Embed Size (px)

Citation preview

Acosta Corporation:-Transactions effect on Accounting cycle of 2011 and 2012

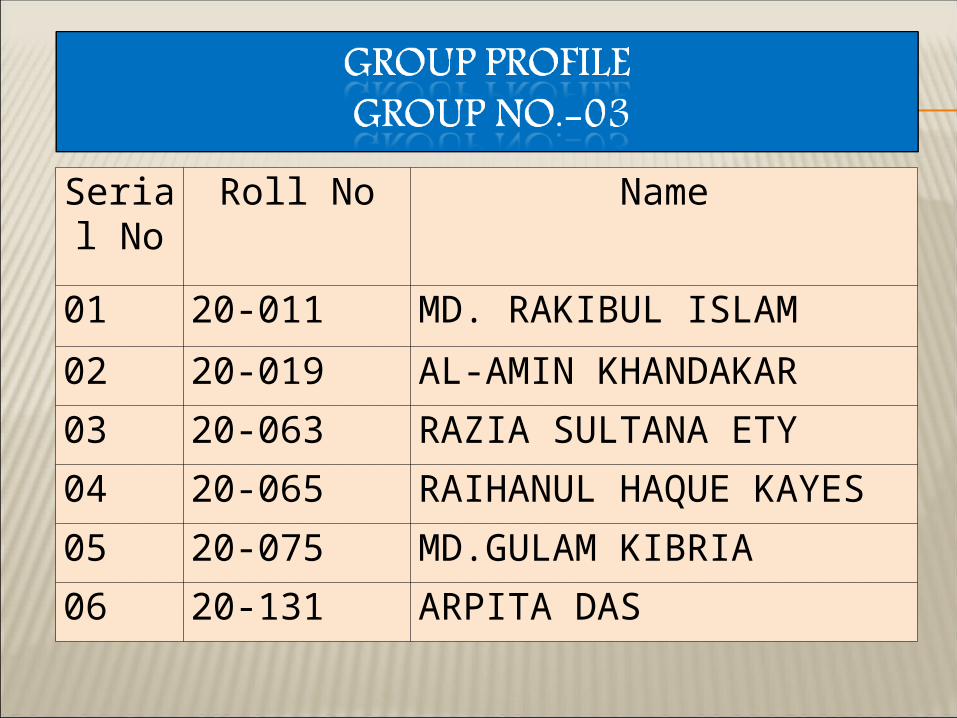

Serial No

Roll No Name

01 20-011 MD. RAKIBUL ISLAM

02 20-019 AL-AMIN KHANDAKAR

03 20-063 RAZIA SULTANA ETY

04 20-065 RAIHANUL HAQUE KAYES

05 20-075 MD.GULAM KIBRIA

06 20-131 ARPITA DAS

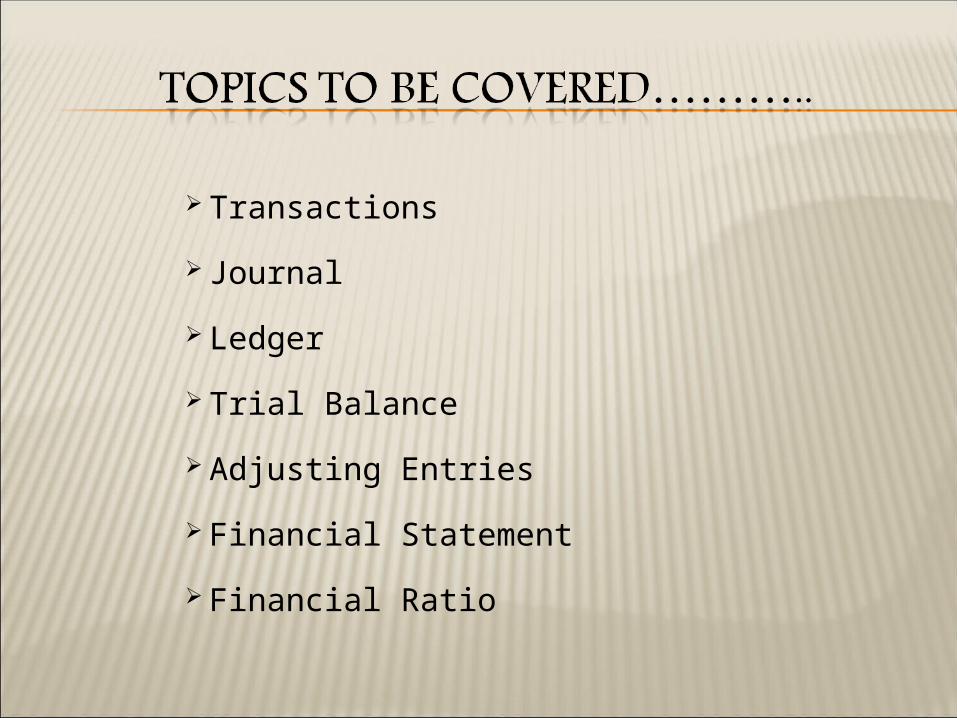

Transactions

Journal

Ledger

Trial Balance

Adjusting Entries

Financial Statement

Financial Ratio

Md. Rakibul Islam

ID: 20-011

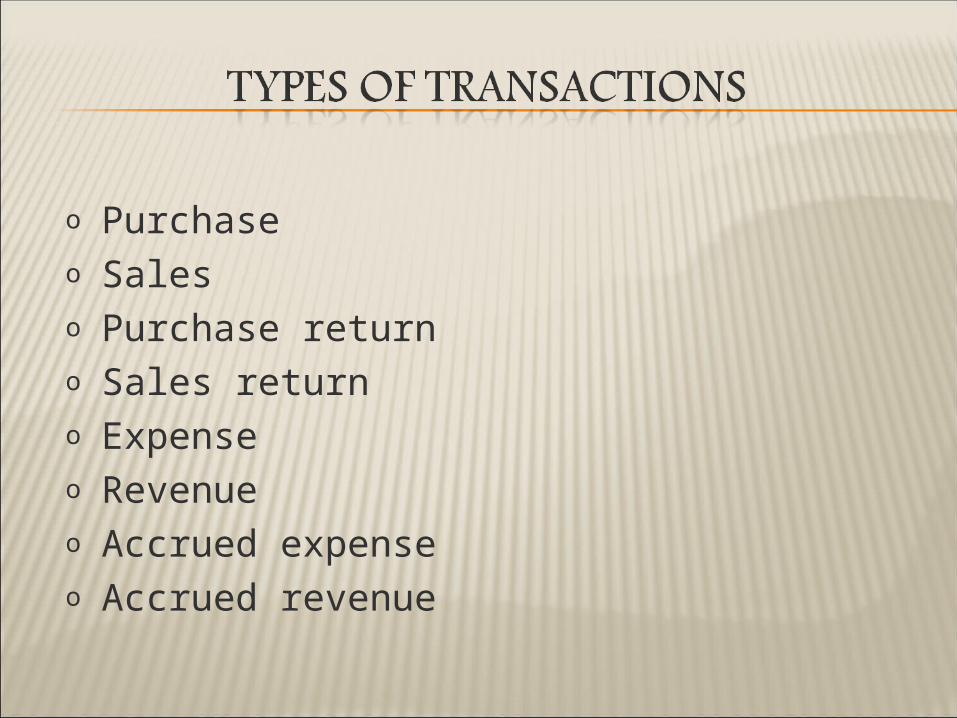

o Purchaseo Saleso Purchase returno Sales returno Expenseo Revenueo Accrued expenseo Accrued revenue

• Prepaid expense• Prepaid revenue• Unearned expense• Unearned revenue• Depreciation

Jan 1: Mr. ShihabHasan started a furniture business with BDT 5,00,000, Land of BDT 7,50,000,Equipment BDT 2,00,000 and Office supplies of BDT 70,000 and merchandise of BDT 3,00,000.

Jan 5: Sold Merchandise for BDT 25,000 to Mr. Rahim, granting the customer terms of 2/10, EOM.The cost of the merchandise was BDT 18000.

Jan 9: Purchased merchandise from Mr.Karim for cash BDT 50,000 Jan 15: Paid freight charge BDT 2,000 in cash for the merchandise purchased

in Jan 9 Jan 18: Brought a truck for the transportation of Furniture BDT 1,00,000 in

cash Jan 30: Paid salaries of employee BDT 40,000 in cash

Now Presenting…… MD. GULAM KIBRIA

ID:20-075

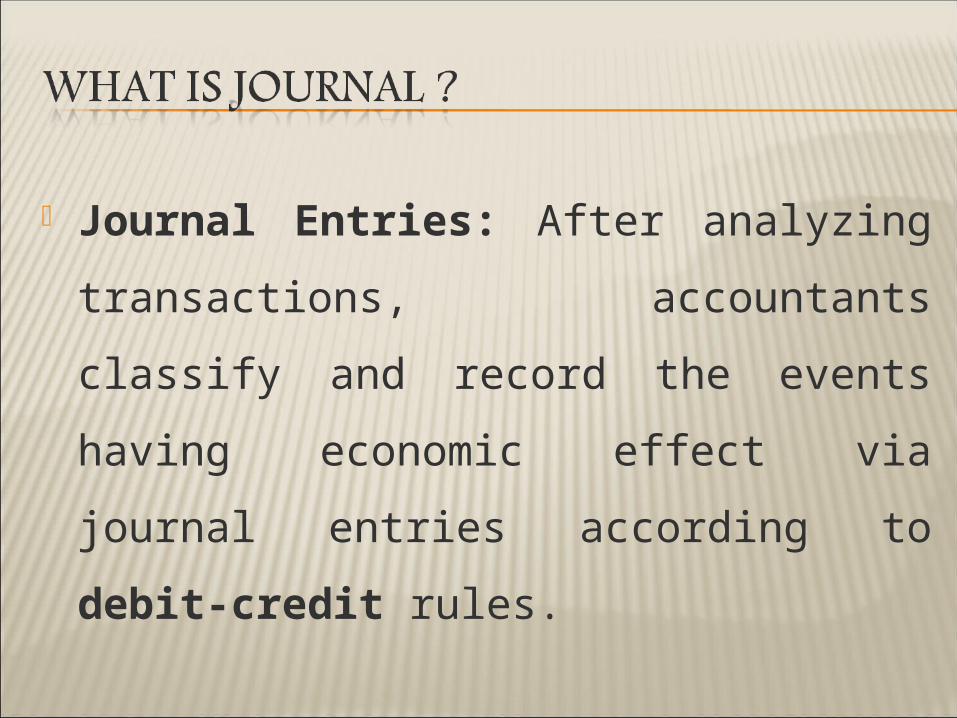

Journal Entries: After analyzing

transactions, accountants classify and

record the events having economic

effect via journal entries according to

debit-credit rules.

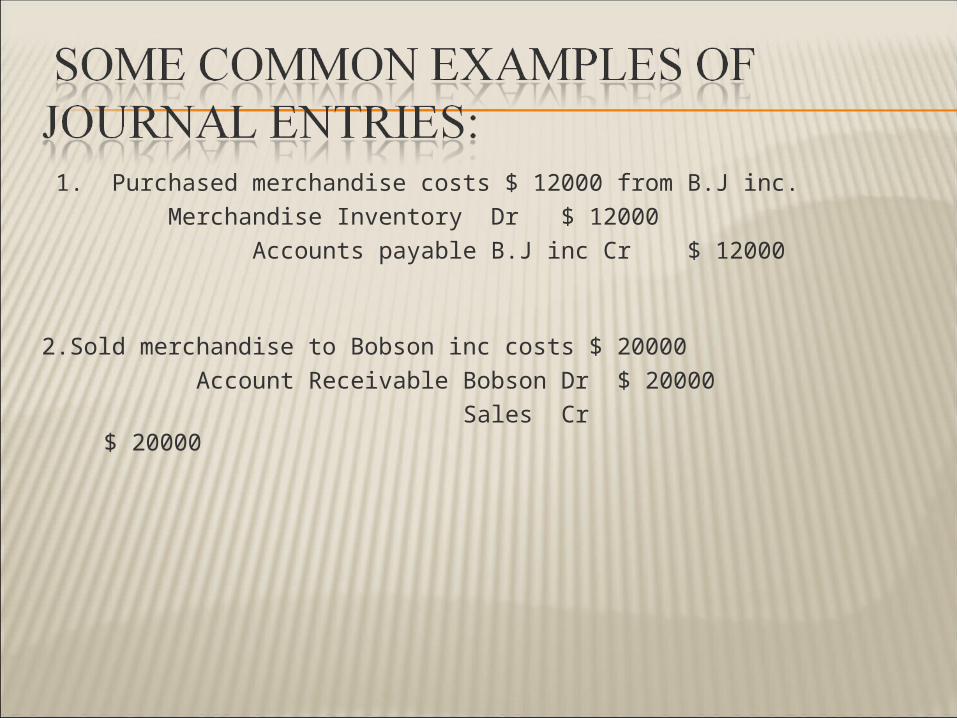

1. Purchased merchandise costs $ 12000 from B.J inc.

Merchandise Inventory Dr $ 12000

Accounts payable B.J inc Cr $ 12000

2.Sold merchandise to Bobson inc costs $ 20000

Account Receivable Bobson Dr $ 20000

Sales Cr $ 20000

3.Unpaid salaries costs $7000

Salaries expense Dr $7000

Salaries payable Cr $7000

4. The Company prepaid insurance premium of $60000

Prepaid insurance Dr $60000

Insurance expense Cr $60000

Now Presenting……RAZIA SULTANA ETY

ID:20-063

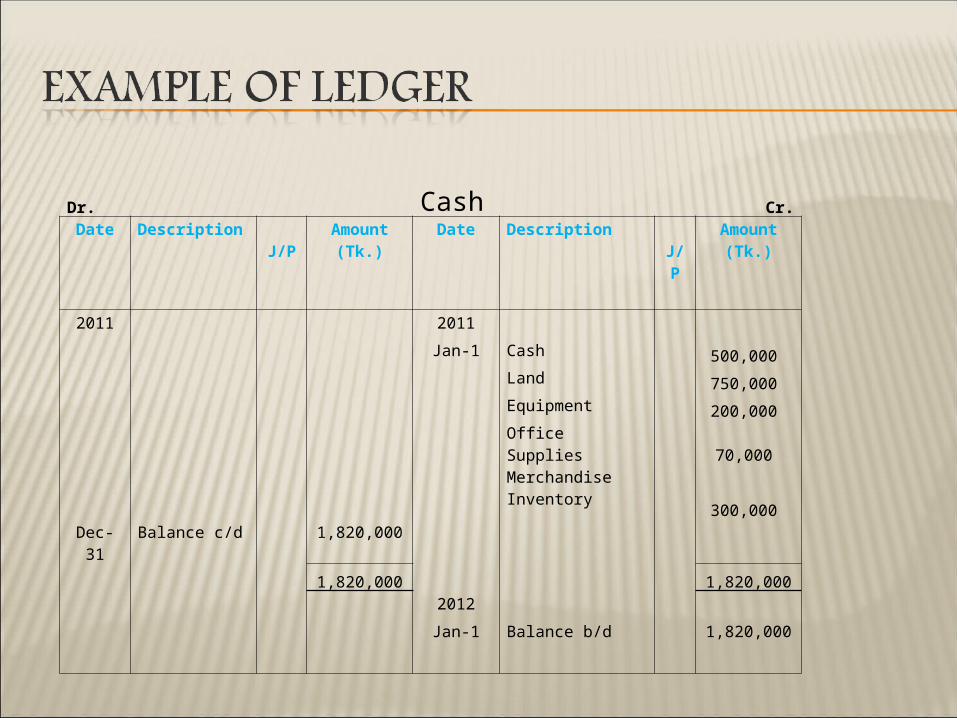

Ledger Accounts: The debit and credit values of journal entries are transferred to ledger accounts one by one in such a way that debit amount of a journal entry is transferred to the debit side of the relevant ledger account and the credit amount is transferred to the credit side of the relevant ledger account

Dr. Cash Cr.Date Description J/P Amount

(Tk.)Date Description J/P Amount

(Tk.)

2011 2011 Jan-1 Cash 500,000 Land 750,000 Equipment 200,000 Office Supplies 70,000 Merchandise

Inventory300,000

Dec-31 Balance c/d 1,820,000 1,820,000 1,820,000 2012 Jan-1 Balance b/d 1,820,000

Now Presenting…… AL-AMIN KHANDAKAR

ID:20-019

Trial balance: It is a list of ledger accounts contained in the ledger of a business. This contains the name and value of the ledger account.

SL No. Particulars L.f Debit(TK) Credit(TK)

12345678910111214151617181920

Cash Common stock Acosta Corporation Bank Merchandise inventory Prepaid insurance Accounts payable Accounts receivable Cost of goods sold SalesFactoring expense Advertising expense Sale return and allowances Store equipment Store utility expense Pick upOffice utility expense Sale discount Office equipment Miscellaneous expense

346400

1050001424009000

30000813000

14040001300020002500450002500360050000500

1820000

50000

1070000

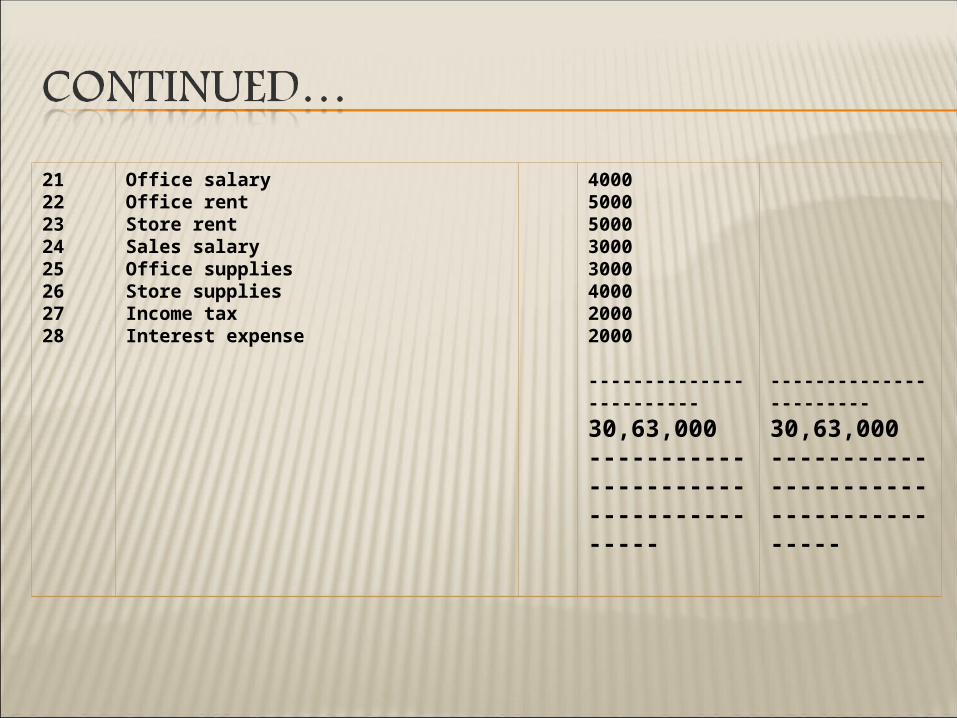

2122232425262728

Office salary Office rent Store rent Sales salary Office supplies Store supplies Income tax Interest expense

40005000500030003000400020002000

------------------------

30,63,000--------------------------------------

-----------------------

30,63,000--------------------------------------

Adjusting Entries: Adjusting entries are journal entries recorded at the end of an accounting period to adjust income and expense accounts so that they comply with the accrual concept of accounting. Their main purpose is to match incomes and expenses to appropriate accounting periods.

Adjusting entries 1. Annual depreciation on the equipment is Tk. 8,500. 2. The supplies on hand at the end of the year had a cost of

Tk.53,000. 3. Advance apprenticeship premium earned Tk. 40,000 for

5 years. 4. Annual depreciation on truck is Tk. 10,000. 5. Unpaid salaries expense was Tk.20,000. 6. Accrued rent expense was Tk.500. 7. Accrued utility expense was Tk.800. 8. Accrued interest earned was Tk.1,000.

Now Presenting……ARPITA DAS

ID:20-131

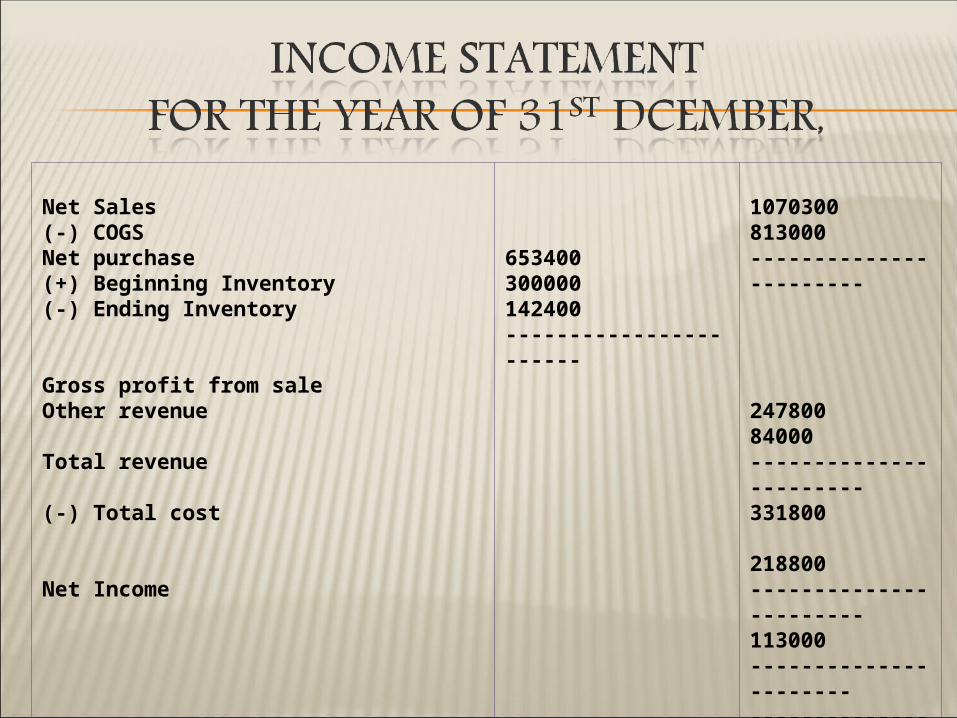

Financial statements: A set of financial statements is a structured representation of the financial performance and financial position of a business and how its financial position changed over time.

Net Sales(-) COGSNet purchase(+) Beginning Inventory(-) Ending Inventory

Gross profit from sale Other revenue

Total revenue

(-) Total cost

Net Income

653400300000142400-----------------------

1070300813000-----------------------

24780084000-----------------------331800

218800-----------------------113000----------------------------------------------

Assets:Cash BankPrepaid InsuranceOffice SuppliesAccounts ReceivablesShort-term InvestmentEnding Merchandise Inventory Long term Asset:LandFurnitureTruckEquipment

3466001050035005300030000240000142400

75000045000100000250000

-----------------2062800----------------------------------

Liabilities:Sales Salary PayableAccounts PayableAccrued rentAccrued utilitiesAccrued ApprenticeshipAccumulated dep.(equipment) Accumulated dep.(Truck)

Stock Holders Equity:Paid In CapitalNet income

20000500005008004000085001000048143

1820000113000

-----------------2062800----------------------------------

Assets:Cash BankPrepaid InsuranceOffice SuppliesAccounts ReceivablesShort-term InvestmentEnding Merchandise Inventory Long term Asset:LandFurnitureTruckEquipment

3466001050035005300030000240000142400

75000045000100000250000

-----------------2062800----------------------------------

Liabilities:Sales Salary PayableAccounts PayableAccrued rentAccrued utilitiesAccrued ApprenticeshipAccumulated dep.(equipment) Accumulated dep.(Truck)

Stock Holders Equity:Paid In CapitalNet income

20000500005008004000085001000048143

1820000113000

-----------------2062800----------------------------------

Now Presenting……RAIHANUL HAQUE KAYES

ID:20-065

A way of expressing the relationship between one accounting result and another, which is intended to provide a useful comparison. Financial ratio assist in measuring the efficiency and profitability of a company based on it’s financial reports. Some important financial ratios are given below:

Cash ratio Liquidity ratio Turn over ratio Accounts receivable ratio

Liquidity Ratio Current ratio = Current asset / Current liabilities =9,17,800 / 1,11,300 = 8.25 Acid Test = Current Asset – Inventory / Current Liabilities = 9,17,800 -1,42,400 /1,11,300 = 6.97 Cash ratio = Cash / Current Liabilities =3,46,400 /1,11,300 = 3.11

Activity Ratio : Receivable Turnover = Net Sales / Average of accounts receivable.

=10,60,800 / 30,000

= 35.36 Payable Turnover = Purchase / Average Trade payable

= 6,85,000 / 50,000

= 13.70 Profitability ratio :

Net Profit = Net Income / Revenue * 100

= 1,13,000 / 3,31,800 * 100

= 34%

Thank You…

![BBA & B.com 1[1] Accounting](https://img.pdfslide.net/doc/110x75/56d6bf2a1a28ab30169522f8/bba-bcom-11-accounting.jpg)