Embed Size (px)

Citation preview

ACFE

Foreign Corrupt Practices Act: Lessons Learned June 13–14, 2011

www.pwc.com

PwC

Agenda

Stage setting: ―FCPA Enforcement Atmosphere‖

Quick primer/level set on FCPA

Trends in cases/settlements

Increased risk areas and red flags

Key lessons learned from recent enforcement cases

PwC

Current U.S. FCPA Climate

To Set the Stage

Lanny Breuer: “We will continue to insist on corporate guilty pleas or to bring criminal charges against corporations in appropriate cases—when the criminal conduct is egregious, pervasive, and systemic, or when the corporation fails to implement compliance reforms, changes to its corporate culture, and undertake other measures designed to prevent the recurrence of the criminal conduct.”

1

PwC

Recent Changes in U.S. FCPA Enforcement Agencies

2

―The SEC has created an FCPA unit to

crack down on cross-border bribery, and

in the first nine months of 2010

alone, we obtained more than $300

million in disgorgement and

penalties.‖ –Robert Khuzami, Director of

SEC‘s Division of Enforcement

In the past year, the U.S. Enforcement

agencies have expanded their FCPA

prosecution capabilities:

DOJ added 25 full-time FCPA prosecutors

FBI established a specialized unit of

agents dedicated to FCPA investigations

SEC created a specialized unit

focused on FCPA enforcement

Attorney General Eric Holder –

―Bribery in international

business transactions weakens economic

development; it undermines

confidence in the marketplace; and it

distorts competition.‖

(October 2010)

PwC

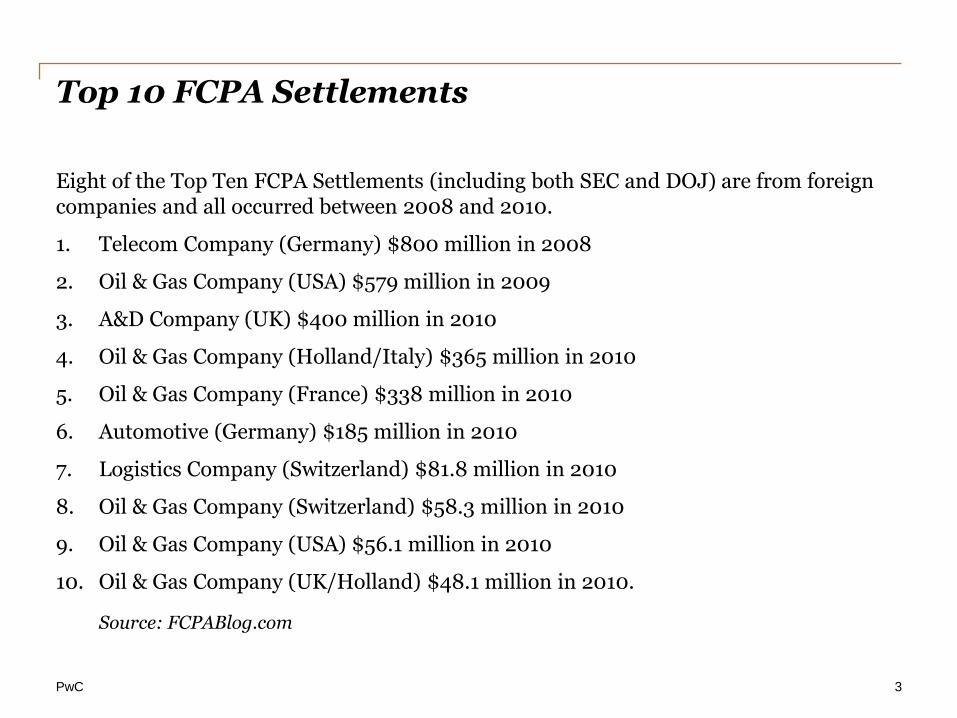

Top 10 FCPA Settlements

3

Eight of the Top Ten FCPA Settlements (including both SEC and DOJ) are from foreign companies and all occurred between 2008 and 2010.

1. Telecom Company (Germany) $800 million in 2008

2. Oil & Gas Company (USA) $579 million in 2009

3. A&D Company (UK) $400 million in 2010

4. Oil & Gas Company (Holland/Italy) $365 million in 2010

5. Oil & Gas Company (France) $338 million in 2010

6. Automotive (Germany) $185 million in 2010

7. Logistics Company (Switzerland) $81.8 million in 2010

8. Oil & Gas Company (Switzerland) $58.3 million in 2010

9. Oil & Gas Company (USA) $56.1 million in 2010

10. Oil & Gas Company (UK/Holland) $48.1 million in 2010.

Source: FCPABlog.com

PwC

FCPA History

4

The Foreign Corrupt Practices Act (FCPA), was created in 1977 as a result of over 400 U.S. companies admitting to making questionable or illegal payments to foreign government officials, politicians, and political parties. Congress enacted the FCPA in an attempt to stop bribery of foreign officials and restore the integrity of American businesses.

The FCPA‘s scope was expanded in 1998. It was amended to mirror language included in the OECD Convention on Combating Bribery of Foreign Public Officials in International Business Transactions.

• Any ―improper advantage‖ vs. ―business‖

• Expanded jurisdictional reach

• Expanded definition of foreign official

PwC

The FCPA Is Violated When

5

―An issuer or any of its officers, directors, employees, agents or shareholders, a domestic concern, or foreign national pays, offers, promises to pay, or authorizes/approves the payment of money or anything of value:

– To a foreign official, foreign political party, candidate for political office, or official of a public international organization

– In a corrupt effort to obtain, retain, or direct business to any person or obtain an improper advantage‖

PwC

Key Elements of the FCPA

6

Anti-Bribery provisions

• It is a crime for any U.S. person or company to directly or indirectly pay or promise anything of value to any foreign official to obtain or retain any improper advantage.

Accounting requirements

• Section 13 (b) (2) (A) of the Exchange Act

• ―Make and keep books, records, and accounts, which in reasonable detail, accurately reflect the transactions and dispositions of assets‖

• Reasonable—such level of detail that would satisfy prudent officials in the conduct of their affairs

Internal controls

• Section 13 (b) (2) (B) of the Exchange Act

• ―Devise and maintain a system of internal accounting controls sufficient to provide reasonable assurance that‖ transactions are recorded appropriately and in accordance with rules and regulations

PwC

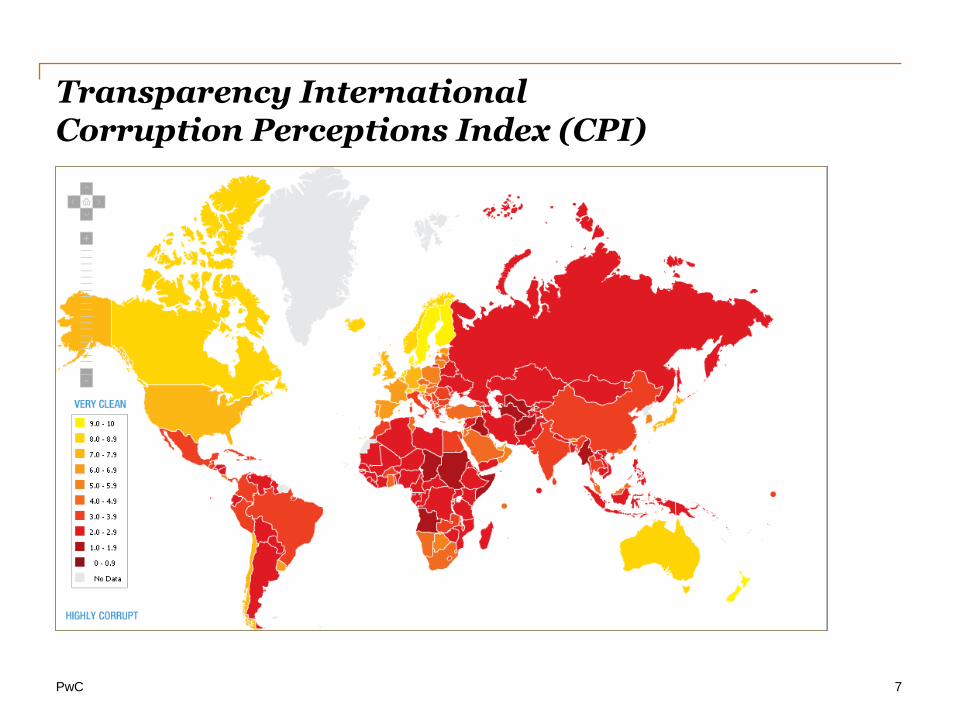

Transparency International Corruption Perceptions Index (CPI)

7

PwC

Why Are Certified Fraud Examiners Typically Involved?

8

Benefits of using a forensic accounting investigator:

• FCPA, accounting, and international investigative experience

• Credibility with regulators

• Expedited global coverage

• Impartial

• Independent

• Relieves internal time and resource constraints

PwC

Red Flags

9

• Use of agents, consultants, and other third parties

• Travel and entertainment for government officials

• Charitable gifts and donations ―in country‖

• Payments to state-owned entity employees for research and/or symposia

• Vague vendor/subcontractor scopes

• What are the deliverables

• What is the scope of work

• Internships/scholarships

• Obtaining licenses/permits, certain government-related efforts

PwC

Specific Red Flags: Local Agents, Consultants, etc.

10

• Request for payment in cash

• Request for payment to someone other than agent

• Request for unreasonable compensation in light of services promised or rendered

• Request for reimbursement of expenses with incomplete documentation

• Emphasis on ―connections‖

• Be aware of possible direct or indirect associations between agent and foreign officials (e.g., payment to consultant who is married to a foreign official could be viewed as indirect benefit to foreign official)

PwC

Areas of Increased Risk of an FCPA Violation

11

• Hot industries—Financial Services, Mining/Extractive Industries, International Manufacturing, Oil & Gas, Telecom, Medical Devices, Pharmaceuticals, Aerospace and Defense, and Infrastructure

• Geographies—BRIC, Asia, Latin America, Africa and Eastern Europe

• Use of third parties (agents, distributors)

• Sales to state-/quasi-government-owned entities

• International M&A activity

• Regulatory Issues

• Client entertainment/travel

• Licensing, tax issues, and product registration

PwC

Enforcement Trends

12

• Larger penalties (Hundreds of millions of dollars and even 1B+ settlements)

• Coordination of regulators globally

• Voluntary disclosures not the only source of leads for regulators (2/3 of cases non voluntary)

• Foreign state-owned entities suing U.S. companies

• Lack of third-party due diligence/agents

• Qui Tam type bounty—whistleblowers could receive from 10–30% of amounts recovered through enforcement actions

• Increasing enforcement by foreign regulators and IFIs

PwC

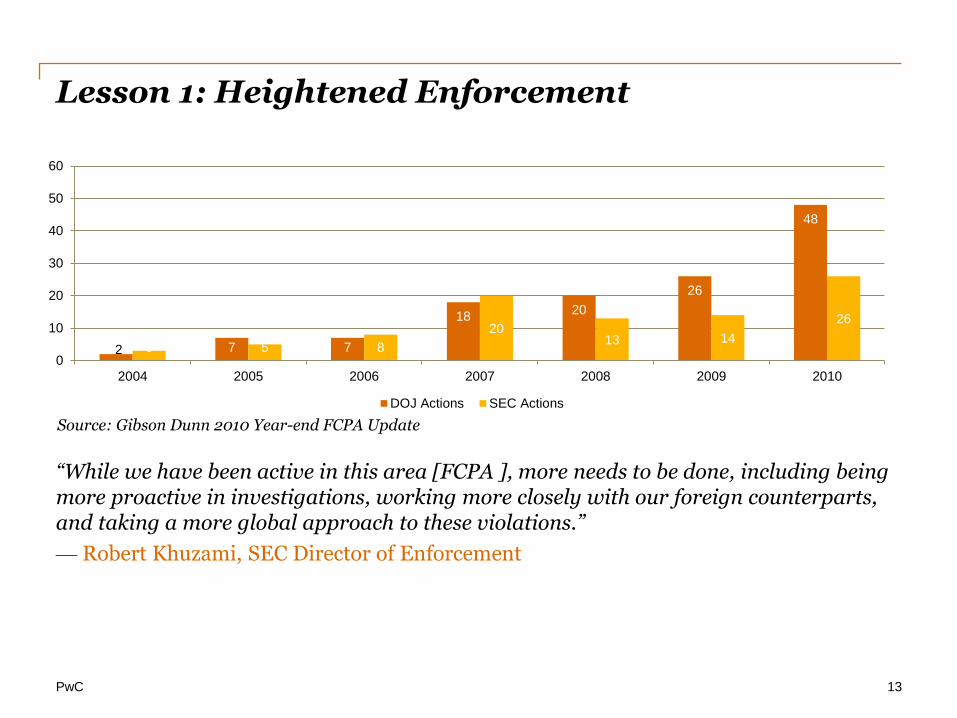

Lesson 1: Heightened Enforcement

13

“While we have been active in this area [FCPA ], more needs to be done, including being more proactive in investigations, working more closely with our foreign counterparts, and taking a more global approach to these violations.”

— Robert Khuzami, SEC Director of Enforcement

Source: Gibson Dunn 2010 Year-end FCPA Update

2 7 7

18 20

26

48

3 5 8

20 13 14

26

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010

DOJ Actions SEC Actions

PwC

Lesson 2: You Don’t Have to be a U.S. Entity (or an SEC Filer)

14

Case Example: A Global Freight Forwarding Company (fine = $82 million)

Alleged misconduct: $30M in payments; sr. management knew of and condoned bribery; payments were made to customs, immigration, tax, and other officials in Nigeria, Angola, Russia, and other countries

The Company reached a settlement with the SEC, which alleged that Global Logistics Company acting as an agent of its [SEC] issuer customers, committed violations of the FCPA‘s anti-bribery provisions, aided and abetted its customers‘ violations of the anti-bribery, books and records, and internal controls provisions.

The company also entered into a settlement with the DOJ and agreed to a two-count criminal information charging conspiracy to violate and violation of the FCPA‘s anti-bribery provisions.

PwC

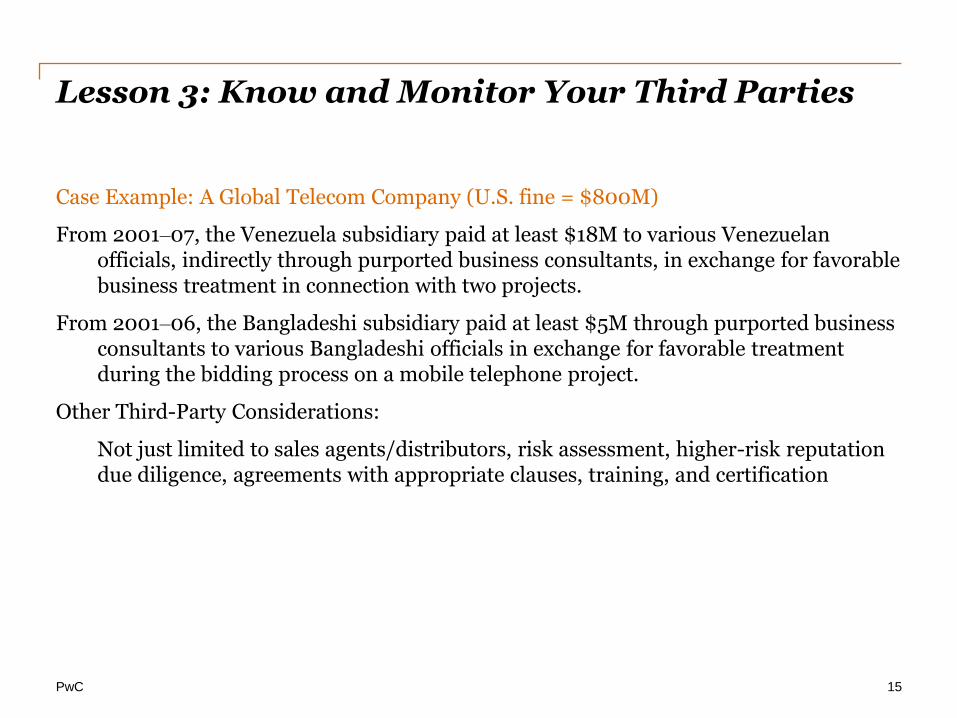

Lesson 3: Know and Monitor Your Third Parties

15

Case Example: A Global Telecom Company (U.S. fine = $800M)

From 2001–07, the Venezuela subsidiary paid at least $18M to various Venezuelan officials, indirectly through purported business consultants, in exchange for favorable business treatment in connection with two projects.

From 2001–06, the Bangladeshi subsidiary paid at least $5M through purported business consultants to various Bangladeshi officials in exchange for favorable treatment during the bidding process on a mobile telephone project.

Other Third-Party Considerations:

Not just limited to sales agents/distributors, risk assessment, higher-risk reputation due diligence, agreements with appropriate clauses, training, and certification

PwC

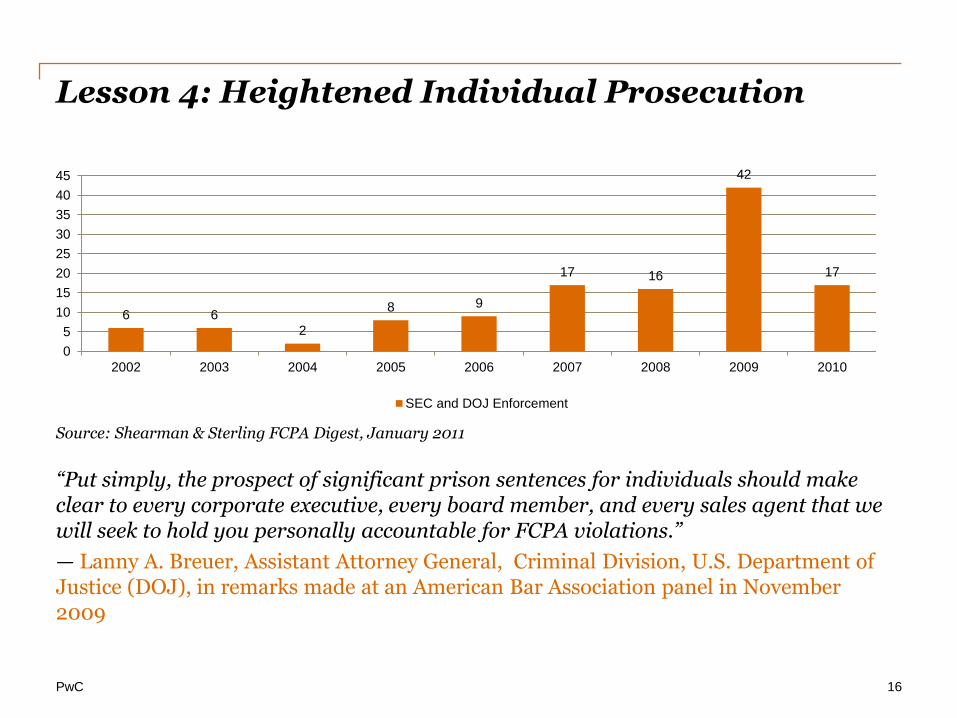

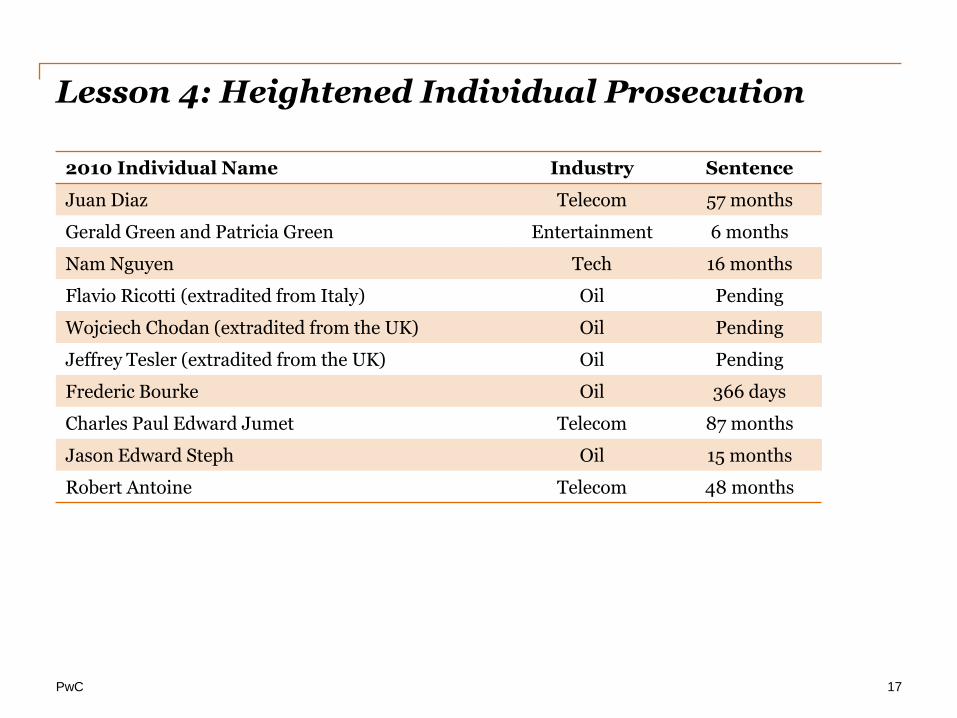

Lesson 4: Heightened Individual Prosecution

16

“Put simply, the prospect of significant prison sentences for individuals should make clear to every corporate executive, every board member, and every sales agent that we will seek to hold you personally accountable for FCPA violations.”

— Lanny A. Breuer, Assistant Attorney General, Criminal Division, U.S. Department of Justice (DOJ), in remarks made at an American Bar Association panel in November 2009

Source: Shearman & Sterling FCPA Digest, January 2011

6 6

2

8 9

17 16

42

17

0

5

10

15

20

25

30

35

40

45

2002 2003 2004 2005 2006 2007 2008 2009 2010

SEC and DOJ Enforcement

PwC

Lesson 4: Heightened Individual Prosecution

17

2010 Individual Name Industry Sentence

Juan Diaz Telecom 57 months

Gerald Green and Patricia Green Entertainment 6 months

Nam Nguyen Tech 16 months

Flavio Ricotti (extradited from Italy) Oil Pending

Wojciech Chodan (extradited from the UK) Oil Pending

Jeffrey Tesler (extradited from the UK) Oil Pending

Frederic Bourke Oil 366 days

Charles Paul Edward Jumet Telecom 87 months

Jason Edward Steph Oil 15 months

Robert Antoine Telecom 48 months

PwC

Lesson 5: Potential Liability/Accountability Without Direct Involvement

18

• In a recent case involving a large herbal vitamin supplements company, the SEC brought claims against the former CEO and CFO for violations of the books and records provision of the FCPA by holding the executives accountable as "control persons" under Section 20(a) of the Securities Exchange Act of 1934, for failing to adequately supervise the miscreant employees of a Brazilian subsidiary.

• The control-person theory of liability raises the stakes for officers and directors who are now faced with the prospect of regulatory and law enforcement scrutiny of their leadership, and perhaps even in situations where they lack direct involvement in activities several layers of management below them.

• However, while much has been written about CEO/CFO involvement, what many have overlooked is the allegations against the Audit Committee Chairman. See KPMG 10A withdrawal letter in which the AC Chair made no attempts to notify the auditors of inaccurate representations made to them despite believing that these could be considered material from an auditing standpoint and could pose a significant problem to our company. On the Special Committee‘s recommendation, the AC Chair resigned.

PwC

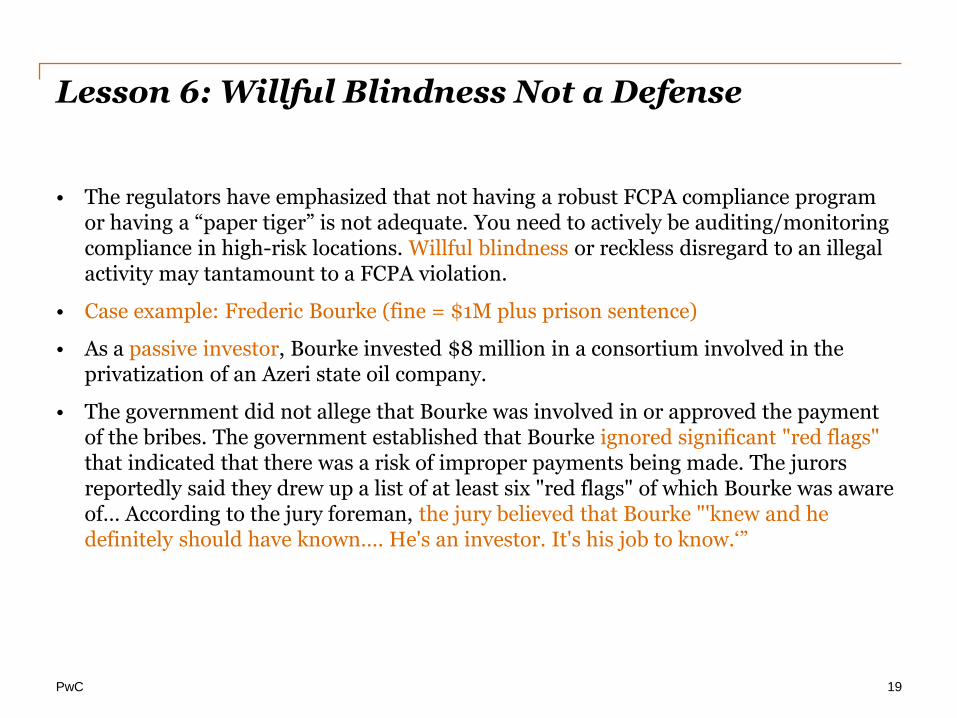

Lesson 6: Willful Blindness Not a Defense

19

• The regulators have emphasized that not having a robust FCPA compliance program or having a ―paper tiger‖ is not adequate. You need to actively be auditing/monitoring compliance in high-risk locations. Willful blindness or reckless disregard to an illegal activity may tantamount to a FCPA violation.

• Case example: Frederic Bourke (fine = $1M plus prison sentence)

• As a passive investor, Bourke invested $8 million in a consortium involved in the privatization of an Azeri state oil company.

• The government did not allege that Bourke was involved in or approved the payment of the bribes. The government established that Bourke ignored significant "red flags" that indicated that there was a risk of improper payments being made. The jurors reportedly said they drew up a list of at least six "red flags" of which Bourke was aware of… According to the jury foreman, the jury believed that Bourke "'knew and he definitely should have known…. He's an investor. It's his job to know.‗‖

PwC

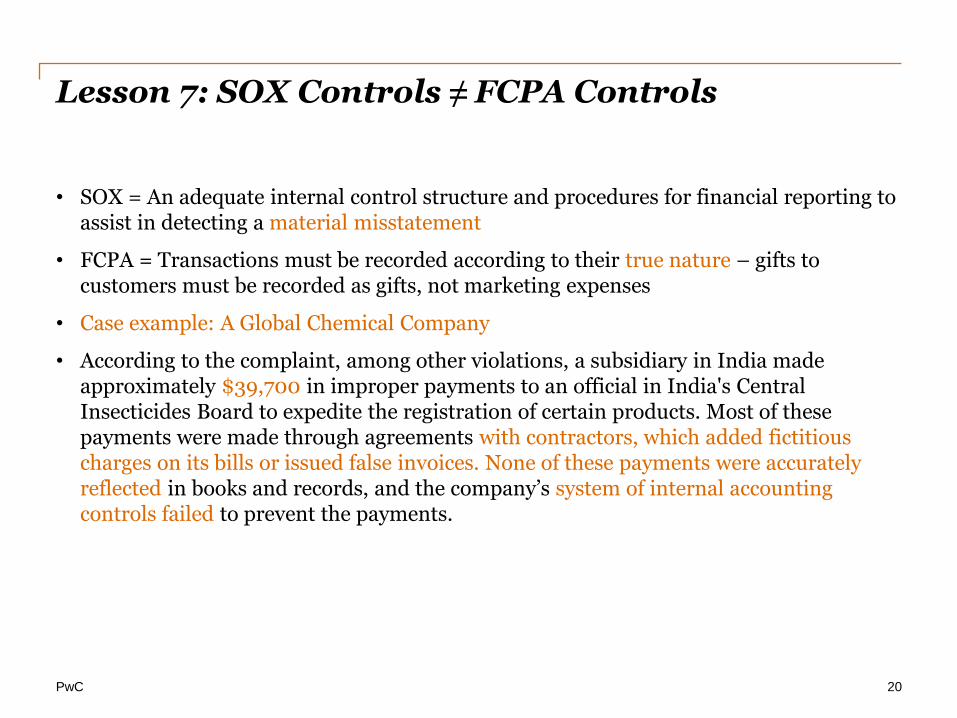

Lesson 7: SOX Controls ≠ FCPA Controls

20

• SOX = An adequate internal control structure and procedures for financial reporting to assist in detecting a material misstatement

• FCPA = Transactions must be recorded according to their true nature – gifts to customers must be recorded as gifts, not marketing expenses

• Case example: A Global Chemical Company

• According to the complaint, among other violations, a subsidiary in India made approximately $39,700 in improper payments to an official in India's Central Insecticides Board to expedite the registration of certain products. Most of these payments were made through agreements with contractors, which added fictitious charges on its bills or issued false invoices. None of these payments were accurately reflected in books and records, and the company‘s system of internal accounting controls failed to prevent the payments.

PwC

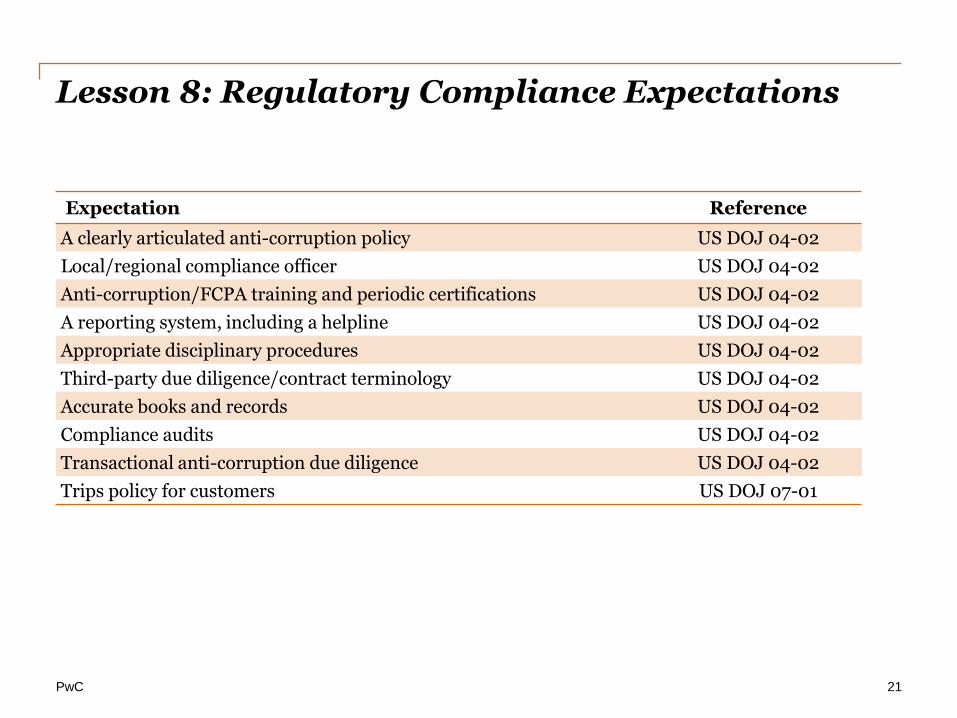

Lesson 8: Regulatory Compliance Expectations

21

Expectation Reference

A clearly articulated anti-corruption policy US DOJ 04-02

Local/regional compliance officer US DOJ 04-02

Anti-corruption/FCPA training and periodic certifications US DOJ 04-02

A reporting system, including a helpline US DOJ 04-02

Appropriate disciplinary procedures US DOJ 04-02

Third-party due diligence/contract terminology US DOJ 04-02

Accurate books and records US DOJ 04-02

Compliance audits US DOJ 04-02

Transactional anti-corruption due diligence US DOJ 04-02

Trips policy for customers US DOJ 07-01

PwC

Lesson 9: Changing U.S. Regulatory Landscape

22

• July 21, 2010: Dodd Frank Act

• May 20, 2010: Overseas Contractor Reform Act

- A bill to require the proposal for debarment from contracting with the Federal Government of persons violating the FCPA of 1977.

• Use of traditional law enforcement techniques (wiretapping, informants, undercover agents):

- SHOT SHOW: 22 individuals were arrested following a two-and-a-half-year-long ―sting‖ operation in which two FBI agents posing as representatives of a foreign government official were introduced to the subjects by a confidential informant

PwC

Lesson 10: Changing Int’l Regulatory Landscape

23

• April 2011: UK Bribery Act 2010

• Commercial and public bribery

• Does not permit facilitating payments exception

• Penalizes distribution and receipt of bribe(s)/not limited to government officials

• Unlimited fines against companies and 10 years imprisonment for individuals

• Requires systems and controls to be put in place to demonstrate compliance

PwC

Lesson 11: Questions to Expect from Regulators

24

• Who owns the FCPA compliance program and to whom does that person report?

• Do we have special policies and procedures dedicated to FCPA/anti-bribery? If so, what are they?

• Are we doing FCPA compliance assessments? In which countries? How often? Is internal audit including FCPA-specific audits in its scope and, if not, why?

• What is our training program like?

- Who gets trained?

- How rigorous is this?

- Is it in-person for ―high-risk‖ people?

• What ―red flags‖ does our system see?

- Last year did we fire anyone for FCPA/anti-bribery issues?

- Last year did we stop doing business with any third party?

- How long does it take for ―compliance issues‖ to be raised to the AC?

- How many reports of potential bribery came to the AC or BOD?

PwC

Questions ?

Sulaksh Shah, Director

FCPA Services PricewaterhouseCoopers

E-mail: [email protected]

Tel: 703-918-4477

© 2011 PwC. All rights reserved. "PwC" refers to PricewaterhouseCoopers LLP, a Delaware limited liability partnership, which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity. This document is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.