Embed Size (px)

Citation preview

Operating with a Restricted Balance Sheet 3

Top Ten Challenges for Investment Banks 2012

Operating with a Restricted Balance Sheet

3

Olorest, optaspellam, con evenit etur? Qui ut liquam, sitaestiore ventus rehentotatia nonsecto dolore utem fugia qui nonsequi omnia illeni

3“ I do have a concern that some regulators seem to believe that ever more capital is the solution to every regulatory problem. Carried too far, this thinking would have profoundly negative consequences. And not just for the banks”.

Marcus Agius, Barclays Group Chairman1

Challenge 3: Operating with a Restricted Balance Sheet

2

New regulation is raising the cost of doing business for investment banks and restricting opportunities for revenue growth. Profitability across a number of business areas is being reduced due to higher funding costs, balance sheet constraints and the need to execute in open venues with higher transaction costs. Banks must find ways to mitigate the costs of regulatory developments, as well as identify areas of revenue growth to restore their profitability.

Challenge 3: Operating with a Restricted Balance Sheet

Challenge 3: Operating with a Restricted Balance Sheet

3

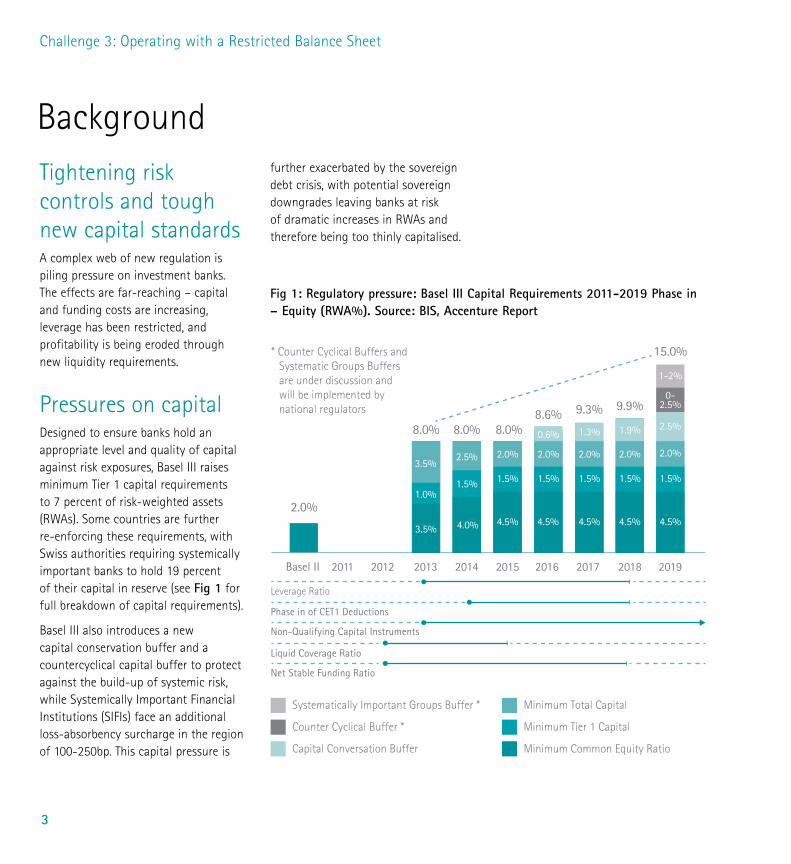

Tightening risk controls and tough new capital standardsA complex web of new regulation is piling pressure on investment banks. The effects are far-reaching – capital and funding costs are increasing, leverage has been restricted, and profitability is being eroded through new liquidity requirements.

Pressures on capitalDesigned to ensure banks hold an appropriate level and quality of capital against risk exposures, Basel III raises minimum Tier 1 capital requirements to 7 percent of risk-weighted assets (RWAs). Some countries are further re-enforcing these requirements, with Swiss authorities requiring systemically important banks to hold 19 percent of their capital in reserve (see Fig 1 for full breakdown of capital requirements).

Basel III also introduces a new capital conservation buffer and a countercyclical capital buffer to protect against the build-up of systemic risk, while Systemically Important Financial Institutions (SIFIs) face an additional loss-absorbency surcharge in the region of 100-250bp. This capital pressure is

Backgroundfurther exacerbated by the sovereign debt crisis, with potential sovereign downgrades leaving banks at risk of dramatic increases in RWAs and therefore being too thinly capitalised.

8%

Basel II

Leverage Ratio

Phase in of CET1 Deductions

Non-Qualifying Capital Instruments

Liquid Coverage Ratio

Net Stable Funding Ratio

2011 2012 2013 2014 2015 2016 2017 2018 2019

2.0%

8.0% 8.0% 8.0%8.6% 9.3% 9.9%

15.0%

1-2%

0-2.5%

2.5%1.9%1.3%0.6%

2.0%2.0%2.0%2.0%2.0%2.5%

1.5%1.5%1.5%1.5%1.5%1.5%1.0%

3.5%

4.5%4.5%4.5%4.5%4.5%4.0%3.5%

Systematically Important Groups Buffer *

Counter Cyclical Buffer *

Capital Conversation Buffer

Minimum Total Capital

Minimum Tier 1 Capital

Minimum Common Equity Ratio

* Counter Cyclical Buffers and Systematic Groups Buffers are under discussion and will be implemented by national regulators

Fig 1: Regulatory pressure: Basel III Capital Requirements 2011-2019 Phase in – Equity (RWA%). Source: BIS, Accenture Report

Pressures on liquidity and fundingBasel III seeks to protect banks against short-term shocks through the introduction of a Liquidity Coverage Ratio (LCR). The LCR requires banks to hold high-quality liquid assets (in essence government bonds) that can be readily sold to offset likely outflows of cash during times of crisis. This will profoundly impact banks’ profitability as they are forced to invest in lower yielding assets. At the same time, Basel III’s Net Stable Funding Ratio will force banks to increase their level of longer-term, more expensive funding in requiring banks to reduce their maturity mismatch.

One of the results of increased funding costs will be a reduction in the level of balance sheet debt banks hold. Investment banks made extensive use of leverage over the last decade to boost their revenues, particularly in their fixed income trading business which grew to contribute around 25 percent of investment banking revenues before the credit crunch (see Fig 2). With less debt available to boost these revenues, banks will need to focus on the operational viability of any fixed income product.

"With less debt available to boost these revenues, banks will need to focus on the operational viability of any fixed income product".

4

8%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

14%16%

17%

22% 22%

25%

21%

24%

27% 27%

0%

2009 2010

31%

5%

Traded Fixed Income

Challenge 3: Operating with a Restricted Balance Sheet

Fig 2: Contribution to investment banking revenues. Source: Company Reports, Accenture Research

As well as the Markets in Financial Instruments Directive (MiFID) and the Dodd-Frank Act driving trading in eligible derivatives from Over-The-Counter (OTC) Derivatives to Central Counterparty (CCP) clearing, the Volcker Rule restricts deposit-taking institutions’ proprietary trading activities and their sponsorship of hedge and private equity funds.

Challenge 3: Operating with a Restricted Balance Sheet

5

Pressures on leverageRegulators are currently planning to introduce a Tier I leverage ratio of 3 percent as part of the Basel III proposals. This will limit banks’ total assets to 33 times their capital – a significant cap on bank risk and criticised in some quarters as excessive in failing to consider risk weightings. Although some countries already operate leverage ratios, in others such as the UK there is debate over whether the leverage ratio should be higher for SIFIs.

Impacts on business modelsAnd there are other developments that are forcing changes to banks’ business models. For example, UK proposals to ring-fence the retail business of universal banks could require significant changes to the way some banks structure their operations. Further limits on the scope of banks’ activities are also being introduced.

Challenge 3: Operating with a Restricted Balance Sheet

7

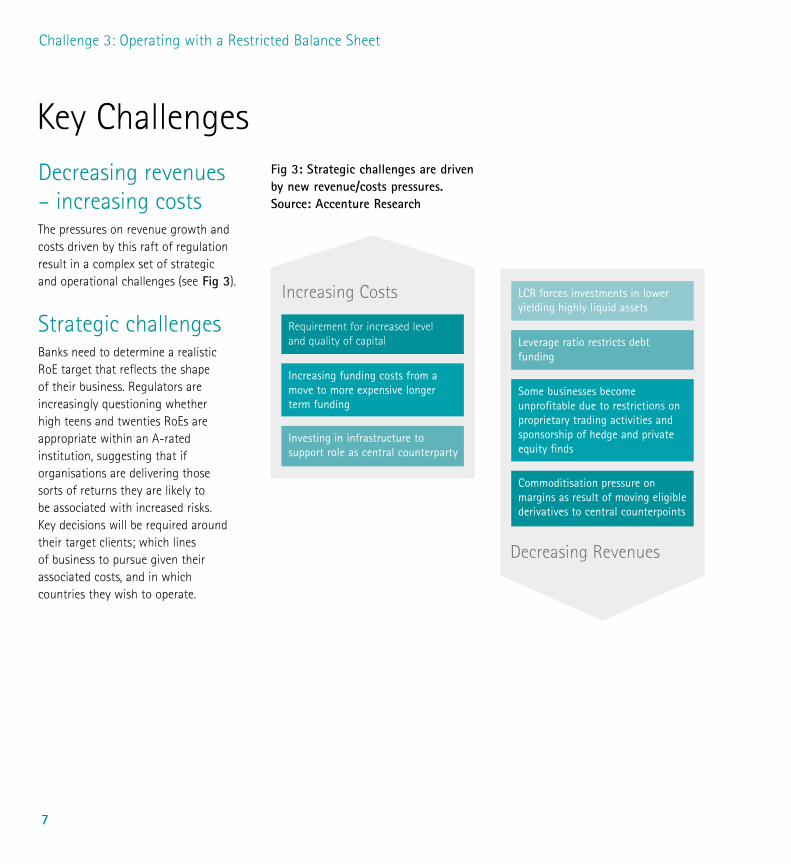

Key ChallengesDecreasing revenues – increasing costsThe pressures on revenue growth and costs driven by this raft of regulation result in a complex set of strategic and operational challenges (see Fig 3).

Strategic challengesBanks need to determine a realistic RoE target that reflects the shape of their business. Regulators are increasingly questioning whether high teens and twenties RoEs are appropriate within an A-rated institution, suggesting that if organisations are delivering those sorts of returns they are likely to be associated with increased risks. Key decisions will be required around their target clients; which lines of business to pursue given their associated costs, and in which countries they wish to operate.

Increasing Costs

Requirement for increased level and quality of capital

Increasing funding costs from a move to more expensive longer term funding

Investing in infrastructure to support role as central counterparty

Decreasing Revenues

LCR forces investments in lower yielding highly liquid assets

Leverage ratio restricts debt funding

Some businesses become unprofitable due to restrictions on proprietary trading activities and sponsorship of hedge and private equity finds

Commoditisation pressure on margins as result of moving eligible derivatives to central counterpoints

Fig 3: Strategic challenges are driven by new revenue/costs pressures. Source: Accenture Research

Challenge 3: Operating with a Restricted Balance Sheet

9

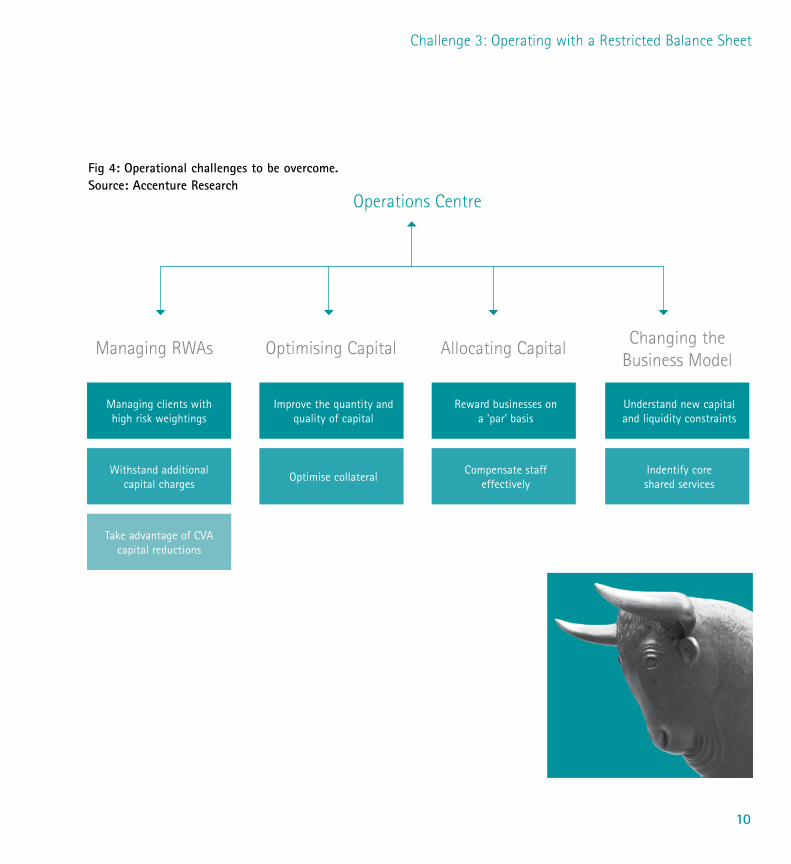

Operational challengesChallenges at the operational level centre around four key themes (as outlined in Fig. 4):

1. Managing RWAs Banks need to address how they manage business with clients that attract a higher risk-weighting; how to withstand additional capital charges from elements like the Credit Valuation Adjustment charge (CVA); and how they take advantage of capital reductions from Expected Positive Exposures (EPEs).

2. Optimising CapitalAlthough the timetable for meeting Basel III requirements extends to 2019, markets are looking favourably on those planning to meet the new requirements earlier. Banks are therefore incentivised to look at their options for improving the quality and quantity of their capital, and optimising collateral to reduce the impact of regulatory pressures on profitability.

3. Allocating Capital Internal allocation of capital needs to align with a principle of rewarding businesses on a ‘par’ basis, considering new measures for risk-adjusted RoE. Alongside this is the challenge of how to address one of the most criticised aspects of the financial crisis: appropriate compensation of staff. Regulatory limits on bonuses have encouraged higher base salaries, which has ultimately reduced flexibility in the cost base and therefore presented another challenge in addressing profitability pressures.

4. Changing the Business ModelFinally, banks need to think through the necessary restructuring in response to new capital and liquidity constraints, such as the potential separation of investment and retail banking in some jurisdictions. This proposal drives uncertainty that needs to be addressed around which are the core shared services across a banking group and therefore what operational efficiencies can be exploited.

10

Challenge 3: Operating with a Restricted Balance Sheet

Managing clients with high risk weightings

Improve the quantity and quality of capital

Reward businesses on a 'par' basis

Understand new capital and liquidity constraints

Optimise collateralCompensate staff

effectivelyIndentify core shared services

Withstand additional capital charges

Take advantage of CVA capital reductions

Managing RWAs Optimising Capital

Operations Centre

Allocating Capital Changing the Business Model

Fig 4: Operational challenges to be overcome. Source: Accenture Research

Challenge 3: Operating with a Restricted Balance Sheet

11

Understanding regulatory impact on capital Banks need to understand the impact of new regulation on the capital base, whilst also reviewing funding models across lines of business to accommodate regulatory change. Working at the local level to understand both regional and global business requirements is equally critical. Engagement with regulators is essential to ensure emerging initiatives are factored into strategic thinking as early as possible.

Achieving business growth with scarce capitalThe way banks respond to regulation is linked to their ability to attract investment and drive business growth. Investors are prepared to accept

utility-level returns from banks provided that these come with utility-level volatility. Banks that can demonstrably align their risk capacity and their response to regulation to their business growth strategies will stand out from their competitors.

More specifically, banks need to reorganise their operations to establish the right combination of clients, products and markets are based on the capital available. Banks can segment customers more effectively to reduce the cost of serving unprofitable clients and focus on more profitable segments per capital employed. Banks also need to identify the products and services that will differentiate the bank’s business from the competition. As well as identifying the most advantageous geographic markets for growth, banks must also identify the business segments where they can compete most effectively.

Our PerspectiveBanks need to identify approaches to simultaneously reduce costs and drive business growth while understanding how regulation will help shape decisions.

"Engagement with regulators is essential to ensure emerging initiatives are factored into strategic thinking as early as possible".

3. Manage cost-of-capitalto pricing strategyEffective pricing strategies are built on a holistic understanding of the cost-of-capital for serving clients. This would include managing counterparty risk performance, increasing product/asset returns and lowering the cost of executing and servicing deals. Each of these initiatives will help banks to develop efficient client management workflows, deliver consistent global pricing for clients and truly reflect the cost-of-capital in each transaction.

Reducing costs It is imperative that steps to grow the business accompany targeted cost reduction measures. Based on Accenture’s experience with investment banks, we believe there are three key ways to achieve the necessary reduction in costs to improve profitability:

1. Achieve operational excellence in RWA processes Certain key processes have direct and indirect impacts on the efficient management of RWAs. Having identified these processes, banks must move to achieve operational excellence for those processes that have a direct impact on regulatory capital release such as collateral, hedging, netting, counterparty limits and client on-boarding. Improvements in the accuracy of RWAs are also key given that regulators will recognise and reward effective operational management of risk mitigation processes and risk oversight.

2. Enhance operationalefficienciesThe operational costs of a bank can adversely impact profitability and therefore raise a number of priority objectives. Cost-income ratios of around 60 percent are a key benchmark for banks to meet, as are efforts to reduce RWAs by improving data quality in front-to-back processes.

12

Challenge 3: Operating with a Restricted Balance Sheet

Challenge 3: Operating with a Restricted Balance Sheet

13

Defining a regulatory roadmap Accenture worked with a Tier I global investment bank to define its strategic response to regulation ranging from Basel, the European Market Infrastructure Regulation, to Dodd-Frank and MiFID.

Accenture worked with the business to develop a programme of workstreams addressing different impacts of the regulation and to action the required mitigation planning. Furthermore, Accenture’s quantitative analysis of the regulatory impact on product portfolios, clients and ROE led to a recommendation of business model changes for the client and a roadmap to achieve these.

In Practice

Diane Nolan Senior Executive, Brussels [email protected] +32 2226 7574 +32 4775 96574

Karl Meekings London [email protected] +44 20 7844 5530 +44 78 2482 3007

Takis Sironis London [email protected] +44 20 3335 0457 +44 77 4094 9497

Accenture ExpertsTo discuss any of the ideas presented in this paper please contact:

References1 http://www.bba.org.uk/download/6858

Copyright © 2011 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with more than 223,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$21.6 billion for the fiscal year ended Aug. 31, 2010. Its home page is www.accenture.com.

Disclaimer This report has been prepared by and is distributed by Accenture. This document is for information purposes. No part of this document may be reproduced in any manner without the written permission of Accenture. While we take precautions to ensure that the source and the information we base our judgments on is reliable, we do not represent that this information is accurate or complete and it should not be relied upon as such. It is provided with the understanding that Accenture is not acting in a fiduciary capacity. Opinions expressed herein are subject to change without notice.

Top Ten Challengesfor Investment Banks 20121 Making Decisions in Uncertain Times 2 Living with the New Trading Environment 3 OperatingwithaRestrictedBalanceSheet4 Addressing the Rise in Buy-Side Power 5 Managing Capital and Collateral Intelligently 6 Valuing Client Relationships, Not Product Profits 7 Marshalling Fluid Architectures for Business Innovation 8 Managing Talent in the New Compensation Paradigm9 Maturing in Emerging Markets10 Achieving Sustainable Cost Reduction