Embed Size (px)

Citation preview

Acquisition Fair Value Allocations: Additional Issues, SFAS No. 141R

Intangibles Current and noncurrent assets

that lack physical substance. Do not include financial

instruments. When should an Intangible

be recognized? Does it arise from contractual

or other legal rights? Can it be sold or otherwise

separated from the acquired enterprise?

Intangibles Current and noncurrent assets

that lack physical substance. Do not include financial

instruments. When should an Intangible

be recognized? Does it arise from contractual

or other legal rights? Can it be sold or otherwise

separated from the acquired enterprise?

2-1

Acquisition Fair Value Allocations: Additional Issues, SFAS No. 141R

Intangible Asset Examples

Customer Base Brand Names Trademarks Customer Routes Royalty agreements Internet domain names Rights (broadcasting,

development, use, etc.)

Customer Base Brand Names Trademarks Customer Routes Royalty agreements Internet domain names Rights (broadcasting,

development, use, etc.)

Databases Technological know-

how Patents & Copyrights Franchise agreements Noncompetition

agreements Many, many, more

Databases Technological know-

how Patents & Copyrights Franchise agreements Noncompetition

agreements Many, many, more

Exh.2-7

2-2

Acquisition Fair Value Allocations: Additional Issues, SFAS No. 141R

In-Process R&D Should be recognized at

acquisition date as an ASSET.

Determination of fair value is critical.

Subsequent to acquisition, the IPR&D assets are tested for impairment at least annually.

In-Process R&D Should be recognized at

acquisition date as an ASSET.

Determination of fair value is critical.

Subsequent to acquisition, the IPR&D assets are tested for impairment at least annually.

2-3

Unconsolidated Subsidiaries

SFAS No . 94

W hen control does notactually rest w ith the 50% ow ners,

e.g., bankruptcy, substantive m inority rights, etc.

W hen can a Parent exclude a 50%ow ned subsidiary from consolidation?

2-4

LEGACY ACCOUNTING METHODS FOR BUSINESS COMBINATIONS

Prior to the SFAS 141R acquisition method (effective 2009), the FASB required either the

Purchase method (GAAP through 2008, SFAS 141)

Pooling of interests method (GAAP through 6/30/02, APB 16)

Purchase Method Situations:GAAP for new combinations through 2008

Dissolution of the acquired company:Purchase Price = Fair

Value

Purchase Price > FV

Purchase Price < FVSeparate

incorporation maintained.

Dissolution of the acquired company:Purchase Price = Fair

Value

Purchase Price > FV

Purchase Price < FVSeparate

incorporation maintained.

2-6

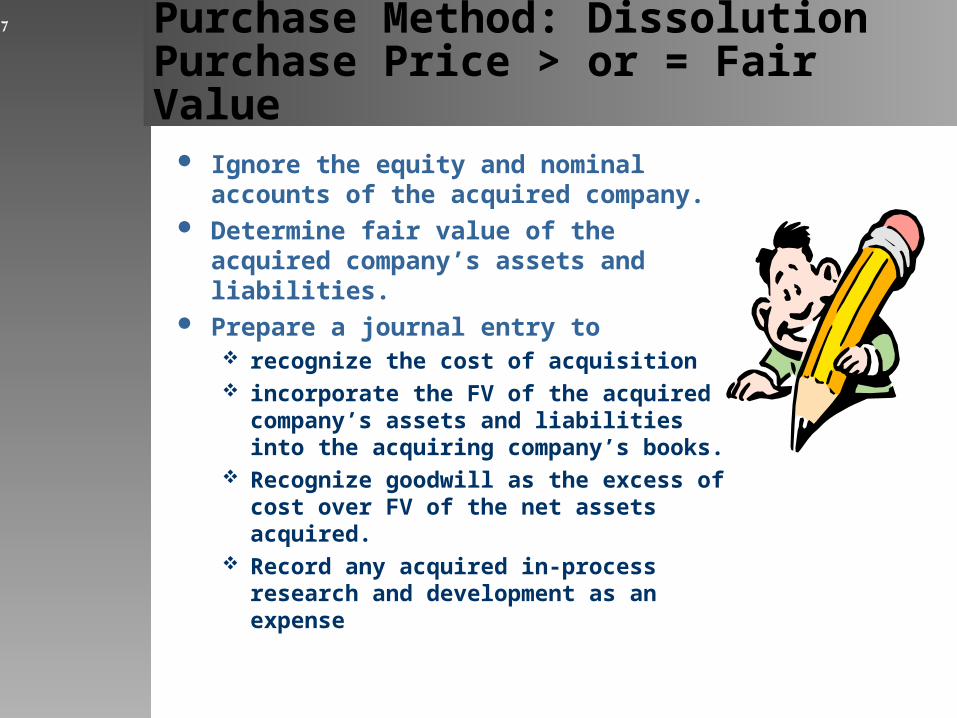

Purchase Method: DissolutionPurchase Price > or = Fair Value

Ignore the equity and nominal accounts of the acquired company.

Determine fair value of the acquired company’s assets and liabilities.

Prepare a journal entry to recognize the cost of acquisition incorporate the FV of the acquired

company’s assets and liabilities into the acquiring company’s books.

Recognize goodwill as the excess of cost over FV of the net assets acquired.

Record any acquired in-process research and development as an expense

2-7

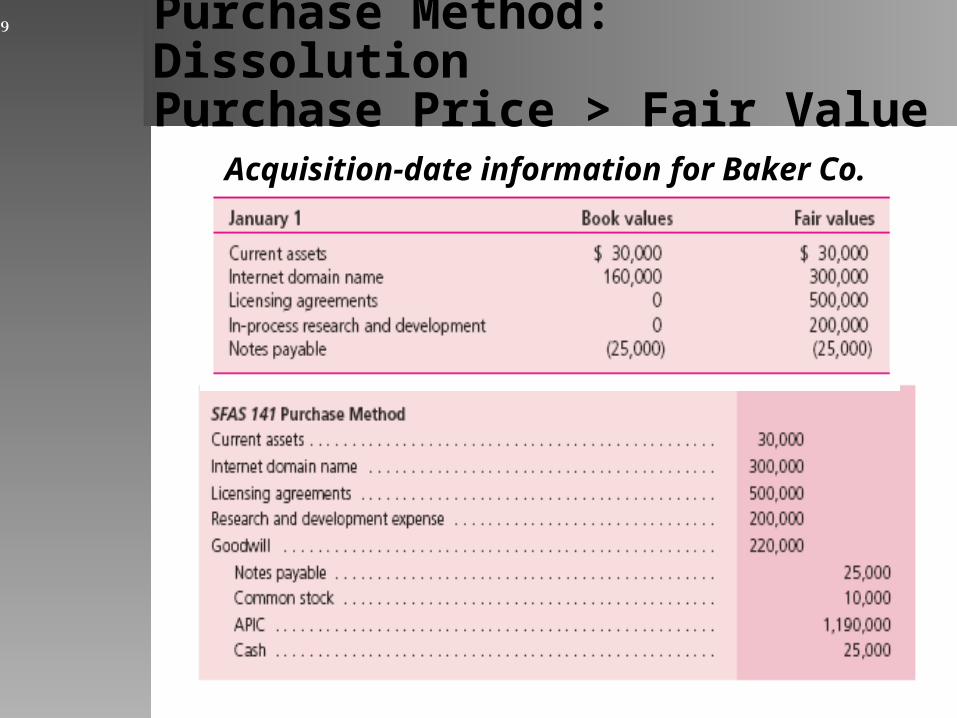

Purchase Method: DissolutionPurchase Price > Fair Value

Archer agrees to pay $1,200,000 (10,000 unissued shares of its $1 par value common stock that is currently selling for $120 per share) for all of Baker’s assets and liabilities. Archer also paid $25,000 cash for legal and accounting fees directly related to the acquisition.

Baker then dissolves itself as a legal entity. Under the purchase method both the fair value of the stock issued and the direct acquisition costs are included in the cost-based valuation of the combination.

2-8

Purchase Method: DissolutionPurchase Price > Fair Value

2-9

Acquisition-date information for Baker Co.

Purchase Method: DissolutionPurchase Price < Fair Value

When fair value exceeds cost, full allocation of fair value is not possible.

Current assets and liabilities should be consolidated at their fair value.

Non-current assets should be proportionately reduced in value (with some exceptions)

2-10

Purchase Method - DissolutionPurchase Price < Fair Value

According to SFAS 141, the following non-current assets are exceptions to the proportionate reduction, and should be recorded at assessed fair values:

Financial assets other than equity method investments

Assets to be disposed of by sale Deferred tax assets Prepaid assets related to pension or other post-

retirement benefit plans

2-11

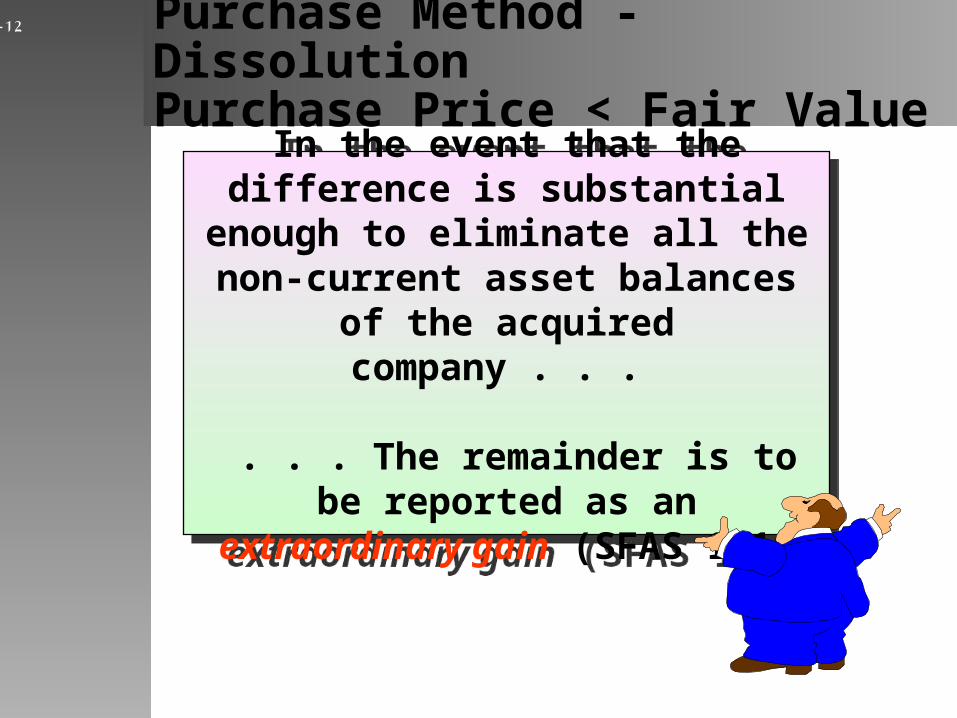

Purchase Method - DissolutionPurchase Price < Fair Value

In the event that the difference is substantial enough to eliminate all the non-current asset balances of

the acquired company . . .

. . . The remainder is to be reported as an extraordinary gain

(SFAS 141)

In the event that the difference is substantial enough to eliminate all the non-current asset balances of

the acquired company . . .

. . . The remainder is to be reported as an extraordinary gain

(SFAS 141)

2-12

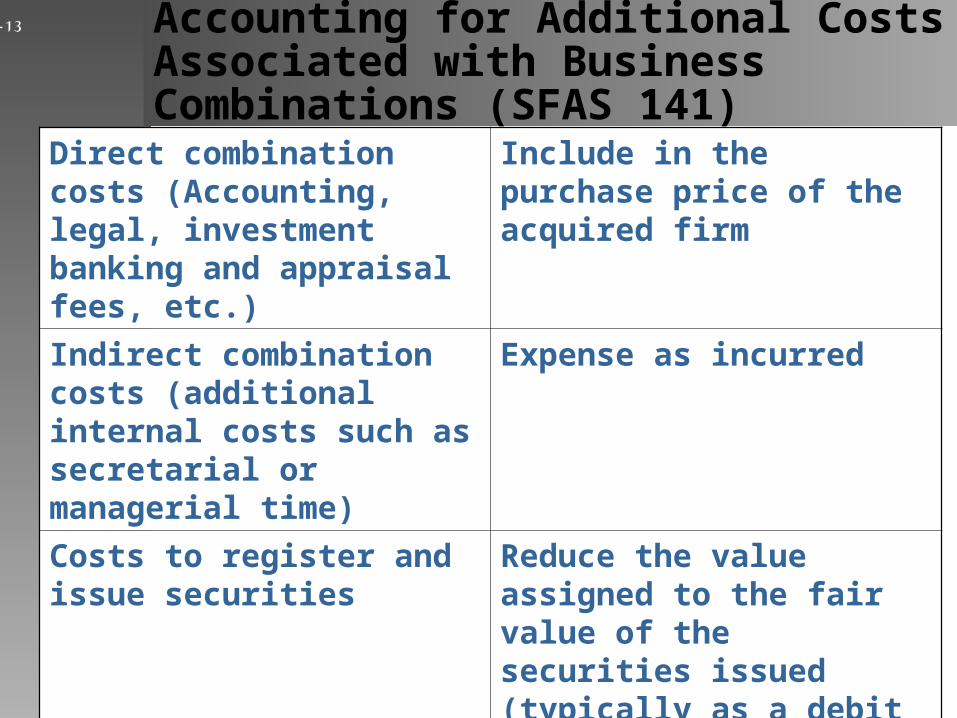

Accounting for Additional Costs Associated with Business Combinations (SFAS 141)

Direct combination costs (Accounting, legal, investment banking and appraisal fees, etc.)

Include in the purchase price of the acquired firm

Indirect combination costs (additional internal costs such as secretarial or managerial time)

Expense as incurred

Costs to register and issue securities

Reduce the value assigned to the fair value of the securities issued (typically as a debit to APIC)

2-13

Pooling of Interests

Historically, many business combinations were

accounted for as “Pooling of Interests.”

In SFAS 141R, “Business Combinations”, the FASB

stated that all business combinations should be accounted for using the “Acquisition MethodAcquisition Method”.

Historically, many business combinations were

accounted for as “Pooling of Interests.”

In SFAS 141R, “Business Combinations”, the FASB

stated that all business combinations should be accounted for using the “Acquisition MethodAcquisition Method”.

2-14

Pooling of Interests

According to SFAS No. 141R, the acquisition method is not to be retrospectively applied to past “Poolings of Interest.”

Past poolings of interests are left intact by SFAS No. 141R.

Therefore, it is important to understand how to account

for PAST poolings.

According to SFAS No. 141R, the acquisition method is not to be retrospectively applied to past “Poolings of Interest.”

Past poolings of interests are left intact by SFAS No. 141R.

Therefore, it is important to understand how to account

for PAST poolings.

2-15

In a pooling, one company obtained

essentially “all” of the other company’s

stock.

In a pooling, one company obtained

essentially “all” of the other company’s

stock.

The transaction involved the

exchange of common stock. No exchange of cash was allowed.

The transaction involved the

exchange of common stock. No exchange of cash was allowed.

The ownership interests of two, or more, companies were combined into one new company.

No single company was dominant.

There was a continuity of previous ownership interests, not a purchase/sale.

To use pooling of interests, 12 strict criteria had to be met.

Historical Review of Pooling of Interests

2-16

Historical Review of Pooling of Interests

The Book Values of the two combining companies were

joined. No Goodwill was recorded. Internally developed intangibles developed by the

sub were typically not recognized.

The Book Values of the two combining companies were

joined. No Goodwill was recorded. Internally developed intangibles developed by the

sub were typically not recognized.

Revenues and expenses were combined retroactively for the

two companies.

Revenues and expenses were combined retroactively for the

two companies.

2-17

Historical Review of Pooling of Interests

Because poolings involved exchanges of voting stock, a continuity of ownership was deemed to exist.

Neither Goodwill nor any unrecorded intangibles were recorded.

Both companies were combined at BV.

The pooling method was often criticized for it’s lack of completeness, comparability to other methods, and relevance for decision makers.

Because poolings involved exchanges of voting stock, a continuity of ownership was deemed to exist.

Neither Goodwill nor any unrecorded intangibles were recorded.

Both companies were combined at BV.

The pooling method was often criticized for it’s lack of completeness, comparability to other methods, and relevance for decision makers.

2-18

Historical Review of Pooling of Interests

Prior Period Adjustments were made to account for differences in the ways the two companies accounted for income.

A journal entry was recorded to recognize either an Investment in Subsidiary (sub not dissolved) or the individually acquired assets and liabilities (if the sub was dissolved).

Prior Period Adjustments were made to account for differences in the ways the two companies accounted for income.

A journal entry was recorded to recognize either an Investment in Subsidiary (sub not dissolved) or the individually acquired assets and liabilities (if the sub was dissolved).

2-19

Accounting for Pooling of Interests in Subsequent Periods: Dissolution

The Investment in Sub account must be eliminated against the Sub’s Equity accounts

Add together the BV’s of the remaining accounts.

No excess amortization is applicable, because no acquisition-date write-ups occurred.

2-20

Summary

Consolidation of financial information is required when one organization gains control of another.

If dissolution occurs, this consolidation is carried out at the date of acquisition and a single set of accounting records is maintained.

If separate identities are maintained, consolidation is a periodic “worksheet” process not involving journal entries. Separate accounting records are maintained.

The acquisition method is GAAP beginning in 2009.

Legacy effects for the purchase method (for combinations occurring through 2008) and the pooling method (through 6/30/2002) remain in subsequent year’s financial reports.

2-21

![ACCOUNTING FOR BUSINESS COMBINATIONSecon.ucsb.edu/~harmon/password2/Ch 2 Jeter5e.pdf · 46 Chapter 2 Accounting for Business Combinations SFAS No. 141R[topic 805] also broadens the](https://img.pdfslide.net/doc/110x75/5b433d607f8b9a80388bd5f6/accounting-for-business-harmonpassword2ch-2-jeter5epdf-46-chapter-2-accounting.jpg)