Embed Size (px)

Citation preview

0

Published by Investor Relations Unit – Republic of Indonesia

Contact: Wiwit Widyastuti K. (International Department - Bank Indonesia, Phone: +6221 2981 8279)

Abdurohman (Fiscal Policy Office – Ministry of Finance, Phone: +6221 384 6379)

Subhan Noor (Debt Management Office - Ministry of Finance, Phone: +6221 381 0175)

E-mail: [email protected]

ABOUT THE REPUBLIC OF INDONESIA INVESTOR RELATIONS UNIT

The Republic of Indonesia Investor Relations Unit (IRU) has been established as the joint effort between the Coordinating Ministry of Economic Affairs,

Ministry of Finance and Bank Indonesia since 2005. The main objective of IRU is to actively communicate Indonesian economic policy and address

concerns of investors, especially financial market investors. IRU is expected to serve as a single point of contact for the financial market participants.

As an important part of its communication measures, IRU maintains a website under Bank Indonesia website which is being administrated by the

International Department of Bank Indonesia. However, investor relations activities involve a coordinated efforts which are supported by all relevant

government agencies, i.e. Bank Indonesia, the Ministry of Finance, the Coordinating Ministry for Economic Affairs, Investment Coordinating Board,

Ministry of Trade, Ministry of Industry, State Ministry of State Owned Enterprises, State Asset Management Company, and the Central Bureau of

Statistics.

IRU also holds an investor conference call on a quarterly basis, answers questions through email, telephone and may arrange direct visit of

banks/financial institutions to Bank Indonesia and other relevant government offices.

About Investor Relations Unit (IRU)

1

Table of Content

Executive Summary

Preserved Macroeconomic Stability

Improved International Perception and Rising Investment

Prudent Fiscal Management

Government Debt Performance

2

Executive Summary

3

Executive Summary

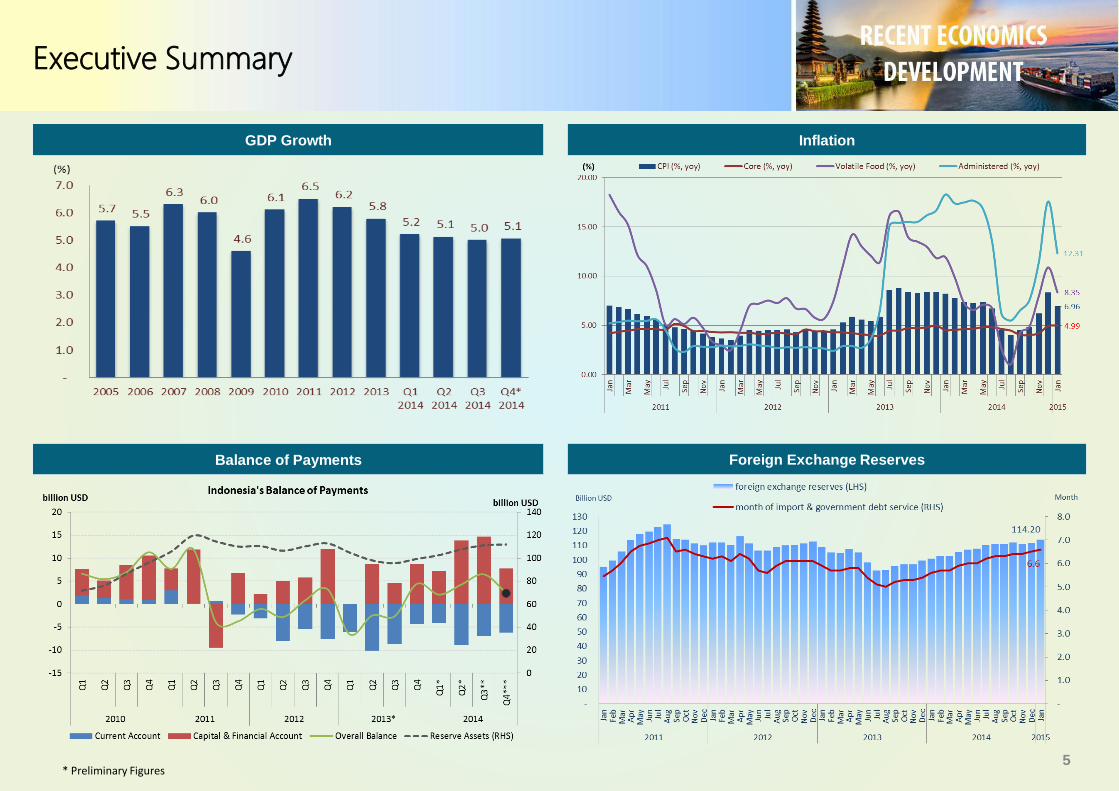

Economic growth accelerated in Indonesia during the fourth quarter of 2014 in comparison to the preceding quarter, despite annual growth

for 2014 slowing down. The Indonesian economy achieved 5.01% (yoy) growth in the fourth quarter, up from 4.92% (yoy) in the previous period.

Despite early signs of improvement during the fourth quarter of 2014, annual growth slowed in 2014 to 5.02%, which is lower than that posted in the

preceding year, consistent with weaker global economic growth and macroeconomic stabilization policy. Stronger economic growth is projected in

2015, in the range of 5.4-5.8%, bolstered by expansive government investment as fiscal capacity expands to catalyze productive economic activity,

including infrastructure development as approved in the 2015 budget.

The Indonesia balance of payments (BOP) improved in the fourth quarter of 2014, primarily due to a smaller current account deficit. The

current account deficit totaled US$6.2 billion (2.81% of GDP) in the fourth quarter, down from US$7 billion (2.99% of GDP) in the third. A growing non-

oil/gas trade surplus, together with a decreasing oil and gas deficit, helped boost current account performance. Meanwhile, the financial and capital

account recorded a large surplus, backed predominantly by foreign direct investment (FDI) congruent with the positive perception investors hold

concerning the domestic economic outlook. In January 2015, the trade surplus totaled US$0.7 billion, exceeding that posted in the preceding quarter,

bolstered by a smaller oil and gas deficit.

Inflation remained under control, thus supporting the prospect of achieving the 2015 inflation target, namely 4±1%. The Consumer Price

Index (CPI) experienced deflation of 0.24% (mtm) in January 2015 as a tangible outcome of lower fuel prices and less intense inflationary pressures on

volatile foods. In addition, core inflation was controlled at a level of 0.61% (mtm) or 4.99% (yoy).

Financial system stability was maintained with the support of steadfast banking system resilience and relatively sound financial market

performance. Banking industry resilience remained solid with credit risk, liquidity risk and market risk well mitigated and the support of a healthy

capital base. At the end of the reporting quarter, the Capital Adequacy Ratio soared to 19.40%, well above the statutory minimum of 8%, while non-

performing loans (NPL) were low and stable at around 2.0%.

On 17th February 2015, the Bank Indonesia Board of Governors decided to lower the BI Rate 25 bps to 7.50%, with the Deposit Facility rate

also reduced 25 bps to 5.50% and the Lending Facility rate maintained at 8.00%, effective 18th February 2015. Such policy measures were

instituted based on Bank Indonesia’s conviction that inflation will remain under control at the lower end of the 4±1% range in 2015 and 2016.

Bank Indonesia will continue to strengthen its monetary and macroprudential policy mix, bolster the payment system and intensify

coordination with the Government in terms of controlling inflation, reducing the current account deficit and promoting structural reforms in order to

support higher economic growth.

On the fiscal front, Indonesia will continue its prudent fiscal management in 2015 with strong commitment to fiscal consolidation. Recent

reform policy represents an essential step and integral part of structural reforms to strengthen economic fundamentals in Indonesia. 2015 revised

budget deficit is projected at a safe level of 1.91% of GDP.4

Executive Summary

GDP Growth Inflation

Foreign Exchange ReservesBalance of Payments

5* Preliminary Figures

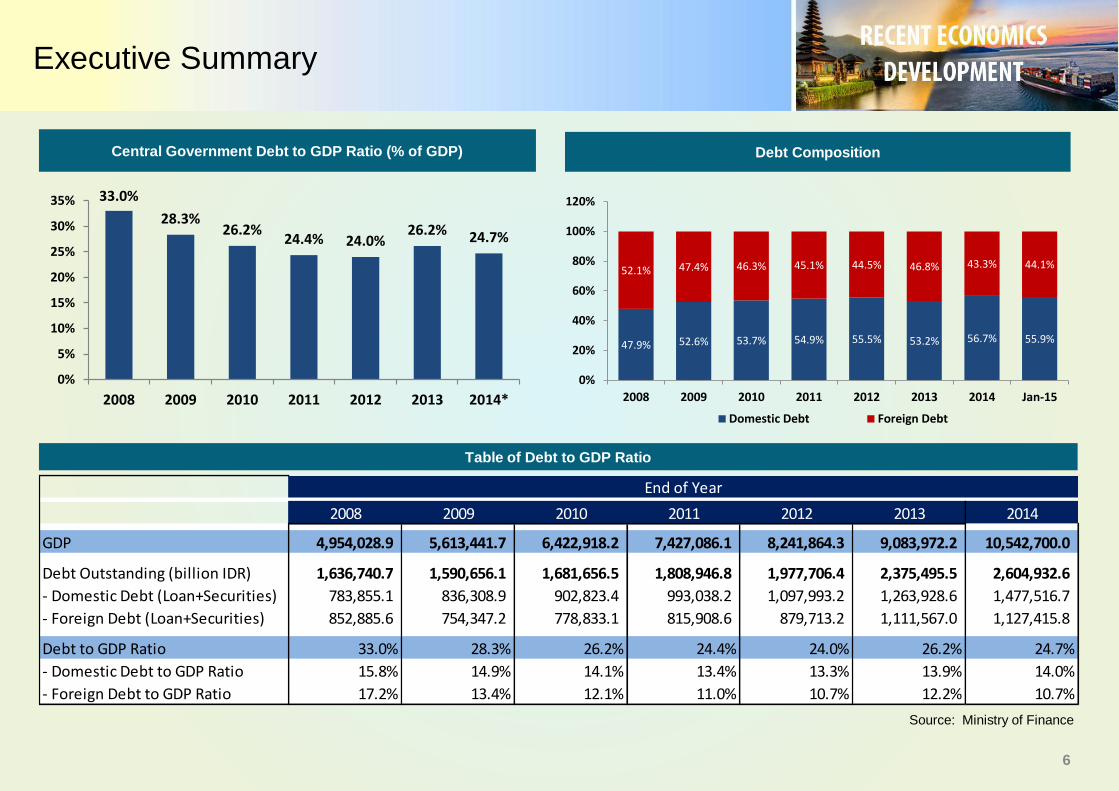

6

Source: Ministry of Finance

Debt Composition

Table of Debt to GDP Ratio

Central Government Debt to GDP Ratio (% of GDP)

47.9% 52.6% 53.7% 54.9% 55.5% 53.2% 56.7% 55.9%

52.1% 47.4% 46.3% 45.1% 44.5% 46.8% 43.3% 44.1%

0%

20%

40%

60%

80%

100%

120%

2008 2009 2010 2011 2012 2013 2014 Jan-15

Domestic Debt Foreign Debt

33.0%

28.3%26.2%

24.4% 24.0%26.2% 24.7%

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2010 2011 2012 2013 2014*

2008 2009 2010 2011 2012 2013 2014

GDP 4,954,028.9 5,613,441.7 6,422,918.2 7,427,086.1 8,241,864.3 9,083,972.2 10,542,700.0

Debt Outstanding (billion IDR) 1,636,740.7 1,590,656.1 1,681,656.5 1,808,946.8 1,977,706.4 2,375,495.5 2,604,932.6

- Domestic Debt (Loan+Securities) 783,855.1 836,308.9 902,823.4 993,038.2 1,097,993.2 1,263,928.6 1,477,516.7

- Foreign Debt (Loan+Securities) 852,885.6 754,347.2 778,833.1 815,908.6 879,713.2 1,111,567.0 1,127,415.8

Debt to GDP Ratio 33.0% 28.3% 26.2% 24.4% 24.0% 26.2% 24.7%

- Domestic Debt to GDP Ratio 15.8% 14.9% 14.1% 13.4% 13.3% 13.9% 14.0%

- Foreign Debt to GDP Ratio 17.2% 13.4% 12.1% 11.0% 10.7% 12.2% 10.7%

End of Year

Executive Summary

2015 Policy Summary

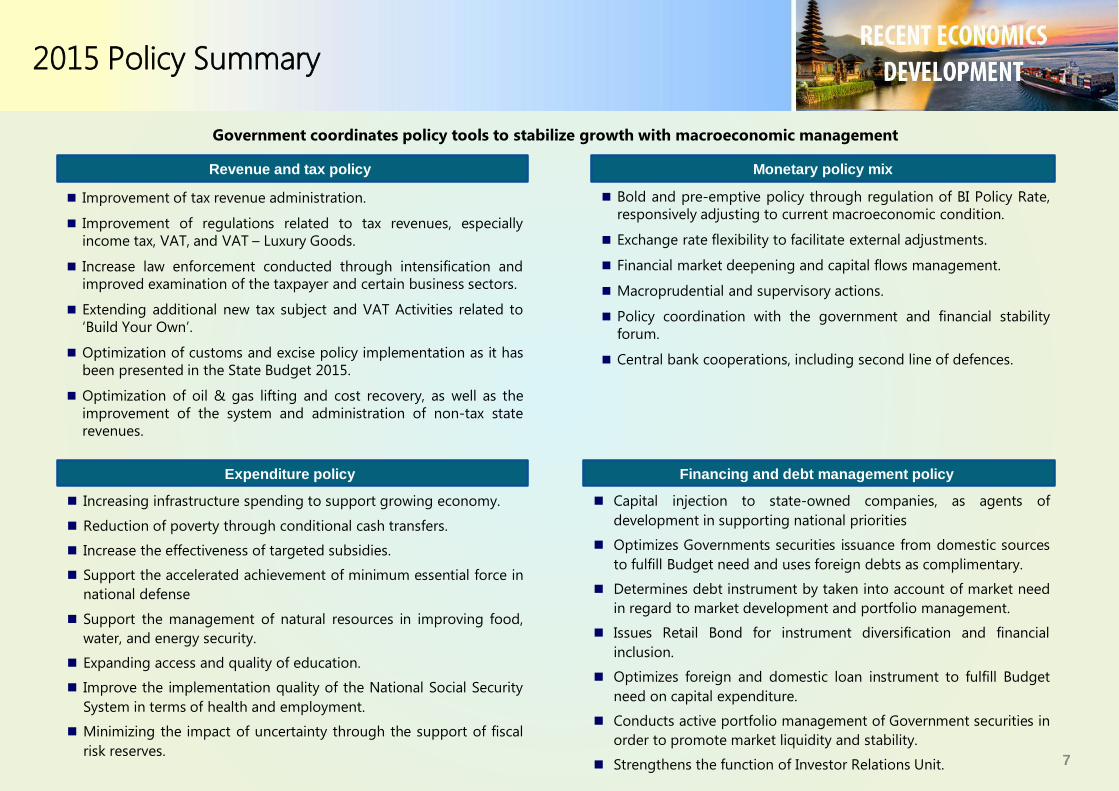

Government coordinates policy tools to stabilize growth with macroeconomic management

Capital injection to state-owned companies, as agents of

development in supporting national priorities

Optimizes Governments securities issuance from domestic sources

to fulfill Budget need and uses foreign debts as complimentary.

Determines debt instrument by taken into account of market need

in regard to market development and portfolio management.

Issues Retail Bond for instrument diversification and financial

inclusion.

Optimizes foreign and domestic loan instrument to fulfill Budget

need on capital expenditure.

Conducts active portfolio management of Government securities in

order to promote market liquidity and stability.

Strengthens the function of Investor Relations Unit.

Revenue and tax policy

Financing and debt management policyExpenditure policy

Monetary policy mix

Bold and pre-emptive policy through regulation of BI Policy Rate,

responsively adjusting to current macroeconomic condition.

Exchange rate flexibility to facilitate external adjustments.

Financial market deepening and capital flows management.

Macroprudential and supervisory actions.

Policy coordination with the government and financial stability

forum.

Central bank cooperations, including second line of defences.

7

Improvement of tax revenue administration.

Improvement of regulations related to tax revenues, especially

income tax, VAT, and VAT – Luxury Goods.

Increase law enforcement conducted through intensification and

improved examination of the taxpayer and certain business sectors.

Extending additional new tax subject and VAT Activities related to

‘Build Your Own’.

Optimization of customs and excise policy implementation as it has

been presented in the State Budget 2015.

Optimization of oil & gas lifting and cost recovery, as well as the

improvement of the system and administration of non-tax state

revenues.

Increasing infrastructure spending to support growing economy.

Reduction of poverty through conditional cash transfers.

Increase the effectiveness of targeted subsidies.

Support the accelerated achievement of minimum essential force in

national defense

Support the management of natural resources in improving food,

water, and energy security.

Expanding access and quality of education.

Improve the implementation quality of the National Social Security

System in terms of health and employment.

Minimizing the impact of uncertainty through the support of fiscal

risk reserves.

Improved International Perception

and Rising Investment

8

Ma

r-99

Dec-9

9

Se

p-0

0

Jun-0

1

Ma

r-02

Dec-0

2

Au

g-0

3

Ma

y-0

4

Feb-0

5

Nov-0

5

Au

g-0

6

Ma

y-0

7

Jan-0

8

Oct-

08

Jul-09

Ap

r-10

Jan-1

1

Oct-

11

Jul-12

Ma

r-13

Dec-1

3

Fitch

Ma

r-99

Dec-9

9

Se

p-0

0

Jun-0

1

Ma

r-02

Dec-0

2

Au

g-0

3

Ma

y-0

4

Feb-0

5

Nov-0

5

Au

g-0

6

Ma

y-0

7

Jan-0

8

Oct-

08

Jul-09

Ap

r-10

Jan-1

1

Oct-

11

Jul-12

Ma

r-13

Dec-1

3

S&P

Ma

r-99

Dec-9

9

Se

p-0

0

Jun-0

1

Ma

r-02

Dec-0

2

Au

g-0

3

Ma

y-0

4

Feb-0

5

Nov-0

5

Au

g-0

6

Ma

y-0

7

Jan-0

8

Oct-

08

Jul-09

Ap

r-10

Jan-1

1

Oct-

11

Jul-12

Ma

r-13

Dec-1

3

Moody's

Mo

od

y’s

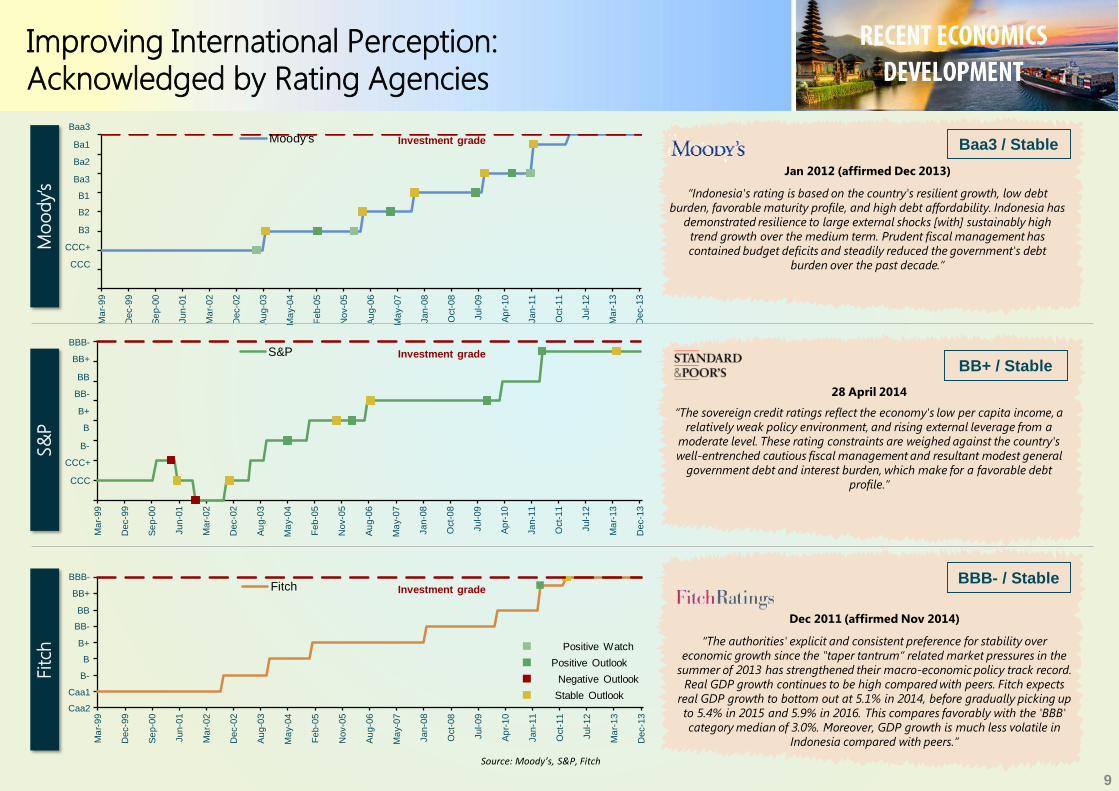

Dec 2011 (affirmed Nov 2014)

“The authorities' explicit and consistent preference for stability over

economic growth since the "taper tantrum“ related market pressures in the

summer of 2013 has strengthened their macro-economic policy track record.

Real GDP growth continues to be high compared with peers. Fitch expects

real GDP growth to bottom out at 5.1% in 2014, before gradually picking up

to 5.4% in 2015 and 5.9% in 2016. This compares favorably with the 'BBB'

category median of 3.0%. Moreover, GDP growth is much less volatile in

Indonesia compared with peers.”

Jan 2012 (affirmed Dec 2013)

“Indonesia's rating is based on the country's resilient growth, low debt

burden, favorable maturity profile, and high debt affordability. Indonesia has

demonstrated resilience to large external shocks [with] sustainably high

trend growth over the medium term. Prudent fiscal management has

contained budget deficits and steadily reduced the government's debt

burden over the past decade.”

28 April 2014

“The sovereign credit ratings reflect the economy's low per capita income, a

relatively weak policy environment, and rising external leverage from a

moderate level. These rating constraints are weighed against the country's

well-entrenched cautious fiscal management and resultant modest general

government debt and interest burden, which make for a favorable debt

profile.”

BBB- / Stable

Baa3 / Stable

BB+ / Stable

Source: Moody’s, S&P, Fitch

Improving International Perception: Acknowledged by Rating Agencies

S&

PFitch

Investment grade

Baa3

B3

B2

B1

Ba3

Ba2

Ba1

CCC+

CCC

Positive Outlook

Negative Outlook

Stable Outlook

Positive Watch

B-

B

B+

BB-

BB

BB+

BBB-

CCC+

CCC

B-

B

B+

BB-

BB

BB+

BBB-

Caa1

Caa2

Investment grade

Investment grade

9

International institutions outlook shows some optimism though there is still downside risk for Indonesia in 2015 …

10

`

IMF Staff Visit (December 2014)

World Bank IEQ (December 2014)

“Sound macroeconomic management has bolstered

policy credibility and external resiliency in Indonesia.”

• GDP growth is projected to be sustained at 5.1 percent in 2015- Recovery in investment

demand - More buoyant manufacture

exports• Inflation is expected to return to

2015 target band (4.0 ±1 percent) by the end of next year.

• Current account deficit is projected to decline to around 2¾ percent of GDP in 2015, supported by rising manufacture exports as well as a lower oil import bill.

Risk• Global headwinds from

weakening commodity prices and tightening financial conditions.

• Slowdown in emerging market trading partners and surges in global financial market volatility.

“The World Bank projects a moderate near-term growth outlook for Indonesia of 5.1-

5.5 %”

• Fuel subsidies adjustment in November 2014 suggests the new government’s commitment and willingness to address many of Indonesia’s long-standing structural priorities.

• The growth in economic activity was moderate in the third quarter of 2014 due to weaker investment and exports while private consumption has continued to support growth.

• The Rupiah has depreciated further against the US dollar since July, but strengthened in real effective terms through October.

Risk• Slower projected global recovery

could weaken commodity price trajectory in the next few years.

• Several implementation challenges faced by the new government, including a complex domestic political environment.

Asian Development Outlook (December 2014)

“GDP growth decelerated further to 5.0% in the third quarter of

2014”

• Private consumption remained robust as expected, however gross fixed investment and net exports contributed less to GDP growth than in the second quarter.

• Investment recovery following the elections has been slower than anticipated, and recovery in export markets remains uncertain.

• The effect of higher administered prices on inflation is expected to be short-lived, and the rate should taper toward the end of 2015.

Risk• Downside risks to this outlook

center on further deterioration of export performance and changes in market sentiment that cause capital outflows

OECD Economic Forecast (November 2014)

“Growth is projected to remain moderate through

2015 before picking up somewhat in 2016…”

• …due largely to an acceleration in investment and firming consumption.

• Economic growth has continued to slow as investment and exports have softened, although household consumption is holding up.

• The current account has widened again, and the rupiah has depreciated as a result.

• The recent second round of cuts in fuel subsidies lift headline inflation, but core measures should remain well anchored,

Risk• Risks to the outlook are

mainly on the external side.

Preserved Macroeconomic Stability

11

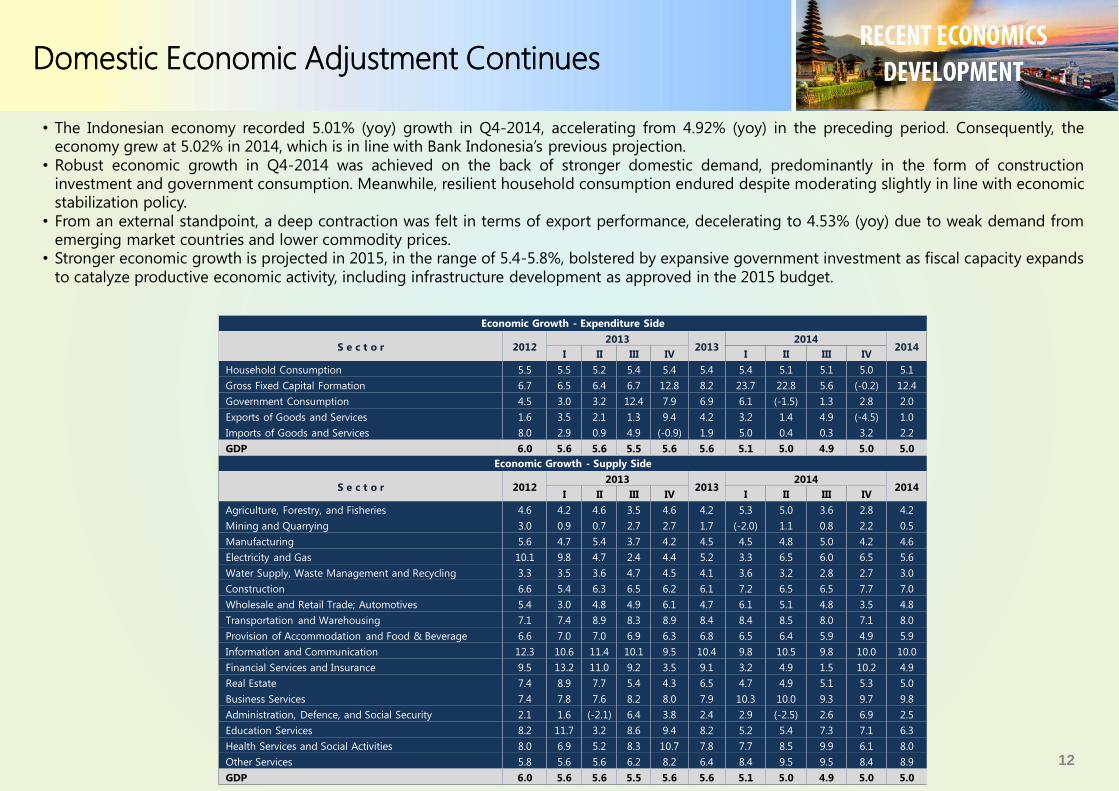

Domestic Economic Adjustment Continues

• The Indonesian economy recorded 5.01% (yoy) growth in Q4-2014, accelerating from 4.92% (yoy) in the preceding period. Consequently, theeconomy grew at 5.02% in 2014, which is in line with Bank Indonesia’s previous projection.

• Robust economic growth in Q4-2014 was achieved on the back of stronger domestic demand, predominantly in the form of constructioninvestment and government consumption. Meanwhile, resilient household consumption endured despite moderating slightly in line with economicstabilization policy.

• From an external standpoint, a deep contraction was felt in terms of export performance, decelerating to 4.53% (yoy) due to weak demand fromemerging market countries and lower commodity prices.

• Stronger economic growth is projected in 2015, in the range of 5.4-5.8%, bolstered by expansive government investment as fiscal capacity expands

to catalyze productive economic activity, including infrastructure development as approved in the 2015 budget.

12

Economic Growth - Expenditure Side

S e c t o r 20122013

20132014

2014I II III IV I II III IV

Household Consumption 5.5 5.5 5.2 5.4 5.4 5.4 5.4 5.1 5.1 5.0 5.1

Gross Fixed Capital Formation 6.7 6.5 6.4 6.7 12.8 8.2 23.7 22.8 5.6 (-0.2) 12.4

Government Consumption 4.5 3.0 3.2 12.4 7.9 6.9 6.1 (-1.5) 1.3 2.8 2.0

Exports of Goods and Services 1.6 3.5 2.1 1.3 9.4 4.2 3.2 1.4 4.9 (-4.5) 1.0

Imports of Goods and Services 8.0 2.9 0.9 4.9 (-0.9) 1.9 5.0 0.4 0.3 3.2 2.2

GDP 6.0 5.6 5.6 5.5 5.6 5.6 5.1 5.0 4.9 5.0 5.0

Economic Growth - Supply Side

S e c t o r 20122013

20132014

2014I II III IV I II III IV

Agriculture, Forestry, and Fisheries 4.6 4.2 4.6 3.5 4.6 4.2 5.3 5.0 3.6 2.8 4.2

Mining and Quarrying 3.0 0.9 0.7 2.7 2.7 1.7 (-2.0) 1.1 0.8 2.2 0.5

Manufacturing 5.6 4.7 5.4 3.7 4.2 4.5 4.5 4.8 5.0 4.2 4.6

Electricity and Gas 10.1 9.8 4.7 2.4 4.4 5.2 3.3 6.5 6.0 6.5 5.6

Water Supply, Waste Management and Recycling 3.3 3.5 3.6 4.7 4.5 4.1 3.6 3.2 2.8 2.7 3.0

Construction 6.6 5.4 6.3 6.5 6.2 6.1 7.2 6.5 6.5 7.7 7.0

Wholesale and Retail Trade; Automotives 5.4 3.0 4.8 4.9 6.1 4.7 6.1 5.1 4.8 3.5 4.8

Transportation and Warehousing 7.1 7.4 8.9 8.3 8.9 8.4 8.4 8.5 8.0 7.1 8.0

Provision of Accommodation and Food & Beverage 6.6 7.0 7.0 6.9 6.3 6.8 6.5 6.4 5.9 4.9 5.9

Information and Communication 12.3 10.6 11.4 10.1 9.5 10.4 9.8 10.5 9.8 10.0 10.0

Financial Services and Insurance 9.5 13.2 11.0 9.2 3.5 9.1 3.2 4.9 1.5 10.2 4.9

Real Estate 7.4 8.9 7.7 5.4 4.3 6.5 4.7 4.9 5.1 5.3 5.0

Business Services 7.4 7.8 7.6 8.2 8.0 7.9 10.3 10.0 9.3 9.7 9.8

Administration, Defence, and Social Security 2.1 1.6 (-2.1) 6.4 3.8 2.4 2.9 (-2.5) 2.6 6.9 2.5

Education Services 8.2 11.7 3.2 8.6 9.4 8.2 5.2 5.4 7.3 7.1 6.3

Health Services and Social Activities 8.0 6.9 5.2 8.3 10.7 7.8 7.7 8.5 9.9 6.1 8.0

Other Services 5.8 5.6 5.6 6.2 8.2 6.4 8.4 9.5 9.5 8.4 8.9

GDP 6.0 5.6 5.6 5.5 5.6 5.6 5.1 5.0 4.9 5.0 5.0

Source: KPMG, Ernst and Young, Jefferies Economist Intelligence Unit, Ministry of Finance, BPS and CIA World Factbook

(1) Working age defined as being between 15-54 years old

13

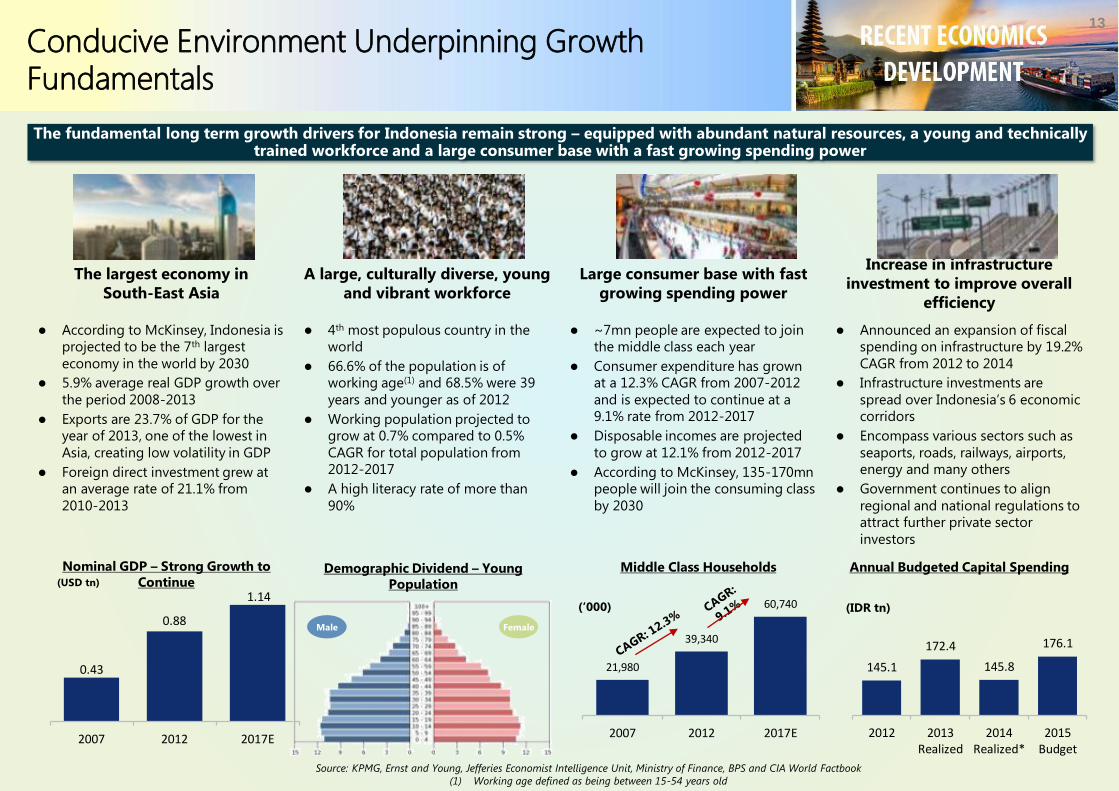

The largest economy in

South-East Asia

A large, culturally diverse, young

and vibrant workforce

Large consumer base with fast

growing spending power

Increase in infrastructure

investment to improve overall

efficiency

According to McKinsey, Indonesia is

projected to be the 7th largest

economy in the world by 2030

5.9% average real GDP growth over

the period 2008-2013

Exports are 23.7% of GDP for the

year of 2013, one of the lowest in

Asia, creating low volatility in GDP

Foreign direct investment grew at

an average rate of 21.1% from

2010-2013

4th most populous country in the

world

66.6% of the population is of

working age(1) and 68.5% were 39

years and younger as of 2012

Working population projected to

grow at 0.7% compared to 0.5%

CAGR for total population from

2012-2017

A high literacy rate of more than

90%

~7mn people are expected to join

the middle class each year

Consumer expenditure has grown

at a 12.3% CAGR from 2007-2012

and is expected to continue at a

9.1% rate from 2012-2017

Disposable incomes are projected

to grow at 12.1% from 2012-2017

According to McKinsey, 135-170mn

people will join the consuming class

by 2030

Announced an expansion of fiscal

spending on infrastructure by 19.2%

CAGR from 2012 to 2014

Infrastructure investments are

spread over Indonesia’s 6 economic

corridors

Encompass various sectors such as

seaports, roads, railways, airports,

energy and many others

Government continues to align

regional and national regulations to

attract further private sector

investors

(USD tn)

Nominal GDP – Strong Growth to

ContinueMiddle Class Households Annual Budgeted Capital Spending

(IDR tn)

145.1

172.4

145.8

176.1

2012 2013Realized

2014Realized*

2015Budget

21,980

39,340

60,740

2007 2012 2017E

(‘000)

Demographic Dividend – Young

Population

0.43

0.88

1.14

2007 2012 2017E

Male Female

The fundamental long term growth drivers for Indonesia remain strong – equipped with abundant natural resources, a young and technically trained workforce and a large consumer base with a fast growing spending power

Conducive Environment Underpinning Growth Fundamentals

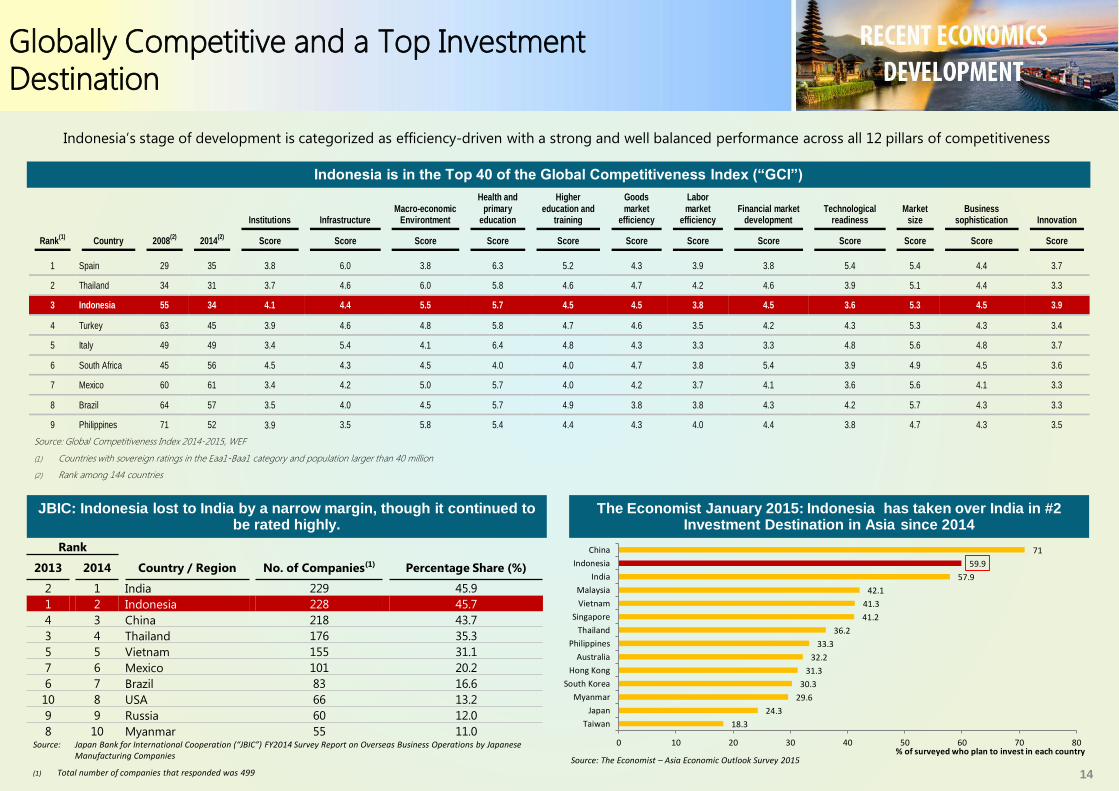

Globally Competitive and a Top Investment Destination

Source: Global Competitiveness Index 2014-2015, WEF

(1) Countries with sovereign ratings in the Eaa1-Baa1 category and population larger than 40 million

(2) Rank among 144 countries

Indonesia’s stage of development is categorized as efficiency-driven with a strong and well balanced performance across all 12 pillars of competitiveness

Source: The Economist – Asia Economic Outlook Survey 2015

Indonesia is in the Top 40 of the Global Competitiveness Index (“GCI”)

JBIC: Indonesia lost to India by a narrow margin, though it continued to be rated highly.

The Economist January 2015: Indonesia has taken over India in #2 Investment Destination in Asia since 2014

Source: Japan Bank for International Cooperation (“JBIC”) FY2014 Survey Report on Overseas Business Operations by Japanese Manufacturing Companies

(1) Total number of companies that responded was 499 14

Rank(1)

Country 2008(2)

2014(2)

Institutions Infrastructure Macro-economic

Environtment

Health and primary

education

Higher education and

training

Goods market

efficiency

Labor market

efficiency Financial market

development Technological

readiness Market

size Business

sophistication Innovation

Score Score Score Score Score Score Score Score Score Score Score Score

1 Spain 29 35 3.8 6.0 3.8 6.3 5.2 4.3 3.9 3.8 5.4 5.4 4.4 3.7

2 Thailand 34 31 3.7 4.6 6.0 5.8 4.6 4.7 4.2 4.6 3.9 5.1 4.4 3.3

3 Indonesia 55 34 4.1 4.4 5.5 5.7 4.5 4.5 3.8 4.5 3.6 5.3 4.5 3.9

4 Turkey 63 45 3.9 4.6 4.8 5.8 4.7 4.6 3.5 4.2 4.3 5.3 4.3 3.4

5 Italy 49 49 3.4 5.4 4.1 6.4 4.8 4.3 3.3 3.3 4.8 5.6 4.8 3.7

6 South Africa 45 56 4.5 4.3 4.5 4.0 4.0 4.7 3.8 5.4 3.9 4.9 4.5 3.6

7 Mexico 60 61 3.4 4.2 5.0 5.7 4.0 4.2 3.7 4.1 3.6 5.6 4.1 3.3

8 Brazil 64 57 3.5 4.0 4.5 5.7 4.9 3.8 3.8 4.3 4.2 5.7 4.3 3.3

9 Philippines 71 52 3.9 3.5 5.8 5.4 4.4 4.3 4.0 4.4 3.8 4.7 4.3 3.5

18.3

24.3

29.6

30.3

31.3

32.2

33.3

36.2

41.2

41.3

42.1

57.9

59.9

71

0 10 20 30 40 50 60 70 80

Taiwan

Japan

Myanmar

South Korea

Hong Kong

Australia

Philippines

Thailand

Singapore

Vietnam

Malaysia

India

Indonesia

China

% of surveyed who plan to invest in each country

Rank

2013 2014 Country / Region No. of Companies(1) Percentage Share (%)

2 1 India 229 45.9

1 2 Indonesia 228 45.7

4 3 China 218 43.7

3 4 Thailand 176 35.3

5 5 Vietnam 155 31.1

7 6 Mexico 101 20.2

6 7 Brazil 83 16.6

10 8 USA 66 13.2

9 9 Russia 60 12.0

8 10 Myanmar 55 11.0

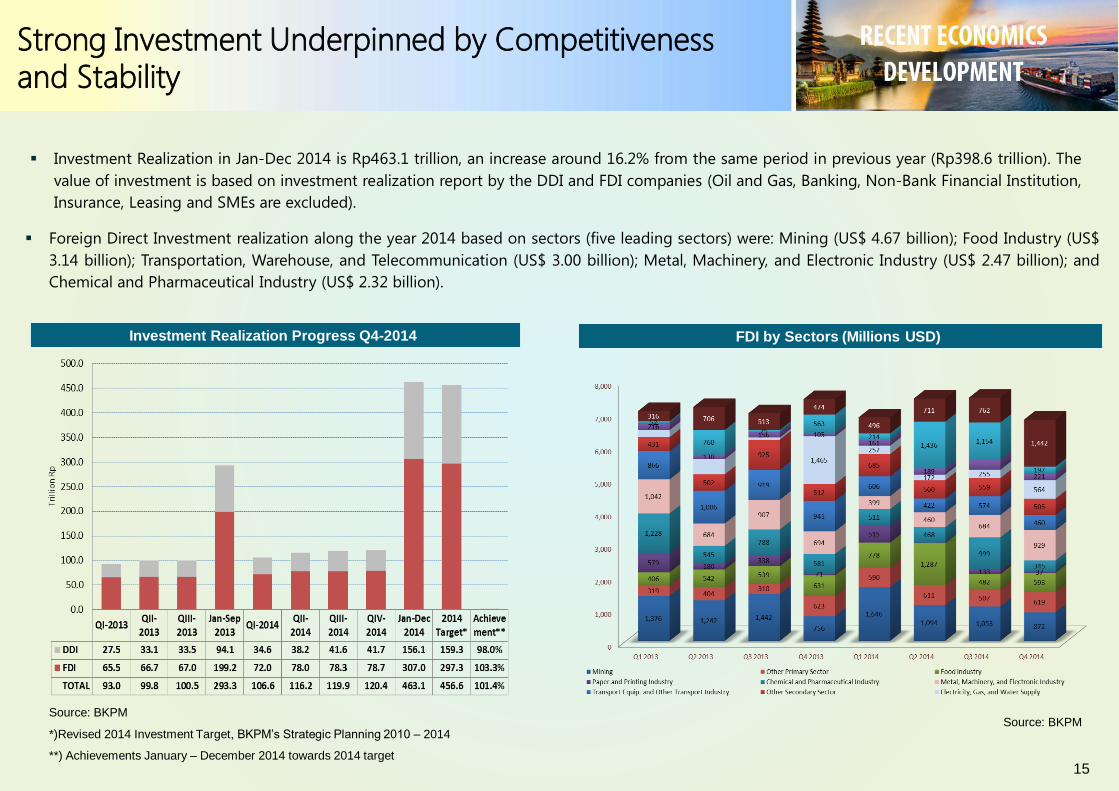

Strong Investment Underpinned by Competitivenessand Stability

Investment Realization Progress Q4-2014

Investment Realization in Jan-Dec 2014 is Rp463.1 trillion, an increase around 16.2% from the same period in previous year (Rp398.6 trillion). The

value of investment is based on investment realization report by the DDI and FDI companies (Oil and Gas, Banking, Non-Bank Financial Institution,

Insurance, Leasing and SMEs are excluded).

Source: BKPMSource: BKPM

*)Revised 2014 Investment Target, BKPM’s Strategic Planning 2010 – 2014

**) Achievements January – December 2014 towards 2014 target

FDI by Sectors (Millions USD)

Foreign Direct Investment realization along the year 2014 based on sectors (five leading sectors) were: Mining (US$ 4.67 billion); Food Industry (US$

3.14 billion); Transportation, Warehouse, and Telecommunication (US$ 3.00 billion); Metal, Machinery, and Electronic Industry (US$ 2.47 billion); and

Chemical and Pharmaceutical Industry (US$ 2.32 billion).

15

16

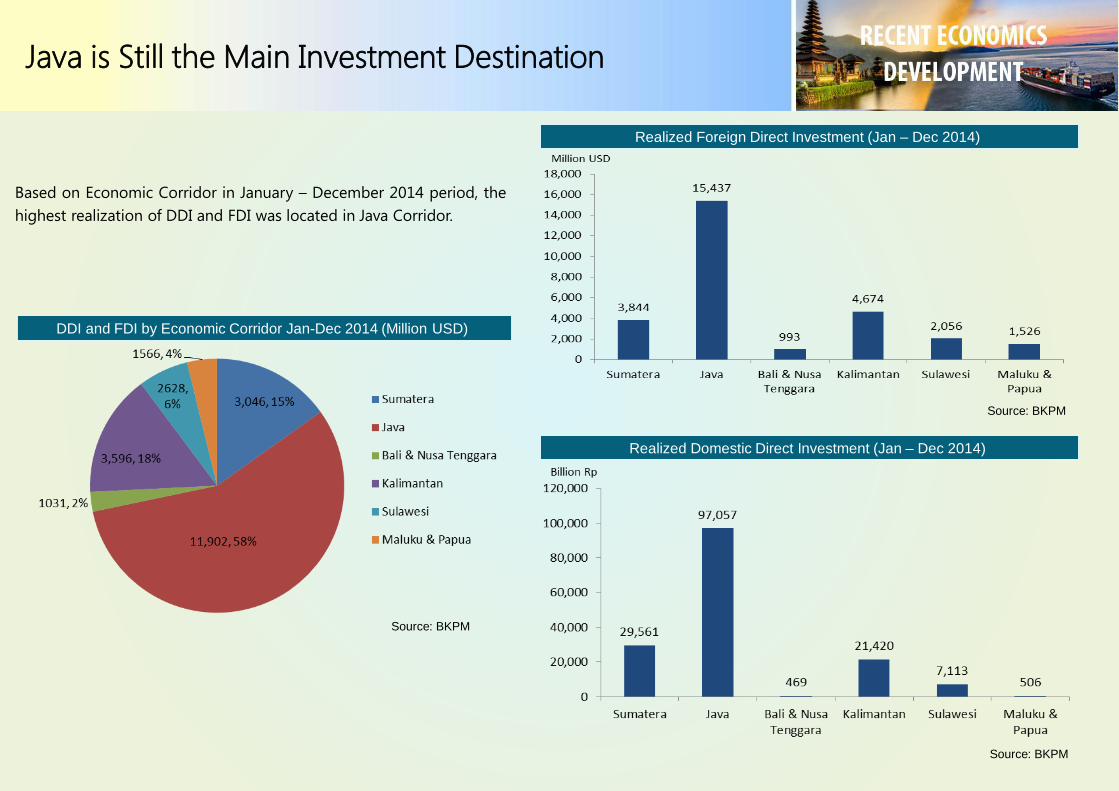

Java is Still the Main Investment Destination

Realized Foreign Direct Investment (Jan – Dec 2014)

Realized Domestic Direct Investment (Jan – Dec 2014)

Source: BKPM

Source: BKPM

DDI and FDI by Economic Corridor Jan-Dec 2014 (Million USD)

Source: BKPM

Based on Economic Corridor in January – December 2014 period, the

highest realization of DDI and FDI was located in Java Corridor.

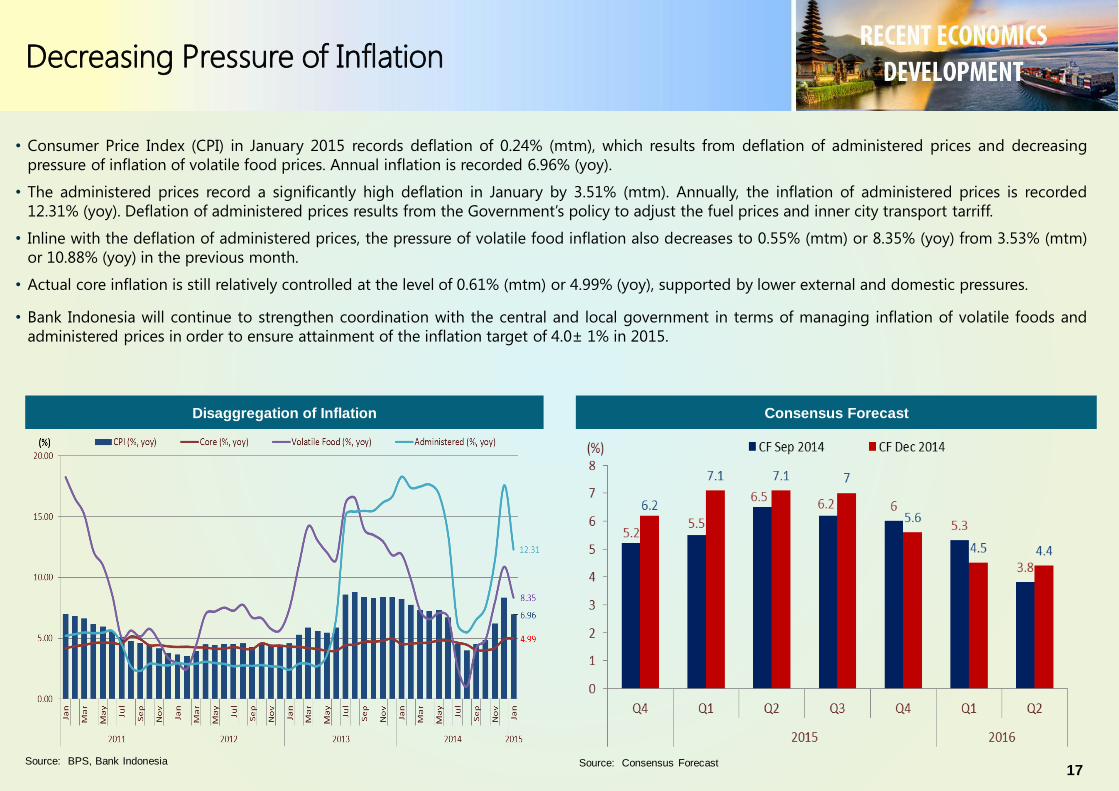

Decreasing Pressure of Inflation

Disaggregation of Inflation

Source: BPS, Bank Indonesia

• Consumer Price Index (CPI) in January 2015 records deflation of 0.24% (mtm), which results from deflation of administered prices and decreasing

pressure of inflation of volatile food prices. Annual inflation is recorded 6.96% (yoy).

• The administered prices record a significantly high deflation in January by 3.51% (mtm). Annually, the inflation of administered prices is recorded

12.31% (yoy). Deflation of administered prices results from the Government’s policy to adjust the fuel prices and inner city transport tarriff.

• Inline with the deflation of administered prices, the pressure of volatile food inflation also decreases to 0.55% (mtm) or 8.35% (yoy) from 3.53% (mtm)

or 10.88% (yoy) in the previous month.

• Actual core inflation is still relatively controlled at the level of 0.61% (mtm) or 4.99% (yoy), supported by lower external and domestic pressures.

• Bank Indonesia will continue to strengthen coordination with the central and local government in terms of managing inflation of volatile foods and

administered prices in order to ensure attainment of the inflation target of 4.0± 1% in 2015.

Consensus Forecast

Source: Consensus Forecast17

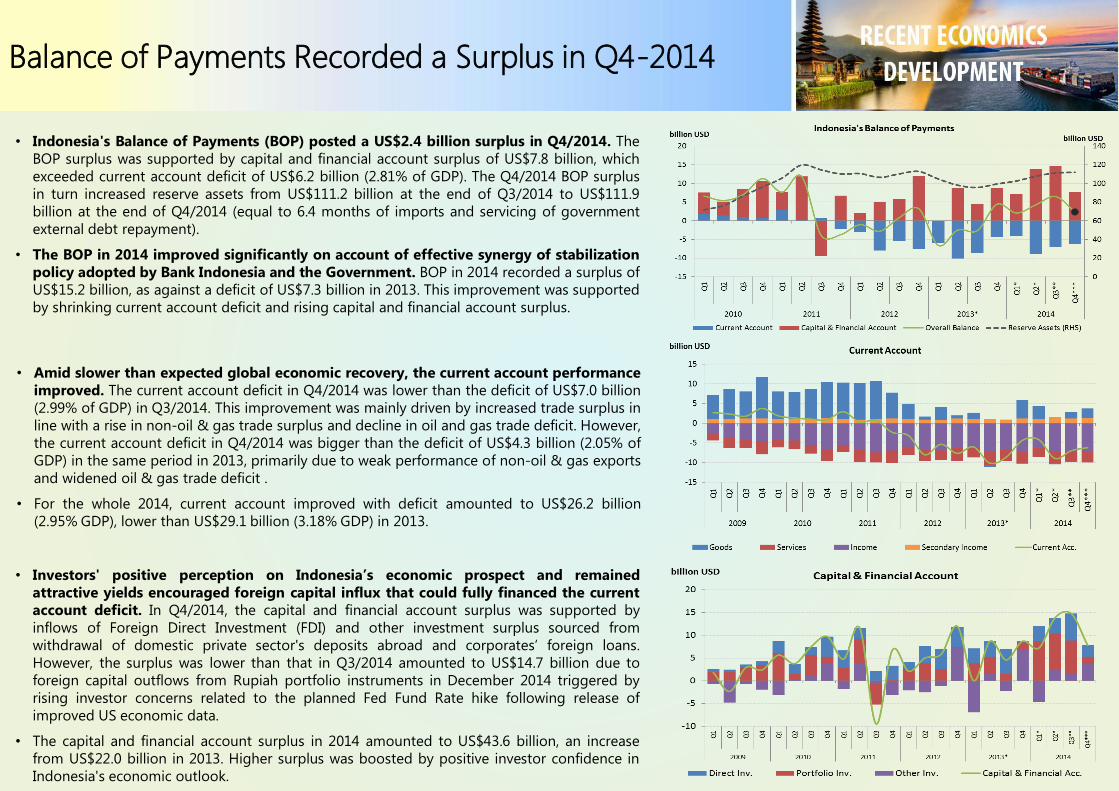

• Indonesia's Balance of Payments (BOP) posted a US$2.4 billion surplus in Q4/2014. The

BOP surplus was supported by capital and financial account surplus of US$7.8 billion, which

exceeded current account deficit of US$6.2 billion (2.81% of GDP). The Q4/2014 BOP surplus

in turn increased reserve assets from US$111.2 billion at the end of Q3/2014 to US$111.9

billion at the end of Q4/2014 (equal to 6.4 months of imports and servicing of government

external debt repayment).

• The BOP in 2014 improved significantly on account of effective synergy of stabilization

policy adopted by Bank Indonesia and the Government. BOP in 2014 recorded a surplus of

US$15.2 billion, as against a deficit of US$7.3 billion in 2013. This improvement was supported

by shrinking current account deficit and rising capital and financial account surplus.

• Amid slower than expected global economic recovery, the current account performance

improved. The current account deficit in Q4/2014 was lower than the deficit of US$7.0 billion

(2.99% of GDP) in Q3/2014. This improvement was mainly driven by increased trade surplus in

line with a rise in non-oil & gas trade surplus and decline in oil and gas trade deficit. However,

the current account deficit in Q4/2014 was bigger than the deficit of US$4.3 billion (2.05% of

GDP) in the same period in 2013, primarily due to weak performance of non-oil & gas exports

and widened oil & gas trade deficit .

• For the whole 2014, current account improved with deficit amounted to US$26.2 billion

(2.95% GDP), lower than US$29.1 billion (3.18% GDP) in 2013.

• Investors' positive perception on Indonesia’s economic prospect and remained

attractive yields encouraged foreign capital influx that could fully financed the current

account deficit. In Q4/2014, the capital and financial account surplus was supported by

inflows of Foreign Direct Investment (FDI) and other investment surplus sourced from

withdrawal of domestic private sector's deposits abroad and corporates’ foreign loans.

However, the surplus was lower than that in Q3/2014 amounted to US$14.7 billion due to

foreign capital outflows from Rupiah portfolio instruments in December 2014 triggered by

rising investor concerns related to the planned Fed Fund Rate hike following release of

improved US economic data.

• The capital and financial account surplus in 2014 amounted to US$43.6 billion, an increase

from US$22.0 billion in 2013. Higher surplus was boosted by positive investor confidence in

Indonesia's economic outlook.

Balance of Payments Recorded a Surplus in Q4-2014

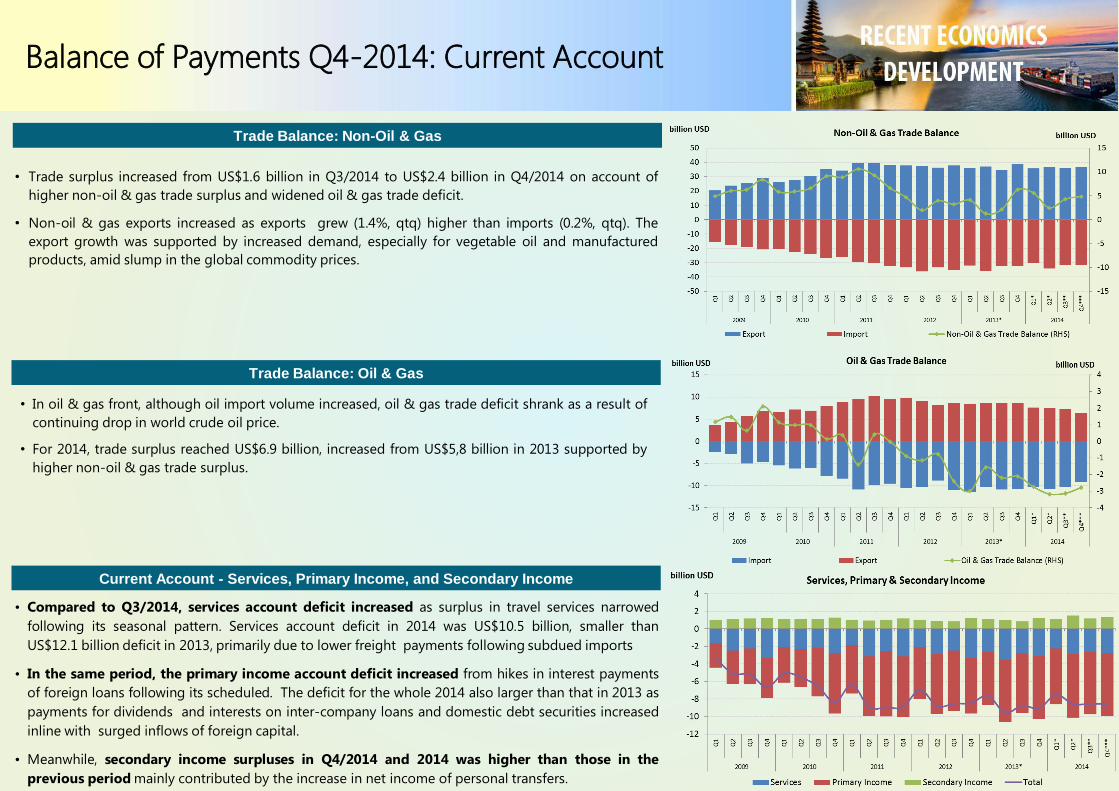

• Trade surplus increased from US$1.6 billion in Q3/2014 to US$2.4 billion in Q4/2014 on account of

higher non-oil & gas trade surplus and widened oil & gas trade deficit.

• Non-oil & gas exports increased as exports grew (1.4%, qtq) higher than imports (0.2%, qtq). The

export growth was supported by increased demand, especially for vegetable oil and manufactured

products, amid slump in the global commodity prices.

Balance of Payments Q4-2014: Current Account

• In oil & gas front, although oil import volume increased, oil & gas trade deficit shrank as a result of

continuing drop in world crude oil price.

• For 2014, trade surplus reached US$6.9 billion, increased from US$5,8 billion in 2013 supported by

higher non-oil & gas trade surplus.

Trade Balance: Non-Oil & Gas

Trade Balance: Oil & Gas

• Compared to Q3/2014, services account deficit increased as surplus in travel services narrowed

following its seasonal pattern. Services account deficit in 2014 was US$10.5 billion, smaller than

US$12.1 billion deficit in 2013, primarily due to lower freight payments following subdued imports

• In the same period, the primary income account deficit increased from hikes in interest payments

of foreign loans following its scheduled. The deficit for the whole 2014 also larger than that in 2013 as

payments for dividends and interests on inter-company loans and domestic debt securities increased

inline with surged inflows of foreign capital.

• Meanwhile, secondary income surpluses in Q4/2014 and 2014 was higher than those in the

previous period mainly contributed by the increase in net income of personal transfers.

Current Account - Services, Primary Income, and Secondary Income

20

Balance of Payments Q4-2014: Capital & Financial Account

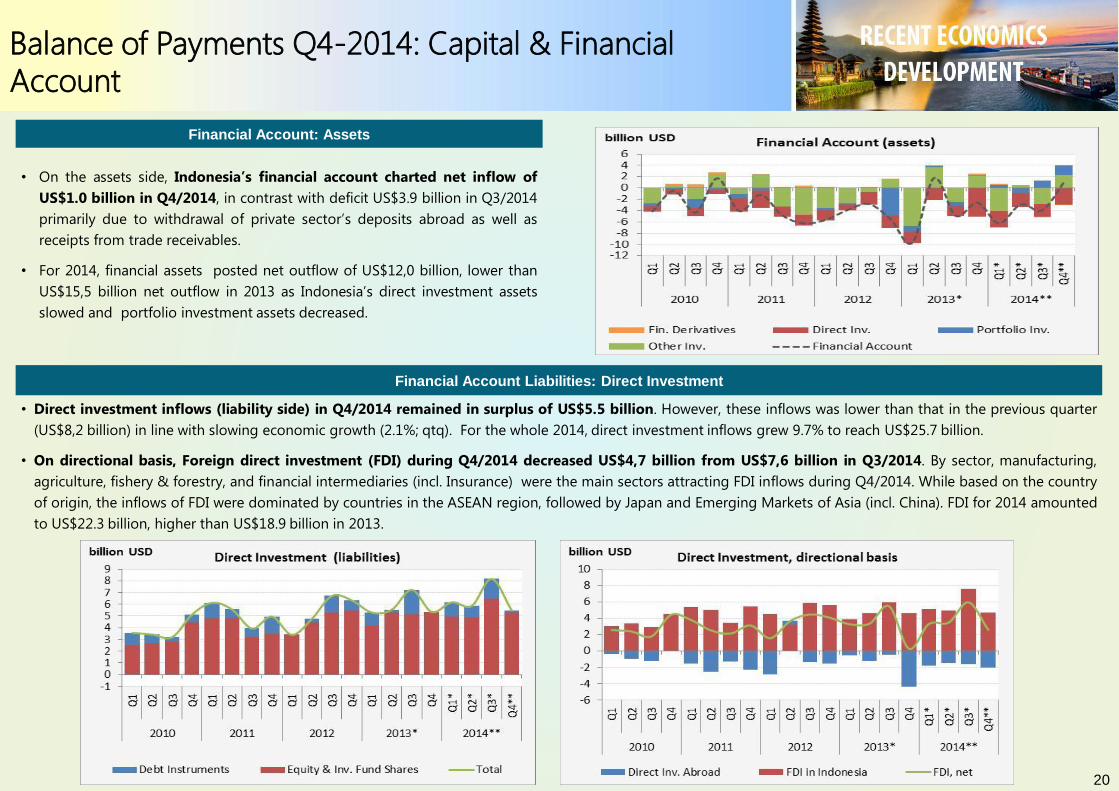

Financial Account: Assets

Financial Account Liabilities: Direct Investment

• On the assets side, Indonesia’s financial account charted net inflow of

US$1.0 billion in Q4/2014, in contrast with deficit US$3.9 billion in Q3/2014

primarily due to withdrawal of private sector’s deposits abroad as well as

receipts from trade receivables.

• For 2014, financial assets posted net outflow of US$12,0 billion, lower than

US$15,5 billion net outflow in 2013 as Indonesia’s direct investment assets

slowed and portfolio investment assets decreased.

• Direct investment inflows (liability side) in Q4/2014 remained in surplus of US$5.5 billion. However, these inflows was lower than that in the previous quarter

(US$8,2 billion) in line with slowing economic growth (2.1%; qtq). For the whole 2014, direct investment inflows grew 9.7% to reach US$25.7 billion.

• On directional basis, Foreign direct investment (FDI) during Q4/2014 decreased US$4,7 billion from US$7,6 billion in Q3/2014. By sector, manufacturing,

agriculture, fishery & forestry, and financial intermediaries (incl. Insurance) were the main sectors attracting FDI inflows during Q4/2014. While based on the country

of origin, the inflows of FDI were dominated by countries in the ASEAN region, followed by Japan and Emerging Markets of Asia (incl. China). FDI for 2014 amounted

to US$22.3 billion, higher than US$18.9 billion in 2013.

21

Balance of Payments Q4-2014: Capital & Financial Account

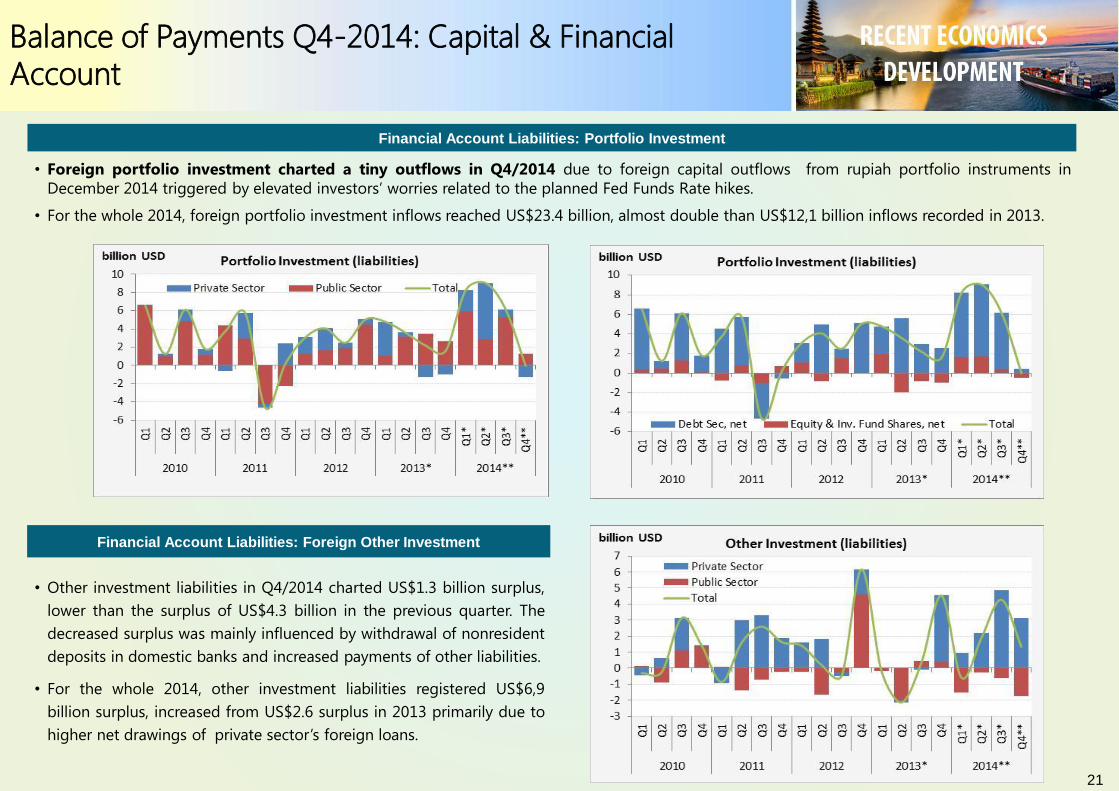

Financial Account Liabilities: Portfolio Investment

Financial Account Liabilities: Foreign Other Investment

• Foreign portfolio investment charted a tiny outflows in Q4/2014 due to foreign capital outflows from rupiah portfolio instruments in

December 2014 triggered by elevated investors’ worries related to the planned Fed Funds Rate hikes.

• For the whole 2014, foreign portfolio investment inflows reached US$23.4 billion, almost double than US$12,1 billion inflows recorded in 2013.

• Other investment liabilities in Q4/2014 charted US$1.3 billion surplus,

lower than the surplus of US$4.3 billion in the previous quarter. The

decreased surplus was mainly influenced by withdrawal of nonresident

deposits in domestic banks and increased payments of other liabilities.

• For the whole 2014, other investment liabilities registered US$6,9

billion surplus, increased from US$2.6 surplus in 2013 primarily due to

higher net drawings of private sector’s foreign loans.

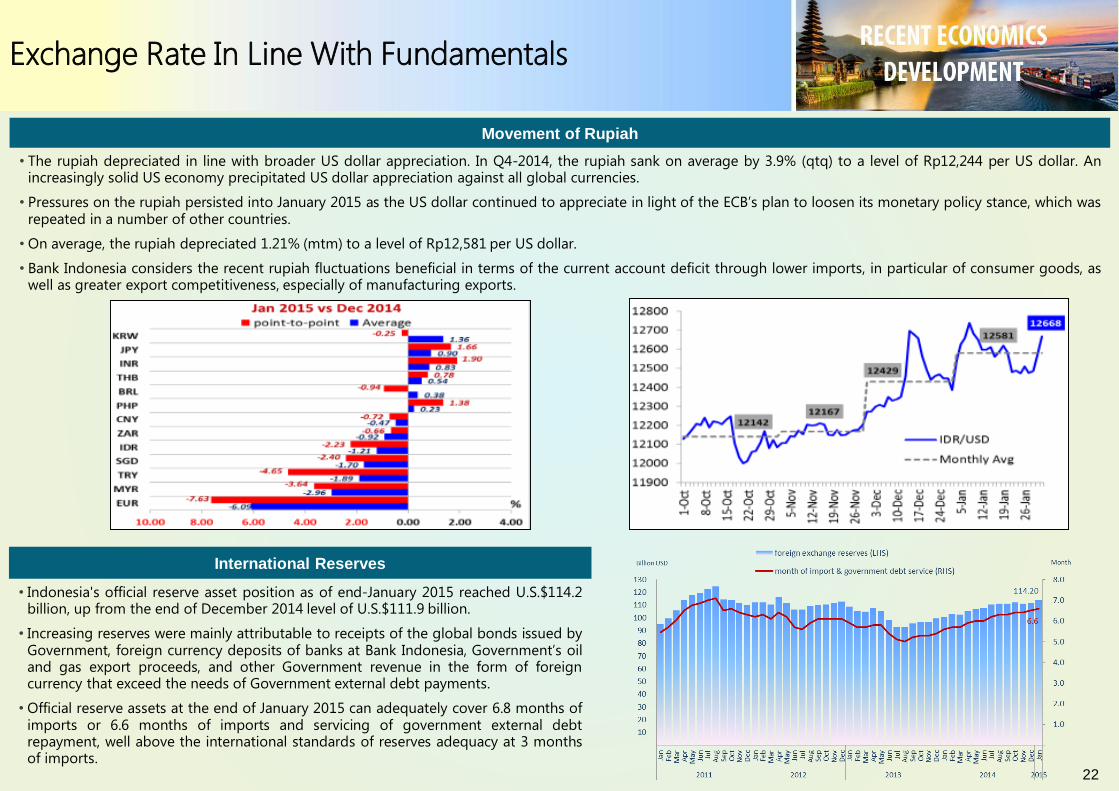

Exchange Rate In Line With Fundamentals

• The rupiah depreciated in line with broader US dollar appreciation. In Q4-2014, the rupiah sank on average by 3.9% (qtq) to a level of Rp12,244 per US dollar. Anincreasingly solid US economy precipitated US dollar appreciation against all global currencies.

• Pressures on the rupiah persisted into January 2015 as the US dollar continued to appreciate in light of the ECB’s plan to loosen its monetary policy stance, which wasrepeated in a number of other countries.

• On average, the rupiah depreciated 1.21% (mtm) to a level of Rp12,581 per US dollar.

• Bank Indonesia considers the recent rupiah fluctuations beneficial in terms of the current account deficit through lower imports, in particular of consumer goods, aswell as greater export competitiveness, especially of manufacturing exports.

Movement of Rupiah

International Reserves

22

• Indonesia's official reserve asset position as of end-January 2015 reached U.S.$114.2billion, up from the end of December 2014 level of U.S.$111.9 billion.

• Increasing reserves were mainly attributable to receipts of the global bonds issued byGovernment, foreign currency deposits of banks at Bank Indonesia, Government’s oiland gas export proceeds, and other Government revenue in the form of foreigncurrency that exceed the needs of Government external debt payments.

• Official reserve assets at the end of January 2015 can adequately cover 6.8 months ofimports or 6.6 months of imports and servicing of government external debtrepayment, well above the international standards of reserves adequacy at 3 monthsof imports.

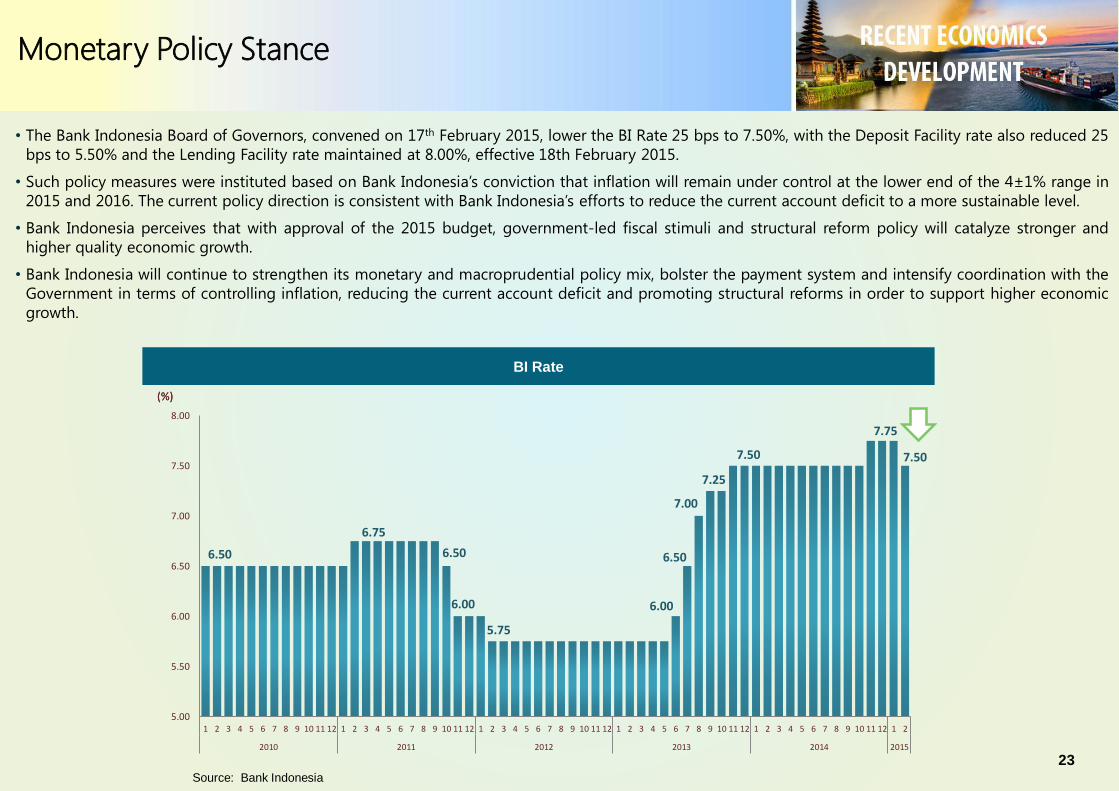

Monetary Policy Stance

BI Rate

Source: Bank Indonesia

• The Bank Indonesia Board of Governors, convened on 17th February 2015, lower the BI Rate 25 bps to 7.50%, with the Deposit Facility rate also reduced 25

bps to 5.50% and the Lending Facility rate maintained at 8.00%, effective 18th February 2015.

• Such policy measures were instituted based on Bank Indonesia’s conviction that inflation will remain under control at the lower end of the 4±1% range in

2015 and 2016. The current policy direction is consistent with Bank Indonesia’s efforts to reduce the current account deficit to a more sustainable level.

• Bank Indonesia perceives that with approval of the 2015 budget, government-led fiscal stimuli and structural reform policy will catalyze stronger and

higher quality economic growth.

• Bank Indonesia will continue to strengthen its monetary and macroprudential policy mix, bolster the payment system and intensify coordination with the

Government in terms of controlling inflation, reducing the current account deficit and promoting structural reforms in order to support higher economic

growth.

23

6.50

6.75

6.50

6.00

5.75

6.00

6.50

7.00

7.25

7.50

7.75

7.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2

2010 2011 2012 2013 2014 2015

(%)(%)

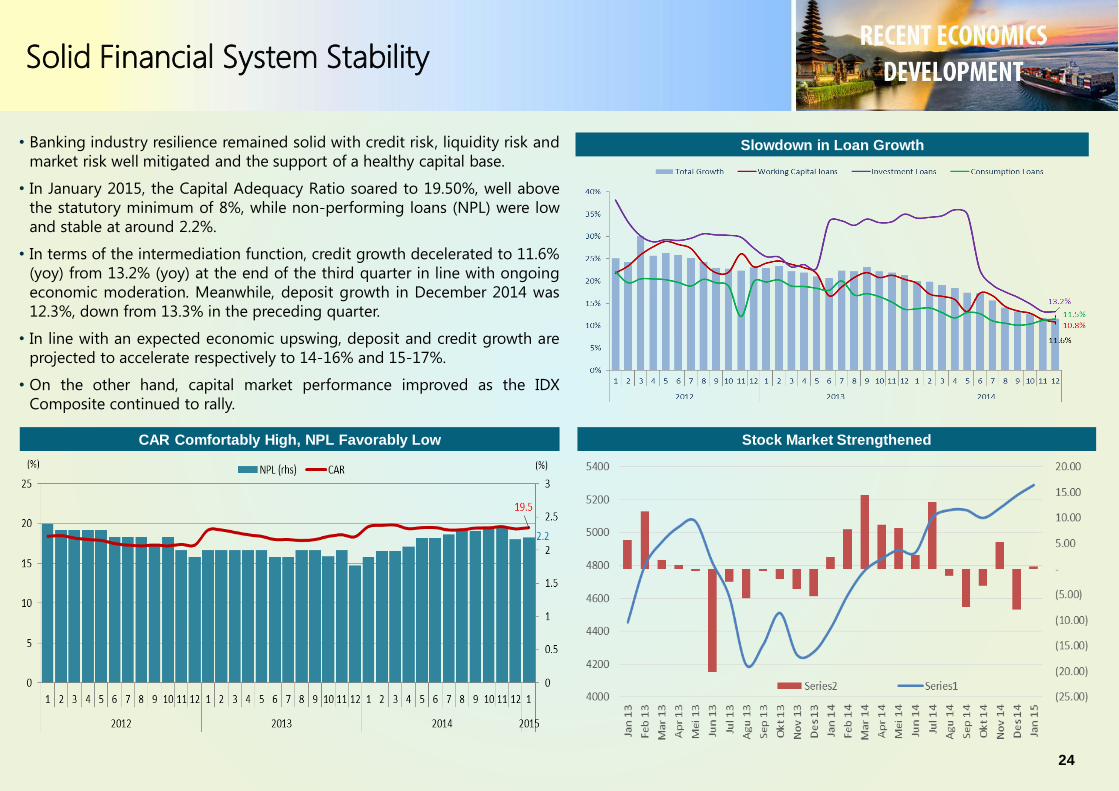

Solid Financial System Stability

• Banking industry resilience remained solid with credit risk, liquidity risk and

market risk well mitigated and the support of a healthy capital base.

• In January 2015, the Capital Adequacy Ratio soared to 19.50%, well above

the statutory minimum of 8%, while non-performing loans (NPL) were low

and stable at around 2.2%.

• In terms of the intermediation function, credit growth decelerated to 11.6%

(yoy) from 13.2% (yoy) at the end of the third quarter in line with ongoing

economic moderation. Meanwhile, deposit growth in December 2014 was

12.3%, down from 13.3% in the preceding quarter.

• In line with an expected economic upswing, deposit and credit growth are

projected to accelerate respectively to 14-16% and 15-17%.

• On the other hand, capital market performance improved as the IDX

Composite continued to rally.

CAR Comfortably High, NPL Favorably Low

Slowdown in Loan Growth

Stock Market Strengthened

24

Prudent Fiscal Management

25

Improving Budget Structure

Manageable Fiscal Deficit

Quality of Spending

Sustainable Revenue Source

• Develop effective taxation policy and tax administration

• Focus not only on the corporate but also on personal income tax & improve value added tax system.

• Provide fiscal incentive for investment with better targeted system

• Change subsidy paradigmShift from price (commodity) subsidy to targeted subsidy system

• Reallocate budget to productive spending, such as infrastructure and direct assistance.

• Prioritize basic infrastructure to support food security, agriculture and fisheries sectors as well as job creation.

• Provide a greater room on our fiscal to anticipate the uncertainty coming from global economic development.

• Encourage private sector to help infrastructure development, among other through PPP scheme

Spending Re-Allocation To Achieve Greater Productivity

Infrastructure Plan 2015-2019

New Sea Ports - 24 Sea Port Development - 59Pioneer Cargo Ships

New Airports - 15 Airport Infrastructure DevelopmentAirplanes - 20

Rail lines - 2,159 kmIntra City Rail Lines - 1,099 km

New Roads - 2,650 kmHighway - 1,000 kmRoad Maintainance - 46,770 kmBus Corridors - 2

Source: Ministry of Finance

Kartu Indonesia Pintar(Indonesian Smart Card) -Education subsidies for the poor and families near the poverty threshold

Kartu Keluarga Sejahtera Bi-monthly credits for eligible families to offset increasing costs of living

Kartu Indonesia Sehat(Indonesian Health Card) -Free health insurance and medical benefits

Reduction of poverty through conditional cash transfersAhead of the fuel subsidy hike, a systemic change in the provision of subsidies to the communities in need was implemented.

IDR Tn % Total Spending

1 2 3

91.3 84 114.2 145.5 155.9 206.6

9.7

8.38.8

9.8

9.0

11.0

6

8

10

12

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014Infrastructure Spending (LHS) % Total Spending (RHS)

Source: Bappenas

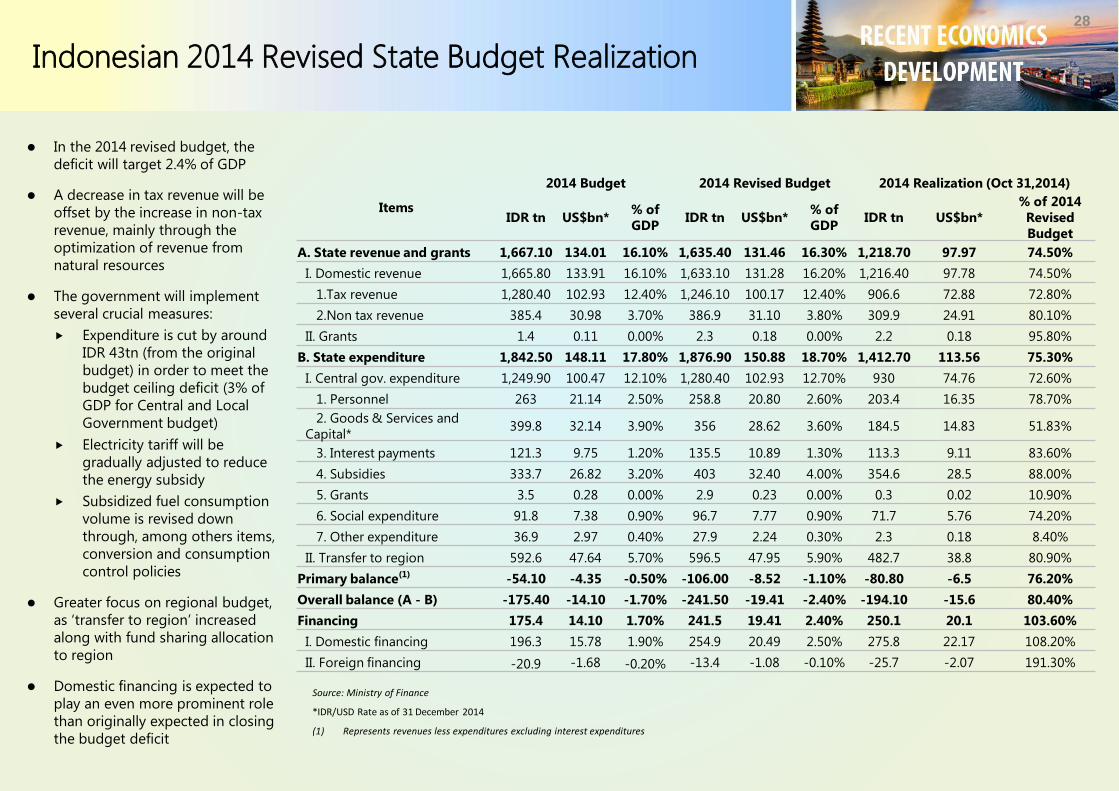

Indonesian 2014 Revised State Budget Realization

28

Source: Ministry of Finance

*IDR/USD Rate as of 31 December 2014

(1) Represents revenues less expenditures excluding interest expenditures

In the 2014 revised budget, the

deficit will target 2.4% of GDP

A decrease in tax revenue will be

offset by the increase in non-tax

revenue, mainly through the

optimization of revenue from

natural resources

The government will implement

several crucial measures:

Expenditure is cut by around

IDR 43tn (from the original

budget) in order to meet the

budget ceiling deficit (3% of

GDP for Central and Local

Government budget)

Electricity tariff will be

gradually adjusted to reduce

the energy subsidy

Subsidized fuel consumption

volume is revised down

through, among others items,

conversion and consumption

control policies

Greater focus on regional budget,

as ‘transfer to region’ increased

along with fund sharing allocation

to region

Domestic financing is expected to

play an even more prominent role

than originally expected in closing

the budget deficit

Items

2014 Budget 2014 Revised Budget 2014 Realization (Oct 31,2014)

IDR tn US$bn*% of

GDPIDR tn US$bn*

% of

GDPIDR tn US$bn*

% of 2014

Revised

Budget

A. State revenue and grants 1,667.10 134.01 16.10% 1,635.40 131.46 16.30% 1,218.70 97.97 74.50%

I. Domestic revenue 1,665.80 133.91 16.10% 1,633.10 131.28 16.20% 1,216.40 97.78 74.50%

1.Tax revenue 1,280.40 102.93 12.40% 1,246.10 100.17 12.40% 906.6 72.88 72.80%

2.Non tax revenue 385.4 30.98 3.70% 386.9 31.10 3.80% 309.9 24.91 80.10%

II. Grants 1.4 0.11 0.00% 2.3 0.18 0.00% 2.2 0.18 95.80%

B. State expenditure 1,842.50 148.11 17.80% 1,876.90 150.88 18.70% 1,412.70 113.56 75.30%

I. Central gov. expenditure 1,249.90 100.47 12.10% 1,280.40 102.93 12.70% 930 74.76 72.60%

1. Personnel 263 21.14 2.50% 258.8 20.80 2.60% 203.4 16.35 78.70%

2. Goods & Services and

Capital*399.8 32.14 3.90% 356 28.62 3.60% 184.5 14.83 51.83%

3. Interest payments 121.3 9.75 1.20% 135.5 10.89 1.30% 113.3 9.11 83.60%

4. Subsidies 333.7 26.82 3.20% 403 32.40 4.00% 354.6 28.5 88.00%

5. Grants 3.5 0.28 0.00% 2.9 0.23 0.00% 0.3 0.02 10.90%

6. Social expenditure 91.8 7.38 0.90% 96.7 7.77 0.90% 71.7 5.76 74.20%

7. Other expenditure 36.9 2.97 0.40% 27.9 2.24 0.30% 2.3 0.18 8.40%

II. Transfer to region 592.6 47.64 5.70% 596.5 47.95 5.90% 482.7 38.8 80.90%

Primary balance(1) -54.10 -4.35 -0.50% -106.00 -8.52 -1.10% -80.80 -6.5 76.20%

Overall balance (A - B) -175.40 -14.10 -1.70% -241.50 -19.41 -2.40% -194.10 -15.6 80.40%

Financing 175.4 14.10 1.70% 241.5 19.41 2.40% 250.1 20.1 103.60%

I. Domestic financing 196.3 15.78 1.90% 254.9 20.49 2.50% 275.8 22.17 108.20%

II. Foreign financing -20.9 -1.68 -0.20% -13.4 -1.08 -0.10% -25.7 -2.07 191.30%

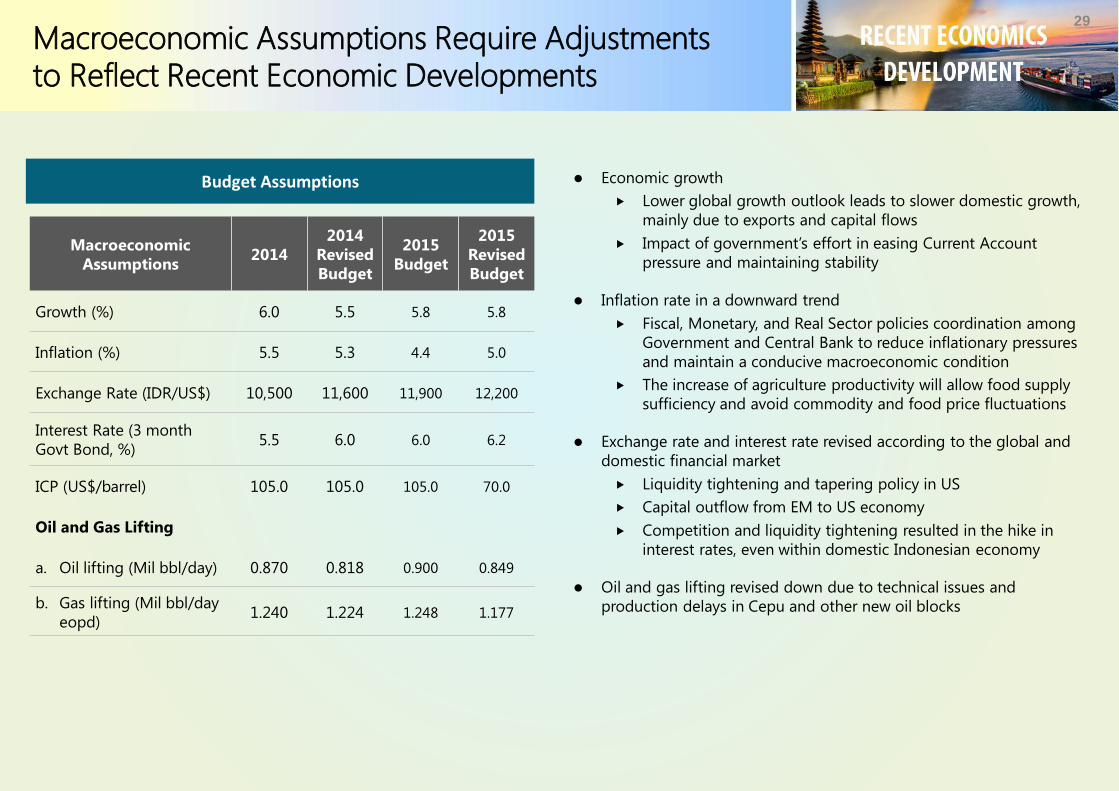

Economic growth

Lower global growth outlook leads to slower domestic growth,

mainly due to exports and capital flows

Impact of government’s effort in easing Current Account

pressure and maintaining stability

Inflation rate in a downward trend

Fiscal, Monetary, and Real Sector policies coordination among

Government and Central Bank to reduce inflationary pressures

and maintain a conducive macroeconomic condition

The increase of agriculture productivity will allow food supply

sufficiency and avoid commodity and food price fluctuations

Exchange rate and interest rate revised according to the global and

domestic financial market

Liquidity tightening and tapering policy in US

Capital outflow from EM to US economy

Competition and liquidity tightening resulted in the hike in

interest rates, even within domestic Indonesian economy

Oil and gas lifting revised down due to technical issues and

production delays in Cepu and other new oil blocks

Macroeconomic

Assumptions2014

2014

Revised

Budget

2015

Budget

2015

Revised

Budget

Growth (%) 6.0 5.5 5.8 5.8

Inflation (%) 5.5 5.3 4.4 5.0

Exchange Rate (IDR/US$) 10,500 11,600 11,900 12,200

Interest Rate (3 month

Govt Bond, %)5.5 6.0 6.0 6.2

ICP (US$/barrel) 105.0 105.0 105.0 70.0

Oil and Gas Lifting

a. Oil lifting (Mil bbl/day) 0.870 0.818 0.900 0.849

b. Gas lifting (Mil bbl/day

eopd)1.240 1.224 1.248 1.177

Macroeconomic Assumptions Require Adjustments to Reflect Recent Economic Developments

29

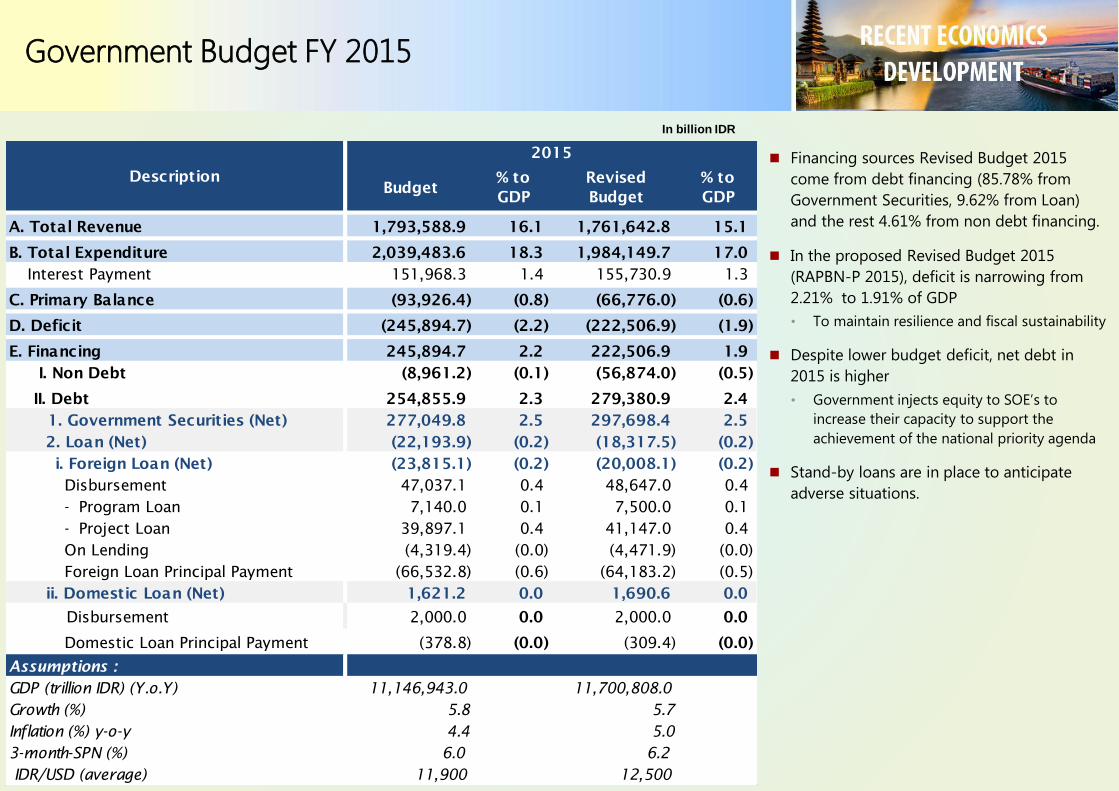

Budget Assumptions

In billion IDR

Financing sources Revised Budget 2015

come from debt financing (85.78% from

Government Securities, 9.62% from Loan)

and the rest 4.61% from non debt financing.

In the proposed Revised Budget 2015

(RAPBN-P 2015), deficit is narrowing from

2.21% to 1.91% of GDP

• To maintain resilience and fiscal sustainability

Despite lower budget deficit, net debt in

2015 is higher

• Government injects equity to SOE’s to

increase their capacity to support the

achievement of the national priority agenda

Stand-by loans are in place to anticipate

adverse situations.

A. Total Revenue 1,793,588.9 16.1 1,761,642.8 15.1

B. Total Expenditure 2,039,483.6 18.3 1,984,149.7 17.0

Interest Payment 151,968.3 1.4 155,730.9 1.3

C. Primary Balance (93,926.4) (0.8) (66,776.0) (0.6)

D. Deficit (245,894.7) (2.2) (222,506.9) (1.9)

E. Financing 245,894.7 2.2 222,506.9 1.9

I. Non Debt (8,961.2) (0.1) (56,874.0) (0.5)

II. Debt 254,855.9 2.3 279,380.9 2.4

1. Government Securities (Net) 277,049.8 2.5 297,698.4 2.5

2. Loan (Net) (22,193.9) (0.2) (18,317.5) (0.2)

i. Foreign Loan (Net) (23,815.1) (0.2) (20,008.1) (0.2)

Disbursement 47,037.1 0.4 48,647.0 0.4

- Program Loan 7,140.0 0.1 7,500.0 0.1

- Project Loan 39,897.1 0.4 41,147.0 0.4

On Lending (4,319.4) (0.0) (4,471.9) (0.0)

Foreign Loan Principal Payment (66,532.8) (0.6) (64,183.2) (0.5)

ii. Domestic Loan (Net) 1,621.2 0.0 1,690.6 0.0

Disbursement 2,000.0 0.0 2,000.0 0.0

Domestic Loan Principal Payment (378.8) (0.0) (309.4) (0.0)

Assumptions :

GDP (trillion IDR) (Y.o.Y) 11,146,943.0 11,700,808.0

Growth (%) 5.8 5.7

Inflation (%) y-o-y 4.4 5.0

3-month-SPN (%) 6.0 6.2

IDR/USD (average) 11,900 12,500

Budget% to

GDP

Revised

Budget

% to

GDP

2015

Description

Government Budget FY 2015

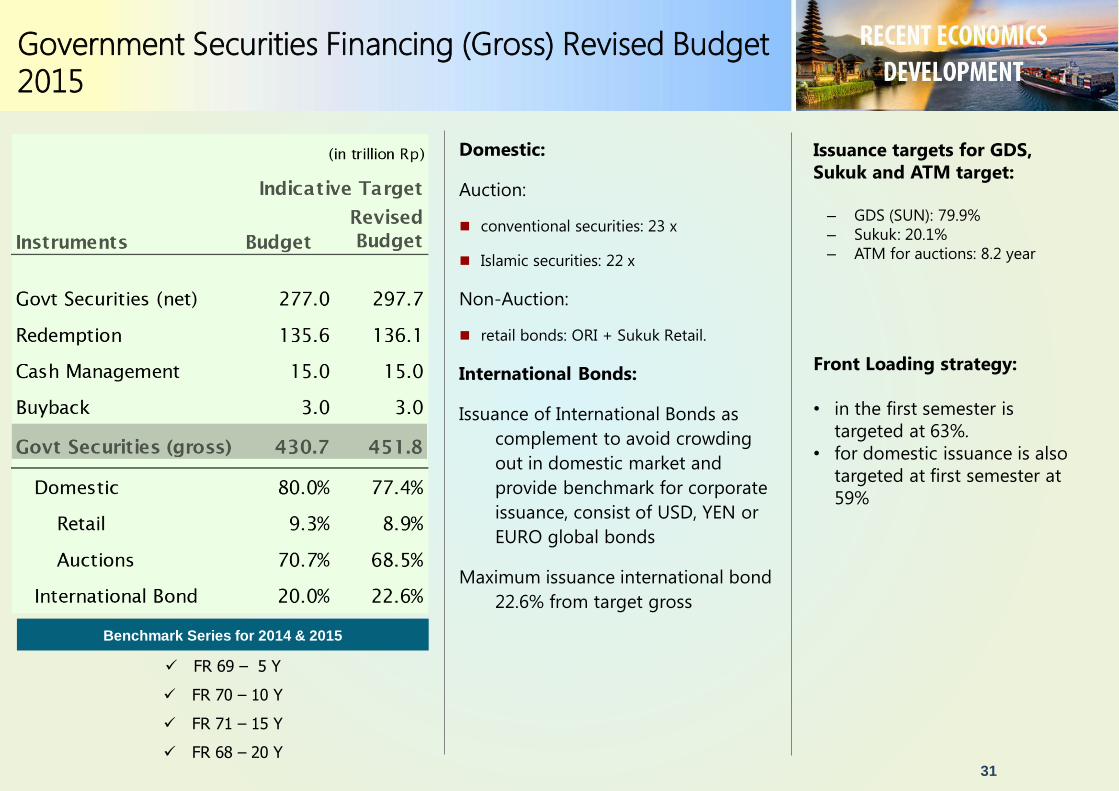

31

Domestic:

Auction:

conventional securities: 23 x

Islamic securities: 22 x

Non-Auction:

retail bonds: ORI + Sukuk Retail.

International Bonds:

Issuance of International Bonds as

complement to avoid crowding

out in domestic market and

provide benchmark for corporate

issuance, consist of USD, YEN or

EURO global bonds

Maximum issuance international bond

22.6% from target gross

Issuance targets for GDS,

Sukuk and ATM target:

– GDS (SUN): 79.9%

– Sukuk: 20.1%

– ATM for auctions: 8.2 year

Front Loading strategy:

• in the first semester is

targeted at 63%.

• for domestic issuance is also

targeted at first semester at

59%

FR 69 – 5 Y

FR 70 – 10 Y

FR 71 – 15 Y

FR 68 – 20 Y

Benchmark Series for 2014 & 2015

Government Securities Financing (Gross) Revised Budget 2015

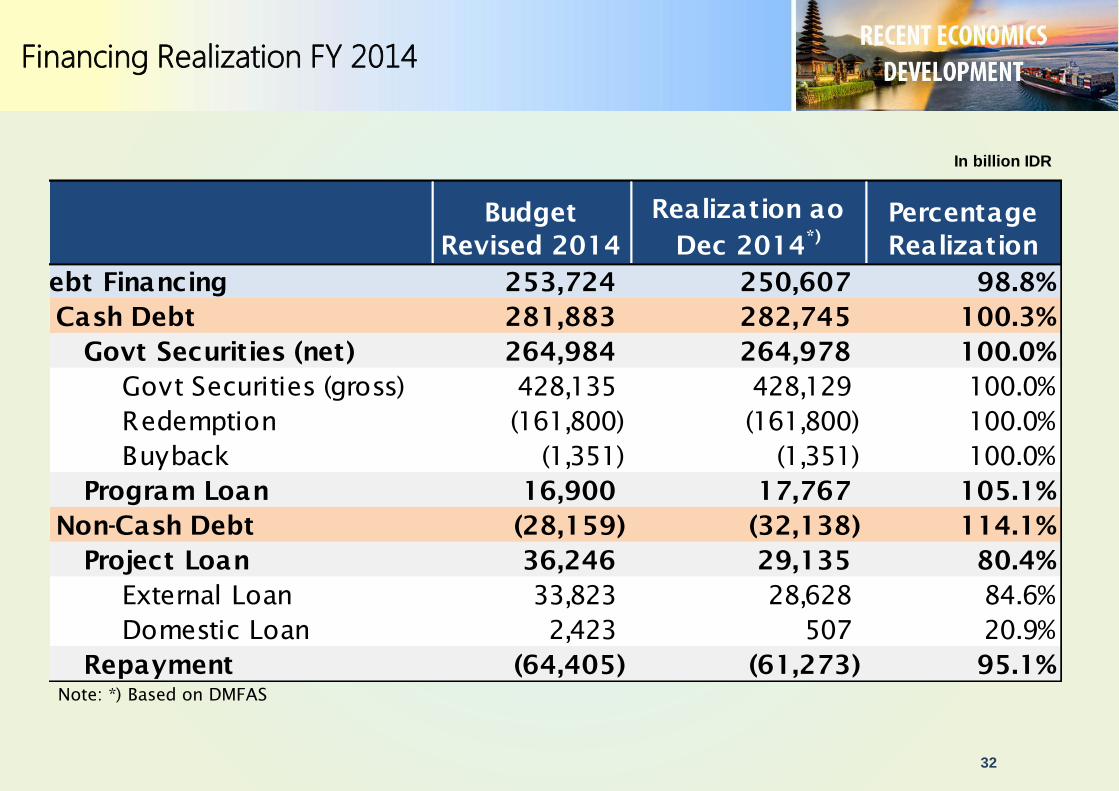

Financing Realization FY 2014

32

In billion IDR

Note: *) Based on DMFAS

Budget

Revised 2014

Realization ao

Dec 2014*)

Percentage

Realization

Debt Financing 253,724 250,607 98.8%

Cash Debt 281,883 282,745 100.3%

Govt Securities (net) 264,984 264,978 100.0%

Govt Securities (gross) 428,135 428,129 100.0%

Redemption (161,800) (161,800) 100.0%

Buyback (1,351) (1,351) 100.0%

Program Loan 16,900 17,767 105.1%

Non-Cash Debt (28,159) (32,138) 114.1%

Project Loan 36,246 29,135 80.4%

External Loan 33,823 28,628 84.6%

Domestic Loan 2,423 507 20.9%

Repayment (64,405) (61,273) 95.1%

Improved Government Debt Position

33

2468

10121416182022

Apr'0

8

Jul'0

8

Oct'0

8

Jan'0

9

Apr'0

9

Jul'0

9

Oct'0

9

Jan'1

0

Apr'1

0

Jul'1

0

Oct'1

0

Jan'1

1

Apr'1

1

Jul'1

1

Oct'1

1

Jan'1

2

Apr'1

2

Jul'1

2

Oct'1

2

Jan'1

3

Apr'1

3

Jul'1

3

Oct'1

3

Jan'1

4

Apr'1

4

Jul'1

4

Oct'1

4

Jan'1

5

5Y 10Y 15Y 20Y

6.82 (5Y), 7.01 (10Y), 7.26 (15Y), 7.37 (20Y)

[In Percentage]

As of Jan 30, 2015 Yield of Benchmark Series

Global

Financial

Crisis

Eurozonesovereign debt

crisis

Source: Ministry of Finance, Bloomberg

Secondary Market Performance of Central Government Bonds

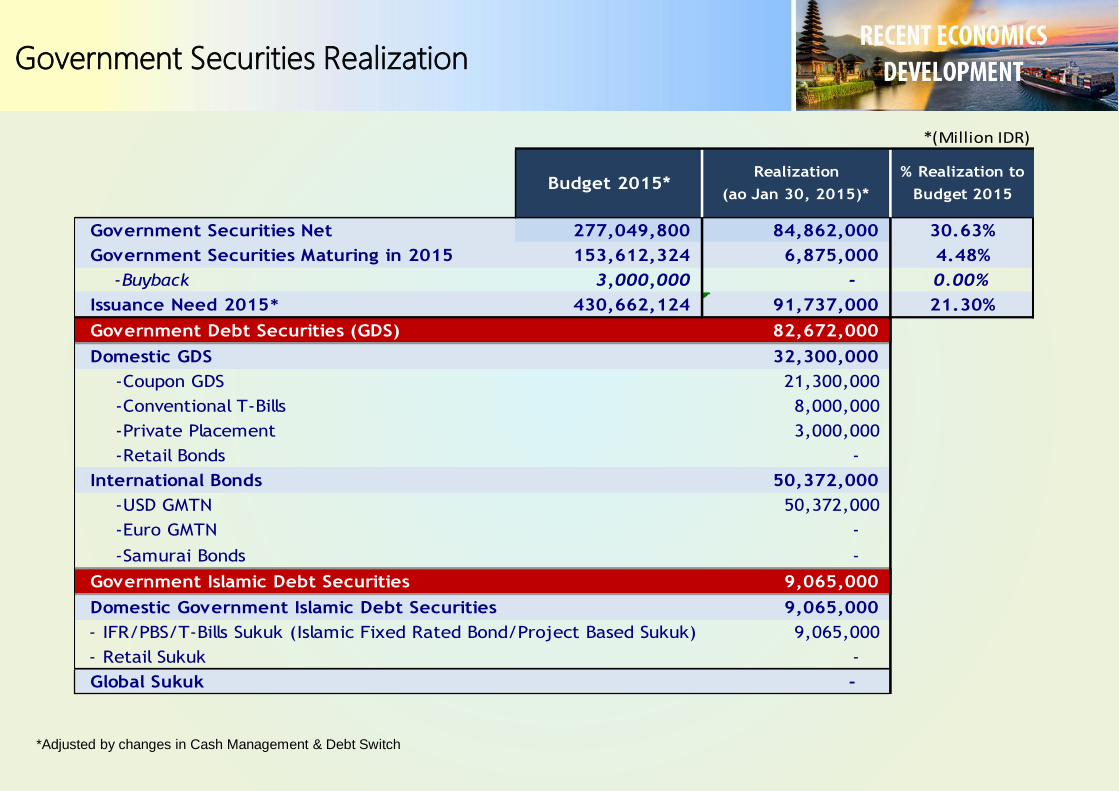

*Adjusted by changes in Cash Management & Debt Switch

*(Million IDR)

Budget 2015*Realization

(ao Jan 30, 2015)*

% Realization to

Budget 2015

Government Securities Net 277,049,800 84,862,000 30.63%

Government Securities Maturing in 2015 153,612,324 6,875,000 4.48%

-Buyback 3,000,000 - 0.00%

Issuance Need 2015* 430,662,124 91,737,000 21.30%

Government Debt Securities (GDS) 82,672,000

Domestic GDS 32,300,000

-Coupon GDS 21,300,000

-Conventional T-Bills 8,000,000

-Private Placement 3,000,000

-Retail Bonds -

International Bonds 50,372,000

-USD GMTN 50,372,000

-Euro GMTN -

-Samurai Bonds -

Government Islamic Debt Securities 9,065,000

Domestic Government Islamic Debt Securities 9,065,000

- IFR/PBS/T-Bills Sukuk (Islamic Fixed Rated Bond/Project Based Sukuk) 9,065,000

- Retail Sukuk -

Global Sukuk -

Government Securities Realization

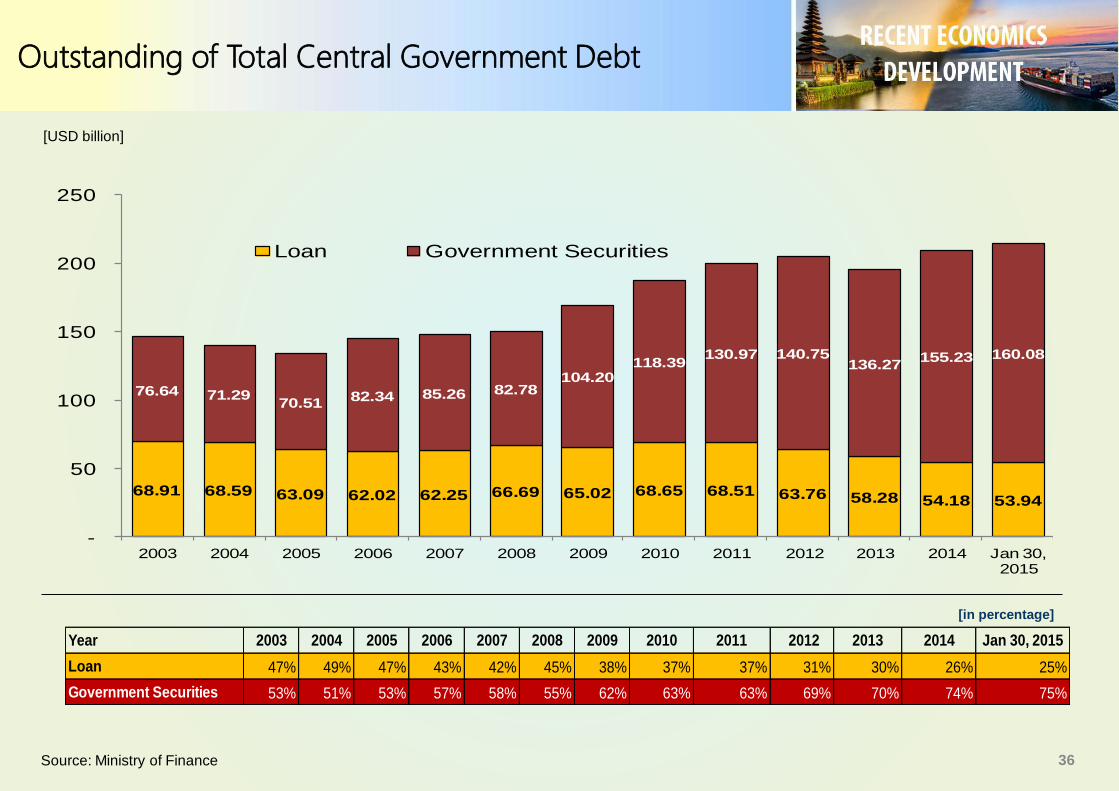

36Source: Ministry of Finance

[in percentage]

[USD billion]

68.91 68.59 63.09 62.02 62.25 66.69 65.02 68.65 68.51 63.76 58.28 54.18 53.94

76.64 71.2970.51

82.34 85.26 82.78104.20

118.39130.97 140.75

136.27155.23 160.08

-

50

100

150

200

250

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Jan 30, 2015

Loan Government Securities

Year 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Jan 30, 2015

Loan 47% 49% 47% 43% 42% 45% 38% 37% 37% 31% 30% 26% 25%

Government Securities 53% 51% 53% 57% 58% 55% 62% 63% 63% 69% 70% 74% 75%

Outstanding of Total Central Government Debt

37

Maturity Profile of Central Government by Instruments (in trillion IDR)

Maturity Profile of Central Government by Currencies (in trillion IDR)

020406080

100120140160180200220240

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

-20

60

Foreign Domestic

020406080

100120140160180200220240

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

-20

60

Gov't Securities Loan

44.1%

55.9%

Foreign

Domestik

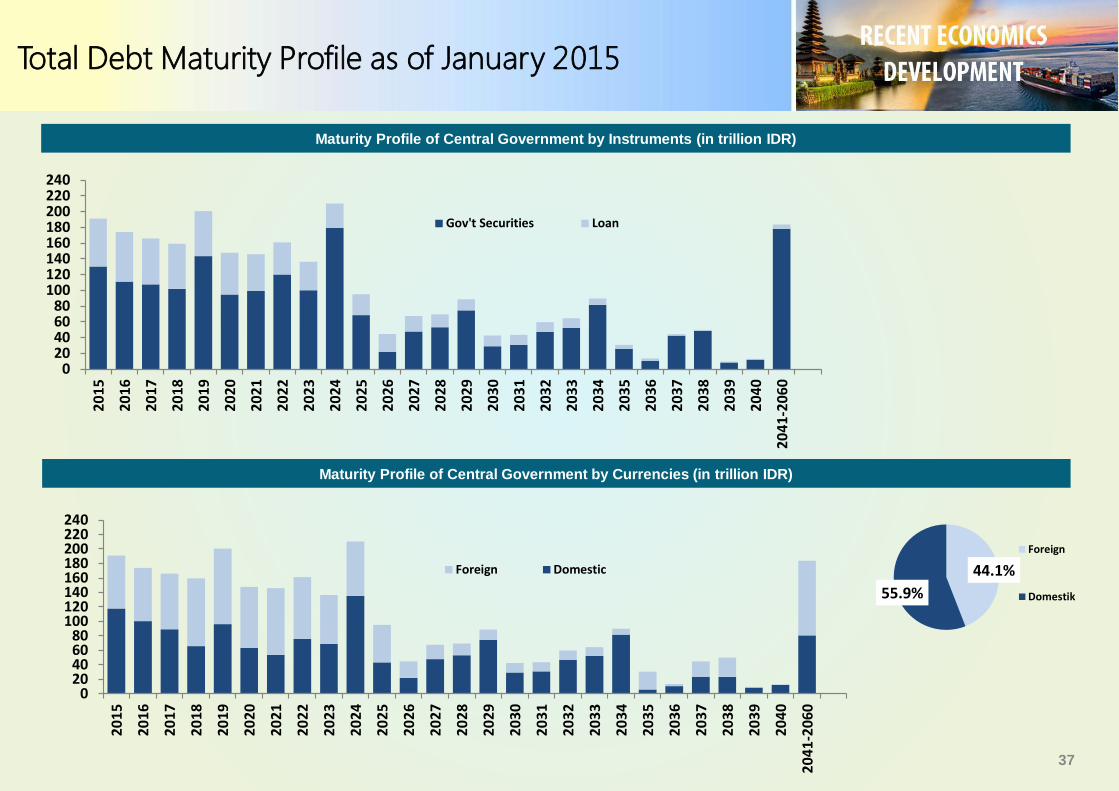

Total Debt Maturity Profile as of January 2015

38

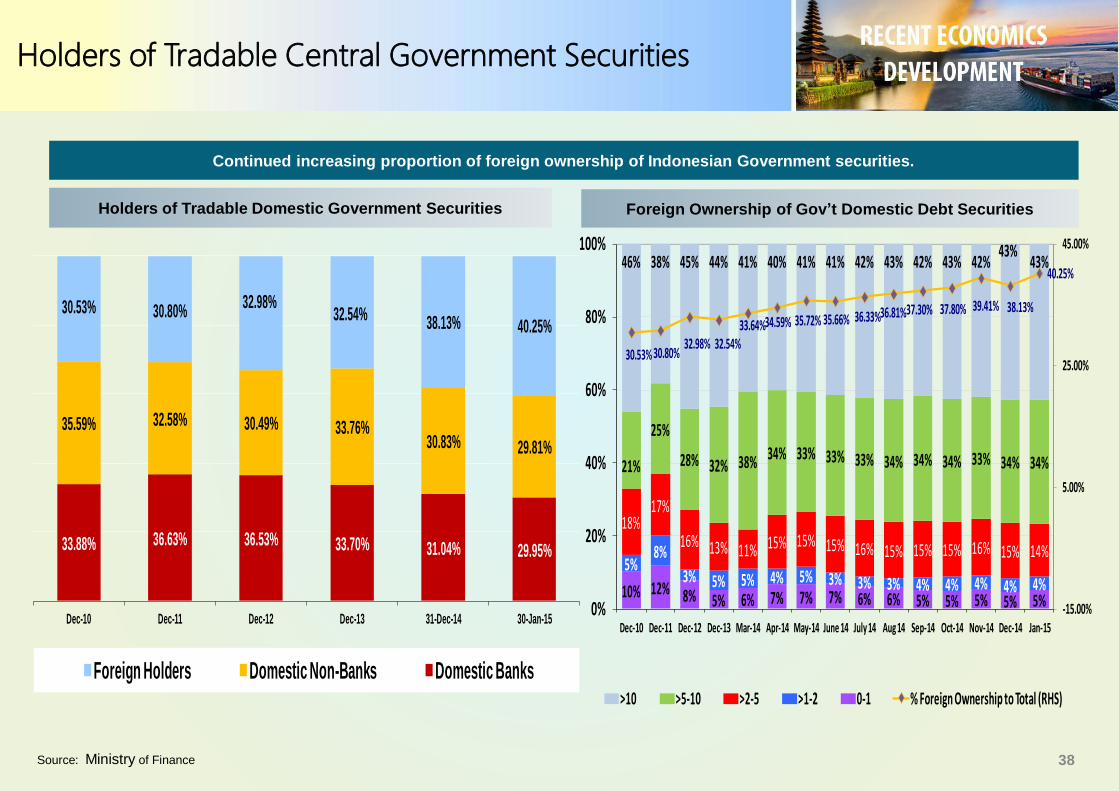

Holders of Tradable Domestic Government Securities Foreign Ownership of Gov’t Domestic Debt Securities

Source: Ministry of Finance

Continued increasing proportion of foreign ownership of Indonesian Government securities.

10% 12% 8% 5% 6% 7% 7% 7% 6% 6% 5% 5% 5% 5% 5%

5%8%

3% 5% 5% 4% 5% 3% 3% 3% 4% 4% 4% 4% 4%

18%17%

16% 13% 11% 15% 15% 15% 16% 15% 15% 15% 16% 15% 14%

21%

25%

28% 32% 38% 34% 33% 33% 33% 34% 34% 34% 33% 34% 34%

46% 38% 45% 44% 41% 40% 41% 41% 42% 43% 42% 43% 42%43%

43%

30.53% 30.80%32.98% 32.54%

33.64%34.59% 35.72% 35.66% 36.33%36.81%37.30% 37.80% 39.41% 38.13%

40.25%

-15.00%

5.00%

25.00%

45.00%

0%

20%

40%

60%

80%

100%

Dec-10 Dec-11 Dec-12 Dec-13 Mar-14 Apr-14 May-14 June 14 July 14 Aug 14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15

>10 >5-10 >2-5 >1-2 0-1 % Foreign Ownership to Total (RHS)

33.88% 36.63% 36.53% 33.70% 31.04% 29.95%

35.59% 32.58% 30.49% 33.76%30.83% 29.81%

30.53% 30.80%32.98%

32.54% 38.13% 40.25%

Dec-10 Dec-11 Dec-12 Dec-13 31-Dec-14 30-Jan-15

Foreign Holders Domestic Non-Banks Domestic Banks

Holders of Tradable Central Government Securities

39Source: Ministry of Finance

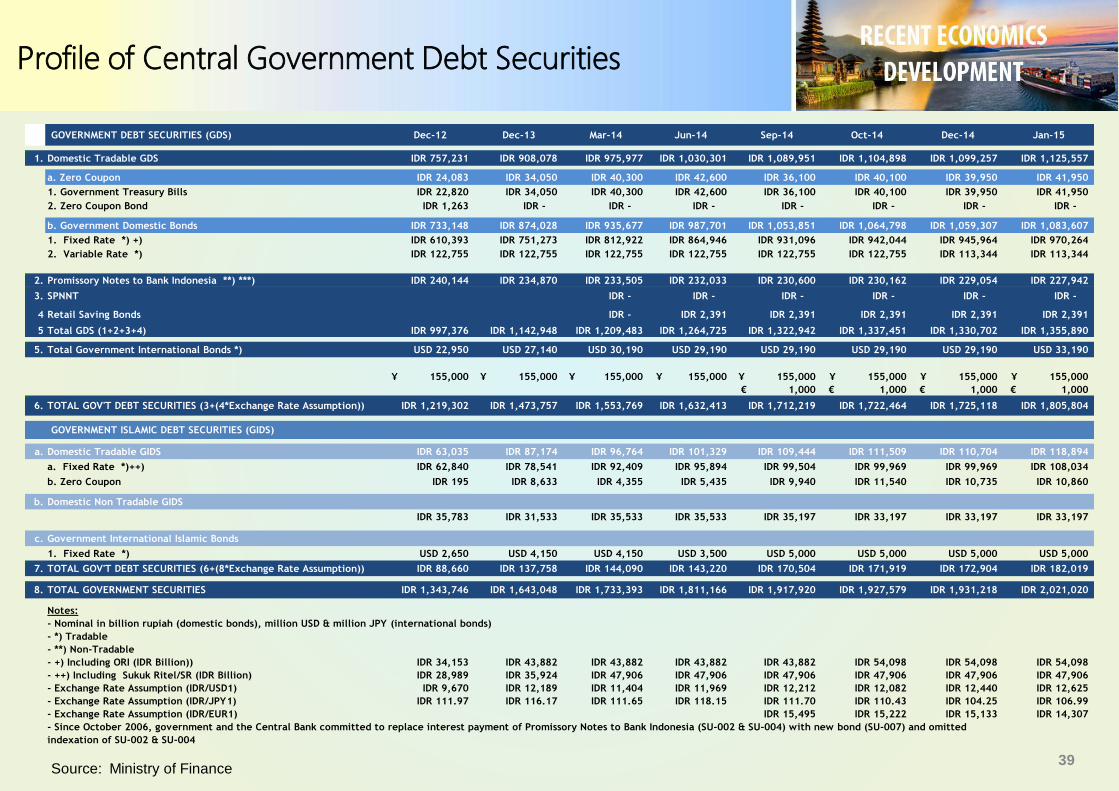

GOVERNMENT DEBT SECURITIES (GDS) Dec-12 Dec-13 Mar-14 Jun-14 Sep-14 Oct-14 Dec-14 Jan-15

1. Domestic Tradable GDS IDR 757,231 IDR 908,078 IDR 975,977 IDR 1,030,301 IDR 1,089,951 IDR 1,104,898 IDR 1,099,257 IDR 1,125,557

a. Zero Coupon IDR 24,083 IDR 34,050 IDR 40,300 IDR 42,600 IDR 36,100 IDR 40,100 IDR 39,950 IDR 41,950

1. Government Treasury Bills IDR 22,820 IDR 34,050 IDR 40,300 IDR 42,600 IDR 36,100 IDR 40,100 IDR 39,950 IDR 41,950

2. Zero Coupon Bond IDR 1,263 IDR - IDR - IDR - IDR - IDR - IDR - IDR -

b. Government Domestic Bonds IDR 733,148 IDR 874,028 IDR 935,677 IDR 987,701 IDR 1,053,851 IDR 1,064,798 IDR 1,059,307 IDR 1,083,607

1. Fixed Rate *) +) IDR 610,393 IDR 751,273 IDR 812,922 IDR 864,946 IDR 931,096 IDR 942,044 IDR 945,964 IDR 970,264

2. Variable Rate *) IDR 122,755 IDR 122,755 IDR 122,755 IDR 122,755 IDR 122,755 IDR 122,755 IDR 113,344 IDR 113,344

2. Promissory Notes to Bank Indonesia **) ***) IDR 240,144 IDR 234,870 IDR 233,505 IDR 232,033 IDR 230,600 IDR 230,162 IDR 229,054 IDR 227,942

3. SPNNT IDR - IDR - IDR - IDR - IDR - IDR -

4 Retail Saving Bonds IDR - IDR 2,391 IDR 2,391 IDR 2,391 IDR 2,391 IDR 2,391

5 Total GDS (1+2+3+4) IDR 997,376 IDR 1,142,948 IDR 1,209,483 IDR 1,264,725 IDR 1,322,942 IDR 1,337,451 IDR 1,330,702 IDR 1,355,890

5. Total Government International Bonds *) USD 22,950 USD 27,140 USD 30,190 USD 29,190 USD 29,190 USD 29,190 USD 29,190 USD 33,190

155,000¥ 155,000¥ 155,000¥ 155,000¥ 155,000¥ 155,000¥ 155,000¥ 155,000¥

1,000€ 1,000€ 1,000€ 1,000€

6. TOTAL GOV'T DEBT SECURITIES (3+(4*Exchange Rate Assumption)) IDR 1,219,302 IDR 1,473,757 IDR 1,553,769 IDR 1,632,413 IDR 1,712,219 IDR 1,722,464 IDR 1,725,118 IDR 1,805,804

GOVERNMENT ISLAMIC DEBT SECURITIES (GIDS)

a. Domestic Tradable GIDS IDR 63,035 IDR 87,174 IDR 96,764 IDR 101,329 IDR 109,444 IDR 111,509 IDR 110,704 IDR 118,894

a. Fixed Rate *)++) IDR 62,840 IDR 78,541 IDR 92,409 IDR 95,894 IDR 99,504 IDR 99,969 IDR 99,969 IDR 108,034

b. Zero Coupon IDR 195 IDR 8,633 IDR 4,355 IDR 5,435 IDR 9,940 IDR 11,540 IDR 10,735 IDR 10,860

b. Domestic Non Tradable GIDS

IDR 35,783 IDR 31,533 IDR 35,533 IDR 35,533 IDR 35,197 IDR 33,197 IDR 33,197 IDR 33,197

c. Government International Islamic Bonds

1. Fixed Rate *) USD 2,650 USD 4,150 USD 4,150 USD 3,500 USD 5,000 USD 5,000 USD 5,000 USD 5,000

7. TOTAL GOV'T DEBT SECURITIES (6+(8*Exchange Rate Assumption)) IDR 88,660 IDR 137,758 IDR 144,090 IDR 143,220 IDR 170,504 IDR 171,919 IDR 172,904 IDR 182,019

8. TOTAL GOVERNMENT SECURITIES IDR 1,343,746 IDR 1,643,048 IDR 1,733,393 IDR 1,811,166 IDR 1,917,920 IDR 1,927,579 IDR 1,931,218 IDR 2,021,020

Notes:

- Nominal in billion rupiah (domestic bonds), million USD & million JPY (international bonds)

- *) Tradable

- **) Non-Tradable

- +) Including ORI (IDR Billion)) IDR 34,153 IDR 43,882 IDR 43,882 IDR 43,882 IDR 43,882 IDR 54,098 IDR 54,098 IDR 54,098

- ++) Including Sukuk Ritel/SR (IDR Billion) IDR 28,989 IDR 35,924 IDR 47,906 IDR 47,906 IDR 47,906 IDR 47,906 IDR 47,906 IDR 47,906

- Exchange Rate Assumption (IDR/USD1) IDR 9,670 IDR 12,189 IDR 11,404 IDR 11,969 IDR 12,212 IDR 12,082 IDR 12,440 IDR 12,625

- Exchange Rate Assumption (IDR/JPY1) IDR 111.97 IDR 116.17 IDR 111.65 IDR 118.15 IDR 111.70 IDR 110.43 IDR 104.25 IDR 106.99

- Exchange Rate Assumption (IDR/EUR1) IDR 15,495 IDR 15,222 IDR 15,133 IDR 14,307

- Since October 2006, government and the Central Bank committed to replace interest payment of Promissory Notes to Bank Indonesia (SU-002 & SU-004) with new bond (SU-007) and omitted

indexation of SU-002 & SU-004

Profile of Central Government Debt Securities

40

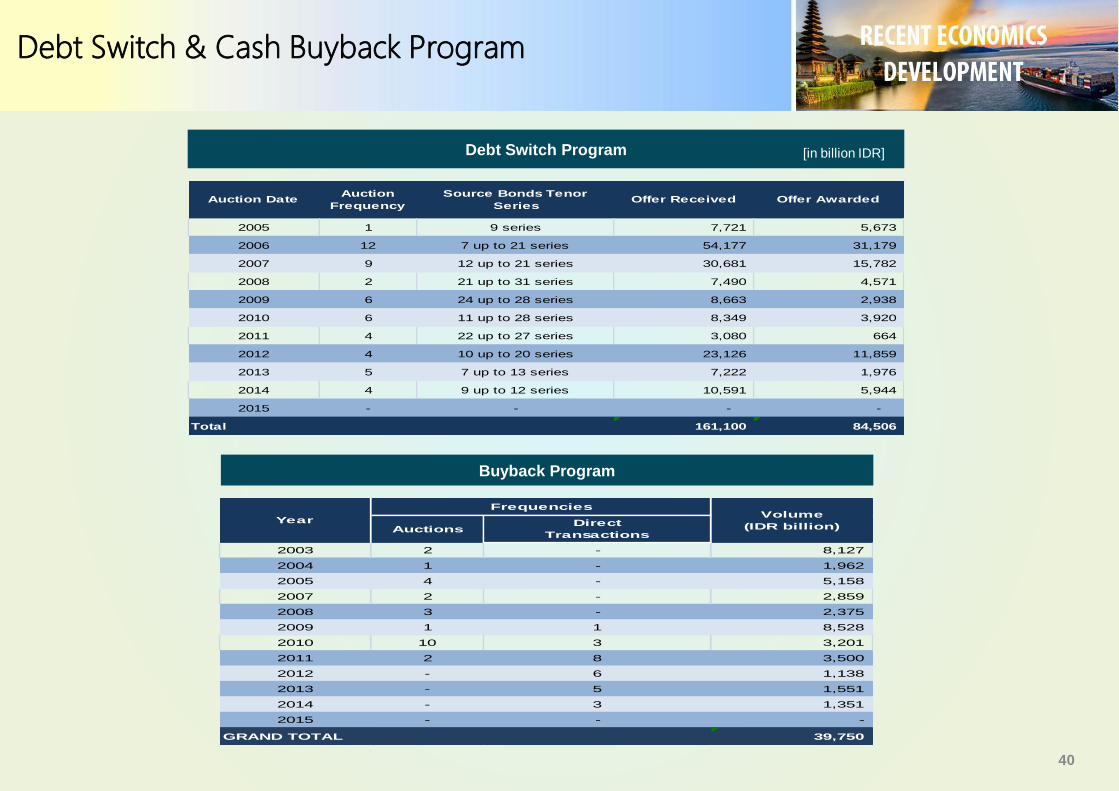

Debt Switch Program

Buyback Program

[in billion IDR]

Auction DateAuction

Frequency

Source Bonds Tenor

SeriesOffer Received Offer Awarded

2005 1 9 series 7,721 5,673

2006 12 7 up to 21 series 54,177 31,179

2007 9 12 up to 21 series 30,681 15,782

2008 2 21 up to 31 series 7,490 4,571

2009 6 24 up to 28 series 8,663 2,938

2010 6 11 up to 28 series 8,349 3,920

2011 4 22 up to 27 series 3,080 664

2012 4 10 up to 20 series 23,126 11,859

2013 5 7 up to 13 series 7,222 1,976

2014 4 9 up to 12 series 10,591 5,944

2015 - - - -

Total 161,100 84,506

AuctionsDirect

Transactions

2003 2 - 8,127

2004 1 - 1,962

2005 4 - 5,158

2007 2 - 2,859

2008 3 - 2,375

2009 1 1 8,528

2010 10 3 3,201

2011 2 8 3,500

2012 - 6 1,138

2013 - 5 1,551

2014 - 3 1,351

2015 - - -

GRAND TOTAL 39,750

Frequencies

YearVolume

(IDR billion)

Debt Switch & Cash Buyback Program

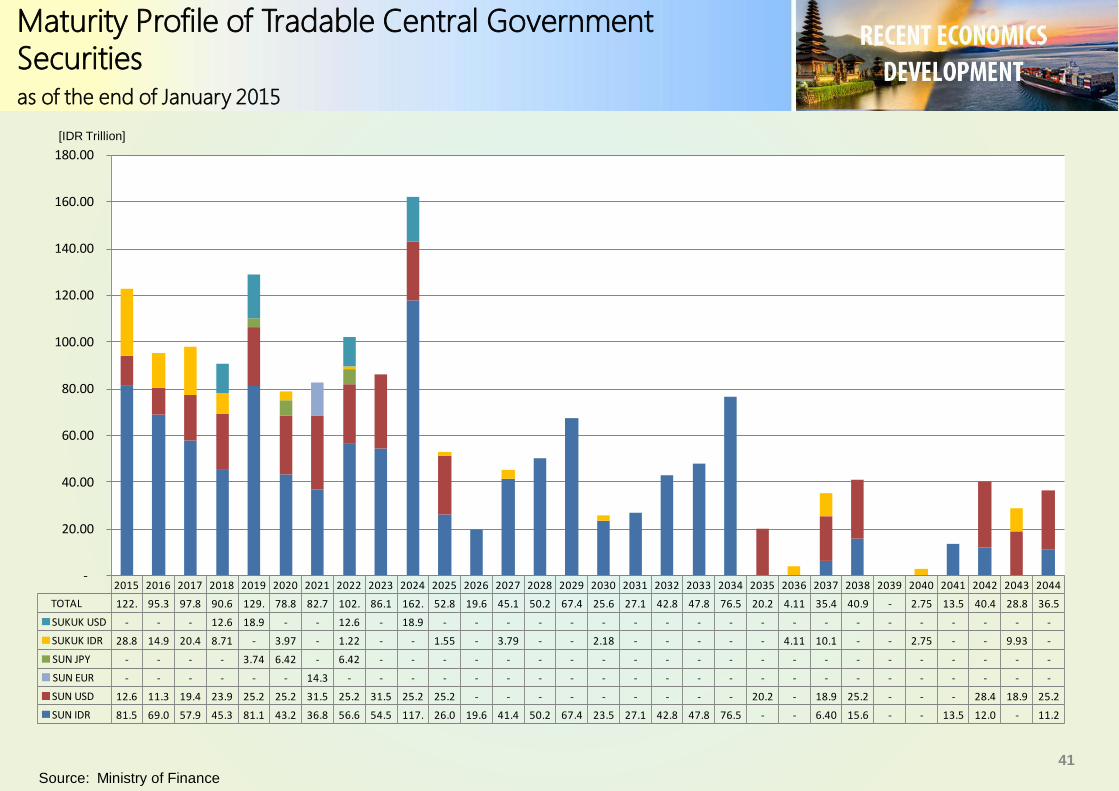

41

Source: Ministry of Finance

[IDR Trillion]

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043 2044

TOTAL 122. 95.3 97.8 90.6 129. 78.8 82.7 102. 86.1 162. 52.8 19.6 45.1 50.2 67.4 25.6 27.1 42.8 47.8 76.5 20.2 4.11 35.4 40.9 - 2.75 13.5 40.4 28.8 36.5

SUKUK USD - - - 12.6 18.9 - - 12.6 - 18.9 - - - - - - - - - - - - - - - - - - - -

SUKUK IDR 28.8 14.9 20.4 8.71 - 3.97 - 1.22 - - 1.55 - 3.79 - - 2.18 - - - - - 4.11 10.1 - - 2.75 - - 9.93 -

SUN JPY - - - - 3.74 6.42 - 6.42 - - - - - - - - - - - - - - - - - - - - - -

SUN EUR - - - - - - 14.3 - - - - - - - - - - - - - - - - - - - - - - -

SUN USD 12.6 11.3 19.4 23.9 25.2 25.2 31.5 25.2 31.5 25.2 25.2 - - - - - - - - - 20.2 - 18.9 25.2 - - - 28.4 18.9 25.2

SUN IDR 81.5 69.0 57.9 45.3 81.1 43.2 36.8 56.6 54.5 117. 26.0 19.6 41.4 50.2 67.4 23.5 27.1 42.8 47.8 76.5 - - 6.40 15.6 - - 13.5 12.0 - 11.2

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

Maturity Profile of Tradable Central Government Securities as of the end of January 2015

42

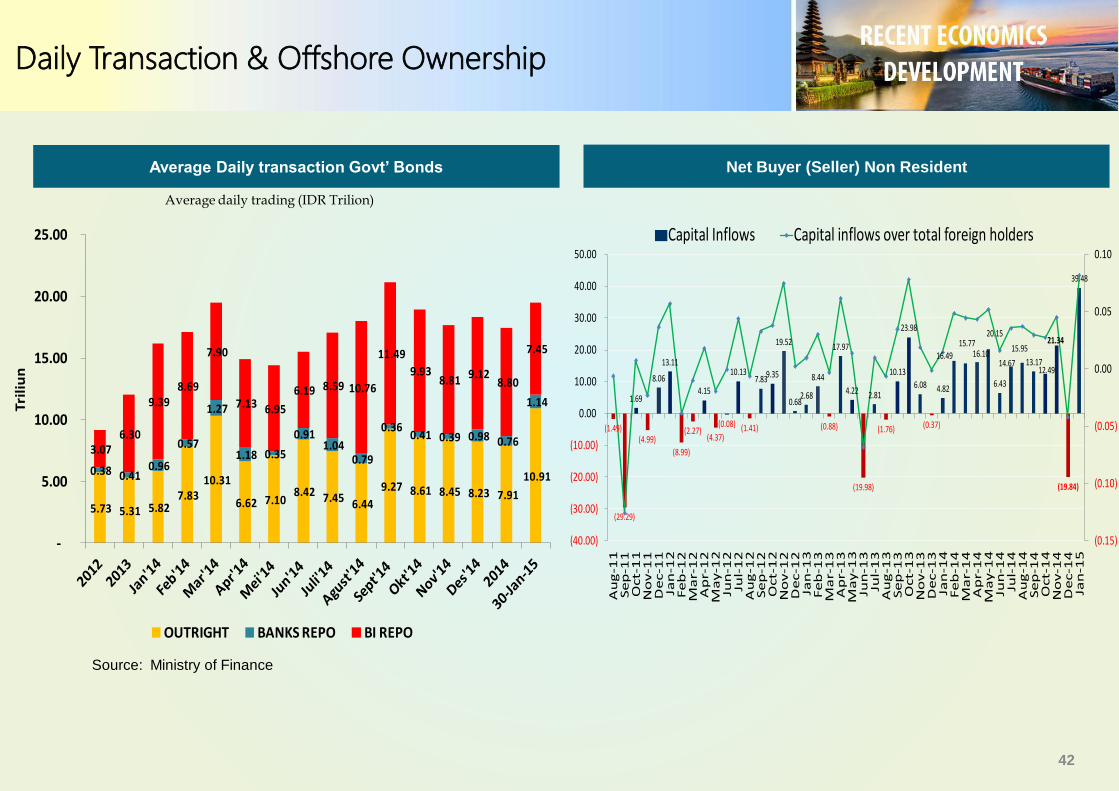

Average Daily transaction Govt’ Bonds Net Buyer (Seller) Non Resident

Source: Ministry of Finance

Average daily trading (IDR Trilion)

(1.49)

(29.29)

1.69

(4.99)

8.06

13.11

(8.99)

(2.27)

4.15

(4.37)

(0.08)

10.13

(1.41)

7.83 9.35

19.52

0.68 2.68

8.44

(0.88)

17.97

4.22

(19.98)

2.81

(1.76)

10.13

23.98

6.08

(0.37)

4.82

16.49

15.77 16.10

20.15

6.43

14.67

15.95

13.17 12.49

21.34

(19.84)

39.48

(0.15)

(0.10)

(0.05)

0.00

0.05

0.10

(40.00)

(30.00)

(20.00)

(10.00)

0.00

10.00

20.00

30.00

40.00

50.00

Au

g-1

1Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

2Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

No

v-1

3D

ec-1

3Ja

n-1

4Fe

b-1

4M

ar-

14

Ap

r-1

4M

ay-1

4Ju

n-1

4Ju

l-1

4A

ug

-14

Se

p-1

4O

ct-

14

No

v-1

4D

ec-1

4Ja

n-1

5

Capital Inflows Capital inflows over total foreign holders

5.73 5.31 5.82 7.83

10.31

6.62 7.10 8.42 7.45 6.44

9.27 8.61 8.45 8.23 7.91

10.91 0.38 0.41 0.96

0.57

1.27

1.18 0.35

0.91 1.04

0.79

0.36 0.41 0.39 0.98 0.76

1.14

3.07 6.30

9.39 8.69

7.90

7.13 6.95

6.19 8.59 10.76

11.49

9.93 8.81 9.12

8.80

7.45

-

5.00

10.00

15.00

20.00

25.00

Tri

liu

n

OUTRIGHT BANKS REPO BI REPO

Daily Transaction & Offshore Ownership

43

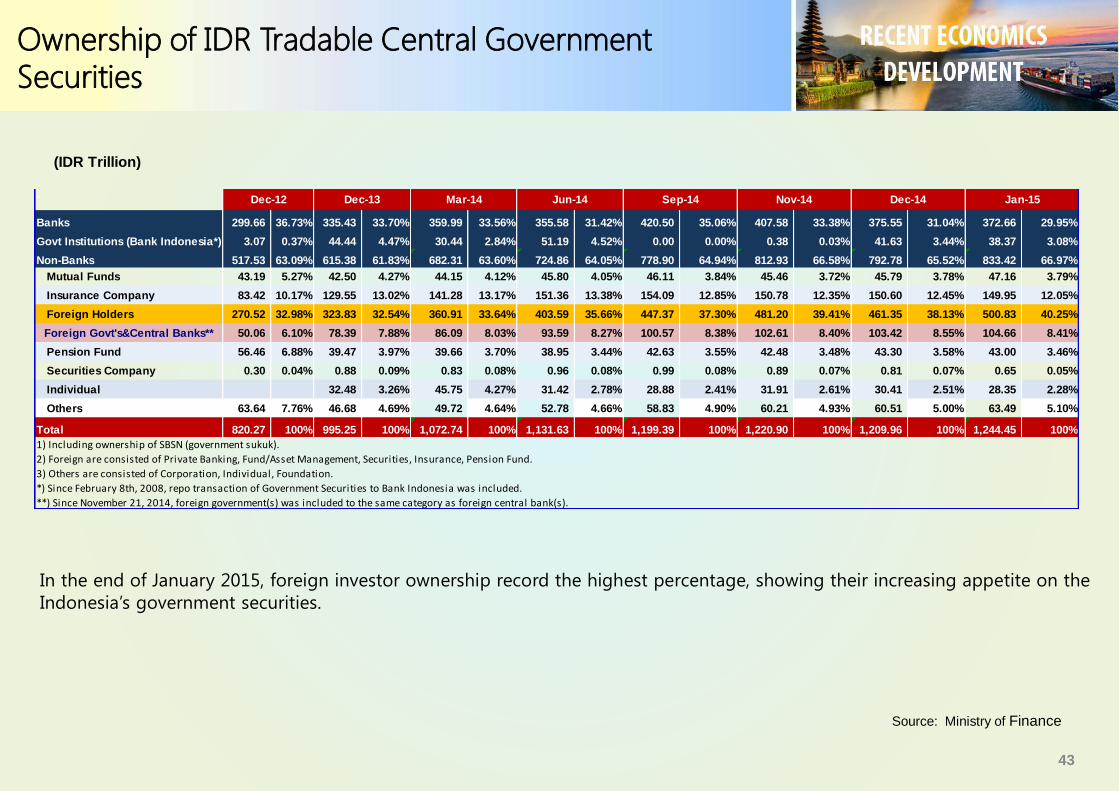

Source: Ministry of Finance

(IDR Trillion)

`

Banks 299.66 36.73% 335.43 33.70% 359.99 33.56% 355.58 31.42% 420.50 35.06% 407.58 33.38% 375.55 31.04% 372.66 29.95%

Govt Institutions (Bank Indonesia*) 3.07 0.37% 44.44 4.47% 30.44 2.84% 51.19 4.52% 0.00 0.00% 0.38 0.03% 41.63 3.44% 38.37 3.08%

Non-Banks 517.53 63.09% 615.38 61.83% 682.31 63.60% 724.86 64.05% 778.90 64.94% 812.93 66.58% 792.78 65.52% 833.42 66.97%

Mutual Funds 43.19 5.27% 42.50 4.27% 44.15 4.12% 45.80 4.05% 46.11 3.84% 45.46 3.72% 45.79 3.78% 47.16 3.79%

Insurance Company 83.42 10.17% 129.55 13.02% 141.28 13.17% 151.36 13.38% 154.09 12.85% 150.78 12.35% 150.60 12.45% 149.95 12.05%

Foreign Holders 270.52 32.98% 323.83 32.54% 360.91 33.64% 403.59 35.66% 447.37 37.30% 481.20 39.41% 461.35 38.13% 500.83 40.25%

Foreign Govt's&Central Banks** 50.06 6.10% 78.39 7.88% 86.09 8.03% 93.59 8.27% 100.57 8.38% 102.61 8.40% 103.42 8.55% 104.66 8.41%

Pension Fund 56.46 6.88% 39.47 3.97% 39.66 3.70% 38.95 3.44% 42.63 3.55% 42.48 3.48% 43.30 3.58% 43.00 3.46%

Securities Company 0.30 0.04% 0.88 0.09% 0.83 0.08% 0.96 0.08% 0.99 0.08% 0.89 0.07% 0.81 0.07% 0.65 0.05%

Individual 32.48 3.26% 45.75 4.27% 31.42 2.78% 28.88 2.41% 31.91 2.61% 30.41 2.51% 28.35 2.28%

Others 63.64 7.76% 46.68 4.69% 49.72 4.64% 52.78 4.66% 58.83 4.90% 60.21 4.93% 60.51 5.00% 63.49 5.10%

Total 820.27 100% 995.25 100% 1,072.74 100% 1,131.63 100% 1,199.39 100% 1,220.90 100% 1,209.96 100% 1,244.45 100%

1) Including ownership of SBSN (government sukuk).

2) Foreign are consisted of Private Banking, Fund/Asset Management, Securities, Insurance, Pension Fund.

3) Others are consisted of Corporation, Individual, Foundation.

*) Since February 8th, 2008, repo transaction of Government Securities to Bank Indonesia was included.

**) Since November 21, 2014, foreign government(s) was included to the same category as foreign central bank(s).

Jan-15Dec-14Nov-14Mar-14Dec-13Dec-12 Jun-14 Sep-14

In the end of January 2015, foreign investor ownership record the highest percentage, showing their increasing appetite on the

Indonesia’s government securities.

Ownership of IDR Tradable Central Government Securities

![Investor Relations - hanatourcompany.comhanatour]ir_presentation_june... · Investor Relations 1 Investor Relations Jun. 2009.(Korean) 2 ... (cf. 국내소비0.3% 증가, 자료:한국은행,2006)](https://img.pdfslide.net/doc/110x75/5a881d307f8b9a87368ecd91/investor-relations-hanatourirpresentationjuneinvestor-relations-1-investor.jpg)