Embed Size (px)

Citation preview

"A Theory of Financing Constraints and FirmDynamics"

G.L. Clementi and H.A. Hopenhayn (QJE, 2006)

Cesar E. TamayoEcon612- Economics - Rutgers

April 30, 2012

1/21

Program

I SummaryI Physical environmentI The contract design problemI Characterization of the optimal contractI Firm growth and survivalI Contract maturity and debt limits

2/21

What they do in a nutshell

I The paper develops a theory of endogenous �nancing constraints.

I Repeated moral hazard problemI The optimal contract (under asymmetric info) determines non-trivialstochastic processes for �rm size, equity and debt.

I This in turn implies non-trivial �rm dynamics even under simple i.i.d.shocks.

3/21

What they do in a nutshell

I The paper develops a theory of endogenous �nancing constraints.I Repeated moral hazard problem

I The optimal contract (under asymmetric info) determines non-trivialstochastic processes for �rm size, equity and debt.

I This in turn implies non-trivial �rm dynamics even under simple i.i.d.shocks.

3/21

What they do in a nutshell

I The paper develops a theory of endogenous �nancing constraints.I Repeated moral hazard problemI The optimal contract (under asymmetric info) determines non-trivialstochastic processes for �rm size, equity and debt.

I This in turn implies non-trivial �rm dynamics even under simple i.i.d.shocks.

3/21

What they do in a nutshell

I The paper develops a theory of endogenous �nancing constraints.I Repeated moral hazard problemI The optimal contract (under asymmetric info) determines non-trivialstochastic processes for �rm size, equity and debt.

I This in turn implies non-trivial �rm dynamics even under simple i.i.d.shocks.

3/21

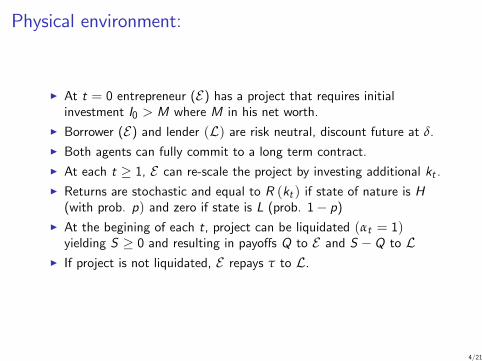

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.

I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .

I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

Physical environment:

I At t = 0 entrepreneur (E) has a project that requires initialinvestment I0 > M where M in his net worth.

I Borrower (E) and lender (L) are risk neutral, discount future at δ.

I Both agents can fully commit to a long term contract.I At each t � 1, E can re-scale the project by investing additional kt .I Returns are stochastic and equal to R (kt ) if state of nature is H(with prob. p) and zero if state is L (prob. 1� p)

I At the begining of each t, project can be liquidated (αt = 1)yielding S � 0 and resulting in payo¤s Q to E and S �Q to L

I If project is not liquidated, E repays τ to L.

4/21

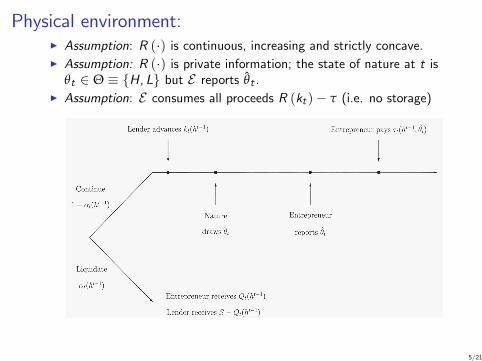

Physical environment:I Assumption: R (�) is continuous, increasing and strictly concave.

I Assumption: R (�) is private information; the state of nature at t isθt 2 Θ � fH, Lg but E reports θt .

I Assumption: E consumes all proceeds R (kt )� τ (i.e. no storage)

5/21

Physical environment:I Assumption: R (�) is continuous, increasing and strictly concave.I Assumption: R (�) is private information; the state of nature at t is

θt 2 Θ � fH, Lg but E reports θt .

I Assumption: E consumes all proceeds R (kt )� τ (i.e. no storage)

5/21

Physical environment:I Assumption: R (�) is continuous, increasing and strictly concave.I Assumption: R (�) is private information; the state of nature at t is

θt 2 Θ � fH, Lg but E reports θt .I Assumption: E consumes all proceeds R (kt )� τ (i.e. no storage)

5/21

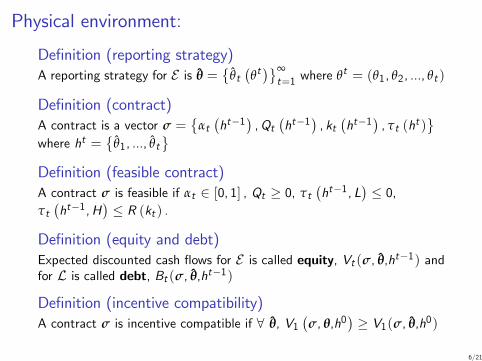

Physical environment:

De�nition (reporting strategy)A reporting strategy for E is θ =

�θt�θt�∞t=1 where θt = (θ1, θ2, ..., θt )

De�nition (contract)A contract is a vector σ =

�αt�ht�1

�,Qt

�ht�1

�, kt

�ht�1

�, τt (ht )

where ht =

�θ1, ..., θt

De�nition (feasible contract)A contract σ is feasible if αt 2 [0, 1] , Qt � 0, τt

�ht�1, L

�� 0,

τt�ht�1,H

�� R (kt ) .

De�nition (equity and debt)Expected discounted cash �ows for E is called equity, Vt (σ, θ,ht�1) andfor L is called debt, Bt (σ, θ,ht�1)

De�nition (incentive compatibility)A contract σ is incentive compatible if 8 θ, V1

�σ, θ,h0

�� V1(σ, θ,h0)

6/21

Physical environment:

De�nition (reporting strategy)A reporting strategy for E is θ =

�θt�θt�∞t=1 where θt = (θ1, θ2, ..., θt )

De�nition (contract)A contract is a vector σ =

�αt�ht�1

�,Qt

�ht�1

�, kt

�ht�1

�, τt (ht )

where ht =

�θ1, ..., θt

De�nition (feasible contract)A contract σ is feasible if αt 2 [0, 1] , Qt � 0, τt

�ht�1, L

�� 0,

τt�ht�1,H

�� R (kt ) .

De�nition (equity and debt)Expected discounted cash �ows for E is called equity, Vt (σ, θ,ht�1) andfor L is called debt, Bt (σ, θ,ht�1)

De�nition (incentive compatibility)A contract σ is incentive compatible if 8 θ, V1

�σ, θ,h0

�� V1(σ, θ,h0)

6/21

Physical environment:

De�nition (reporting strategy)A reporting strategy for E is θ =

�θt�θt�∞t=1 where θt = (θ1, θ2, ..., θt )

De�nition (contract)A contract is a vector σ =

�αt�ht�1

�,Qt

�ht�1

�, kt

�ht�1

�, τt (ht )

where ht =

�θ1, ..., θt

De�nition (feasible contract)A contract σ is feasible if αt 2 [0, 1] , Qt � 0, τt

�ht�1, L

�� 0,

τt�ht�1,H

�� R (kt ) .

De�nition (equity and debt)Expected discounted cash �ows for E is called equity, Vt (σ, θ,ht�1) andfor L is called debt, Bt (σ, θ,ht�1)

De�nition (incentive compatibility)A contract σ is incentive compatible if 8 θ, V1

�σ, θ,h0

�� V1(σ, θ,h0)

6/21

Physical environment:

De�nition (reporting strategy)A reporting strategy for E is θ =

�θt�θt�∞t=1 where θt = (θ1, θ2, ..., θt )

De�nition (contract)A contract is a vector σ =

�αt�ht�1

�,Qt

�ht�1

�, kt

�ht�1

�, τt (ht )

where ht =

�θ1, ..., θt

De�nition (feasible contract)A contract σ is feasible if αt 2 [0, 1] , Qt � 0, τt

�ht�1, L

�� 0,

τt�ht�1,H

�� R (kt ) .

De�nition (equity and debt)Expected discounted cash �ows for E is called equity, Vt (σ, θ,ht�1) andfor L is called debt, Bt (σ, θ,ht�1)

De�nition (incentive compatibility)A contract σ is incentive compatible if 8 θ, V1

�σ, θ,h0

�� V1(σ, θ,h0)

6/21

Physical environment:

De�nition (reporting strategy)A reporting strategy for E is θ =

�θt�θt�∞t=1 where θt = (θ1, θ2, ..., θt )

De�nition (contract)A contract is a vector σ =

�αt�ht�1

�,Qt

�ht�1

�, kt

�ht�1

�, τt (ht )

where ht =

�θ1, ..., θt

De�nition (feasible contract)A contract σ is feasible if αt 2 [0, 1] , Qt � 0, τt

�ht�1, L

�� 0,

τt�ht�1,H

�� R (kt ) .

De�nition (equity and debt)Expected discounted cash �ows for E is called equity, Vt (σ, θ,ht�1) andfor L is called debt, Bt (σ, θ,ht�1)

De�nition (incentive compatibility)A contract σ is incentive compatible if 8 θ, V1

�σ, θ,h0

�� V1(σ, θ,h0)

6/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).

I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

The �rst-best (symmetric info)

I Since both are risk neutral and share δ, the optimal contractmaximizes total exp. discounted pro�ts of the match (E ,L).

I In equilibrium L provides E with the unconst. e¤cient k in every t:

maxk[pR (k)� k ] (1)

I So that R (�) strictly concave) 9 unique k� � 0 that solves (1).I Assume k� > 0 so that per-period total surplus is:

π� = maxk[pR (k)� k ] = pR (k�)� k�

I And PDV of total surplus is W � = π�1�δ > S by assumption.

I Project is undertaken if W � > I0 and once project is started, �rmdoes not grow, shrink or exit.

7/21

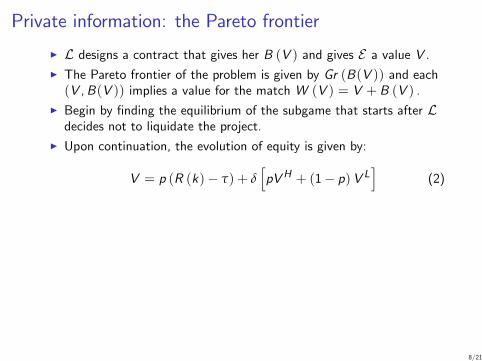

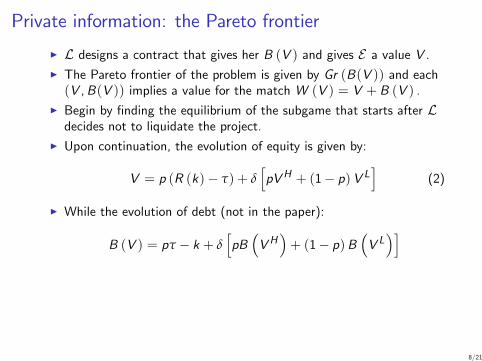

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .

I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

Private information: the Pareto frontier

I L designs a contract that gives her B (V ) and gives E a value V .I The Pareto frontier of the problem is given by Gr (B(V )) and each(V ,B(V )) implies a value for the match W (V ) = V + B (V ) .

I Begin by �nding the equilibrium of the subgame that starts after Ldecides not to liquidate the project.

I Upon continuation, the evolution of equity is given by:

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(2)

I While the evolution of debt (not in the paper):

B (V ) = pτ � k + δhpB�VH

�+ (1� p)B

�V L�i

I The value of equity e¤ectively summarizes all the informationprovided by the history itself (Spear and Srivastava, 1987; Green,1987) so it�s the appropriate state variable in a recursive formulationof the repeated contracting problem.

8/21

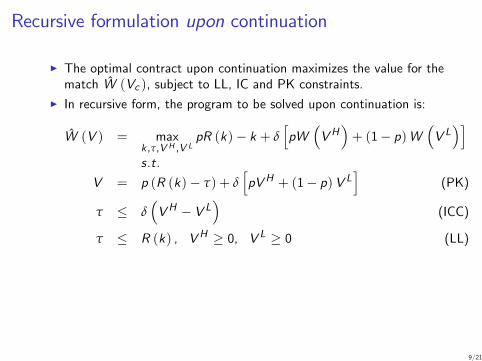

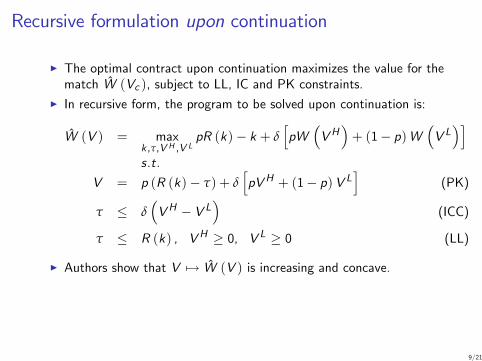

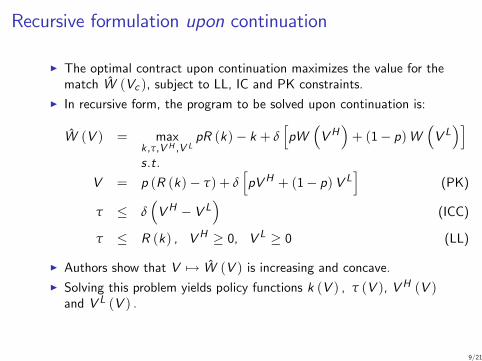

Recursive formulation upon continuation

I The optimal contract upon continuation maximizes the value for thematch W (Vc ), subject to LL, IC and PK constraints.

I In recursive form, the program to be solved upon continuation is:

W (V ) = maxk ,τ,V H ,V L

pR (k)� k + δhpW

�VH

�+ (1� p)W

�V L�i

s.t.

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(PK)

τ � δ�VH � V L

�(ICC)

τ � R (k) , VH � 0, V L � 0 (LL)

I Authors show that V 7! W (V ) is increasing and concave.I Solving this problem yields policy functions k (V ) , τ (V ), VH (V )and V L (V ) .

9/21

Recursive formulation upon continuation

I The optimal contract upon continuation maximizes the value for thematch W (Vc ), subject to LL, IC and PK constraints.

I In recursive form, the program to be solved upon continuation is:

W (V ) = maxk ,τ,V H ,V L

pR (k)� k + δhpW

�VH

�+ (1� p)W

�V L�i

s.t.

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(PK)

τ � δ�VH � V L

�(ICC)

τ � R (k) , VH � 0, V L � 0 (LL)

I Authors show that V 7! W (V ) is increasing and concave.I Solving this problem yields policy functions k (V ) , τ (V ), VH (V )and V L (V ) .

9/21

Recursive formulation upon continuation

I The optimal contract upon continuation maximizes the value for thematch W (Vc ), subject to LL, IC and PK constraints.

I In recursive form, the program to be solved upon continuation is:

W (V ) = maxk ,τ,V H ,V L

pR (k)� k + δhpW

�VH

�+ (1� p)W

�V L�i

s.t.

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(PK)

τ � δ�VH � V L

�(ICC)

τ � R (k) , VH � 0, V L � 0 (LL)

I Authors show that V 7! W (V ) is increasing and concave.

I Solving this problem yields policy functions k (V ) , τ (V ), VH (V )and V L (V ) .

9/21

Recursive formulation upon continuation

I The optimal contract upon continuation maximizes the value for thematch W (Vc ), subject to LL, IC and PK constraints.

I In recursive form, the program to be solved upon continuation is:

W (V ) = maxk ,τ,V H ,V L

pR (k)� k + δhpW

�VH

�+ (1� p)W

�V L�i

s.t.

V = p (R (k)� τ) + δhpVH + (1� p)V L

i(PK)

τ � δ�VH � V L

�(ICC)

τ � R (k) , VH � 0, V L � 0 (LL)

I Authors show that V 7! W (V ) is increasing and concave.I Solving this problem yields policy functions k (V ) , τ (V ), VH (V )and V L (V ) .

9/21

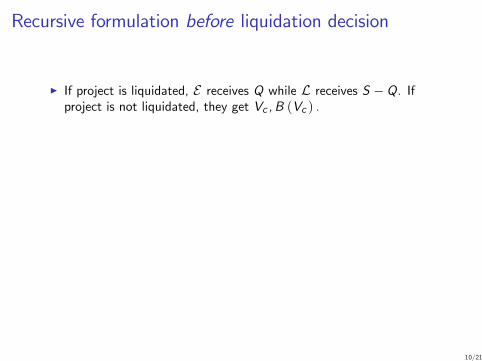

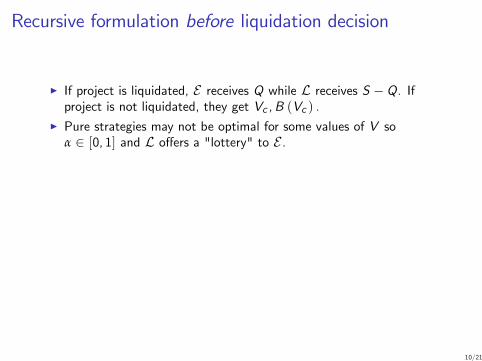

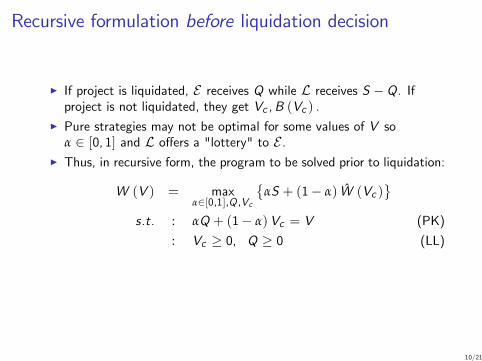

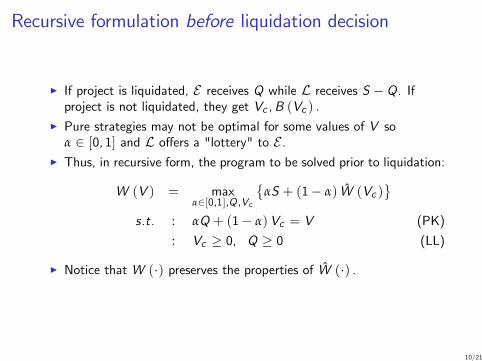

Recursive formulation before liquidation decision

I If project is liquidated, E receives Q while L receives S �Q. Ifproject is not liquidated, they get Vc ,B (Vc ) .

I Pure strategies may not be optimal for some values of V soα 2 [0, 1] and L o¤ers a "lottery" to E .

I Thus, in recursive form, the program to be solved prior to liquidation:

W (V ) = maxα2[0,1],Q ,Vc

�αS + (1� α) W (Vc )

s.t. : αQ + (1� α)Vc = V (PK)

: Vc � 0, Q � 0 (LL)

I Notice that W (�) preserves the properties of W (�) .

10/21

Recursive formulation before liquidation decision

I If project is liquidated, E receives Q while L receives S �Q. Ifproject is not liquidated, they get Vc ,B (Vc ) .

I Pure strategies may not be optimal for some values of V soα 2 [0, 1] and L o¤ers a "lottery" to E .

I Thus, in recursive form, the program to be solved prior to liquidation:

W (V ) = maxα2[0,1],Q ,Vc

�αS + (1� α) W (Vc )

s.t. : αQ + (1� α)Vc = V (PK)

: Vc � 0, Q � 0 (LL)

I Notice that W (�) preserves the properties of W (�) .

10/21

Recursive formulation before liquidation decision

I If project is liquidated, E receives Q while L receives S �Q. Ifproject is not liquidated, they get Vc ,B (Vc ) .

I Pure strategies may not be optimal for some values of V soα 2 [0, 1] and L o¤ers a "lottery" to E .

I Thus, in recursive form, the program to be solved prior to liquidation:

W (V ) = maxα2[0,1],Q ,Vc

�αS + (1� α) W (Vc )

s.t. : αQ + (1� α)Vc = V (PK)

: Vc � 0, Q � 0 (LL)

I Notice that W (�) preserves the properties of W (�) .

10/21

Recursive formulation before liquidation decision

I If project is liquidated, E receives Q while L receives S �Q. Ifproject is not liquidated, they get Vc ,B (Vc ) .

I Pure strategies may not be optimal for some values of V soα 2 [0, 1] and L o¤ers a "lottery" to E .

I Thus, in recursive form, the program to be solved prior to liquidation:

W (V ) = maxα2[0,1],Q ,Vc

�αS + (1� α) W (Vc )

s.t. : αQ + (1� α)Vc = V (PK)

: Vc � 0, Q � 0 (LL)

I Notice that W (�) preserves the properties of W (�) .

10/21

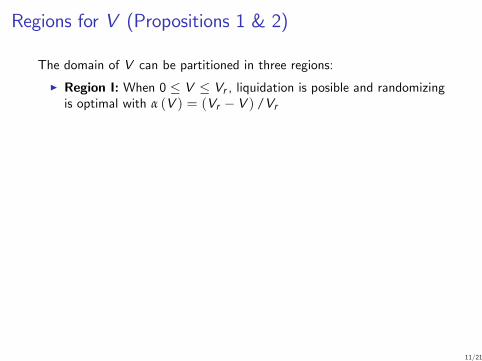

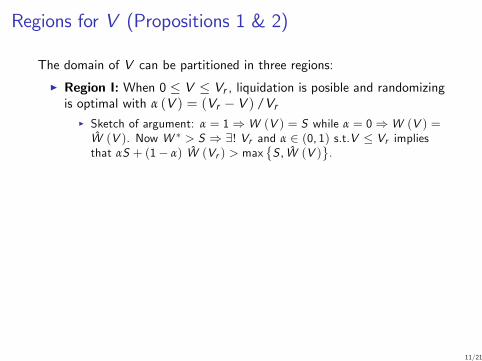

Regions for V (Propositions 1 & 2)

The domain of V can be partitioned in three regions:

I Region I: When 0 � V � Vr , liquidation is posible and randomizingis optimal with α (V ) = (Vr � V ) /Vr

I Sketch of argument: α = 1) W (V ) = S while α = 0) W (V ) =W (V ). Now W � > S ) 9! Vr and α 2 (0, 1) s.t.V � Vr impliesthat αS + (1� α) W (Vr ) > max

�S , W (V )

.

I Intuition: As V ! Vr expected value W (V ) rises above S and Lliquidates with low probability (draw graph).

I Region III: When V � V � = pR (k�) / (1� δ) the total surplus isthe same as under symmetric information (�rst-best), i.e.,W (V �) = W �.

I Intuition: equivalent to E having a balance of k�/(1� δ) in thebank at interest rate (1� δ) /δ that is exactly enough to �nance theproject at its optimum scale. Then L advances k� and collects τ = 0every period.

11/21

Regions for V (Propositions 1 & 2)

The domain of V can be partitioned in three regions:

I Region I: When 0 � V � Vr , liquidation is posible and randomizingis optimal with α (V ) = (Vr � V ) /Vr

I Sketch of argument: α = 1) W (V ) = S while α = 0) W (V ) =W (V ). Now W � > S ) 9! Vr and α 2 (0, 1) s.t.V � Vr impliesthat αS + (1� α) W (Vr ) > max

�S , W (V )

.

I Intuition: As V ! Vr expected value W (V ) rises above S and Lliquidates with low probability (draw graph).

I Region III: When V � V � = pR (k�) / (1� δ) the total surplus isthe same as under symmetric information (�rst-best), i.e.,W (V �) = W �.

I Intuition: equivalent to E having a balance of k�/(1� δ) in thebank at interest rate (1� δ) /δ that is exactly enough to �nance theproject at its optimum scale. Then L advances k� and collects τ = 0every period.

11/21

Regions for V (Propositions 1 & 2)

The domain of V can be partitioned in three regions:

I Region I: When 0 � V � Vr , liquidation is posible and randomizingis optimal with α (V ) = (Vr � V ) /Vr

I Sketch of argument: α = 1) W (V ) = S while α = 0) W (V ) =W (V ). Now W � > S ) 9! Vr and α 2 (0, 1) s.t.V � Vr impliesthat αS + (1� α) W (Vr ) > max

�S , W (V )

.

I Intuition: As V ! Vr expected value W (V ) rises above S and Lliquidates with low probability (draw graph).

I Region III: When V � V � = pR (k�) / (1� δ) the total surplus isthe same as under symmetric information (�rst-best), i.e.,W (V �) = W �.

I Intuition: equivalent to E having a balance of k�/(1� δ) in thebank at interest rate (1� δ) /δ that is exactly enough to �nance theproject at its optimum scale. Then L advances k� and collects τ = 0every period.

11/21

Regions for V (Propositions 1 & 2)

The domain of V can be partitioned in three regions:

I Region I: When 0 � V � Vr , liquidation is posible and randomizingis optimal with α (V ) = (Vr � V ) /Vr

I Sketch of argument: α = 1) W (V ) = S while α = 0) W (V ) =W (V ). Now W � > S ) 9! Vr and α 2 (0, 1) s.t.V � Vr impliesthat αS + (1� α) W (Vr ) > max

�S , W (V )

.

I Intuition: As V ! Vr expected value W (V ) rises above S and Lliquidates with low probability (draw graph).

I Region III: When V � V � = pR (k�) / (1� δ) the total surplus isthe same as under symmetric information (�rst-best), i.e.,W (V �) = W �.

I Intuition: equivalent to E having a balance of k�/(1� δ) in thebank at interest rate (1� δ) /δ that is exactly enough to �nance theproject at its optimum scale. Then L advances k� and collects τ = 0every period.

11/21

Regions for V (Propositions 1 & 2)

The domain of V can be partitioned in three regions:

I Region I: When 0 � V � Vr , liquidation is posible and randomizingis optimal with α (V ) = (Vr � V ) /Vr

I Sketch of argument: α = 1) W (V ) = S while α = 0) W (V ) =W (V ). Now W � > S ) 9! Vr and α 2 (0, 1) s.t.V � Vr impliesthat αS + (1� α) W (Vr ) > max

�S , W (V )

.

I Intuition: As V ! Vr expected value W (V ) rises above S and Lliquidates with low probability (draw graph).

I Region III: When V � V � = pR (k�) / (1� δ) the total surplus isthe same as under symmetric information (�rst-best), i.e.,W (V �) = W �.

I Intuition: equivalent to E having a balance of k�/(1� δ) in thebank at interest rate (1� δ) /δ that is exactly enough to �nance theproject at its optimum scale. Then L advances k� and collects τ = 0every period.

11/21

The borrowing constraint region (Propositions 1 & 2 cont.)

I Region II: When Vr � V < V �:

(a) There is no liquidation in current period and V 7! W (V ) is strictlyincreasing and,

(b) The optimal capital advancement policy is single-valued and s.t.k (V ) < k� (the �rms is debt-constrained)

I Sketch of argument: suppose that the optimal repayment policy forregion II was τ = R (k) implying that the ICC binds (see below theproofs for both of these results). Then:

R (k) = δ(VH � V L)

which implies that increasing k is only incentive compatible ifVH � V L also increases. But W (V ) concave implies that doing sois costly! (draw graph)

12/21

The borrowing constraint region (Propositions 1 & 2 cont.)

I Region II: When Vr � V < V �:(a) There is no liquidation in current period and V 7! W (V ) is strictly

increasing and,

(b) The optimal capital advancement policy is single-valued and s.t.k (V ) < k� (the �rms is debt-constrained)

I Sketch of argument: suppose that the optimal repayment policy forregion II was τ = R (k) implying that the ICC binds (see below theproofs for both of these results). Then:

R (k) = δ(VH � V L)

which implies that increasing k is only incentive compatible ifVH � V L also increases. But W (V ) concave implies that doing sois costly! (draw graph)

12/21

The borrowing constraint region (Propositions 1 & 2 cont.)

I Region II: When Vr � V < V �:(a) There is no liquidation in current period and V 7! W (V ) is strictly

increasing and,(b) The optimal capital advancement policy is single-valued and s.t.

k (V ) < k� (the �rms is debt-constrained)

I Sketch of argument: suppose that the optimal repayment policy forregion II was τ = R (k) implying that the ICC binds (see below theproofs for both of these results). Then:

R (k) = δ(VH � V L)

which implies that increasing k is only incentive compatible ifVH � V L also increases. But W (V ) concave implies that doing sois costly! (draw graph)

12/21

The borrowing constraint region (Propositions 1 & 2 cont.)

I Region II: When Vr � V < V �:(a) There is no liquidation in current period and V 7! W (V ) is strictly

increasing and,(b) The optimal capital advancement policy is single-valued and s.t.

k (V ) < k� (the �rms is debt-constrained)

I Sketch of argument: suppose that the optimal repayment policy forregion II was τ = R (k) implying that the ICC binds (see below theproofs for both of these results). Then:

R (k) = δ(VH � V L)

which implies that increasing k is only incentive compatible ifVH � V L also increases. But W (V ) concave implies that doing sois costly! (draw graph)

12/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:

I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:

I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

Optimal repayment policy (proposition 3)

I The optimal repayment function satis�es τ = R (k) for V < V � andτ = 0 for V � V �.

I Intuition:I We know that maxV 2V W (V ) = W � and from props 1&2 we knowthat W (V �) = W �.

I Now, at given t, L delivers promised utility Vt either by allowingτ < R (k) or by promising higher future value.

I Risk neutrality and common δ ) V ! V � in the shortest timepossible is optimal.

I Limited liability then implies τ = R (k) until V = V �

13/21

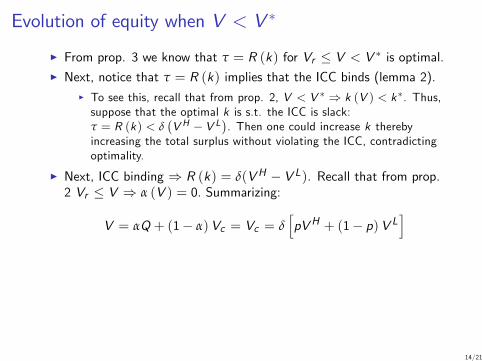

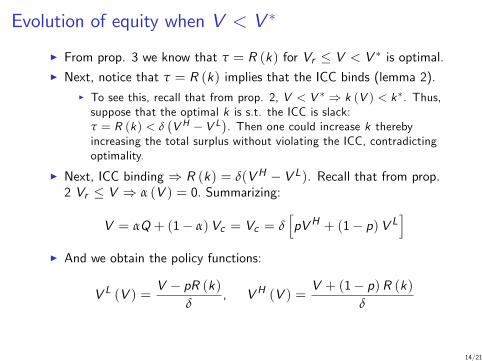

Evolution of equity when V < V �

I From prop. 3 we know that τ = R (k) for Vr � V < V � is optimal.

I Next, notice that τ = R (k) implies that the ICC binds (lemma 2).

I To see this, recall that from prop. 2, V < V � ) k (V ) < k�. Thus,suppose that the optimal k is s.t. the ICC is slack:τ = R (k) < δ

�V H � V L

�. Then one could increase k thereby

increasing the total surplus without violating the ICC, contradictingoptimality.

I Next, ICC binding ) R (k) = δ(VH � V L). Recall that from prop.2 Vr � V ) α (V ) = 0. Summarizing:

V = αQ + (1� α)Vc = Vc = δhpVH + (1� p)V L

iI And we obtain the policy functions:

V L (V ) =V � pR (k)

δ, VH (V ) =

V + (1� p)R (k)δ

14/21

Evolution of equity when V < V �

I From prop. 3 we know that τ = R (k) for Vr � V < V � is optimal.I Next, notice that τ = R (k) implies that the ICC binds (lemma 2).

I To see this, recall that from prop. 2, V < V � ) k (V ) < k�. Thus,suppose that the optimal k is s.t. the ICC is slack:τ = R (k) < δ

�V H � V L

�. Then one could increase k thereby

increasing the total surplus without violating the ICC, contradictingoptimality.

I Next, ICC binding ) R (k) = δ(VH � V L). Recall that from prop.2 Vr � V ) α (V ) = 0. Summarizing:

V = αQ + (1� α)Vc = Vc = δhpVH + (1� p)V L

iI And we obtain the policy functions:

V L (V ) =V � pR (k)

δ, VH (V ) =

V + (1� p)R (k)δ

14/21

Evolution of equity when V < V �

I From prop. 3 we know that τ = R (k) for Vr � V < V � is optimal.I Next, notice that τ = R (k) implies that the ICC binds (lemma 2).

I To see this, recall that from prop. 2, V < V � ) k (V ) < k�. Thus,suppose that the optimal k is s.t. the ICC is slack:τ = R (k) < δ

�V H � V L

�. Then one could increase k thereby

increasing the total surplus without violating the ICC, contradictingoptimality.

I Next, ICC binding ) R (k) = δ(VH � V L). Recall that from prop.2 Vr � V ) α (V ) = 0. Summarizing:

V = αQ + (1� α)Vc = Vc = δhpVH + (1� p)V L

iI And we obtain the policy functions:

V L (V ) =V � pR (k)

δ, VH (V ) =

V + (1� p)R (k)δ

14/21

Evolution of equity when V < V �

I From prop. 3 we know that τ = R (k) for Vr � V < V � is optimal.I Next, notice that τ = R (k) implies that the ICC binds (lemma 2).

I To see this, recall that from prop. 2, V < V � ) k (V ) < k�. Thus,suppose that the optimal k is s.t. the ICC is slack:τ = R (k) < δ

�V H � V L

�. Then one could increase k thereby

increasing the total surplus without violating the ICC, contradictingoptimality.

I Next, ICC binding ) R (k) = δ(VH � V L). Recall that from prop.2 Vr � V ) α (V ) = 0. Summarizing:

V = αQ + (1� α)Vc = Vc = δhpVH + (1� p)V L

i

I And we obtain the policy functions:

V L (V ) =V � pR (k)

δ, VH (V ) =

V + (1� p)R (k)δ

14/21

Evolution of equity when V < V �

I From prop. 3 we know that τ = R (k) for Vr � V < V � is optimal.I Next, notice that τ = R (k) implies that the ICC binds (lemma 2).

I To see this, recall that from prop. 2, V < V � ) k (V ) < k�. Thus,suppose that the optimal k is s.t. the ICC is slack:τ = R (k) < δ

�V H � V L

�. Then one could increase k thereby

increasing the total surplus without violating the ICC, contradictingoptimality.

I Next, ICC binding ) R (k) = δ(VH � V L). Recall that from prop.2 Vr � V ) α (V ) = 0. Summarizing:

V = αQ + (1� α)Vc = Vc = δhpVH + (1� p)V L

iI And we obtain the policy functions:

V L (V ) =V � pR (k)

δ, VH (V ) =

V + (1� p)R (k)δ

14/21

Evolution of equity when V < V �

I The authors show that V L (V ) ,VH (V ) are nondecreasing.

I Moreover, starting from any equity value V0 2 [Vr ,V �) after a �nitesequence of good shocks V0 ! V �.

I Likewise, after a �nite sequence of bad shocks V0 ! Vr or below,triggering randomized liquidation.

I There is an asymmetry between change in equity following good andbad shocks: if p, δ large ) V � V L > VH � V

15/21

Evolution of equity when V < V �

I The authors show that V L (V ) ,VH (V ) are nondecreasing.I Moreover, starting from any equity value V0 2 [Vr ,V �) after a �nitesequence of good shocks V0 ! V �.

I Likewise, after a �nite sequence of bad shocks V0 ! Vr or below,triggering randomized liquidation.

I There is an asymmetry between change in equity following good andbad shocks: if p, δ large ) V � V L > VH � V

15/21

Evolution of equity when V < V �

I The authors show that V L (V ) ,VH (V ) are nondecreasing.I Moreover, starting from any equity value V0 2 [Vr ,V �) after a �nitesequence of good shocks V0 ! V �.

I Likewise, after a �nite sequence of bad shocks V0 ! Vr or below,triggering randomized liquidation.

I There is an asymmetry between change in equity following good andbad shocks: if p, δ large ) V � V L > VH � V

15/21

Evolution of equity when V < V �

I The authors show that V L (V ) ,VH (V ) are nondecreasing.I Moreover, starting from any equity value V0 2 [Vr ,V �) after a �nitesequence of good shocks V0 ! V �.

I Likewise, after a �nite sequence of bad shocks V0 ! Vr or below,triggering randomized liquidation.

I There is an asymmetry between change in equity following good andbad shocks: if p, δ large ) V � V L > VH � V

15/21

Dynamics of equity

16/21

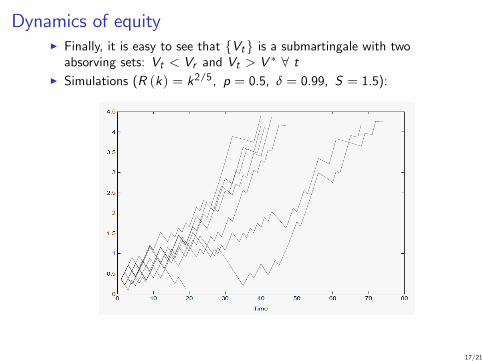

Dynamics of equityI Finally, it is easy to see that fVtg is a submartingale with twoabsorving sets: Vt < Vr and Vt > V � 8 t

I Simulations (R (k) = k2/5, p = 0.5, δ = 0.99, S = 1.5):

17/21

Dynamics of equityI Finally, it is easy to see that fVtg is a submartingale with twoabsorving sets: Vt < Vr and Vt > V � 8 t

I Simulations (R (k) = k2/5, p = 0.5, δ = 0.99, S = 1.5):

17/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Optimal k advancement policy

I We�ve seen that V0 2 [Vr ,V �)) k (V ) < k� (the �rms isdebt-constrained).

I Now, it is di¢ cult to characterize V 7! k (V ) in general (it isnonmonotonic).

I However, simulations show that conditional on success, capital growsat a positve rate, i.e. k(VH )/k (V ) > 1 while k(V L)/k (V ) < 1.

I This contributes to the "cash-�ow coe¢ cient" debate; if Tobin�s q isa su¢ cient statistic for investment, then cash �ows should notmatter.

I But if the optimal contract of this model was the DGP:

1. Cash �ows will matter for investment, k (V ) < k�

2. Cash �ows will matter more, the more constrained is the �rm.

18/21

Firm growth and survival

I Firm size is captured by k

I Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.

I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

I Firm size is captured by kI Starting frm the same V0 2 [Vr ,V �) simulate many di¤erent shockpaths.

I As seen before, �rms eventually either exit or reach theunconstrained optimum size.

I Since k < k� w/e Vt < V � surviving �rms grow with age; size andage are positively correlated in accordance with empirical evidence.

I Mean and variance of equity growth decrease sistematically.I Conditional probability of survival increases with V . Given that Vincreases over time (for surviving �rms), survival rates are positivelycorrelated with age and size.

I The advantage of this model is that requires little structure on thestochastic process driving �rm productivity; a simple i.i.d. process isenough to generate the rich dynamics described above.

19/21

Firm growth and survival

20/21

Beyond �rm dynamics (not presented here)

I The authors show that the optimal (long term) contract can bereplicated by a sequence of one-period contracts i¤ it isrenegotiation-proof.

I The contract is renegotiation-proof i¤ collateral S is greater thanthe maximum sustainable debt.

I Risk aversion?I No capital accumulation is WLOG?I General equilibrium?

21/21

Beyond �rm dynamics (not presented here)

I The authors show that the optimal (long term) contract can bereplicated by a sequence of one-period contracts i¤ it isrenegotiation-proof.

I The contract is renegotiation-proof i¤ collateral S is greater thanthe maximum sustainable debt.

I Risk aversion?I No capital accumulation is WLOG?I General equilibrium?

21/21

Beyond �rm dynamics (not presented here)

I The authors show that the optimal (long term) contract can bereplicated by a sequence of one-period contracts i¤ it isrenegotiation-proof.

I The contract is renegotiation-proof i¤ collateral S is greater thanthe maximum sustainable debt.

I Risk aversion?

I No capital accumulation is WLOG?I General equilibrium?

21/21

Beyond �rm dynamics (not presented here)

I The authors show that the optimal (long term) contract can bereplicated by a sequence of one-period contracts i¤ it isrenegotiation-proof.

I The contract is renegotiation-proof i¤ collateral S is greater thanthe maximum sustainable debt.

I Risk aversion?I No capital accumulation is WLOG?

I General equilibrium?

21/21

Beyond �rm dynamics (not presented here)

I The authors show that the optimal (long term) contract can bereplicated by a sequence of one-period contracts i¤ it isrenegotiation-proof.

I The contract is renegotiation-proof i¤ collateral S is greater thanthe maximum sustainable debt.

I Risk aversion?I No capital accumulation is WLOG?I General equilibrium?

21/21