Embed Size (px)

Citation preview

ACP Market ReportFourth Quarter 2020

Table of Contents

Fourth Quarter Highlights ........................................................................................................................................................................... 3

U.S. Wind Power Capacity Growth ..................................................................................................................................................... 5 • Quarterly U.S. Wind Power Capacity Installations ................................................................................................................... 6 • U.S. Annual and Cumulative Wind Power Capacity Installations .................................................................................. 7 • Wind Power Capacity Installations in 2020 ................................................................................................................................... 8 • Top Owners of 2020 Wind Power Additions ................................................................................................................................. 9 • Wind Power Capacity Under Construction or in Advanced Development ........................................................... 10 • Operational Wind Power Capacity, by State ................................................................................................................................ 11 • Wind Power Capacity Under Construction and in Advanced Development, by State ................................. 12 • Wind Power Pipeline, by State .............................................................................................................................................................. 13 • Wind Power Pipeline, Top States ........................................................................................................................................................ 14

U.S. Offshore Wind Energy Activity ................................................................................................................................................. 15 • Fourth Quarter Offshore U.S Wind Energy Activity ............................................................................................................... 16

Wind Power Procurement Activity ................................................................................................................................................... 17 • Wind Power Capacity Offtake Status ............................................................................................................................................... 18 • Quarterly Wind Power Purchase Agreements .......................................................................................................................... 19

Wind Turbine Market Trends .................................................................................................................................................................. 20 • Wind Turbine Manufacturer Market .................................................................................................................................................. 21

U.S. Utility Solar and Battery Storage Market ............................................................................................................................... 22 • U.S. Annual and Cumulative Utility Solar Power Capacity Growth ............................................................................ 23 • Operational Utility Solar Power, by State ...................................................................................................................................... 24 • U.S. Annual and Cumulative Utility Battery Storage Capacity Growth .................................................................... 25 • Operational Utility Battery Storage Capacity, by State ........................................................................................................ 26

American Clean Power | ACP Market Report Fourth Quarter 2020 2

Fourth Quarter Highlights

American Clean Power | ACP Market Report Fourth Quarter 2020 3

2020 Wind Project Installations • The U.S. wind industry installed 10,593 MW of new

wind power capacity in the fourth quarter of 2020, the highest quarter on record. In fact, more wind was installed at the end of 2020, then any other year except 2012.

• 2020 was a banner year for the wind industry. Developers commissioned 16,913 MW, representing an 85 percent increase over 2019.

• Project owners commissioned 54 new projects across 20 states in the fourth quarter. Texas led with 2,197 MW installed, followed by Wyoming (895 MW), Oklahoma (866), Iowa (861 MW), and Missouri (786 MW).

• There are now 122,468 MW of operating wind power capacity in the United States, with over 60,000 wind turbines operating across 41 states and two U.S. territories.

Wind Capacity Under Construction and in Advanced Development

• Projects totaling 34,757 MW were under construction (17,302 MW) or in advanced development (17,455 MW) at the end of December.

• Projects totaling 3,334 MW started construction in the fourth quarter and 500 MW entered advanced development.

• There are currently 10 states with over 1,000 MW in the near-term pipeline. Federal waters host 26% of the total development pipeline, followed by Texas (13%), Wyoming (10%), Oklahoma (7%), and Kansas (5%).

Wind Power Procurement Activity • Project developers and power purchasers reported

700 MW of new PPAs in the fourth quarter, bringing PPA activity for the year to 5,444 MW.

• Corporate PPA activity declined this quarter, with only one announcement of 200 MW.

Turbine Technology Trends • GE Renewable Energy led turbine installations in

2020, capturing 53% of the market through December. Vestas ranks second with 35%, followed by Siemens Gamesa Renewable Energy with 10% and Nordex USA with 3%.

• Project owners completed 2,899 MW of partial repowerings in 2020. GE Renewable Energy led this market segment as well, repowering 2,086 MW. Vestas repowered 774 MW and Siemens Gamesa repowered 39 MW in the year.

Fourth Quarter Highlights

American Clean Power | ACP Market Report Fourth Quarter 2020 4

U.S. Wind Power Capacity Growth

American Clean Power | ACP Market Report Fourth Quarter 2020 5

Quarterly U.S. Wind Power Capacity Installations• The U.S. wind industry commissioned 10,593 MW of wind power capacity in the fourth quarter of 2020, the highest quarter on record. • Wind capacity additions were up 94% in the fourth quarter of 2020 compared to the same period last year. This year broke the record for capacity installations.• More wind power was installed in the fourth quarter of 2020 than any other year except for 2012.

U.S. WIND POWER CAPACITY GROWTH

5391,118

1,912

2217 333 520

2,000

406

841

1,821

704

1,050

1,213

0

619

1,661

310 351

626 899

2,554

673

1,207

1,834

70419

1,603

895534 612

1,927 1,934

3,299 3,230

8,382

1,016

3,603

4,998

6,480

4,125

5,9455,465

10,593

0

2000

4000

6000

8000

10000

12000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Chart Title

Q1 Q2 Q3 Q4

12,000

10,000

8,000

6,000

4,000

2,000

0

Win

d P

ower

Cap

acity

(MW

)

American Clean Power | ACP Market Report Fourth Quarter 2020 6

U.S. Annual and Cumulative Wind Power Capacity Growth • Wind power installations set a new highwater mark in 2020 as the industry commissioned 16,913 MW. • There are now 122,468 MW of wind energy operating in the United States, with over 60,000 wind turbines spinning across 41 states and two U.S. territories.

U.S. WIND POWER CAPACITY GROWTH

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Annual Gross Capacity Installations

Annual Gross Capacity Installations

9,046

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

120,000

100,000

80,000

60,000

40,000

20,000

0

40,346

122,468

Cum

ulative Wind P

ower C

apacity (MW

)A

nnua

l Win

d P

ower

Cap

acity

Add

ition

s (M

W)

Annual Gross Capacity Installations Cumulative Capacity

73,891

American Clean Power | ACP Market Report Fourth Quarter 2020 7

Wind Repowers• Project owners partially repowered 31 wind phases in 2020. After repowering these projects now total 2,899 MW.• Partial repowering activity was flat in 2020 compared to 2019, though 130% higher than 2018.• GE Renewable Energy dominated this market, repowering projects totaling 2,086 MW. Vestas followed by repowering 774 MW, including many full nacelle

replacements of legacy Clipper turbines.

U.S. WIND POWER CAPACITY GROWTH

72%

27%

1%

GE Renewable Energy Vestas Siemens Gamesa

7,017 7,5889,137

16,9132,077 1,269

3,008

2,899

0

5,000

10,000

15,000

20,000

25,000

2017 2018 2019 2020

New Installs Repowered Capacity

Cap

acity

(MW

)

NEW INSTALLS AND PARTIAL REPOWERING WIND REPOWERINGS, BY OEM

American Clean Power | ACP Market Report Fourth Quarter 2020 8

Wind Power Capacity Installations in 2020U.S. WIND POWER CAPACITY GROWTH

• Developers installed 54 new wind projects, totaling 10,593 across 20 states during the fourth quarter of 2020. • Texas led with 2,197 MW installed, followed by Wyoming (895 MW), Oklahoma (866), Iowa (861 MW), and Missouri (786 MW). • Year-to-date the industry has added 90 projects across 26 states totaling 16,913 MW. Texas leads installations for the year (4,235 MW), followed by Iowa

(1,498 MW) and Wyoming (1,123 MW).

RICT

MA

HI28

ALMS

AR

LA

GA

KYVA

NC

SC

FL

NV

AZ350

DEMD

NH

NJ

TN

UT

VT

PR

AK

MO1,028

IL1,059

IN651

WI MI493

NY

IA1,498

MN455

KS896

ND343

CA111

CO910

ID

NE393

NM770

SD774

OH126

OK866

PA

TX4,235

OR310

WA287

WY1,123

GU

■ 1 to 100MW ■ >100 MW to 250MW ■ 250MW to 500MW ■ >500MW to 1,000MW ■ >1,000MW

Federal Waters

ME73MT

80

WV56

American Clean Power | ACP Market Report Fourth Quarter 2020 9

Top Owners of 2020 Wind Power Additions• Three companies added more than 5,540 MW to their portfolios this year—NextEra, Xcel Energy, and Berkshire Hathaway Energy. NextEra leads the group

after bringing online 13 wind projects totaling 2,898 MW. • Xcel delivered five projects this year, including New Mexico’s largest wind farm to date, the 522 MW Sagamore Wind project and the second largest single

phase wind project, Cheyenne Ridge (496 MW). • Berkshire Hathaway brought nine projects online in 2020, eight of which came online in the fourth quarter with a combined capacity of 1,162 MW. • The top ten owners of 2020 represent 62% of the wind power capacity brought online.

U.S. WIND POWER CAPACITY GROWTH

NextEra Energy2,898

Xcel Energy1,420

Berkshire Hathaway Energy1,223

ENGIE1,108

RWE Renewables

720

Alliant Energy684

Orsted Wind Power

676

Liberty Power

597

Global Infrastructure

Partners569

ALLETE513

Rest of Owners6,505

Chart TitleNextEra Energy Xcel Energy Berkshire Hathaway Energy ENGIE

RWE Renewables Alliant Energy Orsted Wind Power Liberty Power

Global Infrastructure Partners ALLETE Rest of Owners

NextEra Energy2,898

Xcel Energy1,420

Berkshire Hathaway Energy1,223

ENGIE1,108

RWE Renewables

720

Alliant Energy684

Orsted Wind Power

676

Liberty Power

597

Global Infrastructure

Partners569

ALLETE513

Rest of Owners6,505

Chart TitleNextEra Energy Xcel Energy Berkshire Hathaway Energy ENGIE

RWE Renewables Alliant Energy Orsted Wind Power Liberty Power

Global Infrastructure Partners ALLETE Rest of Owners

American Clean Power | ACP Market Report Fourth Quarter 2020 10

RI 75CT 5

MA 120

HI233

ALMS

AR

LA

GA

KYVA

NC 208

SC

FL

NV152

AZ618

DE 2MD 191

NH 214

NJ 9

TN 29

UT391

VT149

PR 125

AK64

MO1,987

IL6,409

IN2,968

WI746 MI

2,681

NY1,987

IA11,660

MN4,299

KS7,016

ND3,989

CA5,922

CO4,692

ID973

NE2,531

NM2,723

SD2,305

OH864

OK9,048

PA1,459

TX33,133

OR3,737

WA3,395

WY2,738

■ 1 to 500MW ■ >500MW to 1,000MW ■ >1,000MW to 2,500MW ■ >2,500MW to 5,000MW ■ >5,000MW to 10,000MW ■ >10,000MW

Federal Waters

ME996MT

880

WV742

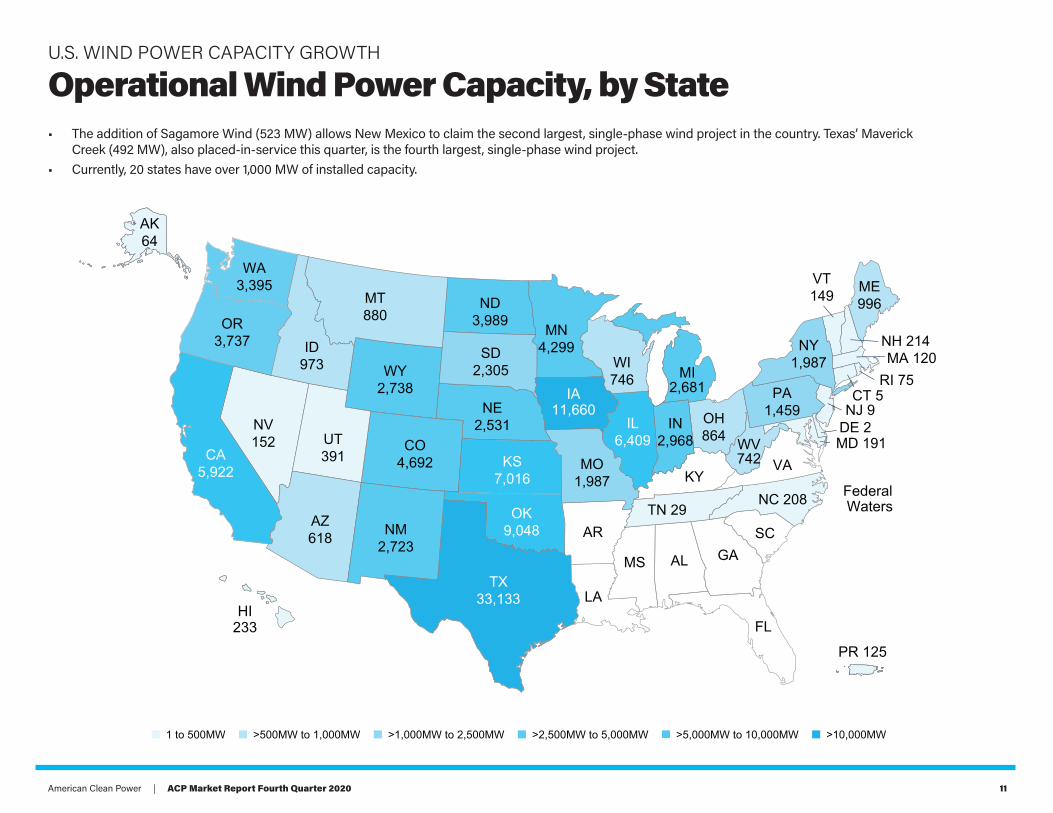

Operational Wind Power Capacity, by StateU.S. WIND POWER CAPACITY GROWTH

• The addition of Sagamore Wind (523 MW) allows New Mexico to claim the second largest, single-phase wind project in the country. Texas’ Maverick Creek (492 MW), also placed-in-service this quarter, is the fourth largest, single-phase wind project.

• Currently, 20 states have over 1,000 MW of installed capacity.

American Clean Power | ACP Market Report Fourth Quarter 2020 11

Wind Power Capacity Under Construction or in Advanced Development

U.S. WIND POWER CAPACITY GROWTH

• At the end of December 2020, there were 34,757 MW of wind power capacity in the near-term pipeline, including 17,302 MW under construction and 17,445 MW in advanced development. Total pipeline activity decreased by 20% from the previous quarter due to the record level of commissioning in 2020.

• Despite continued disruptions from COVID-19, project developers announced 3,834 in combined new development activity in the fourth quarter of 2020, with projects totaling 3,334 MW starting construction and an additional 500 MW entering advanced development.

• Developers continue to report challenges raising tax equity for projects in development. Tax equity supply is reported to be tight, due to economic uncertainty, tighter lending standards, and more limited capital allocations.

15,231

18,279

23,28021,344

23,97725,819

29,634 28,731

33,512

37,857 38,056

35,000

39,086

41,775

46,728

44,136 44,94243,628 43,575

34,757

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q 2017 2Q 2017 3Q 2017 4Q 2017 1Q 2018 2Q 2018 3Q 2018 4Q 2018 1Q 2019 2Q 2019 3Q 2019 4Q 2019 1Q 2020 2Q 2020 3Q 2020 4Q 2020

Grand Total Under Construction Advanced Development

Win

d P

ower

Cap

acity

(MW

)

WIND POWER PIPELINE OVER TIME

American Clean Power | ACP Market Report Fourth Quarter 2020 12

Wind Power Pipeline, by StateU.S. WIND POWER CAPACITY GROWTH

RICT

MA

HI

ALMS

180

LA

GA

KY

VA77

NC

SC

FL

NV

AZ

DEMD

NH

NJ

TN

UT

VT

PR

AK

MO448

IL1,175

IN500

WI MI775

NY1,650

IA433

MN1,100

KS1,672

ND299

CA421

CO455

ID

NE1,111

NM1,656

SD1,101

OH511

OK2,590

PA

TX4,756

OR241

WA600

WY3,551

■ 1 to 250MW ■ >250MW to 500MW ■ >500 MW to 1,000MW ■ >1,000 MW to 2,000MW ■ >2,000MW

FederalWaters9,079

ME27MT

240

WV110

American Clean Power | ACP Market Report Fourth Quarter 2020 13

3,991

3,496

3,000

2,640 2,623

Invenergy Orsted WindPower

PowerCompany of

Wyoming

Dominion Apex CleanEnergy

Capacity (MW)

Wind Power Pipeline, Top StatesU.S. WIND POWER CAPACITY GROWTH

• The 34,757 MW of combined construction and advanced development activity is spread across 177 project phases in 26 states and 15 project phases in federal waters. • Federal waters host 9,079 MW of total development activity, representing 26% of the total development pipeline. • Texas hosts more activity than any other state with 13% of the pipeline, followed by Wyoming (10%), Oklahoma (7%), Kansas (5%), and New Mexico (4%). • A total of 14 states have over 1,000 MW of wind capacity in the pipeline. • Invenergy is currently the top developer of projects under construction or in advanced development, followed by Orsted and Power Company of Wyoming.

3,406

3,551

2,590

729

556

207

212

911

773

9,079

1,350

943

1,100

1,443

963

200

328

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

Federal Waters

Texas

Wyoming

Oklahoma

Kansas

New Mexico

New York

Illinois

Nebraska

South Dakota

Under Construction Advanced Development

TOP DEVELOPERS OF NEAR-TERM WIND PIPELINE TOP STATES

Wind Power Capacity (MW)

3,406

3,551

2,590

729

556

207

212

911

773

9,079

1,350

943

1,100

1,443

963

200

328

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

Federal Waters

Texas

Wyoming

Oklahoma

Kansas

New Mexico

New York

Illinois

Nebraska

South Dakota

Under Construction Advanced Development

American Clean Power | ACP Market Report Fourth Quarter 2020 14

U.S. Offshore Wind Energy ActivityOffshore Wind Updates

American Clean Power | ACP Market Report Fourth Quarter 2020 15

Fourth Quarter U.S. Offshore Wind Energy ActivityU.S. OFFSHORE WIND ENERGY ACTIVITY

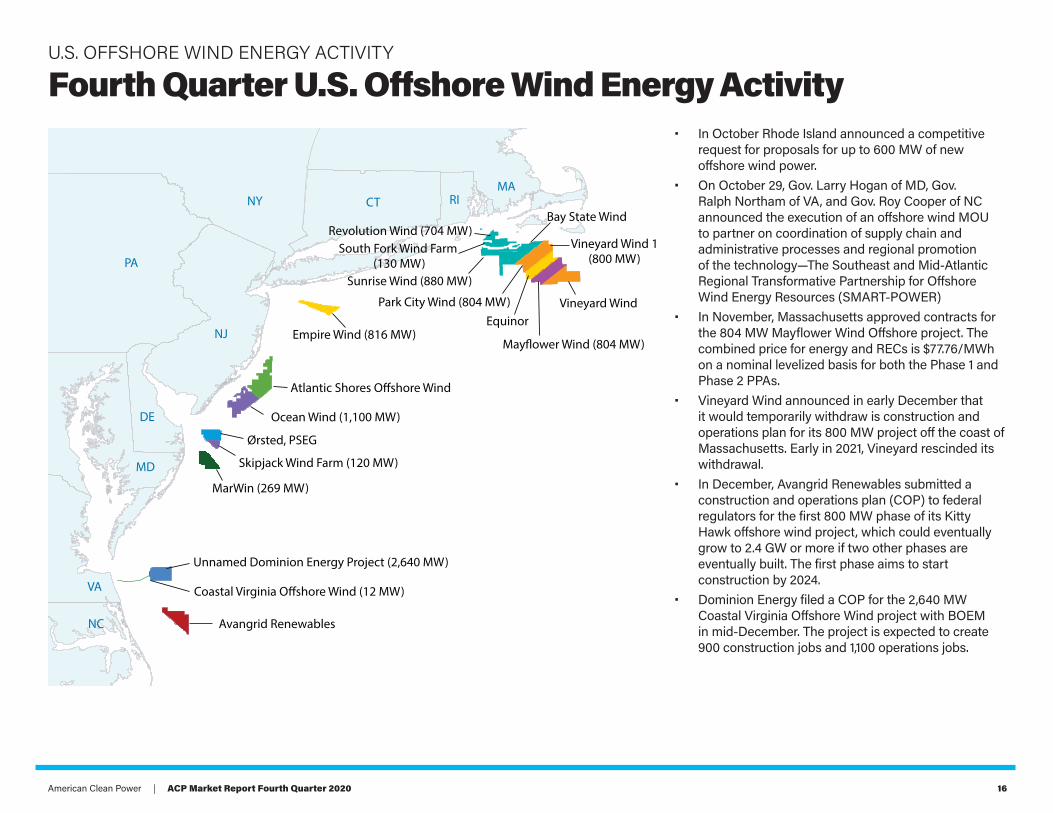

• In October Rhode Island announced a competitive request for proposals for up to 600 MW of new offshore wind power.

• On October 29, Gov. Larry Hogan of MD, Gov. Ralph Northam of VA, and Gov. Roy Cooper of NC announced the execution of an offshore wind MOU to partner on coordination of supply chain and administrative processes and regional promotion of the technology—The Southeast and Mid-Atlantic Regional Transformative Partnership for Offshore Wind Energy Resources (SMART-POWER)

• In November, Massachusetts approved contracts for the 804 MW Mayflower Wind Offshore project. The combined price for energy and RECs is $77.76/MWh on a nominal levelized basis for both the Phase 1 and Phase 2 PPAs.

• Vineyard Wind announced in early December that it would temporarily withdraw is construction and operations plan for its 800 MW project off the coast of Massachusetts. Early in 2021, Vineyard rescinded its withdrawal.

• In December, Avangrid Renewables submitted a construction and operations plan (COP) to federal regulators for the first 800 MW phase of its Kitty Hawk offshore wind project, which could eventually grow to 2.4 GW or more if two other phases are eventually built. The first phase aims to start construction by 2024.

• Dominion Energy filed a COP for the 2,640 MW Coastal Virginia Offshore Wind project with BOEM in mid-December. The project is expected to create 900 construction jobs and 1,100 operations jobs.

NY

PA

NJ

VA

NC

MD

MACT

DE

RI

Atlantic Shores O�shore Wind

Ørsted, PSEG

Ocean Wind (1,100 MW)

Vineyard Wind 1(800 MW)

Bay State Wind

Empire Wind (816 MW)

Skipjack Wind Farm (120 MW)

Unnamed Dominion Energy Project (2,640 MW)

Sunrise Wind (880 MW)

MarWin (269 MW)

Avangrid Renewables

Coastal Virginia O�shore Wind (12 MW)

Revolution Wind (704 MW)

May�ower Wind (804 MW)

Equinor

South Fork Wind Farm (130 MW)

Vineyard WindPark City Wind (804 MW)

American Clean Power | ACP Market Report Fourth Quarter 2020 16

Wind Power Procurement Activity

American Clean Power | ACP Market Report Fourth Quarter 2020 17

Wind Power Offtake StatusWIND POWER PROCUREMENT ACTIVITY

• Long-term PPAs remain the most popular offtake mechanism for wind energy, accounting for 55% of new wind power capacity commissioned in the fourth quarter.

• Direct utility ownership of wind power continues to grow, as four utilities commissioned 4,918 MW in 2020. Dominion and AEP lead these direct ownership additions.

• Hedge contracts account for 8% of capacity installed year-to-date, tied to projects in Illinois, Kansas, and Texas. • Over 16 GW of projects underway have a PPA in place, representing just over half of the current pipeline. Utility ownership accounts for 22% of capacity underway,

while merchant hedge and merchant activity represent 2%. The 25% balance have not yet reported an offtake structure. • Utility purchasers (through direct ownership and PPAs) currently account for 70% of capacity under construction or in advanced development. Dominion Energy

leads utilities with over 2,652 MW underway, followed AEP and Eversource Energy.

UTILITYDIRECT

OWNERSHIP (MW)LONG-TERM

CONTRACT (MW)TOTAL

Dominion 2,652 2,652

AEP 1,484 1,484

Eversource Energy 1,245 1,245

Xcel Energy 728 453 1,181

National Grid 1,037 1,037

Top Utilities by Near-Term Wind Project Pipeline

0%

20%

40%

60%

80%

100%

Online 2020 Under construction or advanced development

Power Purchase Agreement Direct Utility Ownership Hedge Contract Merchant Unknown

0%

20%

40%

60%

80%

100%

Online 2020 Under construction or advanced development

Power Purchase Agreement Direct Utility Ownership Hedge Contract Merchant Unknown

8,830 MW

25%

7,480 MW

22%

1,284 MW

8%

885 MW 5%

4,918 MW

29%

9,296 MW

55%

530 MW 3%

647 MW 2%

16,916 MW

49%

805 MW 2%

0%

20%

40%

60%

80%

100%

Online 2020 Under construction or advanced development

Power Purchase Agreement Direct Utility Ownership Hedge Contract Merchant Unknown

American Clean Power | ACP Market Report Fourth Quarter 2020 18

Wind Power Purchase AgreementsWIND POWER PROCUREMENT ACTIVITY

• PPA announcements this quarter continued to be down noticeably from quarterly levels throughout 2018 and 2019, partially due to uncertainty caused by COVID-19. • Project developers and power purchasers announced 700 MW of new PPAs in the fourth quarter, bringing PPA activity for the year to 5,444 MW. • McDonalds Corporation was the only corporation to announce a PPA from October to December. The burger chain signed a PPA for 200 MW from Caddo Wind Farm. • In a reversal from the third quarter utility PPA activity picked up again—two utilities announced wind power contracts totaling 450 MW.

0

500

1000

1500

2000

2500

3000

2013 2013 2013 2013 2014 2014 2014 2014 2015 2015 2015 2015 2016 2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019 2019 2019 2020 2020 2020 2020

Utility PPA Corporate or Other Non-Utility PPA Undisclosed Purchaser Column1

0

500

1000

1500

2000

2500

3000

2013 2013 2013 2013 2014 2014 2014 2014 2015 2015 2015 2015 2016 2016 2016 2016 2017 2017 2017 2017 2018 2018 2018 2018 2019 2019 2019 2019 2020 2020 2020 2020

Utility PPA Corporate or Other Non-Utility PPA Undisclosed Purchaser Column1

American Clean Power | ACP Market Report Fourth Quarter 2020 19

Wind Turbine Market Trends

American Clean Power | ACP Market Report Fourth Quarter 2020 20

8,777

5,803

1,680

451

202

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

GE

Vestas

SGRE

Nordex

Goldwind

Project Capacity (MW)

8,777

5,803

1,680

451

202

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

GE

Vestas

SGRE

Nordex

Goldwind

Project Capacity (MW)

(1%)

(3%)

(10%)

(53%)

(35%)

Wind Turbine Manufacturer MarketWIND TURBINE MARKET TRENDS

2020 Installations• GE Renewable Energy (GE) led 2020 wind power capacity installations,

capturing 53% of new turbine capacity.

• Vestas ranked second with 35% of installations, followed by Siemens Gamesa Renewable Energy (SGRE) with 10%. Nordex USA represented the remaining 3%.

• On a capacity basis, the majority (71%) of turbines installed in the year are rated between 2 MW to less than 3 MW, while 28%are rated over 3 MW. There are now thirteen projects utilizing 4 MW class turbines totaling 2,229 MW operating in the U.S.

• GE’s 2.82-127 model was the most popular turbine installed this year, accounting for 28% of capacity additions, followed by Vestas’ V120-2.2 andthe GE 2.5-127.

Construction and Advanced Development• For land-based wind projects, GE and Vestas account for 82% of projects

under construction and in advanced development that have reported an OEM. GE currently represents 49% of this market, Vestas represents 33%, and Nordex captures 13%.

• Considering offshore wind projects, SGRE is supplying 68% of projects where an OEM has been reported. GE increased its market share in the fourth quarter capturing 32% of the market.

• Approximately 34% of all projects under construction or in advanced development have not yet reported a turbine manufacturer to ACP.

2020 CAPACITY INSTALLATIONS, BY OEM NEAR-TERM PIPELINE CAPACITY, BY OEM

8,073

5,334

9082,067

9,263

2,020

4,366

2,726

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

GE Vestas SGRE Nordex Undisclosed

Land-Based Wind Offshore Wind

Win

d P

ower

Cap

acity

(MW

)

8,073

5,334

9082,067

9,263

2,020

4,366

2,726

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

GE Vestas SGRE Nordex Undisclosed

Land-Based Wind Offshore Wind

American Clean Power | ACP Market Report Fourth Quarter 2020 21

U.S. Utility Solar and Battery Storage Market

American Clean Power | ACP Market Report Fourth Quarter 2020 22

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DITI

ON

S (M

W)

U.S. UTILITY SOLAR AND STORAGE MARKET

U.S. Annual and Cumulative Utility Solar Power Capacity• Wind, solar, and energy storage set annual capacity addition records in 2020. Utility solar additions more than doubled from 2019 as the industry installed 11,158 MW.

This marks a 37% improvement on the previous record set in 2016.• There are now 47,318 MW of operating utility solar power capacity in the country. Cumulative capacity grew 31% year-over-year.• Operating utility solar projects can power the equivalent of 11 million American homes.

Source: ACP, EIA

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DITI

ON

S (M

W)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DITI

ON

S (M

W)

Annual Gross Capacity Installations Cumulative Capacity

American Clean Power | ACP Market Report Fourth Quarter 2020 23

Operational Utility Solar Power, by StateU.S. UTILITY SOLAR AND STORAGE MARKET

• Forty-seven states and D.C. have operational utility solar power capacity. California leads the solar market with over 13 GW of installed capacity, more than double second placed Texas.

• Nearly 30% of installed utility solar power is in California, followed by Texas (11%), North Carolina (11%), Florida (8%), and Nevada (5%).• In 2020, Texas led solar power additions with 2,852 MW installed. California was in second with 1,726 MW and Florida rounded out the podium with 1,714 MW installed.

Source: ACP, EIA

State Prior-2020 Capacity (MW) 2020 Additions (MW) Total Capacity (MW)

Texas 2,454 2,852 5,306California 11,504 1,726 13,230Florida 2,150 1,714 3,864Virginia 646 844 1,489Georgia 1,470 664 2,134North Carolina 4,567 457 5,024South Carolina 663 400 1,063Arizona 1,846 293 2,138Utah 917 279 1,196Oregon 401 185 585Remaining States 9,543 1,745 11,289

Total 36,160 11,158 47,318

American Clean Power | ACP Market Report Fourth Quarter 2020 24

U.S. Annual and Cumulative Utility Battery Storage Capacity U.S. UTILITY SOLAR AND STORAGE MARKET

• In 2020 battery energy storage broke annual capacity records. Utility battery storage increased over 300% from 2019 as the industry installed 734 MW. • There are now 1,756 MW of operating utility battery energy storage capacity in the U.S. Cumulative capacity grew 72% year-over-year.

Source: ACP, EIA

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DIT

ION

S (M

W)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DITI

ON

S (M

W)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CU

MU

LATI

VE C

APAC

ITY

(MW

)

ANN

UAL

CAP

ACIT

Y AD

DITI

ON

S (M

W)

American Clean Power | ACP Market Report Fourth Quarter 2020 25

Operational Utility Battery Storage, by StateU.S. UTILITY SOLAR AND STORAGE MARKET

• Thirty-four states have operational utility battery storage capacity. California hosts the most battery storage with 876 MW of installed capacity, followed by Texas (134 MW), Illinois (133 MW), Massachusetts (81 MW) and Hawaii (63 MW)

• In 2020, California installed the most battery storage additions, bringing online 621 MW. Massachusetts came in second with 48 MW, with Texas coming in third with 20 MW.

• Ten states installed utility-scale battery storage facilities in 2020, with six of those states installing 10 MW or more.

Source: ACP, EIA

State Prior-2020 Capacity (MW) 2020 Additions (MW) Total Capacity (MW)

California 255 621 876Massachusetts 33 48 81Texas 114 20 134New York 33 12 45Indiana 28 10 38Oklahoma 0 10 10North Carolina 1 9 10Georgia 1 1 2Colorado 11 1 12Washington 6 1 7Remaining States 541 0 541

Total 1,022 734 1,756

American Clean Power | ACP Market Report Fourth Quarter 2020 26

American Clean Power is the voice of companies from across the clean power sector that are

powering America’s future, providing cost-effective solutions to the climate crisis while creating

jobs, spurring massive investment in the U.S. economy and driving high-tech innovation across

the nation. We are uniting the power of America’s renewable energy industry to advance our

shared goals and to transform the U.S. power grid to a low-cost, reliable, and renewable power

system. Learn more about the benefits clean power brings to America at www.cleanpower.org.

Twitter / @USCleanPower

LinkedIn / American Clean Power Association