Embed Size (px)

Citation preview

Dear Student:

Here is your chance to become a licensed tax professional and earn extra income!

You are now a step closer to becoming a licensed tax preparer. Please browse the fol-lowing course pages; it will give you a taste of our latest 60hr comprehensive self-study correspondence course.

Don’t be fooled by ultra-low pricing on tax courses offered by competitors, they usually have hidden fees. Our school doesn’t simply give you printed IRS publications to study, we provide you with complete and comprehensive study materials written for serious tax students.

With our course, you will gain comprehensive practice (using real scenarios) as you com-plete the quizzes throughout the course. Remember that you can e-mail the instructor any question you may have during your study period.

After completing the course, we will provide you with all of the information needed to register as a tax preparer in the State of California. We will also guide you through the CTEC application process.

If you have any questions, please call our office at (818) 505-3537 or e-mail us at [email protected].

Act Now! Become a Tax Professional and Earn The Extra Income You Deserve!

I Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Federal Introduction 1Getting and Staying Organized 3Itemized deductions 4Setting up a recordkeeping system 5Additional Study Material 6Big Picture 13

Chapter 1: General Material 14What Is a Tax Preparer and What Is His Role 14Who Should File a Return 15Filing Requirements for Most Taxpayers 15Dependent Filing Requirements 17Which Form Should be Used 17When Taxes Must be Filed 21Where to File 21How to File 21Social Security Number (SSN) 22Married Filing Joint, if taxpayers on December 31: 24Married Filing Separately, if on December 31: 24Head of Household, if taxpayer on December 31: 25Qualifying Widow(er) With Dependent Child, if taxpayer: 25Paid Preparer’s Signature 32

Chapter 2: Standard Deduction and Exemp-tions 35Standard Deduction 35Standard Deduction Amount 36Decedent’s final return 36Higher Standard Deduction for Age (65 or Older) 36Higher Standard Deduction for Blindness 36Spouse 65 or Older or Blind 37Exemptions 39Dependent Exemptions 40Joint Return Test 41Citizen or Resident Test 41Relationship Test 41Age Test 42Residency Test 42Support Test (To Be a Qualifying Child) 44Special Test for Qualifying Child of More Than One Person 44Gross Income Test 50Total Support 51Decedents 53Survivors 54Tax Withholding 55Tips 57Taxable Fringe Benefits 57Sick Pay 57Pensions and Annuities 57Gambling Winnings 58Unemployment Compensation 58Federal Payments 59Backup Withholding 59

Estimated Tax 59When to Pay Estimated Taxes 60Return Assembly and Processing 61

Chapter 3: Income 63Gross Income 63Wages and Other Compensation 63Income of a Child 64Scholarship and Fellowships 64Employer Provided Educational Assistance Program 64Sick Pay 65Employer Paid Disability Insurance Premiums 65Employer Provided Meals and Lodging 66Cafeteria Plans 66Employer Provided Group Term Life Insurance 66Fringe Benefits 66Tips 68Interest 70Dividends 70Capital Gains and Losses 70State Tax Refunds 70Alimony 71Child Support 72Business Income 72Income from Rents, Royalties, Partnerships, Estates, and Trust 72Unemployment Compensation 73Clergy 74Community Property Issues 74Bartering 76

Chapter 4: Interest and Dividend Income 80Interest Income 80Constructive Receipt 80Form 1099-INT 82Taxable/Nontaxable 83Dividends That Are Interest 83Gifts for Opening Accounts 83Treasury Bills 84Savings Bonds 84Education Savings Bond Program 85Original Issue Discount 85Tax-Exempt Interest 86Municipal Bonds 86Dividend Income 86Ordinary Dividends 88Holding Period 89Mutual Funds 90Return of Capital 90Interviewing Clients 91Common Interview Mistakes 91Common Preparation Mistakes 92

Contents

13Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

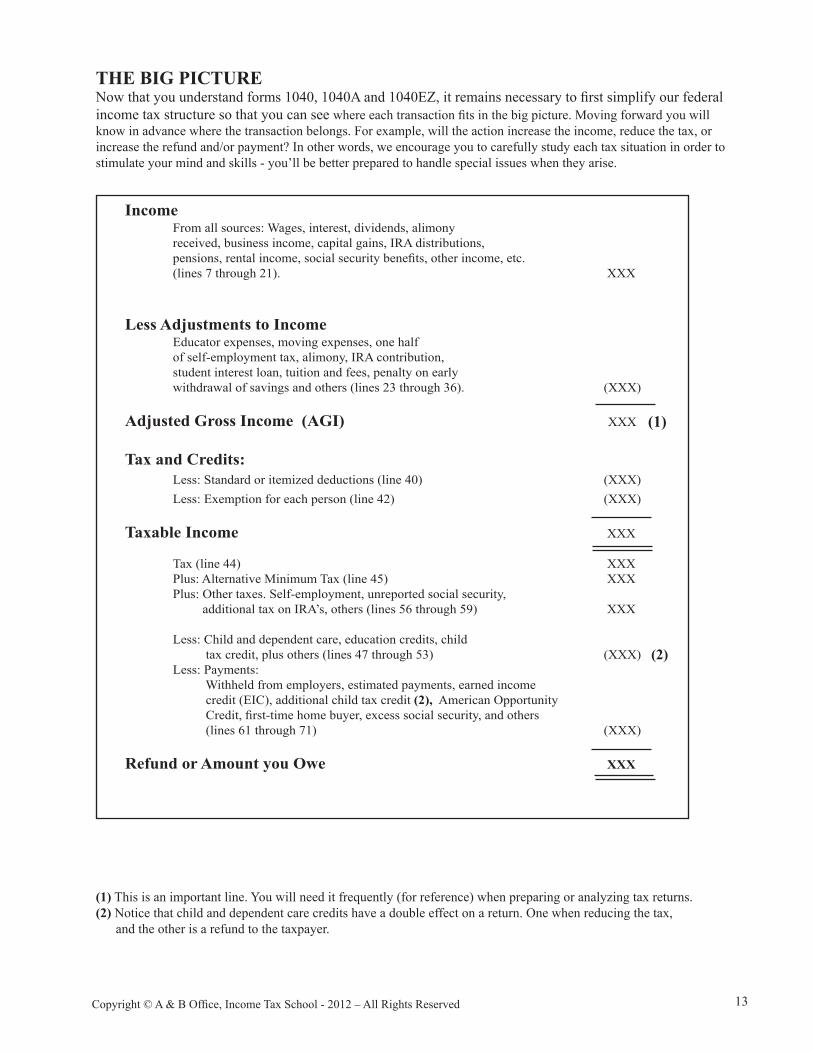

THE BIG PICTURENow that you understand forms 1040, 1040A and 1040EZ, it remains necessary to first simplify our federal income tax structure so that you can see where each transaction fits in the big picture. Moving forward you will know in advance where the transaction belongs. For example, will the action increase the income, reduce the tax, or increase the refund and/or payment? In other words, we encourage you to carefully study each tax situation in order to stimulate your mind and skills - you’ll be better prepared to handle special issues when they arise.

(1) This is an important line. You will need it frequently (for reference) when preparing or analyzing tax returns.(2) Notice that child and dependent care credits have a double effect on a return. One when reducing the tax, and the other is a refund to the taxpayer.

Income From all sources: Wages, interest, dividends, alimony received, business income, capital gains, IRA distributions, pensions, rental income, social security benefits, other income, etc. (lines 7 through 21). XXX

Less Adjustments to Income Educator expenses, moving expenses, one half of self-employment tax, alimony, IRA contribution, student interest loan, tuition and fees, penalty on early withdrawal of savings and others (lines 23 through 36). (XXX)

Adjusted Gross Income (AGI) XXX

Tax and Credits: Less: Standard or itemized deductions (line 40) (XXX) Less: Exemption for each person (line 42) (XXX) Taxable Income XXX Tax (line 44) XXX Plus: Alternative Minimum Tax (line 45) XXX Plus: Other taxes. Self-employment, unreported social security, additional tax on IRA’s, others (lines 56 through 59) XXX

Less: Child and dependent care, education credits, child tax credit, plus others (lines 47 through 53) (XXX) Less: Payments: Withheld from employers, estimated payments, earned income credit (EIC), additional child tax credit (2), American Opportunity Credit, first-time home buyer, excess social security, and others (lines 61 through 71) (XXX)

Refund or Amount you Owe XXX

(1)

(2)

14 Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 1: General MaterialLearning Objective: In this chapter the student will learn to determine who should file a return, what filing status the taxpayer should use, and what forms to use. The student will also learn when returns are due, how to apply for an extension of time to file, and what form to use when filing an application for extension. Accounting periods and methods will also be studied.

What Is a Tax Preparer and What Is His RoleA taxpayer may find that the most efficient and cost effective manner in which to comply with filing a timely and accurate tax return is to employ the services of a professional tax preparer. Because the taxpayer is still respon-sible for the accuracy of his tax return, he should be sure he has chosen an educated professional to assist him. A taxpayer should also remember the following:

“Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pat-tern which will best pay the treasury; there is not even a patriotic duty to increase one’s taxes.”

This quote is from the influential U.S. Court of Appeals judge and noted judicial philosopher, Learned Hand, who is expressing his views on our duty as taxpayers to pay our “fair and legitimate” share of taxes. A professional pre-parer most likely will share U.S. Court of Appeals Judge Learned Hand’s views.

a) Goal: to attain least legitimate tax (minimize tax). b) Works for the taxpayer, not the IRS (do not audit). (The Tax Relief Act of 1997 does require that preparers of returns with Earned Income Credit exercise “due diligence” in preparing Earned In- come Credit (EIC) returns. See Chapter 5 for further explanation.) However, taxpayers may be audited, in which case, they will be required to substantiate entries on their tax returns. c) Interprets "gray" areas to the advantage of the taxpayer, not the IRS. d) Is assertive and asks the taxpayer many questions so that no income or deductions and credits are overlooked. e) Maintains taxpayer's information in complete confidence. f) Meets requirements for competence and professional standing: - Awareness of all tax laws affecting individuals - Ability to research and interpret the tax laws - A thorough and efficient interview technique - Genuine respect and concern for the taxpayer g) If a taxpayer prepares a return that is not in accordance with the tax law or asks a preparer to prepare a return that is not proper, the professional preparer should tell the taxpayer the correct way to report the item and advise him to comply with the tax laws and regulations. The preparer is under no obligation to report the taxpayer to either the IRS or the State. However, the pre- parer is expected to tell the truth if asked by a representative of either the federal or state govern- ment. h) The tax preparer should never prepare a return incorrectly merely because the taxpayer insists on it. i) Preparers should always be alert to fraud. If a client is vague with answers to questions or pro- vides answers that are suspicious, the tax preparer should be assertive and ask additional questions. If the preparer is not comfortable preparing a return for the taxpayer, he should explain his position to the taxpayer and refuse to prepare the return.

A preparer is subject to a $1,000 (or, if greater, 50% of the income derived with respect to the income) fine per return for an understatement of taxpayer’s liability due to an unrealistic position. Understatement due to preparer’s willful or reckless conduct or intentional disregard of rules is punishable by a fine of $5,000 (or, if greater, 50% of the income derived with respect to the income) per return.

35Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

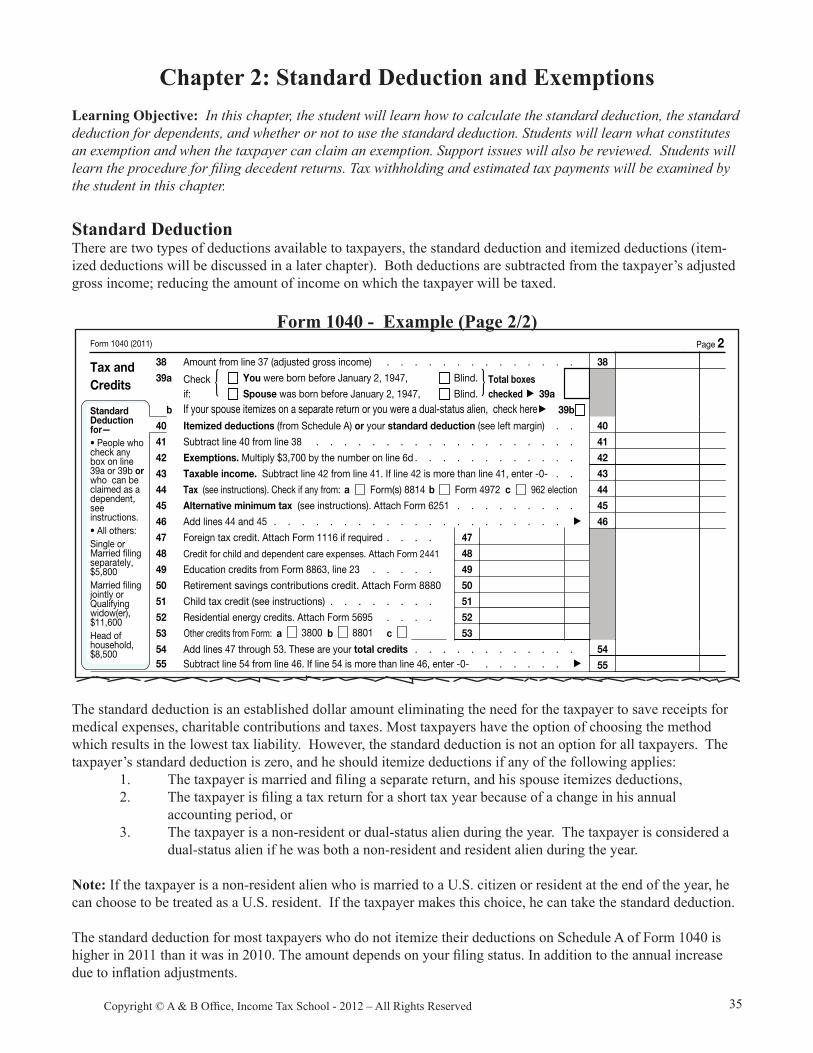

Chapter 2: Standard Deduction and Exemptions Learning Objective: In this chapter, the student will learn how to calculate the standard deduction, the standard deduction for dependents, and whether or not to use the standard deduction. Students will learn what constitutes an exemption and when the taxpayer can claim an exemption. Support issues will also be reviewed. Students will learn the procedure for filing decedent returns. Tax withholding and estimated tax payments will be examined by the student in this chapter.

Standard Deduction There are two types of deductions available to taxpayers, the standard deduction and itemized deductions (item-ized deductions will be discussed in a later chapter). Both deductions are subtracted from the taxpayer’s adjusted gross income; reducing the amount of income on which the taxpayer will be taxed.

Form 1040 - Example (Page 2/2)

The standard deduction is an established dollar amount eliminating the need for the taxpayer to save receipts for medical expenses, charitable contributions and taxes. Most taxpayers have the option of choosing the method which results in the lowest tax liability. However, the standard deduction is not an option for all taxpayers. The taxpayer’s standard deduction is zero, and he should itemize deductions if any of the following applies: 1. Thetaxpayerismarriedandfilingaseparatereturn,andhisspouseitemizesdeductions, 2. Thetaxpayerisfilingataxreturnforashorttaxyearbecauseofachangeinhisannual accounting period, or 3. The taxpayer is a non-resident or dual-status alien during the year. The taxpayer is considered a dual-status alien if he was both a non-resident and resident alien during the year.

Note: If the taxpayer is a non-resident alien who is married to a U.S. citizen or resident at the end of the year, he can choose to be treated as a U.S. resident. If the taxpayer makes this choice, he can take the standard deduction.

The standard deduction for most taxpayers who do not itemize their deductions on Schedule A of Form 1040 is higherin2011thanitwasin2010.Theamountdependsonyourfilingstatus.Inadditiontotheannualincreaseduetoinflationadjustments.

Form 1040 (2011) Page 2

Tax and Credits

38 Amount from line 37 (adjusted gross income) . . . . . . . . . . . . . . 38

39a Check if:

{ You were born before January 2, 1947, Blind.

Spouse was born before January 2, 1947, Blind.} Total boxes

checked ▶ 39a

b If your spouse itemizes on a separate return or you were a dual-status alien, check here ▶ 39b Standard Deduction for— • People who check any box on line 39a or 39b or who can be claimed as a dependent, see instructions. • All others: Single or Married filing separately, $5,800 Married filing jointly or Qualifying widow(er), $11,600 Head of household, $8,500

40 Itemized deductions (from Schedule A) or your standard deduction (see left margin) . . 40

41 Subtract line 40 from line 38 . . . . . . . . . . . . . . . . . . . 41

42 Exemptions. Multiply $3,700 by the number on line 6d . . . . . . . . . . . . 42

43 Taxable income. Subtract line 42 from line 41. If line 42 is more than line 41, enter -0- . . 43

44 Tax (see instructions). Check if any from: a Form(s) 8814 b Form 4972 c 962 election 44

45 Alternative minimum tax (see instructions). Attach Form 6251 . . . . . . . . . 45

46 Add lines 44 and 45 . . . . . . . . . . . . . . . . . . . . . ▶ 46

47 Foreign tax credit. Attach Form 1116 if required . . . . 47

48 Credit for child and dependent care expenses. Attach Form 2441 48

49 Education credits from Form 8863, line 23 . . . . . 49

50 Retirement savings contributions credit. Attach Form 8880 50

51 Child tax credit (see instructions) . . . . . . . . 51

52 Residential energy credits. Attach Form 5695 . . . . 52

53 Other credits from Form: a 3800 b 8801 c 53

54 Add lines 47 through 53. These are your total credits . . . . . . . . . . . . 5455 Subtract line 54 from line 46. If line 54 is more than line 46, enter -0- . . . . . . ▶ 55

Other Taxes

56 Self-employment tax. Attach Schedule SE . . . . . . . . . . . . . . . 56

57 Unreported social security and Medicare tax from Form: a 4137 b 8919 . . 57

58 Additional tax on IRAs, other qualified retirement plans, etc. Attach Form 5329 if required . . 58

59a 59a

b 59bHousehold employment taxes from Schedule H . . . . . . . . . . . . . .

First-time homebuyer credit repayment. Attach Form 5405 if required . . . . . . . .

60 Other taxes. Enter code(s) from instructions 60

61 Add lines 55 through 60. This is your total tax . . . . . . . . . . . . . ▶ 61

Payments 62 Federal income tax withheld from Forms W-2 and 1099 . . 62

63 2011 estimated tax payments and amount applied from 2010 return 63If you have a qualifying child, attach Schedule EIC.

64a Earned income credit (EIC) . . . . . . . . . . 64a

b Nontaxable combat pay election 64b

65 Additional child tax credit. Attach Form 8812 . . . . . . 65

66 American opportunity credit from Form 8863, line 14 . . . 66

67 First-time homebuyer credit from Form 5405, line 10 . . . 67

68 Amount paid with request for extension to file . . . . . 68

69 Excess social security and tier 1 RRTA tax withheld . . . . 69

70 Credit for federal tax on fuels. Attach Form 4136 . . . . 70

71 Credits from Form: a 2439 b 8839 c 8801 d 8885 7172 Add lines 62, 63, 64a, and 65 through 71. These are your total payments . . . . . ▶ 72

Refund

Direct deposit? See instructions.

73 If line 72 is more than line 61, subtract line 61 from line 72. This is the amount you overpaid 73

74a Amount of line 73 you want refunded to you. If Form 8888 is attached, check here . ▶ 74a ▶

▶

b Routing number ▶ c Type: Checking Savings

d Account number

75 Amount of line 73 you want applied to your 2012 estimated tax ▶ 75Amount You Owe

76 Amount you owe. Subtract line 72 from line 61. For details on how to pay, see instructions ▶ 76

77 Estimated tax penalty (see instructions) . . . . . . . 77

Third Party Designee

Do you want to allow another person to discuss this return with the IRS (see instructions)? Yes. Complete below. No

Designee’s name ▶

Phone no. ▶

Personal identification number (PIN) ▶

Sign Here Joint return? See instructions. Keep a copy for your records.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

Spouse’s signature. If a joint return, both must sign.

▲

Date Spouse’s occupation If the IRS sent you an Identity Protection PIN, enter it here (see inst.)

Paid Preparer Use Only

Print/Type preparer’s name Preparer’s signature Date Check if self-employed

PTIN

Firm’s name ▶

Firm’s address ▶

Firm's EIN ▶

Phone no.

Form 1040 (2011)

63 Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

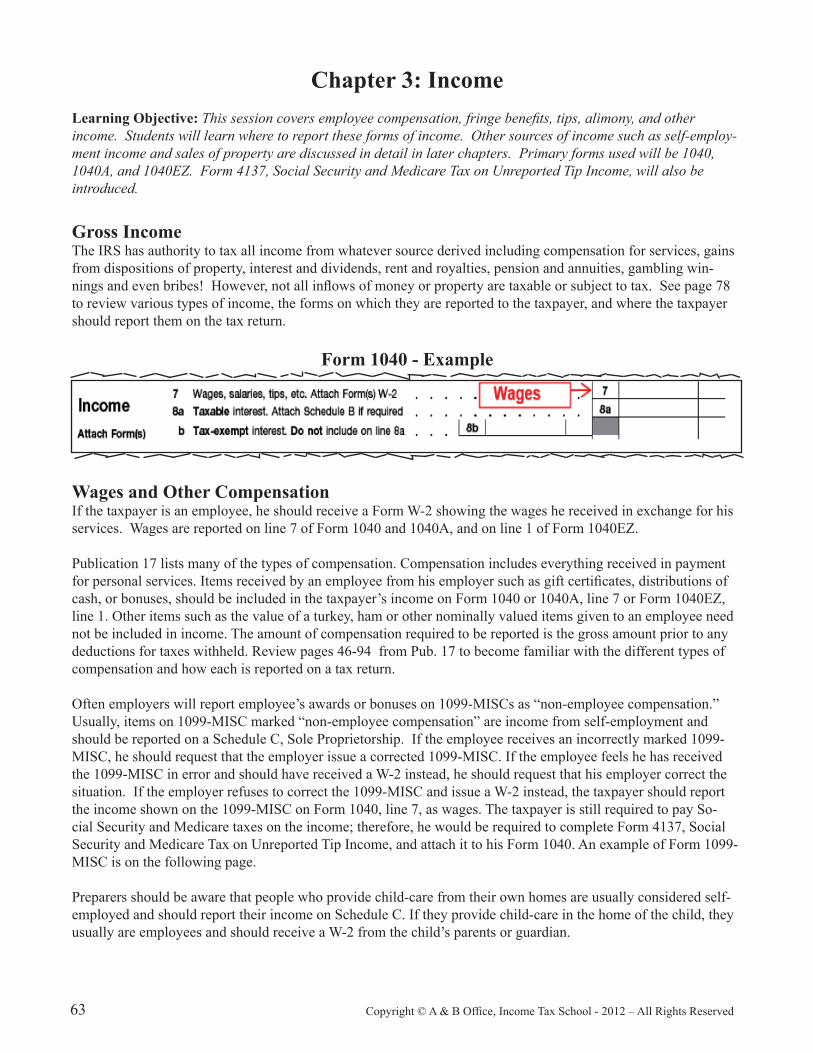

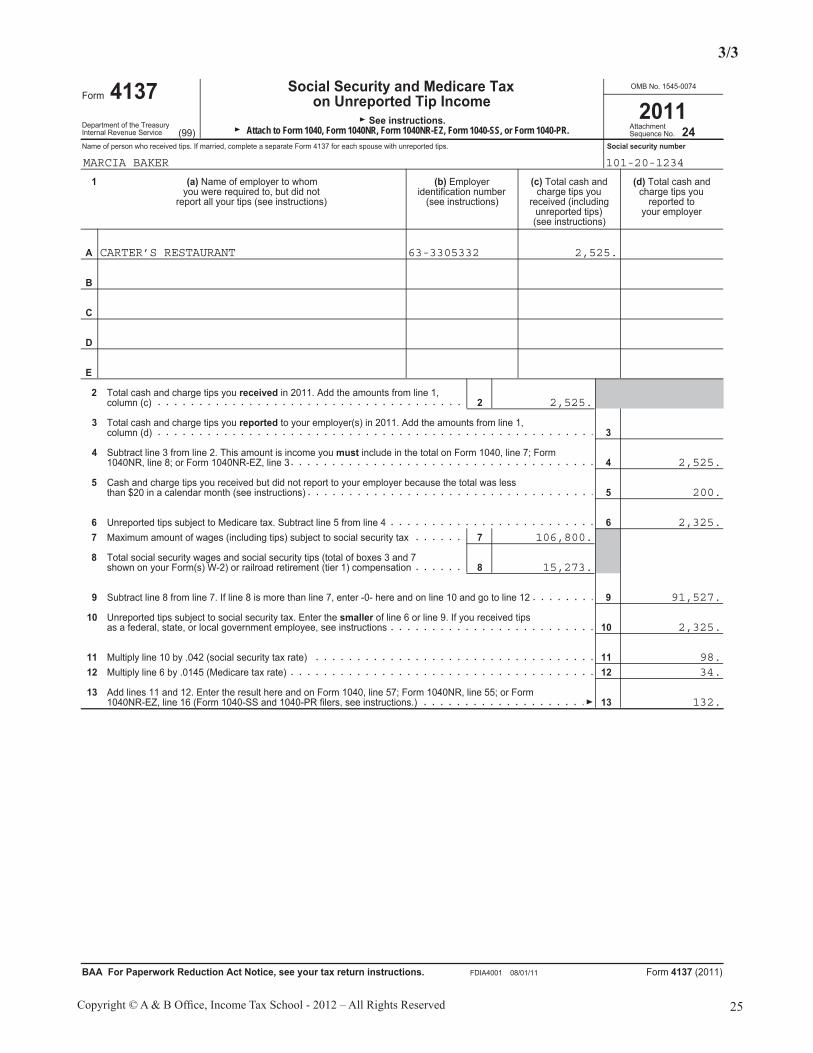

Chapter 3: Income Learning Objective: This session covers employee compensation, fringe benefits, tips, alimony, and other income. Students will learn where to report these forms of income. Other sources of income such as self-employ-ment income and sales of property are discussed in detail in later chapters. Primary forms used will be 1040, 1040A, and 1040EZ. Form 4137, Social Security and Medicare Tax on Unreported Tip Income, will also be introduced.

Gross Income The IRS has authority to tax all income from whatever source derived including compensation for services, gains from dispositions of property, interest and dividends, rent and royalties, pension and annuities, gambling win-nings and even bribes! However, not all inflows of money or property are taxable or subject to tax. See page 78 to review various types of income, the forms on which they are reported to the taxpayer, and where the taxpayer should report them on the tax return.

Form 1040 - Example

Wages and Other Compensation If the taxpayer is an employee, he should receive a Form W-2 showing the wages he received in exchange for his services. Wages are reported on line 7 of Form 1040 and 1040A, and on line 1 of Form 1040EZ.

Publication 17 lists many of the types of compensation. Compensation includes everything received in payment for personal services. Items received by an employee from his employer such as gift certificates, distributions of cash, or bonuses, should be included in the taxpayer’s income on Form 1040 or 1040A, line 7 or Form 1040EZ, line 1. Other items such as the value of a turkey, ham or other nominally valued items given to an employee need not be included in income. The amount of compensation required to be reported is the gross amount prior to any deductions for taxes withheld. Review pages 46-94 from Pub. 17 to become familiar with the different types of compensation and how each is reported on a tax return.

Often employers will report employee’s awards or bonuses on 1099-MISCs as “non-employee compensation.” Usually, items on 1099-MISC marked “non-employee compensation” are income from self-employment and should be reported on a Schedule C, Sole Proprietorship. If the employee receives an incorrectly marked 1099-MISC, he should request that the employer issue a corrected 1099-MISC. If the employee feels he has received the 1099-MISC in error and should have received a W-2 instead, he should request that his employer correct the situation. If the employer refuses to correct the 1099-MISC and issue a W-2 instead, the taxpayer should report the income shown on the 1099-MISC on Form 1040, line 7, as wages. The taxpayer is still required to pay So-cial Security and Medicare taxes on the income; therefore, he would be required to complete Form 4137, Social Security and Medicare Tax on Unreported Tip Income, and attach it to his Form 1040. An example of Form 1099-MISC is on the following page.

Preparers should be aware that people who provide child-care from their own homes are usually considered self-employed and should report their income on Schedule C. If they provide child-care in the home of the child, they usually are employees and should receive a W-2 from the child’s parents or guardian.

81Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

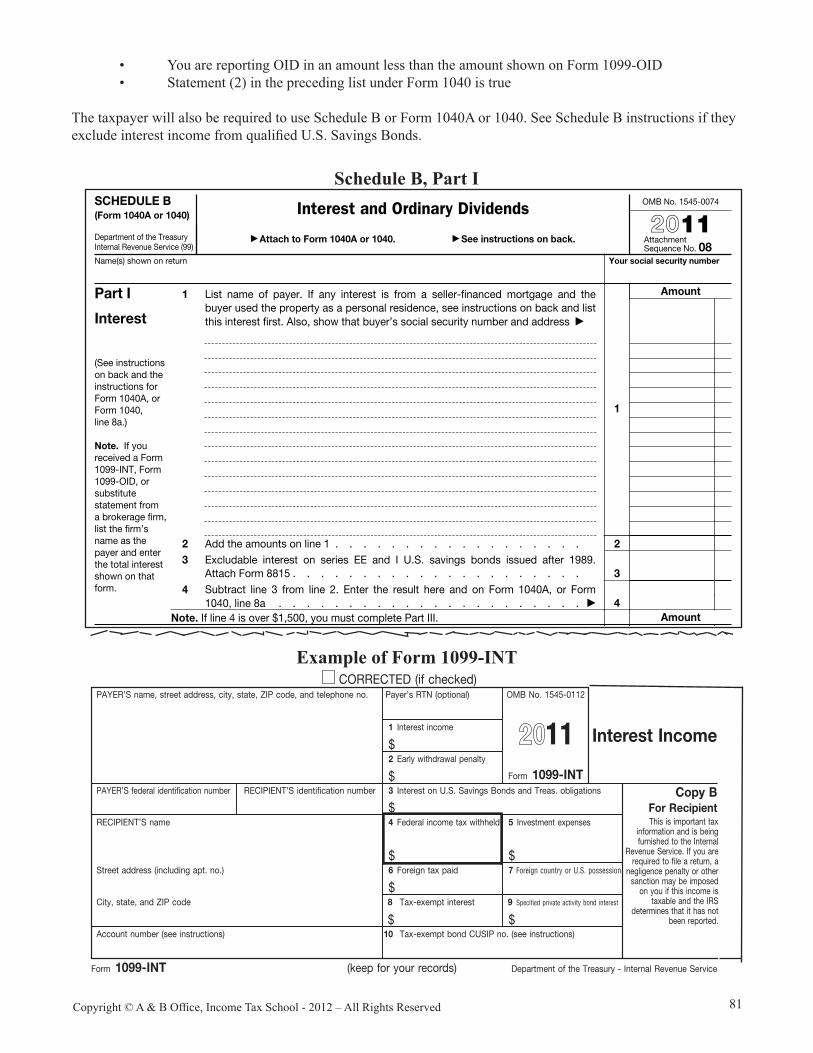

• You are reporting OID in an amount less than the amount shown on Form 1099-OID • Statement (2) in the preceding list under Form 1040 is true

The taxpayer will also be required to use Schedule B or Form 1040A or 1040. See Schedule B instructions if they exclude interest income from qualified U.S. Savings Bonds.

Schedule B, Part I

Example of Form 1099-INT

SCHEDULE B (Form 1040A or 1040)

Department of the Treasury Internal Revenue Service (99)

Interest and Ordinary Dividends

▶ Attach to Form 1040A or 1040. ▶ See instructions on back.

OMB No. 1545-0074

2011Attachment Sequence No. 08

Name(s) shown on return Your social security number

Part I

Interest

(See instructions on back and the instructions for Form 1040A, or Form 1040, line 8a.) Note. If you received a Form 1099-INT, Form 1099-OID, or substitute statement from a brokerage firm, list the firm’s name as the payer and enter the total interest shown on that form.

1

List name of payer. If any interest is from a seller-financed mortgage and the buyer used the property as a personal residence, see instructions on back and list this interest first. Also, show that buyer’s social security number and address ▶

1

Amount

2 Add the amounts on line 1 . . . . . . . . . . . . . . . . . . 2 3

Excludable interest on series EE and I U.S. savings bonds issued after 1989. Attach Form 8815 . . . . . . . . . . . . . . . . . . . . . 3

4

Subtract line 3 from line 2. Enter the result here and on Form 1040A, or Form 1040, line 8a . . . . . . . . . . . . . . . . . . . . . . ▶ 4

Note. If line 4 is over $1,500, you must complete Part III. Amount

Part II

Ordinary Dividends (See instructions on back and the instructions for Form 1040A, or Form 1040, line 9a.)

Note. If you received a Form 1099-DIV or substitute statement from a brokerage firm, list the firm’s name as the payer and enter the ordinary dividends shown on that form.

5 List name of payer ▶

5

6

Add the amounts on line 5. Enter the total here and on Form 1040A, or Form 1040, line 9a . . . . . . . . . . . . . . . . . . . . . . ▶ 6

Note. If line 6 is over $1,500, you must complete Part III.

Part III Foreign Accounts and Trusts (See instructions on back.)

You must complete this part if you (a) had over $1,500 of taxable interest or ordinary dividends; (b) had a foreign account; or (c) received a distribution from, or were a grantor of, or a transferor to, a foreign trust. Yes No

7a At any time during 2011, did you have a financial interest in or signature authority over a financialaccount (such as a bank account, securities account, or brokerage account) located in a foreigncountry? See instructions . . . . . . . . . . . . . . . . . . . . . . . .

b

If “Yes,” are you required to file Form TD F 90-22.1 to report that financial interest or signature authority? See Form TD F 90-22.1 and its instructions for filing requirements and exceptions to those requirements . . . . . . . . . . . . . . . . . . . . . . . . . .If you are required to file Form TD F 90-22.1, enter the name of the foreign country where the financial account is located ▶

8 During 2011, did you receive a distribution from, or were you the grantor of, or transferor to, a foreign trust? If “Yes,” you may have to file Form 3520. See instructions on back . . . . . .

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 17146N Schedule B (Form 1040A or 1040) 2011

CORRECTED (if checked)Payer’s RTN (optional)PAYER’S name, street address, city, state, ZIP code, and telephone no. OMB No. 1545-0112

Interest Income

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City, state, and ZIP code

Account number (see instructions)

Department of the Treasury - Internal Revenue ServiceForm 1099-INT

Copy BFor RecipientThis is important tax

information and is beingfurnished to the Internal

Revenue Service. If you arerequired to file a return, a

negligence penalty or othersanction may be imposed

on you if this income istaxable and the IRS

determines that it has notbeen reported.

(keep for your records)

Form 1099-INTInterest on U.S. Savings Bonds and Treas. obligations3

$Federal income tax withheld Investment expenses54

$$Foreign tax paid6

$7

Early withdrawal penalty2

$

Interest income1

$ 11

Specified private activity bond interest9Tax-exempt interest8

$10 Tax-exempt bond CUSIP no. (see instructions)

$

Foreign country or U.S. possession

101Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 5: Earned Income Credit Learning Objective: In this session we will examine the most common tax credit, the earned income credit. We will learn the definition of earned income for Earned Income Credit. We will also learn the requirements for qualifying children for Earned Income Credit purposes, as well as how taxpayers without children may qualify. Students will learn how to fill out Schedule EIC and where to put the information from that form on the 1040 or 1040A. IRS due diligence requirements will also be discussed.

What Is The EIC? The earned income credit (EIC) is a tax credit for certain people who work and have earned income under $49,078. A tax credit usually means more money in your pocket. It reduces the amount of tax you owe. The EIC may also give you a refund.

Can I Claim the EIC? To claim the EIC, you must meet certain rules. These rules are summarized in Table 5.1, Earned Income Credit in a Nutshell.

Do I Have To Have a Child To Qualify For The EIC?No, you can qualify for the EIC without a qualifying child if you are at least age 25 but under age 65 at the end of 2011 and your earned income is less than $13,660 ($18,740 if married filing jointly).

How Do I Figure the Amount of EIC?If you can claim the EIC, you can either have the IRS figure the amount of your credit, or you can figure it your-self. To figure it yourself, you can complete a worksheet in the instructions for the form you file. To find out how to have the IRS figure it for you, see chapter 4.

Page 242 of 304 of Publication 17 13:55 - 21-DEC-2011

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Table 35-1. Earned Income Credit in a Nutshell

First, you must meet all the rules in this column. Second, you must meet all the rules in one of Third, you must meet thethese columns, whichever applies. rule in this column.

Part A. Part B. Part C. Part D.Rules for Everyone Rules If You Have a Rules If You Do Not Figuring and Claiming the

Qualifying Child Have a Qualifying EICChild

1. Your adjusted gross 2. You must have a valid 8. Your child must meet 11. You must be at 15. Your earned income mustincome (AGI) must be social security number. the relationship, age, least age 25 but under be less than:less than: 3. Your filing status residency, and joint return age 65. • $43,998 ($49,078 for• $43,998 ($49,078 for cannot be “Married filing tests. 12. You cannot be the married filing jointly) if youmarried filing jointly) if separately.” 9. Your qualifying child dependent of another have three or more qualifyingyou have three or more 4. You must be a U.S. cannot be used by more person. children,qualifying children, citizen or resident alien than one person to claim 13. You cannot be a

all year. the EIC. qualifying child of • $40,964 ($46,044 for• $40,964 ($46,044 for 5. You cannot file Form 10. You cannot be a another person. married filing jointly) if youmarried filing jointly) if 2555 or Form 2555-EZ qualifying child of another 14. You must have have two qualifying children,you have two qualifying (relating to foreign person. lived in the Unitedchildren, earned income). States more than half • $36,052 ($41,132 for

6. Your investment of the year. married filing jointly) if you• $36,052 ($41,132 for income must be $3,150 have one qualifying child, or married filing jointly) if or less. you have one qualifying 7. You must have earned • $13,660 ($18,740 forchild, or income. married filing jointly) if you do

not have a qualifying child.• $13,660 ($18,740 formarried filing jointly) ifyou do not have aqualifying child.

Example. Your AGI is $36,550, you are sin- Valid for work only with INS or DHS authori- U.S. Individual Income Tax Return) claim-zation. If your social security card reads “Validgle, and you have one qualifying child. You can- ing the EIC. Attach a filled-in Schedule EICfor work only with INS authorization,” or “Validnot claim the EIC because your AGI is not less if you have a qualifying child.for work only with DHS authorization,” you havethan $36,052. However, if your filing status wasa valid SSN.married filing jointly, you might be able to claim

Rule 3. Your Filing Statusthe EIC because your AGI is less than $41,132.SSN missing or incorrect. If an SSN for you

Community property. If you are married, Cannot Be Married Filingor your spouse is missing from your tax return orbut qualify to file as head of household under is incorrect, you may not get the EIC. Separatelyspecial rules for married taxpayers living apart

Other taxpayer identification number. You(see Rule 3), and live in a state that has commu- If you are married, you usually must file a jointcannot get the EIC if, instead of an SSN, you (ornity property laws, your AGI includes that portion return to claim the EIC. Your filing status cannotyour spouse if filing a joint return) have an indi-of both your and your spouse’s wages that you be “Married filing separately.”vidual taxpayer identification number (ITIN).are required to include in gross income. This isITINs are issued by the Internal Revenue Serv-different from the community property rules that

Spouse did not live with you. If you are mar-ice to noncitizens who cannot get an SSN.apply under Rule 7.ried and your spouse did not live in your home at

No SSN. If you do not have a valid SSN, put any time during the last 6 months of the year,“No” next to line 64a (Form 1040), line 38aRule 2. You Must Have a you may be able to file as head of household,(Form 1040A), or line 8a (Form 1040EZ). You instead of married filing separately. In that case,Valid Social Security cannot claim the EIC. you may be able to claim the EIC. For detailedNumber (SSN) information about filing as head of household,Getting an SSN. If you (or your spouse if

see chapter 2. filing a joint return) do not have an SSN, you canTo claim the EIC, you (and your spouse if filing aapply for one by filing Form SS-5, Application forjoint return) must have a valid SSN issued by thea Social Security Card, with the SSA. You can Rule 4. You Must Be a Social Security Administration (SSA). Any quali-get Form SS-5 online at www.socialsecurity.fying child listed on Schedule EIC also must U.S. Citizen or Resident gov, from your local SSA office, or by calling thehave a valid SSN. (See Rule 8 if you have aSSA at 1-800-772-1213. Alien All Yearqualifying child.)

Filing deadline approaching and still noIf your social security card (or your spouse’sIf you (or your spouse, if married) were a nonres-SSN. If the filing deadline is approaching andif filing a joint return) says “Not valid for employ-ident alien for any part of the year, you cannotyou still do not have an SSN, you have twoment” and your SSN was issued so that you (orclaim the earned income credit unless your filingchoices.your spouse) could get a federally funded bene-status is married filing jointly. You can use thatfit, you cannot get the EIC. An example of a

1. Request an automatic 6-month extension filing status only if one spouse is a U.S. citizen orfederally funded benefit is Medicaid.of time to file your return. You can get this resident alien and you choose to treat the non-If you have a card with the legend “Not valid extension by filing Form 4868, Application resident spouse as a U.S. resident. If you makefor employment” and your immigration status for Automatic Extension of Time to File this choice, you and your spouse are taxed onhas changed so that you are now a U.S. citizen U.S. Individual Income Tax Return. For your worldwide income. If you (or your spouse, ifor permanent resident, ask the SSA for a new more information, see chapter 1. married) were a nonresident alien for any part ofsocial security card without the legend.

the year and your filing status is not married2. File the return on time without claiming thefiling jointly, enter “No” on the dotted line next toU. S. citizen. If you were a U. S. citizen when EIC. After receiving the SSN, file anline 64a (Form 1040) or in the space to the left ofyou received your SSN, you have a valid SSN. amended return (Form 1040X, Amended

Page 240 Chapter 35 Earned Income Credit (EIC)

5.1

153Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 7: Retirement Income And Other Income Types

Learning Objective: Students will learn how to recognize retirement income, including income from pensions, an-nuities, Social Security, and equivalent retirement benefits. Other income discussed includes barter, partnership, recoveries, rental of personal property, repayments, royalties, and income that is not taxed. Students will learn how to “read” Forms 1099-R and SSA-1099-SM.

Pensions and Annuities A pension is generally a series of definitely determinable payments made to the taxpayer after he retires from work. Pension payments are made regularly and are based on certain factors, such as years of service and prior compensation.

An annuity is a series of payments under a contract made at regular intervals over a period of more than one full year. They can be either fixed (under which the taxpayer receives a definite amount) or variable, not fixed. The taxpayer can buy the contract alone or with the help of his employer.

A qualified employee plan is an employer's stock bonus, pension, or profit-sharing plan that is for the exclusive benefit of employees or their beneficiaries and that meets Internal Revenue Code requirements. It qualifies for special tax benefits, such as tax deferral for employer contributions and rollover distributions, and capital gain treatment or the 10-year tax option for lump-sum distributions (if participants qualify).

A qualified employee annuity is a retirement annuity purchased by an employer for an employee under a plan that meets Internal Revenue Code requirements.

A tax-sheltered annuity (TSA) plan (often referred to as a “403(b) plan” or a “tax-deferred annuity plan”) is a retirement plan for employees of public schools and certain tax-exempt organizations. Generally, a TSA plan provides retirement benefits by purchasing annuity contracts for its participants.

A non-qualified employee plan is an employer's plan that does not meet Internal Revenue Code requirements for qualified employee plans. It does not qualify for most of the tax benefits of a qualified plan.

SIMPLE IRAWhat Is a SIMPLE IRA? A SIMPLE IRA is a type of IRA that may receive only contributions made pursuant to a Savings Incentive Match Plan For Employees (SIMPLE). For the most part, other than the rules on contribu-tions, the same rules apply to a SIMPLE IRA as do to a traditional IRA. The significant exception is that the 10 percent premature distribution penalty associated with IRAs is increased to 25 percent for the first two years of participation in a SIMPLE.

What are SIMPLE contributions? SIMPLE contributions are contributions made pursuant to an employer’s savings incentive match plan for employees, under which employees are allowed to defer a portion of their compensation. The employer also makes contributions-either a matching contribution or an employer nonelective contribution. Salary reduction contributions that your employer can make on your behalf are limited $11,500 for 2011 and 2012.

A SIMPLE IRA shares the underlying concept of a 401(k) plan; one of its distinguishing features, however, is that a SIMPLE IRA does not maintain a collective trust. Instead, all SIMPLE contributions must be made into the participants’ SIMPLE IRAs established by or for each participant.

188 Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 9: Itemized Deductions Learning Objective: Students will be able to determine the most advantageous deduction for the taxpayer, using standard or itemized deductions. They will also examine eligible medical expenses, what items qualify as taxes, and eligible interest deductions. Also, they will learn how to value charitable contributions, report casu-alties and thefts, and the different types of miscellaneous deductions that can be taken. Students will complete Schedule A, Form 4684 – Casualties and Thefts, Form 8283 – Noncash Contributions, and learn where to enter the information from these forms.

Itemized Deductions The taxpayer should always choose whichever reduces taxable income more – itemized or standard deduction. As studied in Chapter Two, a standard deduction is a set amount that the taxpayer is allowed to use instead of itemizing his deductions. However, in some circumstances the taxpayer may not be allowed to use the standard deduction (for instance, an individual choosing to use the Married Filing Separate status if the spouse has used the itemized deduction method). Itemized deductions are shown on the tax return using Schedule A – Itemized Deductions.

It is more beneficial for the taxpayer to itemize his deductions if the total of his itemized deductions exceed his standard deduction. Taxpayers should also itemize or consider itemizing if they meet the following criteria: • They do not qualify for the standard deduction, or it is limited • The taxpayers had large unreimbursed medical or dental expenses • The taxpayers paid mortgage interest and taxes on their residence • They had large unreimbursed employee business expenses or other miscellaneous expenses • They had casualty or theft losses not covered by insurance • The taxpayers made large contributions to qualified charities • The total of the taxpayers’ itemized deductions is higher than the standard deduction to which they would be entitled

Married Filing Separate Taxpayers If the taxpayers are filing Married Filing Separate and one spouse itemizes, the other spouse must itemize, regard-less of the fact that his total deductions may be less than the standard deduction to which he would otherwise be entitled. If either taxpayer later amends his return, the spouse must also amend his or her return. Both taxpayers must file a consent to assessment for any additional tax either one may owe as a result of the amendment.

In the case of a spouse who qualifies as Head of Household, this rule will not apply. The spouse who qualifies as Head of Household is not required to itemize deductions even if the spouse who is required to file Married Filing Separately decides to itemize his deductions. However, if the spouse filing Head of Household decides to itemize deductions, the spouse filing Married Filing Separately is required to itemize deductions.

Limitation on Itemized Deductions For 2010, the overall limit on itemized deductions has expired. Under current law, the limit on itemized deduc-tions will resume in 2011.

Medical Expenses Medical care expenses can be deducted if amounts are paid for the diagnosis, cure, treatment or prevention of a disease or ailments affecting any part of or function of the body. Procedures such as facelifts, hair transplants, hair/tattoo removal, and liposuction generally are not deductible. Cosmetic surgery is only deductible if it is to improve a deformity arising from or directly related to, a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease. Medications are only deductible if prescribed by a doctor.

221Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 11: Employee Business Expense and Miscellaneous Itemized Deductions

Objective: Students will be presented with an example of employee business expenses to determine which ex-penses are deductible and when the expenses are allowed. This lesson will focus primarily on expenses relating to business auto use and office-in-home expenses. Students will learn how to complete office-in-home worksheets, Form 2106 - Employee Business Expense, and where to transfer the information from these forms. They will also study other miscellaneous deductions such as investment related expenses. Last, students will learn how to handle reimbursed employee business expenses.

Student note: Depreciation and Schedule C will be discussed in Chapters 14 and 15; however, there are many references to both in this chapter. While this may seem confusing, the references are necessary to adequately explain the subject matter in this chapter.

Miscellaneous Itemized Deduction Limitation The taxpayer can deduct certain expenses as miscellaneous itemized deductions on Schedule A. He can deduct the expenses that exceed 2% of his adjusted gross income. He must calculate his deduction on Schedule A by sub-tracting 2% of his adjusted gross income from the total amount of these expenses.

Schedule A - Example

Generally, the taxpayer applies the 2% limit after he applies any other deduction limit. For example, he applies the 50% limit on business-related meals and entertainment before he applies the 2% limit. Deductions subject to the 2% limit are broken into three categories: 1. Unreimbursed employee expenses (line 21) 2. Tax preparation fees (line 22) 3. Other expenses (line 23)

Employee Business Expenses An employee may deduct un-reimbursed expenses that are paid and incurred during the current tax year. The expenses must be incurred for conducting trade or business as an employee and the expenses must be ordinary and necessary. An expense is considered ordinary if it is common and necessary in the taxpayer’s trade or busi-ness. An expense is considered necessary if it is appropriate and helpful to the taxpayer’s trade or business. For example: a nurse is required to provide malpractice insurance and often required to wear a uniform. Since the employer does not reimburse these expenses, the nurse may deduct them on Schedule A as a miscellaneous deduc-tion subject to the 2% AGI limitation.

249Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Chapter 13: Capital Gains and Losses Learning Objective: Capital gains and losses will be discussed. Sales of property will be studied. Students will learn how to determine the basis of property, the gain or loss, and when and how to report sales of personal resi-dences. Schedule D will be introduced.

Capital Gains and Losses A capital gain or loss is a gain or loss on the sale of almost any asset. These gains and losses are reported on Schedule D, Capital Gains and Losses. If the gain or loss relates to the sale of business property, it is first reported on Form 4797, Sale of Business Property. The figures from Form 4797 are carried over to Schedule D. The sale of a personal residence is reported only if there is a gain in excess of the excludable amount (covered later in this chapter). The gain would be reported on Schedule D.

The rate at which the gain on sale of a capital asset will be taxed depends on the type of capital asset, the holding period, and the taxpayer's tax bracket. If a taxpayer has a capital loss, the loss will be netted with any realized gain. If the taxpayer has a net loss in excess of $3,000, he would be able to deduct up to $3,000 of his loss against his ordinary income in the year of the sale. The unused capital loss would then be carried forward to subsequent years and used to help offset net capital gain or ordinary income up to $3,000 a year until the loss is depleted. If Married Filing Separately, the limit is $1,500.

Capital Assets Capital assets are items held for personal or investment purposes. A capital asset can be anything except inven-tory, depreciable personal and real property used in trade or business, items created by the taxpayer's individual effort (such as a poem), accounts receivable, or certain government publications. Capital assets include stocks and bonds held in the taxpayer’s personal account, home, furnishings, vehicles, collectibles, gems, jewelry, gold, silver, etc. Losses from personal use of assets are not deductible (for example home) unless they resulted from a casualty.

A non-capital asset is property that is not a capital asset. Examples of non-capital assets are: • Property held mainly for sale to customers or property that will physically become part of merchandise for sale to customers • Accounts or notes receivable acquired in the ordinary course of a trade or business for services rendered or from the sale of any properties described above

SCHEDULE D (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Capital Gains and Losses▶ Attach to Form 1040 or Form 1040NR. ▶ See Instructions for Schedule D (Form 1040).

▶ Use Form 8949 to list your transactions for lines 1, 2, 3, 8, 9, and 10.

OMB No. 1545-0074

2011Attachment Sequence No. 12

Name(s) shown on return Your social security number

Part I Short-Term Capital Gains and Losses—Assets Held One Year or Less

( )

( )

( )

Complete Form 8949 before completing line 1, 2, or 3. This form may be easier to complete if you round off cents to whole dollars.

(e) Sales price from Form(s) 8949, line 2,

column (e)

(f) Cost or other basis from Form(s) 8949,

line 2, column (f)

(g) Adjustments to gain or loss from

Form(s) 8949, line 2, column (g)

(h) Gain or (loss) Combine columns (e),

(f), and (g)

1

Short-term totals from all Forms 8949 with box A checked in Part I . . . . . . . . . . . . .

2

Short-term totals from all Forms 8949 with box B checked in Part I . . . . . . . . . . . . .

3

Short-term totals from all Forms 8949 with box C checked in Part I . . . . . . . . . . . . .

4 Short-term gain from Form 6252 and short-term gain or (loss) from Forms 4684, 6781, and 8824 . 4 5

Net short-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

6

Short-term capital loss carryover. Enter the amount, if any, from line 8 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 6 ( )

7 Net short-term capital gain or (loss). Combine lines 1 through 6 in column (h). If you have any long-term capital gains or losses, go to Part II below. Otherwise, go to Part III on the back . . . 7

Part II Long-Term Capital Gains and Losses—Assets Held More Than One Year

( )

( )

( )

Complete Form 8949 before completing line 8, 9, or 10. This form may be easier to complete if you round off cents to whole dollars.

(e) Sales price from Form(s) 8949, line 4,

column (e)

(f) Cost or other basis from Form(s) 8949,

line 4, column (f)

(g) Adjustments to gain or loss from

Form(s) 8949, line 4, column (g)

(h) Gain or (loss) Combine columns (e),

(f), and (g)

8

Long-term totals from all Forms 8949 with box A checked in Part II . . . . . . . . . . . .

9

Long-term totals from all Forms 8949 with box B checked in Part II . . . . . . . . . . . .

10

Long-term totals from all Forms 8949 with box C checked in Part II . . . . . . . . . . . . .

11

Gain from Form 4797, Part I; long-term gain from Forms 2439 and 6252; and long-term gain or (loss) from Forms 4684, 6781, and 8824 . . . . . . . . . . . . . . . . . . . . . . 11

12 Net long-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 12

13 Capital gain distributions. See the instructions . . . . . . . . . . . . . . . . . . 13 14

Long-term capital loss carryover. Enter the amount, if any, from line 13 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 14 ( )

15

Net long-term capital gain or (loss). Combine lines 8 through 14 in column (h). Then go to Part III onthe back . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11338H Schedule D (Form 1040) 2011

Form 4797Department of the Treasury Internal Revenue Service (99)

Sales of Business Property (Also Involuntary Conversions and Recapture Amounts

Under Sections 179 and 280F(b)(2))▶ Attach to your tax return. ▶ See separate instructions.

OMB No. 1545-0184

2011Attachment Sequence No. 27

Name(s) shown on return Identifying number

1 Enter the gross proceeds from sales or exchanges reported to you for 2011 on Form(s) 1099-B or 1099-S (or substitute statement) that you are including on line 2, 10, or 20 (see instructions) . . . . . . . . 1

Part I Sales or Exchanges of Property Used in a Trade or Business and Involuntary Conversions From Other Than Casualty or Theft—Most Property Held More Than 1 Year (see instructions)

2 (a) Description of property

(b) Date acquired (mo., day, yr.)

(c) Date sold (mo., day, yr.)

(d) Gross sales price

(e) Depreciation allowed or

allowable since acquisition

(f) Cost or other basis, plus

improvements and expense of sale

(g) Gain or (loss) Subtract (f) from the

sum of (d) and (e)

3 Gain, if any, from Form 4684, line 39 . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Section 1231 gain from installment sales from Form 6252, line 26 or 37 . . . . . . . . . . . . . . 4

5 Section 1231 gain or (loss) from like-kind exchanges from Form 8824 . . . . . . . . . . . . . . 5

6 Gain, if any, from line 32, from other than casualty or theft. . . . . . . . . . . . . . . . . . 6

7 Combine lines 2 through 6. Enter the gain or (loss) here and on the appropriate line as follows: . . . . . . . 7Partnerships (except electing large partnerships) and S corporations. Report the gain or (loss) following the instructions for Form 1065, Schedule K, line 10, or Form 1120S, Schedule K, line 9. Skip lines 8, 9, 11, and 12 below.

Individuals, partners, S corporation shareholders, and all others. If line 7 is zero or a loss, enter the amount from line 7 on line 11 below and skip lines 8 and 9. If line 7 is a gain and you did not have any prior year section 1231 losses, or they were recaptured in an earlier year, enter the gain from line 7 as a long-term capital gain on the Schedule D filed with your return and skip lines 8, 9, 11, and 12 below.

8 Nonrecaptured net section 1231 losses from prior years (see instructions) . . . . . . . . . . . . . 8

9 Subtract line 8 from line 7. If zero or less, enter -0-. If line 9 is zero, enter the gain from line 7 on line 12 below. If line 9 is more than zero, enter the amount from line 8 on line 12 below and enter the gain from line 9 as a long-term capital gain on the Schedule D filed with your return (see instructions) . . . . . . . . . . . . . . 9

Part II Ordinary Gains and Losses (see instructions)10 Ordinary gains and losses not included on lines 11 through 16 (include property held 1 year or less):

11 Loss, if any, from line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 ( )

12 Gain, if any, from line 7 or amount from line 8, if applicable . . . . . . . . . . . . . . . . . 12

13 Gain, if any, from line 31 . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Net gain or (loss) from Form 4684, lines 31 and 38a . . . . . . . . . . . . . . . . . . . 14

15 Ordinary gain from installment sales from Form 6252, line 25 or 36 . . . . . . . . . . . . . . . 15

16 Ordinary gain or (loss) from like-kind exchanges from Form 8824. . . . . . . . . . . . . . . . 16

17 Combine lines 10 through 16 . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 For all except individual returns, enter the amount from line 17 on the appropriate line of your return and skip lines a and b below. For individual returns, complete lines a and b below:

a If the loss on line 11 includes a loss from Form 4684, line 35, column (b)(ii), enter that part of the loss here. Enter the part of the loss from income-producing property on Schedule A (Form 1040), line 28, and the part of the loss from property used as an employee on Schedule A (Form 1040), line 23. Identify as from “Form 4797, line 18a.” See instructions . . 18a

b Redetermine the gain or (loss) on line 17 excluding the loss, if any, on line 18a. Enter here and on Form 1040, line 14 18b

For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 13086I Form 4797 (2011)

289Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

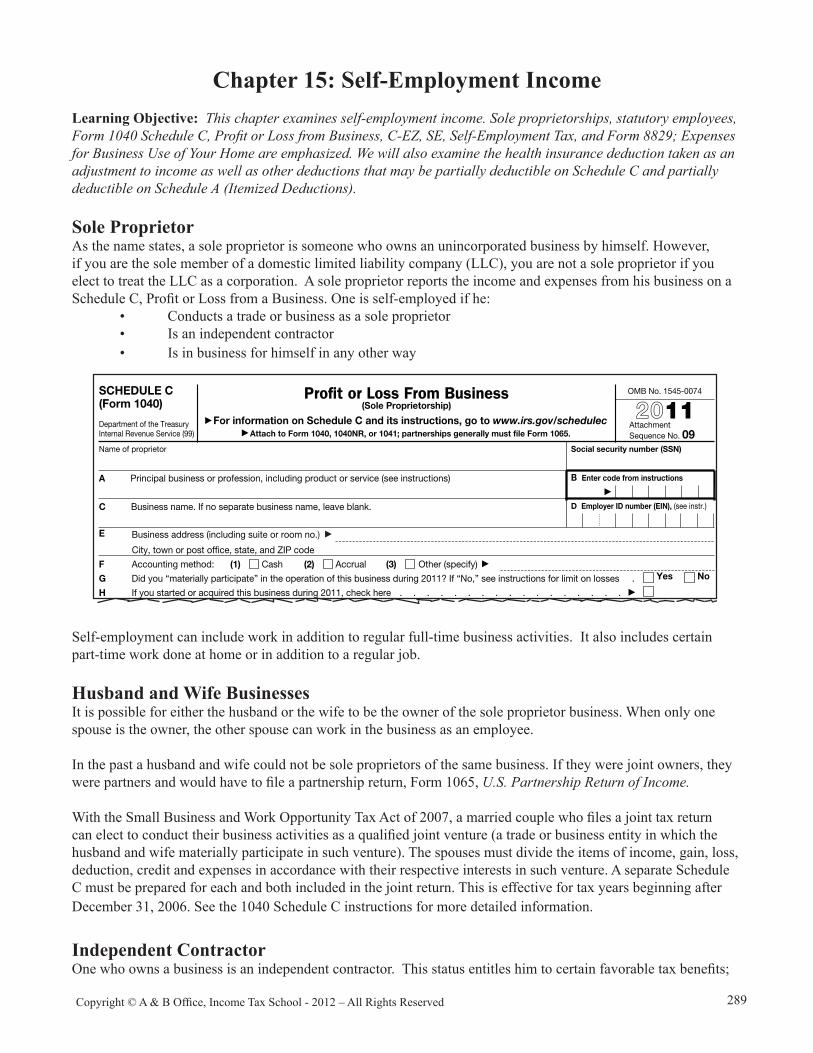

Chapter 15: Self-Employment Income Learning Objective: This chapter examines self-employment income. Sole proprietorships, statutory employees, Form 1040 Schedule C, Profit or Loss from Business, C-EZ, SE, Self-Employment Tax, and Form 8829; Expenses for Business Use of Your Home are emphasized. We will also examine the health insurance deduction taken as an adjustment to income as well as other deductions that may be partially deductible on Schedule C and partially deductible on Schedule A (Itemized Deductions).

Sole Proprietor As the name states, a sole proprietor is someone who owns an unincorporated business by himself. However, if you are the sole member of a domestic limited liability company (LLC), you are not a sole proprietor if you elect to treat the LLC as a corporation. A sole proprietor reports the income and expenses from his business on a Schedule C, Profit or Loss from a Business. One is self-employed if he: • Conducts a trade or business as a sole proprietor • Is an independent contractor • Is in business for himself in any other way

Self-employment can include work in addition to regular full-time business activities. It also includes certain part-time work done at home or in addition to a regular job.

Husband and Wife Businesses It is possible for either the husband or the wife to be the owner of the sole proprietor business. When only one spouse is the owner, the other spouse can work in the business as an employee.

In the past a husband and wife could not be sole proprietors of the same business. If they were joint owners, they were partners and would have to file a partnership return, Form 1065, U.S. Partnership Return of Income.

With the Small Business and Work Opportunity Tax Act of 2007, a married couple who files a joint tax return can elect to conduct their business activities as a qualified joint venture (a trade or business entity in which the husband and wife materially participate in such venture). The spouses must divide the items of income, gain, loss, deduction, credit and expenses in accordance with their respective interests in such venture. A separate Schedule C must be prepared for each and both included in the joint return. This is effective for tax years beginning after December 31, 2006. See the 1040 Schedule C instructions for more detailed information.

Independent Contractor One who owns a business is an independent contractor. This status entitles him to certain favorable tax benefits;

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Profit or Loss From Business (Sole Proprietorship)

▶ For information on Schedule C and its instructions, go to www.irs.gov/schedulec

▶ Attach to Form 1040, 1040NR, or 1041; partnerships generally must file Form 1065.

OMB No. 1545-0074

2011Attachment Sequence No. 09

Name of proprietor Social security number (SSN)

A Principal business or profession, including product or service (see instructions) B Enter code from instructions

▶

C Business name. If no separate business name, leave blank. D Employer ID number (EIN), (see instr.)

E Business address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F Accounting method: (1) Cash (2) Accrual (3) Other (specify) ▶

G Did you “materially participate” in the operation of this business during 2011? If “No,” see instructions for limit on losses . Yes No

H If you started or acquired this business during 2011, check here . . . . . . . . . . . . . . . . . ▶

I Did you make any payments in 2011 that would require you to file Form(s) 1099? (see instructions) . . . . . . . . Yes No

J If "Yes," did you or will you file all required Forms 1099? . . . . . . . . . . . . . . . . . . . . Yes No

Part I Income 1 a 1aMerchant card and third party payments. For 2011, enter -0- . . .

b Gross receipts or sales not entered on line 1a (see instructions) . . 1b

c

Income reported to you on Form W-2 if the “Statutory Employee” box on that form was checked. Caution. See instr. before completing this line 1c

d Total gross receipts. Add lines 1a through 1c . . . . . . . . . . . . . . . . . . 1d

2 Returns and allowances plus any other adjustments (see instructions) . . . . . . . . . . . 2

3 Subtract line 2 from line 1d . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Cost of goods sold (from line 42) . . . . . . . . . . . . . . . . . . . . . . 4

5 Gross profit. Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . 5

6 Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . 6

7 Gross income. Add lines 5 and 6 . . . . . . . . . . . . . . . . . . . . . ▶ 7 Part II Expenses Enter expenses for business use of your home only on line 30.

8 Advertising . . . . . 8

9

Car and truck expenses (see instructions) . . . . . 9

10 Commissions and fees . 10

11 Contract labor (see instructions) 11

12 Depletion . . . . . 12 13

Depreciation and section 179 expense deduction (not included in Part III) (see instructions) . . . . . 13

14

Employee benefit programs (other than on line 19) . . 14

15 Insurance (other than health) 15

16 Interest:

a Mortgage (paid to banks, etc.) 16a

b Other . . . . . . 16b

17 Legal and professional services 17

18 Office expense (see instructions) 18

19 Pension and profit-sharing plans . 19

20 Rent or lease (see instructions):

a Vehicles, machinery, and equipment 20a

b Other business property . . . 20b

21 Repairs and maintenance . . . 21

22 Supplies (not included in Part III) . 22

23 Taxes and licenses . . . . . 23

24 Travel, meals, and entertainment:

a Travel . . . . . . . . . 24a

b

Deductible meals and entertainment (see instructions) . 24b

25 Utilities . . . . . . . . 25

26 Wages (less employment credits) . 26

27 a Other expenses (from line 48) . . 27a

b Reserved for future use . . . 27b

28 Total expenses before expenses for business use of home. Add lines 8 through 27a . . . . . . ▶ 28

29 Tentative profit or (loss). Subtract line 28 from line 7 . . . . . . . . . . . . . . . . . 29

30 Expenses for business use of your home. Attach Form 8829. Do not report such expenses elsewhere . . 30

31 Net profit or (loss). Subtract line 30 from line 29.

• If a profit, enter on both Form 1040, line 12 (or Form 1040NR, line 13) and on Schedule SE, line 2. If you entered an amount on line 1c, see instr. Estates and trusts, enter on Form 1041, line 3.

• If a loss, you must go to line 32.} 31

32 If you have a loss, check the box that describes your investment in this activity (see instructions).

• If you checked 32a, enter the loss on both Form 1040, line 12, (or Form 1040NR, line 13) and on Schedule SE, line 2. If you entered an amount on line 1c, see the instructions for line 31. Estates and trusts, enter on Form 1041, line 3.

• If you checked 32b, you must attach Form 6198. Your loss may be limited.

} 32a All investment is at risk.

32b Some investment is not at risk.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11334P Schedule C (Form 1040) 2011

314 Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

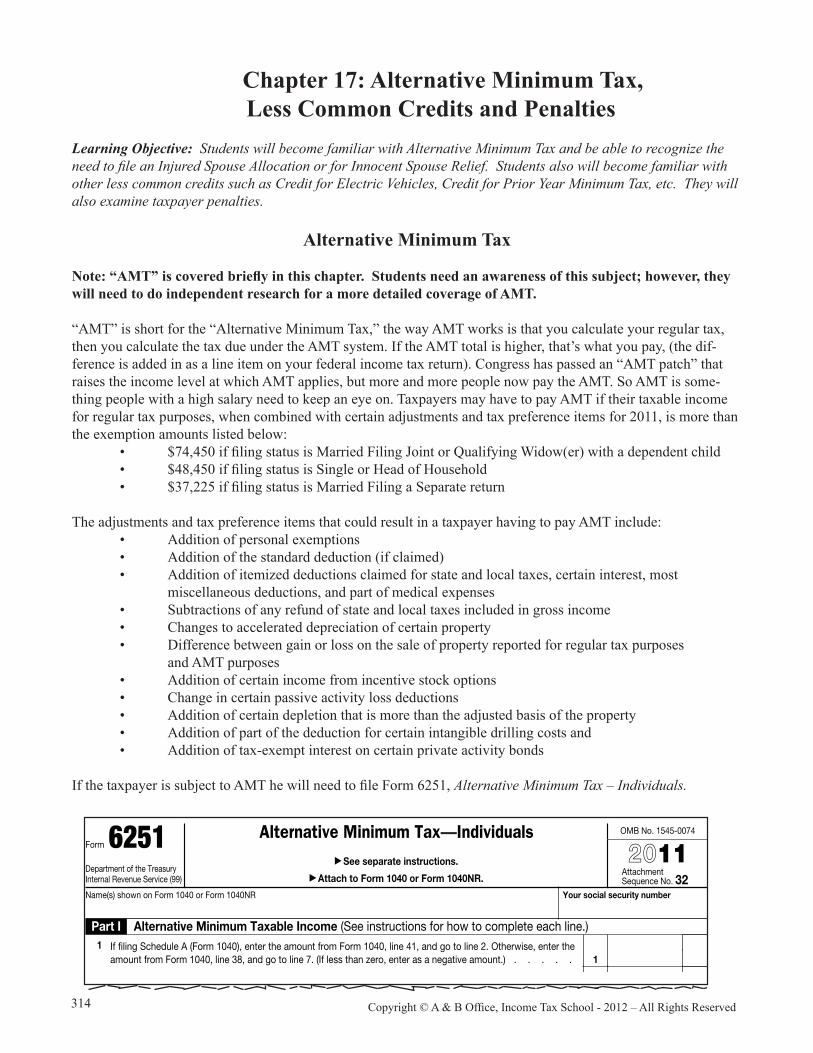

Chapter 17: Alternative Minimum Tax, Less Common Credits and Penalties Learning Objective: Students will become familiar with Alternative Minimum Tax and be able to recognize the need to file an Injured Spouse Allocation or for Innocent Spouse Relief. Students also will become familiar with other less common credits such as Credit for Electric Vehicles, Credit for Prior Year Minimum Tax, etc. They will also examine taxpayer penalties.

Alternative Minimum Tax

Note: “AMT” is covered briefly in this chapter. Students need an awareness of this subject; however, they will need to do independent research for a more detailed coverage of AMT.

“AMT” is short for the “Alternative Minimum Tax,” the way AMT works is that you calculate your regular tax, then you calculate the tax due under the AMT system. If the AMT total is higher, that’s what you pay, (the dif-ference is added in as a line item on your federal income tax return). Congress has passed an “AMT patch” that raises the income level at which AMT applies, but more and more people now pay the AMT. So AMT is some-thing people with a high salary need to keep an eye on. Taxpayers may have to pay AMT if their taxable income for regular tax purposes, when combined with certain adjustments and tax preference items for 2011, is more than the exemption amounts listed below: • $74,450iffilingstatusisMarriedFilingJointorQualifyingWidow(er)withadependentchild • $48,450iffilingstatusisSingleorHeadofHousehold • $37,225iffilingstatusisMarriedFilingaSeparatereturn The adjustments and tax preference items that could result in a taxpayer having to pay AMT include: • Additionofpersonalexemptions • Additionofthestandarddeduction(ifclaimed) • Additionofitemizeddeductionsclaimedforstateandlocaltaxes,certaininterest,most miscellaneous deductions, and part of medical expenses • Subtractionsofanyrefundofstateandlocaltaxesincludedingrossincome • Changestoaccelerateddepreciationofcertainproperty • Differencebetweengainorlossonthesaleofpropertyreportedforregulartaxpurposes and AMT purposes • Additionofcertainincomefromincentivestockoptions • Changeincertainpassiveactivitylossdeductions • Additionofcertaindepletionthatismorethantheadjustedbasisoftheproperty • Additionofpartofthedeductionforcertainintangibledrillingcostsand • Additionoftax-exemptinterestoncertainprivateactivitybonds

IfthetaxpayerissubjecttoAMThewillneedtofileForm6251,Alternative Minimum Tax – Individuals.

Form 6251Department of the Treasury Internal Revenue Service (99)

Alternative Minimum Tax—Individuals▶ See separate instructions.

▶ Attach to Form 1040 or Form 1040NR.

OMB No. 1545-0074

2011Attachment Sequence No. 32

Name(s) shown on Form 1040 or Form 1040NR Your social security number

Part I Alternative Minimum Taxable Income (See instructions for how to complete each line.) 1

If filing Schedule A (Form 1040), enter the amount from Form 1040, line 41, and go to line 2. Otherwise, enter the amount from Form 1040, line 38, and go to line 7. (If less than zero, enter as a negative amount.) . . . . . 1

2

Medical and dental. Enter the smaller of Schedule A (Form 1040), line 4, or 2.5% (.025) of Form 1040, line 38. If zero or less, enter -0- . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Taxes from Schedule A (Form 1040), line 9 . . . . . . . . . . . . . . . . . . . . . 3

4 Enter the home mortgage interest adjustment, if any, from line 6 of the worksheet in the instructions for this line . 4

5 Miscellaneous deductions from Schedule A (Form 1040), line 27 . . . . . . . . . . . . . . . 5

6 Skip this line. It is reserved for future use . . . . . . . . . . . . . . . . . . . . . . 6

7 Tax refund from Form 1040, line 10 or line 21 . . . . . . . . . . . . . . . . . . . . 7 ( )

8 Investment interest expense (difference between regular tax and AMT) . . . . . . . . . . . . . 8

9 Depletion (difference between regular tax and AMT) . . . . . . . . . . . . . . . . . . 9

10 Net operating loss deduction from Form 1040, line 21. Enter as a positive amount . . . . . . . . . 10

11 Alternative tax net operating loss deduction . . . . . . . . . . . . . . . . . . . . . 11 ( )

12 Interest from specified private activity bonds exempt from the regular tax . . . . . . . . . . . . 12

13 Qualified small business stock (7% of gain excluded under section 1202) . . . . . . . . . . . . 13

14 Exercise of incentive stock options (excess of AMT income over regular tax income) . . . . . . . . . 14

15 Estates and trusts (amount from Schedule K-1 (Form 1041), box 12, code A) . . . . . . . . . . . 15

16 Electing large partnerships (amount from Schedule K-1 (Form 1065-B), box 6) . . . . . . . . . . . 16

17 Disposition of property (difference between AMT and regular tax gain or loss) . . . . . . . . . . . 17

18 Depreciation on assets placed in service after 1986 (difference between regular tax and AMT) . . . . . . 18

19 Passive activities (difference between AMT and regular tax income or loss) . . . . . . . . . . . 19

20 Loss limitations (difference between AMT and regular tax income or loss) . . . . . . . . . . . . 20

21 Circulation costs (difference between regular tax and AMT) . . . . . . . . . . . . . . . . 21

22 Long-term contracts (difference between AMT and regular tax income) . . . . . . . . . . . . . 22

23 Mining costs (difference between regular tax and AMT) . . . . . . . . . . . . . . . . . 23

24 Research and experimental costs (difference between regular tax and AMT) . . . . . . . . . . . 24

25 Income from certain installment sales before January 1, 1987. . . . . . . . . . . . . . . . 25 ( )

26 Intangible drilling costs preference . . . . . . . . . . . . . . . . . . . . . . . 26

27 Other adjustments, including income-based related adjustments . . . . . . . . . . . . . . 27

28

Alternative minimum taxable income. Combine lines 1 through 27. (If married filing separately and line 28 is more than $223,900, see instructions.) . . . . . . . . . . . . . . . . . . . . . . 28

Part II Alternative Minimum Tax (AMT) 29 Exemption. (If you were under age 24 at the end of 2011, see instructions.)

IF your filing status is . . . AND line 28 is not over . . . THEN enter on line 29 . . .

Single or head of household . . . . . $112,500 . . . . . . $48,450

Married filing jointly or qualifying widow(er) . 150,000 . . . . . . 74,450

Married filing separately . . . . . . . 75,000 . . . . . . 37,225 } . . .

If line 28 is over the amount shown above for your filing status, see instructions.

29

30

Subtract line 29 from line 28. If more than zero, go to line 31. If zero or less, enter -0- here and on lines 31, 33, and 35, and go to line 34 . . . . . . . . . . . . . . . . . . . . . . . . . . 30

31 • If you are filing Form 2555 or 2555-EZ, see instructions for the amount to enter. • If you reported capital gain distributions directly on Form 1040, line 13; you reported qualified dividends

on Form 1040, line 9b; or you had a gain on both lines 15 and 16 of Schedule D (Form 1040) (as refigured for the AMT, if necessary), complete Part III on the back and enter the amount from line 54 here.

• All others: If line 30 is $175,000 or less ($87,500 or less if married filing separately), multiply line 30 by 26% (.26). Otherwise, multiply line 30 by 28% (.28) and subtract $3,500 ($1,750 if married filing separately) from the result.

} . . . 31

32 Alternative minimum tax foreign tax credit (see instructions) . . . . . . . . . . . . . . . . 32

33 Tentative minimum tax. Subtract line 32 from line 31 . . . . . . . . . . . . . . . . . . 33

34

Tax from Form 1040, line 44 (minus any tax from Form 4972 and any foreign tax credit from Form 1040, line 47). If you used Schedule J to figure your tax, the amount from line 44 of Form 1040 must be refigured without using Schedule J (see instructions) . . . . . . . . . . . . . . . . . . . . . 34

35 AMT. Subtract line 34 from line 33. If zero or less, enter -0-. Enter here and on Form 1040, line 45 . . . . . 35

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 13600G Form 6251 (2011)

25Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Name of person who received tips. If married, complete a separate Form 4137 for each spouse with unreported tips. Social security number

OMB No. 1545-0074Form 4137 Social Security and Medicare Tax

on Unreported Tip Income 2011Department of the TreasuryInternal Revenue Service (99)

G See instructions.G Attach to Form 1040, Form 1040NR, Form 1040NR-EZ, Form 1040-SS, or Form 1040-PR. Attachment

Sequence No. 24

BAA For Paperwork Reduction Act Notice, see your tax return instructions. FDIA4001 08/01/11 Form 4137 (2011)

2 Total cash and charge tips you received in 2011. Add the amounts from line 1,column (c) 2

3 Total cash and charge tips you reported to your employer(s) in 2011. Add the amounts from line 1,column (d) 3

4 Subtract line 3 from line 2. This amount is income you must include in the total on Form 1040, line 7; Form1040NR, line 8; or Form 1040NR-EZ, line 3 4

5 Cash and charge tips you received but did not report to your employer because the total was lessthan $20 in a calendar month (see instructions) 5

6 Unreported tips subject to Medicare tax. Subtract line 5 from line 4 67 Maximum amount of wages (including tips) subject to social security tax 7

8 Total social security wages and social security tips (total of boxes 3 and 7shown on your Form(s) W-2) or railroad retirement (tier 1) compensation 8

9 Subtract line 8 from line 7. If line 8 is more than line 7, enter -0- here and on line 10 and go to line 12 9

Unreported tips subject to social security tax. Enter the smaller of line 6 or line 9. If you received tips10as a federal, state, or local government employee, see instructions 10

11 Multiply line 10 by .042 (social security tax rate) 1112 Multiply line 6 by .0145 (Medicare tax rate) 12

13 Add lines 11 and 12. Enter the result here and on Form 1040, line 57; Form 1040NR, line 55; or Form1040NR-EZ, line 16 (Form 1040-SS and 1040-PR filers, see instructions.) 13

1 (a) Name of employer to whomyou were required to, but did not

report all your tips (see instructions)

(b) Employeridentification number

(see instructions)

(c) Total cash andcharge tips you

received (includingunreported tips)(see instructions)

(d) Total cash andcharge tips you

reported toyour employer

A

B

C

D

E

MARCIA BAKER 101-20-1234

2,525.

2,525.

200.

2,325.106,800.

15,273.

91,527.

2,325.

98.34.

132.

CARTER’S RESTAURANT 63-3305332 2,525.

3/3

15Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

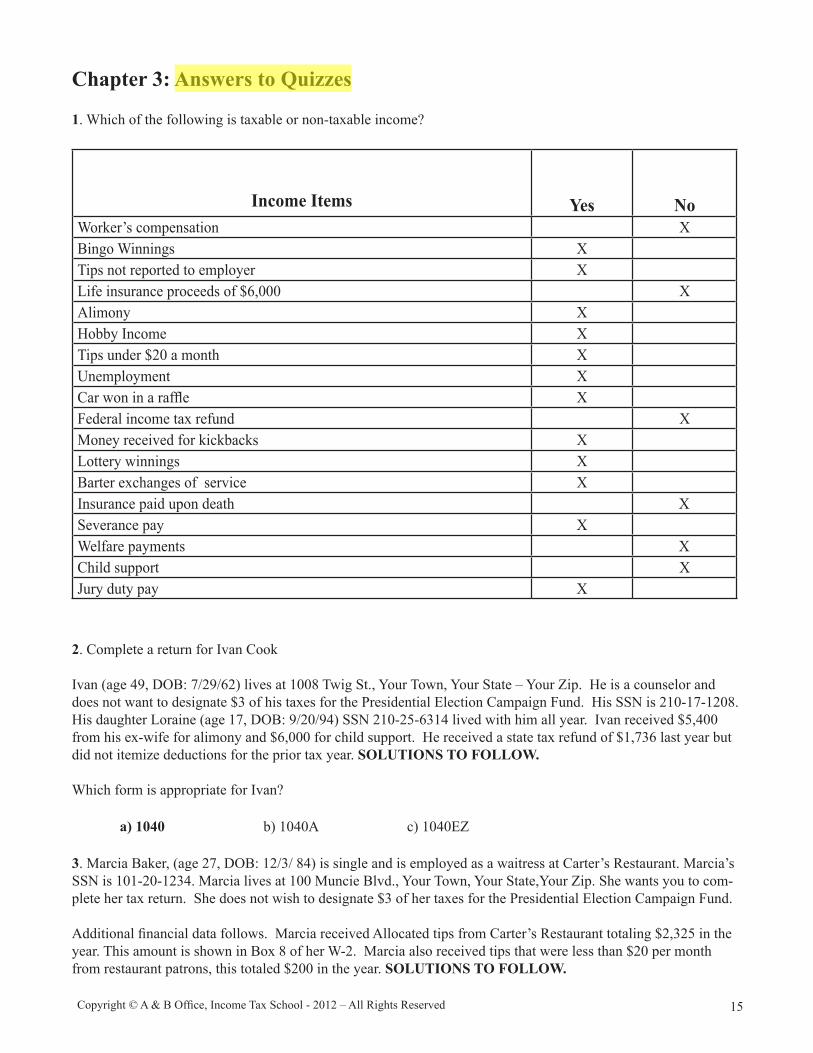

Chapter 3: Answers to Quizzes

1. Which of the following is taxable or non-taxable income?

2. Complete a return for Ivan Cook

Ivan (age 49, DOB: 7/29/62) lives at 1008 Twig St., Your Town, Your State – Your Zip. He is a counselor and does not want to designate $3 of his taxes for the Presidential Election Campaign Fund. His SSN is 210-17-1208. His daughter Loraine (age 17, DOB: 9/20/94) SSN 210-25-6314 lived with him all year. Ivan received $5,400 from his ex-wife for alimony and $6,000 for child support. He received a state tax refund of $1,736 last year but did not itemize deductions for the prior tax year. SOLUTIONS TO FOLLOW.

Which form is appropriate for Ivan?

a) 1040 b) 1040A c) 1040EZ

3. Marcia Baker, (age 27, DOB: 12/3/ 84) is single and is employed as a waitress at Carter’s Restaurant. Marcia’s SSN is 101-20-1234. Marcia lives at 100 Muncie Blvd., Your Town, Your State,Your Zip. She wants you to com-plete her tax return. She does not wish to designate $3 of her taxes for the Presidential Election Campaign Fund.

Additional financial data follows. Marcia received Allocated tips from Carter’s Restaurant totaling $2,325 in the year. This amount is shown in Box 8 of her W-2. Marcia also received tips that were less than $20 per month from restaurant patrons, this totaled $200 in the year. SOLUTIONS TO FOLLOW.

Income Items Yes NoWorker’s compensation XBingo Winnings XTips not reported to employer XLife insurance proceeds of $6,000 XAlimony XHobby Income XTips under $20 a month XUnemployment XCar won in a raffle XFederal income tax refund XMoney received for kickbacks XLottery winnings XBarter exchanges of service XInsurance paid upon death XSeverance pay XWelfare payments XChild support XJury duty pay X

26 Copyright © A & B Office, Income Tax School - 2012 – All Rights ReservedFDIA1312 10/25/11

Department of the Treasury ' Internal Revenue Service

Form 1040A U.S. Individual Income Tax Return (99) 2011 IRS Use Only ' Do not write or staple in this space.

Boxeschecked on6a and 6b

No. of childrenon 6c who:? livedwith you

? did notlive withyou due todivorce orseparation (seeinstructions)

Dependentson 6c notentered above

Add numberson lines above

6 a Yourself. If someone can claim you as a dependent, do not check box 6aExemptions

b Spousec Dependents:

(1) First name Last name

(2) Dependent’ssocial security

number

(3) Dependent’srelationship

to you

(4) bifchild under

age 17qual for

child tax cr(see instrs)

If more than sixdependents,see instructions.

d Total number of exemptions claimed

Income7 Wages, salaries, tips, etc. Attach Form(s) W-2 78 a Taxable interest. Attach Schedule B if required 8 a

b Tax-exempt interest. Do not include on line 8a 8 b9 a Ordinary dividends. Attach Schedule B if required 9 a

Attach Form(s)W-2 here. Alsoattach Form(s)1099-R if taxwas withheld. b Qualified dividends (see instructions) 9 b

10 Capital gain distributions (see instructions) 1011a IRA distributions 11a 11b Taxable amount 11b12a Pensions and annuities 12a 12b Taxable amount 12b

13 Unemployment compensation and Alaska Permanent Fund dividends(see instructions) 13

14a Social securitybenefits 14a 14b Taxable amount 14b

If you did notget a W-2,see instructions.

Enclose, butdo not attach,any payment.Also, pleaseuse Form 1040-V. 15 Add lines 7 through 14b (far right column). This is your total income 15

Your first name and initial Last name OMB No. 1545-0074

Your social security number

If a joint return, spouse’s first name and initial Last name Spouse’s social security number

Home address (number and street). If you have a P.O. box, see instructions. Apartment no.

JMake sure the SSN(s)above and on line 6care correct.

City, town or post office. If you have a foreign address, see instructions. State ZIP code Presidential Election Campaign

Foreign country name Foreign province/county Foreign postal code

Check here if you, or your spouse iffiling jointly, want $3 to go to thisfund. Checking a box below willnot change your tax orrefund.

1 Single 4 Head of household (with qualifying person). (See instructions.)Filingstatus 2 Married filing jointly (even if only one had income) If the qualifying person is a child but not your dependent,

3 Married filing separately. Enter spouse’s SSN above and enter this child’s name here

full name here 5 Qualifying widow(er) with dependent childCheck onlyone box. (see instructions)

You Spouse

16 Educator expenses (see instructions) 1617 IRA deduction (see instructions) 1718 Student loan interest deduction (see instructions) 1819 Tuition and fees. Attach Form 8917 19

Adjustedgrossincome

20 Add lines 16 through 19. These are your total adjustments 20

21 Subtract line 20 from line 15. This is your adjusted gross income 21BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Form 1040A (2011)

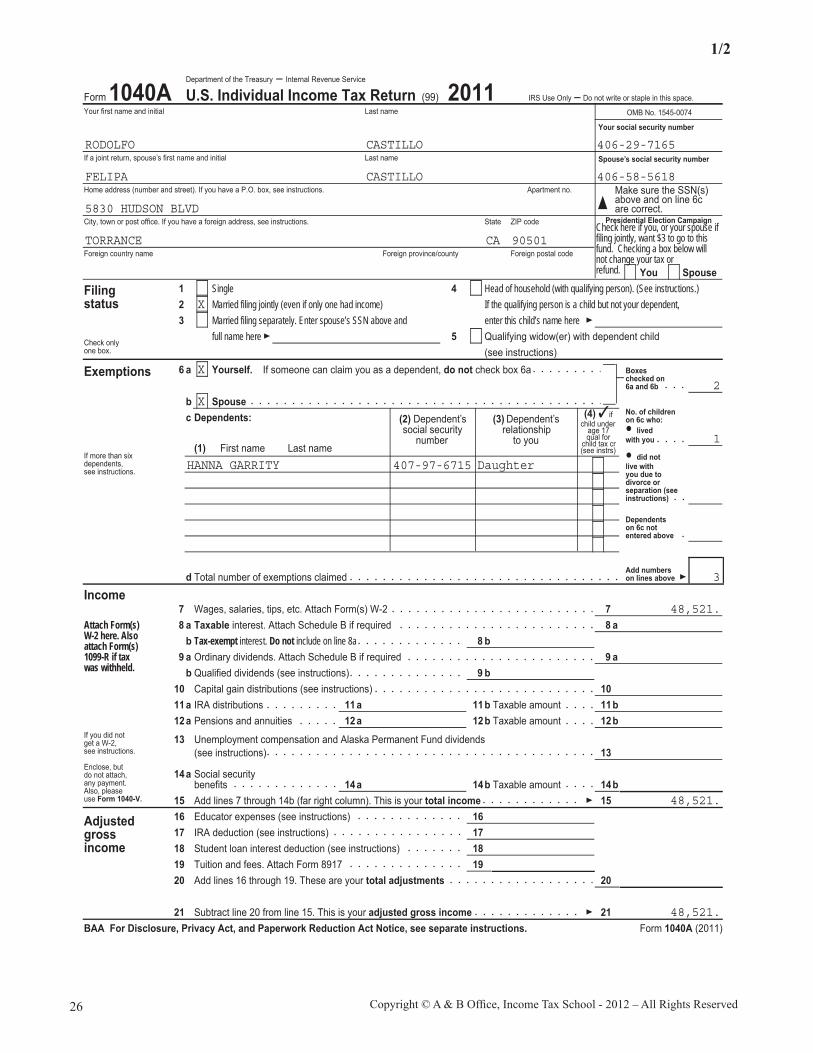

RODOLFO CASTILLO 406-29-7165

FELIPA CASTILLO 406-58-5618

5830 HUDSON BLVD

TORRANCE CA 90501

X

X

X2

1

3

48,521.

48,521.

48,521.

HANNA GARRITY 407-97-6715 Daughter

1/2

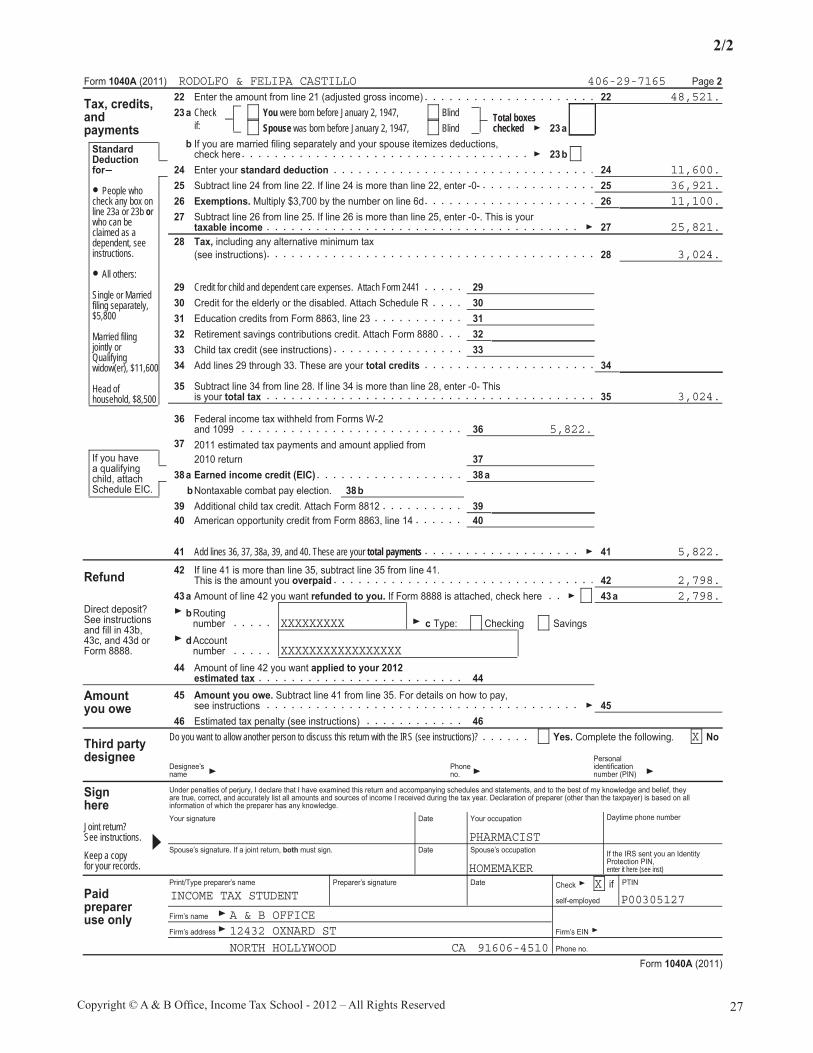

27Copyright © A & B Office, Income Tax School - 2012 – All Rights Reserved

Form 1040A (2011) Page 222 Enter the amount from line 21 (adjusted gross income) 2223a Check You were born before January 2, 1947, Blind

if: Spouse was born before January 2, 1947, BlindTotal boxeschecked 23a

Tax, credits,andpayments

b If you are married filing separately and your spouse itemizes deductions,check here 23b

24 Enter your standard deduction 2425 Subtract line 24 from line 22. If line 24 is more than line 22, enter -0- 2526 Exemptions. Multiply $3,700 by the number on line 6d 2627 Subtract line 26 from line 25. If line 26 is more than line 25, enter -0-. This is your

taxable income 2728 Tax, including any alternative minimum tax

(see instructions) 28

29 Credit for child and dependent care expenses. Attach Form 2441 2930 Credit for the elderly or the disabled. Attach Schedule R 3031 Education credits from Form 8863, line 23 3132 Retirement savings contributions credit. Attach Form 8880 3233 Child tax credit (see instructions) 3334 Add lines 29 through 33. These are your total credits 34

35 Subtract line 34 from line 28. If line 34 is more than line 28, enter -0- Thisis your total tax 35

36 Federal income tax withheld from Forms W-2and 1099 362011 estimated tax payments and amount applied from372010 return 37

38a Earned income credit (EIC) 38abNontaxable combat pay election. 38b