Embed Size (px)

Citation preview

ClaibornElectronics wasproud of their

new activity-basedcosting (ABC) system,which they hadinstalled as a “proof ofconcept” model intheir Test Division.(This division manu-factured electronic testand measurement equipment forsale in the telecommunicationsindustry.) Previously, directlabor hours were used to allo-cate manufacturing overhead toproduct. Now, after a year’sstudy and installation, theirABC system was up and run-ning, and relied on cost driversthat “captured the underlyingnature” of their processes. Theyused numbers of parts, numbersof part insertions, and directmaterial costs as allocationbases. However, could theyexpect to receive the frequentlyheralded benefits of ABC?Indeed, the question is morebasic: Do they in fact have anABC system?

ABC: THE BASIC IDEA

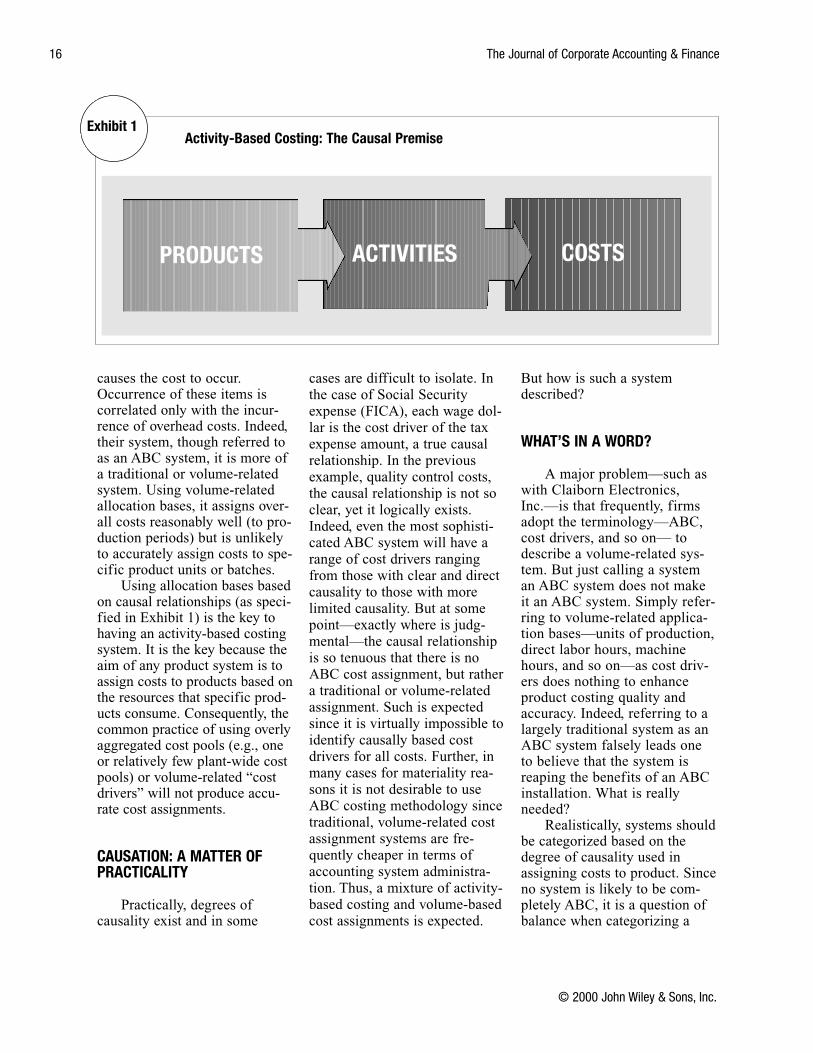

Activity-based costing ispremised on that idea that prod-ucts cause activities that causecosts to occur and that thesecosts should be assigned to theproducts that caused them. (SeeExhibit 1.)

Thus, a product might cause,for example, quality controlinspections and testing thatwould have the direct costs ofquality control inspectors, costof testing equipment, costs ofproduct destroyed duringdestructive testing, and so on.Assuming that the inspectionactivity is triggered whenever a

batch of product isproduced, producing abatch of product caus-es these costs to occur,and thus, they shouldbe assigned to theproduct batch thatcaused them. In fact,an overhead applica-tion rate would bedeveloped to assign

these costs to the product, thatis, budgeted quality control costsdivided by budgeted productionbatches equals quality controlapplication rate. Here, we referto batches of production as thecost driver, where a cost driver isan event whose occurrence caus-es the activity to occur.

Claiborn Electronics usednumbers of parts, part inser-tions, and direct labor dollars astheir “cost drivers” even thoughspecific causal relationships arelacking. Surely, the number ofparts in a product is correlatedwith the overhead cost incur-rence, but one cannot say thathaving a number of parts, inser-tions, or direct material dollars

15© 2000 John Wiley & Sons, Inc.

Claiborn Electronics was proud of their TestDivision’s new activity-based costing (ABC) sys-tem. After all, it took a year to research and install.But in spite of all that effort, did they really havean ABC system?

© 2000 John Wiley & Sons, Inc.

Frank Collins

Activity-Based Costing: Losing the Promise

featu

reartic

le

causes the cost to occur.Occurrence of these items iscorrelated only with the incur-rence of overhead costs. Indeed,their system, though referred toas an ABC system, it is more ofa traditional or volume-relatedsystem. Using volume-relatedallocation bases, it assigns over-all costs reasonably well (to pro-duction periods) but is unlikelyto accurately assign costs to spe-cific product units or batches.

Using allocation bases basedon causal relationships (as speci-fied in Exhibit 1) is the key tohaving an activity-based costingsystem. It is the key because theaim of any product system is toassign costs to products based onthe resources that specific prod-ucts consume. Consequently, thecommon practice of using overlyaggregated cost pools (e.g., oneor relatively few plant-wide costpools) or volume-related “costdrivers” will not produce accu-rate cost assignments.

CAUSATION: A MATTER OFPRACTICALITY

Practically, degrees ofcausality exist and in some

cases are difficult to isolate. Inthe case of Social Securityexpense (FICA), each wage dol-lar is the cost driver of the taxexpense amount, a true causalrelationship. In the previousexample, quality control costs,the causal relationship is not soclear, yet it logically exists.Indeed, even the most sophisti-cated ABC system will have arange of cost drivers rangingfrom those with clear and directcausality to those with morelimited causality. But at somepoint—exactly where is judg-mental—the causal relationshipis so tenuous that there is noABC cost assignment, but rathera traditional or volume-relatedassignment. Such is expectedsince it is virtually impossible toidentify causally based costdrivers for all costs. Further, inmany cases for materiality rea-sons it is not desirable to useABC costing methodology sincetraditional, volume-related costassignment systems are fre-quently cheaper in terms ofaccounting system administra-tion. Thus, a mixture of activity-based costing and volume-basedcost assignments is expected.

But how is such a systemdescribed?

WHAT’S IN A WORD?

A major problem—such aswith Claiborn Electronics,Inc.—is that frequently, firmsadopt the terminology—ABC,cost drivers, and so on— todescribe a volume-related sys-tem. But just calling a systeman ABC system does not makeit an ABC system. Simply refer-ring to volume-related applica-tion bases—units of production,direct labor hours, machinehours, and so on—as cost driv-ers does nothing to enhanceproduct costing quality andaccuracy. Indeed, referring to alargely traditional system as anABC system falsely leads oneto believe that the system isreaping the benefits of an ABCinstallation. What is reallyneeded?

Realistically, systems shouldbe categorized based on thedegree of causality used inassigning costs to product. Sinceno system is likely to be com-pletely ABC, it is a question ofbalance when categorizing a

16 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

Exhibit 1Activity-Based Costing: The Causal Premise

COSTSACTIVITIESPRODUCTS

system as ABC or not. Avoid thetemptation to refer to a largelyvolume-based system as ABC.Furthermore, to prevent overlyestimating the extent of causalassignment, all application basesshould not be referred to as“cost drivers,” only those thatreasonably seem to be causallybased.

REDUCING COST DRIVERSREDUCES THE COST

Here’s another sober-ing story for you to consid-er. Thermostatics, Inc. wason a major cost reductionand quality improvementprogram and hoped thattheir ABC system wouldhelp. They manufacturedrelays, timers, and thermostatsthat were installed in automo-biles, kitchen appliances andlaundry appliances. They identi-fied and used a number of batch-and product-related cost drivers(e.g., production batches forstock transfer costs, number ofengineering change notices perproduct line, setup costs per pro-duction run, etc.) in addition tovolume-related measure whereno true cost driver could befound (total production hours,number of parts per products,etc.). Yet, there was disappoint-ment because although they hadreduced some of the cost driverquantities (for example, havinglarger production batches toreduce the number of productionruns), few cost reductionsoccurred—nor was qualitymarkedly improved. Though theABC study provided impetus fordesigning products with fewerparts, great resistance to thesechanges developed amongdesign engineers and marketing

personnel due to potential effectson quality.

A common misconception isthat reducing cost drivers willlead to commensurate costreductions. Not so, becauseunless you have a “pure” costdriver—such as in the case ofSocial Security expense—reduc-ing the driver consumption quan-tity will not necessarily result incost reductions. Take, for exam-

ple, the earlier example of quali-ty control costs that wereassigned to product using pro-duction batches as a cost driver.Reducing the number of batchesby increasing units per batchwill not reduce costs proportion-ately. Only variable costs will sodiminish. The remaining costsare those that over the long termhave increased (sometimesresulting from “cost creep,”where with little notice there is agradual increase of the costs).Management action must betaken to reduce these costs. If,for example, increased batch sizeand resultantly fewer batcheseliminated the need for one qual-ity control inspector, this posi-tion must be eliminated for thiscost to go away. Simply reducingthe driver consumption (batches)does not reduce this part of thecost.

This is not to say that ABCmethodology is ineffective incost reductions. Rather, it canpoint to activities that might be

restructured or eliminated.Often, these opportunitiesbecome apparent during the sys-tem design and installation phaseof an ABC system, for it is fre-quently necessary to analyzeproductive processes in order toidentify cost drivers of productcosts. It is at this point thatwasteful activities can be discov-ered, and steps taken to eliminatethem.

Traditionally, account-ants think of two cost cate-gories: variable and fixed.Yet, there is a third catego-ry, referred to as long-termvariable costs (costs thatvary over the long run). Tocounteract this tendency,one should recognize the“Law of Two,” which holdsthat if a company has more

than one machine, person,department, or process that per-forms the same function as theother—for instance, three secre-taries in a stenographic pool, twoquality control inspectors, tendelivery trucks—that at one timefewer than the present numberaccomplished the task. Perhapsat one time there was only onesecretary, one inspector, or onetruck. These are the costs thatover the long term haveincreased, sometimes resultingfrom “cost creep.” So coupledwith an ABC analysis and thecritical perspective produced byrecognizing the Law of Two, onecan take steps to achieve truecost reductions.

DIRECT LABOR INERTIA

Until recently, many over-head application systems useddirect labor measures (directlabor hours or direct labor dol-lars) or machine hours to apply

March/April 2000 17

© 2000 John Wiley & Sons, Inc.

A common misconception is thatreducing cost drivers will lead tocommensurate cost reductions.

overhead to product.Accompanying this approach,extensive variance analyses wereperformed to isolate labor effi-ciency and rate variances.Further, analyses were extendedto fixed manufacturing overheadto include the volume variance.Many supervisor and departmentmanager performance reviewsdepended heavily on the per-formance of these variances.

Yet, in an activity-basedatmosphere, we find that thereare other items that drive costsmore profoundly than labor andmachine-hour quantities, particu-larly as businesses become moremechanized and computerized.Often, much of the product costis built into the product duringthe design phase. Later, true costelimination/reduction comesonly after a careful ABC analysisand managerial action.

Nevertheless, these labor-and machine-hour-based meas-ures seem to have a life of theirown and are routinely calculated

even though their relevance ismuch reduced. Indeed, excessivefocus on reducing efficiency andfixed overhead volume variancesmay lead to dysfunctional activi-ty, such as excessive production,even as many companies movetoward just-in-time inventoryprocesses.

WHEN IS THE PROMISE LOST?

Activity-based costing is arevolutionary approach to prod-uct costing and strategic costanalyses that has producedgreat benefits in many cases.Yet, the promise of ABC iscommonly diminished in threecases:

• Identifying a system as ABCwhen it is not.

• Assuming cost reductionnecessarily flows fromreduction in cost drivers.

• Continuing focus on laborand machine hour variances.

The first instance can leadexecutives of an organization tomistakenly believe that theyhave a state-of-the-art system,when really their system repre-sents a source of unrealizedopportunities for better productcosting and cost control. Thesecond mistake misdirects activ-ity away from true cost reduc-tion steps. And the third errordistracts attention from trulyimportant product costing andcontrol factors.

Pay attention to thesecaveats so you will not lose thebenefits of ABC, as too manycompanies have.

18 The Journal of Corporate Accounting & Finance

© 2000 John Wiley & Sons, Inc.

Frank Collins, Ph.D., CPA, is currently PriceWaterhouseCoopers Professor of Accounting at the Universityof Miami. He has extensive experience in advanced cost application procedures, including serving as thechair of the Management Accounting Section of the American Accounting Association’s annual conferenceon cost/management issues.