Embed Size (px)

Citation preview

Issued May 2018

Accounting Manual for Departments

Capital Assets

Capital Assets

Issued May 2018 Page 2

Chapter Content

1 Overview ....................................................................................................................................... 4

2 Key Learning Objectives ............................................................................................................... 4

3 Scope ............................................................................................................................................ 5

4 Control over a capital asset .......................................................................................................... 6

5 Tangible Assets and Intangible assets ......................................................................................... 8

5.1 Tangible Assets .................................................................................................................. 8

5.2 Intangible Assets ................................................................................................................ 8

5.2.1 Identifiability of an intangible asset .......................................................................... 9

5.2.2 Without physical substance .................................................................................... 11

6 Types of Capital Assets .............................................................................................................. 12

6.1 Loose tools, spare parts and servicing equipment ........................................................... 13

6.2 Safety equipment .............................................................................................................. 14

6.3 Library materials ............................................................................................................... 15

6.4 Investment property .......................................................................................................... 15

6.5 Biological assets ............................................................................................................... 18

6.6 Heritage assets ................................................................................................................. 20

6.7 Infrastructure assets ......................................................................................................... 22

6.8 Specialist military equipment ............................................................................................ 23

6.9 Internally generated intangible assets .............................................................................. 23

6.9.1 Research phase ..................................................................................................... 24

6.9.2 Development phase ............................................................................................... 24

6.9.3 Website costs ......................................................................................................... 25

6.10 Immovable assets ............................................................................................................. 26

7 Recording of Capital Assets ....................................................................................................... 28

7.1 General ............................................................................................................................. 28

7.2 Asset register .................................................................................................................... 28

7.3 Components ..................................................................................................................... 29

8 Measurement of Capital assets .................................................................................................. 30

Capital Assets

Issued May 2018 Page 3

8.1 Initial measurement .......................................................................................................... 30

8.1.1 Movable assets: ..................................................................................................... 32

8.1.2 Immovable assets: ................................................................................................. 32

8.2 Elements of cost ............................................................................................................... 33

8.3 Warranty costs .................................................................................................................. 40

8.4 Leasehold improvements ................................................................................................. 40

8.5 Assets transferred between departments ......................................................................... 42

8.6 Fair value .......................................................................................................................... 42

9 Subsequent Measurement .......................................................................................................... 47

9.1 Subsequent costs ............................................................................................................. 47

10 Removal (Derecognition) ............................................................................................................ 47

11 Disclosures ................................................................................................................................. 49

12 Summary of Key Principles ......................................................................................................... 52

12.1 Definition and identification ............................................................................................... 52

12.2 Recording and measurement ........................................................................................... 52

12.3 Disclosure ......................................................................................................................... 53

Capital Assets

Issued May 2018 Page 4

1 Overview

The purpose of this Chapter is to provide guidance on how to identify and report on capital assets.

The Office of the Accountant-General has compiled a Modified Cash Standard (MCS) and this manual serves as an application guide to the MCS which should be used by departments in the preparation of their financial statements.

Any reference to a “Chapter” in this document refers to the relevant chapter in the MCS and / or the corresponding chapter of the Accounting Manual.

Explanation of images used in the manual:

2 Key Learning Objectives

Understanding the definition for and different types of capital assets

Understand the capital asset transactions and what needs to be disclosed and recorded

Definition

Take note

Management process and decision making

Example

Capital Assets

Issued May 2018 Page 5

3 Scope

The Chapter on Capital Assets in the MCS, and consequently this guide does not apply to:

The accounting requirements in respect of the primary financial information for expenditure on capital assets (i.e. the expenditure relating to the acquisition / maintenance etc.). This is dealt with in the Chapter on Expenditure. A department must however consider the provisions of this Chapter in order to correctly classify the type of asset acquired.

The recording of a capital asset subject to a finance lease. This is discussed in more detail in the Chapter on Leases. A department must however apply the provisions of this Chapter on expiry of the lease if the department takes control over the leased asset;

Intangible assets arising from powers and rights conferred to a department by legislation, the Constitution, or by equivalent means;

Departments may execute a regulatory right over certain activities, for example fishing, mining or industries such as telecommunications and energy. These regulatory rights and the power to transfer, license, rent or execute such rights are excluded from the scope of this chapter as these powers and rights are conferred to the department by legislation, the Constitution or other equivalent means. These rights once issued, are usually an intangible asset of those individuals or entities that acquired each right, provided that the acquirer can demonstrate that the definition and criteria for recording an intangible asset are met.

Similarly, a department’s right to levy taxes is granted in terms of statute and are thus excluded from the scope of this Chapter and not required to be valued for the purposes of recording in the financial statements.

Inventories. These are discussed in more detail in the Chapter on Inventory;

Agricultural produce after the point of harvest. This is discussed in more detail in the Chapter on Inventory;

Departments are at present not required to include assets acquired through finance leases in their asset registers until the finance lease period has expired.

These assets must however be reflected in the finance lease register maintained by the department.

Where a finance lease agreement has expired and the department continues to use the asset, and ownership of the asset transfers to the department, the asset must be recorded at its fair value at the date of expiry of the lease in the department’s asset register.

Supply chain regulations should be followed to extend or to enter into a new lease agreement.

Some departments acquire capital assets for distribution as part of their service delivery mandate. These capital assets should be classified as inventory only if they meet the definition of inventory as outlined in the Chapter on Inventory.

These items should also be budgeted for as inventory not capital assets.

Where the budget allocation is for capital assets, the newly acquired capital asset must be recorded in the asset register and if it was to be transferred to

Capital Assets

Issued May 2018 Page 6

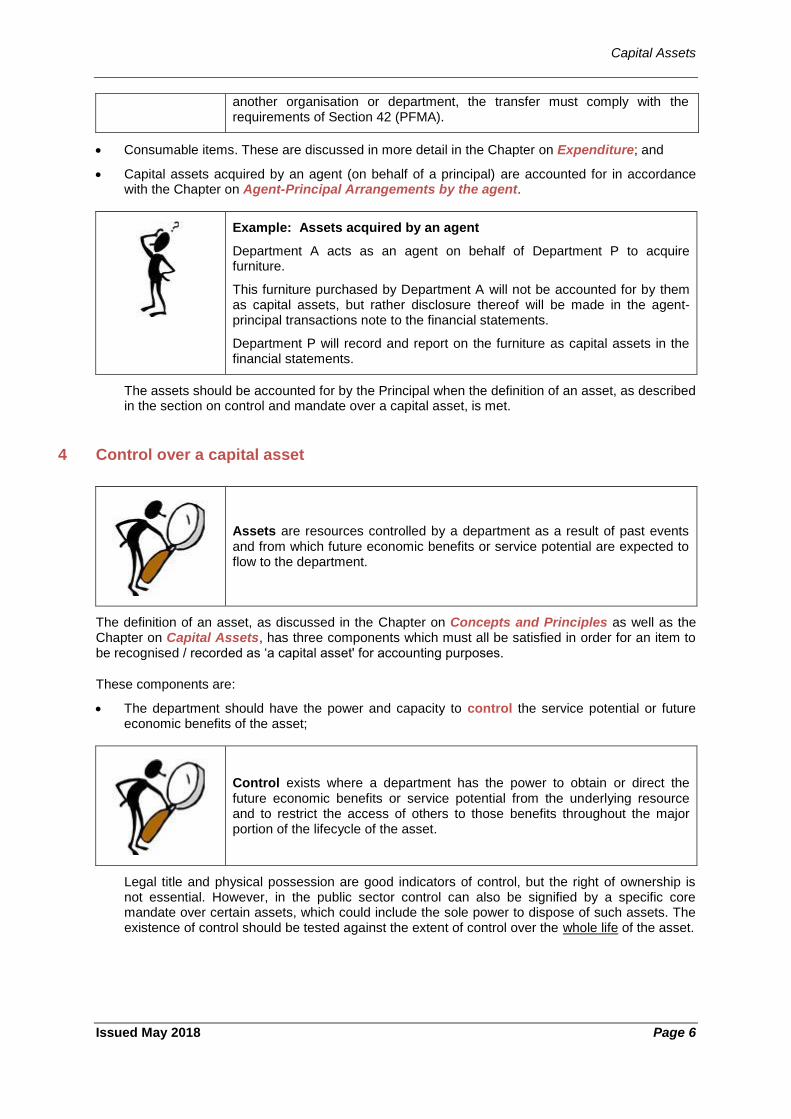

Consumable items. These are discussed in more detail in the Chapter on Expenditure; and

Capital assets acquired by an agent (on behalf of a principal) are accounted for in accordance with the Chapter on Agent-Principal Arrangements by the agent.

The assets should be accounted for by the Principal when the definition of an asset, as described in the section on control and mandate over a capital asset, is met.

4 Control over a capital asset

The definition of an asset, as discussed in the Chapter on Concepts and Principles as well as the Chapter on Capital Assets, has three components which must all be satisfied in order for an item to be recognised / recorded as ‘a capital asset' for accounting purposes.

These components are:

The department should have the power and capacity to control the service potential or future economic benefits of the asset;

Legal title and physical possession are good indicators of control, but the right of ownership is not essential. However, in the public sector control can also be signified by a specific core mandate over certain assets, which could include the sole power to dispose of such assets. The existence of control should be tested against the extent of control over the whole life of the asset.

another organisation or department, the transfer must comply with the requirements of Section 42 (PFMA).

Example: Assets acquired by an agent

Department A acts as an agent on behalf of Department P to acquire furniture.

This furniture purchased by Department A will not be accounted for by them as capital assets, but rather disclosure thereof will be made in the agent-principal transactions note to the financial statements.

Department P will record and report on the furniture as capital assets in the financial statements.

Assets are resources controlled by a department as a result of past events and from which future economic benefits or service potential are expected to flow to the department.

Control exists where a department has the power to obtain or direct the future economic benefits or service potential from the underlying resource and to restrict the access of others to those benefits throughout the major portion of the lifecycle of the asset.

Capital Assets

Issued May 2018 Page 7

The key principle is that of control or power of direction over the utilisation of the economic benefits or service potential of the asset rather than mere 'physical' control.

The capacity of a department to control benefits may be the result of legal rights, but benefits may satisfy the definition of an asset even when there is no legal right.

The service potential or future economic benefits arose from past transactions or events;

Capital assets are recorded from the point when some event or transaction transfers control over the asset to the department. It is essential that the past event giving rise to control be identified, since transactions or events expected to occur in future will not necessarily give rise to assets.

The asset should have future service potential or economic benefit for the department.

Assets that are used to generate net cash inflows are usually described as embodying ‘future economic benefits’. Assets that are used to deliver goods and services in accordance with a department’s mandate, but do not directly generate net cash inflows are often described as embodying ‘service potential’.

The concept of ‘commercial return’ for assessing whether an asset should be recognised / recorded is not always applicable to public sector entities, as they provide public services and redistribute wealth for a variety of social and economic purposes. Therefore in applying the asset definition to the public sector environment, the focus is mostly on service potential rather than future economic benefits.

Example: Existence of control

An ambulance used by a state owned hospital meets the definition of control because (a) the ambulance contributes to the achievement of the department’s overall objectives and thus embodies service potential; and (b) the department can restrict access to the ambulance – only qualified officials of the department can operate the ambulance.

Example: Indicators of past transactions or events are:

When the department pays for the asset;

When it takes possession of the asset; or

When it budgets for a project to develop / construct the asset.

Legislation is enacted that mandates a department to administer the asset.

Future economic benefit or service potential embodied in an asset is the potential to contribute directly, or indirectly, to the flow of cash and cash equivalents to the department or to the rendering of services by the department.

Service potential is the capacity of an asset, singularly or in combination with other assets, to contribute directly or indirectly to the achievement of an objective of a department.

This objective may include provision of services to other institutions or the public at large for which the department receives no or little economic return.

Capital Assets

Issued May 2018 Page 8

5 Tangible Assets and Intangible assets

5.1 Tangible Assets

Tangible assets are assets that one can touch, hold or feel that a department uses in the production or supply of goods and or services. Typical examples of tangible capital assets are facilities, equipment and vehicles. Since they are tangible items, they also have the risk of being destroyed by fire, wind/rain, or other disasters or accidents.

These assets form the majority of assets used by departments in the day to day administration of their functions and amounts to huge numbers and billions of rand. Tangible assets can further be separated based on whether they are movable (vehicles, furniture and computer equipment) or immovable (land, school buildings and office buildings). Recording capital assets and reporting thereon has a material impact on financial statements due to the continued investment in new assets on an annual basis and the value involved.

5.2 Intangible Assets

Not all intangible items meet the definition of an intangible asset for the purposes of financial reporting as they are not identifiable. The fact that software is contained on a CD or the right to use included in an agreement on paper, does not mean that the asset has physical substance because there is a physical item to touch. The asset is the knowledge or know-how which cannot be seen or touched. If an item within the scope of this section does not meet the definition of an intangible asset, expenditure to acquire it or generate it internally will be expensed through the statement of financial performance as part of goods and services rather than capital assets.

Example: Service potential

Provincial department of public works (DPW) builds office accommodation as part of its service delivery mandate. The objective is not to make a profit in rendering this service as would be the case for a landlord with a profit motive. Instead, by providing and maintaining the office accommodation for use by other departments it ensures that the service potential of the asset is utilised as well as the objectives/ mandate of the department realised.

Tangible assets are non-monetary assets having physical substance that:

are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes or for the development, construction, maintenance or repair of other capital assets; and

are expected to be used during more than one reporting period.

An intangible asset is an identifiable non-monetary asset without physical substance.

Capital Assets

Issued May 2018 Page 9

5.2.1 Identifiability of an intangible asset

An asset meets the identifiability criterion in the definition of an intangible asset when it:

is separable, i.e. is capable of being separated or divided from the department and sold, transferred, licenced, rented or exchanged, either individually or together with a related contract, identifiable asset or liability, regardless of whether the department intends to do so; or

arises from binding arrangements (including rights from contracts) regardless of whether those rights are transferable or separable from the department or from other rights and obligations.

For the purpose of this section, a binding arrangement describes an arrangement that confers similar rights and obligations on the parties to it as if it were in the form of a contract.

Example: Examples of intangible assets

Software;

Department X purchases 1 Lenovo Desktop T440 for R12 000. This laptop came with Windows Vista as the operating software.

Windows Vista is not separable (doesn’t meet the identifiability criterion) from the hardware and is the integral part of the laptop without which the laptop wouldn’t work and therefore should be treated as part of the hardware (Computer Equipment) and not disclosed separately as an Intangible asset.

Dr Computer Equipment (Tangible Asset) R12 000

Cr Bank R12 000

Department Y purchases Windows 7 package to replace the still working Windows Vista initially purchased with the laptop as Windows 7 is more advanced and as a result more desirable for R6 000

The newly acquired Windows 7 is not an integral part of the hardware even though it performs the same function as Windows Vista, however this software was purchased separately (Can be sold individually and monitory value attached – Off the shelf package is always likely to be an intangible asset as defined and meet the identifiability criterion)

The acquisition meets the definition on intangible assets and separable and should therefore be treated as the Intangible asset and be disclosed separately

Dr Software (Intangible Asset) R6 000

Cr Bank R6 000

Software licence fees;

Department X purchases Microsoft Office package for R10 000 cash and the department is also to pay R1 000 licence fee on an annual basis for as long as the package is in use. This licence fee will entitle the department to any Microsoft Office update or upgrades in future. Although the benefit of the license will be realised in future and thus it could be seen as a capital asset it would be written off within one year. As the MCS does not make provision for depreciation on assets the license fee is expensed on payment.

The Microsoft Office package is the intangible as per previous example above and annual licence fee will be expensed (Current Expenditure) as the amount relates to the maintenance of the package.

Capital Assets

Issued May 2018 Page 10

Initial recognition

Dr Software (Intangible Asset) = R10 000

Dr Annual licence fee = R1 000

Cr Bank R11 000

Subsequent years

Dr Annual License fee (Current expenditure) R1 000

Cr Bank R1 000

The treatment of the licence fee is closely linked to the period it will entitle the department to the use of the software. If the licence fee payable is for benefits for more than 12 months, it becomes a capital expenditure, intangible asset in its own right however, if the department is paying the annual licence fee for the next few years in order to take advantage of a discount, the licence fee still remains current expenditure since contractually it is payable yearly for annual benefits.

Other types of intangible assets include the following:

Rights under licensing agreements for films, videos, plays and manuscripts in entities such as broadcasting, tourism, arts and culture;

Patents and copyrights held by government entities in fields such as tourism, research, education, health, agriculture, archives;

Databases and database management software created and maintained by government entities, such as those containing information on the demographic statistics of the population, land ownership, private sector entity ownership and registers of securities and charges;

Airport landing rights;

Licenses to operate radio or television stations;

Import / export licenses; and

Right to control the extraction of mineral resources.

Termed software licenses versus perpetual software licenses

A distinction should be made between the license fee and the annual maintenance and support paid to the license holder (or its agent).

The software license fee may be regarded as an intangible asset (see discussion below), whereas the annual maintenance and support fee is regarded as a current expense when paid.

Departments either acquire a termed license or a perpetual license in terms of:

(a) A termed license – a department will acquire the “right to use” the software a period specified in the license agreement;

(b) A perpetual license – a department acquires the “right to use” the software in perpetuity.

Where a department acquires a termed license it must assess the term of use and whether the term exceeds 12 months. Where the term of use is greater than 12 months the software shall be classified as a capital intangible asset.

Perpetual software licenses are classified as capital intangible assets when acquired.

Capital Assets

Issued May 2018 Page 11

5.2.2 Without physical substance

Intangible Physical substance Why is it still seen as “without physical substance”?

Licenses (software licenses, etc.)

Licence document / agreement

The department pays for the right of use of, e.g. software. Thus a department does not pay for the tangible item being the piece of paper on which the license agreement is printed, but rather for the right to use the knowledge imbedded in the software (you can’t touch a right of use).

Application software CD The value of application software is not driven by the CD that it is loaded on, but rather by the knowledge that it embodies. Thus the physical substance is deemed to be incidental.

Contracts must be analysed to determine what the department is paying for and a policy developed to indicate the criteria used for splitting capital from expense and also update budget processes where the amounts are incorrectly budgeted for.

SITA Act Implications regarding software

Section 7 of the SITA Act 88 of 1998 as amended, provides for the State IT Agency's duties and powers consisting of the “Must” (mandatory) services and “May” (non-mandatory) services with regards to the application software development and maintenance services for both information technology software or infrastructure -[Section 7(1)(b)(ii) & (iii)].

It is therefore not always a requirement that the Agency provides the services. That being said, one must always bear in mind that every department is required to procure all (mandatory or non-mandatory) in terms of section 7(3) of the SITA Act as amended.

In case where the department has procured the services without the assistance of SITA, SITA Regulation 17, with particular reference to 17(1) and 17(2), the department should provide reasons why SITA was not used and if exemption was provided to procure the services without SITA.

Section 7(8) provides that in the performance of the Agency's duties and exercise of its powers, the Agency must amongst others eliminate unnecessary duplication of information technology goods or services. In order to eliminate duplication, SITA Act Regulation 4(6) provides for SITA to compile and maintain an up-to-date inventory of all information systems of departments to serve as basis for determining duplication of information systems. This is to ensure that if any department is trying to procure, or develop a new software application that already exists, SITA will be able to advise of the same so that the product can be used by other departments who have similar needs instead of duplicating what already exists.

It must be noted, that the services rendered to the department, either from or through SITA, becomes the product of the department, and ownership of such product belongs to the department. SITA is only used as a procurement arm of government, and does not become the owner of any product requested for by any department.

Capital Assets

Issued May 2018 Page 12

Intangible Physical substance Why is it still seen as “without physical substance”?

Electronic books or books for learners with eye impairment

CD The department buys 20 CD’s for the library. These CD’s can be borrowed and listened to, similar to books being borrowed for reading purposes.

Should a CD be damaged in any way, it will be

replaced by a new CD which must be bought, In

this instance the ‘asset’ is the tangible CD as there

is no right to the information contained on the CD

other than to listen to it.

Although the cost of the CD in question is greater

than that of an ‘empty’ one, the price paid is not for

the ‘right’ to the information contained thereon but

for the work to copy the material onto a CD format.

This is the same with a book. If a department

purchases a book full of information, that

department does not ‘own’ the information but a

physical representation of the information for use

or application of the information. The information

cannot be utilised for future benefit or copied or

sold without specific authorisation.

Educational Material CD In a case where the department purchases a CD from the creator of educational material with the rights to copy, distribute and place the educational material in the library, The ‘asset’ would be the ‘right to copy’. A right to the information on the CD and the ‘asset’ will be intangible. In this instance the CD is the incidental physical embodiment of the right.

Patents Patent registration document

The value of a patent is not driven by the piece of paper that indicates its registration but rather by the knowledge that it embodies. Thus the physical substance is deemed to be incidental.

6 Types of Capital Assets

Capital assets are non-current tangible or intangible assets of a department that are expected to be used or held by that department for longer than one year.

Capital Assets

Issued May 2018 Page 13

To distinguish between the different types of capital assets the department should request the Basic Accounting System (BAS) reports that contain the details of the asset segment.

Exclusion list

PFMA section 38(1)(d) states “The accounting officer for a department, trading entity or constitutional institution is responsible for the management, including the safe-guarding and the maintenance of the assets, and for the management of the liabilities, of the department, trading entity or constitutional institution.”

Keeping the above quoted legislation in mind, if the department has capital assets by definition but for whatsoever reason(s) chooses to have the exclusion list of capital assets:

a) The criteria for coming up with that exclusion list must be clearly documented and included in the departmental asset management policy

b) The criteria to be consistently applied and be accompanied by the enforceable alternative control procedures and

c) Those excluded capital assets still need to be controlled and managed.

Examples of capital assets in the public sector:

buildings (including investment properties);

land

biological assets;

specialised military equipment;

heritage assets;

infrastructure assets;

motor vehicles; and

intangible assets.

Capital assets are split into major capital assets and minor capital assets for administrative convenience.

Currently, minor capital assets include those items costing less than R5 000. To align this practice to the budget process they are budgeted for as “current” expenditure.

Costs incurred for research purposes are also classified as “current expenses” without considering the threshold.

6.1 Loose tools, spare parts and servicing equipment

Spare parts and servicing equipment are usually accounted for as inventory or consumables. However, certain spare parts and stand-by equipment qualify as capital assets when a department expects to use them during more than one period. Similarly, if the spare parts and servicing equipment can be used only in connection with a specific capital asset, they are accounted for as

Capital Assets

Issued May 2018 Page 14

capital assets. Examples of spare parts and servicing equipment are propellers and engines of aircrafts and vessels.

Some loose tools can be used for more than one year. Such tools can be small and relatively inexpensive and can be treated as inventory, consumables or minor capital assets. Examples of loose tools:

saws (manual or electronic);

spades;

axes and hammers;

screwdrivers;

spanners or wrenches; and

hand-held drills and grinders;

6.2 Safety equipment

Safety equipment acquired to meet environmental regulations, qualify as capital assets if they enable related assets to generate future economic benefits or service potential in excess of what these benefits would have been if this safety equipment was not acquired.

Some flexibility is however needed. Depending on the nature and significance of such tools, they may be treated as major capital assets and their acquisition and disposal recorded as such.

An example is where toolboxes are used. The toolbox including all tools can be treated as one unit and as a major capital asset since the value of all the tools in the box could be significant and collectively exceed the capitalisation threshold.

Example: Loose tools

Scenario 1

Department B purchases a medical toolkit which includes scalpels, forceps and tongs for R10 000. The equipment can be treated as one unit.

The toolkit is a major capital asset and will be recorded in the major asset register as a unit since the toolkit can be allocated to a specific custodian who can be held responsible for the content therein.

Scenario 2

A forceps included in the toolkit as per scenario 1 is lost and the Department purchases a new forceps for R300 to replace the lost one

The purchase of individual items within the toolbox is treated as maintenance (Current Expenditure – Goods & Services), the R300 would therefore be expensed. The total value of the toolkit does not change significantly by the replacement of an individual item so the original value remains relevant.

Example: Safety equipment

New legislation is enacted that requires x number of fire hydrants per floor of every building. The installation of the hydrants is needed to enable the continued use of the building and its future economic or service potential, in compliance with the new safety standards. The cost of the hydrants and the installation thereof will be recorded as a capital asset, major or

Capital Assets

Issued May 2018 Page 15

6.3 Library materials

Library materials under the control of the department that meet the definition of a capital asset must be accounted for by the department using the principles contained in this chapter, no matter how it was acquired. When testing for control the mandate and ultimate accountability must be considered not just the physical possession or location of the material itself.

6.4 Investment property

In determining whether a capital asset should be classified as investment property, a department considers if the main purpose and most significant use of the property is to earn rental or for capital appreciation.

minor depending on the cost.

An old building still in use has asbestos ceilings which were installed when the building was constructed. As a result of medical conditions that are directly attributed to asbestos the building can no longer be used as is. To enable further use the ceilings must be removed or covered up. A decision is made to cover up the existing ceilings with a new false ceiling made from special material that will protect users of the building from the asbestos particles. The cost of the new technology and installation thereof will be recorded as capital assets;

For detailed guidance on library materials refer to the Accounting for Library Material Guide on the Office of the Accountant-General’s (OAG’s) website.

Investment property is a property (land or a building or part of a building or both) held with the primary purpose of earning rentals or for capital appreciation or both, rather than for:

use in the production or supply of goods or services, or

for administrative purposes; or

sale in the ordinary course of operations.

Example: Investment property

A building owned by the department that is leased out under one or more operating leases in accordance with their service delivery objectives;

Property that is being redeveloped for continued use as an investment property;

Property that is being constructed or developed for future use as investment property;

Land held for an undetermined use.

Capital Assets

Issued May 2018 Page 16

Distinction between Investment Property and Other Buildings

Investment property Other buildings

The asset generates its own cash flows (on a commercial basis).

Rental income earned is incidental; the asset is made available for service delivery purposes.

For example, DPW, the mandated custodian of immovable property, in this case, buildings, provides one of those buildings to another government department (Department A) for use and Department A is charged a rental of R20 000 a month. The rent charged in this case is considered as incidental as DPW is doing so in execution of its service delivery mandated

The asset is held for capital appreciation. The asset is held to achieve service delivery objectives rather than to earn rental or for capital appreciation.

For example, all the buildings held by DPW whether occupied by DPW itself or by another department as a result of its service delivery mandate are not held specifically to earn rent or for capital appreciation purposes but rather for service delivery purposes

Includes property that is being constructed or developed for future use as investment property.

Includes owner-occupied property such as office buildings and residential buildings occupied by staff members.

[Assets used by employees, irrespective of whether or not the employees pay rent at market rates, are owner occupied – outside the scope of investment property]

Includes land held for an undetermined use. Includes assets held for strategic purposes.

Investment property is disclosed as part of Buildings and other fixed structures in the financial statements. To distinguish between the different types of buildings and other fixed structures the department must request the Basic Accounting System (BAS) reports that contain the details of the asset segment.

Example: Distinguishing between different types of properties

A department has three properties which are used as follows:

the first property is used as employee accommodation;

the second property is used as the offices of the department; and

the third property was specifically developed and constructed to earn rental income and is rented out to another entity for a monthly rental income.

Capital Assets

Issued May 2018 Page 17

First property

The property is held for employee housing to contribute to the department’s provision of services and therefore is not investment property. The building should be classified as residential buildings. It is not important whether there is alternative accommodation available for the employees or not - [Property housing the employees is specifically excluded from the scope of Investment Property]

Second property

The property is held by the department for administrative purposes and is specifically excluded from the definition of investment property. The building should be classified as non-residential buildings.

Third Property

The property is held exclusively to earn rentals and this property is specifically included in the definition of investment property and should therefore be classified as investment property.

There are instances where a portion of a property is held to earn rentals and another portion is used by the department itself for administrative purposes or for delivering goods and services. If the portions of the property can be sold separately then the portion held to earn rental is investment property.

Example: One property used as owner-occupied property and to earn rentals

Scenario1

A department owns a building of 750 square meters. The building consists of four floors of which the bottom floor of 210 square meters are offices used by the department and the top three floors consists of the remaining 540 square meters with 9 apartments which are being rented out to unrelated tenants. The office space and each apartment can be sold separately.

In this example the department has one property with a portion being owner-occupied and a portion being used to earn rentals. These portions are easily identifiable and as a result require different accounting treatment. The portion of the building used to earn rentals is investment property and the portion used by the department itself will be classified as owner-occupied (non-residential buildings).

Scenario 2

Department A owns a property which consists of two adjoining warehouses. The department uses the smaller warehouse of 100 square meters to store inventory and the larger warehouse of 700 square meters is being rented out and the department cannot dispose of these warehouses separately. According to Department A’s policy, significance regarding the classification between the investment property and other buildings is anything more than 40% of the floor space

In this example the department has one property with a portion being owner-occupied and a portion being used to earn rentals.

Before the department can classify the property as investment property it first needs to determine if the owner-occupied portion of the warehouse is insignificant or significant.

Total size of the warehouses = 800 square meters

Owner-occupied portion of total size = 12.5% (100 sqm / 800 sqm)

Capital Assets

Issued May 2018 Page 18

Investment Property portion of the total size = 87.5% (700 sqm / 800 sqm)

As per the asset management policy of department A, the property would

therefore be classified as an Investment Property since the owner-occupied

portion is significantly less than 40% of the floor space

6.5 Biological assets

The above definitions are explained by way of the examples below:

Biological assets Agricultural produce Products that are the result of processing after harvest

Sheep Wool Yarn, carpet

Trees in a plantation forest Logs Furniture

Plants Cotton Thread, clothing

Dairy cattle Milk Cheese

Pigs Meat Sausages, bacon

Bushes Leaf Tea, cured tobacco

Vines Grapes Wine

Fruit trees Picked fruit Processed fruit

Wildlife (game) Meat Venison

The key feature that differentiates agricultural activities from other related activities is the intended use of the assets.

Departments often encounter difficulties in deciding what type of asset category should be applied to a biological asset owned by a department. In deciding under which asset category a biological asset should be accounted for, a department should consider the intended use of such asset.

If an activity is for recreational purposes, it is specifically excluded from this section.

Biological assets are living animals or plants.

Agricultural produce is the harvested product of the department’s biological assets and will be reflected as inventory.

Biological transformation is the process of growth, degeneration, production or procreation that causes qualitative and quantitative changes in a biological asset.

For reporting purposes, we do not differentiate between biological assets held for agricultural purposes and other purposes as long as they all meet the definition of biological assets

Agricultural activity is the management by a department of the biological transformation of biological assets: for sale, into agricultural produce, or into additional biological assets.

For example, the Department of Correctional Services operates farms where crops are planted, tended and harvested for sale to the market or for use in the kitchens at the correctional facilities to feed the inhabitants. The Department is actively managing the process and is therefore involved in agricultural activity.

Capital Assets

Issued May 2018 Page 19

If the department does not actively manage the activity (being the biological transformation) or the assets do not undergo a biological transformation, it is not an agricultural activity and the assets should be treated as biological capital asset if it meets the definition.

As the MCS does not distinguish between biological assets and agricultural activities all biological assets will be reflected as capital assets where the definition is met.

Slaughtered animals and harvested crops are no longer biological assets, because once a biological asset is slaughtered or harvested it no longer meets the definition of a biological asset and should then be regarded as inventory until it is sold or distributed. Refer to paragraphs below.

Biological assets exclude any cultures, cells, bacteria and viruses used in laboratories for research purposes or as inputs into vaccines, etc. Items used for research purposes are classified as “current expenses”.

An important principle in the MCS is that departments should apply this chapter for agricultural produce only up to the point of harvest.

After harvesting the principles of inventory will apply to the produce.

Harvest is the detachment of produce from a biological asset or the cessation of a biological asset’s life processes.

Biological Assets examples

Scenario 1

Department A farms chickens, the chickens are to be sold or consumed within three months after their acquisition or birth date.

The chickens are biological assets by nature however due to their purpose or use in this case; they will not be treated as a capital asset since they do not meet the definition of capital assets as per MCS paragraph .09 of Capital assets chapter as they are never kept for more than a year.

These chickens should be classified as inventory

Scenario 2

Department A is mandated to manage the animal numbers for conservation purposes such as in National Parks. The department does not manage these animals individually but as a group (the environment).

The department is therefore not expected to tag these animals and record them in the asset register since the department does not have control as defined over each animal. The same applies for plants, bees flying over and so on.

The department is not also not expected to account for the randomly visiting animals that belong to the neighbouring farms (Animals belonging to the other institutions)

The activities conducted to manage the environment would be part of

Capital Assets

Issued May 2018 Page 20

6.6 Heritage assets

performance information.

However in a case of a Zoo where they do not only manage the numbers but

have control over the animals they keep, the animals will be individually

classified and recorded as biological assets

Scenario 3

Department B purchases ten heads of dairy cattle for R20 000 each on the 1st of June 2014.

At year end (31/03/2015), the fair value of the dairy cattle is R25 000 each.

The cattle will be disclosed at R250 000 at year end if the department’s policy is to show the dairy cattle at fair value, if not it must be reported at cost. The MCS Chapter on Capital assets allows the departments to use either of the two.

The department’s choice of either reporting at fair value or cost regarding biological assets must be clearly indicated in the department’s asset management policy.

It is advised that a department that has biological assets maintains a policy and standard operating procedures that clearly state the nature, management, accounting treatment and other useful information on the management of the department’s biological assets.

Heritage assets are assets that have a cultural, environmental, historical, natural, scientific, technological or artistic significance and are held indefinitely for the benefit of present and future generations.

Characteristics of heritage assets, include the following:

Their value in cultural, environmental, educational and historical terms is unlikely to be fully reflected in a financial value based purely on a market price;

Legal and/or statutory obligations may impose prohibitions or severe restrictions on disposal by sale;

They are often irreplaceable and their value may increase over time even if their physical condition deteriorates; and

It may be difficult to estimate their useful lives, which in some cases could be several hundred years.

Capital Assets

Issued May 2018 Page 21

Older buildings can be of an age where they may attain heritage status. Prior to any alterations being done the relevant national or provincial agency should be contacted to ascertain whether the structure is considered a heritage assets or not. There may be different conditions attached such as preserving of the façade but the interior could be altered or the entire structure may not be altered. Any conditions should be noted and flagged in the asset register.

In summary, some key features of heritage assets that can be used in identifying an asset as a heritage asset:

The asset is held indefinitely;

A national or provincial agency has declared the asset to be of historical significance;

The asset is protected, cared for and preserved for present and future generations;

The asset’s value increases over time; and

It may be difficult to determine a monetary value of the asset.

If a department still cannot determine whether the asset is a heritage asset or other tangible asset, it should ascertain the purpose of holding the asset, i.e. is it used to execute the department’s activities or for another purpose.

There are instances where heritage assets can have a dual purpose, for example where an historical building meets the definition of a heritage asset, but it is also used for offices.

These assets that are used for more than one purpose should be classified as a heritage asset when a significant portion of the asset meets the definition of a heritage asset.

The department cannot split an asset into more than one classification. For example: a portion of a property cannot be classified as buildings and another portion classified as heritage assets. The full asset is either a heritage asset or it is not a heritage asset.

Examples of heritage assets

Historical buildings and monuments e.g. Union Buildings;

Archaeological sites e.g. Sterkfontein Caves;

Conservation areas and nature reserves e.g. Cradle of mankind; and

Works of art e.g. paintings.

Determining whether or not the heritage portion is significant or not is a judgement that should be made by management. This determination does not have to be performed by an expert though the management is not prohibited from contracting one. Departments are encouraged to err on the side of caution and protection (Heritage assets classification) where it is not clear, rather than allowing disposal that might be costly or impossible to reverse in the future. This judgement should be applied consistently over all the assets.

To ensure consistent application of the criteria, it is recommended that management include the judgement criteria as part of their asset management policy. The asset management policy is also expected to indicate the identification and the valuation criteria of these heritage assets. The valuation technique will depend on the type of asset as some will have

Capital Assets

Issued May 2018 Page 22

6.7 Infrastructure assets

Some assets are commonly described as “infrastructure assets”. While there is no universally accepted definition of infrastructure assets, these assets usually display some or all of the following characteristics:

they are part of a system or network;

they are specialised in nature and do not have alternative uses;

they are generally immovable; and

they may be subject to constraints on disposal.

Although ownership of infrastructure assets is not confined to entities in the public sector, significant infrastructure assets are frequently found in the public sector. Infrastructure assets meet the definition for capital assets and must be accounted for in accordance with this chapter.

The examples above illustrate that infrastructure systems or networks consist of multiple different assets that work together to achieve a specific service such as a water supply or purification of water. As a result the asset should be unbundled into its components before recording in the asset register.

active markets, such as paintings, or the restoration or reproduction cost can be determined for constructed heritage assets such as buildings and monuments.

Examples of infrastructure assets

Department A procures fingerprint biometrics systems amounting to R1 Million. This system consists of biometric time and attendance readers, s-bus relay boxes and no-touch exit buttons and other items including the cabling specifications.

As much as this infrastructure would most likely be attached to the building, it is not necessarily immovable asset as it could still be detached from the building when the department permanently vacates the building depending on the occupation contract.

If any of the required items in the infrastructure is not working or malfunctioning, the whole system would fail, therefore the department manages the whole system rather than the individual “components” of the system. For reporting purposes, the department would record this infrastructure in the asset register as a one line item though the management records of the system would list each component for maintenance purposes.

On expiry of the contract or when the department permanently vacates the building and prohibited from detaching the system from the building, the total costs as per the asset register on that day will be

transferred to the books of DPW if the building belongs to DPW via PFMA section 42

written off if the building belongs to the private landlord

Other examples of infrastructure assets

Road networks;

Sewer systems;

Water systems;

Power supply systems;

Telecommunication networks;

Railways; and

Harbours.

Capital Assets

Issued May 2018 Page 23

The asset management policies of the department should specify how this should be done and to what level components should be individually recorded.

Departments usually have specific mandated portfolios of infrastructure to administer for example roads are the responsibility of the department of transport or roads and public works depending on the mandate. All roads should therefore be recorded by the mandated department in sections for identification and management and its policies should specify how for example intersections are recorded.

6.8 Specialist military equipment

Specialised military equipment will normally meet the definition for capital assets and should be recorded as such in accordance with this chapter. These assets are only for the use of the Department of Defence.

6.9 Internally generated intangible assets

It is sometimes difficult to assess whether an internally generated intangible asset qualifies as an intangible asset because of problems in:

identifying whether and when there is an identifiable asset that will generate expected future economic benefits or service potential; and

determining the cost of the asset reliably. In some cases, the cost of generating an intangible asset internally cannot be distinguished from the cost of maintaining or enhancing the department’s day-to-day operations.

To assess whether an internally generated intangible asset meets the criteria for being recorded, a department classifies the generation of the asset into:

Guidance on infrastructure assets is included in the following documents:

SCOA Classification Circular 3 of 2009 – SCOA Website

SCOA learners toolkit

MFMA Local Government Capital Asset Management Guide, Annexure C – Although this is a guide for Municipalities which are in an accrual environment, guidance may be of use to departments. – MFMA Website

COGTA (DPLG) guide on Infrastructure

Example: Specialised military assets

Weapons;

Weapons delivery systems;

Exposure equipment;

Flying suits;

Rigging; and

Ships and marine equipment.

Military hospitals and military airports are not included in this category even if they are used by these departments. These are non-residential buildings.

Capital Assets

Issued May 2018 Page 24

a research phase; and

a development phase.

Although the terms ‘research’ and ‘development’ are defined, the terms ‘research phase’ and ‘development phase’ have a broader meaning for the purpose of this chapter.

If a department cannot distinguish the research phase from the development phase of an internal project to create an intangible asset, the department treats the expenditure on that project as if it was incurred in the research phase only. NB: The department must keep in mind at conception of project and institute processes in order to be able to control spending which should be compared to budget and value for money.

6.9.1 Research phase

No intangible asset arising from research (or from the research phase of an internal project) must be recorded as a capital asset. Research expenditure is included as part of current expenditure in the financial statements.

In the research phase of an internal project, a department cannot demonstrate that an intangible asset exists that will generate probable future economic benefits or service potential.

Examples of research activities are:

activities aimed at obtaining new knowledge;

the search for, evaluation and final selection of, applications or research findings or other knowledge;

the search for alternatives for materials, devices, products, processes, systems or services; and

the formulation, design, evaluation and final selection of possible alternatives for new or improved materials, devices, products, processes, systems or services.

6.9.2 Development phase

Recognising / recording of costs to the cost of the capital asset commences with the development phase.

An intangible asset arising from development (or from the development phase of an internal project) must be recorded if, and only if, the department can demonstrate all of the following criteria:

the technical feasibility of completing the intangible asset so that it will be available for use or sale;

its intention to complete the intangible asset and use or sell it;

its ability to use or sell the intangible asset;

Research is the original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding.

Development is the application of research findings or other knowledge to a plan or design for the production of new or substantially improved materials, devices, products, processes, systems or services before the start of production or use.

Capital Assets

Issued May 2018 Page 25

how the intangible asset will generate probable future economic benefits or service potential. Among other things, the department can demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset;

the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset; and

its ability to measure reliably the expenditure attributable to the intangible asset during its development.

In the development phase of an internal project, a department can, in some instances, identify an intangible asset and demonstrate that the asset will generate probable future economic benefits or service potential. This is because the development phase of a project is further advanced than the research phase.

Examples of development activities are:

the design, construction and testing of pre-production or pre-use prototypes and models;

the design of tools, jigs, moulds and dies involving new technology;

the design, construction and operation of a pilot plant that is not of a scale economically feasible for commercial production; and

the design, construction and testing of a chosen alternative for new or improved materials, devices, products, processes, systems or services.

Availability of resources to complete, use and obtain the benefits from an intangible asset can be demonstrated by, for example, a strategic plan showing the technical, financial and other resources needed and the department’s ability to secure those resources.

Example: Research and development costs – restoration costs incurred

Department R&D received information of the existence of voice recordings of private conversations between Jan Smuts and Winston Churchill during the Second World War that may be of historical significance and subsequently underwent exploration costs to search for the recordings. At the reporting date, 31 March 20x4, nothing was found as yet.

The exploration cost for the period amounted to R500 000.

On 1 April 20x4, department R&D discovered the voice recordings and preliminarily verified the authenticity. No further costs were incurred.

However, the recordings were badly damaged and had to be restored and digitally re-mastered, after which an extensive verification process was followed to guarantee the authenticity. The costs of the verification, restoration and re-mastering amounted to R300 000.

The R500 000 will be treated as research cost under current expenditure.

The R300 000 will be treated as development cost under capital expenditure - heritage assets.

6.9.3 Website costs

A website does not have physical substance. As a result, development costs associated with a website are intangible assets if they meet the definition of an intangible asset and the development phase criteria.

Some websites are developed to comply with a statute or to be used mainly to provide information on the function, services, objective and performance of a department to the public at large. These websites will not meet the development phase criterion regarding generating probable future economic benefits or service potential and as such the costs incurred for the development of these websites should be expensed.

Capital Assets

Issued May 2018 Page 26

Example: Website cost - Determining whether a website can be capitalised as an intangible asset

It is important to note that a department will need to demonstrate how the website will generate probable future economic benefits or service potential, in order to capitalise the website as an intangible asset. If the department cannot demonstrate this, all expenditure on such a website should be recognised as a current expense under goods and services when it is incurred.

It is difficult to demonstrate that probable future economic benefits or service potential will be generated from a website developed solely or primarily to promote and advertise its own products or services; consequently all costs on developing such a website will be classified as a current expense. It is thus treated in the same manner as traditional ‘advertising’ cost as the impact thereof on the business is difficult to estimate or measure.

Where an entity created a website specifically for the use of e-learning students, where study material can be accessed after paying the relevant fees, the entity can show that future economic benefit or service potential will flow to the entity and the cost incurred in development of the website can be recorded as an intangible asset.

Example: Website costs

Department A decided to develop a website for its own use as well as the use by its target market.

Since the department had never developed a website previously, it was decided to first undertake a feasibility study and if successful, define hardware and software specifications, evaluate alternative products and suppliers and then select preferences. These steps were executed and eventually expenses of R60 000 were incurred in this regard.

In the next stage of the project, hardware was purchased, a domain name was obtained and operating software was developed. These developed applications were installed on the web server and the total cost incurred in this stage amounted to R220 000, of which the hardware comprised R80 000, the software R100 000 and the remainder was spent on obtaining the domain name.

Once the above had been completed, the appearance of the web pages was designed. A graphic designer rendered an account of R18 000, which was paid in cash immediately.

The content of the website was then developed. The cost involved in this development amounted to R25 000.

The website was brought into use on 01 April 20xx. During the 6 months following on it being commissioned, graphics were updated, the website was registered with a few new search engines and the usage of the website was analysed to establish the effectiveness thereof as a marketing tool. The costs amounted to R20 000.

Capital Assets

Issued May 2018 Page 27

6.10 Immovable assets

Immovable assets are always major assets. However, since some immovable assets were initially recorded in the asset register at a nominal amount they may have been allocated to the minor asset register. It is important to note that separate disclosure in the secondary information is required for immovable assets so recorded.

Description Amount (R) Classification

Feasibility study 60 000 Current Expenditure

Hardware 80 000 Tangible capital asset

Software 100 000 Intangible asset

Domain name

(220 000 – 80 000 – 100 000)

40 000 Intangible asset if the department can demonstrate how the website will generate probable future economic benefits or service potential or else its current expenditure

Graphical design development stage

18 000 Intangible asset if the department can demonstrate how the website will generate probable future economic benefits or service potential or else its current expenditure

Content development stage

25 000 Intangible asset if the department can demonstrate how the website will generate probable future economic benefits or service potential or else its current expenditure

Website testing 20 000 Current expenditure

An immovable asset is a capital asset consisting of land, infrastructure, buildings or a combination of thereof.

Capital Assets

Issued May 2018 Page 28

7 Recording of Capital Assets

7.1 General

For the purposes of recording capital assets, a department should maintain an asset register that will enable it to manage its assets, which includes the maintenance and replacement thereof, as well as to ensure that appropriate safekeeping measures can be put in place. It also assists with compliance with the disclosure requirements in the notes to the financial statements - refer to the Section on Disclosures below which sets out the disclosure required.

Upon initially recording a capital asset, a department must determine whether the capital asset is a minor or major capital asset and record the asset as such.

The threshold value for distinguishing between minor and major capital assets is determined by the Office of the Accountant-General (OAG), which is currently R5 000,meaning any asset costing R5 000 or above should be recorded as a major capital asset.

7.2 Asset register

An adequate asset register is integral to effective asset management and provides details of the values (figures) to be disclosed in the financial statements. Information can be contained in different databases but it is important that the information can be identified as belonging to a specific asset throughout. Where there is no identifier to link the information the management of assets will be negatively impacted.

All capital assets owned and controlled (which includes leased assets and minor assets) should be included in a register regardless of the funding source or value thereof. This need not be the same register. For example, during the lease term of a finance lease, the finance lease assets should be in a lease register and with regards to minor assets these can be included in a separate minor capital assets register.

For detailed guidance on departments that have the responsibility to account for the immovable assets belonging to the state, refer to the Immovable Asset Guide on the Office of the Accountant-General’s (OAG’s) website.

The document takes into account legislation and specific mandates in the vesting and custodianship of immovable assets.

Even though minor capital assets are not recorded under expenditure for capital assets, the total rand value and quantities of these assets are separately disclosed under the capital assets notes (refer to the Section on Notes for the disclosures required). The minor capital assets register must be made available to the external auditors at year-end. The controls over safekeeping, etc. of these assets are the same as for major capital assets. The register should be as at 31 March of the respective year. The minimum requirements of the minor capital assets register are the same as those of the major capital assets register.

An asset register is a database of information on each asset that supports the effective financial and technical management of the assets, and allows for the meeting of statutory requirements.

The asset register should also facilitate proper financial reporting

Capital Assets

Issued May 2018 Page 29

7.3 Components

Components are parts of a capital asset. Such items form part of the main capital asset, but have a useful life and/or value that are different to that of the main asset or is significant in value in relation to the asset as a whole and is therefore managed separately. Components may or may not be functional in their own right. These items are often replaced over the lifetime of the main asset. Where an asset is recorded in its component parts and a component is replaced, it is removed from the asset register and the replacement part recorded in the asset register, thus affecting the overall value of the asset.

Thresholds are not applied at a component level where the asset has been recorded in the asset register on a component level.

Examples of components are propellers and engines of aircrafts and vessels as well as ventilation systems of buildings.

The asset register should comply with the “Minimum Requirements for an Asset Register”. This document is available on the OAG website.

Example: Computer equipment

Department A purchases a desktop computer for a new employee. The desktop provided to the new employee comprises of a screen, a keyboard and the CPU. The total cost of the desktop is R8 300 and is made up as follows:

• Screen R2 000

• Keyboard R1 200

• CPU R5 100

The screen, keyboard and the CPU are components of the main asset, the desktop. If any of the parts is not there, the asset is unusable.

How should the department record this acquisition in its asset register?

Under normal circumstances, the components should be capitalised as part of the main asset in the asset register of the department (The main linked with its components whose total would amount to R8 300. However, the departments are currently not required to componentise their capital assets and therefore will record the computer as a unit with the total cost of R8 300

Should a component be replaced at a future date, the transaction will be classified as maintenance. The records are however updated with the new serial number but without amending the existing value of the asset.

Alternatively, systems allowing, where the components are recorded separately as part of the computer asset, replacement of a component will impact on the asset register. The old component will be removed and the new component recorded. The overall value of the asset ‘the computer’ will thus change to reflect the ‘new’ component.

Capital Assets

Issued May 2018 Page 30

8 Measurement of Capital assets

A department evaluates all costs on the date of acquisition and subsequent costs to add to, replace part of, or service it. The principles in the following paragraphs should be applied in determining the cost or fair value of a capital asset.

8.1 Initial measurement

A capital asset that qualifies for recording as a capital asset is measured at its cost.

The cost is the cash price equivalent, which for the purpose of this chapter, is the actual amount paid for the asset. Payment can be made as either a single payment or a series of payments over a period of time.

Where a capital asset is acquired through a non-exchange transaction from a non-government entity, its cost must be measured at its fair value as at the date of acquisition. In the case of an interdepartmental transfer the transferring department must fair value the asset if the cost price is not available before transferring the asset in accordance with Section 42 (PFMA) requirements. This ensures that one department is not burdening another department with the requirement to determine a fair value.

The exception to this fair value requirement is for movable assets acquired before 1 April 2002 (or another date as approved by the OAG), where the cost is not available or a fair value had not been determined before the implementation of the MCS. These assets can consequently be transferred at a R1 value, if so recorded in the transferring department’s asset register. Where these assets were however carried at cost or fair value by the transferring department they should be transferred at that value.

Departments are not at present required to componentise their assets in the asset register. The above discussion offers guidance on when a department elects to do so.

The application of a threshold does not apply at a component level. Components are always capital in nature by virtue of being part of a capital asset even where separately recorded in the asset register; they still form part of the overall asset.

Departments are encouraged to begin the process of componentising, where the system capability exists. Policies can be developed to indicate the level of componentising per asset that should be done, based on the asset management strategy. Guidance on componentising will be issued prior to the requirement thereof.

The cost of an asset that must be recorded in the asset register and the financial statements must be the cash price equivalent at the acquisition date, to bring the asset to the position and in the state to be ready for use as intended by management.

Capital Assets

Issued May 2018 Page 31

Example: Capital assets acquired through a non-exchange transaction

Scenario 1

Hi & Bye (Pty) Ltd, a private entity not related to any government institution donates a laptop to Government Department A together with all its historical supporting documentation including the original invoice and the asset register details on the 28th of February 2014 and the details as per the asset register are as follows:

Cost Price = R9 000 (Agrees to the invoice supplied)

Accumulated depreciated = R3 000

Book Value = R6 000

Purchase Date = 01/03/2013

The asset is a donation from a non- government entity, therefore Department A is still required to fair value the donated asset even though all the supporting documentation was provided.

This is to ensure that the asset is initially recorded at its fair value as required by the MCS and since the book value of an asset doesn’t translate to the fair value of the asset.

Government in general is gaining an asset that was never on its books

Scenario 2

Government Department A donates a laptop to Government Department B on the 15th of September 2014.

Accompanying the donation is the original purchase invoice amounting to R10 000 with the purchase date of 01/06/2010 and all the applicable PFMA S42 requirements being complied with.

This is a transfer from one department to the other department, therefore Department B will accept and record the laptop at the provided amount of R10 000

Government in general is not gaining any additional asset as the asset was already within the government environment

Scenario 3

Same scenario as in 2 above except Department A recorded the laptop at a value of R1 as it did not keep a proper asset register at the time of acquisition. As the Department did not retain documentation as required by the Treasury Regulations it cannot provide substantiating documentation on the cost of the laptop. Department A must therefore determine the fair value of the laptop; update its asset register, and then transfer (Section 42) to Department B providing documentation as to how the fair value was arrived at. Department B will record the laptop at its fair value as provided.

Scenario 4

Example: Asset was acquired before 1 April 2002

Department A wants to donate a laptop to Department B

(a) Department A could not determine the cost amount of the laptop when the asset register was compiled and recorded the asset at a value of R1 as allowed by the OAG.

Department A will transfer the asset at R1 and Department B will record the asset in its asset register at R1.

Capital Assets

Issued May 2018 Page 32

8.1.1 Movable assets:

Where the cost cannot be determined accurately, capital assets are measured at its fair value and where fair value cannot be determined, the capital asset is measured at R1. The use of fair value or R1 as initial measurement for initial recording of a capital asset is deemed cost. This alternative may not be applied where the cost is or should be available (e.g. current year additions). Where the fair value could not be determined a department should have documentation explaining the steps taken to determine a fair value and motivate why it came to the conclusion that it was not possible. This evidence should be retained for audit purposes.

Assets acquired before 1 April 2002 (or another day as approved by the OAG), where the cost is not available for any reason, may be recorded at R1 with no need to determine a fair value. Where an entity however reliably determined the fair value of such assets before the implementation of the MCS they could continue to carry them in the asset register at the determined value.

8.1.2 Immovable assets:

Immovable assets are valued at cost or fair value. The valuation hierarchy on initial recognition is cost of acquisition / construction, then fair value.

A department uses the principles and guidance in the Section on Fair value below in determining the fair value of a capital asset including the municipal valuation roll values where appropriate