Embed Size (px)

Citation preview

September 2017

home executive summary

audit deficiencies continue to be significant

pcaob inspections 2017 inspection cycle

description of a deficiency

audit deficiency trends

fvm deficiencies impairment deficiencies

methodology pcaob’s ownobservations

concluding thoughts

acuitas, inc.’s survey of fair value audit deficienciesacuitas, inc.’s survey of fair value audit deficiencies

Executive Summary

Public Company Accounting Oversight Board (“PCAOB”) inspection reports provide insight into recent audit quality trends. Acuitas, Inc.’s Survey of Fair Value Audit Deficiencies (“Survey”) is intended to assist financial statement preparers, auditors, and valuation specialists in understanding the root causes of fair value measurement (“FVM”) and impairment audit deficiencies, as reported by the PCAOB. There are a number of key findings and trends that we noted from the 2009 to 2016 inspection reports and from PCAOB speeches and Inspection Briefs.

§ Audit deficiencies declined in 2015 for the second year in a row but are still quite high. The PCAOB considered 31.6% of the inspected audits for annually inspected firms to be deficient in 2015 which is down from 39.2% in 2014 and 42.9% in 2013. The PCAOB also observed this trend in its 2015 inspection cycle and attributes improved audit quality to the use of practice-aids, checklists, coaching, support teams and efforts to monitor the quality of audit work. However, because the PCAOB’s issuer selection process is risk-weighted, and not random, conclusions cannot be drawn about the quality of all audits, only those inspected.

§ Three key areas of PCAOB concern continue to be auditing internal control, assessing and responding to the risk of material misstatement and auditing accounting estimates including fair value measurements. The June 2017 release of proposed auditing standard Auditing Accounting Estimates, Including Fair Value Measurements reinforces the PCAOB’s commitment to seeing improvements in these areas.

§ Audit deficiencies attributable to FVM and impairment engagements continue to be significant and made up approximately 31% of all audit deficiencies. Failures to assess audit risks, test internal controls and to test assumptions underlying prospective financial information are the root causes of most FVM and impairment audit deficiencies.

§ FVM audit deficiencies are increasingly attributable to business combination engagements. The PCAOB considers the high pace of merger and acquisition activity as companies seek to fulfill growth objectives to be an economic risk that increases the risk of material misstatement.1

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

1

1 PCAOB Staff Inspection Brief, Information about 2017 inspections, Volume 2017 / 3, August 2017.

Fair Value Measurement Audit Deficiencies Continue To Be Significant

Audit deficiencies attributable to FVM and impairment engagements continue to be significant and made up approximately 31% of all audit deficiencies in 20152. The purpose of the Survey is to help financial statement preparers, auditors, and valuation specialists understand the root causes of FVM and impairment audit deficiencies and failures, according to PCAOB inspections. The purpose is also to highlight trends in the PCAOB inspection findings, in aggregate. The information contained in the study should be of benefit not only to public entities and their auditors, but by extension, to private entities and their auditors. The survey begins with a brief overview of the PCAOB inspection process and specific plans for the 2016 inspection cycle. It defines an audit deficiency and examines trends in audit deficiencies with graphs that cover a seven year period. Additional sections of the survey provide information about the root causes of FVM and impairment audit deficiencies. A final section provides some of the PCAOB’s own observations at the conclusion of the 2015 inspection cycle.

PCAOB Inspections3

The purpose of PCAOB inspections is to protect the interests of investors and further the public interest in the preparation of informative, accurate and independent audit reports. The PCAOB inspects registered public accounting firms to assess compliance with the Sarbanes-Oxley Act, the Rules of the Board, the rules of the Securities and Exchange Commission and professional standards in connection with the firm’s performance of audits, issuance of audit reports and related matters involving issuers. The inspections are designed to identify and address weaknesses and deficiencies related to how a firm conducts audits. According to Helen Munter, the PCAOB’s Director of Inspections, “The goal of the inspection regime has never been to simply identify deficiencies. The goal has always been to help auditors improve the quality of their audits and the value that they bring to their clients and investors. (The) priority is to address a firm’s systemic issues, and the potential deficiencies in a firm’s system of quality control.”4

The PCAOB inspection process has two designated programs, one for global network firms and one for non-affiliate firms. The global network firms include the six largest U.S. firms; BDO International Limited, Deloitte Touche Tohmatsu Limited, Ernst & Young Global Limited, Grant Thornton International Limited, KPMG International Cooperative and PricewaterhouseCoopers International Limited. The global network firms’ affiliates are primarily located outside the U.S. The six global network firms are required to be inspected annually and their member affiliated firms are required to be inspected triennially. Non-affiliate firms include four large U.S. firms that are required to be inspected annually because they perform audit on more than 100 issuers; Crowe Horwath

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

2

2 2015 financial statements of issuers were reviewed by the PCAOB as part of the 2016 inspection cycle. Reports on 2015 financial statements for the annually inspected firms were issued between June 2016 and February 2017.

3 PCAOB Staff Inspection Brief, Information about 2017 inspections, Volume 2017 / 3, August 2017.4 The State of Audit Quality, a speech delivered by Helen A. Munter, PCAOB Director, Division of Registration and Inspections to the

AICPA Conference on Current SEC and PCAOB Developments, December 11, 2015, Washington, DC.

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

3

5 2015 financial statements of issuers were reviewed by the PCAOB as part of the 2016 inspection cycle.

LLP, MaloneBailey, LLP, Marcum LLP and RSM US, LLP. Approximately 550 other domestic and non-U.S. firms in the non-affiliate firm category are required to be inspected triennially.

The PCAOB has recently begun providing more information about the inspection process including the plan, scope and objectives of each year’s inspection cycle. Audit engagements are not selected randomly for inspection and they are not necessarily representative samples of the firms’ audits. Instead, the PCAOB uses a risk-weighted selection process that considers risk from economic trends, company or industry developments and the audit firm’s inspection history. The PCAOB focuses on areas that present auditing challenges, significant audit risk, financial reporting risks and recurring audit deficiencies. These areas of focus also tend to be those financial statement items that involve higher levels of uncertainty, require a higher degree of management judgment and present a higher risk of material misstatement.

The following graphs present information about the issuers and financial statement areas of focus selected by the PCAOB for the 2016 inspection cycle.5 They also illustrate differences in inspections for global network firms and non-affiliated firms.

Global Network Inspections by Issuer Market Capitalization

$0 - $100M

> $100M - $500M

> $500M - $1B

> $1B - $5B

> $5B - $10B

> $10B - $100B

> $100B

8%18%18%

13%30%

13%

0%

Non-Affiliated Firm Inspections by Issuer Market Capitalization

$0 - $100M

> $100M - $500M

> $500M - $1B

> $1B - $5B

71%

15%

7%7%

Non-Affiliated Inspections by Issuer Industry

Global Network Inspections by Issuer Industry

Industrials & Materials

Financial Services & Benefit Plans

IT & Telecom

Consumer Discretionary & Staples

Energy & Utilities

Health Care

Financial Services & Benefit Plans

Industrials & Materials

Consumer Discretionary & Staples

IT & Telecom

Health Care

Energy & Utilities

Other

26%

7%12%

18%17%

20% 16%

35%

16%

10%6%

3%

14%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

4

Two of the top five financial reporting areas of focus for PCAOB inspections are reported using FVM; financial instruments and non-financial assets. Financial instruments that receive a higher level of focus are investments in higher-yielding, hard-to-value securities. Non-financial assets are those acquired in a business combination including goodwill, other intangible assets and other long-lived assets. The PCAOB has indicated that these financial reporting areas will continue to be selected in the 2016 inspection cycle.

% of the total audits inspected

Global Network – Top 5 Areas Inspected

Revenue & Non-financial Inventory Income Financial Receivables Assets Taxes Instruments

13%21%

83%

62%

37%

% of the total audits inspected

Non-Affiliated Firms – Top 5 Areas Inspected

Revenue & Financial Non-financial Equity Benefit Related Receivables Instruments Assets Transactions Liabilities & Other

52%

38%

25%

14% 16%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

5

The 2017 Inspection Cycle6

The 2017 inspection cycle relates to the PCAOB’s review of audits primarily performed in 2017 of issuers’ 2016 financial statements. Two fair value measurement related concerns are among the focus areas for 2017 inspections.

§ Recurring Audit Deficiencies include FVM – The PCAOB considered the most frequent and recurring audit deficiencies from recent inspection cycles and identified three troubling categories for further inspection focus. They are 1) deficiencies relating to testing of internal control over financial reporting, 2) auditor’s failures to properly assess and respond to the risk of material misstatement, and 3) deficiencies related to complex estimates including FVM. In particular, inspections will consider procedures auditors perform to understand how estimates are developed, how data is tested and how management assumptions that are significant to the estimate are evaluated.

§ Economic Risks Including High Merger Activity and FVM in Business Combinations – The PCAOB cites the high pace of merger and acquisition activity as a factor that introduces financial reporting risks related to the complexity of transactions and of fair value measurement of acquired assets and liabilities in business combinations. The risk of material misstatement associated with the identification of all intangible assets, assignment of goodwill to reporting units and the measurement of contingent consideration can arise from business combinations.

Other areas of focus for the 2017 inspection cycle are financial reporting elements that require significant levels of judgments such as consideration of an entity’s ability to continue as a going concern and evaluation of income tax accounting and disclosures. A new area of focus relates to changes in firm processes and procedures required by new accounting standards for revenue recognition and lease accounting. The PCAOB will continue to focus on audit procedures to address the risk of material misstatement posed by cyber security. Of particular note is the PCAOB’s quality control initiative to encourage firms to identify the root causes of audit deficiencies. The data analyzed in this survey may be useful to firms trying to understand the root causes of deficiencies cited by the PCAOB in 2016 and prior inspection cycles.

Description of a Deficiency

The individual PCAOB inspection reports themselves do not define deficiency. However, Auditing Standard No. 7 Engagement Quality Review provides a description, saying that a significant audit engagement deficiency “exists when (1) the engagement team failed to obtain sufficient appropriate evidence in accordance with the standards of the PCAOB, (2) the engagement team reached an inappropriate overall conclusion on the subject matter of the engagement, (3) the engagement report is not appropriate in the circumstances, or (4) the firm is not independent of its client.”7

6 PCAOB Staff Inspection Brief, Information about 2017 Inspections, Volume 2017 / 3, August 2017.7 PCAOB Auditing Standard No. 7 Engagement Quality Review

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

6

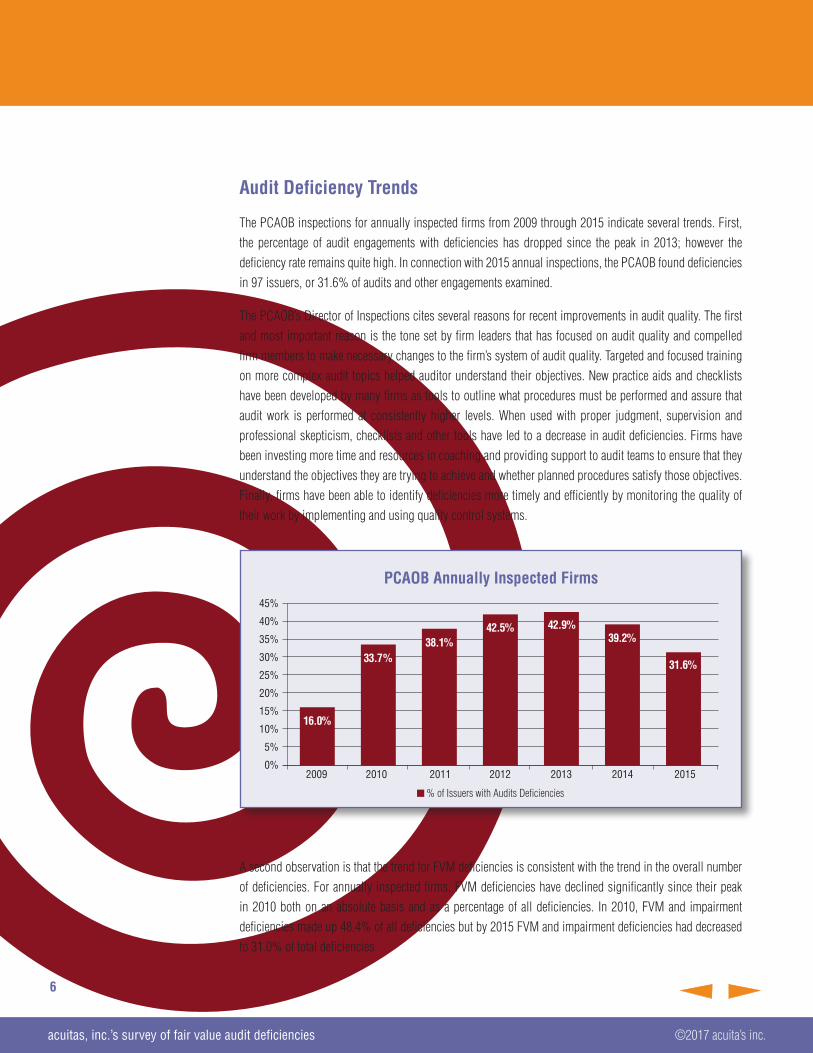

Audit Deficiency Trends

The PCAOB inspections for annually inspected firms from 2009 through 2015 indicate several trends. First, the percentage of audit engagements with deficiencies has dropped since the peak in 2013; however the deficiency rate remains quite high. In connection with 2015 annual inspections, the PCAOB found deficiencies in 97 issuers, or 31.6% of audits and other engagements examined.

The PCAOB’s Director of Inspections cites several reasons for recent improvements in audit quality. The first and most important reason is the tone set by firm leaders that has focused on audit quality and compelled firm members to make necessary changes to the firm’s system of audit quality. Targeted and focused training on more complex audit topics helped auditor understand their objectives. New practice aids and checklists have been developed by many firms as tools to outline what procedures must be performed and assure that audit work is performed at consistently higher levels. When used with proper judgment, supervision and professional skepticism, checklists and other tools have led to a decrease in audit deficiencies. Firms have been investing more time and resources in coaching and providing support to audit teams to ensure that they understand the objectives they are trying to achieve and whether planned procedures satisfy those objectives. Finally, firms have been able to identify deficiencies more timely and efficiently by monitoring the quality of their work by implementing and using quality control systems.

A second observation is that the trend for FVM deficiencies is consistent with the trend in the overall number of deficiencies. For annually inspected firms, FVM deficiencies have declined significantly since their peak in 2010 both on an absolute basis and as a percentage of all deficiencies. In 2010, FVM and impairment deficiencies made up 48.4% of all deficiencies but by 2015 FVM and impairment deficiencies had decreased to 31.0% of total deficiencies.

% of Issuers with Audits Deficiencies

PCAOB Annually Inspected Firms 45%

40%

35%

30%

25%

20%

15%

10%

5%

0%2009 2010 2011 2012 2013 2014 2015

16.0%

33.7%38.1%

42.5% 42.9%39.2%

31.6%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

7

A third trend related to the increase in the number of FVM deficiencies cited by the PCAOB related to business combinations is discussed in the next section.

FVM Deficiencies

For 2009 to 2013, 75% of FVM deficiencies were attributable to financial instruments; however in 2014 the primary source of FVM deficiencies shifted to business combinations. In 2014 56% of fair value deficiencies cited related to business combinations and this figure increased to 68% in 2015. The PCAOB’s Director of Inspections indicated that audit work on business transactions has been an area of PCAOB focus due to the complex nature of the FVM for acquired assets. In addition, their subjective nature and required level of judgment make them susceptible to management bias. Inspections continue to identify instances when auditors do not fully understand how FVM were developed and do not sufficiently test significant inputs or evaluate significant assumptions used by management. Increased merger and acquisition activity has also contributed to the increase in deficiencies cited by the PCAOB related to business combinations.8 Another likely cause for the shift away from FVM deficiencies related to financial instrument is audit improvements due to intense PCAOB focus on this area in the wake of the financial crisis. Issuers and auditors made significant improvements in controls and procedures related to the pricing of financial instruments which is apparent in the FVM Deficiency Causes graphs that follow.

8 The State of Audit Quality.

2015 FVM Deficiencies

Financial Instruments Business Combinations Financial Instruments Business CombinationsPension Plans

2009 to 2014 FVM Deficiencies

32%

68% 71%

26%

3%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

8

An increase in the number of FVM deficiencies cased by failures related to risk assessment and testing of internal controls is another inspection trend. For 2015, risk assessment and control failures were the root cause for 32% of all FVM deficiencies, up from 28% in previous years. In recent inspection reports, we have noted many instances where the PCAOB cited audit deficiencies relating to testing internal controls over FVM without citing a related substantive testing deficiency.

The PCAOB’s Director of Inspections indicated that deficiencies related to non-compliance with risk-assessment standards continue to plague the PCAOB. Of particular concern are failures related to Auditing Standard No. 13, The Auditor’s Responses to the Risks of Material Misstatement. Due to the relatively high dollar amounts typically paid for target entities, business combinations are susceptible to failures relating to material misstatements. The following deficiency from one of the annually inspected firms illustrates this point.

“The Firm selected for testing three management review controls over the valuation of the assets acquired and liabilities assumed as a result of business combination activity. The Firm’s’ testing of one of these controls was insufficient. Specifically, the Firm’s procedures to test this one control were substantive in nature and did not constitute a direct test of the control as the procedures were limited to holding discussions with management and observing evidence that the reviews occurred. The Firm, however, failed to determine whether the control was designed and operated at a sufficient level of precision to identify a material misstatement because it failed to evaluate the criteria used to identify items for investigation and/or determine whether specific items that were investigated were resolved.” 9

9 Report on 2105 Inspection of Redacted Firm Issued by the Public Company Accounting Oversight Board, https://pcaobus.org/Inspections/Reports.

2015 FVM Deficiencies Causes 2009 to 2014 FVM Deficiencies Causes

Pricing

Failure to Test

Disclosures

Risk Assessment/ Controls

PFI Assumptions

OTTI Classification

Pricing

Failure to Test

Disclosures

Risk Assessment/ Controls

PFI Assumptions

27%27%

32%

7%

7%

28%10%

3%

22%

28%

9%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

9

Descriptions of Fair Value Measurement Deficiencies

Pricing – Includes failure to understand the methods, models and assumptions used by pricing services or valuation specialists; using the same pricing service to corroborate prices that the issuer used when measuring fair value; failure to investigate significant differences between prices from different sources; failure to investigate pricing differences identified by internal audit; failure to investigate adjustments made to third party prices by issuers; and inappropriately applying the yield or discount rate from one population to test securities prices or values in the test population without assessing the comparability of the two groups.

Failure to Test – Includes relying on interim testing and failing to test the assertion there was no material change in value; relying on interim testing and failing to perform procedures at year end; failing to perform sufficient substantive procedures when significant risks are identified; failing to perform year end tests when broker quotes were older than 30 days; failing to perform substantive tests when too much reliance is placed on internal controls or internal audit; failure to assess whether all assets and liabilities had been identified in a business combination; failure to test data provided to outside valuation specialist; failure to test the accuracy and completeness of data that valuation specialists relied on; failure to test fair value when requested pricing information was not received; failure to test all items in a selected sample; and outright failure to test certain assets and liabilities.

Disclosures – Includes failure to identify and test controls over FVM hierarchy disclosures; failure to test FVM hierarchy classification as Level 2 or Level 3; and failure to assess whether an input is observable or unobservable when testing the FVM hierarchy classification.

Risk Assessment / Controls – Includes the failure to identify and test controls over inputs to FVMs; setting risk thresholds so high that material errors are not detected; failure to investigate controls over resolution of pricing differences; failure to identify weakness due to lack of supervision by qualified personnel in the testing of hard-to-value financial instruments; failure to test controls over the budgetary process; and failure to test controls over the classification of securities as available for sale.

Projected Financial Information (PFI) Assumptions – Includes failure to evaluate the reasonableness of assumptions relating to revenue growth rates, capital expenditures, terminal growth rates and the discount rate; failure to assess the reasonableness of improved margins; failure to consider industry growth rates; erroneously using PFI from a period prior to a reorganization; failure to evaluate customer attrition rates; failure to evaluate the risk premium in the issuer’s weighted average cost of capital; failure to evaluate a significant difference between value indications from the market and income approaches; and failure to assess a change in weights assigned to various indications of value.

Other Than Temporary Impairment (OTTI) – Includes failure to test controls over the classification of securities as OTTI; failure to test the issuers’ evaluation of securities as potentially OTTI; and failure to evaluate the assumptions, calculations and completeness of the issuer’s OTTI test.

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

10

Impairment Deficiencies

The number of impairment deficiencies has remained relatively flat since 2011 and these deficiencies were primarily related to testing goodwill every year.

The root causes of impairment audit deficiencies highlights the need for audit firms to understand and test assumptions underlying management’s prospective financial information (“PFI”). In 2015, 48.0% of impairment deficiencies were caused by failures related to PFI, up from 40.0% in previous years. Another significant cause of impairment audit deficiencies relates to failures to adequately test fair value measurements.

The following is typical of audit deficiency cited by the PCAOB that relates to the failure to test significant assumptions underlying management’s PFI in an impairment test. The auditors have performed procedures to assess significant assumptions, but the PCAOB has deemed those procedures to be inadequate.

“The Firm failed to sufficiently evaluate the reasonableness of the significant assumptions underlying the undiscounted cash-flow forecasts that the issuer used in evaluating this property, plant, and equipment for possible impairment. Specifically, the Firm’s procedures were limited to inquiring of management, testing the mathematical accuracy of certain schedules, performing a sensitivity analysis for certain assumptions, and comparing the assumptions used in the cash-flow forecasts to historical industry data or the issuer’s historical performance for the last five years, without considering the possible effect of adverse events and circumstances that the issuer and Firm identified.” 10

10 Report on 2105 Inspection of Redacted Flrm Issued by the Public Company Accounting Oversight Board, https://pcaobus.org/Inspections/Reports.

2015 Impairment Deficiencies 2009 to 2014 Impairment Deficiencies

Goodwill

Long Lived Asset Groups

Intangible Assets

Goodwill

Long Lived Asset Groups

Intangible Assets52%20%

28%

56%31%

13%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

11

The following descriptions of audit deficiencies relating to goodwill impairments and impairments of fixed asset groups were taken from the PCAOB inspection reports. The descriptions relate to the Impairment Deficiency Causes graphs.

Descriptions of Impairment Deficiencies

PFI Assumptions – In addition to the PFI assumption deficiencies mentioned for FVM, a deficiency relating to the failure to test the model, inputs and assumptions used to value a loan portfolio in connection with a goodwill impairment analysis was identified.

Risk Assessment / Controls – Additional deficiencies were failure to assess the issuer’s methodology for determining fair value of reporting units, failure to identify deficiencies in controls relating to triggering events; and failure to assess whether the timing of impairment charge was appropriate.

Failure to Test – An additional deficiency was failure to test the issuer’s assertion that assets were not impaired and ignoring evidence that triggering events had occurred.

Asset Mismatch – Including failure to identify a mismatch between the group of assets being tested for impairment and the group of assets included in the calculation of carrying value; and failure to identify an issuer’s departure from GAAP by allocating goodwill to reporting units.

2015 Impairment Deficiency Causes

2009 to 2014 Impairment Deficiency Causes

PFI Assumptions

Risk Assessment/ Controls

Failure to Test

PFI Assumptions

Risk Assessment/ Controls

Failure to Test

Asset Mismatch

48%

20%

32%

40%

32%

25%

3%

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

12

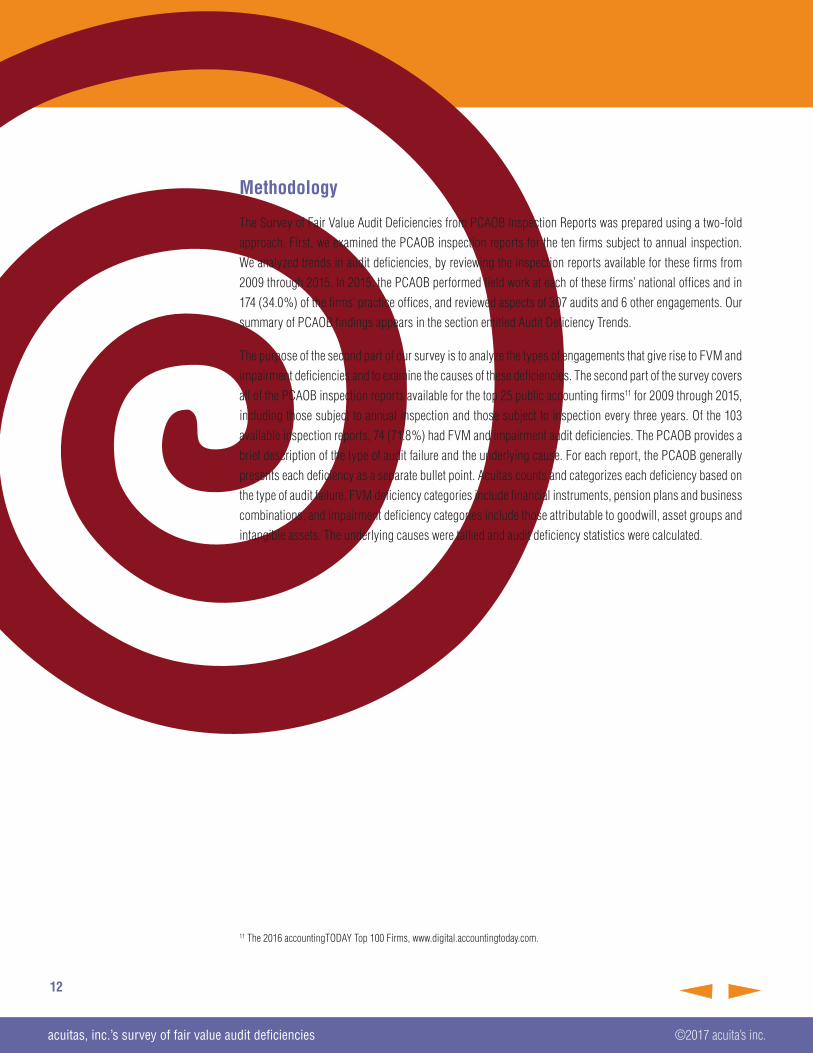

Methodology

The Survey of Fair Value Audit Deficiencies from PCAOB Inspection Reports was prepared using a two-fold approach. First, we examined the PCAOB inspection reports for the ten firms subject to annual inspection. We analyzed trends in audit deficiencies, by reviewing the inspection reports available for these firms from 2009 through 2015. In 2015, the PCAOB performed field work at each of these firms’ national offices and in 174 (34.0%) of the firms’ practice offices, and reviewed aspects of 307 audits and 6 other engagements. Our summary of PCAOB findings appears in the section entitled Audit Deficiency Trends.

The purpose of the second part of our survey is to analyze the types of engagements that give rise to FVM and impairment deficiencies and to examine the causes of these deficiencies. The second part of the survey covers all of the PCAOB inspection reports available for the top 25 public accounting firms11 for 2009 through 2015, including those subject to annual inspection and those subject to inspection every three years. Of the 103 available inspection reports, 74 (71.8%) had FVM and impairment audit deficiencies. The PCAOB provides a brief description of the type of audit failure and the underlying cause. For each report, the PCAOB generally presents each deficiency as a separate bullet point. Acuitas counts and categorizes each deficiency based on the type of audit failure. FVM deficiency categories include financial instruments, pension plans and business combinations, and impairment deficiency categories include those attributable to goodwill, asset groups and intangible assets. The underlying causes were tallied and audit deficiency statistics were calculated.

11 The 2016 accountingTODAY Top 100 Firms, www.digital.accountingtoday.com.

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

13

12 PCAOB Staff Inspection Brief, Preview of Observations from 2015 Inspections of Auditors of Issuers, Volume 2016/ 1, April 2016.

The PCAOB’s Own Observations

At the conclusion of its 2015 inspection fieldwork, the PCAOB provided a preview of inspection findings in its April 2016 Staff Inspection Brief. The number of audit deficiencies decreased for the annually inspected firms over the 2014 inspection cycle. The PCAOB cited improved audit quality as a result of new practice aids and checklists, coaching and quality monitoring. However, the PCAOB also cited an overall high number of deficiencies for triennially inspected firms. The three key areas of concern continue to be auditing internal control, assessing and responding to the risk of material misstatement and auditing accounting estimates including fair value measurements.

In its preview of inspection findings, the PCAOB provided several examples of deficiencies that pertain to fair value measurement and impairment.

§ Auditors failed to take into account relevant audit evidence that appears to contradict certain financialstatement assertions and indicate impairment of certain long-lived assets. The auditor failed to consider net losses, negative cash flows from operations and substantial doubt about the issuer’s ability tocontinue as a going concern.

§ Auditors failed to test accounting estimates arising from the fair value measurement of assets andliabilities acquired in business combinations.

§ Auditors failed to test internal controls and perform substantive testing for business combinations. Theinspection staff continues to see instances in which auditors do not perform testing beyond inquiry ofmanagement in both testing of controls and substantive testing.

§ Auditors failed to test controls over the accuracy and completeness of information used in valuation ofthe purchase price consideration.

§ Auditors’ failures to perform sufficient procedures to obtain an understanding of the specific methodsand assumptions underlying the fair value measurement of investments. In addition, there werefailures to evaluate the appropriateness of the valuation methods used and the reasonableness ofsignificant assumptions.12

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

14

In connection with the release of its proposed auditing standard, Auditing Accounting Estimates, Including Fair Value Measurements in 2017, the PCAOB reviewed its own internal data gathered from inspection reports for the eight firms inspected every year since 2008. The PCAOB’s focus was slightly different than our study and includes inspection deficiencies relating to existing audit standards for FVM and accounting estimates. The PCAOB also used a different methodology. They combined deficiencies relating to estimates and FVM, but they counted only “unique” deficiencies. Deficiencies that relate to multiple auditing standards were only counted once. The PCAOB’s findings are summarized in the following graph.

In spite of the different methodologies, our conclusions are consistent with the PCAOB’s conclusions. While there has been a recent decline in the overall number of deficiencies, the number remains high. The continued observation of a high percentage of deficiencies related to estimates including FVM reflects the complexity and subjectivity of these estimates and the requirement for better judgment and heightened skepticism on the part of the auditor. These challenges were one factor that influenced the PCAOB’s decision to improve audit standards for estimates including FVM.13

13 PCAOB Release No. 2017-002, Proposed Auditing Standard: Auditing Accounting Estimates, Including Fair Value Measurements, pp. 24 – 26.

Other Deficiencies Auditing Estimates & Fair Value

PCAOB Findings – Deficiencies Relating to Auditing Estimates & Fair Value

140

120

100

80

60

40

20

02009 2010 2011 2012 2013 2014 2015

acuitas, inc.’s survey of fair value audit deficiencies ©2017 acuita’s inc.

15

Concluding Thoughts

Based on our analysis of PCAOB inspection reports and based on information published in PCAOB Inspection Briefs, the percentage of audits with deficiencies dropped to 31.6% in 2015 for the second year in a row from a peak of 42.9% in 2013. The PCAOB has observed indications of improved audit quality over time in inspected firms. The PCAOB attributes improvement to heightened responsiveness by firm leaders, the use of practice-aids, checklists, coaching, support teams and efforts to monitor the quality of audit work. The PCAOB has emphasized that firms need to perform detailed and comprehensive analysis to determine the root cause of audit deficiencies.

However, it is apparent that the number of audits with deficiencies remains high. Consistent with our findings in prior surveys, a significant number of these deficiencies relate to the auditing of fair value measurements and impairment testing. Based on our analysis, the root cause of most fair value measurement audit deficiencies is the failure to assess risks including the risk of material misstatement and failures to adequately test internal controls. Another significant cause of FVM deficiencies and the primary cause of impairment audit deficiencies is the failure to adequately test management PFI.

While professional judgment is required in both the audit engagements and the PCAOB inspection process, professionals may reach different conclusions as to the adequacy of the audit process. PCAOB inspection deficiencies relate to the audit process where the deficiencies were of such significance that the firm failed to obtain sufficient appropriate audit evidence to support its audit opinion on the financial statements and / or the effectiveness of internal control. This survey is a summary of publicly available information, the purpose of which is to high light trends in audit deficiencies related to fair value measurements and impairments. A more complete presentation of the underlying data can be found in the inspection report themselves.

Acuitas, Inc.

Acuitas, Inc. is an Atlanta, Georgia based forensic accounting and valuation firm. Additional information about our firm can be found at www.acuitasinc.com.

For more information about how Acuitas, Inc. can help address your fair value measurement related issues, please contact Mark Zyla, Managing Director at 404-898-1137 or [email protected].