Embed Size (px)

Citation preview

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 1/50

NIK AZIDA BINTI ABD GHANI

013-933 7550

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 2/50

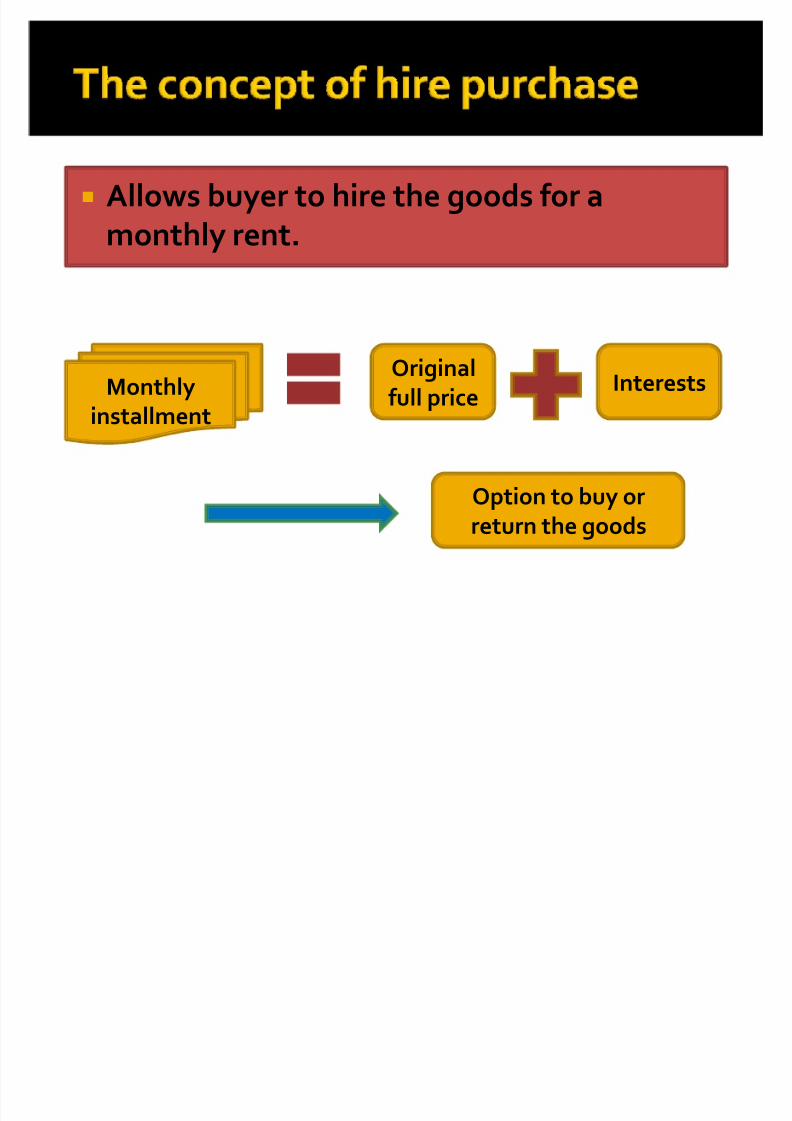

� Allows buyer to hire the goods for amonthly rent.

Monthlyinstallment

Original

full price

Interests

Option to buy or

return the goods

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 3/50

buyer who has the useof the goods is not thelegal owner during the

term of the hire-purchase contract.

If the buyer defaults inpaying the installments, the

owner may repossess the

goods.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 4/50

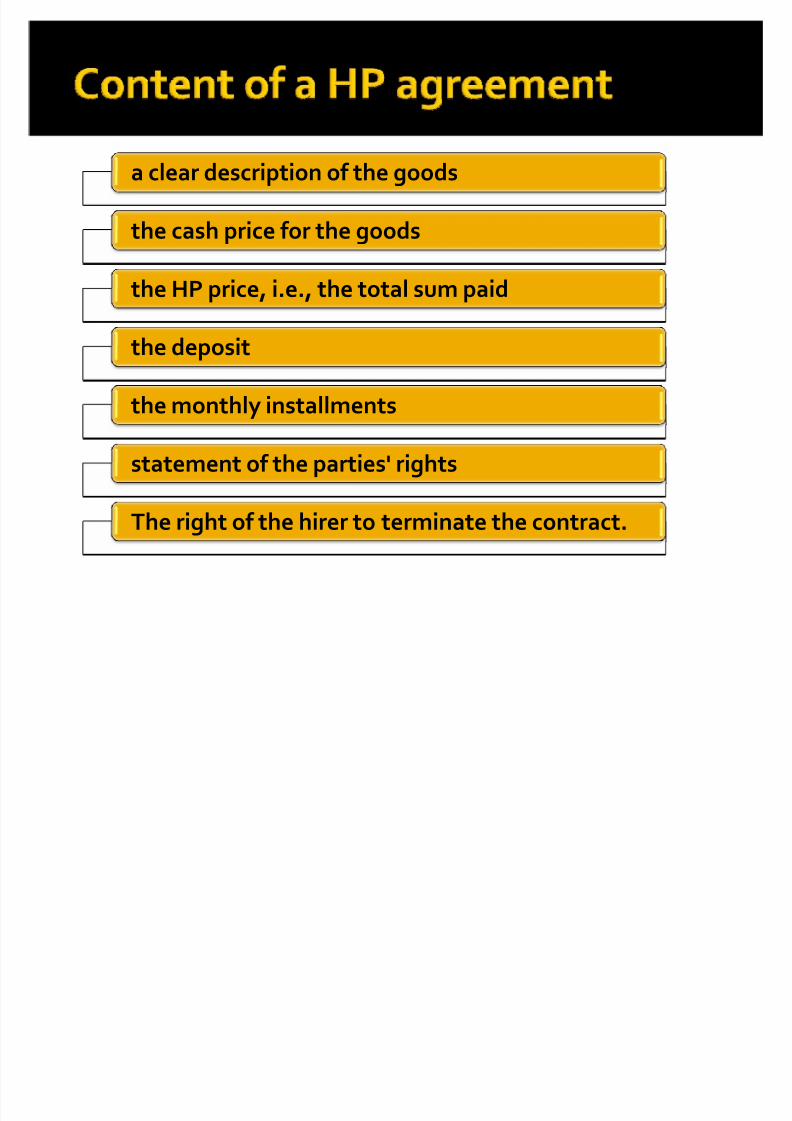

a clear description of the goods

the cash price for the goods

the HP price, i.e., the total sum paid

the deposit

the monthly installments

statement of the parties' rights

The right of the hirer to terminate the contract.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 5/50

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 6/50

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 7/50

rights

To buy the goods at any timeby giving notice and paying

the balance less a rebate. To return the goods to the

owner subject to penalty.

To assign both the benefitand the burden of the

contract to a third person. Where the owner wrongfullyrepossesses the goods,either to recover the goodsplus damages or value of thegoods lost.

obligations

to pay the hire installments

to take reasonable care of

the goods (if the hirerdamages the goods by usingthem in a non-standard way,he or she must continue topay the installments and, if appropriate, compensate theowner for any loss in assetvalue)

to inform the owner wherethe goods will be kept.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 8/50

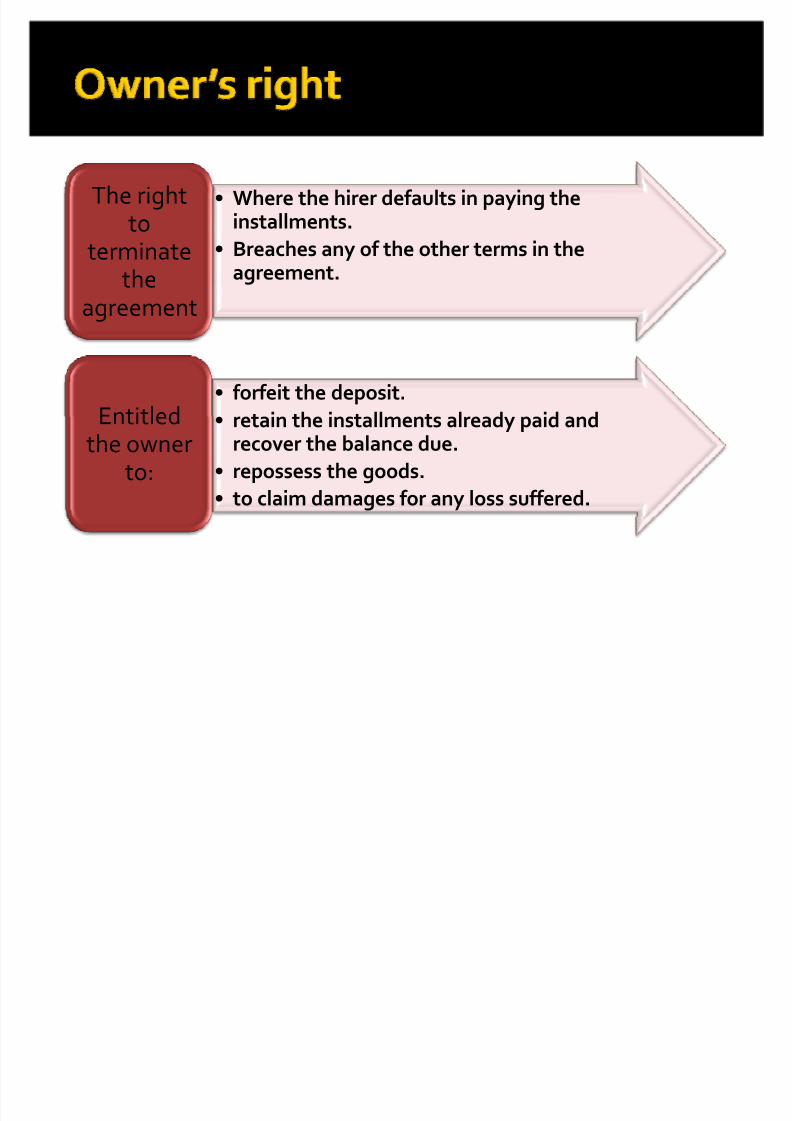

Where the hirer defaults in paying theinstallments.

Breaches any of the other terms in the

agreement.

The rightto

terminatethe

agreement

forfeit the deposit.

retain the installments already paid andrecover the balance due.

repossess the goods.

to claim damages for any loss suffered.

Entitledthe owner

to:

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 9/50

Hire purchase

Title of the goods: Thelegal title does not pass tothe hirer until he has paidhis final installment andexercise his option topurchase.

In case of default payment: The seller hasthe right torepossess/reclaim thegoods if the hirer fail topay.

Credit purchase

Title of the goods: Transferto the buyer immediatelyon delivery and thepurchase price is payableby installment or at sometime in the future.

In case of default payment: The seller hasno right to repossess thegoods but can sue forunpaid balance/installment.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 10/50

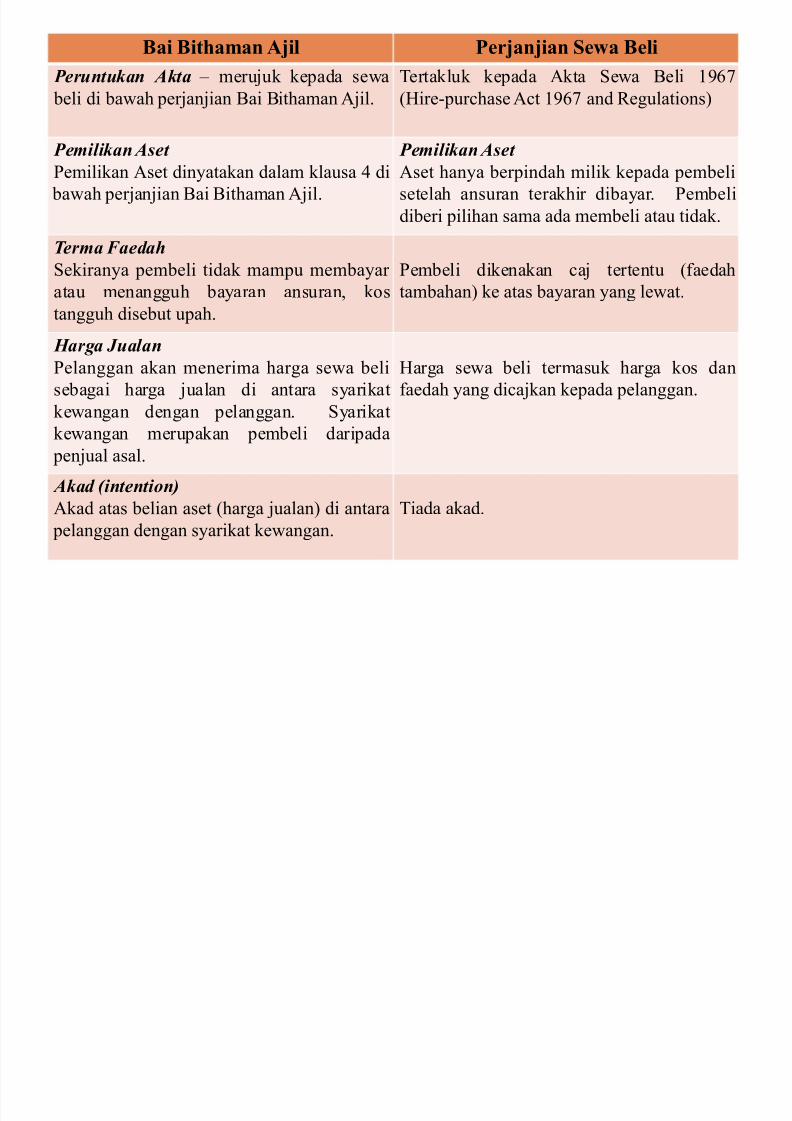

Bai Bithaman Ajil Perjanjian Sewa Beli

Peruntukan Akta ± merujuk kepada sewa

beli di bawah perjanjian Bai Bithaman Ajil.

Tertakluk kepada Akta Sewa Beli 1967

(Hire-purchase Act 1967 and Regulations)

Pemilikan Aset

Pemilikan Aset dinyatakan dalam klausa 4 di

bawah perjanjian Bai Bithaman Ajil.

Pemilikan Aset

Aset hanya berpindah milik kepada pembeli

setelah ansuran terakhir dibayar. Pembeli

diberi pilihan sama ada membeli atau tidak.

Terma Faedah

Sekiranya pembeli tidak mampu membayar atau menangguh bayaran ansuran, kos

tangguh disebut upah.

Pembeli dikenakan caj tertentu (faedahtambahan) ke atas bayaran yang lewat.

Harga Jualan

Pelanggan akan menerima harga sewa beli

sebagai harga jualan di antara syarikat

kewangan dengan pelanggan. Syarikatkewangan merupakan pembeli daripada

penjual asal.

Harga sewa beli termasuk harga kos dan

faedah yang dicajkan kepada pelanggan.

Akad (intention)

Akad atas belian aset (harga jualan) di antara

pelanggan dengan syarikat kewangan.

Tiada akad.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 11/50

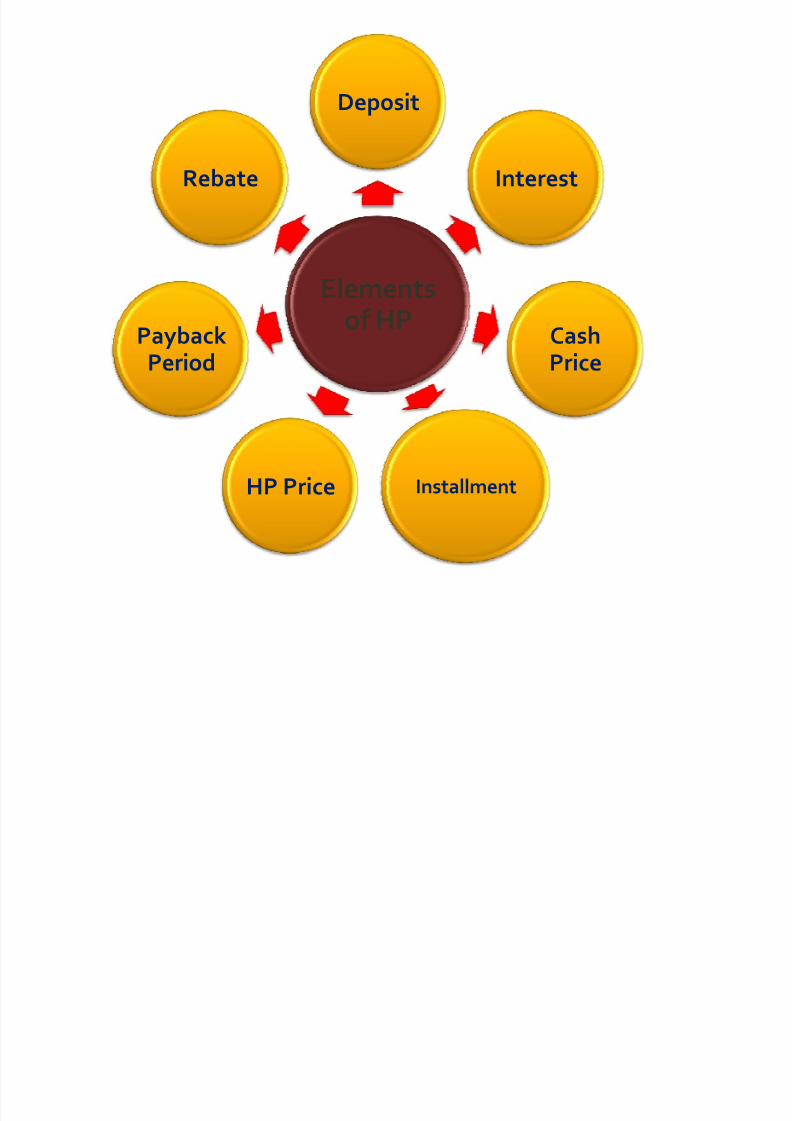

Elementsof HP

Deposit

Interest

CashPrice

InstallmentHP Price

PaybackPeriod

Rebate

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 12/50

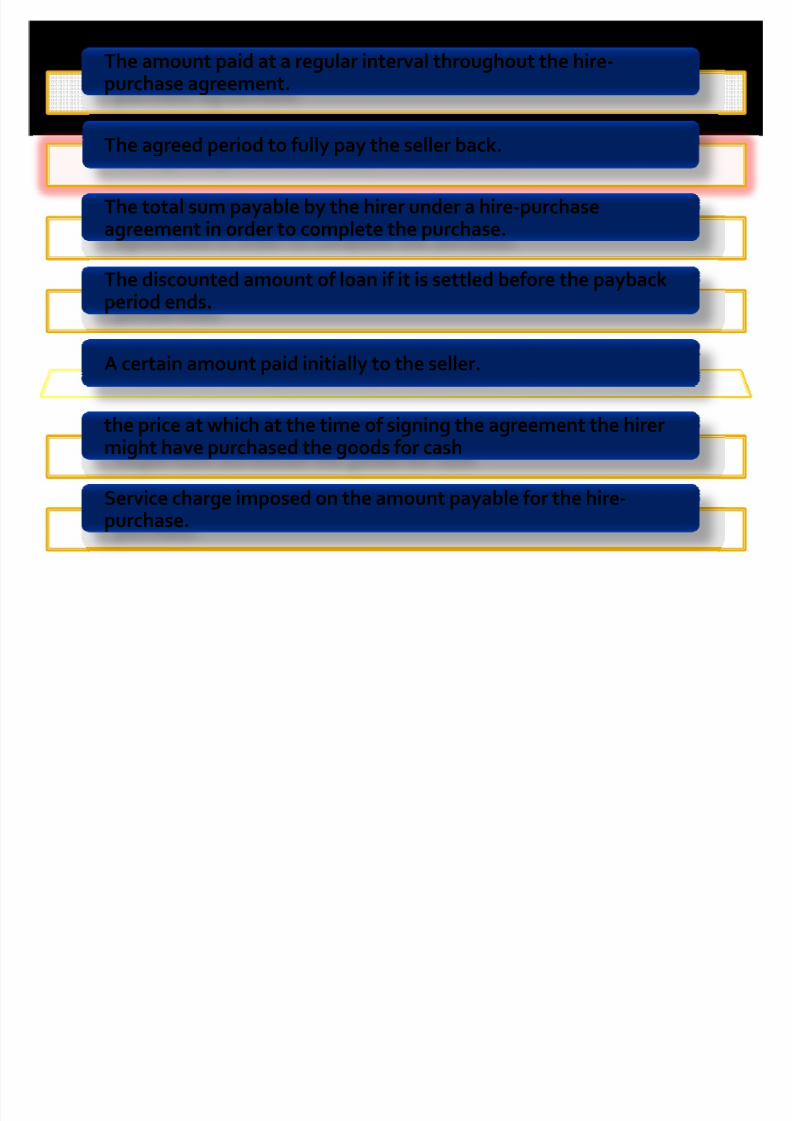

The amount paid at a regular interval throughout the hire-purchase agreement.

The agreed period to fully pay the seller back.

The total sum payable by the hirer under a hire-purchaseagreement in order to complete the purchase.

The discounted amount of loan if it is settled before the paybackperiod ends.

A certain amount paid initially to the seller.

the price at which at the time of signing the agreement the hirermight have purchased the goods for cash

Service charge imposed on the amount payable for the hire-purchase.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 13/50

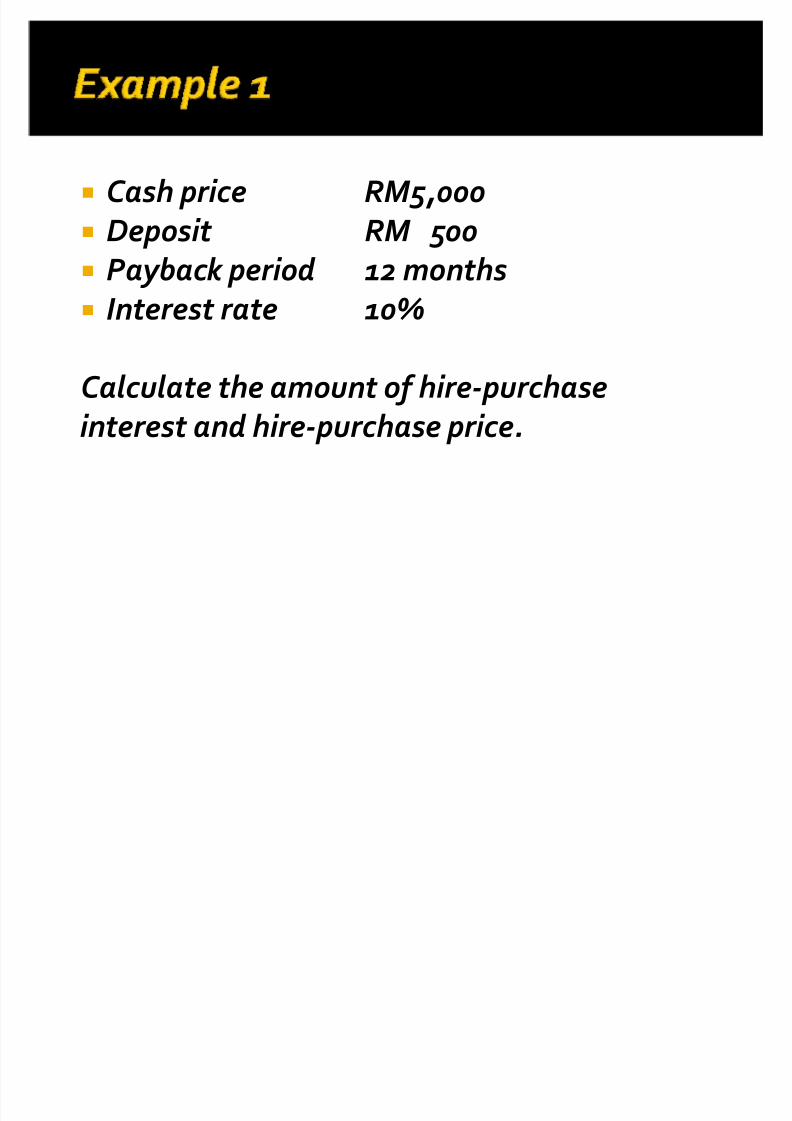

� C ash price RM5,000

� Deposit RM 500

� Payback period 12 months� Interest rate 10%

C alculate the amount of hire-purchase

i nterest and hire-purchase price.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 14/50

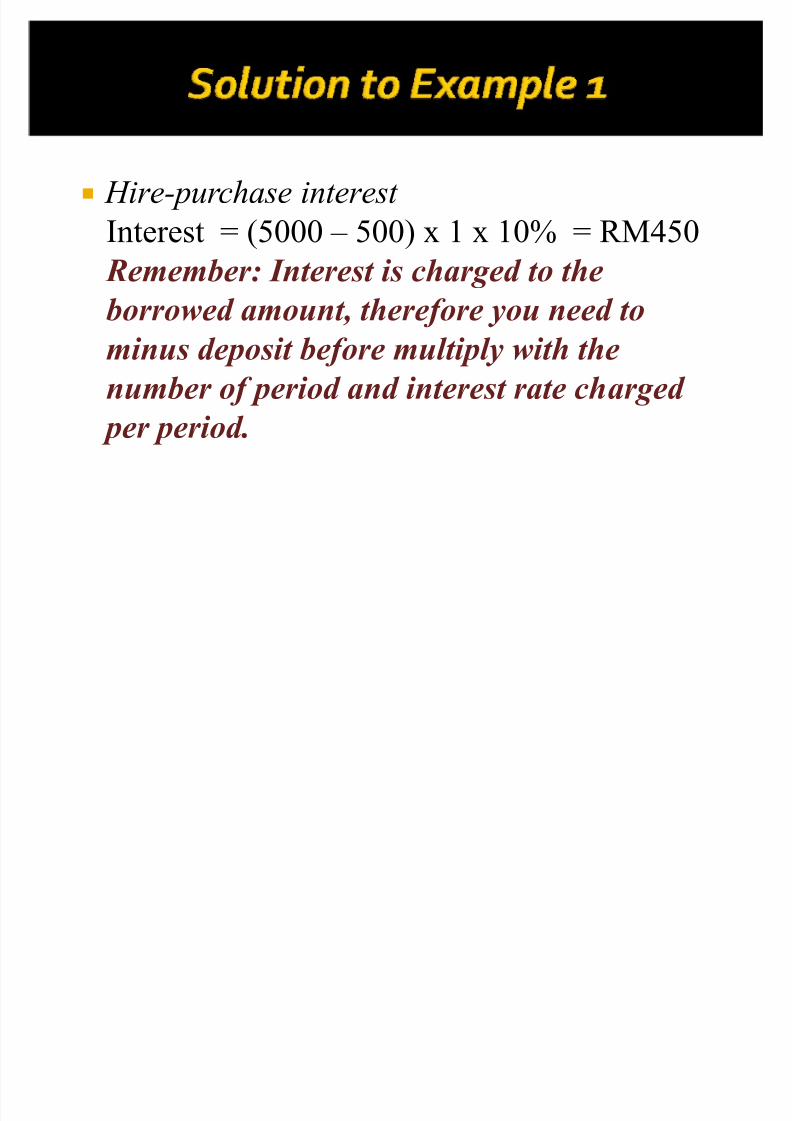

� Hire-purchase interest

Interest = (5000 ± 500) x 1 x 10% = RM450

Remember: Interest is charged to theborrowed amount, therefore you need to

minus deposit before multiply with the

number of period and interest rate charged

per period.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 15/50

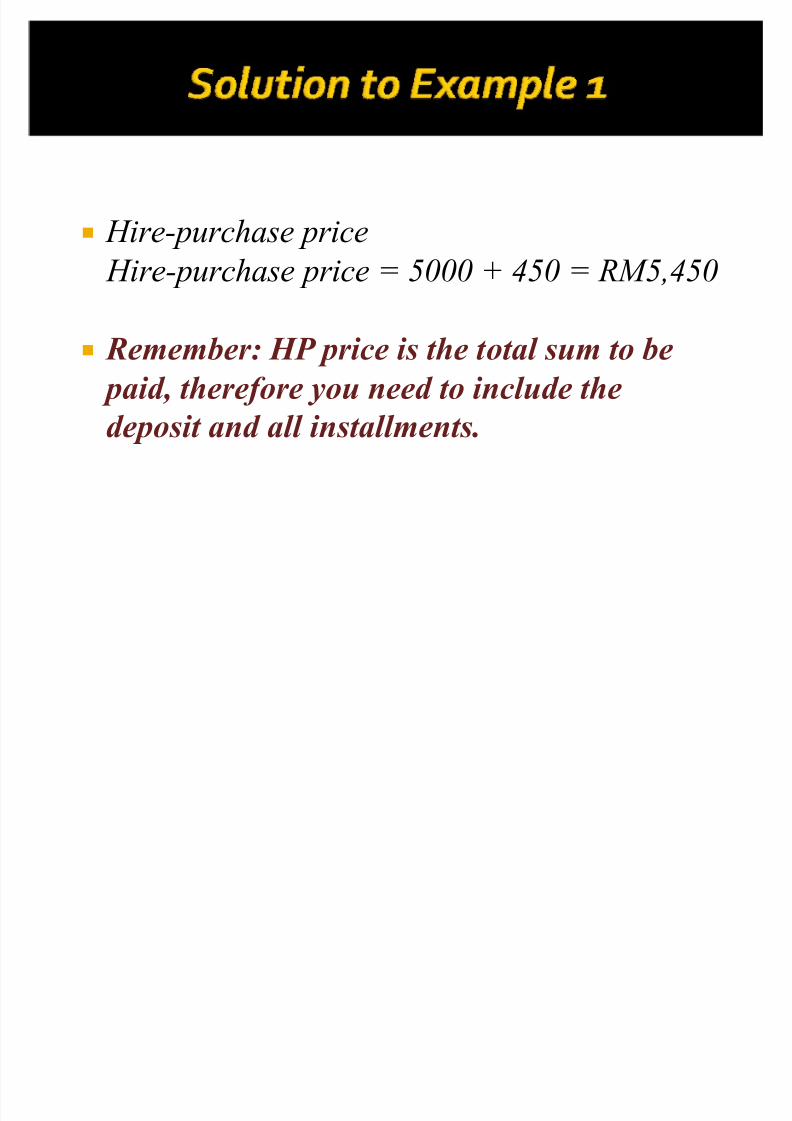

� Hire-purchase price

Hire-purchase price = 5000 + 450 = RM5,450

� Remember: HP price is the total sum to be

paid, therefore you need to include the

deposit and all installments.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 16/50

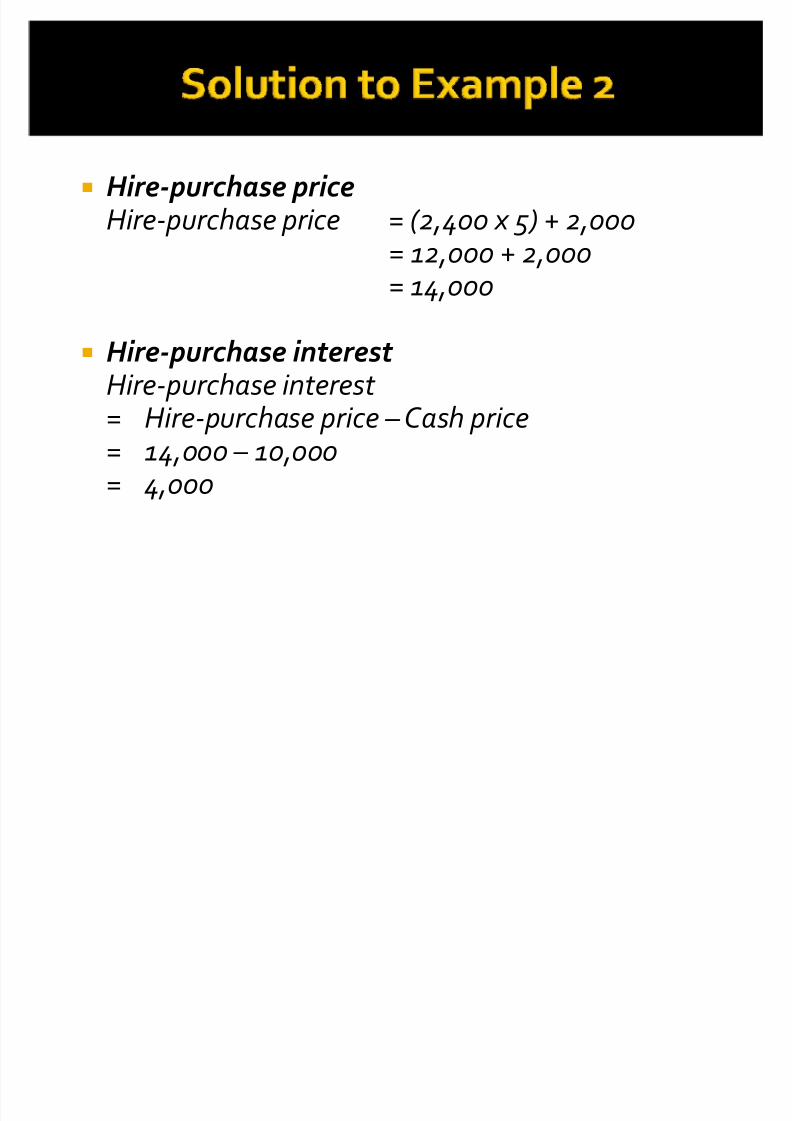

� Cash price RM10,000

� Deposit RM 2,000

� Installment 5 times RM 2,400 each

Calculate the amount of hire-purchase interest and hire-purchase price.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 17/50

� H ire-purchase priceHire-purchase price = (2,400 x 5) + 2,000

= 12,000 + 2,000= 14,000

� H ire-purchase i nterest Hire-purchase interest = Hire-purchase price Cash price= 14,000 10,000= 4,000

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 18/50

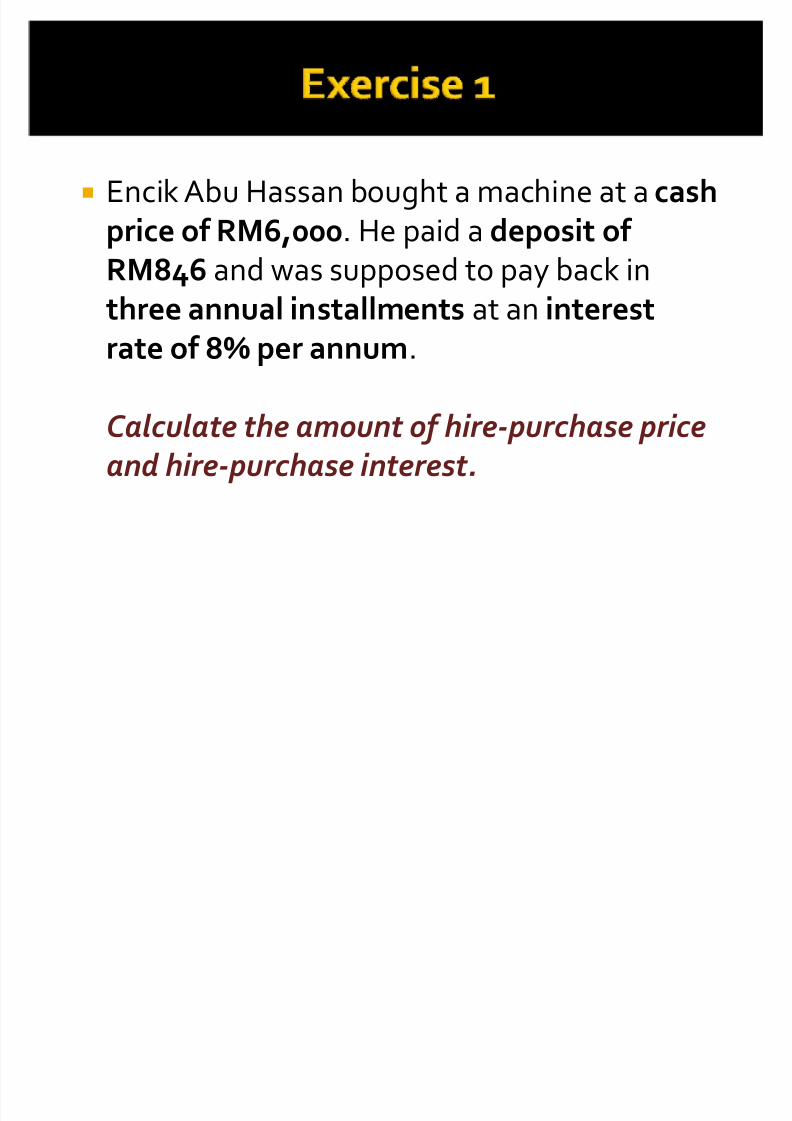

� Encik Abu Hassan bought a machine at a cash

price of RM6,000. He paid a deposit of

RM846 and was supposed to pay back inthree annual installments at an interest

rate of 8% per annum.

C alculate the amount of hire-purchase priceand hire-purchase i nterest.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 19/50

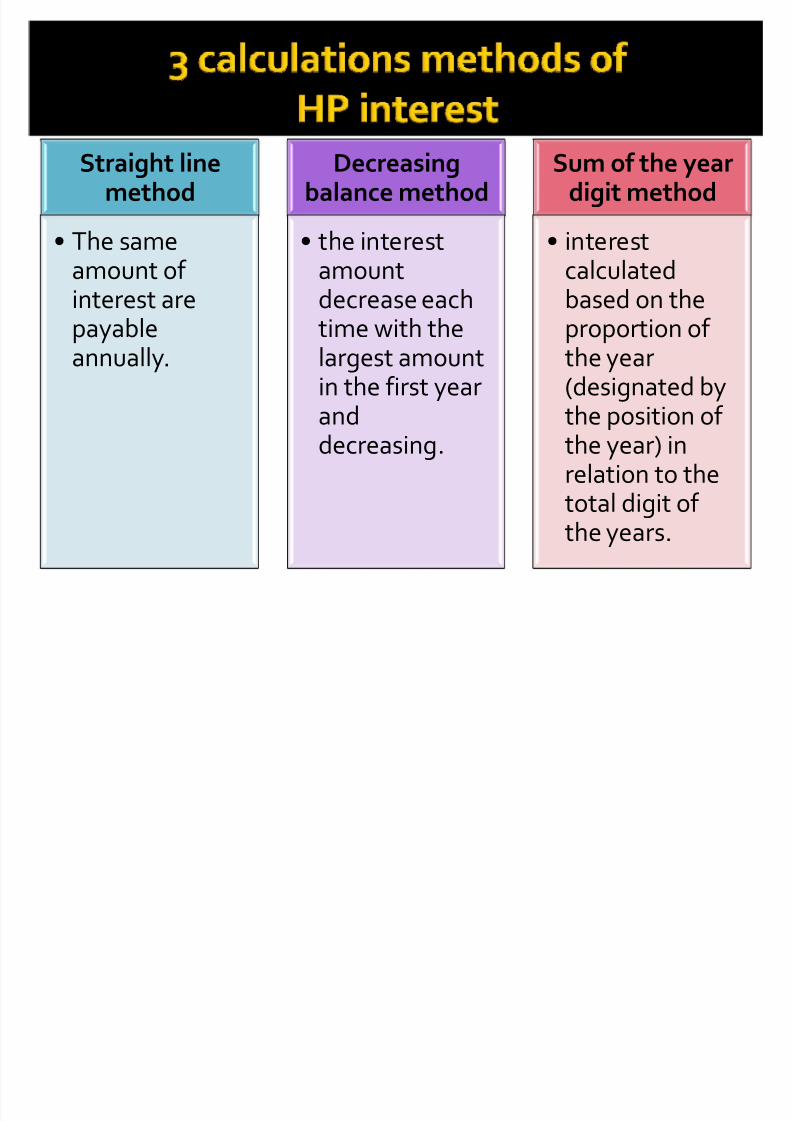

Straight linemethod

The same

amount of interest arepayableannually.

Decreasingbalance method

the interest

amountdecrease eachtime with thelargest amountin the first yearanddecreasing.

Sum of the yeardigit method

interest

calculatedbased on theproportion of the year(designated bythe position of the year) inrelation to thetotal digit of

the years.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 20/50

Principal payment = cash price depositinstallment times

Interest payment = total interestinstallment times

Principalpayment

Interestpayment

Installment

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 21/50

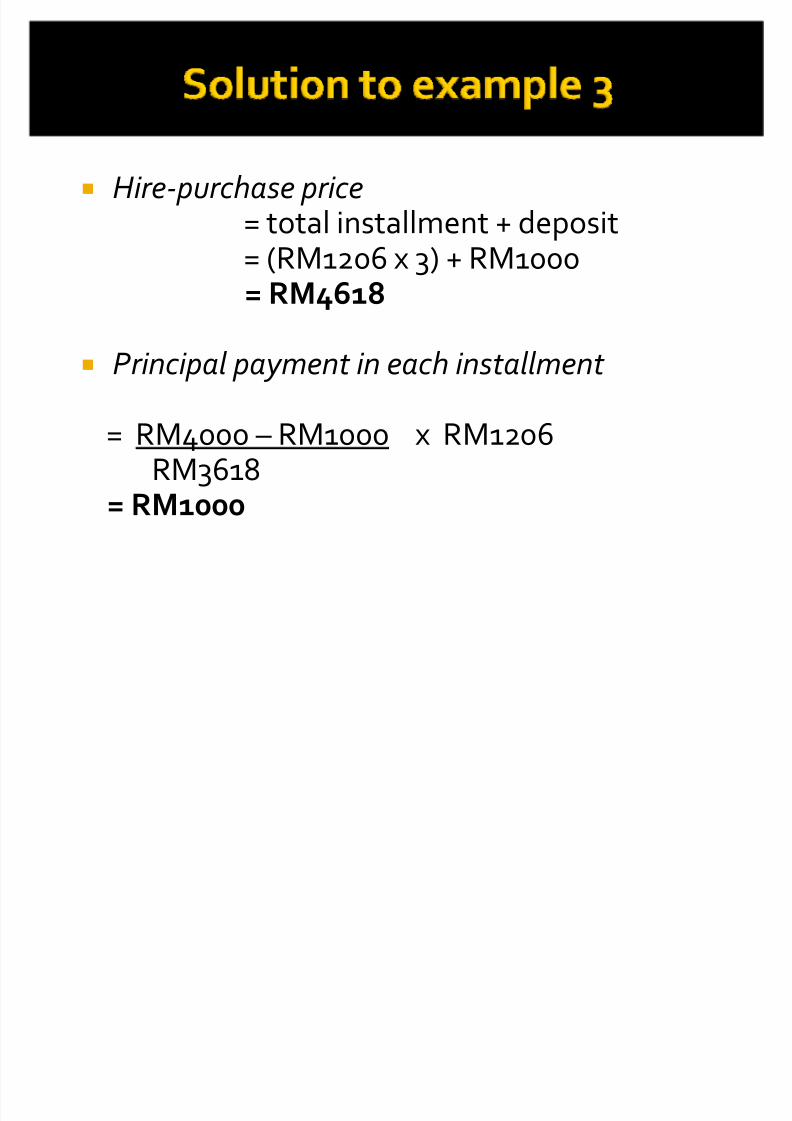

Cash price RM4,000

Deposit RM1,000

Installment 3 times RM1,206 each installment

Calculate:

�

hire-purchase price� the amount of pri ncipal payment i n each i nstallment � total i nterest � the amount of i nterest payment i n each i nstallment.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 22/50

� Hire-purchase price= total installment + deposit

= (RM1206 x 3) + RM1000= RM4618

� Principal payment in each installment

= RM4000 RM1000 x RM1206RM3618

= RM1000

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 23/50

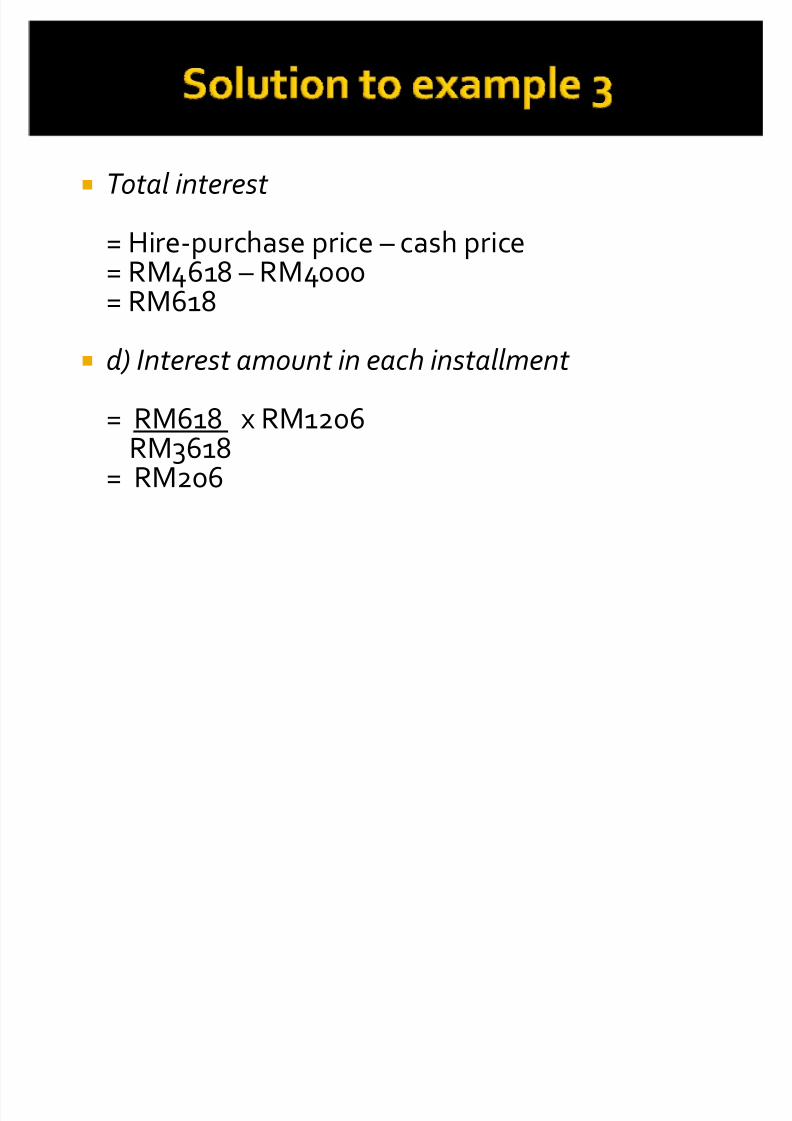

� T otal interest

= Hire-purchase price cash price

= RM4618 RM4000= RM618

� d) Interest amount in each installment

= RM618 x RM1206RM3618

= RM206

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 24/50

Question 1

Cash price RM25,000

Installment 24 times RM1,000 eachDeposit RM5,000

Calculate:� hire-purchase price� the amount of principal payment in each installment � total interest � the amount of interest payment in each installment.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 25/50

Question 2

Cash price RM10,000

Hire-purchase interest 10% per annumDeposit RM 1,000Annual installment of 5 times

Calculate:

� hire-purchase price� the amount of annual installment � the amount of principal payment in each installment � total interest and � the amount of interest payment in each installment.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 26/50

� To calculate total interest and the amount ineach installment, interest computation tablemust be prepared.

Ex ample 4Puan Halimah purchased a used vehicle at a cash

price of RM60,000. She paid deposit for the amount of 21% of the cash price of the vehicle. Hire-

purchase interest was calculated at 8% per annum.She also had to pay 4 annual installments of RM12,000 each and a final installment of RM11,246.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 27/50

Cash price 60,000

(-) deposit 12,600

47,400

(+) Interest 1 3,792

51,192 (-) Installment 1 12,000

39,192

(+) Interest 2 3,135

42,327

(-) Installment 2 12,000

30,327 (+) Interest 3 2,426

32,753

(-) Installment 3 12,000

20,753

(+) Interest 4 1,660

22,413(-)Installment 4 12,000

10,413

(+) Interest 5 833

11,246

(-) Installment 5 11,246

0

Table of interest

computation

Start with cashprice less

deposit

Interest is usuallycalculated at the

beginning of the period

Installmentfollows after

interest

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 28/50

Question 1

Cash price RM2,500

Deposit RM 500Installments 4 times RM 631 eachInterest rate 10% per annum

Calculate:� the amount of interest payable at each

installment.� the total amount of hire-purchase interest .

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 29/50

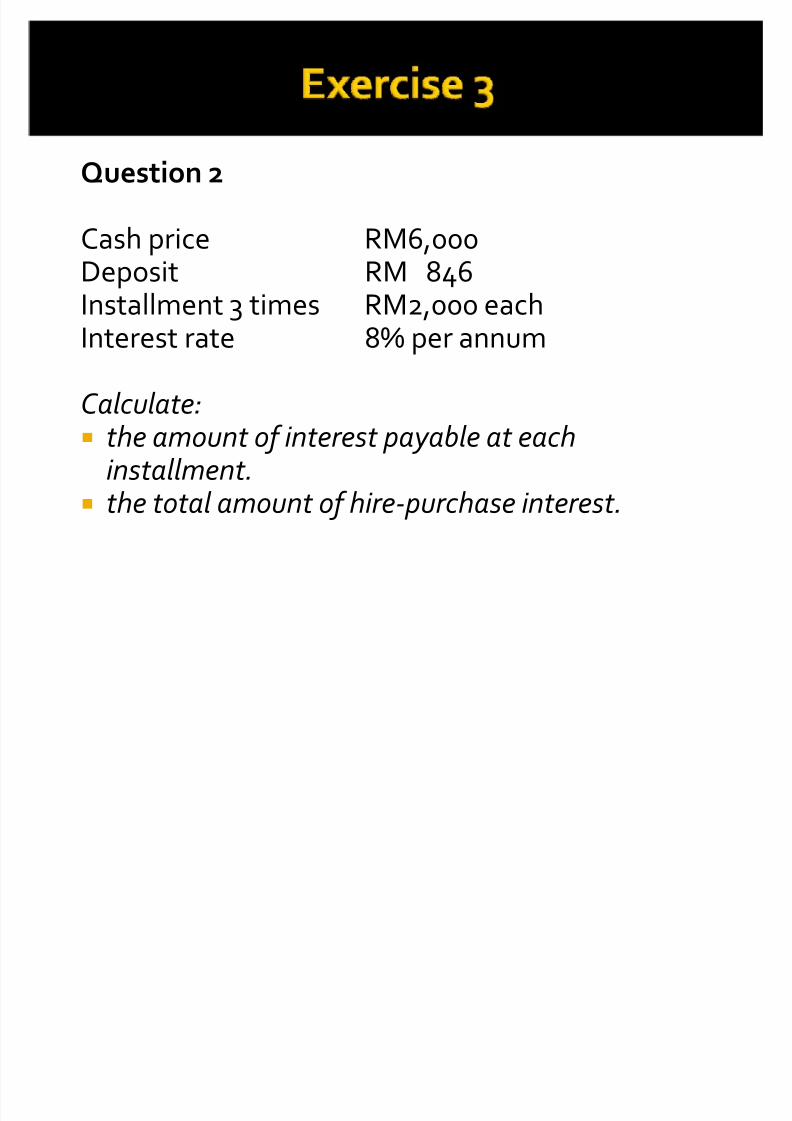

Question 2

Cash price RM6,000

Deposit RM 846Installment 3 times RM2,000 eachInterest rate 8% per annum

Calculate:� the amount of interest payable at each

installment.� the total amount of hire-purchase interest.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 30/50

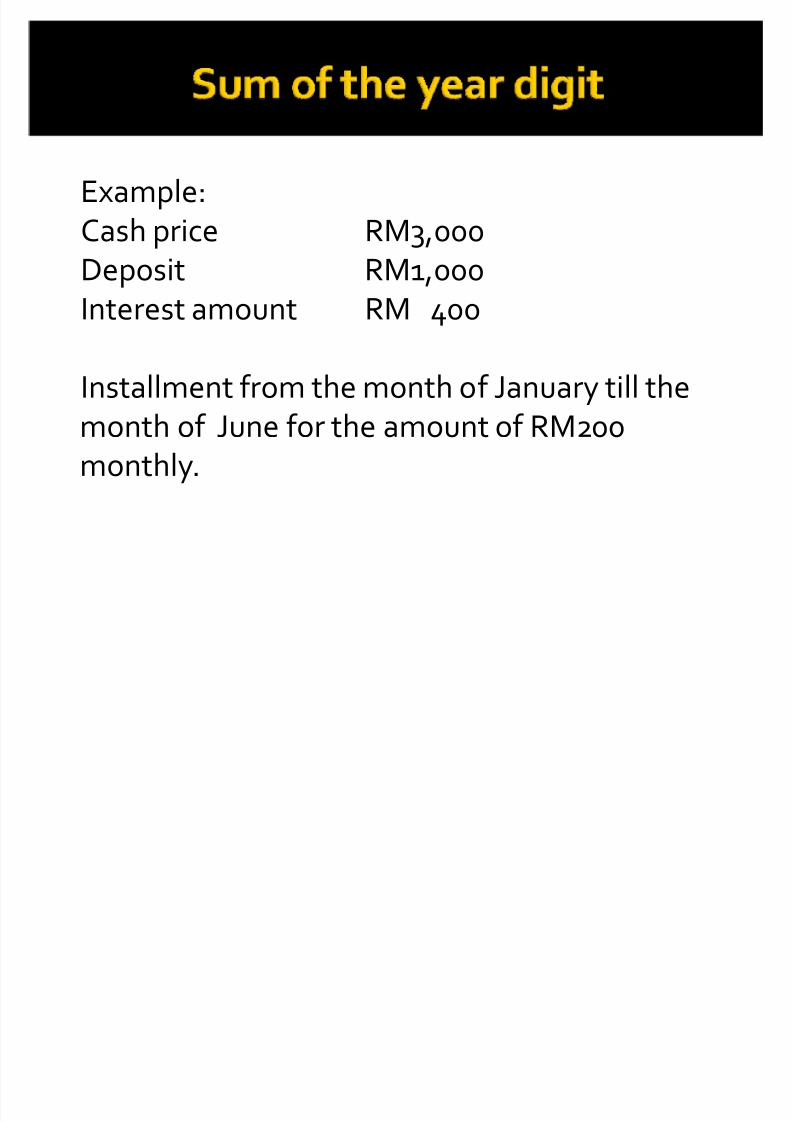

Example:

Cash price RM3,000

Deposit RM1,000Interest amount RM 400

Installment from the month of January till the

month of June for the amount of RM200monthly.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 31/50

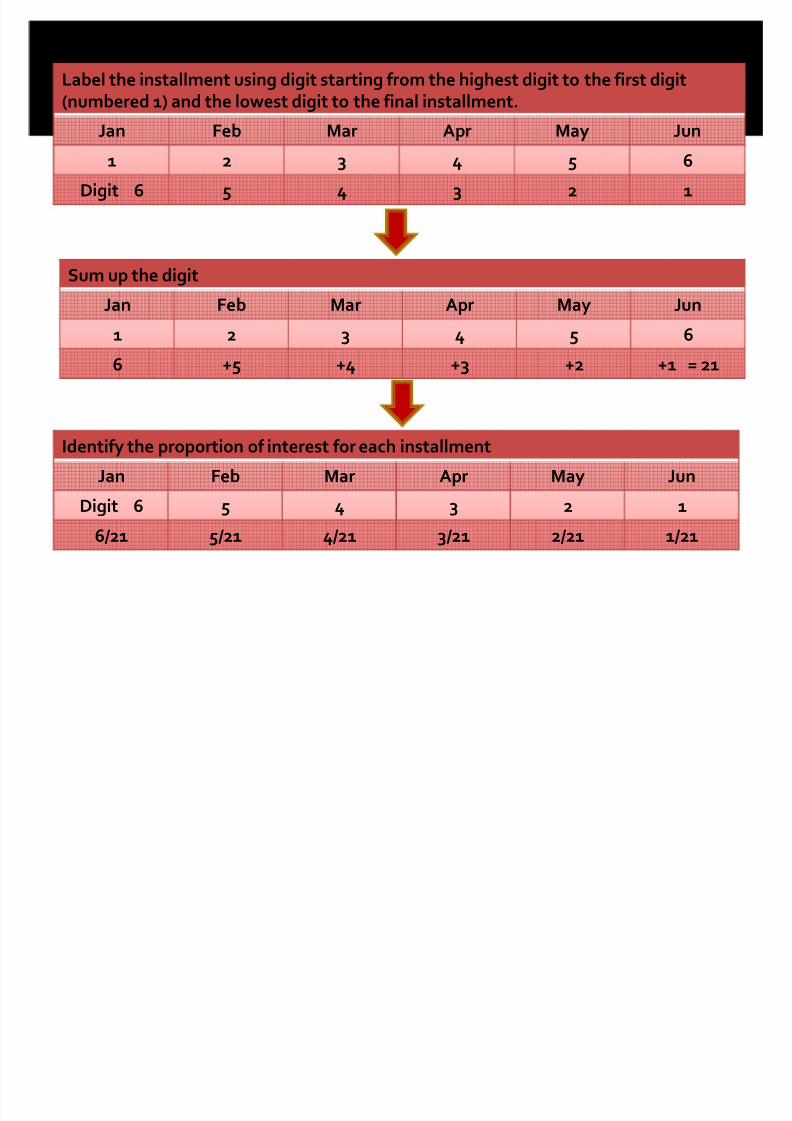

Label the installment using digit starting from the highest digit to the first digit(numbered 1) and the lowest digit to the final installment.

Jan Feb Mar Apr May Jun1 2 3 4 5 6

Digit 6 5 4 3 2 1

Sum up the digit

Jan Feb Mar Apr May Jun

1 2 3 4 5 6

6 +5 +4 +3 +2 +1 = 21

Identify the proportion of interest for each installment

Jan Feb Mar Apr May Jun

Digit 6 5 4 3 2 1

6/21 5/21 4/21 3/21 2/21 1/21

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 32/50

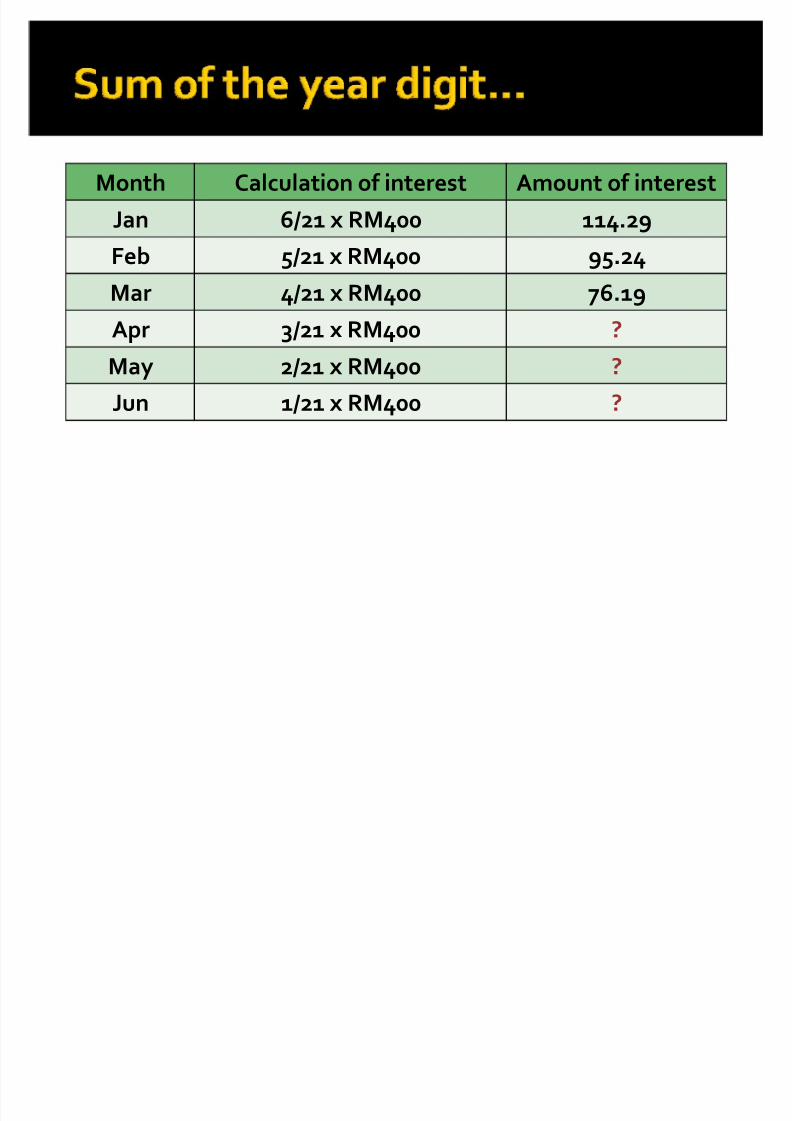

Month Calculation of interest Amount of interest

Jan 6/21 x RM400 114.29

Feb 5/21 x RM400 95.24

Mar 4/21 x RM400 76.19

Apr 3/21 x RM400 ?

May 2/21 x RM400 ?

Jun 1/21 x RM400 ?

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 33/50

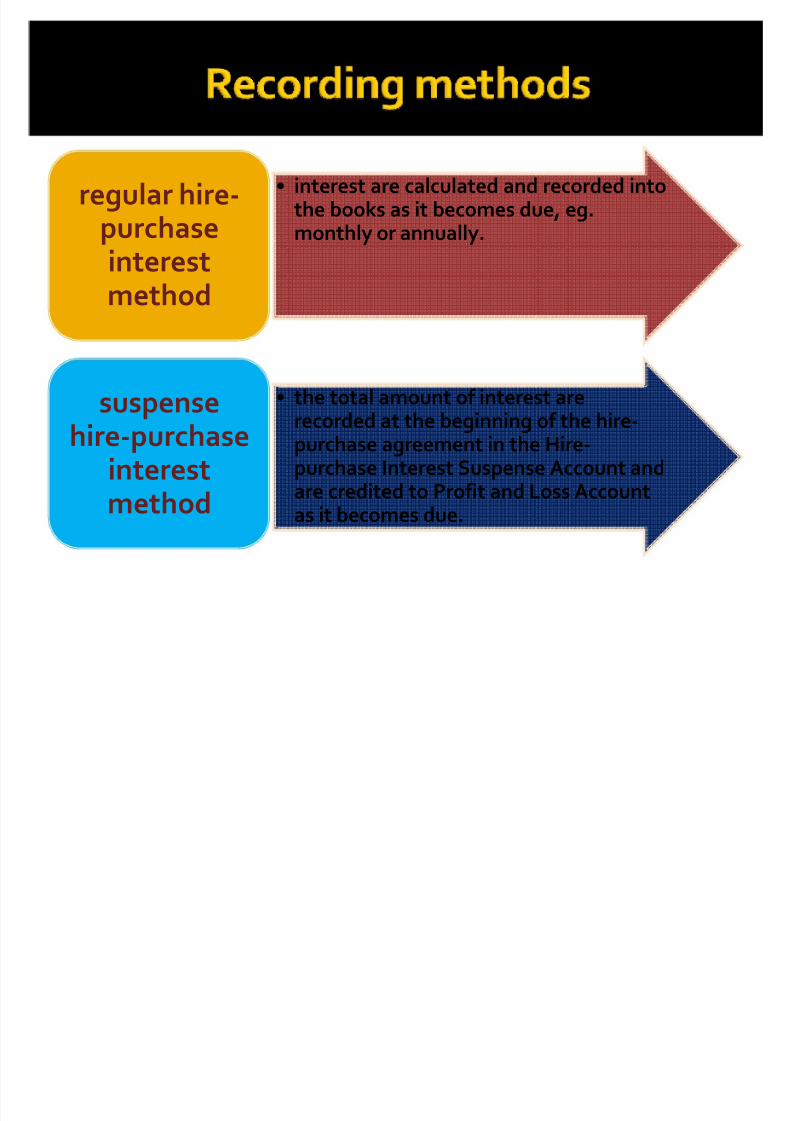

interest are calculated and recorded intothe books as it becomes due, eg.monthly or annually.

regular hire-purchase

interestmethod

the total amount of interest arerecorded at the beginning of the hire-purchase agreement in the Hire-purchase Interest Suspense Account andare credited to Profit and Loss Accountas it becomes due.

suspensehire-purchaseinterestmethod

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 34/50

Hire purchase creditor (seller)

Asset XX

Asset

Hire-purchase creditor XX

When HP agreement is prepared

Dr. Asset account Cr. Hire-purchase creditor account

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 35/50

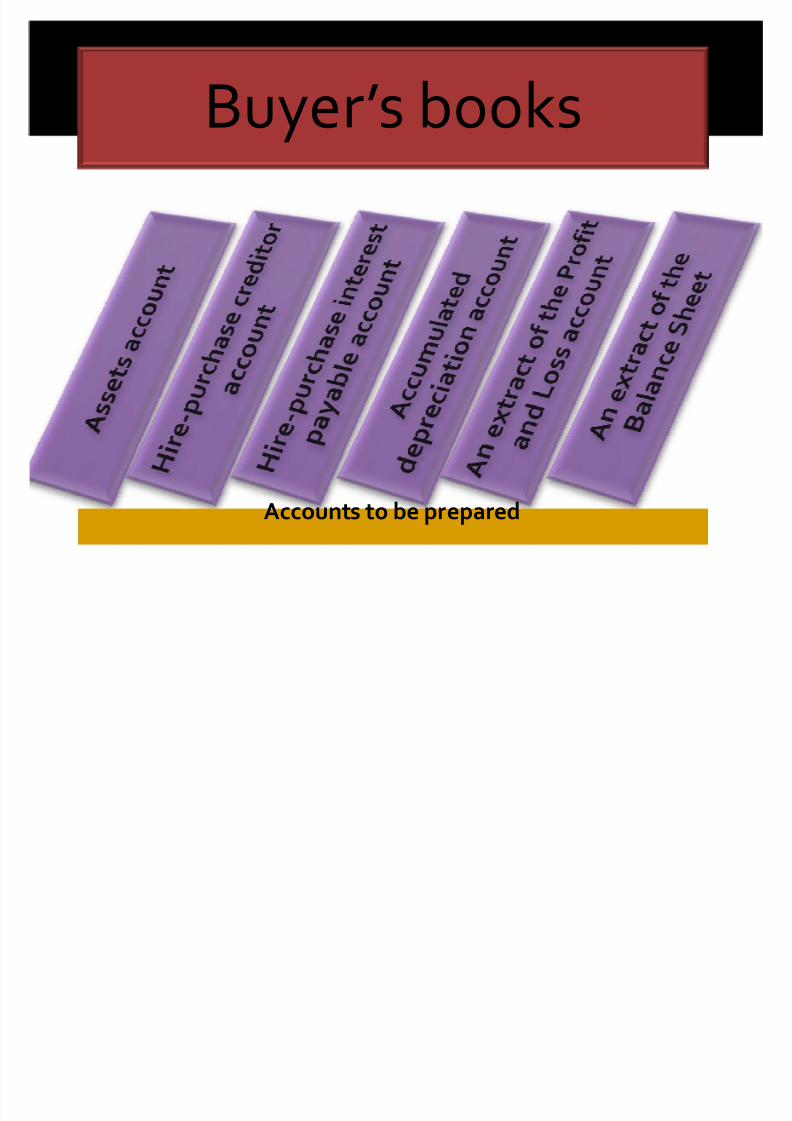

B

uyers books

Accounts to be prepared

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 36/50

Hire-purchase creditor

Hire purchase interest expense XX

Hire-purchase interest expense

Hire-purchase creditor account XX

To record HP interestDr. Hire-purchase interest

expenseCr. Hire-purchase creditor account

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 37/50

Bank account

Hire-purchase creditor account XX

Hire purchase creditor

Bank XX

To record payment of deposit or installment

r. Hire-purchase creditoraccount

Cr. Bank account

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 38/50

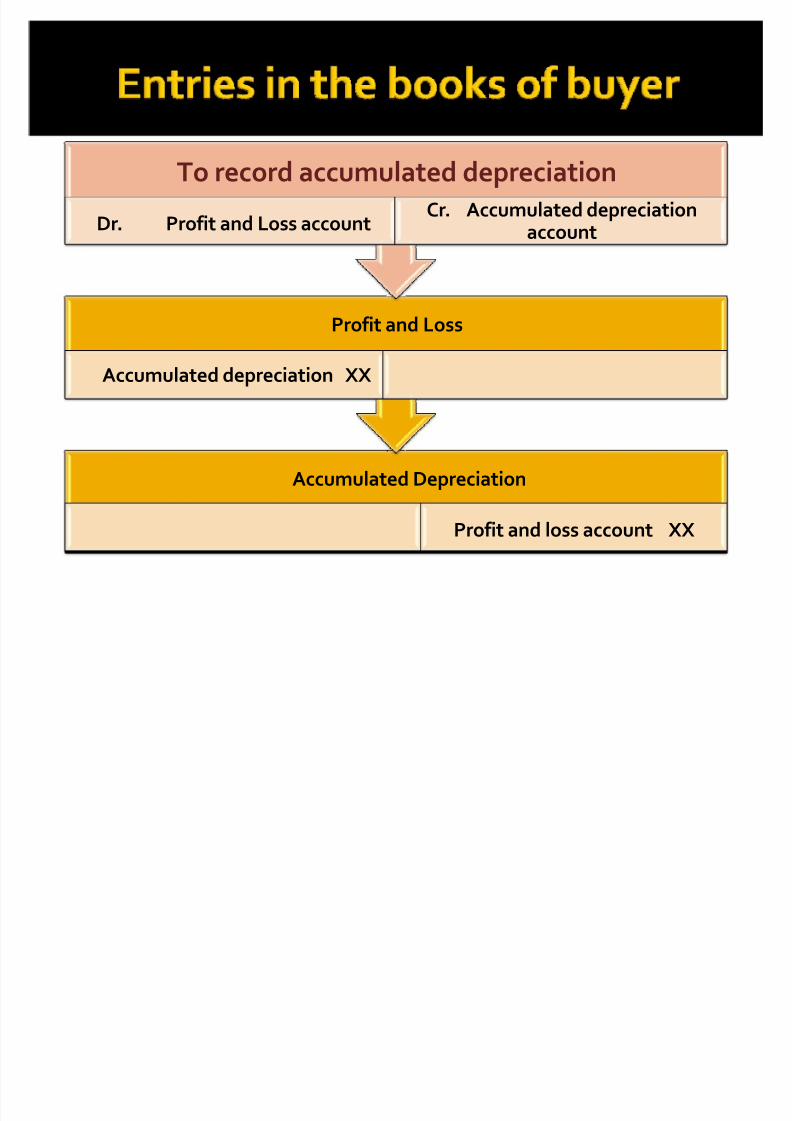

Accumulated Depreciation

Profit and loss account XX

Profit and Loss

Accumulated depreciation XX

To record accumulated depreciation

Dr. Profit and Loss accountCr. Accumulated depreciation

account

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 39/50

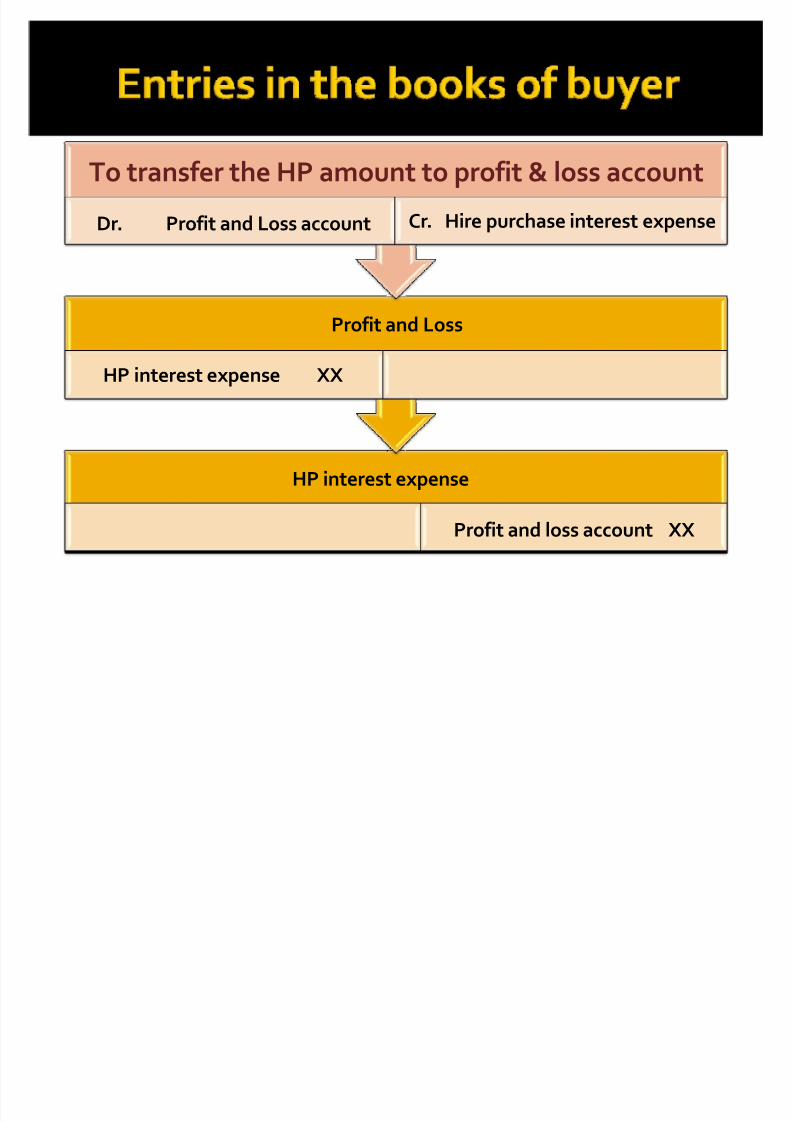

HP interest expense

Profit and loss account XX

Profit and Loss

HP interest expense XX

To transfer the HP amount to profit & loss account

Dr. Profit and Loss account Cr. Hire purchase interest expense

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 40/50

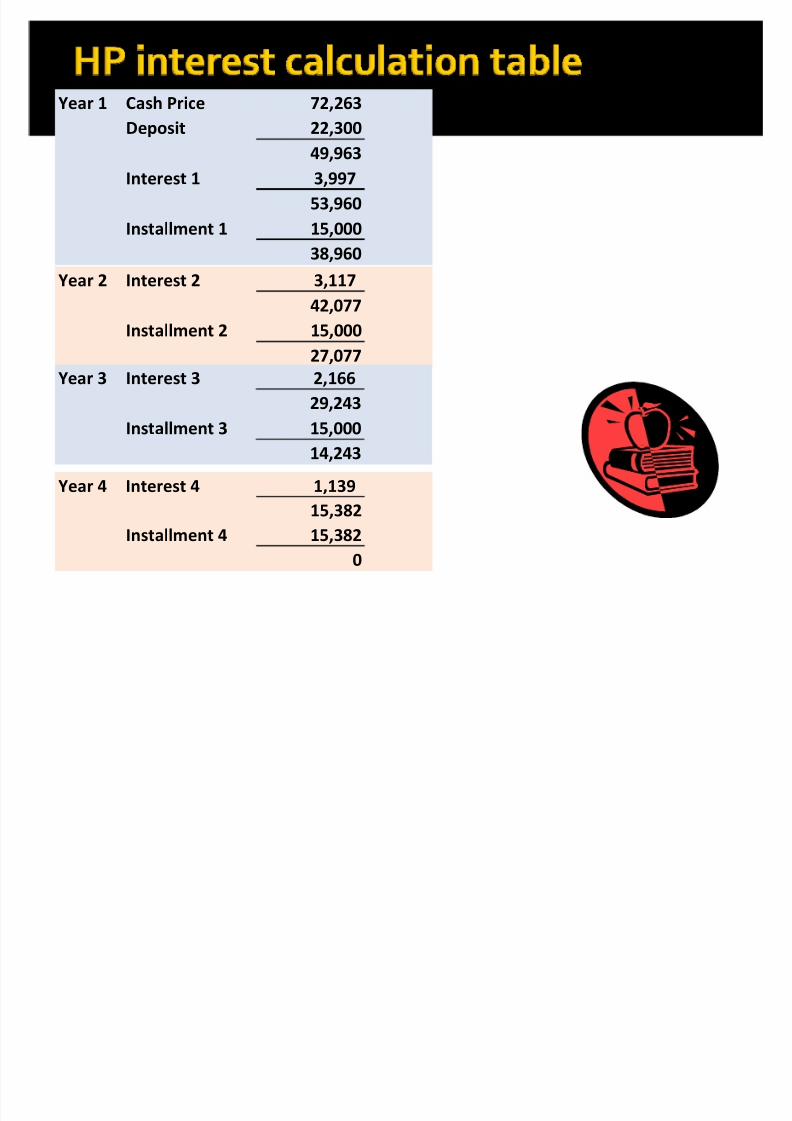

Danial bought a motor vehicle on hire-purchasefrom Syarikat Motor DFateha on 1 January 2008. The hire-purchase agreement stated the following:

Cost RM 58,263Cash price 72,263Deposit 22,300

Hire-purchase interest was charged at 8% perannum using the declining balance method. Instalments of RM15,000 were to be paid at theend of each year for a period of three years and thefinal instalment of RM15,382.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 41/50

Prepare the followi n g accounts:

� Motor vehicle account

�H ire-purchase creditor account

� H ire-purchase i nterest account

� Ex tract of profit and loss account

� Ex tract of balance sheet

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 42/50

Year 1 Cash Price 72,263

Deposit 22,300

49,963

Interest 1 3,997

53,960

Installment 1 15,000

38,960

Year 2 Interest 2 3,117

42,077

Installment 2 15,000

27,077

Year 3 Interest 3 2,166

29,243Installment 3 15,000

14,243

Year 4 Interest 4 1,139

15,382

Installment 4 15,382

0

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 43/50

On 1 January 2008, Encik Faidzul bought amachine from Syarikat Umar Al-Atif on hire- purchase. T he hire-purchase price was

RM10,030. Deposit RM2,000 was paid at thetime of purchase. T hree installment for theamount of RM2,000, RM3,000 and RM3,030 areto be paid. Each installment was paid on 31

December. Interest rate charged at 15% per annum based on declining balance method.Depreciation was calculated at 20% per annum onstraight line basis.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 44/50

Prepare the followi n g accounts:

� Machi ne

�H ire-purchase creditor account

� H ire-purchase i nterest account

� Accumulated depreciation account

� Profit and loss account

� Balance sheet

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 45/50

Most of the time, the questions do not statewhich method to use.

� Pay attention to the type of accounts to beprepared.

� The account Hire-purchase Interest Suspense

would suggest that the suspense method is used.

� If it is not mentioned, then the method to be usedis the regular hire-purchase interest suspense.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 46/50

Prepare the followi n g accounts:

� Motor vehicle account

�

H ire-purchase creditor account � H ire-purchase i nterest suspense account

� Ex tract of profit and loss account

� Ex tract of balance sheet

� Note that the i nterest suspense account is to

be show n.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 47/50

Question 1

On 1 January 2006, Syarikat Motor Berhad sold an asset to EncikAhmad. A deposit of RM67,350 was paid at the time of purchase. The hire-purchase agreement was for 3 years withinstallment payment of RM50,000 on 31 December 2006 to2008. Interest was charged at 5% per annum based on thebalance on total debt outstanding. A hire-purchase interestaccount was opened to allocate the interest throughout theperiod under agreeement.

You are required to:� C alculate the cash price and hire-purchase price of the asset.� C alculate the i nterest payable on each year.� Use the regular hire-purchase i nterest method to record the

transactions i nto the books of E ncik Ahmad.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 48/50

Question 2

Mega Sdn. Bhd sold a machine under a hire-purchase agreement toEncik Farouq on 1 January 2006. The agreement stated the followingdetails:

Deposit RM10,000Installment 4 times every 6 months of RM4,000 eachFirst installment due on 30 June 2006. Interest rate charged at 10% per annum based on balance outstandingand depreciation charged at 5% based on straight-line method.

You are required to:� calculate the cash price of the machine� prepare the accounts in the book of the buyer using the regular hire-

purchase interest method of recording and � prepare the accounts in the books of the buyer using the suspense hire-

purchase interest method of recording.

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 49/50

Question 3

Based on Question 1 above, use the hire- purchase interest suspense method to record the

transactions into the books of Encik Ahmad (thebuyer).

8/6/2019 Accounting for Hire Purchase_ppt

http://slidepdf.com/reader/full/accounting-for-hire-purchaseppt 50/50

Question 4

Based on Question 2 above, use the regular hire- purchase interest method to record the

transactions into the books of Encik Farouq (thebuyer).