Embed Size (px)

Citation preview

Actuarial

Valuation Hot Topics

March 4, 2013

1

Introduction and Agenda

Shawna MeyerCorporate Vice President and ActuaryNew York Life

GAAP Issues Relating to Inforce Rate IncreasesIncreases

Ed Mullen Implications of HoldingEd MullenVice President and Appointed ActuaryPhysicians Mutual Insurance Co.

Implications of Holding Contract Reserves and Claim Reserves for Persons on ClaimPersons on Claim

Carl Friedrich ValuationCarl FriedrichConsulting Actuary and PrincipalMilliman Inc.

Valuation Considerations -Combination Plans

2Session 09: Valuation Hot Topics

Actuarial

GAAP Issues Relating to Inforce RateGAAP Issues Relating to Inforce Rate Increases

Shawna Meyer, FSA, MAAACorporate Vice President and Actuary

New York LifeNew York Life

March 4, 2013

3

Loss Recognition Testing

• DAC asset must be supportable from future profits:PV Premium + Reserves > PV Claims + PV Expenses If this test is failed, DAC should be reduced and a

loss should be taken immediately whenloss should be taken immediately when1. Loss is recognized as likely2. Amount can be reasonably estimated

Performed on inforce policies as of valuation date Should perform test periodically at least annually

4Session 09: Valuation Hot Topics

Recoverability Testing

• Similar to loss recognition but performed at issue

• Method:– GPV– GPV – Compare net to gross premiums

5Session 09: Valuation Hot Topics

Reserve Testing

• If you fail either test typically:– Reduce DAC, if this is not enough theneduce C, s s o e oug e– Increase Reserves

• Assumptions are “locked in”• Assumptions are locked in– Cannot unlock unless you are in loss

recognitionrecognition– SEC no longer allows prospective unlocking

6Session 09: Valuation Hot Topics

FAS 60 Paragraph 37Profits Followed by Losses

• If you have profits in early years followed by losses in later years, the liability needs y y , yto be increased to offset the losses– No guidance on how to set up this additional g p

reserve– Rate increases can create this situation

because additional premium has a different pattern than the expenses

7Session 09: Valuation Hot Topics

FAS 60 Paragraph 37Example 1 – Original Pricing

• Loss Ratio: 60%• Profit / Premium: 12%Profit / Premium: 12%

Valuation Date Net GAAP Reserve PV of Cash Flows* Margin Margin/PV Prem

1/1/2013 (45,937) (166,385) 120,448 12%

1/1/2016 115,014 13,165 101,849 12%

1/1/2019 242,856 159,600 83,256 12%

1/1/2022 331,517 266,467 65,050 12%

1/1/2025 372,520 324,651 47,868 12%

1/1/2028 317,407 285,949 31,458 12%

1/1/2031 197 807 182 228 15 579 12%

8Session 09: Valuation Hot Topics

1/1/2031 197,807 182,228 15,579 12%

*PV of Cash Flows = PV Claims + PV Expenses – PV Premium

FAS 60 Paragraph 37Example 2 – Higher Claims

• Loss Ratio: 72%• Profit / Premium: ‐2%Profit / Premium: 2%

Valuation Date Net GAAP Reserve PV of Cash Flows* Margin Margin/PV Prem

1/1/2013 (45,937) (13,427) (32,511) -3%

1/1/2016 115,014 184,319 (69,305) -8%

1/1/2019 242,856 346,168 (103,312) -15%

1/1/2022 331,517 461,858 (130,341) -24%

1/1/2025 372,520 517,051 (144,531) -36%

1/1/2028 317,407 447,448 (130,042) -49%

1/1/2031 197 807 283 530 (85 723) -65%

9Session 09: Valuation Hot Topics

1/1/2031 197,807 283,530 (85,723) -65%

*PV of Cash Flows = PV Claims + PV Expenses – PV Premium

FAS 60 Paragraph 37Example 3 – With Rate Increase

• Loss Ratio: 60%• Profit / Premium: 16%Profit / Premium: 16%

• Rate Increase: 20%Valuation Date Net GAAP Reserve PV of Cash Flows* Margin Margin/PV Premg g

1/1/2013 (46,240) (222,748) 176,811 335%

1/1/2016 108,537 7,320 107,695 61%

1/1/2019 218,492 201,481 41,375 18%

1/1/2022 277,999 348,809 (17,292) -7%

1/1/2025 277,378 433,862 (61,342) -22%

1/1/2028 182,286 392,779 (75,372) -25%

1/1/2031 90 2 3 2 6 6 ( 8 6 9) 18%

10Session 09: Valuation Hot Topics

1/1/2031 90,273 256,456 (58,649) -18%*PV of Cash Flows = PV Claims + PV Expenses – PV Premium

FAS 60 Paragraph 37Example 1 – Original Pricing

O i i l P i d Cl i

100,000

120,000

Original Premiums and ClaimsPV Claims / PV Prem = 60%

40,000

60,000

80,000

‐

20,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Original Premium Original ClaimsOriginal Premium Original Claims

11Session 09: Valuation Hot Topics

FAS 60 Paragraph 37Example 3 – With Rate Increase

O i i l d R i d P i d Cl i

140,000

160,000

Original and Revised Premiums and ClaimsPV Claims / PV Prem = 60%

40 000

60,000

80,000

100,000

120,000

‐

20,000

40,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Original Premium Original Claims New Premium New ClaimsOriginal Premium Original Claims New Premium New Claims

12Session 09: Valuation Hot Topics

FAS 60 Paragraph 37Example 3 – With Rate Increase

Additi l P i d Cl i

100,000.0

120,000.0

Additional Premiums and ClaimsPV Claims / PV Prem = 60%

40,000.0

60,000.0

80,000.0

‐

20,000.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Additional Premium Additional ClaimsAdditional Premium Additional Claims

13Session 09: Valuation Hot Topics

Internal Replacements

• Insureds may choose to decrease benefit options to offset premium increasep p

• Must determine if this constitutes an internal replacementinternal replacement

• Paragraph 10 – not an internal replacement if:replacement if:– Reduction if coverage

A ll d i th t t– As allowed in the contract• Further defined in paragraph 9 and 15

14Session 09: Valuation Hot Topics

Internal Replacements

• Paragraph 20:– “Where the modification is a reduction in e e e od ca o s a educ o

benefits with a directly proportionate reduction in premiums, the modification should result in an immediate proportionate reduction in unamortized deferred acquisition costs”

– Proportionate reduction should be based on ORIGINAL premium

15Session 09: Valuation Hot Topics

Actuarial

Implications of Holding Contract R d Cl i R fReserves and Claim Reserves for

Persons on Claim

Ed Mullen FSA MAAAEd Mullen, FSA, MAAAVice President and Appointed Actuary

Physicians Mutual Insurance Co.

March 4, 2013

16

Intuitive Question

Who has asked, or been asked, the following question:g q

“If we are holding a contract (aka “activeIf we are holding a contract (aka active life”) reserve, when someone goes on claim and we set up a claim (aka “disabled life”)and we set up a claim (aka disabled life ) reserve, aren’t we ‘over-reserving’?”

17Session 09: Valuation Hot Topics

Industry Practice

Milliman LTC Valuation Surveys*

• 2006 Survey– “Almost all companies surveyed held active life p y

reserves for those on claim.”• 2012 Survey

– 21 of 25 companies hold both a contract reserve and a claim reserve for persons on claim

*Courtesy of Allen Schmitz, Milliman Inc.

18Session 09: Valuation Hot Topics

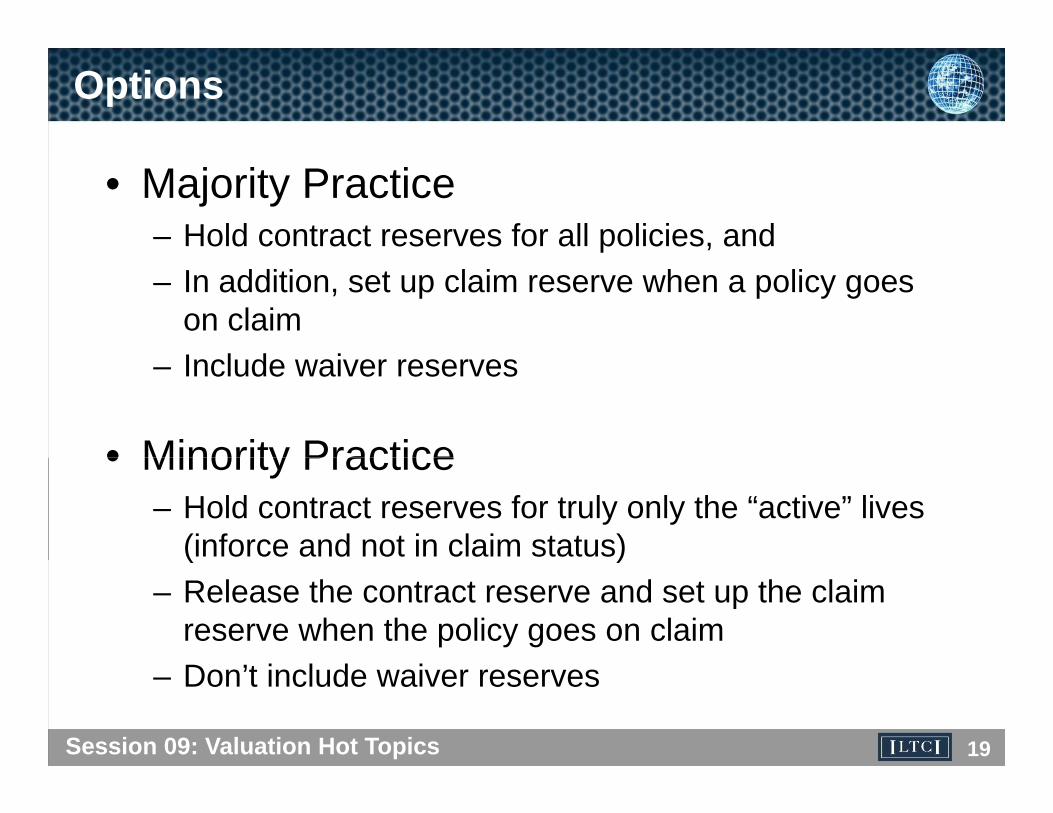

Options

• Majority Practice– Hold contract reserves for all policies, and– In addition, set up claim reserve when a policy goes

on claimI l d i– Include waiver reserves

• Minority Practice• Minority Practice– Hold contract reserves for truly only the “active” lives

(inforce and not in claim status)( )– Release the contract reserve and set up the claim

reserve when the policy goes on claim

19Session 09: Valuation Hot Topics

– Don’t include waiver reserves

Regulatory Authority/Guidance

• Appendix A-010 Minimum Reserve Standards for Individual and Group Health Insurance Contracts (NAIC HIRMR)(NAIC HIRMR)– Contract Reserves 33c. “The contract reserve is in addition to

claim reserves and premium reserves.”A di A E hibit 2 di W i f P i d th– Appendix A, Exhibit 2: discusses Waiver of Premium and the exposure basis of the underlying claim costs (disability).

• SSAP #54 Individual and Group and Accident Health Insurance Contracts– Paragraph 8: “The aggregate reserve for individual and group

accident and health contracts generally consists of a policy g y p yreserve and a claim reserve as well as certain other miscellaneous reserve…”

20Session 09: Valuation Hot Topics

Regulatory Authority/Guidance

• NAIC Health Insurance Reserves Guidance Manual– Section III. Claim Reserves B. Relationship to Other Reserves:

“The claim reserve is in addition to deficiency and contractThe claim reserve is in addition to deficiency and contract reserves….”

– Section IV. Contract Reserves A. General Definition: “Contract reserves are in addition to claim and premium reserves ”reserves are in addition to claim and premium reserves.

• AAA Health Practice Council Practice Note: Statutory Reserves for Individual Disability Income Insurance– Q: Is it redundant to hold active life reserves on policies with

open claims? A: No, active life reserves typically are calculated on all policies, whether on claim or not. In the development of l i f i lif i ll b dclaim costs for active life reserves, exposure is usually based on

all in-force policies without regard to claim status. Policies on claim normally continue in force, often due to the waiver-of-premium provision

21Session 09: Valuation Hot Topics

premium provision

Other topical references

• 1995 Society of Actuaries Long-Term Care Insurance Valuation Methods Task Force Final Report

– Page 66: “The approach used to compute Active Life Reserves (ALR) generally will d t i hi h f t t h i h ld b l d t l l W i f P idetermine which of two techniques should be employed to properly value Waiver of Premium Benefits.” If the ALR assumes future premiums are received form all inforce policies regardless of benefit status, a correcting adjustment is necessary. This is commonly accomplished by explicitly recognizing future waived premiums as an additional benefit amount. The adjusted benefit amount is applied to Active Life Reserve and Claim Reserve j ppfactors. If the ALR omits premiums to be waived from the present value of future premiums, then no additional adjustments may be required. When properly constructed, either approach can be expected to produce equivalent aggregate reserves.”

• Individual Health Insurance edited by Francis O’Grady 1988d dua ea t su a ce ed ted by a c s O G ady 988– Chapter 5, page 113: “…This view is somewhat dependent on whether or not

the tabular reserve claim costs were developed for active lives only or for active and disabled lives combined (and similarly on whether tabular reserves are maintained on active lives only or on total lives) Under this view if grossmaintained on active lives only or on total lives)…Under this view, if gross premiums were calculated assuming that premiums and claims stem only from active lives, then no additional claim liability is seen to arise for policyholders under waiver…”

22Session 09: Valuation Hot Topics

Claim Cost Exposure

• The key is in the claim cost exposures.• It dictates the approachIt dictates the approach.• Difficulty getting management to accept it:

– Not intuitive– Not intuitive– Nuances/proof are embedded in the underlying calculations

23Session 09: Valuation Hot Topics

Sizing things up:

• What is distinctively absent:– theoretical/algebraic demonstration/proof.– or, even a convincing layperson’s argument.– certainly discussion of the pros and cons of the

happroaches

• Today, with an (admittedly) elementary Excel worksheet:– “prove” equivalence by example, and,…– more interestingly, explore the implications when

i diff f t ti

24Session 09: Valuation Hot Topics

experience differs from expectations.

Example

• First project number of lives: total, actives, disabled– Total lives reduced by 94GAM deaths– Disabled life mortality rates are a multiple of total mortality rates– Active life mortality is the balancey– Claim incidence is arbitrary, benefits for duration of projection

• Project reserve balances– Contract reserves and disabled live reserves

• Project income statement on net basisN t i– Net premiums

– Investment income rate = valuation rate

25Session 09: Valuation Hot Topics

Projection of “Lives” by status

1000

1200

800

600 All Lives

Active Lives

Disable Lives

400

0

200

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

26Session 09: Valuation Hot Topics

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Reserve Equivalency (base scenario)

Majority Practice: All Lives Minority Practice: Active Lives OnlyPolicy Total Policy Claim Claim Total Policy Active Policy Claim Total

Duration Lives Reserve Reserve Waiver Reserve Duration Lives Reserve Reserve Reserve(EOY) (w/WOP) (ex.WOP) Reserve (EOY)

1000.0 1000.0

1 991.4 10,223 9,805 553 20,581 1 988.9 10,776 9,805 20,581

2 981.8 20,950 18,840 1,062 40,853 2 976.8 22,012 18,840 40,853

3 971.2 31,961 27,284 1,538 60,783 3 963.7 33,499 27,284 60,783

4 959.8 43,038 35,293 1,990 80,321 4 949.7 45,028 35,293 80,321

5 947.6 53,953 43,014 2,425 99,392 5 934.7 56,379 43,014 99,392

6 934.6 64,455 50,585 2,852 117,893 6 918.6 67,308 50,585 117,893

7 920.6 74,254 58,148 3,279 135,681 7 901.2 77,533 58,148 135,681

8 905.4 83,004 65,850 3,713 152,566 8 882.0 86,717 65,850 152,566

9 888.8 90,286 73,845 4,164 168,295 9 860.8 94,450 73,845 168,295

10 870 7 95 594 82 295 4 640 182,530 10 837 1 100 235 82 295 182,530

27Session 09: Valuation Hot Topics

10 870.7 95,594 82,295 4,640 182,530 10 837.1 100,235 82,295 182,530

Net Income (base scenario)

Majority Practice: All LivesChg. In "Paid" Chg. In Chg. In

Cash Waiver Total Inv. Paid Claim Wvr Prem Wvr Prem Total PolicyYr Premiums Premiums Premiums Inc Claims Reserve Claims Reserve Claims Reserve IncomeYr. Premiums Premiums Premiums Inc. Claims Reserve Claims Reserve Claims Reserve Income1 19,790 0 19,790 792 0 9,805 0 553 10,358 10,223 0 2 19,570 49 19,619 1,606 905 9,035 49 509 10,498 10,726 0 3 19,331 98 19,429 2,407 1,807 8,443 98 476 10,825 11,011 0 4 19,072 148 19,220 3,194 2,728 8,009 148 452 11,336 11,077 0 5 18,794 200 18,993 3,965 3,687 7,720 200 435 12,043 10,915 0

10 17,035 554 17,589 7,413 10,213 8,450 554 476 19,694 5,308 0 15 13,978 1,464 15,441 9,078 26,998 10,370 1,464 585 39,416 (14,897) 0

All yrs 314,526 23,551 338,077 119,837 434,363 0 23,551 0 457,913 0 0

Minority Practice: Active Lives OnlyMinority Practice: Active Lives OnlyChg. In Chg. In Chg. In

Cash Waiver Total Inv. Paid Claim Wvr Prem Wvr Prem Total PolicyYr. Premiums Premiums Premiums Inc. Claims Reserve Claims Reserve Claims Reserve Income1 19,790 0 19,790 792 0 9,805 0 0 9,805 10,776 0 2 19,570 0 19,570 1,606 905 9,035 0 0 9,940 11,236 0 3 19,331 0 19,331 2,407 1,807 8,443 0 0 10,251 11,487 0 4 19,072 0 19,072 3,194 2,728 8,009 0 0 10,737 11,529 0 5 18,794 0 18,794 3,965 3,687 7,720 0 0 11,408 11,351 0

10 17,035 0 17,035 7,413 10,213 8,450 0 0 18,663 5,785 0 15 13,978 0 13,978 9,078 26,998 10,370 0 0 37,368 (14,312) 0

All yrs 314,526 0 314,526 119,837 434,363 0 0 0 434,363 0 0

28Session 09: Valuation Hot Topics

All yrs 314,526 0 314,526 119,837 434,363 0 0 0 434,363 0 0

Scenario tests

• Retain “base scenario” reserve assumptions– Contract terminal reserve factors remain unchanged– Claim reserves per disabled life remain unchanged (unless otherwiseClaim reserves per disabled life remain unchanged (unless otherwise

specified)

• What does change: underlying experienceWhat does change: underlying experience– Claim Incidence

• So more/fewer people in active/disabled status• So more/fewer people paying cash premium• So more/fewer people paying cash premium

– Claims “severity”– Voluntary lapsation

• Year to year income:– Remember: base scenario was zero income in all years

29Session 09: Valuation Hot Topics

– Scenario tests: ?????

Caveat

• Although 94GAM mortality assumption is appropriate, claims incidence and pp p ,“severity” are arbitrary

• Analyzing Results:No conclusion on the magnitude– No conclusion on the magnitude

– More interested in patterns

30Session 09: Valuation Hot Topics

Scenario #1: increase incidence in dur 2

Majority: All Lives Minority: Actives Only DifferenceTotal Total Total

Reserves Income Reserves Income Reserves Income

1 20,581 (0) 20,581 0 0 (0)

2 42,870 (2,017) 42,751 (1,898) 119 (119)

3 62 682 (65) 62 564 (66) 118 03 62,682 (65) 62,564 (66) 118 0

4 82,101 (61) 81,984 (61) 118 1

5 101,052 (56) 100,935 (57) 117 1

6 119,431 (51) 119,315 (52) 116 1

7 137,097 (46) 136,983 (48) 114 2

8 153,860 (41) 153,749 (43) 112 2

9 169,466 (35) 169,357 (39) 109 3

10 183,577 (30) 183,473 (34) 104 4

31Session 09: Valuation Hot Topics

All years (2,421) (2,421) 0

Scenario #1: increase incidence in dur 2

Net Income

All ActivesLives Only Diff.

1 (0) 0 (0)1 (0) 0 (0)2 (2,017) (1,898) (119)3 (65) (66) 0 4 (61) (61) 1 5 (56) (57) 1 6 (51) (52) 16 (51) (52) 1 7 (46) (48) 2 8 (41) (43) 2 9 (35) (39) 3

10 (30) (34) 4 11 ( ) ( )11 (24) (30) 6 12 (18) (25) 7 13 (12) (21) 9 14 (6) (17) 11 15 0 (13) 14 16 6 (9) 15 17 11 (6) 16 18 13 (2) 15 19 10 0 10 20 1 1 0

32Session 09: Valuation Hot Topics

All yrs (2,421) (2,421) (0)

Scenario #2: decrease Incidence in dur 2

Majority: All Lives Minority: Actives Only DifferenceTotal Total Total

Reserves Income Reserves Income Reserves Income

1 20,581 (0) 20,581 0 0 (0)

2 38,835 2,017 38,954 1,898 (119) 119

3 58,884 65 59,003 66 (118) (0)( ) ( )

4 78,541 61 78,659 61 (118) (1)

5 97,733 56 97,850 57 (117) (1)

6 116,354 51 116,470 52 (116) (1)

7 134,264 46 134,378 48 (114) (2)

8 151,272 41 151,384 43 (112) (2)

9 167,124 35 167,233 39 (109) (3)

10 181,483 30 181,587 34 (104) (4)All years 2,421 2,421 0

33Session 09: Valuation Hot Topics

Scenario #2: decrease incidence in dur 2

Net Income

All ActivesLives Only Diff.

1 (0) 0 (0)1 (0) 0 (0)2 2,017 1,898 119 3 65 66 (0)4 61 61 (1)5 56 57 (1)6 51 52 (1)6 51 52 (1)7 46 48 (2)8 41 43 (2)9 35 39 (3)

10 30 34 (4)11 ( )11 24 30 (6)12 18 25 (7)13 12 21 (9)14 6 17 (11)15 (0) 13 (14)16 (6) 9 (15)17 (11) 6 (16)18 (13) 2 (15)19 (10) (0) (10)20 (1) (1) 0

34Session 09: Valuation Hot Topics

All yrs 2,421 2,421 (0)

Scenario #3: Increase incidence in dur 2-10

Net Income

All ActivesLives Only Diff.

1 (0) 0 (0)1 (0) 0 (0)2 (2,017) (1,898) (119)3 (2,071) (1,946) (125)4 (2,160) (2,027) (134)5 (2,287) (2,141) (146)6 (2 454) (2 292) (162)6 (2,454) (2,292) (162)7 (2,668) (2,485) (183)8 (2,934) (2,725) (209)9 (3,262) (3,022) (240)

10 (3,662) (3,386) (276)11 (370) (456) 8611 (370) (456) 86 12 (279) (390) 111 13 (185) (325) 140 14 (89) (262) 173 15 6 (201) 207 16 95 (142) 237 17 165 (87) 252 18 197 (37) 234 19 157 2 155 20 12 12 (0)

35Session 09: Valuation Hot Topics

All yrs (23,806) (23,806) (0)

Scen #4: increase claims “severity” all dur.

Net Income

All ActivesLives Only Diff.

1 (981) (981) 01 (981) (981) 0 2 (994) (994) 0 3 (1,025) (1,025) 0 4 (1,074) (1,074) 0 5 (1,141) (1,141) 0 6 (1 228) (1 228) 06 (1,228) (1,228) 0 7 (1,340) (1,340) 0 8 (1,479) (1,479) 0 9 (1,652) (1,652) 0

10 (1,866) (1,866) 0 11 (2 129) (2 129)11 (2,129) (2,129) 0 12 (2,448) (2,448) 0 13 (2,828) (2,828) 0 14 (3,266) (3,266) 0 15 (3,737) (3,737) 0 16 (4,175) (4,175) 0 17 (4,433) (4,433) 0 18 (4,223) (4,223) 0 19 (3,064) (3,064) 0 20 (354) (354) 0

36Session 09: Valuation Hot Topics

All yrs (43,436) (43,436) 0

Scen #5: decrease “all lives” mortality dur 2

• Kept disabled lives mortality rates = base scenario rates• Fewer total terminations, therefore more active and disabled lives

Net Income

All ActivesLives Only Diff.

1 (0) 0 0.00 2 (61) (62) 1.13 3 (42) (42) (0.00)( ) ( ) ( )4 (43) (43) (0.01)5 (44) (44) (0.01)6 (45) (45) (0.01)7 (46) (46) (0.02)8 (47) (47) (0.02)( ) ( ) ( )9 (47) (47) (0.03)

10 (48) (48) (0.04)11 (48) (48) (0.05)12 (48) (48) (0.07)13 (47) (47) (0.09)( ) ( ) ( )14 (47) (46) (0.11)15 (45) (45) (0.13)16 (43) (43) (0.15)17 (40) (40) (0.16)18 (36) (35) (0.15)

37Session 09: Valuation Hot Topics

( ) ( ) ( )19 (29) (29) (0.10)20 (21) (21) 0.00

All yrs (826) (826) (0.00)

Scen #6: decrease “all lives” mort. dur 2-10

Net Income

All ActivesLives Only Diff.

1 (0) 0 01 (0) 0 0 2 (61) (62) 1 3 (134) (136) 3 4 (218) (222) 4 5 (312) (319) 6 6 (418) (427) 96 (418) (427) 9 7 (538) (550) 12 8 (676) (692) 16 9 (831) (852) 21

10 (1,003) (1,030) 27 11 (627) (621) (5)11 (627) (621) (5)12 (631) (624) (7)13 (630) (622) (9)14 (624) (614) (11)15 (611) (598) (13)16 (587) (572) (15)17 (549) (533) (16)18 (491) (477) (14)19 (407) (397) (10)20 (288) (288) 0

38Session 09: Valuation Hot Topics

All yrs (9,635) (9,635) (0)

Conclusion

• When actual experience equals the valuation assumptions:

Both approaches produce the same total reserves– Both approaches produce the same total reserves– Both approaches produce the same net income

• When experience begins to diverge from valuation assumptions:

T o approaches prod ce different total reser es– Two approaches produce different total reserves– The income will differ between the two approaches

• “Actives Only” seems to dampen the effect

L f i f h i i i– Lots of moving parts, warrants further investigation

39Session 09: Valuation Hot Topics

Actuarial

V l ti C id tiValuation Considerations -Combination Plans

Carl Friedrich, FSA, MAAAConsulting Actuary and Principalg y p

Milliman, Inc.

March 4 2013March 4, 2013

40

Background

C bi ti lif /LTC b i• Combination life/LTC coverages becoming more common– Shrinking number of insurers selling stand-alone LTC, and g g ,

higher average premiums for new LTC sales– Companies willing to gain experience through reduced risk

plans; first tier of monthly LTC benefits come out of insuredplans; first tier of monthly LTC benefits come out of insured base plan values

• Interesting new annuity/LTC combinations • Some life/chronic illness combinations feature same

triggers as LTCSubject to Model Reg 620 lump sum option required– Subject to Model Reg 620, lump sum option required, benefits treated as life insurance

41Session 09: Valuation Hot Topics

Life/LTC Product Basics

$160,000

$200,000 DBCVDB after

LifeInsurance

Values

$40,000

$80,000

$120,000 CV afterValues (Year 3 claim)

$01 2 3 4 5 6 7 8 9 10 11 12

$600,000

$300 000

$400,000

$500,000

EOB

CumulativeLTC

Benefits (4 Year ADB

$100,000

$200,000

$300,000 IPRADB

(4 Year ADB+ 4 Yr EOB)

42Session 09: Valuation Hot Topics

$01 2 3 4 5 6 7 8 9 10 11 12

Life/LTC Product Variations

• Single premium universal life or whole life• Flexible premium universal life• Accelerated Benefit LTC rider

– YRT or level charge structure• Extension of Benefit LTC rider• Extension of Benefit LTC rider

– Level charge structure• Inflation benefit optionsp

– Level charge structure

43Session 09: Valuation Hot Topics

Life/LTC Product Variations

• Nonforfeiture Benefits• Return of Premium Options• Residual death benefits• Guaranteed minimum death benefits

No lapse guarantees• No lapse guarantees• Waiver

44Session 09: Valuation Hot Topics

Consumer and Company Benefits

• ABR reduces rates for consumer• ABR reduces risks for insurer• EBR extends coverage to address full LTC need• Package still less risky than stand-alone LTC

Cost of LTC benefits less expensive than stand alone• Cost of LTC benefits less expensive than stand-alone coverage

• Policy inherently avoid use it or lose it characteristic, as y y ,those who never go on LTC claim still receive a DB or surrender benefit

45Session 09: Valuation Hot Topics

Interactions Among Benefits

• Acceleration and Life• Inflation benefits

– Monthly maximums– Lifetime maximums

• Partial withdrawals and Loans• Partial withdrawals and Loans– LTC Benefits– ROP Benefits

• Nonforfeiture

46Session 09: Valuation Hot Topics

Annuity/LTC Combinations

• Deferred annuity platform– AV paid out without SC’s over several years when LTC

trigger is mettrigger is met– Potential extension of independent LTC benefits over

specified period– Some plans concurrently pay independent LTC benefits

while AV is being paid• E.g., as AV is being reduced $8000 per month, anotherE.g., as AV is being reduced $8000 per month, another

$2000 per month is paid as independent benefits

47Session 09: Valuation Hot Topics

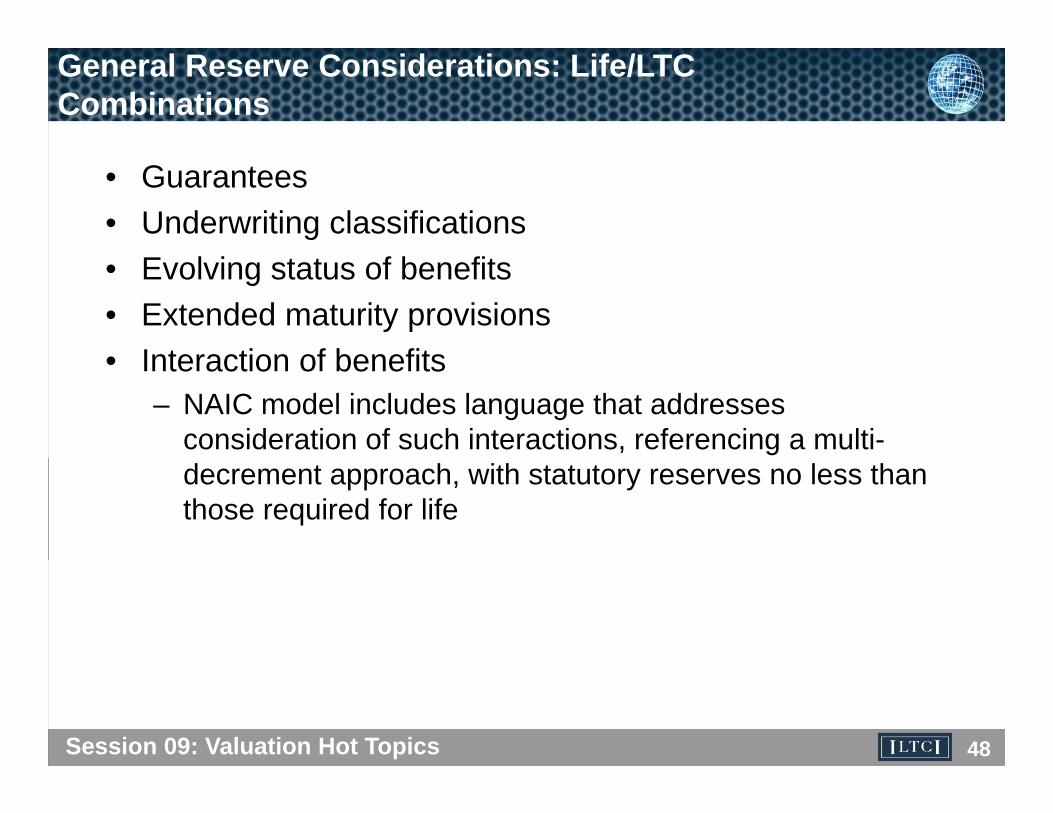

General Reserve Considerations: Life/LTC Combinations

• Guarantees• Underwriting classifications• Evolving status of benefits• Extended maturity provisions

Interaction of benefits• Interaction of benefits– NAIC model includes language that addresses

consideration of such interactions, referencing a multi-decrement approach, with statutory reserves no less than those required for life

48Session 09: Valuation Hot Topics

NAIC Model Reg Statutory Reserve Considerations: Life/LTC Combinations

• Policy reserves must be established for the ADB rider benefits consistent with life valuation requirements

• Claim reserves shall also be established if the policy or rider is in l i t tclaim status

• Reserves for policies and riders shall be based on the multiple decrement model utilizing all relevant decrements except for voluntary termination ratesvoluntary termination rates

• Single decrement approximations may be used if the calculation produces essentially similar reserves, if the reserve is clearly more conservative or if the reserve is immaterialconservative, or if the reserve is immaterial

• The calculations may take into account the reduction in life insurance benefits due to the payment of long-term care benefits

• However, in no event shall the reserves for the long-term care benefit , gand the life insurance benefit be less than the reserves for the life insurance benefit assuming no long-term care benefit

49Session 09: Valuation Hot Topics

NAIC Model Reg Reserve Considerations: Life/LTC Combinations

I th d l t d l l ti f f li i d• In the development and calculation of reserves for policies and riders, due regard shall be given to the applicable policy provisions, marketing methods, administrative procedures, and all other considerations that have an impact on projected claim costs, including, but not limited to, all of the following:

– (a) Definition of insured events.– (b) Covered long-term care facilities.– (c) Existence of home convalescence care coverage.

(d) D fi iti f f iliti– (d) Definition of facilities.– (e) Existence or absence of barriers to eligibility.– (f) Premium waiver provision.

(g) Renewability– (g) Renewability.– (h) Ability to raise premiums.– (i) Marketing method.– (j) Underwriting procedures.

50Session 09: Valuation Hot Topics

(j) Underwriting procedures.

NAIC Model Reg Reserve Considerations (continued)

• In the development and calculation of reserves for policies and riders, due regard shall be given to the applicable policy provisions, marketing methods, administrative procedures, and all other

id ti th t h i t j t d l i tconsiderations that have an impact on projected claim costs, including, but not limited to, all of the following:

(k) Claims adjustment procedures– (k) Claims adjustment procedures.– (l) Waiting period.– (m) Maximum benefit.– (n) Availability of eligible facilities.– (o) Margins in claim costs.– (p) Optional nature of benefit.– (q) Delay in eligibility for benefit.– (r) Inflation protection provisions(r) Inflation protection provisions.– (s) Guaranteed insurability option.

• Any applicable valuation morbidity table shall be certified as

51Session 09: Valuation Hot Topics

appropriate as a statutory valuation table by a member of the American Academy of Actuaries.

Guarantees

• 1980 CSO vs. 2001 CSO• Substandard• ROP• Traditional No-Lapse Secondary Guarantees

LTC• LTC• GMB• Residual DBResidual DB• Extended Maturity Options

52Session 09: Valuation Hot Topics

Statutory Reserving Assumptions

• LTC claim costs– Best estimates with margins

M li• Mortality – Guarantee basis, and special guarantees for life– Consider mortality basis for standalone LTC 94 GAMConsider mortality basis for standalone LTC, 94 GAM– Consider expected underwriting for life coverage and

implications for mortality• Lapses

– Applicable as allowed for LTC reserve calculations

53Session 09: Valuation Hot Topics

Statutory Life Reserves

• UL base reserve developed under general UL reserving principles, including application of AXXXEBR h ld fl t t diti l LTC ti lif• EBR reserves should reflect traditional LTC active life reserves, e.g.– One Year FPT– Margins– Interest rate maximum

C f– Consideration of lapses– Mortality table (94 GAM e.g.)– Sufficiency of difference between gross and net premiumsSufficiency of difference between gross and net premiums

to cover renewal expenses

54Session 09: Valuation Hot Topics

Statutory Life Reserves

• ABR reserves, when charge structure is YRT, are normally sufficiently addressed by one half cx calculationscalculations

• Inflation benefits should reflect traditional health active life reserves

• Claim reserves should be established for LTC riders– Could reduce for portion of benefit to be paid from CV

ff f f ’– Possible offset for value of DB’s being reduced

55Session 09: Valuation Hot Topics

Reserving Issues of Interest

• Substandard calculations• Extended maturity issues• ABR with level charges• Residual DB’s

LTC recovery rates• LTC recovery rates• Redundancies of LTC reserves and life reserves

– While on claimWhile on claim– Elsewhere

56Session 09: Valuation Hot Topics

Future Considerations - Stochastic Analysis and Principle based Reserves

• How critical is stochastic analysis to understand the risk?• ERM views• Short cut evaluations• Possible requirement in future for principles-based

reserves for both life and LTCreserves for both life and LTC• Computer needs for stochastic analysis on massive

models

57Session 09: Valuation Hot Topics

Filing Requirements

• Actuarial memoranda – life– Nonforfeiture and reserve requirements

A i l ifi i LTC• Actuarial certifications – LTC– Reserve requirements

58Session 09: Valuation Hot Topics

Annuity/LTC reserves

• CARVM for base annuity– Recognition of LTC withdrawal stream

I d d LTC b fi i ddi i l LTC i• Independent LTC benefits require additional LTC active life and claim reserves

• Reserves for integrated rider benefits will depend onReserves for integrated rider benefits will depend on particulars of those designs– Possible recognition as integrated benefit stream under

CARVMCARVM

59Session 09: Valuation Hot Topics

GAAP Reserves

• FAS 60 or FAS 97?• SOP03-1

– Can come into play if statutory losses occur in the tail– Mortality table disconnect between LTC mortality basis and

life mortality expected can create tail losses and the need y pto create SOP03-1 reserves

60Session 09: Valuation Hot Topics