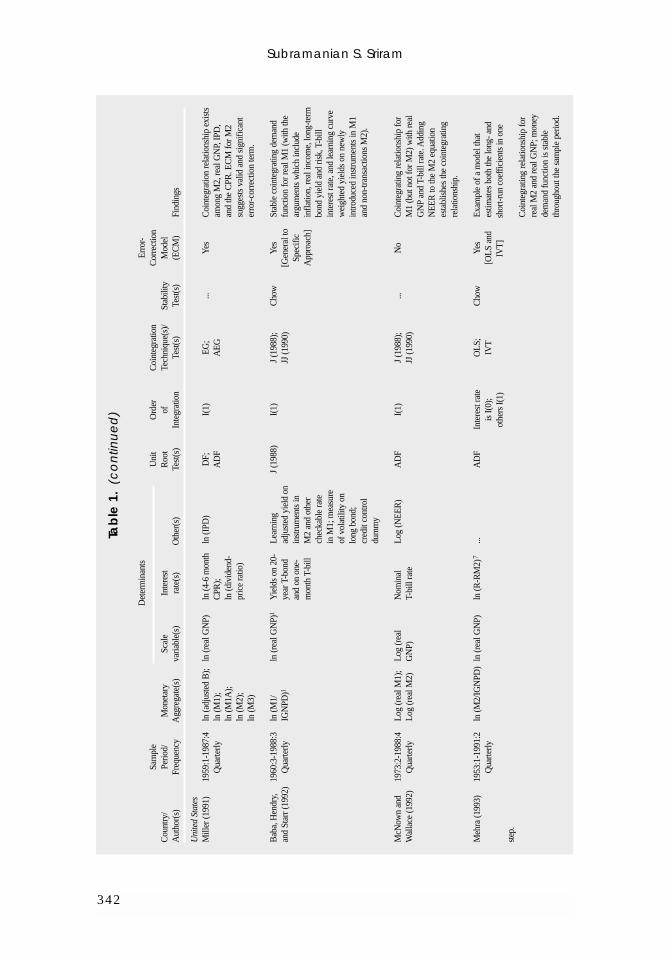

Bab

a, H

endr

y,19

60:3

-198

8:3

ln (M

1/ln

(rea

l GN

P)1

Yie

lds

on 2

0-L

earn

ing

J (1

988)

I(1)

J (1

988)

;C

how

Yes

Stab

le c

oint

egra

ting

dem

and

and

Star

r (19

92)

Qua

rterly

IGN

PD)1

year

T-b

ond

adju

sted

yie

ld o

nJJ

(199

0)[G

ener

al to

func

tion

for r

eal M

1 (w

ith th

ean

d on

one

-in

stru

men

ts in

Spec

ific

argu

men

ts w

hich

incl

ude

mon

th T

-bill

M2

and

othe

rA

ppro

ach]

infla

tion,

real

inco

me,

long

-term

ch

ecka

ble

rate

bond

yie

ld a

nd ri

sk, T

-bill

in

M1;

mea

sure

inte

rest

rate

, and

lear

ning

cur

ve

of v

olat

ility

on

wei

ghte

d yi

elds

on

new

ly

long

bon

d;

intro

duce

d in

stru

men

ts in

M1

cred

it co

ntro

lan

d no

n-tra

nsac

tions

M2)

.du

mm

y

McN

own

and

1973

:2-1

988:

4L

og (r

eal M

1);

Log

(rea

lN

omin

alL

og (N

EE

R)

AD

FI(

1)J

(198

8);

...N

oC

oint

egra

ting

rela

tions

hip

for

Wal

lace

(199

2)Q

uarte

rlyL

og (r

eal M

2)G

NP)

T-bi

ll ra

teJJ

(199

0)

M1

(but

not

for M

2) w

ith re

al

GN

Pan

d T-

bill

rate

. Add

ing

NE

ER

to th

e M

2 eq

uatio

nes

tabl

ishe

s th

e co

inte

grat

ing

rela

tions

hip.

Meh

ra (1

993)

1953

:1-1

991:

2ln

(M2/

IGN

PD)

ln (r

eal G

NP)

ln (R

-RM

2)7

...A

DF

Inte

rest

rate

OL

S;C

how

Yes

Exa

mpl

e of

a m

odel

that

Qua

rterly

is I(

0);

IVT

[OL

S an

des

timat

es b

oth

the

long

- and

ot

hers

I(1)

IVT]

shor

t-run

coe

ffic

ient

s in

one

step

.C

oint

egra

ting

rela

tions

hip

for

real

M2

and

real

GN

P; m

oney

dem

and

func

tion

is s

tabl

e th

roug

hout

the

sam

ple

perio

d.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

343

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

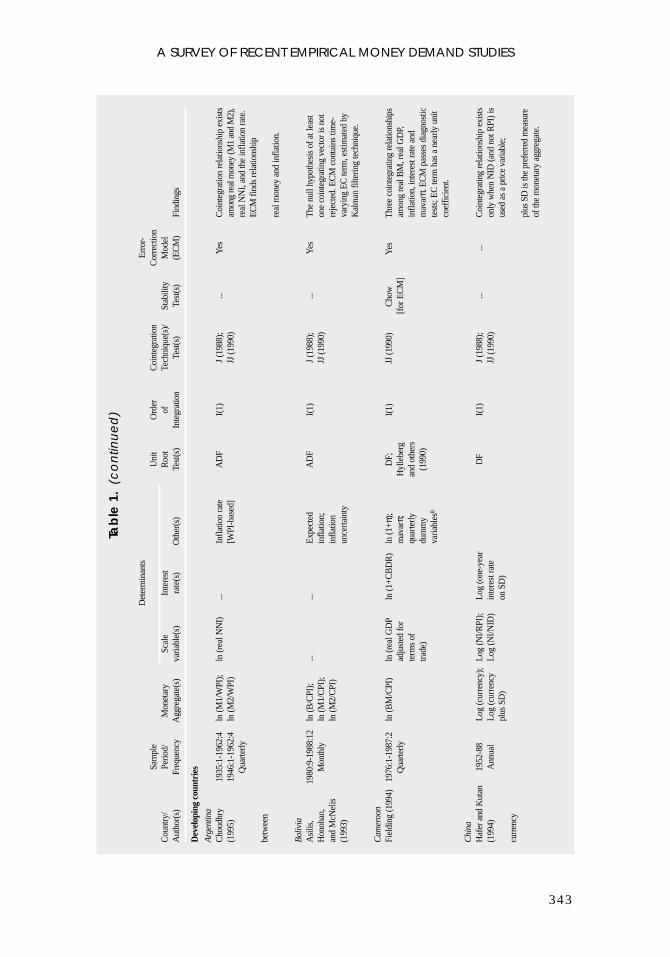

Dev

elop

ing

coun

trie

sA

rgen

tina

Cho

udhr

y19

35:1

-196

2:4

ln (M

1/W

PI);

ln (r

eal N

NI)

...In

flatio

n ra

teA

DF

I(1)

J (1

988)

;...

Yes

Coi

nteg

ratio

n re

latio

nshi

p ex

ists

(199

5)19

46:1

-196

2:4

ln (M

2/W

PI)

[WPI

-bas

ed]

JJ (1

990)

amon

g re

al m

oney

(M1

and

M2)

,Q

uarte

rlyre

al N

NI,

and

the

infla

tion

rate

. E

CM

find

s re

latio

nshi

pbe

twee

nre

al m

oney

and

infla

tion.

Bol

ivia

Asi

lis,

1980

:9-1

988:

12ln

(B/C

PI);

......

Exp

ecte

dA

DF

I(1)

J (1

988)

;...

Yes

The

nul

l hyp

othe

sis

of a

t lea

stH

onoh

an,

Mon

thly

ln (M

1/C

PI);

infla

tion;

JJ (1

990)

one

coin

tegr

atin

g ve

ctor

is n

otan

d M

cNel

isln

(M2/

CPI

)in

flatio

nre

ject

ed. E

CM

con

tain

s tim

e-(1

993)

unce

rtain

tyva

ryin

g E

C te

rm, e

stim

ated

by

Kal

man

filte

ring

tech

niqu

e.

Cam

eroo

nFi

eldi

ng (1

994)

1976

:1-1

987:

2ln

(BM

/CPI

)ln

(rea

l GD

Pln

(1+C

BD

R)

ln (1

+π);

DF;

I(1)

JJ (1

990)

Cho

wY

esTh

ree

coin

tegr

atin

g re

latio

nshi

psQ

uarte

rlyad

just

ed fo

rm

avar

π;

Hyl

lebe

rg[f

or E

CM

]am

ong

real

BM

, rea

l GD

P,te

rms

of

quar

terly

an

d ot

hers

infla

tion,

inte

rest

rate

and

trade

)du

mm

y(1

990)

mav

arπ.

EC

M p

asse

s di

agno

stic

varia

bles

8te

sts;

EC

term

has

a n

early

uni

tco

effic

ient

.

Chi

naH

afer

and

Kut

an19

52-8

8L

og (c

urre

ncy)

;L

og (N

I/RPI

);L

og (o

ne-y

ear

DF

I(1)

J (1

988)

;...

...C

oint

egra

ting

rela

tions

hip

exis

ts

(199

4)A

nnua

lL

og (c

urre

ncy

Log

(NI/N

ID)

inte

rest

rate

JJ (1

990)

only

whe

n N

ID (a

nd n

ot R

PI) i

spl

us S

D)

on S

D)

used

as

a pr

ice

varia

ble;

curr

ency

plus

SD

is th

e pr

efer

red

mea

sure

of th

e m

onet

ary

aggr

egat

e.

Subramanian S. Sriram

344

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

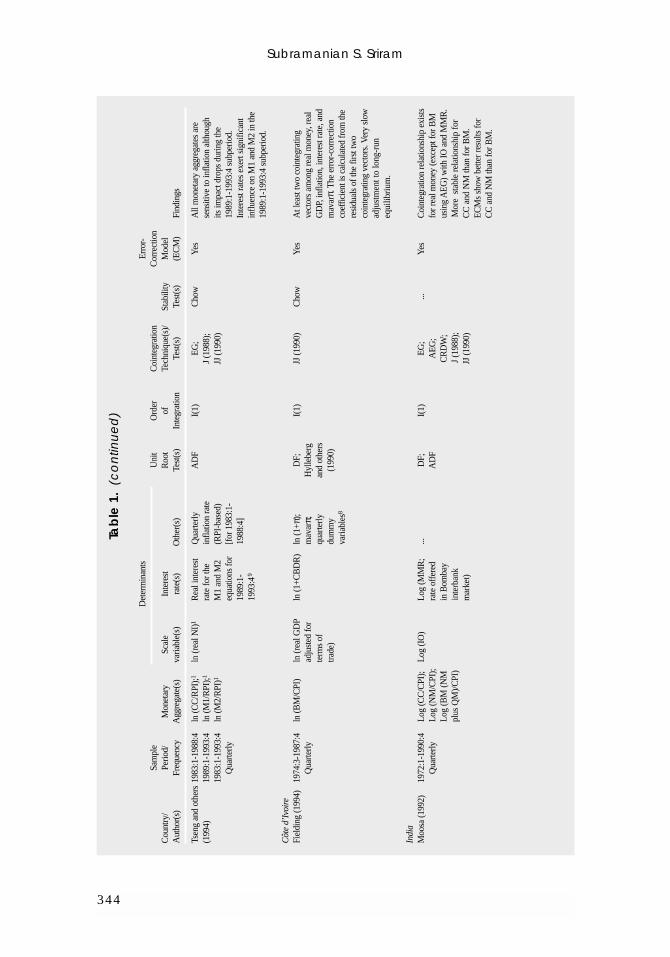

Tsen

g an

d ot

hers

1983

:1-1

988:

4ln

(CC

/RPI

);1ln

(rea

l NI)

1R

eal i

nter

est

Qua

rterly

AD

FI(

1)E

G;

Cho

wY

esA

ll m

onet

ary

aggr

egat

es a

re

(199

4)19

89:1

-199

3:4

ln (M

1/R

PI);1

rate

for t

hein

flatio

n ra

teJ

(198

8);

sens

itive

to in

flatio

n al

thou

gh19

83:1

-199

3:4

ln (M

2/R

PI)1

M1

and

M2

(RPI

-bas

ed)

JJ (1

990)

its im

pact

dro

ps d

urin

g th

e Q

uarte

rlyeq

uatio

ns fo

r[f

or 1

983:

1-19

89:1

-199

3:4

subp

erio

d.

1989

:1-

1988

:4]

Inte

rest

rate

s ex

ert s

igni

fican

t 19

93:4

9in

fluen

ce o

n M

1 an

d M

2 in

the

1989

:1-1

993:

4 su

bper

iod.

Côt

e d’

Ivoi

reFi

eldi

ng (1

994)

1974

:3-1

987:

4ln

(BM

/CPI

)ln

(rea

l GD

Pln

(1+C

BD

R)

ln (1

+π);

DF;

I(1)

JJ (1

990)

Cho

wY

esA

t lea

st tw

o co

inte

grat

ing

Qua

rterly

adju

sted

for

mav

arπ;

H

ylle

berg

vect

ors

amon

g re

al m

oney

, rea

l te

rms

of

quar

terly

an

d ot

hers

GD

P, in

flatio

n, in

tere

st ra

te, a

ndtra

de)

dum

my

(199

0)m

avar

π. T

he e

rror

-cor

rect

ion

varia

bles

8co

effic

ient

is c

alcu

late

d fr

om th

ere

sidu

als

of th

e fir

st tw

oco

inte

grat

ing

vect

ors.

Ver

y sl

owad

just

men

t to

long

-run

eq

uilib

rium

.

Indi

aM

oosa

(199

2)19

72:1

-199

0:4

Log

(CC

/CPI

);L

og (I

O)

Log

(MM

R;

...D

F;I(

1)E

G;

...Y

esC

oint

egra

tion

rela

tions

hip

exis

tsQ

uarte

rlyL

og (N

M/C

PI);

rate

off

ered

AD

FA

EG

;fo

r rea

l mon

ey (e

xcep

t for

BM

L

og (B

M (N

Min

Bom

bay

CR

DW

;us

ing

AE

G) w

ith IO

and

MM

R.

plus

QM

)/CPI

)in

terb

ank

J (1

988)

;M

ore

sta

ble

rela

tions

hip

for

mar

ket)

JJ (1

990)

CC

and

NM

than

for B

M.

EC

Ms

show

bet

ter r

esul

ts fo

r C

C a

nd N

M th

an fo

r BM

.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

345

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

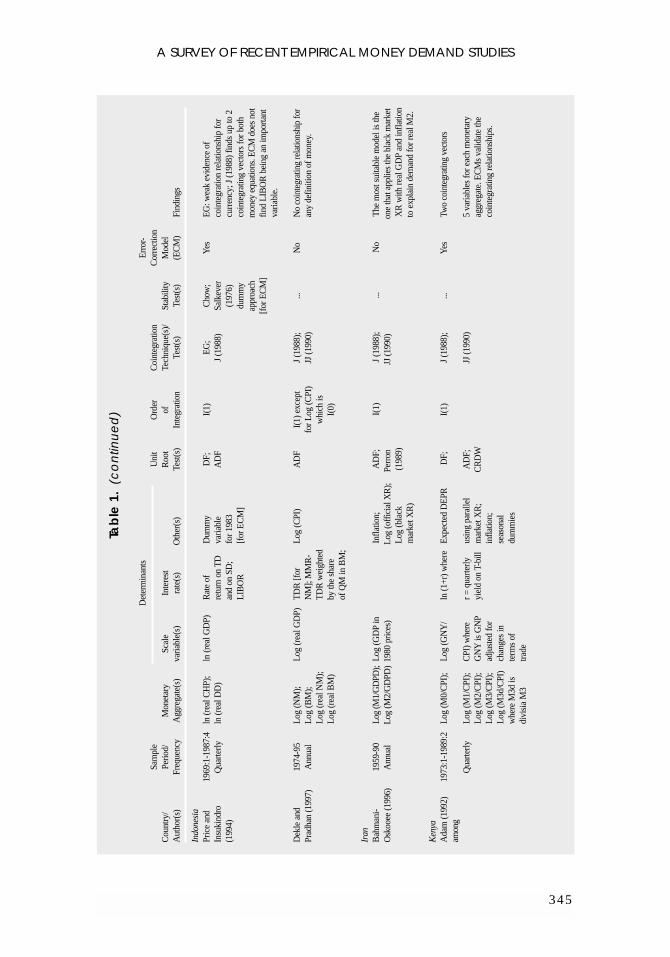

Indo

nesi

aPr

ice

and

1969

:1-1

987:

4ln

(rea

l CH

P);

ln (r

eal G

DP)

Rat

e of

D

umm

yD

F;I(

1)E

G;

Cho

w;

Yes

EG

: wea

k ev

iden

ce o

f In

suki

ndro

Qua

rterly

ln (r

eal D

D)

retu

rn o

n T

Dva

riabl

eA

DF

J (1

988)

Salk

ever

coin

tegr

atio

n re

latio

nshi

p fo

r(1

994)

and

on S

D;

for 1

983

(197

6)cu

rren

cy; J

(198

8) fi

nds

up to

2L

IBO

R[f

or E

CM

]du

mm

yco

inte

grat

ing

vect

ors

for b

oth

appr

oach

mon

ey e

quat

ions

. EC

M d

oes

not

[for

EC

M]

find

LIB

OR

bei

ng a

n im

porta

ntva

riabl

e.

Dek

le a

nd19

74-9

5L

og (N

M);

Log

(rea

l GD

P)T

DR

[for

Log

(CPI

)A

DF

I(1)

exc

ept

J (1

988)

;...

No

No

coin

tegr

atin

g re

latio

nshi

p fo

rPr

adha

n (1

997)

Ann

ual

Log

(BM

);N

M];

MM

R-

for L

og (C

PI)

JJ (1

990)

any

defin

ition

of m

oney

.L

og (r

eal N

M);

TD

R w

eigh

ted

whi

ch is

Log

(rea

l BM

)by

the

shar

eI(

0)of

QM

in B

M;

Iran

Bah

man

i-19

59-9

0Lo

g (M

1/G

DPD

);L

og (G

DP

inIn

flatio

n;

AD

F;I(

1)J

(198

8);

...N

oT

he m

ost s

uita

ble

mod

el is

the

Osk

ooee

(199

6)A

nnua

lL

og (M

2/G

DPD

)19

80 p

rices

)L

og (o

ffic

ial X

R);

Perr

onJJ

(199

0)on

e th

at a

pplie

s th

e bl

ack

mar

ket

Log

(bla

ck(1

989)

XR

with

real

GD

Pan

d in

flatio

n m

arke

t XR

)to

exp

lain

dem

and

for r

eal M

2.

Ken

yaA

dam

(199

2)19

73:1

-198

9:2

Log

(M0/

CPI

);L

og (G

NY

/ln

(1+r

) whe

reE

xpec

ted

DE

PRD

F;I(

1)J

(198

8);

...Y

esTw

o co

inte

grat

ing

vect

ors

amon

gQ

uarte

rlyL

og (M

1/C

PI);

CPI

) whe

rer =

qua

rterly

usin

g pa

ralle

lA

DF;

JJ (1

990)

5 va

riabl

es fo

r eac

h m

onet

ary

Log

(M2/

CPI

);G

NY

is G

NP

yiel

d on

T-b

illm

arke

t XR

;C

RD

Wag

greg

ate.

EC

Ms

valid

ate

the

Log

(M3/

CPI

);ad

just

ed fo

rin

flatio

n;co

inte

grat

ing

rela

tions

hips

.L

og (M

3d/C

PI)

chan

ges

inse

ason

al

whe

re M

3d is

term

s of

du

mm

ies

divi

sia

M3

trade

Subramanian S. Sriram

346

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Fiel

ding

(199

4)19

75:2

-198

9:2

ln (B

M/C

PI)

ln (r

eal G

DP

ln (1

+T-b

illln

(1+π

);D

F;I(

0) fo

rJJ

(199

0)C

how

Yes

Thre

e co

inte

grat

ing

rela

tions

hips

Qua

rterly

adju

sted

for

rate

)ln

(1+D

EPR

)H

ylle

berg

ln (1

+DE

PR);

[for

EC

M]

amon

g re

al m

oney

, rea

l GD

P,te

rms

of

usin

g pa

ralle

lan

d ot

hers

I(1)

for

infla

tion,

inte

rest

rate

, mav

arr,

trade

)m

arke

t XR

;(1

990)

othe

rsan

d m

avar

π. T

he E

C te

rm is

mav

arπ;

ca

lcul

ated

bas

ed o

n th

e re

sidu

als

mav

arr;

from

the

first

two

coin

tegr

atin

gqu

arte

rly d

umm

yve

ctor

s. S

-Tel

astic

ities

are

varia

bles

8sm

alle

r tha

n th

ose

of lo

ng ru

n.

Kor

eaA

rize

(199

4)19

73:1

-199

0:1

ln (M

1/C

PI);

ln (r

eal G

DP)

CB

R;

Exp

ecte

d ra

teA

DF;

I(1)

EY

(198

7);

Cho

wY

esTw

o to

thre

e co

inte

grat

ing

Qua

rterly

ln (M

2/C

PI)

inte

rest

rate

of in

flatio

n;

Hyl

lebe

rgJ

(198

8);

vect

ors

amon

g re

al m

oney

(bot

hon

loan

s an

dE

ER

; sta

ndar

dan

d ot

hers

JJ (1

990)

M1

and

M2)

, rea

l inc

ome,

T

D o

n N

CB

;de

viat

ion

of(1

990)

;in

tere

st ra

te, a

nd fo

reig

nw

eigh

ed a

vg.

the

chan

ge in

Osb

orn

exch

ange

rate

risk

and

retu

rn.

of S

-Tin

tere

stth

e lo

g of

the

(199

0);

Wel

l-spe

cifie

d E

CM

.ra

tes

in 9

EE

R; d

umm

yH

asza

and

indu

stria

lva

riabl

e to

Fulle

rco

untri

es;

mea

sure

the

(198

2);

unco

vere

dch

ange

inPe

rron

inte

rest

rate

circ

umst

ance

s(1

988)

diff

eren

tial i

nfa

vor o

f fo

reig

nco

untry

Leba

non

Eke

n an

d ot

hers

1964

-93

Log

(B/C

PI);

Log

(rea

l...

Log

(CPI

);PP

(198

8)I(

1)E

G (1

987)

;...

...C

oint

egra

ting

rela

tions

hip

exits

(199

5)A

nnua

lL

og (M

1/C

PI);

GD

P); L

ogL

og (U

.S. C

PI);

PO (1

990)

betw

een

vario

us d

efin

ition

s of

Log

FC

D$;

10(U

.S. d

olla

r-ex

pect

edm

oney

and

with

real

GD

P,

Log

(M2L

Lde

nom

inat

edin

flatio

n; w

arpr

ices

, and

dom

estic

infla

tion.

/CPI

);10

GD

P)ye

ar d

umm

y

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

347

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Mal

aysi

aSr

iram

(199

9a)

1973

:8-

ln (M

2/C

PI)

ln (I

IP)

CB

TD

3M;

Exp

ecte

d D

F;ln

(IIP

) and

J (1

988)

;C

how

Yes

Coi

nteg

ratio

n re

latio

nshi

p ex

ists

1995

:12

disc

ount

rate

in

flatio

n;A

DF

expe

cted

JJ (1

990)

[Gen

eral

betw

een

real

M2

and

its

Mon

thly

on 3

-mon

thno

min

al X

R;

infla

tion

to s

peci

ficde

term

inan

ts u

nder

bot

h th

eT-

bills

seas

onal

and

are

I(0)

;A

ppro

ach]

clos

ed- a

nd o

pen-

econ

omy

stru

ctur

alot

hers

are

fram

ewor

k; fa

irly

stab

le E

CM

sdu

mm

ies

I(1)

unde

r bot

h si

tuat

ions

.

Mex

ico

Kha

mis

and

1983

:1-

ln (C

C/C

PI)

ln (r

eal p

rivat

e60

-day

TD

RIn

flatio

nA

DF

I (1)

J (1

988)

;C

how

Yes

Coi

nteg

ratio

n re

latio

nshi

p am

ong

Leo

ne (1

999)

1997

:6co

nsum

ptio

nJJ

(199

0)re

al C

C, s

cale

var

iabl

e, a

nd

Mon

thly

expe

nditu

re)

60-d

ay T

DR

; sta

ble

EC

M.

Mor

occo

Hof

fman

and

19

59:1

-198

8:2

Log

(M1)

;L

og (G

DP/

Swis

s S-

TL

og (C

PI);

AD

F;I(

1) p

ossi

bly

J (1

988)

;H

anse

n an

dN

oSi

ngle

coi

nteg

ratin

g ve

ctor

Ta

hiri

(199

4)Q

uarte

rlyL

og (M

2)C

PI);

inte

rest

rate

;se

ason

alK

PSS

abou

t a

J (1

991b

);Jo

hans

en

amon

g m

easu

res

of n

omin

alL

og (G

NP/

inte

rest

rate

dum

mie

s(1

992)

dete

rmin

istic

JJ (1

990)

;(1

993)

mon

ey, p

rices

, rea

l inc

ome,

and

CPI

)on

TD

trend

; KPS

SO

LS;

Swis

s S-

Tin

tere

st ra

te.

test

fails

toD

OL

Sre

ject

the

null

of s

tatio

nary

for S

wis

s S-

Tin

tere

st ra

tead

just

ed fo

r TD

R

Nig

eria

Fiel

ding

(199

4)19

76:1

-198

9:2

ln (B

M/C

PI)

ln (r

eal G

DP

ln (1

+T-b

illln

(1+π

);D

F;I(

0) fo

rJJ

(199

0)C

how

Yes

One

coi

nteg

ratin

g re

latio

nshi

pQ

uarte

rlyad

just

ed fo

rra

te)

ln (1

+DE

PR)

Hyl

lebe

rgln

(1+D

EPR

);[f

or E

CM

]am

ong

real

mon

ey, r

eal G

DP,

term

s of

us

ing

para

llel

and

othe

rsI(

1) fo

rin

flatio

n, in

tere

st ra

te a

ndtra

de)

mar

ket X

R;

(199

0)ot

hers

mav

arπ.

mav

arπ;

8

seas

onal

dum

mie

s

Subramanian S. Sriram

348

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Terib

a (1

997)

1960

-94

Log

(CO

B);

Log

(rea

l DA

)L

og (i

nter

est

Log

(DA

D);

DF

I(1)

exc

ept

EG

;...

Yes

Coi

nteg

ratio

n re

latio

nshi

p ex

ists

Ann

ual

Log

(M1)

;ra

te fo

r 12-

Log

(LT

BR

info

r Log

M1

AE

Gam

ong

the

mon

etar

y ag

greg

ates

,19

62:1

-199

5:2

Log

(M2)

mon

th T

D);

Nig

eria

/LT

BR

(I(2

)) a

ndD

A, D

AD

, and

inte

rest

rate

s.fo

r M1;

and

Log

(int

eres

tin

the

Uni

ted

for p

aral

lel

Fore

ign

oppo

rtuni

ty c

ost v

aria

ble

1962

:1-1

992:

4ra

te fo

r 3-

Stat

es)

mar

ket X

Rha

s in

fluen

ce o

n M

1 eq

uatio

n fo

r M2

mon

th T

D)

(I(0

))on

ly.

Qua

rterly

Pak

ista

nA

rize

(199

4)19

73:1

-199

0:1

ln (M

1/C

PI);

ln (r

eal G

DP)

CM

R; G

ovt.

Exp

ecte

d ra

teA

DF;

I(1)

EY

(198

7);

Cho

wY

esTw

o to

thre

e co

inte

grat

ing

Qua

rterly

ln (M

2/C

PI)

[WPI

-bas

ed]

bond

yie

ld;

of in

flatio

n;

Hyl

lebe

rgJ

(198

8);

vect

ors

exis

t am

ong

real

mon

eyw

eigh

ted

avg.

EE

R; s

tand

ard

and

othe

rsJJ

(199

0)(b

oth

M1

and

M2)

, rea

l GD

P,of

S-T

inte

rest

devi

atio

n of

(199

0);

inte

rest

rate

, and

fore

ign

rate

s in

9th

e ch

ange

inO

sbor

nex

chan

ge ra

te ri

sk a

nd re

turn

.in

dust

rial

the

log

of th

e(1

990)

;W

ell-s

peci

fied

EC

M.

coun

tries

;E

ER

; dum

my

Has

za a

ndun

cove

red

varia

ble

toFu

ller

inte

rest

rate

mea

sure

the

(198

2);

diff

eren

tial

chan

ge in

Perr

on

in fa

vor o

fci

rcum

stan

ces

(198

8)fo

reig

nco

untry

Hos

sain

(199

4)19

51-9

1L

og (M

1/C

PI);

ln (r

eal G

DP)

ln (y

ield

on

Exp

ecte

dD

F;E

xpec

ted

EG

;...

No

EG, A

EG, a

nd C

RD

Wte

sts sh

ow19

72-9

1L

og (M

2/C

PI)

Gov

t. bo

nds)

;in

flatio

nA

DF

infla

tion

isA

EG

;co

nflic

ting

resu

lts. B

ut J

J (1

990)

Ann

ual

ln (m

arke

t I(

0); o

ther

sC

RD

W;

test

find

s 2

coin

tegr

atin

gve

ctor

sca

ll ra

te o

fI(

1)J

(198

8);

amon

g m

oney

, rea

l GD

P, a

nd

inte

rest

)JJ

(199

0)ca

ll ra

te o

f int

eres

t for

197

2-91

and

one

for 1

953-

91. M

1 is

fo

und

to b

e m

ore

stab

le th

an M

2.

A SURVEY OF RECENT EMPIRICAL MONEY DEMAND STUDIES

349

Tab

le 1

.(c

on

tinu

ed

)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Sing

apor

eA

rize

(199

4)19

73:1

-199

0:1

ln (M

1/C

PI);

ln (r

eal G

DP)

CM

R; 3

-E

xpec

ted

rate

AD

F;I(

1) e

xcep

tE

Y(1

987)

;C

how

Yes

2-3

coin

tegr

atin

g ve

ctor

s am

ong

Qua

rterly

ln (M

2/C

PI)

[WPI

-bas

ed]

mon

th F

DR

;of

infla

tion;

H

ylle

berg

for e

xpec

ted

J (1

988)

;re

al m

oney

(bot

h M

1 an

d M

2),

wei

ghed

avg

.E

ER

; sta

ndar

dan

d ot

hers

rate

of

JJ (1

990)

real

GD

P, in

tere

st ra

te, a

ndof

S-T

inte

rest

devi

atio

n of

(199

0);

infla

tion

fore

ign

exch

ange

rate

risk

and

rate

s in

9th

e ch

ange

inO

sbor

nw

hich

isre

turn

. Wel

l-spe

cifie

d E

CM

.in

dust

rial

the

log

of th

e(1

990)

;I(

0)co

untri

es;

EE

R; d

umm

yH

asza

and

unco

vere

dva

riabl

e to

Fulle

rin

tere

st ra

tem

easu

re th

e(1

982)

;di

ffer

entia

l in

chan

ge in

Perr

onfa

vor o

f ci

rcum

stan

ces

(198

8)fo

reig

nco

untry

Dek

le a

nd19

75-9

5L

og (N

M);

Log

(rea

l GD

P)T

DR

[for

Log

(CPI

);A

DF

I(1)

J (1

988)

;...

No

Coi

nteg

ratin

g re

latio

nshi

ps fo

rPr

adha

n (1

997)

Ann

ual

Log

(BM

);N

M];

MM

R-

expe

cted

JJ

(199

0)no

min

al N

M a

nd B

M.

Log

(rea

l NM

);T

DR

wei

ghte

dde

prec

iatio

nL

og (r

eal B

M)

by th

e sh

are

rate

QM

in B

M;

LIB

OR

Thai

land

Dek

le a

nd19

78-9

5L

og (N

M);

Log

(rea

l GD

P)T

DR

[for

Log

(CPI

)A

DF

I(1)

J (1

988)

;...

No

Coi

nteg

ratin

g re

latio

nshi

p fo

rPr

adha

n (1

997)

Ann

ual

Log

(BM

);N

M];

MM

R-

JJ (1

990)

nom

inal

NM

onl

y.L

og (r

eal N

M);

TD

R w

eigh

ted

Log

(rea

l BM

)by

the

shar

eof

QM

in B

M;

Subramanian S. Sriram

350

Tab

le 1

.(c

on

clu

de

d)

Det

erm

inan

tsE

rror

-Sa

mpl

eU

nit

Ord

erC

oint

egra

tion

Cor

rect

ion

Cou

ntry

/Pe

riod/

Mon

etar

ySc

ale

Inte

rest

Roo

tof

Tech

niqu

e(s)

/St

abili

tyM

odel

Aut

hor(

s)Fr

eque

ncy

Agg

rega

te(s

)va

riabl

e(s)

rate

(s)

Oth

er(s

)Te

st(s

)In

tegr

atio

nTe

st(s

)Te

st(s

)(E

CM

)Fi

ndin

gs

Tuni

sia

Trei

chel

(199

7)19

63-9

5ln

(M2/

CPI

);ln

(rea

l GD

P)M

onth

ly y

ield

Infla

tion

rate

;A

DF

I(1)

exc

ept

AE

G;

Rec

ursi

veY

esSt

able

long

-term

rela

tions

hip

Ann

ual

ln (M

4/C

PI)

on T

-bill

;se

ason

al

for i

nfla

tion

J (1

988)

;C

how

amon

g re

al m

oney

, rea

l GD

P,19

90-9

5re

disc

ount

dum

mie

sra

te w

hich

isJJ

(199

0)[f

or E

CM

]an

d th

e m

onth

ly y

ield

on

T-bi

ll.M

onth

lyra

te; M

MR

I(0)

Stab

le E

CM

.

Not

e: T

he fo

llow

ing

abbr

evia

tions

are

use

d:

Mon

etar

y ag

greg

ates

: B =

bas

e m

oney

; BM

= b

road

mon

ey; C

HP

= cu

rren

cy h

eld

by p

ublic

; CC

= c

urre

ncy

in c

ircul

atio

n; C

OB

= c

urre

ncy

outs

ide

bank

s; D

D =

dem

and

depo

sits

;N

M =

nar

row

mon

ey; Q

M =

qua

si-m

oney

; SD

= s

avin

gs d

epos

its; a

nd T

D =

tim

e de

posi

ts.

Scal

e va

riab

le: D

A=

dom

estic

abs

orpt

ion;

GD

E =

gro

ss d

omes

tic e

xpen

ditu

re; G

DP

= gr

oss

dom

estic

pro

duct

; GN

P=

gros

s na

tiona

l pro

duct

; IIP

= in

dex

of in

dust

rial p

rodu

ctio

n; IO

= in

dust

rial o

utpu

t;N

I = n

atio

nal i

ncom

e; a

nd N

NI =

net

nat

iona

l inc

ome.

Inte

rest

rat

e: C

MR

= c

all m

oney

rate

; CB

DR

= C

entra

l Ban

k di

scou

nt ra

te; C

PR =

com

mer

cial

pap

er ra

te; C

BR

= c

orpo

rate

bon

d ra

te;

FDR

= fi

xed

depo

sit r

ate;

LIB

OR

= L

ondo

n in

terb

ank

offe

red

rate

; LT

BR

= L

ong-

term

bor

row

ing

rate

; MM

R =

mon

ey m

arke

t rat

e; C

BT

D3M

= T

hree

-mon

th d

epos

it ra

tes

at c

omm

erci

al b

anks

; TD

R =

tim

e de

posi

t rat

e; T

-bill

= T

reas

ury

bill;

an

d T-

bond

= T

reas

ury

bond

.E

xcha

nge

rate

: DE

PR =

dep

reci

atio

n; X

R =

exc

hang

e ra

te; E

ER

= e

ffec

tive

exch

ange

rate

; and

NE

ER

= n

omin

al e

ffec

tive

exch

ange

rate

.Pr

ices

: CPI

= c

onsu

mer

pric

e in

dex;

RPI

= re

tail

pric

e in

dex;

and

WPI

= w

hole

sale

pric

e in

dex.

Def

lato

rs: D

AD

= d

omes

tic a

bsor

ptio

n de

flato

r; G

DE

D =

gro

ss d

omes

tic e

xpen

ditu

re d

efla

tor;

GD

PD =

gro

ss d

omes

tic p

rodu

ct d

efla

tor;

GN

PD =

gro

ss n

atio

nal p

rodu

ct d

efla

tor;

IGD

PD =

impl

icit

GD

Pde

flato

r; IG

NPD

= im

plic

it G

NP

defla

tor;

IPD

= im

plic

it pr

ice

defla

tor;

and

NID

= n

atio

nal i

ncom

e de

flato

r.U

nit r

oot t

ests

: AD

F =

augm

ente

d D

icke

y-Fu

ller;

CR

DW

= co

inte

grat

ion

regr

essi

on D

urbi

n-W

atso

n; D

F =

Dic

key-

Fulle

r; J

(198

8) =

Joh

anse

n (1

988)

; KPS

S =

Kw

iatk

owsk

i, Ph

illip

s, S

chm

idt,

and

Shin

(199

2);

P(1

987)

= P

hilli

ps (1

987)

; PO

(199

0) =

Phi

llips

and

Oul

iaris

(199

0); a

nd P

P(1