Embed Size (px)

Citation preview

8th Proof

of

KANRICH FINANCE LTD.Annual Report 2014/15

submitted

by

Smart Media (Pvt) Ltd.

on

16th July 2015

K a n r i c h F i n a n c e L t d A n n u a l R e p o r t 2 0 1 4 / 1 5

Ka

nrich

Fin

an

ce L

td A

nn

ua

l Re

po

rt 20

14

/15

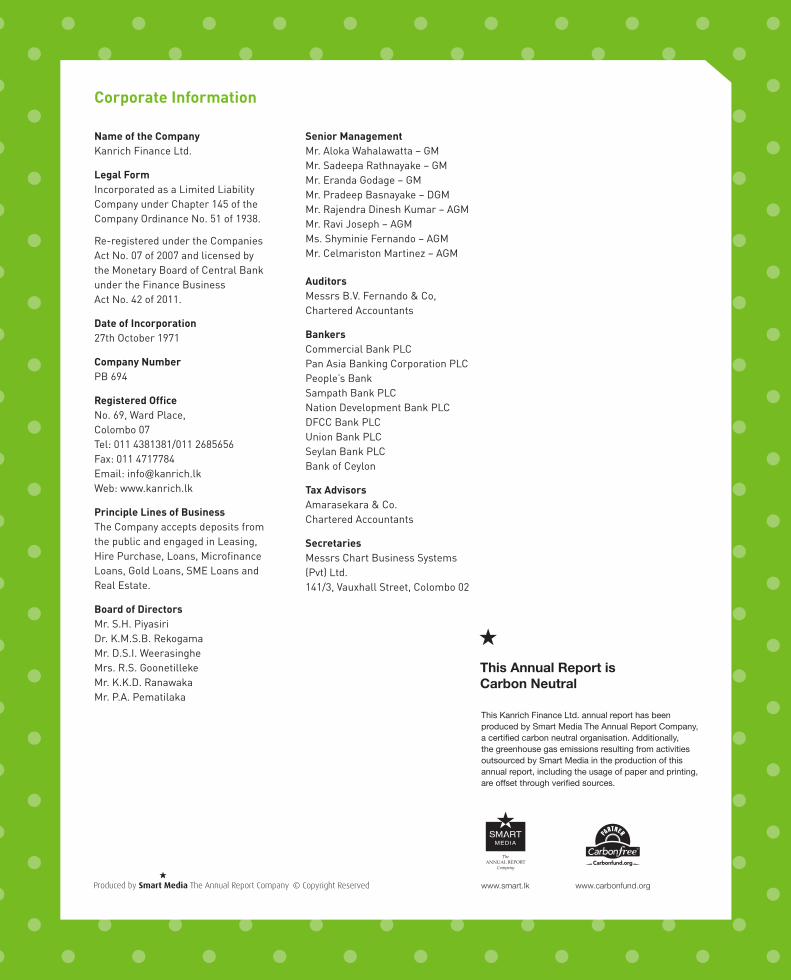

Kanrich Finance Ltd.

No. 69, Ward Place, Colombo 7, Sri LankaHotline: +94 114 381 381 Tel: +94 112 685 656 E-mail: [email protected]

A VALUABLEPROPOSITION

kanrich.lk

Vision StatementWe move towards our goal of being a best corporate entity in the country, performing in steady practices and surpassing the desires of customers.

Mission StatementWe foresee of being a best corporate entity in the country, performing in steady practices, conducting business with responsibility, consistently outperforms our peers and surpassing the desires of customers through excellence in delivering innovative products. We continuously promote a learning culture and provide a dynamic and challenging environment for our employees whilst creating lasting value for our shareholders.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

01

a valuableproposition

Our strategic and sustainable growth over the years

is underpinned by the powerful and superior value

propositions we consistently offer to all our stakeholders

in all their interactions with us. This is because we

consider our offer to be a ‘gift’, carefully selected and

pleasantly wrapped in a way that brings the desired

outcomes to the recipients as well as the giver.

Be it our range of products and services, attractive

returns, conducive working environment, commitment

to governance, risk management and corporate

responsibility, ours is a valuable proposition indeed, as

borne out by our figures.

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

About Us

02

The Company started its journey in 1971 with the incorporation of Mutual Investment and Finance Ltd., and was registered under the Companies Ordinance No. 51 of 1938.

The Company re-registered under the new Companies Act No. 07 of 2007. In 2010, it was rebranded as Kanrich Finance Ltd., revolutionary changing the path towards a brand new direction.

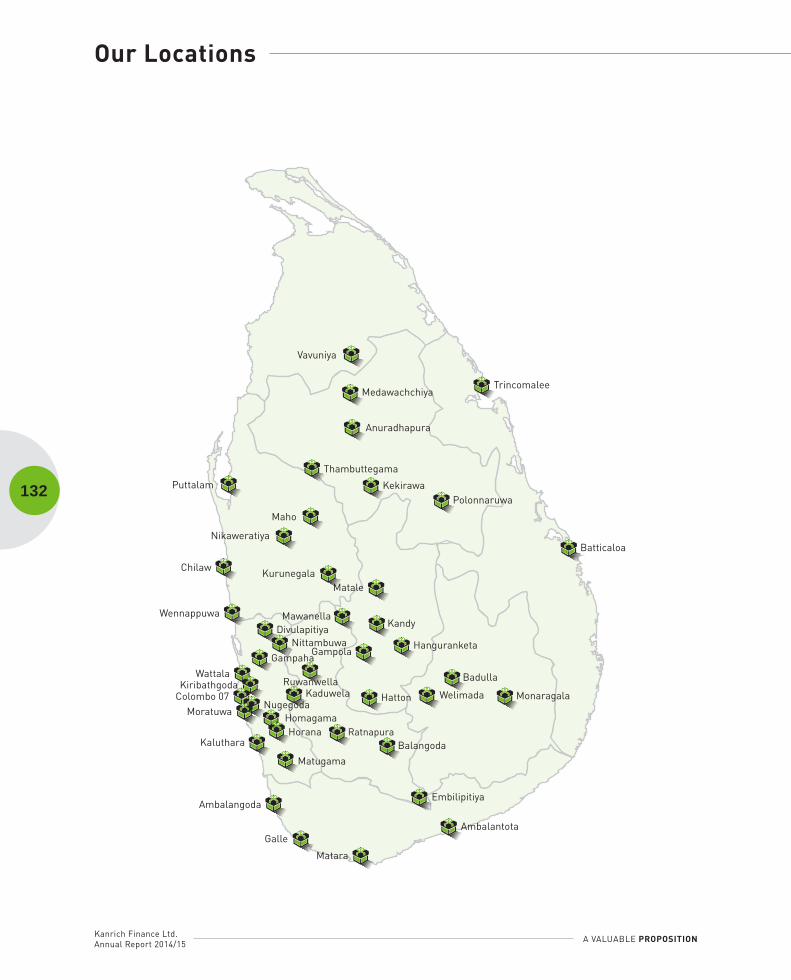

With a strong financial tradition of over 43 years, KFL offers a portfolio of financial solutions including deposits, savings, leasing, hire purchase, real estate and microfinance products. KFL started its operations with 60 employees and an asset base of Rs. 600 million. Today, the total workforce is over 1,200 employees

and the asset base is more than Rs. 11 billion. The Company has expanded its reach with its presence in 44 locations spread across the country except in the Northern Province.

KFL was completely transformed after taking over by Mutual Holdings Ltd. (MHL) to what it is today and presently it ranks among the top finance companies in Sri Lanka.

KFL is led by a highly experienced and professional Board of Directors and a young and dynamic management team.

The Company is guided by its core principles and values and is on a well-planned strategic path to achieve market leadership. The Company serves its clientele with an unmatched product spread, coupled with supreme service quality by customising the core products to attract the market. With a customer base exceeding 260,000, KFL has already established itself in the financial services industry and will continue to remain firm and focused with a strong brand of financial stewardship.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

03

10

15

129

71

31

66

04

06

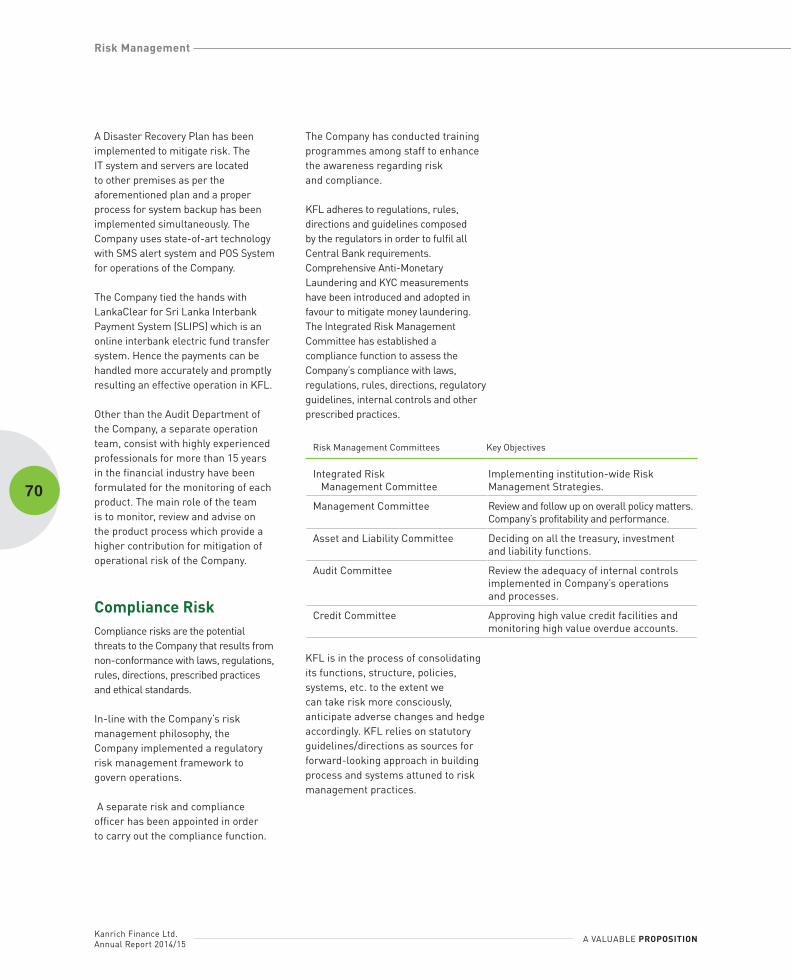

Chief Executive Officer’s Review

Sustainability Report

Risk Management

Management Discussion and Analysis

Highlights of the Year

Annexes

Chairman’s Message

Contents

Financial Reports

39Stewardship

46

Corporate Governance Report

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

04

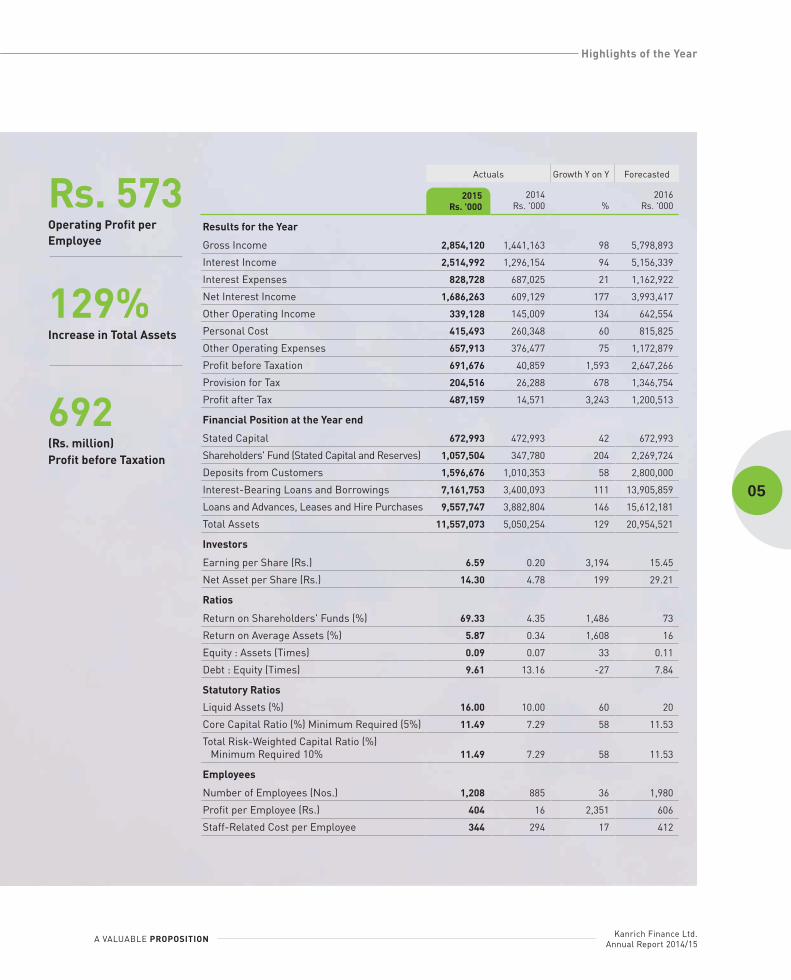

Highlights of the Year Highlights of the Year

Rs. 2,854

Rs. 6.59

1,208

11.49%

Gross Income

Earnings per Share

No. of Employees

Core Capital

million

Rs.11,557Asset Base

million

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

05

Highlights of the Year Highlights of the Year

Actuals Growth Y on Y Forecasted

2015 Rs. '000

2014 Rs. '000 %

2016 Rs. '000

Results for the Year

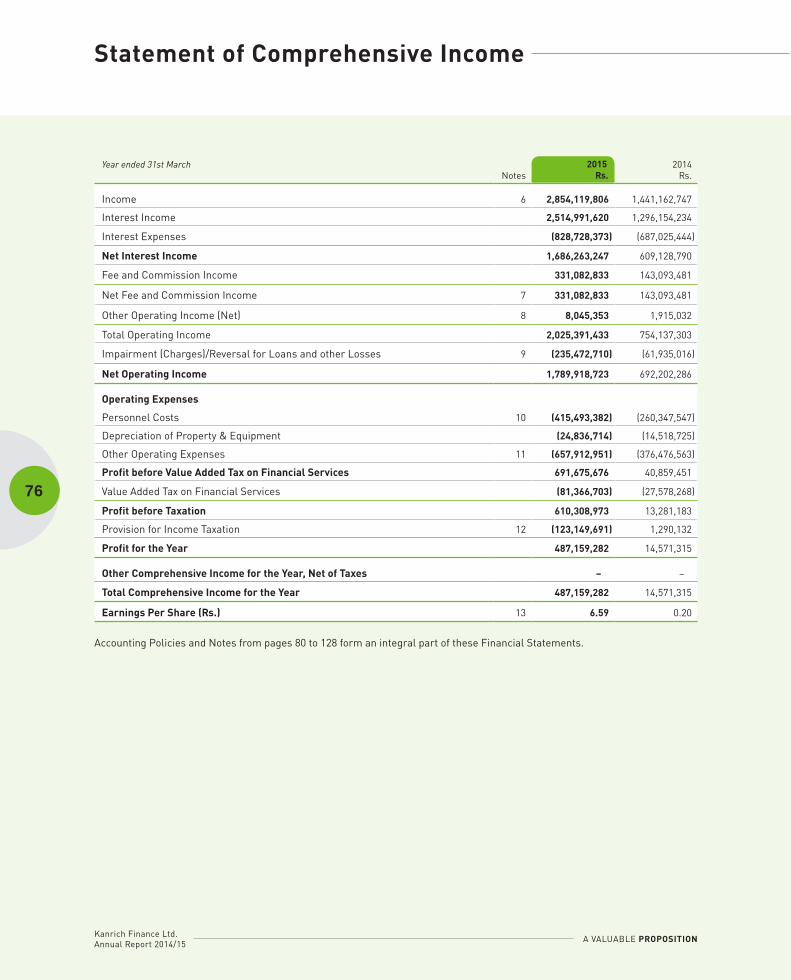

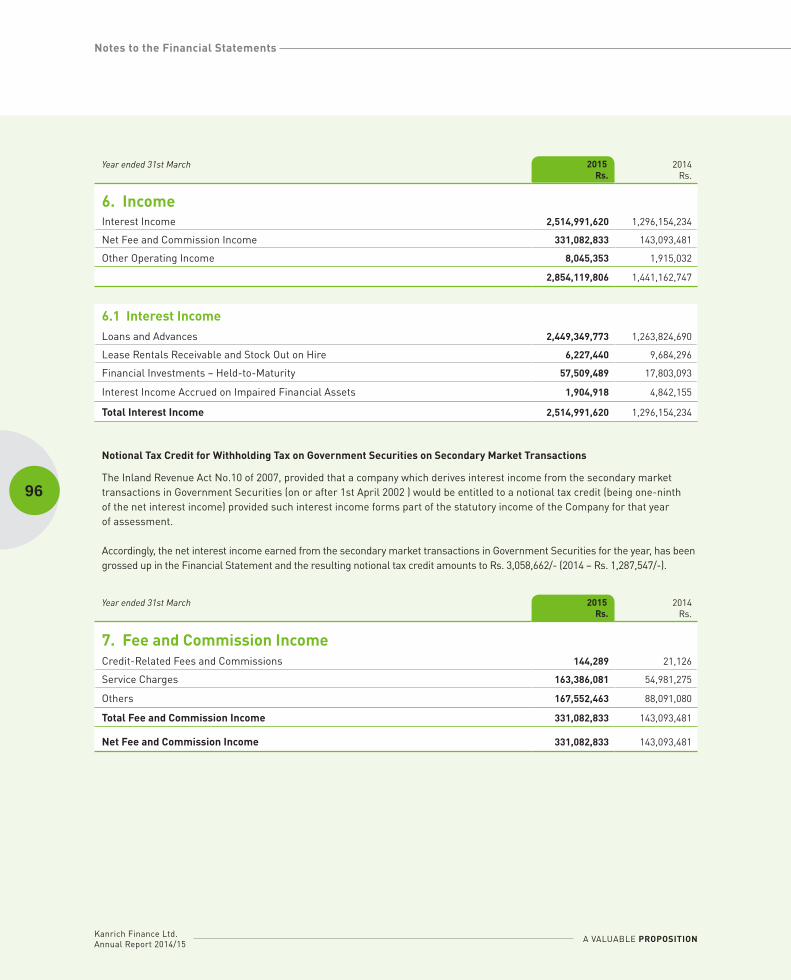

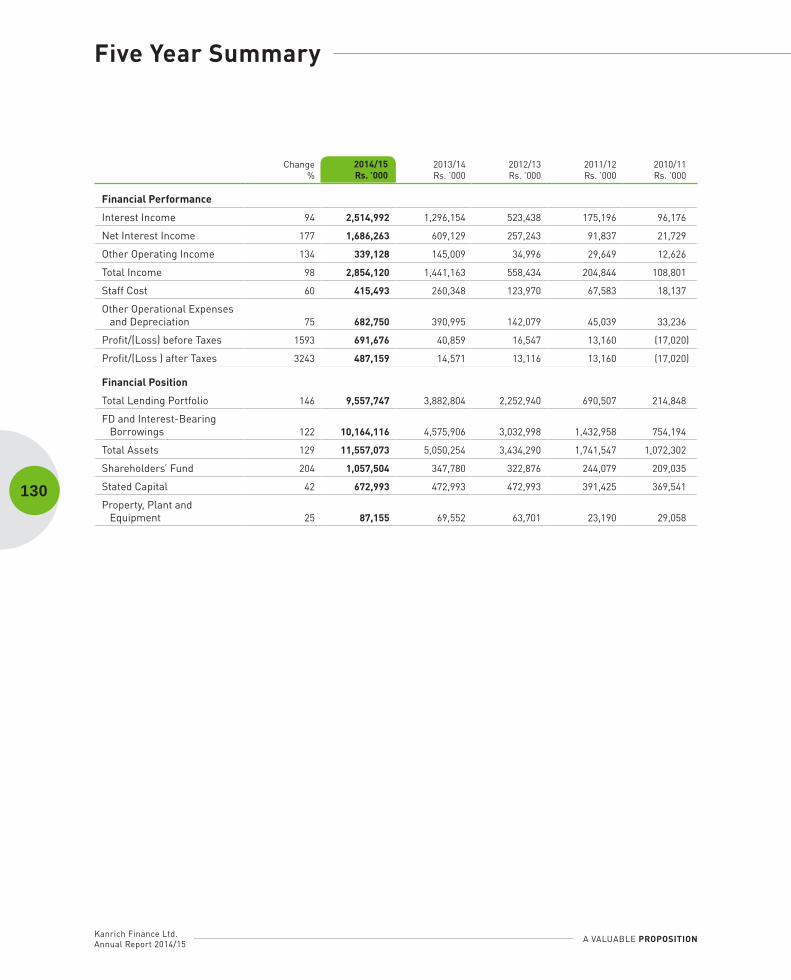

Gross Income 2,854,120 1,441,163 98 5,798,893

Interest Income 2,514,992 1,296,154 94 5,156,339

Interest Expenses 828,728 687,025 21 1,162,922

Net Interest Income 1,686,263 609,129 177 3,993,417

Other Operating Income 339,128 145,009 134 642,554

Personal Cost 415,493 260,348 60 815,825

Other Operating Expenses 657,913 376,477 75 1,172,879

Profit before Taxation 691,676 40,859 1,593 2,647,266

Provision for Tax 204,516 26,288 678 1,346,754

Profit after Tax 487,159 14,571 3,243 1,200,513

Financial Position at the Year end

Stated Capital 672,993 472,993 42 672,993

Shareholders' Fund (Stated Capital and Reserves) 1,057,504 347,780 204 2,269,724

Deposits from Customers 1,596,676 1,010,353 58 2,800,000

Interest-Bearing Loans and Borrowings 7,161,753 3,400,093 111 13,905,859

Loans and Advances, Leases and Hire Purchases 9,557,747 3,882,804 146 15,612,181

Total Assets 11,557,073 5,050,254 129 20,954,521

Investors

Earning per Share (Rs.) 6.59 0.20 3,194 15.45

Net Asset per Share (Rs.) 14.30 4.78 199 29.21

Ratios

Return on Shareholders' Funds (%) 69.33 4.35 1,486 73

Return on Average Assets (%) 5.87 0.34 1,608 16

Equity : Assets (Times) 0.09 0.07 33 0.11

Debt : Equity (Times) 9.61 13.16 -27 7.84

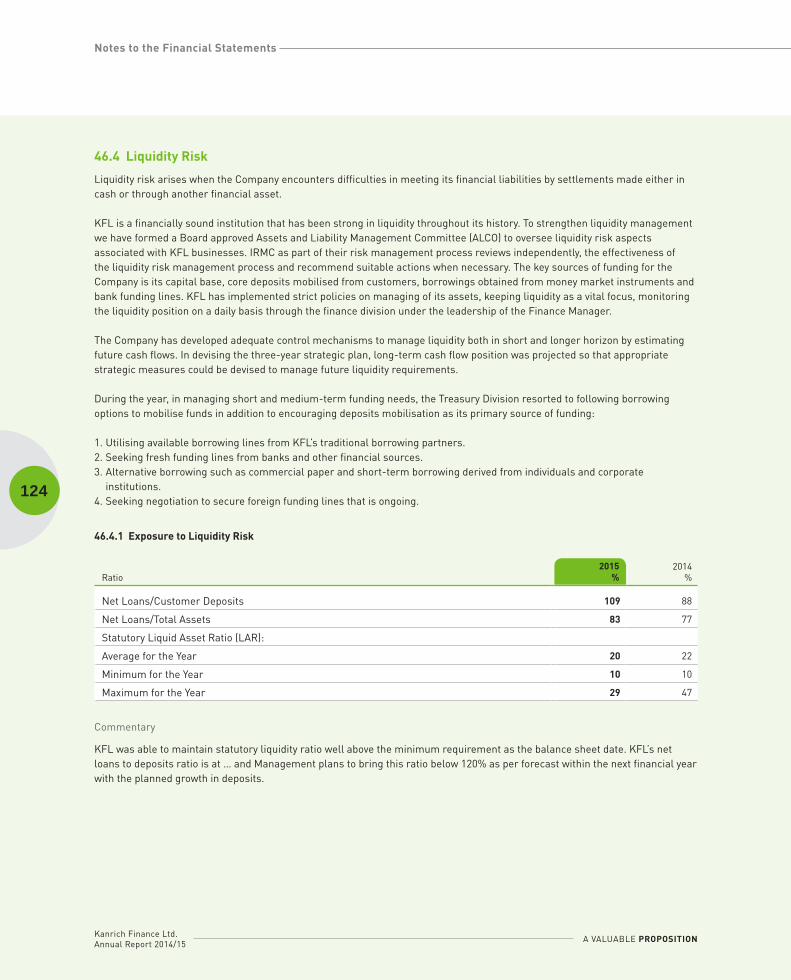

Statutory Ratios

Liquid Assets (%) 16.00 10.00 60 20

Core Capital Ratio (%) Minimum Required (5%) 11.49 7.29 58 11.53

Total Risk-Weighted Capital Ratio (%) Minimum Required 10% 11.49 7.29 58 11.53

Employees

Number of Employees (Nos.) 1,208 885 36 1,980

Profit per Employee (Rs.) 404 16 2,351 606

Staff-Related Cost per Employee 344 294 17 412

Rs. 573Operating Profit per Employee

129%Increase in Total Assets

692(Rs. million)Profit before Taxation

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

06

Chairman’s Message Chairman’s Message

Year 2014/15 was for Kanrich Finance Ltd., an important juncture in its 43-year history; a prudent and necessary transformation of the size, structure and scope of our Company.

It was also a year of challenges and significant accomplishments; if we step back and view the year in context, we can see how far our Company has come in a short time – exemplifying the effectiveness of our value propositions.

Operating EnvironmentGlobal growth in 2014 was a modest 3.4%, reflecting an increased growth in advanced economies compared to the previous year and a slowdown in emerging market and developing economies. However, despite the slowdown, emerging market and developing economies still accounted for three-fourths of global growth. South Asia was the fastest-growing region in the world in the last quarter of 2014 on account of the strong expansion in India, coupled with favourable oil prices.

Amidst uneven developments in the global economy, Sri Lanka recorded an economic growth of 7.4%, compared to 7.2% in 2013. This was largely due to the favourable macroeconomic conditions supported by relaxed monetary policy stance on par with low and stable inflation during the year. The credit demand was low for most parts of the year, on account of decline in gold prices, the rapid growth of the corporate debt market and increased foreign borrowings by Sri Lankan corporates.

The banking sector remained robust, maintaining its lead role in the financial sector and continued to expand its asset base. The asset growth of the Licensed Finance Companies and the Specialised Leasing Company sector moderated during 2014 due to lower demand for credit, particularly during the early

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

07

Chairman’s Message Chairman’s Message

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

08

part of the year. However, the demand for credit picked up during the second half of 2014. The lower interest rate scenario facilitated the improvement of credit demand and maintenance of the rising non-performing loans at a manageable level.

Turning Challenge to an OpportunityOur overarching strategic objective for the year in review was to support the Consolidation Programme of the Central Bank of Sri Lanka (CBSL). Having been categorised as a Group ‘B’ company by the CBSL, we were required to either merge with a local bank or a category ‘A’ company or, upgrade ourselves to a Group ‘A’ company. Opting for the latter option, we set about to accomplish the ambitious target of raising our core capital to Rs.1 billion and our asset base to Rs. 7.5 billion by December 2014. The asset base of our Company at that time was Rs. 4 billion, whilst the core capital was Rs. 305 million.

What would seem as a challenge we successfully converted into an opportunity to grow and expand our Company. Our corporate plan was accelerated to create a reshaped Kanrich; one that is bigger, stronger and positioned to succeed over the long term and deliver increased value for shareholders. Our monthly profits were increased substantially to build capital. This was achieved by expanding our operations island wide, except in the North, increasing our staff strength to over 1,200 and increasing our lending targets significantly. I am extremely encouraged by the significant feat we have accomplished by attaining these ambitious targets before the time frame set by the CBSL.

Our corporate plan was accelerated to create a reshaped Kanrich; one that is bigger, stronger and positioned to succeed over the long term and deliver increased value for shareholders.

Chairman’s Message Chairman’s Message

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

09

When formulating our corporate plan in year 2010, we made a conscious decision to move away from the conventional products such as hire purchase, leasing and pawning and particularly focus on the microfinance and the SME sector. Operating in a market atmosphere in which conventional business approach would be difficult to sustain on account of declining gold prices and fluctuation of vehicle prices, our strategic focus brought in resounding results to the Company. Our lending was not affected due to our central focus on microlending during the year. Amid stagnant loan growth in the industry, the loan growth of our Company recorded an upward movement achieving an assets growth of over 129% year on year. Our capital adequacy which was less than the required minimum of 10% at the commencement of the financial year was increased to over 12% by year end. Despite the industry’s Non-Performing Loan (NPL) escalating to levels as high as 5%, I am happy to state that the NPL of our Company remained at a low level of 2%; below the industry average. Most importantly, we stepped up our compliance as well. Our compliance score awarded by the CBSL was increased to 94% by year end compared to the score of 62% three years ago. These results amply demonstrate that we have accomplished much during the year and our growth is unique in the industry.

Positioned for Long-Term SuccessDuring the year, we did not diversify due the adverse market conditions that prevailed for leasing, hire purchase and pawning products. However, we will move into the

conventional product segment to balance our asset base in the upcoming year. New products will be developed, especially information technology based products to expand our product offering. In addition, our support services will be enhanced to sustain the business growth. Accordingly, areas such as human resources, information technology, finance and administration will be upgraded in 2015/16. I am personally committed to ensuring that ethical standards continue to be embedded in our culture across our Company. Our processes and procedures will be developed to the standard of a banking institution. It is our ambition, to build up our Company to a bank in the future, which also complements the intention of the CBSL to strengthen the financial sector of Sri Lanka. Hence, the processes, procedures, policies and business ethics of our Company will be strengthened further.

AcknowledgementAs we journey on, we will continue to build on the solid foundations we have put in place to deliver on our commitments to customers, shareholders, business partners, regulators and the broader society. Every year a new chapter is written into the history of our Company and I am sure, 2014/15 will be considered in the future to have been an important, positively transformational, period in KFL’s history.

In closing I extend my deep appreciation to all the employees of Kanrich Finance Ltd. for contributing to the excellent results through their dedication and ingenuity. I commend Shiran Weerasinghe, our Chief Executive Officer/Director, and his entire management team, for their leadership and resourcefulness

Chairman’s Message Chairman’s Message

during a year that will be remembered as the defining point of Kanrich Finance Ltd. I wish to thank my fellow Board members for their wisdom and insight in guiding the Company to yet another commendable performance. I especially thank the Governor and the officials of CBSL and in particular the Director of the Department of Supervision of Non-Bank Institutions for the guidance and support extended at all times. I am grateful to our customers and shareholders for their continued patronage and loyalty.

S.H. PiyasiriChairman

27th May 2015

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

10

Chief Executive Officer’s Review Chief Executive Officer’s Review

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

11

Chief Executive Officer’s Review Chief Executive Officer’s Review

The strong operating results for 2014/15 reflect the collective actions of our employees to meet the high expectations of all our stakeholders.

2014 was a successful year for Kanrich Finance Ltd., in many respects. We have progressed considerably in terms of assets, profitability and corporate governance to reach the level of a leading financial company currently operating in Sri Lanka. Our collective efforts have enabled us to achieve these impressive results and at the same time positioned us well to produce overall stronger returns in the years to come.

Record Results Driven by Sound Strategy The strength of our business focused lending in microfinancing, as well as our client-driven strategy allowed us to outperform despite curtailed credit growth in the economy during the fiscal year. The strong operating

results for 2014/15 reflect the collective actions of our employees to meet the high expectations of all our stakeholders. In order to achieve these results, we accelerated our corporate plan to increase our monthly profits, strengthen the Balance Sheet and increase the efficiency of our operations. Within a short period of 9 months we successfully increased our core capital by Rs. 600 million and asset base by Rs. 4,038 million.

We achieved the highest level of lending targets in the history of our Company. Microfinance lending soared to Rs. 13.8 billion in the fiscal year 2015, compared to Rs. 5 billion the previous year. Accordingly, the monthly lending increased to Rs. 1 billion from under Rs. 0.4 billion a month. This escalated our interest income to Rs. 2,515 million, which was

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

12

Chief Executive Officer’s Review Chief Executive Officer’s Review

Rs. 1,296 million the previous year. As a result, total income increased from Rs. 1,441 million to Rs. 2,854 million in FY 2014/15 recording a growth of 98% year on year.

Our asset base swelled by 129% to Rs. 11.5 billion compared to Rs. 5.1 billion in 2013/14. Overall our net profit after tax increased by 3243 % to Rs. 487 million, compared to Rs. 14 million the previous year.

In addition, we are proud to be the first financial institute in Sri Lanka to securitise microfinance receivables. Accordingly, Rs. 1 billion was raised in debt through as issue of asset receivable backed trust certificates on our microfinance portfolio.

Our customer based crossed 250,000 whilst our staff strength increased to over 1,200 during the year. Our successful performance continued to gain recognition in various platforms in 2014. Kanrich Finance Ltd., was named the 'Best Microfinance Services Provider and the Fastest Growing and Emerging Finance Company in Sri Lanka - 2014' by the Global Banking and Finance Review - London.

Our Operations Our plan was to diversify our product offering by moving into conventional products such as hire purchase, leasing and pawning during the financial year in review. However, we continued to focus on our specialised area of microfinance lending as the economic milieu was not conducive for these products during the fiscal year.

Our asset base swelled by 129% to Rs. 11.5 billion compared to Rs. 5.1 billion in 2013/14. Overall our net profit after tax increased by 3,243% to Rs. 487 million, compared to Rs. 14 million the previous year.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

13

Chief Executive Officer’s Review Chief Executive Officer’s Review

In addition, our priority remained on meeting the consolidation targets of increasing our core capital level and the asset base as stipulated by the Central Bank of Sri Lanka. I am happy to state that our Non-Performing Levels (NPLs) remained below industry average, whilst our lending base grew substantially during the year. Over the past 3 years we have focused on growing our business-lending portfolio in contrast to consumer lending which has a higher tendency to increase the NPL levels. Due to the high turnover in microfinance facilities, we did not have a maturity mismatch in our cash flows as well.

We joined the Sri Lanka Interbank Payment System (SLIPS), which is a fund transfer system for the handling of interbank payments in Sri Lanka. With the new arrangement, we are able to offer an efficient fund transfer facility to a large number of our microfinance customers island-wide to obtain their loan disbursements in a timely manner.

In addition, we introduced a branchless banking solution over GPRS networks powered by ATSL TeleSoft, an Access Group Company. This has equipped us with a robust software solution and the GPRS network-based Point of Sale (POS) equipment to launch branchless banking solutions to our customers. As the first stage, our micro loan recoveries will be automated, providing a more efficient, reliable and accurate service to our micro loan clients numbering over 250,000. Going forward, we will facilitate the collection of other loan recoveries, bill payments at customer’s door-steps and finally

introduce the payments using clients’ credit cards using the POS facility. The solution provides the much needed easy access to financial services to small scale rural entrepreneurs who do not get convenient access to finance from the conventional banking system.

Since our concentration was on microfinance lending, we opened microfinance centres, instead of branches during the year. However, in the upcoming year we will be upgrading these centres to fully-fledged branches to complement our diversification strategy. In addition, we will move into the North as well.

We also strengthened our efforts to help the communities we serve. For instance, we deployed specialised resource personnel and conducted workshops for our customers in various industry segments to impart industry-related knowledge.

Strengthening Risk Management One of our primary responsibilities as a financial institution is to guarantee the safety and security of customers’ deposits and make payments with absolute confidence. Therefore, it is imperative to conduct our operations with integrity and respect at all times, and balance our risks to produce sustainable profitability. Whilst we have taken stringent measures to strengthen our risk management processes, we have been graded very high by the Central Bank of Sri Lanka on governance as well.

An Exemplary Team Only a strong team can drive excellent performance, especially in a challenging economic milieu. We remained deeply committed to the ongoing development of our team. They have energy and optimism and their passion and ingenuity are contagious. In fiscal 2014, we invested significantly in training and professional development to help ensure that our employees have the skills they need to serve our clients at the highest level. We also foster a culture that is open and transparent whilst the decision-making process is delegated down the hierarchy within the set framework.

Future Outlook Everyone at Kanrich Finance Ltd., is fully-committed to our strategy and targets. We are well on track and will continue relentlessly to implement our strategy and to deliver excellent performance in the years ahead. As we journey on, whilst diversifying our product offering through conventional products, we will continue to expand our microfinance and SME lending portfolio. Our focus would be on expanding the business-lending portfolio of our Company. We will also expand ‘Welanda Warama’ the new product launched for the SME sector. Business loans will be extended to the higher level customers in the SME segment as well. In addition, more funds will be allocated for employee training on leadership and risk management.

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

14

Chief Executive Officer’s Review ManagementDiscussion

and AnalysisAppreciations My appreciation is extended to the Chairman and the Board of Directors for their valuable insight and direction. I thank each and every one of our employees for their dedication and passion to the Company and for the support they have shown me through my career. I extend my appreciation to the Governor of the Central Bank of Sri Lanka and the Director and the officials of the Non-Banking Financial Institution Supervision Unit for their extremely valuable advice and guidance. I especially thank you, our shareholders, for your trust and support and appreciate the confidence and trust extended by our customers in our Company.

Shiran Weerasinghe Chief Executive Officer/Director

27th May 2015

We are well on track and will continue relentlessly to implement our strategy and to deliver excellent performance in the years ahead.

Kanrich Finance Ltd. Annual Report 2014/15

Chief Executive Officer’s Review ManagementDiscussion

and Analysis

21

16

OperationsReview

FinancialReview

Operating Environment

28

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

16

Operating Environment

Global Economy in Perspective

The global economy continued to struggle due to the disappointing out-turns, with developed countries still failing and trying to gain momentum and free themselves from the legacies left behind from the global financial crisis. In 2014, global growth was lower than initially expected, closing at 2.6% from last year's 2.5%, dubbing 2014 as a year of secular stagnation that continues to be convoluted due to numerous global problems that keep persevering. Russia's economic collapse, threat of deflation and another year of record low interest rates are primary reasons.

The low inflationary stance seen throughout the world is primarily due to the collapse in oil prices, which had much to do with the Russian economy

Management Discussion and Analysis Management Discussion and Analysis

Life’s Key Moments

Supporting...

contracting by 4% in 2015. It is this combination of low oil prices, the conflict in Ukraine and sanctions on the Russian Government prompting a dive in markets that figure prominently in Russia’s somewhat lacklustre performance.

Having performed very impressively, albeit somewhat artificially in the last few years to prop the global economy into a sense of slight stability, China is now undergoing a carefully managed slowdown. Other developing countries too showcased disappointing growth due to weak external demand, domestic policy tightening, political uncertainties and supply-side constraints.

Soft commodity prices, persistently low interest rates and increasingly divergent monetary policies across major economies, weak world trade and the sharp decline in oil prices are the factors that are currently driving

global outlook. It is these that will support global activity which is hoped to be seen in oil-importing developing economies, billed to take advantage of this milieu. However, on the converse, oil-exporting countries will undoubtedly be impacted negatively, while the oil-importing countries gain an advantage, which in the short to medium-term see regional repercussions emerging.

With the World Bank titling South Asia as the fastest growing region in the world, it is interesting that by end 2014, South Asia inclined 5.5% from a ten year low of 4.9% in 2013. It is India that became the champion for the region emerging with impressive growth post-two years of modest growth. Regional growth is expected to incline therefore 6.8% by 2017 due to a number of positives that are currently being instituted.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

17

Management Discussion and Analysis Management Discussion and Analysis

It is estimated by the World Bank that global growth will observe a moderate rise to 3% in 2015 and 3.3% by 2017. High-income countries will average 2.2% growth in the next three years, a marginal increase from 1.8% which will be the outlook for 2015, attributed primarily to gradually recovering labour markets, ebbing fiscal consolidation and continuing low financing costs. The features that stifled 2014 growth will ease with recovering strengthening in high-income countries and developing countries echoing the advantages with accelerated growth. Growth outlook therefore will see positive increases from the 4.4% posted in 2014 to 4.8% in 2015 and 5.4% by 2017.

The Sri Lankan Economy

Seen as one of the fastest growth economies among Asia's developing economies in recent years by the International Monetary Fund (IMF), Sri Lanka’s GDP grew by 7.4% during 2014, up slightly from 7.2% a year earlier. The country's economic performance was certainly better than expected despite currents

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

18

Sri Lanka's unemployment remains well below regional and global average speaking well for the progressive policies implemented to spur entrepreneurship, especially in the micro and SME sectors. Unemployment rate declined marginally due to increased employment opportunities, to 4.3% from 4.4%, due to labour productivity levels continuing to increase across all sectors of the economy. Core inflation remained at low levels throughout moving to 3.2% YoY, having taken advantage of the combination of prudent monetary management, moderation in international commodity prices, stable exchange rate and fiscal policy measures taken to address supply side volatilities.

Management Discussion and Analysis Management Discussion and Analysis

experienced from chronic market turbulence and climatic shocks. Sri Lanka’s short-term outlook appears broadly positive, as the country is well-positioned to benefit from the global economic recovery, and particularly, stronger growth in advanced economies.

It is to be noted however that Sri Lanka did not achieve the growth forecast of 7.8% for 2014, although compared to the region, the country did perform quite robustly. According to the Asian Development Bank, inflation fell markedly and the current account deficit narrowed. The election in January 2015 heralded a mandate for political and economic change, auguring well for investor confidence and growth prospects.

GDP expanded to Rs. 9,740,853 million compared to last year's Rs. 8,674,230 million with the continued high growth being driven by faster expansion in industry,

which offset substantially weaker growth in agriculture. This sector remains one of the three main pillars of the economy but performed disappointingly, slowing down to 0.3% from 4.7% last year. However, the industry sector inclined an impressive 11.4% compared to 9.9% last year, primarily attributed to fast expansion in construction and the apparel sector's impressive performance. The services sector moved upwards by 6.5%.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

19

Management Discussion and Analysis

Sri Lanka's impressive performance in global indices has added credence to its consistent growth pattern, billed to continue for the next few years at least and its ambition of achieving a GDP per capita income of US $ 4,000 by 2016. The country is the highest ranked in South Asia in the Global Prosperity Index, Ease of Doing Business Index and Economic Freedom Index, which positions it well on a stable path to progress, despite external macro challenges that could plague other economies.

Challenges will continue to emerge however, especially on the political front which thus far remains stable and augurs well for the political transition that will invariably happen in the coming year. The revised priorities of the new Government must be envisaged and trends focused on, as there is concern that political uncertainty could retard private

investment. Construction, which was led primarily by large Government led infrastructure projects is expected to slow after leading growth in recent years. Government consumption in the meanwhile is expected to increase with the shift seen in the budget towards recurrent expenditure and private consumption too will pick up with reductions in food and fuel.

The faster growth experienced in advanced economies will benefit export industries, including Sri Lanka's vibrant apparel and tourism sector. However, according to the Asian Development Bank, agriculture remains uncertain due to climatic changes impacting this sector quite negatively. Increases in Government-guaranteed prices for several agricultural products will boost production however. With the assumption of stability in the political arena and a rebound in investment, Sri Lanka's growth prospects are billed

at 7% for 2015 and 7.3% for 2016, well aligned with regional growth and certainly well above, global growth.

Overall Performance of the Non-Banking Financial Institution (NBFI) Sector

In the financial sector, the strengthened regulatory and supervisory framework, improved risk management capabilities and adequate buffers to mitigate risks, enabled financial institutions to remain resilient during the year. Momentum was moderately higher in the performance of the finance companies and specialised leasing companies which comprise the NBFI sector, posting improved performance. Continuous and consistent business strategies and a prudent financial recovery process begun in preceding years are now cascading positive tenets. As detailed in the Central Bank

Empowering...the Entrepreneurial Spirit

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

20

of Sri Lanka's Annual Report 2014, the performance of the financial sector was primarily led by the continuation of relaxed monetary policy and improved macroeconomic performance.

The financial sector consolidation programme continued throughout most of the year, envisaged to contribute positively in building a more resilient Licensed Finance Company (LFC) and Specialised Leasing Company (SLC) sector. The process has now been realigned with the current Government's economic policy, aimed at strengthening and sustaining the country's financial stability. The new direction will be conducted primarily in consultation with shareholders and stakeholders. It is expected that the capital and asset base will increase as a result of this process, enabling LFCs and SLCs to mobilise low cost, long-term funds. Accordingly, the plan envisaged is to reduce the number of non-banking financial institutions to around 20 from 58 with regulatory support and tax incentives. By end 2014, 10 mergers were completed and 22 were still on a states of work-in-progress. However, given the several concerns that have arisen, the programme has been temporarily halted pending the findings of the Consolidation Review Committee appointed by the new Government.

The LFC and SLC sector encompasses 7% of Sri Lanka’s financial system, comprising 48 LFCs and 8 SLCs. The sector expanded its branch network by 72 to now collate a total of 1,132. In the drive that began a few years ago to permeate the concept of financial inclusivity across the country, the concerted effort to reach the geographical locations beyond the Western Province therefore, saw a total of 44 accessible points opened inside and outside the Western Province.

Management Discussion and Analysis Management Discussion and Analysis

Asset growth moderated due to lower demand for credit, particularly during the early part of the year, but saw upward inclines thereafter. The lower interest rate scenario helped improve credit demand and maintain inclining non-performing loans at prudent levels. Mergers and acquisitions did assist in building resilience and improving the soundness of the sector. Strengthening risk management and building capacity of the sector to facilitate better absorption of risks was also focused upon, aligned with macroeconomic plans. Despite the dips and turns, the entire sector saw growth of 18.9% in its total asset base, growing to Rs. 853 billion compared to the growth of 20.3% experienced last year.

With interest rates in most segments declining to historically low levels in 2014, due to the relaxed monetary stance of the CBSL and high excess liquidity in the domestic money market, credit granted to the private sector contracted in the first eight months of 2014. This was due to the decline in pawning advances and increased access to alternative financing sources. But private sector credit did rebound during the latter part of 2014, finally taking advantage of the low interest rates, CBSL’s policy measures and contraction in pawning advances.

The 2013 impact of the high lending interest rates prevailing over most of that year and the fluctuations in gold prices permeated the pawning business considerably, permeating to increased Non-Performing Assets (NPA), which this year increased by 19.9% in 2014. NPAs now stand at Rs. 44.3 billion, higher than last year's Rs. 36.9 billion, symptomatic of the pervasive impacts of both these factors combined. However, it is to be noted that NPAs relative to the total outstanding loans increased only marginally to 6.9% from 6.7% last year. Taking into consideration the loan

provision, the net NPA ratio decreased marginally from 2.5% in 2013 to 2.3% this year, with total provision coverage increasing to 58.9% in 2014, compared to 56.1% in 2013.

Net interest income increased by 40.9% to Rs. 62.2 billion from Rs. 44.1 billion posted the previous year. The interest margin which is net interest income as a percentage of total assets of the sector also showcased an incline of 8%, compared to 6.6% last year. Overall statutory liquid assets available within the sector showed a surplus of Rs. 29.5 billion from the stipulated minimum requirement of Rs. 52.8 billion. The liquid assets to total assets ratio increased to 9.6% from 8% in 2013, directly attributed to the steady growth in deposits in relation to the moderate credit growth of the sector. Hence, liquid assets rose to Rs. 25 billion, similar to the increase of last year.

Profitability was sound as evidenced with the sector recording a profit after tax of Rs. 13.9 billion, compared to Rs. 7.7 billion in 2013, contributed mainly through increased net interest income. This is despite increased operational costs and provisioning requirements. Loan loss provision increased by Rs. 3.7 billion in 2014, when compared with the upward movement of Rs. 6.6 billion in 2013. ROA and ROE increased to 3% and 13.1% respectively, from 2.1% and 8.2% last year.

Internally generated funds contributed significantly to the increase seen in capital funds, which rose by 20.9% to Rs. 114 billion at the end of this year, compared to the 9.6% increase in 2013. Another significant positive for the sector was that it maintained its capital adequacy ratios well above the minimum requirements,

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

21

Management Discussion and Analysis Management Discussion and Analysis

although a decrease due to growth in risk-weighted assets was experienced. The total capital adequacy ratio (as a percentage of risk-weighted assets) decreased to 13.5% as at end of 2014 from 14.8% as at end of 2013. Core capital ratio (as a percentage of risk-weighted assets) also experienced declined by a marginal 13% compared to 13.5% last year. The ratio of capital funds to total deposits of LFCs also decreased marginally from 23.3% in 2013 to 22.9% this year.

National Development Gains Momentum

The country is on a concerted effort to imbibe entrepreneurship spirit into the national development agenda. Thus far, access to funding has been challenging for the micro and SME sectors, with funding entities positing a risk averse attitude and hence, growth in these sectors not achieving their full potential. Promoting market-based alternative financing rather than conventional bank-based financing to ensure adequate long-term financing is being promoted. While the banking sector has been the major source of financing for the SME and corporate sectors, raising funds for expansion in economic activity through capital markets has been limited to only large corporates. There is a need to have and support inclusive growth which can only be achieved if the potential of the SME sector is optimised.

The lack of access to financing, human resource and technological capabilities have been inherent constraints holding back the SME sector and remedial measures must be introduced to ensure availability of funds to this sector. Available credit guarantee schemes, credit advisory and counselling services as well as Business Development

Services, can play an imperative role in enhancing scope and facilitating the technical capabilities of SMEs. In addition, industrial clusters that will pool experiences, expertise and improve efficiencies will also be established. Upgrading the SME sector is vital to push the overall development strategy of the country, where a viable dynamic SME sector encompassing agriculture, industry and services can play a pivotal role in generating employment and income and alleviating poverty.

Operations Review

KFL Adds Prowess to Macro Picture

The year has certainly been a significant one for Kanrich Finance Ltd. This is a definite laurel for us given the intensely competitive environment we operate in and adds credence to the face that we achieved our financial targets. This is due to astute imperatives instituted through the years within our unique operational dynamic of relationships without borders. We are strong, stable and ready for a future that is undoubtedly driven by sound strategy and an extraordinary team that has taken ownership of our goals and vision.

In a nutshell, our financial performance has been commendable, primarily due to our pragmatic outlook in accelerating our corporate plan, which was designed to increase monthly profits, strengthen the balance sheet and increase efficiency and productivity. This resulted in achieving lending targets at the highest level in our entire history, increasing our core capital by Rs. 710 million and asset base of by Rs. 6,507 million. NPAT spiralled upwards to Rs. 487 million from

Rs. 14 million last year, which is a noteworthy growth of 3,243%. The emphasis we employed in developing our microfinance business saw extraordinary results with lending to this sector posted at an impressive 11.5 billion, impressive primarily due to this figure being just Rs. 5 billion last year. This also pushed monthly lending in excess of Rs. 1 billion.

The fact that we are the first financial institution in Sri Lanka to securitise microfinance receivables and to be named Best Micro Finance Services Provider and the Fastest Growing and Emerging Finance Company in Sri Lanka 2014 by Global Banking and Finance Review London are all crowns we don proudly. These remain evidence of our progressive stance in the NBFI sector in Sri Lanka.

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

22

With microfinance being a strategic element in our business plan, Kanrich Finance Ltd., began infusing the dynamics within that plan to build our microfinance business. We began the initial step of launching microfinance centres, which in the next year will see these centres upgraded to fully-fledged branches, covering the North of the country as well, where we see immense potential for this segment of business.

Technology was also optimised within our operations as an imperative tool to aid small scale entrepreneurs gain added convenience for access to finance. We have now introduced branchless banking using GPRS networks, based POS equipment via a robust software solution. Micro loan recovery will be automated with collection of loans, bill payments at a location of a customer's choice and credit cards using POS as well as adding the payment of utility bills in the field via POS machines, will be added into the solution very soon.

Given our emphasis on relationships without borders, we strengthened our relationships with our stakeholders. One of these initiatives was in deploying team members and resource persons to conduct workshops for customers who operate in diverse industries, imparting specialist and expert knowledge and tools in these varied industries. This is an initiative that adds immense value to our efforts of encompassing an expansive customer portfolio, from high-end corporates to SMEs and micro enterprises, as well as customers permeating the entire income spectrum, high to low-end. By astutely adding to our product portfolio, we will have a diversified portfolio of products

that will be able to compete more competitively with a better product mix. Customer service excellence remains vital to the growth of our business and we will be embarking on the pragmatic feature of restructuring the customer care unit to better reflect customer expectations and aspiration. To gain better analysis of these expectations, periodic customer satisfaction surveys will be conducted and the feedback acted upon accordingly.

In our bid to achieve the status of being among the first five finance companies in the NBFI sector in Sri Lanka within the next financial year, we have been extremely cognisant on building a solid financial base for us to grow sustainably. By February 2015, we posted an impressive asset base of Rs. 10 billion, an increase of over 236% compared three years ago, which unequivocally showcases outstanding performance and the fastest growth in the history of Kanrich Finance Ltd. The short-term will prompt us to increase our Tier II capital with a debenture issue to maintain our capital adequacy.

Our initiatives of launching branchless banking and mobile banking will gain further momentum with the agreement signed with ATSL TeleSoft for the branchless banking solution. This GPRS network based Point of Sales system will be the tool in automating our microfinance operations and augmenting our future pathway in this area of business. In adding further value added services to our customers, the launch of our SME loan product, Welanda Warama has been extremely successful. We also launched business loans, gold loans and have begun aggressively expanding leasing operations and

purview have added to maximising the accessibility of our portfolio of products and services to our customers. This accessibility will also include the launch of more fully-fledged branches in strategic locations in order to ensure our presence will have the maximum impact to our stakeholders.

We are constantly improving the bar of convenience, flexibility and innovation, which we believe we will add the newer dimension of being a preferred employer within this industry. The ambitious expansion strategy we have planned in the immediate, will also mean that our team must reflect these futuristic goals and be equipped with knowledge, skill and tools to achieve these goals. Our team will also be presented with rewards, benefits and remuneration that are well above industry norms, including housing, vehicle and educational loans at low interest rates, medical insurance including accident cover, while training and development will continue being a priority. We will be adding professionals and experts into our team, while also bringing in a young group of trainees who will be trained and developed to take ownership for our vision and etch the Company into the annals of the NBFI sector indelibly. Employee Satisfaction Surveys will form an integral foundation to the plans we have for our team.

There is also a dire need for the Company to look inwards, infuse effective cost management strategies and work on strategic initiatives that would create a lean organisation that is well aligned to evolutionary paradigms emerging within the industry locally and globally.

Management Discussion and Analysis Management Discussion and Analysis

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

23

This therefore would encourage the decrease of unnecessary costs and increase low interest funds including securitised loans, which we believe will be a prudent stance. We will be pursuing foreign funding opportunities and new credit lines to expand our funding potential.

Customer Service

Customer service excellence remains vital to the growth of our business and we will be embarking on the pragmatic feature of restructuring the customer care unit to better reflect customer expectations and aspiration. To gain better analysis of these expectations, periodic customer satisfaction surveys were conducted and the feedback acted upon accordingly.

As customers have grown accustomed to personalised solutions in other industries, the demand has begun to receive the same attention from their financial services providers. With all the innovation that is ongoing in other sectors, KFL too, always tries to implement new strategies that offer more convenience to customers. Products such as our GPRS network based Point of Sales (POS) system will be the tool in automating our microfinance operations and augmenting our future pathway in this area of business.

This accessibility will also include the launch of more fully-fledged branches in strategic locations in order to ensure our presence will have the maximum impact with our stakeholders.

Branding

To remain as a trusted partner in the hearts and minds of all our stakeholders, it is necessary that we sponsor useful events whilst also engaging in community development projects with a broader scope.

And we strongly believe in Below The Line (BTL) communication methods in order to sustain in widespread customer base which is more than 5% of Sri Lankan population. Positive word of mouth endorsements also make our KANRICH brand across Sri Lanka in a very affirmative influence to be a finance brand in Sri Lankan finance context. Apart from that, we also do media conferences and press releases about KFL’s achievements and CSR events in order to remain in the minds of our stakeholders.

Technology

KFL is very proud to say that we have strong IT literate human resources as we have implemented our very own IT system which is handling all KFL integrated transactions.

Micro loan recovery will be automated with collection of loans, bill payments at a location of a customer's choice and credit cards using POS as well as adding the payment of utility bills in the field via POS machines, will be added into the solution very soon. We also joined SLIPS, the Sri Lanka Interbank Payment System, which enables an efficient fund transfer

facility and is certainly a boon to our microfinance customers, as they can now facilitate loan disbursements much faster. Given the crucial role played by IT in the future of finance the world over, we intend improving our IT system aggressively to support the expansion of our product portfolio for increased efficiency, productivity and better information management encompassing an expansive customer portfolio, from high-end corporate to SMEs and micro enterprises, as well as customers permeating the entire income spectrum, high to low-end. By astute, we are planning on developing mobile banking system and more door step solutions with the help of IT developments in KFL's near future.

Corporate Social Responsibility (CSR)

Giving Total Financial solutions for our customers is our business. Beyond financial responsibilities, KFL has chartered new territories by identifying needs and providing just the right kind of service when required. The KFL Social Responsibility Trust, founded for this purpose, has reached out to the core to uplift creatively, socially, culturally and ethically in an outstanding manner.

Our diversified approaches to social responsibility positions our interventions at many levels with microfinance, as mentioned above, being the driving sustainability platform in our social responsibility dynamic.

Management Discussion and Analysis

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

Combining...Value Addition with Familial Aspirations

KFL CSR philosophy is linked with our Microfinance Strategy and through our Microfinance services, we provide many CSR strategies. We provide financial services, training and leadership programs focusing on empowering women. After three decades of war now over, Sri Lanka is moving forward with an emerging economy in every sector. This has given KFL great opportunities in the Microfinance industry. KFL expanded Microfinance projects with a scientific approach where Loans are granted only to women borrowers. Now the programme maintains a 99% recovery rate with every loan covered by loan protection insurance.

The new approach focuses on women where they undergo three weeks of training regarding the development of a new business and then loans are granted to fund the new venture. This creates an opportunity to empower women to earn an income. This unique approach makes a huge impact on our society where more women participate to contribute to the GDP. Highly experienced and trained KFL staff are working on developing their business with them with weekly visits educating customers with various issues like marketing their product and the economics changes.

We also develop rural leadership programs as a CSR initiative. In the micro model, we create groups in the villages with a group leader. We carry out train the trainer, programme with the leaders being trained first who in turn will train their own members in the village. The Company provides this as a charity service, with technical support from the Central Bank.

The importance of a healthy nation to drive national development, remains at the forefront of our sustainability focus, into which the annual blood donation is a firm contributor. Two highly successful campaigns were organised this year in Anuradhapura and Ratnapura.

Management Discussion and Analysis Management Discussion and Analysis

24

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

As discussed above, given our emphasis on relationships without borders, we strengthened our relationships with our stakeholders. One of these initiatives was in deploying team members and resource persons to conduct workshops for customers who operate in diverse industries, imparting specialist and expert knowledge and tools in these varied industries. This was an initiative that added immense value to our efforts of encompassing an expansive customer portfolio,

Management Discussion and Analysis

25

from high end corporates to SMEs and microenterprises, as well as customers permeating the entire income spectrum, high to low end. By astutely adding to our product portfolio, we will have a diversified portfolio of products that will be able to compete more competitively with a better product mix.

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

26

Management Discussion and Analysis

Future Outlook

We will be adding professionals and experts into our team, while also bringing in a young group of trainees who will be trained and developed to take ownership for our vision and etch the Company into the annals of the NBFI sector indelibly. Employee Satisfaction is also a dire need for the Company to look inwards, infuse effective cost management strategies and work on strategic initiatives that would create a lean organisation that is well aligned to evolutionary paradigms emerging within the industry locally and globally.

Management Discussion and Analysis

This therefore would encourage the decrease of unnecessary costs and increase low interest funds including securitised loans, which we believe will be a prudent stance. We will be pursuing foreign funding opportunities and new credit lines to expand our funding potential. Surveys will form an integral foundation to the plans we have for our team.

We are also planning to launch business loans, gold loans and have begun aggressively expanding leasing operations. Expanding our savings account purview and maximising the accessibility of our

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

27

Welcoming...Young Stakeholder

Management Discussion and Analysis

enter a new era. Each of our team remains fully committed to achieving our vision, delivering performance excellence well beyond expected boundaries. The diversification of our products and services are well aligned to the evolutionary milieu expected in the next few years, where we believe that microfinance will drive economic development and the SME sector will be the standard bearer in pushing growth into higher realms. To achieve

all this however, we know that the secret to our formula of success is, 'Relationships without borders', and this is the tenet we will continue to maintain as the overarching principle in building a sustainable business.

portfolio of products and services to our customers are also in-line for one future. This accessibility will also include the launch of more fully-fledged branches in strategic locations in order to ensure our presence will have the maximum impact with our stakeholders.

As we have been crowned with some very impressive laurels this year, we are now paving the way for us to

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

28

Management Discussion and Analysis Management Discussion and Analysis

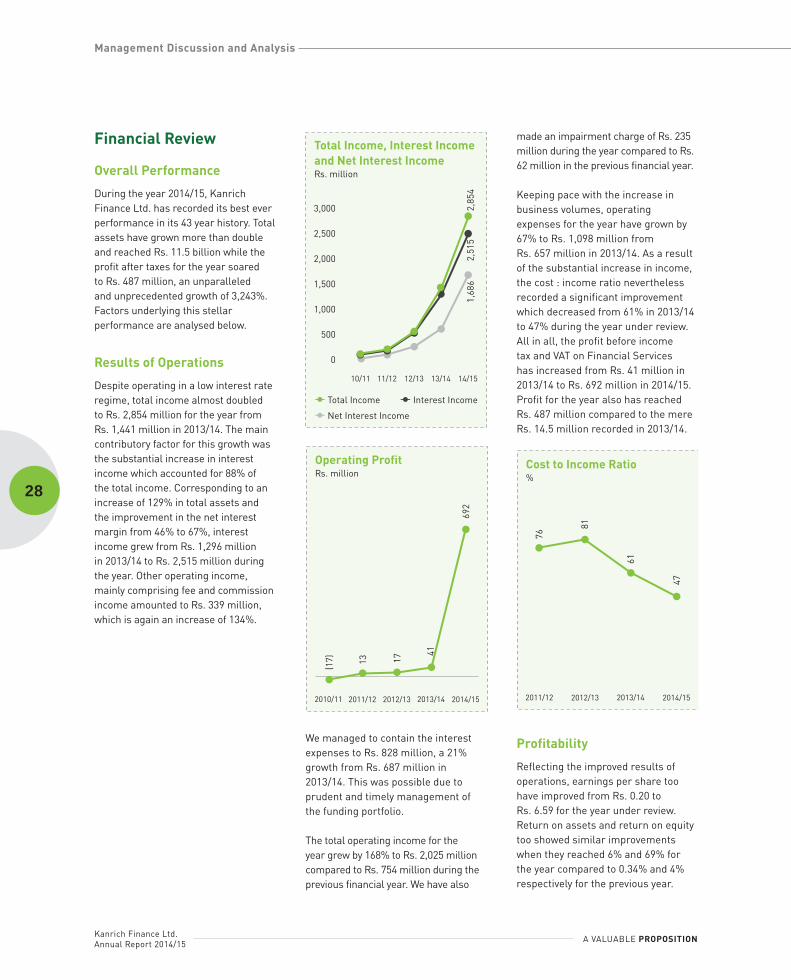

Financial Review

Overall Performance

During the year 2014/15, Kanrich Finance Ltd. has recorded its best ever performance in its 43 year history. Total assets have grown more than double and reached Rs. 11.5 billion while the profit after taxes for the year soared to Rs. 487 million, an unparalleled and unprecedented growth of 3,243%. Factors underlying this stellar performance are analysed below.

Results of Operations

Despite operating in a low interest rate regime, total income almost doubled to Rs. 2,854 million for the year from Rs. 1,441 million in 2013/14. The main contributory factor for this growth was the substantial increase in interest income which accounted for 88% of the total income. Corresponding to an increase of 129% in total assets and the improvement in the net interest margin from 46% to 67%, interest income grew from Rs. 1,296 million in 2013/14 to Rs. 2,515 million during the year. Other operating income, mainly comprising fee and commission income amounted to Rs. 339 million, which is again an increase of 134%.

Total Income, Interest Income

and Net Interest IncomeRs. million

11/12 14/1513/1412/1310/11

3,000

2,000

1,500

2,500

500

1,000

0

Net Interest Income

2,8

54

1,6

86

2,5

15

Total Income Interest Income

2013/142012/132011/122010/11 2014/15

Operating ProfitRs. million

(17

)

13 17 4

1

69

2

We managed to contain the interest expenses to Rs. 828 million, a 21% growth from Rs. 687 million in 2013/14. This was possible due to prudent and timely management of the funding portfolio.

The total operating income for the year grew by 168% to Rs. 2,025 million compared to Rs. 754 million during the previous financial year. We have also

made an impairment charge of Rs. 235 million during the year compared to Rs. 62 million in the previous financial year.

Keeping pace with the increase in business volumes, operating expenses for the year have grown by 67% to Rs. 1,098 million from Rs. 657 million in 2013/14. As a result of the substantial increase in income, the cost : income ratio nevertheless recorded a significant improvement which decreased from 61% in 2013/14 to 47% during the year under review. All in all, the profit before income tax and VAT on Financial Services has increased from Rs. 41 million in 2013/14 to Rs. 692 million in 2014/15. Profit for the year also has reached Rs. 487 million compared to the mere Rs. 14.5 million recorded in 2013/14.

2013/142012/132011/12 2014/15

Cost to Income Ratio%

76

81

61

47

Profitability

Reflecting the improved results of operations, earnings per share too have improved from Rs. 0.20 to Rs. 6.59 for the year under review. Return on assets and return on equity too showed similar improvements when they reached 6% and 69% for the year compared to 0.34% and 4% respectively for the previous year.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

29

Management Discussion and Analysis

2013/142012/132011/12 2014/15

Return on Equity%

06

05

04

69

5.8

7

2013/142012/132011/12 2014/15

Return on Assets%

0.9

4

0.6

4

0.3

4

Financial Position

Total assets of the Company as at 31st March 2015 reached Rs. 11,557 million compared to Rs. 5,050 million as at 31st March 2014, an unprecedented 129% growth. The net loans and advances portfolio has grown from Rs. 3,882 million to

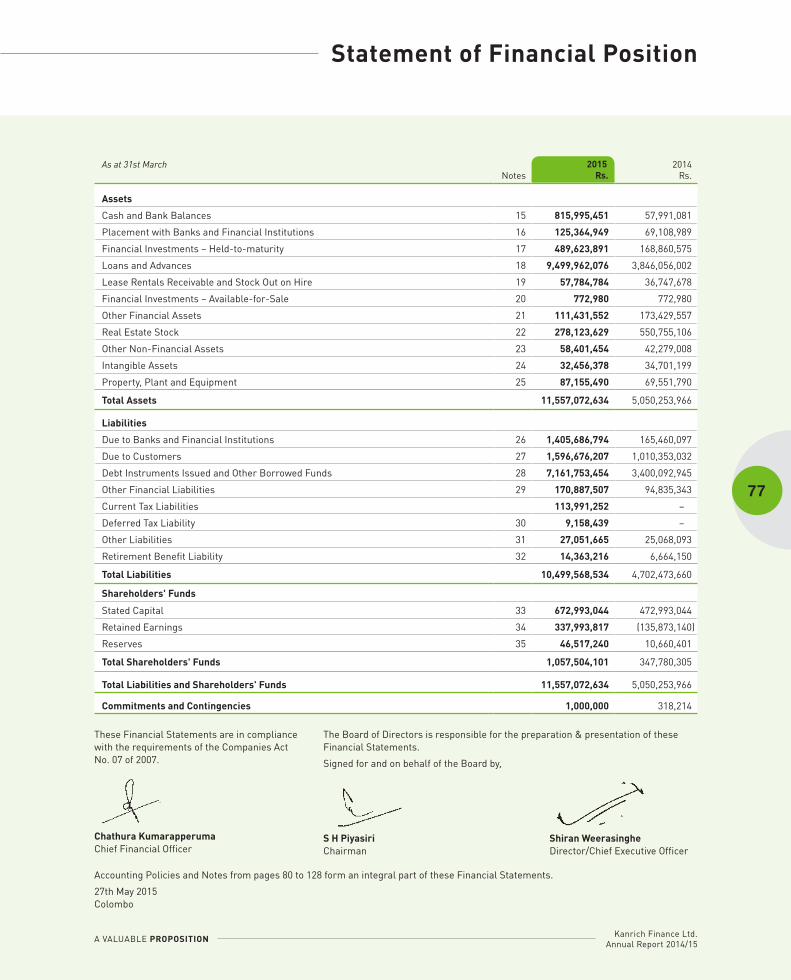

Rs. 9,557 million during the year which constituted 82% of the total assets and it has been the single biggest contributor for this overwhelming asset growth. Within the gross loans and advances portfolio, Rs. 9,789 million and Rs. 3,924 million recorded significant growth of 149% compared to the previous year. Reflecting the overall market trend, the non-performing loans and advances portfolio increased from Rs. 112 million as at 31st March 2014 to Rs. 338 million as at the current year end, causing asset quality to somewhat deteriorate. This of course led to the gross NPL ratio to rise to 3.45% from 2.86% as of previous year end. With the enhanced impairment provisioning, net NPL ratio however remained, when compared to as at 31st March 2014. Other assets that recorded significant growth included placement with bank and financial institution, cash and bank balances from Rs. 127 million to Rs. 941 million and financial investments – held-to-maturity from Rs. 168 million to Rs. 489 million.

09/10 11/1210/11 12/13 13/14 14/15

89

0

1,0

72

1,7

42

5,0

50

3,4

34

11

,55

7

Rs. million

Asset Base

Lending Portfolio

2010/11 2011/12 2012/13 2013/14 2014/15

21

5 69

1

2,2

53

3,8

83

9,5

58

Rs. million

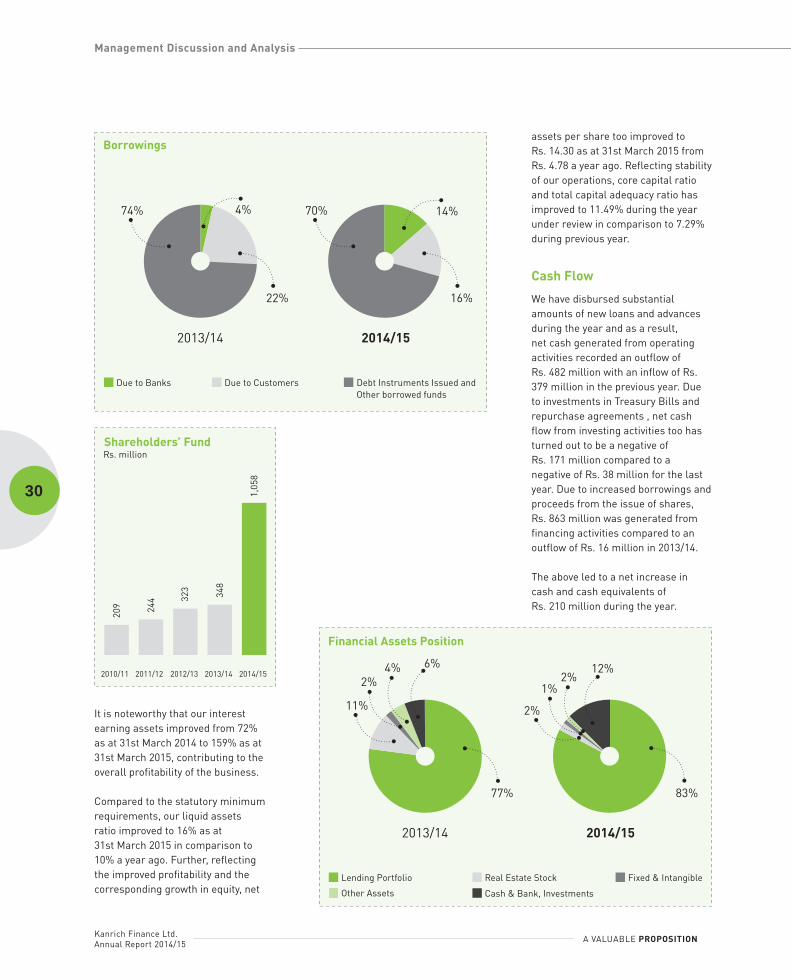

The growth in asset base was primarily funded through debt instruments issued/other borrowed funds and due to banks and financial institutions which recorded increases from Rs. 3,400 million and Rs. 165 million to Rs. 7,161 million and Rs. 1,405 million respectively as at 31st March 2015. Deposits from customers too have increased from Rs. 1,010 million to Rs. 1,597 million. Reflecting the improved profitability and new funds infused through the issue of shares, total equity has increased from Rs. 347 million to Rs. 1,057 million as at 31st March 2015.

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

30

Sustainability Report

Management Discussion and Analysis

74%

22%

Due to Banks Due to Customers

2013/14 2014/15

Borrowings

Debt Instruments Issued and

Other borrowed funds

4% 70%

16%

14%

2010/11 2011/12 2012/13 2013/14 2014/15

20

9 24

4 32

3

34

8

1,0

58

Rs. million

Shareholders’ Fund

It is noteworthy that our interest earning assets improved from 72% as at 31st March 2014 to 159% as at 31st March 2015, contributing to the overall profitability of the business.

Compared to the statutory minimum requirements, our liquid assets ratio improved to 16% as at 31st March 2015 in comparison to 10% a year ago. Further, reflecting the improved profitability and the corresponding growth in equity, net

assets per share too improved to Rs. 14.30 as at 31st March 2015 from Rs. 4.78 a year ago. Reflecting stability of our operations, core capital ratio and total capital adequacy ratio has improved to 11.49% during the year under review in comparison to 7.29% during previous year.

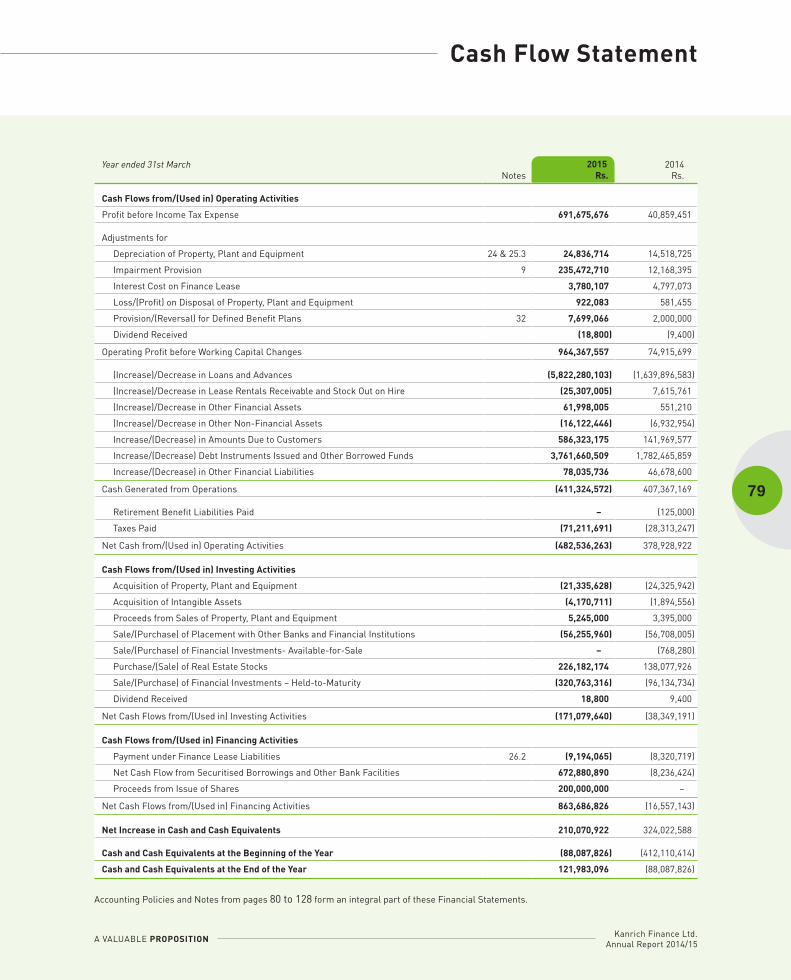

Cash Flow

We have disbursed substantial amounts of new loans and advances during the year and as a result, net cash generated from operating activities recorded an outflow of Rs. 482 million with an inflow of Rs. 379 million in the previous year. Due to investments in Treasury Bills and repurchase agreements , net cash flow from investing activities too has turned out to be a negative of Rs. 171 million compared to a negative of Rs. 38 million for the last year. Due to increased borrowings and proceeds from the issue of shares, Rs. 863 million was generated from financing activities compared to an outflow of Rs. 16 million in 2013/14.

The above led to a net increase in cash and cash equivalents of Rs. 210 million during the year.

Fixed & Intangible

Cash & Bank, InvestmentsOther Assets

Financial Assets Position

11% 2%

2%1%

4%2%

6% 12%

77% 83%

Lending Portfolio Real Estate Stock

2013/14 2014/15

Kanrich Finance Ltd. Annual Report 2014/15

Sustainability Report

37

37

38

32

34

35

Suppliers

Government

Future Outlook

The Kanrich Sustainability

Philosophy

Employees

Community and Environment

3232

33

Stakeholder Engagement

Investors

Customers

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

32

Sustainability Report Sustainability Report

Reporting on sustainability initiatives is a practice that enables us to look inwards at ourselves, make the necessary changes, bridge the gaps that will enable us to propel our performance to the next realm and take advantage of the opportunities that emerge in a constantly evolving landscape. Sustainability to us is all about empowering our stakeholders, but it's an empowerment that is brought about by focusing on the decisions we make and the impacts that our decisions have on them. We strive to create a milieu where we forge and nurture long-term relationships with our stakeholders, which also spotlights our responsibility towards the environment.

This sustainability report highlights the work we do with our stakeholders, the issues we engage with and the results that have emerged from this engagement. We have striven to quantify and qualify our actions, highlighting areas that need improvements and strengthening the areas that have shown results and have potential. At KFL, sustainability is a way of life and as you read through this report, you will gain some insight into the way we do business, the rich relationships we have with our stakeholders and the responsible consciousness we espouse in everything we do.

The Kanrich Sustainability PhilosophyOur name is derived from our roots, encased in a language that has existed for over three millennia. And it is this name that remains the quintessence of our sustainability philosophy. The word Kanrich has its genesis in the Sinhala language and means mutual wish or the agreement of a group. This truly embodies our philosophy of collaborated decision-making for the mutual

benefit of each of our stakeholders. This is further augmented in our ethos of 'Relationships without borders', where we develop and innovate financial solutions constructed on a platform of responsibility, accountability and absolute sustainability.

Stakeholder EngagementStakeholder engagement is a crucial truss to sustainable development as it is this engagement process that prompts the two-way dialogue and communication process which eventually, aligns the strong relationships among our stakeholders and forms the foundation to our sustainability journey. We are extremely committed to be engaged in all of our stakeholders, both internally and externally, to become the most sustainable, responsible company we can possibly make. By listening to, partnering with and considering the perspectives of our associates, customers, shareholders, academic leaders, Government and valued business partners, we can truly ensure that quantifiable and qualitative returns are assured.

Having identified our stakeholder groups, as discussed further in this Report also, we engage with them at various forums related to their interests and expectations, in an effort to adapt to changing needs and issues, which continue to evolve. As we pursue our corporate sustainability goals, we intend to further strengthen these relationships. Together, we are establishing transparency and enhancing our relevancy with the customers and communities we serve.

We have created more formal channels for interacting with stakeholders both to learn from their expertise and to provide a forum for them to give us their feedback.

InvestorsAs a player in the financial landscape, one of our primary objectives is to create value for the investors and enhance wealth through superior earnings in terms of their investment. As business operations have been restructured for better productivity and our tireless efforts have already brought us consistent financial performance in the recent past.

Growth Summary%

2013/14 2014/152012/13

9.0

6.0

4.5

7.5

1.5

3.0

1,800

1,200

900

1,500

300

600

00

Rs.

Earnings per Share (Rs.)

Profit Growth (%)

Asset Base Growth (%)

Our business strategies are aligned to create shareholder wealth growth by embracing economic, social and environmental aspects. Accordingly, we build and maintain a close relationships with our stakeholders and also deliver a sound return through a well qualified Board. Our continuous innovation and product development enhance final value of our products and keep us ahead of competition, thus securing our stakeholders trust in the Board and the Company’s Management.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

33

Sustainability Report Sustainability Report

KFL publishes and issues a comprehensive Annual Report and holds an Annual General Meeting (AGM), Extraordinary General Meetings (EGM) in-line with the Companies Act, annually and as and when necessary. These provide ample opportunities for stakeholders to interact with the Board and obtain their invaluable feedback. The Company is committed to conduct periodic, individualised mailings and conference calls between senior management and investors and/or analysts when necessary. Our corporate website is being updated continually in order to provide extensive information on Company and financial statistics. We publish Interim Financial Statements quarterly and conduct press conferences and media releases regarding new products, branch opening and achievements continuously, which are helpful to our investors.

CustomersThe customer base of KFL comprises both depositors as well as borrowers. Each deposit customer is treated as a premier customer and is assigned to a staff member in order to provide a better service. Further, special privileges are provided to the senior citizens by maintaining a strong relationship and providing door step service.

KFL serves more than 250,000 micro customers across the country. Most of them are in the segment that is not served by competitive banking and finance companies. The mission of KFL in providing micro loan facilities is to uplift the lives of the community and it was a success throughout the period by reaching the aforementioned number of households. The strong relationship has been built by meeting them on a weekly basis which make them comfortable and further strengthen the bond.

Book donation conducted by the Horana branch.

Mass Medical campaign arranged at Anuradhapura serving more than 7,500 people.

Kanrich Sasunata Diriyak

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

34

Training programmes are organised by KFL to enhance knowledge and skills of customers with the proposition of development of their earning potentials. Further, KFL open up opportunities to the community by creating a new market to sell their products and services by participating in numerous events organised by the Company.

'Welanda Waramma', the product solution for the SME sector negates the hindrance of growth of the sector. The convenient and door step service enable the customer to focus more on the business thereby.

Use of state-of-the-art technology enables more efficient service to rural communities. KFL implemented POS system for field officers and new services to clientele are yet to be implemented.

EmployeesThe human resource base exceeding 1,200 is a key competitive asset for KFL. The Company is strongly built on relationship between its employees. Young and dynamic, our team is a professional one that understands the evolutionary concept of operating in challenging paradigms. Our approach to developing our team begins even before recruitment, where we headhunt or look for team members who will complement our forward journey and our commitment to the tenets of sustainable development. This focus on gaining commitment and ownership is a trait that lies inherent in our team. Given that, at recruitment, we focus on attracting the right talent and retaining it, honing personal aptitudes and providing guided career progression.

Sustainability Report Sustainability Report

Dansala Organised by head office staff on Vesak Poya Day.

A valuable contribution given to Dalada Maligawa for the Esala Perahera from the Kandy Branch.

KFL Pirith ceremony.

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

35

Age Analysis of Employees

Below 20 20 - 30

31 - 40 41 - 50

51 - 71

21%1%

1% 2%

75%

KFL is an equal opportunity employer and we provide employment not only on the basis of qualifications but also based on experience. The Company culture promotes comprehensiveness and team spirit among all employees.

With reference to the above graph, since we have a young team with a good spirit, the Company continue to invest in strengthening its human capital base to face intensifying competition and to sustain future growth plans throughout the year. There are growth opportunities for employees in our Company since we have a flat structure consisting 7 Strategic Business Units which are operated as separate units. This gives very competitive opportunities for employees to groom within the Company. Also we practice an ‘open-door ‘policy so that any employee at KFL can easily reach the management.

The Company policies and procedures are very well-communicated from top to bottom. There is transparency and all employees at KFL are very much

secured with their jobs. In addition, KFL believes strongly that rewards and remuneration remains an intrinsic feature in nurturing a contented team. Therefore, wage ranges are also very attractive when compared to competitors. The staff are benefited by incentives, performance-based bonuses, annual increments, festival advances and allowances.

Most of the employees of the Company are from rural areas and majority of them are attached to the microfinance sector of the Company. As a company with the ambition of upgrading rural life, it is a privilege for us to develop their carrier. Low employee turnover has proved that KFL is a great place to work at.

Training and Development

Our team gains extensive training from recruitment, ensuring their transition seamlessly into our collaborative yet competitive work environment. Training is provided in key areas of technical knowledge, practical experience, personal development and career development, enabling our team to excel in mindset and action, while ensuring that a positive work/life balance is maintained throughout their working careers.

Some of the trainings we provided during the year are, Modern Office Management for Work Life Productivity, Customer Service, Laws, Regulating Mergers and Acquisitions of Finance Companies, Employee Misconduct and Preliminary Investigation, Managing Time or Planning Work, Employee Motivation, Social Media and Marketing and Franklin Covey's Leadership; Great Leaders, Great Teams, Great Results, etc.

Welfare

KFL believes its key success factor is its employees. Hence the Company ensures that its people develop to their utmost and invests in continuous enhancement of skills, knowledge and expertise to drive the Company towards excellence. Therefore we always look forward to retain them by enhancing staff welfare by providing a good medical scheme, accident cover for field staff, subscriptions for professional associations and staff loans.

The Company helps employees by giving cash payment in an event of child birth, wedding or funeral, offered by welfare. We have given gym facilities to staff in order to keep them physically fit. Our team is constantly engaged in initiatives that would harness their team spirit and instil camaraderie.

From celebrating religious festivals akin to Christmas carols and Pirith ceremonies, to KFL Night, which is the annual get-together for teams and their families, where one thousand KFL families unite to enjoy music, fun and games and the Sports Day, showcasing the sporting prowess of our team.

Community and EnvironmentOur multifold approach to social responsibility positions our interventions at many levels with microfinance, as mentioned above, being the driving sustainability platform in our social responsibility dynamic. Reaching more than 250,000 families through our microfinancing and development programmes, the accessibility to funding has been a keen feature in empowering communities, who now have thriving livelihoods and are maximising their potential. KFL caters to more than 5% of the Sri Lanka population through microfinance.

Sustainability Report

Kanrich Finance Ltd. Annual Report 2014/15 A VALUABLE PROPOSITION

36

Sustainability Report

Microfinance is promoted as an entry point in the context of a wider strategy for women’s economic and sociopolitical empowerment. women’s access to savings and credit gives them a greater economic role in decision-making. When women control decisions regarding credit and savings, they optimise their own and the household’s welfare. Investments in women’s economic activities will improve employment opportunities for women and KFL has identified the value of women empowerment through microfinance engagements in most of the rural communities in Sri Lanka.

KFL has implemented continuous development plans to enhance the combination of women’s increased economic activity and control over income, by providing access to microfinance which would improve their skills, mobility, access to knowledge and support networks by conducting weekly meetings.

Believing strongly in gender equality and women’s empowerment, the entrepreneurial spirit of women was promoted through a series of highly successful workshops for women in Ratnapura, Thambuththegama and Anuradhapura areas.

Through “Micro-Finance” and “Welanda Warama” products we are catering to small and medium enterprises as well as entrepreneurs which is the backbone of the Sri Lankan economy to climb up with success stories in a competitive business world. This will be a great impact to creation of indirect and direct employment in the Sri Lankan communities. The value created will directly impact the GDP growth in Sri Lanka.

Road signboards are given to a Number of Police Stations as a part of the Corporate Social Responsibility initiative.

KFL Night 2014.

Sustainability Report

Kanrich Finance Ltd. Annual Report 2014/15A VALUABLE PROPOSITION

37

KFL has conducted drought relief campaigns in the North-Central Province to help affected residents in the area by conducting medical campaigns and distributing dry rations.

Also, in a bid to create an enabling environment through education, we implemented a book donation campaign and built libraries for the communities in Thambuththegama, Ratnapura, Horana and identified rural communities within the country.