Embed Size (px)

Citation preview

1

A100 Introduction to Auditing and Deloitte Audit Approach.

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Objectives – Session 1

You will be able to:

• Describe what an audit is and its elements.

• Describe why an audit is performed.

• Describe the key principles and purpose of an audit.

• Describe why an auditor should be independent of an entity when conducting an audit.

• Describe and identify how the financial statement audit is governed by the Deloitte Audit Approach.

1 A100 Introduction to Auditing and Deloitte Audit Approach

2

©2012 Deloitte Touche Tohmatsu. All rights reserved.

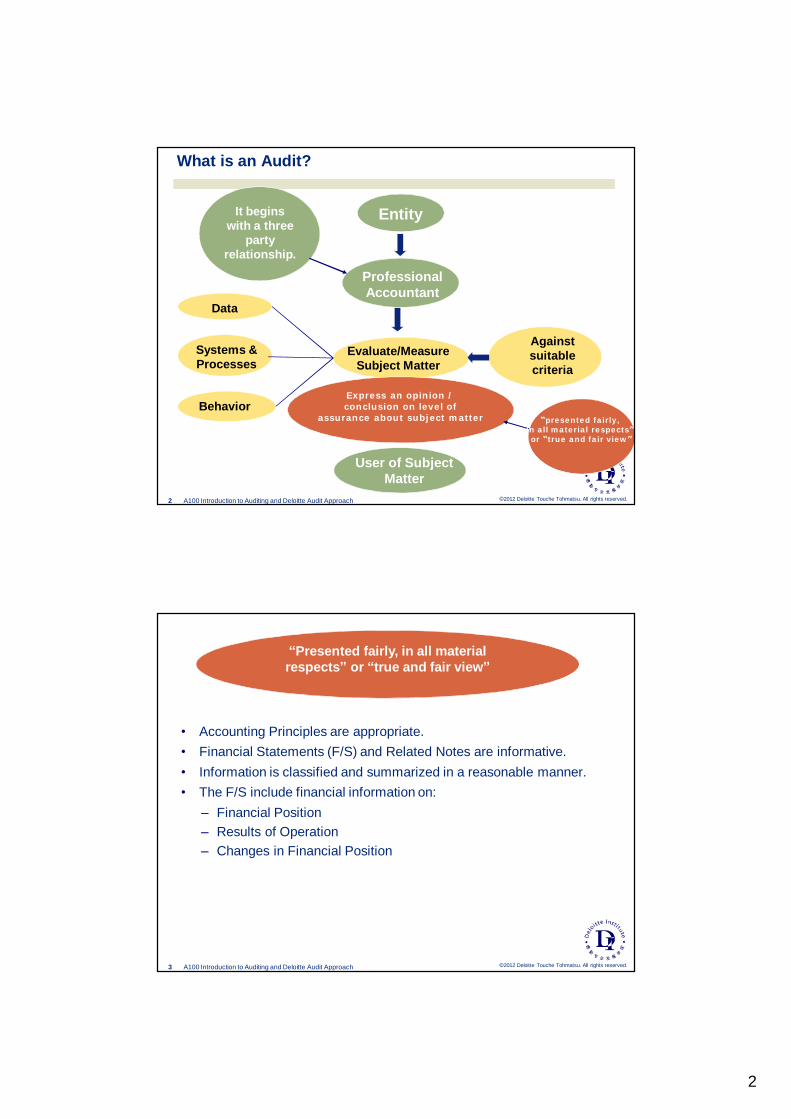

What is an Audit?

Entity

Professional Accountant

User of Subject Matter

It begins with a three

party relationship.

2 A100 Introduction to Auditing and Deloitte Audit Approach

Systems & Processes

Data

Behavior

Evaluate/Measure Subject Matter

Against suitable criteria

Express an opinion /conclusion on level of

assurance about subject matter “presented fairly, in all material respects” or “true and fair view”

©2012 Deloitte Touche Tohmatsu. All rights reserved.

“Presented fairly, in all material respects” or “true and fair view”

• Accounting Principles are appropriate.• Financial Statements (F/S) and Related Notes are informative.• Information is classified and summarized in a reasonable manner.• The F/S include financial information on:

– Financial Position– Results of Operation– Changes in Financial Position

3 A100 Introduction to Auditing and Deloitte Audit Approach

3

©2012 Deloitte Touche Tohmatsu. All rights reserved.

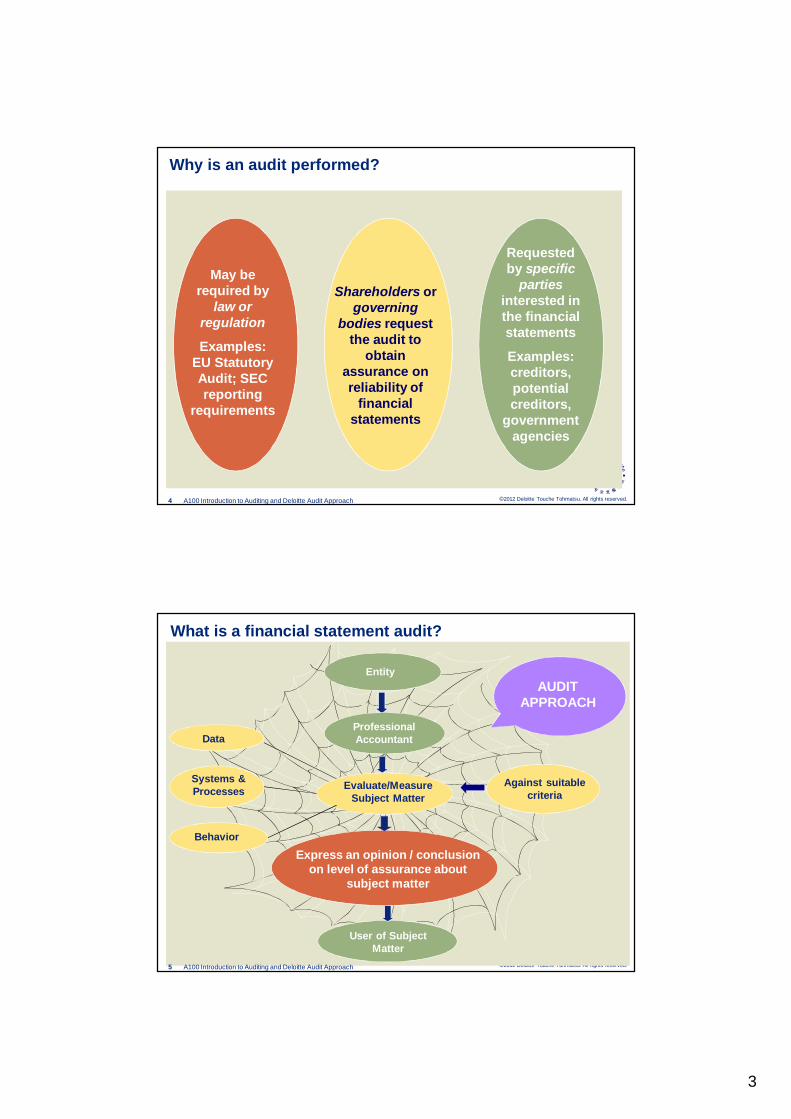

Why is an audit performed?

May be required by

law or regulation

Examples: EU Statutory Audit; SEC reporting

requirements

Shareholders or governing

bodies request the audit to

obtain assurance on reliability of

financial statements

Requested by specific

partiesinterested in the financial statements

Examples: creditors, potential creditors,

government agencies

4 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

What is a financial statement audit?

Entity

Professional Accountant

Evaluate/Measure Subject Matter

Against suitable criteria

Systems & Processes

Behavior

User of Subject Matter

Express an opinion / conclusion on level of assurance about

subject matter

Data

AUDIT APPROACH

5 A100 Introduction to Auditing and Deloitte Audit Approach

4

©2012 Deloitte Touche Tohmatsu. All rights reserved.

DTT Audit Approach…AuditSystem/2

6 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit – Some Key Principles

• Fair presentation

• Material misstatement

• Risk based approach

• Management integrity

• Independence

7 A100 Introduction to Auditing and Deloitte Audit Approach

5

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Objectives – Session 2

You will be able to:

• Describe the major activities of the Deloitte Audit Approach.

• Understand the key activities of the Deloitte Audit Approach performed by the Assistant.

8 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

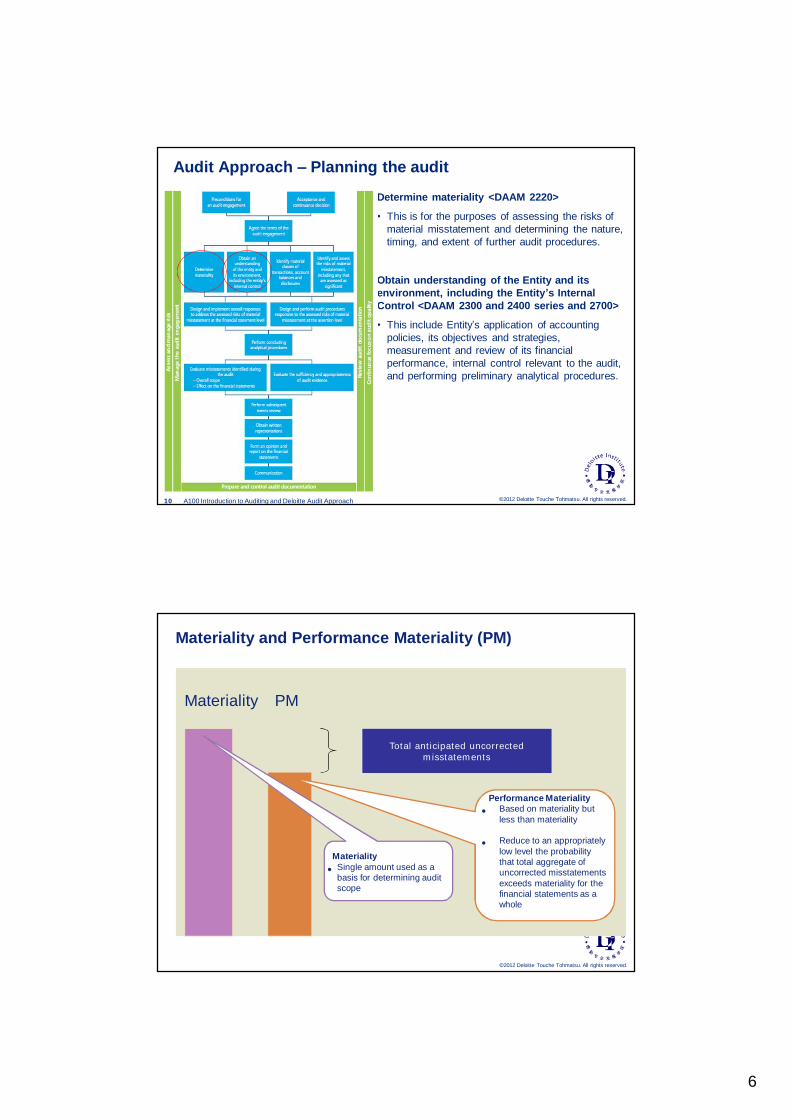

Audit Approach – Preliminary Activities

Preconditions for an audit <DAAM 1310>

• Obtaining agreement with Management about certain matters (preconditions) that are within the control of the Entity and which are to be present in order for us to accept the proposed audit engagement.

Acceptance and continuance decision <DAAM 1300>

• Evaluating the acceptability of prospective audit engagements and assessing the related engagement risks.

Agree the terms of the audit engagement <DAAM 1400>

• Recording the agreed terms of the audit engagement (e.g. objective and scope of audit, management and our responsibilities, expected financial reporting framework, form and content of any reports to be issued).

9 A100 Introduction to Auditing and Deloitte Audit Approach

6

©2012 Deloitte Touche Tohmatsu. All rights reserved.

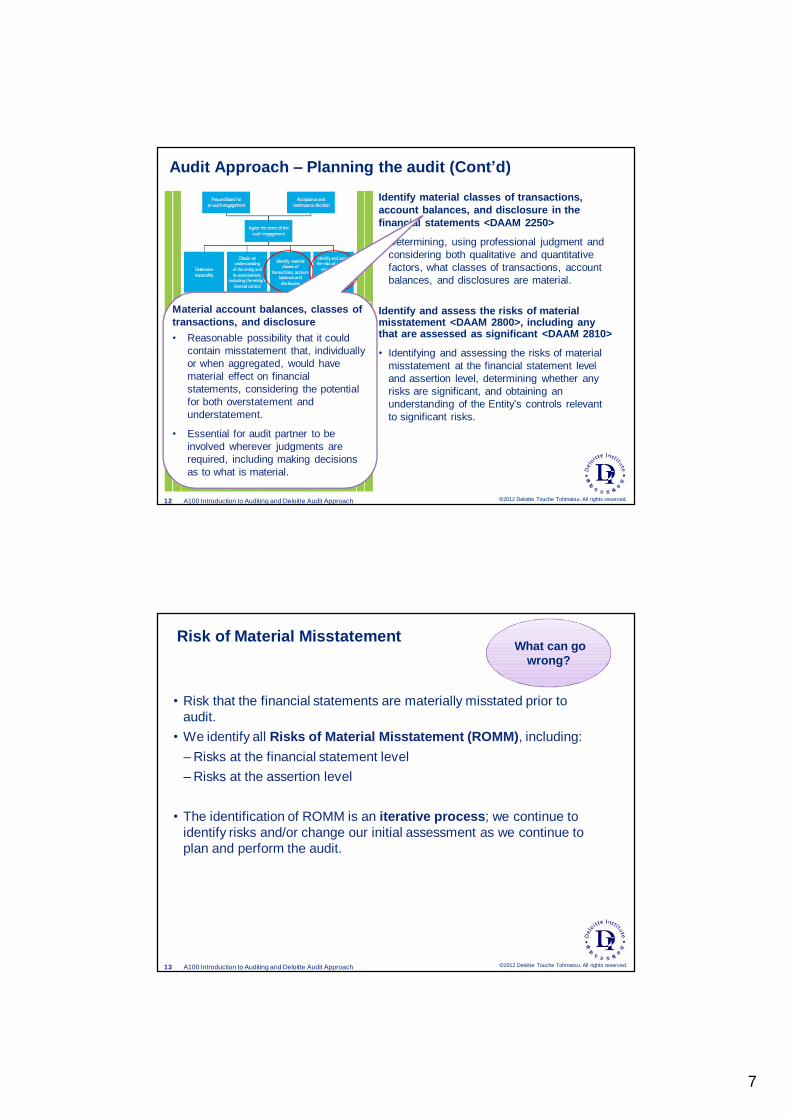

Audit Approach – Planning the audit

Determine materiality <DAAM 2220>

• This is for the purposes of assessing the risks of material misstatement and determining the nature, timing, and extent of further audit procedures.

Obtain understanding of the Entity and its environment, including the Entity’s Internal Control <DAAM 2300 and 2400 series and 2700>

• This include Entity’s application of accounting policies, its objectives and strategies, measurement and review of its financial performance, internal control relevant to the audit, and performing preliminary analytical procedures.

10 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Materiality and Performance Materiality (PM)

Materiality PM

Total anticipated uncorrected misstatements

Performance Materiality• Based on materiality but

less than materiality

• Reduce to an appropriately low level the probability that total aggregate of uncorrected misstatements exceeds materiality for the financial statements as a whole

Materiality• Single amount used as a

basis for determining audit scope

7

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit Approach – Planning the audit (Cont’d)

Identify material classes of transactions, account balances, and disclosure in the financial statements <DAAM 2250>

• Determining, using professional judgment and considering both qualitative and quantitative factors, what classes of transactions, account balances, and disclosures are material.

Identify and assess the risks of material misstatement <DAAM 2800>, including any that are assessed as significant <DAAM 2810>

• Identifying and assessing the risks of material misstatement at the financial statement level and assertion level, determining whether any risks are significant, and obtaining an understanding of the Entity’s controls relevant to significant risks.

12 A100 Introduction to Auditing and Deloitte Audit Approach

Material account balances, classes of transactions, and disclosure• Reasonable possibility that it could

contain misstatement that, individually or when aggregated, would have material effect on financial statements, considering the potential for both overstatement and understatement.

• Essential for audit partner to be involved wherever judgments are required, including making decisions as to what is material.

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Risk of Material Misstatement

• Risk that the financial statements are materially misstated prior to audit.

• We identify all Risks of Material Misstatement (ROMM), including:– Risks at the financial statement level – Risks at the assertion level

• The identification of ROMM is an iterative process; we continue to identify risks and/or change our initial assessment as we continue to plan and perform the audit.

13 A100 Introduction to Auditing and Deloitte Audit Approach

What can go wrong?

8

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Process for identifying and responding to ROMMs

14 A100 Introduction to Auditing and Deloitte Audit Approach

• Identify material COT/AB/Ds in financial statements by considering both qualitative and quantitative factors

Material COT/AB/Ds

• Identify risks based on our understanding of material COT/AB/Ds

•At “assertion” or “financial statement” level?

• Is it a fraud risk? Or significant risk?

ROMMS• Understand

controls to respond to risk?

• Any controls identified to address the risk?

• Plan to rely on controls?

Controls

• Plan test of control and substantive procedures

• Perform planned audit procedures and document work done

Procedures

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit Approach – Plan and perform audit procedures

Design and implement overall responses to address the assessed risks of material misstatement at the financial statement level <DAAM 2820>

• Designing and implementing appropriate overall responses (e.g., incorporating additional elements of unpredictability in the selection of further audit procedures to be performed) to address the assessed risks of material misstatement at the financial statement level.

Design and perform audit procedures responsive to the risks of material misstatement at the assertion level <DAAM G275>

• Determining whether the further audit procedures responsive to the assessed risks of material misstatement at the assertion level should include performing tests of controls in addition to the substantive audit procedures, and determining the nature, timing, and extent of the further audit procedures.

15 A100 Introduction to Auditing and Deloitte Audit Approach

Primarily carried out by the field senior and the assistants

9

©2012 Deloitte Touche Tohmatsu. All rights reserved.

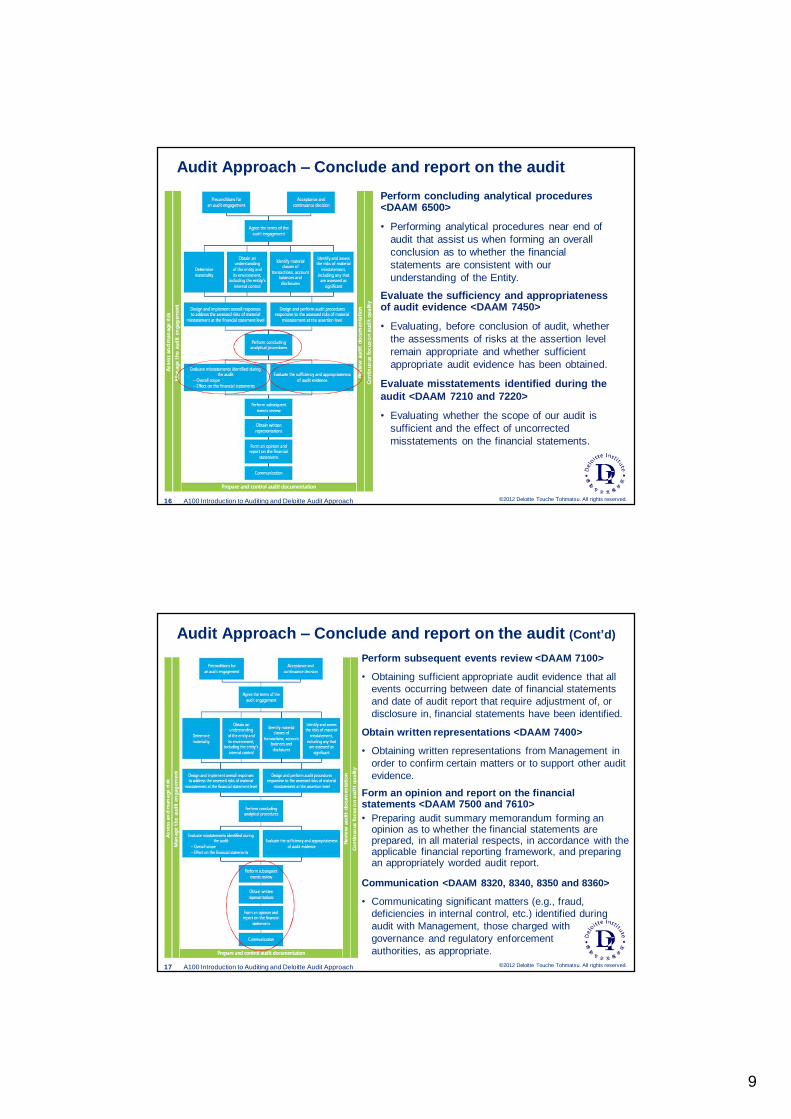

Audit Approach – Conclude and report on the auditPerform concluding analytical procedures <DAAM 6500>

• Performing analytical procedures near end of audit that assist us when forming an overall conclusion as to whether the financial statements are consistent with our understanding of the Entity.

Evaluate the sufficiency and appropriateness of audit evidence <DAAM 7450>

• Evaluating, before conclusion of audit, whether the assessments of risks at the assertion level remain appropriate and whether sufficient appropriate audit evidence has been obtained.

Evaluate misstatements identified during the audit <DAAM 7210 and 7220>

• Evaluating whether the scope of our audit is sufficient and the effect of uncorrected misstatements on the financial statements.

16 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit Approach – Conclude and report on the audit (Cont’d)

Perform subsequent events review <DAAM 7100>

• Obtaining sufficient appropriate audit evidence that all events occurring between date of financial statements and date of audit report that require adjustment of, or disclosure in, financial statements have been identified.

Obtain written representations <DAAM 7400>

• Obtaining written representations from Management in order to confirm certain matters or to support other audit evidence.

Form an opinion and report on the financial statements <DAAM 7500 and 7610>• Preparing audit summary memorandum forming an

opinion as to whether the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework, and preparing an appropriately worded audit report.

Communication <DAAM 8320, 8340, 8350 and 8360>

• Communicating significant matters (e.g., fraud, deficiencies in internal control, etc.) identified during audit with Management, those charged with governance and regulatory enforcement authorities, as appropriate.

17 A100 Introduction to Auditing and Deloitte Audit Approach

10

©2012 Deloitte Touche Tohmatsu. All rights reserved.

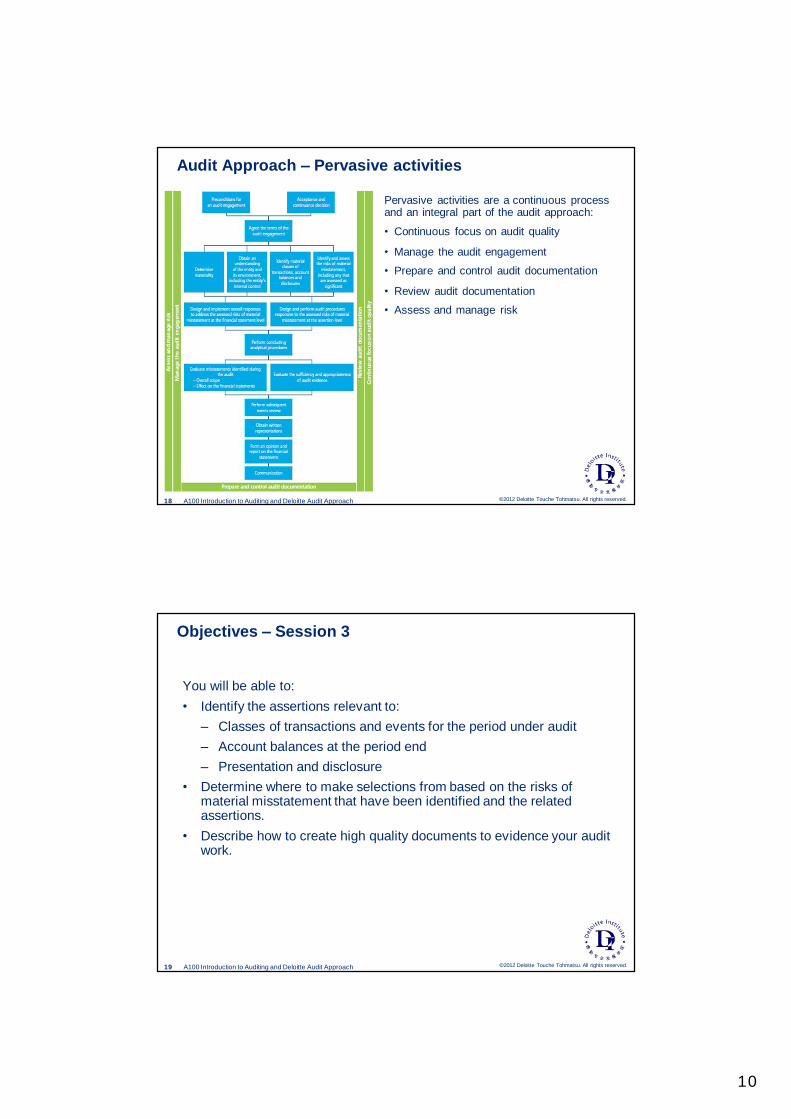

Audit Approach – Pervasive activities

Pervasive activities are a continuous process and an integral part of the audit approach:

• Continuous focus on audit quality

• Manage the audit engagement

• Prepare and control audit documentation

• Review audit documentation

• Assess and manage risk

18 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Objectives – Session 3

You will be able to:• Identify the assertions relevant to:

– Classes of transactions and events for the period under audit– Account balances at the period end– Presentation and disclosure

• Determine where to make selections from based on the risks of material misstatement that have been identified and the related assertions.

• Describe how to create high quality documents to evidence your audit work.

19 A100 Introduction to Auditing and Deloitte Audit Approach

11

©2012 Deloitte Touche Tohmatsu. All rights reserved.

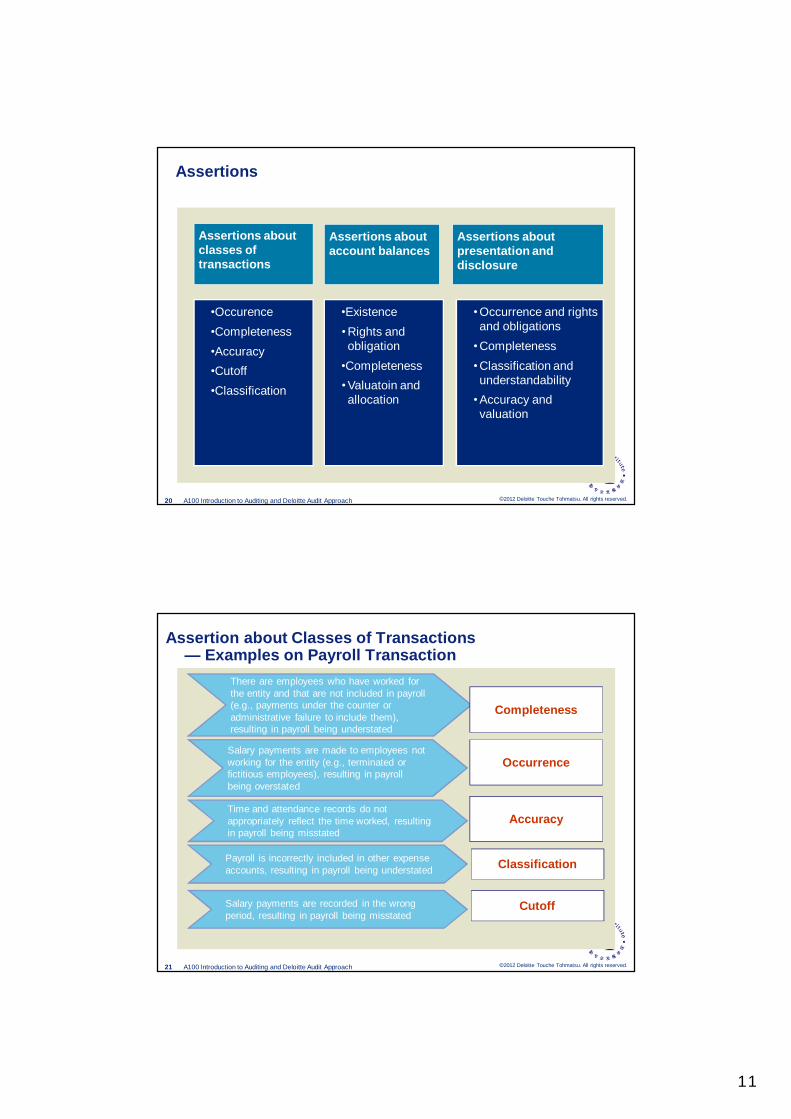

Assertions

•Occurence•Completeness•Accuracy•Cutoff•Classification

Assertions about classes of transactions

•Occurrence and rights and obligations

•Completeness•Classification and understandability

•Accuracy and valuation

Assertions about account balances

Assertions about presentation and disclosure

•Existence•Rights and obligation

•Completeness•Valuatoin and allocation

20 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Assertion about Classes of Transactions — Examples on Payroll Transaction

There are employees who have worked for the entity and that are not included in payroll (e.g., payments under the counter or administrative failure to include them), resulting in payroll being understated

Completeness

Occurrence

Accuracy

Salary payments are made to employees not working for the entity (e.g., terminated or fictitious employees), resulting in payroll being overstated

Time and attendance records do not appropriately reflect the time worked, resulting in payroll being misstated

Payroll is incorrectly included in other expense accounts, resulting in payroll being understated

Salary payments are recorded in the wrong period, resulting in payroll being misstated

Cutoff

Classification

21 A100 Introduction to Auditing and Deloitte Audit Approach

12

©2012 Deloitte Touche Tohmatsu. All rights reserved.

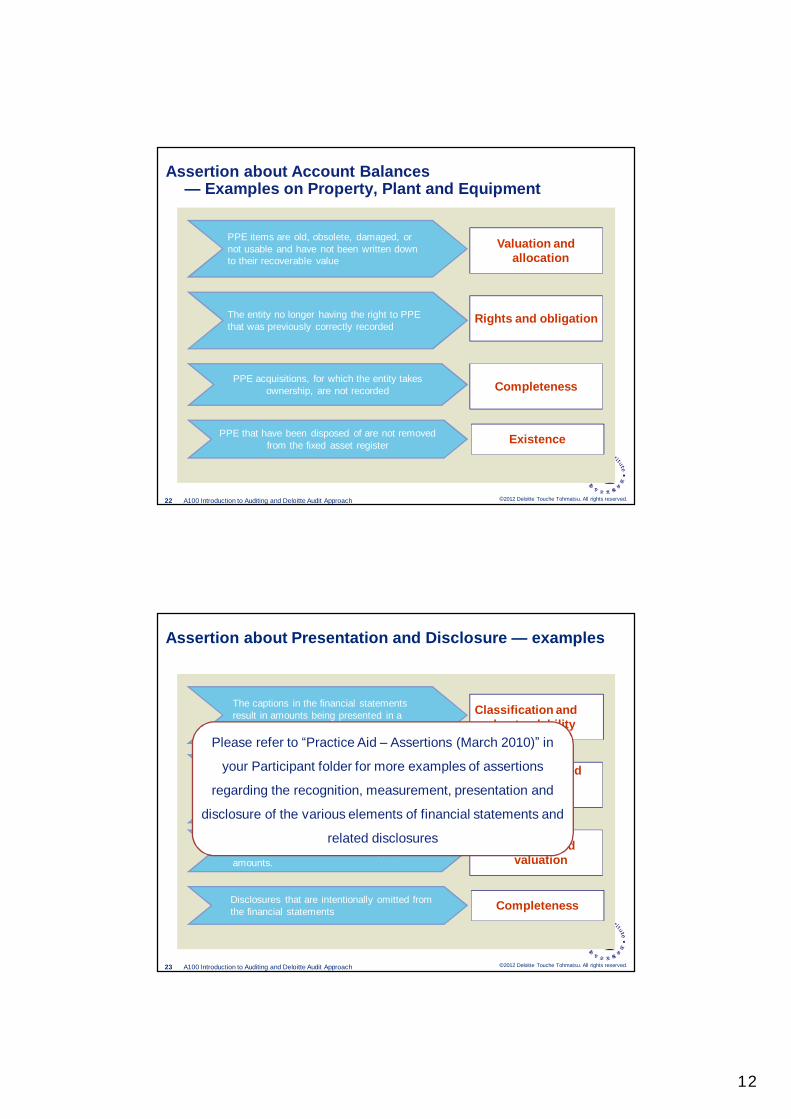

Assertion about Account Balances — Examples on Property, Plant and Equipment

PPE items are old, obsolete, damaged, or not usable and have not been written down to their recoverable value

Valuation and allocation

Rights and obligation

Completeness

The entity no longer having the right to PPE that was previously correctly recorded

PPE acquisitions, for which the entity takes ownership, are not recorded

PPE that have been disposed of are not removed from the fixed asset register Existence

22 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Assertion about Presentation and Disclosure — examples

The captions in the financial statements result in amounts being presented in a misleading way

Classification and understandability

Occurrence and rights and obligations

Accuracy and valuation

Fictitious or unauthorized disclosures are included in the financial statements and disclosures of contingent liabilities for which the entity no longer has an obligation for

Input into the financial statements reflects amounts in excess or less than appropriate amounts.

Disclosures that are intentionally omitted from the financial statements Completeness

23 A100 Introduction to Auditing and Deloitte Audit Approach

Please refer to “Practice Aid – Assertions (March 2010)” in

your Participant folder for more examples of assertions

regarding the recognition, measurement, presentation and

disclosure of the various elements of financial statements and

related disclosures

13

©2012 Deloitte Touche Tohmatsu. All rights reserved.

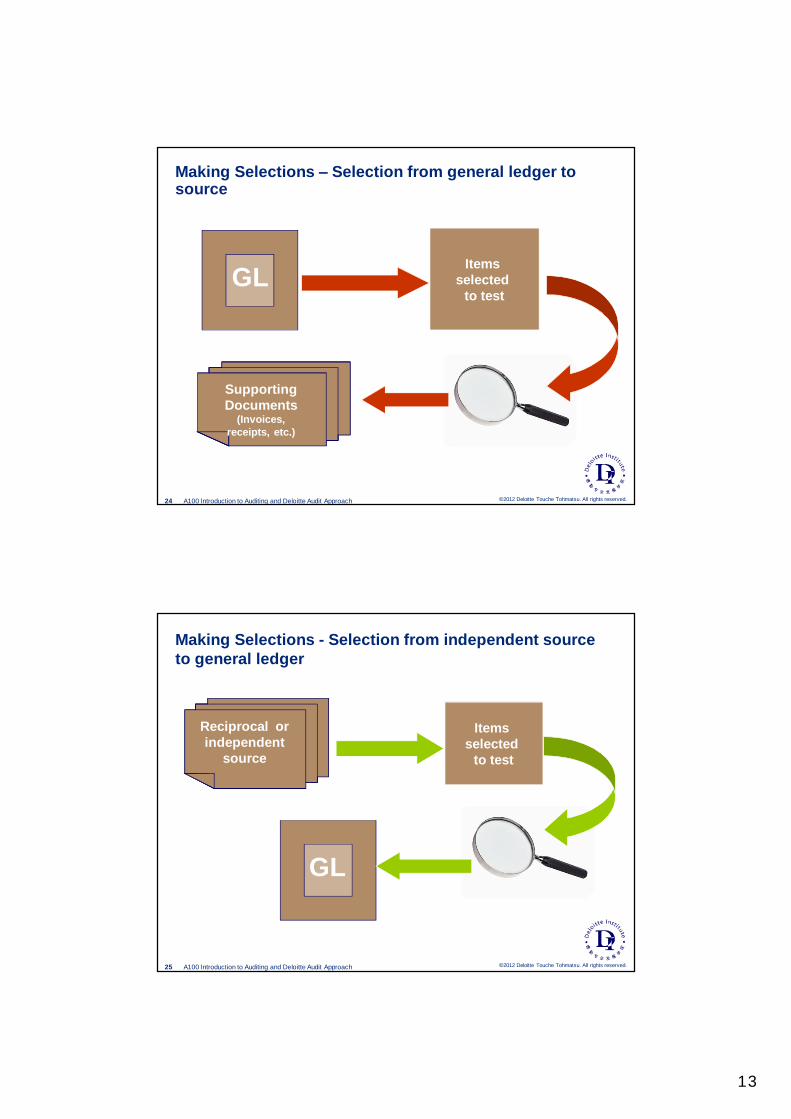

Making Selections – Selection from general ledger to source

GL Items selected

to test

receipts, etc.)

SupportingDocuments

(Invoices, receipts, etc.)

24 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

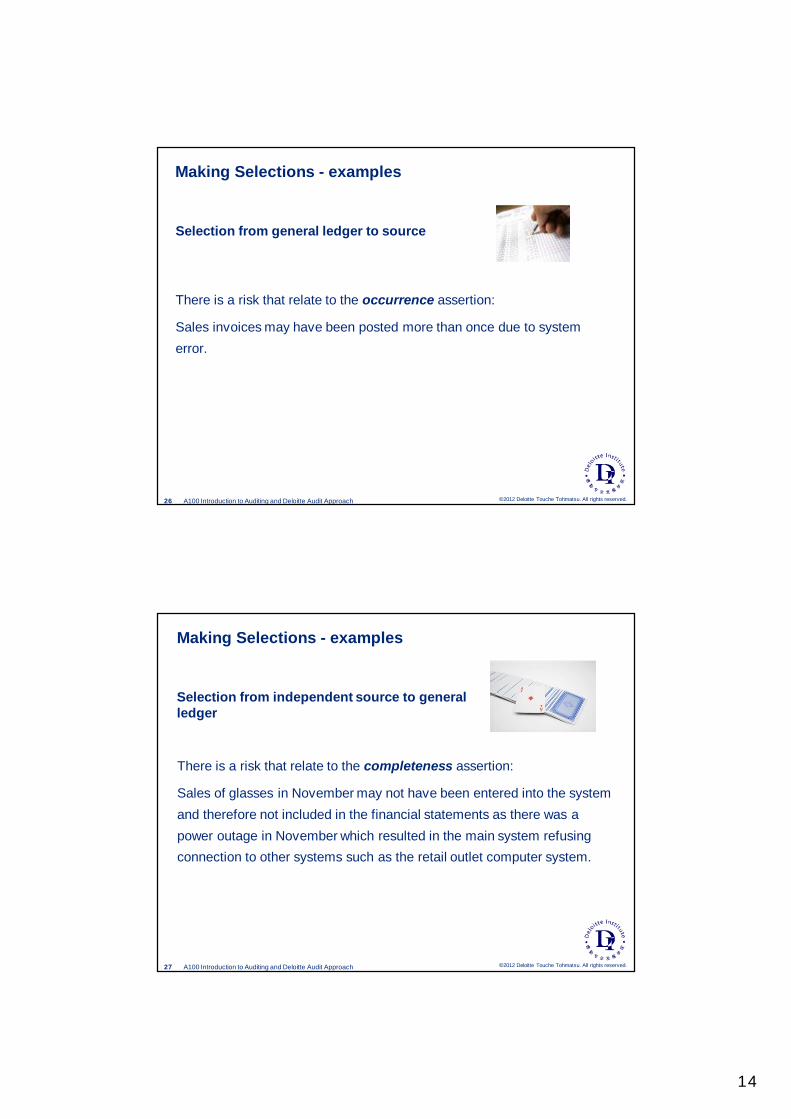

Making Selections - Selection from independent source to general ledger

GL

Items selected

to test

Reciprocal or independent

source

25 A100 Introduction to Auditing and Deloitte Audit Approach

14

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Making Selections - examples

There is a risk that relate to the occurrence assertion:

Sales invoices may have been posted more than once due to system error.

Selection from general ledger to source

26 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Making Selections - examples

There is a risk that relate to the completeness assertion:

Sales of glasses in November may not have been entered into the system and therefore not included in the financial statements as there was a power outage in November which resulted in the main system refusing connection to other systems such as the retail outlet computer system.

Selection from independent source to general ledger

27 A100 Introduction to Auditing and Deloitte Audit Approach

15

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit evidence

Do we need to verify authentication of evidence?• We are not trained or expected to be authentication experts.• However, we should be skeptical and alert for suspicious items.• When suspicious, we should discuss with Field Senior and Manager.• You should not be satisfied with less-than-persuasive evidence.

28 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit evidence

Audit evidence can be classified in two ways:• By its nature — documentary or oral.• By its source:

– Auditor-generated evidence.– External (third-party) evidence.– Information produced by the entity. This information becomes audit

evidence if we use it in performing audit procedures.

29 A100 Introduction to Auditing and Deloitte Audit Approach

16

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit evidence

What is an appropriate level of professional skepticism?• Always maintain attitude of professional skepticism.• Neither assume management is dishonest nor assume unquestioned

honesty.• Objectively evaluate evidence.• Do not be satisfied with less-than-persuasive audit evidence.• Consider the reasonableness of all information given by corroborating it

with different evident sources.

30 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

Audit evidence

How can you, as an Assistant, apply professionalskepticism?• Be inquisitive and skeptical. • Always verify received information.• Remain skeptical and alert for suspicious items.• Discuss with your Field Senior or Manager if you are not sure about the

response you have received.

ASSISTANTS ARE THE EYES AND EARS OF THE FIELD SENIOR AND AUDIT MANAGER.

31 A100 Introduction to Auditing and Deloitte Audit Approach

17

©2012 Deloitte Touche Tohmatsu. All rights reserved.

• The auditor should prepare the audit documentation that is sufficient to enable an experienced auditor, having no previous connection with the audit, to understand:

– The nature, timing, and extent of the audit procedures performed to comply with our policies, applicable professional standards, and regulatory and legal requirements.

– The results of the audit procedures performed and audit evidence obtained.

– Significant matters arising during the audit and conclusions reached thereon.

“If it is NOT documented, it is NOT done!”

Audit documentation

32 A100 Introduction to Auditing and Deloitte Audit Approach

©2012 Deloitte Touche Tohmatsu. All rights reserved.

• Each working paper should document:

– Nature of preparer and reviewer

– Audit purpose

– Audit procedures and results, and

– References and tickmarks to supporting work (if appropriate)

Audit documentation – Cont’d

33 A100 Introduction to Auditing and Deloitte Audit Approach

18

©2012 Deloitte Touche Tohmatsu. All rights reserved.