Embed Size (px)

Citation preview

Copyright reserved Please turn over

Metro East Education District

MARKS: 300 TIME: 3 hours

This question paper consists of 20 pages and an answer book of 19 pages.

ACCOUNTING

GRADE 12

SEPTEMBER 2015

Accounting 2 MEED September 2015

Copyright reserved Please turn over

INSTRUCTIONS AND INFORMATION

Read the following instructions carefully and follow them precisely.

1. Answer ALL the questions 2. A special ANSWER BOOK is provided in which to answer ALL the questions. 3. Workings must be shown in the answer book in order to achieve part-marks. 4. Non-programmable calculators may be used. 5. You may use dark pencil or blue/black ink to answer the questions. 6. Where applicable, show ALL calculations to ONE decimal point.

Accounting 3 MEED September 2015

Copyright reserved Please turn over

7. Use the information in the table below as a guide when answering the question

paper. Try NOT to deviate from it:

QUESTION 1: 50 marks; 30 minutes

Topic of this question This question integrates:

Cost Accounting

Managerial Accounting Production Cost Statement and Notes Analysis and interpretation of unit costs and break-even point

Managing Resources Internal control

QUESTION 2: 40 marks; 25 minutes

Topic of this question This question integrates:

Bank and Creditors Reconciliation Internal control

Financial Accounting Bank reconciliation Reconciling a Creditors' Ledger account with a statement of account

Managing Resources Internal control

QUESTION 3: 65 marks; 40 minutes

Topic of this question This question integrates:

Companies - Financial statements:

Income Statement Notes to Balance Sheet

Financial Accounting GAAP Principles; Prepare Income Statement Inventory note

QUESTION 4: 60 marks; 35 minutes

Topic of this question This question integrates:

Cash Flow Statement Ratio analysis

Financial accounting Cash flow calculations Analyse and interpret financial information

QUESTION 5: 50 marks; 30 minutes

Topic of this question This question integrates:

Cash budget Projected Income Statement

Managerial Accounting Analyse and interpret a cash budget Problem solving

Managing resources Internal control and internal audit Ethical behaviour in a financial environment

QUESTION 6: 35 marks; 20 minutes

Topic of this question This question integrates:

Inventory and internal control

Managing resources Inventory valuation: FIFO, specific identification Problem solving

Accounting 4 MEED September 2015

Copyright reserved Please turn over

QUESTION 1 MANUFACTURING AND INTERNAL CONTROL (50 marks; 30 minutes)

SUPA BAKERY

Supa Bakery is owned by James May. The bakery bakes and sells loaves of bread direct to the consumer.

REQUIRED:

1.1 Complete the following: The note for Direct (Raw) Material Cost (9) Production Cost Statement for August 2015. (8) 1.2 Calculate the cost of each loaf of bread for August 2015. (3) 1.3 Total raw material cost increased drastically from July to August 2015. Give TWO

possible reasons for this increase. (4) 1.4 Calculate the variable cost per loaf of bread (to the nearest cent). (6) 1.5 James is not sure if the level of production for July and August was satisfactory.

Calculate the break-even point for August 2015. (6) Do you consider the level of production to be satisfactory or not? Explain and

quote figures to support your opinion. (4)

1.6 James is worried about the overtime payment to factory workers.

Quote figures from the information (on page 5) that will confirm his concern. (2) Explain TWO possible reasons that may justify the overtime. (4) Suggest TWO internal control measures that James could implement to

monitor and reduce overtime. (4)

Accounting 5 MEED September 2015

Copyright reserved Please turn over

INFORMATION: A. The bakery has no work-in-process as all the loaves are sold each day. Any bread

left over is donated to the local night shelter. B. Information extracted from the financial records

August 2015

Raw Materials:

Stock on hand: 1 August 2015 12 000

31 August 2015 15 000

Purchases: Credit 52 000

Cash 28 000

Carriage on raw materials 8 000

Administration Costs 9 000

Selling and Distribution Costs 7 200

Direct Labour Cost: Normal wages 30 000

Factory Overhead Costs 45 000

C. The following information was not taken into account: Raw materials of R5 000, not according to order, were returned to suppliers.

No reverse entries have been made yet. The bakery employs 5 workers. Each worker earned R8 000 overtime for

August 2015. Advertising (selling and distribution costs) includes R3 600 for a three month

contract which ends on 31 October 2015. D. Additional information

August 2015 July 2015

Direct raw materials costs ? R60 000

Fixed costs R 54 000 R 50 000

Selling price per loaf of bread R9 R9

Number of loaves produced 30 000 20 000

Break-even point ? 12 500

50

Accounting 6 MEED September 2015

Copyright reserved Please turn over

QUESTION 2 BANK RECONCILIATION AND INTERNAL CONTROL (40 marks, 25 minutes)

2.1 BANK RECONCILIATION

You are provided with information from the records of Langa Stores.

REQUIRED:

2.1.1 Calculate the correct Bank balance in the General Ledger of Langa Stores on 31 August 2015. (11)

2.1.2 Prepare the Bank Reconciliation Statement on 31 August 2015. (11)

2.1.3 Refer to the outstanding deposit of R18 600 dated 14 August 2015.

Give TWO reasons why the internal auditor should be concerned about this deposit.

Suggest TWO internal control measures that will monitor cash deposits more effectively. (6)

2.1.4 Refer to the dishonoured cheque, R7 400, received from the debtor (information E). Explain TWO measures to prevent dishonoured cheques in future. (4)

INFORMATION:

A. Extract from the Bank Reconciliation Statement on 31 July 2015

Bank statement balance (31 July 2015) (credit) R10 962

Deposit not processed by the bank R11 340

Cheques not yet presented to the bank for payment:

No 512 (dated 3 February 2015) R10 150

No 766 (dated 25 July 2015) R11 700

No 767 (dated 27 July 2015) R12 630

B. The bookkeeper of Langa Stores calculated the Bank account balance in the ledger as R13 138 on 28 August 2015, before any reconciliation with the August bank statement was completed.

C. Cheque no 766 and the deposit (shown in A above) appeared on the

August bank statement received from CA Bank.

Cheque no 512 is now stale and must be cancelled. No cheque will be issued to replace it.

D. Cheque 781 entered as R15 153, appeared on the August bank statement as R15 513. The amount on the bank statement is correct.

Accounting 7 MEED September 2015

Copyright reserved Please turn over

E. Amounts that appeared only on the August bank statement and that were not recorded in the cash journals:

Bank charges, R480

Cheque 1020 for R15 540. On investigation CA Bank found that this cheque was issued by Bunga Stores. CA Bank promised to correct this error before the next bank statement date in September.

Direct deposits:

- from Africa Bank, R10 800. It is for a fixed deposit that matured in August 2015, including interest of R800.

- from the tenant, R8 000 for the monthly rent income.

A dishonoured cheque, R7 400, received from a debtor, in settlement of his debt of R7 535.

F. The following cheques were entered in the CPJ before 28 August 2015,

but do not appear on the August bank statement.

Cheque 786, R2 340, issued to a creditor in settlement of an account of R2 600.

Cheque 802 for R9 000, dated 28 September 2015, issued to the builder

for maintenance to be completed in September. G. A deposit of R18 600, dated 14 August 2015, does not appear on the bank

statement for August 2015. H. The bank statement showed a favourable balance of R23 678 on

31 August 2015.

Accounting 8 MEED September 2015

Copyright reserved Please turn over

2.2 CREDITORS RECONCILIATION PC Traders received a statement of account for July 2015 from a creditor,

DH Suppliers. The balance of statement did not agree with that on the account of DH Suppliers in the Creditors' Ledger of PC Traders.

REQUIRED:

Complete the table in the ANSWER BOOK to show how the differences must be treated in order to reconcile the Creditors' Ledger account balance with the statement balance.

Write the amounts in the appropriate columns and indicate the increase or decrease with a (+) or (-) with each amount.

Total the columns to show the correct balances at the end of July 2015. (8) INFORMATION: Balances on 31 July 2015

DH Suppliers in the Creditors' Ledger of PC Traders R14 905

Statement received from DH Suppliers R15 120

A comparison between the Creditors' Ledger account for DH Suppliers and the

statement of account showed the following differences: 2.2.1 The statement reflects interest of R415 on the overdue account.

DH Suppliers acknowledged that it was an error and promised to reverse the entry in the August statement.

2.2.2 An invoice, received from DH Suppliers, was entered in the Creditors'

Ledger account as R2 080. The statement of account reflects the correct amount of R2 800.

2.2.3 A credit note for R460 received from DH Suppliers for goods returned was

incorrectly recorded as an invoice by PC Traders.

40

Accounting 9 MEED September 2015

Copyright reserved Please turn over

QUESTION 3 CONCEPTS, INCOME STATEMENT, NOTES TO BALANCE SHEET (65 marks; 40 minutes)

3.1 CONCEPTS Choose the GAAP principle from the table below that is described by each of the

following examples. Write only the GAAP principle next to the question number (3.1.1-3.1.4) in the ANSWER BOOK.

Materiality Prudence Business entity

Matching Historical cost Going concern

3.1.1 Property and trading stock are valued and reflected in the financial

statements at the original cost to the business. 3.1.2 Commission income is recorded in the period in which it was earned. 3.1.3 Trade debtors are shown at a lower value in the balance sheet to provide

for irrecoverable debts that may occur in the near future. 3.1.4 Financing cost should be shown separately in financial statements, as it

influences a decision on how to raise additional funds. (4) 3.2 METRO SUPERMARKET LTD You are provided with information for the financial year ended 31 July 2015. REQUIRED: 3.2.1 Refer to Information E and calculate the profit or loss on the trade-in of the

delivery vehicle. (8) 3.2.2 Complete the Income Statement for the year ended 31 July 2015. (47) 3.2.3 Prepare the Inventories Note to the Balance Sheet as at 31 July 2015. (6)

Accounting 10 MEED September 2015

Copyright reserved Please turn over

INFORMATION: EXTRACT FROM THE PRE-ADJUSTMENT TRIAL BALANCE ON 31 JULY 2015

Balance Sheet accounts section Dr Cr

Ordinary share capital 2 500 000

Delivery vehicle (one vehicle only) 125 000

Accumulated depreciation on vehicle 75 000

Equipment 230 000

Accumulated depreciation on equipment 110 000

Fixed deposit: YC Bank (9% p.a.) 80 000

Trading stock 289 000

Consumable stores on hand (1 August 2014) 3 500

Debtors control 49 400

Provision for bad debts 2 380

Nominal accounts section

Sales ?

Cost of sales 935 500

Bad debts recovered 2 500

Commission income 14 800

Interest on fixed deposit 5 400

Auditors' fees ?

Advertising 8 000

Bad debts 2 100

Directors' fees 75 000

Insurance 5 110

Packing material 45 300

Salaries and wages 102 000

ADJUSTMENTS AND ADDITIONAL INFORMATION: A. Selling prices are determined by using a mark-up of 60% on cost. Trade

discounts of R23 300 were allowed to special customers during the year. B. A fire in the storeroom caused damage to stock, valued at R4 000. The

insurance company refused to cover these damages as flammable materials were not stored according to safety regulations. No entries have been made.

Accounting 11 MEED September 2015

Copyright reserved Please turn over

C. The bookkeeper has neglected to reverse the stock of packing

materials on hand at the beginning of the accounting period.

Packing material used during the year, R44 200.

D. The physical stocktaking on 31 July 2015 reflected the value of the trading stock on hand as R283 000.

E. The delivery vehicle was traded-in on 1 May 2015 for R42 000 on a new vehicle, but no entries have been made. Vehicles are depreciated at 20% p.a. on the fixed instalment method. The cost of the new vehicle was R210 000.

F. Equipment is to be depreciated at 10% p.a. on the diminishing balance.

G. Provide for outstanding interest on the fixed deposit for 3 months. Interest is to be capitalised.

H. Commission, R1 500, is owed to Metro Supermarket by Sticky Ice Cream in respect of a promotion of new ice-cream held at the supermarket during May 2015.

I. Directors' fees, R15 000, were still owing to directors at the end of the accounting period.

J. A payment of R960 was made in July 2015 to the local radio station for an advert that will be broadcasted during August 2015.

K. Further bad debts of R1 400 must be written off. Provision for bad debts is to be maintained at 6% of good book debts.

L. One of the employees who was on sick leave was omitted from the Salaries Journal for July 2015. Her salary details were as follows:

Gross Salary Deductions Net salaries

Employers’ contribution

? R5 000 R12 000 R3 000

M. Income tax for the financial year is calculated as R53 325. This is 30% of the net profit before tax.

N. The amount for the Auditors' fees is the balancing figure in the Income statement.

65

Accounting 12 MEED September 2015

Copyright reserved Please turn over

QUESTION 4 CASH FLOW STATEMENT, INTERPRETATION AND RATIO ANALYSIS (60 marks; 35 minutes)

You are provided with information relating to Neonell Hardware Ltd, a public company whose financial year ends annually on 28 February.

REQUIRED:

4.1 Explain the difference between a Balance Sheet and a Cash Flow Statement. (2) 4.2 Calculate the following amounts as it would appear in the Cash Flow Statement on

28 February 2015: Dividends paid (5) Cash flow from financing activities (10) Net change in cash and cash equivalents (4) 4.3 At the AGM a shareholder stated that she is unhappy about the bank overdraft on

28 February 2015. She feels that the directors made some poor decisions that resulted in this situation. Explain TWO such decisions, with relevant figures, to support her opinion. (6)

4.4 Calculate the following financial indicators for the year ended 28 February 2015: 4.4.1 Acid test ratio (5) 4.4.2 Net asset value per share (3) 4.4.3 Debt-equity ratio (3) 4.5 The directors wanted to expand business operations and therefore chose to

increase loans during the current financial year, instead of issuing more shares.

Explain and quote TWO financial indicators (actual figures/ratios/percentages) that are relevant to their choice. Explain whether this was a good choice or not. (8)

4.6 The directors are of the opinion that the liquidity has deteriorated. Explain and

quote THREE financial indicators (with figures) to support their opinion. (9) 4.7 The Nel family owns 740 000 shares in this company. Explain the effect that the

repurchase of shares on 31 December 2014 had on their control of the company. Give a calculation(s) to support your answer. (5)

Accounting 13 MEED September 2015

Copyright reserved Please turn over

INFORMATION: A. Information from the Income Statement for the year ended 28 February 2015:

Depreciation 370 200

Interest on loan (capitalised) 88 500

Net profit before tax 1 575 000

Income tax 441 000

B. Information from the Balance Sheet as at:

28 Feb. 2015 28 Feb. 2014

Fixed Assets (carrying value) 8 473 400 4 569 000

Current Assets 3 337 300 4 641 000

Inventories 818 200 641 000

Trade debtors 2 377 600 1 512 000

SARS: income tax 128 000 -

Cash and cash equivalents 13 500 2 488 000

Shareholders' equity 8 839 000 7 400 000

Ordinary share capital 8 700 000 6 600 000

Retained Income 139 000 800 000

Mortgage Loan: Star Bank (12,5% p.a.) 908 000 508 000

Current Liabilities 2 063 700 1 302 000

Trade creditors 678 700 700 000

Shareholders for dividends 870 000 480 000

Bank overdraft 515 000 -

SARS: Income tax 122 000

C. Shareholders' register:

DATE DETAILS

1 March 2014 1 200 000 shares in issue

31 March 2014 300 000 additional shares issued at R8 each

31 December 2014 50 000 shares bought back at R9,50 each. Average price of all shares issued to date was R6 per share.

28 February 2015 1 450 000 shares in issue

Accounting 14 MEED September 2015

Copyright reserved Please turn over

D. Dividends for the financial year ending 28 February 2015:

Interim dividends paid on 31 August 2014 50c per share

Final dividends declared on 28 February 2015 R870 000

E. Details regarding movement of fixed assets in 2015

New, larger premises (land and buildings) acquired 4 051 000

A new vehicle purchased, to replace vehicle traded in 330 000

A vehicle traded in at carrying value (after 1½ years in operation) 106 400

F. Some financial indicators

28 Feb. 2015 28 Feb. 2014

Debt-equity ratio ? 0,1 : 1

Net asset value per share (NAV) ? 617 cents

Current ratio 1,6 : 1 3,6 : 1

Acid test ratio ? 3,1 : 1

Stock turnover rate 6,8 times p.a. 5,1 times p.a.

Debtors' collection period 40 days 35 days

Return on average capital employed (ROTCE) 18,8% 16,4%

60

Accounting 15 MEED September 2015

Copyright reserved Please turn over

QUESTION 5 CASH BUDGET and PROJECTED INCOME STATEMENT (50 marks, 30 minutes)

5.1 CASH BUDGET AND PROJECTED INCOME STATEMENT

You are provided with information relating to Quality Traders for the period ending

31 July 2015. REQUIRED: Complete the table in the ANSWER BOOK by filling in only the amounts in the

appropriate columns. EXAMPLE: Commission will be received on promotion items sold, R3 000

No Amount in the Cash Budget for July 2015

Amount in the Projected Income Statement for July 2015

RECEIPT PAYMENT INCOME EXPENSE

Example R3 000 R3 000

5.1.1 Interim dividends to be paid to shareholders, R25 000. 5.1.2 Expected cash sales for July 2015 will amount to R45 000 (cost of sales,

R21 000) 5.1.3 Bad debts to be written off in July 2015 will amount to R1 200. 5.1.4 Payments to creditors, R18 000, are expected to be made during

July 2015. Discount of R900 will be claimed. 5.1.5 Directors fees to be paid in July 2015, R50 000. 5.1.6 Depreciation for the 2015 financial year will be R33 600. (12)

Accounting 16 MEED September 2015

Copyright reserved Please turn over

5.2 CASH BUDGET

You are provided with an incomplete Cash Budget of CKC Traders for the period 1 October 2015 to 30 November 2015. Chase Khumalo is the owner.

REQUIRED:

5.2.1 Calculate the credit sales for October 2015 and then complete the Debtors' Collection Schedule for November 2015. (6)

5.2.2 Calculate the missing amounts indicated by (i)-(v) on the Cash Budget. (12) 5.2.3 On 31 October 2015 you compared the budgeted amounts with the actual

amounts and found the following:

OCTOBER 2015

BUDGETED ACTUAL

Sales R108 000 R84 000

Cost of sales 72 000 60 000

Gross profit 36 000 24 000

Delivery costs 10 800 12 600

Telephone costs 5 000 7 500

5.2.3.1 Chase decided to offer special discounts to customers during

October. They will be reminded weekly by telephone or sms about this offer.

In your opinion, has this benefitted the business? Provide figures to support your answer. (4)

5.2.3.2 Explain what you would say to Chase about the control of: Delivery costs Telephone costs Quote figures to support your answer and provide ONE point of

advice in EACH case. (6) 5.2.4 Refer to information F and G. Chase has required your advice regarding the new vehicle. 5.2.4.1 Calculate the purchase price of the new vehicle. (4) 5.2.4.2 Apart from the deposit and the monthly instalment of R6 250,

explain how the next Cash Budget will be affected. State THREE points. (6)

Accounting 17 MEED September 2015

Copyright reserved Please turn over

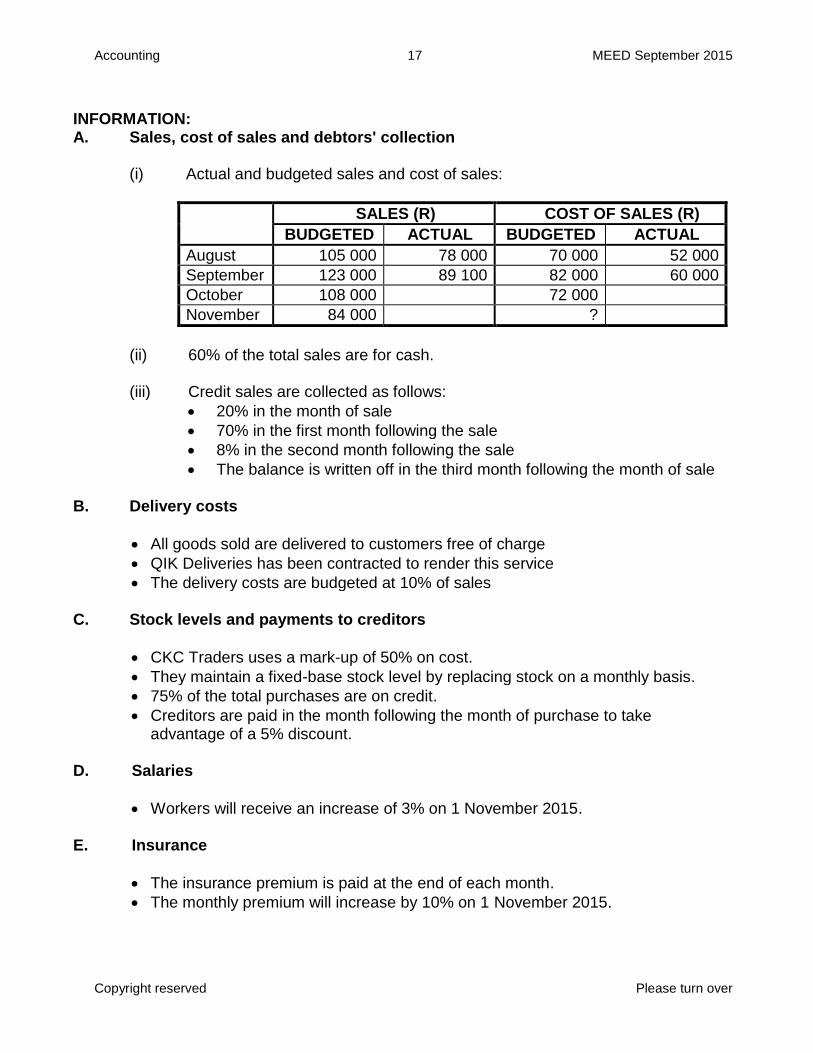

INFORMATION: A. Sales, cost of sales and debtors' collection

(i) Actual and budgeted sales and cost of sales:

SALES (R) COST OF SALES (R)

BUDGETED ACTUAL BUDGETED ACTUAL

August 105 000 78 000 70 000 52 000

September 123 000 89 100 82 000 60 000

October 108 000 72 000

November 84 000 ?

(ii) 60% of the total sales are for cash. (iii) Credit sales are collected as follows:

20% in the month of sale 70% in the first month following the sale 8% in the second month following the sale The balance is written off in the third month following the month of sale

B. Delivery costs All goods sold are delivered to customers free of charge QIK Deliveries has been contracted to render this service The delivery costs are budgeted at 10% of sales

C. Stock levels and payments to creditors CKC Traders uses a mark-up of 50% on cost. They maintain a fixed-base stock level by replacing stock on a monthly basis. 75% of the total purchases are on credit. Creditors are paid in the month following the month of purchase to take

advantage of a 5% discount.

D. Salaries Workers will receive an increase of 3% on 1 November 2015. E. Insurance The insurance premium is paid at the end of each month. The monthly premium will increase by 10% on 1 November 2015.

Accounting 18 MEED September 2015

Copyright reserved Please turn over

F. Details relating to the delivery costs and new vehicle Chase is considering purchasing a delivery vehicle in December 2015 and

stopping using QIK Deliveries for this service. He hopes to improve his cash flow.

CKC Traders would have to pay a 10% deposit. Chase’s uncle has agreed to provide interest-free finance for the balance of the cost of the vehicle. Repayments to his uncle will be R6 250 per month over 36 months.

G. Extract from the Cash Budget for the two months ending 30 November 2015

Receipts October November

Cash sales of goods 64 800 50 400

Collection from debtors 46 440

Rent income 7 500 8 250

Additional capital to be contributed 100 000

Total receipts

Payments

Cash purchase of trading stock 18 000 (i)

Payment to creditors (ii) 51 300

Salary: five workers 32 000 (iii)

Telephone 5 000 6 000

Advertising 18 000 12 000

Insurance (iv) 2 904

Delivery costs (payable to QIK Deliveries) 10 800 8 400

Other operating expenses

Drawings 15 000 15 000

Total payments

Cash surplus /deficit (22 600)

Bank balance at beginning of month (10 200) (v)

Bank balance at end of month

50

Accounting 19 MEED September 2015

Copyright reserved Please turn over

QUESTION 6 INVENTORY AND INTERNAL CONTROL (35 marks, 20 minutes)

6.1 Choose the advantage from COLUMN B that matches the term/concept in COLUMN A. Write only the letter (A–E) next to the question number (6.1.1–6.1.3) in the ANSWER BOOK.

COLUMN A COLUMN B

6.1.1 FIFO A Price fluctuations are not taken into account at all

6.1.2 Specific identification

B Accurately calculate the value of closing stock based on most recent purchase prices

6.1.3 Weighted Average C Drastic economic fluctuations may result in very low valuation of closing stock

D Number of items on hand can easily be determined through inspection

E Best suited when large volumes of identical small stock items are sold

(3)

6.2 STYLE FURNISHERS

Style Furnishers sells microwave ovens. The owner is Steve Smart. As he has other businesses to run, he cannot be at the shop very often. He employed Jane Jonker to manage the shop for him. They use the periodic inventory system and the first-in-first-out (FIFO) method to value the stock. The financial year ends annually on 30 June.

REQUIRED:

6.2.1 Calculate the value of the closing stock of 145 microwave ovens on 30 June 2015 using the FIFO method. (6)

6.2.2 Calculate the following: Cost of sales

Average mark-up% achieved for the year (6) (4)

6.2.3 Refer to Information D.

Provide a calculation to prove whether the information given by the storeroom supervisor is accurate or not. (6)

6.2.4 Jane is concerned that the final stock of 145 microwave ovens is not appropriate for the business. Provide a calculation or figures to support her opinion, and explain. (3)

Accounting 20 MEED September 2015

Copyright reserved

6.2.5 Jane has adjusted the selling prices during the year to attract new customers.

Comment on whether or not this strategy has benefitted the business. Provide figures to support your answer. (3)

6.2.6 Provide TWO points to assist Jane in improving internal control of inventory in

the business. (4)

INFORMATION:

A. Stock balances:

NUMBER OF UNITS

UNIT PRICE (including carriage)

TOTAL

1 July 2014 (inclusive of transport costs) 70 R5 500 R385 000

30 June 2015 145 ? ?

B. Purchases of microwave ovens during the financial year ended 30 June 2015:

NUMBER OF UNITS

UNIT PRICE

CARRIAGE TOTAL

September 2014 150 R5 000 R18 750 R768 750

December 2014 120 R4 750 R15 000 R585 000

April 2015 90 R4 450 R11 250 R411 750

TOTAL 360 R45 000 R1 765 500

C. Returns to suppliers:

Three microwave ovens from the December 2014 purchases were faulty and returned to suppliers. The suppliers also reversed the carriage on these items.

D. Possible theft of microwaves:

The storeroom supervisor informed Steve that he suspects Jane of giving away micro-wave ovens to family members and friends.

E. Sales for the year were as follows:

Selling Price Quantity TOTAL

July to October 2014 R9 100 80 units R728 000

November 2014 to March 2015 R9 800 30 units R294 000

April 2015 R7 500 150 units R1 125 000

May to June 2015 R9 800 16 units R156 000

276 units R2 303 800

35

TOTAL: 300

![BY VANAIR Installation Instructions - R44Installation Instructions - R44 INSTALLATION BearPaw Installation Reference Documentation: [1] Robinson R44 - Maintenance Manual & Instruction](https://img.pdfslide.net/doc/110x75/611c1e10c6d43953dc4a519f/by-vanair-installation-instructions-installation-instructions-r44-installation.jpg)