Embed Size (px)

Citation preview

Accounting Level 3

Model Answers Series 4 2007 (Code 3001)

© Education Development International plc 2007 Company Registration No: 3914767 All rights reserved. This publication in its entirety is the copyright of Education Development International plc.

Reproduction either in whole or in part is forbidden without written permission from Education Development International plc.

International House Siskin Parkway East Middlemarch Business Park Coventry CV3 4PE Telephone: +44 (0) 8707 202909 Facsimile: + 44 (0) 24 7651 6566

Email: [email protected]

Vision Statement Our vision is to contribute to the achievements of learners around

the world by providing integrated assessment and learning services, adapted to meet both local market and wider occupational needs

and delivered to international standards.

Page 1 of 15

Accounting Level 3 Series 4 2007

How to use this booklet

Model Answers have been developed by Education Development International plc (EDI) to offer additional information and guidance to Centres, teachers and candidates as they prepare for LCCI International Qualifications. The contents of this booklet are divided into 3 elements: (1) Questions – reproduced from the printed examination paper (2) Model Answers – summary of the main points that the Chief Examiner expected to

see in the answers to each question in the examination paper, plus a fully worked example or sample answer (where applicable)

(3) Helpful Hints – where appropriate, additional guidance relating to individual

questions or to examination technique Teachers and candidates should find this booklet an invaluable teaching tool and an aid to success. EDI provides Model Answers to help candidates gain a general understanding of the standard required. The general standard of model answers is one that would achieve a Distinction grade. EDI accepts that candidates may offer other answers that could be equally valid.

© Education Development International plc 2007 All rights reserved; no part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission of the Publisher. The book may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover, other than that in which it is published, without the prior consent of the Publisher.

Page 2 of 15

3001/4/07/MA Page 3 of 15

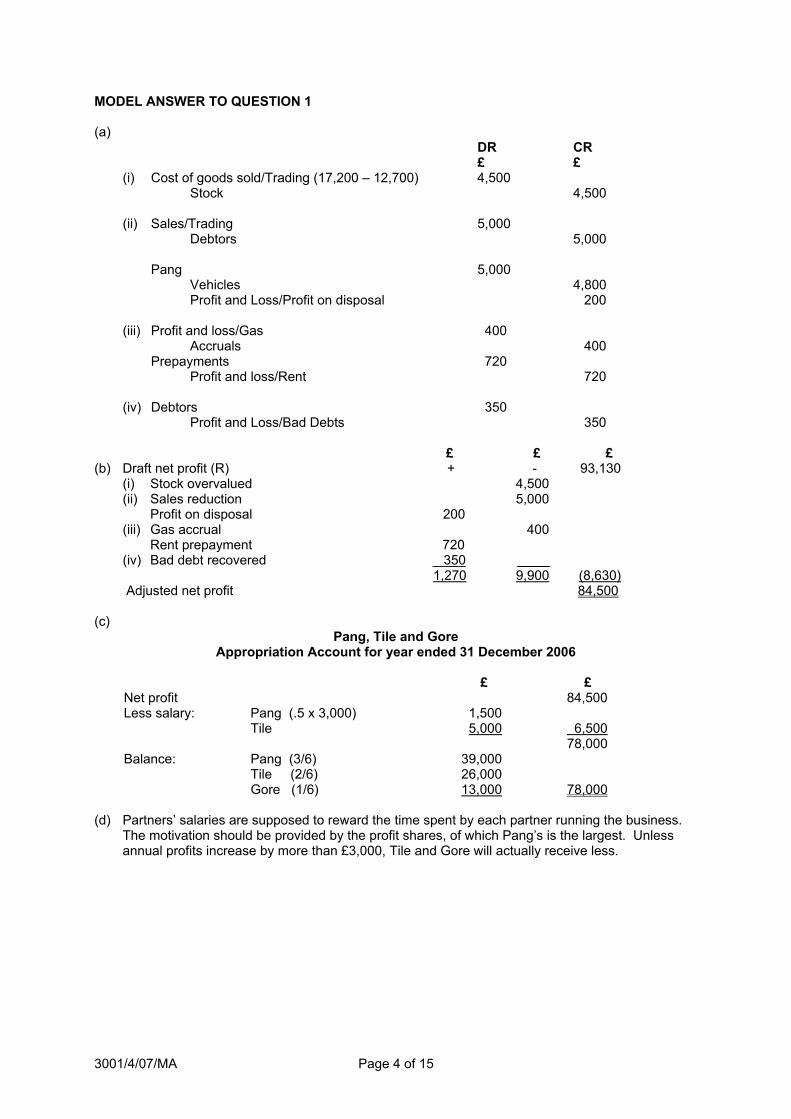

Accounting Level 3 Series 4 2007 QUESTION 1 Pang, Tile and Gore are in partnership sharing profits/losses in the ratio 3:2:1 respectively, after allowing for a salary of £5,000 per year to Tile. From 1 July 2006, Pang became entitled to a salary of £3,000 per year. After calculating the draft net profit for 2006, the following matters were discovered: (i) Closing stock had been included in the accounts as £17,200, when it should have been recorded

as £12,700 (ii) On 31 December 2006, Pang had taken over a vehicle (net book value £4,800) at an agreed

valuation of £5,000. This had been recorded by increasing sales and debtors by £5,000. The partnership does not record accumulated depreciation separately

(iii) No entries had been made in respect of accrued gas expense of £400 and prepaid rent expense

of £720 (iv) In December 2006, a debt of £350, written off during 2006 as bad, was unexpectedly received in

full. This had been recorded by debiting the bank and crediting the debtor, but no other entry had been made.

AFTER adjusting for the matters above, the net profit of the partnership for 2006 was £84,500. REQUIRED Prepare: (a) journal entries, (without narratives), showing how matters (i) to (iv) above were corrected in the

books of the partnership. (7 marks)

(b) a statement showing the draft net profit of the partnership for 2006 BEFORE the corrections

shown in (a) above. (5 marks)

(c) the Appropriation Account of the partnership for the year ended 31 December 2006.

(4 marks) “Giving a salary to Pang will increase his motivation and increase the amount of profit available for Tile and Gore”. REQUIRED (d) Briefly discuss the above statement. (4 marks)

(Total 20 marks)

3001/4/07/MA Page 4 of 15

MODEL ANSWER TO QUESTION 1 (a) DR CR £ £

(i) Cost of goods sold/Trading (17,200 – 12,700) 4,500 Stock 4,500 (ii) Sales/Trading 5,000

Debtors 5,000 Pang 5,000 Vehicles 4,800 Profit and Loss/Profit on disposal 200

(iii) Profit and loss/Gas 400 Accruals 400

Prepayments 720 Profit and loss/Rent 720

(iv) Debtors 350 Profit and Loss/Bad Debts 350

£ £ £ (b) Draft net profit (R) + - 93,130

(i) Stock overvalued 4,500 (ii) Sales reduction 5,000

Profit on disposal 200 (iii) Gas accrual 400

Rent prepayment 720 (iv) Bad debt recovered 350

1,270 9,900 (8,630) Adjusted net profit 84,500 (c)

Pang, Tile and Gore Appropriation Account for year ended 31 December 2006

£ £ Net profit 84,500 Less salary: Pang (.5 x 3,000) 1,500 Tile 5,000 6,500 78,000 Balance: Pang (3/6) 39,000 Tile (2/6) 26,000 Gore (1/6) 13,000 78,000

(d) Partners’ salaries are supposed to reward the time spent by each partner running the business.

The motivation should be provided by the profit shares, of which Pang’s is the largest. Unless annual profits increase by more than £3,000, Tile and Gore will actually receive less.

3001/4/07/MA Page 5 of 15

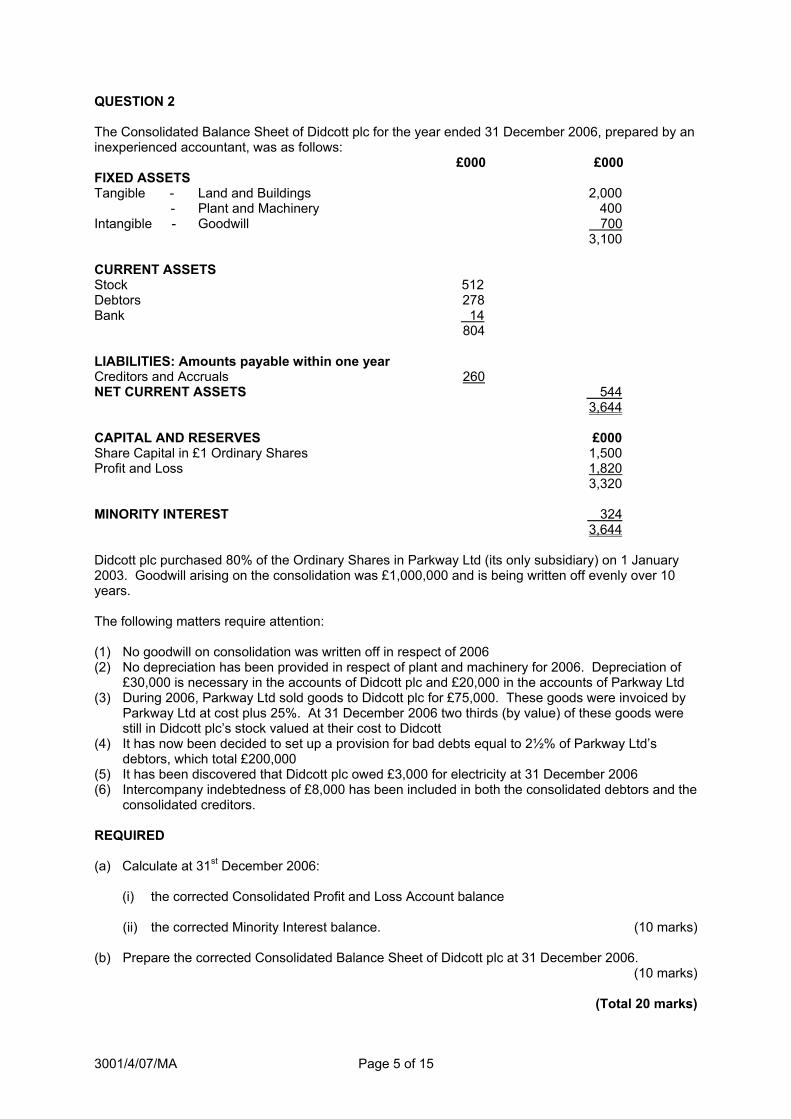

QUESTION 2 The Consolidated Balance Sheet of Didcott plc for the year ended 31 December 2006, prepared by an inexperienced accountant, was as follows: £000 £000 FIXED ASSETS Tangible - Land and Buildings 2,000 - Plant and Machinery 400 Intangible - Goodwill 700 3,100 CURRENT ASSETS Stock 512 Debtors 278 Bank 14 804 LIABILITIES: Amounts payable within one year Creditors and Accruals 260 NET CURRENT ASSETS 544 3,644 CAPITAL AND RESERVES £000 Share Capital in £1 Ordinary Shares 1,500 Profit and Loss 1,820 3,320 MINORITY INTEREST 324 3,644 Didcott plc purchased 80% of the Ordinary Shares in Parkway Ltd (its only subsidiary) on 1 January 2003. Goodwill arising on the consolidation was £1,000,000 and is being written off evenly over 10 years. The following matters require attention: (1) No goodwill on consolidation was written off in respect of 2006 (2) No depreciation has been provided in respect of plant and machinery for 2006. Depreciation of £30,000 is necessary in the accounts of Didcott plc and £20,000 in the accounts of Parkway Ltd (3) During 2006, Parkway Ltd sold goods to Didcott plc for £75,000. These goods were invoiced by

Parkway Ltd at cost plus 25%. At 31 December 2006 two thirds (by value) of these goods were still in Didcott plc’s stock valued at their cost to Didcott

(4) It has now been decided to set up a provision for bad debts equal to 2½% of Parkway Ltd’s debtors, which total £200,000

(5) It has been discovered that Didcott plc owed £3,000 for electricity at 31 December 2006 (6) Intercompany indebtedness of £8,000 has been included in both the consolidated debtors and the

consolidated creditors. REQUIRED (a) Calculate at 31st December 2006: (i) the corrected Consolidated Profit and Loss Account balance (ii) the corrected Minority Interest balance. (10 marks) (b) Prepare the corrected Consolidated Balance Sheet of Didcott plc at 31 December 2006.

(10 marks)

(Total 20 marks)

3001/4/07/MA Page 6 of 15

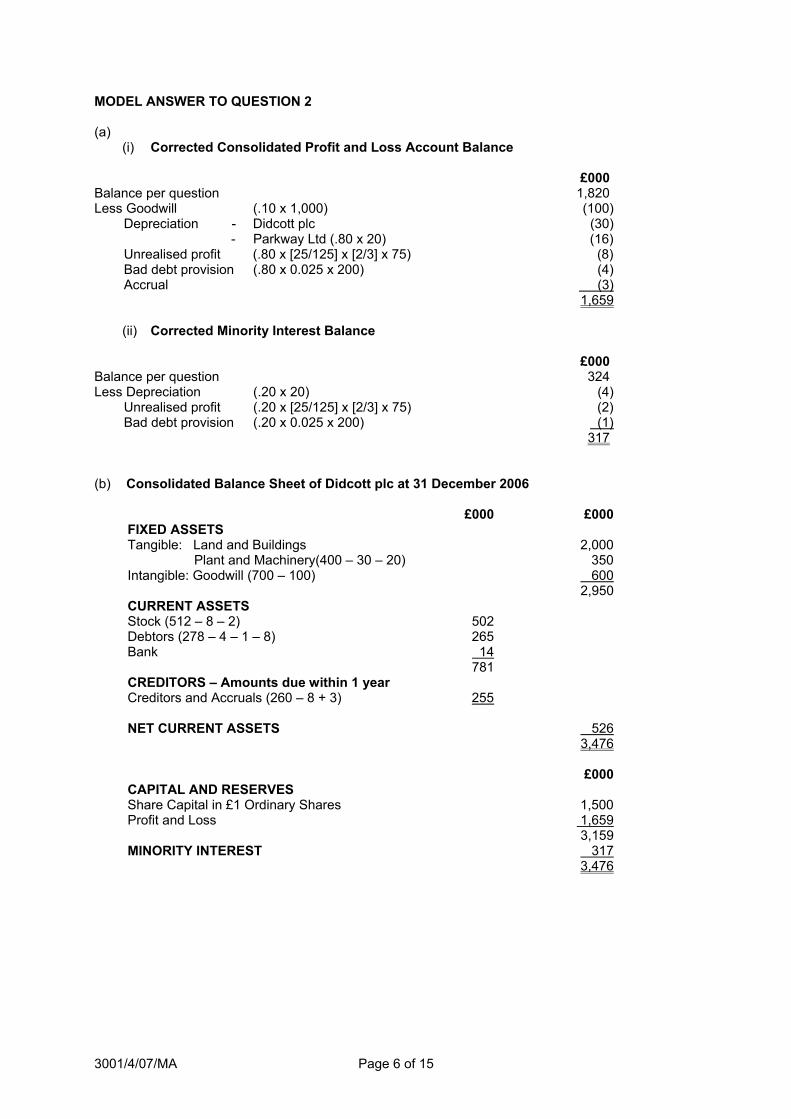

MODEL ANSWER TO QUESTION 2 (a)

(i) Corrected Consolidated Profit and Loss Account Balance £000 Balance per question 1,820 Less Goodwill (.10 x 1,000) (100) Depreciation - Didcott plc (30) - Parkway Ltd (.80 x 20) (16) Unrealised profit (.80 x [25/125] x [2/3] x 75) (8) Bad debt provision (.80 x 0.025 x 200) (4) Accrual (3) 1,659

(ii) Corrected Minority Interest Balance

£000 Balance per question 324 Less Depreciation (4) Unrealised profit (2) Bad debt provision (1)

(.20 x 20) (.20 x [25/125] x [2/3] x 75) (.20 x 0.025 x 200)

317

(b) Consolidated Balance Sheet of Didcott plc at 31 December 2006 £000 £000 FIXED ASSETS Tangible: Land and Buildings 2,000 Plant and Machinery(400 – 30 – 20) 350 Intangible: Goodwill (700 – 100) 600 2,950 CURRENT ASSETS Stock (512 – 8 – 2) 502 Debtors (278 – 4 – 1 – 8) 265 Bank 14 781 CREDITORS – Amounts due within 1 year Creditors and Accruals (260 – 8 + 3) 255 NET CURRENT ASSETS 526 3,476 £000 CAPITAL AND RESERVES Share Capital in £1 Ordinary Shares 1,500 Profit and Loss 1,659 3,159 MINORITY INTEREST 317 3,476

3001/4/07/MA Page 7 of 15

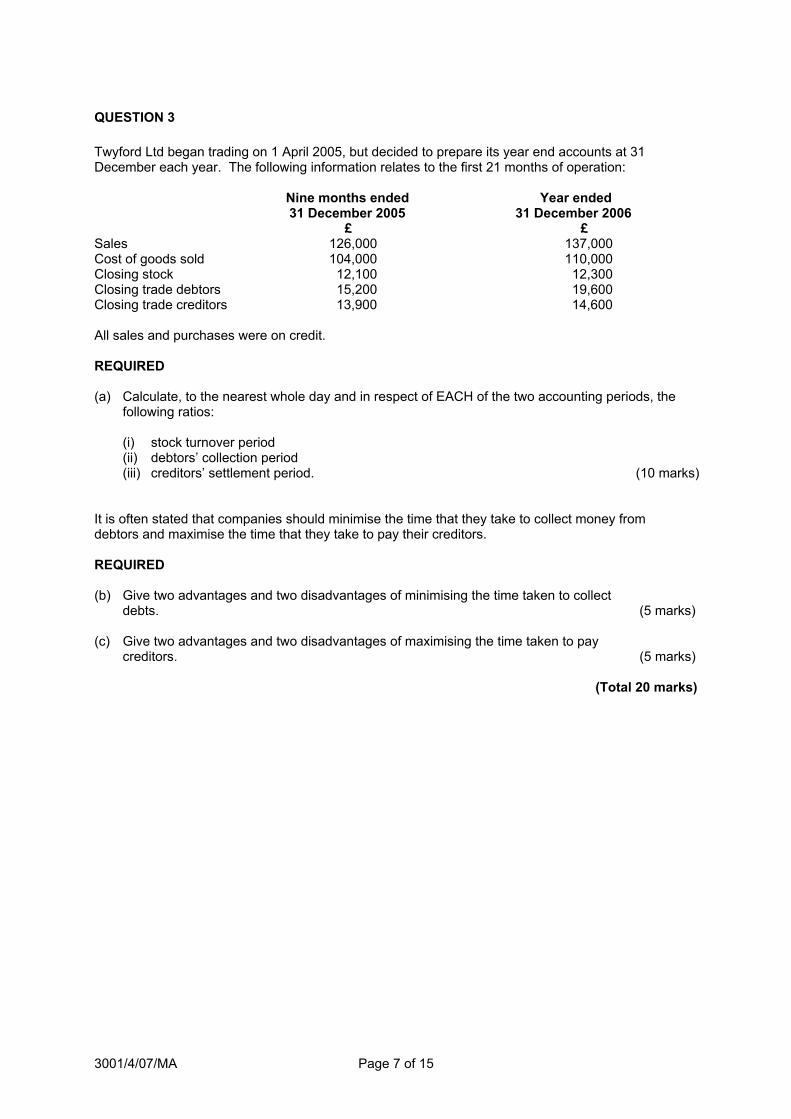

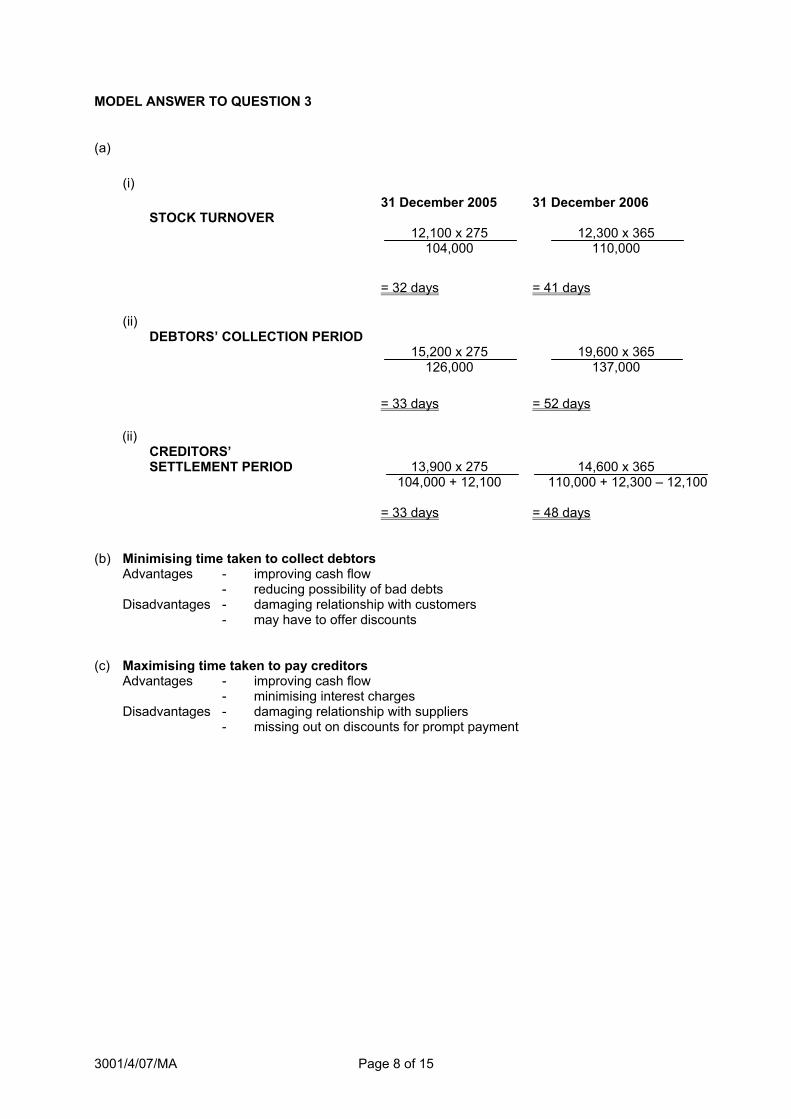

QUESTION 3 Twyford Ltd began trading on 1 April 2005, but decided to prepare its year end accounts at 31 December each year. The following information relates to the first 21 months of operation: Nine months ended Year ended 31 December 2005 31 December 2006 £ £ Sales 126,000 137,000 Cost of goods sold 104,000 110,000 Closing stock 12,100 12,300 Closing trade debtors 15,200 19,600 Closing trade creditors 13,900 14,600 All sales and purchases were on credit. REQUIRED (a) Calculate, to the nearest whole day and in respect of EACH of the two accounting periods, the following ratios: (i) stock turnover period (ii) debtors’ collection period (iii) creditors’ settlement period. (10 marks) It is often stated that companies should minimise the time that they take to collect money from debtors and maximise the time that they take to pay their creditors. REQUIRED (b) Give two advantages and two disadvantages of minimising the time taken to collect debts. (5 marks) (c) Give two advantages and two disadvantages of maximising the time taken to pay creditors. (5 marks)

(Total 20 marks)

3001/4/07/MA Page 8 of 15

MODEL ANSWER TO QUESTION 3

(a)

(i) 31 December 2005 31 December 2006 STOCK TURNOVER 12,100 x 275 12,300 x 365 104,000 110,000 = 32 days = 41 days

(ii)

DEBTORS’ COLLECTION PERIOD 15,200 x 275 19,600 x 365 126,000 137,000 = 33 days = 52 days

(ii)

CREDITORS’ SETTLEMENT PERIOD 13,900 x 275 14,600 x 365 104,000 + 12,100 110,000 + 12,300 – 12,100 = 33 days = 48 days

(b) Minimising time taken to collect debtors Advantages - improving cash flow

- reducing possibility of bad debts Disadvantages - damaging relationship with customers

- may have to offer discounts (c) Maximising time taken to pay creditors Advantages - improving cash flow

- minimising interest charges Disadvantages - damaging relationship with suppliers - missing out on discounts for prompt payment

3001/4/07/MA Page 9 of 15

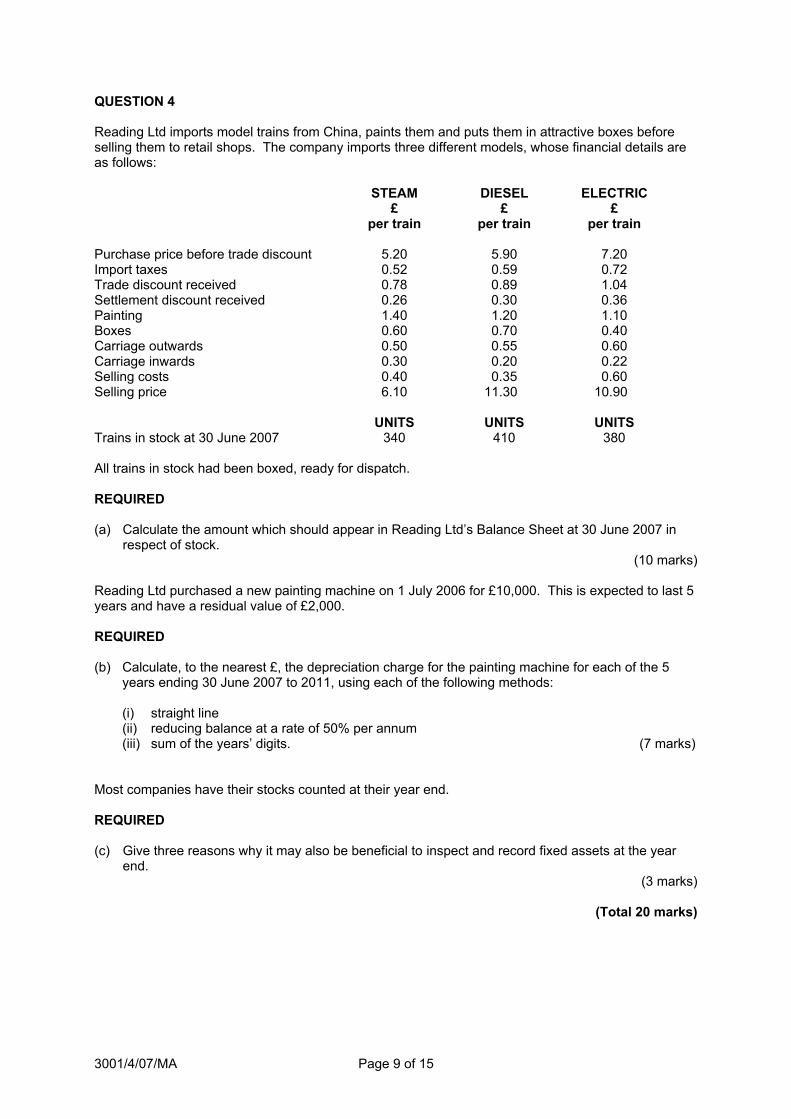

QUESTION 4 Reading Ltd imports model trains from China, paints them and puts them in attractive boxes before selling them to retail shops. The company imports three different models, whose financial details are as follows: STEAM DIESEL ELECTRIC £ £ £ per train per train per train Purchase price before trade discount 5.20 5.90 7.20 Import taxes 0.52 0.59 0.72 Trade discount received 0.78 0.89 1.04 Settlement discount received 0.26 0.30 0.36 Painting 1.40 1.20 1.10 Boxes 0.60 0.70 0.40 Carriage outwards 0.50 0.55 0.60 Carriage inwards 0.30 0.20 0.22 Selling costs 0.40 0.35 0.60 Selling price 6.10 11.30 10.90 UNITS UNITS UNITS Trains in stock at 30 June 2007 340 410 380 All trains in stock had been boxed, ready for dispatch. REQUIRED (a) Calculate the amount which should appear in Reading Ltd’s Balance Sheet at 30 June 2007 in respect of stock.

(10 marks) Reading Ltd purchased a new painting machine on 1 July 2006 for £10,000. This is expected to last 5 years and have a residual value of £2,000. REQUIRED (b) Calculate, to the nearest £, the depreciation charge for the painting machine for each of the 5

years ending 30 June 2007 to 2011, using each of the following methods: (i) straight line (ii) reducing balance at a rate of 50% per annum (iii) sum of the years’ digits. (7 marks) Most companies have their stocks counted at their year end. REQUIRED (c) Give three reasons why it may also be beneficial to inspect and record fixed assets at the year end.

(3 marks)

(Total 20 marks)

3001/4/07/MA Page 10 of 15

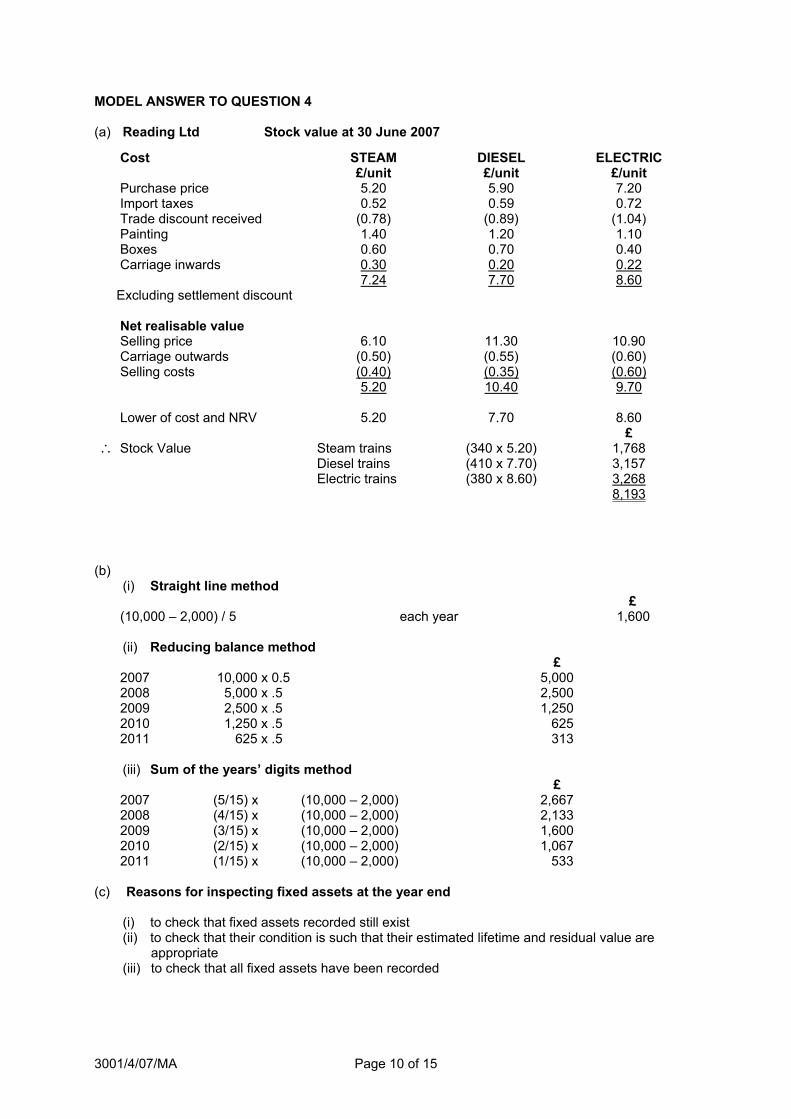

MODEL ANSWER TO QUESTION 4 (a) Reading Ltd Stock value at 30 June 2007

(b)

(i) Straight line method £ (10,000 – 2,000) / 5 each year 1,600

(ii) Reducing balance method

£ 2007 10,000 x 0.5 5,000 2008 5,000 x .5 2,500 2009 2,500 x .5 1,250 2010 1,250 x .5 625 2011 625 x .5 313

(iii) Sum of the years’ digits method

£ 2007 (5/15) x (10,000 – 2,000) 2,667 2008 (4/15) x (10,000 – 2,000) 2,133 2009 (3/15) x (10,000 – 2,000) 1,600 2010 (2/15) x (10,000 – 2,000) 1,067 2011 (1/15) x (10,000 – 2,000) 533 (c) Reasons for inspecting fixed assets at the year end

(i) to check that fixed assets recorded still exist (ii) to check that their condition is such that their estimated lifetime and residual value are

appropriate (iii) to check that all fixed assets have been recorded

Cost STEAM DIESEL ELECTRIC £/unit £/unit £/unit Purchase price 5.20 5.90 7.20 Import taxes 0.52 0.59 0.72 Trade discount received (0.78) (0.89) (1.04) Painting 1.40 1.20 1.10 Boxes 0.60 0.70 0.40 Carriage inwards 0.30 0.20 0.22 7.24 7.70 8.60 Excluding settlement discount Net realisable value Selling price 6.10 11.30 10.90 Carriage outwards (0.50) (0.55) (0.60) Selling costs (0.40) (0.35) (0.60) 5.20 10.40 9.70 Lower of cost and NRV 5.20 7.70 8.60 £ ∴ Stock Value Steam trains (340 x 5.20) 1,768 Diesel trains (410 x 7.70) 3,157 Electric trains (380 x 8.60) 3,268 8,193

3001/4/07/MA Page 11 of 15

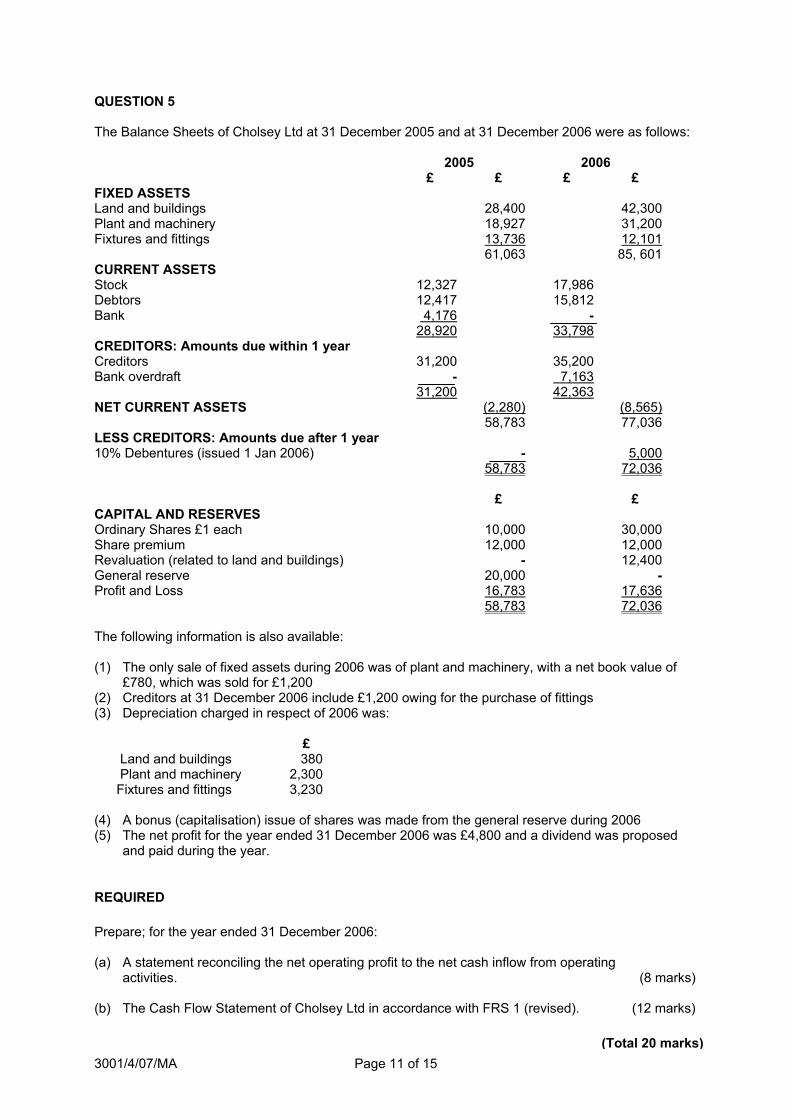

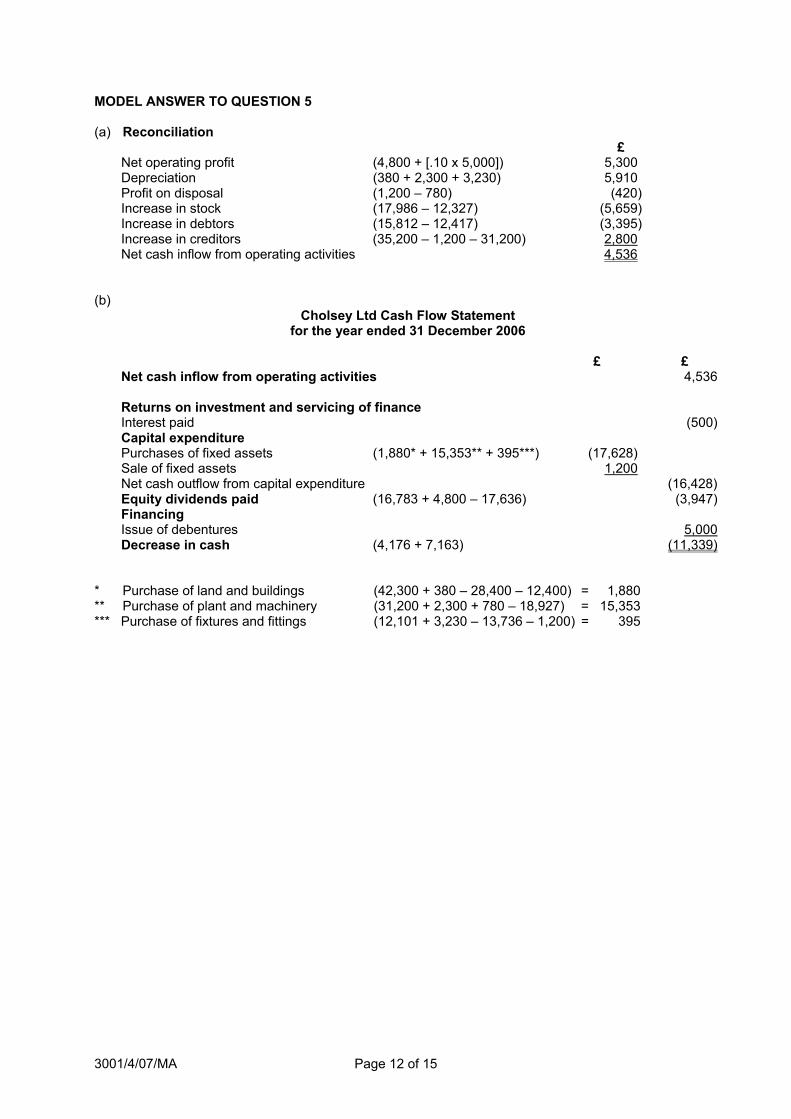

QUESTION 5 The Balance Sheets of Cholsey Ltd at 31 December 2005 and at 31 December 2006 were as follows: 2005 2006 £ £ £ £ FIXED ASSETS Land and buildings 28,400 42,300Plant and machinery 18,927 31,200Fixtures and fittings 13,736 12,101 61,063 85, 601CURRENT ASSETS Stock 12,327 17,986 Debtors 12,417 15,812 Bank 4,176 - 28,920 33,798 CREDITORS: Amounts due within 1 year Creditors 31,200 35,200 Bank overdraft - 7,163 31,200 42,363 NET CURRENT ASSETS (2,280) (8,565) 58,783 77,036LESS CREDITORS: Amounts due after 1 year 10% Debentures (issued 1 Jan 2006) - 5,000 58,783 72,036 £ £ CAPITAL AND RESERVES Ordinary Shares £1 each 10,000 30,000Share premium 12,000 12,000Revaluation (related to land and buildings) - 12,400General reserve 20,000 -Profit and Loss 16,783 17,636 58,783 72,036 The following information is also available: (1) The only sale of fixed assets during 2006 was of plant and machinery, with a net book value of

£780, which was sold for £1,200 (2) Creditors at 31 December 2006 include £1,200 owing for the purchase of fittings (3) Depreciation charged in respect of 2006 was: £ Land and buildings 380 Plant and machinery 2,300 Fixtures and fittings 3,230 (4) A bonus (capitalisation) issue of shares was made from the general reserve during 2006 (5) The net profit for the year ended 31 December 2006 was £4,800 and a dividend was proposed

and paid during the year.

REQUIRED Prepare; for the year ended 31 December 2006: (a) A statement reconciling the net operating profit to the net cash inflow from operating activities. (8 marks) (b) The Cash Flow Statement of Cholsey Ltd in accordance with FRS 1 (revised). (12 marks)

(Total 20 marks)

3001/4/07/MA Page 12 of 15

MODEL ANSWER TO QUESTION 5 (a) Reconciliation

£ Net operating profit (4,800 + [.10 x 5,000]) 5,300 Depreciation (380 + 2,300 + 3,230) 5,910 Profit on disposal (1,200 – 780) (420) Increase in stock (17,986 – 12,327) (5,659) Increase in debtors (15,812 – 12,417) (3,395) Increase in creditors (35,200 – 1,200 – 31,200) 2,800 Net cash inflow from operating activities 4,536

(b)

Cholsey Ltd Cash Flow Statement for the year ended 31 December 2006

£ £ Net cash inflow from operating activities 4,536 Returns on investment and servicing of finance Interest paid (500) Capital expenditure Purchases of fixed assets (1,880* + 15,353** + 395***) (17,628) Sale of fixed assets 1,200 Net cash outflow from capital expenditure (16,428) Equity dividends paid (16,783 + 4,800 – 17,636) (3,947) Financing Issue of debentures 5,000 Decrease in cash (4,176 + 7,163) (11,339)

* Purchase of land and buildings (42,300 + 380 – 28,400 – 12,400) = 1,880 ** Purchase of plant and machinery (31,200 + 2,300 + 780 – 18,927) = 15,353 *** Purchase of fixtures and fittings (12,101 + 3,230 – 13,736 – 1,200) = 395

3001/4/07/MA Page 13 of 15

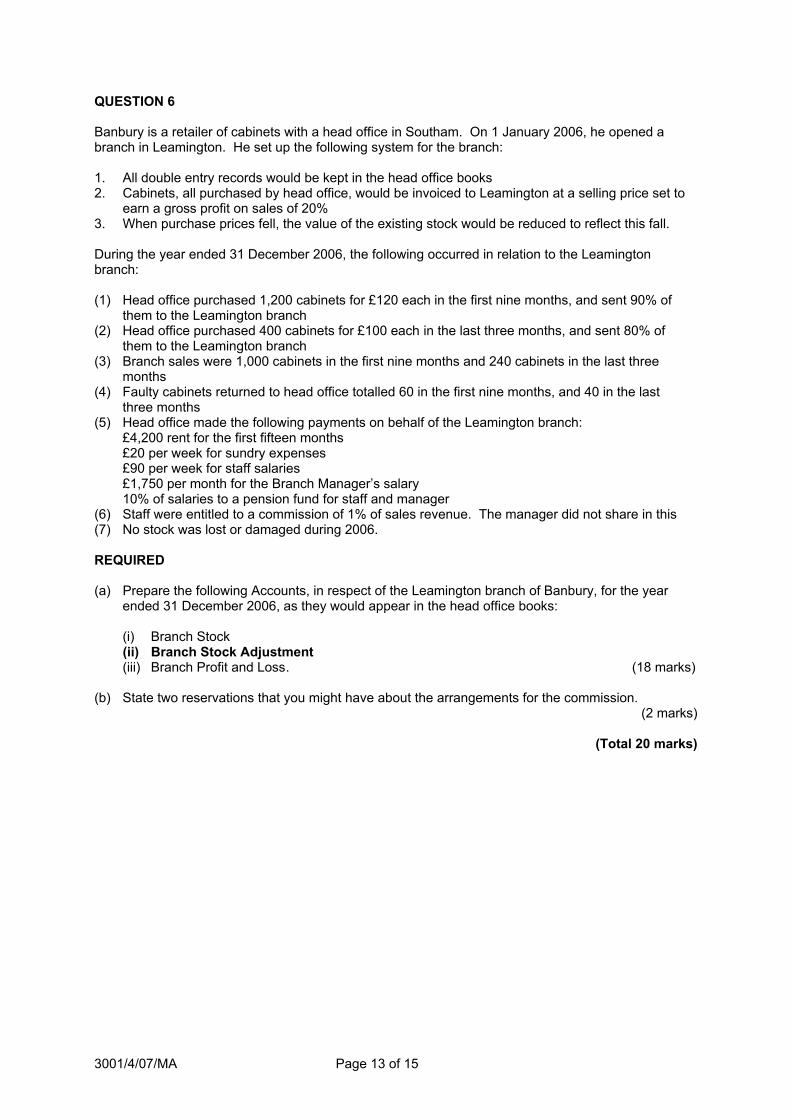

QUESTION 6 Banbury is a retailer of cabinets with a head office in Southam. On 1 January 2006, he opened a branch in Leamington. He set up the following system for the branch: 1. All double entry records would be kept in the head office books 2. Cabinets, all purchased by head office, would be invoiced to Leamington at a selling price set to

earn a gross profit on sales of 20% 3. When purchase prices fell, the value of the existing stock would be reduced to reflect this fall. During the year ended 31 December 2006, the following occurred in relation to the Leamington branch: (1) Head office purchased 1,200 cabinets for £120 each in the first nine months, and sent 90% of

them to the Leamington branch (2) Head office purchased 400 cabinets for £100 each in the last three months, and sent 80% of

them to the Leamington branch (3) Branch sales were 1,000 cabinets in the first nine months and 240 cabinets in the last three

months (4) Faulty cabinets returned to head office totalled 60 in the first nine months, and 40 in the last

three months (5) Head office made the following payments on behalf of the Leamington branch:

£4,200 rent for the first fifteen months £20 per week for sundry expenses £90 per week for staff salaries £1,750 per month for the Branch Manager’s salary 10% of salaries to a pension fund for staff and manager

(6) Staff were entitled to a commission of 1% of sales revenue. The manager did not share in this (7) No stock was lost or damaged during 2006. REQUIRED (a) Prepare the following Accounts, in respect of the Leamington branch of Banbury, for the year ended 31 December 2006, as they would appear in the head office books: (i) Branch Stock (ii) Branch Stock Adjustment (iii) Branch Profit and Loss . (18 marks) (b) State two reservations that you might have about the arrangements for the commission.

(2 marks)

(Total 20 marks)

3001/4/07/MA Page 14 of 15

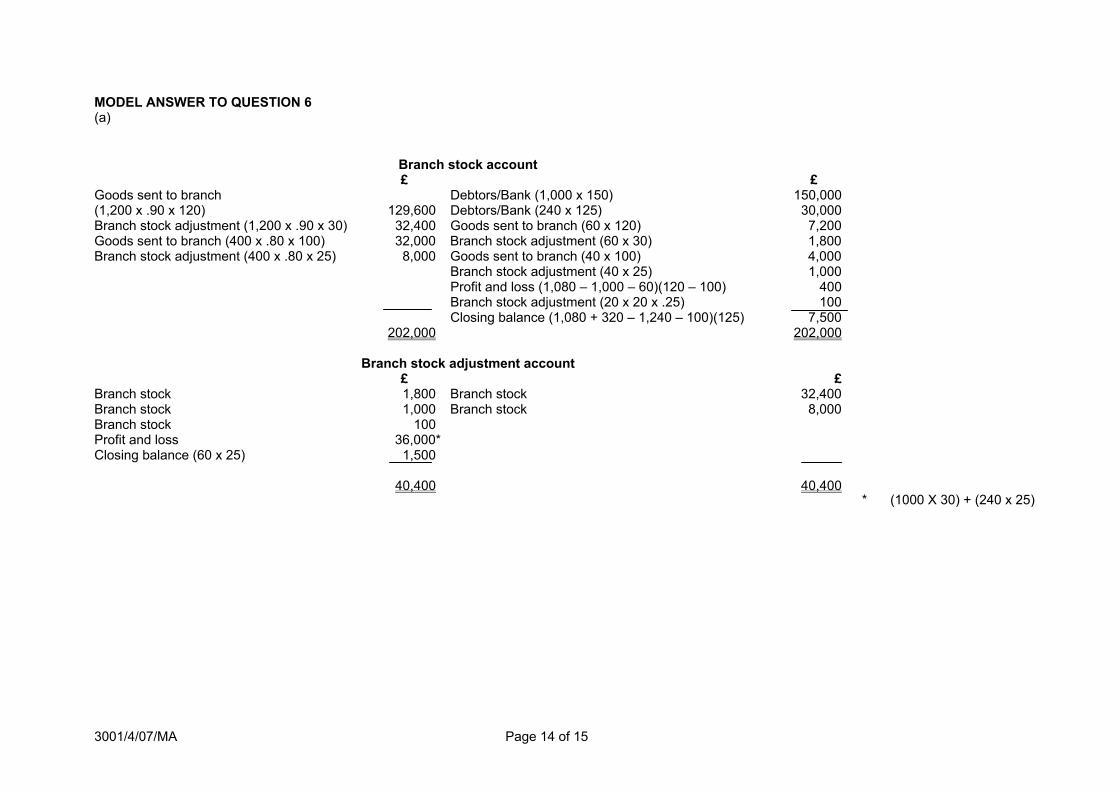

MODEL ANSWER TO QUESTION 6 (a)

* (1000 X 30) + (240 x 25)

Branch stock account £ £ Goods sent to branch (1,200 x .90 x 120)

129,600

Debtors/Bank (1,000 x 150) Debtors/Bank (240 x 125)

150,000 30,000

Branch stock adjustment (1,200 x .90 x 30) 32,400 Goods sent to branch (60 x 120) 7,200Goods sent to branch (400 x .80 x 100) 32,000 Branch stock adjustment (60 x 30) 1,800Branch stock adjustment (400 x .80 x 25) 8,000 Goods sent to branch (40 x 100) 4,000 Branch stock adjustment (40 x 25) 1,000 Profit and loss (1,080 – 1,000 – 60)(120 – 100) 400 Branch stock adjustment (20 x 20 x .25) 100 Closing balance (1,080 + 320 – 1,240 – 100)(125) 7,500 202,000 202,000

Branch stock adjustment account £ £Branch stock 1,800 Branch stock 32,400Branch stock 1,000 Branch stock 8,000Branch stock 100 Profit and loss 36,000* Closing balance (60 x 25) 1,500 40,400 40,400

3001/4/07/MA Page 15 of 15 © Education Development International plc 2007

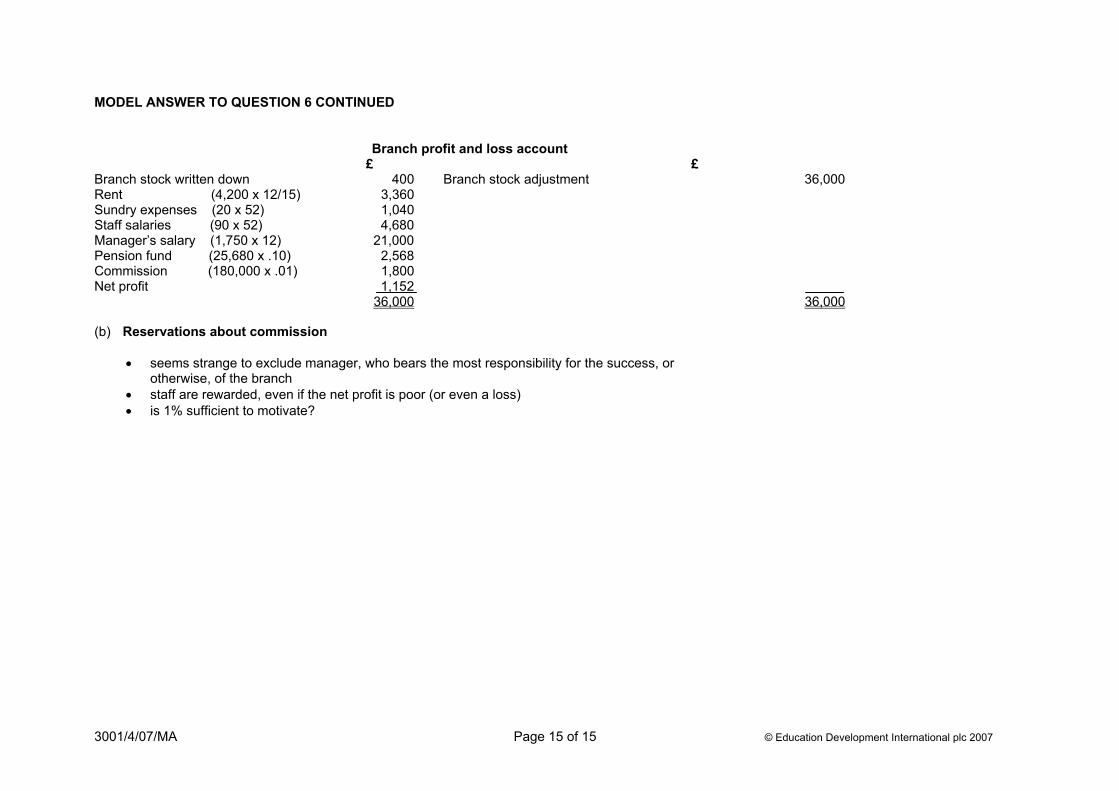

MODEL ANSWER TO QUESTION 6 CONTINUED

(b) Reservations about commission

• seems strange to exclude manager, who bears the most responsibility for the success, or otherwise, of the branch • staff are rewarded, even if the net profit is poor (or even a loss) • is 1% sufficient to motivate?

Branch profit and loss account £ £ Branch stock written down 400 Branch stock adjustment 36,000Rent (4,200 x 12/15) 3,360 Sundry expenses (20 x 52) 1,040 Staff salaries (90 x 52) 4,680 Manager’s salary (1,750 x 12) 21,000 Pension fund (25,680 x .10) 2,568 Commission (180,000 x .01) 1,800 Net profit 1,152 36,000 36,000