Embed Size (px)

Citation preview

Sistema Universitario Ana G. Méndez

School for Professional Studies

Florida Campuses

Universidad del Este, Universidad Metropolitana, Universidad del Turabo

ACCO 710

ADVANCED AUDITING lI

AUDITORIA AVANZADA lI

© Sistema Universitario Ana G. Méndez, 2010

Derechos Reservados.

© Ana G. Méndez University System, 2010. All rights reserved.

ACCO 710 Advanced Auditing lI 2

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

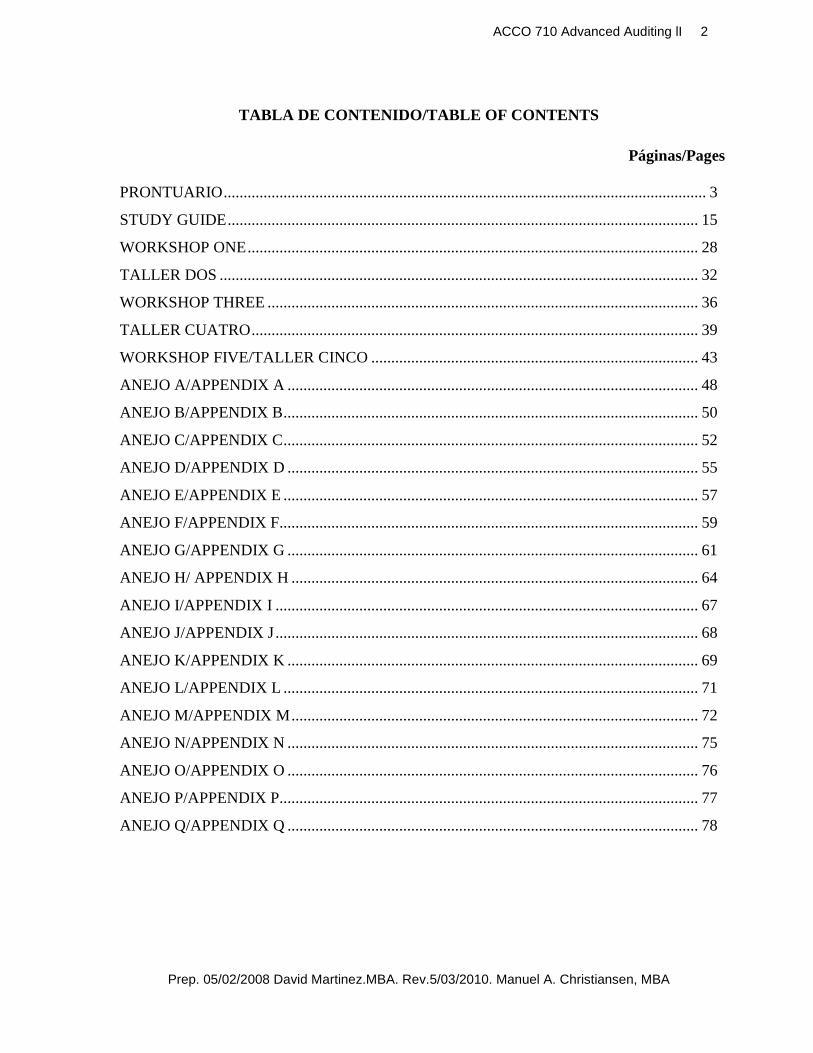

TABLA DE CONTENIDO/TABLE OF CONTENTS

Páginas/Pages

PRONTUARIO ......................................................................................................................... 3

STUDY GUIDE ...................................................................................................................... 15

WORKSHOP ONE ................................................................................................................. 28

TALLER DOS ........................................................................................................................ 32

WORKSHOP THREE ............................................................................................................ 36

TALLER CUATRO ................................................................................................................ 39

WORKSHOP FIVE/TALLER CINCO .................................................................................. 43

ANEJO A/APPENDIX A ....................................................................................................... 48

ANEJO B/APPENDIX B ........................................................................................................ 50

ANEJO C/APPENDIX C ........................................................................................................ 52

ANEJO D/APPENDIX D ....................................................................................................... 55

ANEJO E/APPENDIX E ........................................................................................................ 57

ANEJO F/APPENDIX F......................................................................................................... 59

ANEJO G/APPENDIX G ....................................................................................................... 61

ANEJO H/ APPENDIX H ...................................................................................................... 64

ANEJO I/APPENDIX I .......................................................................................................... 67

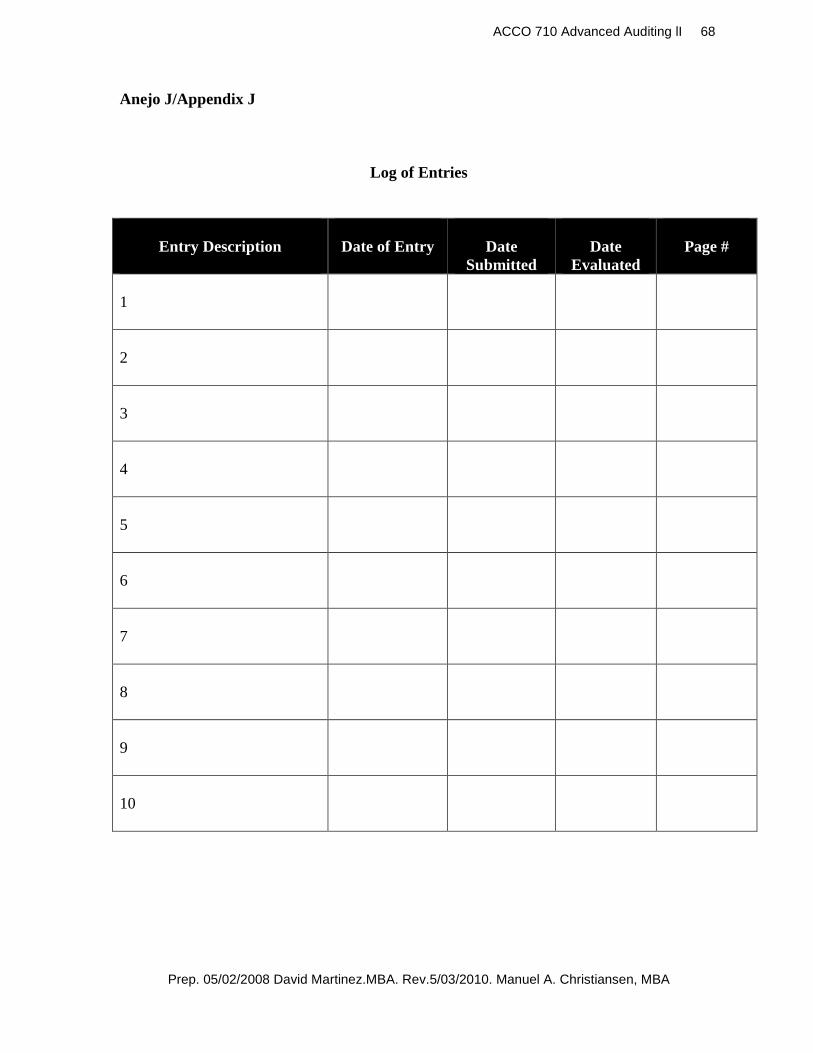

ANEJO J/APPENDIX J .......................................................................................................... 68

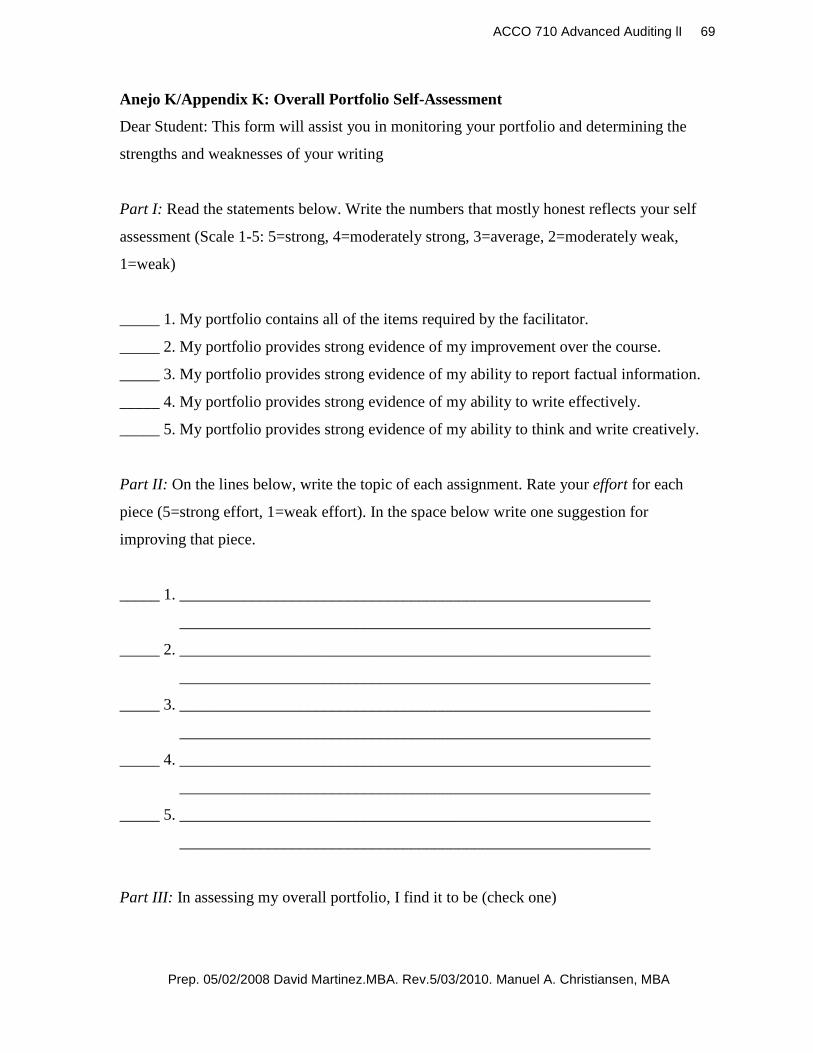

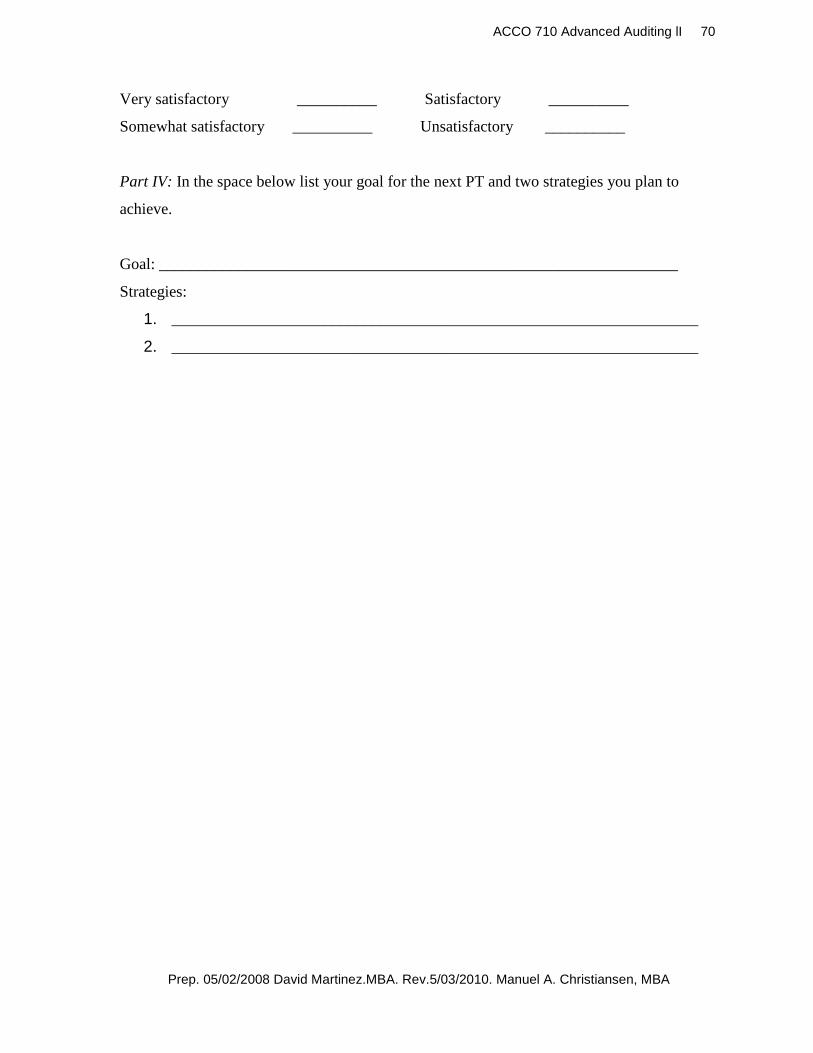

ANEJO K/APPENDIX K ....................................................................................................... 69

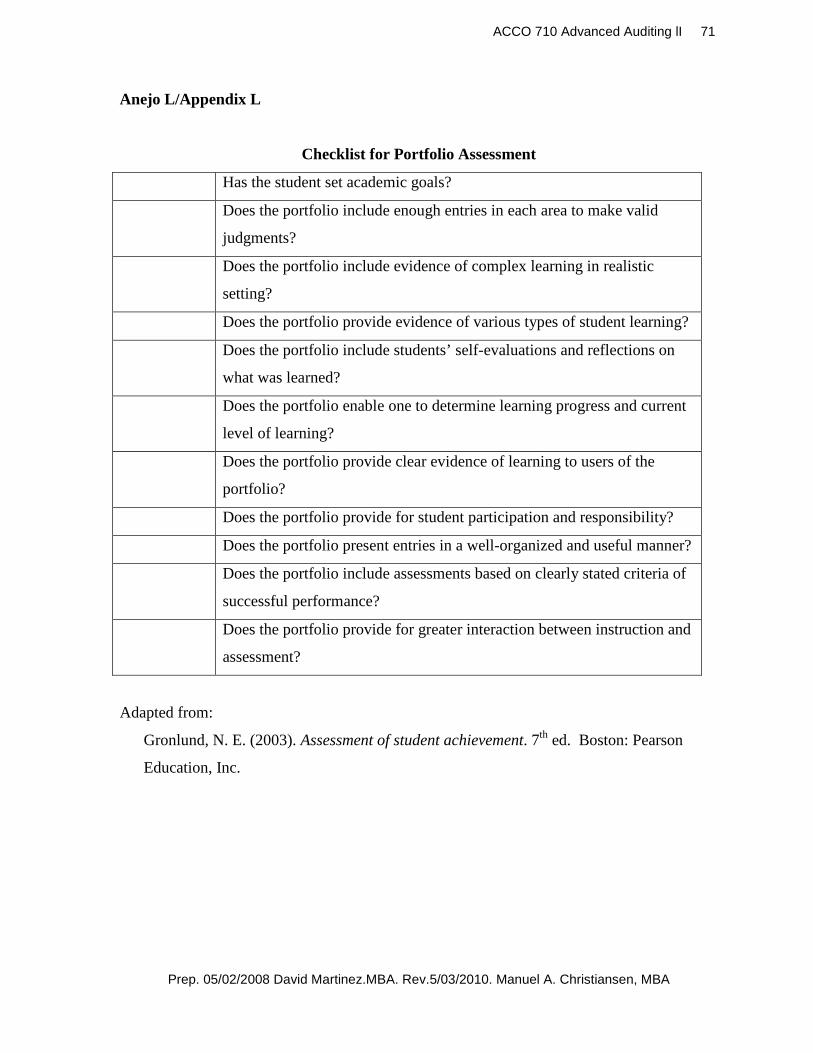

ANEJO L/APPENDIX L ........................................................................................................ 71

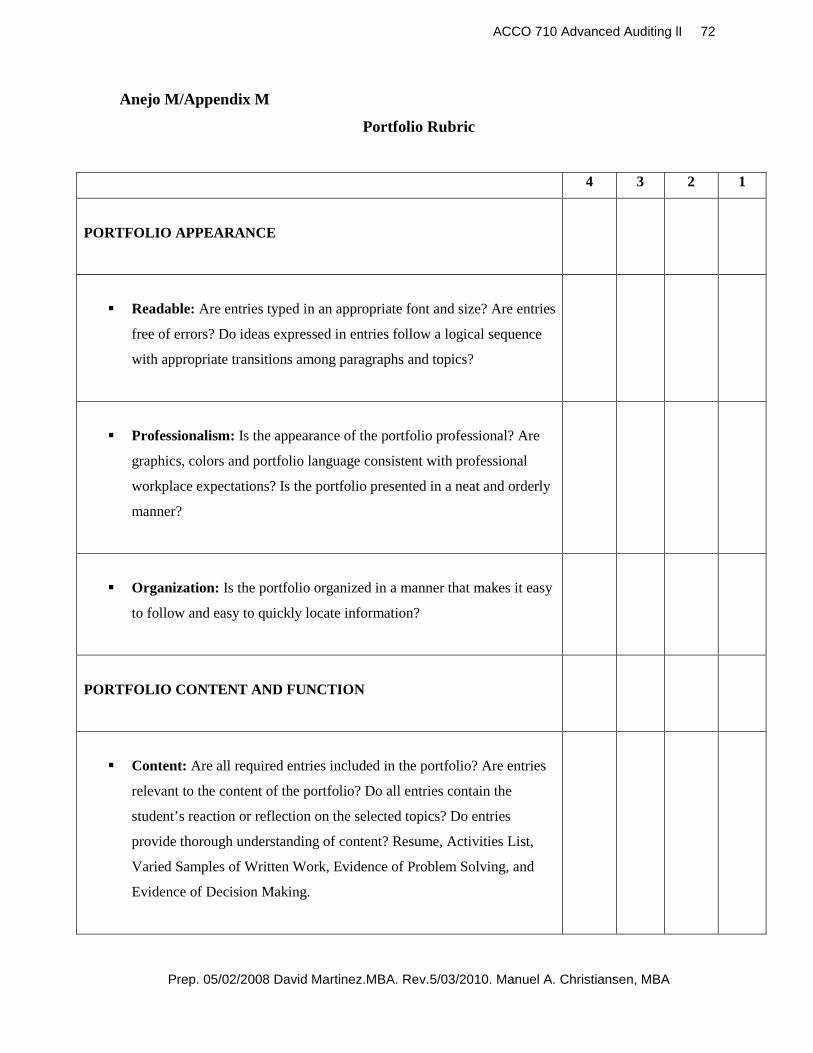

ANEJO M/APPENDIX M ...................................................................................................... 72

ANEJO N/APPENDIX N ....................................................................................................... 75

ANEJO O/APPENDIX O ....................................................................................................... 76

ANEJO P/APPENDIX P......................................................................................................... 77

ANEJO Q/APPENDIX Q ....................................................................................................... 78

ACCO 710 Advanced Auditing lI 3

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

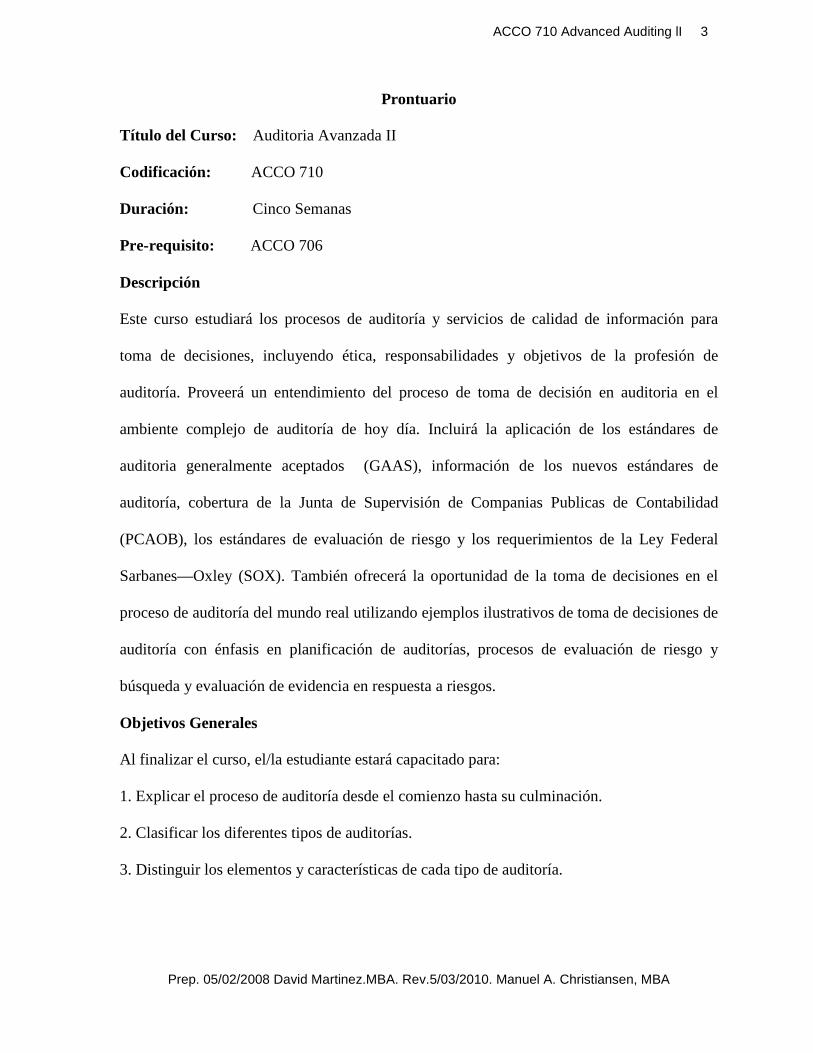

Prontuario

Título del Curso: Auditoria Avanzada II

Codificación: ACCO 710

Duración: Cinco Semanas

Pre-requisito: ACCO 706

Descripción

Este curso estudiará los procesos de auditoría y servicios de calidad de información para

toma de decisiones, incluyendo ética, responsabilidades y objetivos de la profesión de

auditoría. Proveerá un entendimiento del proceso de toma de decisión en auditoria en el

ambiente complejo de auditoría de hoy día. Incluirá la aplicación de los estándares de

auditoria generalmente aceptados (GAAS), información de los nuevos estándares de

auditoría, cobertura de la Junta de Supervisión de Companias Publicas de Contabilidad

(PCAOB), los estándares de evaluación de riesgo y los requerimientos de la Ley Federal

Sarbanes—Oxley (SOX). También ofrecerá la oportunidad de la toma de decisiones en el

proceso de auditoría del mundo real utilizando ejemplos ilustrativos de toma de decisiones de

auditoría con énfasis en planificación de auditorías, procesos de evaluación de riesgo y

búsqueda y evaluación de evidencia en respuesta a riesgos.

Objetivos Generales

Al finalizar el curso, el/la estudiante estará capacitado para:

1. Explicar el proceso de auditoría desde el comienzo hasta su culminación.

2. Clasificar los diferentes tipos de auditorías.

3. Distinguir los elementos y características de cada tipo de auditoría.

ACCO 710 Advanced Auditing lI 4

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

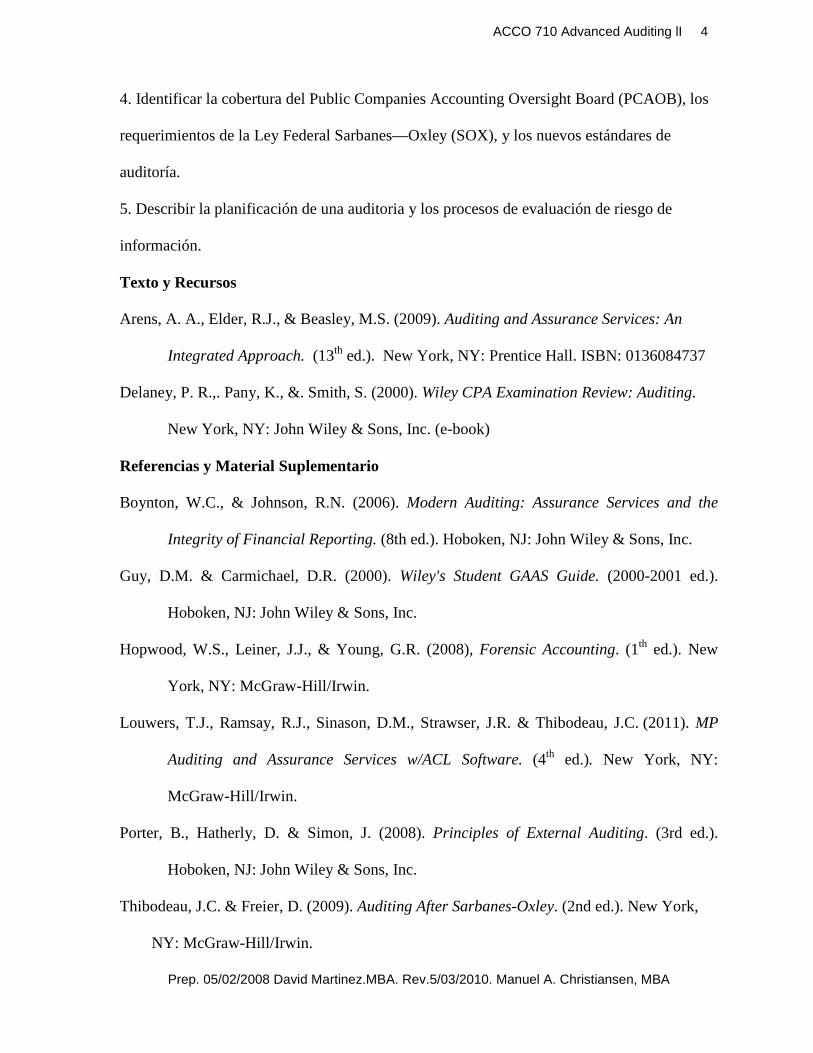

4. Identificar la cobertura del Public Companies Accounting Oversight Board (PCAOB), los

requerimientos de la Ley Federal Sarbanes—Oxley (SOX), y los nuevos estándares de

auditoría.

5. Describir la planificación de una auditoria y los procesos de evaluación de riesgo de

información.

Texto y Recursos

Arens, A. A., Elder, R.J., & Beasley, M.S. (2009). Auditing and Assurance Services: An

Integrated Approach. (13th ed.). New York, NY: Prentice Hall. ISBN: 0136084737

Delaney, P. R.,. Pany, K., &. Smith, S. (2000). Wiley CPA Examination Review: Auditing.

New York, NY: John Wiley & Sons, Inc. (e-book)

Referencias y Material Suplementario

Boynton, W.C., & Johnson, R.N. (2006). Modern Auditing: Assurance Services and the

Integrity of Financial Reporting. (8th ed.). Hoboken, NJ: John Wiley & Sons, Inc.

Guy, D.M. & Carmichael, D.R. (2000). Wiley's Student GAAS Guide. (2000-2001 ed.).

Hoboken, NJ: John Wiley & Sons, Inc.

Hopwood, W.S., Leiner, J.J., & Young, G.R. (2008), Forensic Accounting. (1th ed.). New

York, NY: McGraw-Hill/Irwin.

Louwers, T.J., Ramsay, R.J., Sinason, D.M., Strawser, J.R. & Thibodeau, J.C. (2011). MP

Auditing and Assurance Services w/ACL Software. (4th ed.). New York, NY:

McGraw-Hill/Irwin.

Porter, B., Hatherly, D. & Simon, J. (2008). Principles of External Auditing. (3rd ed.).

Hoboken, NJ: John Wiley & Sons, Inc.

Thibodeau, J.C. & Freier, D. (2009). Auditing After Sarbanes-Oxley. (2nd ed.). New York,

NY: McGraw-Hill/Irwin.

ACCO 710 Advanced Auditing lI 5

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

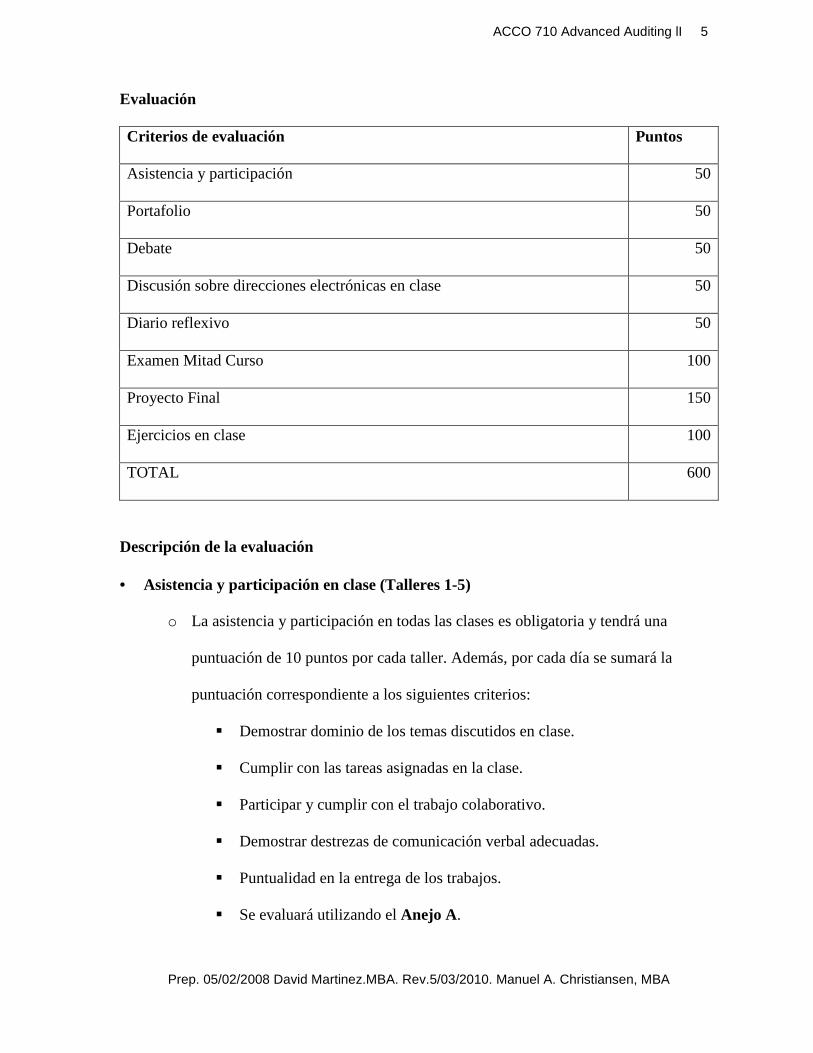

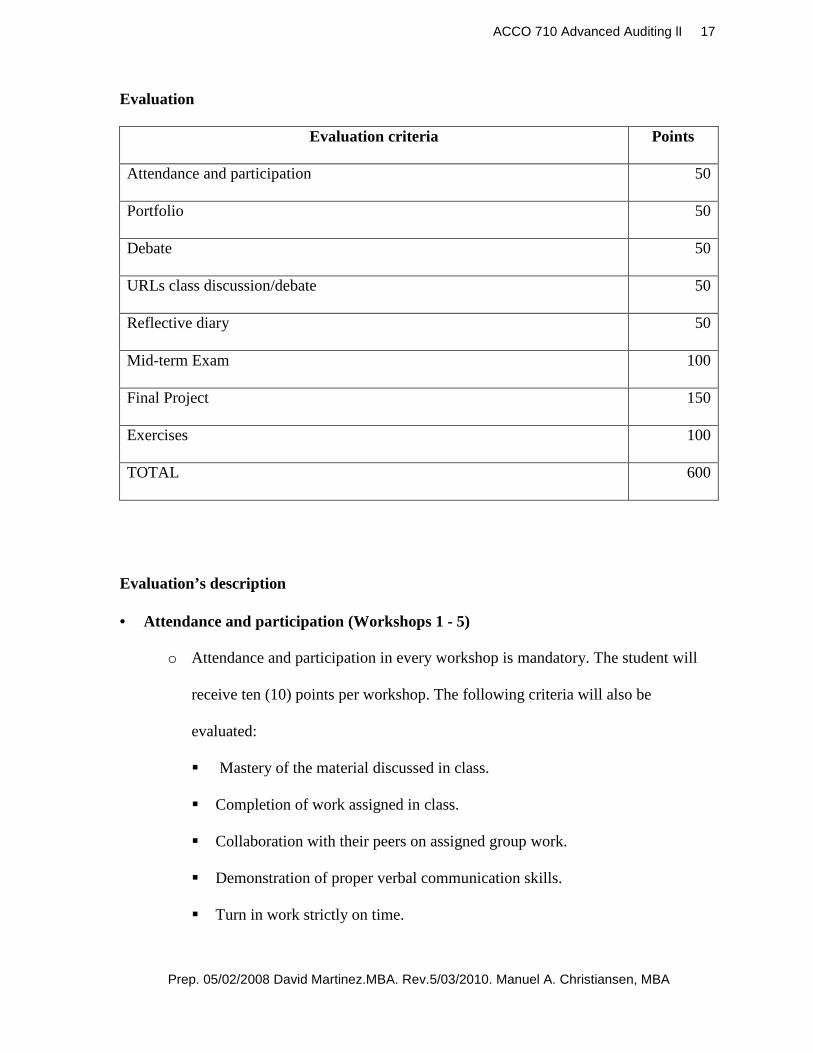

Evaluación

Criterios de evaluación Puntos

Asistencia y participación 50

Portafolio 50

Debate 50

Discusión sobre direcciones electrónicas en clase 50

Diario reflexivo 50

Examen Mitad Curso 100

Proyecto Final 150

Ejercicios en clase 100

TOTAL 600

Descripción de la evaluación

• Asistencia y participación en clase (Talleres 1-5)

o La asistencia y participación en todas las clases es obligatoria y tendrá una

puntuación de 10 puntos por cada taller. Además, por cada día se sumará la

puntuación correspondiente a los siguientes criterios:

� Demostrar dominio de los temas discutidos en clase.

� Cumplir con las tareas asignadas en la clase.

� Participar y cumplir con el trabajo colaborativo.

� Demostrar destrezas de comunicación verbal adecuadas.

� Puntualidad en la entrega de los trabajos.

� Se evaluará utilizando el Anejo A.

ACCO 710 Advanced Auditing lI 6

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Las ausencias afectarán su nota final (2 puntos por asistencia y 8 puntos por participación en

cada taller). El estudiante que se ausente al taller deberá presentar una excusa razonable al

facilitador. El facilitador evaluará si la ausencia es justificada y decidirá como el estudiante

repondrá el trabajo perdido, de ser necesario. El facilitador decidirá uno de los siguientes:

permitirle al estudiante reponer el trabajo o asignarle trabajo adicional en adición al trabajo a

ser repuesto.

Toda tarea a ser completada antes del taller deberá ser entregada en la fecha asignada. El

facilitador ajustará la nota de las tareas propuestas. Si un estudiante se ausenta a más de un

taller el facilitador tendrá las siguientes opciones:

a. Si es a dos talleres, el facilitador reducirá una nota por debajo basado en la nota existente.

b. Si el estudiante se ausenta a tres talleres, el facilitador reducirá la nota a dos por debajo de

la nota existente.

• Laboratorio de Ididomas (Talleres 1-5)

En adición a la asistencia mandataria al salón de clase y participación durante la misma, el

estudiante deberá cumplir veinte (20) horas de ejercicio en el laboratorio de idiomas. A

través de los cinco talleres el estudiante deberá recopilar evidencia de su trabajo para ser

entregada al facilitador en el quinto taller. El facilitador determinara la distribución de horas

entre ambos idiomas – inglés y español – de acuerdo a las necesidades individuales de cada

estudiante. El estudiante deberá completar sus horas físicamente en el laboratorio de idiomas

– en cada centro – o desde su casa/trabajo a través del programa “Tell Me More”.

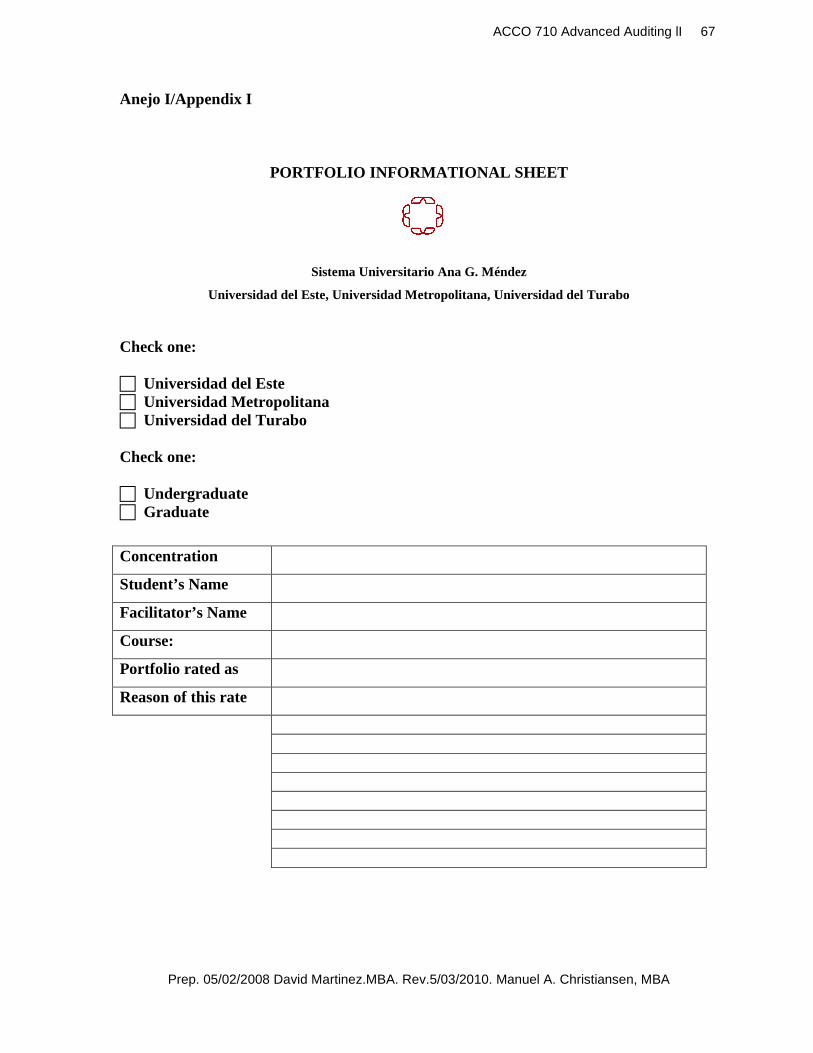

• Portafolio (Talleres 1, 3, and 5)

o Todas las asignaciones escritas, juntas con la selección del trabajo hecho durante

el curso, deberán ser colocadas en un portafolio y seguir estrictamente las

especificaciones de su elaboración ubicadas en los Anejos H-P.

ACCO 710 Advanced Auditing lI 7

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

o El portafolio se presentará dos veces durante este curso: La primera evaluación en

el taller 3 y la evaluación final en el taller cinco.

o El portafolio se evaluará usando el Anejo M.

• Debate (Taller 2 y 4)

o Cada grupo traerá a la discusión contenido relevante al tema asignado o escogido

y utilizará todos los recursos que le ayuden a su presentación del tema a discutir

(por ejemplo: ayudas visuales, libros, afiches, etc.).

o Cada grupo podrá usar sus notas o leer pasajes cortos de lo que dicen los

investigadores sobre su tema asignado.

o Esta actividad se evaluará usando el Anejo G.

• Examen Mitad Curso (Taller 4)

o Este examen es para hacerlo en la casa.

o Se distribuirá en el taller tres.

o Será entregado al comienzo del taller cuatro.

o La actividad se evaluará a base de una escala de 100 puntos.

• Final Project (Workshop 5)

o Este es un trabajo de grupo. Los detalles están especificados en el Anejo Q.

o Los detalles serán explicados y discutidos en el taller uno.

o Será entregado al comienzo del taller cinco.

o La actividad se evaluará a base de una escala de 150 puntos.

o Esta actividad se evaluará usando el Anejos B y C.

• Discusión sobre las Direcciones Electrónicas (URL) (Talleres 1- 5)

o Los estudiantes se prepararán para discutir en grupo las direcciones electrónicas

asignadas para en taller.

ACCO 710 Advanced Auditing lI 8

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

o La discusión se evaluará usando el Anejo D.

• Diario Reflexivo (Talleres 1, 3, and 5)

o Los estudiantes expresarán sus ideas en las materias aprendidas en el taller, cómo

éstas le ayudarán y el uso de éstas en su vida.

o El escrito será evaluado usando el Anejo E.

• Auto-evaluación (Talleres 2, 4 y 5)

o Los estudiantes prepararán una evaluación considerando los aspectos generales,

vocabulario, estructura y organización.

o El escrito será evaluado usando el Anejo F.

• Ejercicios (Talleres 1 – 5)

o El estudiante preparará los ejercicios asignados en el taller.

Curva de evaluación

100-90% A 89-80% B 79-70% C 69-60% D 59-00% F

Descripción de las Normas del Curso

1. Este curso sigue el modelo “Discipline-Based Dual Language Immersion Model®”

del Sistema Universitario Ana G. Méndez, el mismo está diseñado para promover el

desarrollo de cada estudiante como un profesional bilingüe. Cada taller será

facilitado en inglés y español, utilizando el modelo 50/50. Esto significa que cada

taller deberá ser conducido enteramente en el lenguaje especificado. Los lenguajes

serán alternados en cada taller para asegurar que el curso se ofrece 50% en inglés y

50% en español. Para mantener un balance, el módulo debe especificar que se

utilizarán ambos idiomas en el quinto taller, dividiendo el tiempo y las actividades

equitativamente entre ambos idiomas. Si un estudiante tiene dificultad en hacer una

ACCO 710 Advanced Auditing lI 9

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

pregunta en el idioma especificado, bien puede escoger el idioma de preferencia para

hacer la pregunta. Sin embargo, el facilitador deberá contestar la misma en el idioma

designado para ese taller. Esto deberá ser una excepción a las reglas pues es

importante que los estudiantes utilicen el idioma designado. Esto no aplica a los

cursos de lenguaje que deben ser desarrollados en el idioma propio todo en inglés o

todo en español según aplique.

2. El curso es conducido en formato acelerado, eso requiere que los estudiantes se

preparen antes de cada taller de acuerdo al módulo. Cada taller requiere un promedio

de diez (10) horas de preparación y en ocasiones requiere más.

3. La asistencia a todos los talleres es obligatoria. El estudiante que se ausente al taller

deberá presentar una excusa razonable al facilitador. El facilitador evaluará si la

ausencia es justificada y decidirá como el estudiante repondrá el trabajo perdido, de

ser necesario. El facilitador decidirá uno de los siguientes: permitirle al estudiante

reponer el trabajo o asignarle trabajo adicional en adición al trabajo a ser repuesto.

Toda tarea a ser completada antes del taller deberá ser entregada en la fecha asignada.

El facilitador ajustará la nota de las tareas repuestas.

4. Si un estudiante se ausenta a más de un taller el facilitador tendrá las siguientes

opciones:

a. Si es a dos talleres, el facilitador reducirá una nota por debajo basado en

la nota existente.

b. Si el estudiante se ausenta a tres talleres, el facilitador reducirá la nota a

dos por debajo de la nota existente.

5. La asistencia y participación en clase de actividades y presentaciones orales es

extremadamente importante pues no se pueden reponer. Si el estudiante provee una

ACCO 710 Advanced Auditing lI 10

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

excusa válida y verificable, el facilitador determinará una actividad equivalente a

evaluar que sustituya la misma. Esta actividad deberá incluir el mismo contenido y

componentes del lenguaje como la presentación oral o actividad a ser repuesta.

6. En actividades de grupo, el grupo será evaluado por su trabajo final. Sin embargo,

cada miembro de grupo deberá participar y cooperar para lograr un trabajo de

excelencia, pero recibirán una calificación individual.

7. Se espera que todo trabajo escrito sea de la autoría de cada estudiante y no plagiado.

Se debe entender que todo trabajo sometido esta citado apropiadamente o

parafraseado y citado dando atención al autor. Todo estudiante debe ser el autor de su

propio trabajo. Todo trabajo que sea plagiado, copiado o presente trazos de otro será

calificado con cero. El servicio de SafeAssign TM de Blackboard será utilizado por los

facilitadores para verificar la autoría de los trabajos escritos de los estudiantes. Es

responsabilidad del estudiante el leer la política de plagio de su universidad. Si usted

es estudiante de UT, deberá leer la Sección 11.1 del Manual del Estudiante. Si es

estudiante de UMET y UT, refiérase al Capítulo 13, secciones 36 y 36.1 de los

respectivos manuales.

Se espera un comportamiento ético en todas las actividades del curso. Esto implica

que TODOS los trabajos tienen que ser originales y que de toda referencia utilizada

deberá indicarse la fuente, bien sea mediante citas o bibliografía. No se tolerará el

plagio y, en caso de que se detecte casos del mismo, el estudiante se expone a recibir

cero en el trabajo y a ser referido al Comité de Disciplina de la institución. Los

estudiantes deben observar aquellas prácticas dirigidas a evitar incurrir en el plagio de

documentos y trabajos.

ACCO 710 Advanced Auditing lI 11

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

8. Si el facilitador hace cambios al módulo o guía de estudio, deberá discutirlos y

entregar copia a los estudiantes por escrito al principio del primer taller.

9. El facilitador establecerá los medios para contactar a los estudiantes proveyendo su

correo electrónico, teléfonos, y el horario disponibles.

10. EL uso de celulares está prohibido durante las sesiones de clase; de haber una

necesidad, deberá permanecer en vibración o en silencio.

11. La visita de niños y familiares no registrados en el curso no está permitida en el salón

de clases.

12. Todo estudiante está sujeto a las políticas y normas de conducta y comportamiento

que rigen al SUAGM y el curso.

Nota: Si por alguna razón no puede acceder las direcciones electrónicas ofrecidas en el

módulo, no se limite a ellas. Existen otros motores de búsqueda y sitios Web que podrá

utilizar para la búsqueda de la información deseada. Entre ellas están:

• www.google.com

• www.ask.com

• www.pregunta.com

• www.findarticles.com

• www.bibliotecavirtualut.suagm.edu

• www.eric.ed.gov/

• www.flelibrary.org/

• http://www.apastyle.org/

Para comprar o alquilar libros de texto o referencias nuevas o usadas puede visitar:

• http://www.chegg.com/ (alquiler)

ACCO 710 Advanced Auditing lI 12

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

• http://www.bookswim.com/ (alquiler)

• http://www.allbookstores.com/ (compra)

• http://www.alibris.com/ (compra)

Estos son sólo algunas de las muchas compañías donde puede comprar o alquilar

libros.

El/la facilitador(a) puede realizar cambios a las direcciones electrónicas y/o añadir algunas de

ser necesario.

Nota: Del facilitador o el estudiante requerir o desear una investigación o la administración

de cuestionarios o entrevistas, deben referirse a las normas y procedimientos de la Oficina de

Cumplimiento y solicitar su autorización. Para acceder a los formularios de la Oficina de

Cumplimiento pueden visitar este enlace

http://www.suagm.edu/ac_aa_re_ofi_formularios.asp y seleccionar los formularios que

necesite.

Además de los formularios el estudiante/facilitador puede encontrar las instrucciones para la

certificación en línea. Estas certificaciones incluyen: IRB Institutional Review Board, Health

Information Portability Accounting Act (HIPAA), y Responsibility Conduct for Research

Act (RCR).

De tener alguna duda, favor de comunicarse con la Coordinadoras Institucionales o a la

Oficina de Cumplimiento a los siguientes teléfonos:

Sra. Evelyn Rivera Sobrado, Directora Oficina de Cumplimiento

Tel. (787) 751-0178 Ext. 7196

Srta. Carmen Crespo, Coordinadora Institucional Cumplimiento – UMET

Tel. (787) 766-1717 Ext. 6366

ACCO 710 Advanced Auditing lI 13

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Sra. Josefina Melgar, Coordinadora Institucional Cumplimiento – Turabo

Tel. (787) 743-7979 Ext.4126

Dra. Rebecca Cherry, Coordinadora Institucional Cumplimiento – UNE

Tel. (787) 257-7373 Ext. 3936

Filosofía y Metodología Educativa

Este curso está basado en la teoría educativa del Constructivismo. Constructivismo

es una filosofía de aprendizaje fundamentada en la premisa, de que, reflexionando a través de

nuestras experiencias, podemos construir nuestro propio conocimiento sobre el mundo en el

que vivimos.

Cada uno de nosotros genera nuestras propias “reglas “y “métodos mentales” que

utilizamos para darle sentido a nuestras experiencias. Aprender, por lo tanto, es simplemente

el proceso de ajustar nuestros modelos mentales para poder acomodar nuevas experiencias.

Como facilitadores, nuestro enfoque es el mantener una conexión entre los hechos y fomentar

un nuevo entendimiento en los estudiantes. También, intentamos adaptar nuestras estrategias

de enseñanza a las respuestas de nuestros estudiantes y motivar a los mismos a analizar,

interpretar y predecir información.

Existen varios principios para el constructivismo, entre los cuales están:

1. El aprendizaje es una búsqueda de significados. Por lo tanto, el aprendizaje debe

comenzar con situaciones en las cuales los estudiantes estén buscando activamente

construir un significado.

2. Significado requiere comprender todas las partes. Y, las partes deben entenderse en el

contexto del todo. Por lo tanto, el proceso de aprendizaje se enfoca en los conceptos

primarios, no en hechos aislados.

ACCO 710 Advanced Auditing lI 14

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

3. Para enseñar bien, debemos entender los modelos mentales que los estudiantes utilizan

para percibir el mundo y las presunciones que ellos hacen para apoyar dichos modelos.

4. El propósito del aprendizaje, es para un individuo, el construir su propio significado, no

sólo memorizar las contestaciones “correctas” y repetir el significado de otra persona.

Como la educación es intrínsecamente interdisciplinaria, la única forma válida para

asegurar el aprendizaje es hacer del avalúo parte esencial de dicho proceso, asegurando

que el mismo provea a los estudiantes con la información sobre la calidad de su

aprendizaje.

5. La evaluación debe servir como una herramienta de auto-análisis.

6. Proveer herramientas y ambientes que ayuden a los estudiantes a interpretar las múltiples

perspectivas que existen en el mundo.

7. El aprendizaje debe ser controlado internamente y analizado por el estudiante.

ACCO 710 Advanced Auditing lI 15

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

STUDY GUIDE

Course Title: Advanced Auditing II

Code: ACCO 710

Time Length: Five Weeks

Pre-requisite: ACCO 706

Description

This course will study the auditing process and other assurance services, including ethics,

responsibilities, and objectives of the auditing profession. It will provide an understanding of

the audit decision making in today’s complex auditing environment. It includes the

application of the Generally Accepted Auditing Standards (GAAS), information on new

auditing standards, coverage of the Public Companies Accounting Oversight Board

(PCAOB), the risk assessment standards, and the requirements of the Sarbanes—Oxley Act.

It will offer the opportunity to face real-world audit decision making by using illustrative

examples of key audit decisions, with an emphasis on audit planning, risk assessment

processes, and collecting and evaluating evidence in response to risks including international

coverage, international auditing standards, and emphasizes issues affecting audits of multi-

national entities and international issues.

General Objectives

As the course finishes, the student will be capable of:

1. Explain the auditing process from start to finish.

2. Classify the different types of auditing processes.

3. Distinguish the elements and characteristics of each ones.

ACCO 710 Advanced Auditing lI 16

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

4. Identify the coverage of the Public Companies Accounting Oversight Board

(PCAOB), the requirements of the Sarbanes—Oxley Act, and the new auditing

standards.

5. Describe the audit planning and risk assessment processes.

Textbooks and Resources

Arens, A. A., Elder, R.J., & Beasley, M.S. (2009). Auditing and Assurance Services: An

Integrated Approach. (13th ed.). New York, NY: Prentice Hall. ISBN: 0136084737

Delaney, P. R.,. Pany, K., &. Smith, S. (2000). Wiley CPA Examination Review: Auditing.

New York, NY: John Wiley & Sons, Inc. (e-book)

Reference and Supplementary Material

Boynton, W.C., & Johnson, R.N. (2006). Modern Auditing: Assurance Services and the

Integrity of Financial Reporting. (8th ed.). Hoboken, NJ: John Wiley & Sons, Inc.

Guy, D.M. & Carmichael, D.R. (2000). Wiley's Student GAAS Guide. (2000-2001 ed.).

Hoboken, NJ: John Wiley & Sons, Inc.

Hopwood, W.S., Leiner, J.J., & Young, G.R. (2008), Forensic Accounting. (1th ed.). New

York, NY: McGraw-Hill/Irwin.

Louwers, T.J., Ramsay, R.J., Sinason, D.M., Strawser, J.R. & Thibodeau, J.C. (2011). MP

Auditing and Assurance Services w/ACL Software. (4th ed.). New York, NY:

McGraw-Hill/Irwin.

Porter, B., Hatherly, D. & Simon, J. (2008). Principles of External Auditing. (3rd ed.).

Hoboken, NJ: John Wiley & Sons, Inc.

Thibodeau, J.C. & Freier, D. (2009). Auditing After Sarbanes-Oxley. (2nd ed.). New York,

NY: McGraw-Hill/Irwin.

ACCO 710 Advanced Auditing lI 17

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Evaluation

Evaluation criteria Points

Attendance and participation 50

Portfolio 50

Debate 50

URLs class discussion/debate 50

Reflective diary 50

Mid-term Exam 100

Final Project 150

Exercises 100

TOTAL 600

Evaluation’s description

• Attendance and participation (Workshops 1 - 5)

o Attendance and participation in every workshop is mandatory. The student will

receive ten (10) points per workshop. The following criteria will also be

evaluated:

� Mastery of the material discussed in class.

� Completion of work assigned in class.

� Collaboration with their peers on assigned group work.

� Demonstration of proper verbal communication skills.

� Turn in work strictly on time.

ACCO 710 Advanced Auditing lI 18

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Absences will affect your final grade as follows: 2 points for your attendance and 8 points for

your participation in class. A student that is absent to a workshop must present the facilitator

a reasonable excuse. The facilitator will evaluate if the absence is justified and decide how

the student will make up the missing work, if applicable. The facilitator will decide on the

following: allow the student to make up the work, or allow the student to make up the work

and assign extra work to compensate for the missing class time.

Assignments required prior to the workshop must be completed and turned in on the

assigned date. The facilitator may decide to adjust the grade given for late assignments and

make-up work.

If a student is absent to more than one workshop the facilitator will have the following

options:

a. If a student misses two workshops, the facilitator may lower one grade based on the

students existing grade.

b. If the student misses three workshops, the facilitator may lower two grades based on the

students existing grade.

Attendance and participation (Workshops 1 - 5)

In addition to the mandatory attendance and class participation the student will complete

twenty (20) hours of language laboratory. Throughout each week the student will keep

evidence of his/her work to turn in on the fifth workshop. The facilitator will determine the

distribution of hours among the two languages – English and Spanish – according to the

individual needs of each student. The student can complete the laboratory requirements

either physically at the centers – language laboratories – or at home/work through the web-

based program “Tell Me More.”

• Portfolio (Workshops 1, 3, and 5)

ACCO 710 Advanced Auditing lI 19

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

o All self assessment and reflection written assignments, together with the selection

of work done during the course, will be assembled in a portfolio strictly following

the guidelines of portfolio elaboration in Appendices (H-P).

o The portfolio should be submitted twice during this course: First partial

evaluation (Workshop 3) and final evaluation (Workshop 5).

o The portfolio will be evaluated using Appendix M.

• Debate (Workshops 2 and 4)

o Every group of students will bring into discussion the content relevant to the

assigned topic and use all the resources that help the presentation of the topic to

be discussed (e.g. visual aids, books, posters, etc.).

o Every group can use notes or read short excerpts of what researchers say about

their assigned topics.

o This activity will be evaluated using Appendix G.

• Mid-term Exam (Workshop 4)

o This is a take-home exam.

o It will be distributed on workshop three.

o Must be turn in at the beginning of workshop four.

o This activity will be evaluated using a scale of 100 points.

• Final Project (Workshop 5)

o This is a team assignment. You will find the details on Appendix Q.

o It will be explained and discussed on workshop one.

o Must be turn in at the beginning of workshop five.

o This activity will be evaluated using a scale of 150 points.

o This activity will be evaluated using Appendixes B and C.

ACCO 710 Advanced Auditing lI 20

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

• URL Discussions (Workshops 1 - 5)

o The students will be prepared to discuss the URLs assigned for the workshop.

o The discussions will be evaluated using Appendix D.

• Reflective Diary (Workshops 1, 3, and 5)

o The students will express their thoughts on the subjects learned, how would they

help them, and how to apply these concepts in their life.

o This write-up would be evaluated using Appendix E.

• Auto-evaluation (Workshops 2, 4, and 5)

o The students will prepare an evaluation considering the general aspects,

vocabulary, structure, and organization.

o The write-up would be evaluated using Appendix F.

• Exercises (Workshops 1 - 5)

o Students will prepare the exercises as assigned during the workshop.

Evaluation curve

100-90% A 89-80% B 79-70% C 69-60% D 59-00% F

ACCO 710 Advanced Auditing lI 21

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Description of course policies

1. This course follows the Sistema Universitario Ana G. Méndez Discipline-Based Dual

Language Immersion Model® designed to promote each student’s development as a Dual

Language Professional. Workshops will be facilitated in English and Spanish, strictly

using the 50/50 model. This means that each workshop will be conducted entirely in the

language specified. The language used in the workshops will alternate to insure that 50%

of the course will be conducted in English and 50% in Spanish. To maintain this balance,

the course module may specify that both languages will be used during the fifth

workshop, dividing that workshop’s time and activities between the two languages. If

students have difficulty with asking a question in the target language in which the activity

is being conducted, students may choose to use their preferred language for that particular

question. However, the facilitator must answer in the language assigned for that particular

day. This should only be an exception as it is important for students to use the assigned

language. The 50/50 model does not apply to language courses where the delivery of

instruction must be conducted in the language taught (Spanish or English only).

2. The course is conducted in an accelerated format and requires that students prepare in

advance for each workshop according to the course module. Each workshop requires an

average ten hours of preparation but could require more.

3. Attendance at all class sessions is mandatory. A student that is absent to a workshop

must present the facilitator a reasonable excuse. The facilitator will evaluate if the

absence is justified and decide how the student will make up the missing work, if

applicable. The facilitator will decide on the following: allow the student to make up the

work, or allow the student to make up the work and assign extra work to compensate for

the missing class time.

ACCO 710 Advanced Auditing lI 22

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Assignments required prior to the workshop must be completed and turned in on the

assigned date. The facilitator may decide to adjust the grade given for late assignments

and make-up work.

4. If a student is absent to more than one workshop the facilitator will have the

following options:

a. If a student misses two workshops, the facilitator may lower one grade based

on the students existing grade.

b. If the student misses three workshops, the facilitator may lower two grades

based on the students existing grade.

5. Student attendance and participation in oral presentations and special class activities are

extremely important as it is not possible to assure that they can be made up. If the student

provides a valid and verifiable excuse, the facilitator may determine a substitute

evaluation activity if he/she understands that an equivalent activity is possible. This

activity must include the same content and language components as the oral presentation

or special activity that was missed.

6. In cooperative activities the group will be assessed for their final work. However, each

member will have to collaborate to assure the success of the group and the assessment

will be done collectively as well as individually.

7. It is expected that all written work will be solely that of the student and should not be

plagiarized. That is, the student must be the author of all work submitted. All quoted or

paraphrased material must be properly cited, with credit given to its author or publisher.

It should be noted that plagiarized writings are easily detectable and students should not

risk losing credit for material that is clearly not their own. SafeAssignTM, a Blackboard

plagiarism deterrent service, will be used by the facilitators to verify students’ ownership

ACCO 710 Advanced Auditing lI 23

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

of written assignments. It is the student’s responsibility to read the university’s

plagiarism policy. If you are a UT student, read Section 11.1 of the Student Manual, and

if you belong to UMET or UNE, refer to Chapter 13, Sections 36 and 36.1 of the

respective manuals.

Ethical behavior is expected from the students in all course related activities. This means

that ALL papers submitted by the student must be original work and that all references

used will be properly cited or mentioned in the bibliography. Plagiarism will not be

tolerated and, in case of detecting an incidence, the student will obtain a zero in the

assignment or activity and could be referred to the Discipline Committee.

8. If the Facilitator makes changes to the study guide, such changes should be discussed

with and given to students in writing at the beginning of the first workshop.

9. The facilitator will establish a means of contacting students by providing an email

address, phone number, hours to be contacted and days.

10. The use of cellular phones is prohibited during sessions; if there is a need to have one, it

must be on vibrate or silent mode during class session.

11. Children or family members that are not registered in the course are not allowed to the

classrooms.

12. All students are subject to the policies regarding behavior in the university community

established by the institution and in this course.

Note: If for any reason you cannot access the URL’s presented in the module, do not

stop your investigation. There are many search engines and other links you can use

to search for information. These are some examples:

• www.google.com

• www.ask.com

ACCO 710 Advanced Auditing lI 24

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

• www.pregunta.com

• www.findarticles.com

• www.bibliotecavirtualut.suagm.edu

• www.eric.ed.gov/

• www.flelibrary.org/

• www.google.com

• www.ask.com

• www.pregunta.com

• www.findarticles.com

• www.bibliotecavirtualut.suagm.edu

• www.eric.ed.gov/

• www.flelibrary.org/

• http://www.apastyle.org/

To buy or rent new or used textbooks or references you can visit:

• http://www.chegg.com/ (rent)

• http://www.bookswim.com/ (rent)

• http://www.allbookstores.com/ (buy)

• http://www.alibris.com/ (buy)

The facilitator may make changes or add additional web resources if deemed necessary.

Note: If the facilitator or the student is required or wants to perform a research or needs to

administer a questionnaire or an interview, he/she will need to refer to the norms and

procedures of the Institutional Review Board Office (IRB) and ask for authorization. To

ACCO 710 Advanced Auditing lI 25

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

access the forms from the IRB Office or for additional information, visit the following link:

http://www.suagm.edu/ac_aa_re_ofi_formularios.asp and select the forms needed.

Furthermore, in this website the student/facilitator will find instructions for several online

certifications related to IRB processes. These certifications include: IRB Institutional

Review Board, Health Information Portability Accounting Act (HIPAA), y Responsibility

Conduct for Research Act (RCR).

If you have any question, please contact the following Institutional Coordinators:

Mrs. Evelyn Rivera Sobrado, Director of IRB Office (PR)

Tel. (787) 751-0178 Ext. 7196

Miss. Carmen Crespo, IRB Institutional Coordinator– UMET

Tel. (787) 766-1717 Ext. 6366

Sra. Josefina Melgar, IRB Institutional Coordinator – Turabo

Tel. (787) 743-7979 Ext.4126

Rebecca Cherry, Ph.D., IRB Institutional Coordinator – UNE

Tel. (787) 257-7373 Ext. 3936

ACCO 710 Advanced Auditing lI 26

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Teaching Philosophy and Methodology

This course is grounded in the learning theory of Constructivism. Constructivism is a

philosophy of learning founded on the premise that, by reflecting on our experiences, we

construct our own understanding of the world in which we live.

Each of us generates our own “rules” and “mental models,” which we use to make sense

of our experiences. Learning, therefore, is simply the process of adjusting our mental models

to accommodate new experiences. As teachers, our focus is on making connections between

facts and fostering new understanding in students. We will also attempt to tailor our teaching

strategies to student responses and encourage students to analyze, interpret and predict

information.

There are several guiding principles of constructivism:

1. Learning is a search for meaning. Therefore, learning must start with the issues around

which students are actively trying to construct meaning.

2. Meaning requires understanding wholes as well as parts. And parts must be understood in

the context of wholes. Therefore, the learning process focuses on primary concepts, not

isolated facts.

3. In order to teach well, we must understand the mental models that students use to

perceive the world and the assumptions they make to support those models.

4. The purpose of learning is for an individual to construct his or her own meaning, not just

memorize the "right" answers and regurgitate someone else's meaning. Since education is

inherently interdisciplinary, the only valuable way to measure learning is to make the

assessment part of the learning process, ensuring it provides students with information on

the quality of their learning.

5. Evaluation should serve as a self-analysis tool.

ACCO 710 Advanced Auditing lI 27

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

6. Provide tools and environments that help learners interpret the multiple perspectives of

the world.

7. Learning should be internally controlled and mediated by the learner.

ACCO 710 Advanced Auditing lI 28

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Workshop One

Specific Objectives

At the end of this workshop, students will:

1. Describe the auditing process, distinguishing between auditing and accounting.

2. Identify the objectives, purposes, and functions of the Generally Accepted Auditing

Standards (GAAS).

3. Understand the role of the Public Companies Accounting Oversight Board (PCAOB), the

Securities and Exchange Commission (SEC), and the effects of the Sarbanes—Oxley Act

(SOX) on the CPA profession.

4. Differentiate the three main types of audits and identify the primary type of auditors.

5. Explain the importance of auditing in reducing information risk.

Specific Language Objectives

Students will:

1. Use cooperative learning strategies to analyze and discuss the URL content.

2. Write a clear and accurate report by describing the accounting basic principles using

appropriate vocabulary, grammar, and style.

3. Use the reading process effectively, present verbal comments, and support his /her ideas

about the subjects assigned for this workshop with facts.

URLs

The Institute of Internal Auditors

http://www.theiia.org/

The Global Resource for Auditors

http://www.auditnet.org/

American Institute of Certified Public Accountants

ACCO 710 Advanced Auditing lI 29

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

http://www.aicpa.org/

The General Accounting Office (GAO)

http://www.gao.gov/about/

Public Companies Accounting Oversight Board (PCAOB)

http://pcaobus.org

Securities and Exchange Commission (SEC)

http://www.sec.gov/

SEC’s EDGAR database

http://www.sec.gov/edgar.shtml

State Board of Accountancy

http://www.aicpa.org/yellow/ypsboa.htm

PricewaterhouseCoopers’ 2010 Global Internal Audit Study

http://www.pwc.com/gx/en/press-room/2010/PwC-2010-Global-Internal-Audit-Study.jhtml

United Nations Panel of External Auditors

http://www.un.org/auditors/panel/

Assignments before Workshop One

1. Read the recommended URL’s, textbooks and other reference materials. Pay close

attention to the rubrics in the Appendix section. These rubrics will be used to assess your

knowledge and will be used to assess your knowledge, language skills and participation.

2. Research, define, and describe in no more than three paragraphs the role of these

institutions in the auditing process:

a. Public Companies Accounting Oversight Board (PCAOB)

b. The Sarbanes-Oxley Act

c. Securities and Exchange Commission

ACCO 710 Advanced Auditing lI 30

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

d. The United States General Accounting Office

e. SEC’s EDGAR database

3. Study the URLs addresses for this workshop and come prepared to discuss their content

in class.

4. Research and be prepared to discuss in class the similarities and differences between

financial statement audits, operational audits, and compliance audits. Give an example of

each type.

5. Research and be prepared to discuss in class the similarities and differences between the

roles of independent auditors, GAO auditors, internal revenue agents, and internal

auditors.

Activities:

1. General presentation of the course, module, students, and facilitator.

2. The facilitator will perform an ice breaking activity with students.

3. The facilitator will discuss with the students the subjects assigned.

4. The facilitator will divide the class into groups of three students to discuss an “URL”

provided for this workshop. The facilitator will assign to each group of students. The

groups will discuss their summaries in class of the information on it, and how does it

relate to any subject(s) discuss in the workshop.

5. Students will prepare on the whiteboard the exercises assigned during the workshop by

the facilitator and will discuss them with the rest of the class.

6. The facilitator will reinforce the concepts discussed in class with additional exercises as

necessary.

7. The students will begin working on their portfolios following the guidelines of portfolio

elaboration included in this module.

ACCO 710 Advanced Auditing lI 31

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

8. The facilitator explains the work to be completed before Workshop two.

9. The student will write a reflective diary to react critically about the concepts, feelings and

related attitudes about the subject matters covered in this workshop.

Assessment

Each student will be assessed based on:

1. Appendix A rubric for class participation.

2. Appendix D for the URL discussion.

3. Appendix E for the reflective diary.

4. Appendix M for the portfolio.

ACCO 710 Advanced Auditing lI 32

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Taller Dos

Objetivos Específicos

Al final el taller dos, los estudiantes:

1. Explicar el objetivo de conducir una auditoria de los estados financieros y de los

controles internos.

2. Identificar las fases de una auditoria de los estados financieros y el rol de un auditor

en cada una de ellas.

3. Diferenciar las responsabilidades del Gerente y del Auditor.

4. Entender los propósitos del uso de documentación de auditoria.

5. Identificar los diferentes tipos de evidencia en un proceso de auditoria y como los

registros de contabilidad son utilizados como evidencia de auditoria.

6. Entender los usos y limitaciones de los índices financieros y su aplicación en el

proceso de auditoria.

7. Explicar el proceso de planificación y ejecución de un proceso de auditoria.

Objetivos específicos de lenguaje:

1. Los estudiantes utilizarán estrategias efectivas para llevar a cabo discusiones formales

e informales incluyendo actividades de reflexión y análisis, respetando diversos

puntos de vista.

2. Los estudiantes utilizarán el proceso de lectura efectivamente.

3. Los estudiantes expresarán sus ideas en español oralmente de manera efectiva usando

organizadores gráficos.

Direcciones Electrónicas

Descripción de Trabajo de un Auditor Externo

ACCO 710 Advanced Auditing lI 33

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

http://www.ehow.com/about_5513152_external-auditor-job-description.html

Plan de Auditoria de un Auditor Externo

http://www.irs.gov/pub/irs-utl/proposed_wp_audit_plan_qihpg.pdf

Directorio de Auditores Externos

http://www.oas.org/documents/eng/boardexternalauditors.asp

Revista “Auditoria: Una Publicación de Practica y Teoría”

http://aaapubs.aip.org/aud/

Publicación “Contabilidad y Auditoria”

http://info.emeraldinsight.com/products/journals/journals.htm

Base de Datos SEC - EDGAR

http://www.sec.gov/edgar.shtml

El Instituto de Auditores Internos

http://www.theiia.org/

Public Companies Accounting Oversight Board (PCAOB)

http://pcaobus.org

Las 100 Firmas más importantes de Contabilidad en 2010

http://www.webcpa.com/news/Accounting-Today-Top-100-Firms-2010-53590-1.html

AICPA Código de Conducta Profesional

http://www.aicpa.org/About/code/index.html

Tareas a realizar antes del Taller Dos

1. Revise el contenido de las direcciones electrónicas del taller dos y vaya preparado/a al

salón para discutir los temas del taller.

2. Discutir las diferencias entre errores, fraudes y actos ilegales. Provea un ejemplo de cada

uno.

ACCO 710 Advanced Auditing lI 34

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

3. Completar los ejercicios asignados para este taller.

4. Los estudiantes prepararán un bosquejo del proceso de auditoria de los reportes anuales o

10-Ks de una empresa pública. Los estudiantes podrán utilizar la base de datos de la SEC

(EDGAR).

Actividades:

1. El facilitador comenzará la clase con un breve repaso.

2. El facilitador discutirá con los estudiantes los temas asignados.

3. En un ejercicio de torbellino de ideas, los estudiantes – con la ayuda del facilitador –

desarrollarán una lista que les ayude a explicar los distintos componentes del estado de

ingresos y gastos.

4. El facilitador asignará a cada grupo una dirección de Internet (URL) provista para el

taller. Cada grupo presentará un resumen sobre la información en el mismo y sobre cómo

ésta se relaciona a los temas discutidos en este taller

5. Los estudiantes reaccionarán a las presentaciones de sus compañeros, ya sea comentando

a favor de sus puntos sobre los temas, o retando los mismos exponiendo claramente su

posición.

6. Los estudiantes prepararán en la pizarra los ejercicios asignados durante el taller por el

facilitador.

7. El facilitador asignará ejercicios adicionales según crea conveniente para ampliar y/o

aclarar el conocimiento de los temas presentados, individual o en forma grupal.

8. Los estudiantes trabajarán en grupos en clase para evaluar reportes anuales o 10-Ks.

Deberán presentar el objetivo de una auditoria en relación a cada reporte anual e

identificar tanto el negocio del cliente así como la industria donde se desempeña el

negocio.

ACCO 710 Advanced Auditing lI 35

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

9. El facilitador mencionará las tareas a ser realizadas para el taller tres.

Avalúo

1. El Anejo A incluye la matriz de valoración para la participación en clase.

2. El Anejo C se utilizará para la actividad del bosquejo y bibliografía.

3. El Anejo D se utilizará para la actividad de “URL”.

4. El Anejo F se utilizará par la actividad de auto evaluación.

5. El Anejo G se utilizará para la actividad del torbellino de ideas.

ACCO 710 Advanced Auditing lI 36

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Workshop Three

Specific Objectives

At the end of this workshop, students will:

1. Describe the auditing process applied to the sales and collection cycle.

2. Identify the different accounts and classes of transactions in the sales and collection

cycle.

3. Understand the methodology for designing Tests of Controls and Substantive Tests of

Transactions for Sales.

4. Describe the auditing sampling process.

5. Indicate the four audit evidence decisions.

Specific Language Objectives

Students will:

1. Use cooperative learning strategies to analyze and discuss the URL content.

2. Write a clear and accurate report by describing the accounting basic principles using

appropriate vocabulary, grammar, and style.

3. Use the reading process effectively, present verbal comments, and support his /her ideas

about the subjects assigned for this workshop with facts.

URLs

Audit Sampling

http://findarticles.com/p/articles/mi_m4153/is_1_58/ai_71268474/

Managing risk

http://www.pwc.com/us/en/private-company-services/publications/managing-risk-internal-

controls.jhtml?WT.srch=1&wt.mc_id=MRK100401WS2

Audit committees

ACCO 710 Advanced Auditing lI 37

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

http://www.ey.com/US/en/Services/Assurance/External-Audit-Services/

Financial reporting issues for 2010

http://www.ey.com/US/en/Services/Assurance/BoardMatters-Quarterly--January-2010---

Financial-reporting-issues-for-2010

Fraud risks facing audit committees

http://www.ey.com/US/en/Services/Assurance/BoardMatters-Quarterly--January-2010---

Fraud-risks-facing-audit-committees

Compensation, risk, and the role of the audit committee

http://www.ey.com/Publication/vwLUAssets/ACLN_ViewPoints28_CompensationAndRisk_

CJ0150.pdf/$FILE/ACLN_ViewPoints28_CompensationAndRisk_CJ0150.pdf

Global resources for Auditors

http://www.auditnet.org/

Financial statement assertions

http://findarticles.com/p/articles/mi_m4153/is_2_61/ai_n6152651/

The Confirmation Process

http://www.aicpa.org/download/members/div/auditstd/AU-00330.PDF

Auditing Dictionary of Terms

http://www.ais-cpa.com/glosa.html

Assignments before Workshop Three

1. Prepare the exercises assigned for this workshop.

2. Revise the content of the Internet addresses, and come prepared to discuss in class the

subjects for this workshop.

3. Read, study, and come to class prepared to discuss the Substantive Tests of Accounts

Receivable Assertions.

ACCO 710 Advanced Auditing lI 38

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

4. Come prepared to actively participate in class.

Activities:

1. The facilitator will begin the class with a short review.

2. The facilitator will clarify any doubt about the subjects covered thus far in the course.

3. The facilitator will assign to each group of students an “URL” provided for this workshop.

The groups will discuss their summaries in class of the information on it, and how does it

relate to any subject(s) discuss in the workshop.

4. Students will prepare on the whiteboard the exercises assigned during the workshop by the

facilitator and will discuss them with the rest of the class.

5. The facilitator will reinforce the concepts discussed in class with additional exercises as

necessary.

6. Students will continue working on their portfolios and insert all the documents written

and/or completed so far, following the guidelines of portfolio elaboration.

7. Students will hand in the portfolio to the facilitator for its first partial evaluation.

8. The facilitator explains the work to be completed before Workshop four.

9. The facilitator will handle the take home exam to be submitted on Workshop Four.

10. The student will write a reflective diary to react critically about the concepts, feelings and

related attitudes about the subject matters covered in this workshop.

Assessment

Each student will be assessed based on:

1. Appendix A rubric for class participation.

2. Appendix D for the URL discussion.

3. Appendix E for the reflective diary.

4. Appendix M for the portfolio.

ACCO 710 Advanced Auditing lI 39

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Taller Cuatro

Objetivos específicos

Al final el taller cuatro, los estudiantes:

1. Indicar cómo reportar el efectivo y partidas relacionadas.

2. Distinguir las auditorias de las cuentas de ingreso y de gastos.

3. Efectuar los procedimientos de programas de auditoria para los ciclos de adquisiciones y

desembolsos de efectivo.

4. Identificar los distintos tipos de cuentas por cobrar.

5. Evaluar los métodos apropiados de desglosar las ventas y las cuentas por cobrar en los

estados financieros.

6. Reconocer los métodos correctos de contabilizar y valorar los pagarés por cobrar.

Objetivos específicos de lenguaje:

Los estudiantes:

1. Los estudiantes utilizarán estrategias efectivas para llevar a cabo discusiones formales e

informales incluyendo actividades de reflexión y análisis, respetando diversos puntos de

vista.

2. Los estudiantes utilizarán el proceso de lectura efectivamente.

3. Los estudiantes expresarán sus ideas en español oralmente de manera efectiva usando

organizadores gráficos.

Direcciones Electrónicas

Que es un Procedimiento Substantivo

http://www.blurtit.com/q170142.html

Pruebas Substantivas

ACCO 710 Advanced Auditing lI 40

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

http://www.answers.com/topic/substantive-test

Generalidades en la Auditoria

http://www.eumed.net/cursecon/libreria/rgl-genaud/1z.htm

Cómo realizar pruebas sustantivas efectivas?

http://www.consultenos.org/index.php?option=com_content&view=article&id=74:auditoria

&catid=1:latest-news&Itemid=18

Cómo realizar pruebas sustantivas del ciclo de ventas, cuentas por cobrar y recaudos, de

forma efectiva?

http://www.actualicese.com/opinion/como-realizar-pruebas-sustantivas-del-ciclo-de-ventas-

cuentas-por-cobrar-y-recaudos-de-forma-efectiva-nasaudit/

La Auditoria Contable

http://html.rincondelvago.com/auditoria-contable.html

El planeamiento de la auditoría y las pruebas sustantivas o de validación

http://www.contadoresyempresas.com.pe/boletines_revistas/setiembre_05/bc_06_09.pdf

Cómo realizar pruebas sustantivas en el ciclo de compras, cuentas por pagar y desembolsos?

http://www.actualicese.com/opinion/como-realizar-pruebas-sustantivas-en-el-ciclo-de-

compras-cuentas-por-pagar-y-desembolsos-nasaudit/

Pruebas Sustantivas antes de la fecha de cierre de los estados financieros

http://www.ayudacontador.cl/ayudacontador/nagas/313.html

Evidencia de Auditoria

http://fccea.unicauca.edu.co/old/muestreo.htm

ACCO 710 Advanced Auditing lI 41

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Tareas a realizar antes del Taller Cuatro

1. Preparar los ejercicios asignados para este taller y el examen para la cas entregado

durante el taller anterior.

2. Revise el contenido de las direcciones electrónicas del taller cuatro y vaya preparado/a al

salón para discutir los temas del taller.

3. Determinar el numero total de facturas y el total de facturas sin pagar en circulación para

compararlas con el mayor general (general ledger)

4. Describir las funciones de negocios y los documentos relacionados y los registros en el

ciclo de pago y adquisición.

5. Entender el control interno y el diseño y realizar las pruebas de control y las pruebas

substantivas de las transacciones para los ciclos de pago y adquisición.

6. Describir la metodología para diseñar las pruebas de detalles de los balances para las

cuentas a pagar utilizando el modelo de riesgo de la auditoria.

Actividades:

1. El facilitador comenzará la clase con un repaso breve.

2. El facilitador discutirá con los estudiantes los temas asignados.

3. El facilitador asignará a cada grupo una dirección de Internet (URL) provista para el

taller. Cada grupo presentará un resumen sobre la información en el mismo y sobre cómo

ésta se relaciona a los temas discutidos en este taller

4. El facilitador dividirá la clase en cuatro grupos pequeños. Cada grupo seleccionará un

proceso/tema de los asignados para el taller para representarlo en una discusión utilizando

la técnica del debate.

5. Los estudiantes prepararán en la pizarra los ejercicios asignados durante el taller por el

facilitador.

ACCO 710 Advanced Auditing lI 42

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

6. El facilitador asignará ejercicios adicionales según crea conveniente para ampliar y/o

aclarar el conocimiento de los temas presentados, individual o en forma grupal.

7. Los estudiantes reaccionarán a las presentaciones de sus compañeros, ya sea comentando

a favor de sus puntos sobre los temas, o retando los mismos exponiendo claramente su

posición.

8. Los estudiantes continuarán trabajando en sus portafolios siguiendo las indicaciones

dadas en este módulo.

9. Los estudiantes prepararán una evaluación propia sobre su desempeño en el taller.

10. El facilitador explicará las tareas a ser completadas antes del Taller cinco.

Avalúo

1. El Anejo A incluye la matriz de valoración para la participación en clase.

2. El Anejo G se utilizará para la actividad del debate.

3. El Anejo D se utilizará para la actividad de “URL”.

4. El Anejo F se utilizará par la actividad de auto evaluación.

ACCO 710 Advanced Auditing lI 43

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Workshop Five/Taller Cinco

NOTA: Este taller es bilingüe. Tanto, el

Facilitador como los estudiantes,

deberán utilizar el idioma asignado para

cada tarea y actividad.

NOTE: This is a bilingual workshop.

Both the facilitator and student should

use the language assigned for each

homework and activity.

Specific Objectives

At the end of this workshop, students will:

1. Identify the auditor’s responsibilities that occur at the end of the audit.

2. Distinguish between the auditor responsibilities at the end of the audit and the post-audit

responsibilities.

3. Understand the internal controls over financial reporting.

4. Identify the auditor’s responsibilities for illegal acts.

5. Understand the variety of attest and assurance services.

6. Understand the role of the CPA in the auditing process.

Specific Language Objectives

Students will:

1. Use cooperative learning strategies to analyze and discuss the URL content in English.

2. Write, in Spanish, a clear and accurate report by describing the accounting basic

principles using appropriate vocabulary, grammar, and style.

3. Use the reading process effectively, present verbal comments in English, and support his

/her ideas about the subjects assigned for this workshop with facts.

ACCO 710 Advanced Auditing lI 44

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

ULRs

Audit Committee Effectiveness Center

http://www.aicpa.org/audcommctr/homepage.htm

Audit Committee

http://www.corpgov.deloitte.com/site/us/audit-

committee/;jsessionid=JM1TLXyZySC5VKlGND6vpsRVLnyrnbL2cdM8gkDpy2w2SbSKb

L0N!-860565013!505087471

Audit documentation review

http://www.aicpa.org/download/members/div/auditstd/AU-00339.PDF

Auditing Standard No. 3 - Audit Documentation

http://pcaobus.org/Standards/Auditing/Pages/Auditing_Standard_3.aspx

The Association of College and University Auditors (ACUA)

http://www.acua.org/

Audit Legal Representation Letter Guidance

http://www.fasab.gov/aapc/legalgud.htm

Letter of Representation

http://www.answers.com/topic/letter-of-representation

The Management Representation Letter

http://www.pkfnewyork.com/Publications/PDF/Perspectives-RepLtrs-FINAL%204_06.pdf

Engagement Letters

http://www.rigos.net/loss_control/LC_Engage.shtml

Auditing documents

http://www.cpadirectory.com/cpasecretary/list.cfm

Assignments before Workshop Five

ACCO 710 Advanced Auditing lI 45

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

1. Work on the exercises assigned for this workshop.

2. Revise the content of the Internet addresses, and come prepared to discuss in class the

subjects for this workshop.

3. Prepare and discuss in class:

a. What is the purpose of a client representation letter and what should be included

in the letter?

b. Discuss the purposes of performing analytical procedures during the audit

completion phase.

c. Discuss the three matters which Sarbanes-Oxley requires auditors of public

companies to report to the audit committee.

4. Complete your Final Project

Activities:

1. The facilitator will start the class with a short review and will clarify any doubt of the

material covered in this course thus far (in Spanish).

2. Students will discuss their essays (in Spanish).

3. The facilitator will start the class with a short review (in Spanish).

4. The facilitator will clarify any doubt about the subjects covered thus far in the course (in

Spanish).

5. The facilitator will assign to each group of students an “URL” provided for this

workshop. The groups will discuss their summaries in class of the information on it, and

how does it relate to any subject(s) discuss in the workshop (in English).

6. Students will prepare on the whiteboard the exercises assigned during the workshop by

the facilitator and will discuss them with the rest of the class (in English).

ACCO 710 Advanced Auditing lI 46

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

7. The facilitator will reinforce the concepts discussed in class with additional exercises as

necessary (in English).

8. Students will continue working on their portfolios and insert all the documents written

and/or completed so far, following the guidelines of portfolio elaboration.

9. Students will hand in the portfolio to the facilitator for its partial evaluation.

10. The groups present their final projects (in Spanish).

11. The student will write a reflective diary to react critically about the concepts, feelings and

related attitudes about the subject matters covered in this workshop (in English).

Assessment

Each student will be assessed based on:

1. Appendix A rubric for class participation.

2. Appendix D for the URL discussion.

3. Appendix E for the reflective diary.

4. Appendix M for the portfolio.

5. Appendixes B and C for the evaluation of the final project.

6. Appendix Q for the final project.

ACCO 710 Advanced Auditing lI 47

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Anejos/Appendices

ACCO 710 Advanced Auditing lI 48

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

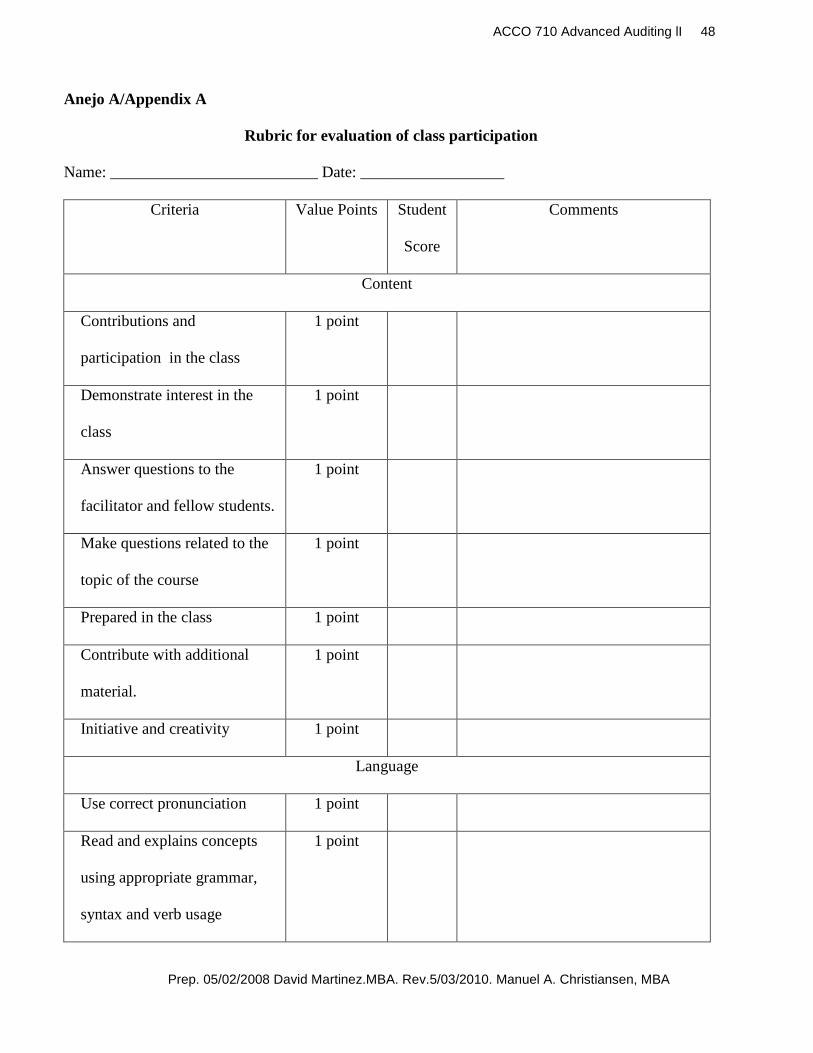

Anejo A/Appendix A

Rubric for evaluation of class participation

Name: __________________________ Date: __________________

Criteria Value Points Student

Score

Comments

Content

Contributions and

participation in the class

1 point

Demonstrate interest in the

class

1 point

Answer questions to the

facilitator and fellow students.

1 point

Make questions related to the

topic of the course

1 point

Prepared in the class 1 point

Contribute with additional

material.

1 point

Initiative and creativity 1 point

Language

Use correct pronunciation 1 point

Read and explains concepts

using appropriate grammar,

syntax and verb usage

1 point

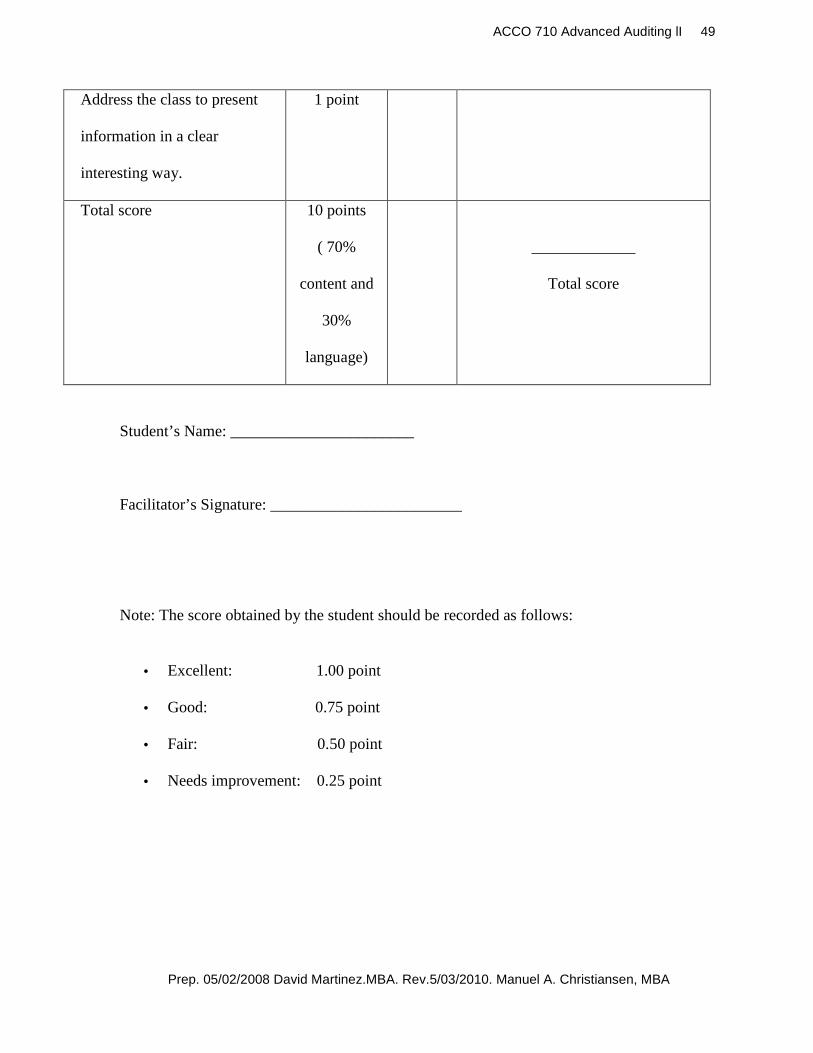

ACCO 710 Advanced Auditing lI 49

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Address the class to present

information in a clear

interesting way.

1 point

Total score 10 points

( 70%

content and

30%

language)

_____________

Total score

Student’s Name: _______________________

Facilitator’s Signature: ________________________

Note: The score obtained by the student should be recorded as follows:

• Excellent: 1.00 point

• Good: 0.75 point

• Fair: 0.50 point

• Needs improvement: 0.25 point

ACCO 710 Advanced Auditing lI 50

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

Anejo B/Appendix B

Matriz de valoración de la presentación oral

Integrantes del grupo _______________________________________________

Curso: ______________________ Fecha: ________________________

Tema: _______________________ Tiempo: ________________________

Criterios Valor Puntaje obtenido

Presentación

Mantiene la atención de toda la audiencia

utilizando el contacto visual directo, y mirando

las notas raramente.

1 punto

Los movimientos son adecuados y ayudan a la

audiencia a visualizar el contenido de la

presentación.

1 punto

El estudiante demuestra estar relajado y

tranquilo, sin hacer errores.

1 punto

El estudiante utiliza una voz clara con Buena

proyección y entonación.

1 punto

El estudiante demuestra un conocimiento

completo al responder todas las preguntas con

explicaciones y elaboraciones.

1 punto

El estudiante presenta la información en una 1 punto

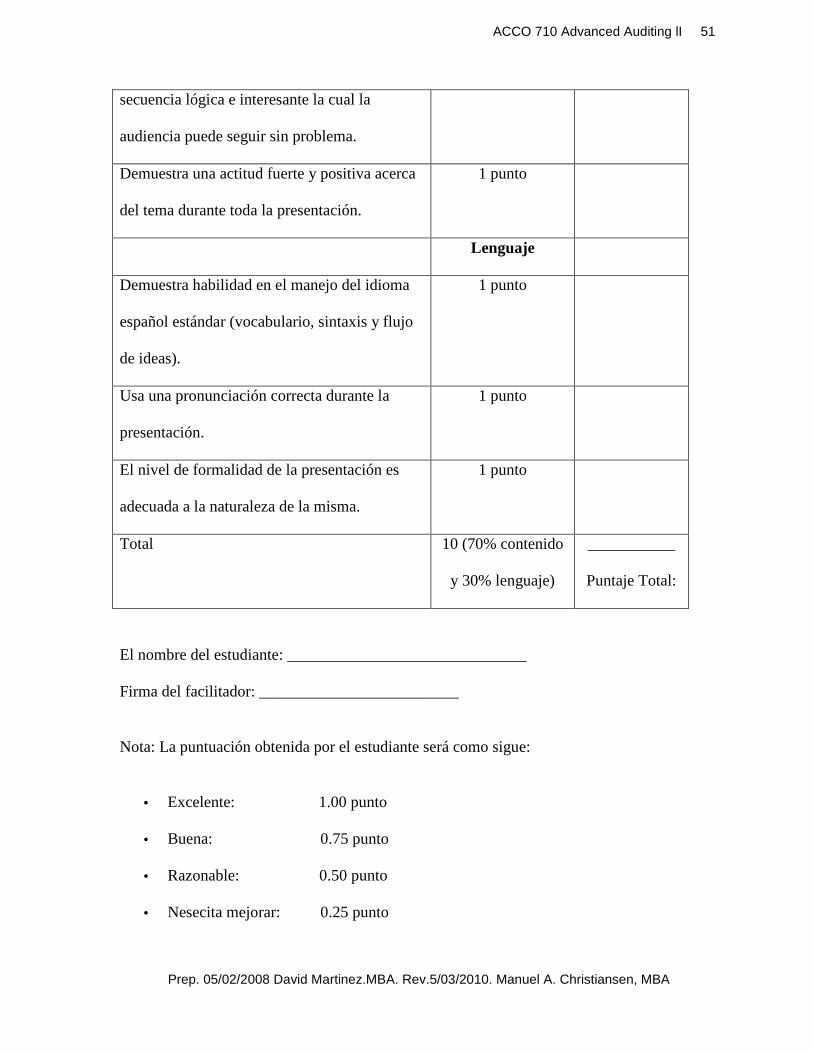

ACCO 710 Advanced Auditing lI 51

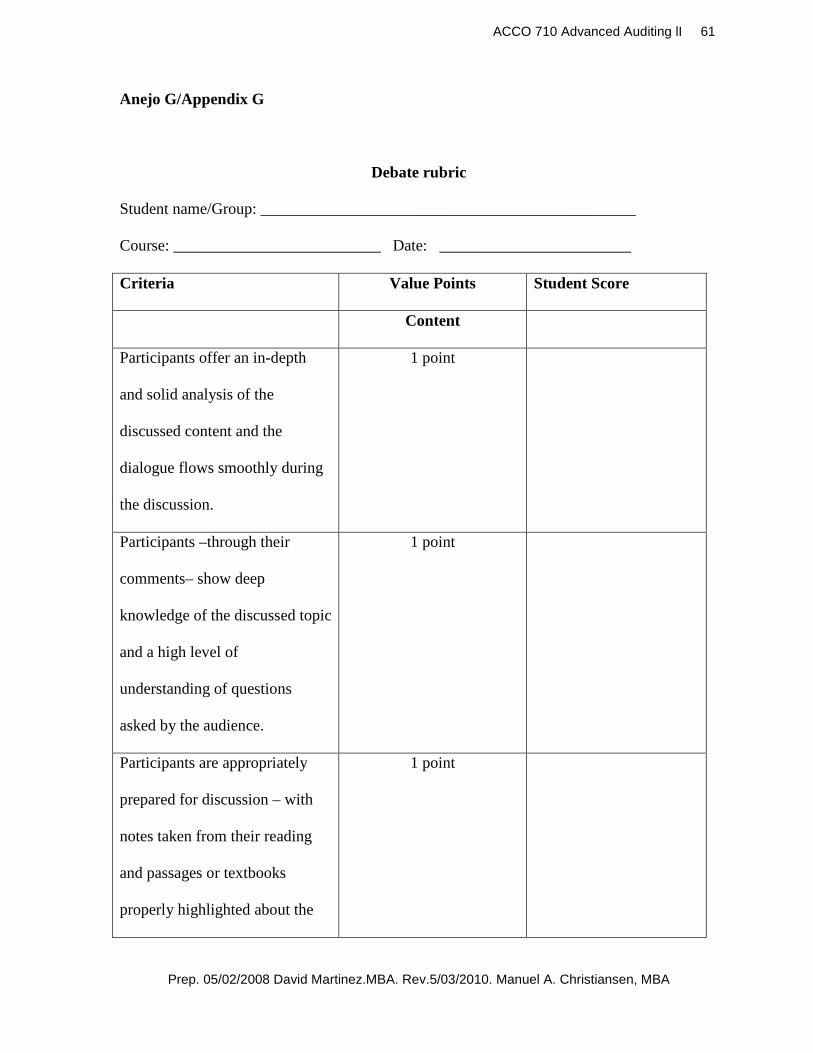

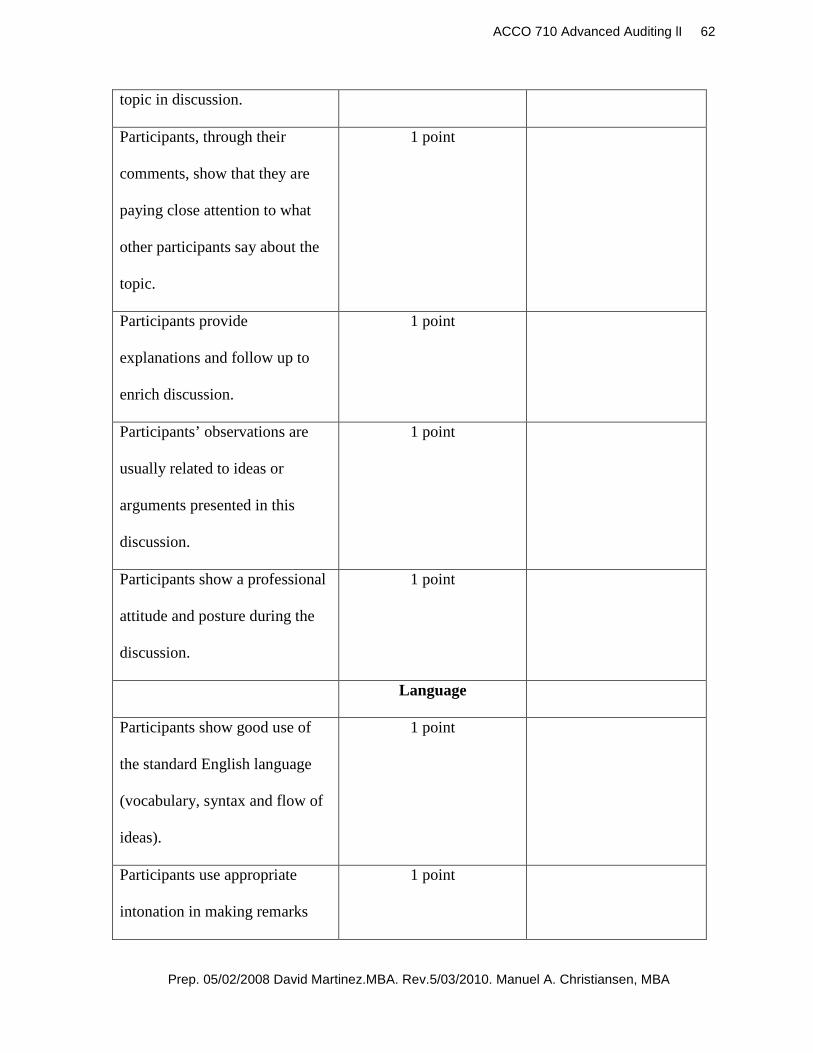

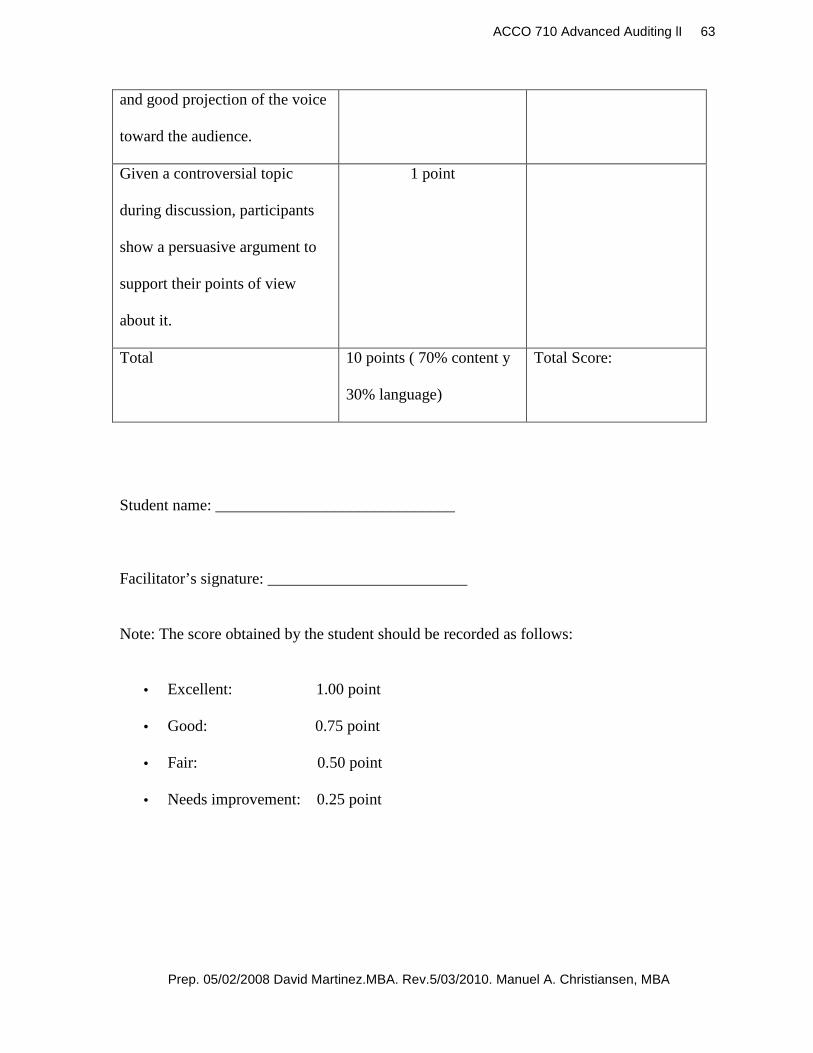

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

secuencia lógica e interesante la cual la

audiencia puede seguir sin problema.

Demuestra una actitud fuerte y positiva acerca

del tema durante toda la presentación.

1 punto

Lenguaje

Demuestra habilidad en el manejo del idioma

español estándar (vocabulario, sintaxis y flujo

de ideas).

1 punto

Usa una pronunciación correcta durante la

presentación.

1 punto

El nivel de formalidad de la presentación es

adecuada a la naturaleza de la misma.

1 punto

Total 10 (70% contenido

y 30% lenguaje)

___________

Puntaje Total:

El nombre del estudiante: ______________________________

Firma del facilitador: _________________________

Nota: La puntuación obtenida por el estudiante será como sigue:

• Excelente: 1.00 punto

• Buena: 0.75 punto

• Razonable: 0.50 punto

• Nesecita mejorar: 0.25 punto

ACCO 710 Advanced Auditing lI 52

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

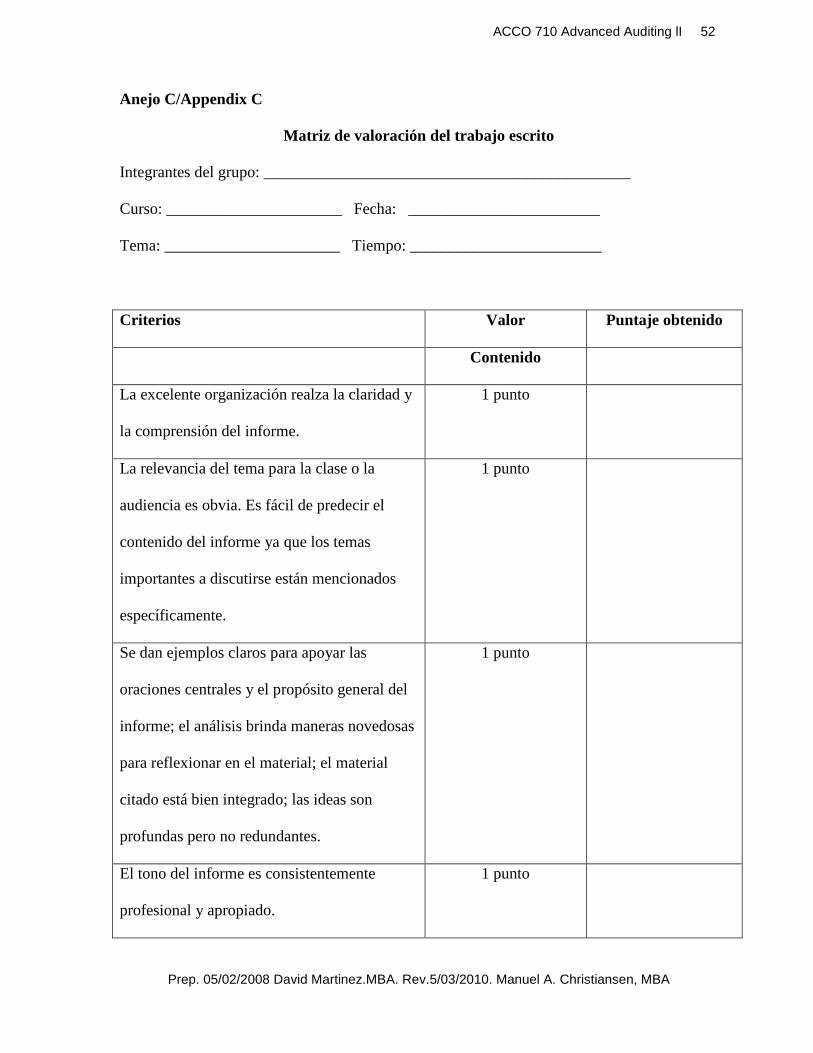

Anejo C/Appendix C

Matriz de valoración del trabajo escrito

Integrantes del grupo: ______________________________________________

Curso: ______________________ Fecha: ________________________

Tema: ______________________ Tiempo: ________________________

Criterios Valor Puntaje obtenido

Contenido

La excelente organización realza la claridad y

la comprensión del informe.

1 punto

La relevancia del tema para la clase o la

audiencia es obvia. Es fácil de predecir el

contenido del informe ya que los temas

importantes a discutirse están mencionados

específicamente.

1 punto

Se dan ejemplos claros para apoyar las

oraciones centrales y el propósito general del

informe; el análisis brinda maneras novedosas

para reflexionar en el material; el material

citado está bien integrado; las ideas son

profundas pero no redundantes.

1 punto

El tono del informe es consistentemente

profesional y apropiado.

1 punto

ACCO 710 Advanced Auditing lI 53

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

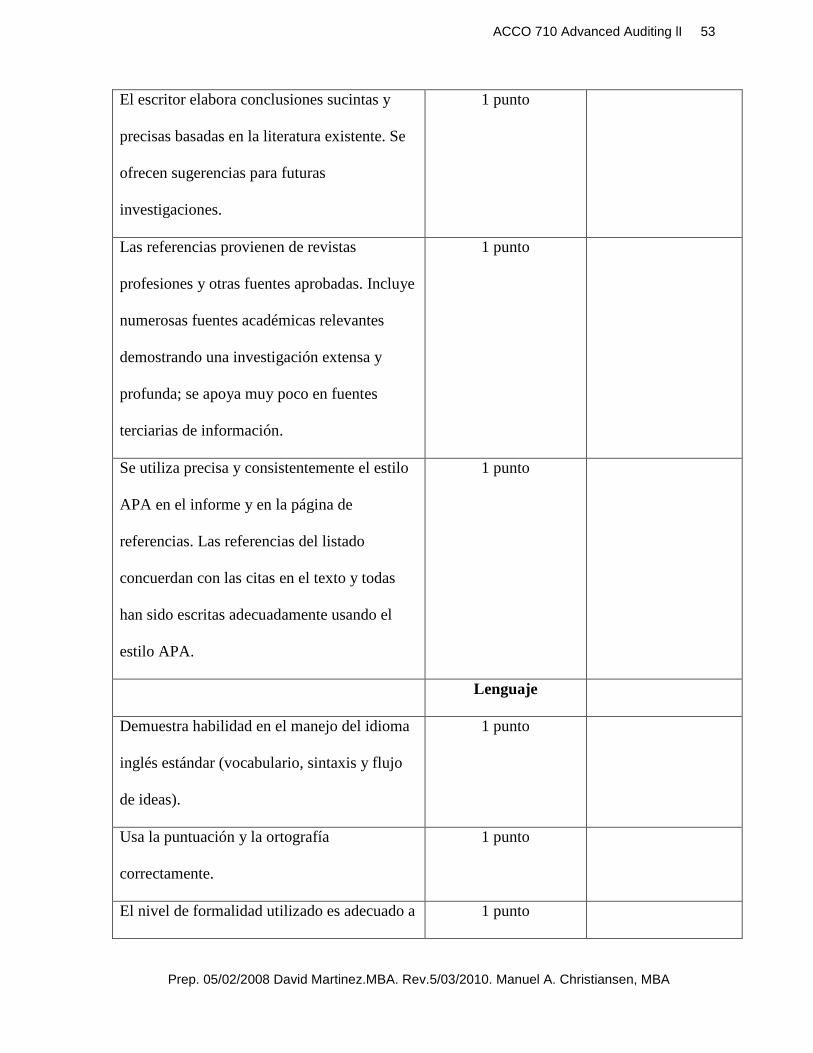

El escritor elabora conclusiones sucintas y

precisas basadas en la literatura existente. Se

ofrecen sugerencias para futuras

investigaciones.

1 punto

Las referencias provienen de revistas

profesiones y otras fuentes aprobadas. Incluye

numerosas fuentes académicas relevantes

demostrando una investigación extensa y

profunda; se apoya muy poco en fuentes

terciarias de información.

1 punto

Se utiliza precisa y consistentemente el estilo

APA en el informe y en la página de

referencias. Las referencias del listado

concuerdan con las citas en el texto y todas

han sido escritas adecuadamente usando el

estilo APA.

1 punto

Lenguaje

Demuestra habilidad en el manejo del idioma

inglés estándar (vocabulario, sintaxis y flujo

de ideas).

1 punto

Usa la puntuación y la ortografía

correctamente.

1 punto

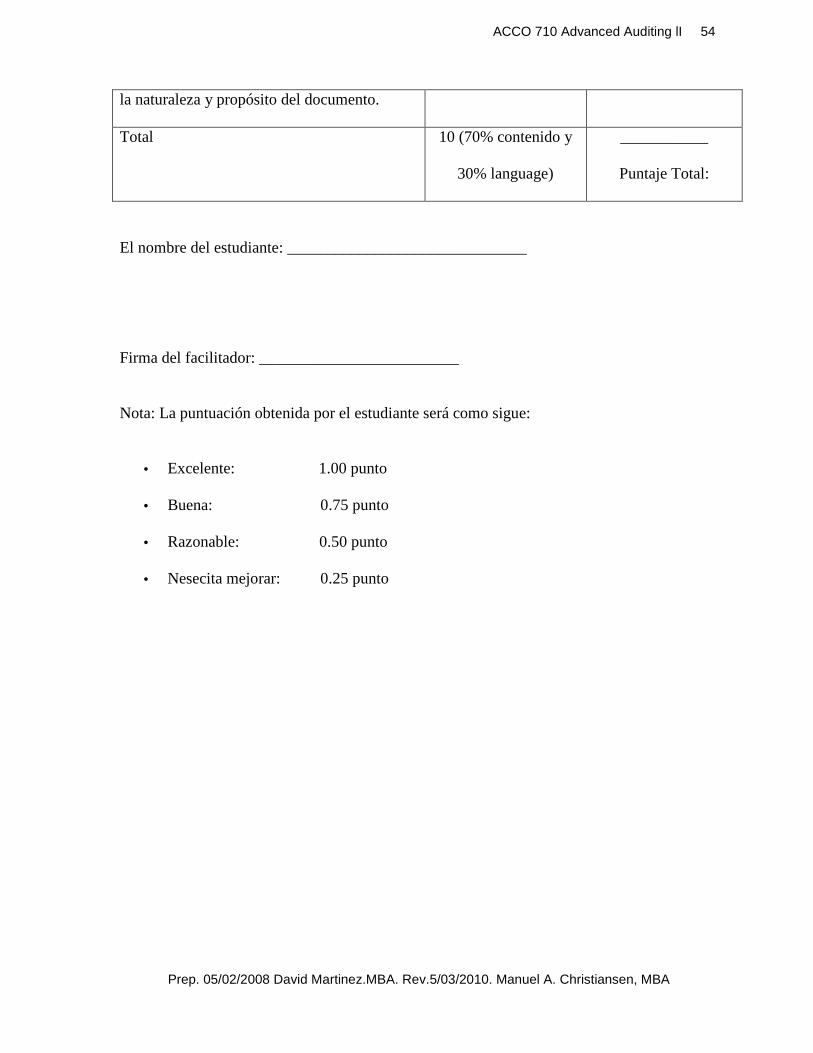

El nivel de formalidad utilizado es adecuado a 1 punto

ACCO 710 Advanced Auditing lI 54

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

la naturaleza y propósito del documento.

Total 10 (70% contenido y

30% language)

___________

Puntaje Total:

El nombre del estudiante: ______________________________

Firma del facilitador: _________________________

Nota: La puntuación obtenida por el estudiante será como sigue:

• Excelente: 1.00 punto

• Buena: 0.75 punto

• Razonable: 0.50 punto

• Nesecita mejorar: 0.25 punto

ACCO 710 Advanced Auditing lI 55

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

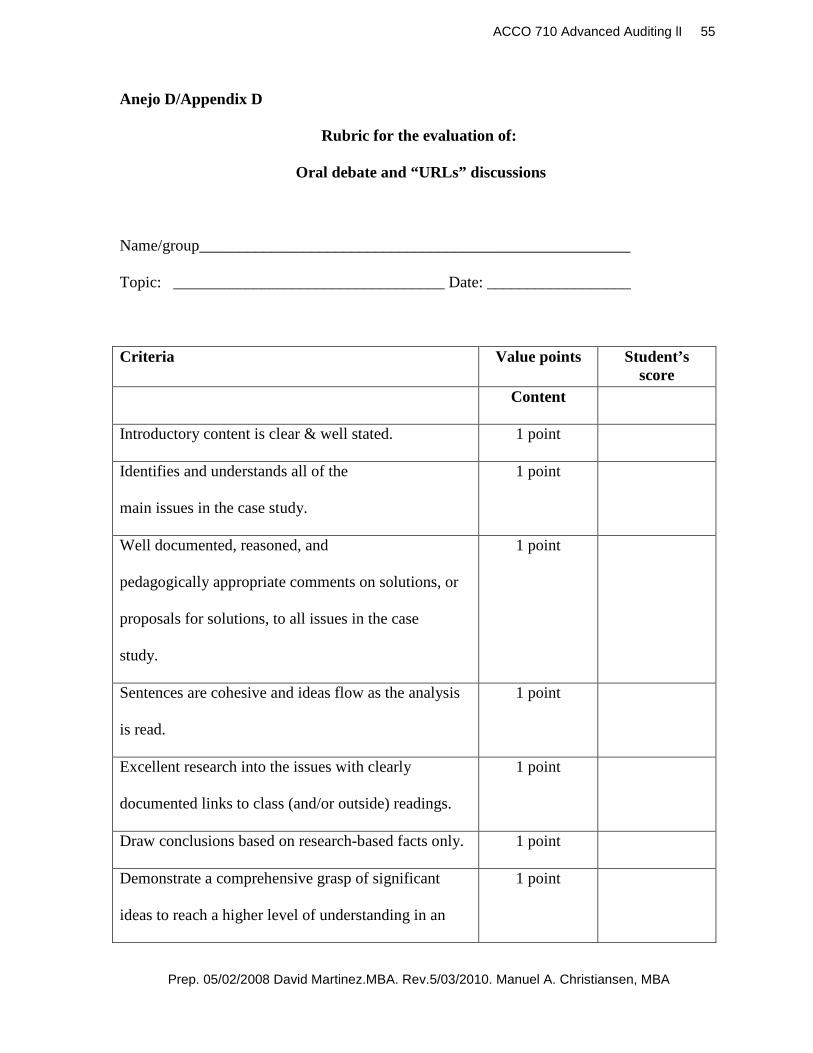

Anejo D/Appendix D

Rubric for the evaluation of:

Oral debate and “URLs” discussions

Name/group______________________________________________________

Topic: __________________________________ Date: __________________

Criteria Value points Student’s score

Content

Introductory content is clear & well stated. 1 point

Identifies and understands all of the

main issues in the case study.

1 point

Well documented, reasoned, and

pedagogically appropriate comments on solutions, or

proposals for solutions, to all issues in the case

study.

1 point

Sentences are cohesive and ideas flow as the analysis

is read.

1 point

Excellent research into the issues with clearly

documented links to class (and/or outside) readings.

1 point

Draw conclusions based on research-based facts only. 1 point

Demonstrate a comprehensive grasp of significant

ideas to reach a higher level of understanding in an

1 point

ACCO 710 Advanced Auditing lI 56

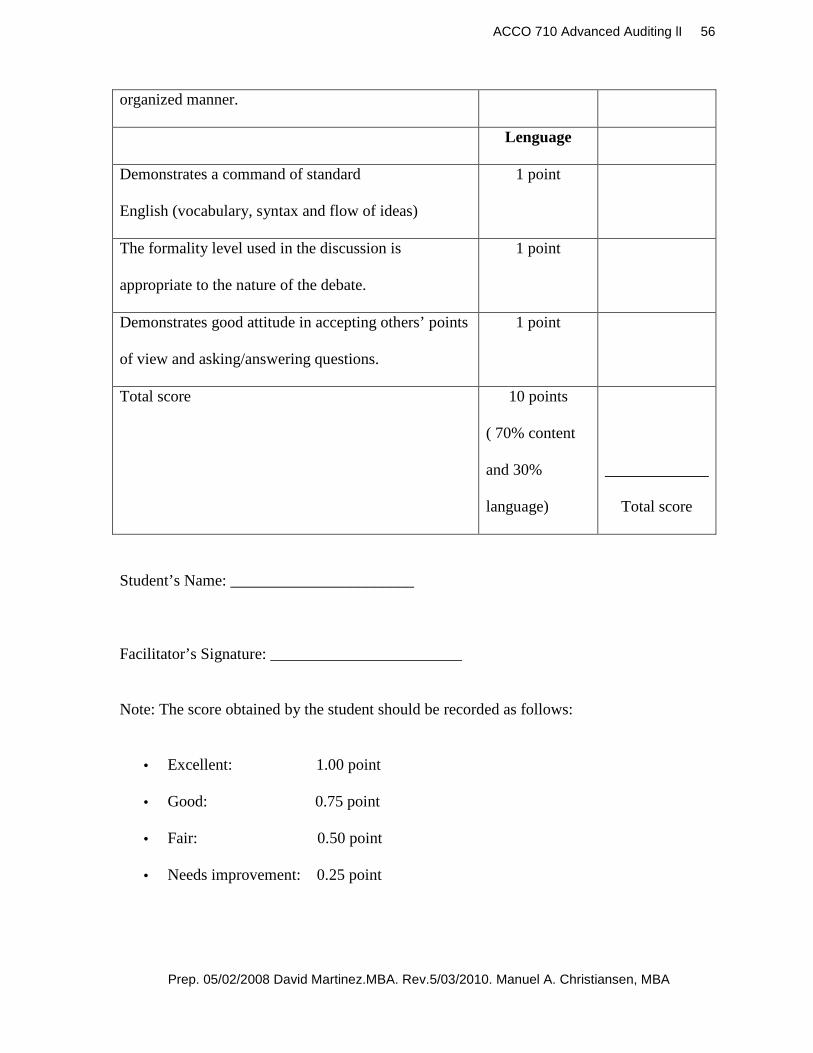

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

organized manner.

Lenguage

Demonstrates a command of standard

English (vocabulary, syntax and flow of ideas)

1 point

The formality level used in the discussion is

appropriate to the nature of the debate.

1 point

Demonstrates good attitude in accepting others’ points

of view and asking/answering questions.

1 point

Total score 10 points

( 70% content

and 30%

language)

_____________

Total score

Student’s Name: _______________________

Facilitator’s Signature: ________________________

Note: The score obtained by the student should be recorded as follows:

• Excellent: 1.00 point

• Good: 0.75 point

• Fair: 0.50 point

• Needs improvement: 0.25 point

ACCO 710 Advanced Auditing lI 57

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

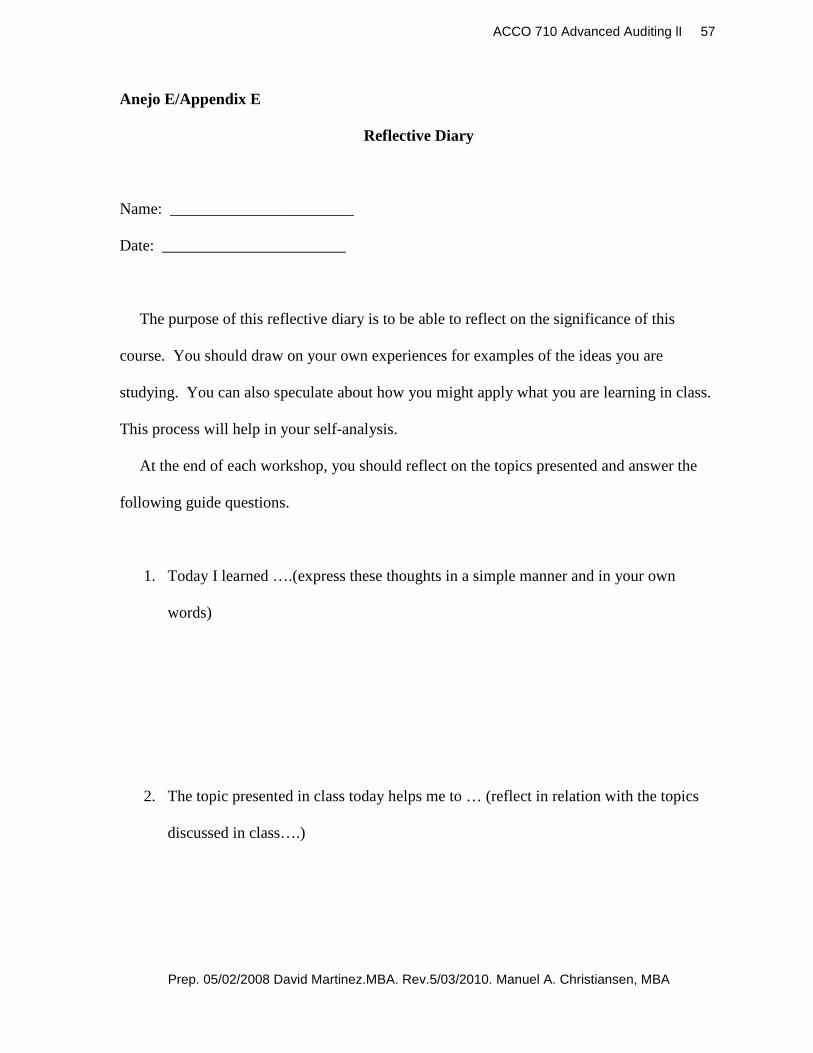

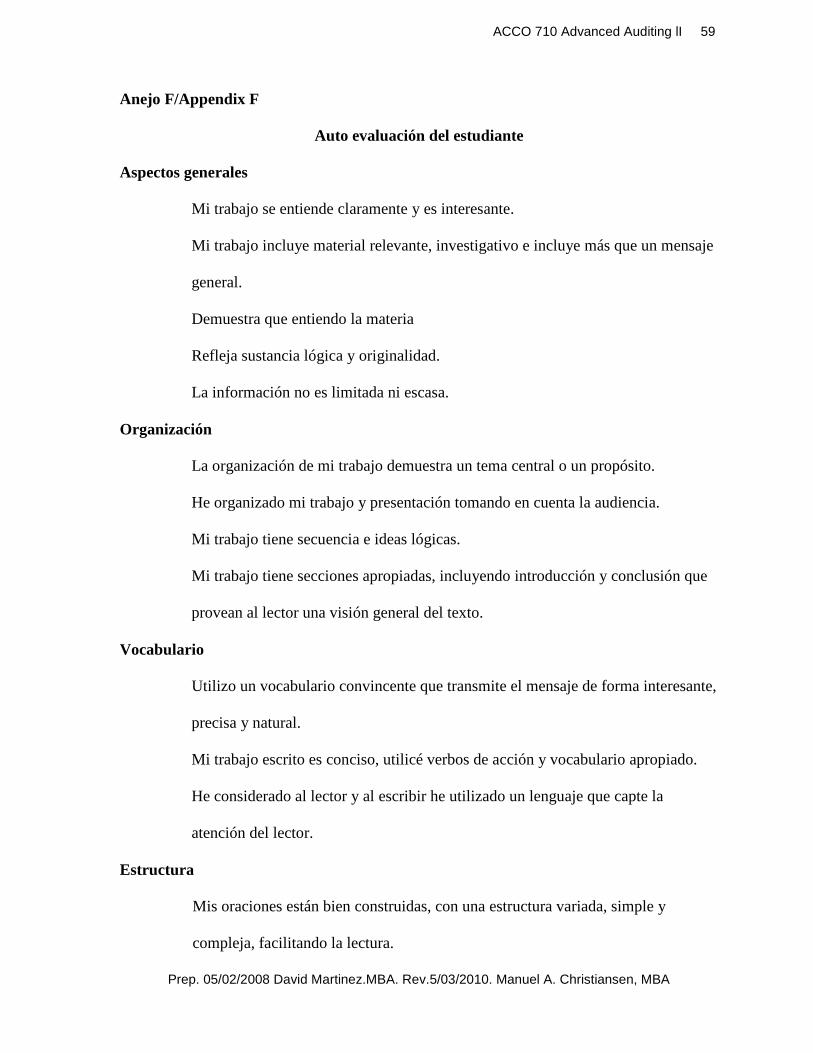

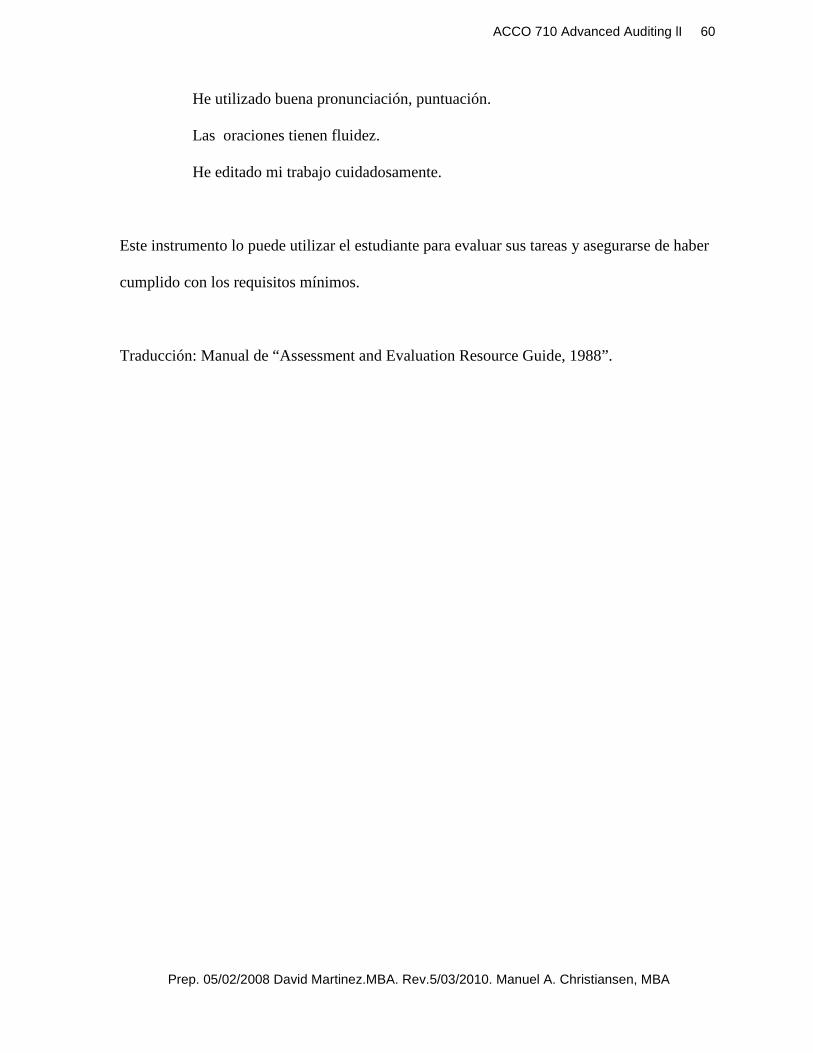

Anejo E/Appendix E

Reflective Diary

Name: _______________________

Date: _______________________

The purpose of this reflective diary is to be able to reflect on the significance of this

course. You should draw on your own experiences for examples of the ideas you are

studying. You can also speculate about how you might apply what you are learning in class.

This process will help in your self-analysis.

At the end of each workshop, you should reflect on the topics presented and answer the

following guide questions.

1. Today I learned ….(express these thoughts in a simple manner and in your own

words)

2. The topic presented in class today helps me to … (reflect in relation with the topics

discussed in class….)

ACCO 710 Advanced Auditing lI 58

Prep. 05/02/2008 David Martinez.MBA. Rev.5/03/2010. Manuel A. Christiansen, MBA

3. I can apply what was presented in class today to some aspects of my personal life or

to any other past experience …