Embed Size (px)

Citation preview

Accessing the Global Markets

Through London

London Stock Exchange Masala Bonds

January 2017

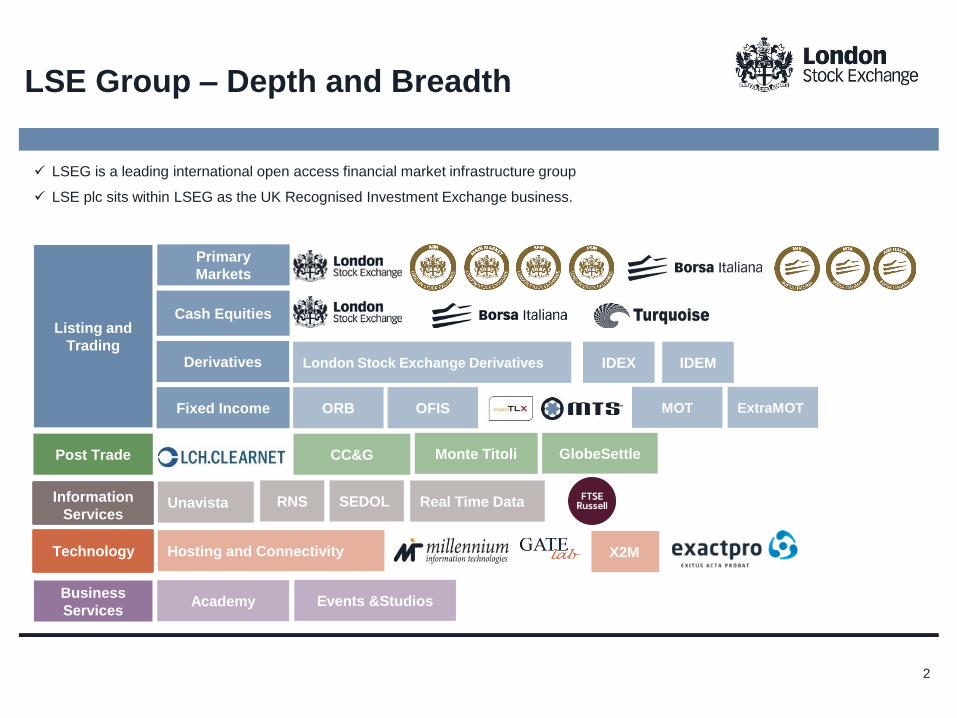

Primary

Markets

Cash Equities

Derivatives

Fixed Income

IDEM

RNS

MOT

X2M Technology

Monte Titoli CC&G

ORB ExtraMOT

London Stock Exchange Derivatives IDEX

GlobeSettle

SEDOL Unavista Real Time Data

Information

Services

Post Trade

Listing and

Trading

Business

Services Academy Events &Studios

OFIS

Hosting and Connectivity

LSEG is a leading international open access financial market infrastructure group

LSE plc sits within LSEG as the UK Recognised Investment Exchange business.

LSE Group – Depth and Breadth

2

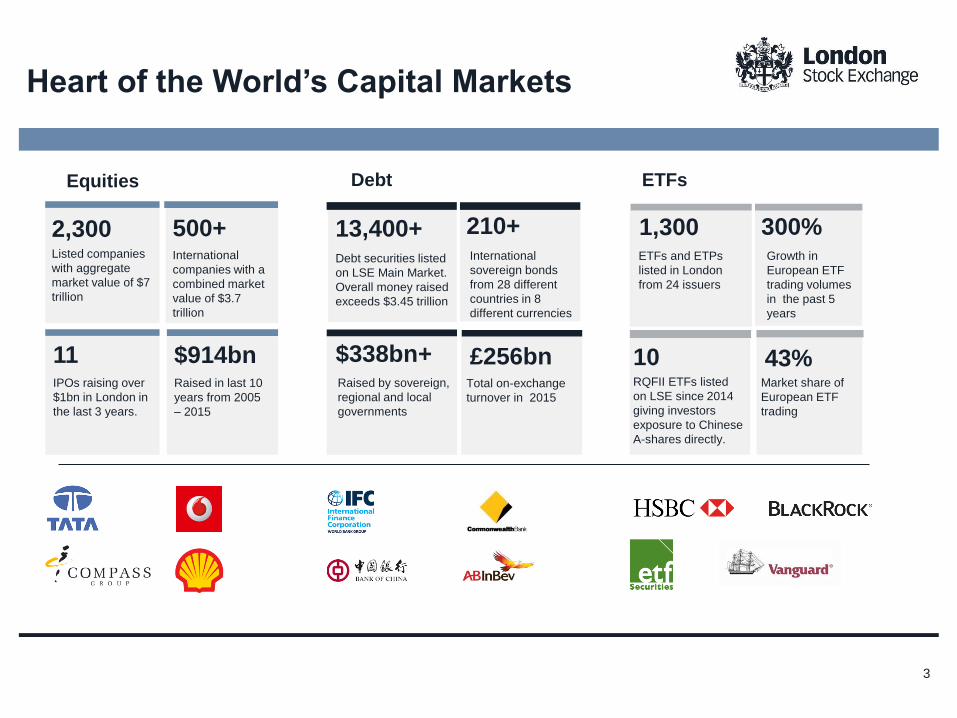

Equities

2,300 Listed companies

with aggregate

market value of $7

trillion

500+ International

companies with a

combined market

value of $3.7

trillion

$914bn Raised in last 10

years from 2005

– 2015

Debt

13,400+ Debt securities listed

on LSE Main Market.

Overall money raised

exceeds $3.45 trillion

210+ International

sovereign bonds

from 28 different

countries in 8

different currencies

$338bn+ Raised by sovereign,

regional and local

governments

£256bn Total on-exchange

turnover in 2015

ETFs

1,300 ETFs and ETPs

listed in London

from 24 issuers

43% Market share of

European ETF

trading

10 RQFII ETFs listed

on LSE since 2014

giving investors

exposure to Chinese

A-shares directly.

300% Growth in

European ETF

trading volumes

in the past 5

years

Heart of the World’s Capital Markets

3

11 IPOs raising over

$1bn in London in

the last 3 years.

The London

Proposition

4

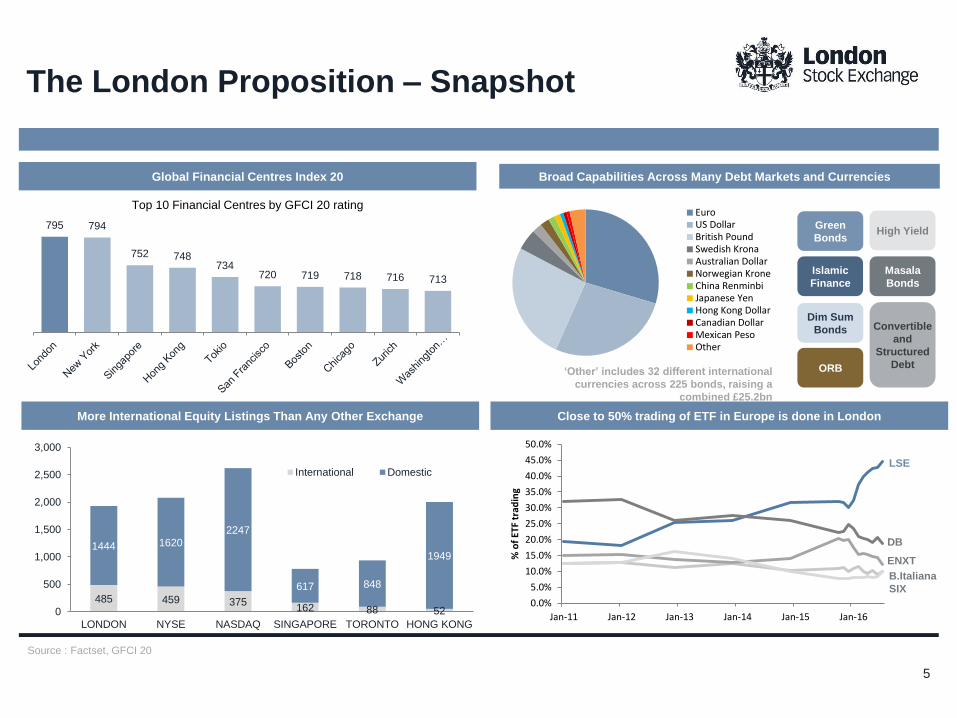

Global Financial Centres Index 20

Source : Factset, GFCI 20

Broad Capabilities Across Many Debt Markets and Currencies

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

% o

f ET

F tr

adin

g

Green

Bonds

Islamic

Finance

Dim Sum

Bonds

High Yield

Convertible

and

Structured

Debt ORB

Masala

Bonds

EuroUS DollarBritish PoundSwedish KronaAustralian DollarNorwegian KroneChina RenminbiJapanese YenHong Kong DollarCanadian DollarMexican PesoOther

‘Other’ includes 32 different international

currencies across 225 bonds, raising a

combined £25.2bn

More International Equity Listings Than Any Other Exchange Close to 50% trading of ETF in Europe is done in London

LSE

DB

ENXT

B.Italiana

SIX

The London Proposition – Snapshot

795 794

752 748 734

720 719 718 716 713

Top 10 Financial Centres by GFCI 20 rating

5

485 459 375 162 88 52

1444 1620

2247

617 848

1949

0

500

1,000

1,500

2,000

2,500

3,000

LONDON NYSE NASDAQ SINGAPORE TORONTO HONG KONG

International Domestic

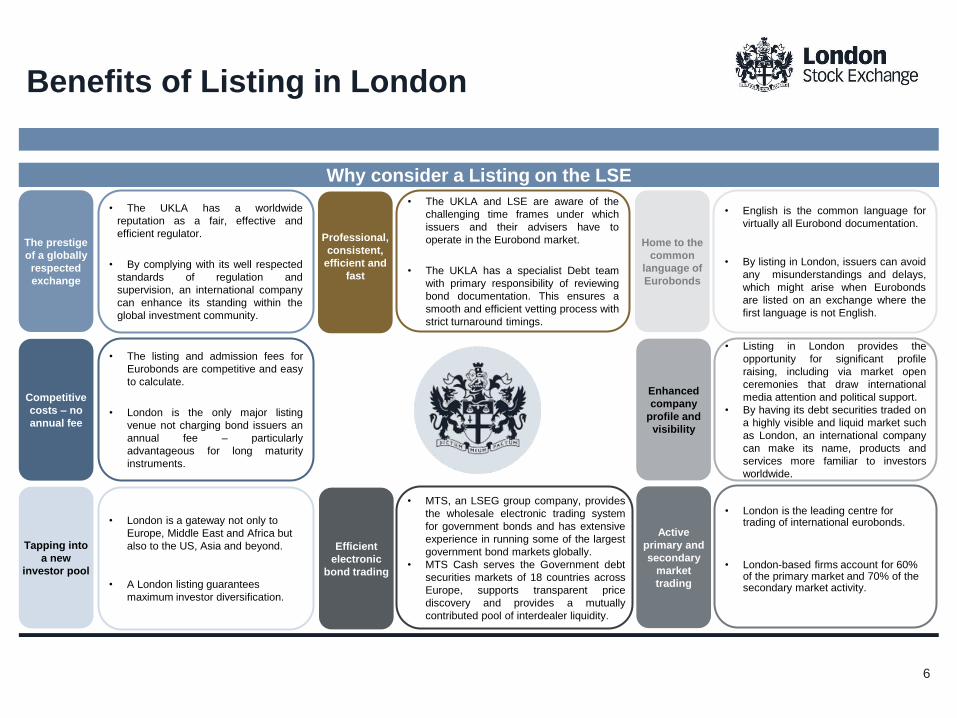

Why consider a Listing on the LSE

Benefits of Listing in London

6

• The UKLA has a worldwide

reputation as a fair, effective and

efficient regulator.

• By complying with its well respected

standards of regulation and

supervision, an international company

can enhance its standing within the

global investment community.

• The listing and admission fees for

Eurobonds are competitive and easy

to calculate.

• London is the only major listing

venue not charging bond issuers an

annual fee – particularly

advantageous for long maturity

instruments.

The prestige

of a globally

respected

exchange

Competitive

costs – no

annual fee

Tapping into

a new

investor pool

Home to the

common

language of

Eurobonds

• English is the common language for

virtually all Eurobond documentation.

• By listing in London, issuers can avoid

any misunderstandings and delays,

which might arise when Eurobonds

are listed on an exchange where the

first language is not English.

Enhanced

company

profile and

visibility

• Listing in London provides the

opportunity for significant profile

raising, including via market open

ceremonies that draw international

media attention and political support.

• By having its debt securities traded on

a highly visible and liquid market such

as London, an international company

can make its name, products and

services more familiar to investors

worldwide.

Efficient

electronic

bond trading

• MTS, an LSEG group company, provides

the wholesale electronic trading system

for government bonds and has extensive

experience in running some of the largest

government bond markets globally.

• MTS Cash serves the Government debt

securities markets of 18 countries across

Europe, supports transparent price

discovery and provides a mutually

contributed pool of interdealer liquidity.

Professional,

consistent,

efficient and

fast

• The UKLA and LSE are aware of the

challenging time frames under which

issuers and their advisers have to

operate in the Eurobond market.

• The UKLA has a specialist Debt team

with primary responsibility of reviewing

bond documentation. This ensures a

smooth and efficient vetting process with

strict turnaround timings.

Active

primary and

secondary

market

trading

• London is the leading centre for trading of international eurobonds.

• London-based firms account for 60% of the primary market and 70% of the secondary market activity.

• London is a gateway not only to

Europe, Middle East and Africa but

also to the US, Asia and beyond.

• A London listing guarantees

maximum investor diversification.

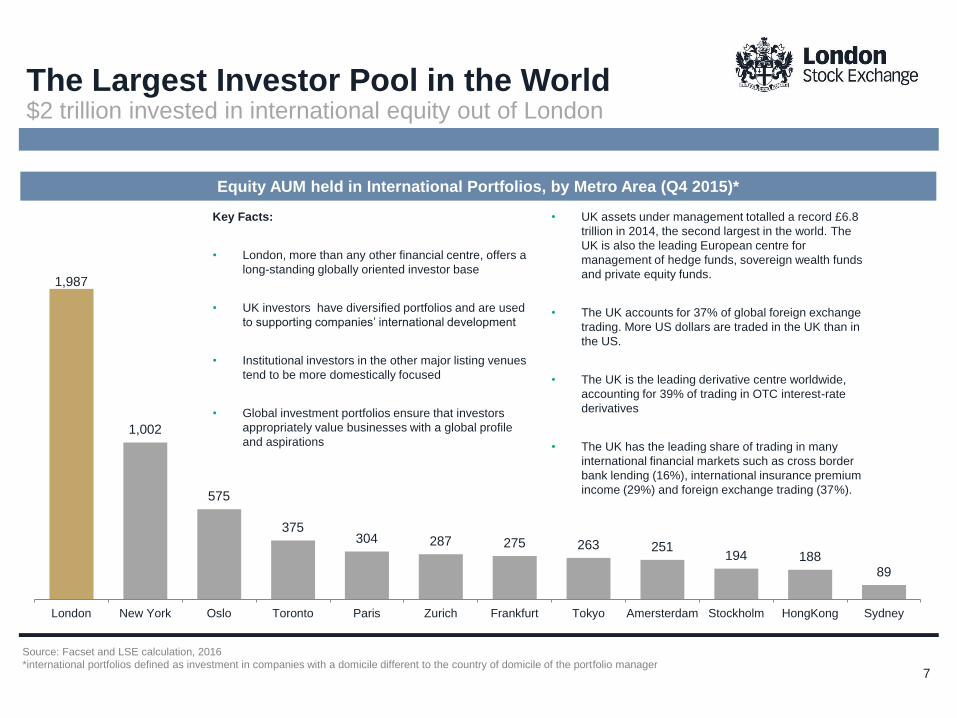

• UK assets under management totalled a record £6.8

trillion in 2014, the second largest in the world. The

UK is also the leading European centre for

management of hedge funds, sovereign wealth funds

and private equity funds.

• The UK accounts for 37% of global foreign exchange

trading. More US dollars are traded in the UK than in

the US.

• The UK is the leading derivative centre worldwide,

accounting for 39% of trading in OTC interest-rate

derivatives

• The UK has the leading share of trading in many

international financial markets such as cross border

bank lending (16%), international insurance premium

income (29%) and foreign exchange trading (37%).

Equity AUM held in International Portfolios, by Metro Area (Q4 2015)*

Key Facts:

• London, more than any other financial centre, offers a

long-standing globally oriented investor base

• UK investors have diversified portfolios and are used

to supporting companies’ international development

• Institutional investors in the other major listing venues

tend to be more domestically focused

• Global investment portfolios ensure that investors

appropriately value businesses with a global profile

and aspirations

The Largest Investor Pool in the World $2 trillion invested in international equity out of London

7

1,987

1,002

575

375 304 287 275 263 251

194 188 89

London New York Oslo Toronto Paris Zurich Frankfurt Tokyo Amersterdam Stockholm HongKong Sydney

Source: Facset and LSE calculation, 2016

*international portfolios defined as investment in companies with a domicile different to the country of domicile of the portfolio manager

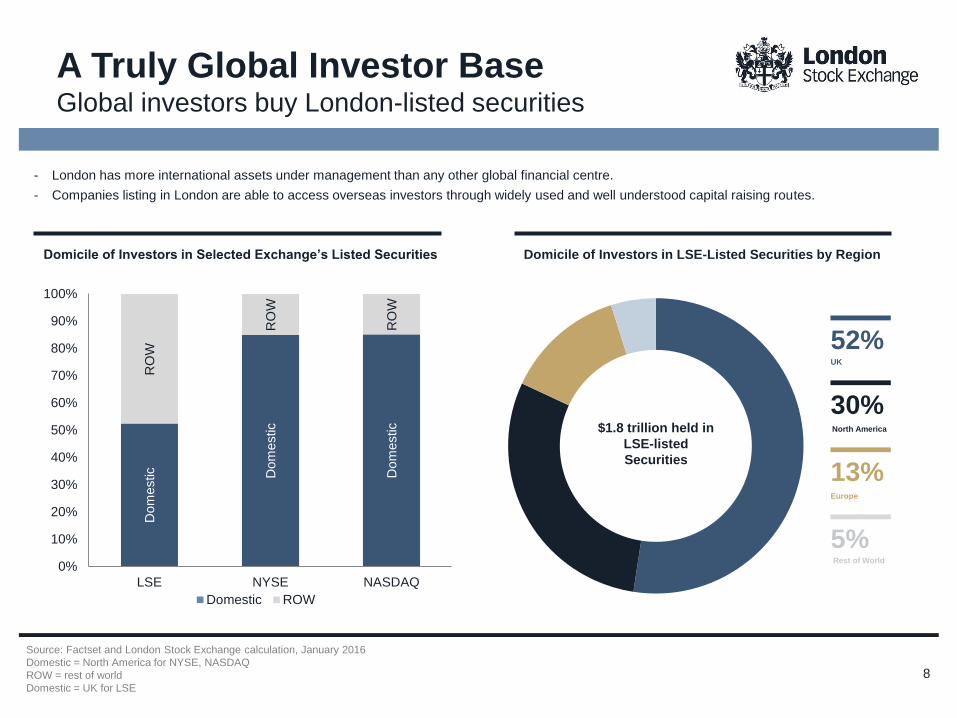

Source: Factset and London Stock Exchange calculation, January 2016

Domestic = North America for NYSE, NASDAQ

ROW = rest of world

Domestic = UK for LSE

- London has more international assets under management than any other global financial centre.

- Companies listing in London are able to access overseas investors through widely used and well understood capital raising routes.

Domicile of Investors in LSE-Listed Securities by Region

5% Rest of World

30% North America

13% Europe

Domicile of Investors in Selected Exchange’s Listed Securities

52% UK

A Truly Global Investor Base Global investors buy London-listed securities

$1.8 trillion held in

LSE-listed

Securities

Dom

estic

Dom

estic

Dom

estic

RO

W

RO

W

RO

W

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

LSE NYSE NASDAQ

Domestic ROW

8

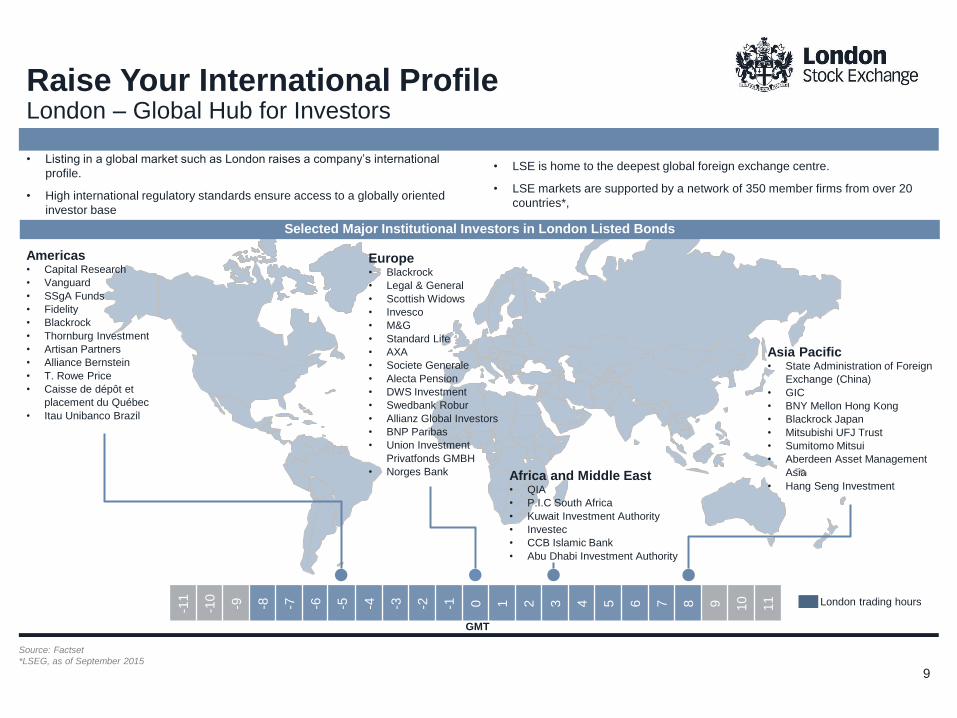

Asia Pacific • State Administration of Foreign

Exchange (China)

• GIC

• BNY Mellon Hong Kong

• Blackrock Japan

• Mitsubishi UFJ Trust

• Sumitomo Mitsui

• Aberdeen Asset Management

Asia

• Hang Seng Investment

Europe • Blackrock

• Legal & General

• Scottish Widows

• Invesco

• M&G

• Standard Life

• AXA

• Societe Generale

• Alecta Pension

• DWS Investment

• Swedbank Robur

• Allianz Global Investors

• BNP Paribas

• Union Investment

Privatfonds GMBH

• Norges Bank

Americas • Capital Research

• Vanguard

• SSgA Funds

• Fidelity

• Blackrock

• Thornburg Investment

• Artisan Partners

• Alliance Bernstein

• T. Rowe Price

• Caisse de dépôt et

placement du Québec

• Itau Unibanco Brazil

Africa and Middle East

• QIA

• P.I.C South Africa

• Kuwait Investment Authority

• Investec

• CCB Islamic Bank

• Abu Dhabi Investment Authority

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

London trading hours

Selected Major Institutional Investors in London Listed Bonds

GMT

Source: Factset

*LSEG, as of September 2015

• Listing in a global market such as London raises a company’s international

profile.

• High international regulatory standards ensure access to a globally oriented

investor base

• LSE is home to the deepest global foreign exchange centre.

• LSE markets are supported by a network of 350 member firms from over 20

countries*,

Raise Your International Profile London – Global Hub for Investors

9

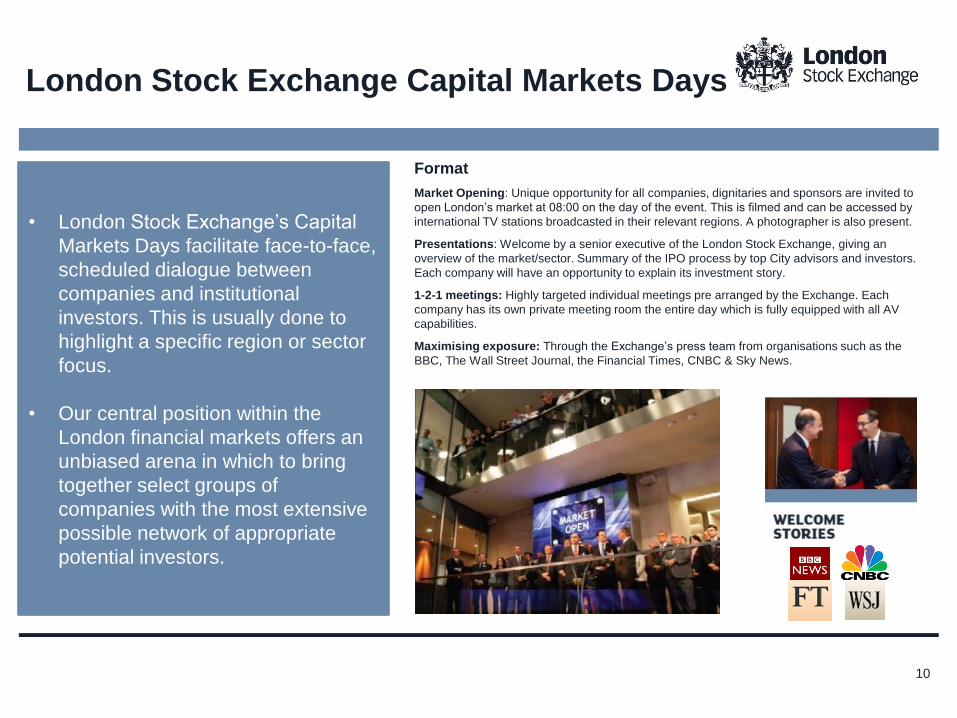

• London Stock Exchange’s Capital

Markets Days facilitate face-to-face,

scheduled dialogue between

companies and institutional

investors. This is usually done to

highlight a specific region or sector

focus.

• Our central position within the

London financial markets offers an

unbiased arena in which to bring

together select groups of

companies with the most extensive

possible network of appropriate

potential investors.

Format

Market Opening: Unique opportunity for all companies, dignitaries and sponsors are invited to

open London’s market at 08:00 on the day of the event. This is filmed and can be accessed by

international TV stations broadcasted in their relevant regions. A photographer is also present.

Presentations: Welcome by a senior executive of the London Stock Exchange, giving an

overview of the market/sector. Summary of the IPO process by top City advisors and investors.

Each company will have an opportunity to explain its investment story.

1-2-1 meetings: Highly targeted individual meetings pre arranged by the Exchange. Each

company has its own private meeting room the entire day which is fully equipped with all AV

capabilities.

Maximising exposure: Through the Exchange’s press team from organisations such as the

BBC, The Wall Street Journal, the Financial Times, CNBC & Sky News.

London Stock Exchange Capital Markets Days

10

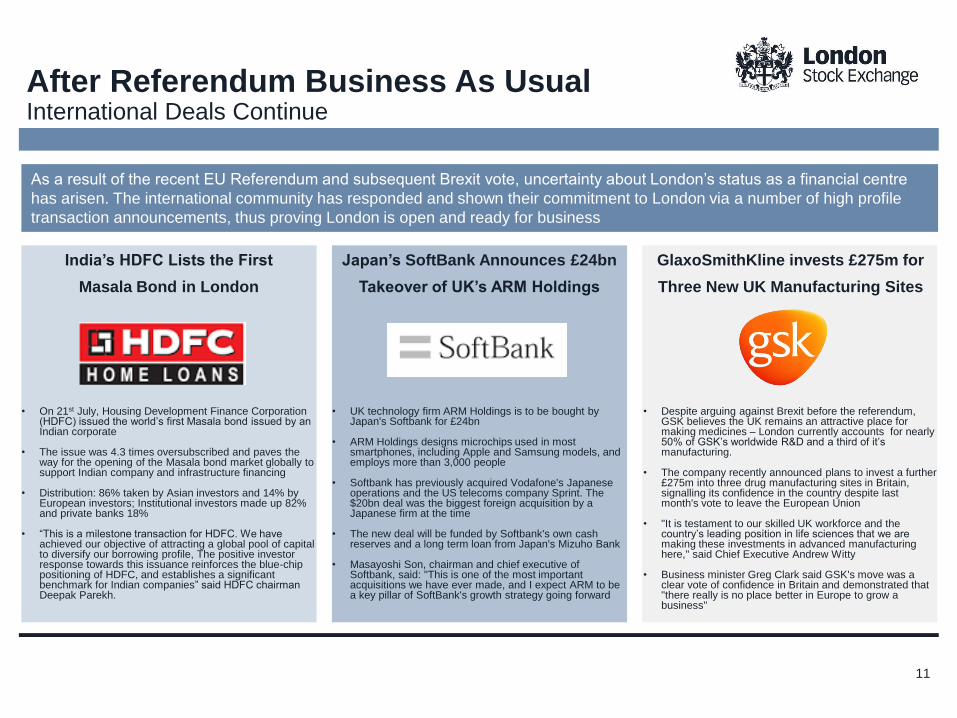

As a result of the recent EU Referendum and subsequent Brexit vote, uncertainty about London’s status as a financial centre

has arisen. The international community has responded and shown their commitment to London via a number of high profile

transaction announcements, thus proving London is open and ready for business

India’s HDFC Lists the First

Masala Bond in London

Japan’s SoftBank Announces £24bn

Takeover of UK’s ARM Holdings

GlaxoSmithKline invests £275m for

Three New UK Manufacturing Sites

• On 21st July, Housing Development Finance Corporation (HDFC) issued the world’s first Masala bond issued by an Indian corporate

• The issue was 4.3 times oversubscribed and paves the way for the opening of the Masala bond market globally to support Indian company and infrastructure financing

• Distribution: 86% taken by Asian investors and 14% by European investors; Institutional investors made up 82% and private banks 18%

• “This is a milestone transaction for HDFC. We have achieved our objective of attracting a global pool of capital to diversify our borrowing profile, The positive investor response towards this issuance reinforces the blue-chip positioning of HDFC, and establishes a significant benchmark for Indian companies” said HDFC chairman Deepak Parekh.

• UK technology firm ARM Holdings is to be bought by Japan's Softbank for £24bn

• ARM Holdings designs microchips used in most

smartphones, including Apple and Samsung models, and employs more than 3,000 people

• Softbank has previously acquired Vodafone's Japanese operations and the US telecoms company Sprint. The $20bn deal was the biggest foreign acquisition by a Japanese firm at the time

• The new deal will be funded by Softbank's own cash

reserves and a long term loan from Japan's Mizuho Bank

• Masayoshi Son, chairman and chief executive of Softbank, said: "This is one of the most important acquisitions we have ever made, and I expect ARM to be a key pillar of SoftBank's growth strategy going forward

• Despite arguing against Brexit before the referendum, GSK believes the UK remains an attractive place for making medicines – London currently accounts for nearly 50% of GSK’s worldwide R&D and a third of it’s manufacturing.

• The company recently announced plans to invest a further £275m into three drug manufacturing sites in Britain, signalling its confidence in the country despite last month's vote to leave the European Union

• "It is testament to our skilled UK workforce and the country’s leading position in life sciences that we are making these investments in advanced manufacturing here," said Chief Executive Andrew Witty

• Business minister Greg Clark said GSK's move was a clear vote of confidence in Britain and demonstrated that "there really is no place better in Europe to grow a business"

After Referendum Business As Usual International Deals Continue

11

London Stock Exchange’s

Fixed Income Offering

12

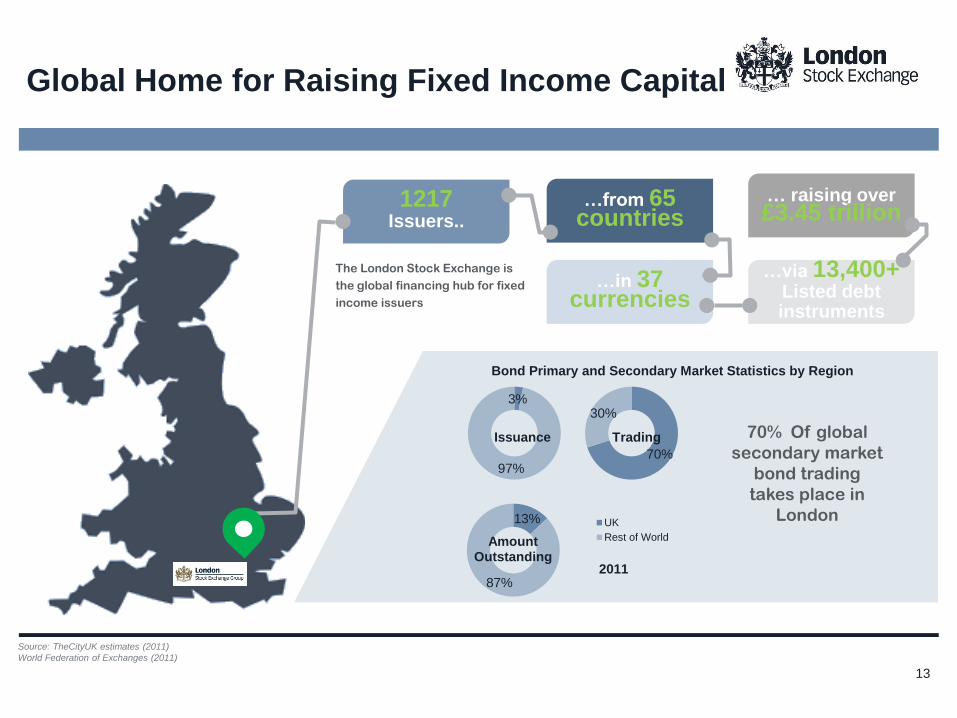

…via 13,400+ Listed debt instruments

… raising over £3.45 trillion

…from 65 countries

…in 37 currencies

1217 Issuers..

3%

97%

Issuance

70%

30%

Trading

13%

87%

Amount Outstanding

UK

Rest of World

2011

The London Stock Exchange is

the global financing hub for fixed

income issuers

Source: TheCityUK estimates (2011)

World Federation of Exchanges (2011)

Bond Primary and Secondary Market Statistics by Region

70% Of global

secondary market

bond trading

takes place in

London

Global Home for Raising Fixed Income Capital

13

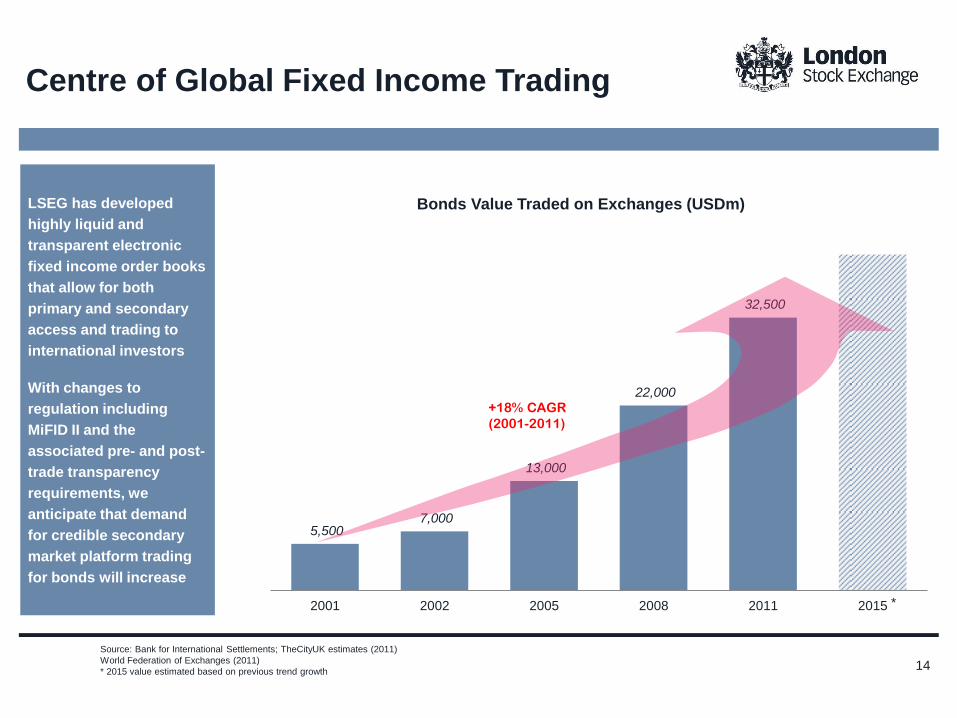

Centre of Global Fixed Income Trading

5,500 7,000

13,000

22,000

32,500

2001 2002 2005 2008 2011 2015

Bonds Value Traded on Exchanges (USDm)

+18% CAGR

(2001-2011)

*

Source: Bank for International Settlements; TheCityUK estimates (2011)

World Federation of Exchanges (2011)

* 2015 value estimated based on previous trend growth

LSEG has developed

highly liquid and

transparent electronic

fixed income order books

that allow for both

primary and secondary

access and trading to

international investors

With changes to

regulation including

MiFID II and the

associated pre- and post-

trade transparency

requirements, we

anticipate that demand

for credible secondary

market platform trading

for bonds will increase

14

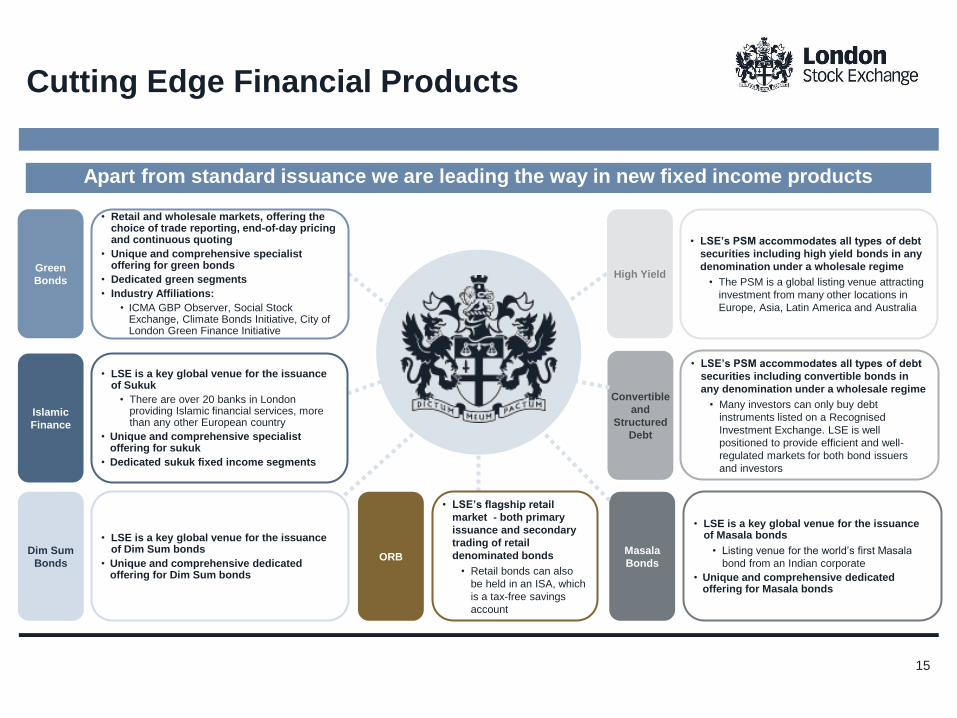

Apart from standard issuance we are leading the way in new fixed income products

Green

Bonds

• Retail and wholesale markets, offering the choice of trade reporting, end-of-day pricing and continuous quoting

• Unique and comprehensive specialist offering for green bonds

• Dedicated green segments

• Industry Affiliations:

• ICMA GBP Observer, Social Stock Exchange, Climate Bonds Initiative, City of London Green Finance Initiative

Islamic

Finance

• LSE is a key global venue for the issuance of Sukuk

• There are over 20 banks in London providing Islamic financial services, more than any other European country

• Unique and comprehensive specialist offering for sukuk

• Dedicated sukuk fixed income segments

Dim Sum

Bonds

High Yield

• LSE’s PSM accommodates all types of debt

securities including high yield bonds in any

denomination under a wholesale regime

• The PSM is a global listing venue attracting

investment from many other locations in

Europe, Asia, Latin America and Australia

Convertible

and

Structured

Debt

• LSE’s PSM accommodates all types of debt

securities including convertible bonds in

any denomination under a wholesale regime

• Many investors can only buy debt

instruments listed on a Recognised

Investment Exchange. LSE is well

positioned to provide efficient and well-

regulated markets for both bond issuers

and investors

ORB

• LSE’s flagship retail

market - both primary

issuance and secondary

trading of retail

denominated bonds

• Retail bonds can also

be held in an ISA, which

is a tax-free savings

account

Masala

Bonds

• LSE is a key global venue for the issuance of Masala bonds

• Listing venue for the world’s first Masala

bond from an Indian corporate

• Unique and comprehensive dedicated offering for Masala bonds

• LSE is a key global venue for the issuance of Dim Sum bonds

• Unique and comprehensive dedicated offering for Dim Sum bonds

Cutting Edge Financial Products

15

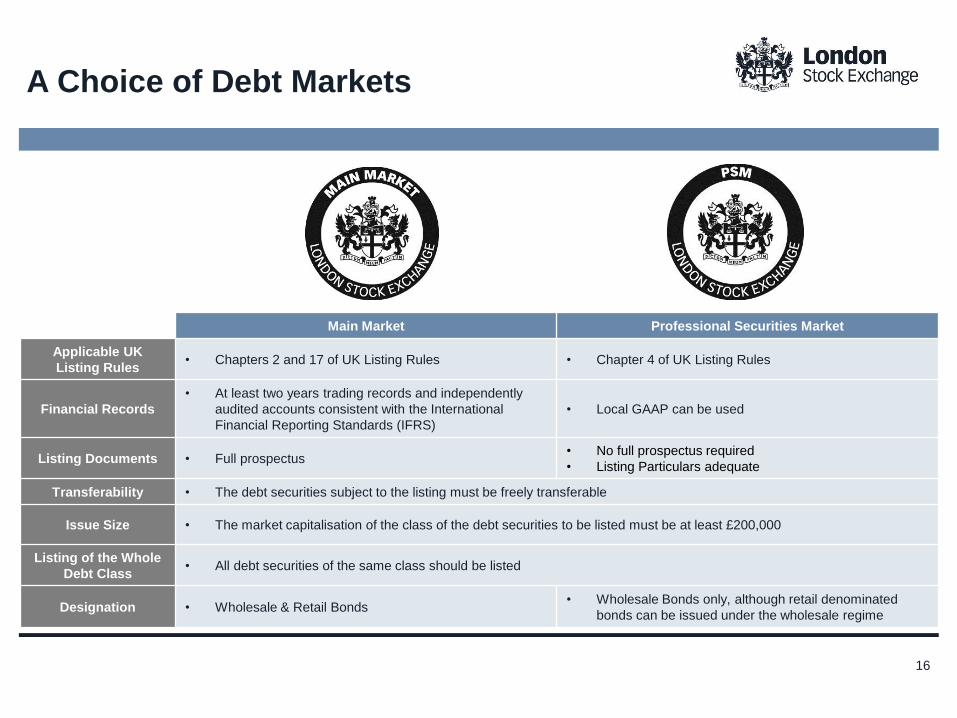

Main Market Professional Securities Market

Applicable UK

Listing Rules • Chapters 2 and 17 of UK Listing Rules • Chapter 4 of UK Listing Rules

Financial Records

• At least two years trading records and independently

audited accounts consistent with the International

Financial Reporting Standards (IFRS)

• Local GAAP can be used

Listing Documents • Full prospectus • No full prospectus required

• Listing Particulars adequate

Transferability • The debt securities subject to the listing must be freely transferable

Issue Size • The market capitalisation of the class of the debt securities to be listed must be at least £200,000

Listing of the Whole

Debt Class • All debt securities of the same class should be listed

Designation • Wholesale & Retail Bonds • Wholesale Bonds only, although retail denominated

bonds can be issued under the wholesale regime

A Choice of Debt Markets

16

Listing & Admissions Process

17

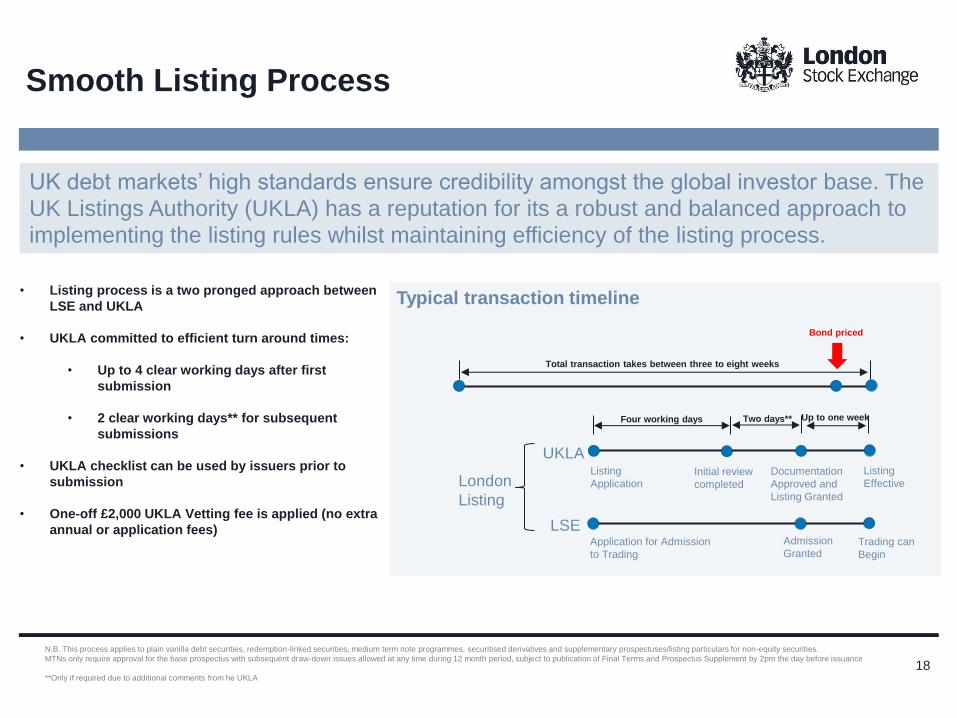

Smooth Listing Process

UK debt markets’ high standards ensure credibility amongst the global investor base. The

UK Listings Authority (UKLA) has a reputation for its a robust and balanced approach to

implementing the listing rules whilst maintaining efficiency of the listing process.

• Listing process is a two pronged approach between

LSE and UKLA

• UKLA committed to efficient turn around times:

• Up to 4 clear working days after first

submission

• 2 clear working days** for subsequent

submissions

• UKLA checklist can be used by issuers prior to

submission

• One-off £2,000 UKLA Vetting fee is applied (no extra

annual or application fees)

N.B. This process applies to plain vanilla debt securities, redemption-linked securities, medium term note programmes, securitised derivatives and supplementary prospectuses/listing particulars for non-equity securities.

MTNs only require approval for the base prospectus with subsequent draw-down issues allowed at any time during 12 month period, subject to publication of Final Terms and Prospectus Supplement by 2pm the day before issuance

**Only if required due to additional comments from he UKLA

Typical transaction timeline

Total transaction takes between three to eight weeks

Up to one week Four working days Two days**

UKLA Documentation

Approved and

Listing Granted

Listing

Effective

Listing

Application

LSE

London

Listing

Application for Admission

to Trading

Admission

Granted Trading can

Begin

Bond priced

Initial review

completed

18

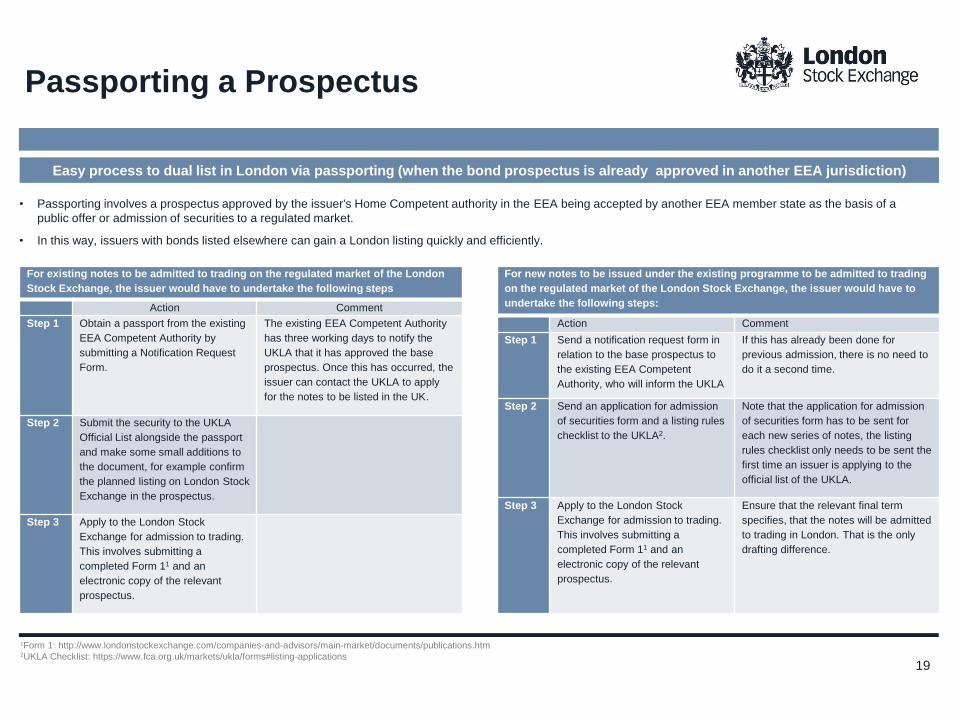

Passporting a Prospectus

Easy process to dual list in London via passporting (when the bond prospectus is already approved in another EEA jurisdiction)

For existing notes to be admitted to trading on the regulated market of the London

Stock Exchange, the issuer would have to undertake the following steps

Action Comment

Step 1

Obtain a passport from the existing

EEA Competent Authority by

submitting a Notification Request

Form.

The existing EEA Competent Authority

has three working days to notify the

UKLA that it has approved the base

prospectus. Once this has occurred, the

issuer can contact the UKLA to apply

for the notes to be listed in the UK.

Step 2

Submit the security to the UKLA

Official List alongside the passport

and make some small additions to

the document, for example confirm

the planned listing on London Stock

Exchange in the prospectus.

Step 3

Apply to the London Stock

Exchange for admission to trading.

This involves submitting a

completed Form 11 and an

electronic copy of the relevant

prospectus.

1Form 1: http://www.londonstockexchange.com/companies-and-advisors/main-market/documents/publications.htm 2UKLA Checklist: https://www.fca.org.uk/markets/ukla/forms#listing-applications

For new notes to be issued under the existing programme to be admitted to trading

on the regulated market of the London Stock Exchange, the issuer would have to

undertake the following steps:

Action Comment

Step 1

Send a notification request form in

relation to the base prospectus to

the existing EEA Competent

Authority, who will inform the UKLA

If this has already been done for

previous admission, there is no need to

do it a second time.

Step 2

Send an application for admission

of securities form and a listing rules

checklist to the UKLA2.

Note that the application for admission

of securities form has to be sent for

each new series of notes, the listing

rules checklist only needs to be sent the

first time an issuer is applying to the

official list of the UKLA.

Step 3

Apply to the London Stock

Exchange for admission to trading.

This involves submitting a

completed Form 11 and an

electronic copy of the relevant

prospectus.

Ensure that the relevant final term

specifies, that the notes will be admitted

to trading in London. That is the only

drafting difference.

• Passporting involves a prospectus approved by the issuer's Home Competent authority in the EEA being accepted by another EEA member state as the basis of a

public offer or admission of securities to a regulated market.

• In this way, issuers with bonds listed elsewhere can gain a London listing quickly and efficiently.

19

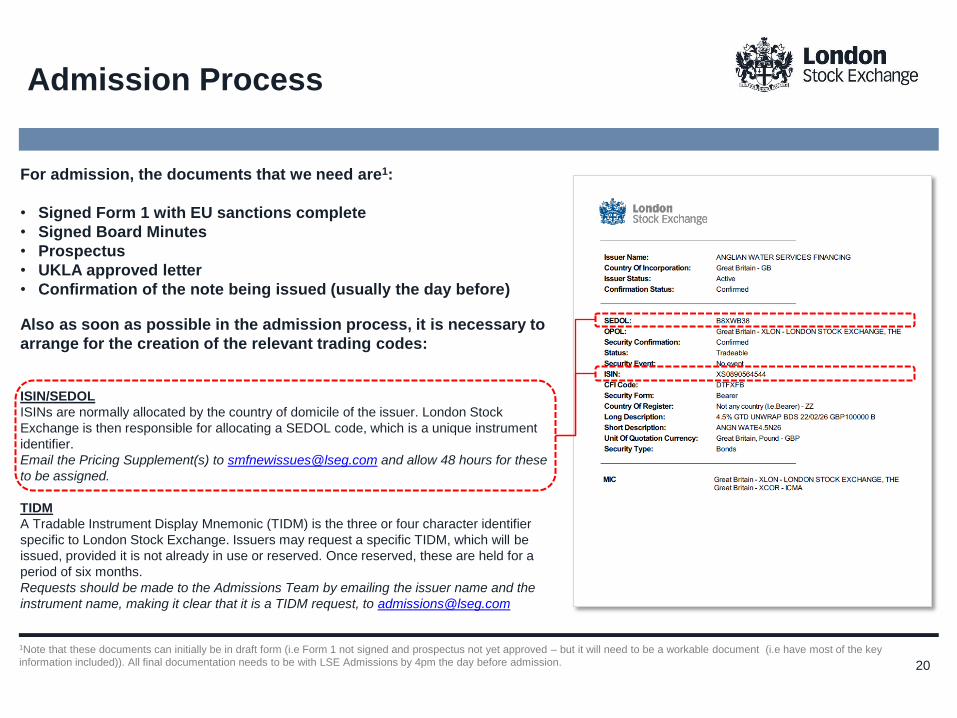

Admission Process

For admission, the documents that we need are1:

• Signed Form 1 with EU sanctions complete

• Signed Board Minutes

• Prospectus

• UKLA approved letter

• Confirmation of the note being issued (usually the day before)

Also as soon as possible in the admission process, it is necessary to

arrange for the creation of the relevant trading codes:

ISIN/SEDOL

ISINs are normally allocated by the country of domicile of the issuer. London Stock

Exchange is then responsible for allocating a SEDOL code, which is a unique instrument

identifier.

Email the Pricing Supplement(s) to [email protected] and allow 48 hours for these

to be assigned.

TIDM

A Tradable Instrument Display Mnemonic (TIDM) is the three or four character identifier

specific to London Stock Exchange. Issuers may request a specific TIDM, which will be

issued, provided it is not already in use or reserved. Once reserved, these are held for a

period of six months.

Requests should be made to the Admissions Team by emailing the issuer name and the

instrument name, making it clear that it is a TIDM request, to [email protected]

1Note that these documents can initially be in draft form (i.e Form 1 not signed and prospectus not yet approved – but it will need to be a workable document (i.e have most of the key

information included)). All final documentation needs to be with LSE Admissions by 4pm the day before admission. 20

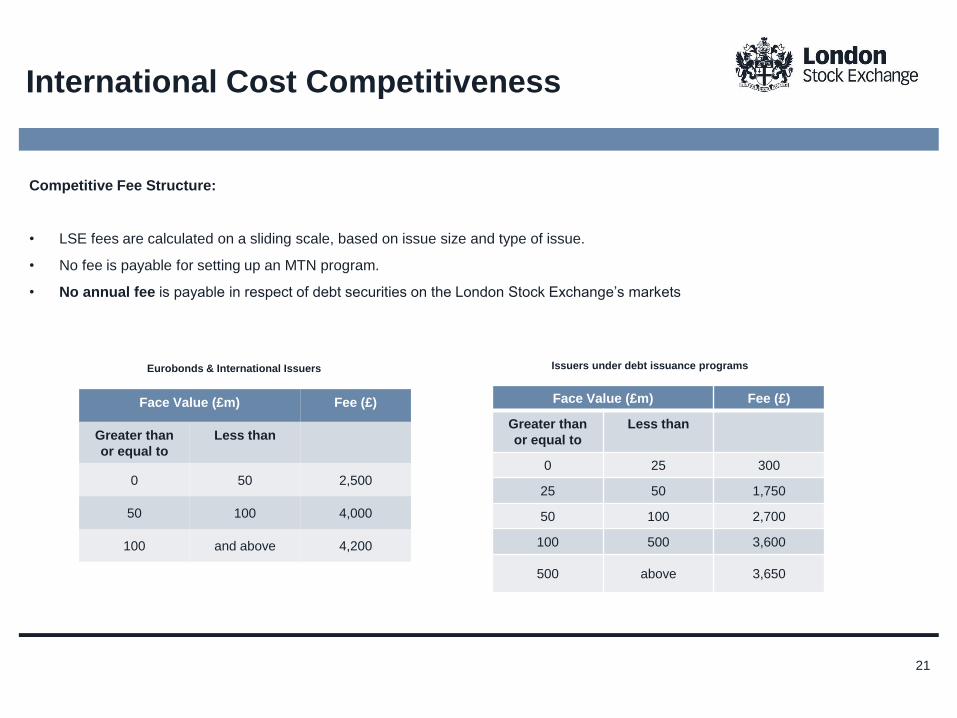

International Cost Competitiveness

Competitive Fee Structure:

• LSE fees are calculated on a sliding scale, based on issue size and type of issue.

• No fee is payable for setting up an MTN program.

• No annual fee is payable in respect of debt securities on the London Stock Exchange’s markets

Face Value (£m) Fee (£)

Greater than

or equal to

Less than

0 50 2,500

50 100 4,000

100 and above 4,200

Face Value (£m) Fee (£)

Greater than

or equal to

Less than

0 25 300

25 50 1,750

50 100 2,700

100 500 3,600

500 above 3,650

Eurobonds & International Issuers Issuers under debt issuance programs

21

Masala Bonds

22

“Today, we have outlined a bold and ambitious vision for

our strategic partnership, and the decisions we have

taken today reflect our firm commitment to pursue it and

the confidence to achieve it. Indeed, the outcomes today

have shown that we have already taken our relationship

to a new level.”

Narendra Modi

“It’s a real opportunity to open a new chapter in the

relationship between our two countries.”

David Cameron

“We will also increasingly raise funds in

London’s financial market. I am pleased

that we will issue a railways rupee bond

in London stock market. This is – for

this is where the journey of Indian

Railways had begun.”

Narendra Modi

“We will work together with the British

Government, industry, and the financial market

to deepen our relationship and harness that

interest in India’s infrastructure. Very soon,

these bonds will become strong instruments for

engagement between our financial markets.”

Narendra Modi

Source: Joint press release UK-India Summit, 12 November 2015, https://www.gov.uk/

“रूपी ब ॉंड अपने आप में भारत की आर्थिक

सॉंपन्नता का एक महत्वपरू्ि ममश्रर् है और

हहॉंदसु्तान के हर नागररक को इसको गौरव के रूप

में देखना चाहहए और इसको उजागर करना चाहहए, तभी तो भारत की ताक़त बढ़ती है“

Narendra Modi

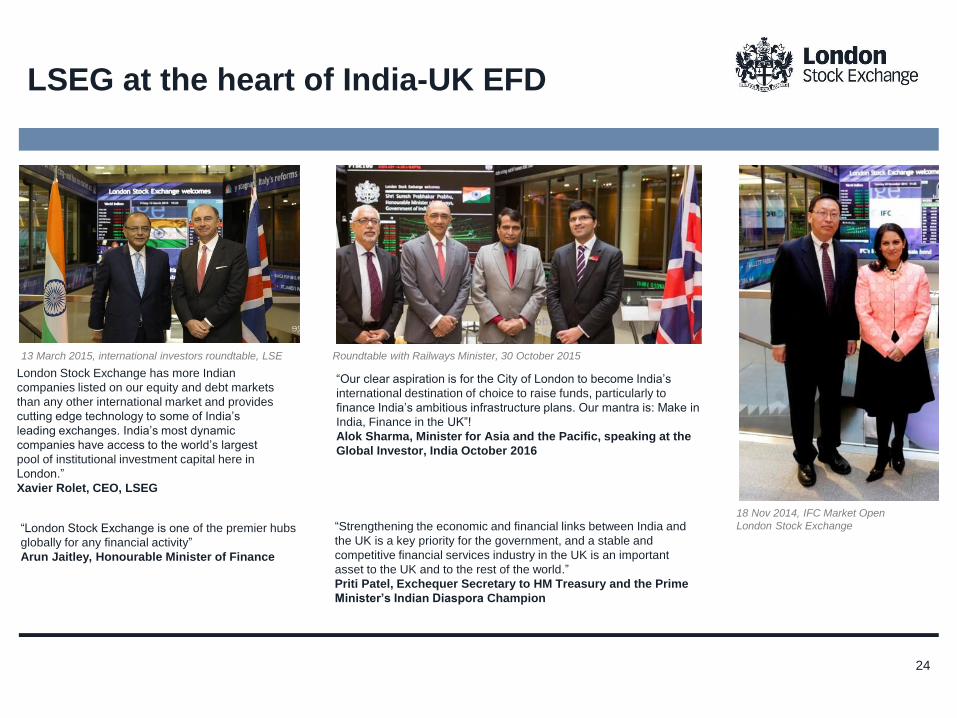

India – UK Finance Partnership

23

“Strengthening the economic and financial links between India and

the UK is a key priority for the government, and a stable and

competitive financial services industry in the UK is an important

asset to the UK and to the rest of the world.”

Priti Patel, Exchequer Secretary to HM Treasury and the Prime

Minister’s Indian Diaspora Champion

“London Stock Exchange is one of the premier hubs

globally for any financial activity”

Arun Jaitley, Honourable Minister of Finance

London Stock Exchange has more Indian

companies listed on our equity and debt markets

than any other international market and provides

cutting edge technology to some of India’s

leading exchanges. India’s most dynamic

companies have access to the world’s largest

pool of institutional investment capital here in

London.”

Xavier Rolet, CEO, LSEG

Roundtable with Railways Minister, 30 October 2015 13 March 2015, international investors roundtable, LSE

18 Nov 2014, IFC Market Open

London Stock Exchange

LSEG at the heart of India-UK EFD

24

“Our clear aspiration is for the City of London to become India’s

international destination of choice to raise funds, particularly to

finance India’s ambitious infrastructure plans. Our mantra is: Make in

India, Finance in the UK”!

Alok Sharma, Minister for Asia and the Pacific, speaking at the

Global Investor, India October 2016

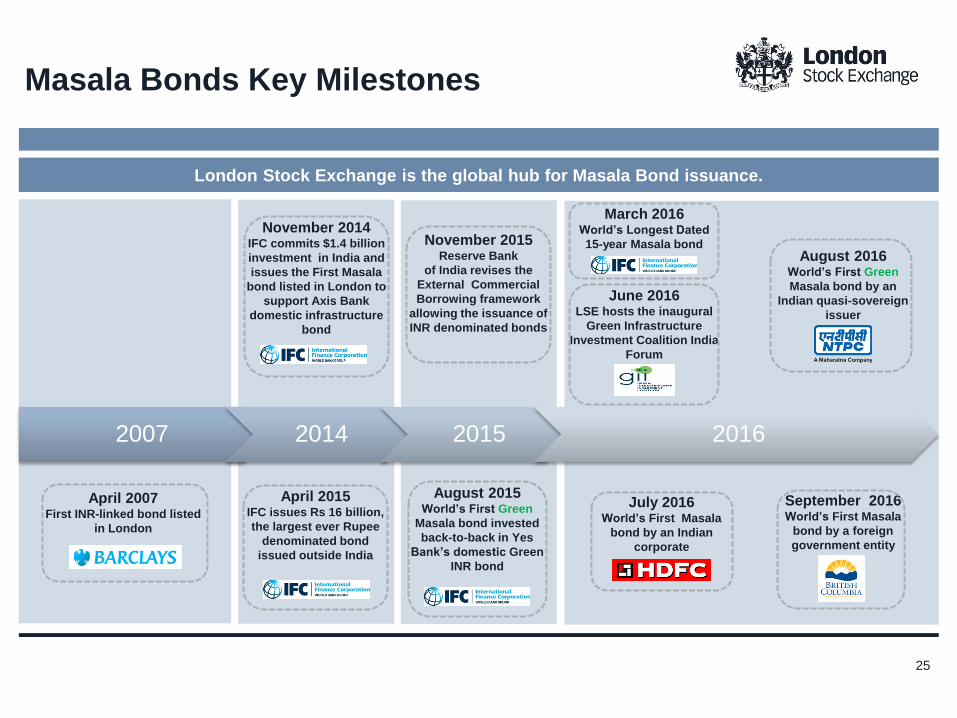

2007 2014 2015 2016

London Stock Exchange is the global hub for Masala Bond issuance.

Masala Bonds Key Milestones

September 2016 World’s First Masala

bond by a foreign

government entity

July 2016 World’s First Masala

bond by an Indian

corporate

November 2014 IFC commits $1.4 billion

investment in India and

issues the First Masala

bond listed in London to

support Axis Bank

domestic infrastructure

bond

August 2016 World’s First Green

Masala bond by an

Indian quasi-sovereign

issuer

November 2015 Reserve Bank

of India revises the

External Commercial

Borrowing framework

allowing the issuance of

INR denominated bonds

August 2015 World’s First Green

Masala bond invested

back-to-back in Yes

Bank’s domestic Green

INR bond

25

April 2007 First INR-linked bond listed

in London

March 2016 World’s Longest Dated

15-year Masala bond

April 2015 IFC issues Rs 16 billion,

the largest ever Rupee

denominated bond

issued outside India

June 2016 LSE hosts the inaugural

Green Infrastructure

Investment Coalition India

Forum

Hosted by the London stock Exchange, the inaugural India Forum of the Green Infrastructure Investment Coalition (GIIC)

brought together European institutional investors, Indian green infrastructure developers and financiers, development banks

and perspectives from both governments.

The aim of the event was to allow investors to understand the various ways of gaining exposure

to this quickly growing asset class.

The Forum covered India’s goals, policy measures being implemented, and investment

opportunities becoming available.

We invited participants to present 5 year pipelines of green investment opportunities, including

bonds and equity, with ticket sizes of $100 million and over.

India has huge green infrastructure plans: a target of 175 GW of renewables by 2022, a ramp-

up of rail transport, energy efficiency projects and development of 100 “smart cities”.

Speakers included:

• Sir Roger Gifford, Head of London’s Climate Finance Initiative

• Dr Rathin Roy, Director NIPFP

• Alok Sharma, MP UK Government Infrastructure Envoy

• Pierre Ducret, Special Advisor on Climate Change COP22

• Ajungla Jamir, First Secretary at India High Commissioner

• Sean Kidney, CEO Climate Bonds

• Abhay L. Bongirwar, Executive Director IDBI

26

June 2016 India Forum

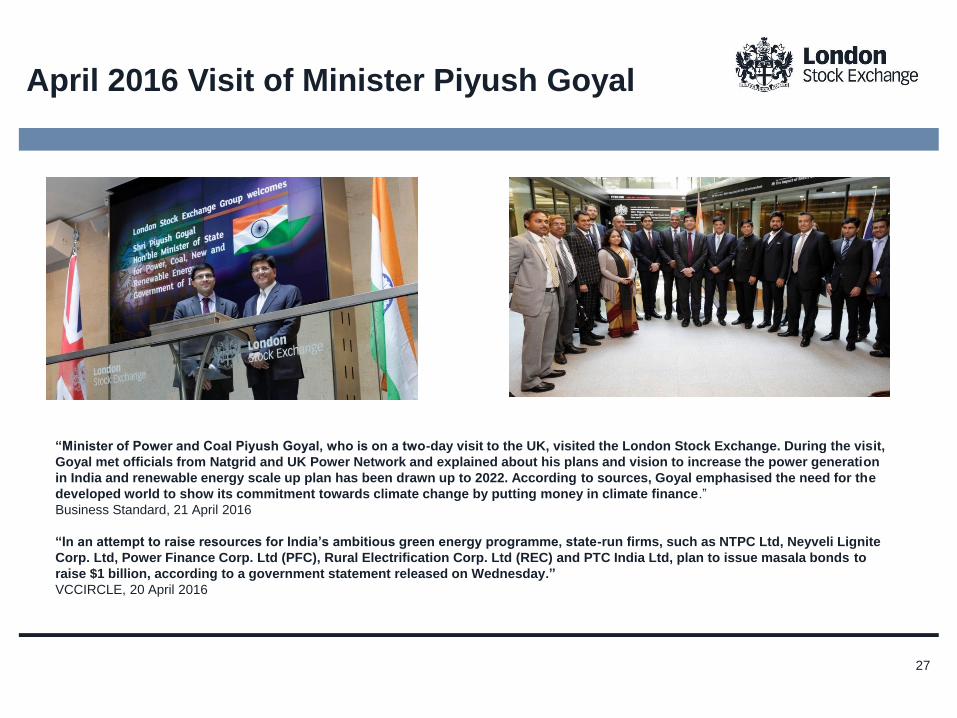

April 2016 Visit of Minister Piyush Goyal

“Minister of Power and Coal Piyush Goyal, who is on a two-day visit to the UK, visited the London Stock Exchange. During the visit,

Goyal met officials from Natgrid and UK Power Network and explained about his plans and vision to increase the power generation

in India and renewable energy scale up plan has been drawn up to 2022. According to sources, Goyal emphasised the need for the

developed world to show its commitment towards climate change by putting money in climate finance.”

Business Standard, 21 April 2016

“In an attempt to raise resources for India’s ambitious green energy programme, state-run firms, such as NTPC Ltd, Neyveli Lignite

Corp. Ltd, Power Finance Corp. Ltd (PFC), Rural Electrification Corp. Ltd (REC) and PTC India Ltd, plan to issue masala bonds to

raise $1 billion, according to a government statement released on Wednesday.”

VCCIRCLE, 20 April 2016

27

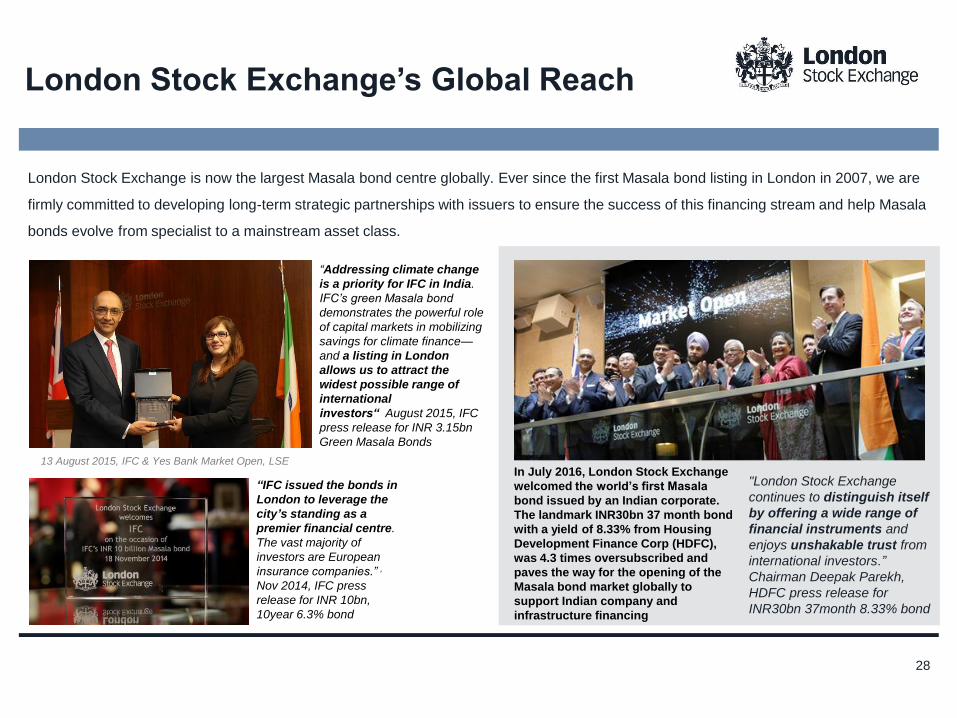

London Stock Exchange is now the largest Masala bond centre globally. Ever since the first Masala bond listing in London in 2007, we are

firmly committed to developing long-term strategic partnerships with issuers to ensure the success of this financing stream and help Masala

bonds evolve from specialist to a mainstream asset class.

“IFC issued the bonds in

London to leverage the

city’s standing as a

premier financial centre.

The vast majority of

investors are European

insurance companies.” ,

Nov 2014, IFC press

release for INR 10bn,

10year 6.3% bond

“Addressing climate change

is a priority for IFC in India.

IFC’s green Masala bond

demonstrates the powerful role

of capital markets in mobilizing

savings for climate finance—

and a listing in London

allows us to attract the

widest possible range of

international

investors“ August 2015, IFC

press release for INR 3.15bn

Green Masala Bonds

13 August 2015, IFC & Yes Bank Market Open, LSE

London Stock Exchange’s Global Reach

In July 2016, London Stock Exchange

welcomed the world’s first Masala

bond issued by an Indian corporate.

The landmark INR30bn 37 month bond

with a yield of 8.33% from Housing

Development Finance Corp (HDFC),

was 4.3 times oversubscribed and

paves the way for the opening of the

Masala bond market globally to

support Indian company and

infrastructure financing

"London Stock Exchange

continues to distinguish itself

by offering a wide range of

financial instruments and

enjoys unshakable trust from

international investors.”

Chairman Deepak Parekh,

HDFC press release for

INR30bn 37month 8.33% bond

28

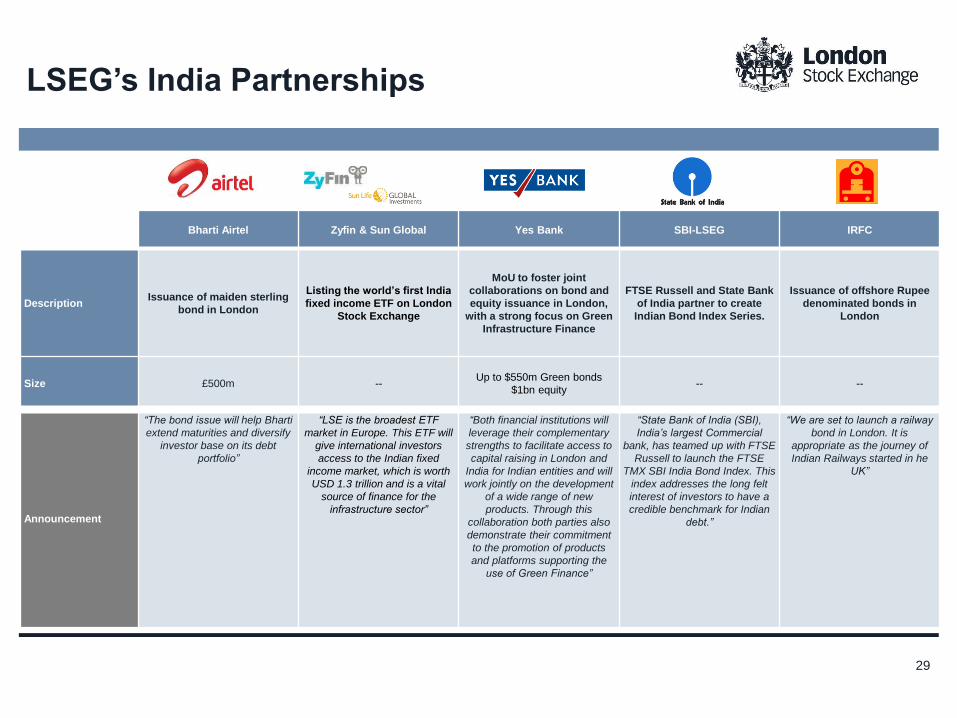

Bharti Airtel Zyfin & Sun Global Yes Bank SBI-LSEG IRFC

Description Issuance of maiden sterling

bond in London

Listing the world’s first India

fixed income ETF on London

Stock Exchange

MoU to foster joint

collaborations on bond and

equity issuance in London,

with a strong focus on Green

Infrastructure Finance

FTSE Russell and State Bank

of India partner to create

Indian Bond Index Series.

Issuance of offshore Rupee

denominated bonds in

London

Size £500m -- Up to $550m Green bonds

$1bn equity -- --

Announcement

“The bond issue will help Bharti

extend maturities and diversify

investor base on its debt

portfolio”

“LSE is the broadest ETF

market in Europe. This ETF will

give international investors

access to the Indian fixed

income market, which is worth

USD 1.3 trillion and is a vital

source of finance for the

infrastructure sector”

“Both financial institutions will

leverage their complementary

strengths to facilitate access to

capital raising in London and

India for Indian entities and will

work jointly on the development

of a wide range of new

products. Through this

collaboration both parties also

demonstrate their commitment

to the promotion of products

and platforms supporting the

use of Green Finance”

“State Bank of India (SBI),

India’s largest Commercial

bank, has teamed up with FTSE

Russell to launch the FTSE

TMX SBI India Bond Index. This

index addresses the long felt

interest of investors to have a

credible benchmark for Indian

debt.”

“We are set to launch a railway

bond in London. It is

appropriate as the journey of

Indian Railways started in he

UK”

LSEG’s India Partnerships

29

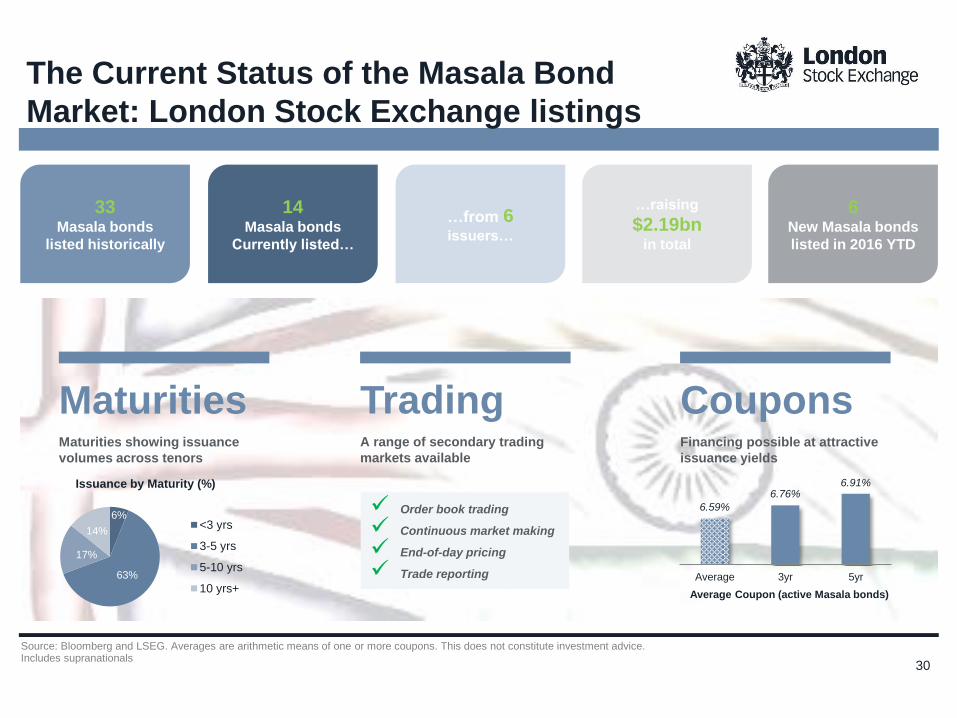

The Current Status of the Masala Bond

Market: London Stock Exchange listings

Source: Bloomberg and LSEG. Averages are arithmetic means of one or more coupons. This does not constitute investment advice. Includes supranationals

…raising

$2.19bn in total

…from 6 issuers…

33 Masala bonds

listed historically

14 Masala bonds

Currently listed…

Maturities Maturities showing issuance

volumes across tenors

Trading A range of secondary trading

markets available

Coupons Financing possible at attractive

issuance yields

Order book trading

Continuous market making

End-of-day pricing

Trade reporting

6.59%

6.76% 6.91%

Average 3yr 5yr

Average Coupon (active Masala bonds)

30

6 New Masala bonds

listed in 2016 YTD

6%

63%

17%

14%

Issuance by Maturity (%)

<3 yrs

3-5 yrs

5-10 yrs

10 yrs+

Masala Bond Case Studies

31

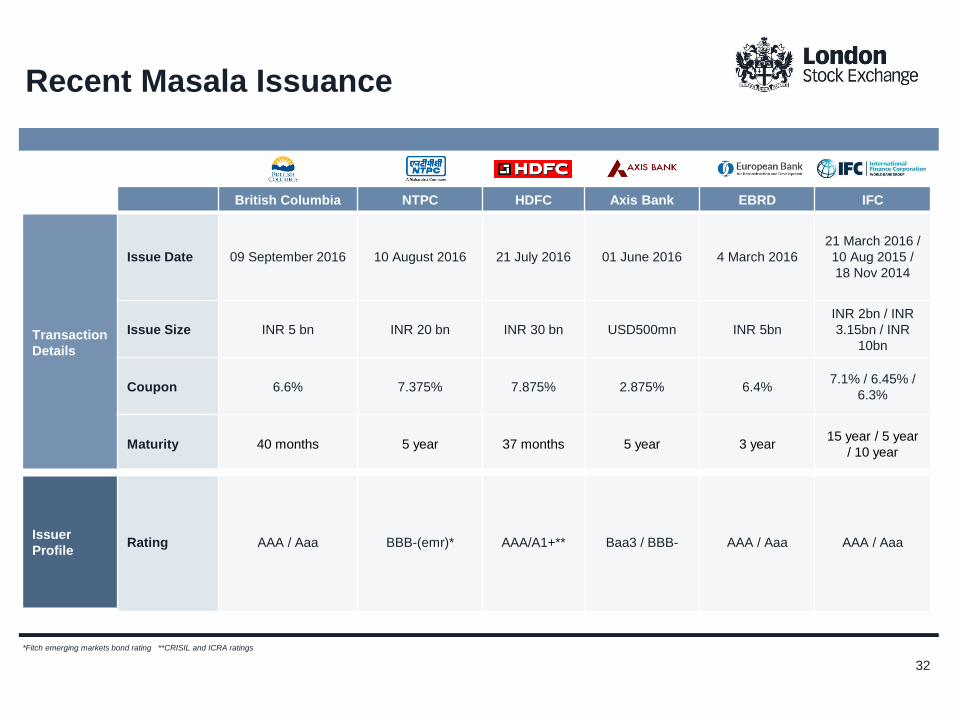

British Columbia NTPC HDFC Axis Bank EBRD IFC

Transaction

Details

Issue Date 09 September 2016 10 August 2016 21 July 2016 01 June 2016 4 March 2016

21 March 2016 /

10 Aug 2015 /

18 Nov 2014

Issue Size INR 5 bn INR 20 bn INR 30 bn USD500mn INR 5bn

INR 2bn / INR

3.15bn / INR

10bn

Coupon 6.6% 7.375% 7.875% 2.875% 6.4% 7.1% / 6.45% /

6.3%

Maturity 40 months 5 year 37 months 5 year 3 year 15 year / 5 year

/ 10 year

Issuer

Profile Rating AAA / Aaa BBB-(emr)* AAA/A1+** Baa3 / BBB- AAA / Aaa AAA / Aaa

Recent Masala Issuance

*Fitch emerging markets bond rating **CRISIL and ICRA ratings

32

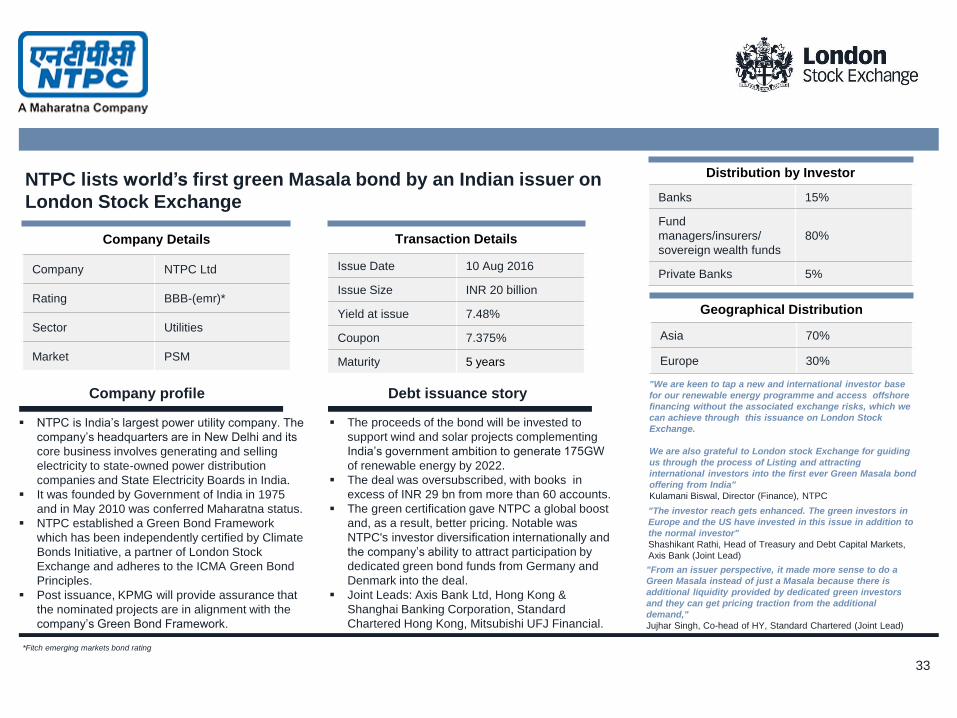

Company Details

Company NTPC Ltd

Rating BBB-(emr)*

Sector Utilities

Market PSM

Transaction Details

Issue Date 10 Aug 2016

Issue Size INR 20 billion

Yield at issue 7.48%

Coupon 7.375%

Maturity 5 years

Company profile

NTPC is India’s largest power utility company. The

company’s headquarters are in New Delhi and its

core business involves generating and selling

electricity to state-owned power distribution

companies and State Electricity Boards in India.

It was founded by Government of India in 1975

and in May 2010 was conferred Maharatna status.

NTPC established a Green Bond Framework

which has been independently certified by Climate

Bonds Initiative, a partner of London Stock

Exchange and adheres to the ICMA Green Bond

Principles.

Post issuance, KPMG will provide assurance that

the nominated projects are in alignment with the

company’s Green Bond Framework.

Debt issuance story

The proceeds of the bond will be invested to

support wind and solar projects complementing

India’s government ambition to generate 175GW

of renewable energy by 2022.

The deal was oversubscribed, with books in

excess of INR 29 bn from more than 60 accounts.

The green certification gave NTPC a global boost

and, as a result, better pricing. Notable was

NTPC's investor diversification internationally and

the company’s ability to attract participation by

dedicated green bond funds from Germany and

Denmark into the deal.

Joint Leads: Axis Bank Ltd, Hong Kong &

Shanghai Banking Corporation, Standard

Chartered Hong Kong, Mitsubishi UFJ Financial.

Geographical Distribution

Asia 70%

Europe 30%

Distribution by Investor

Banks 15%

Fund

managers/insurers/

sovereign wealth funds

80%

Private Banks 5%

*Fitch emerging markets bond rating

NTPC lists world’s first green Masala bond by an Indian issuer on

London Stock Exchange

"The investor reach gets enhanced. The green investors in

Europe and the US have invested in this issue in addition to

the normal investor"

Shashikant Rathi, Head of Treasury and Debt Capital Markets,

Axis Bank (Joint Lead)

"From an issuer perspective, it made more sense to do a

Green Masala instead of just a Masala because there is

additional liquidity provided by dedicated green investors

and they can get pricing traction from the additional

demand,"

Jujhar Singh, Co-head of HY, Standard Chartered (Joint Lead)

"We are keen to tap a new and international investor base

for our renewable energy programme and access offshore

financing without the associated exchange risks, which we

can achieve through this issuance on London Stock

Exchange.

We are also grateful to London stock Exchange for guiding

us through the process of Listing and attracting

international investors into the first ever Green Masala bond

offering from India"

Kulamani Biswal, Director (Finance), NTPC

33

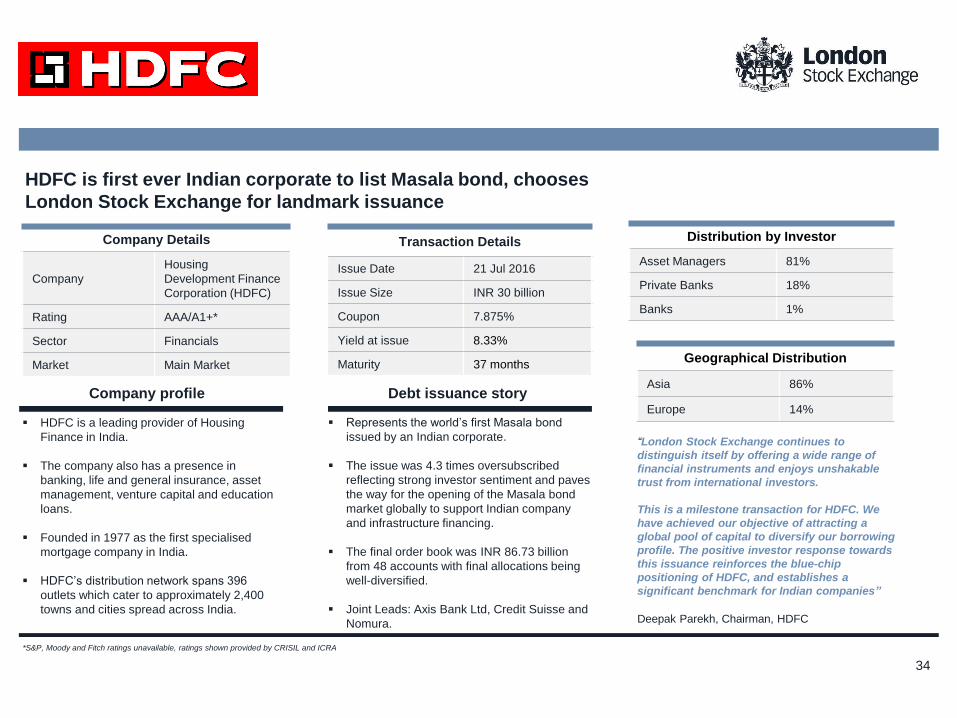

Company Details

Company

Housing

Development Finance

Corporation (HDFC)

Rating AAA/A1+*

Sector Financials

Market Main Market

Transaction Details

Issue Date 21 Jul 2016

Issue Size INR 30 billion

Coupon 7.875%

Yield at issue 8.33%

Maturity 37 months

Company profile

HDFC is a leading provider of Housing

Finance in India.

The company also has a presence in

banking, life and general insurance, asset

management, venture capital and education

loans.

Founded in 1977 as the first specialised

mortgage company in India.

HDFC’s distribution network spans 396

outlets which cater to approximately 2,400

towns and cities spread across India.

Debt issuance story

Represents the world’s first Masala bond

issued by an Indian corporate.

The issue was 4.3 times oversubscribed

reflecting strong investor sentiment and paves

the way for the opening of the Masala bond

market globally to support Indian company

and infrastructure financing.

The final order book was INR 86.73 billion

from 48 accounts with final allocations being

well-diversified.

Joint Leads: Axis Bank Ltd, Credit Suisse and

Nomura.

HDFC is first ever Indian corporate to list Masala bond, chooses

London Stock Exchange for landmark issuance

“London Stock Exchange continues to

distinguish itself by offering a wide range of

financial instruments and enjoys unshakable

trust from international investors.

This is a milestone transaction for HDFC. We

have achieved our objective of attracting a

global pool of capital to diversify our borrowing

profile. The positive investor response towards

this issuance reinforces the blue-chip

positioning of HDFC, and establishes a

significant benchmark for Indian companies”

Deepak Parekh, Chairman, HDFC

*S&P, Moody and Fitch ratings unavailable, ratings shown provided by CRISIL and ICRA

Geographical Distribution

Asia 86%

Europe 14%

Distribution by Investor

Asset Managers 81%

Private Banks 18%

Banks 1%

34

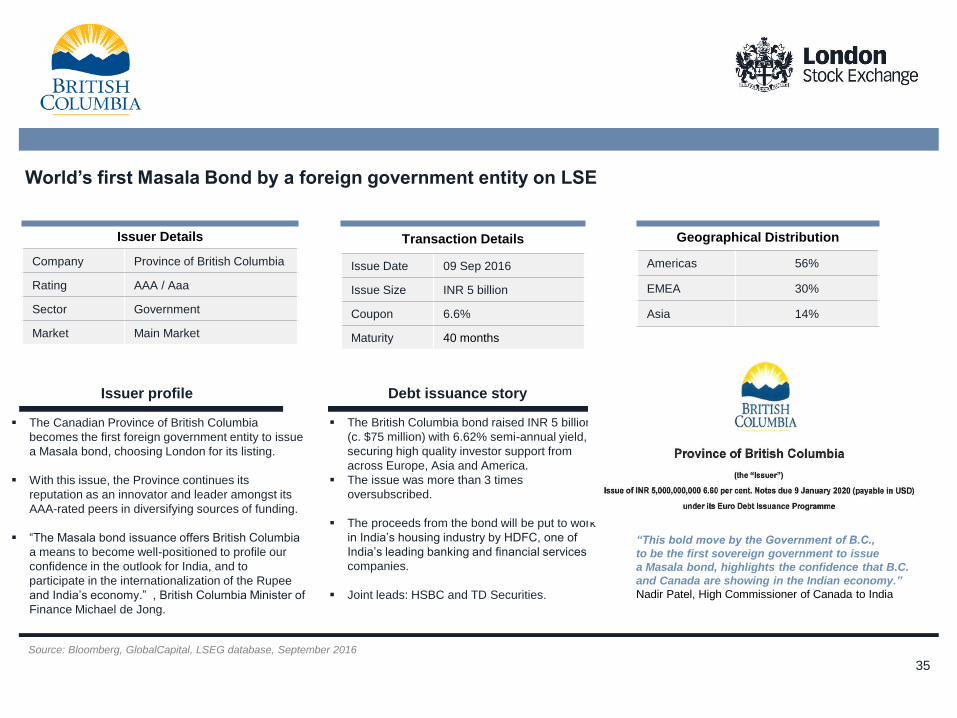

Issuer Details

Company Province of British Columbia

Rating AAA / Aaa

Sector Government

Market Main Market

Transaction Details

Issue Date 09 Sep 2016

Issue Size INR 5 billion

Coupon 6.6%

Maturity 40 months

Issuer profile

The Canadian Province of British Columbia

becomes the first foreign government entity to issue

a Masala bond, choosing London for its listing.

With this issue, the Province continues its

reputation as an innovator and leader amongst its

AAA-rated peers in diversifying sources of funding.

“The Masala bond issuance offers British Columbia

a means to become well-positioned to profile our

confidence in the outlook for India, and to

participate in the internationalization of the Rupee

and India’s economy.” , British Columbia Minister of

Finance Michael de Jong.

Debt issuance story

The British Columbia bond raised INR 5 billion

(c. $75 million) with 6.62% semi-annual yield,

securing high quality investor support from

across Europe, Asia and America.

The issue was more than 3 times

oversubscribed.

The proceeds from the bond will be put to work

in India’s housing industry by HDFC, one of

India’s leading banking and financial services

companies.

Joint leads: HSBC and TD Securities.

Geographical Distribution

Americas 56%

EMEA 30%

Asia 14%

World’s first Masala Bond by a foreign government entity on LSE

“This bold move by the Government of B.C.,

to be the first sovereign government to issue

a Masala bond, highlights the confidence that B.C.

and Canada are showing in the Indian economy.”

Nadir Patel, High Commissioner of Canada to India

Source: Bloomberg, GlobalCapital, LSEG database, September 2016

35

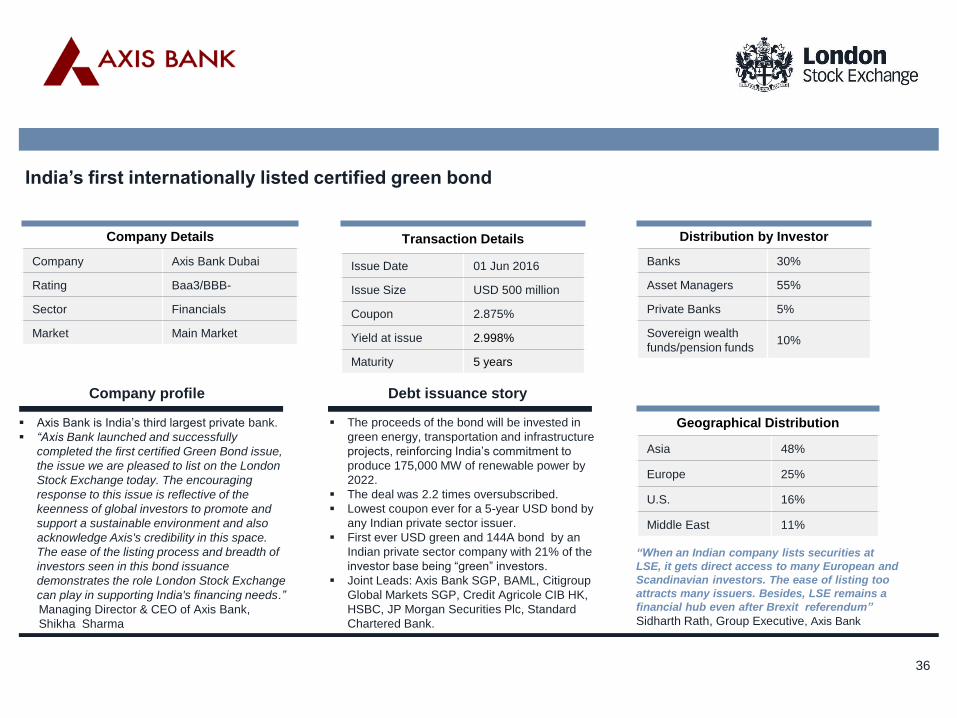

Company Details

Company Axis Bank Dubai

Rating Baa3/BBB-

Sector Financials

Market Main Market

Transaction Details

Issue Date 01 Jun 2016

Issue Size USD 500 million

Coupon 2.875%

Yield at issue 2.998%

Maturity 5 years

Company profile

Axis Bank is India’s third largest private bank.

“Axis Bank launched and successfully

completed the first certified Green Bond issue,

the issue we are pleased to list on the London

Stock Exchange today. The encouraging

response to this issue is reflective of the

keenness of global investors to promote and

support a sustainable environment and also

acknowledge Axis's credibility in this space.

The ease of the listing process and breadth of

investors seen in this bond issuance

demonstrates the role London Stock Exchange

can play in supporting India's financing needs.”

Managing Director & CEO of Axis Bank,

Shikha Sharma

Debt issuance story

The proceeds of the bond will be invested in

green energy, transportation and infrastructure

projects, reinforcing India’s commitment to

produce 175,000 MW of renewable power by

2022.

The deal was 2.2 times oversubscribed.

Lowest coupon ever for a 5-year USD bond by

any Indian private sector issuer.

First ever USD green and 144A bond by an

Indian private sector company with 21% of the

investor base being “green” investors.

Joint Leads: Axis Bank SGP, BAML, Citigroup

Global Markets SGP, Credit Agricole CIB HK,

HSBC, JP Morgan Securities Plc, Standard

Chartered Bank.

Geographical Distribution

Asia 48%

Europe 25%

U.S. 16%

Middle East 11%

Distribution by Investor

Banks 30%

Asset Managers 55%

Private Banks 5%

Sovereign wealth

funds/pension funds 10%

India’s first internationally listed certified green bond

“When an Indian company lists securities at

LSE, it gets direct access to many European and

Scandinavian investors. The ease of listing too

attracts many issuers. Besides, LSE remains a

financial hub even after Brexit referendum”

Sidharth Rath, Group Executive, Axis Bank

36

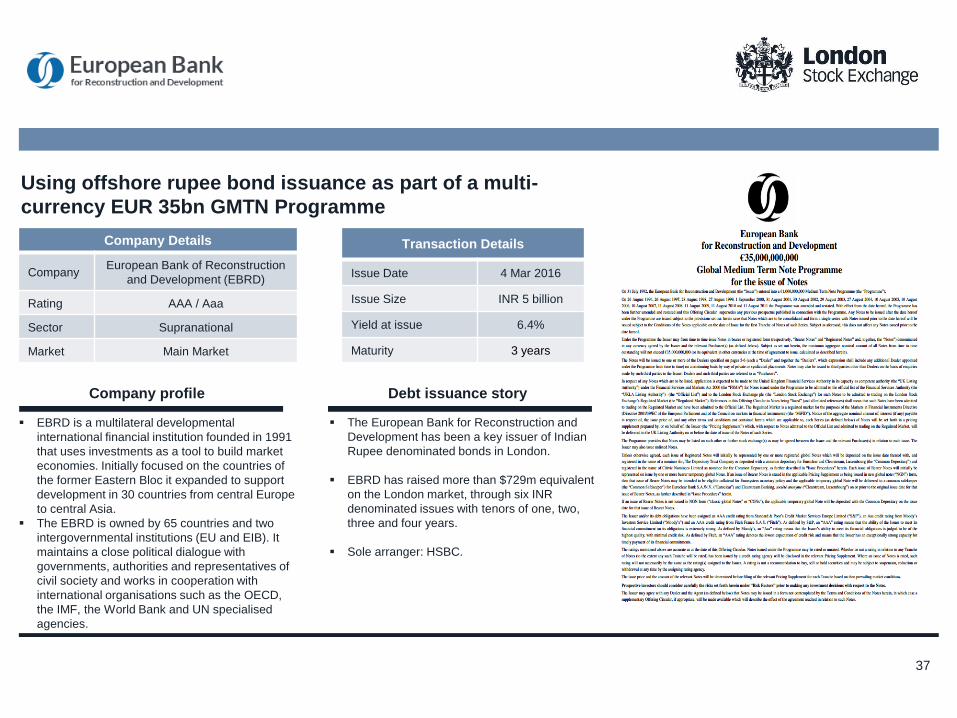

Company Details

Company European Bank of Reconstruction

and Development (EBRD)

Rating AAA / Aaa

Sector Supranational

Market Main Market

Transaction Details

Issue Date 4 Mar 2016

Issue Size INR 5 billion

Yield at issue 6.4%

Maturity 3 years

Company profile

EBRD is a multilateral developmental

international financial institution founded in 1991

that uses investments as a tool to build market

economies. Initially focused on the countries of

the former Eastern Bloc it expanded to support

development in 30 countries from central Europe

to central Asia.

The EBRD is owned by 65 countries and two

intergovernmental institutions (EU and EIB). It

maintains a close political dialogue with

governments, authorities and representatives of

civil society and works in cooperation with

international organisations such as the OECD,

the IMF, the World Bank and UN specialised

agencies.

Debt issuance story

The European Bank for Reconstruction and

Development has been a key issuer of Indian

Rupee denominated bonds in London.

EBRD has raised more than $729m equivalent

on the London market, through six INR

denominated issues with tenors of one, two,

three and four years.

Sole arranger: HSBC.

Using offshore rupee bond issuance as part of a multi-

currency EUR 35bn GMTN Programme

37

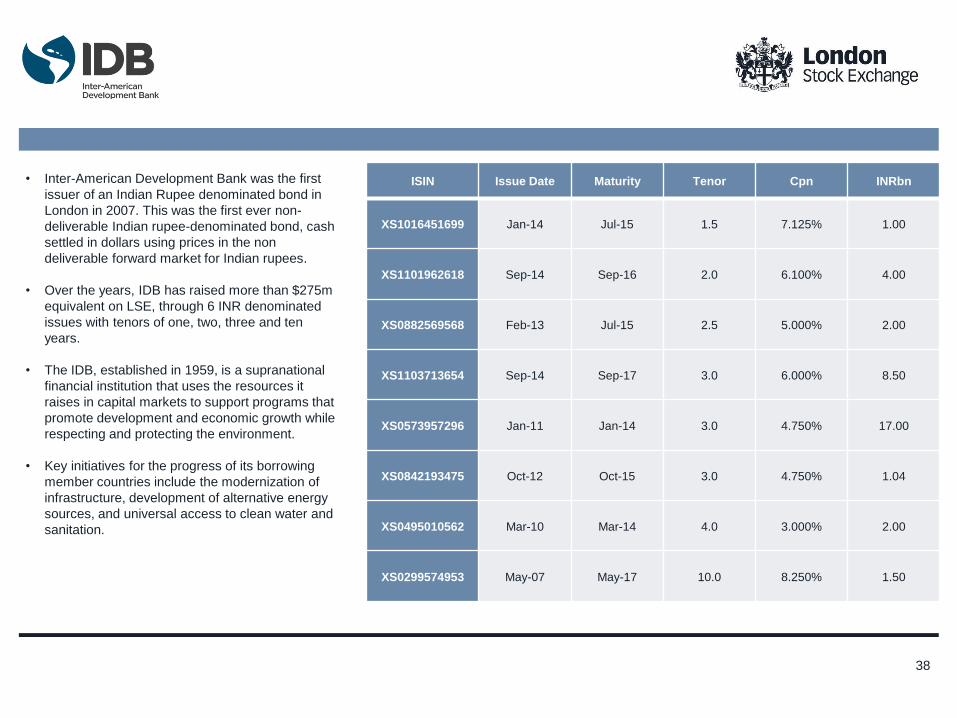

• Inter-American Development Bank was the first

issuer of an Indian Rupee denominated bond in

London in 2007. This was the first ever non-

deliverable Indian rupee-denominated bond, cash

settled in dollars using prices in the non

deliverable forward market for Indian rupees.

• Over the years, IDB has raised more than $275m

equivalent on LSE, through 6 INR denominated

issues with tenors of one, two, three and ten

years.

• The IDB, established in 1959, is a supranational

financial institution that uses the resources it

raises in capital markets to support programs that

promote development and economic growth while

respecting and protecting the environment.

• Key initiatives for the progress of its borrowing

member countries include the modernization of

infrastructure, development of alternative energy

sources, and universal access to clean water and

sanitation.

ISIN Issue Date Maturity Tenor Cpn INRbn

XS1016451699 Jan-14 Jul-15 1.5 7.125% 1.00

XS1101962618 Sep-14 Sep-16 2.0 6.100% 4.00

XS0882569568 Feb-13 Jul-15 2.5 5.000% 2.00

XS1103713654 Sep-14 Sep-17 3.0 6.000% 8.50

XS0573957296 Jan-11 Jan-14 3.0 4.750% 17.00

XS0842193475 Oct-12 Oct-15 3.0 4.750% 1.04

XS0495010562 Mar-10 Mar-14 4.0 3.000% 2.00

XS0299574953 May-07 May-17 10.0 8.250% 1.50

38

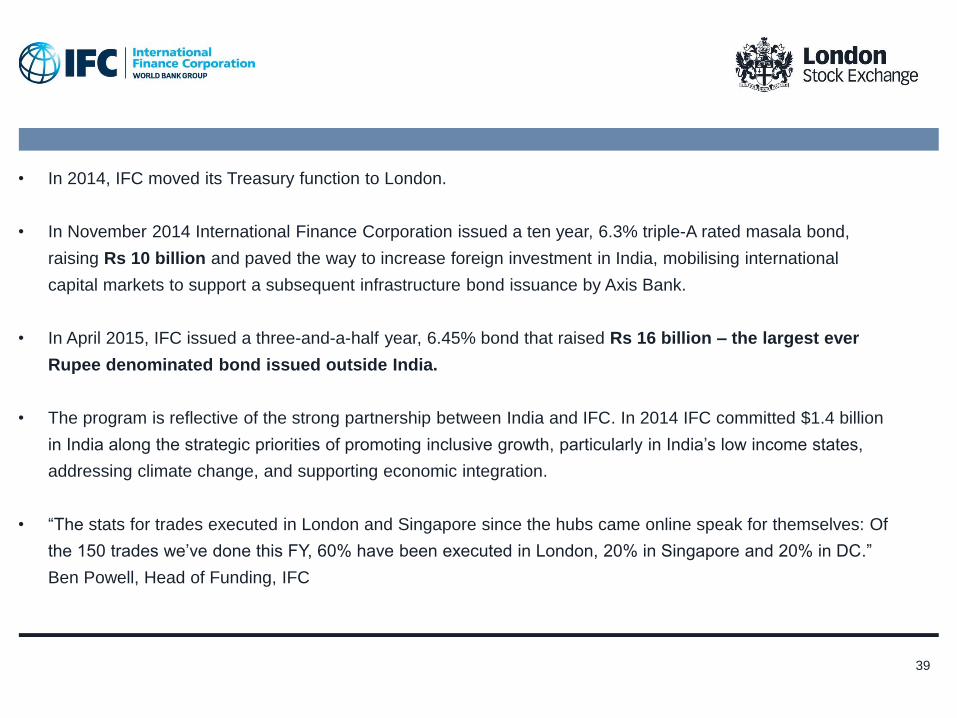

• In 2014, IFC moved its Treasury function to London.

• In November 2014 International Finance Corporation issued a ten year, 6.3% triple-A rated masala bond,

raising Rs 10 billion and paved the way to increase foreign investment in India, mobilising international

capital markets to support a subsequent infrastructure bond issuance by Axis Bank.

• In April 2015, IFC issued a three-and-a-half year, 6.45% bond that raised Rs 16 billion – the largest ever

Rupee denominated bond issued outside India.

• The program is reflective of the strong partnership between India and IFC. In 2014 IFC committed $1.4 billion

in India along the strategic priorities of promoting inclusive growth, particularly in India’s low income states,

addressing climate change, and supporting economic integration.

• “The stats for trades executed in London and Singapore since the hubs came online speak for themselves: Of

the 150 trades we’ve done this FY, 60% have been executed in London, 20% in Singapore and 20% in DC.”

Ben Powell, Head of Funding, IFC

39

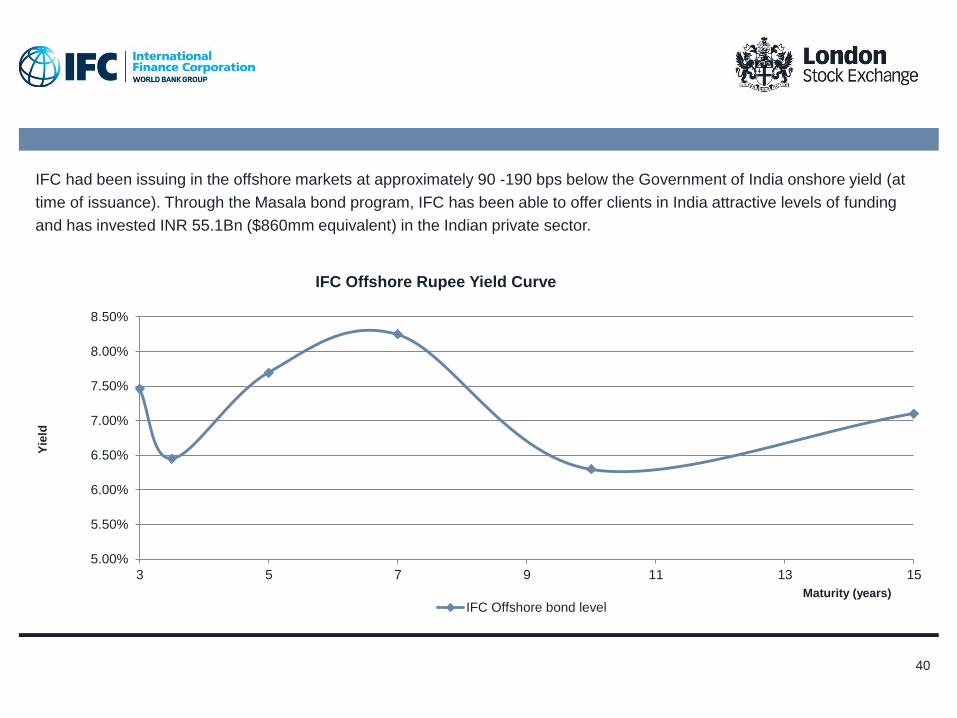

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

3 5 7 9 11 13 15

Yie

ld

Maturity (years)

IFC Offshore Rupee Yield Curve

IFC Offshore bond level

IFC had been issuing in the offshore markets at approximately 90 -190 bps below the Government of India onshore yield (at

time of issuance). Through the Masala bond program, IFC has been able to offer clients in India attractive levels of funding

and has invested INR 55.1Bn ($860mm equivalent) in the Indian private sector.

40

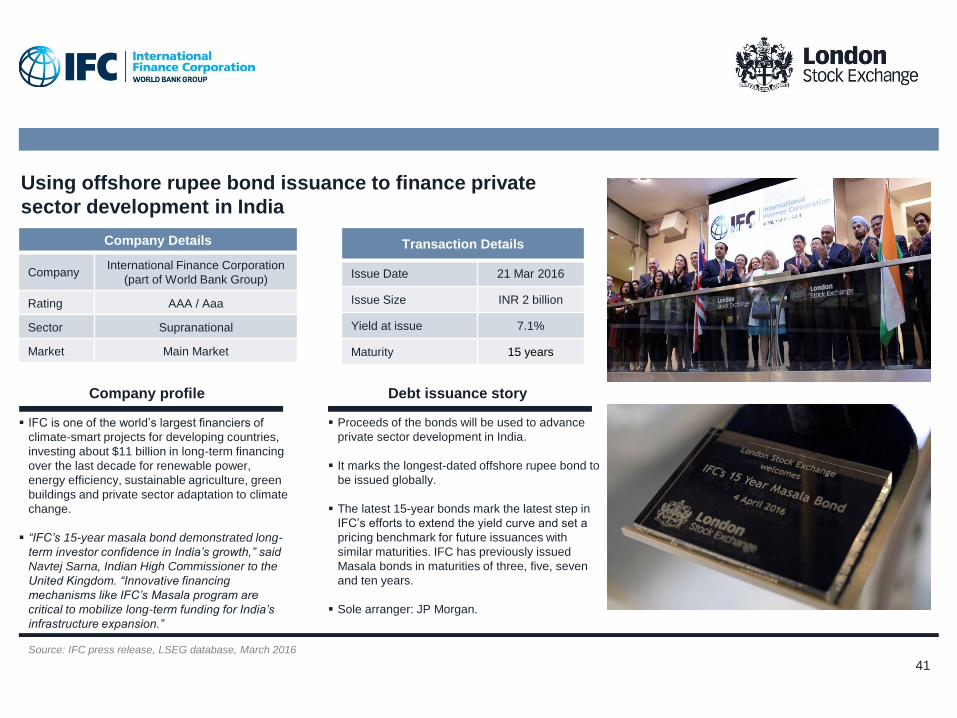

Company Details

Company International Finance Corporation

(part of World Bank Group)

Rating AAA / Aaa

Sector Supranational

Market Main Market

Transaction Details

Issue Date 21 Mar 2016

Issue Size INR 2 billion

Yield at issue 7.1%

Maturity 15 years

Company profile

IFC is one of the world’s largest financiers of

climate-smart projects for developing countries,

investing about $11 billion in long-term financing

over the last decade for renewable power,

energy efficiency, sustainable agriculture, green

buildings and private sector adaptation to climate

change.

“IFC’s 15-year masala bond demonstrated long-

term investor confidence in India’s growth,” said

Navtej Sarna, Indian High Commissioner to the

United Kingdom. “Innovative financing

mechanisms like IFC’s Masala program are

critical to mobilize long-term funding for India’s

infrastructure expansion.”

Debt issuance story

Proceeds of the bonds will be used to advance

private sector development in India.

It marks the longest-dated offshore rupee bond to

be issued globally.

The latest 15-year bonds mark the latest step in

IFC’s efforts to extend the yield curve and set a

pricing benchmark for future issuances with

similar maturities. IFC has previously issued

Masala bonds in maturities of three, five, seven

and ten years.

Sole arranger: JP Morgan.

Using offshore rupee bond issuance to finance private

sector development in India

Source: IFC press release, LSEG database, March 2016

41

Company Details

Company International Finance Corporation

(part of World Bank Group)

Rating AAA/Aaa

Sector Supranational

Market Main Market

Transaction Details

Issue Date 10 Aug 2015

Issue Size INR 3.15 billion

Yield at issue 6.45%

Maturity 5 years

Company profile

IFC is one of the world’s largest financiers of

climate-smart projects for developing countries,

investing about $11 billion in long-term financing

over the last decade for renewable power,

energy efficiency, sustainable agriculture, green

buildings and private sector adaptation to climate

change.

“Addressing climate change is a priority for IFC in

India. IFC’s green Masala bond demonstrates

the powerful role of capital markets in mobilizing

savings for climate finance—and a listing in

London allows us to attract the widest possible

range of international investors. Adding the rupee

as a new green bond currency also supports our

goals to strengthen this important asset class.”

Debt issuance story

Proceeds from the offering used to finance a

green bond issued by Yes Bank, one of India’s

largest commercial banks. Yes Bank invested the

proceeds of its bond in renewable energy and

energy efficiency projects, mainly in the solar and

wind sectors.

Under its $3 billion offshore rupee Masala bond

program, IFC has issued bonds worth over 103

billion rupees ($1.66 billion) in a range of tenors,

building a triple-A yield curve and attracting new

investors to the London offshore rupee market.

Sole arranger: JP Morgan.

Using Green offshore rupee bond issuance to finance

Indian infrastructure

Source: IFC press release, LSEG database, August 2015

42

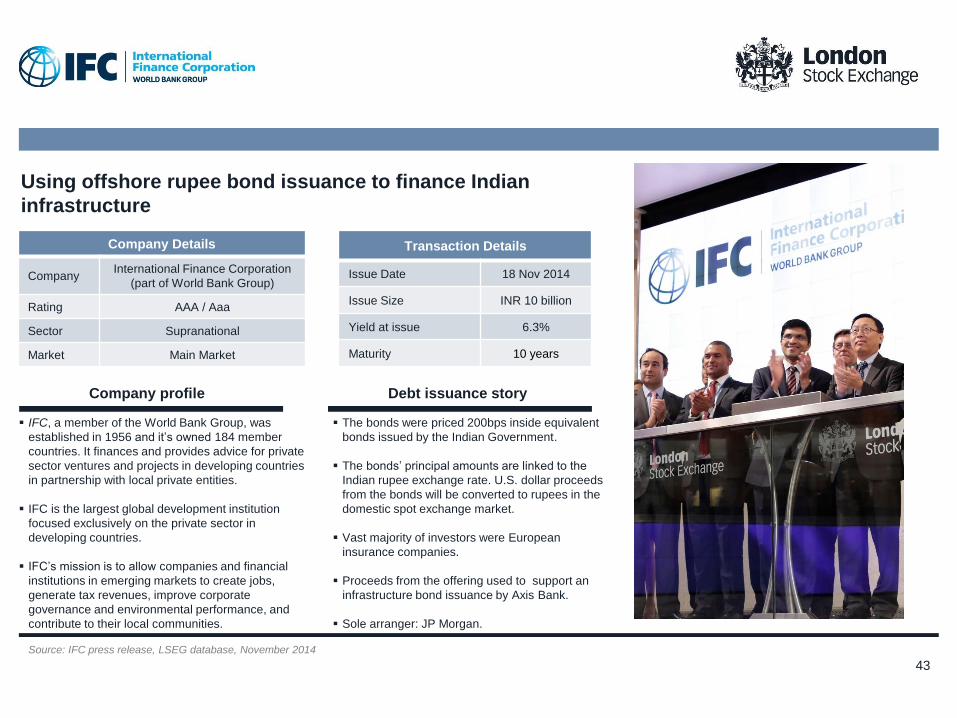

Company Details

Company International Finance Corporation

(part of World Bank Group)

Rating AAA / Aaa

Sector Supranational

Market Main Market

Transaction Details

Issue Date 18 Nov 2014

Issue Size INR 10 billion

Yield at issue 6.3%

Maturity 10 years

Company profile

IFC, a member of the World Bank Group, was

established in 1956 and it’s owned 184 member

countries. It finances and provides advice for private

sector ventures and projects in developing countries

in partnership with local private entities.

IFC is the largest global development institution

focused exclusively on the private sector in

developing countries.

IFC’s mission is to allow companies and financial

institutions in emerging markets to create jobs,

generate tax revenues, improve corporate

governance and environmental performance, and

contribute to their local communities.

Debt issuance story

The bonds were priced 200bps inside equivalent

bonds issued by the Indian Government.

The bonds’ principal amounts are linked to the

Indian rupee exchange rate. U.S. dollar proceeds

from the bonds will be converted to rupees in the

domestic spot exchange market.

Vast majority of investors were European

insurance companies.

Proceeds from the offering used to support an

infrastructure bond issuance by Axis Bank.

Sole arranger: JP Morgan.

Source: IFC press release, LSEG database, November 2014

Using offshore rupee bond issuance to finance Indian

infrastructure

43

Appendix

(general slides)

44

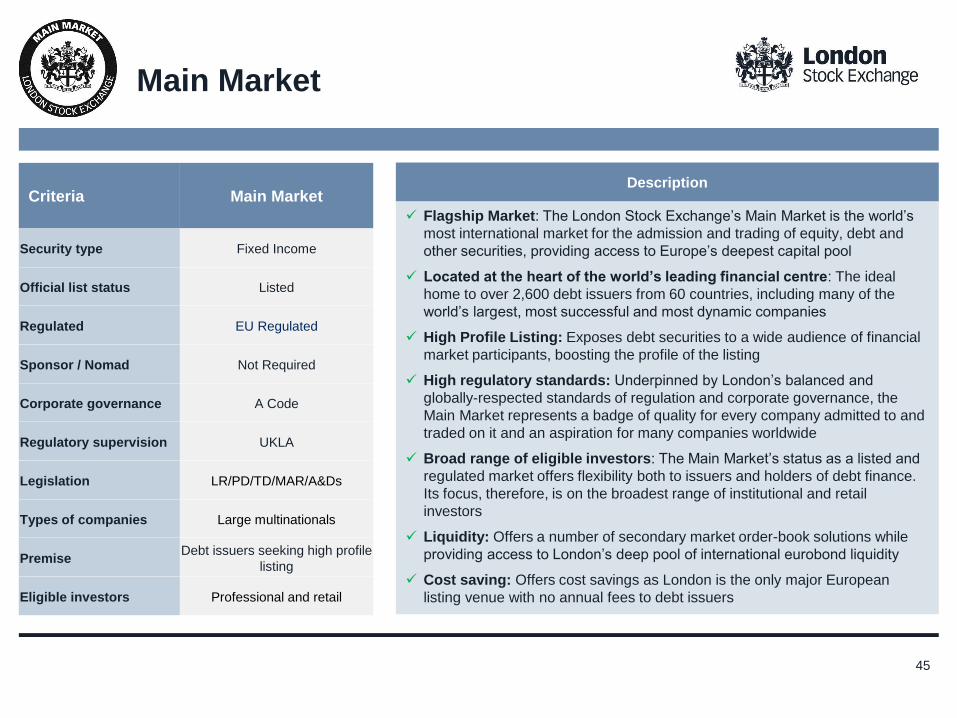

Criteria Main Market

Security type Fixed Income

Official list status Listed

Regulated EU Regulated

Sponsor / Nomad Not Required

Corporate governance A Code

Regulatory supervision UKLA

Legislation LR/PD/TD/MAR/A&Ds

Types of companies Large multinationals

Premise Debt issuers seeking high profile

listing

Eligible investors Professional and retail

Main Market

Description

Flagship Market: The London Stock Exchange’s Main Market is the world’s

most international market for the admission and trading of equity, debt and

other securities, providing access to Europe’s deepest capital pool

Located at the heart of the world’s leading financial centre: The ideal

home to over 2,600 debt issuers from 60 countries, including many of the

world’s largest, most successful and most dynamic companies

High Profile Listing: Exposes debt securities to a wide audience of financial

market participants, boosting the profile of the listing

High regulatory standards: Underpinned by London’s balanced and

globally-respected standards of regulation and corporate governance, the

Main Market represents a badge of quality for every company admitted to and

traded on it and an aspiration for many companies worldwide

Broad range of eligible investors: The Main Market’s status as a listed and

regulated market offers flexibility both to issuers and holders of debt finance.

Its focus, therefore, is on the broadest range of institutional and retail

investors

Liquidity: Offers a number of secondary market order-book solutions while

providing access to London’s deep pool of international eurobond liquidity

Cost saving: Offers cost savings as London is the only major European

listing venue with no annual fees to debt issuers

45

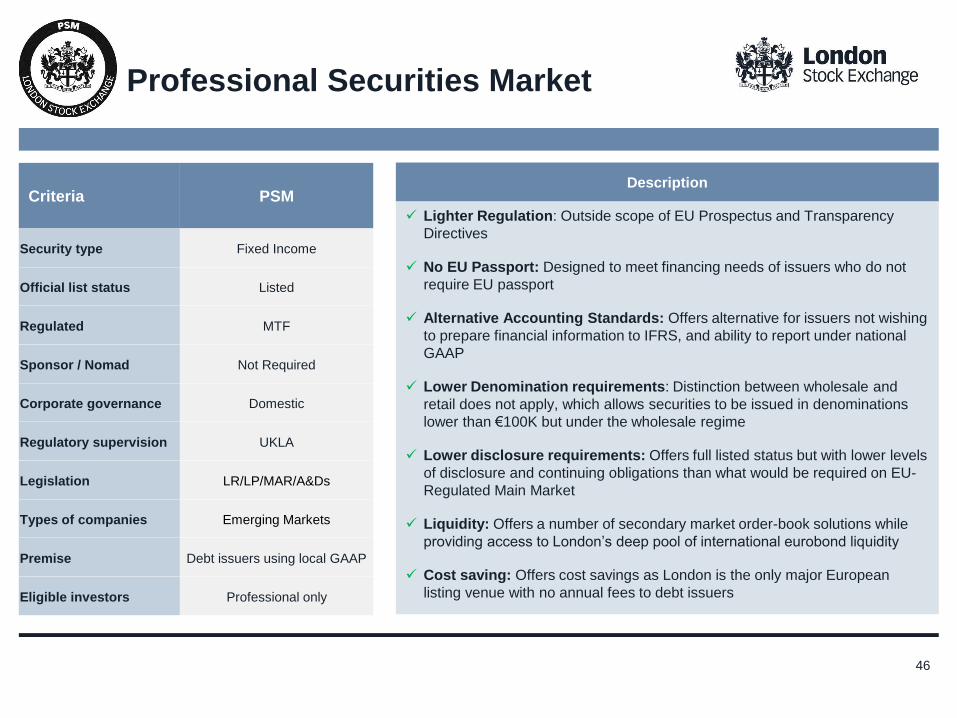

Criteria PSM

Security type Fixed Income

Official list status Listed

Regulated MTF

Sponsor / Nomad Not Required

Corporate governance Domestic

Regulatory supervision UKLA

Legislation LR/LP/MAR/A&Ds

Types of companies Emerging Markets

Premise Debt issuers using local GAAP

Eligible investors Professional only

Description

Lighter Regulation: Outside scope of EU Prospectus and Transparency

Directives

No EU Passport: Designed to meet financing needs of issuers who do not

require EU passport

Alternative Accounting Standards: Offers alternative for issuers not wishing

to prepare financial information to IFRS, and ability to report under national

GAAP

Lower Denomination requirements: Distinction between wholesale and

retail does not apply, which allows securities to be issued in denominations

lower than €100K but under the wholesale regime

Lower disclosure requirements: Offers full listed status but with lower levels

of disclosure and continuing obligations than what would be required on EU-

Regulated Main Market

Liquidity: Offers a number of secondary market order-book solutions while

providing access to London’s deep pool of international eurobond liquidity

Cost saving: Offers cost savings as London is the only major European

listing venue with no annual fees to debt issuers

Professional Securities Market

46

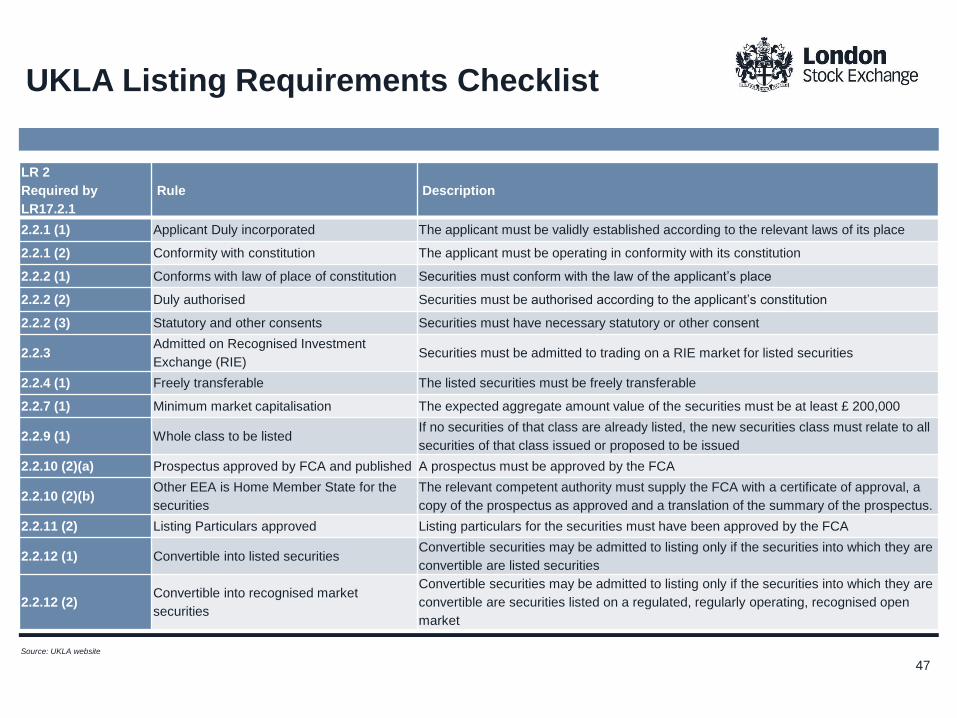

UKLA Listing Requirements Checklist

Source: UKLA website

LR 2

Required by

LR17.2.1

Rule Description

2.2.1 (1) Applicant Duly incorporated The applicant must be validly established according to the relevant laws of its place

2.2.1 (2) Conformity with constitution The applicant must be operating in conformity with its constitution

2.2.2 (1) Conforms with law of place of constitution Securities must conform with the law of the applicant’s place

2.2.2 (2) Duly authorised Securities must be authorised according to the applicant’s constitution

2.2.2 (3) Statutory and other consents Securities must have necessary statutory or other consent

2.2.3 Admitted on Recognised Investment

Exchange (RIE) Securities must be admitted to trading on a RIE market for listed securities

2.2.4 (1) Freely transferable The listed securities must be freely transferable

2.2.7 (1) Minimum market capitalisation The expected aggregate amount value of the securities must be at least £ 200,000

2.2.9 (1) Whole class to be listed If no securities of that class are already listed, the new securities class must relate to all

securities of that class issued or proposed to be issued

2.2.10 (2)(a) Prospectus approved by FCA and published A prospectus must be approved by the FCA

2.2.10 (2)(b) Other EEA is Home Member State for the

securities

The relevant competent authority must supply the FCA with a certificate of approval, a

copy of the prospectus as approved and a translation of the summary of the prospectus.

2.2.11 (2) Listing Particulars approved Listing particulars for the securities must have been approved by the FCA

2.2.12 (1) Convertible into listed securities Convertible securities may be admitted to listing only if the securities into which they are

convertible are listed securities

2.2.12 (2) Convertible into recognised market

securities

Convertible securities may be admitted to listing only if the securities into which they are

convertible are securities listed on a regulated, regularly operating, recognised open

market

47

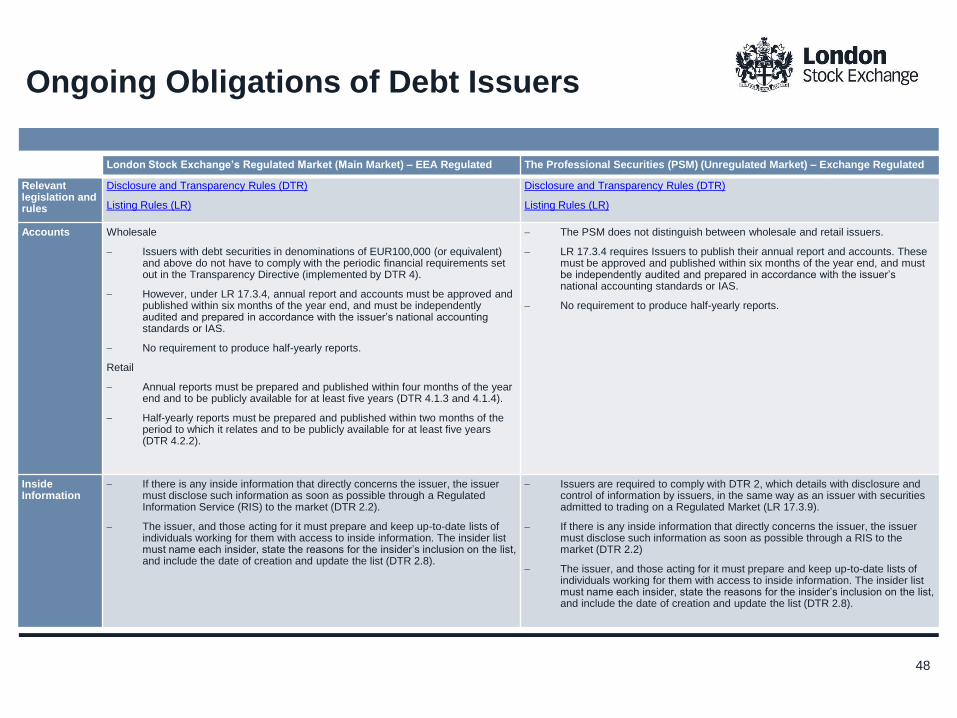

Ongoing Obligations of Debt Issuers

London Stock Exchange’s Regulated Market (Main Market) – EEA Regulated The Professional Securities (PSM) (Unregulated Market) – Exchange Regulated

Relevant legislation and rules

Disclosure and Transparency Rules (DTR)

Listing Rules (LR)

Disclosure and Transparency Rules (DTR)

Listing Rules (LR)

Accounts Wholesale

Issuers with debt securities in denominations of EUR100,000 (or equivalent) and above do not have to comply with the periodic financial requirements set out in the Transparency Directive (implemented by DTR 4).

However, under LR 17.3.4, annual report and accounts must be approved and published within six months of the year end, and must be independently audited and prepared in accordance with the issuer’s national accounting standards or IAS.

No requirement to produce half-yearly reports.

Retail

Annual reports must be prepared and published within four months of the year end and to be publicly available for at least five years (DTR 4.1.3 and 4.1.4).

Half-yearly reports must be prepared and published within two months of the period to which it relates and to be publicly available for at least five years (DTR 4.2.2).

The PSM does not distinguish between wholesale and retail issuers.

LR 17.3.4 requires Issuers to publish their annual report and accounts. These must be approved and published within six months of the year end, and must be independently audited and prepared in accordance with the issuer’s national accounting standards or IAS.

No requirement to produce half-yearly reports.

Inside Information

If there is any inside information that directly concerns the issuer, the issuer must disclose such information as soon as possible through a Regulated Information Service (RIS) to the market (DTR 2.2).

The issuer, and those acting for it must prepare and keep up-to-date lists of individuals working for them with access to inside information. The insider list must name each insider, state the reasons for the insider’s inclusion on the list, and include the date of creation and update the list (DTR 2.8).

Issuers are required to comply with DTR 2, which details with disclosure and control of information by issuers, in the same way as an issuer with securities admitted to trading on a Regulated Market (LR 17.3.9).

If there is any inside information that directly concerns the issuer, the issuer must disclose such information as soon as possible through a RIS to the market (DTR 2.2)

The issuer, and those acting for it must prepare and keep up-to-date lists of individuals working for them with access to inside information. The insider list must name each insider, state the reasons for the insider’s inclusion on the list, and include the date of creation and update the list (DTR 2.8).

48

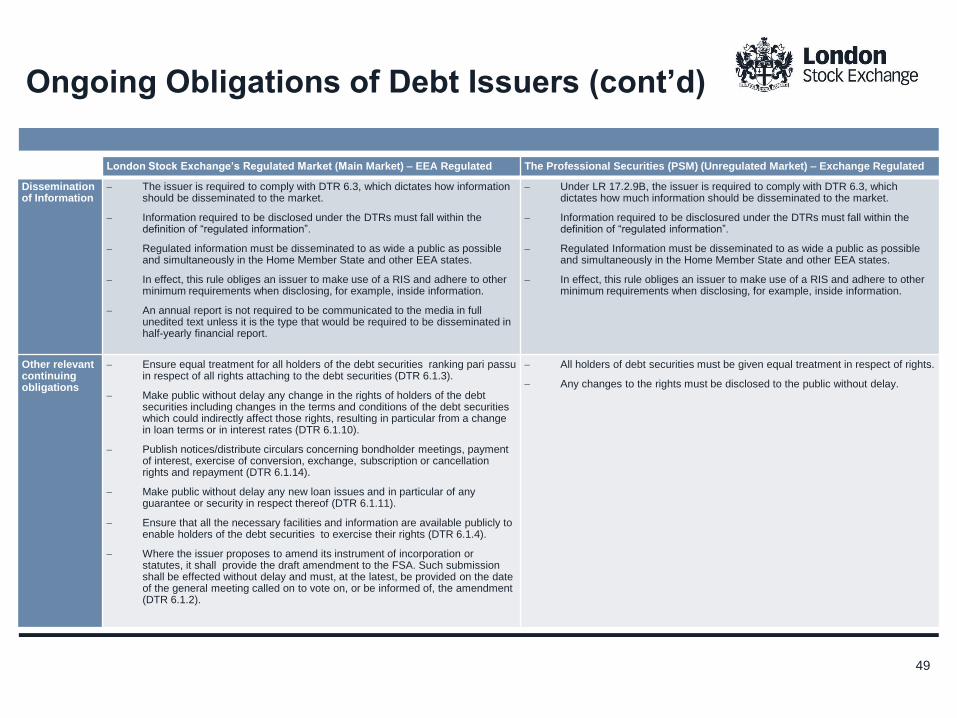

Ongoing Obligations of Debt Issuers (cont’d)

London Stock Exchange’s Regulated Market (Main Market) – EEA Regulated The Professional Securities (PSM) (Unregulated Market) – Exchange Regulated

Dissemination of Information

The issuer is required to comply with DTR 6.3, which dictates how information should be disseminated to the market.

Information required to be disclosed under the DTRs must fall within the definition of “regulated information”.

Regulated information must be disseminated to as wide a public as possible and simultaneously in the Home Member State and other EEA states.

In effect, this rule obliges an issuer to make use of a RIS and adhere to other minimum requirements when disclosing, for example, inside information.

An annual report is not required to be communicated to the media in full unedited text unless it is the type that would be required to be disseminated in half-yearly financial report.

Under LR 17.2.9B, the issuer is required to comply with DTR 6.3, which dictates how much information should be disseminated to the market.

Information required to be disclosured under the DTRs must fall within the definition of “regulated information”.

Regulated Information must be disseminated to as wide a public as possible and simultaneously in the Home Member State and other EEA states.

In effect, this rule obliges an issuer to make use of a RIS and adhere to other minimum requirements when disclosing, for example, inside information.

Other relevant continuing obligations

Ensure equal treatment for all holders of the debt securities ranking pari passu in respect of all rights attaching to the debt securities (DTR 6.1.3).

Make public without delay any change in the rights of holders of the debt securities including changes in the terms and conditions of the debt securities which could indirectly affect those rights, resulting in particular from a change in loan terms or in interest rates (DTR 6.1.10).

Publish notices/distribute circulars concerning bondholder meetings, payment of interest, exercise of conversion, exchange, subscription or cancellation rights and repayment (DTR 6.1.14).

Make public without delay any new loan issues and in particular of any guarantee or security in respect thereof (DTR 6.1.11).

Ensure that all the necessary facilities and information are available publicly to enable holders of the debt securities to exercise their rights (DTR 6.1.4).

Where the issuer proposes to amend its instrument of incorporation or statutes, it shall provide the draft amendment to the FSA. Such submission shall be effected without delay and must, at the latest, be provided on the date of the general meeting called on to vote on, or be informed of, the amendment (DTR 6.1.2).

All holders of debt securities must be given equal treatment in respect of rights.

Any changes to the rights must be disclosed to the public without delay.

49

Appendix

(data sets)

50

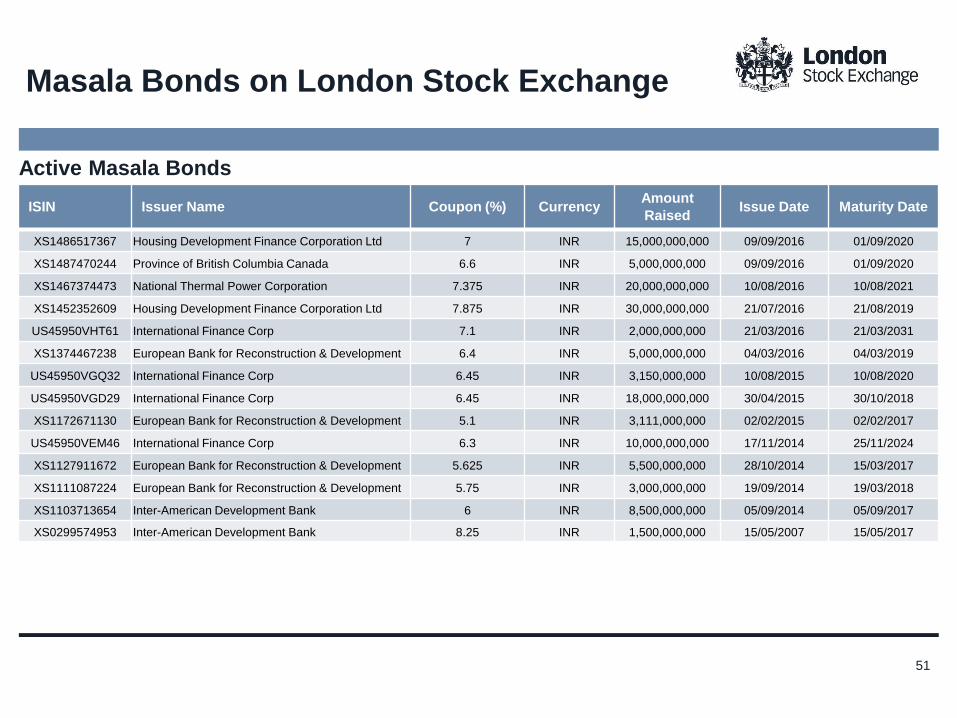

Active Masala Bonds

ISIN Issuer Name Coupon (%) Currency Amount

Raised Issue Date Maturity Date

XS1486517367 Housing Development Finance Corporation Ltd 7 INR 15,000,000,000 09/09/2016 01/09/2020

XS1487470244 Province of British Columbia Canada 6.6 INR 5,000,000,000 09/09/2016 01/09/2020

XS1467374473 National Thermal Power Corporation 7.375 INR 20,000,000,000 10/08/2016 10/08/2021

XS1452352609 Housing Development Finance Corporation Ltd 7.875 INR 30,000,000,000 21/07/2016 21/08/2019

US45950VHT61 International Finance Corp 7.1 INR 2,000,000,000 21/03/2016 21/03/2031

XS1374467238 European Bank for Reconstruction & Development 6.4 INR 5,000,000,000 04/03/2016 04/03/2019

US45950VGQ32 International Finance Corp 6.45 INR 3,150,000,000 10/08/2015 10/08/2020

US45950VGD29 International Finance Corp 6.45 INR 18,000,000,000 30/04/2015 30/10/2018

XS1172671130 European Bank for Reconstruction & Development 5.1 INR 3,111,000,000 02/02/2015 02/02/2017

US45950VEM46 International Finance Corp 6.3 INR 10,000,000,000 17/11/2014 25/11/2024

XS1127911672 European Bank for Reconstruction & Development 5.625 INR 5,500,000,000 28/10/2014 15/03/2017

XS1111087224 European Bank for Reconstruction & Development 5.75 INR 3,000,000,000 19/09/2014 19/03/2018

XS1103713654 Inter-American Development Bank 6 INR 8,500,000,000 05/09/2014 05/09/2017

XS0299574953 Inter-American Development Bank 8.25 INR 1,500,000,000 15/05/2007 15/05/2017

Masala Bonds on London Stock Exchange

51

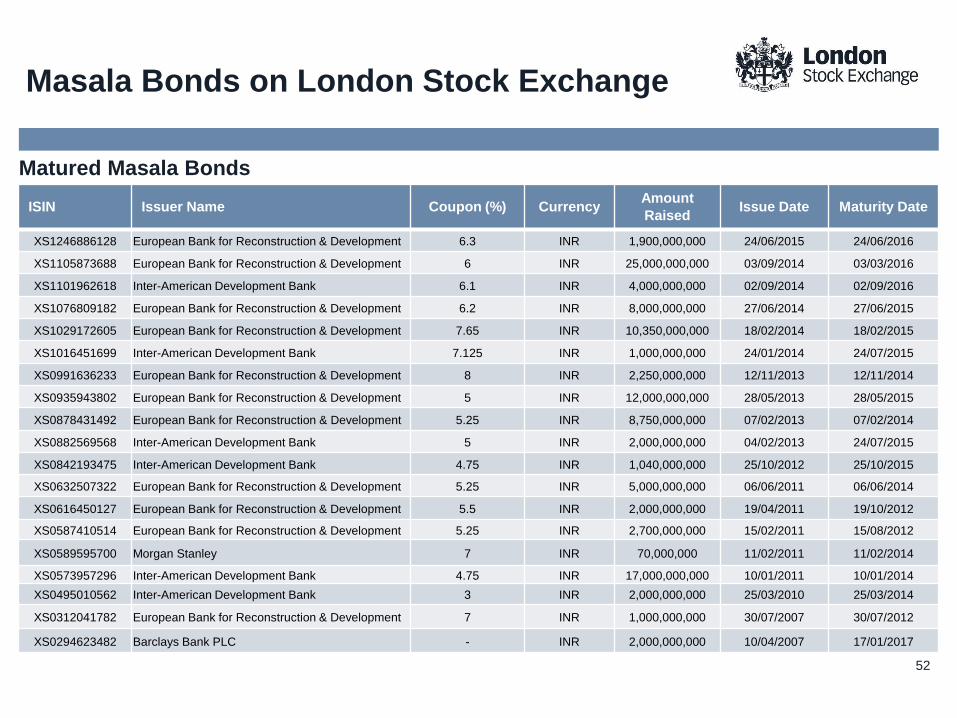

Matured Masala Bonds

ISIN Issuer Name Coupon (%) Currency Amount

Raised Issue Date Maturity Date

XS1246886128 European Bank for Reconstruction & Development 6.3 INR 1,900,000,000 24/06/2015 24/06/2016

XS1105873688 European Bank for Reconstruction & Development 6 INR 25,000,000,000 03/09/2014 03/03/2016

XS1101962618 Inter-American Development Bank 6.1 INR 4,000,000,000 02/09/2014 02/09/2016

XS1076809182 European Bank for Reconstruction & Development 6.2 INR 8,000,000,000 27/06/2014 27/06/2015

XS1029172605 European Bank for Reconstruction & Development 7.65 INR 10,350,000,000 18/02/2014 18/02/2015

XS1016451699 Inter-American Development Bank 7.125 INR 1,000,000,000 24/01/2014 24/07/2015

XS0991636233 European Bank for Reconstruction & Development 8 INR 2,250,000,000 12/11/2013 12/11/2014

XS0935943802 European Bank for Reconstruction & Development 5 INR 12,000,000,000 28/05/2013 28/05/2015

XS0878431492 European Bank for Reconstruction & Development 5.25 INR 8,750,000,000 07/02/2013 07/02/2014

XS0882569568 Inter-American Development Bank 5 INR 2,000,000,000 04/02/2013 24/07/2015

XS0842193475 Inter-American Development Bank 4.75 INR 1,040,000,000 25/10/2012 25/10/2015

XS0632507322 European Bank for Reconstruction & Development 5.25 INR 5,000,000,000 06/06/2011 06/06/2014

XS0616450127 European Bank for Reconstruction & Development 5.5 INR 2,000,000,000 19/04/2011 19/10/2012

XS0587410514 European Bank for Reconstruction & Development 5.25 INR 2,700,000,000 15/02/2011 15/08/2012

XS0589595700 Morgan Stanley 7 INR 70,000,000 11/02/2011 11/02/2014

XS0573957296 Inter-American Development Bank 4.75 INR 17,000,000,000 10/01/2011 10/01/2014

XS0495010562 Inter-American Development Bank 3 INR 2,000,000,000 25/03/2010 25/03/2014

XS0312041782 European Bank for Reconstruction & Development 7 INR 1,000,000,000 30/07/2007 30/07/2012

XS0294623482 Barclays Bank PLC - INR 2,000,000,000 10/04/2007 17/01/2017

Masala Bonds on London Stock Exchange

52

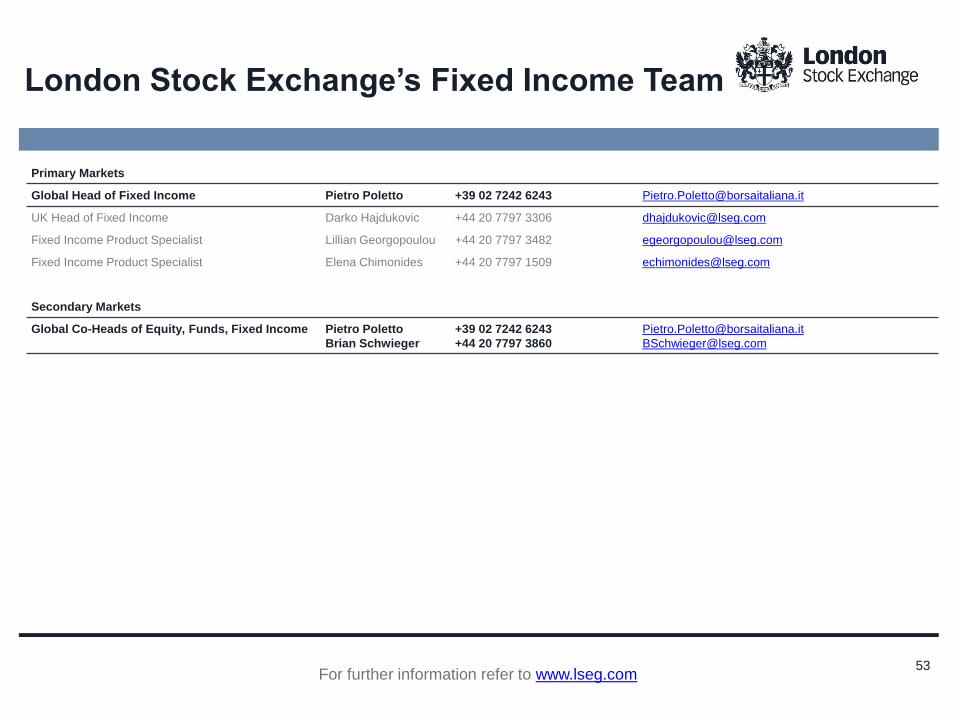

London Stock Exchange’s Fixed Income Team

Primary Markets

Global Head of Fixed Income Pietro Poletto +39 02 7242 6243 [email protected]

UK Head of Fixed Income Darko Hajdukovic +44 20 7797 3306 [email protected]

Fixed Income Product Specialist Lillian Georgopoulou +44 20 7797 3482 [email protected]

Fixed Income Product Specialist Elena Chimonides +44 20 7797 1509 [email protected]

Secondary Markets

Global Co-Heads of Equity, Funds, Fixed Income Pietro Poletto

Brian Schwieger

+39 02 7242 6243

+44 20 7797 3860

For further information refer to www.lseg.com 53

This presentation/document contains text, data, graphics, photographs, illustrations, artwork, names, logos, trade marks, service marks and information (“Information”) connected with

London Stock Exchange Group plc (“LSEG”). LSEG attempts to ensure Information is accurate, however Information is provided “AS IS” and on an “AS AVAILABLE” basis and may not be

accurate or up to date. Information in this presentation/document may or may not have been prepared by LSEG but is made available without responsibility on the part of LSEG. LSEG

does not guarantee the accuracy, timeliness, completeness, performance or fitness for a particular purpose of the presentation/document or any of the Information. No responsibility is

accepted by or on behalf of the Exchange for any errors, omissions, or inaccurate Information in this presentation/document.

No action should be taken or omitted to be taken in reliance upon Information in this presentation/document. We accept no liability for the results of any action taken on the basis of the

Information.

London Stock Exchange, the London Stock Exchange coat of arms device are trade marks of London Stock Exchange plc.

Disclaimer

54