Embed Size (px)

Citation preview

ACCOUNTING PROCEDURES

MEETING WITH ALL SENIOR ACCOUNTS/JUNIOR ACCOUNTS AND ACCOUNTS OFFICERS

MEETING ON 20.4.2015 AT 11.00 AM

Accounting system is a series of tasks in an organisation by which transactions are processed as a means of maintaining financial records.

NEED FOR MUNICIPAL ACCOUNTS

Essential for Good GovernanceNecessary for collection of all taxes

and Non-TaxesProvide a true status of financial

positionUtilization of funds in confirmation

with financial standards.Adherence to budget provisionEssential for preparation of Budget

estimates and Administration Report

ROLES & RESPONSIBILITY OF ACCOUNTANTS

Accountant is the head of accounts section.

Plays a key role in maintenance of the accounts

Administrative ResponsibilitiesFinancial Responsibilities

ROLES & RESPONSIBILITY OF ACCOUNTANTS (CONTD.)

Administrative Responsibilities: - He/She is responsible for preparation

of monthly and annual accounts.- He/She is responsible for

preparation of budget estimate and RBE. - Preparation and consolidation of

replies to objections raised in the audit. Financial Responsibilities:

- He/She is responsible for proper maintenance of cash book, cheque book, and treasury / bank pass book and custody.

ROLES & RESPONSIBILITY OF ACCOUNTANTS (CONTD.)

He/she is responsible to ensure that all payments from municipal funds are made as per principles of Municipal Accounts Code, the rules & instructions by the GovernmentTo close the cash book every month by 10th of

succeeding month.

To reconcile each cash book with chitta, bank remittances and subsidiary registers including e-seva remittances.

To reconcile the cash books with treasury / bank pass book every month.

ROLES & RESPONSIBILITY OF ACCOUNTANTS (CONTD.)

To maintain Posting Register.To keep all paid vouchers in safe-custody

and produce the same before audit. To ensure maintenance all subsidiary

registers. To maintain prescribed for accounts

section. To scrutinize and pass all bills including

work bills. To ensure recovery of Income tax from

the bills paid to the contractors and its prompt remittance to income tax department

ROLES & RESPONSIBILITY OF ACCOUNTANTS (CONTD.)

To ensure relevant recoveries are made from employees, contractors, suppliers etc. and ensure their prompt remittance to the respective heads/departments without any delay.

To ensure prompt adjustment of assigned revenues, non-plan grants, plan grants etc. to the municipal funds.

To ensure prompt payment of loan annuities.

ROLES & RESPONSIBILITY OF ACCOUNTANTS (CONTD.)

• To ensure adjustment /recovery of all kinds of advances pending over three months.• He is responsible for all the investments made by municipality and ensure prompt realization / renewal of interest / investment• To ensure prompt maintenance of Budget allocation register to avoid excess expenditure on budget head.• Responsible for placing the financial position of the municipality before the Council every month.• Responsible to attend the council meetings and preparation of agenda of accounts section

RECIEPTSAfter verification by Tax clerk he permits

the BCs to deposit money in Mpl. Treasury.Shorff receives money and acknowledges

and enter in chitta.All monies received from BCs,other

staff,Public are entered in chitta by Shorff.Daily collection including cheques should

be sent to bank through challan on next working day.

Entries to be made in DEABAS on daily basis

EXPENDITURE- ACCOUNT

VoucherEvery person having a claim against

Mpl.fund shall present a billIt shall be signed and dated, and

stampedAll payments shall be made only after

bills are passed by the CommissionerBill after passed for payment is called a

“Voucher”Vouchers are entered in cash book on

debt sideSerial No. to be given

EXPENDITUREAll payments to be made in form of

chequeWhen inevitable cash payment may

be made for meager amounts. Mostly to be avoidedCash payments to be made by shorffTo be vigilant while incurring

expenditure Head wise posting to be made in

DEABAS on daily basis without fail.

EXPENDITURE (CONTD.)CC charges to be paid promptlyRecoveries from bills

VATIT

Besides recovery and remittance, online entries to be made on quarterly basis

Seniorage EPFESIAll Delayed payments attracts interest and

freezing of accounts.

CHECK LIST T.N.NO Name of the work Estimate Cost General Funds/Scheme Funds Council Resolution No Technical Sanction No T.A.C.R.NO Work Order Date Name of the Contractor Agreement No M.A.E M.B.NO 1% E.M.D

D.D.NO._____________Dt.__________Rs.____________ 1.5% E.M.D

D.D.NO._____________Dt.__________Rs.____________

EXPENDITURE Thumb Rules

All expenditure should be sanctioned by council

No payments without Administrative sanctions

work bills below Rs 1.00 lakhs is through tenders only.

Work bills above Rs 1.00 lakhs is through e-procurement

Materials should be entered in stock registers

Item wise watch registers to be maintainedAll entries to be made in DEABAS MAARC will monitor entries in DEABAS

PREPARATION OF ACCOUNTS

Classification of all amounts received and spent head wise.

If made in DEABAS, system will generate

Closing of Chitta with daily and monthly abstracts

Monthly abstracts in all cash books. 001,002,003 and all bank accounts

Reconciliation with Treasury, Bank pass book most important.

BUDGET It is a statement of receipts and expenditure

for a financial year.Revised estimate of current year and BE of

the following year are generally preparedBudget contains probable receipts and

expenditure during following year.Accountant in consultation with all section

head should prepare draft budgetBudget to be placed before council 31st

December.Budget to be earmarked as per Government

instructions from time to time

ACCOUNTING MAL-PRACTICESMis appropriations Mis UtilisationExcess Utilization Irregular paymentsShort remittances Irregular purchasePending AdvancesProcedural lapsesDiversion of fundsNon Production of recordsNon Payment of dues to Government

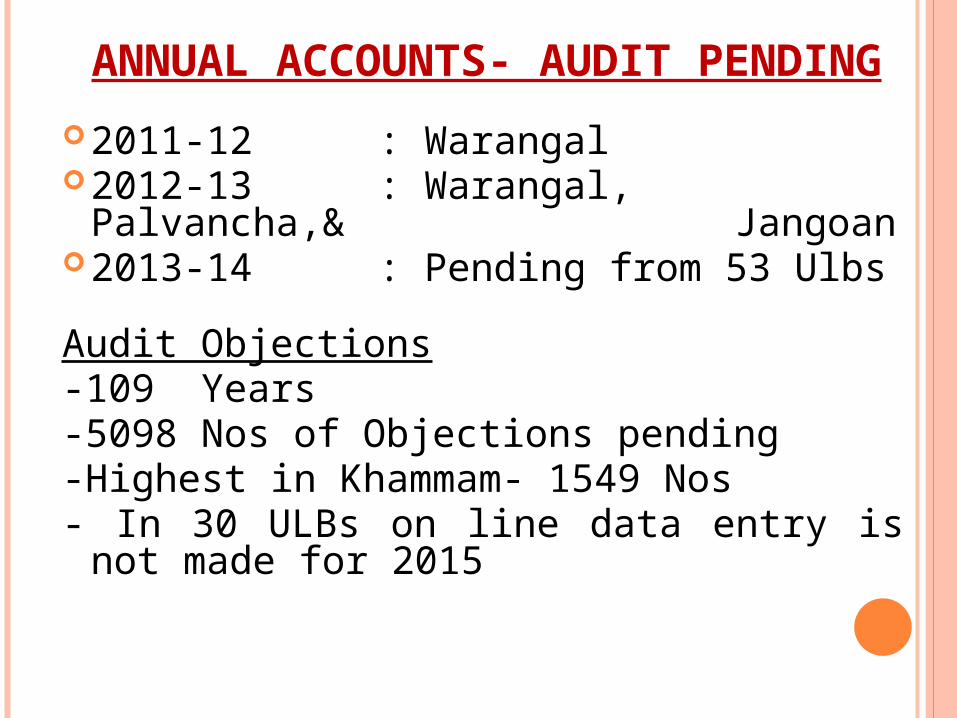

ANNUAL ACCOUNTS- AUDIT PENDING

2011-12 : Warangal 2012-13 : Warangal, Palvancha,&

Jangoan2013-14 : Pending from 53 Ulbs

Audit Objections-109 Years -5098 Nos of Objections pending-Highest in Khammam- 1549 Nos- In 30 ULBs on line data entry is not made

for 2015

REFORMS IN ACCOUNTING DEABAS introduced in 40 ULBs RCA firms being identified for 2014-15 for 27

newly constituted ULBs All older Ulbs to prepare Annual Accounts in

DEABAS for 2014-15 by themselves using CGG tool. MAARC cell to assist. Deputation of Accounting personnel.

Usage of Online CGG’s Accrual Based Accounting Software

MAARC cell available in C&DMA office for any time assistance.

Help desk also being placed in C&DMA office

EXPECTED OUT COMESTo establish standard accounting

practices in all ULBsConverting to DEABAS by all the ULBs All older ULBs to sustain themselves

with DEABASMinimize Accounting Mal practicesCurtail MisappropriationsAchieve 100% performance grants

under 14th Finance Commission grantsTo make Telangana a Model State