Embed Size (px)

Citation preview

Abide Financial

Trade & Transaction Reporting

25 November 2016 Confidential 2

Trade and Transaction Reporting – Recent Updates

Trading Obligation Discussion Paper Published

Final Version of Level 3 Guidance Published

Mandatory Systematic Internaliser Regime Deferred for 6 Months Due to unavailability of data for threshold calculations Does not extend to post-trade transparency – this will start from Jan

2018 on the basis of ESMA liquidity estimates Fewer SIs available to take on transparency reporting More post-trade reporting to APAs, especially by

Bond traders Asset Managers

Share trading obligation means Opt-In SIs likely in this market

25 November 2016 Confidential 3

Trading Obligation Update

Discussion Paper published in September 2016

Process to be followed is:

Clearing obligation under EMIR established for instrument class and in effect Trading of instrument begins on trading venues Liquidity and other factors assessed by ESMA Trading obligation declared

Current DP Proposal

Only major currency interest rate swaps, FRAs and CDS so far slated for Clearing Obligation

FRAs excluded for Trading Obligation, leaving IRS and Index CDS Earliest TO date for IR and CDS 3 January 2018 TO for Derivatives, unlike shares, mandates trading on RMs, MTFs or OTFs, excludes SIs

25 November 2016 Confidential 4

Level 3 Final Guidance

Entity Identifiers CONCAT cannot be used as a default No obligation to monitor or follow up on expired national identifiers, eg passport SIs have a MIC code, which must be used by them and by those dealing with them

Transactions Re-use of TRNs for amended trades. Previously new TRN was required. Obliges correct order. OTFs and Investment Firms can use INTC in MTCH capacity when matching disparate buy/sell

quantities

Instruments

For XXXX underlying can be ISIN OR Index Name

Other

Removal of give-up differentiation Downstream reporting requirements for venues with non-MiFID members

25 November 2016 Confidential 5

Transaction Reportability Assessment – MiFID 2Qualifying criteriaMiFID 2 Included in the ESMA Reference Data OTC based on immediate underlying ISIN(s) from the Reference Data, or Named Index or Basket with at least one ISIN from the Reference Data

Sources of Reference Data Regulated Markets, MTFs, OTFs Benchmark Index Publishers (eg FTSE, LIBOR)

Practical outcomesIN Equities, Bonds, ETFS etc listed in EEA (any venue) EEA Exchange Traded Derivatives OTC derivatives on EEA products above OTC derivatives based on Indices with 1+ underlying Non-EEA ETDs with immediate underlying in ESMA list

OUT Non-EEA ETDs without immediate underlying in ESMA

list OTC derivatives based on spot prices (EUR/USD, Gold) OTC derivatives based on non-EEA ETDs (CBOT,CME) OTC derivatives based on non-EEA Index Futures (no imm

u/l)

25 November 2016 Confidential 6

Transaction Reporting and Trade Publication Summary

Trade Category Transaction Reporting Trade Publication

EEA Venue-listed instrument, traded on-venue Y Y (Venue) *

EEA Venue-listed instrument, traded off-venue Y Y (SI or Firm) *

Non-EEA ETD with underlying in ESMA List Y N

Non-EEA ETD with no underlying in ESMA List N N

Unlisted derivative with underlying in ESMA list Y N

Unlisted derivative with no underlying in ESMA list N N

* Trade Publication obligation is on the first of the parties below to be involved in the transaction

1 EEA Venue

2 Selling Systematic Internaliser

3 Buying Systematic Internaliser

4 Selling Investment Firm

5 Buying Investment Firm

6 if none of the above are involved, no trade publication is required

25 November 2016 Confidential 7

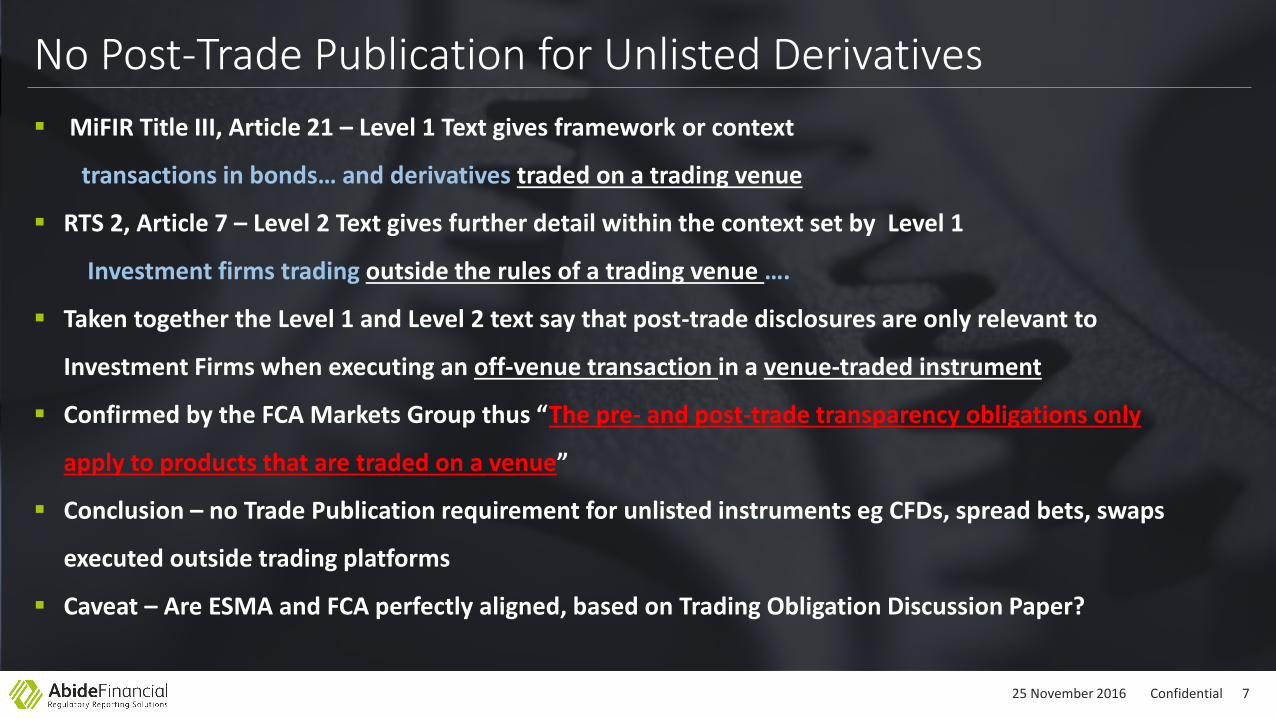

No Post-Trade Publication for Unlisted Derivatives

MiFIR Title III, Article 21 – Level 1 Text gives framework or context

transactions in bonds… and derivatives traded on a trading venue

RTS 2, Article 7 – Level 2 Text gives further detail within the context set by Level 1

Investment firms trading outside the rules of a trading venue ….

Taken together the Level 1 and Level 2 text say that post-trade disclosures are only relevant to

Investment Firms when executing an off-venue transaction in a venue-traded instrument

Confirmed by the FCA Markets Group thus “The pre- and post-trade transparency obligations only

apply to products that are traded on a venue”

Conclusion – no Trade Publication requirement for unlisted instruments eg CFDs, spread bets, swaps

executed outside trading platforms

Caveat – Are ESMA and FCA perfectly aligned, based on Trading Obligation Discussion Paper?

25 November 2016 Confidential 8

The Lightest Reporting Burden – Trading XXXX without Opt-In

Trades

Trading Day Close of Business

Back Office Systems

NCAABIDE ARM

T+1

25 November 2016 Confidential 9

Trades

Trading Day Close of Business

Back Office Systems

NCA

InstrumentReference Data

ABIDE ARM

ConfirmationsError DetailsMI Reports

Transactions

T+1

Half and Half – The Opt-In XXXX Systematic Internaliser

25 November 2016 Confidential 10

Trades

Trading Day Close of Business

Back Office Systems

CTP

Trade Detailsinc waivers

ConfirmationsReference IDs

Nacks

NCA

InstrumentReference Data

ARM (or NCA)Confirmations

Error DetailsMI Reports

Transactions

T+1

Quotes

A Day In The Life – The EU Venue

Public

25 November 2016 Confidential 11

OTC Derivatives Trading – Choose your own destiny?

Venue Listing Opt-In Systematic Internaliser Unlisted Bilateral Trading

Obtain MIC Code Obtain MIC code -

Obtain instrument ISINs from NNA Obtain instrument ISINs from ANNA/EZT tool -

Submit reference data to NCA Submit reference data to NCA -

Pre-Trade Transparency (Quotes) - -

Post-Trade Publication to Market - -

T+1 Transaction Report (non-MiFID members) T+1 Transaction Report (Own Trades) T+1 Transaction Report (Own Trades)

For unlisted OTC derivatives which are transaction reportable (CFDs, Swaps, Forwards), you can:1. List on a venue and trigger all of the requirements in the first column2. Register as an opt-in systematic internaliser for that class and submit reference data, or3. Carry on trading bilaterally and have no obligations except for T+1 Transaction Reporting

ESMA Tools for moving instruments towards the left column – Trading Obligation and Equivalence

25 November 2016 Confidential 12

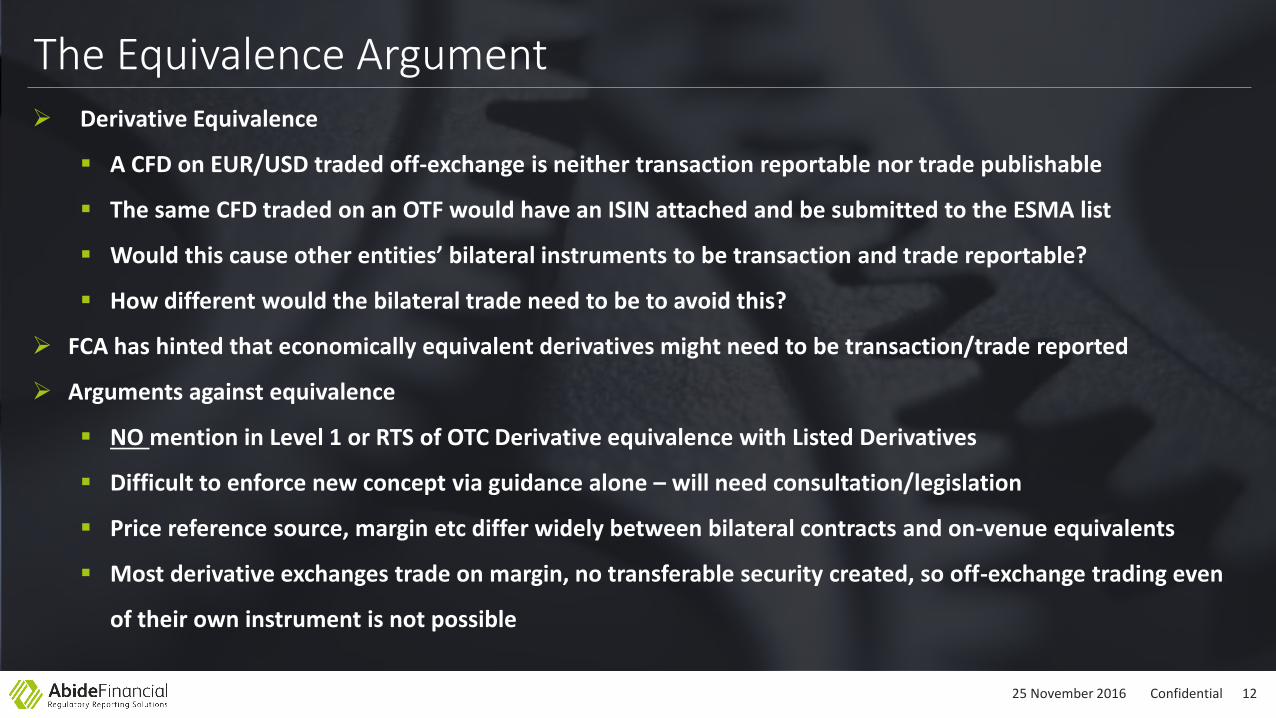

The Equivalence Argument Derivative Equivalence

A CFD on EUR/USD traded off-exchange is neither transaction reportable nor trade publishable

The same CFD traded on an OTF would have an ISIN attached and be submitted to the ESMA list

Would this cause other entities’ bilateral instruments to be transaction and trade reportable?

How different would the bilateral trade need to be to avoid this?

FCA has hinted that economically equivalent derivatives might need to be transaction/trade reported

Arguments against equivalence

NO mention in Level 1 or RTS of OTC Derivative equivalence with Listed Derivatives

Difficult to enforce new concept via guidance alone – will need consultation/legislation

Price reference source, margin etc differ widely between bilateral contracts and on-venue equivalents

Most derivative exchanges trade on margin, no transferable security created, so off-exchange trading even

of their own instrument is not possible

25 November 2016 Confidential 13

What does OTC Mean? Equity and Equity-like instruments and Bonds

Transferable Securities, which can be held in inventory or with a custodian, and traded on to a third

party without reference to the listing exchange or other venue

OTC means off-exchange trading in a venue-listed instrument (Think XOFF in MiFID 1 terms)

Expect many equity and bond trading houses to publish post-trade and register as SIs

Derivatives

ETDs are not transferable securities. Once bought from a venue, however long the execution chain, a

trade can only be closed out by passing back across the same venue

Trade Publication requirement for EEA listed derivatives traded on margin always falls on the venue,

and no Investment Firm can trigger a post-trade reporting or SI registration requirement.

OTC derivative therefore means an unlisted instrument, created bilaterally between buyer and seller

(Think XXXX in MiFID 1 terms)

25 November 2016 Confidential 14

Summary - Current State of Understanding

Instrument T+1 TR Off-exchange? SI-eligible IF Transparency

EU Venue-traded Transferable Securities (equities and equiv) Y Y Y N

EU Venue-traded Transferable Securities (bonds) Y Y Y Y

EU Venue-traded Securitised Derivatives (eg warrants) Y Y Y Y

EU Venue-traded Margined Futures and Options Y N N N

IR Derivatives subject to Trading Obligation Y N N N

IR Derivatives not subject to Trading Obligation N NA N N

CDS subject to Trading Obligation Y N N N

CDS not subject to Trading Obligation Y Y Y y

Non-EEA ETDs with underlying in reference data Y N N N

Non-EEA ETDs without underlying in reference data N N N N

Unlisted derivative with underlying in reference data Y NA Y N

Unlisted derivative without underlying in reference data N NA N N

Unlisted derivs on index/basket with listed component Y NA Y N

Unlisted derivs on index/basket without listed component N NA N N