Embed Size (px)

Citation preview

1

A Tour of the World Economy:

Global, Regional and Local Risks and

Opportunities

Dr Florian Kohlbacher

Director, North Asia

Economist Corporate Network

7 September 2016

2

Agenda

1) Global Context

2) Regional Context

3) Local Context

3

Global Context

4

Global economy – key points for 2016

• The new normal

Lower for longer: oil and commodity prices

Lower for longer: interest rates

Lower for longer: economic growth

• Tour of the world

US: Trump presidency? US consumers powering the global economy

Europe: Brexit and immigration policy; European project in reverse?

China: smooth landing not possible; choice is bumpy or hard landing

• Bright spots

India: fastest growing large economy

Iran: rejoins global economy

5

Global context

2.1% 2.4%

Brexit Vote

Slowdown in the US

6

Global context

2016 will be the fifth

consecutive year in

which global growth is

below its long-term

average of 3.7%

7

Emerging Asia the growth hotspot – again – in 2016

-0.52.3

2.0

1.6

5.8

2.5

2.0

7.14.4

-1.3

0.5

Real GDP growth, %

Policymaking once again key(-) BR, ZA, NG, RU (+) IN, VN, IR, AR

Global growth

8

Global growth

9

Asia outperforms RoW

10

Poll of Forecasters

11

Risks to the global economy

12

Stagnant living

standards?

Political risk: on the rise

Is there a pattern to the latest surge?

Anti-establishment Long running

disputes

13

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60 70 80 90 100

Cu

mu

lati

ve

gro

wth

ra

te (

%)

of

rea

l P

PP

in

co

me

Percentile of global income distribution

Winners and losers of globalisation

Global growth incidence curve (1988 – 2008)

Source: Branko Milanovic

Very poorest

locked out of

growth

Fast income

growth in EMs

(mainly China)

Global elite: rich

get richer!

Stagnating incomes

for middle class in

rich countries

14

Trans Pacific Partnership: mission impossible?

Chance of US ratifying the key policy of Obama’s Asia pivot has fallen to 30%

“The Trans-Pacific Partnership, which has some serious flaws, will not be acted

upon this year.” – Mitch McConnell, US Senate majority leader

Source: Peterson Institute for International Economics

15

Monetary policy in a new normal

Central banks are unprepared for the next recession

Policy options

Quantitative easing ✓Forward guidance ✓

Negative interest rates ?

Higher inflation target ?

Target nominal GDP ?

Helicopter money ?

0

2

4

6

8

10

12

14

1983 1988 1993 1998 2003 2008 2013

US federal funds rate (%) “ I know you think

you understand

what you thought

I said but I'm not

sure you realise

that what you

heard is not what

I meant”

Source: The Economist Intelligence Unit

16

The oil price will rise, but not by much

High stocks and higher OPEC production will prevent a surge in oil price

Source: The Economist Intelligence Unit

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2013 2014 2015 2016 2017 2018 2019 2020

Production growth Consumption growth

17

Since the financial crisis,

shipping has suffered from the

global trade slowdown, plus too

much shipbuilding and not

enough scrapping.

The Baltic Dry index, a measure

of freight rates, has plummeted

by more than 90% since 2008.

Container lines might lose $10

billion this year (according to

consultancy Drewry)

Maersk, the world’s largest

shipping firm, may break itself

up to stay sea-worthy

That sinking feeling: shipping in crisis

18

Trade, a secular decline

Global trade having its worst year since 2009, but will improve modestly in 2017

-20

-15

-10

-5

0

5

10

15

20

2009m01 2010m01 2011m01 2012m01 2013m01 2014m01 2015m01 2016m01

Global merchandise trade (% change yoy)

Volume terms Value terms

0

4

8

12

16

1991 1996 2001 2006 2011 2016

Share of global trade (%)

China Germany Japan US

19

Where is the growth?

Higher commodity prices will support Emerging Markets in 2017

-4

-2

0

2

4

6

8

10

Ind

ia

Chin

a

AS

EA

N

Sou

th K

ore

a

Mid

dle

Ea

st

Latin

Am

eri

ca

Russia

US

Euro

zo

ne

Ja

pa

n

Glo

ba

l

2015 2016 2017

Source: The Economist Intelligence Unit

Real GDP growth; % change, year on year

20

A four decade slump in productivity

Are our best inventions behind us?

21

Long term forecast to 2050

The rise of Asia

Regional share of the global economy

Real GDP growth; % change, year on year

2222

China was going to overtake the US in 2026: now 2033

Green = Lower rank since Nov 2015, Red = Higher rank, Grey = same rank

Nominal GDP, US$ trn.

0

5

10

15

20

25

30

35

TH, MY, PO

drop out

Source: The Economist Intelligence Unit.

World’s largest economies in 2030

23

Regional outlooks: US, Europe, Asia

24

US election: the unpopularity contest

Two of the most disliked presidential candidates in history

25

We forecast Clinton presidency, Democratic Senate, Republican House

US election: the unpopularity contest

26

US economy

1.6%

27

US: a two-speed economy

Consumers are driving the economy, as firms fail to invest

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2

(%)

Consumer spending Business investment Real GDP

Source: Bureau of Labor Statistics

28

US: a turning point

Workers are gaining power, at the expense of corporations

29

European Union

30

EU: growth and the ECB

The EU should grow by 1.6% in

2016

ECB pushing hard on stimulus

・Aim to encourage banks to lend to

companies

・Deposit rate cut from -0.3% to -0.4%;

policy rate cut to zero

・Investment grade non-bank corporate

debt added to QE programme

・Impact limited by demand side

constraints and strong euro

・Political climate means ECB getting

little assistance from governments or

investment

-0.2 0.8 1.8

2015

2016

2017

Contribution to GDP growth (%)

Cons Govt Inv External

31

Brexit: profound consequences for UK and Europe

Brexit will have damaging political

and economic consequences

UK recession in 2017

Euro zone annual real GDP growth

forecast for 2016-20 trimmed by 0.2

percentage points

Contagion: boost for anti-establishment

and anti-EU parties across Europe

EU referendums in other countries—

Netherlands and France–could trigger

euro zone crisis

Scotland independence, united Ireland?

32

Europe: on the brink?

Italy is the next pressure point

33

China: another two-speed economy

34

China: slowing industries

Source: The Economist

35

China: difficulties ahead

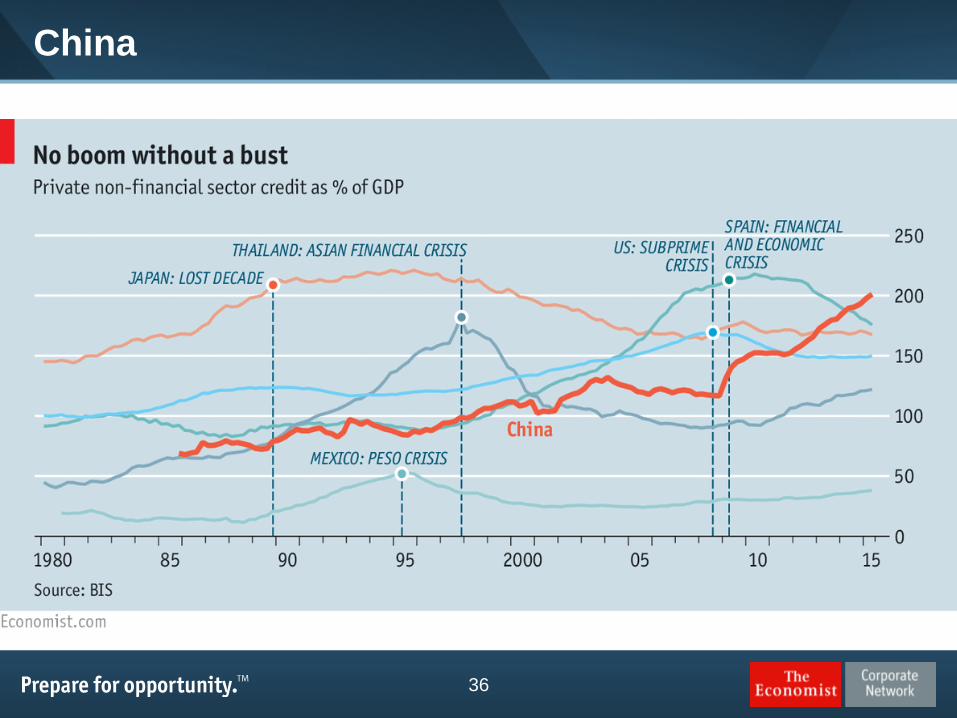

36

China

37

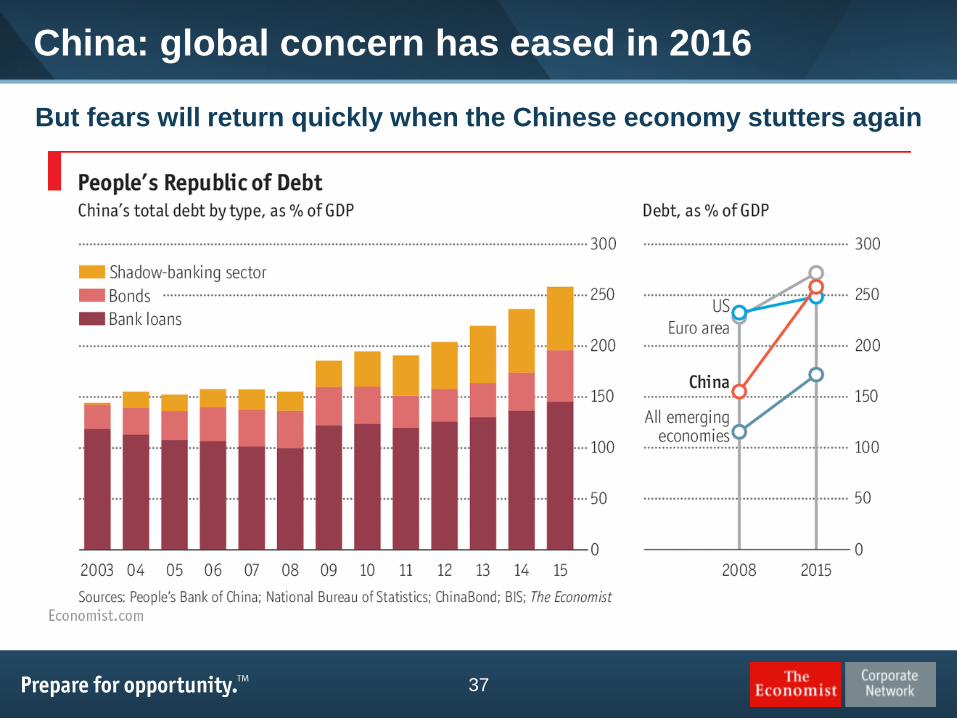

China: global concern has eased in 2016

But fears will return quickly when the Chinese economy stutters again

38

Hard landing in China is major global risk

• We think there is a 40% risk of a China

hard landing (defined as 2ppt

deceleration in real GDP growth)

• Triggers? Banking crisis, housing crash

or slump in private investment

• Housing bubble? Property sales value

up by 40% in January-Jul over the

year-earlier period

• Debt now at dizzying levels; domestic

credit growing 3.2 x faster than nominal

GDP

We forecast real GDP growth of 6.6% in 2016, slowing to 4.2% in 2020

39

India: catching up?

0

2

4

6

8

10

12

14

16

1990 1995 2000 2005 2010 2015 2020

Economic growth (%)

China India

Forecast

4040

• India has overtaken China as the fastest growing large emerging market

• Source: The Economist Intelligence Unit.

0

2

4

6

8

10

12

14

16

1990 1995 2000 2005 2010 2015 2020

Economic growth (%)

China India

Forecast

India: catching up?

41

India – macroeconomic trends

Real GDP growth will average 7.3% a year in

2016/17 – 2020/21, well below its potential・Constrained by overcapacity in some industrial

sectors, infrastructure bottlenecks, shortages of labor

in key sectors and the difficulties in shifting resources

to higher-productivity manufacturing. Bankruptcy

reform legislation (expected to be passed this year)

will free up distressed assets and improve capital

allocation. Services sector will still lead output basis.

Nationwide GST unifies India’s 29 states into

a single market・Expect huge efficiency savings for business,

greater competitiveness for local firms, a wider tax

base, and less administrative burden.

.

42

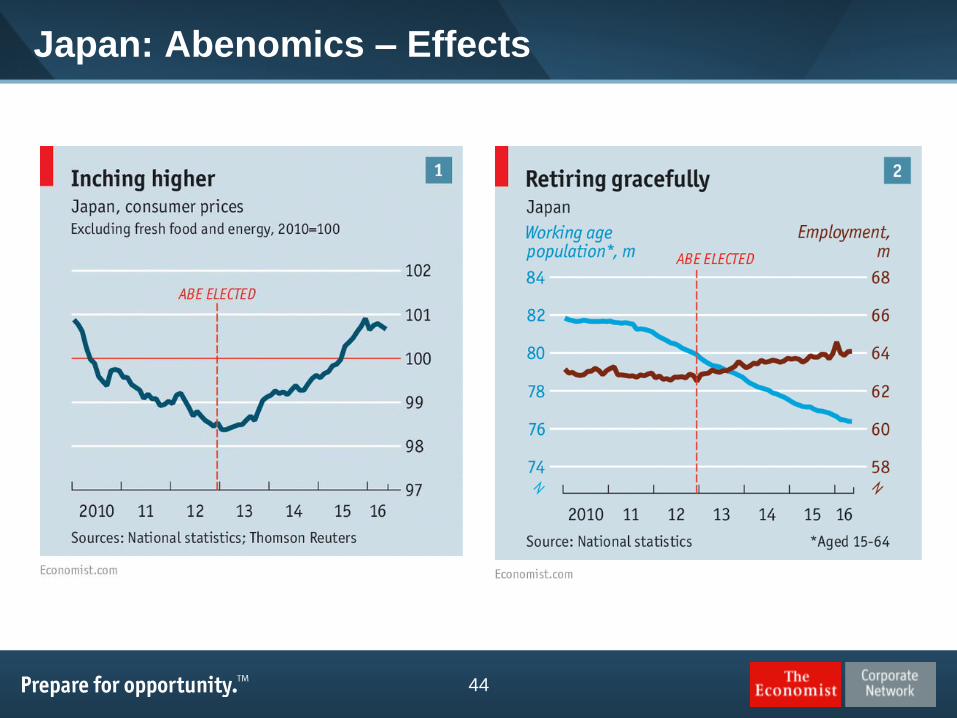

Japan: Abenomics

43

Japan: running to a stand still

• Growth in nominal yen terms has been stronger

• Falling population means falling real GDP may become the norm

Per capita growth looks better

• Abenomics not a long-term solution

Monetary and fiscal √

Structural reform X

44

Japan: Abenomics – Effects

45

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Real GDP (% change)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

BOJ’s inflation

target

Govt’s target

growth rateAbe in office

Consumption

tax rate hike

2nd consumption

tax hike (Oct ‘19);

Tokyo Olympics

Consumer prices (% change)

We forecast GDP growth of 0.4% in 2016, and avg of 0.3% in 2017-20

Japan: Abenomics is not succeeding

46

Japan: macroeconomic trends

Expected growth of economy is 0.4% this year, compared with

previous forecast of 0.8%.

・Economy predicted to fail in picking up significant momentum in 2017-2020, but

Olympic Games in 2020 will help boost consumer and business confidence.

Demographic factors will be main constraint on potential GDP

growth in the forecast period.

・Population and workforce to contract steadily, acting to crimp consumption and

investment. Promised structural reforms will proceed haltingly, and TPP benefits

for Japan’s external sector will show only after 2020.

Fiscal stimulus not as powerful as it looks

・Only around a quarter of the headline figure of \28tn constitutes new spending,

and that will be spread over two years.

47

ASEAN: growth led by CLMV

• CLMV countries to grow rapidly – but

from a low base

• Philippines will remain the fastest

growing ASEAN-6 economy, although

we lowered our forecast because of

the election result

• Indonesia’s growth will pick up

because of improvements to

business environment and

government infrastructure investment

• Thailand still struggling and growth

will be below potential

• Region set to benefit as China, Japan

& India seek to gain influence

0

2

4

6

8

10

Myanm

ar

Laos

Cam

bodia

Vie

tnam

Phili

ppin

es

Indonesia

Mala

ysia

Thaila

nd

Sin

gapore

Bru

nei

Economic growth in ASEAN, 2016-20

(% real change pa; avg)

Source: The Economist Intelligence Unit.

48

ASEAN: China’s slowdown

49

ASEAN: rising incomes and consumption

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2016

2020

GDP per head (US$)

52,150

66,280

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000 2016

2020

Private consumption per head (US$)

19,910

25,590

Source: Economist Intelligence Unit

50

ASEAN: expanding middle and upper classes

Source: Economist Intelligence Unit

51

ASEAN: Political challenges

For how long can the

army hold the peace?

Jokowi struggles to

remain popular

Conflicts with China

Najib clings on but

investors are spooked

Much-needed reforms,

fragile institutions

Rodrigo Duterte’s war

on drugs

52

Regional outlook:

Economic integration in Asia

53

The innovation imperative

54

The innovation imperative

55

Asia’s infrastructure imperative

56

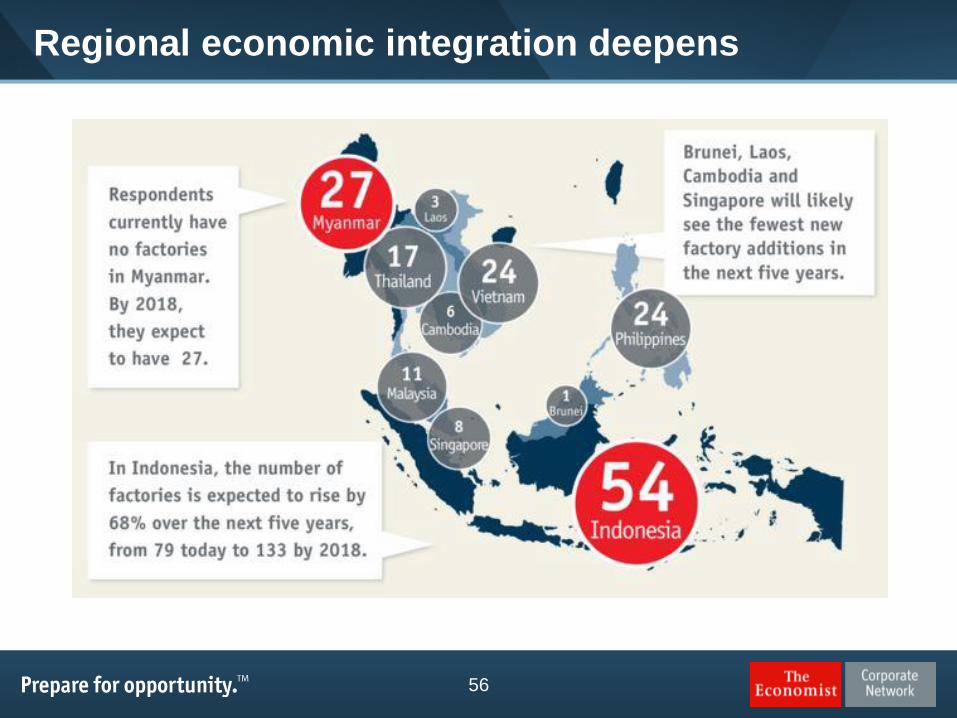

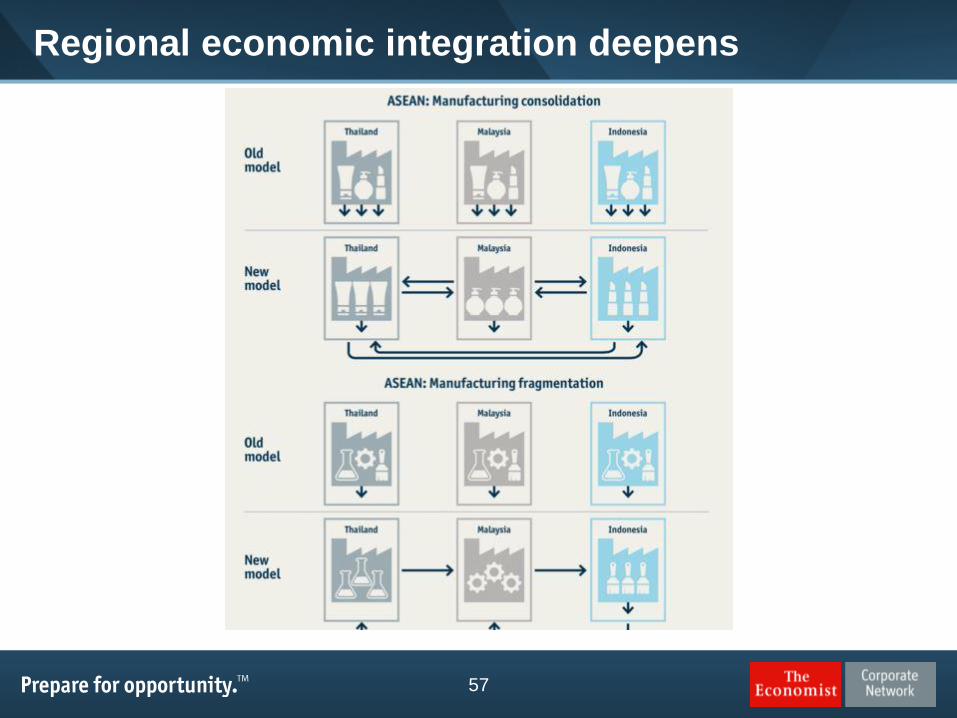

Regional economic integration deepens

57

Regional economic integration deepens

58

Regional economic integration deepens

59

• Annual survey of business

expectations in Asia for

the year ahead

What are you expecting for

your company’s Asia sales

performance in 2016 relative

to 2015?

• South-east Asia ranks 2nd

(after India) in terms of

sales growth expectations

Source: The Economist Intelligence Unit

Asia Business Outlook Survey 2016: sales expectations

60

• Most positive factors: economic growth (2nd in survey), technology (3rd)

• Most negative factors: currency, competition Source: The Economist Intelligence Unit

Asia Business Outlook Survey 2016: Profitability factors in SEA

61

Asia Business Outlook Survey 2016: Profitability factors in Japan

• Most positive factor: technology

• Most negative factors: currency, competition Source: The Economist Intelligence Unit

62

Longer term positives: Major trade deals ahead

• RCEP: Links ASEAN economies with major Asian economies

Pop. of 3.5 billion; 32% of world exports, 4.58% avg. GDP growth (2016-2020)

Championed by China

• TPP: Links Asian economies to Americas

32% of world GDP

Championed by the US

63

Longer term positives: Major trade deals ahead

64

Longer term positives: Major trade deals ahead

65

Longer term positives: “one belt, one road”

66

Longer term positives: “one belt, one road”

67

Longer term positives: “one belt, one road”

68

Regional economic integration deepens

69

Local outlook: Korea

70

Korea: Political risk

71

South Korea: GDP

• Sluggish GDP growth

• Conforming to the New Normal?

• EIU forecast: GDP to grow by an

average of 2.5% a year in 2016-

20

72

South Korea: GDP growth

73

South Korea: GDP per capita

• GDP per Capita is at 84%

of Japan and the gap is

closing

• Will exceed US$ 30,000 by

2022

74

South Korea: consumer prices

• Slowly rising consumer

prices

• “Inflation Report” by BoK

• Inflation target 2016: 1.4%

• Inflation target 2017: 2%

• EIU: Inflation to average

0.8% in 2016 but will

accelerate to an average

annual rate of 1.8% in

2017-18

75

South Korea: household debt

• Household debt is increasing at an

alarming rate

Total debt: KRW 1,200 trillion.

• Low interest rate leads to

excessive loan of household

76

South Korea: Foreign Direct Investment

• FDI has decreased in recent

years so the government is

implementing new set of policies

Reduced corporate taxes

New system to better protect

intellectual property rights

Shorter process of establishing

an industrial complex

Maximum amount of foreign

capital that can be lent or

borrowed without the need to

report the transaction has been

increased

International financial reporting

standards have been adopted

77

South Korea: the Won

• Bank of Korea tries to keep the

Won low for price

competitiveness over other

export-oriented economies

• EIU: won to weaken from an

estimated average value of

W1,168:US$1 in 2016 to

W1,238:US$1 in 2020

78

South Korea: Women in the economy

79

South Korea: Aging population & low birthrate

• Birth rate in 2014: 1.25 (Unit: Number of births per woman)

Failure in policy to support working women

80

Finally

81

Five big questions for 2016

1. Will the oil price reach a bottom?

Yes, but price rises will be gradual

2. Will the US elect Donald Trump as president?

Probably not, but risk rises if there is a recession or terrorist attack

3. Can the EU survive the migration crisis and Brexit vote?

Yes, but “ever closer union” is over for now

4. Can China meet its ambitious growth targets?

No, but slower growth reduces risk of hard landing

5. Will weak currencies and low commodity prices crush EMs?

No, but most will struggle. Gradual improvement from 2017 onwards

82

Q&A

Anti-establishment Long running

disputes

Stagnant living

standards?

The return of political risk