Embed Size (px)

Citation preview

Additional Solved Problems

Rate Conversions

The Problem

• Your credit card states that you are to pay 18% per year interest compounded monthly.

• What is the annual rate compounded annually?

Data Extraction

– Macro Period = 1 year– Micro Period = 1 month– Micro Periods per Micro Period = 12– Rate = 18% per year compounded monthly– Find Rate in terms of compounding annually

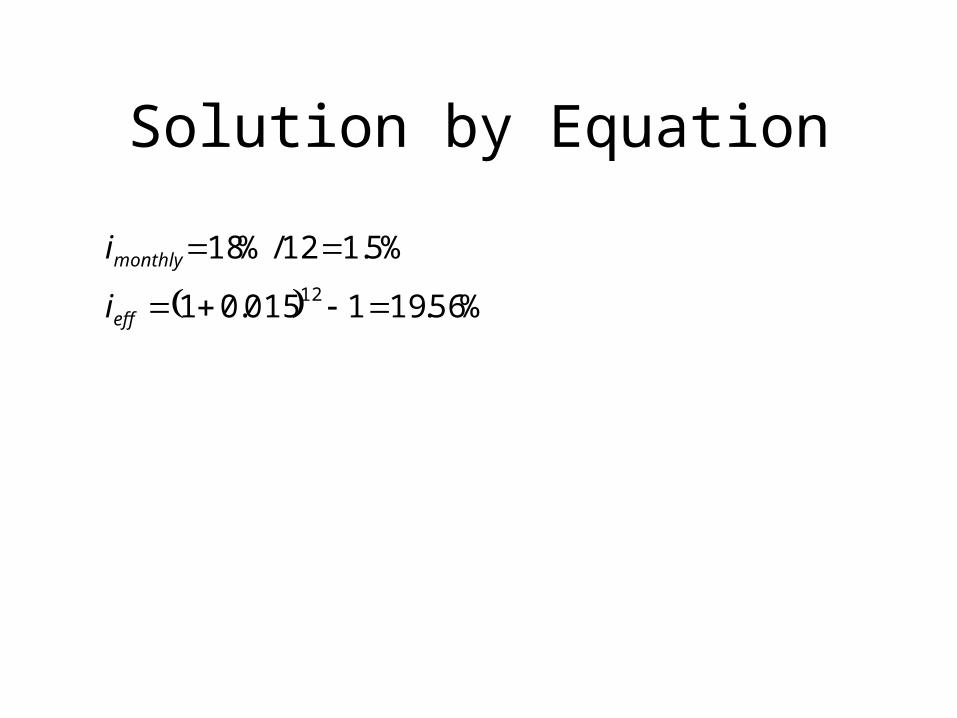

Solution by Equation

%56.191015.01

%5.112/%1812

eff

monthly

i

i

Continuous Compounding

• If the bank was able to claim a lower rate than the true rate by quoting a nominal rate, can it do even better by compounding even more frequently?

• The answer is yes. Let look at 19.56% in terms of compounding continuously

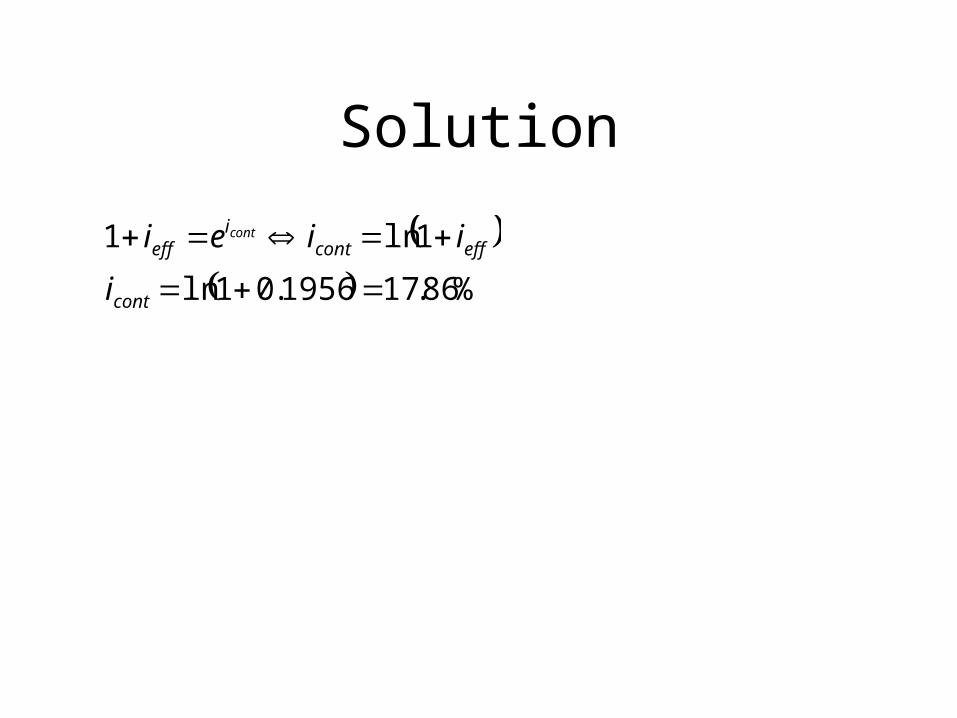

Solution

%86.171956.01ln

1ln1

cont

effconti

eff

i

iiei cont

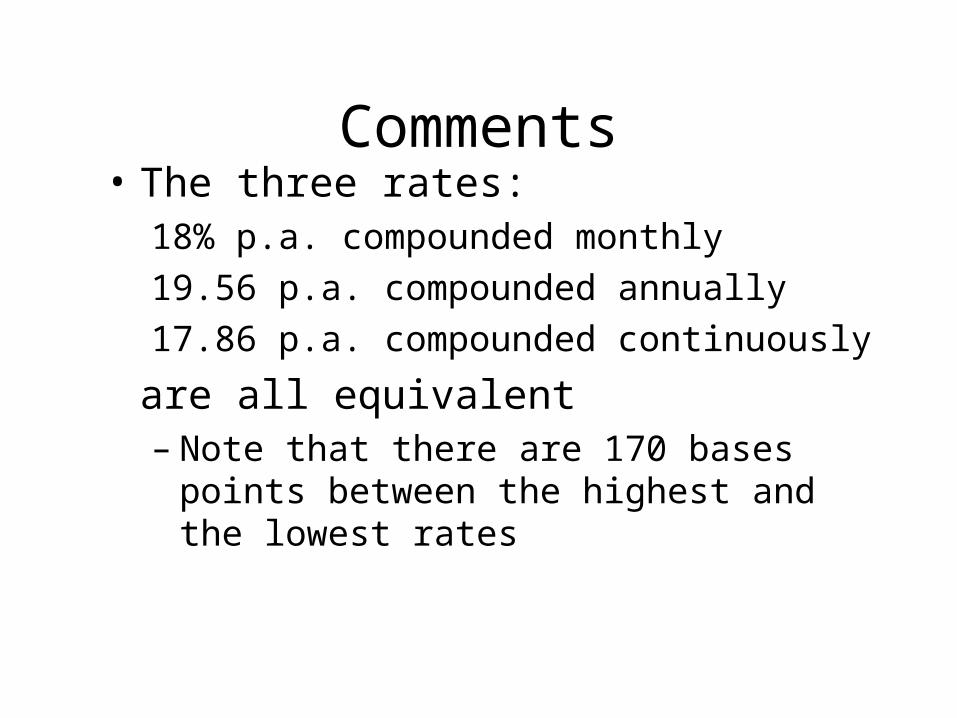

Comments• The three rates:

18% p.a. compounded monthly

19.56 p.a. compounded annually

17.86 p.a. compounded continuously

are all equivalent – Note that there are 170 bases points between

the highest and the lowest rates

Additional Solved Problems

Future Value of Annuity

The Problem

• How much will I have available in my retirement account if I deposit $2,000 per year into an IRA that pays on average 16% per year if I plan to retire in 40 years time?

• If inflation is 3% per year, what is the real value of this amount?

• Comment about this plan, given that I expect to live 20-years beyond retirement

Categorization

– Here we are talking about an a sequence of annual payments, so it is some kind of annuity

– The problem is written loosely, and there is no indication of when the first cash flow occurs, right now at year-0, or at the end of this “year” in year-1. Assume at the end of the year at the beginning of year 1

Categorization (Continued)

– The evaluation point is not completely clear, but appears to be exactly 40-years from now

– We are then looking at the future value of a regular annuity

– We are searching for a future cash flow– The problem is to find the FV of a regular

annuity

Data Extraction

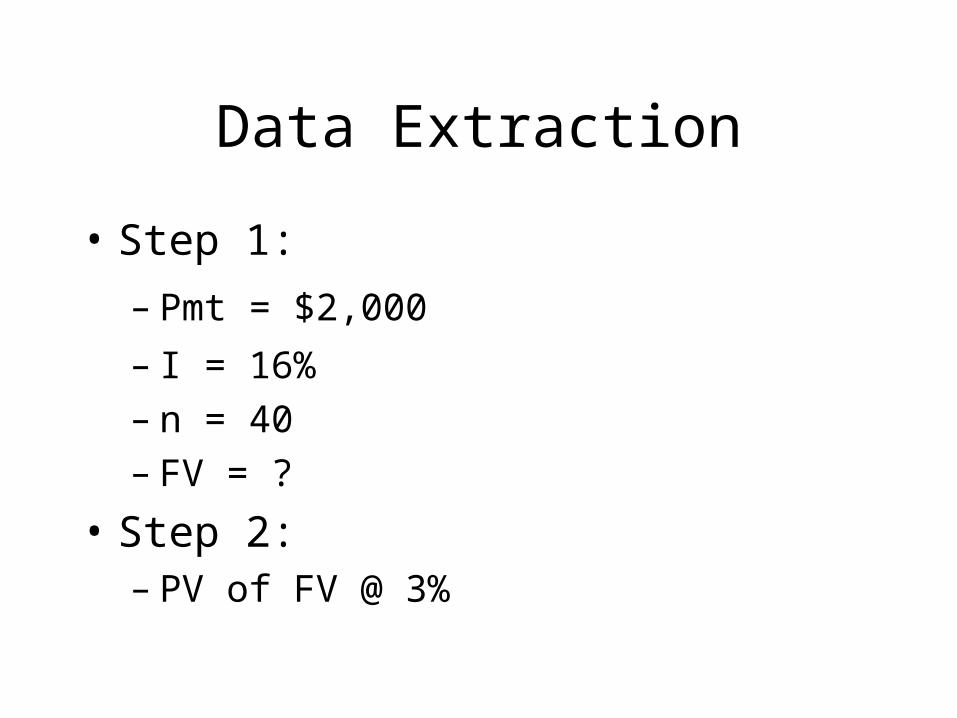

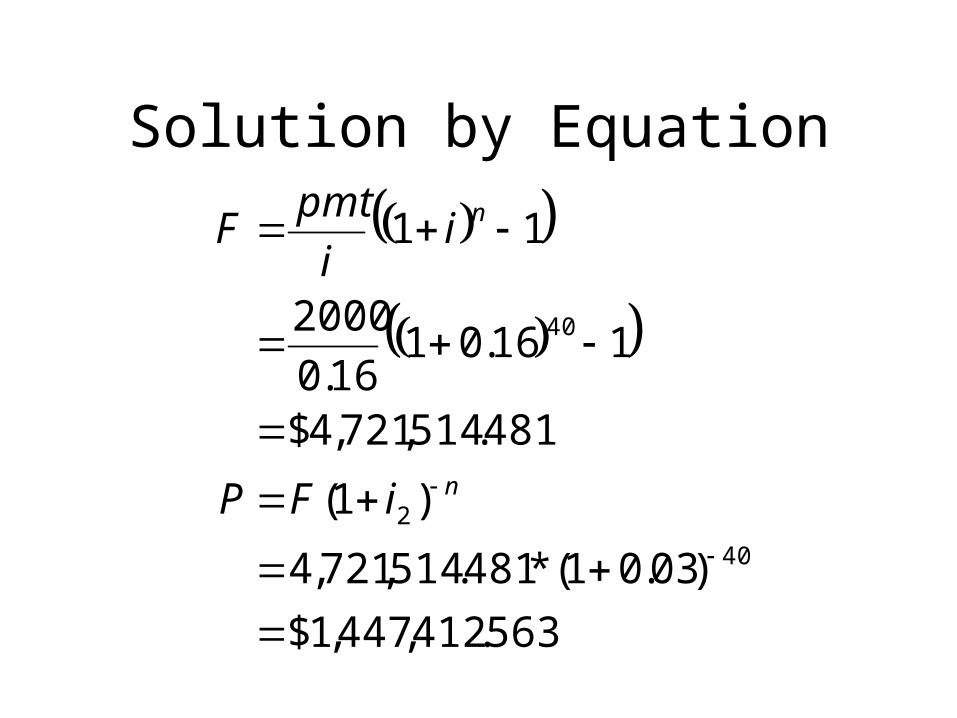

• Step 1:

– Pmt = $2,000

– I = 16%– n = 40– FV = ?

• Step 2:– PV of FV @ 3%

Solution by Equation

563.412,447,1$

)03.01(*481.514,721,4

)1(

481.514,721,4$

116.0116.0

2000

11

40

2

40

n

n

iFP

ii

pmtF

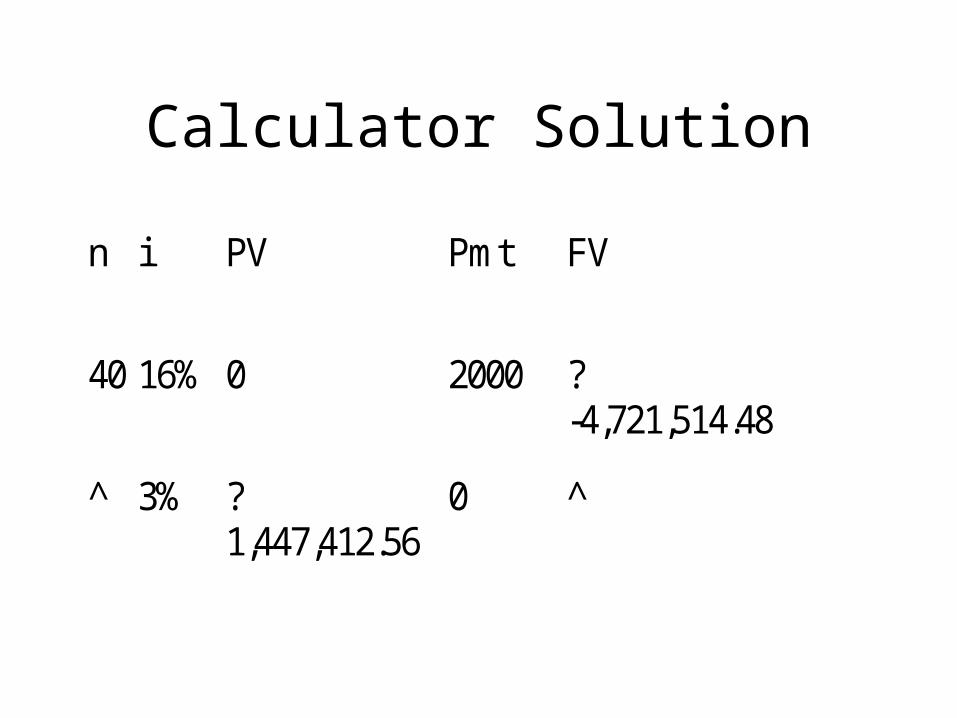

Calculator Solution

n i PV Pmt FV

40 16% 0 2000 ?-4,721,514.48

^ 3% ?1,447,412.56

0 ^

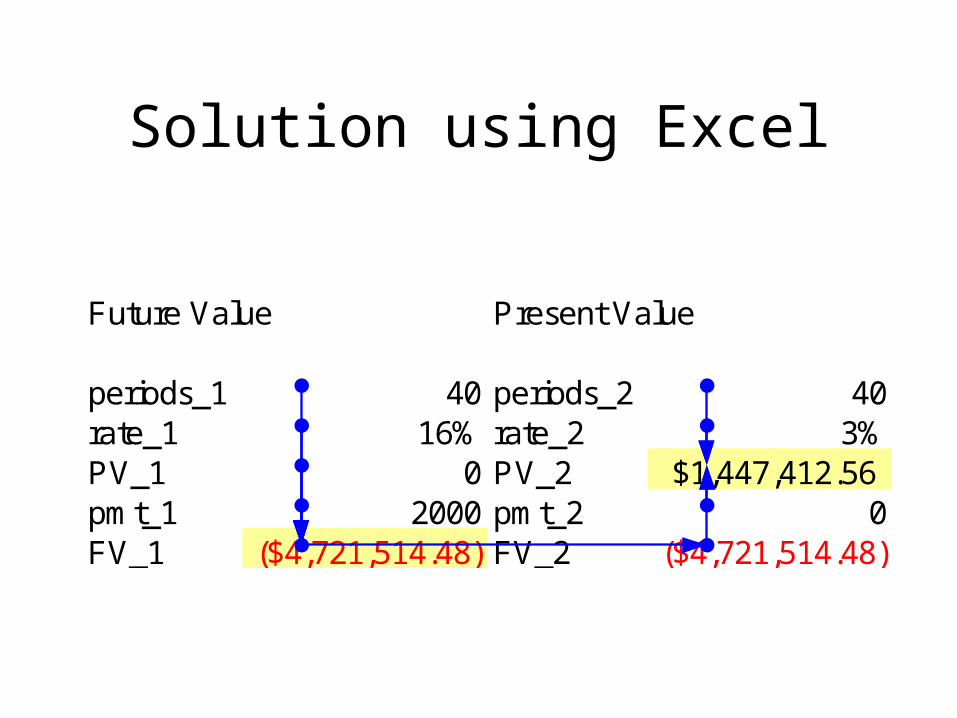

Solution using Excel

Future Value Present Value

periods_1 40 periods_2 40rate_1 16% rate_2 3%PV_1 0 PV_2 $1,447,412.56pmt_1 2000 pmt_2 0FV_1 ($4,721,514.48) FV_2 ($4,721,514.48)

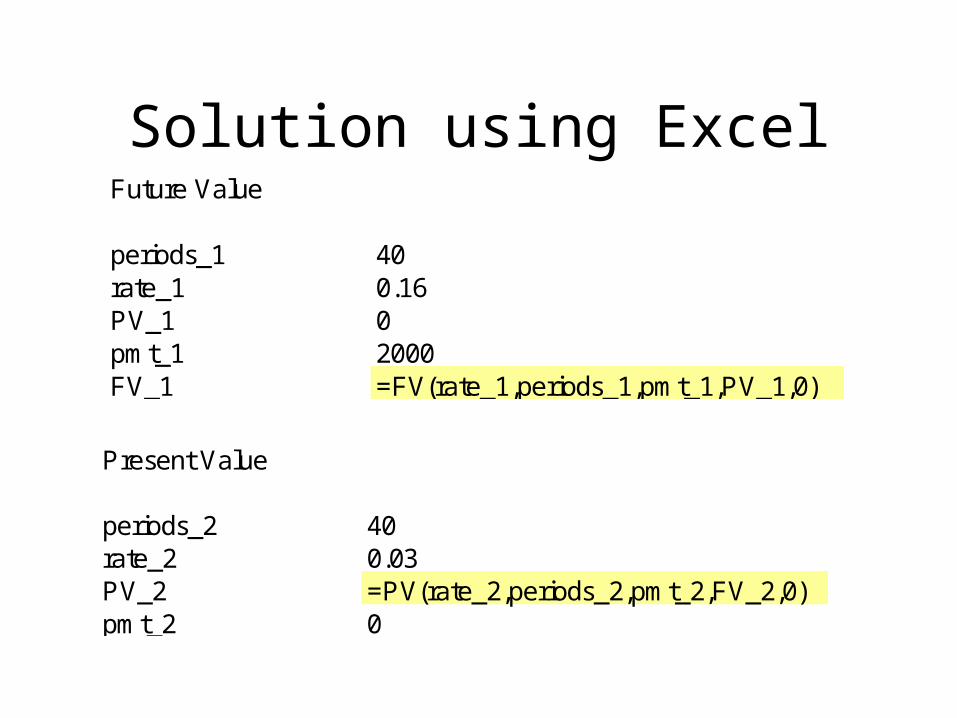

Solution using ExcelFuture Value

periods_1 40rate_1 0.16PV_1 0pmt_1 2000FV_1 =FV(rate_1,periods_1,pmt_1,PV_1,0)

Present Value

periods_2 40rate_2 0.03PV_2 =PV(rate_2,periods_2,pmt_2,FV_2,0)pmt_2 0

Comments

– Normally, you are not permitted to take a sum of money and distribute it over a number of years by simple division

– e.g, you are not permitted to divide the FV by 20-years, your remaining life

– The present value in this case is in real terms, and division is permitted. This gives $72,370.63 /year @ today’s spending power

Additional Solved Problems

Future Value Annuity

Rate

The Problem

• Guaranteed!

• Invest just $1000 per year Oddmann’s and we guarantee you to quadruple your investment in just 20 years!

• Is this a good deal?

Categorization

• This is an annuity, because money is invested every year for a period of years

• It is a future value of annuity, because the promise is to give money back to you at the end of the investment

• In this case we solve for interest rate

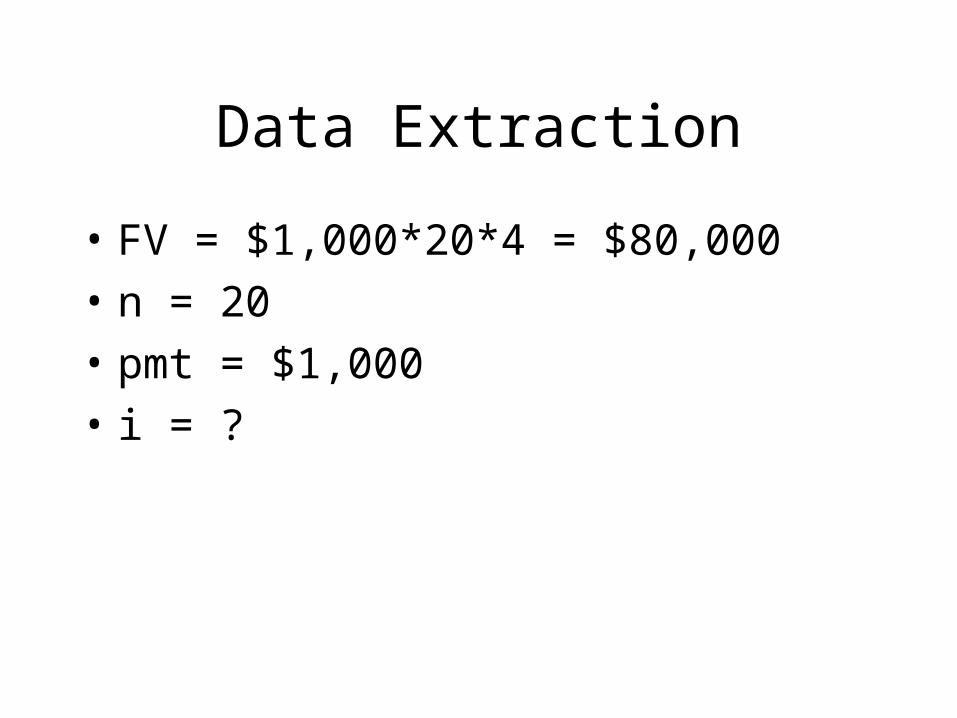

Data Extraction

• FV = $1,000*20*4 = $80,000

• n = 20

• pmt = $1,000

• i = ?

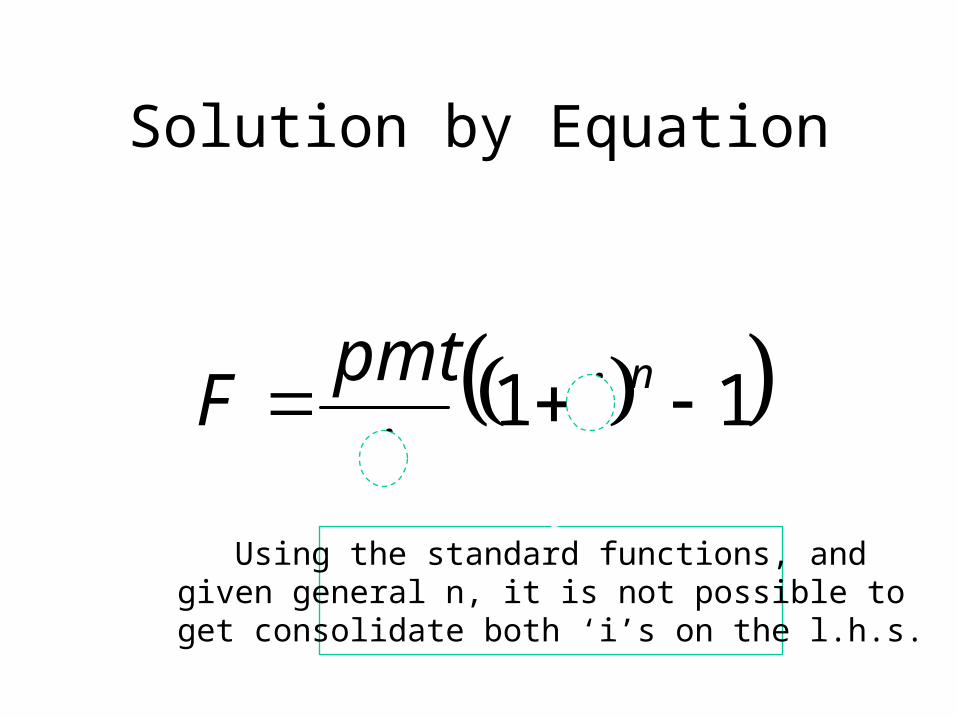

Solution by Equation

11 nii

pmtF

Using the standard functions, andgiven general n, it is not possible to get consolidate both ‘i’s on the l.h.s.

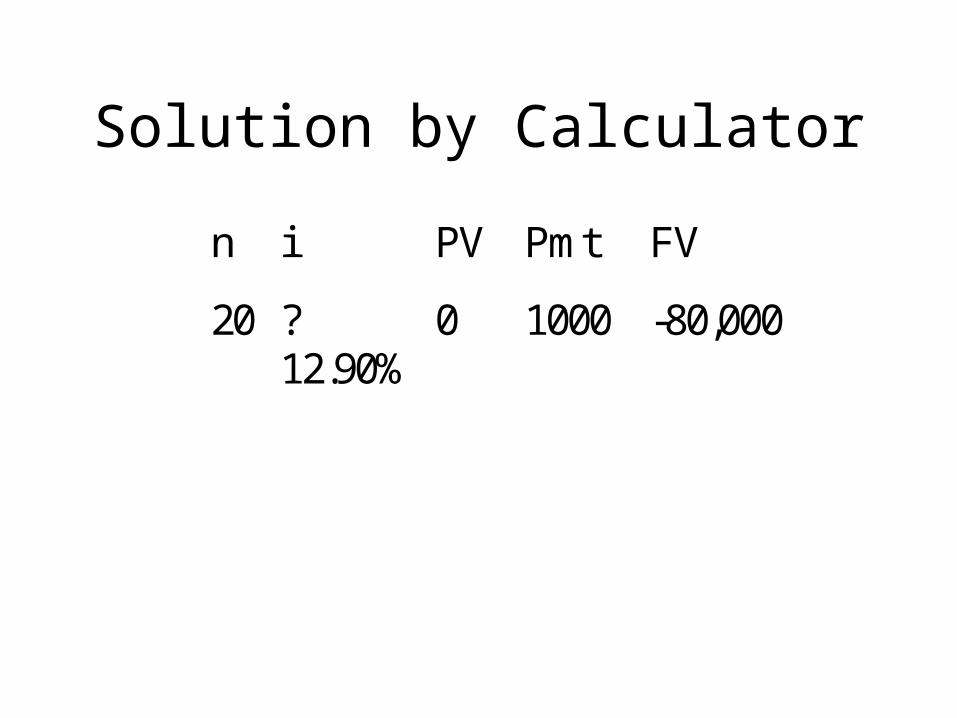

Solution by Calculator

n i PV Pmt FV

20 ?12.90%

0 1000 -80,000

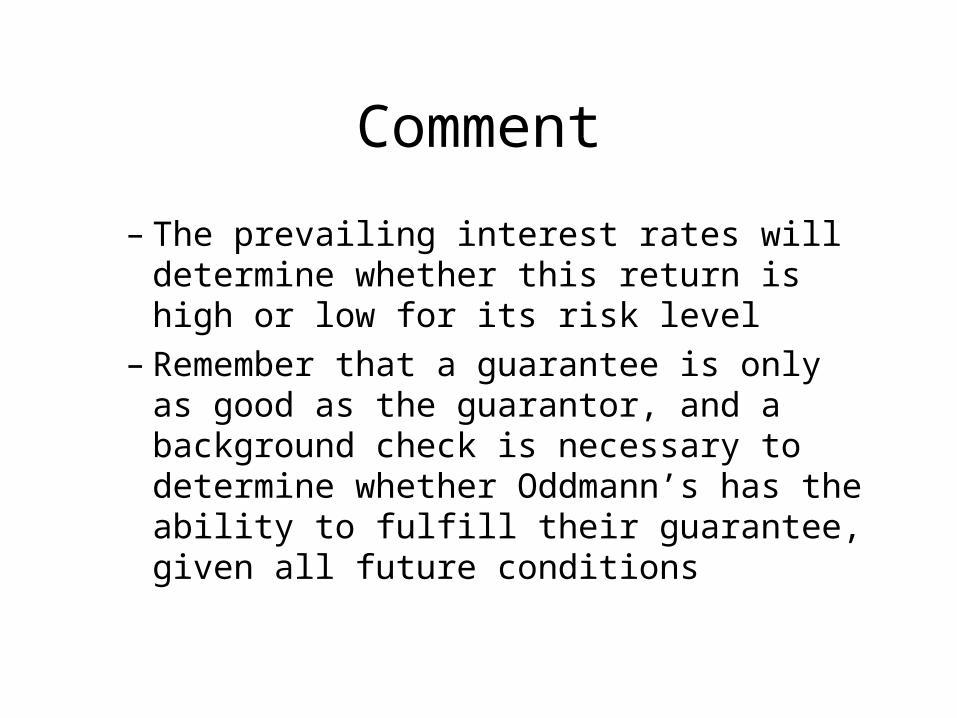

Comment

– The prevailing interest rates will determine whether this return is high or low for its risk level

– Remember that a guarantee is only as good as the guarantor, and a background check is necessary to determine whether Oddmann’s has the ability to fulfill their guarantee, given all future conditions

Comments (Continued)

– How liquid is your investment? The term indicates that the investment is for 20-years and can not be liquidated

– If you stop paying after, say 5 years, as the contract may permit, and you still quadruple your money in the plan, is this a good deal?

– This problem can’t be solved using n/I/PV/pmt/FV but is solved using your calculator’s IRR function, or Excel’s “Solve”

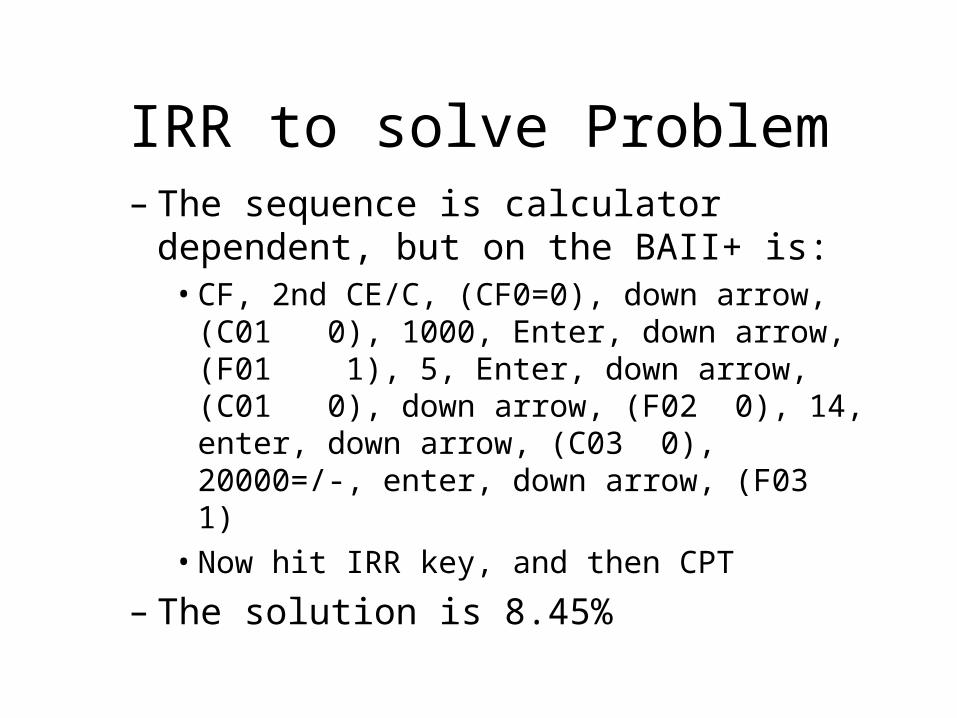

IRR to solve Problem– The sequence is calculator dependent, but on

the BAII+ is:• CF, 2nd CE/C, (CF0=0), down arrow, (C01 0),

1000, Enter, down arrow, (F01 1), 5, Enter, down arrow, (C01 0), down arrow, (F02 0), 14, enter, down arrow, (C03 0), 20000=/-, enter, down arrow, (F03 1)

• Now hit IRR key, and then CPT

– The solution is 8.45%

Final Comment

• The rate for investing over the whole period is 12.90%, but if you stop investing after 5-years the rate is 8.45%

• Oddmann’s appears to have found a way to incorporate an implicit penalty for early withdrawal into their financial product

Additional Solved Problems

FV of an Annuity

Solve for Periods

Technical Issue

– Some problems (other) textbooks are not realistic. They ask “How long it will take to save for …”, and assume that there is no final price inflation. An example is

• How long will it take to save the $30,000 deposit on a new home if I can save $500 per month at a return of 0.7% per month?

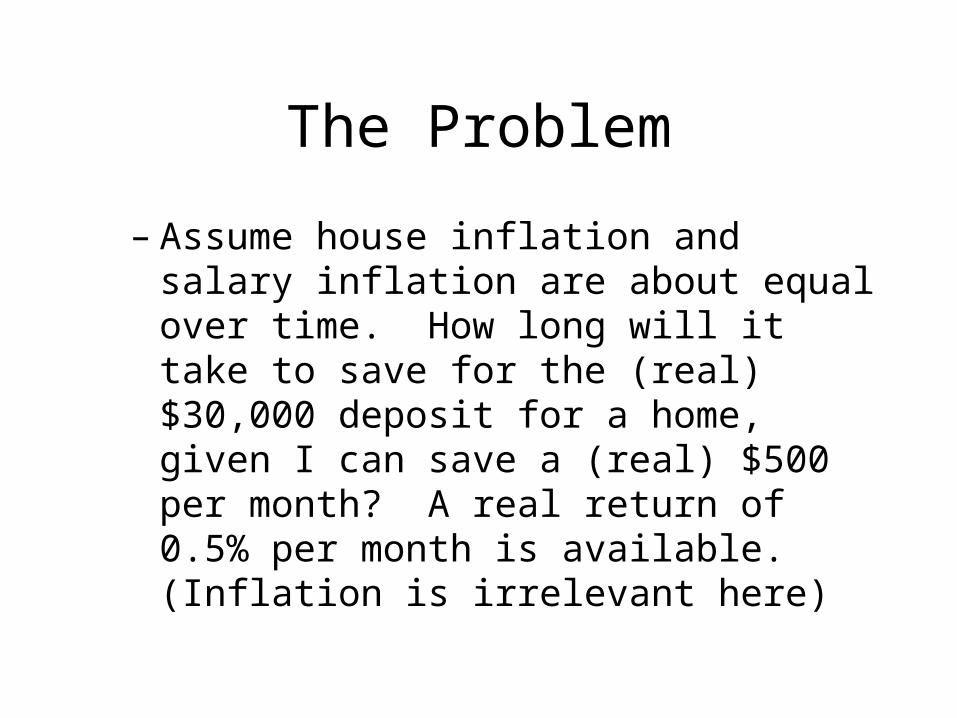

The Problem

– Assume house inflation and salary inflation are about equal over time. How long will it take to save for the (real) $30,000 deposit for a home, given I can save a (real) $500 per month? A real return of 0.5% per month is available. (Inflation is irrelevant here)

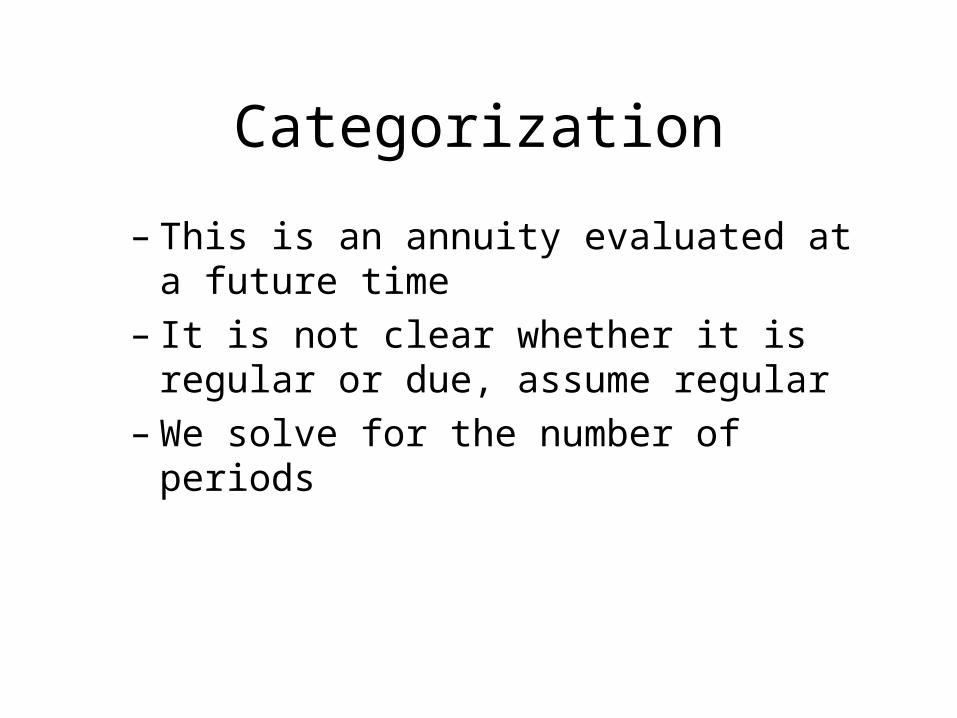

Categorization

– This is an annuity evaluated at a future time– It is not clear whether it is regular or due,

assume regular– We solve for the number of periods

Data Extraction

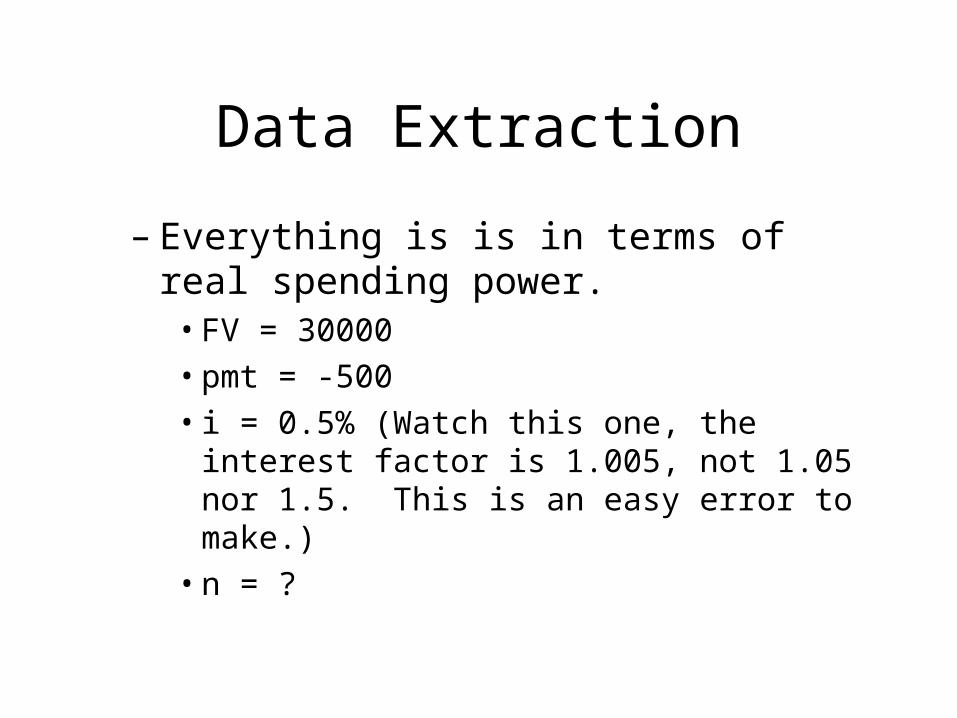

– Everything is is in terms of real spending power.

• FV = 30000

• pmt = -500

• i = 0.5% (Watch this one, the interest factor is 1.005, not 1.05 nor 1.5. This is an easy error to make.)

• n = ?

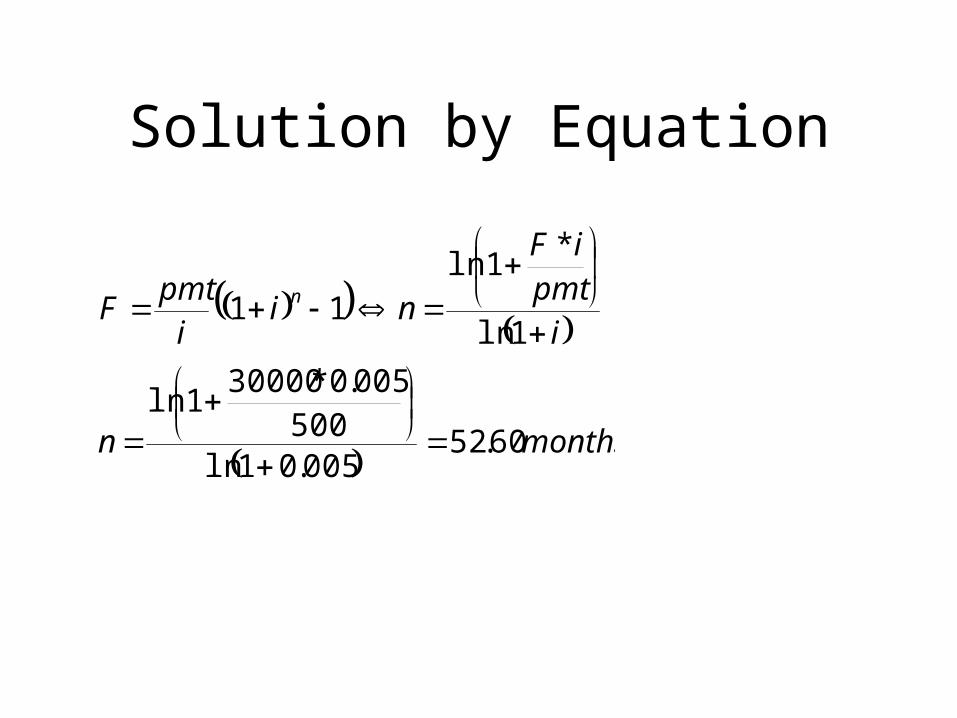

Solution by Equation

monthsn

i

pmtiF

nii

pmtF n

60.52005.01ln

500005.0*30000

1ln

1ln

*1ln

11

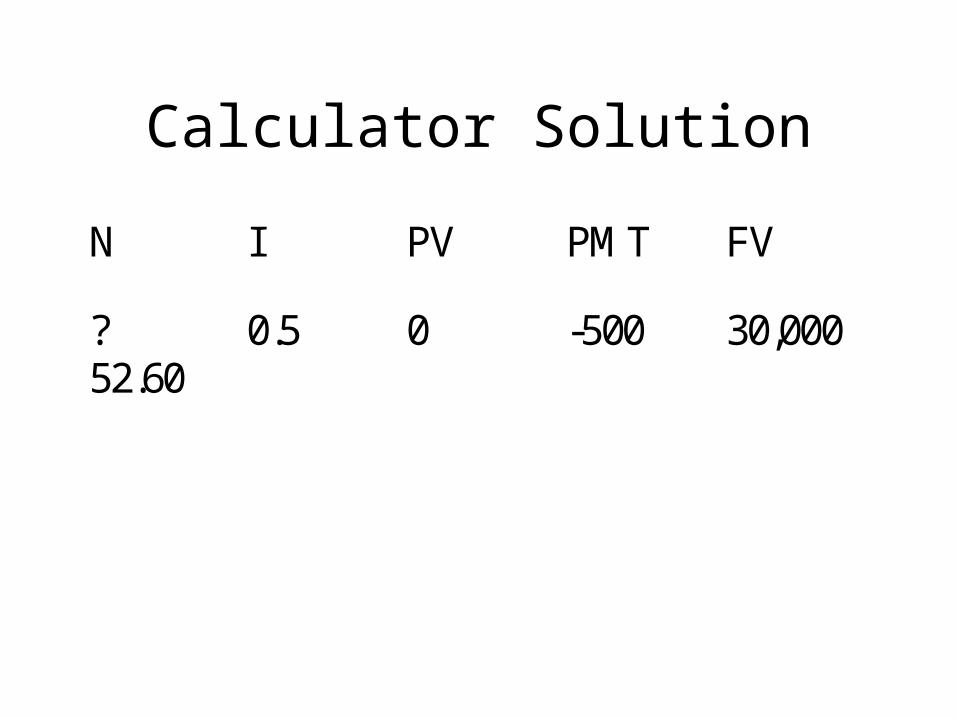

Calculator Solution

N I PV PMT FV

?52.60

0.5 0 -500 30,000

Comments

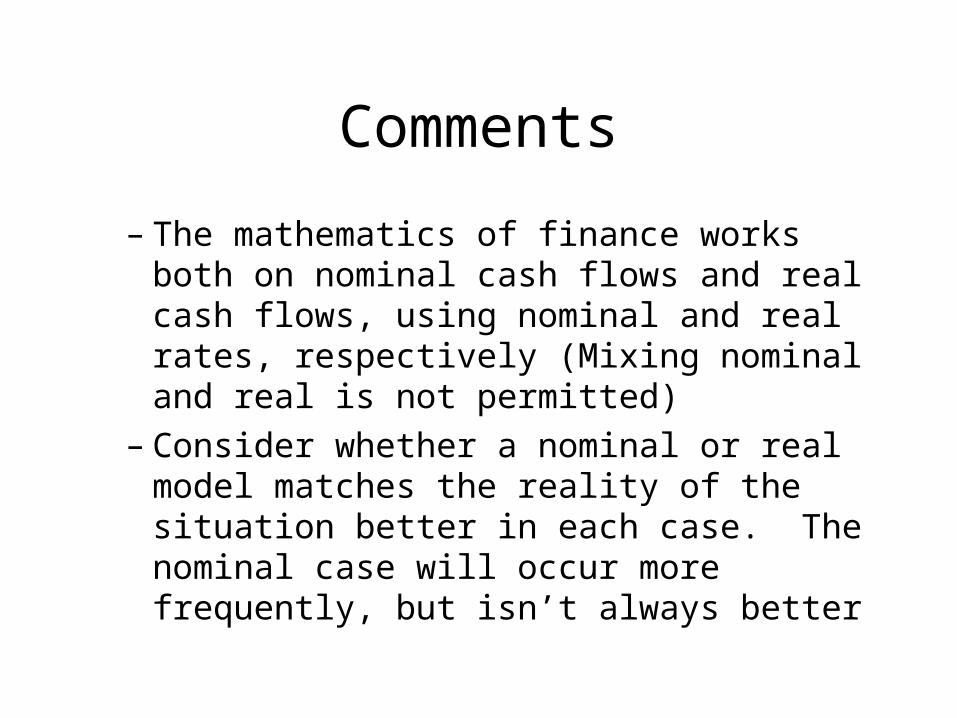

– The mathematics of finance works both on nominal cash flows and real cash flows, using nominal and real rates, respectively (Mixing nominal and real is not permitted)

– Consider whether a nominal or real model matches the reality of the situation better in each case. The nominal case will occur more frequently, but isn’t always better

Additional Solved Problems

Future Value of an Annuity

Find Payment

The Problem

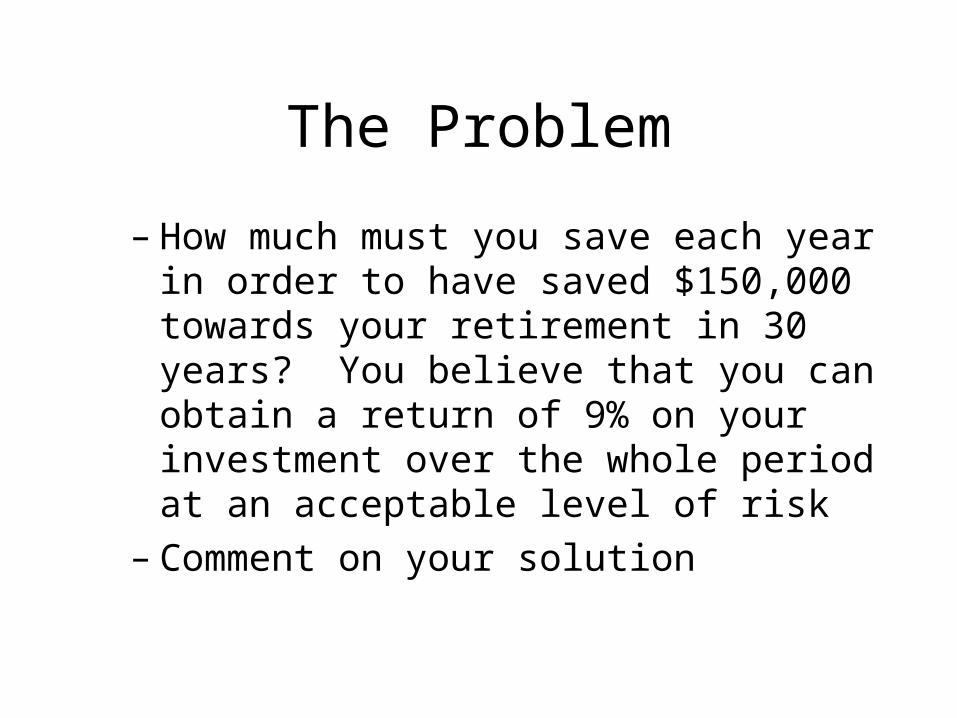

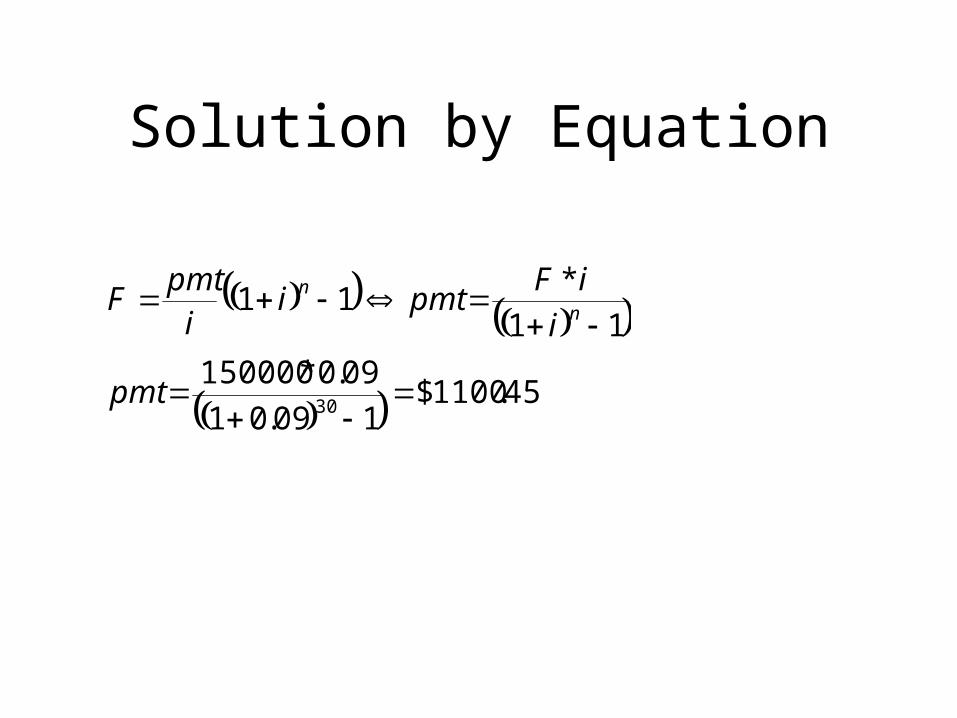

– How much must you save each year in order to have saved $150,000 towards your retirement in 30 years? You believe that you can obtain a return of 9% on your investment over the whole period at an acceptable level of risk

– Comment on your solution

Categorization

– Routine saving is an annuity, and we know what its future value is. We are not told of the starting date of the investment. Assume a regular annuity

– We solve for annual payment

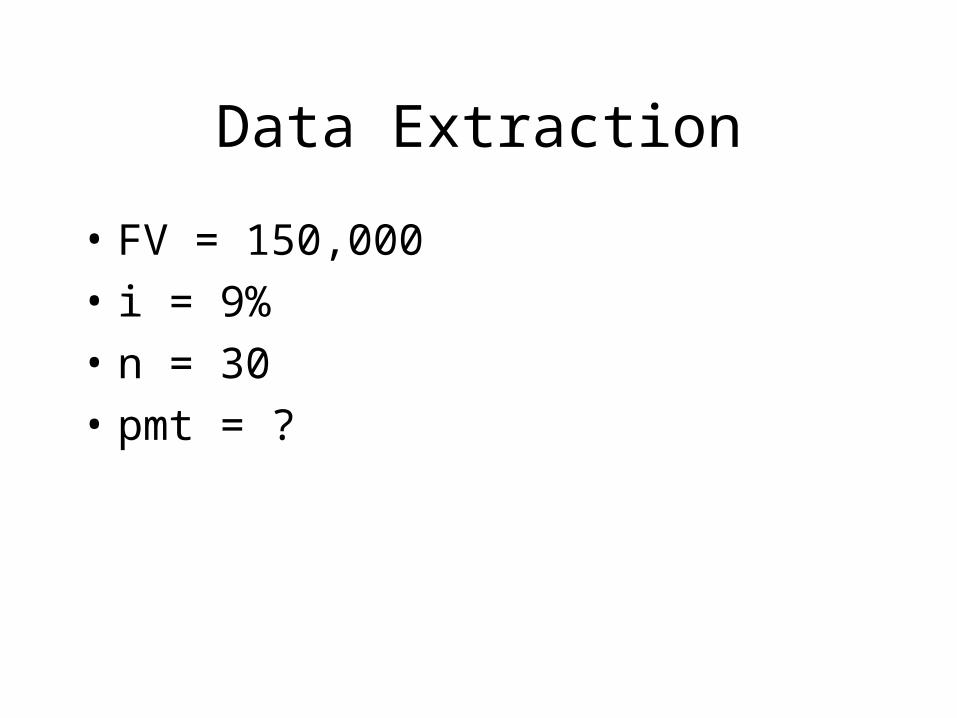

Data Extraction

• FV = 150,000

• i = 9%

• n = 30

• pmt = ?

Solution by Equation

45.1100$109.01

09.0*150000

11

*11

30

pmt

i

iFpmti

ipmt

F n

n

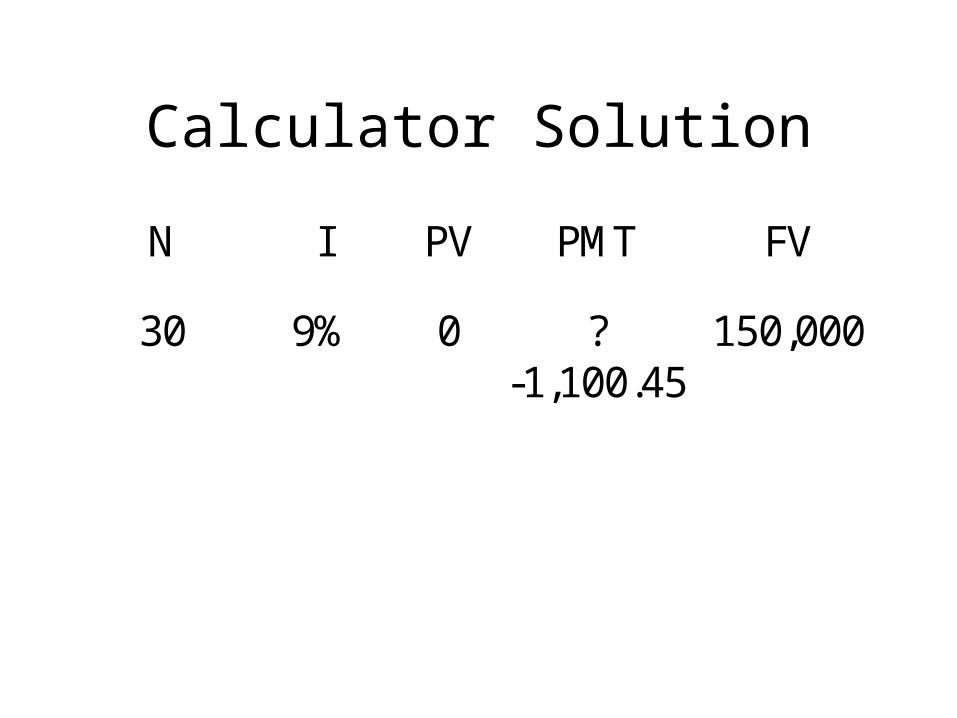

Calculator Solution

N I PV PMT FV

30 9% 0 ?-1,100.45

150,000

Comments

– A financial plan must be tailored to the needs of the individual. We need to take existing wealth, health, financial needs, current income, et cetera, into account

– Given inflation, this plan is almost certainly inadequate for most individuals today

Additional Solved Problems

Special Category

Why Growing Annuities?

– I have all the tools necessary with regular annuities to solve growing annuity problems, so why the additional theory?

• You had all that was required to solve annuities when you learned about lump-sums. Annuities gave you a tool that was faster to use, and corresponded with the real world

• Growing annuities are computationally fast and safe to use, and reflect the real world

The Problem

– The last year’s cash-flow (just received) of the Diamond division of A&A Co was $1,000,000. A&A wishes to sell the division for strategic reasons

– You are the CFO of the Diamond division, and you are planning a leveraged buyout

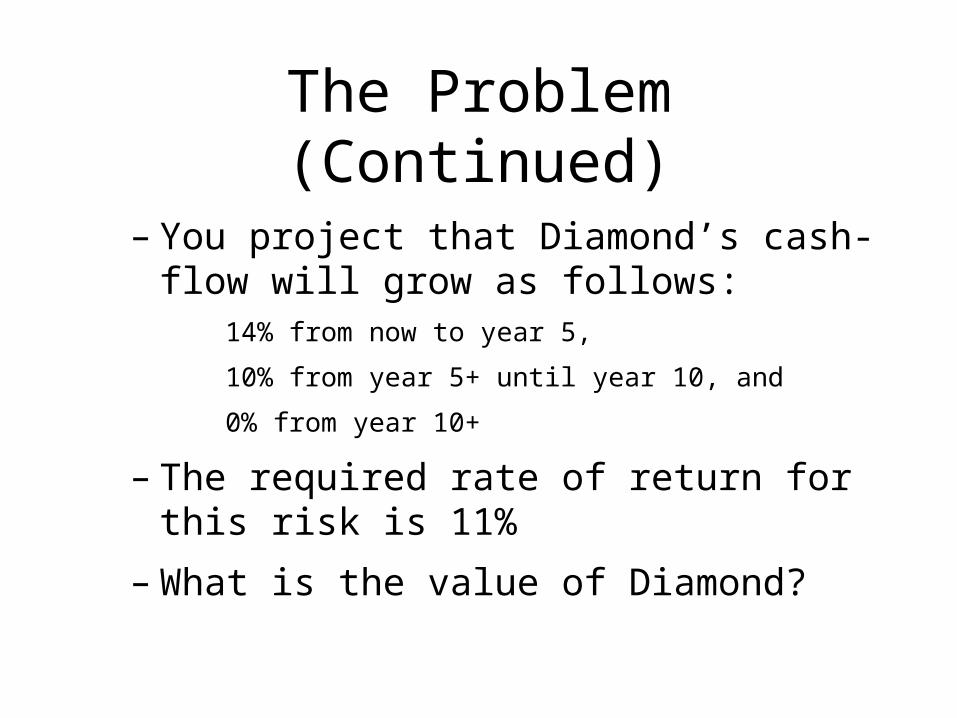

The Problem (Continued)

– You project that Diamond’s cash-flow will grow as follows:

14% from now to year 5,

10% from year 5+ until year 10, and

0% from year 10+

– The required rate of return for this risk is 11%

– What is the value of Diamond?

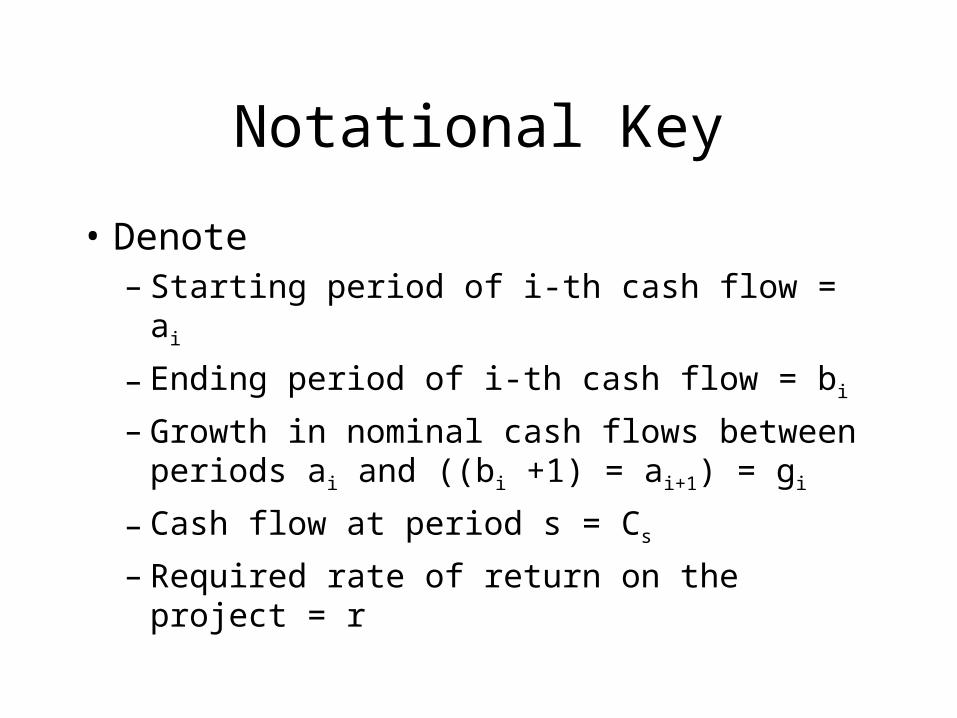

Notational Key

• Denote– Starting period of i-th cash flow = ai

– Ending period of i-th cash flow = bi

– Growth in nominal cash flows between periods ai and ((bi +1) = ai+1) = gi

– Cash flow at period s = Cs

– Required rate of return on the project = r

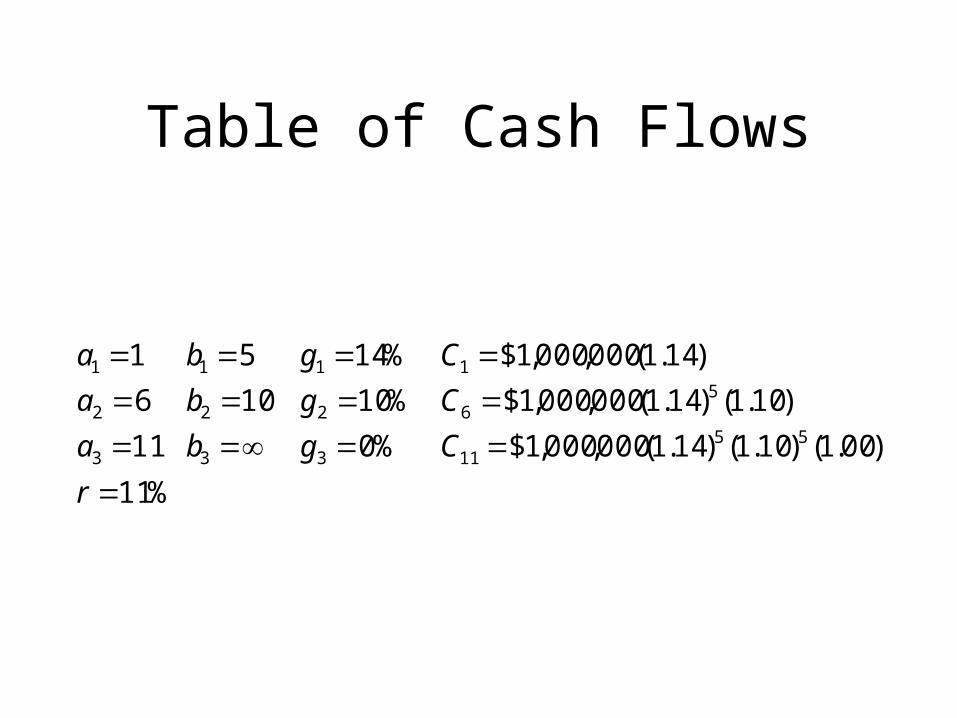

Table of Cash Flows

%11

)00.1()10.1()14.1(000,000,1$%011

)10.1()14.1(000,000,1$%10106

)14.1(000,000,1$%1451

5511333

56222

1111

r

Cgba

Cgba

Cgba

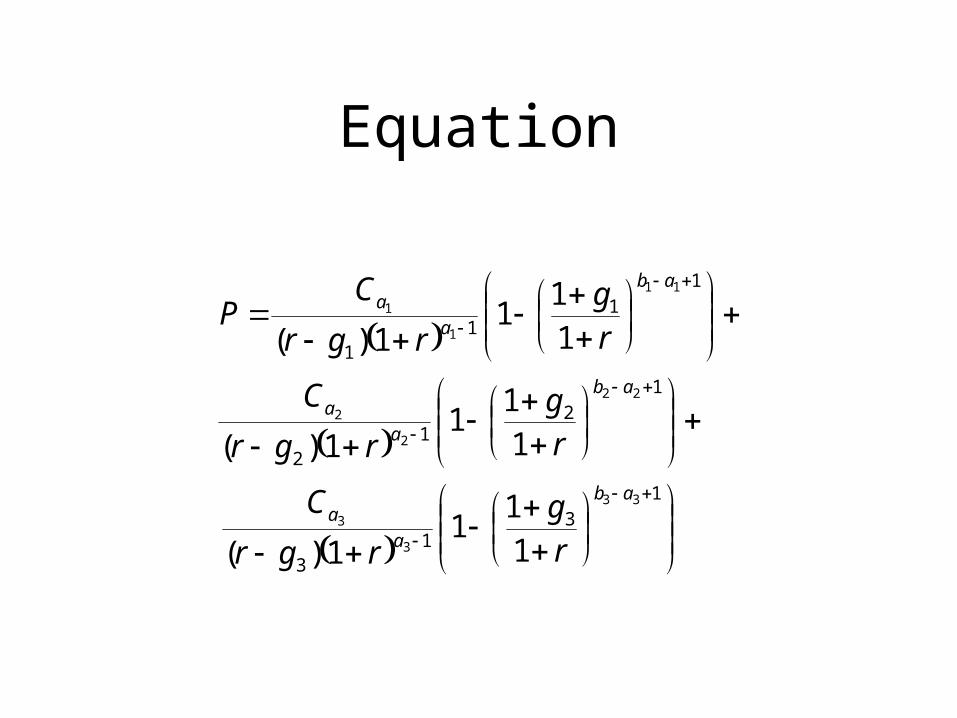

Equation

1

31

3

1

21

2

1

11

1

33

3

3

22

2

2

11

1

1

11

11)(

11

11)(

11

11)(

ab

a

a

ab

a

a

ab

a

a

rg

rgr

C

rg

rgr

C

rg

rgr

CP

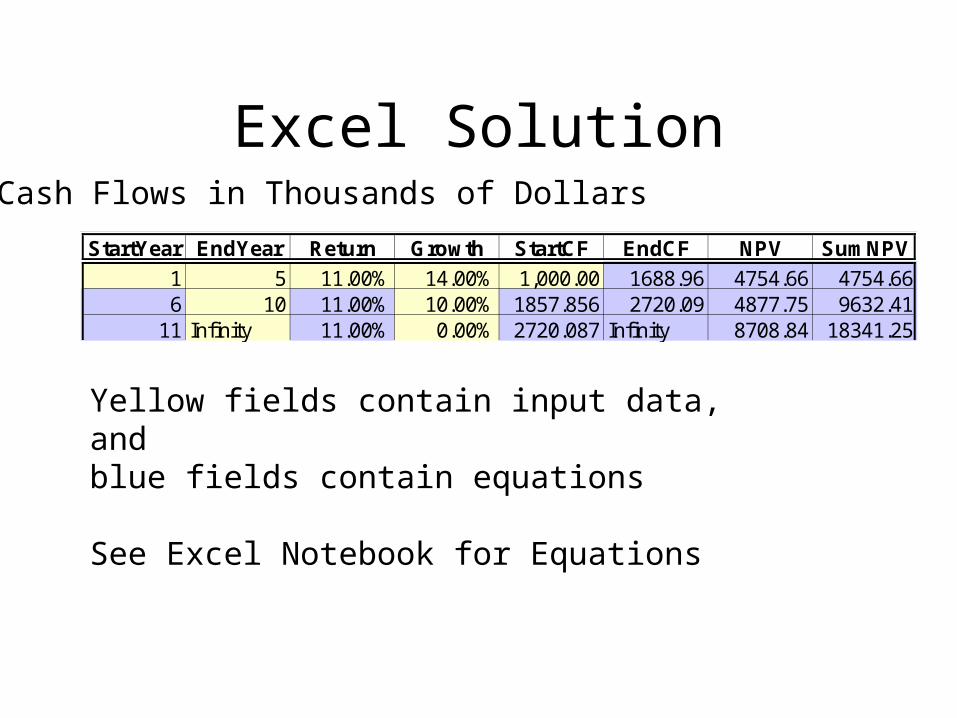

Excel Solution

StartYear EndYear Return Growth StartCF EndCF NPV SumNPV

1 5 11.00% 14.00% 1,000.00 1688.96 4754.66 4754.666 10 11.00% 10.00% 1857.856 2720.09 4877.75 9632.41

11 Infinity 11.00% 0.00% 2720.087 Infinity 8708.84 18341.25

Cash Flows in Thousands of Dollars

Yellow fields contain input data, andblue fields contain equations

See Excel Notebook for Equations

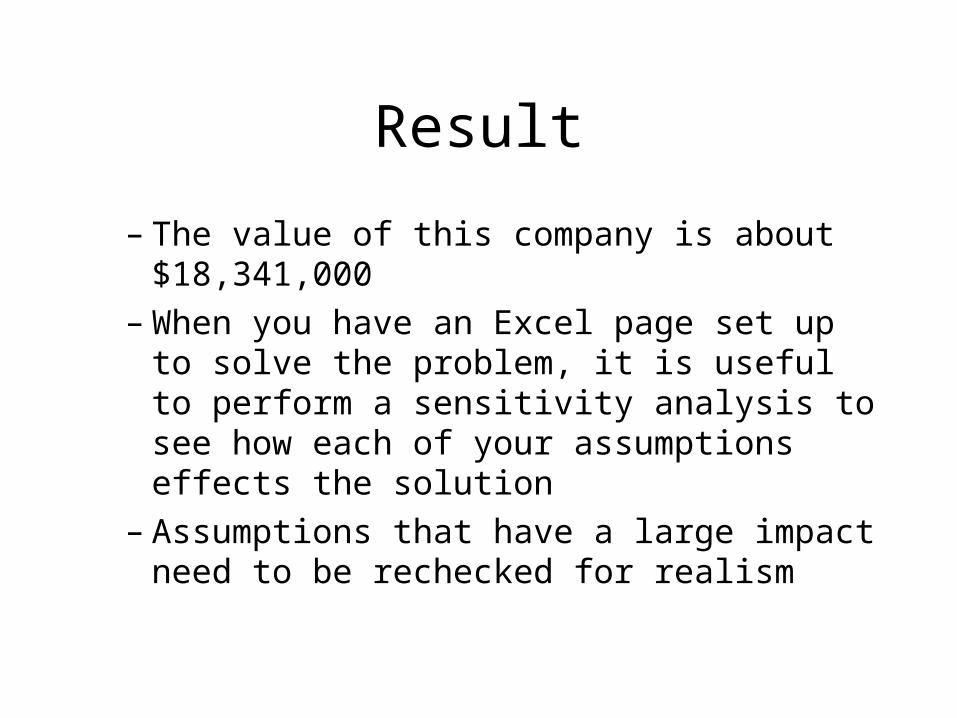

Result

– The value of this company is about $18,341,000

– When you have an Excel page set up to solve the problem, it is useful to perform a sensitivity analysis to see how each of your assumptions effects the solution

– Assumptions that have a large impact need to be rechecked for realism

Comments

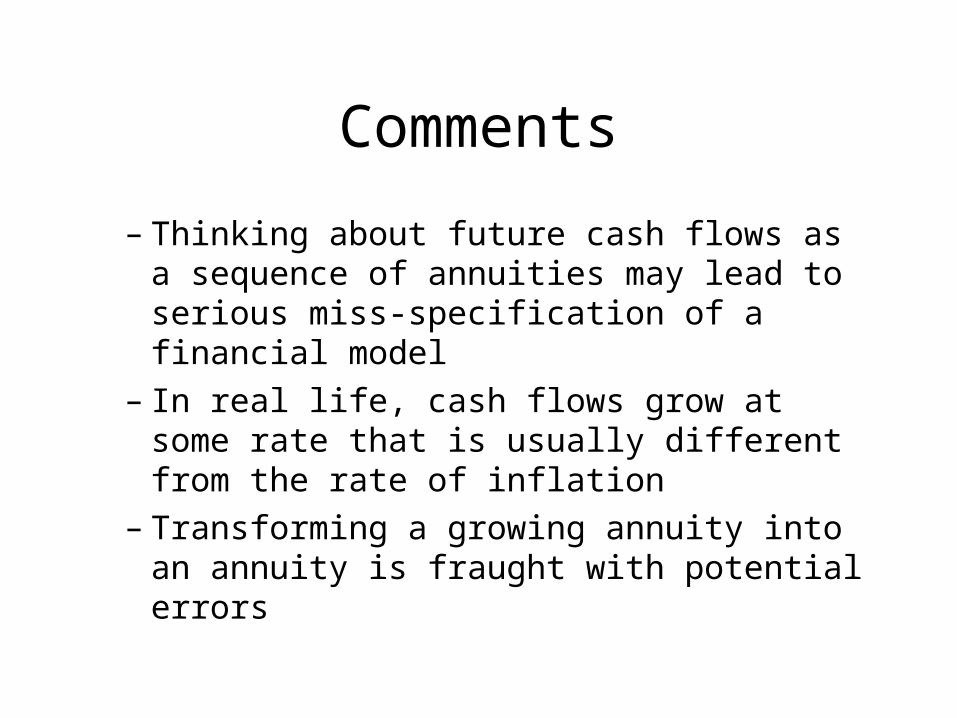

– Thinking about future cash flows as a sequence of annuities may lead to serious miss-specification of a financial model

– In real life, cash flows grow at some rate that is usually different from the rate of inflation

– Transforming a growing annuity into an annuity is fraught with potential errors

Additional Solved Problems

PV Annuity--Mortgage

Payment, Time, PV, & Interest

The Problem

– You took out a mortgage exactly 5-years ago, and have just made the 5th annual payment, leaving 25 more. The interest rate on the mortgage was 8%, and the loan amount was $100,000

– How long would it take to repay the mortgage if you now doubled your repayments?

Solution

– The first step is to determine the annual payments, and the outstanding amount.

– We will use equations

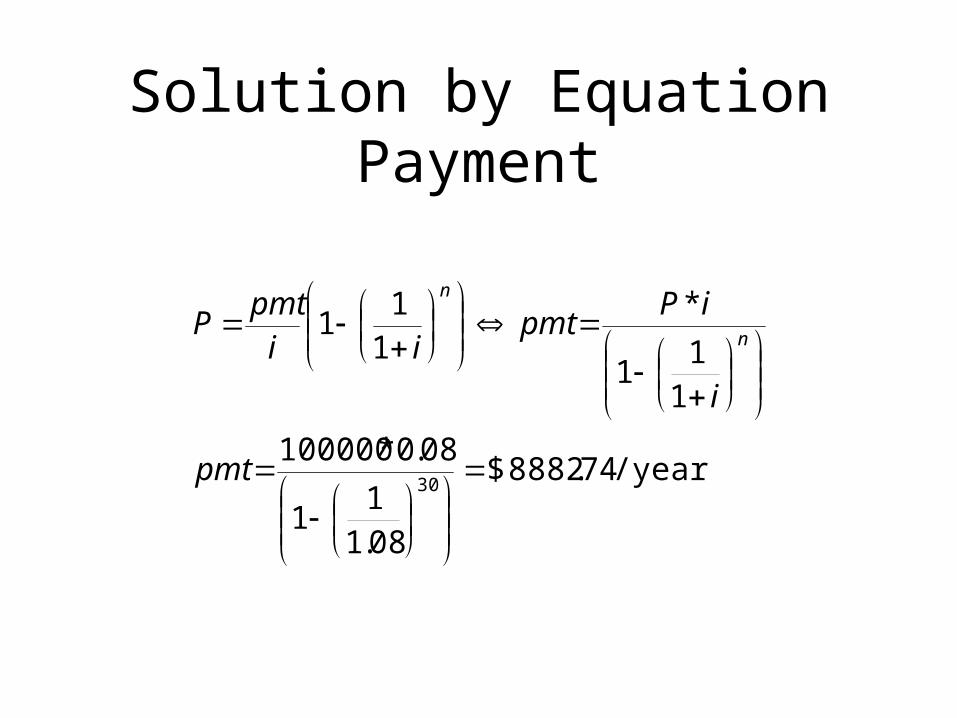

Solution by EquationPayment

/year74.8882$

08.11

1

08.0*100000

11

1

*1

11

30

pmt

i

iPpmt

iipmt

Pn

n

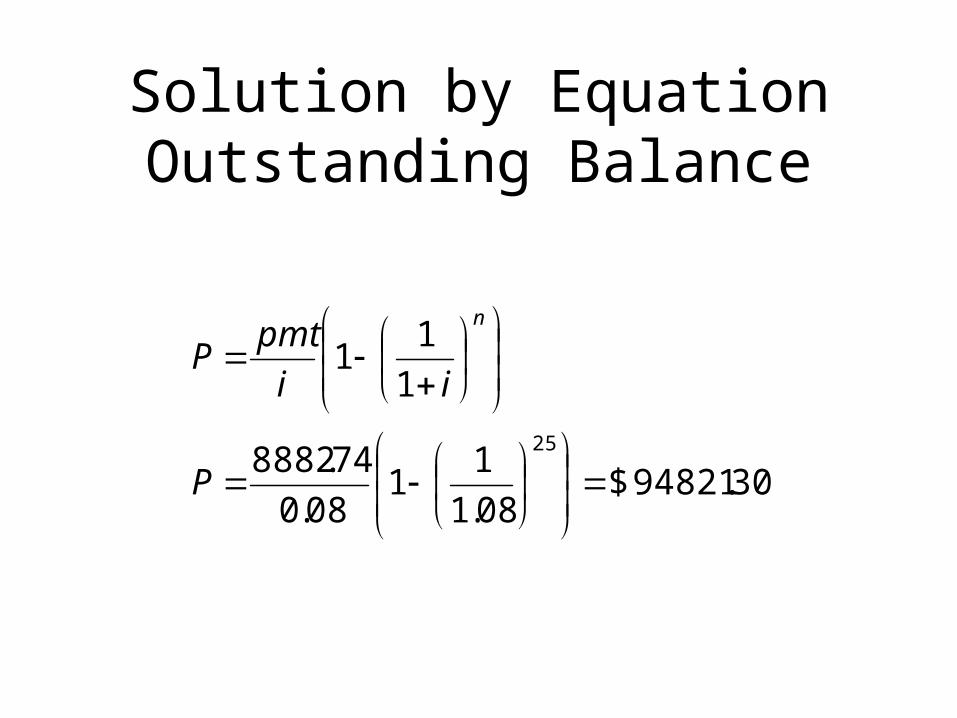

Solution by EquationOutstanding Balance

30.94821$08.1

11

08.0

74.8882

1

11

25

P

ii

pmtP

n

Solution (Continued)

• The next step is to find how long it takes to repay the mortgage with double payments

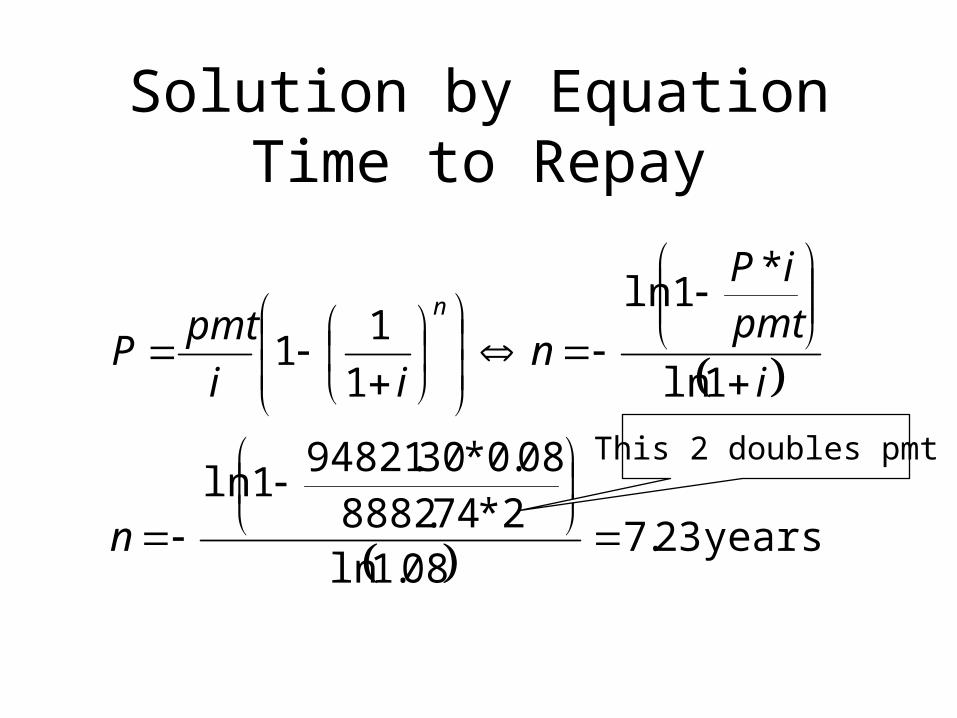

Solution by EquationTime to Repay

years23.708.1ln

2*74.888208.0*30.94821

1ln

1ln

*1ln

1

11

n

i

pmtiP

nii

pmtP

n

This 2 doubles pmt

Problem (Continued)Finding the Rate

– The mortgage was obtained by paying 3 points, that is although the $100,000 was borrowed, the lender charged an up-front fee, or prepayment of interest, of $1000000 * 0.03

– If the mortgage were repaid 5 years after it was obtained, what was the implied interest rate on the transaction?

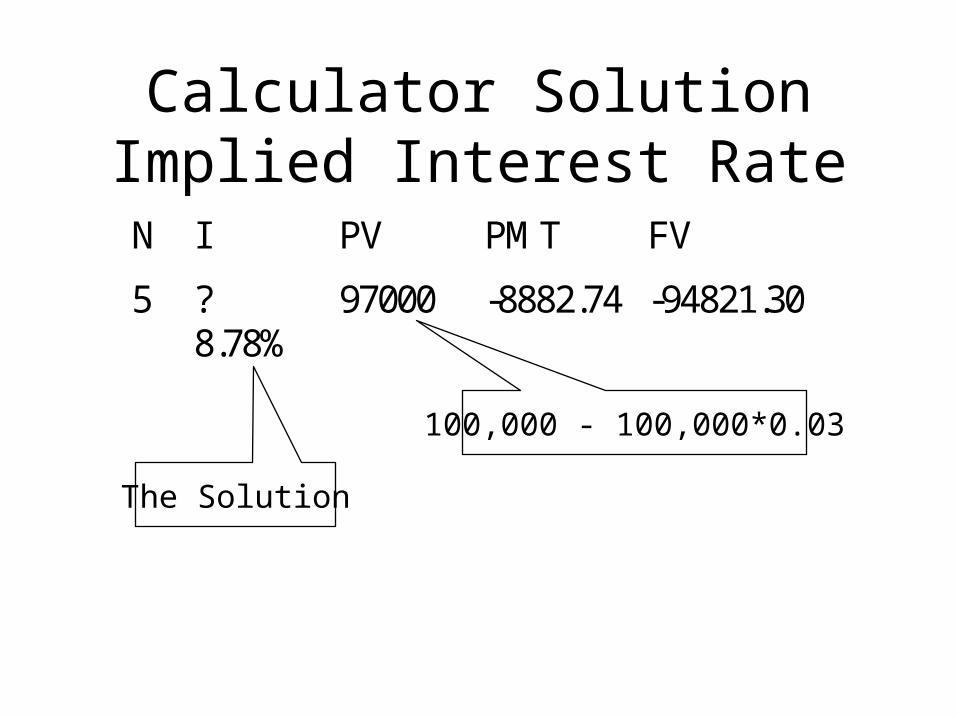

Calculator SolutionImplied Interest Rate

N I PV PMT FV

5 ?8.78%

97000 -8882.74 -94821.30

100,000 - 100,000*0.03

The Solution

Comments

• This mortgage problem has covered all cases of the PV of an annuity problem

• The financial calculator was used to solve the implied interest part because there is no closed form algebraic form

Additional Solved Problems

Valuing a bond against another bond

Generality of Treatment

– Real-life bonds often pay their coupon semi-annually, and these will be investigated later

– We will examine bonds that pay annual coupons to simplify the problem

– A flat yield curve is assumed

The Problem

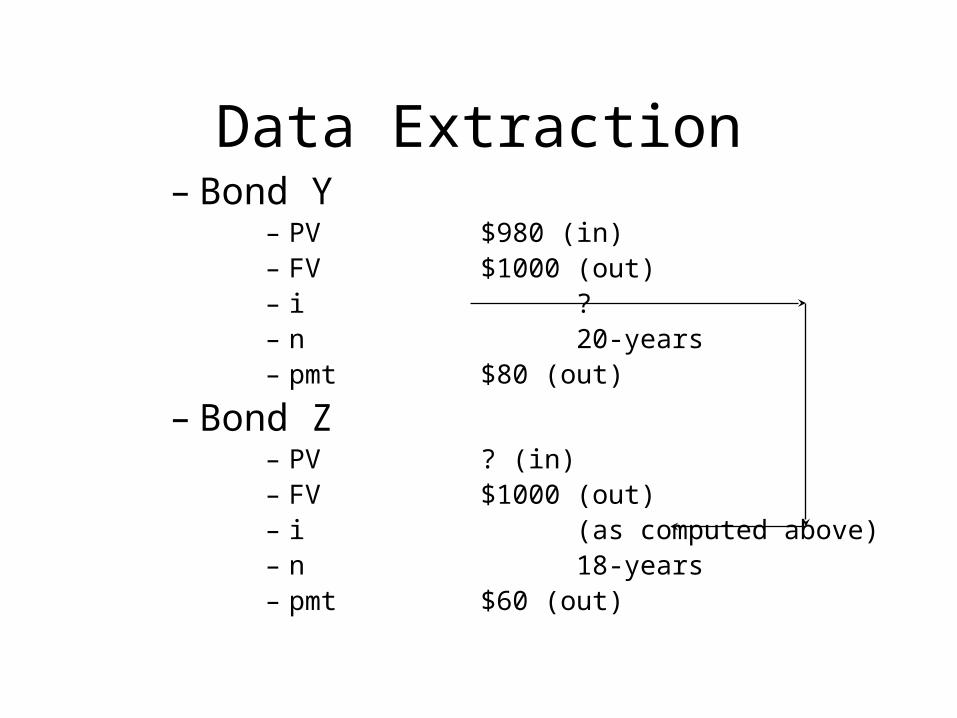

• You have discovered two bonds that should have the same yields-to-maturity– Bond Y is currently trading at $980, has a

remaining life of 20-years, an annual coupon of $80, and a face value of $1000

– Bond Z has a remaining life of 18-years, a face of $1000, and an annual coupon of $60. What’s the value bond Z?

Categorization

– To solve this problem you need to • Determine the yield-to-maturity on bond Y

• Using this ytm, compute the value of bond Z

– The quickest way to solve the problem is to use your financial calculator, or Excel

– An algebraic method is also given because it uses a powerful solution method you may not have seen before

Data Extraction– Bond Y

– PV $980 (in)– FV $1000 (out)– i ?– n 20-years– pmt $80 (out)

– Bond Z– PV ? (in)– FV $1000 (out)– i (as computed above)– n 18-years– pmt $60 (out)

Finding the Yield-to-Maturity

– We have already discovered that finding the implied interest rate on an annuity is not possible (in general) using standard algebra

– Determining bond yields is a common problem for investors

– The following method applies to solving any problem in algebra, but some work is required to create the solution algorithm

Finding the Yield-to-Maturity

– A theorem that states that if x = F(x), inserting an arbitrary value of x into F(x) always leads to a value of x that is either (a) always closer to the true value of x, or else (b) always further from the true value

• The trick is to find an F(.) that leads to case (a), convergence

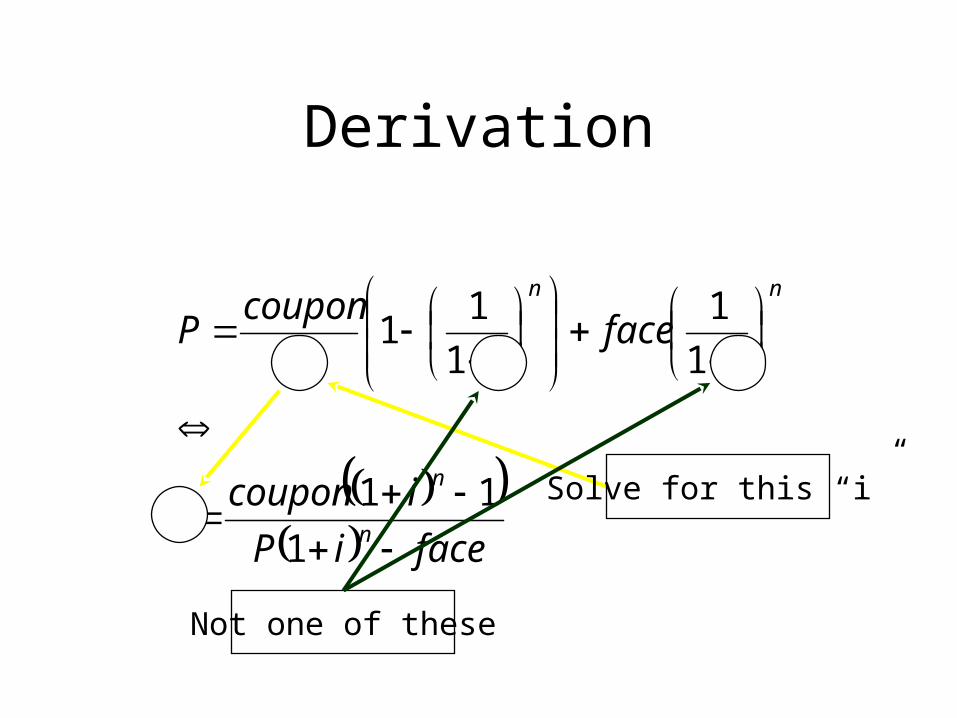

Derivation

faceiP

icouponi

iface

ii

couponP

n

n

nn

1

11

1

1

1

11

Solve for this “i”

Not one of these

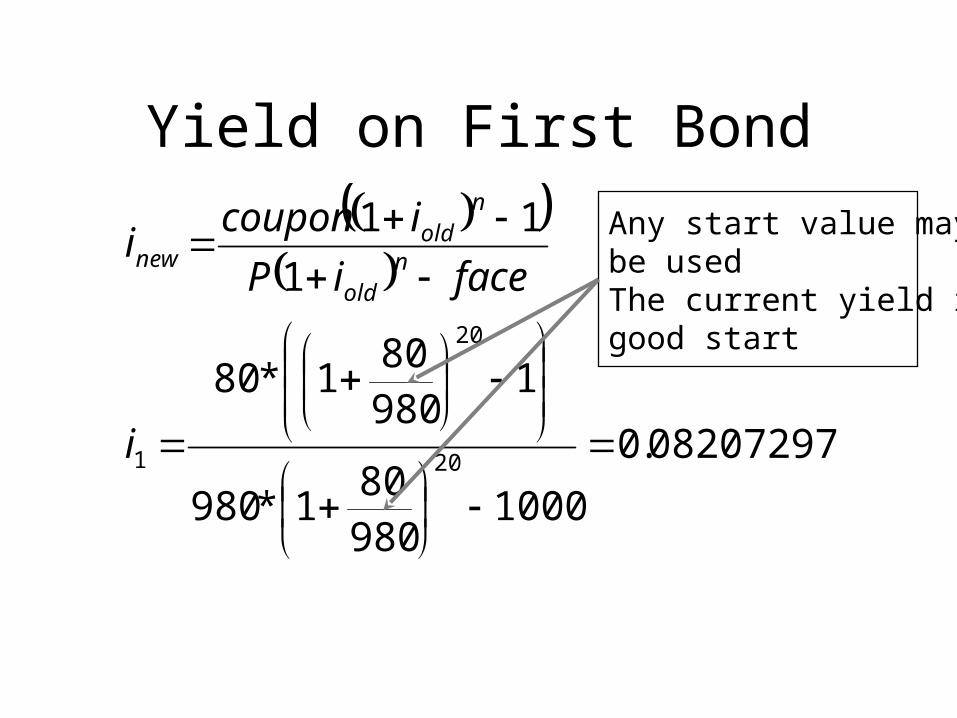

Yield on First Bond

082072977.0

100098080

1*980

198080

1*80

1

11

20

20

1

i

faceiP

icouponi n

old

nold

new

Any start value may be usedThe current yield is a good start

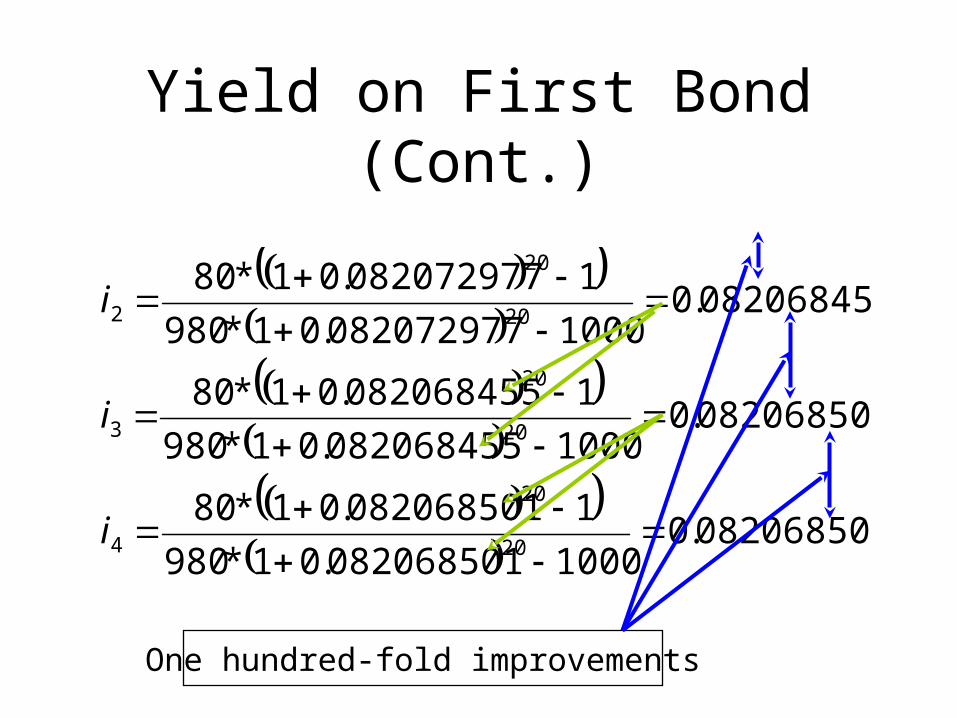

Yield on First Bond (Cont.)

082068500.0

1000082068501.01*980

1082068501.01*80

082068501.01000082068455.01*980

1082068455.01*80

082068455.01000082072977.01*980

1082072977.01*80

20

20

4

20

20

3

20

20

2

i

i

i

One hundred-fold improvements

Observation

– Convergence has occurred in 4 iterations– Common sense would have permitted us to stop

at the end of the second iteration when the nearest basis point had been achieved

– In bond calculations it is traditional to round to the nearest basis point, 1% of 1%. Doing so will save you iterations, but result in only minor inaccuracies

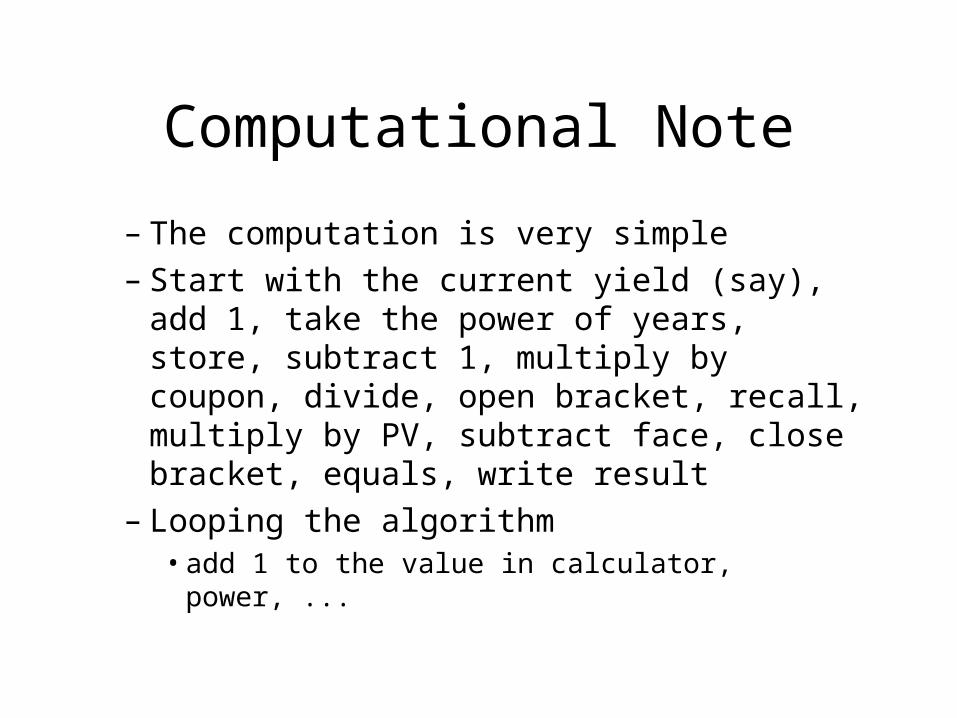

Computational Note

– The computation is very simple – Start with the current yield (say), add 1, take

the power of years, store, subtract 1, multiply by coupon, divide, open bracket, recall, multiply by PV, subtract face, close bracket, equals, write result

– Looping the algorithm• add 1 to the value in calculator, power, ...

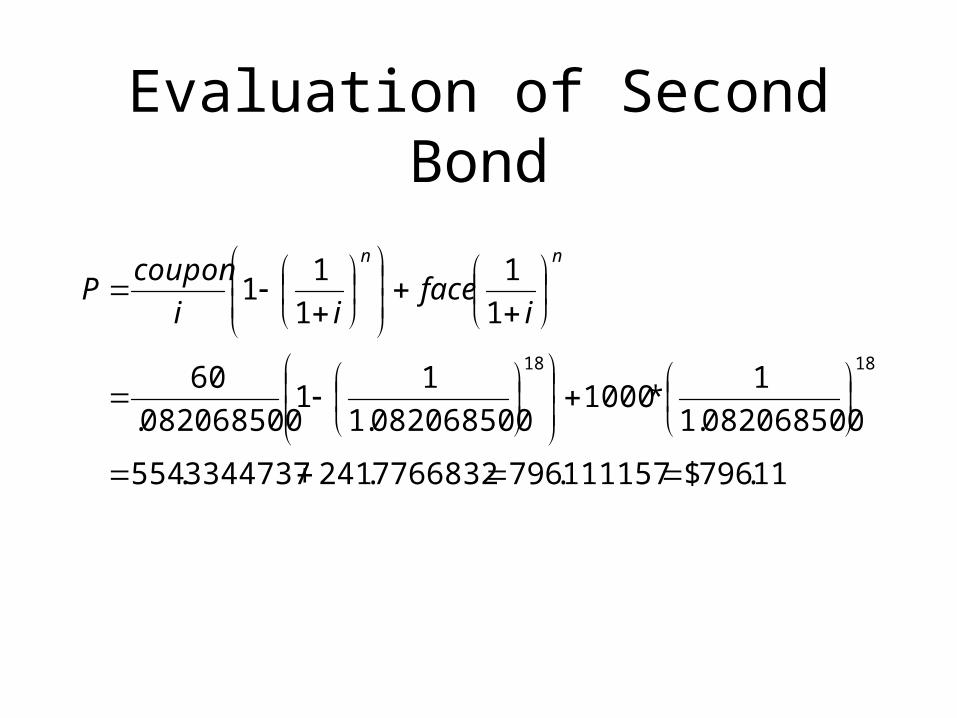

Evaluation of Second Bond

11.796$111157.7967766832.2413344737.554

082068500.1

1*1000

082068500.1

11

082068500.

60

1

1

1

11

1818

nn

iface

ii

couponP

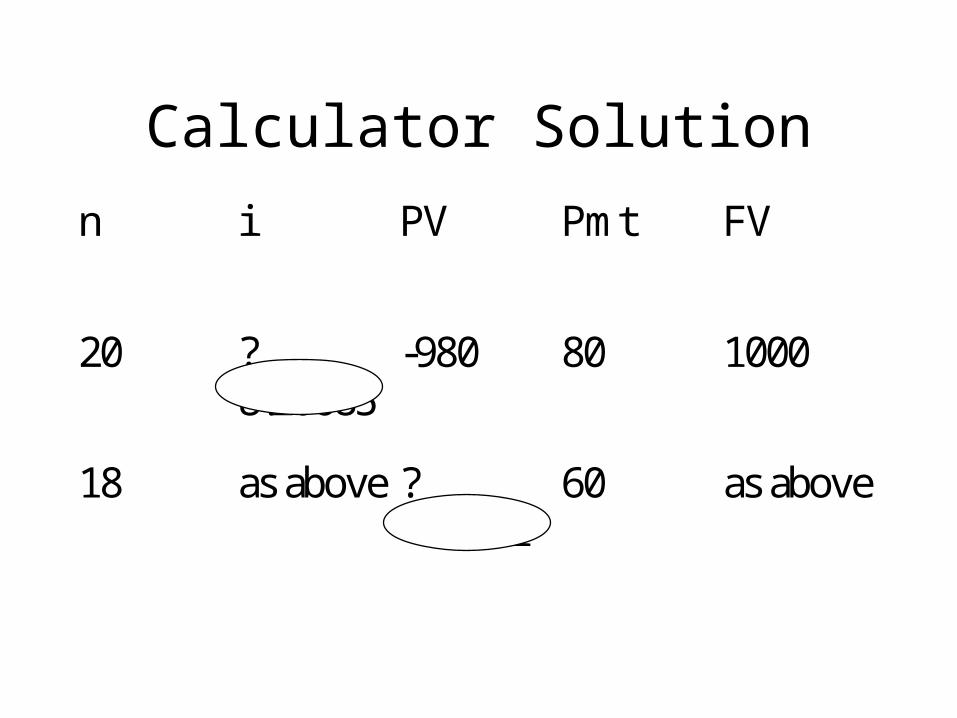

Calculator Solution

n i PV Pmt FV

20 ?8.20685

-980 80 1000

18 as above ?-796.11

60 as above

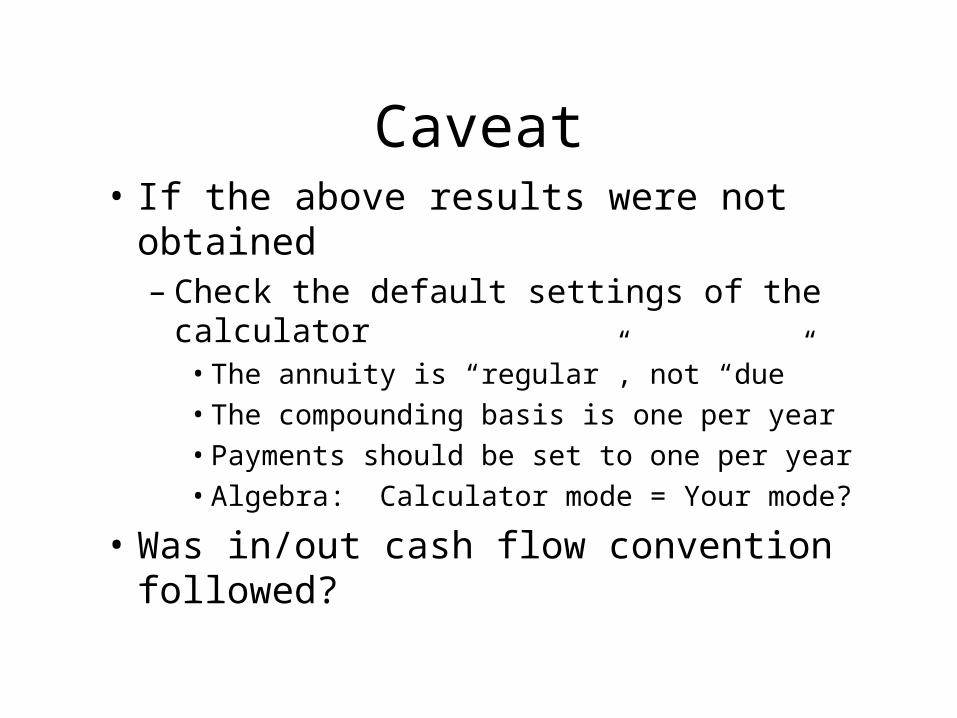

Caveat• If the above results were not obtained

– Check the default settings of the calculator• The annuity is “regular”, not “due”

• The compounding basis is one per year

• Payments should be set to one per year

• Algebra: Calculator mode = Your mode?

• Was in/out cash flow convention followed?

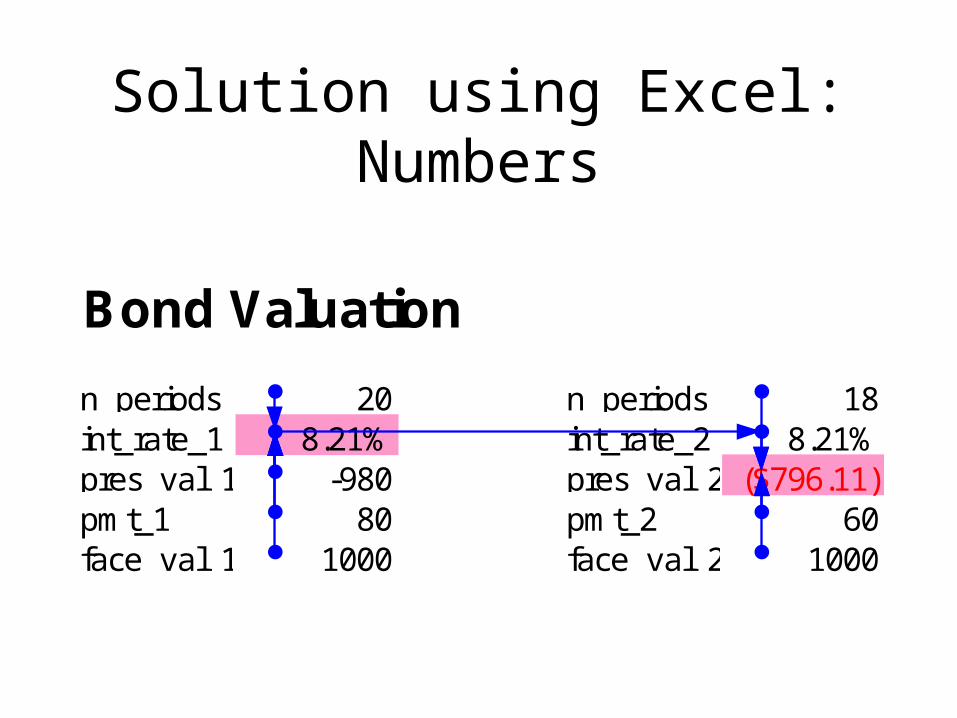

Solution using Excel: Numbers

Bond Valuation

n_periods_1 20 n_periods_2 18int_rate_1 8.21% int_rate_2 8.21%pres_val_1 -980 pres_val_2 ($796.11)pmt_1 80 pmt_2 60face_val_1 1000 face_val_2 1000

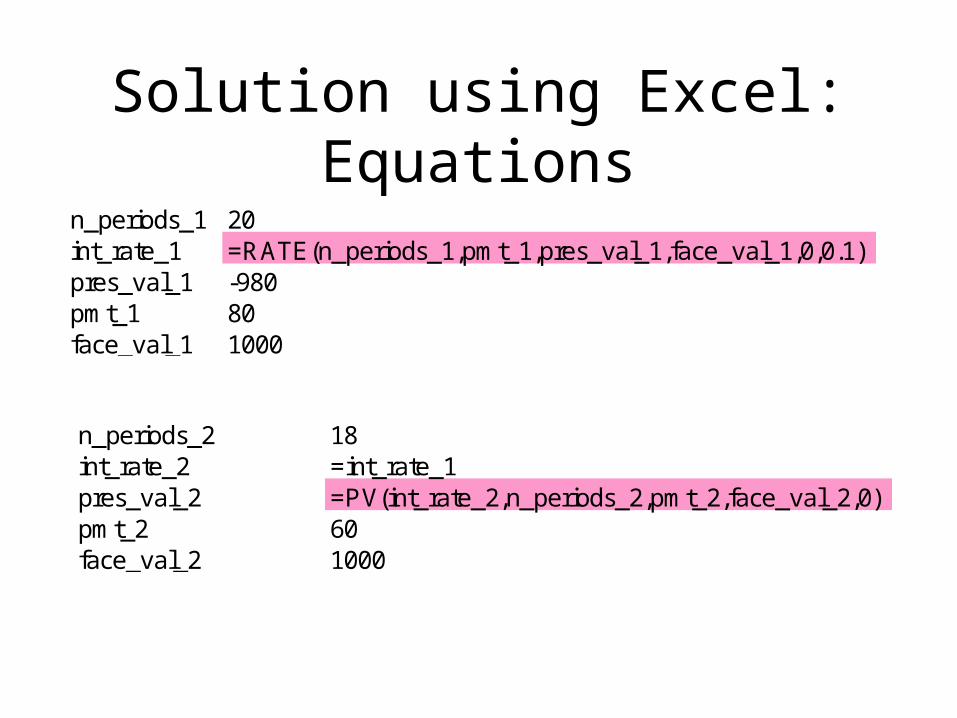

Solution using Excel: Equations

n_periods_2 18int_rate_2 =int_rate_1pres_val_2 =PV(int_rate_2,n_periods_2,pmt_2,face_val_2,0)pmt_2 60face_val_2 1000

n_periods_1 20int_rate_1 =RATE(n_periods_1,pmt_1,pres_val_1,face_val_1,0,0.1)pres_val_1 -980pmt_1 80face_val_1 1000

Naming of Variables

– Rather than use the cell references (difficult to follow), each variable was named using the “Insert, Name, Create” menu

– Some of the statistical and financial functions don’t work quite as expected

• Before using a function the first time, either check it using a known solution, or check the function’s documentation

Comments

– The x = F(x) trick works very well for regular bonds. However, as the ratio of FV to PV becomes small, the convergence rate starts to declines drastically. An alternative function therefore needs to be found to find the yield on a mortgage

– The method may be generalized to “solve” non-linear simultaneous equations