Embed Size (px)

Citation preview

151

© 2014 Pearson Canada Inc.

Accounting, Vol. 2, 9e Cdn. Ed. (Horngren)

Chapter 13 Corporations: Share Capital and the Balance Sheet

Objective 13-1

1) A corporation is a separate legal entity apart from its owners.

Answer: TRUE Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

2) Shareholders in a corporation are personally liable for the debts of the corporation.

Answer: FALSE Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

3) All shares issued by a corporation have voting rights.

Answer: FALSE Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

4) Double taxation refers to the fact that a corporation pays tax on its taxable earnings and the

shareholder also pays personal tax on all of the corporation's taxable income.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

5) It is easier to achieve continuous life using the corporate structure for an organization.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Comprehension

Objective: 13-1 Identify the characteristics of a corporation

6) Unlimited liability is one of the advantages of the corporate structure for an organization.

Answer: FALSE

Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

152

© 2014 Pearson Canada Inc.

7) Mutual agency is one of the disadvantages of the corporate structure for an organization.

Answer: FALSE

Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

8) The most that a shareholder can lose on an investment in a corporation's shares is the cost of the

investment.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

9) Corporations pay the same taxes as partnerships and proprietorships.

Answer: FALSE

Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

10) Retained earnings is debited to transfer net income to the retained earnings account during the closing

process.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

11) Retained earnings represents investments by the shareholders of the corporation.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

12) A debit balance in retained earnings is referred to as a deficit.

Answer: TRUE

Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

13) The policy-making body of a corporation is called the board of directors.

Answer: TRUE

Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

153

© 2014 Pearson Canada Inc.

14) Corporate bylaws are established by provincial governments to regulate company operations in the

interest of the public.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

15) The document(s) used by a government to grant permission to form a corporation is called (a):

A) proxy

B) articles of incorporation

C) share certificate

D) bylaw agreement

Answer: B

Diff: 1 Type: MC

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

16) All of the following represent advantages of corporations over other business entities except:

A) unlimited shareholders' liability

B) continuity of existence

C) separate legal entity

D) ease of transferring ownership

Answer: A Diff: 2 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

17) Which of the following statements describing a corporation is true?

A) Shareholders are the creditors of a corporation.

B) Shareholders own the business and manage its day-to-day operations.

C) A corporation is subject to greater governmental regulation than a proprietorship or a partnership.

D) When ownership of a corporation changes, the corporation terminates.

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

18) Which of the following forms of business organizations is a distinct legal entity?

A) partnership

B) corporation

C) proprietorship

D) only proprietorship and partnership

Answer: B Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

154

© 2014 Pearson Canada Inc.

19) Shareholders' liability for corporation debts is generally limited to:

A) the cost of their investment

B) the market value of the shares

C) the par value of the shares

D) total shareholders' equity

Answer: A

Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

20) Which of the following is a disadvantage of the corporate form of business organization?

A) mutual agency

B) government regulation

C) limited liability

D) difficulty in transferring ownership

Answer: B Diff: 2 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

21) Which of the following forms of business organizations terminates when the ownership structure

changes?

A) corporation

B) partnership

C) share capital

D) shareholders' equity

Answer: B Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

22) Share capital represents:

A) investments by the creditors of a corporation

B) capital that the corporation has earned through profitable operations

C) investments by the shareholders of a corporation

D) retained earnings

Answer: C Diff: 1 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

155

© 2014 Pearson Canada Inc.

23) Retained earnings:

A) is classified as an asset on the corporate balance sheet

B) is part of contributed capital

C) represents investments by the shareholders of the corporation

D) represents capital earned by profitable operations

Answer: D

Diff: 2 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

24) The owners of a corporation are referred to as:

A) creditors

B) shareholders

C) partners

D) debtors

Answer: B Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

25) All of the following transactions increase shareholders' equity except:

A) issuance of common shares

B) profitable operations

C) declaration of a cash dividend

D) issuance of convertible preferred shares

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

26) A profitable corporation would close out Income Summary by:

A) debiting Income Summary and crediting Share Capital

B) debiting Income Summary and crediting Retained Earnings

C) crediting Income Summary and debiting Retained Earnings

D) crediting Income Summary and debiting Share Capital

Answer: B Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

156

© 2014 Pearson Canada Inc.

27) A corporation operating at a loss would close out Income Summary by:

A) debiting Income Summary and crediting Retained Earnings

B) debiting Income Summary and crediting Share Capital

C) crediting Income Summary and debiting Retained Earnings

D) crediting Income Summary and debiting Share Capital

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

28) A debit balance in retained earnings is referred to as a(n):

A) normal balance

B) asset

C) deficit

D) liability

Answer: C Diff: 1 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

29) Cash dividends:

A) do not affect the retained earnings of a corporation

B) decrease both the assets and the total shareholders' equity of the corporation

C) increase retained earnings

D) increase the assets and decrease the total shareholders' equity of the corporation

Answer: B

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

30) All of the following are basic rights of a common shareholder except:

A) the right to receive a proportionate share of the corporate assets remaining after the corporation pays

its liabilities in liquidation

B) the right to receive a proportionate share of the corporate assets prior to the payment of liabilities in

liquidation

C) the right to receive a proportionate share of any dividend

D) the right to vote

Answer: B Diff: 2 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

157

© 2014 Pearson Canada Inc.

31) The heading, contributed capital, appears on which section of the balance sheet?

A) current assets

B) long-term liabilities

C) property, plant and equipment

D) shareholders' equity

Answer: D

Diff: 1 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

32) Which of the following statements describes the corporate characteristic termed limited liability?

A) The liabilities of the corporation cannot be extended to the personal assets of the shareholder.

B) Shares of stock can be readily bought and sold by investors on the open market.

C) Shareholders are not authorized to sign contracts or make business commitments on behalf of the

corporation.

D) Corporations pay income tax on corporate earnings, and shareholders pay personal income tax on

corporate dividends and gains from sale of stock.

Answer: A

Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

33) Which of the following statements describes the corporate characteristic termed double taxation?

A) The liabilities of the corporation cannot be extended to the personal assets of the shareholder.

B) Shares of stock can be readily bought and sold by investors on the open market.

C) Shareholders are not authorized to sign contracts or make business commitments on behalf of the

corporation.

D) Corporations pay income tax on corporate earnings, and shareholders pay personal income tax on

corporate dividends and gains from sale of stock.

Answer: D Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

34) Which of the following statements describes the corporate characteristic termed no mutual agency?

A) The liabilities of the corporation cannot be extended to the personal assets of the shareholder.

B) Shares of stock can be readily bought and sold by investors on the open market.

C) Shareholders are not authorized to sign contracts or make business commitments on behalf of the

corporation.

D) Corporations pay income tax on corporate earnings, and shareholders pay personal income tax on

corporate dividends and gains from sale of stock.

Answer: C Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

158

© 2014 Pearson Canada Inc.

Table 13-9

Following is the JenWu Corporation December 31, 2015 shareholders' equity section of the balance sheet,

prior to the closing entries:

Contributed capital:

Preferred shares, cumulative, $5.00, 6,000 shares outstanding,

liquidation value $42 per share $220,000

Common shares, 30,000 shares outstanding 500,000

Retained earnings/(deficit) (240,000)

Note: No dividends were declared in 2013 or 2014. The net income for 2015 was $260,000.

35) Referring to Table 13-9, what is the journal entry to close the Income Summary account?

A)

Dr. Retained Earnings 260,000

Cr. Income Summary 260,000

B)

Dr. Retained Earnings 350,000

Cr. Preferred Dividend Payable 90,000

Cr. Income Summary 260,000

C)

Dr. Income Earnings 260,000

Cr. Retained Earnings 260,000

D)

Dr. Income Summary 260,000

Cr. Preferred Dividend Expense 90,000

Cr. Retained Earnings 170,000

Answer: C Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-1 Identify the characteristics of a corporation

159

© 2014 Pearson Canada Inc.

Match the following.

A) common shares

B) outstanding shares

C) shareholders' equity

D) board of directors

E) President

F) limited liability

G) deficit

H) organization costs

I) retained earnings

J) underwriter

K) authorization of shares

L) articles of incorporation

M) corporate law firm

36) Documents used by a government to grant its permission to form a corporation Diff: 1 Type: MA

Learning Outcome:

Skill: Knowledge

A-03 Analyze and record transactions and their effect on the financial statements

Objective: 13-1 Identify the characteristics of a corporation

37) Chief operating officer in charge of managing the day-to-day operations of a corporation. Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

38) Owners' equity of a corporation Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

39) Shares in the hands of shareholders

Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

40) Group elected by the shareholders to set policy for a corporation and to appoint its officers.

Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

160

© 2014 Pearson Canada Inc.

41) Provision in the articles of incorporation that permits a corporation to sell a certain number of shares

of stock.

Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

42) Debit balance in the retained earnings account Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

43) The costs of organizing a corporation, including legal fees, taxes, and charges by promoters for selling

the shares.

Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

44) No personal obligation of a shareholder for corporation debts. The most that a shareholder can lose on

an investment in a corporation's shares is the cost of the investment.

Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

45) A corporation's capital that is earned through profitable operation of the business

Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

46) The most basic form of share capital Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

47) The firm engaged to sell shares on behalf of the issuing corporation Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

Answers: 36) L 37) E 38) C 39) B 40) D 41) K 42) G 43) H 44) F 45) I 46) A 47) J

161

© 2014 Pearson Canada Inc.

48) Discuss the characteristics of a corporation. Indicate, wherever appropriate, if the characteristic is an

advantage or a disadvantage of the corporate form of business.

Answer:

Students should mention the following characteristics:

Separate legal entity

Ability to raise more capital-advantage

Continuous life-advantage

Ease of ownership transfer-advantage

No mutual agency - advantage

Limited liability of shareholders - advantage

Separation of management and owners - disadvantage

Possible double taxation - disadvantage

Government regulation - disadvantage

Additional costs unique to corporations - disadvantage Diff: 2 Type: ES

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Comprehension

Objective: 13-1 Identify the characteristics of a corporation

49) List some of the shareholder rights normally attached to common shares.

Answer: -The right to sell the shares

-The right to vote at shareholders' meetings

-The right to receive a proportionate share of any dividends declared by the directors

-The right to receive a proportionate share of any assets on the winding-up of the company, after

the creditors and any higher ranking classes of shares have been paid.

-The right to maintain one's proportionate ownership in the corporation.

Diff: 2 Type: ES

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-1 Identify the characteristics of a corporation

162

© 2014 Pearson Canada Inc.

Objective 13-2

1) No-par-value shares are shares of stock that do not have a value assigned to them by the articles of

incorporation.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

2) Preferred shares normally have no voting rights.

Answer: TRUE Diff: 1 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

3) When a corporation issues shares in exchange for noncash assets, the noncash assets are debited for

their book value.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

4) The shareholders' equity section of a balance sheet lists common shares first, followed by preferred

shares second, and retained earnings last.

Answer: FALSE

Diff: 2 Type: TF

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

5) Organization costs are intangible assets classified with property, plant and equipment.

Answer: FALSE

Diff: 1 Type: TF

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

163

© 2014 Pearson Canada Inc.

6) Increases in contributed capital and in retained earnings come from producing revenue.

Answer: FALSE

Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Comprehension

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

7) Convertible preferred shares must be converted into common shares when the corporation declares the

conversion.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

8) If a company has both preferred and common shares outstanding, the preferred shareholders have the

first claim to shareholders' equity.

Answer: TRUE

Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

9) Convertible preferred shares may be exchanged for another specified class of shares in the corporation

if the preferred shareholder chooses.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

10) Corporations may use an underwriter to sell their shares rather than selling them directly to investors.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

164

© 2014 Pearson Canada Inc.

11) Which of the following is a priority granted to preferred shareholders?

A) voting for the corporate board of directors

B) receiving assets before creditors if the corporation liquidates

C) receiving dividends before common shareholders

D) receiving a guaranteed fixed dollar amount of dividends each year

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

12) A corporation may issue:

A) common shares and preferred shares

B) preferred shares but not common shares

C) common shares but not preferred shares

D) either common shares or preferred shares but not both

Answer: A Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

13) Why might corporations prefer issuing preferred shares to debt?

A) dividends are payable at the discretion of the corporation

B) debt payments are payable at the discretion of the corporation

C) dividends are tax deductible to the corporation

D) interest expense is tax deductible to the corporation

Answer: A

Diff: 2 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

14) An owner investment of cash in a corporation increases:

A) assets and increases liabilities

B) one asset and decreases another asset

C) assets and decreases shareholders' equity

D) assets and increases shareholders' equity

Answer: D Diff: 1 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

165

© 2014 Pearson Canada Inc.

15) The entry to record the issuance of 5,000 common shares for $12.50 per share includes a:

A) debit to Retained Earnings for $62,500

B) debit to Cash for $62,500

C) credit to Retained Earnings for $62,500

D) debit to Common Shares for $62,500

Answer: B

Diff: 1 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

16) The entry to record the issuance of 6,000 common shares for $12.50 per share includes a:

A) credit to Cash for $75,000

B) debit to Common Shares for $75,000

C) credit to Common Shares for $75,000

D) credit to Retained Earnings for $75,000

Answer: C Diff: 1 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

17) The entry to record the issuance of 55,000 common shares at $13.50 per share includes a:

A) credit to Retained Earnings $742,500

B) credit to Cash for $742,500

C) debit to Retained Earnings for $742,500

D) credit to Common Shares for $742,500

Answer: D Diff: 1 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

18) When 35,000 common shares are issued at $16.50 per share, total contributed capital:

A) increases by $577,500

B) increases by $350,000

C) increases by $227,500

D) decreases by $577,500

Answer: A

Diff: 1 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

166

© 2014 Pearson Canada Inc.

19) Land is acquired by issuing 500 common shares. The land has a current market value of $12,000.

There is no market value for the common shares available. The journal entry requires a:

A) debit to Cash for $12,000

B) debit to Common Shares for $12,000

C) credit to Retained Earnings for $12,000

D) credit to Common Shares for $12,000

Answer: D Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

20) A corporation issues common shares in exchange for equipment with a market value of $15,000. This

transaction would:

A) increase retained earnings by $15,000

B) increase liabilities by $15,000

C) increase common shares by $15,000

D) decrease total shareholders' equity by $15,000

Answer: C Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

21) Accounting for the incorporation of an unincorporated going business involves:

A) closing the owner equity accounts of the prior entity and setting up the shareholder equity accounts of

the corporation

B) leaving the owner equity accounts as is and setting up the shareholders' equity accounts for the

corporation

C) closing the owner equity accounts of the prior entity to the retained earnings account of the

corporation

D) closing the withdrawals accounts to the dividends payable accounts

Answer: A Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

167

© 2014 Pearson Canada Inc.

22) Organization costs appear on which section of the balance sheet?

A) current assets

B) intangible assets

C) shareholders' equity

D) long-term liabilities

Answer: B

Diff: 2 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

Table 13-1

The following selected list of accounts with their normal balances was taken from the general ledger of

Grant Corporation as of December 31, 2014:

Cash $173,500

Common shares, 100,000 shares authorized, 50,000 shares issued 190,000

Retained earning 131,500

Cash dividends payable 25,000

Preferred shares, 200,000 shares authorized 100,000 shares

issued 500,000

23) Refer to Table 13-1. The average issue price of a common share was:

A) $3.80

B) $1.90

C) $5.00

D) $0.95

Answer: A Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

24) Refer to Table 13-1. The average issue price of a preferred share was:

A) $2.50

B) $6.90

C) $5.00

D) $3.80

Answer: C Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

168

© 2014 Pearson Canada Inc.

25) Refer to Table 13-1. Which account should be listed first in the shareholders' equity section?

A) Retained earnings

B) Common shares

C) Contributed surplus

D) Preferred shares

Answer: D

Diff: 2 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

26) Refer to Table 13-1. The total shareholders' equity as of December 31, 2014 was:

A) $190,000

B) $846,500

C) $881,500

D) $821,500

Answer: D Diff: 3 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Analysis

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

Table 13-6

The following selected list of accounts with their normal balances was taken from the general ledger of

Gore Ltd. as of December 31, 2014:

Cash $199,000

Common shares, 10,000 shares authorized, 5,000 shares issued 265,000

Retained earnings 131,5000

Cash dividends payable 20,000

Preferred shares, 500,000 shares authorized 100,000 shares

issued 800,000

27) Refer to Table 13-6. Which account should be listed first in the shareholders' equity section?

A) Retained earnings

B) Common shares

C) Contributed surplus

D) Preferred shares

Answer: D Diff: 2 Type: MC

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

169

© 2014 Pearson Canada Inc.

28) Notebook Company had the following transactions in 2013, its first year of operations.

• Issued 2,000 common shares. Shares were issued at $50.00 per share.

• Issued 100 preferred shares. Shares were issued at $100 per share.

• Earned net income of $95,000.

• Paid dividends of $5,000.

At the end of 2013, how much was the total Shareholders' equity?

A) $200,000

B) $110,000

C) $90,000

D) $100,000

Answer: A

Explanation: A) Calculations: (2,000 × $50) + (100 × $100) + ($95,000 - $5,000) = $200,000 Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

29) Overton Company had the following transactions in 2013, its first year of operations.

• Issued 5,000 common shares at $30.00 per share.

• Earned net income of $200,000.

• Paid dividends of $5.00 per share.

At the end of 2013, how much is the total contributed capital?

A) $150,000

B) $325,000

C) $175,000

D) $200,000

Answer: A

Explanation: A) Calculations: (5,000 × $30) = $150,000

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

170

© 2014 Pearson Canada Inc.

30) Beta Company was founded in 2014. Its yearly earnings and dividend payments are shown here:

2012: Net income $4,000, paid zero dividends

2013: Net income $20,000, paid $10,000 dividends

2014: Net income of $8,000, paid $5,000 dividends

2015: Net loss of $22,000, paid zero dividends

At the end of 2015, which of the following statements would be accurate?

A) Beta has a cumulative operating loss.

B) Beta has a retained earnings deficit.

C) Beta has retained earnings surplus.

D) Beta has negative contributed capital.

Answer: B

Explanation: B) Calculation: $4,000 + $20,000 - $10,000 + $8,000 -$5,000 - $22,000 = $(5,000)

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

171

© 2014 Pearson Canada Inc.

Match the following.

A) preferred shares

B) convertible

C) par value

D) no-par-value shares

E) amortization

F) cumulative

G) liquidation value

31) Shares that do not have a value assigned to them by the articles of incorporation

Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

32) Shares of stock that gives its owners certain advantages over the common shareholders. Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

33) The amount a preferred shareholder would receive for their shares in the event the corporation is

liquidated Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

34) Preferred shares that can be exchanged by the preferred shareholders

Diff: 1 Type: MA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

35) The method of recognizing organization costs under ASPE Diff: 1 Type: MA

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

172

© 2014 Pearson Canada Inc.

36) An arbitrary value assigned to each share in the articles of incorporation Diff: 1 Type: MA

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

Answers: 31) D 32) A 33) G 34) B 35) E 36) C

37) Prepare a journal entry for each of the following transactions.

a) Masters Corporation sells 10,000 common shares for $13.25 per share.

b) Masters Corporation sells 5,000 shares of $5, cumulative preferred shares for $55 per share.

c) Received a building with a market value of $160,000, and issued 6,400 common shares in exchange.

d) Masters Corporation reports a net income for the current year of $56,000. Prepare the entry to close

the income summary account.

Date Accounts Debit Credit

Answer:

Date Accounts Debit Credit

a) Cash 132,500

Common Shares 132,500

b) Cash 275,000

Preferred Shares 275,000

d) Building 160,000

Common Shares 160,000

e) Income Summary 56,000

Retained Earnings 56,000

Diff: 2 Type: SA

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

173

© 2014 Pearson Canada Inc.

38) Prepare a journal entry for each of the following transactions.

a) Struthers Corporation sells 100,000 common shares for $4.50 per share.

b) Struthers Corporation sells 6,000 shares of $3, cumulative preferred shares for $70 per share.

c) Received equipment with a market value of $60,000, and issued 12,400 common shares in exchange.

d) Struthers Corporation reports a net income for the current year of $241,000. Prepare the entry to close

the income summary account.

Date Accounts Debit Credit

Answer:

Date Accounts Debit Credit

a) Cash 450,000

Common Shares 450,000

b) Cash 420,000

Preferred Shares 420,000

d) Equipment 60,000

Common Shares 60,000

e) Income Summary 241,000

Retained Earnings 241,000

Diff: 2 Type: SA

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

174

© 2014 Pearson Canada Inc.

39) Prepare journal entries for the following transactions reported by Evans Corporation for the month of

May:

May 1 Issued 35,000 common shares at $15 per share.

21 Issued 1,400 shares of $5, cumulative preferred shares for a total of

$144,200.

28 Exchanged 5,000 common shares for a patent valued at $82,000.

31 Jet Corporation reported a net loss for May amounting to $10,500.

Prepare the entry to close the income summary account.

Date Accounts Debit Credit

Answer:

Date Accounts Debit Credit

May 1 Cash 525,000

Common Shares 525,000

21 Cash 144,200

Preferred Shares 144,200

28 Patent 82,000

Common Shares 82,000

31 Retained Earnings 10,500

Income Summary 10,500

Diff: 2 Type: SA

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

175

© 2014 Pearson Canada Inc.

40) From the following alphabetical list of selected accounts taken from the general ledger of Dorlin

Corporation as of December 31, 2014, select the accounts that are part of shareholders' equity. Then

prepare the shareholders' equity section of the balance sheet on December 31, 2014.

Accounts receivable 50,000

Cash dividends payable 20,000

Common shares, 20,000 shares outstanding 550,000

Inventory 75,000

Note payable 25,000

Notes receivable 20,000

Preferred shares, $10 cumulative,

1,000 shares outstanding 250,000

Retained earnings 250,000

Unearned revenue 15,000

Answer: Dorlin Corporation

Partial Balance Sheet

December 31, 2014

Shareholders' equity

Contributed capital:

Preferred shares, $10, cumulative,

1,000 shares outstanding $ 250,000

Common shares, 20,000 shares outstanding 550,000

Total contributed capital 800,000

Retained earnings 250,000

Total shareholders' equity $1,050,000

Diff: 3 Type: SA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

176

© 2014 Pearson Canada Inc.

41) Nevada Corporation was created on January 2, 2014. The articles of incorporation from the

Government of Canada authorize Nevada Corporation to issue an unlimited number of common shares

and 500,000 shares of $0.50 preferred shares. The company had the following transactions:

2014

Jan. 2 Gave 5,000 common shares to the corporation's legal firm for incorporating the business.

The total legal fee was $5,000.

3 Issued 200,000 common shares for cash at $1 per share.

4 Issued 10,000 preferred shares for cash at $10 per share.

4 Exchanged $50,000 cash and 200,000 common shares for a building with a market value of

$260,000.

Dec. 31 Close Income Summary to Retained Earnings assuming that Nevada had $63,000 of net

income for the year

a) Journalize the above transactions. Explanations are not needed.

b) Prepare the shareholders' equity section of the balance sheet as of the close of business on December

31, 2014.

Journal

Date Description Debit Credit

177

© 2014 Pearson Canada Inc.

Answer: Journal

Date

2010 Description Debit Credit

Jan. 2 Organization Costs 5,000

Common Shares 5,000

Jan. 3 Cash 200,000

Common Shares 200,000

Jan. 4 Cash 100,000

Preferred Shares 100,000

Jan. 4 Building 260,000

Cash 50,000

Common Shares 210,000

Dec. 31 Income Summary 63,000

Retained Earnings 63,000

Nevada Corporation

Partial Balance Sheet

December 31, 2014

Shareholders' Equity

Contributed capital

Preferred shares,$0.50, 500,000 shares authorized,

10,000 shares issued $ 100,000

Common shares, unlimited number of shares

authorized, 405,000 shares issued 415,000

Total contributed capital 515,000

Retained earnings 63,000

Total shareholders' equity $578,000

Diff: 3 Type: SA

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

178

© 2014 Pearson Canada Inc.

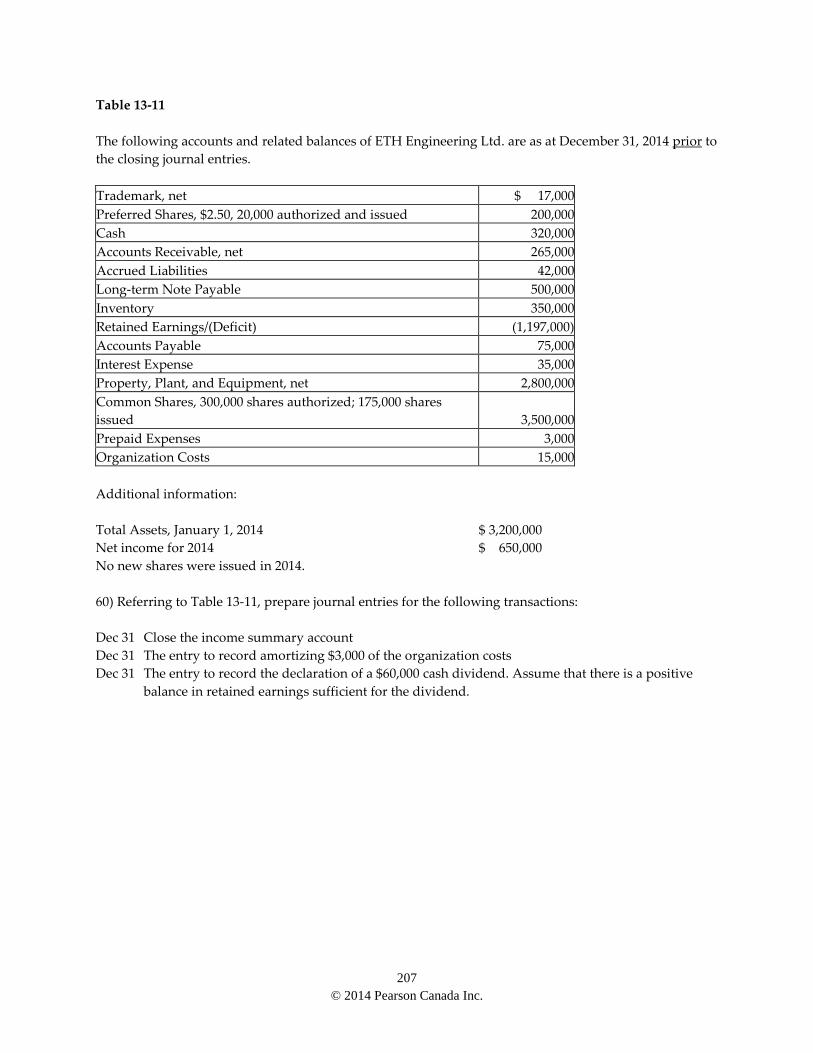

Table 13-11

The following accounts and related balances of ETH Engineering Ltd. are as at December 31, 2014 prior to

the closing journal entries.

Trademark, net $ 17,000

Preferred Shares, $2.50, 20,000 authorized and issued 200,000

Cash 320,000

Accounts Receivable, net 265,000

Accrued Liabilities 42,000

Long-term Note Payable 500,000

Inventory 350,000

Retained Earnings/(Deficit) (1,197,000)

Accounts Payable 75,000

Interest Expense 35,000

Property, Plant, and Equipment, net 2,800,000

Common Shares, 300,000 shares authorized; 175,000 shares

issued 3,500,000

Prepaid Expenses 3,000

Organization Costs 15,000

Additional information:

Total Assets, January 1, 2014 $ 3,200,000

Net income for 2014 $ 650,000

No new shares were issued in 2014.

179

© 2014 Pearson Canada Inc.

42) Referring to Table 13-11, prepare a classified balance sheet as at December 31, 2014.

180

© 2014 Pearson Canada Inc.

Answer: ETH Engineering Ltd.

Balance Sheet

December 31, 2014

Assets

Current Assets:

Cash $ 320,000

Accounts Receivable, net 265,000

Inventory 350,000

Prepaid Expenses 3,000

Total Current Assets $ 938,000

Property, Plant, and Equipment, net 2,800,000

Intangible Assets:

Trademark, net $ 17,000

Organization Costs 15,000

Total Intangible Assets 32,000

Total Assets $ 3,770,000

Liabilities

Current Liabilities:

Accounts Payable $ 75,000

Accrued Liabilities 42,000

Total Current Liabilities $ 117,000

Long-term Note Payable 500,000

Total Liabilities $ 617,000

Shareholders' Equity

Preferred Shares, $2.50, cumulative, 20,000 authorized and

issued $ 200,000

Common Shares, 300,000 shares authorized; 175,000 shares

issued 3,500,000

Retained Earnings/(Deficit) (547,000)

Total Shareholders' Equity 3,153,000

Total Liabilities and Shareholders' Equity $ 3,770,000

Diff: 3 Type: SA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

181

© 2014 Pearson Canada Inc.

Table 13-12

The following accounts and related balances of FYI Advertising Ltd. are as at December 31, 2014 prior to

the closing journal entries.

Accrued Liabilities $ 50,400

Preferred Shares, $2.50, cumulative, 24,000 authorized and

issued 240,000

Prepaid Expenses 3,600

Accounts Payable 90,000

Trademark, net 20,400

Long-term Note Payable 600,000

Property, Plant, and Equipment, net 3,360,000

Retained Earnings 623,600

Accounts Receivable, net 318,000

Interest Expense 29,000

Inventory 420,000

Common Shares, 300,000 shares authorized; 200,000 shares

issued 2,500,000

Cash 384,000

Organization Costs 18,000

Additional information:

Total Assets, January 1, 2014 $ 4,100,000

Net income for 2014 $ 420,000

No new shares were issued in 2014.

182

© 2014 Pearson Canada Inc.

43) Referring to Table 13-12, prepare a classified balance sheet as at December 31, 2014.

183

© 2014 Pearson Canada Inc.

Answer: FYI Advertising Ltd.

Balance Sheet

December 31, 2014

Assets

Current Assets:

Cash $ 384,000

Accounts Receivable, net 318,000

Inventory 420,000

Prepaid Expenses 3,600

Total Current Assets $ 1,125,600

Property, Plant, and Equipment, net 3,360,000

Intangible Assets:

Trademark, net $ 20,400

Organization Costs 18,000

Total Intangible Assets 38,400

Total Assets $ 4,524,000

Liabilities

Current Liabilities:

Accounts Payable $ 90,000

Accrued Liabilities 50,400

Total Current Liabilities $ 140,400

Long-term Note Payable 600,000

Total Liabilities $ 740,400

Shareholders' Equity

Preferred Shares, $2.50, cumulative, 24,000 authorized and

issued $ 240,000

Common Shares, 300,000 shares authorized; 200,000 shares

issued 2,500,000

Retained Earnings 1,043,600

Total Shareholders' Equity 3,783,600

Total Liabilities and Shareholders' Equity $ 4,524,000

Diff: 3 Type: SA

Learning Outcome: A-02 Describe the components of and prepare the four basic financial statements

Skill: Application

Objective: 13-2 Record the issuance of shares and prepare the shareholders' equity section of a corporation's balance

sheet

184

© 2014 Pearson Canada Inc.

Objective 13-3

1) Dividends distributed increase the assets and decrease the retained earnings of the business.

Answer: FALSE

Diff: 1 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

2) Cash dividends decrease both the assets and the retained earnings of a corporation.

Answer: TRUE

Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

3) The entry on the payment date for a cash dividend involves a debit to retained earnings and a credit to

cash.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

4) Dividends become a liability of the corporation on the declaration date.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

5) Dividends in arrears on cumulative preferred shares are not a liability to the corporation.

Answer: TRUE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

6) Dividends payable are normally a long-term liability.

Answer: FALSE

Diff: 1 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

185

© 2014 Pearson Canada Inc.

7) In order to receive a cash dividend, an investor must own the share by the payment date.

Answer: FALSE

Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

8) The declaration date and the payment date of a cash dividend are the same thing.

Answer: FALSE

Diff: 1 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

9) Dividends cannot accumulate for common shares.

Answer: TRUE

Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

10) If the preferred shares are not designated as cumulative, the corporation is obligated to pay any

dividends in arrears.

Answer: FALSE Diff: 2 Type: TF

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

11) Dividends become a liability of the corporation:

A) on the payment date

B) on the date of record

C) on the declaration date

D) on the day immediately following the date of declaration

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

186

© 2014 Pearson Canada Inc.

12) The dividends payable liability of the corporation is eliminated:

A) on the payment date

B) on the date of record

C) on the declaration date

D) on the day immediately following the date of declaration

Answer: A

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

13) The entry to record the declaration of a $0.50 per share dividend on 12,500 outstanding common

shares requires a:

A) credit to Cash for $6,250

B) debit to Dividends Payable for $6,250

C) debit to Retained Earnings for $6,250

D) credit to Retained Earnings for $6,250

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-3 Account for cash dividends

14) The entry to pay a previously declared dividend of $0.50 per share on 12,500 outstanding common

shares requires a:

A) debit to Cash for $6,250

B) credit to Dividends Payable for $6,250

C) debit to Retained Earnings for $6,250

D) debit to Dividends Payable for $6,250

Answer: D

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-3 Account for cash dividends

15) The declaration of a dividend:

A) increases total shareholders' equity

B) reduces total assets

C) increases total assets

D) increases total liabilities

Answer: D Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Comprehension

Objective: 13-3 Account for cash dividends

187

© 2014 Pearson Canada Inc.

16) The payment of a dividend:

A) reduces total shareholders' equity

B) increases total shareholders' equity

C) reduces total liabilities

D) has no effect on total assets

Answer: C

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Comprehension

Objective: 13-3 Account for cash dividends

17) A dividend is declared by the:

A) president of the corporation

B) board of directors

C) chief financial officer

D) corporate controller

Answer: B Diff: 1 Type: MC

Learning Outcome: A-03 Analyze and record transactions and their effect on the financial statements

Skill: Knowledge

Objective: 13-3 Account for cash dividends

18) Dividends on cumulative preferred shares of $2,500 are in arrears for 2013. During 2014, the total

dividends declared amount to $10,000. There are 6,000 shares of $1 cumulative preferred shares

outstanding and 10,000 common shares outstanding. The total amount of dividends payable to each class

of shares in 2014 amounts to:

A) $8,500 to preferred, $1,500 to common

B) $6,000 to preferred, $4,000 to common

C) $5,000 to preferred, $5,000 to common

D) $10,000 to preferred, $0 to common

Answer: A Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

188

© 2014 Pearson Canada Inc.

19) Dividends on cumulative preferred shares of $2,500 are in arrears for 2013 and 2014. During 2015, the

total dividends declared amount to $10,000. There are 3,000 shares of $1 cumulative preferred shares

outstanding and 10,000 common shares outstanding. The total amount of dividends payable to each class

of shares in 2015 amounts to:

A) $5,500 to preferred, $4,500 to common

B) $3,000 to preferred, $7,000 to common

C) $8,000 to preferred, $2,000 to common

D) $10,000 to preferred, $0 to common

Answer: C

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

20) Dividends on cumulative preferred shares of $2,500 are in arrears for 2012, 2013, and 2014. During

2015, the total dividends declared amount to $10,000. There are 3,000 shares of $1 cumulative preferred

shares outstanding and 10,000 common shares outstanding. The total amount of dividends payable to

each class of shares in 2015 amounts to:

A) $5,500 to preferred, $4,500 to common

B) $3,000 to preferred, $7,000 to common

C) $8,000 to preferred, $2,000 to common

D) $10,000 to preferred, $0 to common

Answer: D

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

21) Dividends were not declared by Royal Inc. in 2013 or 2014. During 2015, total dividends declared

amount to $20,000. There are 6,000 shares of $1 cumulative preferred shares outstanding and 10,000

common shares outstanding. The total amount of dividends payable to each class of shares in 2015

amounts to:

A) $18,000 to preferred, $2,000 to common

B) $6,000 to preferred, $14,000 to common

C) $12,000 to preferred, $8,000 to common

D) $10,000 to preferred, $10,000 to common

Answer: A

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

189

© 2014 Pearson Canada Inc.

22) Dividends were not declared by Royal Inc. in 2012. During 2013, total dividends declared amount to

$20,000. There are 6,000 shares of $1 cumulative preferred shares outstanding and 10,000 common shares

outstanding. The total amount of dividends payable to each class of shares in 2013 amounts to:

A) $18,000 to preferred, $2,000 to common

B) $6,000 to preferred, $14,000 to common

C) $12,000 to preferred, $8,000 to common

D) $10,000 to preferred, $10,000 to common

Answer: C Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

23) During 2014, total dividends declared by Par Corporation amounted to $29,000. There were 5,000

shares of $2 noncumulative preferred shares outstanding and 10,000 common shares outstanding. No

dividends were declared in 2012 or 2013. The total amount of dividends payable to each class of shares in

2014 amounted to:

A) $19,000 to preferred, $10,000 to common

B) $0 to preferred, $29,000 to common

C) $10,000 to preferred, $19,000 to common

D) $29,000 to preferred, $0 to common

Answer: C Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

24) During 2014, total dividends declared by Par Corporation amounted to $29,000. There were 5,000

shares of $2 cumulative preferred shares outstanding and 10,000 common shares outstanding. No

dividends were declared in 2012 or 2013. The total amount of dividends payable to each class of shares in

2014 amounted to:

A) $19,000 to preferred, $10,000 to common

B) $0 to preferred, $29,000 to common

C) $10,000 to preferred, $19,000 to common

D) $29,000 to preferred, $0 to common

Answer: D Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

190

© 2014 Pearson Canada Inc.

25) During 2014, total dividends declared by Jackson Corp. amounted to $29,000. There were 5,000 shares

of $2 cumulative preferred shares outstanding and 10,000 common shares outstanding. No dividends

were declared in 2013. The total amount of dividends payable to each class of shares in 2014 amounted to:

A) $10,000 to preferred, $19,000 to common

B) $20,000 to preferred, $9,000 to common

C) $29,000 to preferred, $0 to common

D) $9,000 to preferred, $20,000 to common

Answer: B Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

26) During 2013, total dividends declared by Jackson Corp. amounted to $29,000. There were 5,000 shares

of $2 noncumulative preferred shares outstanding and 10,000 common shares outstanding. No dividends

were declared in 2012. The total amount of dividends payable to each class of shares in 2013 amounted to:

A) $10,000 to preferred, $19,000 to common

B) $20,000 to preferred, $9,000 to common

C) $29,000 to preferred, $0 to common

D) $9,000 to preferred, $20,000 to common

Answer: A

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

27) Passed dividends on cumulative preferred shares:

A) remain a liability of the corporation until they are paid

B) are forever lost by the preferred shareholders

C) are referred to as dividends in arrears

D) are paid after common shareholders receive their dividends

Answer: C Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

28) Dividends in arrears:

A) are a liability on the balance sheet

B) are passed dividends on cumulative preferred shares

C) are never reported in the notes to the financial statements

D) are forever lost by the preferred shareholders

Answer: B Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Knowledge

Objective: 13-3 Account for cash dividends

191

© 2014 Pearson Canada Inc.

29) Magic Corp. has 20,000 shares of noncumulative, $5 preferred shares outstanding as well as 100,000

common shares. The board of directors have declared and distributed the required dividends for the past

three years, not counting the current year. The board wants to give the common shareholders a $1.25

dividend per share for the current year. The total dividends to be declared must be:

A) $225,000

B) $125,000

C) $525,000

D) $250,000

Answer: A

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

30) Newco Corporation has 20,000 shares of cumulative, $5 preferred shares outstanding as well as

100,000 common shares. As of the beginning of this fiscal year, there were three years of dividends in

arrears on the preferred shares. The board of directors wants to give the common shareholders a $1.25

dividend per share. The total dividends to be declared must be:

A) $225,000

B) $400,000

C) $525,000

D) $425,000

Answer: C

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

31) Resco Corporation has had 10,000 shares of $3, cumulative preferred shares outstanding as well as

35,000 common shares since it was incorporated. During the first, second, and third years of operations,

$15,000, $18,000 and $50,000 in dividends, respectively, were paid. The dividends paid to the common

shareholders in year three amounted to:

A) $30,000

B) $0

C) $27,000

D) $18,000

Answer: B

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

192

© 2014 Pearson Canada Inc.

32) Resco Corporation has had 10,000 shares of $3, cumulative preferred shares outstanding as well as

35,000 common shares since it was incorporated. During the first, second, and third years of operations,

$10,000, $20,000 and $80,000 in dividends, respectively, were paid. The dividends paid to the common

shareholders in year three amounted to:

A) $30,000

B) $0

C) $20,000

D) $18,000

Answer: C

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

Table 13-2

Falcon Corporation has 12,000 shares of $5, noncumulative preferred shares outstanding and 16,000

common shares outstanding. At the end of the current year, Falcon Corporation declares a dividend of

$120,000.

33) Refer to Table 13-2. How is the dividend allocated between preferred and common shareholders?

A) $12,000 to preferred, $108,000 to common

B) $80,000 to preferred, $40,000 to common

C) $60,000 to preferred, $60,000 to common

D) $40,000 to preferred, $80,000 to common

Answer: C Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

34) Refer to Table 13-2. What is the dividend per share to preferred and common shareholders?

A) $5.00 to preferred, $3.75 to common

B) $3.75 to preferred, $5.00 to common

C) $6.67 to preferred, $1.50 to common

D) $1.00 to preferred, $6.75 to common

Answer: A

Diff: 2 Type: MC

Learning Outcome: A-16 Define and use the different types of financial statement analysis tools

Skill: Analysis

Objective: 13-3 Account for cash dividends

193

© 2014 Pearson Canada Inc.

Table 13-3

Spencer Corporation has 15,000 shares of $5, cumulative preferred shares outstanding and 25,000

common shares. At the end of the current year, Spencer Corporation declares a dividend of $120,000.

Dividends of $37,500 are in arrears as of January 1 of the current year.

35) Refer to Table 13-3. How is the dividend allocated between preferred and common shareholders?

A) $112,500 to preferred, $7,500 to common

B) $75,000 to preferred, $45,000 to common

C) $120,000 to preferred, $0 to common

D) $0 to preferred, $120,000 to common

Answer: A Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Analysis

Objective: 13-3 Account for cash dividends

36) Refer to Table 13-3. What is the dividend per share to preferred and common shareholders?

A) $5.00 to preferred, $1.80 to common

B) $7.50 to preferred, $0.30 to common

C) $5.00 to preferred, $0.30 to common

D) $1.80 to preferred, $5.00 to common

Answer: B

Diff: 3 Type: MC

Learning Outcome: A-16 Define and use the different types of financial statement analysis tools

Skill: Analysis

Objective: 13-3 Account for cash dividends

37) From its inception through the year of 2014, Quicksales Company was profitable and made strong

dividend payments each year. In the year 2015, Quicksales had major losses and paid no dividends. In

2016, the company started making large profits again, and was able to pay dividends to all

shareholders—both common and preferred. There are 1,500 cumulative, $7 dividend, preferred shares

outstanding. What is the total amount of dividends which should be paid to the preferred shareholders in

December 2016?

A) $210

B) $22,000

C) $10,500

D) $21,000

Answer: D

Explanation: D)

Calculations: 1,500 × $7 = $10,500

$10,500 × 2 = $21,000

Diff: 2 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits

Skill: Application

Objective: 13-3 Account for cash dividends

194

© 2014 Pearson Canada Inc.

38) Orleans Company was incorporated on January 1, 2012. Orleans issued 4,000 common shares and 500

preferred shares on that date. The preferred shares are cumulative, with a $8 dividend. Orleans has not

paid any dividends yet. In 2015, Orleans had its first profitable year, and on November 1, 2015, Orleans

declared a total dividend of $28,000. What is the total amount that will be paid out to common

shareholders?

A) $4,000

B) $16,000

C) $12,000

D) $28,000

Answer: C

Explanation: C)

Calculations: [(500 × $8)] × 4 = $16,000

$28,000 - $16,000 = $12,000

Diff: 3 Type: MC

Learning Outcome: A-14 Apply basic accounting methods to record and evaluate share transactions, cash and stock

dividends, and stock splits