Embed Size (px)

Citation preview

i

Digitally Signed by: Content manager’s Name

DN : CN = Webmaster’s name

O = University of Nigeria, Nsukka

OU = Innovation Centre

Ugboaku, Edith J.

FACULTY OF BUSINESS ADMINISTRATION

DEPARTMENT OF DEPARTMENT OF DEPARTMENT OF DEPARTMENT OF BANKIBANKIBANKIBANKING AND FINANCENG AND FINANCENG AND FINANCENG AND FINANCE

MONETARY POLICY TRANSMISSION MECHANISM AND

THE NIGERIAN ECONOMY

ABDULLAHI, BASHIR MUHAMMED

PG/M.Sc./09/54238

ii

MONETARY POLICY TRANSMISSION MECHANISM AND

THE NIGERIAN ECONOMY

BY

ABDULLAHI, BASHIR MUHAMMED

PG/M.Sc./09/54238

BEING A DISSERTATION PRESENTED TO THE

DEPARTMENT OF BANKING/FINANCE FACULTY OF

BUSINESS ADMINISTRATION UNIVERSITY OF NIGERIA,

ENUGU CAMPUS IN PARTIAL FULFILMENT OF THE

REQUIREMENT FOR THE AWARD OF MASTER OF

SCIENCE (M.Sc.) DEGREE IN BANKING/FINANCE

SUPERVISOR: PROF. J.U.J ONWUMERE

NOVEMBER, 2014

iii

APPROVAL PAGE

This is to certify that this dissertation by Abdullahi Bashir Muhammed with registration

number PG/M.Sc./09/54238 is submitted to the department of Banking and Finance in partial

fulfilment for the award of the Master of Science (M.Sc.) degree of University of Nigeria in

Banking and Finance.

………………………………………… ...........................

PROF. J. U. J ONWUMERE DATE

(SUPERVISOR)

……………………………………........ ............................

ASSOC. PROF. E CHUKE NWUDE DATE

(HEAD OF DEPARTMENT)

iv

DECLARATION

I, Abdullahi Bashir Muhammed, a post-graduate student in the department of Banking

and Finance of the University of Nigeria Enugu Campus, with Registration Number

PG/M.Sc./09/54238 has satisfactorily completed the requirement for research work for

Master of Science degree in Banking and Finance.

This work incorporated in this dissertation is original and has not, to the best of my

knowledge, been submitted in part or in full for any other Diploma or Degree of this or

any other University

………………………………. ...........................

Abdullahi Bashir Muhammed DATE

(PG/M. Sc./09/54238)

v

DEDICATION

To my parents (Prof. O. E. Abdullahi and Mrs H. O. Obajimoh)

vi

ACKNOWLEDGEMENTS

It is my pleasure to use this opportunity to express my profound gratitude to all those who

were instrumental to the successful completion of this work

My gratitude first goes to my supervisor, Dr. J. U. J Onwumere, who gave me all the support

and counsel that has produced this dissertation. His challenge and wilful assistance benefited

me immensely. He is a rear gentle man. Dr. Austin Ujunwa is remembered all for his

benevolence, including his brotherly advice when the going was tough.

My gratitude also goes to all my lecturers in the programme most especially, Prof. Chibuike

C. Uche who made me have and appreciate a better understanding of academic life. Dr. (Mrs)

N. J. Modebe, Mummy, your motherly way of impacting knowledge was really appreciated.

My gratitude also goes to Dr. Chuke Nwude, Dr. E. Onah and Dr. B. E. Chikeleze and all

other members of the Department of Banking and Finance.

Special thanks go to Mrs S. O. Abdullahi (Special Mummy) for the motherly role she has

been playing in my life. This will not be complete without acknowledging the love and

support from my dear wife Asmaau (MPTW) and also my brothers and sisters (Yoonu,

Munira, Nafisa, Raheema, Halima, Abdulmumin and Abdulrasheed). May God All Mighty

continue to guide you all

I will also like to appreciate the efforts of my HOD, Department of Banking and Finance,

University of Abuja and also Malam Abdulmaliq Yekeen towards to completion of my study.

Special thanks also go to my friends; Khalid, Charles, Sly, Ahmad Tijani, Sadiq Daddy,

Dangana (Na-Morocco) and all others that cannot be mentioned.

Finally, to Allah SWT be the glory and thanksgiving for ever. Amen.

vii

ABSTRACT

The effectiveness of monetary transmission mechanism channels in promoting monetary policy objectives has generated serious debate among scholars and practitioners. The controversies centre largely on the complexity of the medium of transmission, the difficulty in quantifying the overall effect of policy change on the economy and the problem of imperfect knowledge about transmission mechanisms which are likely to adversely affect inflation and output volatility and timing of transmission channels. Specifically, it is generally argued that an understanding of transmission process is essential to the appropriate design and implementation of monetary policy. For monetary policy to be successful in achieving its objectives, the monetary authorities must have a reasonable assessment of the effect of their policy on the economy, thus requiring the understanding of the mechanism through which monetary policy affect the economy. It is against this background that this study sought to examine the importance of interest rate channel of monetary policy transmission mechanism on monetary policy target; effectiveness of credit channel of transmission mechanism in achieving the desired combination of monetary policy goals and the effectiveness of exchange rate channel on the monetary policy target. Time series data for 30-years period, 1980-2010, were collated from Central Bank of Nigeria published annual reports and statistical bulletin for the country aggregate data. The Vector Autoregressive model (VAR) was used to estimate the monetary transmission mechanism on the Nigerian economy. Values of Real Gross Domestic Product (RGDP) were used as the exogenous variable while Consumer Price Index (CPI), Monetary Aggregate (M2), Monetary Policy Rate (MPR), Core Credit to the Sector (CCPS), Nominal Exchange Rate (NER) were used as the endogenous variables for the three hypotheses. Descriptive statistics on both the exogenous and endogenous variables were computed and graphed to complement the vector autoregressive estimates. The result revealed that: i.) The interest rate channel of monetary policy transmission mechanism was the most effective channel of monetary policy transmission in Nigeria within the period; ii.) The credit channel is not an efficient monetary policy transmission mechanism in Nigeria and iii.) Exchange rate channel is weak in explaining monetary policy transmission mechanism in Nigeria. The study recommends, among others, that the role of deposit money banks as agents of financial intermediation in the Nigerian economy should not be neglected. Thus, the Central Bank of Nigeria should strive to make these deposit money banks in Nigeria loans transaction more amendable to monetary policy actions or seek a more effective channel of transmitting monetary actions to the economy. Such measures will include sufficient control over the reserves of deposit money banks and the timely application of reserve requirements in monetary policy control. The study also recommends that further studies could be undertaken to establish the suitability of asset price channel, balance sheet channel and expectation channel in cash based economy like Nigeria.

viii

TABLE OF CONTENTS

Title Page. . . . . . . . i

Approval Page . . . . . . . ii

Declaration . . . . . . . iii

Dedication . . . . . . . iv

Acknowledgment . . . . . . . v

Abstract . . . . . . . vi

CHAPTER ONE INTRODUCTION

1.1 Background of the Study. . . . . . . . 1

1.2 Statement of the Problem. . . . . . . . 5

1.3 Objectives of the Study. . . . . . . . 7

1.4 Research Questions. . . . . . . . . 7

1.5 Research Hypotheses. . . . . . . . . 7

1.6 Scope of the Study. . . . . . . . . 8

1.7 Significance of the Study. . . . . . . . 8

1.8 Limitation of the Study. . . . . . . . 9

1.9 Operational Definition of Terms. . . . . . . 9

References. . . . . . . . . . 11

CHAPTER TWO REVIEW OF RELATED LITERATURE

2.1 Theoretical Review. . . . . . . . . . 12

2.1.1 The General Framework of Monetary Policy Transmission Theory. . . 14

2.1.2 The Channels of Monetary Transmission. . . . . . . . . . 20

2.1.3 Financial Crises. . . . . . . 33

2.1.4 The Lending Channel and Consumer Credit . . . . . 35 2.1.5 Monetary Theory of Exchange Rate Determination. . . . . 39

2.1.6 Recent Developments . . . . . . . . 43 2.1.7 International Monetary Policy Regimes . . . . . 50

2.2 Empirical Review. . . . . . . . 68

2.2.1 Interest Rate Channel. . . . . . . . . . 68

2.2.2 The Exchange Rate Channel. . . . . . . . 71

2.2.3 The Asset Price Channel. . . . . . 74

2.2.4 Inflation Expectation Channel. . . . . . . . . . 76

2.3 Review Summary. . . . . . . . 79

References. . . . . . . . . . . 81

ix

CHAPTER THREE RESEARCH METHODOLOGY

3.1 Research design. . . . . . . . . 89

3.2 Nature and Sources of Data. . . . . . . . 89

3.3 Description of Research Variables. . . . . . . . 89

3.4 Techniques of Analysis. . . . . . . 92

3.5 Model Specification. . . . . . . . 93

References. . . . . . . . . . 96 CHAPTER FOUR PRESENTATION AND ANALYSIS OF DATA

4.1 Presentation of Data. . . . . . . . . 97

4.2 Descriptive Statistics of Aggregate Data. . . . . - 98

4.3 Determination of Research Variable . . . . . 100

4.4 Correlation Matrix . . . . - - - - 104

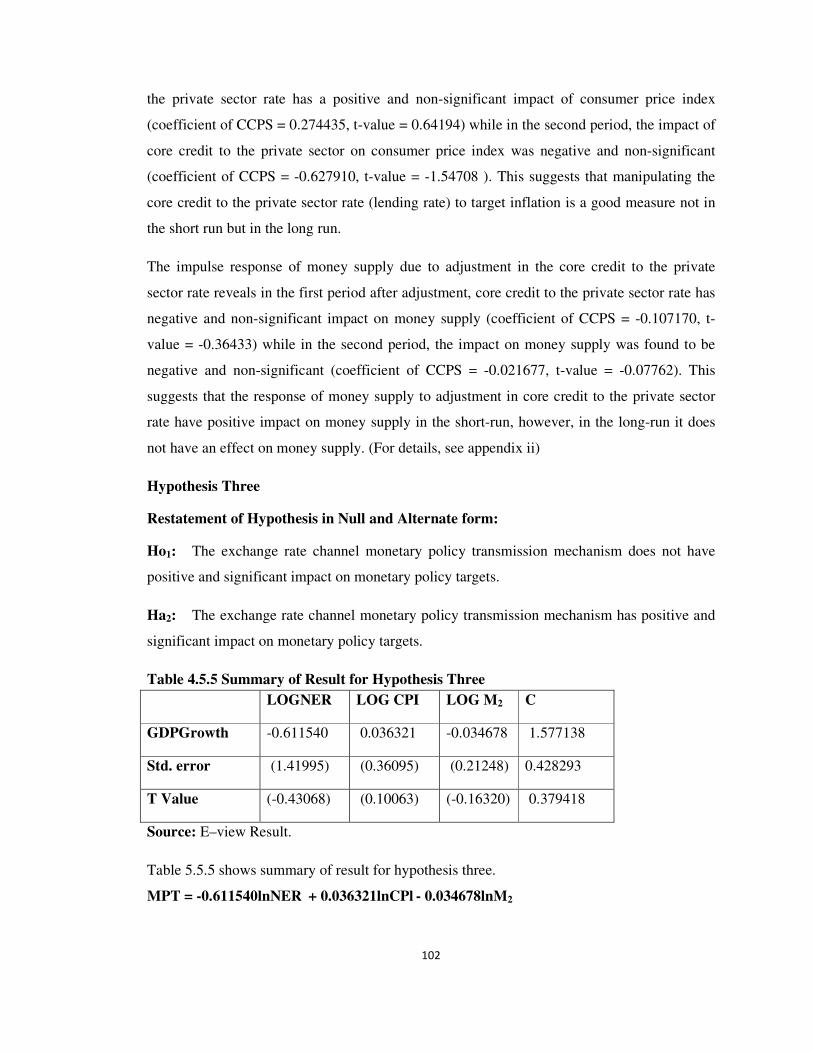

4.5 Test of hypotheses . . . . . . - - 106

4.6 Robustness Test - - - - - - - - 111

4.7 Discussion of Results - - - - - 111

References - - - - - - - - - 114

CHAPTER FIVE: SUMMARY OF FINDINGS, CONCLUSION AND

RECOMMENDATIONS

5.1 Summary. . . . . . . . . 115

5.2 Conclusion. . . . . . . . . 116

5.3 Recommendations . . . . . . . 117

5.4 Contribution to Knowledge - - - - - - - 117

5.5 Recommended Areas for Further Studies - - - - - 118

Bibliography . . . . . . . . . 119

Appendixes - . . . . . 12

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

The last three decades has seen industrialized countries around the world face multitude of

shocks, which led to the inflationary experience of many countries during the 1970s, to the

exchange rate crises during the early 1990s (Yamin, 2004). The monetary experiences faced

by these countries have also led to numerous questions. These questions rage from what kind

of policy should central bank follow when shocks occur to how should central banks react to

such shock that hits the economy and the welfare effect of such shocks? Any hope of

answering this type of question relies on researchers having a clear idea of the transmission

mechanism of monetary policy. The formulation and implementation of appropriate monetary

policy is one of the major responsibilities of central bank worldwide (Ajayi, 2007).

Monetary policy can be described as the central banks action to influence the availability and

the cost of money and credit as a means of promoting national economic goals (Patrick and

Xavier, 2000). Specifically it can be defined as a combination of measures designed to

regulate the value, supply and cost of credit in an economy in consonance with the expected

level of economic activity (Olekah, 2006). Uchendu (2009) posits that monetary policy is the

use of the instruments at the disposal of the monetary authorities to influence the availability

and cost of credit/money with the ultimate objective of achieving price stability. In the same

vein, Okafor (2009) also argues that monetary policy is a blend of measures and or set of

instruments designed by the central bank to regulate the value, supply and cost of money

consistent with the absorptive capacity of the economy or the expected level of economic

activity without necessarily generating undue pressure on domestic prices and the exchange

rate.

The centrality of these definitions is that monetary policy is a measure designed to influence

the availability, volume and direction of money and credit to achieve the desired economic

objectives. The set objectives are achieved through the use of monetary policy instruments

(Ajayi, 2007). The policy tools under the control of central bank are not however directly

linked to the policy objectives. Consequently, the usual practice is that intermediate target

such as money supply; interest rate and bank credit are employed to achieve monetary policy

objectives. Generally developing a practical understanding of how monetary policy action

transmits to the economy remains a day to day challenge to the central banks.

2

According to Mbutor (2009), the financial repressive policies that preceded the adjustment era

of the late 1980s seem to have made the understanding of the channels of monetary

transmission more difficult due to interest rate volatility. When central bank takes a policy

action, it sets in motion a series of economic events. The consequence of these events start

with the initial influence on the financial market, which in turn slowly work its way through

changes in the current expenditure level, especially, private consumption and investment.

Changes in domestic demand influences the current production levels, wages and employment

and in the process eventually lead to a change in domestic prices (Ajayi, 2007). The chain of

event which link change in the monetary policy with changes in prices and output is known as

the transmission mechanism of monetary policy

In Nigeria, monetary policy formulation is the sole prerogative of the Monetary Policy

Committee (MPC) of the Central Bank of Nigeria (CBN). The MPC which was formally

consolidated in 1999, consisting of the governor of the bank as the chairman, the four deputy

governors of the bank, two members of the board of directors of the bank, three members

appointed by the president and two members appointed by the governor. The MPC has the

responsibility for formulating monetary and credit policies. The traditional function of Central

Bank of Nigeria is to ensure financial stability, favourable macroeconomic environment and

safe guard the external value of Naira.

Since monetary policy covers the monetary aspect of the general economic policy, a high

level of co-ordination is required between monetary policy and its transmission channel so as

to achieve effective monetary policy objectives. Such objectives include price stability (or low

inflation rate), full employment and growth in aggregate income. A successful implementation

of monetary policy requires an accurate assessment of how fast the effects of policy changes

propagate to other part of the economy and how large these effects are (Thorarinn, 2001). This

requires a thorough understanding of the mechanism through which monetary policy affects

economic activity. The priority of price stability over other monetary policy objectives tends

to be potentially accepted in most countries, if not enshrines in the laws governing the central

banks (Norman and Klaus 2002). The channels through which monetary policy actions are

transmitted to the economy are so vast and vary across countries. In the Nigerian, there are

some many channels through which monetary policies transmit to the economy. However,

scholars and practitioners usually identify three major channels which include; interest rate

3

channel, exchange rate channel and credit channel (Mbutor, 2009; Boivin, Kiley, and

Mishkin, 2010; Francisco, 1998).

The Interest rate channel has featured predominantly in literature over several decades as the

key monetary transmission mechanism which was influenced by basic Keynesian model.

Most central banks implement daily liquidity expansions or contractions by charging or

paying an overnight or very short-run interest rate. This rate will influence the whole structure

of interest rate in a variety of ways. Since the overnight rate is views by the market as a bench

mark, arbitrage possibilities will ensure that market interest rate on some 28-day instruments

will tend to equal (1+d), where d is the daily expected central bank interest rate. In turn other

term deposit will react to the changes in one-month so that the one day rate will end up

influencing overall term structure of interest rate. Francisco (1998) posits that another

powerful transmission mechanism is the implicit announcement effects of an interest rate

change. An adjustment of the daily interest rates by the central bank may signal to the market

that the central aims for a tighter or looser stance. Such a change could have an amplified

effect on the level of interest beyond that impact via the arbitrage mechanism described

above.

Exchange rate channel is an important element on the conventional open economy micro

economic model. With the growing internationalization and the advent of flexible exchange

rates, more attention has been paid to monetary policy transmission operating through

exchange rate effects on net exports. Indeed, this transmission mechanism is now a standard

feature in the leading textbooks in macroeconomics and money and banking. This channel

also involves interest rate effects because when domestic real interest rates fall, domestic

dollar deposits become less attractive relative to deposits denominated in foreign currencies,

leading to a fall in the value of dollar deposits relative to other currency deposits, that is, a

depreciation of the dollar (denoted by E↓). The lower value of the domestic currency makes

domestic goods cheaper than foreign goods, thereby causing a rise in net exports (NX↑) and

hence in aggregate output. This exchange rate channel plays an important role in how

monetary policy affects the domestic economy as is evident in research, such as Bryant,

Hooper and Mann (1993) and Taylor (1993).

Credit channel is generally argued to have greater effect on expenditure of smaller firms, since

they are more dependent on bank loans when compared with large firms Taylor (1993). This

is because large firms can access the credit market directly through stock and bond market.

4

Dissatisfaction with the conventional stories about how interest rate effects explain the impact

of monetary policy on expenditure on long-lived assets has led to a new view of the monetary

transmission mechanism that emphasizes asymmetric information in financial markets.

According to Mishkin (1996), there are two basic channels of monetary transmission that arise

as a result of information problems in credit markets: the bank lending channel and the

balance-sheet channel. The bank lending channel is based on the view that banks play a

special role in the financial system because they are especially well suited to solve

asymmetric information problems in credit markets Mishkin (1996). Because of banks' special

role, certain borrowers will not have access to the credit markets unless they borrow from

banks. As long as there is no perfect substitutability of retail bank deposits with other sources

of funds, the bank lending channel of monetary transmission operates as follows.

Expansionary monetary policy, which increases bank reserves and bank deposits, increases

the quality of bank loans available. Given banks' special role as lenders to classes of bank

borrowers, this increase in loans will cause investment (and possible consumer) spending to

rise.

The balance-sheet channel also arises from the presence of asymmetric information problems

in credit markets. The lower the net worth of business firms, the more severe the adverse

selection and moral hazard problems are in lending to these firms. Lower net worth means

that lenders in effect have less collateral for their loans, and so losses from adverse selection

are higher. A decline in net worth, which raises the adverse selection problem, thus leads to

decreased lending to finance investment spending. The lower net worth of business firms also

increases the moral hazard problem, because it means that owners have a lower equity stake in

their firms, giving them more incentive to engage in risky investment projects. Since taking

on riskier investment projects makes it more likely that lenders will not be paid back, a

decrease in business firms' net worth leads to a decrease in lending and hence in investment

spending.

The cash based nature of Nigerian economy and the oil revenue has the ability to distort the

channel of monetary policy transmission mechanisms that is put in place by the Central Bank

of Nigeria. This argument is supported by Nissanke and Aryeetey (1998), when they argue

that in the presence of excess liquidity, it becomes difficult to regulate the money supply

using the required reserve ratio and the money multiplier, so that the use of monetary policy

for stabilization process is undermined. In other words one would expect excess liquidity to

5

weaken the monetary policy transmission mechanism. The transmission mechanisms of

monetary policy work through various channel thus affecting variables and different market

and at various speed and intensities. Identifying these transmission channels is important

because they determine the most effective set of policy instruments, and timing of policy

changes and hence the main restrictions that central banks faces in making their decisions

(Norman and Loayza, 2002).

Given the paramount importance of the transmission mechanism for the understanding of

monetary policy it is surprising that, until very recently, relatively little effort have been

invested in understanding exactly how the transmission mechanisms have been effective in

achieving monetary policy objectives. This study is geared towards filling this important

knowledge gap.

1.2 Statement of Problem

The effectiveness of monetary transmission mechanism channels in promoting monetary

policy objectives has generated serious debate among scholars and practitioners. The

controversies centers on largely on the complexity of the medium of transmission, the

difficulty in quantifying the overall effect of policy change in the economy and the problem of

imperfect knowledge about transmission mechanisms which is likely to adversely affect

inflation and output volatility and, hence, timing of transmission channels (Ajayi, 2007).

According to Mbutor (2009), monetary policy transmission through the monetary policy rate

does not have a contemporaneous effect on the gross domestic product and consumer price

index. However, the heist dip in price as a result of the policy shock is observed, hence

variance decomposition shows that the change in the CPI was mainly caused by GDP and lags

of CPI itself. The inference from the study shows that the lending rate provides the shortest

nexus for the propagation of monetary policy impulse in Nigeria.

Ajayi (2007) also examine the monetary policy transmission mechanism in Nigeria and argue

that, monetary policy transmission mechanism varies in detail between different economies

because it depends partly upon the institutional structures. However, these differences are

small and involve the relative importance of different channels rather than the existence of the

channel itself. He posits that the design and implementation of monetary policy in a given

economy depends on its financial structure and macroeconomic importance. His study

concluded saying that channel of transmission mechanism at one time or the other have been

6

relevant to the Nigerian economy. However recent preliminary study indicates that the

exchange rate channel was very strong in Nigeria between 1980s and 2005 while the interest

rate and the credit channel were week during the period.

Boivin, Kiley, and Mishkin (2009) discussed the evolution in macroeconomics through the

monetary policy transmission mechanism and presented related empirical evidence. They

argued that the core channel of policy transmission i.e. neoclassical link between short term

policy interest rates, other asset prices such as long term interest rate, equity price and the

exchange rates, and the consequent effect on house hold and business demand have remain

steady from early policy oriented model to modern dynamic stochastic general equilibrium

model. In contrast, non neoclassical channels such as credit channels have remain outside the

core models which are responsible for a notable change in the policy behavior and in the

reduced form of correlation policy interest rates with economic activities.

Monetary policy research has centered on some major controversies such as the complexity

of the medium of transmission, the difficulty in quantifying the overall effect of policy change

and the problem of imperfect knowledge about transmission mechanisms. However, none of

these works has looked at the most effective channel of monetary policy transmission. Hence,

this study strived to fill this important research gap by empirically investigating the most

efficient channel of monetary policy transmission in Nigeria.

. Specifically, it is generally argued that an understanding of transmission process is essential

to the appropriate design and implementation of monetary policy. For monetary policy to be

successful in achieving its objectives, the monetary authorities must have a reasonable

assessment of the effect of their policy on the economy, thus requiring the understanding of

the mechanism through which monetary policy affect the economy. Given the inconclusive

findings of the above scholars, need arise to do an empirical work on Nigeria which is the

problem this research work needs to solve.

1.3 Objectives of the Study

The main objective of this study is to examine specifically the dominant channel of monetary

policy transmission mechanism in Nigeria. To achieve this objective, the study strives;

a. To examine the impact of interest rate channel of monetary policy transmission

mechanism on monetary policy target.

7

b. To determine the impact of credit channel of monetary policy transmission

mechanism on monetary policy target.

c. To evaluate the impact of exchange rate channel of monetary policy mechanism on the

monetary policy target.

1.4 Research Questions

This research work was tailored in such a way that provides answers to the following

questions;

a. What is the relationship between interest rate channel of monetary policy transmission

mechanism and monetary policy target?

b. Does credit channel of monetary policy transmission mechanism have impact on

monetary targets?

c. What is the relationship between the exchange rate channels of monetary policy

transmission mechanism on monetary policy targets?

1.5 Research Hypotheses

To achieve the above objectives and provide answers to the research questions, the following

hypotheses were put in place:

a. The interest rate channel of monetary policy transmission mechanism does not have

positive and significant impact on monetary policy target.

b. The credit channel of monetary policy transmission mechanism does not have positive

and significant impact on monetary policy target.

c. The exchange rate channel of monetary policy transmission mechanism does not have

positive and significant impact on monetary policy target.

1.6 Scope of the Study

The study covers the period, 1980-2012. This time period is necessitated by the desire of the

researcher to examine the dominant channel of monetary policy from the second republic

which started in 1979 to the present democratic dispensation in Nigeria. In line with previous

study along this area, the study focuses on channel of monetary policy transmission

mechanism such as; Exchange rates, Lending rates, Gross Domestic Product (GDP) and

Consumer Price Index (CPI). The study also focuses on the effectiveness of the above

mentioned channels as regards to the achievement of monetary policy targets.

8

1.7 Significance of the Study

A successful implementation of monetary policy requires an accurate assessment of how fast

the effect of policy changes propagate to other parts of the economy and the degree these

effect (Thorarinn, 2001). The process that describes how a change in the monetary policy

propagates to the other parts of the economy is called transmission mechanism of the

monetary policy. The end result of this study will prove to be beneficial and lend more

support to the improvement of monetary policy transmission mechanism in Nigeria. The study

is expected to be significant to key stake holders in the following ways:

a. Policy Makers and Regulators

When the CBN announces the Monetary Policy Rate (MPR) as required by law: It is essential

to signal its intention about the rate of interest and to influence the term structure of interest

rates. The inter-bank call rate has thus become the focal point of attention. The inter-bank call

market and the government securities market since the reforms have been unveiled through

the secondary market transaction have not acquired adequate depth (Mbutor, 2009).

It is against this background, that the CBN has reviled its intention to move from the current

policy framework that is a hybrid of monetary targeting and a loose form of interest rate

targeting to inflation targeting framework. There is, therefore, a more urgent need to

understand as to which of the channels of monetary policy transmission and which of the

others are need to be kept in view in short-to-medium term.

b. General Public

The outcome of this study is expected to educate the general public about the general

objective of monetary policy framework, policy target and its direction, dominant channel of

policy transmission and its effectiveness whose importance in general economic decision

making cannot be overemphasized. This study is expected to provide a platform for further

research on the subject matter.

1.8 Limitation of the Study

This research work is faced with the usual limitation associated with student research works

such limitations include; funds as a limiting factor, insufficient time and other difficulty of

data collection from the CBN such as obeying serious protocols. However, this limitation will

not invalidate the result of the study.

9

1.9 Definition of Terms

Monetary Policy

Monetary policy is a blend of measures and set of instruments designed by the central bank to

regulate the value, supply and cost of money consistent with the absorptive capacity of the

economy or the expected level economic activity without necessarily generating undue

pressure on domestic prizes and exchange rate (Okafor, 2009).

Monetary Policy Objectives

Monetary policy objectives are the set goals and targets that monetary authorities of any

country intends to achieve. In Nigeria, the objectives of monetary policy include;

Achievement of domestic price and exchange rate stability, maintenance of a healthy balance

of payments position, development of a sound financial system, and promotion of rapid and

sustainable rate of economic growth and development.

Monetary Policy Transmission Mechanism

The monetary policy transmission mechanism describes how the policy induce changes in the

nominal monetary stock or short term nominal rate impact on real variables such as aggregate

output and employment.

Monetary Policy Committee (MPC)

The monetary policy committee consolidated in 1999 consists of the governor of the bank as

the chairman, the four deputy governors of the bank, and two members of the board of

directors of the bank. Three members are appointed by the president and while members are

appointed by the governor. The MPC have responsibility within the bank for formulating

monetary and credit policy.

Open Market Operations (OMO)

The market-based tools which specify the proportion of a bank’s total deposit liabilities that

should be kept with the central bank. Open market operation may be undertaken through

outright transactions or through repurchase transaction.

10

References

Ajayi M. (2007), Monetary Policy Transmission Mechanism in Nigeria: Economic and

Financial Review, Abuja: Central Bank of Nigeria. Boivin, J., M.T. Kiley, and F. S. Mushkin (2009), “How Has the Transmission Mechanism

Evolved Over Time” Financial and Economic Discussion Series (FEDS) Humanity Research Council of Canada

Bryant, R., P. Hooper and M. C. Mann (1993), “Evaluating Policy Regimes: New Empirical

Research in Empirical Macroeconomics”, Brookings Institution Washington D.C Chalesn, B.,L. Jens and N. Kalin (2002), Financial Friction and the Monetary Transmission

Mechanism: Theory, Evidence and Policy Implementation, England: ECB Publishers. Freixas, X., A. Martin and D. Skeie, (2009), “Bank liquidity, interbank markets, and monetary

policy” Federal Reserve Bank of New York Staff Reports 371 Keneth, N. K. and C.M Patricia (2002), “Monetary transmission mechanism: Some answers

and further questions”, FRBNY Economic Policy Review New York:. Mbutor, O. M. (2009), “The Dominant Channel of Monetary Policy Transmission in Nigeria:

An Empirical Investigation”, Nigeria Economic and Financial Review, 2(1), 23-34. Modigliani, F. (1971), “Monetary policy and Consumption In consumer Spending and

Monetary Policy: the Linkages”, Federal Reserve Bank of Boston Working Paper Mohanty, M. S. and P. Turner (2008), “Monetary Policy Transmission in Emerging Market

Economies: What Is New?” Bank for International Settlements Papers, 35, 1-59 Mushkin, F.S. (1996), “The Channel of Monetary Transmission: Lessons for Monetary

Policy”, Banquet De France Bulletin Digest Colombian University, 2(3), 103-113. Mushkin, F.S. (2007), Housing and the Monetary Transmission Mechanism, Massachustts,

Cambridge: Prentice Hall Nissanke N. and R. Aryeetey (1998), “Excess Liquidity and Effectiveness of monetary Policy:

Evidence from Sub-Saharan Africa”, IMF Working Paper N0 06/115 Norman, L. and Klaus, S. H. (2002), “Monetary Policy Functions and Transmission

Mechanisms: An Overview”, World Bank working Paper. Olekah, J. K. A. (1995), “Central Bank of Nigeria’s New Monetary Policy Initiatives” a paper

Presented at the 15th, Delegates Conference/Annual General Meeting of the Monetary

Market Association of Nigeria

Okafor P. N. (2009), “Monetary Policy Frame Work in Nigeria: Issues and Challenges.”

Central Bank of Nigeria Bullion, 30(2), 23-35.

11

Ooi, S. K. (2009), “The Monetary Policy Transmission Mechanism in Malaysia: Current Development and Issues” Malaysia Bis Pepers No. 35.

Patrick, B. and Xavier, F. (2006), Coporate Finance and the Monetary Transmission

Mechanism, London: Oxford University Press Peter, N. I. (2008), The new Palgrave Dictionary of Economics, Second Editon,

USA: Macmillan Peter, N. I. (2005), The Monetary Transmission Mechanism, Second Edition: Boston College

and NBER Chestnut Hill, MA. Thorarinn, G. P. (2001), The Transmission Mechanism of Monetary Policy: Analyzing the

Financial Market Pass-through, London: George Allen and Union Ltd. Uchendu A. O. (2009), “Overview of Monetary Policy in Nigeria”, Monetary Policy

Department Central Bank of Nigeria Bullion 30 (2), 107-123. Yamin S. A. (2004), “The Transmission Mechanism Of Monetary Policy” A Dissertation

submitted to the Faculty of the Graduate School of Arts and Sciences of Georgetown

University in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Economics: M.Sc.Washington D.C.

12

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.1 Theoretical Review

A successful implementation of monetary policy requires an accurate assessment of how fast

the effects of policy changes propagate to other parts of the economy and how large these

effects are. This requires a thorough understanding of the mechanism through which monetary

policy affects economic activity. The process that describes how changes in monetary policy

propagate to other parts of the economy is called the transmission mechanism of monetary

policy. It describes how changes in policy transmit through the financial system, via financial

prices and quantities, to the real economy, affecting aggregate spending decisions of

households and firms, and from there to aggregate demand and inflation. Given the paramount

importance of the transmission mechanism for the understanding of monetary policy it is

surprising that, until very recently, relatively little effort has been invested in understanding

exactly how the transmission mechanism Bernanke and Gertler (1995).

Sims (1986) posits that the transmission mechanism logically involves two stages. The first

stage involves the propagation of changes in monetary policy through the financial system.

This stage of the transmission mechanism explains how changes in the market operations of

central banks transmit through the money market to markets which directly affect spending

decisions of individuals and firms, i.e. the bond market and the bank loan market. This

involves the term structure, through which short term money market rates affect longer-term

bond rates, and the marginal cost of loan funding, through which bank loan rates are affected.

The second stage of the transmission mechanism involves the propagation of monetary policy

shocks from the financial system to the real economy. This explains how monetary policy

shocks affect real production and aggregate prices. It seems obvious that in order to fully

understand the transmission from central bank actions to the real economy, the first stage

needs to be fully understood.

The first stage of the transmission mechanism focuses only on a particular part of the

transmission mechanism, namely the interest rate channel. This implies that other important

transmission channels, such as the exchange rate channel, which should be of great

importance for a small open economy, are not considered. Given the small size and the

considerable weight on exchange rate stabilization in domestic monetary policy, one could

13

expect that world market interest rate shocks would influence interest rate determination.

Given that capital movements were only fully liberalized in 1995, and the fact that it is only in

the last few years that foreign interest rates have started to play a role in monetary policy,

detecting this effect in the data sample used here might be difficult.

The ideal measure of monetary policy would be one that is under direct control of the central

bank and is, in the short run, unaffected by changes in the demand for money. Early studies of

the transmission mechanism, such as Sims (1986), used monetary aggregates, while later

studies have tended to use measures that are under more direct control of the central bank,

such as non-borrowed reserves (Strongin, 1995 and Christiano, Eichenbaum and Evans,

1996), or some short-term interest rate under control of the central bank (Bernanke and

Blinder, 1992 and Sims, 1992).

The choice between these measures of monetary policy obviously depends on the strategy and

operating procedures of the central bank. For banks which conduct monetary policy by

targeting the liquidity of the financial system, measures such as narrow money or reserves

seem appropriate. For central banks which use the interest rate on loans from the central bank

to the financial system as the target variable, the appropriate measure of monetary policy is

this target rate.

2.1.1 THE GENERAL FRAME WORK OF MONETARY POLICY TRANSMISION

THEORY

One way of posing the fundamental question associated with understanding the monetary

transmission mechanism is to ask how seemingly trivial changes in the supply of an outside

asset can create large shifts in the gross quantity of assets that are in zero net supply, how low

is it that small movements in the monetary base translate into large changes in demand

deposits, loans, bonds and other securities, thereby affecting aggregate investment and output?

The various answers no this puzzle can be understood within the framework originally

proposed by Brainard and Tobin (1963). Their paradigm emphasizes the effects of monetary

policy on investor portfolios, and is easy to present using the insights from Fama’s (1980)

seminal paper on the relationship between financial intermediation and central banks. Fama’s

view of financial intermediaries is the limit of the current type of financial innovation,

because it involves the virtual elimination of banks as depository institutions. The setup

focuses on an investor’s portfolio problem in which an individual must choose which assets to

14

hold given the level of real wealth. Labeling the portfolio weight on asset i as w1, and total

wealth as W then the holding of asset, i the asset demand is just X1 = w1W. In general, the

investor is dividing wealth among real assets real estate, equity and bonds and outside money

each asset has stochastic return, ẑ1 with expectation ẑ1 and the vector of asset returns, ẑ1 has a

covariance structure F. Given a utility function, as well as a process for consumption, it is

possible to compute the utility maximizing portfolio weights. These will depend on the mean

and variance of the returns ẑ1 and F, the moments of the consumption process represented as

µc and a vector of taste parameters that is label ф, and assume to be constants. The utility

maximizing asset demands can be expressed as X* = wi*( ẑ1, F, µc, ф) W2 This representation

makes clear than asset demands can change for two reasons. Changes in either the returns

process ẑ1 F or macroeconomic quantities (µc, W) will affect the X*, S3. At the most abstract

level, financial intermediaries exist to carry out two functions. First, they execute instructions

to change portfolio weights. That is, following a change in one or all of the stochastic

processes driving consumption, wealth or returns, the intermediary will adjust investors’

portfolios so that they continue to maximize utility In addition, if one investor wishes to

transfer some wealth to another for some reason, the intermediary will effect the transaction.

For policy to even exist, some government authority, such as a central bank, must be the

monopoly supplier of a nominally denominated asset that is imperfectly substitutable with all

other assets (outside money). In the current environment, it is the monetary base. Reserve

requirements and the use of reserves for certain types of hank clearings are examples.

With this as background, it is now possible to sketch the two major views of the monetary

transmission mechanism. There are a number of excellent surveys of these theories, including

Bernanke (1993a), Gertler and Gilchrist (1993), Kashyap and Stein (l994a) and Hubbard

(1995).

MONEY VIEV

The first theory commonly labeled the money view is based on the notion that reductions in

the quantity of outside money raise real rates of return; this in turn reduces investment

because fewer profitable projects are available at higher required rates of return. This is a

movement along a fixed marginal efficiency of investment schedule. The less substitutable

outside money is for other assets and the larger the interest rate changes. There is no real need

to discuss banks in this context; In fact, there is no reason to distinguish any of the “other”

assets in investors’ portfolios. In terms of the simple portfolio model, the money view implies

15

that the shift in the Wi* s for all of the assets excluding outside money are equal. An

important implication of this traditional model of the transmission mechanism involves the

incidence of the investment decline. Since there are no externalities or market imperfections,

it is only the least socially productive projects that go unfunded. The capital stock is

marginally lower. But, given that a decline is going to occur, the allocation of the decline

across sectors is socially efficient.

This theory actually points to a measure of money that is rarely studied, most empirical

investigations of monetary policy transmission focus on M2, but the logic of the portfolio

view suggests that the monetary base is more appropriate. It is also worth pointing out that

investigators have found it extremely difficult to measure economically significant responses

of either fixed or inventory investment to changes in interest rates that are plausibly the result

of policy shifts, In fact, most of the evidence that is interpreted as supporting the money view

is actually evidence that fails to support the lending view.

THE LENDING VIEW BALANCE SHEET THEORY

The second theory of monetary transmission is the lending view. It has two parts, one that

does not require introduction of assets such as hank loans, and one that does. The first is

sometimes referred to as the broad lending channel, or financial accelerator, and emphasizes

the impact of policy changes on the balance sheets of borrowers. It has substantial similarity

to the mechanism operating in the money view, because it involves the impact of changes in

the real interest rate on investment. According to this view, there are credit market

imperfections that make the calculation of the marginal efficiency of investment schedule

more complex. Due to information asymmetries and moral hazard problems, as well as

bankruptcy laws, the state of a firm’s balance sheet has implications for its ability to obtain

external finance. Policy-induced increases in interest rates (which are both real and nominal)

can cause deterioration in the firm’s net worth, by both reducing expected future sales and

increasing the real value of nominally denominated debt, with lower net worth, the firm is less

creditworthy because it has an increased incentive to misrepresent the riskiness of potential

projects. As a result, potential lenders will increase the risk premium they require when

making a loan. The asymmetry of information makes internal finance of new investment

projects cheaper than external finance.

16

The balance sheet effects imply that the shape of the marginal efficiency of investment curve

is itself a function of the debt-equity ratio in the economy and can be affected by monetary

policy In terms of a simple textbook analysis, policy moves both the IS and the LM curves.

For a given change in the rate of return on outside money (which may be the riskless rate), a

lender is less willing to finance a given investment the more debt a potential borrower has.

This point to two clear distinctions between the money and the lending views; the latter

stresses both the distributional impact of monetary policy and explains how seemingly small

changes in interest rates can have a large impact on investment (the financial accelerator).

Returning to the portfolio choice model, the presence of credit market imperfections means

that policy affects the covariance structure of asset returns. As a result, the Wi*s will shift

differentially in response to monetary tightening as the perceived riskiness of debt issued by

firms with currently high debt-equity ratios will increase relative to that of others. The second

mechanism articulated by proponents of the lending channel can be described by dividing the

“other” assets in investors’ portfolios into at least three categories: outside money, “loans”

and all the others. Next, assume that there are firms for which loans are the only source of

external funds some firms cannot issue securities. Depending on the solution to the portfolio

allocation problem, a policy action may directly change both the interest rate and the quantity

of loans, It is not necessary to have a specific institutional framework in mind to understand

this, Instead, it occurs whenever loans and outside money are complements in investor

portfolios; that is, whenever the portfolio weight on loans is a negative function of the return

on outside money for given means and covariance of other asset returns.

These arguments have two clear parts. First, there are borrowers who cannot finance new

projects except through loans, and second, policy changes have a direct effect on loan supply

Consequently the most important impact of a policy innovation is cross-sectional, as it affects

the quantity of loans to loan-dependent borrowers. Most of the literature on the lending view

focuses on the implications of this mechanism in a world in which banks are the only source

of loans and whose abilities are largely reservable deposits. In this case, a reduction in the

quantity of reserves forces a reduction in the level of deposits, which must be matched by a

fall in loans. The resulting change in the interest rate on outside money will depend on access

to close bank deposit substitutes. But the contraction in bank balance sheets reduces the level

of loans. Lower levels of bank loans will only have an impact on the real economy insofar as

there are firms without an alternative source of investment funds. As a theoretical matter, it is

17

not necessary to focus narrowly on contemporary banks in trying to understand the different

possible ways in which policy actions have real effects. As emphasized, bank responses to

changes in the quantity of reserves are just one mechanism that can lead to a complementarity

between outside money and loans. As pointed out by Romer and Romer (1990), to the extent

that there exist ready substitutes in bank portfolios for reservable deposits such as CDs, this

specific channel could he weak to nonexistent. But it remains a real possibility that the

optimal response of investors to a policy contraction would be to reduce the quantity of loans

in their portfolios. The portfolio choice model also helps to make clear that the manner in

which policy actions translate into loan changes need not be a result of loan rationing,

although it may as Stiglitz and Weiss (1981) originally pointed out, a form of rationing may

arise in equilibrium as a consequence of adverse selection, But the presence of a lending

channel does not require that there be borrowers willing to take on debt at the current price

who are not given loans. It arises when there are firms which do not have equivalent

alternative sources of investment funds and loans are imperfect substitutes in investors’

portfolios. Obviously, the central bank can take explicit actions directed at controlling the

quantity of loans. Again, lowering the level of loans will have a differential impact that

depends on access to financing substitutes. But the mechanism by which explicit credit

controls influence the real economy is a different question.

Distinguishing the two Views; General Consideration

Distinguishing between these two views is difficult because contractionary monetary policy

actions have two consequences, regardless of the relative importance of the money and

lending mechanisms. It both lowers current real wealth and changes the portfolio weights.

Assuming that there are real effects, contractionary actions will reduce future output and

lower current real wealth, reducing the demand for all assets. In the context of standard

discussions of the transmission mechanism, this is the reduction in investment demand that

arises from a cyclical downturn. The second effect of policy is to change the mean and

covariance of expected asset returns, this changes the w1’s. In the simplest case in which there

are two assets, outside money and everything else, the increase in the return on outside money

will reduce the demand for everything else. This is a reduction in real investment. The lending

view implies that the change in portfolio weights is more complex and in an important way

there may be some combination of balance sheet and loan supply effects. This immediately

18

suggests that looking at aggregates for evidence of the right degree of imperfect

substitutability or timing of changes may be very difficult, What seems promising is to focus

on the other distinction between the two views the lending view’s assumption that some firms

are dependent on loans for financing. In addition to differences stemming from the relative

importance of shifts in loan demand and loan supply the lending view also predicts cross-

sectional differences arising from balance sheet considerations; these are also likely to be

testable. In particular, it may be possible to observe whether, given the quality of potential

investment projects, firms with higher net worth are more likely to obtain external funding.

Again, the major implications are cross-sectional.

2.1.2 THE CHANNELS OF MONETARY TRANSMISSION

There are three main types of monetary transmission mechanism models found in the

literature: the interest rate channel, the asset channel and the credit channel (Seyrek and

others, 2004). According to the monetary transmission mechanism, money supply is active

and, in the short term, monetary tools and increased money supply reduce interest rates.

Hence the liquidity effect is only short-term. The drop in interest rates increases credit value.

This situation causes a short-term increase in income. In the long term, the increased price in

money supply increases its general level and the real value of money stock declines.

According to the Monetarist approach, money supply is active during these processes and is

controlled by the Central Bank. According to the Keynesian approach, monetary politics tools

affect the monetary base first, then the money supply. Following this, the changes in money

supply affect interest rates, which in turn affect investments and then revenues. New

Keynesian economics argues that money supply is passive. Rather than the Central Banks’

exported money supply, credit money is determined according to the banks’ credit

preferences. When economic units use credit, deposits created by credit multiply. The passive

money hypothesis presumes that causality moves away from credits towards deposits. Credit

demands are set by the preferences of the credit applicants and creditor. For this reason,

Central Banks do not have control over credits, and therefore, money stocks (Shanmugan and

others, 2003). There are three approaches with regard to passive money stock;

accommodationalist, structuralist and liquidity preference. According to the

accommodationalists (Moree, 1989) credits are the source of money supply and money base,

and that money supply and money revenue (GDP) are co-integrated and interdependent.

According to the structuralists (Palley, 1996, 1998; Pollin 1991) credits are the source of

19

money supply, money base and money multipliers and that money supply and money revenue

(GDP) are co-integrated and interdependent. Finally, according to liquidity preference

theorists (Howells, 1995), credits and money supply are co-integrated and interdependent.

There is a wide argument that monetary policy is a tool promoting economic growth and

stabilizing inflation. However there is a less argument about how policy exactly exacts its

influence. Most of these frequently regard monetary transmission mechanism as a ‘black box’.

In other to make accurate assessment of the magnitude, timing and duration of monetary

policy, the policy maker needs to understand the mechanism through which monetary policy

affects the economy. Mishkin (1995) points out that the monetary transmission mechanism

includes the interest rate channel, the exchange rate channel the asset price channel and the

credit channel.

The Interest Rate Channel

The interest rate channel is the primary monetary transmission mechanism in the

conventional macroeconomic models, such as the IS-LM model. Those models holds that

monetary policy operates through the liability side of the balance sheets: giving some degree

of price stickiness, a change in money is transmitted to the real economy through its impact on

the cost of capital and consumption. In contrast, bank loans, which are one of the bank assets,

are regarded as the instrument in the bond market and then it can conveniently be suppressed

by Walras’ Law. However as pointed out by Bernaken and Gertler (1995), the study have had

a great difficulty in identifying quantitatively important effects of interest policy induced

interest charges is considerable large than that implied by conventional estimate of the interest

elasticity of consumption and investment these observation suggest that mechanism other than

interest rate channel may also work in the transmission of monetary policy.

Drawing from the various theories on the channels of monetary policy transmission the

Keynesian theory of the channel of monetary policy is prescribed as the framework for

analyzing the transmission channels of monetary policy to real sectorial outputs Mishkin

(2004). In the Keynesian approach, a discretionary change in monetary policy affected the real

economy through the two sides of market forces, the demand and supply sides. From the

aggregate demand side, monetary policy is transmitted either directly through three channels;

the exchange rate, the interest rate and asset channel or indirectly through the bank credit

which is transmitted through two channels: the bank-lending channel and the balance sheet

20

channel. From the supply side, monetary policy impulse affected real variables via changes in

inventory cost (Baksh and Craitgwell, 1997), or indirectly through the bank credit which was

transmitted through two channels: the bank-lending channel and the balance sheet channel.

From the supply side, monetary policy impulse affected real variables via changes in

inventory cost (Baksh and Craitgwell, 1997). While acknowledging the supply side channel,

this study adopted aggregate demand side channels. For two reasons; first, in Keynesian

framework, the aggregate supply was relatively fixed due to stickiness of price at least in the

short run. Second, the Nigerian economy is structurally weak and not well developed to allow

the necessary adjustment to take place if the inventory cost approach is to be relevant. The

economic intuition behind the aggregate demand channels of policy influence on real

variables is usually described by the traditional Keynesian (IS-LM) framework. The

framework focused on the equilibrium position between the demand for and the supply of

money to determine the rate of interest, which influenced investment spending and

consequently output level (Dornbusch et al, 2002). It dichotomized the economy into real and

money sector. The IS curve represented equilibrium in the real sector while the LM curve

represented equilibrium in the money

An important observation with the theoretical exposition above is that interest rate is cardinal

in any channel monetary policy passes through to the real sector. So in recognizing this fact,

the channel that formed the basis for the subsequent analysis was represented schematically

as:

Ms↑→i↓→ PSC↑→Ps↑→Er↓→I↑→Y↑

Ms↑ indicates expansionary monetary policy resulting from government purchases of

securities in the open market, leading to a fall in real interest rate, which in turn: (a) increases

the amount of credit by banks to the private sector; (b) increases in the price of security prices

given the inverse relationship between security prices and interest rate and (c) decreases in

exchange rate; these effects stimulate investment and consequently output.

According to the traditional Keynesian interest rate channel, a policy-induced in the short-

term nominal interest rate leads first to a long-term nominal interest rates. Investors act to

arbitrage away differences I risk-adjusted expected return on debt instrument of various

maturities as described by the expectation hypotheses of the term structure. When nominal

prices are slow to adjust, these movement in nominal interest rest rate translate in to

movement in real interest rate. Firms finding their real cost of borrowing over all horizons has

21

increased, cut back on their investment expenditure. Likewise, house hold facing higher real

borrowing cost scale back on their consumption, thereby reducing the aggregate demand,

output and employment. This interest rate channel lies at the heart of the traditional

Keynesians-LM model, due originally to Hicks (1937). And also appear in more recent new

Keynesian models. The interest rate channel is the key monetary policy transmission

mechanism in the basic Keynesian IS-LM model. It is the traditional mechanism and the one

often regarded as the main channel of monetary policy transmission it can be summarized as

follows: M↑ → ir ↓ → I → Y↑. Where: M = money supply, ir = Real Interest Rate, I =

Investment spending and Y = Output. These shows that the expansionary monetary policy

leads to a fall in real interest rates, which in turn lower the cost of capital causing a rise in

investment spending which then increases aggregate demand and output (Mishkin 1996).

The basic idea is straightforward: given some degree of price stickiness, an increase in

nominal interest rates, for example, translates into an increase in the real rate of interest and

the user cost of capital. These changes in turn lead to a postponement in consumption or a

reduction in investment spending and, hence, the output level and prices. The effectiveness of

monetary policy will depend not only on its ability to affect the real interest rate, but also on

the sensitivity of consumption and investment to changes in the price of inter-temporal

substitution. The elasticity of aggregate demand to the interest rate both absolute and relative

will determine how, when, and to what extent the monetary policy will affect the economy.

This basic model, however, would only be complete if the economy‘s financial portfolio

consisted solely of bonds and money, with no other assets available to agents. If a richer

economic structure is recognized, the economy no longer depends on a single interest rate, so

the direct effect of policy actions on consumption and investment fades.

This is precisely the mechanism embodied in conventional specifications of the IS curve

whether of the Old Keynesian variety, or the forward-looking equations at the heart of the

New Keynesianẑ macro models developed by Rotemberg and Woodford (1997) and Clarida,

Galí, and Gertler (1999), among others. But as Bernanke and Gertler (1995) have pointed out,

the macroeconomic response to policy-induced interest rate changes is considerably larger

than that implied by conventional estimates of the interest elasticity of consumption and

investment. This observation suggests that mechanisms other than the narrow interest rate

channel may also be at work in the transmission of monetary policy.

22

However Arto Kovanen (2011) posits that monetary policy implementation in countries where

financial markets are sufficiently deep and liquid rests on the interest rate channel whereas

monetary aggregates usually are less important for monetary policy. This increased “market

orientation” of monetary policy implementation involves a short-term market interest rate as

the operating target of monetary policy. In this type of framework, for monetary policy to

have a desired impact on the real economy and inflation, which is the ultimate objective of

monetary policy, it is essential that changes in the short-term market interest rate eventually

translate into changes in other interest rates in the economy (that is, interest rate changes are

passed through to retail interest rates for loans and deposits), which then influence the overall

level of economic activity and prices. The interest rate channel is increasingly relevant in

many developing and emerging market countries as well, as countries find it difficult to

achieve their quantitative targets in these countries; monetary policy usually operates through

the targeting of the quantity of reserve money. These countries often have less developed,

shallow financial markets, which itself introduces challenges for monetary policy

implementation and contributes to the weaknesses in the transmission through the interest rate

channel. A good example of such country includes Nigeria and Ghana where monetary policy

is presently implemented in the context of an inflation-targeting framework which Ghana

formally introduced in 2007. This replaced “money targeting” as the operating model for

monetary policy. The Bank of Ghana uses a short-term money market interest rate as its

operating target where changes in the short-term interest rate are expected to influence the

cost of funding for banks and eventually the level of retail deposit and lending interest rates.

The ability to hit the interest rate target consistently plays a critical role in monetary policy

effectiveness. It is also essential for the communication of central bank’s policy stance to the

public Keister (2008). If the market interest rate were to deviate time and again from the

central bank’s announced target, the public might begin to question whether these deviations

represent a glitch in the implementation process or whether they amount to an undisclosed

change in the stance of monetary policy. Such easing or tightening by “stealth”, as one might

call it, would undermine the credibility of monetary policy. An important issue in this respect

is whether central bank’s liquidity forecasting and liquidity management are adequate or

whether short coming in these areas contribute to the rate deviations from the target.

Furthermore, when short-term market interest rates are sensitive to changes in the supply and

demand for liquidity, small errors in central bank’s liquidity forecasts could lead to large

23

swings in the short-term interest rates. In such an environment, the central bank might find it

difficult to an important exception is the European Central Bank, which has assigned a role

for broad money in monetary policy. In the U.S., on the other hand, monetary aggregates are

considered to be of limited importance. The effects of these shocks may be amplified by

illiquid or shallow financial markets.

Goodfriend (1991) posits that the transmission of interest rate changes through the interest

rate channel should ideally take place over a relatively short period of time as a faster

transmission would strengthen the impact of monetary policy on the real economy. Due to a

confluence of factors, however, the short-run interest rate pass-through may be less than

complete in reality and interest rates may also adjust asymmetrically to rising and falling

policy interest rates. The sluggishness of pass-through is evident in the many studies that have

examined the speed of interest rate adjustment. Countries with deep and well developed

financial markets, such as the U.S. and the European common currency area, the speed and

completeness of the interest rate pass-through differs (Kwapil and Scharler (2010) and

Karagiannis et al. (2010)). These differences in part reflect the country-specific features of

financial markets (for instance, in Europe the banking system plays a more significant role in

lending than in the U.S.). In developing countries, due to the underdevelopment and

shallowness of financial markets and the transmission process dominated by bank lending

channel, the structure of financial markets plays an important role in the transmission process

(Mishra, Montiel, and Spilimbergo (2010)). Deficiencies in the financial system and high

concentration among banks reduces competitiveness, while large excess reserves make central

bank’s monetary policy less effective and impairs the interest rate channel. Sander and

Kleimeier (2006) note that in the Southern African Customs Union (SACU) countries the

interest rate channel works differently for deposits and lending rates. While the pass-through

is rather uniform and complete for retail lending interest rates, there is a great deal of

heterogeneity across the national markets and differing degrees of interest rate stickiness and

asymmetry in the adjustment of retail deposit interest rates.

Despite its increasing relevance for monetary policy implementation, the interest rate

transmission process is not extensively studies in most African countries. An exception is

Ghartey (2005) who examines the impact of monetary policy on the term structure of interest

rates in Ghana during 1994-2004 and reports that there is a significant effect from monetary

policy to Treasury bill interest rates.

24

The traditional Keynesian ISLM view of the monetary transmission mechanism can be

characterized by the following schematic showing the effects of a monetary expansion.

M↑→ir↓→ ir↓→Y↑

Where M↑ indicates an expansionary monetary policy leading policy to a fall in real interest

(ir↓), which in turn lowers the cost of capital, causing a rise in investment spending (ir↓),

there by leading to an increase in aggregate demand a rise in output (Y↑). Although Keynes

originally emphasized this channel as operating through businesses’ decision about

investment spending. Thus, the interest rate channel of monetary transmission outlined in the

schematic above applies equally to consumer spending in which I represent residential

housing and consumer durable expenditure. An important feature of the interest transmission

mechanism is its emphases on the real rather than the nominal interest rate as that which

affects consumer and business decisions. In addition, it is often the real long-term interest rate

and not the short-term interest rate that is viewed as having the major impact on spending. It is

that that changes in the short-term nominal interest rate induced by a central bank result in a

corresponding change in the real interest rate on both long and short-term bonds. The key is

sticky prices, so that expansionary monetary policy which lowers the short-term nominal

interest rate and also lowers the short-term real interest rate, and this would still be true even

in a world with rational expectations. The expectation hypotheses of the term structure, which

states that the long interest rate is an average of expected future short-term interest rate,

suggest that lower real short-term interest rate leads to a fall in real long-term interest rate.

These lower real interest rates then leads to rise in business fixed investment, residential

housing investment, consumer durable expenditure and inventory investment, all of which

produce the rise in aggregate output.

The fact that it is the real interest rate that impact on the spending rather than the nominal rate

provides an important mechanism for how monetary policy can stimulate the economy, even

if nominal interest rates hits a floor of zero during a deflationary episode. With nominal

interest rate at a floor of zero, an expansionary in the money supply (M↑) can raise the

expected price level (Pe↑) and hence expected inflation ( ), thereby lowering the real interest

rate (ir↓) even when the nominal interest is fixes at zero, and stimulating spending through the

interest rate channel. That is, M↑→ Pe↑→ ↓→ ir↓→ I↑ Y↑

25

This mechanism thus indicates that monetary policy can still be effective even when nominal

interest rate have already been driven down to zero by the monetary authorities. Indeed, this

mechanism is a key element in monetarist discussion of why the U.S economy was not stuck

in liquidity during the Great depression and why expansionary monetary policy could have

prevented the sharp decline in output during this period.

Taylor (1995) has an excellent survey of the recent research on interest rate channel and he

takes a position that there is strong empirical evidence for substantial interest rate effect on

consumer and investment spending, making the interest rate monetary transmission a stronger

one. His position is highly a controversial one because many researchers, for example

Bernake and Gertler (1995), have an alternative view that empirical studies have had great

difficulty in identifying sufficient effect if interest rate through the cost of capital.

The Credit Channel

According to the credit channel theory of the monetary transmission mechanism, frictions in

credit markets that generate a wedge between the costs of raising funds externally and

internally, the external finance premium, help explain the effect of monetary policy on real

variables. For example, the cost of monitoring in credit markets suggests poorly collateralized

borrowers will pay a higher premium for external funds than larger, more-collateralized

borrowers. The credit channel of monetary policy is a mechanism through which the impact of

monetary policy shocks on the real economy is amplified through its effect on external

finance premiums. In particular, by affecting this wedge counter cyclically, monetary policy

has an additional impact on real variables beyond its standard effect through the cost of

capital.

Bernanke and Gertler (1995), posits that the credit channel mainly operates through two

conduits: the balance sheet channel, in which monetary policy affects borrowers’ net worth

and debt collateral, and the bank lending channel, in which policy impacts the level of

intermediated credit. These channels have been incorporated into general equilibrium models

through costly-state-verification to enhance their empirical relevance. (Bernanke et al., 1999).

A key result from these models is that the strength of both channels and therefore the broader

credit channel increases with the level of financial frictions. Since alternative sources of credit

are very limited or even non-existent customers in developing countries cannot replace lost

bank credit with other types of finance and so are forced to cut back on investment spending.

26

If the credit channel is operational it means monetary policy is likely to have its impact via the

asset side of the balance sheet because a fall in reserves reduces the quantity of loans that can

be made available. According to Ramey (1993) there are two key conditions that must be

satisfied before a lending channel can be made operational. First, banks must not be able to

shield their loan portfolio from changes in monetary policy and, second, borrowers must not

be able to fully insulate their real spending from changes in the availability of bank credit.

Due to the dissatisfaction with the money view prompted an alternative the credit channel

approach. The credit channel comprises two separate channels: a broad lending channel and a

bank-lending channel. The idea of the broad lending channel is that information asymmetries

and moral hazard restrict the ability of firms to obtain external finance to the extent that a

restrictive monetary policy causes deterioration in the firm’s net worth and credit worthiness.

This aspect of the credit channel resembles the money view since it involves the impact on

investment of changes in the real interest rate. To this end the broad lending channel may be

regarded as an enhancement of the money channel. The bank-lending channel is perhaps more

relevant in developing countries because it is based on the premise that investment projects

are primarily financed by bank loans and that the supply of loans is directly influenced by

changes in policy. Since alternative sources of credit are very limited or even non-existent

customers in developing countries cannot replace lost bank credit with other types of finance

and so are forced to cut back on investment spending.