Embed Size (px)

Citation preview

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Authorization

Starting a new business could be highly strenuous task. The matter becomes more difficult when

your new business needs Authorization

FCA Authorization application can be very complex depending on the categories of industry under

which your business fall and litany of criteria you need to satisfy. It is the time when you may

consider taking an expert advice for obtaining

extensive experience dealing with FCA

if you choose us.

‘’The Financial Services & Markets Act 2000 (FSMA)

services and markets in the UK. Under

activity in the UK must be authorised by the FCA or exempt (an appointed representative or some

other exemption). Breach of section 19 may b

maximum term of two years imprisonment and/or a fine.’’

To determine whether you need

http://fshandbook.info/FS/html/handbook/PERG/2/Annex1

Regulated activities that we are working on include

• Consumer credit.

• Financial adviser.

• Investment managers and stockbrokers

• Insurers.

• Wholesale investment firms

• Sole advisers.

• Insurance intermediaries

• E-Money institutions.

• Mortgage brokers and H

• Payment services institutions

o Small Payment Institutions

o Authorised Payment Institutions

• Asset management.

• Authorised and recognised funds

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

COMPLIANCE

Authorization and Registration

FCA Authorization

Starting a new business could be highly strenuous task. The matter becomes more difficult when

Authorization from FCA sometimes even before open for customers. The

application can be very complex depending on the categories of industry under

which your business fall and litany of criteria you need to satisfy. It is the time when you may

consider taking an expert advice for obtaining Authorization from FCA. At Acumen Group we have

extensive experience dealing with FCA Authorization application and we can give you peace of mind

Do you need Authorization?

‘’The Financial Services & Markets Act 2000 (FSMA) is concerned with the regulation of financial

services and markets in the UK. Under Section 19 of FSMA, anyone who carries on a regulated

activity in the UK must be authorised by the FCA or exempt (an appointed representative or some

other exemption). Breach of section 19 may be a criminal offence and punishable on indictment by a

maximum term of two years imprisonment and/or a fine.’’

To determine whether you need Authorization or Not, Please click on the following

http://fshandbook.info/FS/html/handbook/PERG/2/Annex1

Regulated activities that we are working on include:

Investment managers and stockbrokers.

Wholesale investment firms.

Insurance intermediaries.

Mortgage brokers and Home finance lenders.

Payment services institutions:

Small Payment Institutions

Authorised Payment Institutions

Authorised and recognised funds.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

Starting a new business could be highly strenuous task. The matter becomes more difficult when

from FCA sometimes even before open for customers. The

application can be very complex depending on the categories of industry under

which your business fall and litany of criteria you need to satisfy. It is the time when you may

FCA. At Acumen Group we have

application and we can give you peace of mind

regulation of financial

who carries on a regulated

activity in the UK must be authorised by the FCA or exempt (an appointed representative or some

e a criminal offence and punishable on indictment by a

or Not, Please click on the following link:

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

• Innovator businesses: Project Innovate

If you want any support in terms of your application

committed to solve all your needs.

Authorization of your firm so you can run your business smoothly with confidence.

We are delivering HMRC MLR Registration services to the following industr

assessment and guidance:

• Money Remitters.

• Bureau De Change/Money Exchangers

• High Value Dealers.

• Trust or Company Service

• Accountancy Services Providers

• Estate Agency Businesses

New registration fees are applicable from 1

https://www.gov.uk/money-laundering

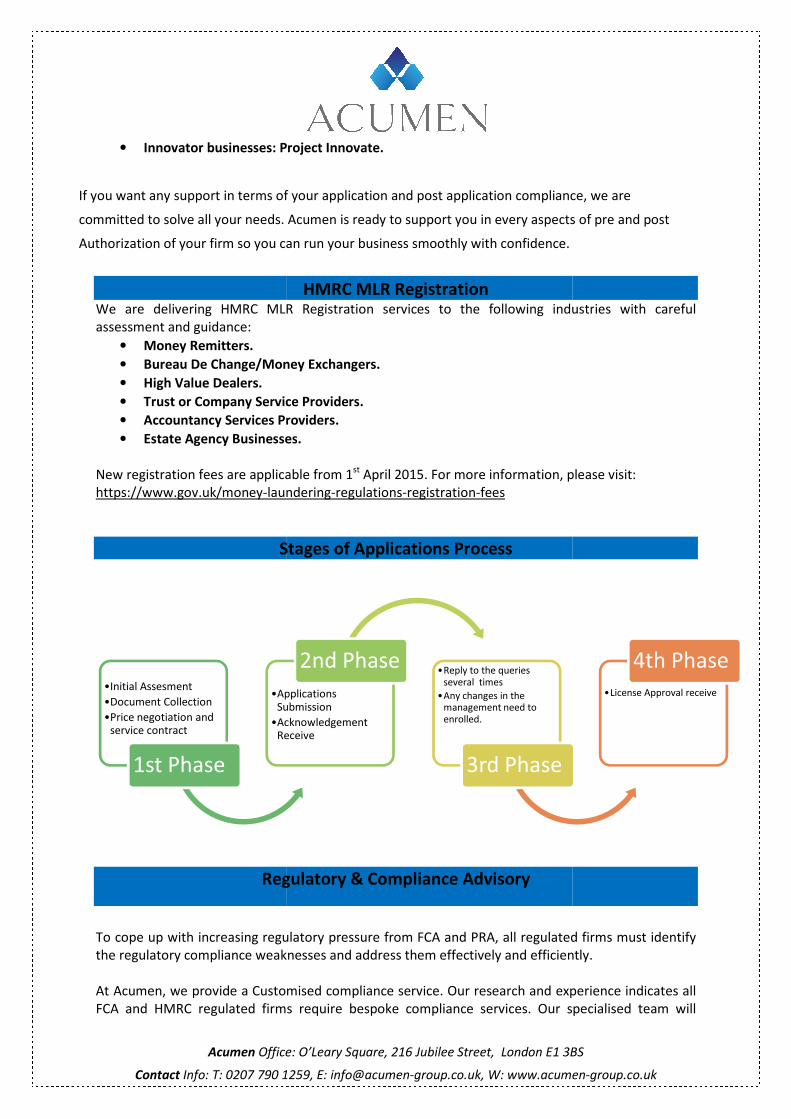

Stages of Applications Process

Regulatory &

To cope up with increasing regulatory pressure from FCA and

the regulatory compliance weakness

At Acumen, we provide a Customised

FCA and HMRC regulated firms requi

•Initial Assesment

•Document Collection

•Price negotiation and service contract

1st Phase

•Applications Submission

•Acknowledgement Receive

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Innovator businesses: Project Innovate.

t in terms of your application and post application compliance, we are

needs. Acumen is ready to support you in every aspects of pre and post

your firm so you can run your business smoothly with confidence.

HMRC MLR Registration RC MLR Registration services to the following industr

Bureau De Change/Money Exchangers.

Service Providers.

Providers.

Businesses.

New registration fees are applicable from 1st

April 2015. For more information, please visit:

laundering-regulations-registration-fees

Stages of Applications Process

Regulatory & Compliance Advisory

increasing regulatory pressure from FCA and PRA, all regulated firms must identify

the regulatory compliance weaknesses and address them effectively and efficiently.

Customised compliance service. Our research and experience indicates all

MRC regulated firms require bespoke compliance services. Our specialised team will

Applications Submission

Acknowledgement Receive

2nd Phase•Reply to the queries

several times

•Any changes in the management need to enrolled.

3rd Phase

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

application compliance, we are

ts of pre and post

RC MLR Registration services to the following industries with careful

April 2015. For more information, please visit:

PRA, all regulated firms must identify

efficiently.

Our research and experience indicates all

. Our specialised team will

•License Approval receive

4th Phase

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

recognise where you are falling behind and need

We have the compliance proficiency

latest regulatory regime. Our bespoke

• Compliance outsourcing

• Planning and performance

• Regulatory training courses

• Autonomous review of compliance matters

management.

• Compliance Gap analysis, assessment

• Prepare and implementation of compliance m

• Appointment with senior

very early stages.

• Assurance to the management

effectively.

• Preparation and Submission of all FCA Returns with appropriate consultation.

The details of the services we provide for

• Initial Assessment in terms of Compliance and Test of Application of the relevant laws.

• On-going Compliance Audit of the organization. [i.e. Monthly Basis]

• Identification of compliance weakness

• Continuous monitoring of Transaction and Compli

basis and reporting Director

• Advising on new rules and regulations and updating the AML Policy and other policy those

are relevant to your MSB.

• Risk Assessment on a periodic

• Gabriel Return and other Re

• HMRC Annual Audit Preparation and Representation.

• Transaction monitoring reports presentation and

control with new ideas which is consistent with regulations.

• Bank/Suppliers Audit Representation

• FCA Audit Representation

• Training your staffs and Agents as well under

will be awarded.]

• Updating the Training Manual and providing training contents.

• Fee Tariffs Data Form fill

• Preparing and Auditing the client money Safeguarding and segregations.

• Bank reconciliation and Segregations of Funds of the client money.

• Review & Preparation of proposed

• Design Thresholds and preparation

• Design all due diligence forms and template

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

recognise where you are falling behind and need help and deliver a package that is just right for you

proficiency, skills and resources to help you in productively

Our bespoke compliance services include:

Compliance outsourcing arrangements to our expert professional s.

performance of risk-based compliance monitoring frameworks.

Regulatory training courses in accordance with FCA Training competency requirements

review of compliance matters and Reporting to financial instructions

ap analysis, assessment and effectiveness reviews.

and implementation of compliance manuals, policies and procedures.

with senior executive in decision-making process in terms of

Assurance to the management that the regulatory risks are being supervised

d Submission of all FCA Returns with appropriate consultation.

provide for MLR Registered institutions under HMRC and FCA.

Initial Assessment in terms of Compliance and Test of Application of the relevant laws.

Compliance Audit of the organization. [i.e. Monthly Basis]

compliance weaknesses and providing solutions.

Continuous monitoring of Transaction and Compliance by Visiting Premises on a regular

basis and reporting Director/owner with valuable feedback.

Advising on new rules and regulations and updating the AML Policy and other policy those

are relevant to your MSB.

Risk Assessment on a periodic basis.

Gabriel Return and other Returns that need to be updated to FCA –if required

Audit Preparation and Representation.

Transaction monitoring reports presentation and advice to update the software for robust

control with new ideas which is consistent with regulations.

Bank/Suppliers Audit Representation.

FCA Audit Representation-if required.

Training your staffs and Agents as well under pre-arrangement on periodic

Updating the Training Manual and providing training contents.

Fee Tariffs Data Form fill-up and submissions by calculating yearly volume

Preparing and Auditing the client money Safeguarding and segregations.

Bank reconciliation and Segregations of Funds of the client money.

of proposed & finale suspicious activities.

Design Thresholds and preparation of Corporate due Diligence.

Design all due diligence forms and template.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

help and deliver a package that is just right for you.

productively navigate the

ompliance monitoring frameworks.

FCA Training competency requirements.

instructions

anuals, policies and procedures.

process in terms of compliance at

supervised and eliminated

d Submission of all FCA Returns with appropriate consultation.

MLR Registered institutions under HMRC and FCA.

Initial Assessment in terms of Compliance and Test of Application of the relevant laws.

ance by Visiting Premises on a regular

Advising on new rules and regulations and updating the AML Policy and other policy those

if required.

to update the software for robust

periodic basis. [Certificate

up and submissions by calculating yearly volume and transactions.

Preparing and Auditing the client money Safeguarding and segregations.

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Regulatory

ACUMEN offers diverse dimension of complian

regulatory compliance in financial institutions from

recommendation and management report presentation. The Audit findings and management report

will provide our clients an appropriate guidance to rectify their compliance weakness

the regulatory compliance audit on time. We also support the financial institutions to be compliant

performing the day to day compliance checking

weaknesses in compliance practise of financial institutions.

We highly recommend our clients

compliance management by considering the size and scope of the regulatory compliance burden.

We will guide you in exactly what

Regulatory

• Initial assessment of the firm/institutions through meetings.

• Identify and justify firm’s

• Identify and justify the management team

• Evaluate the AML Policies and procedures along with data protection & complain

management.

• Examine the Customer Due Diligence,

Risk evaluation.

• Verify and justify the personnel Training records and their effectiveness by taking staff

knowledge test.

• Verify and examine the due diligence records and their appropriateness using different

sampling method. I.e. Random Sampling.

• Examine the firms risk evaluat

• Investigate the in-house

• Prove the inter-communications of the set policies, procedures and their

• Identify the errors and miscon

different aspects of the business.

• Checking the Compliance practise for Principal, Supplier and Bank within the firms and

identify the weakness.

• Checking the compliance management in relation to FCA approach book, PSRS

Guidance and Joint Money Laundering Steering Group

• Identify new compliance challenge for the firms and upcoming issues tha

• Checking and verifying the client money Safeguarding and segregations.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Regulatory Compliance Audit

diverse dimension of compliance Audit services which digs

regulatory compliance in financial institutions from initial assessment of business to

recommendation and management report presentation. The Audit findings and management report

will provide our clients an appropriate guidance to rectify their compliance weakness

t on time. We also support the financial institutions to be compliant

performing the day to day compliance checking on a periodic basis. Our reports

in compliance practise of financial institutions.

We highly recommend our clients to meet with us in an initial meeting to roadmap the future

compliance management by considering the size and scope of the regulatory compliance burden.

what you need for your compliance management in your business.

Regulatory Compliance Audit Scopes

Initial assessment of the firm/institutions through meetings.

firm’s legal position through MLR, FCA and other relevant

the management team appropriateness in terms of fit and proprietary

Evaluate the AML Policies and procedures along with data protection & complain

Examine the Customer Due Diligence, Enhanced Due Diligence, Corporate Due Diligence &

and justify the personnel Training records and their effectiveness by taking staff

Verify and examine the due diligence records and their appropriateness using different

. Random Sampling.

Examine the firms risk evaluation and their action plan to reduce the risk.

house control, the monitoring and management of compliance

communications of the set policies, procedures and their

Identify the errors and misconception about compliance management by discussing

different aspects of the business.

Checking the Compliance practise for Principal, Supplier and Bank within the firms and

Checking the compliance management in relation to FCA approach book, PSRS

Joint Money Laundering Steering Group guidance.

Identify new compliance challenge for the firms and upcoming issues tha

Checking and verifying the client money Safeguarding and segregations.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

ce Audit services which digs in all aspects of

initial assessment of business to

recommendation and management report presentation. The Audit findings and management report

will provide our clients an appropriate guidance to rectify their compliance weaknesses and fit for

t on time. We also support the financial institutions to be compliant

reports focus the key

to meet with us in an initial meeting to roadmap the future

compliance management by considering the size and scope of the regulatory compliance burden.

for your compliance management in your business.

relevant registration.

of fit and proprietary.

Evaluate the AML Policies and procedures along with data protection & complain

Corporate Due Diligence &

and justify the personnel Training records and their effectiveness by taking staff

Verify and examine the due diligence records and their appropriateness using different

ion and their action plan to reduce the risk.

control, the monitoring and management of compliance of the firm.

communications of the set policies, procedures and their effectiveness.

ception about compliance management by discussing

Checking the Compliance practise for Principal, Supplier and Bank within the firms and

Checking the compliance management in relation to FCA approach book, PSRS-2009, HMRC

Identify new compliance challenge for the firms and upcoming issues that firms unaware.

Checking and verifying the client money Safeguarding and segregations.

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

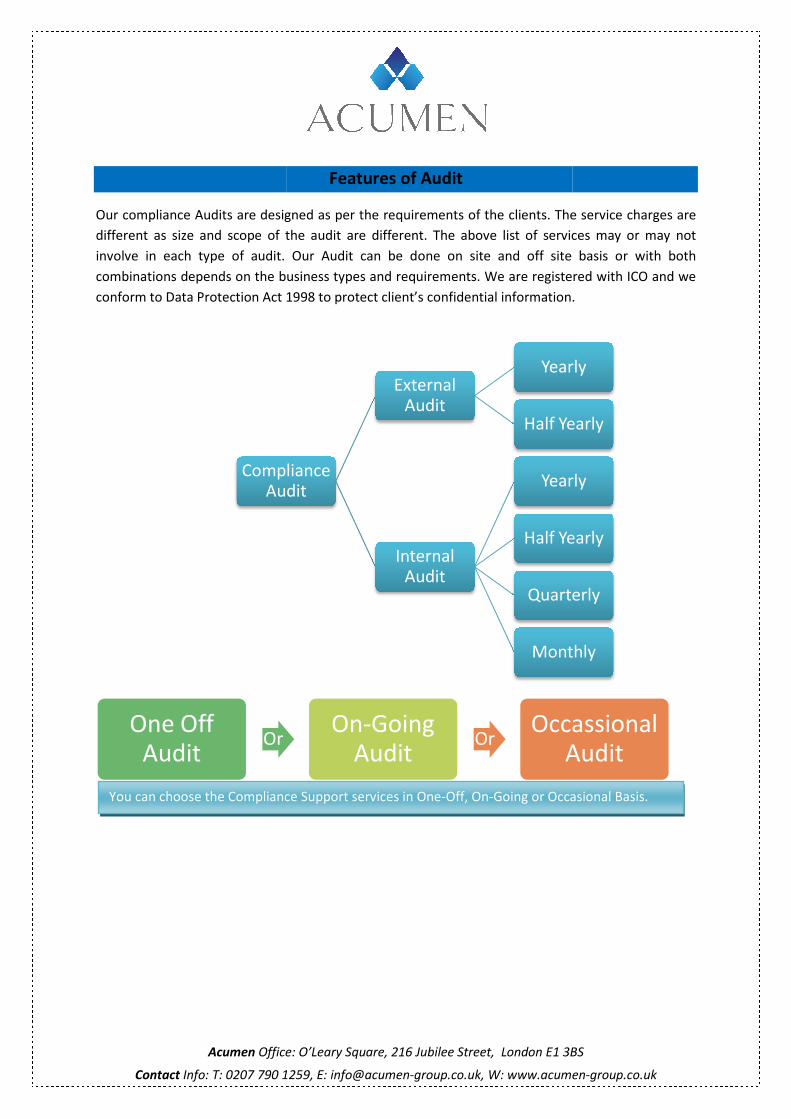

Our compliance Audits are designed as per the requirements of the clients. The service charges are

different as size and scope of the audit are different.

involve in each type of audit.

combinations depends on the business types and requirements. We are regis

conform to Data Protection Act 1998

Compliance Audit

One Off Audit

Or

You can choose the Compliance Support

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Features of Audit

are designed as per the requirements of the clients. The service charges are

different as size and scope of the audit are different. The above list of services may or may not

Our Audit can be done on site and off site basis o

combinations depends on the business types and requirements. We are registered with ICO and we

ct 1998 to protect client’s confidential information.

Compliance Audit

External Audit

Yearly

Half Yearly

Internal Audit

Yearly

Half Yearly

Quarterly

Monthly

On-Going Audit

OrOccassional

Audit

Compliance Support services in One-Off, On-Going or Occasional

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

are designed as per the requirements of the clients. The service charges are

The above list of services may or may not

Our Audit can be done on site and off site basis or with both

tered with ICO and we

to protect client’s confidential information.

Yearly

Half Yearly

Yearly

Half Yearly

Quarterly

Monthly

Occassional Audit

Occasional Basis.

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

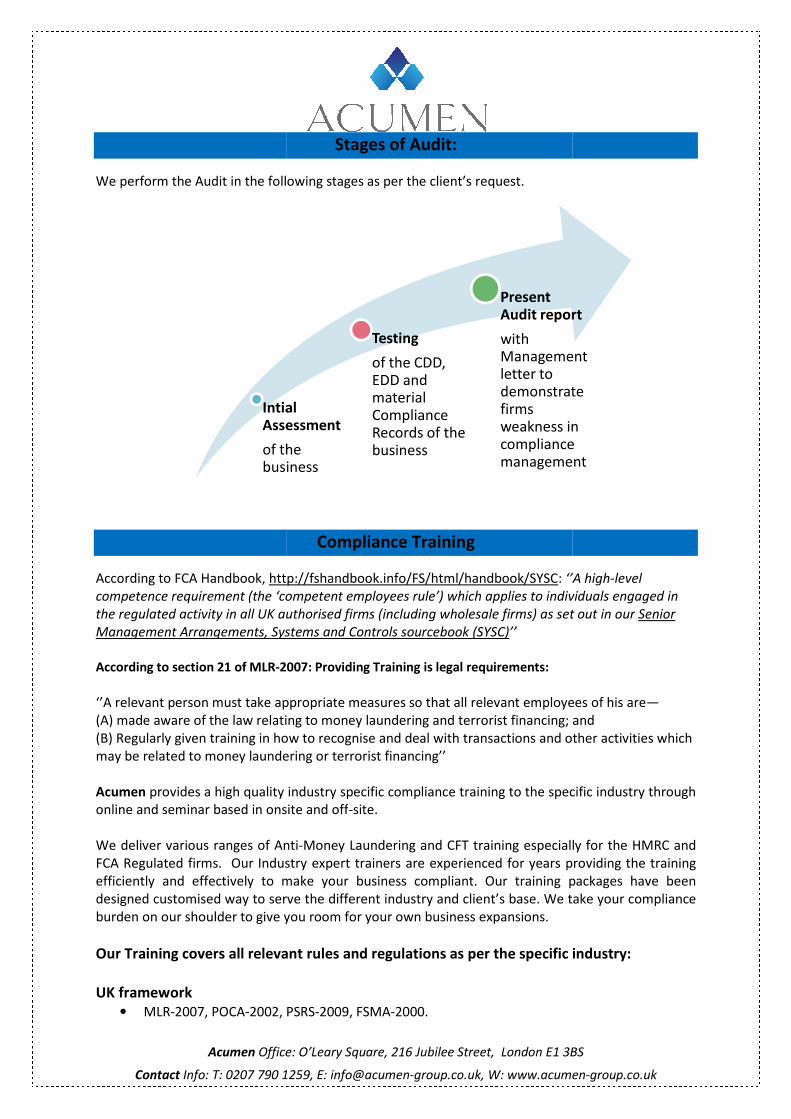

We perform the Audit in the following stages as per the client’s request.

According to FCA Handbook, http://fshandbook.info/FS/html/handbook/SYSC

competence requirement (the ‘competent employees rule’) which applies to individuals engaged in

the regulated activity in all UK authorise

Management Arrangements, Systems and Controls sourcebook (SYSC)

According to section 21 of MLR-2007: Providing Training i

‘’A relevant person must take appropriate measures so that all relevant employees of his are

(A) made aware of the law relating to money laundering and terrorist financing; and

(B) Regularly given training in how to recognise and de

may be related to money laundering or terrorist financing’’

Acumen provides a high quality industry specific compliance training to the specific industry through

online and seminar based in onsite and off

We deliver various ranges of Anti

FCA Regulated firms. Our Industry expert trainers are experienced for years providing the training

efficiently and effectively to make your business compliant. Our training packages have been

designed customised way to serve the different industry and client’s base. W

burden on our shoulder to give you room for your own business expansions.

Our Training covers all relevant rules and regulations

UK framework

• MLR-2007, POCA-2002, PSRS

Intial Assessment

of the business

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Stages of Audit:

We perform the Audit in the following stages as per the client’s request.

Compliance Training

http://fshandbook.info/FS/html/handbook/SYSC: ‘’A high

competence requirement (the ‘competent employees rule’) which applies to individuals engaged in

the regulated activity in all UK authorised firms (including wholesale firms) as set out in our

Management Arrangements, Systems and Controls sourcebook (SYSC)’’

2007: Providing Training is legal requirements:

‘’A relevant person must take appropriate measures so that all relevant employees of his are

(A) made aware of the law relating to money laundering and terrorist financing; and

(B) Regularly given training in how to recognise and deal with transactions and other activities which

may be related to money laundering or terrorist financing’’

provides a high quality industry specific compliance training to the specific industry through

online and seminar based in onsite and off-site.

We deliver various ranges of Anti-Money Laundering and CFT training especially for the HMRC and

Our Industry expert trainers are experienced for years providing the training

efficiently and effectively to make your business compliant. Our training packages have been

designed customised way to serve the different industry and client’s base. We take your compliance

burden on our shoulder to give you room for your own business expansions.

relevant rules and regulations as per the specific industr

2002, PSRS-2009, FSMA-2000.

Intial Assessment

of the business

Testing

of the CDD, EDD and material Compliance Records of the business

Present Audit report

with Management letter to demonstrate firms weakness in compliance management

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

‘’A high-level

competence requirement (the ‘competent employees rule’) which applies to individuals engaged in

d firms (including wholesale firms) as set out in our Senior

‘’A relevant person must take appropriate measures so that all relevant employees of his are—

(A) made aware of the law relating to money laundering and terrorist financing; and

al with transactions and other activities which

provides a high quality industry specific compliance training to the specific industry through

Money Laundering and CFT training especially for the HMRC and

Our Industry expert trainers are experienced for years providing the training

efficiently and effectively to make your business compliant. Our training packages have been

e take your compliance

specific industry:

Audit report

Management

demonstrate

weakness in compliance management

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

• MSB Guidance, JMLSG Guidance

• Terrorism Act 2000 (as amended by the Anti

• Counter-terrorism Act 2008, S

• Financial Sanctions: HM Treasury Sanctions Notices and News Releases

• Regulatory regime: FCA Handbook

• FCA Financial Crime Guide.

International recommendations and authorities

• FATF Recommendations (February

• UN Security Council Resolutions 1267 (1999), 1373 (2001) and 1390 (2002)

International regulatory pronouncements

• Basel paper – Sound management of risks related to money laundering and financing of

terrorism.

• IAIS Guidance Paper 5.

• IOSCO Principles paper.

EU Directives

• First Money Laundering Directive 91/308/EEC

• Second Money Laundering Directive 2001/97/EC

• Third Money Laundering Directive 2005/60/EC

• Implementing Measures Directive 2006/70/EC

EU Regulations

• EC Regulation 2580/2001

• EC Regulation 1781/2006 (the Wire Transfer Regulation)

Off-Training

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

JMLSG Guidance, the Terrorist Asset-freezing Act 2010.

Terrorism Act 2000 (as amended by the Anti-terrorism, Crime and Security Act 2001)

terrorism Act 2008, Schedule 7.

Financial Sanctions: HM Treasury Sanctions Notices and News Releases.

Regulatory regime: FCA Handbook –APER, COND, DEPP, PRIN, and SYSC.

FCA Financial Crime Guide.

International recommendations and authorities

FATF Recommendations (February 2012).

UN Security Council Resolutions 1267 (1999), 1373 (2001) and 1390 (2002)

International regulatory pronouncements

Sound management of risks related to money laundering and financing of

First Money Laundering Directive 91/308/EEC.

Second Money Laundering Directive 2001/97/EC.

Third Money Laundering Directive 2005/60/EC.

Implementing Measures Directive 2006/70/EC.

EC Regulation 2580/2001.

EC Regulation 1781/2006 (the Wire Transfer Regulation).

Training Packages:

Online Training

Onsite Training

Seminer Based Training

-Site Training

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

terrorism, Crime and Security Act 2001).

UN Security Council Resolutions 1267 (1999), 1373 (2001) and 1390 (2002).

Sound management of risks related to money laundering and financing of

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Prepara

We prepare the range of policies and procedures for FCA and HMRC regulated firms for application

preparation and meet post applications compliance challenge. Our expert professional prepare the

following documents and policies in tailed way to suit with yo

FCA Requirements during applications process.

• Opening balance sheet, Forecast Balance sheet, Monthly cash flow forecast and monthly

profit and loss forecast.

• Annual accounts and management accounts

• Firm’s Regulatory business plan

• Firms key business risks and mitigation plan.

• List of outsourcing plan accompanied with monitoring and controlling plans

• Client’s disclosure documents

• Remuneration structures

• Distance marketing plans and procedures

• Responsible lending procedures to make loan to customers

• Treating customers fairly outcomes procedures and firms consideration in business plan and

culture.

• IT systems and procedures

• Business disaster and Continuity Plan

• Compliance Procedures.

• Compliance monitoring programme documents

• Anti-Financial Crime and Market abuse Policy

• IT assessment review

• Business Operations Overview

• Conduct of Business Policy

• Data Telephone Preference Service (TPS) and Mail Preference Service (MPS) checked Policy

as per regulations.

• Complaints Policy

• Sign off of Marketing materials Policy

• Data Protection Policy

• Monitoring sales activity policy

• Terms of business & Consent form for data protection

• Sales scripts

• Conflict of interest policy

• Introducer Agreement

• Product Literature

• FCA Scripts-Verbal Disclosures.

• Training & Competency scheme

• sales policy, processes and controls

• Intermediaries’ guidance and second charge lending gui

• Day 1 ‘and ‘day 8 ‘letters to customers.

• Affordability assessment format and process.

• Prevent Financial Crime procedures.

• Procedures to identify and deal with borrowers who may have a mental capacity limitation

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Preparation of Policies and Procedures

We prepare the range of policies and procedures for FCA and HMRC regulated firms for application

preparation and meet post applications compliance challenge. Our expert professional prepare the

following documents and policies in tailed way to suit with your business as per the requirements of

FCA Requirements during applications process.

Opening balance sheet, Forecast Balance sheet, Monthly cash flow forecast and monthly

Annual accounts and management accounts.

ry business plan.

Firms key business risks and mitigation plan.

List of outsourcing plan accompanied with monitoring and controlling plans

disclosure documents.

Remuneration structures.

Distance marketing plans and procedures.

procedures to make loan to customers-if appropriate

Treating customers fairly outcomes procedures and firms consideration in business plan and

IT systems and procedures.

Business disaster and Continuity Plan.

.

nitoring programme documents

Financial Crime and Market abuse Policy

Business Operations Overview

Conduct of Business Policy

Data Telephone Preference Service (TPS) and Mail Preference Service (MPS) checked Policy

Sign off of Marketing materials Policy

Monitoring sales activity policy

Terms of business & Consent form for data protection

Conflict of interest policy

Verbal Disclosures.

Training & Competency scheme policy

sales policy, processes and controls

Intermediaries’ guidance and second charge lending guidance for brokers and lenders.

ay 1 ‘and ‘day 8 ‘letters to customers.

ssment format and process.

Prevent Financial Crime procedures.

to identify and deal with borrowers who may have a mental capacity limitation

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

We prepare the range of policies and procedures for FCA and HMRC regulated firms for application

preparation and meet post applications compliance challenge. Our expert professional prepare the

ur business as per the requirements of

Opening balance sheet, Forecast Balance sheet, Monthly cash flow forecast and monthly

List of outsourcing plan accompanied with monitoring and controlling plans.

if appropriate.

Treating customers fairly outcomes procedures and firms consideration in business plan and

Data Telephone Preference Service (TPS) and Mail Preference Service (MPS) checked Policy

dance for brokers and lenders.

to identify and deal with borrowers who may have a mental capacity limitation.

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

At Acumen, Our Professional Adviser will assess your business from financial and No

financial aspects to identify the potential and existing risk, taking and recommending the

possible mitigating approach to lessen the risk running the business smoothly.

the following risk in the business.

• Compliance risk assessment.

• Product risk assessment.

• Security risk assessment.

• Information technology risk assessment.

• Project risk assessment.

• Strategic risk assessment.

• Operational risk assessment.

• Internal audit risk assessment.

• Financial statement risk assessment.

• Credit risk assessment.

• Customer risk assessment.

• Supply chain risk assessment.

• Fraud risk assessment.

• Market risk assessment.

Client Money Safeguarding and Segregation Audit

The FCA’s requirement is to appoint (annually) an external aud

client assets arrangements and funds deposit

maintained systems adequate to comply with the FCA’s client money and custody rules.

The FCA requires firms to keep any records a

distinguish safe custody assets held for one client from those of other clients, and from our own

assets. Even clients funds should be kept separate than the firms other funds. Reconciliations are

made to ensure the accuracy of firm’s records and accounts, and to ensure that they correspond to

the records of third parties holding client assets.

If asset reconciliation showed a discrepancy, firms should make good any shortfall for which they

were responsible. If another organisation was responsible, firms should take reasonable steps to

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Risk Assessment

Our Professional Adviser will assess your business from financial and No

inancial aspects to identify the potential and existing risk, taking and recommending the

possible mitigating approach to lessen the risk running the business smoothly.

the following risk in the business.

Compliance risk assessment.

Product risk assessment.

Security risk assessment.

Information technology risk assessment.

Project risk assessment.

Strategic risk assessment.

Operational risk assessment.

Internal audit risk assessment.

Financial statement risk assessment.

Customer risk assessment.

Supply chain risk assessment.

Market risk assessment.

Client Money Safeguarding and Segregation Audit

to appoint (annually) an external auditor to independently assess firm’s

and funds deposit. The auditor gives their opinion on whether firms

maintained systems adequate to comply with the FCA’s client money and custody rules.

The FCA requires firms to keep any records and accounts necessary to enable firms at any time to

distinguish safe custody assets held for one client from those of other clients, and from our own

assets. Even clients funds should be kept separate than the firms other funds. Reconciliations are

o ensure the accuracy of firm’s records and accounts, and to ensure that they correspond to

the records of third parties holding client assets.

If asset reconciliation showed a discrepancy, firms should make good any shortfall for which they

were responsible. If another organisation was responsible, firms should take reasonable steps to

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

Our Professional Adviser will assess your business from financial and No-

inancial aspects to identify the potential and existing risk, taking and recommending the

possible mitigating approach to lessen the risk running the business smoothly. We assess

Client Money Safeguarding and Segregation Audit

dependently assess firm’s

their opinion on whether firms have

maintained systems adequate to comply with the FCA’s client money and custody rules.

nd accounts necessary to enable firms at any time to

distinguish safe custody assets held for one client from those of other clients, and from our own

assets. Even clients funds should be kept separate than the firms other funds. Reconciliations are

o ensure the accuracy of firm’s records and accounts, and to ensure that they correspond to

If asset reconciliation showed a discrepancy, firms should make good any shortfall for which they

were responsible. If another organisation was responsible, firms should take reasonable steps to

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

resolve the position with them. Firms must inform the FCA wit

with the reconciliation requirements, including reconciliation discrepancies and making good any

differences.

If cash reconciliation showed a discrepancy, firms should investigate to identify the reason for it and

ensure that any shortfall is paid into

account/clients’ accounts on the day the reconciliation was performed. If firms identified a shortfall

of client money in a third party account, firms

account/clients’ accounts pendin

FCA Authorization

Do you need FCA Consumer Credit

If your business is involved in provision of lending, debt management, Credit Broking, hiring or credit

Information services to consumers then your business must be authorised by Financial Conduct

Authority (FCA). FCA is the watchdog that regulates the con

protect the interest of consumers and efficient running of the industry.

Businesses which formerly held a consumer credit license with the Office of Fair Trad

have temporary permission from FCA must apply fo

otherwise known as ‘Landing Slot’. Any new business wishes to offer consumer credit services may

apply for approval from FCA any time.

Challenges

A firm should familiarise themselves with

and ensure they meet all criteria before making an application.

To begin with, a firm must obtain through understanding of the Consumer Credit rules must be

complied with and requirements

policies and procedures and Compliance Monitoring Programme

application.

Business managers often find it challenging to give necessary time to the application process and

therefore hire an external firm to do the job for them.

It is part of FCA policy that they interview applicant to understand of their business and regulatory

knowledge. Therefore, you must familiarise yourself with the types of question they might ask and

to give them appropriate response.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

resolve the position with them. Firms must inform the FCA without delay of any failure to comply

with the reconciliation requirements, including reconciliation discrepancies and making good any

reconciliation showed a discrepancy, firms should investigate to identify the reason for it and

re that any shortfall is paid into – or any excess withdrawn from

accounts on the day the reconciliation was performed. If firms identified a shortfall

ney in a third party account, firms should pay their own money into the client bank

pending resolution of the discrepancy.

Authorization on Consumer Credit

A Consumer Credit Authorization

If your business is involved in provision of lending, debt management, Credit Broking, hiring or credit

Information services to consumers then your business must be authorised by Financial Conduct

is the watchdog that regulates the conduct of UK Consumer Credit

protect the interest of consumers and efficient running of the industry.

Businesses which formerly held a consumer credit license with the Office of Fair Trad

have temporary permission from FCA must apply for Authorization within allocated time frame

otherwise known as ‘Landing Slot’. Any new business wishes to offer consumer credit services may

apply for approval from FCA any time.

A firm should familiarise themselves with Procedures of obtaining FCA Consumer Credit Approval

and ensure they meet all criteria before making an application.

To begin with, a firm must obtain through understanding of the Consumer Credit rules must be

s of application. A regulatory business plan, various

policies and procedures and Compliance Monitoring Programme must be submitted along with

Business managers often find it challenging to give necessary time to the application process and

m to do the job for them.

It is part of FCA policy that they interview applicant to understand of their business and regulatory

knowledge. Therefore, you must familiarise yourself with the types of question they might ask and

onse.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

hout delay of any failure to comply

with the reconciliation requirements, including reconciliation discrepancies and making good any

reconciliation showed a discrepancy, firms should investigate to identify the reason for it and

or any excess withdrawn from – the client bank

accounts on the day the reconciliation was performed. If firms identified a shortfall

money into the client bank

on Consumer Credit

If your business is involved in provision of lending, debt management, Credit Broking, hiring or credit

Information services to consumers then your business must be authorised by Financial Conduct

UK Consumer Credit firms to

Businesses which formerly held a consumer credit license with the Office of Fair Trading (OFT) and

within allocated time frame

otherwise known as ‘Landing Slot’. Any new business wishes to offer consumer credit services may

FCA Consumer Credit Approval

To begin with, a firm must obtain through understanding of the Consumer Credit rules must be

various compliance

must be submitted along with

Business managers often find it challenging to give necessary time to the application process and

It is part of FCA policy that they interview applicant to understand of their business and regulatory

knowledge. Therefore, you must familiarise yourself with the types of question they might ask and

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Getting Authorization is the primary stage of beginning to be regulated by FCA and a firm must

continue to manage their relationship with FCA by meeting all regulatory requirements including

compliance and reporting to retain the FCA regulatory

How to Apply

Three ways of application you should consider before you decide which one is best matches your

circumstances and then you make application with your chosen route.

Manage the application yourself

Applying for FCA Authorization is

initiative to make the application

If you are confident and have knowledge

ensure you read the guidance properly

Manage the application with

If you have decided to submit the application by yourself but you want a last minute review by

someone specialist in this sector

any requirement then you can contact us and we will happily arrange a meeting with one of our

compliance team member to have your application reviewed.

Outsource the managem

If you think you don’t have enough time to d

can hire any expert to do the job for you. They will prepare your application and collect all necessary

documentation from you.

Our compliance team are very skilled to prepare and submit FCA

Managing Compliance with FCA

Reasons for running on-going Compliance M

When you apply for approval from FCA for your Consumer Credit Business, you are

Authorization on conditions that you have met all required standards and procedures and you will

continue to meet the compliance obligation going forward. An on

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

is the primary stage of beginning to be regulated by FCA and a firm must

continue to manage their relationship with FCA by meeting all regulatory requirements including

compliance and reporting to retain the FCA regulatory status.

Three ways of application you should consider before you decide which one is best matches your

circumstances and then you make application with your chosen route.

yourself

is not learning quantum physics for first time and

application process as easy as possible for you through guidance

knowledge of this application process, you may give

properly and visit the FCA website for more information.

with expert guidance

decided to submit the application by yourself but you want a last minute review by

in this sector to ensure your application pack are completed and you did not skip

any requirement then you can contact us and we will happily arrange a meeting with one of our

compliance team member to have your application reviewed.

management of whole application

If you think you don’t have enough time to dedicate for preparation of application by yourself, you

can hire any expert to do the job for you. They will prepare your application and collect all necessary

compliance team are very skilled to prepare and submit FCA Authorization application.

Managing Compliance with FCA

going Compliance Management.

When you apply for approval from FCA for your Consumer Credit Business, you are

on conditions that you have met all required standards and procedures and you will

continue to meet the compliance obligation going forward. An on-going compliance management

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

is the primary stage of beginning to be regulated by FCA and a firm must

continue to manage their relationship with FCA by meeting all regulatory requirements including

Three ways of application you should consider before you decide which one is best matches your

and FCA took every

guidance and checklist.

give it a go. Please

information.

decided to submit the application by yourself but you want a last minute review by

to ensure your application pack are completed and you did not skip

any requirement then you can contact us and we will happily arrange a meeting with one of our

edicate for preparation of application by yourself, you

can hire any expert to do the job for you. They will prepare your application and collect all necessary

application.

Managing Compliance with FCA

When you apply for approval from FCA for your Consumer Credit Business, you are given the

on conditions that you have met all required standards and procedures and you will

going compliance management

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

programme will allow FCA to monitor how you are meeting y

therefore compulsory.

Obligations under On-going

- Implementation and manage your Compliance Monitoring Programme

- Follow your compliance policies and

compliance training.

- Stay up-to-date with the FCA's regulations that apply to your business

- Prepare and submit your GABRIEL returns to the FCA

Our Compliance Solutions Package

We have designed a package to meet all your compliance needs under one

features of the service give you everything you need to manage your on

obligations. The "Pro" version also includes support for businesses preparing their own app

for FCA Authorization.

Please contact us for more information.

Some Important Information about

Credit Authorization

What is Consumer Credit

Consumer CREDIT is the general

services offered by businesses to consumers. For the purposes of regulation, a consumer is defined

as a private individual, a sole trader or a partnership of three partners or fewer.

Does your business need to be authorised

If your business deals with regulated services then you are required to be authorised by the FCA for

Consumer Credit. Regulated services include lending, debt

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

programme will allow FCA to monitor how you are meeting your compliance obligation and it is

going compliance management programme.

and manage your Compliance Monitoring Programme

Follow your compliance policies and procedures, including ensuring your staffs receive

date with the FCA's regulations that apply to your business

Prepare and submit your GABRIEL returns to the FCA on time.

Our Compliance Solutions Package

to meet all your compliance needs under one Engagement.

features of the service give you everything you need to manage your on-going FCA compliance

" version also includes support for businesses preparing their own app

Please contact us for more information.

Some Important Information about Consumer

Authorization

What is Consumer Credit

term used to describe credit, LOAN and debt-related activities and

services offered by businesses to consumers. For the purposes of regulation, a consumer is defined

as a private individual, a sole trader or a partnership of three partners or fewer.

Does your business need to be authorised

lated services then you are required to be authorised by the FCA for

Consumer Credit. Regulated services include lending, debt-related activities, credit broking, hire and

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

our compliance obligation and it is

compliance management programme.

r staffs receive appropriate

Engagement. The core

going FCA compliance

" version also includes support for businesses preparing their own application

Consumer

related activities and

services offered by businesses to consumers. For the purposes of regulation, a consumer is defined

lated services then you are required to be authorised by the FCA for

related activities, credit broking, hire and

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Credit Information. The FCA website provides a

services.

If you are not sure whether your business falls under regulated service or not, please contacts us and

we can help you.

The FCA

The Financial Conduct Authority (FCA) is

of the financial services industry in the UK. It is accountable to the Treasury and Parliament, but does

not receive any government subsidy

businesses. The FCA replaced the Office of Fair Trading (OFT) as the regulator of Consumer Credit in

April 2014.

Type of application your business need to submit.

There are two types of FCA Consumer

Permission. Whether you need to apply for Limited or Ful

Consumer CREDIT SERVICES your busines

Tool document to help you determine which type

guidance on the kind of application you need to m

Procedures of submitting an Consumer Credit

FCA's Authorization application is in the core of the whole pro

FCA Connect system. The FCA provides sample forms for both Limited

Permission applications that you can download to see the degree of the information required. In

addition to the form, a regulatory

and number of compliance policies and procedures need to be documented. Upon completion of

application form, the application and supporting files are submitted

is paid.

Interim Permission

Businesses that formerly held a Consumer

register for Interim Permission with the FCA before Ap

temporary Authorization to continue offering Consumer

submitted for FCA Authorization

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

. The FCA website provides a Jargon Buster that includes a full li

If you are not sure whether your business falls under regulated service or not, please contacts us and

The Financial Conduct Authority (FCA) is a self-governing organisation responsible for the regulation

of the financial services industry in the UK. It is accountable to the Treasury and Parliament, but does

subsidy. The FCA is funded by the fees it charges to

businesses. The FCA replaced the Office of Fair Trading (OFT) as the regulator of Consumer Credit in

Type of application your business need to submit.

types of FCA Consumer Credit Authorization known as Limited Permission and Full

Permission. Whether you need to apply for Limited or Full Permission depends on the type

your business offers. The FCA website features a Decision

o help you determine which type of Permission you need. If you'd like further

guidance on the kind of application you need to make, please contact us.

Procedures of submitting an Consumer Credit Authorization Application

application is in the core of the whole process and it can be completed online by

system. The FCA provides sample forms for both Limited and Full

applications that you can download to see the degree of the information required. In

addition to the form, a regulatory and compliance monitoring programme need to be formulated

and number of compliance policies and procedures need to be documented. Upon completion of

application form, the application and supporting files are submitted to the FCA and

held a Consumer Credit Licence from the OFT were given the

register for Interim Permission with the FCA before April 2014. Interim Permission is

to continue offering Consumer Credit Services until an application

Authorization during the allocated application period. If your business didn't have

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

that includes a full list of regulated

If you are not sure whether your business falls under regulated service or not, please contacts us and

organisation responsible for the regulation

of the financial services industry in the UK. It is accountable to the Treasury and Parliament, but does

authorised

businesses. The FCA replaced the Office of Fair Trading (OFT) as the regulator of Consumer Credit in

Limited Permission and Full

l Permission depends on the type of

Decision

of Permission you need. If you'd like further

Application

cess and it can be completed online by

applications that you can download to see the degree of the information required. In

need to be formulated

and number of compliance policies and procedures need to be documented. Upon completion of

to the FCA and application fees

Licence from the OFT were given the chance to

ril 2014. Interim Permission is effectively a

an application is

. If your business didn't have

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

a Consumer Credit Licence from the OFT and wishes to offer reg

Interim Permission doesn't apply and you need to make fresh application to FCA.

Differences between Limited and Full Permission

Broadly speaking, the two categories of Limited and Full Permission distinguish between the

potential levels of risk of different activities to consumers. For Instance, a car dealer acting as

a Credit Broker and introduces customers to 3rd party for

the lower end of the risk scale and eligible for Limite

or a debt collection agency involved in higher risk activities would have to apply for Full Permission.

Achieving and maintaining Full Permission

Landing Slot

Businesses with Interim Permission

Application Period, also known as a Landing Slot, by the FCA in April

application for Authorization during your Application Period if you wish to continue offering

regulated services. If you don't, your Interim Permission will

Period. Once you've submitted your application, your Interi

either grants Authorization or rejects your applicatio

review your application and confirm

Regulatory Business Plan

The FCA describes a Regulatory Business Plan as a document that,

and objectives and detail how you

that your plan goes into should be

business plan will help us assess

model. If you apply for full permission

application form. If you apply for

application but you should be able

Compliance Monitoring Programme

The FCA uses the term Compliance Monitoring Programme to describe,

how you establish, maintain and

and continues to comply with its

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

a Consumer Credit Licence from the OFT and wishes to offer regulated services for the first time,

esn't apply and you need to make fresh application to FCA.

Differences between Limited and Full Permission

Broadly speaking, the two categories of Limited and Full Permission distinguish between the

potential levels of risk of different activities to consumers. For Instance, a car dealer acting as

Credit Broker and introduces customers to 3rd party for financing would be considered as being at

the lower end of the risk scale and eligible for Limited Permission. By comparison, a

or a debt collection agency involved in higher risk activities would have to apply for Full Permission.

Achieving and maintaining Full Permission Authorization is more difficult than Limited Permission.

Permission for Consumer Credit Service were given three

Application Period, also known as a Landing Slot, by the FCA in April 2014. You must submit

during your Application Period if you wish to continue offering

regulated services. If you don't, your Interim Permission will terminate at the end of your Application

Period. Once you've submitted your application, your Interim Permission will be valid

or rejects your application. It may take the FCA up to six months to

confirm whether or not it has been successful.

Regulatory Business Plan

a Regulatory Business Plan as a document that, "...will set out

you will organise your resources to achieve them. The

be proportionate to the complexity and scale of your

the adequacy of your resources and the suitability

permission you must attach Regulatory Business Plan

for limited permission you won’t need to include it

able to provide it later if FCA request it”.

Compliance Monitoring Programme

The FCA uses the term Compliance Monitoring Programme to describe, "A document

and carry out a programme of actions to check that

its compliance procedures."

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

ulated services for the first time,

esn't apply and you need to make fresh application to FCA.

Broadly speaking, the two categories of Limited and Full Permission distinguish between the

potential levels of risk of different activities to consumers. For Instance, a car dealer acting as

would be considered as being at

d Permission. By comparison, a LOAN COMPANY

or a debt collection agency involved in higher risk activities would have to apply for Full Permission.

is more difficult than Limited Permission.

three months

2014. You must submit your

during your Application Period if you wish to continue offering

at the end of your Application

Permission will be valid until the FCA

up to six months to

your business aims

The level of detail

your business. Your

suitability of your business

to the online

with your

document that shows

your firm complies

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Post Application Assessment

Once an application has been submitted, the FCA will appoint

Officer always need to evaluate

you prepared your own application, the Case Officer will send their queries to you. If

managing the application on your behalf, we will provide you with tailored guidance about your

expected response to any query

Alternatively, a telephone interview may be

your application) as part of their due diligence process.

expect from this kind of call, which are included in the "Pro

Time Lengths of Application Review

It is stated policy of FCA that it may take up to six months to make a decision on an application.

However, often they process the application much earlier than their stated time lengths.

Cost of Authorization

The FCA charges an Authorization

application the fee is £100 or £500 depending on whether regulated turnover is below or above

£50k. For Full Permission applications the fee ranges from £600 up to £15,000. Further information

about FCA fees is available on their website. If you're unsure what level of fee will apply to your

business, CALL US on 0207 790 1259

information about Authorization

GABRIEL Return

The FCA requires authorised businesses to submit regular reports wi

their consumer credit activities. The reporting requirements are somewhat more involved for Full

Permission than Limited Permission. Businesses with Limited Permission have to make an annual

return, while Full Permissions holde

stands for Gathering Better Regulatory Information

reporting system. The Compliance

of our consultants.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Post Application Assessment

en submitted, the FCA will appoint a Case Officer to review it. Case

specific details and may request further information’s if necessary.

you prepared your own application, the Case Officer will send their queries to you. If

your behalf, we will provide you with tailored guidance about your

.

Alternatively, a telephone interview may be scheduled by the Case Officer (even if we're managing

your application) as part of their due diligence process. We've produced guidance notes on what to

which are included in the "Pro" version of the Compliance

Time Lengths of Application Review

It is stated policy of FCA that it may take up to six months to make a decision on an application.

However, often they process the application much earlier than their stated time lengths.

Authorization fee based on forecast annual turnover. For Limited Permission

the fee is £100 or £500 depending on whether regulated turnover is below or above

£50k. For Full Permission applications the fee ranges from £600 up to £15,000. Further information

is available on their website. If you're unsure what level of fee will apply to your

0207 790 1259737 to chat about your specific circumstances.

Authorization fees please contact us or visit the FCA website.

The FCA requires authorised businesses to submit regular reports with updated information about

. The reporting requirements are somewhat more involved for Full

Permission than Limited Permission. Businesses with Limited Permission have to make an annual

holder needs to make return every six months. The word

Better Regulatory Information Electronically and is the name of the FCA's online

The Compliance service includes a formal review of your GABRIEL returns by one

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

o review it. Case

information’s if necessary. If

you prepared your own application, the Case Officer will send their queries to you. If we are

your behalf, we will provide you with tailored guidance about your

Case Officer (even if we're managing

We've produced guidance notes on what to

the Compliance service.

It is stated policy of FCA that it may take up to six months to make a decision on an application.

However, often they process the application much earlier than their stated time lengths.

turnover. For Limited Permission

the fee is £100 or £500 depending on whether regulated turnover is below or above

£50k. For Full Permission applications the fee ranges from £600 up to £15,000. Further information

is available on their website. If you're unsure what level of fee will apply to your

737 to chat about your specific circumstances. For more

th updated information about

. The reporting requirements are somewhat more involved for Full

Permission than Limited Permission. Businesses with Limited Permission have to make an annual

r needs to make return every six months. The word GABRIEL

and is the name of the FCA's online

service includes a formal review of your GABRIEL returns by one

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

FCA Recommended Training & Competence

Training & Competence is a specific aspect of the FCA's regulations and one of the compliance

procedures you're required to conform.

competent business employees. The rules on Training & Competence cover assessing an

maintaining competence and record keeping.

the compliance topics you and your staff may need

Benefits of Compliance Solution S

Our Compliance Solution Service and its Pro Version

-Preparation of FCA Authorization

-Guidance on expected questions and answers once application has been submitted.

-On-going Monitoring Compliance

-Preparation of applicable Policies and Procedures

The Contract Length

The minimum contract period of joining our ‘Compliance Solution Service’ and ‘Compliance Solution

Service Pro’ is 12 months.

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

ecommended Training & Competence

is a specific aspect of the FCA's regulations and one of the compliance

required to conform. It refers to their aim of ensuring consumers interaction with

competent business employees. The rules on Training & Competence cover assessing an

maintaining competence and record keeping. Acumen Group offers a set of learning courses on all

the compliance topics you and your staff may need training on.

of Compliance Solution Service

Our Compliance Solution Service and its Pro Version gives you following benefits

Authorization application

Guidance on expected questions and answers once application has been submitted.

going Monitoring Compliance

Preparation of applicable Policies and Procedures

The minimum contract period of joining our ‘Compliance Solution Service’ and ‘Compliance Solution

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk

is a specific aspect of the FCA's regulations and one of the compliance

r aim of ensuring consumers interaction with

competent business employees. The rules on Training & Competence cover assessing and

learning courses on all

gives you following benefits

Guidance on expected questions and answers once application has been submitted.

The minimum contract period of joining our ‘Compliance Solution Service’ and ‘Compliance Solution

Acumen Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

Contact Info: T: 0207 790 125

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

0 1259, E: [email protected], W: www.acumen

Office: O’Leary Square, 216 Jubilee Street, London E1 3BS

men-group.co.uk