Embed Size (px)

Citation preview

Absa AgriBusiness

Presenter nameSubject

Disclaimer: Although everything has been done to ensure the accuracy of the information, the Bank takes no responsibility for actions or losses that might occur due to the usage of this information.

ABSA AgriBusiness

Agric-Economic Outlook

1 October 2009

Absa AgriBusiness

Discussion agenda

1. Macro economic trends – World social spend supports agriculture

2. Agricultural insights - Golden days for agriculture is back

3. Africa the new frontier – Food security

4. Commodity outlook for Selected Agricultural commodities

Absa AgriBusiness

Economic outlook – Supply and demand

Absa AgriBusiness

Summery of world economic impact on South African Agriculture

• This lead to a shift in demand with a resulting increase in commodity prices

• The demand for bio-fuels also impacted positively on commodity prices

• Commodity prices was further supported by lower world stocks

• Food demand remain sticky

US Maize prices($/t)

-

50.0

100.0

150.0

200.0

250.0

1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

• Shift in world soft commodity demand – After capitalism replaced communism as economic system in the late 90’s

world economic growth increased to more than 4.9% per annum for the four years preceding 2008

– In 2008 - 2009 world experienced a financial meltdown• World wide approximately one billion jobs will be lost during 2009 • In SA approximately 600 000 jobs is expected to be lost in 2009• If you loos your job you loos your house and your car but you do not loos the need to eat

– In a world economic crisis the poor of the poor (job less) is supported by social spend (Dole, Workmen's compensation, Food stamps, Social spend) supporting demaand.

The net result is higher commodity prices in spite of a world economic meltdown

Absa AgriBusiness

Exchange rate impact on South African Agriculture

Absa AgriBusiness

Economic outlook – Balance of Payment

• Exchange rate indicators

• The rand will continue to strengthen against the US Dollar and Chinese currencies while the dollar will tend to weaken against the Euro

• This is mainly due to the link between the US dollar and the Chinese Yuan as well as the current account deficit of the US (- 3% of GDP)

• The Rand is expected to continue to weaken against the bulk of the other currencies

Relation between Long-term capital movements and Balance on current Account (R '000 000)

Nominal exchange rates(SA cents / Fc unit)

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

Ma

r-0

1

Ma

r-0

2

Ma

r-0

3

Ma

r-0

4

Ma

r-0

5

Ma

r-0

6

Ma

r-0

7

Ma

r-0

8Current accountCapital movements

10

210

410

610

810

1010

1210

1410

1610

1810

2010

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Aus Dollar US Dollar UK PoundEuro Yuan

Sources: SA Reserve Bank, ABSA

Absa AgriBusiness

Economic outlook – Inflation

Pointers• Due to higher inflation in 2007 and 2008 the Reserve Bank increased interests rates in a

bid to control inflation. • All indication are that inflation is under control and it is expected that inflation will

continue to decline creating some leeway for the Reserve Bank to lower interest rates even further.

Relation between consumer price (CPI) and Producer price (PPI) index (% change)

Relation between agricultural input and output prices (%

change)

0%

5%

10%

15%

20%

25%

30%

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

PPI All items CPI All items CPI Food CPIX

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1990 1995 2000 2005 2010

Agricultural PPI

Farming requisites

Producer price

Sources: SA Reserve Bank, own calculations

Absa AgriBusiness

Discussion agenda

1. Macro economic trends – World social spend supports agriculture

2. Agricultural insights - Golden days for agriculture is back

3. Africa the new frontier – Food security

4. Commodity outlook for Selected Agricultural commodities

Absa AgriBusiness

Effective Market

Absa AgriBusiness

Primary agricultural confidence index

WEIGHTED AGRIC INDEX (2000 = 100)

50

100

150

200

250

300

Jan-2000 Jan-2001 Jan-2002 Jan-2003 Jan-2004 Jan-2005 Jan-2006 Jan-2007 Jan-2008 Jan-2009

Ag

ric

ind

ex

50

250

450

650

850

1050

NF

I In

dex

Price Indexs Cost Indexs Agri Profit Index One Year Profit Average NFI Index Linear (Agri Profit Index)

Cost index was adjusted downward to reflect percentage deferential between Gross Producer Value (GDV) and total spend on Intermediary inputs in 2000 (cost = 52% of revenue)

Absa AgriBusiness

Discussion agenda

1. Macro economic trends – World social spend supports agriculture

2. Agricultural insights - Golden days for agriculture is back

3. Africa the new frontier – Food security

4. Commodity outlook for Selected Agricultural commodities

Absa AgriBusiness

Absa AgriBusiness

12

3

45

6

7

Pool gebied

Berg gebied

Toendra / Taiga

Gematigde

Mediterreens

Droë Grassvelde

Woestyn

Subtrope

Trope

Klimaat Topografie

12

3

45

6

7

Pool gebied

Berg gebied

Toendra / Taiga

Gematigde

Mediterreens

Droë Grassvelde

Woestyn

Subtrope

Trope

Klimaat Topografie

Polar area

Mountain area

Tundra / Taiga

Moderate

Mediterranean

Dry grasslands

Desert

Subtropical

Tropical

Climatic topography

World Climatic topography

Absa AgriBusiness

Market environment – World Market growth potential (2)

Pointers• Production growth

potential for 2050 must be viewed against expected growth in demand of approximately 40 – 60 % over the same period

• This is mainly the result of an expected population growth rate of between 0,9% to 1,1% and improvements in the economic welfare of consumers due to economic growth.

• Only a portion of economic growth will impact on the growth in demand for food as food is classified as one of the basic needs.

1980

2004

Growth 1980 tot

2004

Expected Production

2050

%

North and Central America

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

624 279 337 13 31

621 272 478 23 50

-0.5% -2.3% 41.9% 79.4% 64.2%

611 278 579 38 73

-1.7% 2.0%

21.0% 66.0% 44.0%

Europe

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

227 141 258

5 39

487 304 466 16 53

114.4% 116.0%

80.6% 229.9%

33.3%

477 289 671 31 87

-2.0% -5.0% 44.0%

102.0% 66.0%

Russia

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

553 232 170

3 15

567 207 157

5 10

2.4% -10.8%

-7.8% 56.7%

-36.9%

578 217 171

8 18

2.0% 5.0% 9.0%

65.0% 88.0%

South America and Caribbean Agricultural Land (Ha million)

Arable Land (Ha million) Coarse grain production (Ton million)

Oil seed production (Ton million) Meat production (Ton million)

717 146 88 6

16

784 169 158 21 38

9.4% 16.0% 79.2%

220.8% 138.4%

831 235 253 46

101

6.0% 39.0% 59.9%

124.0% 168.0%

Absa AgriBusiness

Market environment – World market growth potential (3)

Pointers• In the short term stiff

competition in terms of production expansion will come from South America.

• The most significant untapped opportunity is Africa

• As production expansion exceed demand expectations, prices of soft commodities will remain fairly depressed forcing farmers to improve efficiencies. This is only possible if producers incorporate new technology to improve efficiencies or use efficiencies of scale.

1980

2004

Growth 1980 tot

2004

Expected Production

2050

%

Africa

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

1,077 178 73

4 7

1,111 211 128

8 12

3.2% 18.3% 75.9% 67.4% 79.9%

1,200 337 323

20 28

8.0% 60.0%

153.0% 172.0% 132.0%

Asia

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

1,153 458 632 18 29

1,684 573

1,038 66

108

46.1% 25.1% 64.2%

261.0% 277.1%

1,852 642

1,525 149 239

10.0% 12.0% 47.0%

126.0% 121.0%

Australia and New-Zeeland

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

483 44 16

0 3

447 49 31 1 4

-7.4% 10.0% 91.1%

504.2% 41.0%

429 59 61 2 7

-4.0% 22.0% 94.0%

223.0% 80.0%

World

Agricultural Land (Ha million) Arable Land (Ha million)

Coarse grain production (Ton million) Oil seed production (Ton million)

Meat production (Ton million)

4,117 1,332 1,486

43 123

4,917 1,616 2,298

117 236

19.4% 21.3% 54.6%

170.7% 91.8%

5,978 2,057 3,584

295 552

4.9% 15.3% 45.9%

114.0% 101.5%

Absa AgriBusiness

Discussion agenda

1. Macro economic trends – World social spend supports agriculture

2. Agricultural insights - Golden days for agriculture is back

3. Africa the new frontier – Food security

4. Commodity outlook for Selected Agricultural commodities

Absa AgriBusiness

Summery – every thing is market driven

Absa AgriBusiness

World maize trends

World maize price and stock trends International maize price trends (US$/ton)

0

200000

400000

600000

800000

1000000

1988 1991 1994 1997 2000 2003 2006 2009 2012

0

50

100

150

200

250

Consumption Production

Stocks Price

(US $/t)('000 ton)

60

110

160

210

260

310

360

Jan-01

Jan-03

Jan-05

Jan-07

Jan-09

Jan-11

White Yellow

FAO, USDA - Economic Research Services, USDA - Agricultural Marketing Services

Absa AgriBusiness

South African maize trends

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

83/84 86/87 89/90 92/93 95/96 98/99 01/02 04/05 '07/08'10/11

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Consumption Production Stocks

Price - white Price - yellow(R/ton)('000 ton)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

82/83 86/87 90/91 94/95 98/99 02/03 06/07 '10/11

White maize Yellow maize

Source: FAO, USDA, SAGIS, SAFEX

Absa AgriBusiness

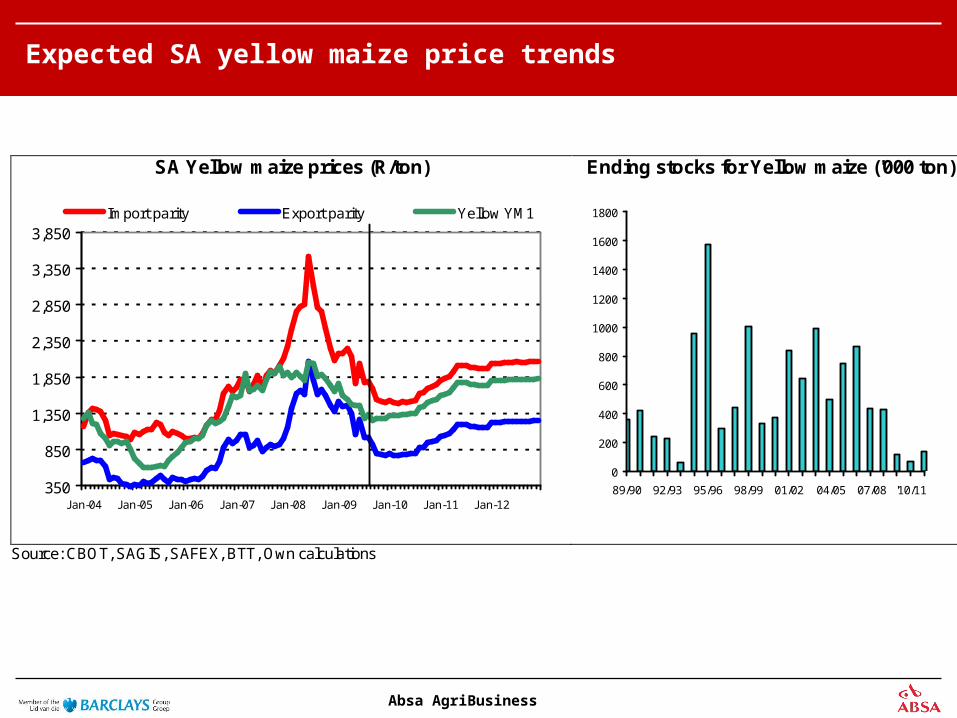

Expected SA yellow maize price trends

SA Yellow maize prices (R/ton) Ending stocks for Yellow maize ('000 ton)

350

850

1,350

1,850

2,350

2,850

3,350

3,850

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Import parity Export parity Yellow YM1

0

200

400

600

800

1000

1200

1400

1600

1800

89/90 92/93 95/96 98/99 01/02 04/05 07/08 '10/11

Source: CBOT, SAGIS, SAFEX, BTT, Own calculations

Absa AgriBusiness

Expected SA white maize price trends

SA White maize prices (R/ton) Ending stocks for white maize ('000 ton)

200

700

1,200

1,700

2,200

2,700

3,200

3,700

4,200

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Import Parity Export Parity Domestic

0

500

1000

1500

2000

2500

3000

90/91 93/94 96/97 99/00 02/03 05/06 08/09

Absa AgriBusiness

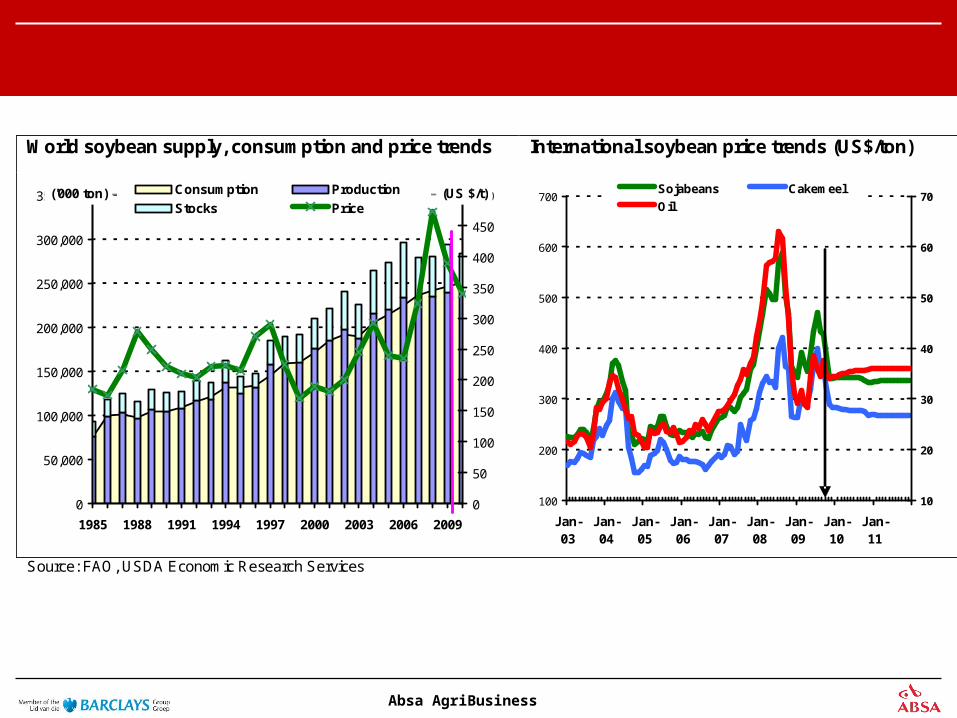

World soybean supply, consumption and price trends International soybean price trends (US$/ton)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1985 1988 1991 1994 1997 2000 2003 2006 2009

0

50

100

150

200

250

300

350

400

450

500Consumption Production

Stocks Price(US $/t)('000 ton)

100

200

300

400

500

600

700

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

10

20

30

40

50

60

70Sojabeans Cakemeel

Oil Oil US c/lb)US $/ton)

Source: FAO, USDA Economic Research Services

Absa AgriBusiness

Relationship between soybean supply, demand And price for South Africa

Soybean Future Prices (R/ton)

0

100

200

300

400

500

600

700

800

1985 1990 1995 2000 2005 2010

0

500

1000

1500

2000

2500

3000

3500

4000

4500Consumption ProductionImports StocksPrice

(R/ton)('000 ton)

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Derived Importparity SAFEX

Source: SAGIS, SA Weather Bureau, SAFEX, Own calculations

Absa AgriBusiness

SA sunflower prices (R/ton) SA sunflower ending stocks ('000 ton)

900

1900

2900

3900

4900

5900

6900

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Sunflower Import parity Sunflower domestic

0

50

100

150

200

250

300

350

400

450

500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: USDA Agricultural Market Services, SAGIS, Own calculations

Absa AgriBusiness

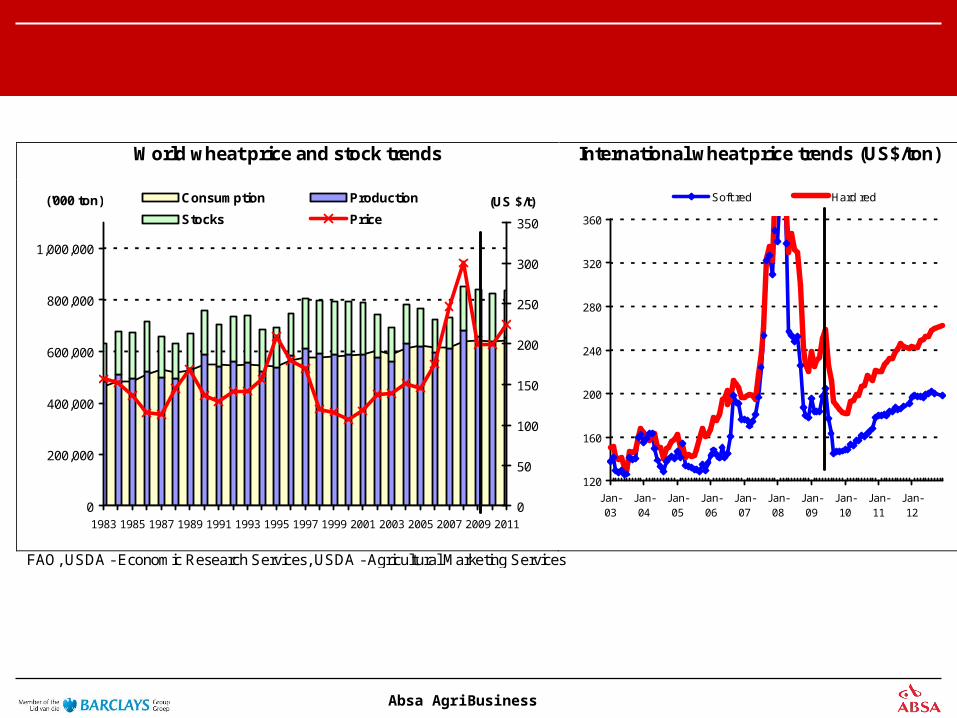

World wheat price and stock trends International wheat price trends (US$/ton)

0

200,000

400,000

600,000

800,000

1,000,000

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

0

50

100

150

200

250

300

350

Consumption Production

Stocks Price

(US $/t)('000 ton)

120

160

200

240

280

320

360

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Soft red Hard red

FAO, USDA - Economic Research Services, USDA - Agricultural Marketing Services

Absa AgriBusiness

Relationship between supply, demand and price for South Africa

SAFEX Futures Price Trends

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

200

700

1200

1700

2200

2700

3200

Consumption Production ImportsStocks Price

(R/ton)('000 ton)

1,200

1,700

2,200

2,700

3,200

3,700

4,200

4,700

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

SAFEX

Source: SAGIS, SA Weather Bureau

Absa AgriBusiness

SA Wheat prices (R/ton) Ending stocks for wheat ('000 ton)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Import parity Export parity Domestic

0

200

400

600

800

1000

1200

1990 1994 1998 2002 2006 2010

Source: CBOT, SAGIS, SAFX, BTT, Own calculations

Absa AgriBusiness

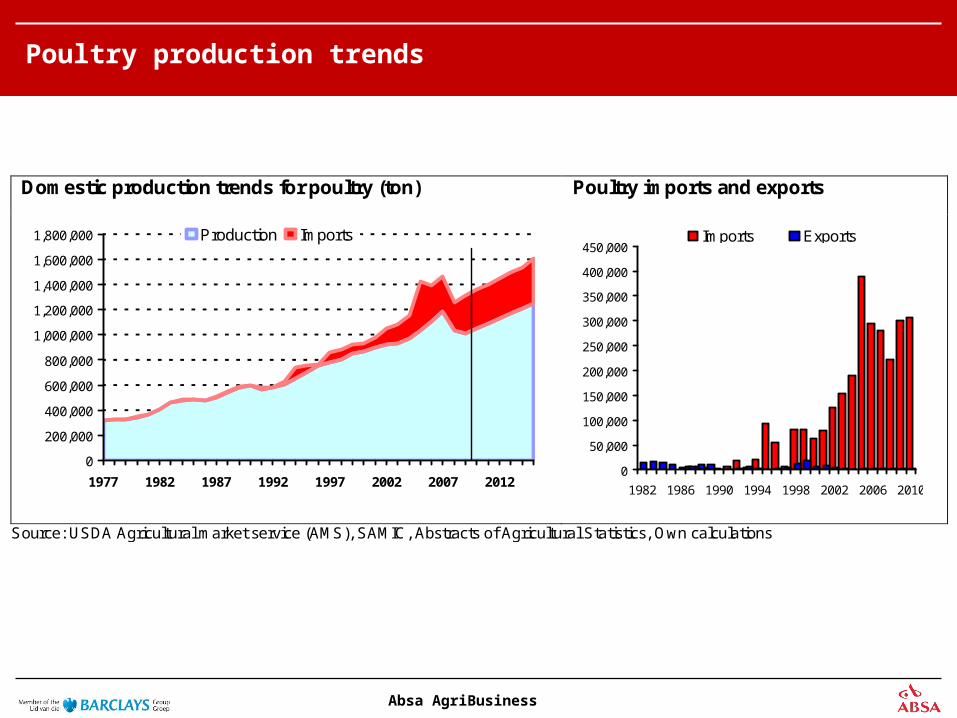

Poultry production trends

Domestic production trends for poultry (ton) Poultry imports and exports

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

1977 1982 1987 1992 1997 2002 2007 2012

Production Imports

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

1982 1986 1990 1994 1998 2002 2006 2010

Imports Exports

Source: USDA Agricultural market service (AMS), SAMIC, Abstracts of Agricultural Statistics, Own calculations

Absa AgriBusiness

Poultry Price trends

300

500

700

900

1100

1300

1500

1700

1900

2100

2300

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Frozen Fresh IQF Import

4

6

8

10

12

14

16

18

20

22

Jan-04 Jan-06 Jan-08 Jan-10

200

400

600

800

1000

1200

1400

1600

1800

Poulrty / maize ratioFrozen whole birdBreakeven Ratio

(c/kg)

Source: USDA Agricultural market service (AMS), SAMIC, Abstracts of Agricultural Statistics, SAFEX, Own calculations

Absa AgriBusiness

SA Beef prices

South African Beef Price trends and the relation between Maize and Weaner Calf Prices

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Class A Class C Contract A2/A3 NZ Cow

0.00

250.00

500.00

750.00

1,000.00

1,250.00

1,500.00

1,750.00

2,000.00

2,250.00

2,500.00

2,750.00

3,000.00

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

8

10

12

14

16

18

20

22

24

26

28

Beef / Maize Contract A2Weaner calf B/E Contract

(c/kg) (Ratio)

Source: SAMIC, Stock Owners, Noord Kaap Lewendehawe, selected feedlots, Own calculations

Absa AgriBusiness

Mutton Price trends

Domestic mutton prices (c/kg) Relation between mutton and maize prices

1000

1500

2000

2500

3000

3500

4000

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

SA Class A SA Class C Contract Class ANZ Lamb NZ Ewe

200

700

1,200

1,700

2,200

2,700

3,200

3,700

4,200

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

0

10

20

30

40

50

60

Meat / maize ratio Contract LambFeeder lamb Class A * 0.5Breakeven ratio

Price (c/kg) Price ratio

Source: SAMIC, SAFEX, and own calculations.

Absa AgriBusiness

Expected clean wool equivalent production and price trends for South African (SA c/kg)

0

20,000

40,000

60,000

80,000

100,000

120,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 20120

10

20

30

40

50

60

70Production (ton) Price (R/kg)

1,500.00

2,500.00

3,500.00

4,500.00

5,500.00

6,500.00

7,500.00

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Australian South Africa

Source: National department of Agriculture, Cape wools, Wesfarmers Landmark, AWEX, Own calculations

Absa AgriBusiness

Producer milk price trends (c/l) Milk to maize price ratio

60

110

160

210

260

310

360

410

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

Brake even Producer price

0

0.5

1

1.5

2

2.5

3

3.5

Jan-00 Jan-03 Jan-06 Jan-09

0

50

100

150

200

250

300

350

400

RatioBreakeven

Producer milk price

Ratio c/l

Sources: Milk producers Association (MPO), SAFEX and Own calculations

Absa AgriBusiness

Thank you for the opportunity to share some ideas

Contact details

E JanovskyTel (011) 350 6102

Email [email protected]

Disclaimer: Although everything has been done to ensure the accuracy of the information, the Bank takes no responsibility for actions or losses that might occur due to the usage of this information.