Embed Size (px)

Citation preview

ACCA Members: Africa Conference

PUBLICSECTORFINANCEInternationallyrecognisedPublicSectorAccounting

Standardsaretakingthemarketbystormwithmilitaryprecision-Zimbabwemilitaryinterventiontype,

by2020

ThefutureofPublicSectorFinanceinAfrica-2020Perspective

IPSASimplementationislifeordeathforAfrica

Don’tbeleftoutGo&implementnow

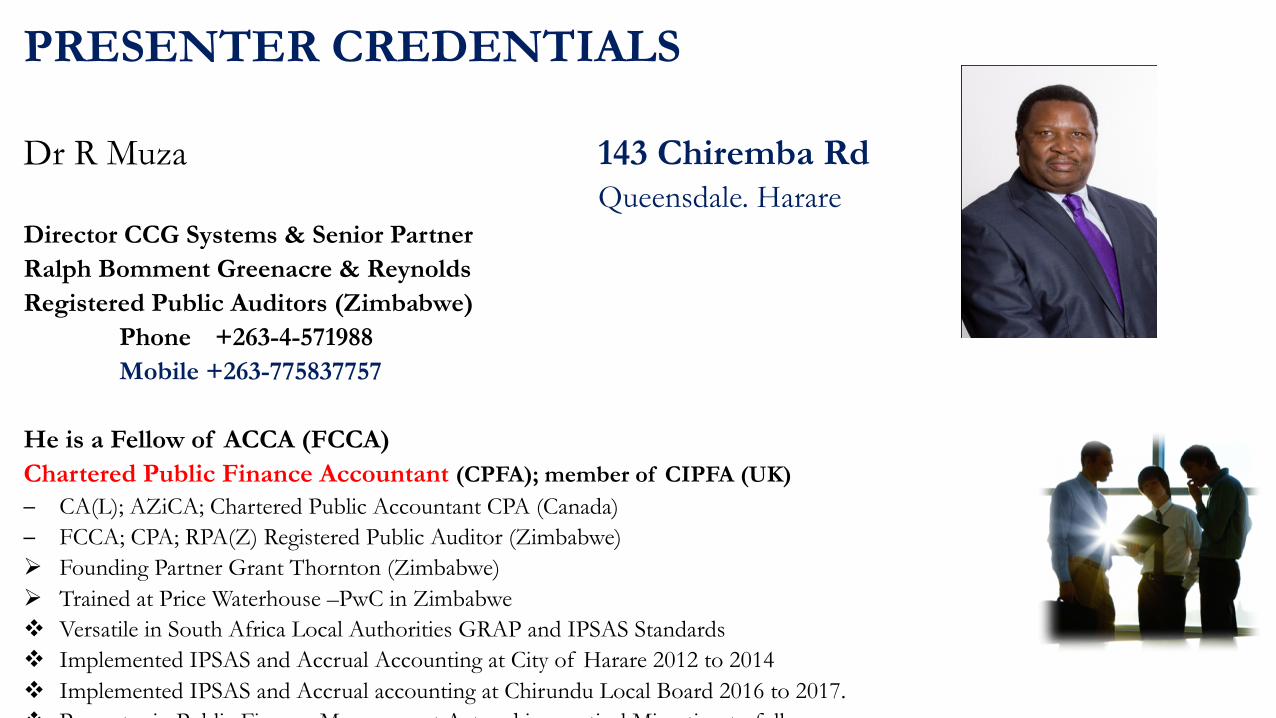

PRESENTER CREDENTIALS

Dr R Muza 143 Chiremba RdQueensdale. Harare

Director CCG Systems & Senior Partner Ralph Bomment Greenacre & ReynoldsRegistered Public Auditors (Zimbabwe)

Phone +263-4-571988 Mobile +263-775837757

He is a Fellow of ACCA (FCCA)Chartered Public Finance Accountant (CPFA); member of CIPFA (UK)– CA(L); AZiCA; Chartered Public Accountant CPA (Canada)– FCCA; CPA; RPA(Z) Registered Public Auditor (Zimbabwe)Ø Founding Partner Grant Thornton (Zimbabwe)Ø Trained at Price Waterhouse –PwC in Zimbabwev Versatile in South Africa Local Authorities GRAP and IPSAS Standardsv Implemented IPSAS and Accrual Accounting at City of Harare 2012 to 2014v Implemented IPSAS and Accrual accounting at Chirundu Local Board 2016 to 2017.v Presenter in Public Finance Management Act and in practical Migration to full

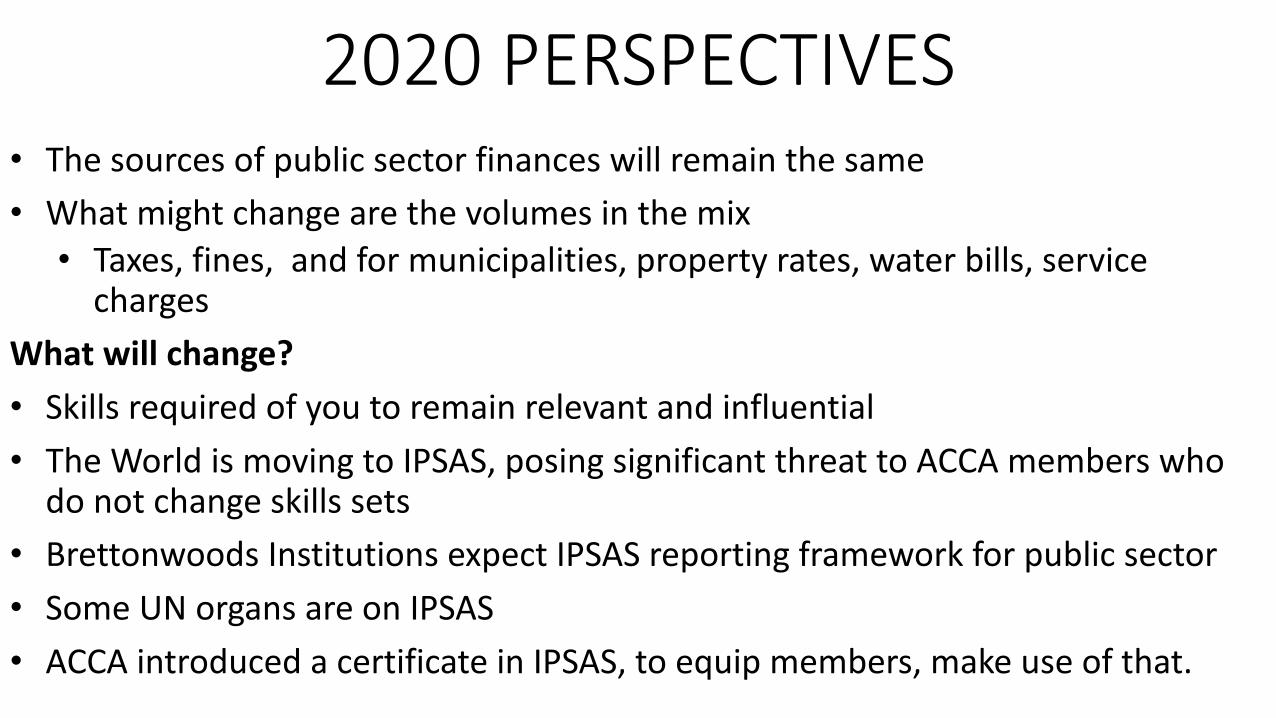

2020PERSPECTIVES• Thesourcesofpublicsectorfinanceswillremainthesame• Whatmightchangearethevolumesinthemix• Taxes,fines,andformunicipalities,propertyrates,waterbills,servicecharges

Whatwillchange?• Skillsrequiredofyoutoremainrelevantandinfluential• TheWorldismovingtoIPSAS,posingsignificantthreattoACCAmemberswhodonotchangeskillssets

• Brettonwoods InstitutionsexpectIPSASreportingframeworkforpublicsector• SomeUNorgansareonIPSAS• ACCAintroducedacertificateinIPSAS,toequipmembers,makeuseofthat.

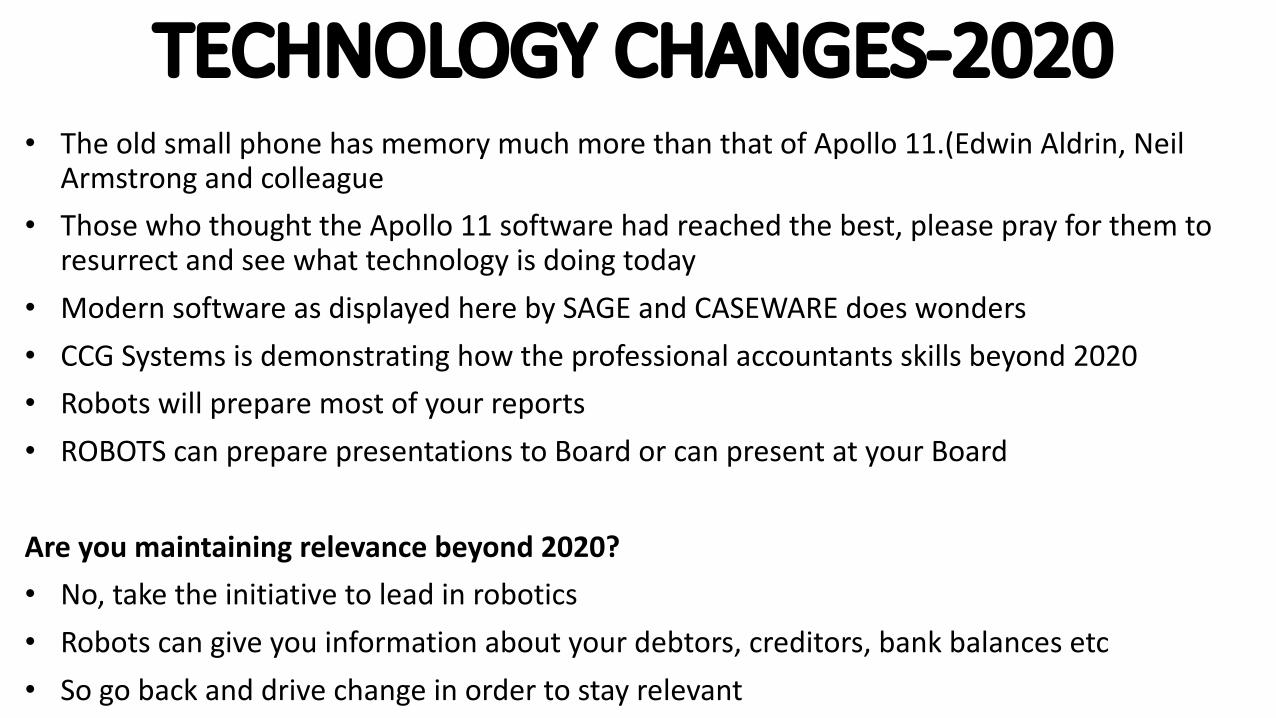

TECHNOLOGYCHANGES-2020• TheoldsmallphonehasmemorymuchmorethanthatofApollo11.(EdwinAldrin,Neil

Armstrongandcolleague• ThosewhothoughttheApollo11softwarehadreachedthebest,pleaseprayforthemto

resurrectandseewhattechnologyisdoingtoday• ModernsoftwareasdisplayedherebySAGEandCASEWAREdoeswonders• CCGSystemsisdemonstratinghowtheprofessionalaccountantsskillsbeyond2020• Robotswillpreparemostofyourreports• ROBOTScanpreparepresentationstoBoardorcanpresentatyourBoard

Areyoumaintainingrelevancebeyond2020?• No,taketheinitiativetoleadinrobotics• Robotscangiveyouinformationaboutyourdebtors,creditors,bankbalancesetc• Sogobackanddrivechangeinordertostayrelevant

LEVERAGINGONTECHNOLOGY

•AfricaGovernmentscancutdownonfavouritismlinkedwithcorruptioninpaymentcycle•NewERPselectsuppliersforyou•ERPSqueu paymentsinthepriorityfashionauthorisedbyauthorities•Reducehumaninvolvementindecisionexecution•Lettechnologyincreasetransparencyinfinancialmanagement

WHATISCOMING?

• Uniformreportsforpublicsector- IPSAS• Abusinessapproachtofinancialreportinginpublicsector• Automatedpreparationofreportsintheformatuserswantthem• Automaticdispatchofreportstomanagementwithouthumaninvolvement• Automatedpreparationoffinancialstatementseg CasewareFinancials• CorruptioninpaymentofcreditorscanbereducedthroughuseofERP• Rapidfinancialreporting,financialinformationuptodateatalltimes• Focusonanalysisofreportsasopposedtopreparationoffinancialstatements

• Exampleofsoftwaredoingthis,SAGEEVOLUTION,justacrossfromourboothdownstairs

OBJECTIVEOFIPSASWHOINAFRICAISNOTTALKINGTRANSPARENCYTODAY?

• Toprescribethemannerinwhichgeneralpurposefinancialstatementsshouldbepresentedtoensurecomparabilitybothwiththeentity’sfinancialstatementsofpreviousperiodsandwiththefinancialstatementsofotherentities.• Setsoutoverallconsiderationsforthepresentationoffinancialstatements,guidancefortheirstructure,andminimumrequirementsforthecontentoffinancialstatementspreparedundertheaccrualbasisofaccounting.

SCOPE•AppliedtoallgeneralpurposefinancialstatementspreparedandpresentedundertheaccrualbasisofaccountinginaccordancewithIPSASs.•Doesnotapplytocondensedinterimfinancialinformation•AppliestoallpublicsectorentitiesotherthanGovernmentBusinessEnterprises(GBEs)/SOES.

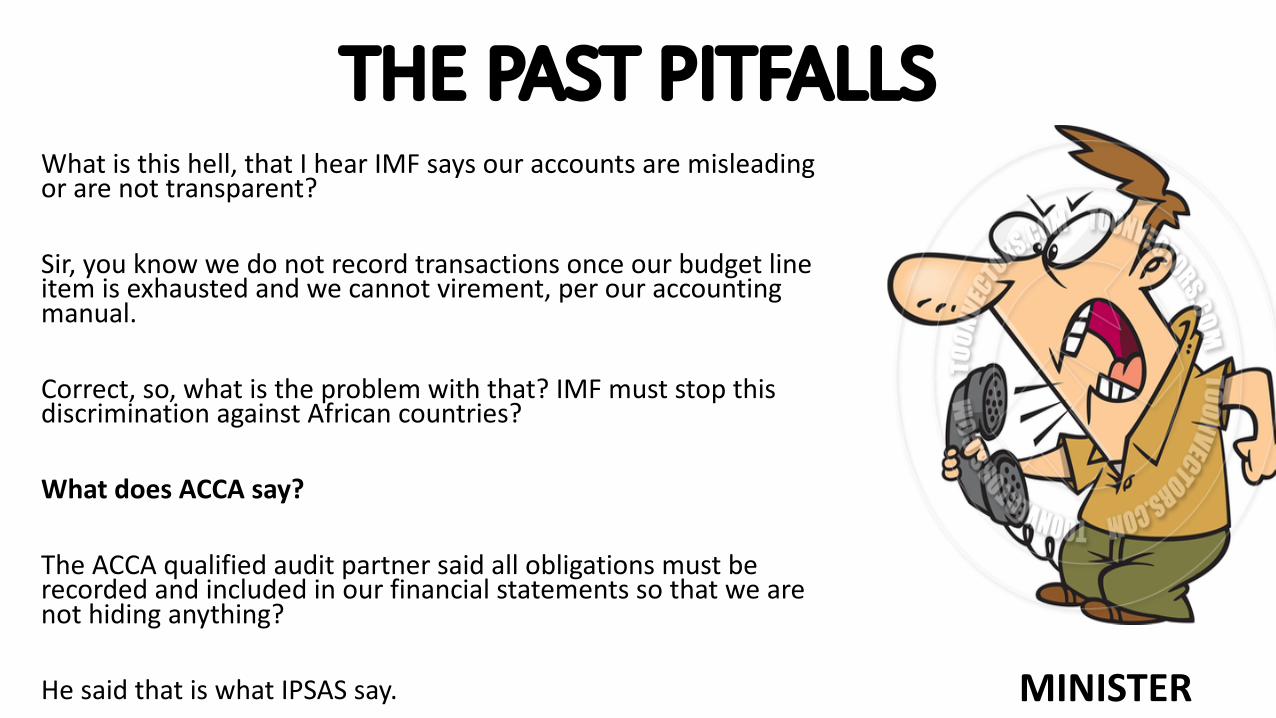

THEPASTPITFALLSWhatisthishell,thatIhearIMFsaysouraccountsaremisleadingorarenottransparent?

Sir,youknowwedonotrecordtransactionsonceourbudgetlineitemisexhaustedandwecannotvirement,perouraccountingmanual.

Correct,so,whatistheproblemwiththat?IMFmuststopthisdiscriminationagainstAfricancountries?

WhatdoesACCAsay?

TheACCAqualifiedauditpartnersaidallobligationsmustberecordedandincludedinourfinancialstatementssothatwearenothidinganything?

HesaidthatiswhatIPSASsay. MINISTER

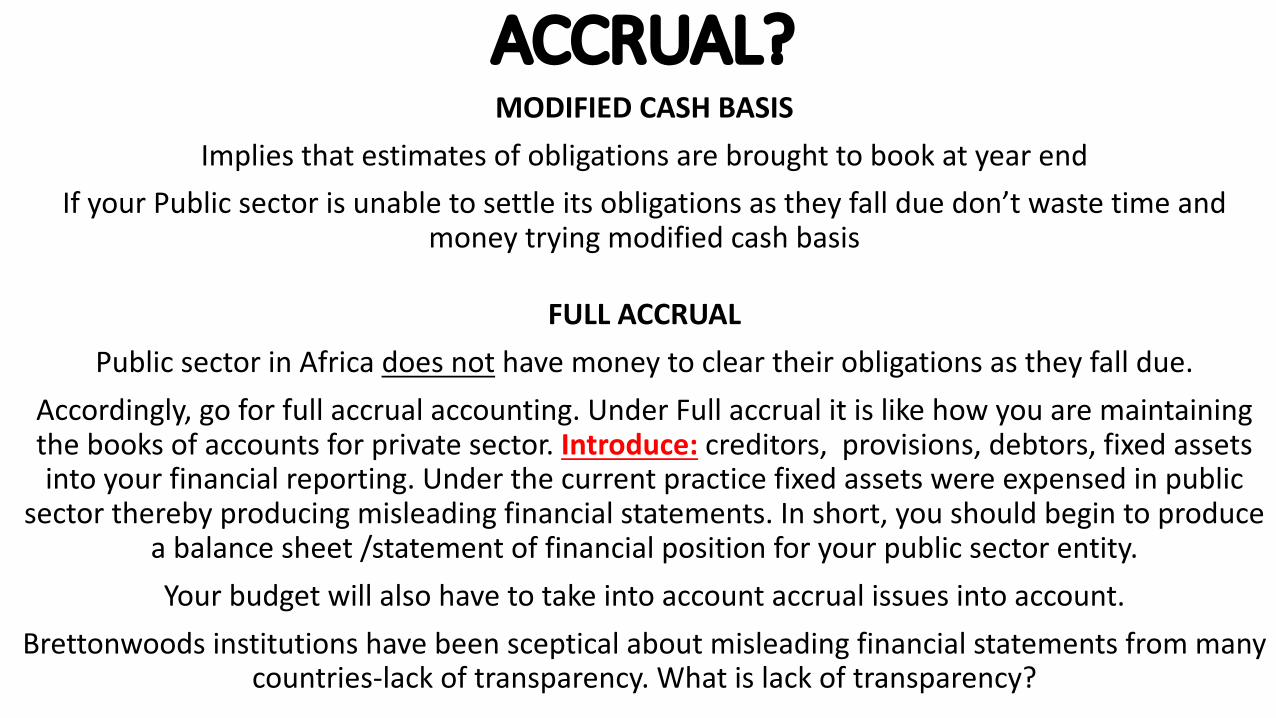

MODIFIEDCASHBASISORFULLACCRUAL?MODIFIEDCASHBASIS

ImpliesthatestimatesofobligationsarebroughttobookatyearendIfyourPublicsectorisunabletosettleitsobligationsastheyfallduedon’twastetimeand

moneytryingmodifiedcashbasis

FULLACCRUALPublicsectorinAfricadoesnot havemoneytocleartheirobligationsastheyfalldue.

Accordingly,goforfullaccrualaccounting.UnderFullaccrualitislikehowyouaremaintainingthebooksofaccountsforprivatesector.Introduce: creditors,provisions,debtors,fixedassetsintoyourfinancialreporting.Underthecurrentpracticefixedassetswereexpensedinpublic

sectortherebyproducingmisleadingfinancialstatements.Inshort,youshouldbegintoproduceabalancesheet/statementoffinancialpositionforyourpublicsectorentity.Yourbudgetwillalsohavetotakeintoaccountaccrualissuesintoaccount.

Brettonwoods institutionshavebeenscepticalaboutmisleadingfinancialstatementsfrommanycountries-lackoftransparency.Whatislackoftransparency?

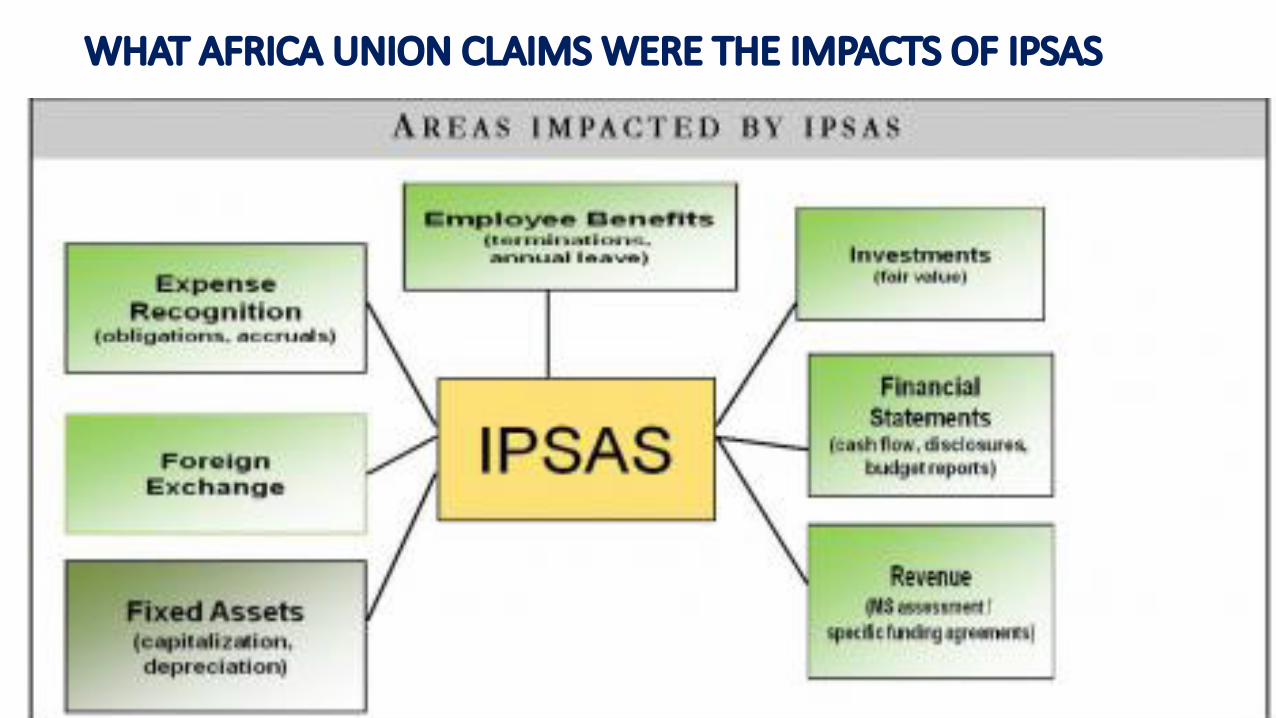

WHATAFRICAUNIONCLAIMSWERETHEIMPACTSOFIPSAS

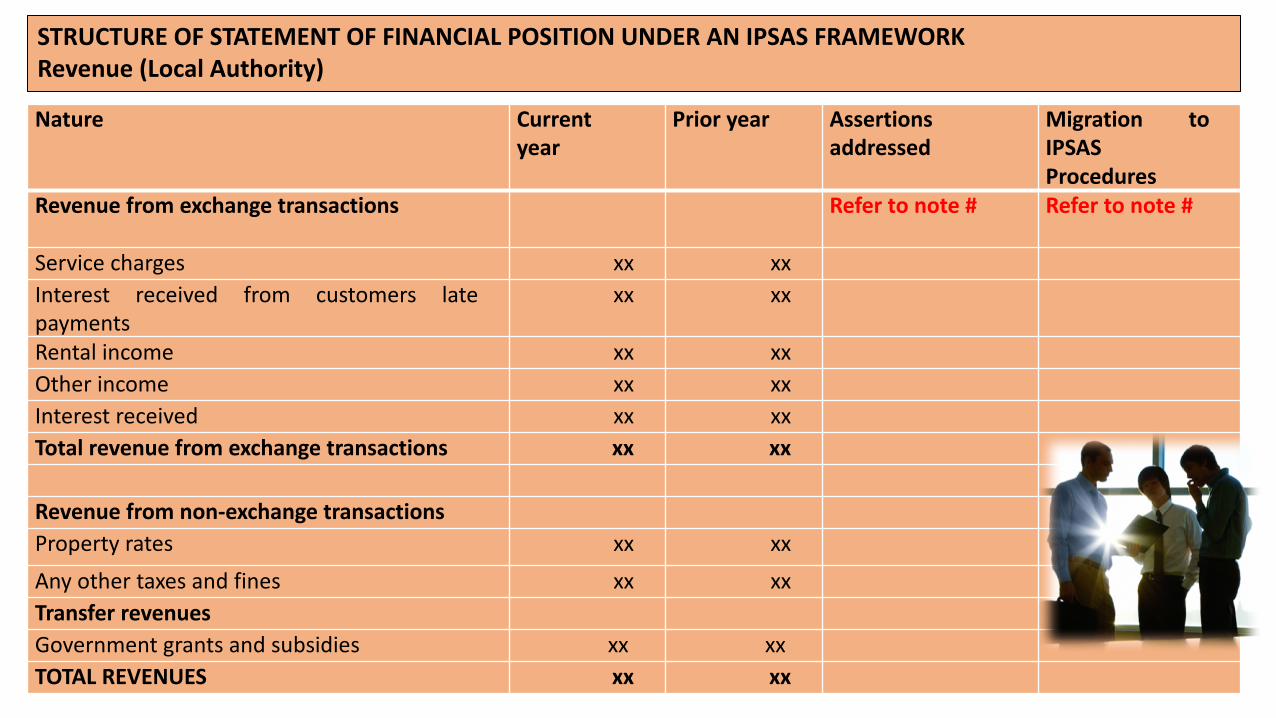

Nature Currentyear

Prior year Assertionsaddressed

Migration toIPSASProcedures

Revenue from exchange transactions Refer to note # Refer to note #

Service charges xx xxInterest received from customers latepayments

xx xx

Rental income xx xxOther income xx xxInterest received xx xxTotal revenue from exchange transactions xx xx

Revenue from non-exchange transactionsProperty rates xx xxAny other taxes and fines xx xxTransfer revenuesGovernment grants and subsidies xx xxTOTAL REVENUES xx xx

STRUCTUREOFSTATEMENTOFFINANCIALPOSITIONUNDERANIPSASFRAMEWORKRevenue(LocalAuthority)

Nature Current year Prior year Assertions addressed Migration to IPSASProcedures

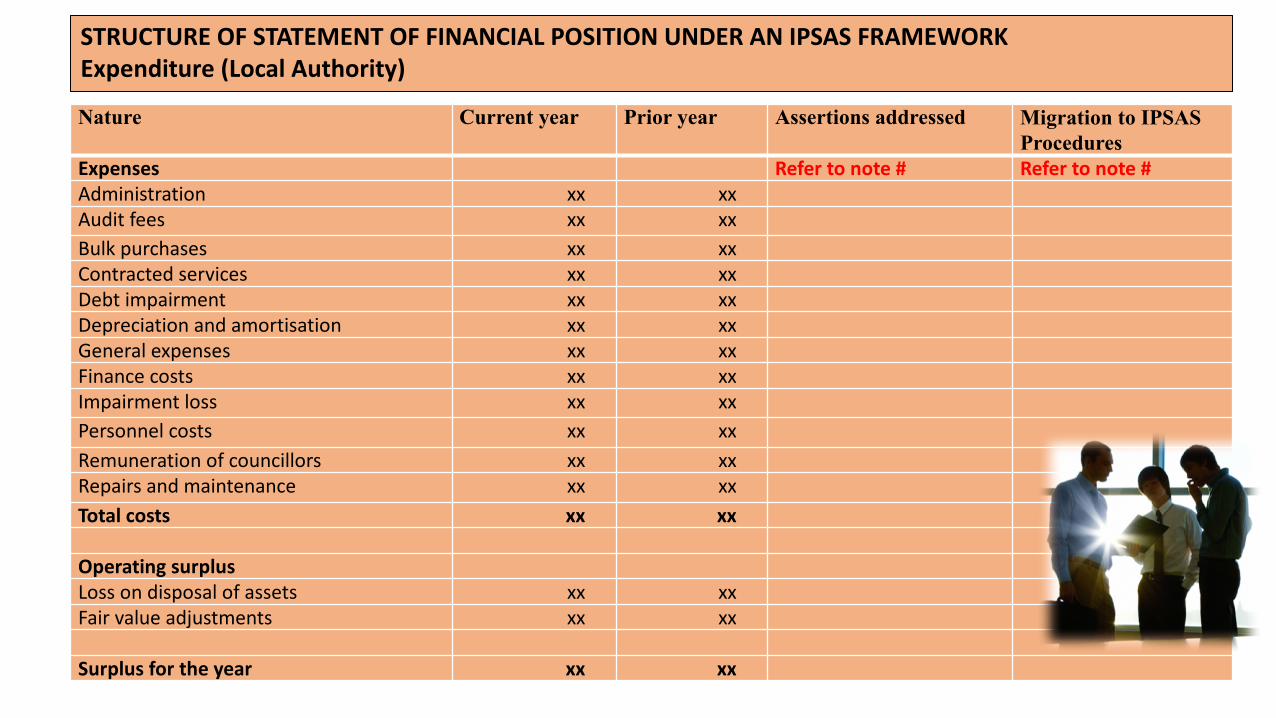

Expenses Refer to note # Refer to note #Administration xx xxAudit fees xx xxBulk purchases xx xxContracted services xx xxDebt impairment xx xxDepreciation and amortisation xx xxGeneral expenses xx xxFinance costs xx xxImpairment loss xx xxPersonnel costs xx xxRemuneration of councillors xx xxRepairs and maintenance xx xxTotal costs xx xx

Operating surplusLoss on disposal of assets xx xxFair value adjustments xx xx

Surplus for the year xx xx

STRUCTUREOFSTATEMENTOFFINANCIALPOSITIONUNDERANIPSASFRAMEWORKExpenditure(LocalAuthority)

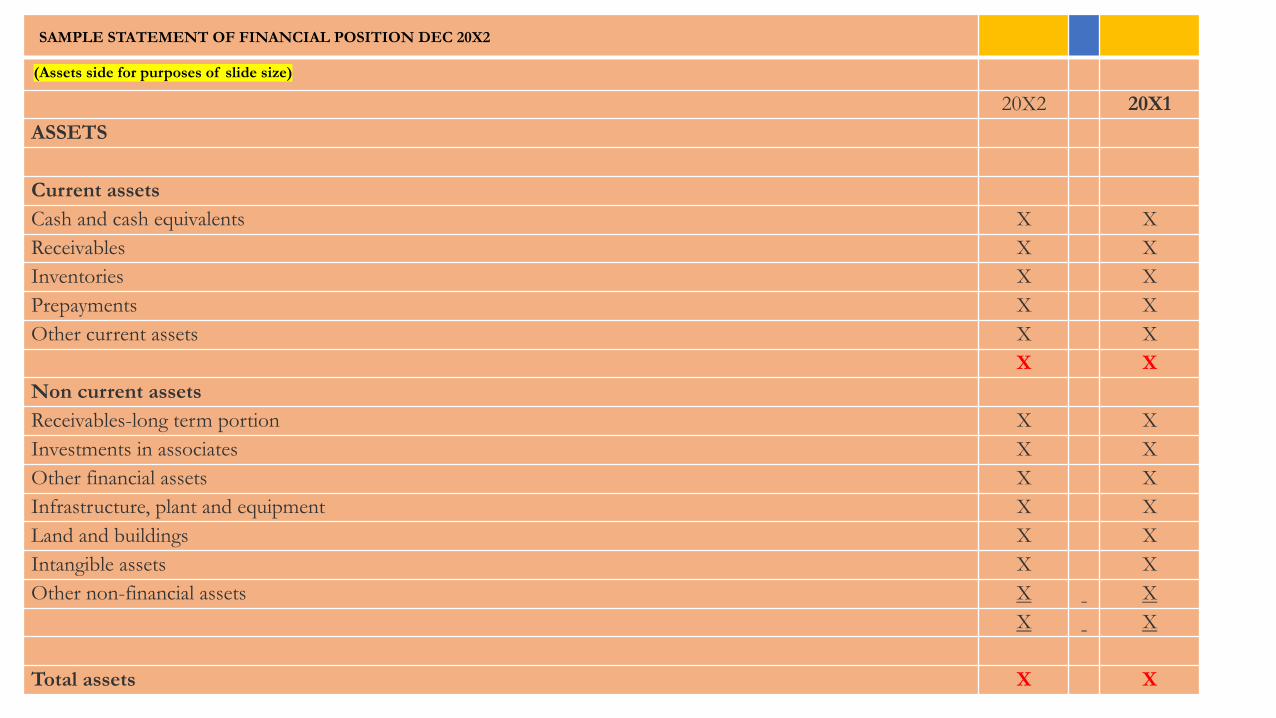

SAMPLE STATEMENT OF FINANCIAL POSITION DEC 20X2

(Assets side for purposes of slide size)

20X2 20X1ASSETS

Current assetsCash and cash equivalents X XReceivables X XInventories X XPrepayments X XOther current assets X X

X XNon current assetsReceivables-long term portion X XInvestments in associates X XOther financial assets X XInfrastructure, plant and equipment X XLand and buildings X XIntangible assets X XOther non-financial assets X X

X X

Total assets X X

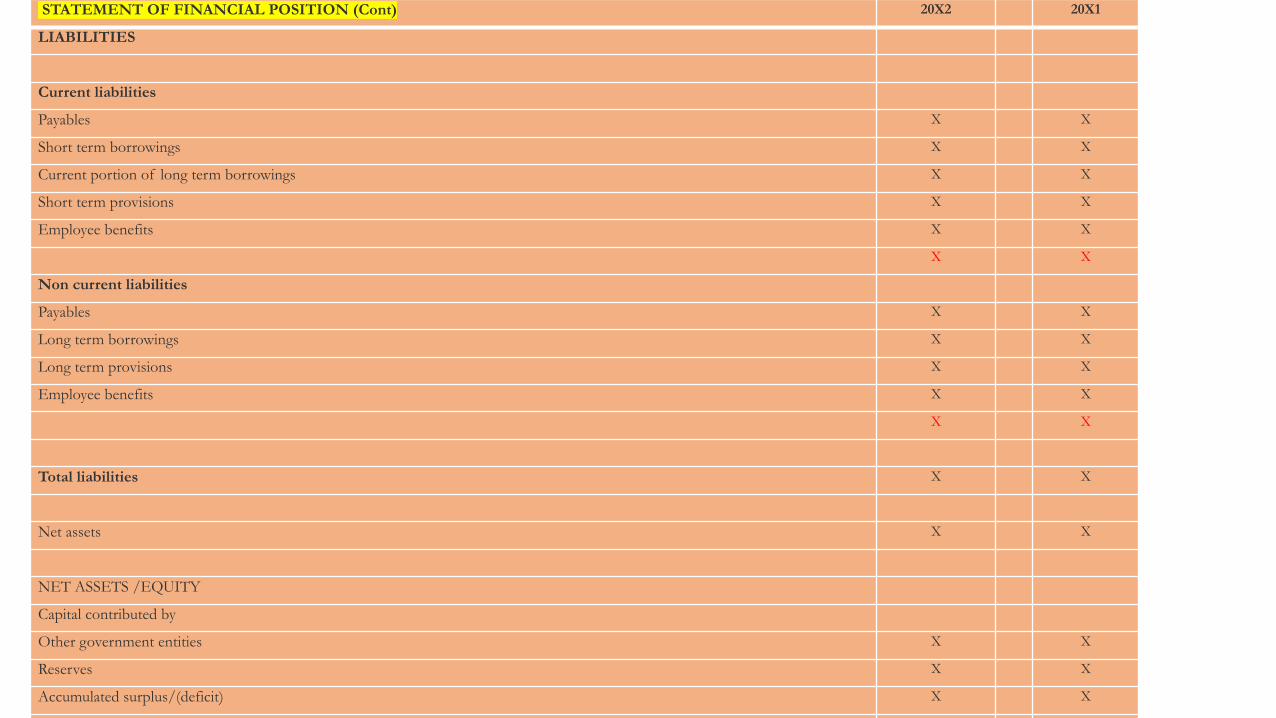

STATEMENT OF FINANCIAL POSITION (Cont) 20X2 20X1

LIABILITIES

Current liabilities

Payables X X

Short term borrowings X X

Current portion of long term borrowings X X

Short term provisions X X

Employee benefits X X

X X

Non current liabilities

Payables X X

Long term borrowings X X

Long term provisions X X

Employee benefits X X

X X

Total liabilities X X

Net assets X X

NET ASSETS /EQUITY

Capital contributed by

Other government entities X X

Reserves X X

Accumulated surplus/(deficit) X X

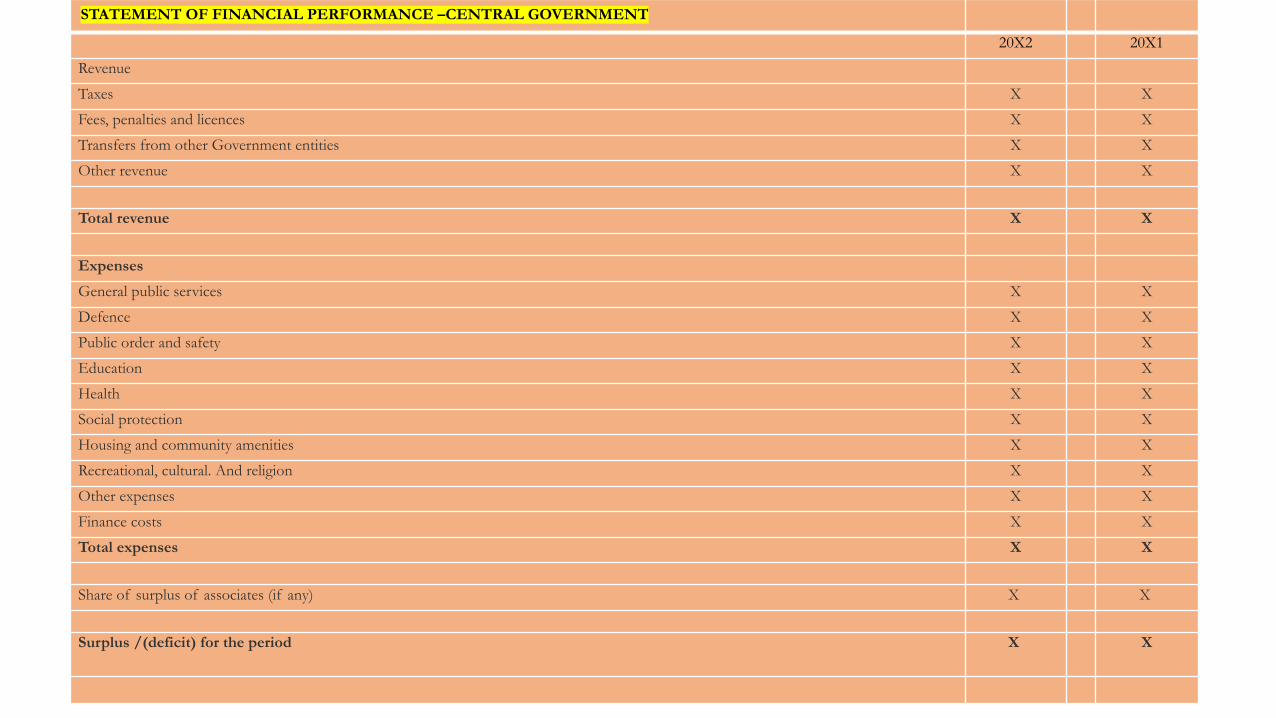

STATEMENT OF FINANCIAL PERFORMANCE –CENTRAL GOVERNMENT

20X2 20X1

Revenue

Taxes X X

Fees, penalties and licences X X

Transfers from other Government entities X X

Other revenue X X

Total revenue X X

ExpensesGeneral public services X X

Defence X X

Public order and safety X X

Education X X

Health X X

Social protection X X

Housing and community amenities X X

Recreational, cultural. And religion X X

Other expenses X X

Finance costs X X

Total expenses X X

Share of surplus of associates (if any) X X

Surplus /(deficit) for the period X X

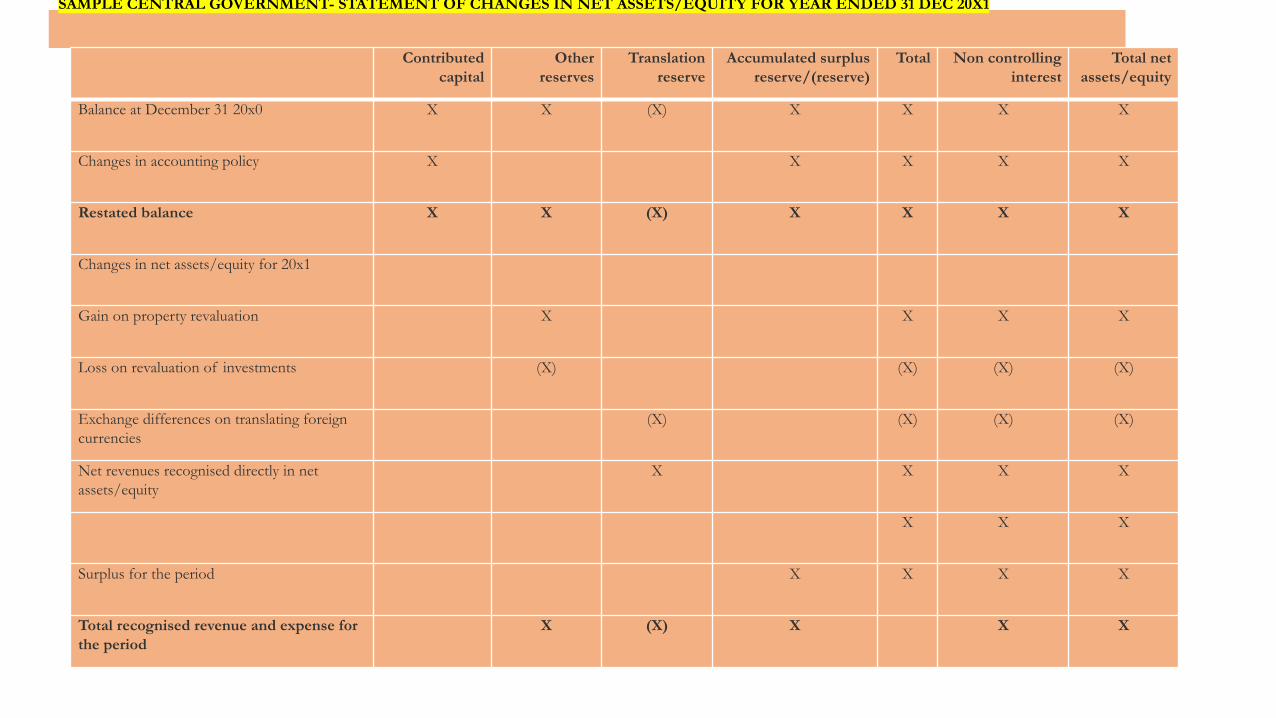

SAMPLE CENTRAL GOVERNMENT- STATEMENT OF CHANGES IN NET ASSETS/EQUITY FOR YEAR ENDED 31 DEC 20X1

Contributed capital

Other reserves

Translation reserve

Accumulated surplus reserve/(reserve)

Total Non controlling interest

Total net assets/equity

Balance at December 31 20x0 X X (X) X X X X

Changes in accounting policy X X X X X

Restated balance X X (X) X X X X

Changes in net assets/equity for 20x1

Gain on property revaluation X X X X

Loss on revaluation of investments (X) (X) (X) (X)

Exchange differences on translating foreign currencies

(X) (X) (X) (X)

Net revenues recognised directly in net assets/equity

X X X X

X X X

Surplus for the period X X X X

Total recognised revenue and expense for the period

X (X) X X X

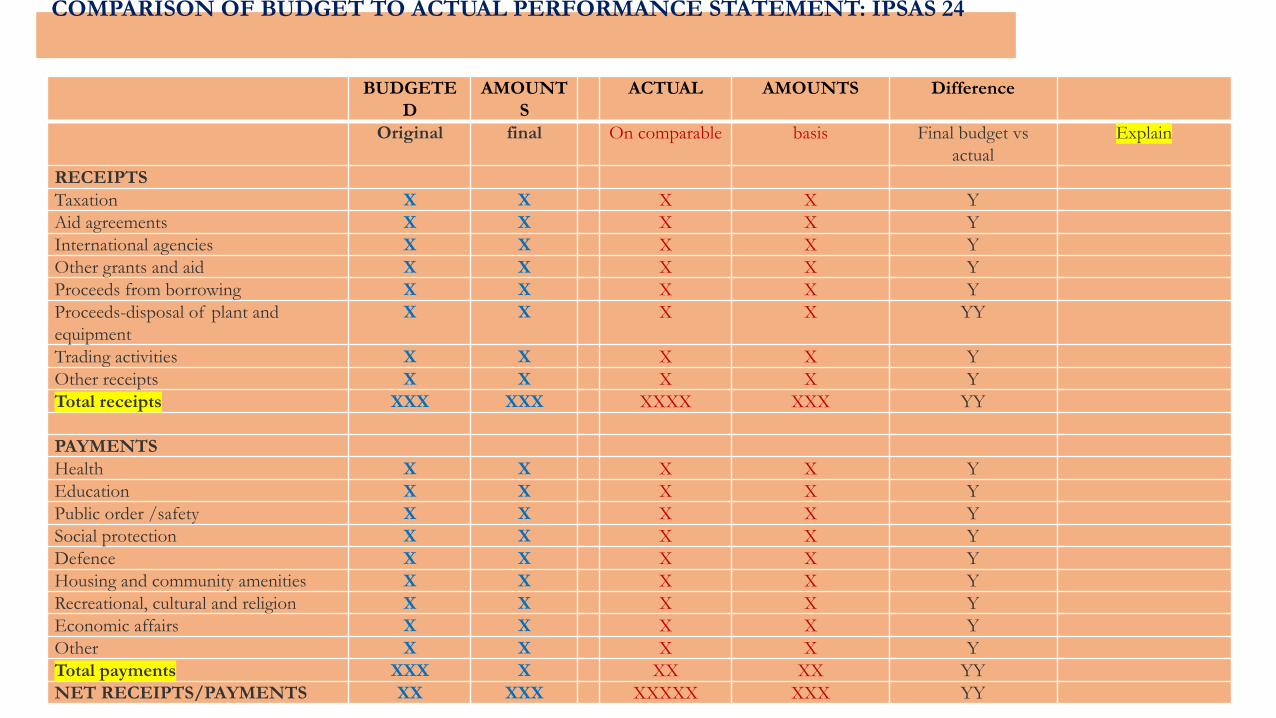

COMPARISON OF BUDGET TO ACTUAL PERFORMANCE STATEMENT: IPSAS 24

BUDGETED

AMOUNTS

ACTUAL AMOUNTS Difference

Original final On comparable basis Final budget vsactual

Explain

RECEIPTSTaxation X X X X YAid agreements X X X X YInternational agencies X X X X YOther grants and aid X X X X YProceeds from borrowing X X X X YProceeds-disposal of plant and equipment

X X X X YY

Trading activities X X X X YOther receipts X X X X YTotal receipts XXX XXX XXXX XXX YY

PAYMENTSHealth X X X X YEducation X X X X YPublic order /safety X X X X YSocial protection X X X X YDefence X X X X YHousing and community amenities X X X X YRecreational, cultural and religion X X X X YEconomic affairs X X X X YOther X X X X YTotal payments XXX X XX XX YYNET RECEIPTS/PAYMENTS XX XXX XXXXX XXX YY

STATEMENTOFFINANCIALPERFOMANCE

CLASSIFICATIONOFEXPENSES(NATURE/FUNCTION)

IFYOUCLASSIFYBYFUNCTION,THEREMAYBEADDITIONALINFORMATIONTHATMAYBE

DISCLOSEDABOUTTHENATUREOFEXPENSESINCLUDING

DEPRECIATION,ARMOTISATION,EMPLOYEEBENEFITSANDFINANCE

COSTS.

PUBLICSECTORFINANCEMANAGEMENT/IPSASIMPLEMENTATIONOURREF.SITES:SOUTHAFRICA

SOUTHAFRICASITES

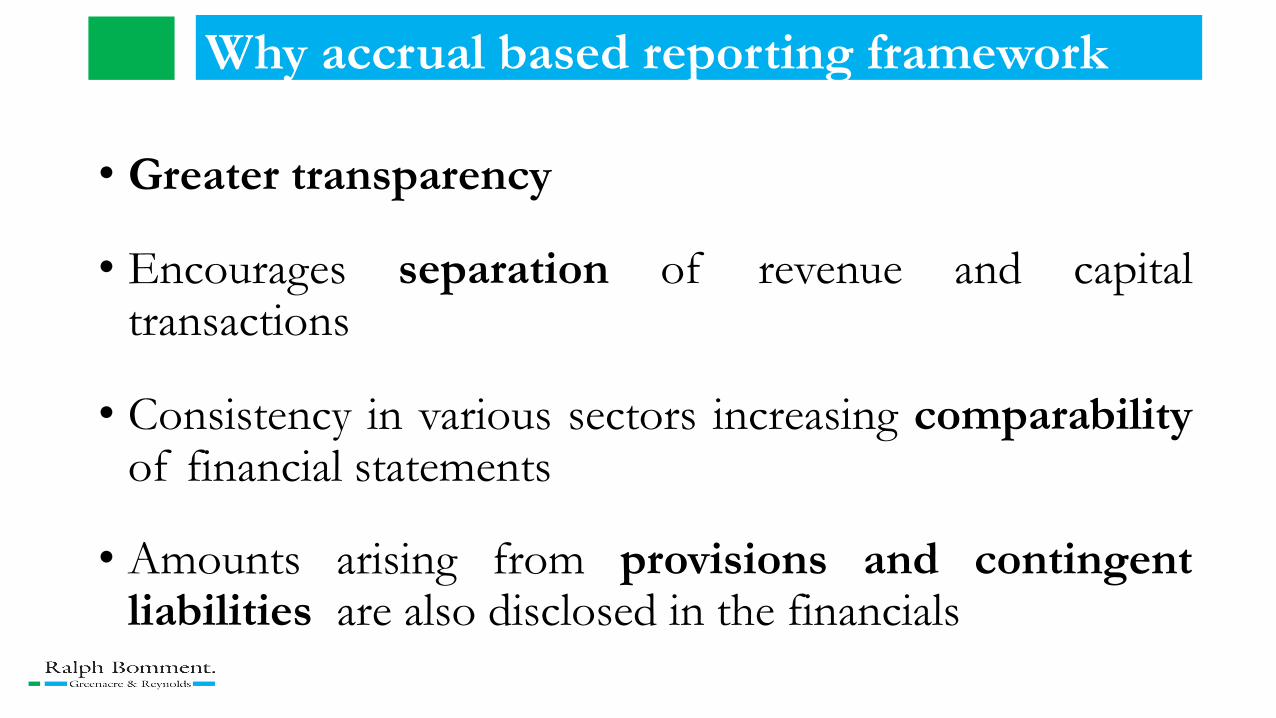

• Greater transparency

• Encourages separation of revenue and capitaltransactions

• Consistency in various sectors increasing comparabilityof financial statements

• Amounts arising from provisions and contingentliabilities are also disclosed in the financials

Why accrual based reporting framework migration process by 2020?

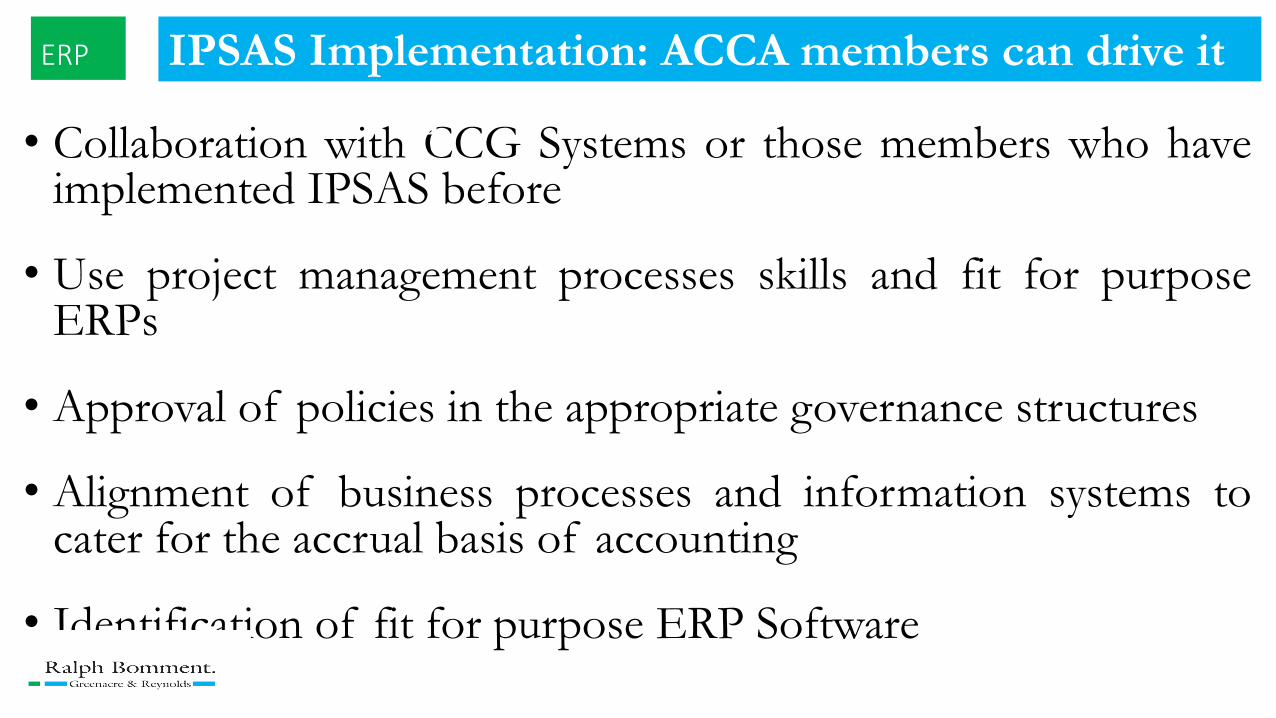

• Collaboration with CCG Systems or those members who haveimplemented IPSAS before

• Use project management processes skills and fit for purposeERPs

• Approval of policies in the appropriate governance structures

• Alignment of business processes and information systems tocater for the accrual basis of accounting

• Identification of fit for purpose ERP Software

ERP IPSAS Implementation: ACCA members can drive it driverive the process

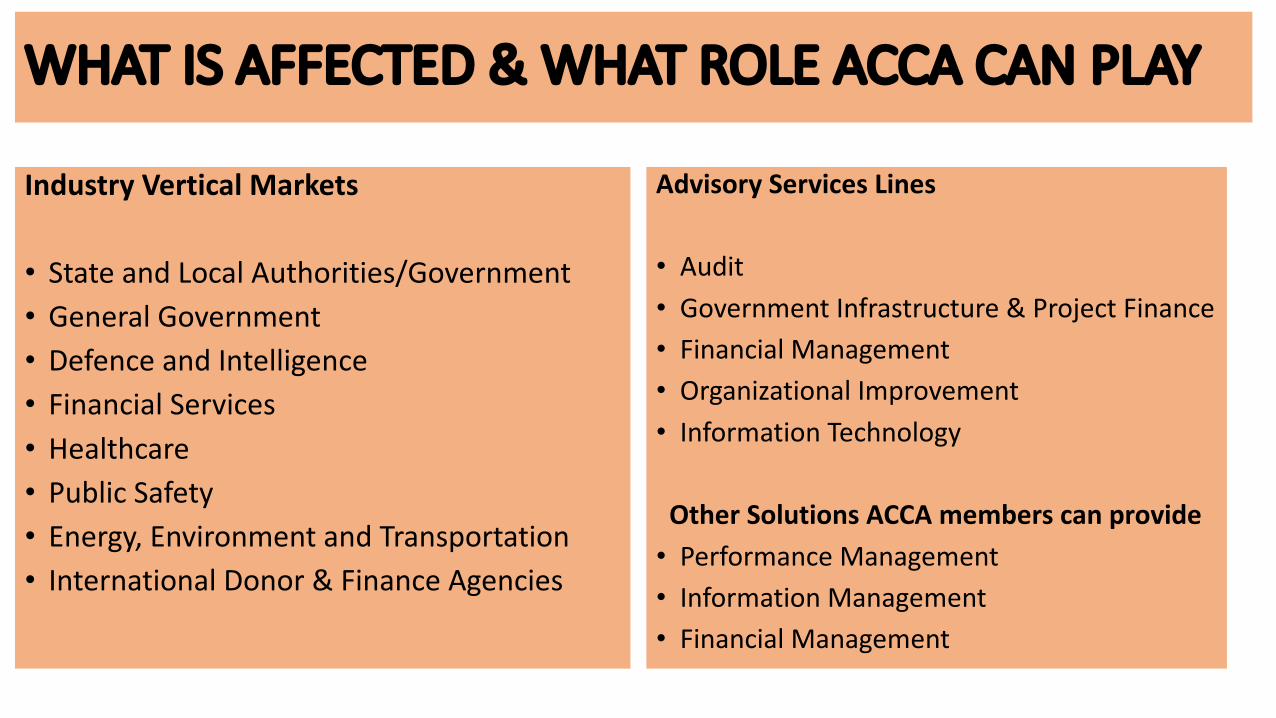

WHATISAFFECTED&WHATROLEACCACANPLAY

IndustryVerticalMarkets

• StateandLocalAuthorities/Government• GeneralGovernment• Defence andIntelligence• FinancialServices• Healthcare• PublicSafety• Energy,EnvironmentandTransportation• InternationalDonor&FinanceAgencies

AdvisoryServicesLines

• Audit• GovernmentInfrastructure&ProjectFinance• FinancialManagement• OrganizationalImprovement• InformationTechnology

OtherSolutionsACCAmemberscanprovide• PerformanceManagement• InformationManagement• FinancialManagement

DISCUSSION

Amasegnalehu !!Thankyouverymuchall!!Tatendazvikuru mose !!

Siabonga khakhulu mahlabezulu !!Asantesana !!Goededankie !!

Zikomo kwambiri nonseinu !!Obregado