Embed Size (px)

Citation preview

“Addressing Long Term Care Needs”

Presented by: Robert B. McCalla, PhD, CLU, ChFC, CFP®

Outline

• IntroducEon • Brief review of Long Term Care Needs • Long Term Care—what are the opEons? • Long Term Care Insurance—what is it? • QuesEons

IntroducEon

• Robert B. McCalla, PhD, CLU, ChFC, CFP® • Director, Personal Finance Program • Department of Consumer Science • School of Human Ecology

– [email protected] – (608) 262-‐1810

What are long-‐term care needs?

• Long-‐Term care can be thought of as a “range of services and supports needed for day-‐to-‐day living”

• These needs are independent of age – For our purposes though, we will discuss them in the context of reErees

• As a shorthand, we can call them “Ac#vi#es of Daily Living”

• We can discuss “Basic ADLs” and “Instrumental ADLs”

AcEviEes of Daily Living

Basic • Bathing • Dressing • Using the toilet • Transferring (Bed to chair,

etc) • EaEng • Caring for InconEnence

Instrumental • Housework • Managing money • Taking medicaEons • Meal preparaEon and clean

up • Shopping for food and

clothing • CommunicaEons • Caring for pets • Awareness of surroudings

What is the challenge?

Simply put… • As a person ages, the odds of being able to successfully carry out various AcEviEes of Daily Living decrease

• Many will make it through their lives without ever being challenged by ADLs

• Many won’t. • The challenge: What to do?

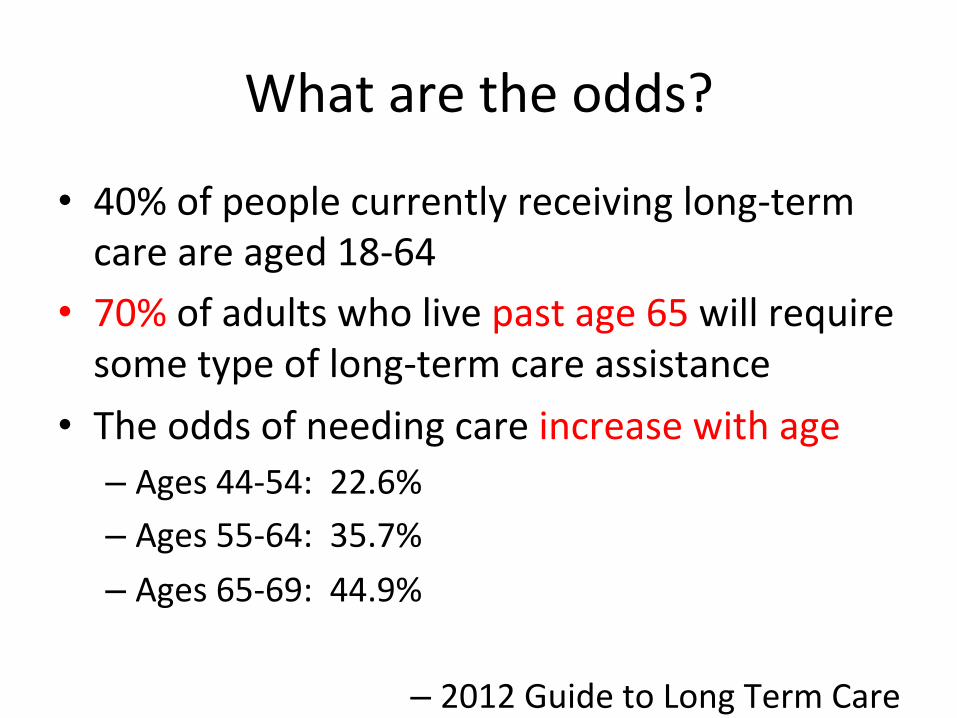

What are the odds?

• 40% of people currently receiving long-‐term care are aged 18-‐64

• 70% of adults who live past age 65 will require some type of long-‐term care assistance

• The odds of needing care increase with age – Ages 44-‐54: 22.6% – Ages 55-‐64: 35.7% – Ages 65-‐69: 44.9%

– 2012 Guide to Long Term Care

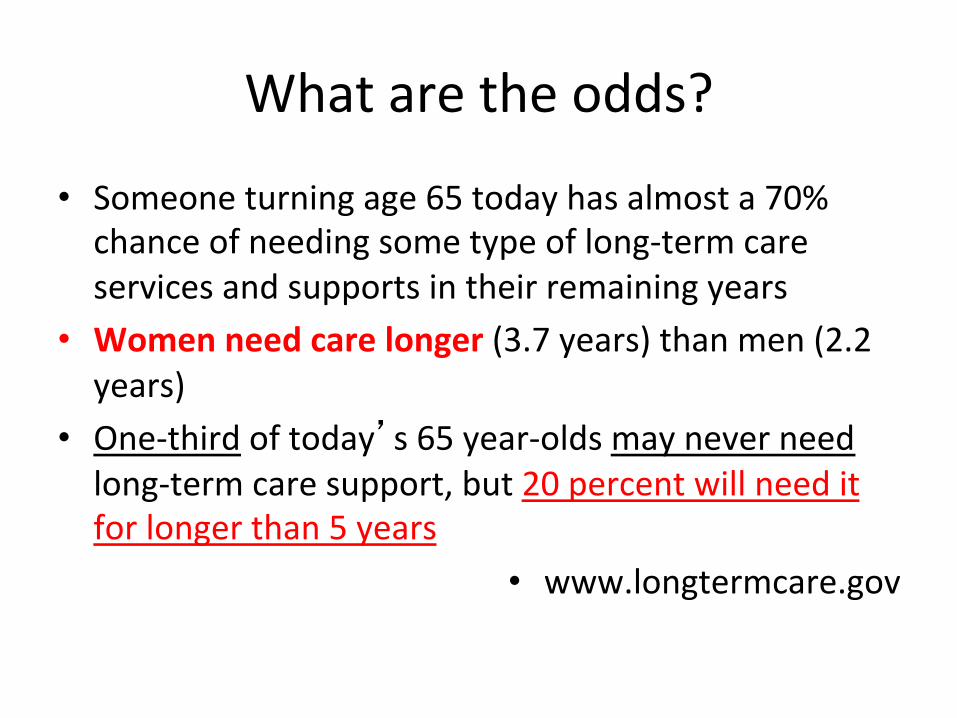

What are the odds?

• Someone turning age 65 today has almost a 70% chance of needing some type of long-‐term care services and supports in their remaining years

• Women need care longer (3.7 years) than men (2.2 years)

• One-‐third of today’s 65 year-‐olds may never need long-‐term care support, but 20 percent will need it for longer than 5 years

• www.longtermcare.gov

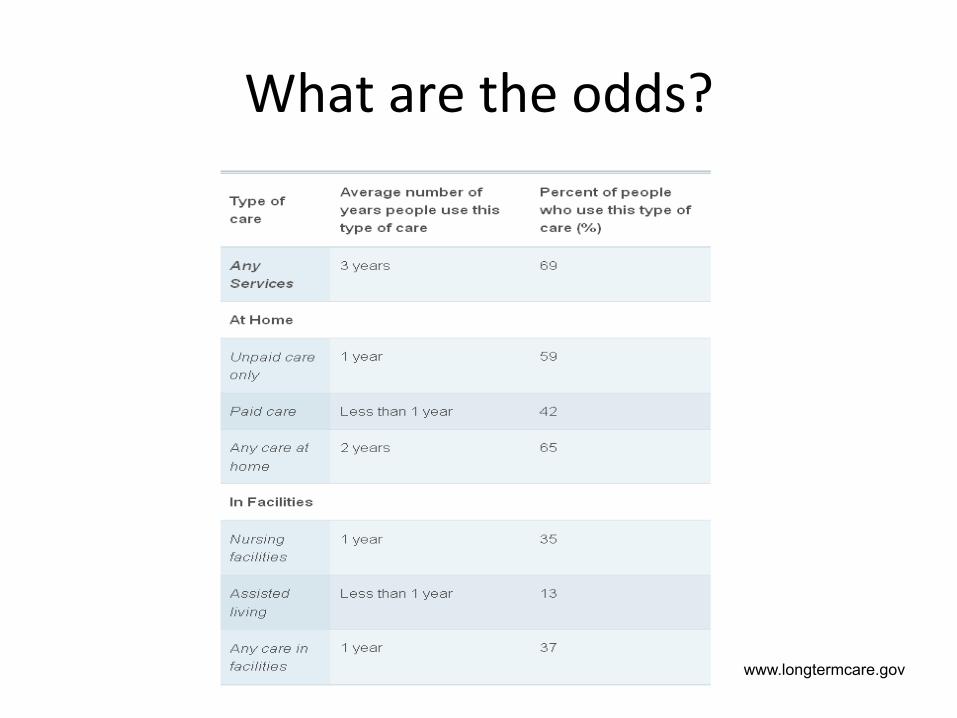

What are the odds?

www.longtermcare.gov

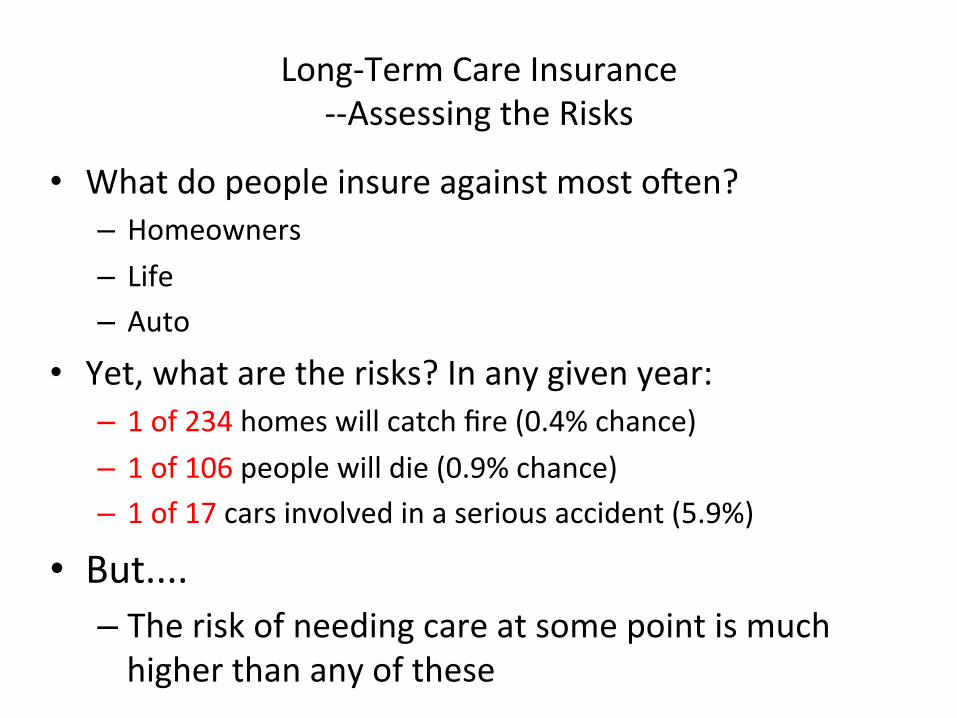

Long-‐Term Care Insurance -‐-‐Assessing the Risks

• What do people insure against most oeen? – Homeowners – Life – Auto

• Yet, what are the risks? In any given year: – 1 of 234 homes will catch fire (0.4% chance) – 1 of 106 people will die (0.9% chance) – 1 of 17 cars involved in a serious accident (5.9%)

• But.... – The risk of needing care at some point is much higher than any of these

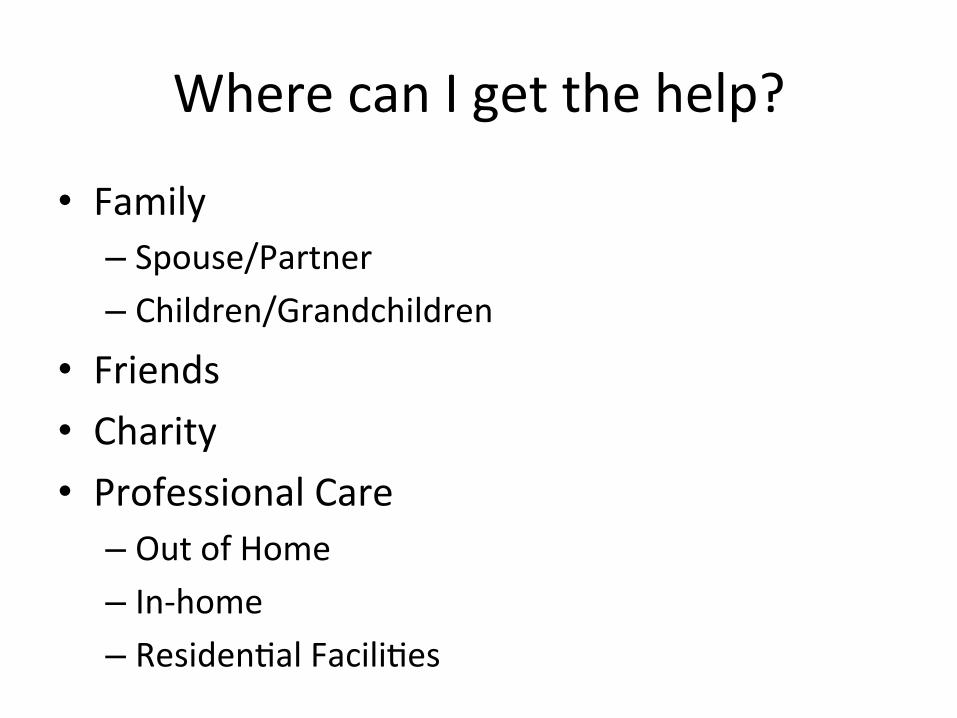

Where can I get the help?

• Family – Spouse/Partner – Children/Grandchildren

• Friends • Charity • Professional Care

– Out of Home – In-‐home – ResidenEal FaciliEes

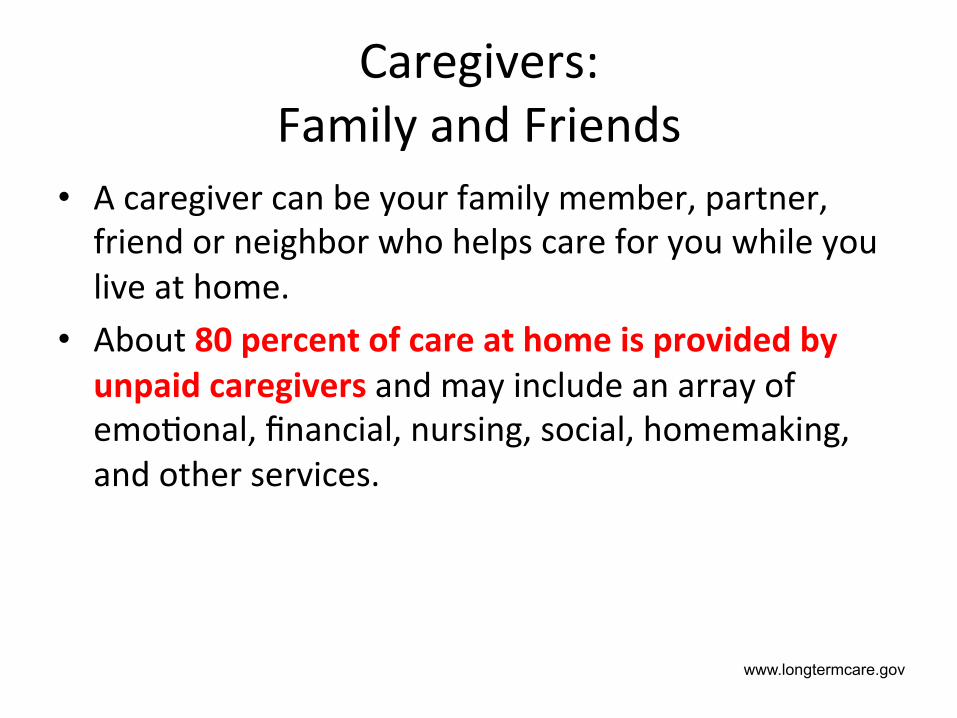

Caregivers: Family and Friends

• A caregiver can be your family member, partner, friend or neighbor who helps care for you while you live at home.

• About 80 percent of care at home is provided by unpaid caregivers and may include an array of emoEonal, financial, nursing, social, homemaking, and other services.

www.longtermcare.gov

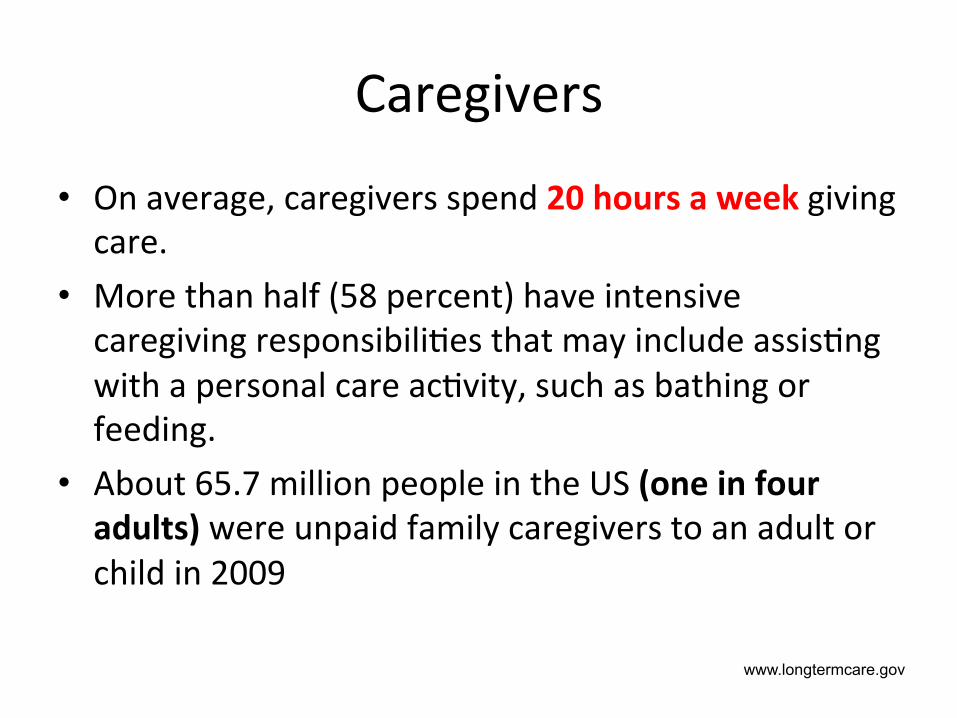

Caregivers

• On average, caregivers spend 20 hours a week giving care.

• More than half (58 percent) have intensive caregiving responsibiliEes that may include assisEng with a personal care acEvity, such as bathing or feeding.

• About 65.7 million people in the US (one in four adults) were unpaid family caregivers to an adult or child in 2009

www.longtermcare.gov

Caregivers

• About two-‐thirds are women • Fourteen percent who care for older adults are themselves age 65 or more

• Most people can live at home for many years with help from unpaid family and friends, and from other paid community support

www.longtermcare.gov

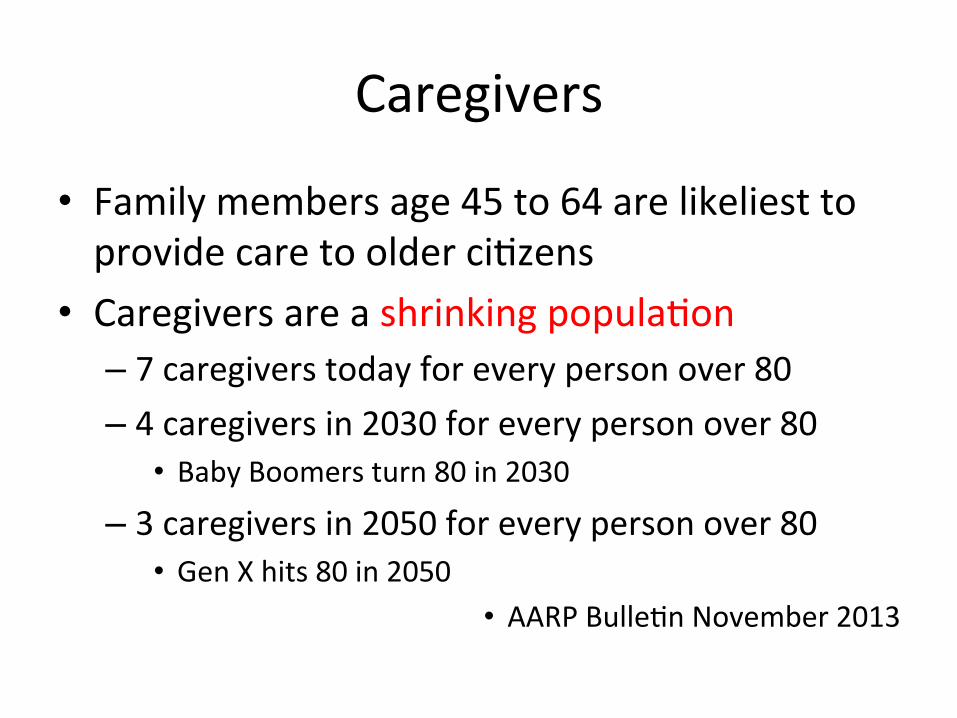

Caregivers

• Family members age 45 to 64 are likeliest to provide care to older ciEzens

• Caregivers are a shrinking populaEon – 7 caregivers today for every person over 80 – 4 caregivers in 2030 for every person over 80

• Baby Boomers turn 80 in 2030

– 3 caregivers in 2050 for every person over 80 • Gen X hits 80 in 2050

• AARP BulleEn November 2013

What if this is too much for family and friends?

What if I need professional help?

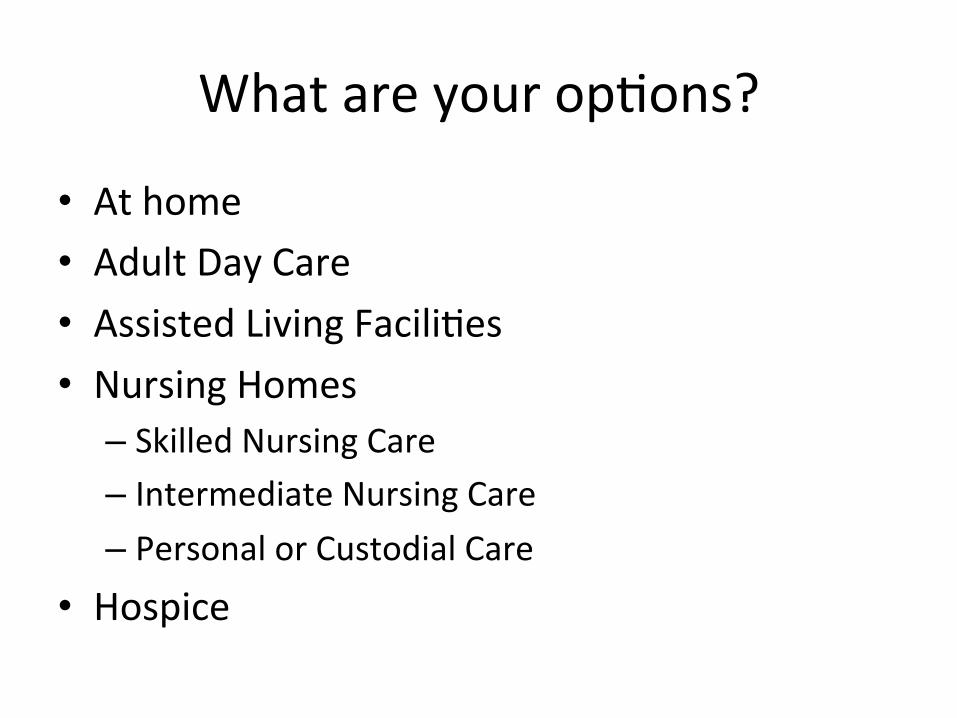

What are your opEons?

• At home • Adult Day Care • Assisted Living FaciliEes • Nursing Homes

– Skilled Nursing Care – Intermediate Nursing Care – Personal or Custodial Care

• Hospice

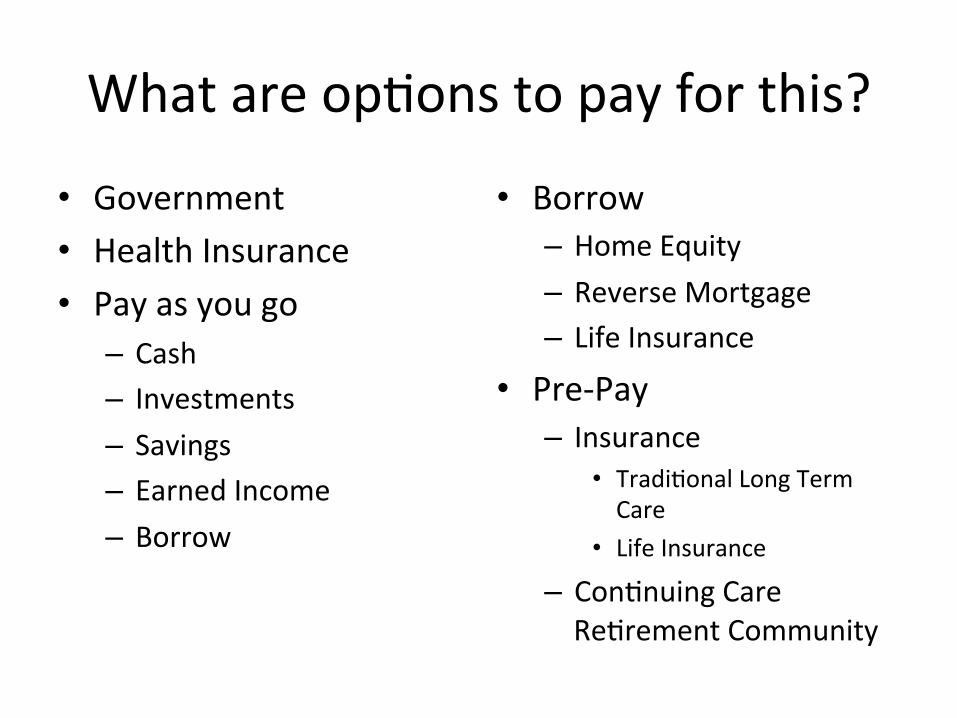

What are opEons to pay for this?

• Government • Health Insurance • Pay as you go

– Cash – Investments – Savings – Earned Income – Borrow

• Borrow – Home Equity – Reverse Mortgage – Life Insurance

• Pre-‐Pay – Insurance

• TradiEonal Long Term Care

• Life Insurance – ConEnuing Care ReErement Community

“I’ve paid my taxes…let the government pay for it!!!!!!”

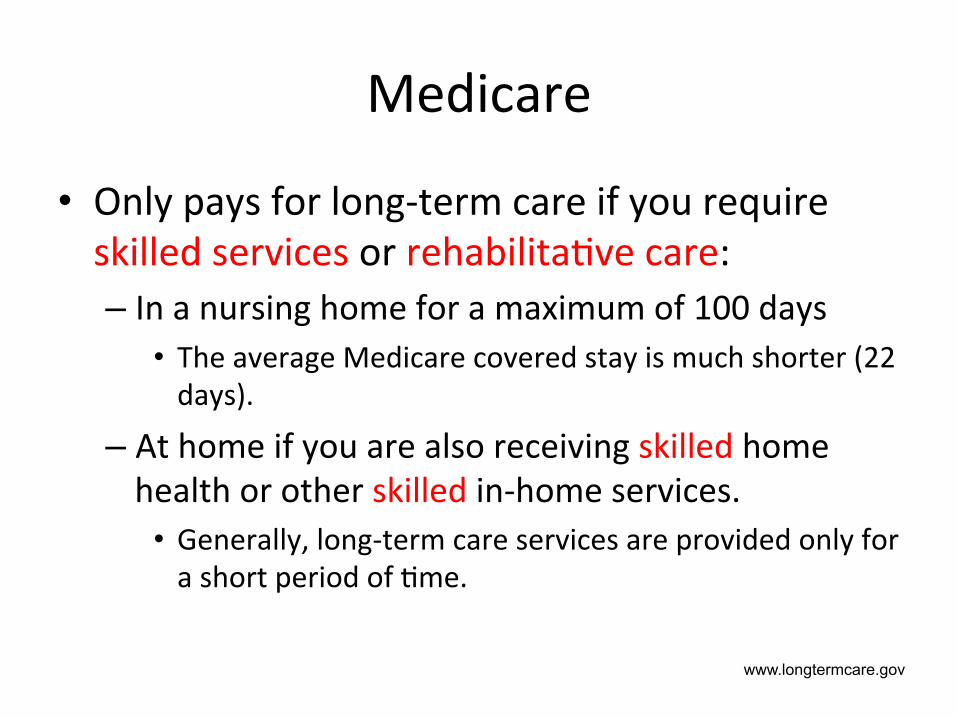

Medicare

• Only pays for long-‐term care if you require skilled services or rehabilitaEve care: – In a nursing home for a maximum of 100 days

• The average Medicare covered stay is much shorter (22 days).

– At home if you are also receiving skilled home health or other skilled in-‐home services.

• Generally, long-‐term care services are provided only for a short period of Eme.

www.longtermcare.gov

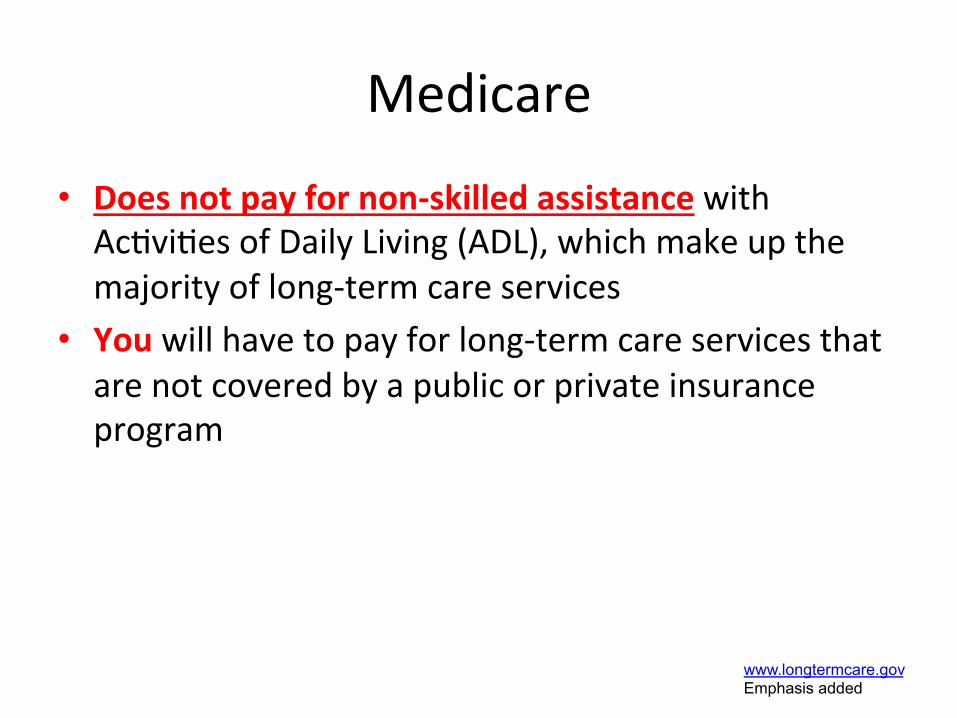

Medicare

• Does not pay for non-‐skilled assistance with AcEviEes of Daily Living (ADL), which make up the majority of long-‐term care services

• You will have to pay for long-‐term care services that are not covered by a public or private insurance program

www.longtermcare.gov Emphasis added

Medicare

• Very few nursing home stays are covered by Medicare.

• Medicare provides only limited coverage for long-‐term care related primarily to recuperaEng from a sickness or injury. Medicare pays only for skilled nursing care and medically necessary services. You should not rely on Medicare to pay for your long-‐term care needs.

State of Wisconsin “Guide to Long Term Care” (emphasis added)

Long-‐Term Care -‐-‐Medicare Supplements

• Medicare Supplement policies usually cover only co-‐pays and deducEbles for Medicare covered benefits and services

• Worth considering as a backup but not worth relying on

• More likely to cover Dr. and hospital expenses

Medicaid • Medicaid, also known as Medical Assistance or Title XIX, is a government health care program paid for by state and federal governments.

• To be eligible for Medicaid: – You must be 65 or over, or disabled, or in a family with dependent children; and

– You must have low income and few assets; or – You must be paying so much money for health care that you have very liole income lee.

• If you are eligible, Medicaid will pay for most health care costs, including nursing home and community-‐based care. State of Wisconsin

“Guide to Long Term Care” (emphasis added)

Long-‐Term Care -‐-‐Medicaid

• Medicaid is a “means-‐tested” program that provides coverage for those who fall below specified levels for: – Income – Assets

• In other words, you have to be poor. • Is this what you want to plan for?

Medicaid

• AddiEonal Issues… – Not all faciliEes accept Medicaid paEents – Limited or no control over which facility you can use

– May be placed far away from your home – Medicaid may recover a porEon of your estate aeer your death

– Your surviving spouse may have liole lee – Your surviving partner may have nothing lee

“I’m sEll working…what about my health insurance?”

Health Insurance

• Most employer-‐sponsored or private health insurance, including health insurance plans, cover only the same kinds of limited services as Medicare

• If they do cover long-‐term care, it is typically only for skilled, short-‐term, medically necessary care

• If you are disabled and have disability insurance, that can help with expenses

OK—what if I have to pay for this myself?

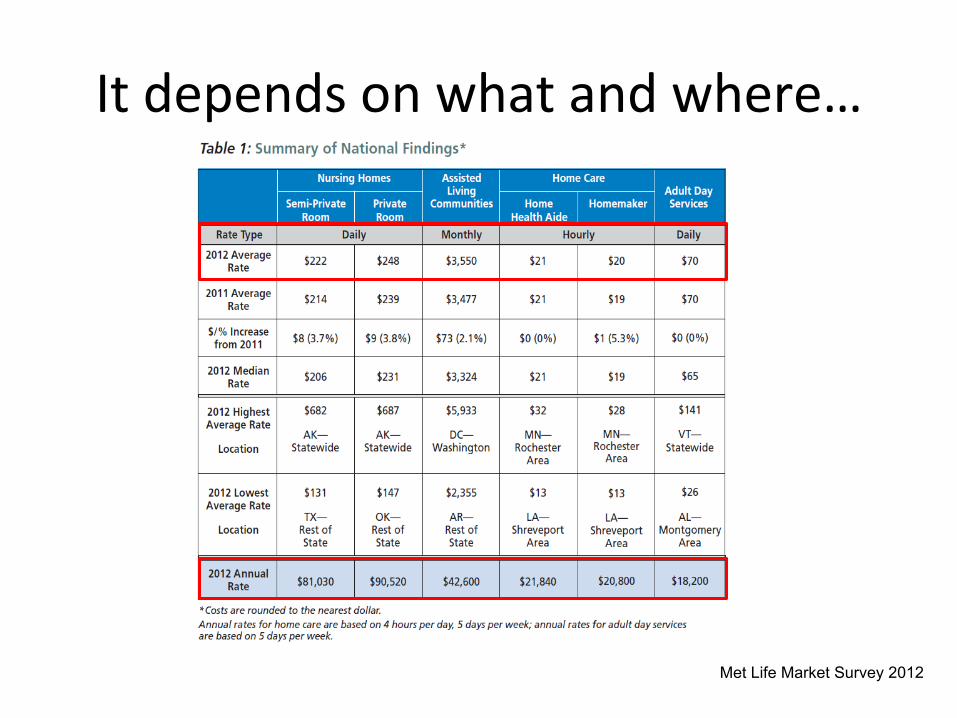

How expensive is it?

It depends on what and where…

Met Life Market Survey 2012

“Ok—what about Wisconsin?”

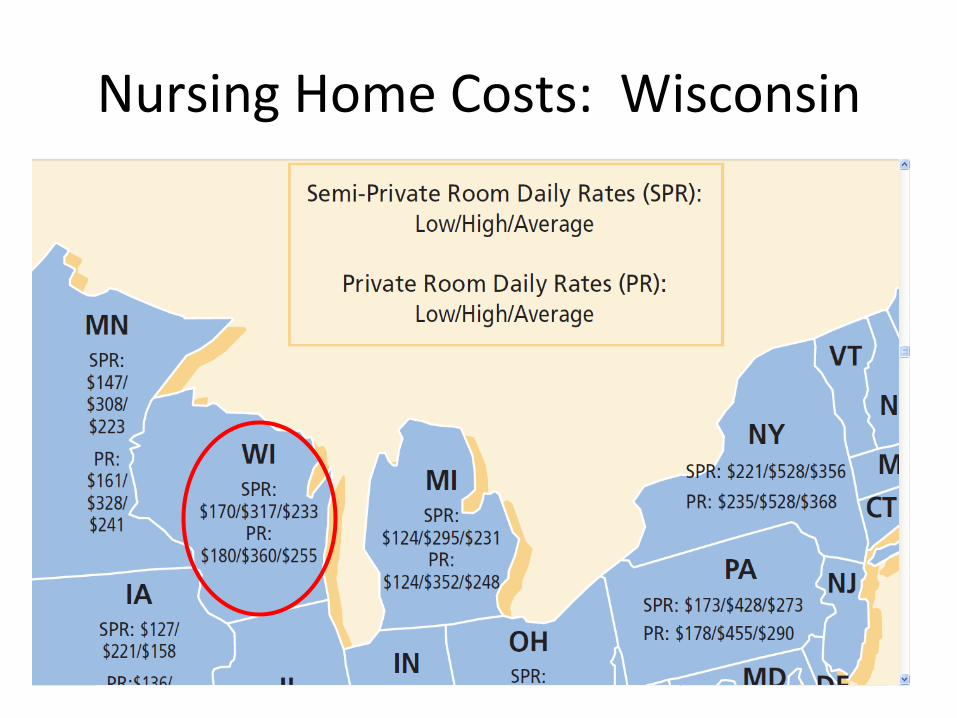

Nursing Home Costs: Wisconsin

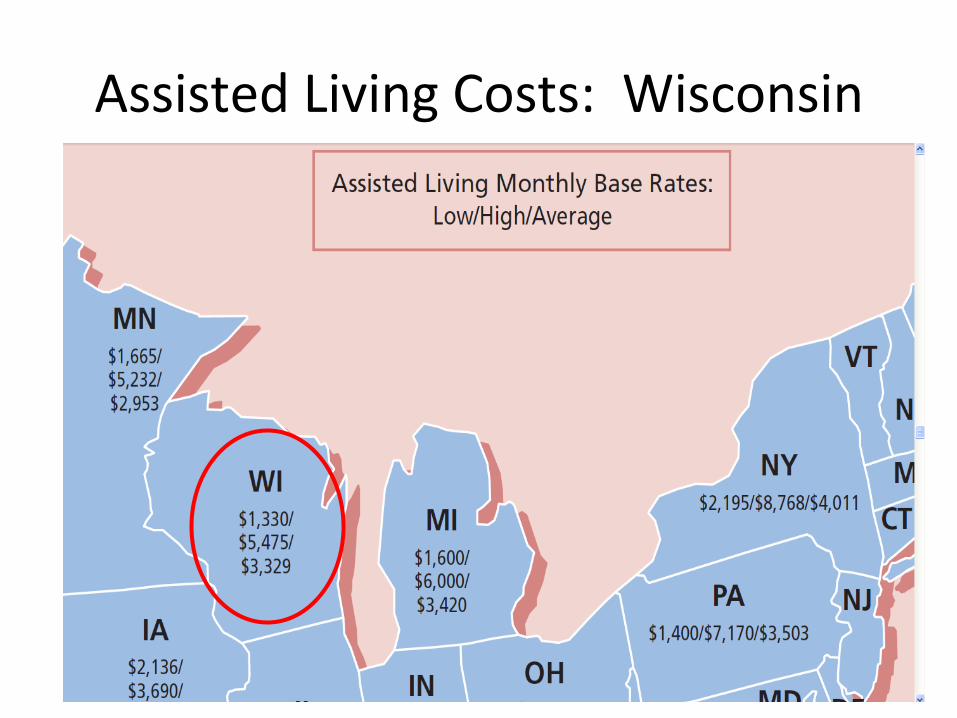

Assisted Living Costs: Wisconsin

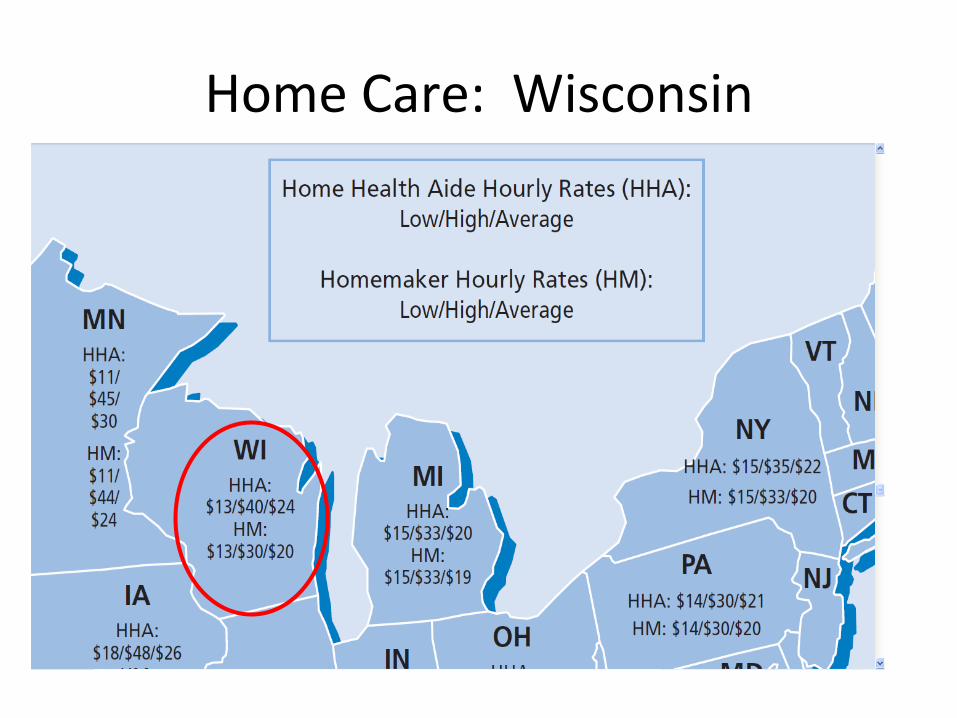

Home Care: Wisconsin

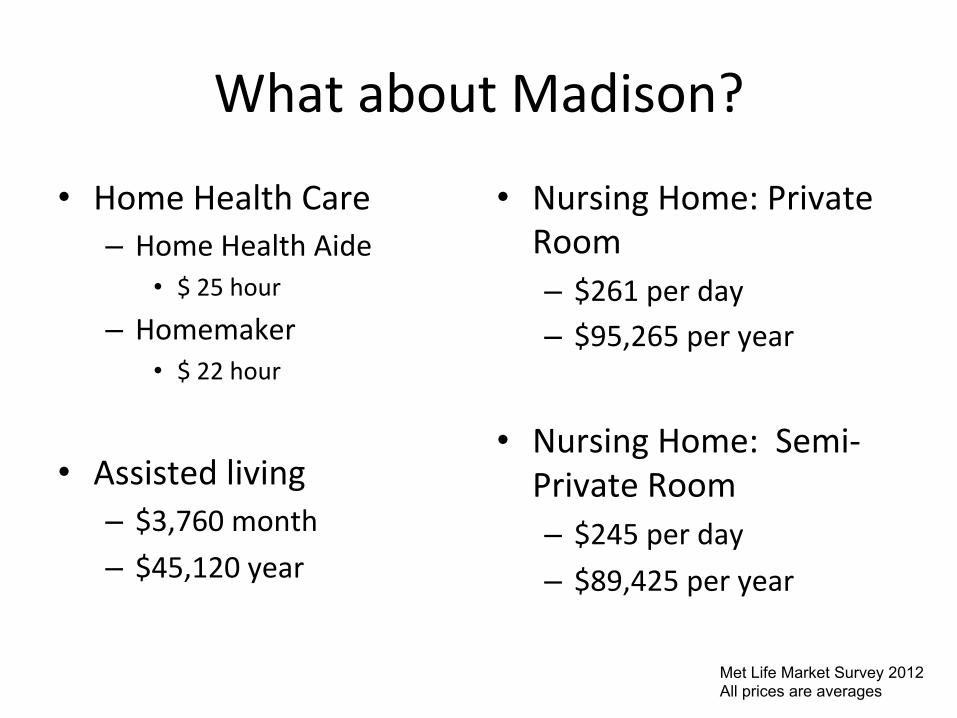

What about Madison?

• Home Health Care – Home Health Aide

• $ 25 hour – Homemaker

• $ 22 hour

• Assisted living – $3,760 month – $45,120 year

• Nursing Home: Private Room – $261 per day – $95,265 per year

• Nursing Home: Semi-‐Private Room – $245 per day – $89,425 per year

Met Life Market Survey 2012 All prices are averages

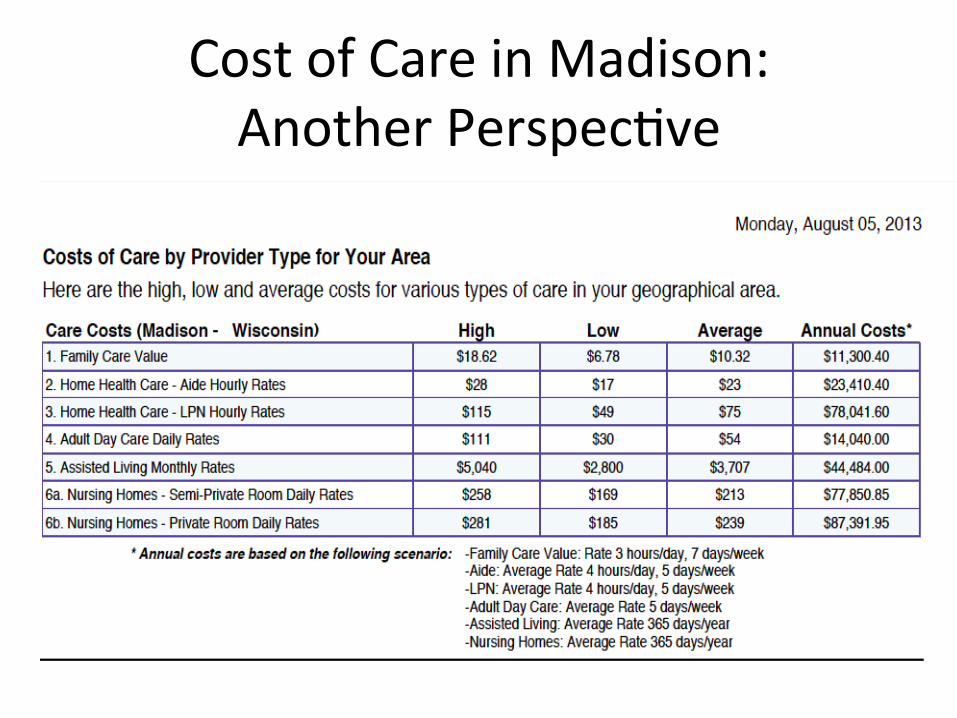

Cost of Care in Madison: Another PerspecEve

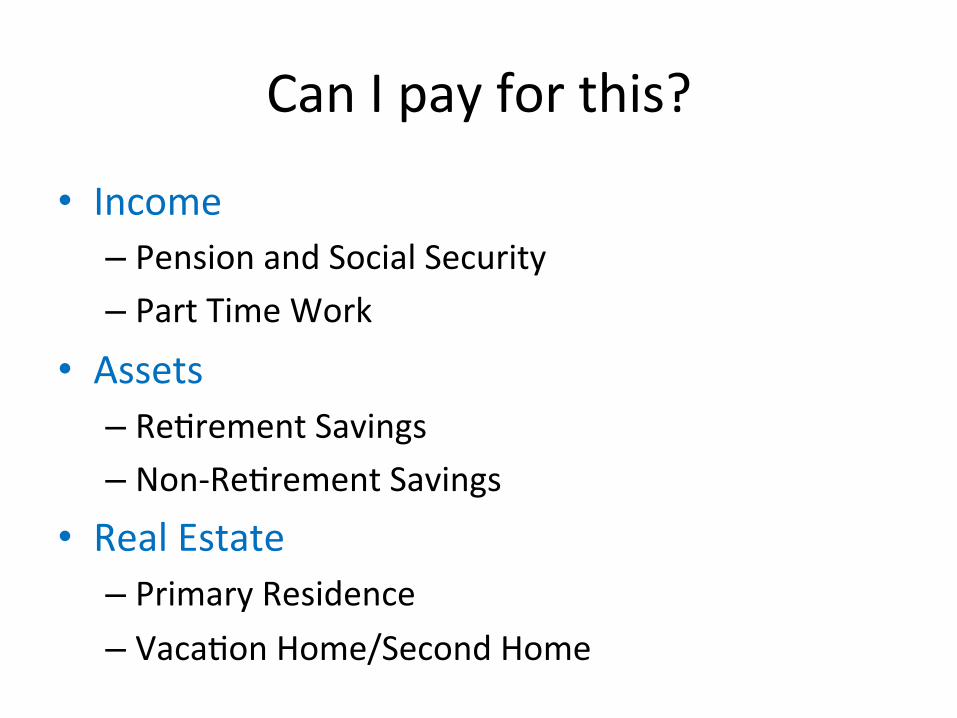

Can I pay for this?

• Income – Pension and Social Security – Part Time Work

• Assets – ReErement Savings – Non-‐ReErement Savings

• Real Estate – Primary Residence – VacaEon Home/Second Home

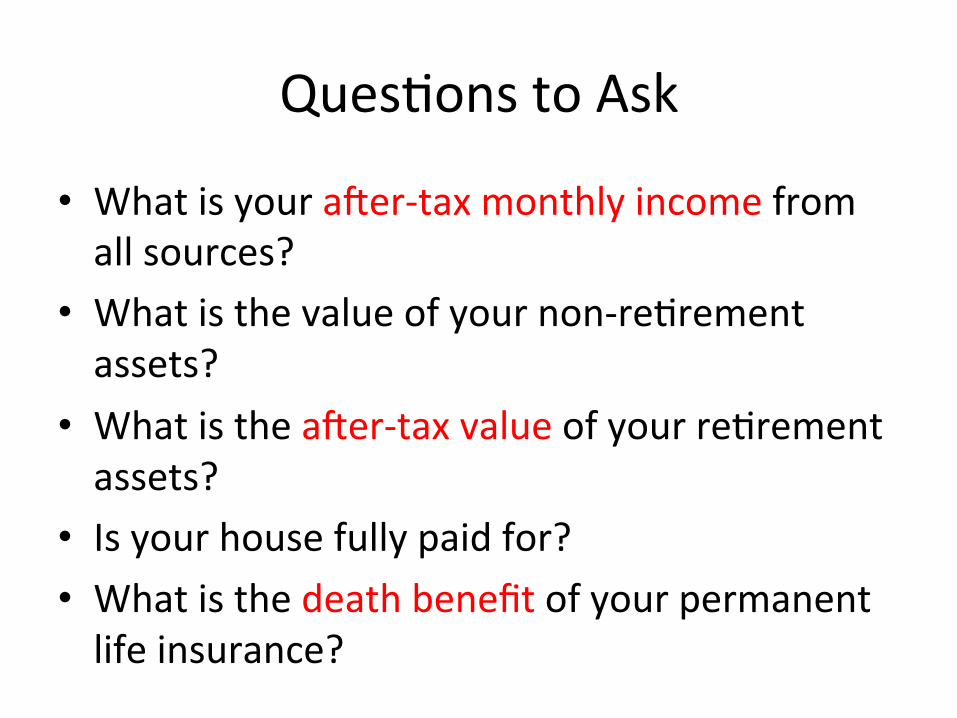

QuesEons to Ask

• What is your aeer-‐tax monthly income from all sources?

• What is the value of your non-‐reErement assets?

• What is the aeer-‐tax value of your reErement assets?

• Is your house fully paid for? • What is the death benefit of your permanent life insurance?

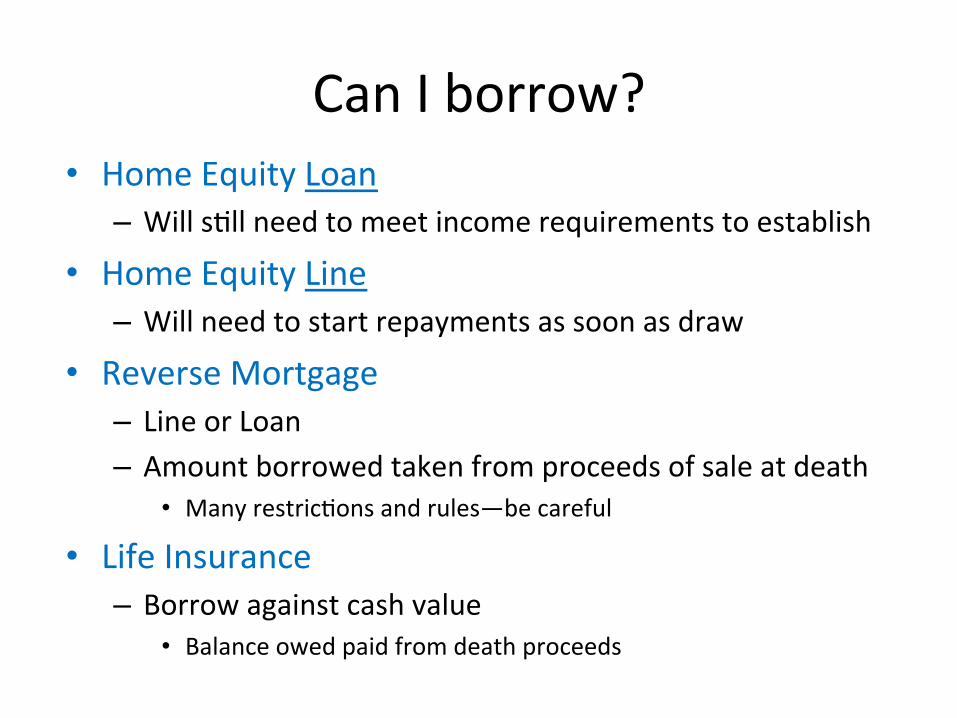

Can I borrow? • Home Equity Loan

– Will sEll need to meet income requirements to establish

• Home Equity Line – Will need to start repayments as soon as draw

• Reverse Mortgage – Line or Loan – Amount borrowed taken from proceeds of sale at death

• Many restricEons and rules—be careful

• Life Insurance – Borrow against cash value

• Balance owed paid from death proceeds

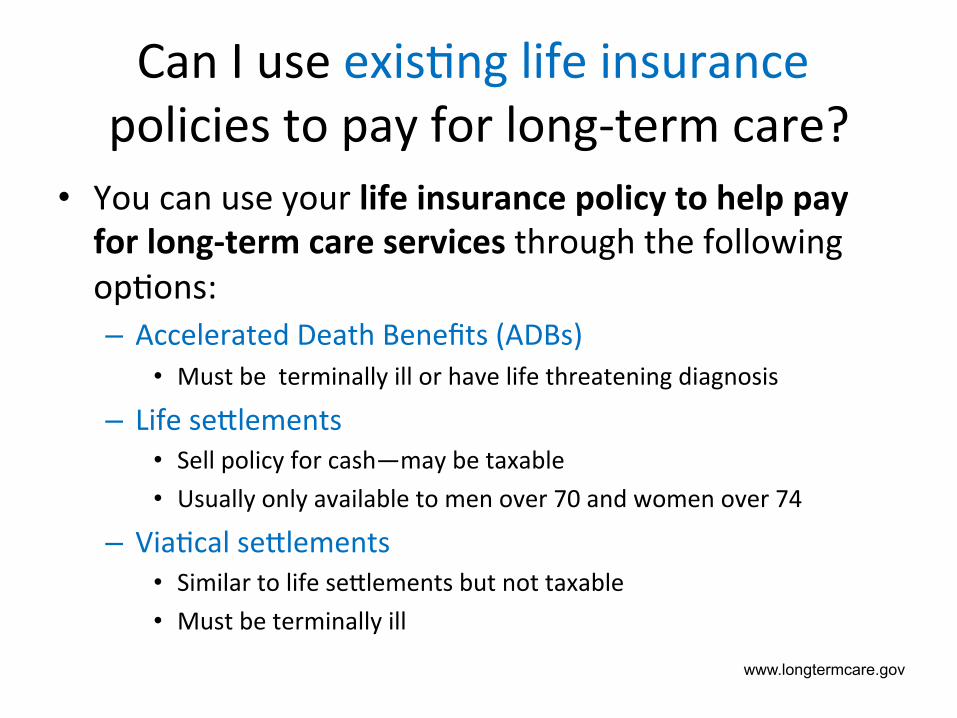

Can I use exisEng life insurance policies to pay for long-‐term care?

• You can use your life insurance policy to help pay for long-‐term care services through the following opEons: – Accelerated Death Benefits (ADBs)

• Must be terminally ill or have life threatening diagnosis

– Life seolements • Sell policy for cash—may be taxable • Usually only available to men over 70 and women over 74

– ViaEcal seolements • Similar to life seolements but not taxable • Must be terminally ill

www.longtermcare.gov

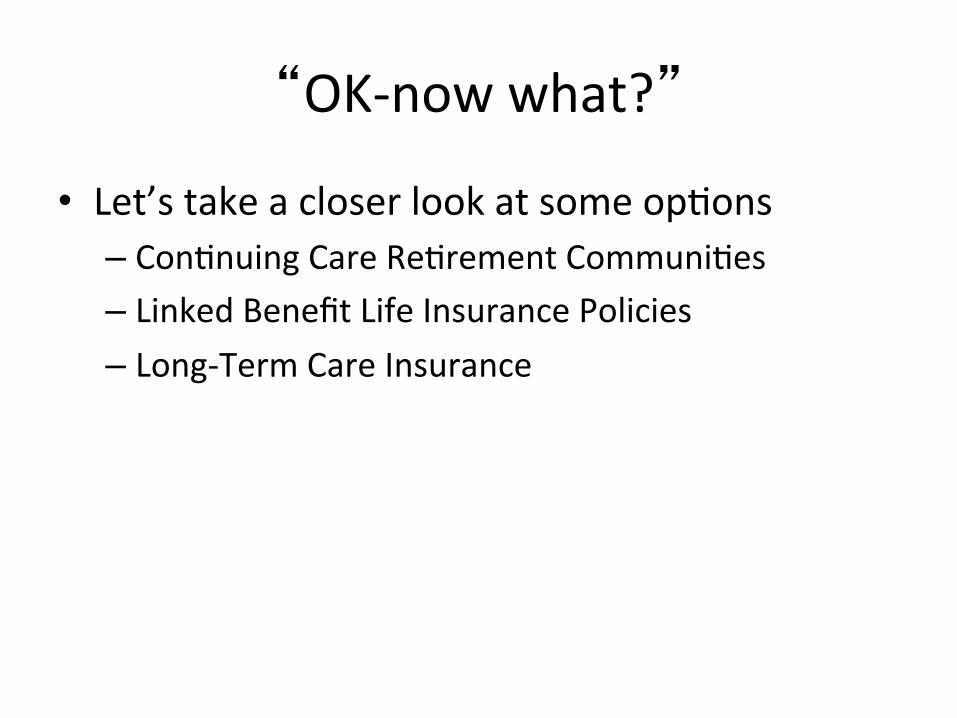

“OK-‐now what?”

• Let’s take a closer look at some opEons – ConEnuing Care ReErement CommuniEes – Linked Benefit Life Insurance Policies – Long-‐Term Care Insurance

Con#nuing Care Re#rement Communi#es

ConEnuing Care ResidenEal CommuniEes

• RelaEvely new form of long-‐term care for seniors

• Blend of independent living, assisted living, and nursing home care

• Can provide guarantee of lifeEme housing, social interacEon, and increased levels of care as needed

CCRC Living OpEons

• Living op#ons can include: – Independent apartments – Assisted living – Memory Care – Skilled Nursing Care

• Addi#onal services can be included as needed – Meals – Housekeeping – Laundry – Health and wellness – Social and RecreaEonal AcEviEes

– TransportaEon – MedicaEon monitoring

Paying for CCRCs • Most require an upfront payment as well as monthly charges depending on services

• Can ‘pre-‐pay’ for lifeEme care but fees may range from $100,000 to $1,000,000 or more

• Contract opEons can include: – Life care or extended care: pre-‐pay for unlimited care as needed

– Modified care contract: pre-‐pay for specified period of Eme and then renew as needed

– Fee-‐for-‐Service: Pay as you go

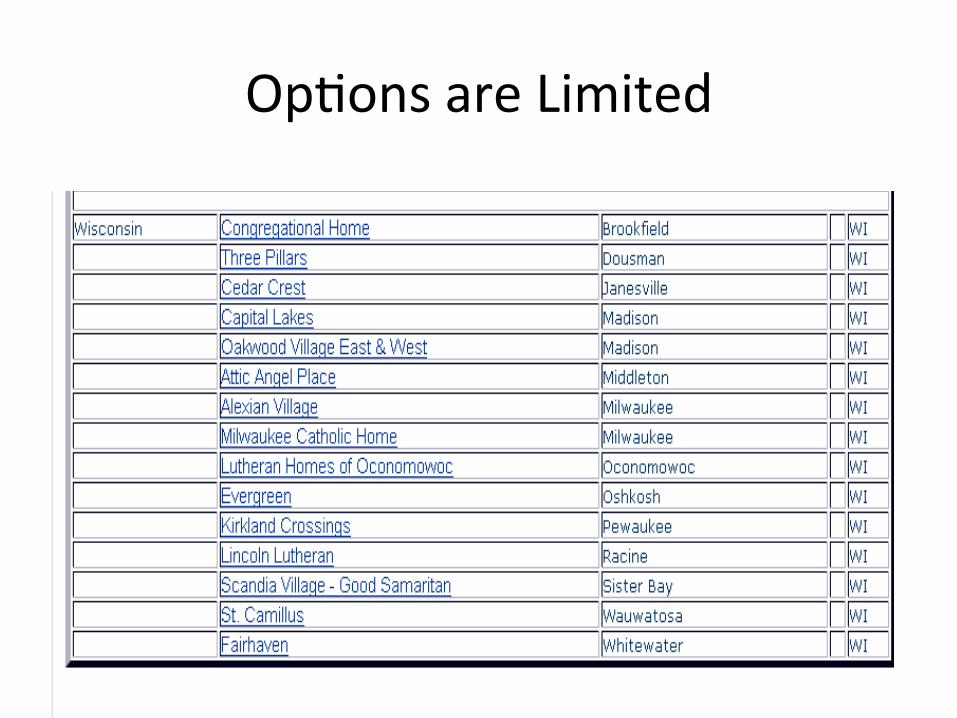

OpEons are Limited

Capitol Lakes

Oakwood Village

Asc Angel Place

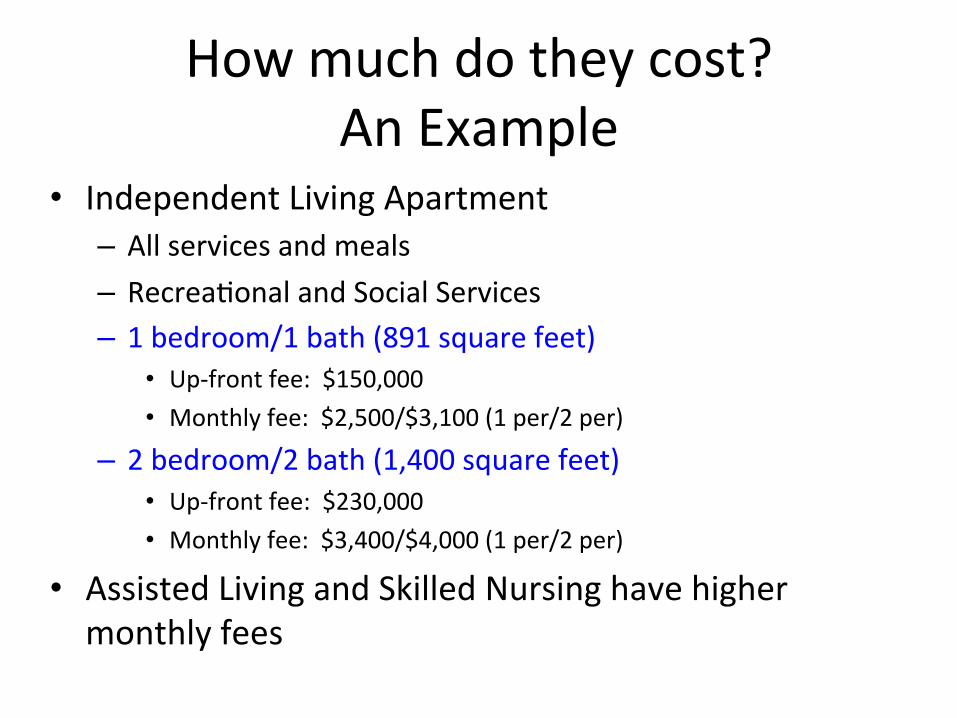

How much do they cost? An Example

• Independent Living Apartment – All services and meals – RecreaEonal and Social Services – 1 bedroom/1 bath (891 square feet)

• Up-‐front fee: $150,000 • Monthly fee: $2,500/$3,100 (1 per/2 per)

– 2 bedroom/2 bath (1,400 square feet) • Up-‐front fee: $230,000 • Monthly fee: $3,400/$4,000 (1 per/2 per)

• Assisted Living and Skilled Nursing have higher monthly fees

CCRCs—Are they for you?

• Like most things….it depends • How important is it for you to have some guarantees of coverage?

• Can you afford the upfront fee? • What are your feelings about a legacy? • Will your family understand “giving away” assets to pay for? – Will you?

“Linked Benefit Life Insurance”

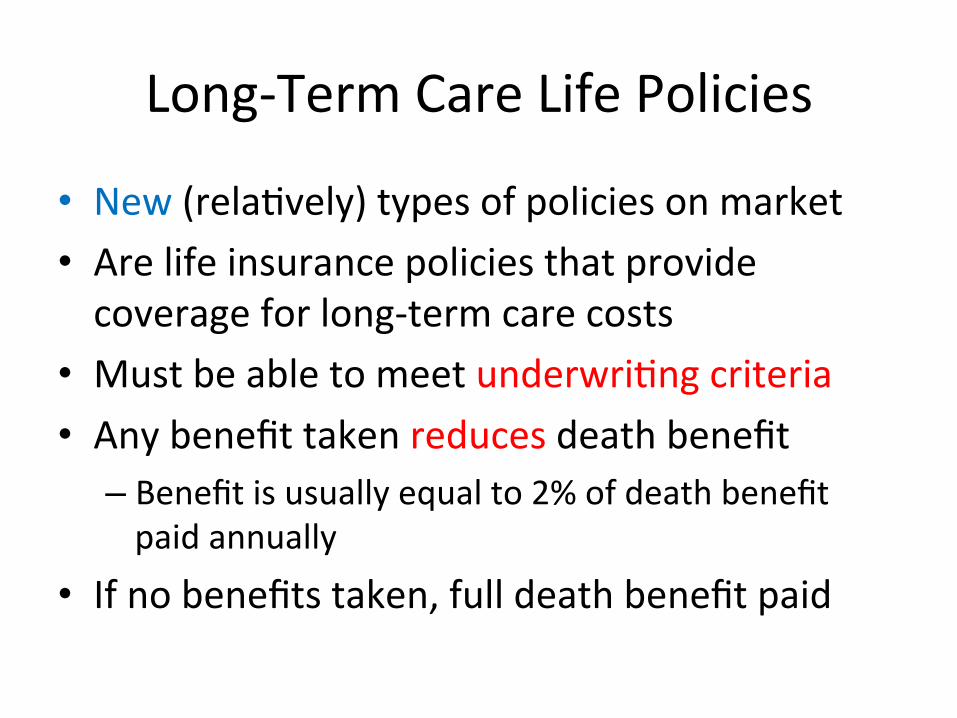

Long-‐Term Care Life Policies

• New (relaEvely) types of policies on market • Are life insurance policies that provide coverage for long-‐term care costs

• Must be able to meet underwriEng criteria • Any benefit taken reduces death benefit

– Benefit is usually equal to 2% of death benefit paid annually

• If no benefits taken, full death benefit paid

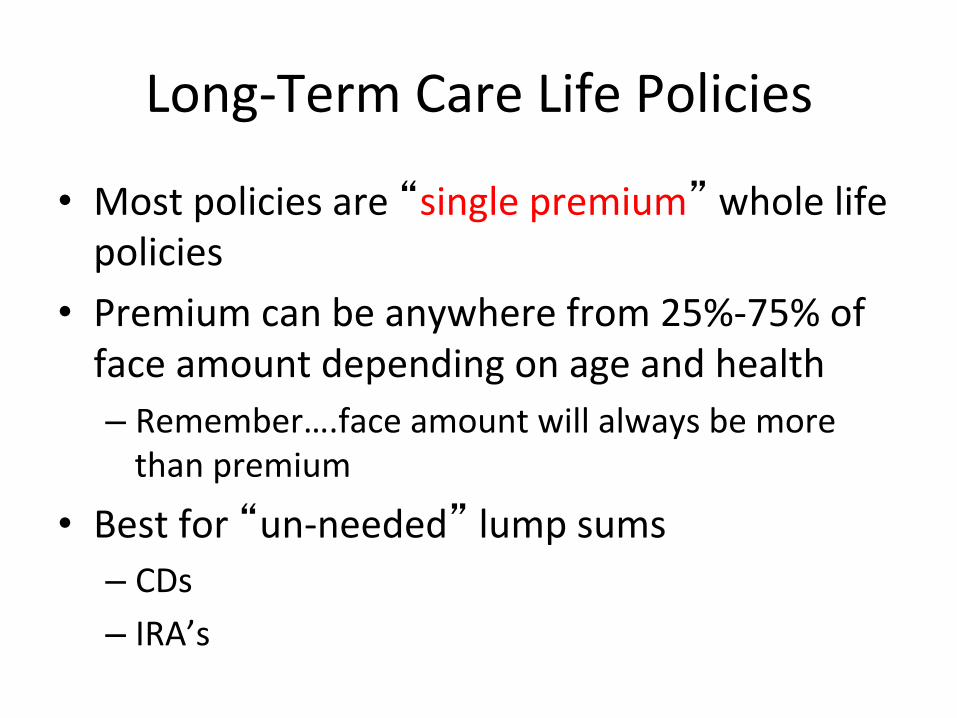

Long-‐Term Care Life Policies

• Most policies are “single premium” whole life policies

• Premium can be anywhere from 25%-‐75% of face amount depending on age and health – Remember….face amount will always be more than premium

• Best for “un-‐needed” lump sums – CDs – IRA’s

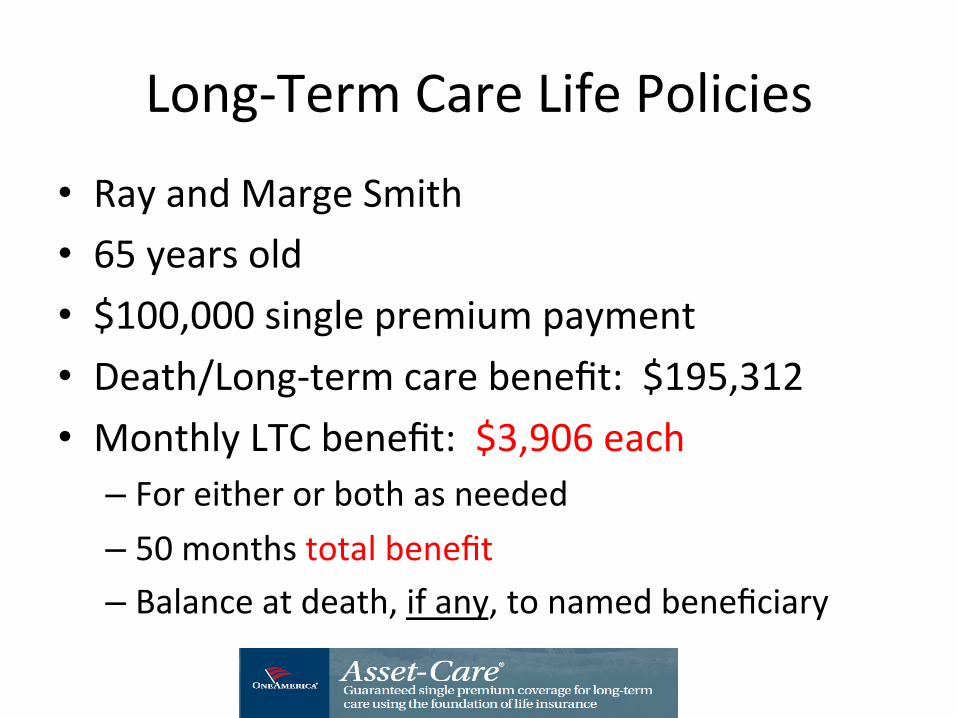

Long-‐Term Care Life Policies

• Ray and Marge Smith • 65 years old • $100,000 single premium payment • Death/Long-‐term care benefit: $195,312 • Monthly LTC benefit: $3,906 each

– For either or both as needed – 50 months total benefit – Balance at death, if any, to named beneficiary

Long Term Care Insurance

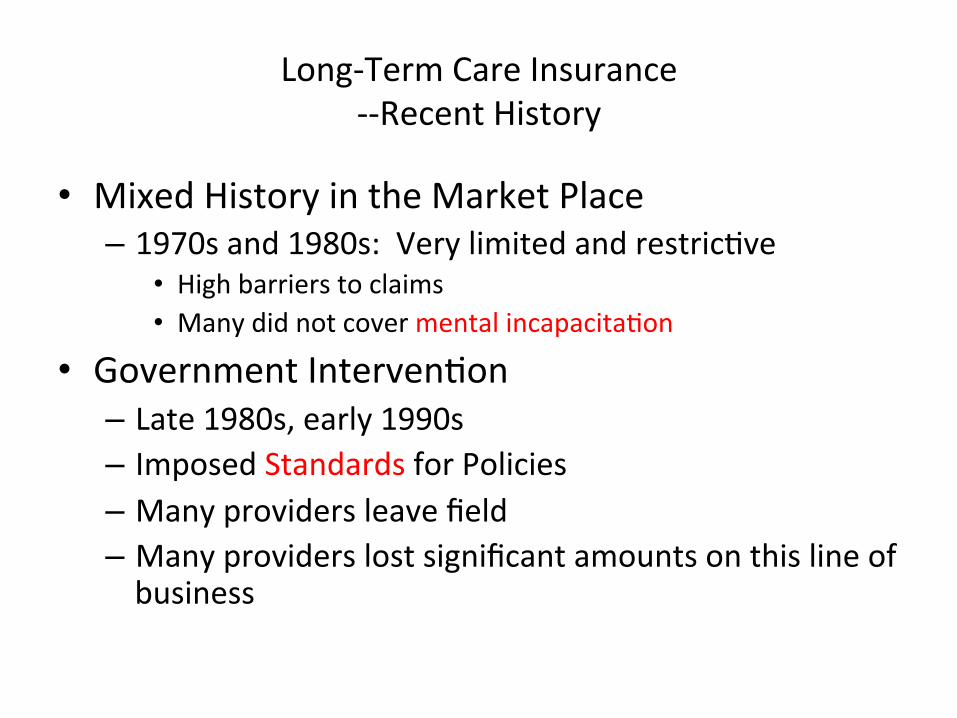

Long-‐Term Care Insurance -‐-‐Recent History

• Mixed History in the Market Place – 1970s and 1980s: Very limited and restricEve

• High barriers to claims • Many did not cover mental incapacitaEon

• Government IntervenEon – Late 1980s, early 1990s – Imposed Standards for Policies – Many providers leave field – Many providers lost significant amounts on this line of business

Long-‐Term Care Insurance -‐-‐Current SituaEon

• Many Providers Returning to the LTC Marketplace

• Generally beoer policies – More responsive to consumer needs – More adherence to government rules – Beoer underwriEng – Beoer understanding of costs and long-‐term reserve needs

Long Term Care Insurance: Current SituaEon

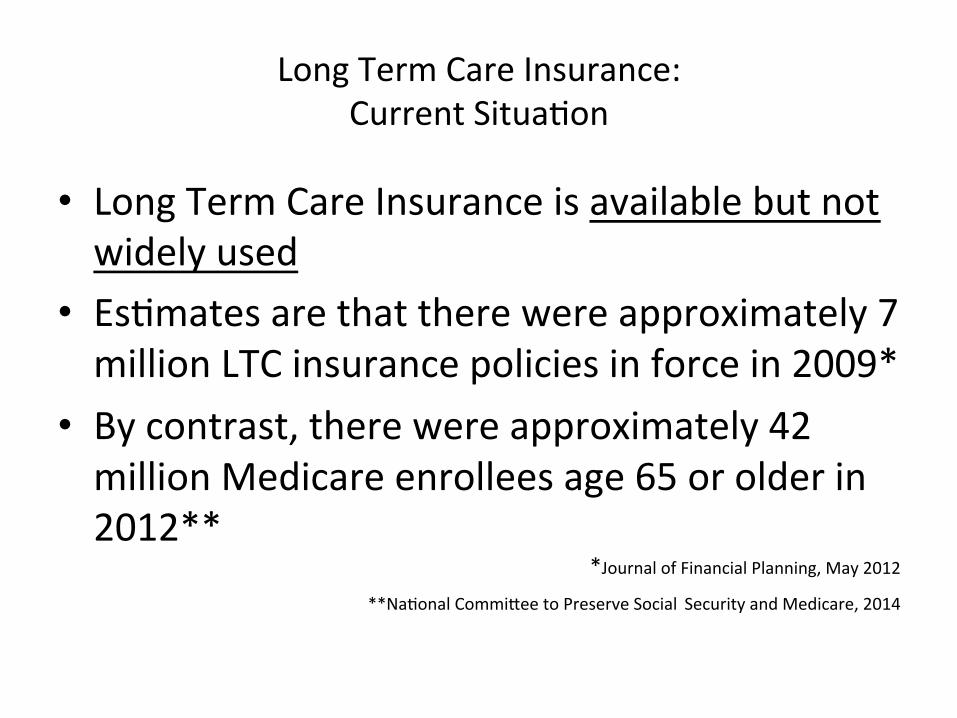

• Long Term Care Insurance is available but not widely used

• EsEmates are that there were approximately 7 million LTC insurance policies in force in 2009*

• By contrast, there were approximately 42 million Medicare enrollees age 65 or older in 2012**

*Journal of Financial Planning, May 2012

**NaEonal Commioee to Preserve Social Security and Medicare, 2014

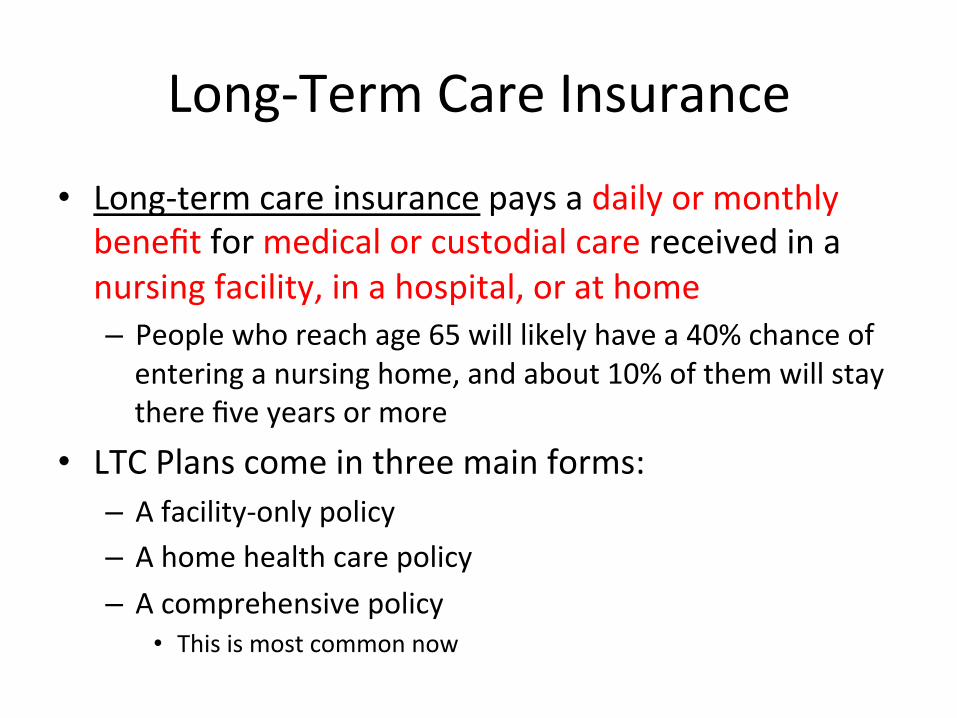

Long-‐Term Care Insurance

• Long-‐term care insurance pays a daily or monthly benefit for medical or custodial care received in a nursing facility, in a hospital, or at home – People who reach age 65 will likely have a 40% chance of entering a nursing home, and about 10% of them will stay there five years or more

• LTC Plans come in three main forms: – A facility-‐only policy – A home health care policy – A comprehensive policy

• This is most common now

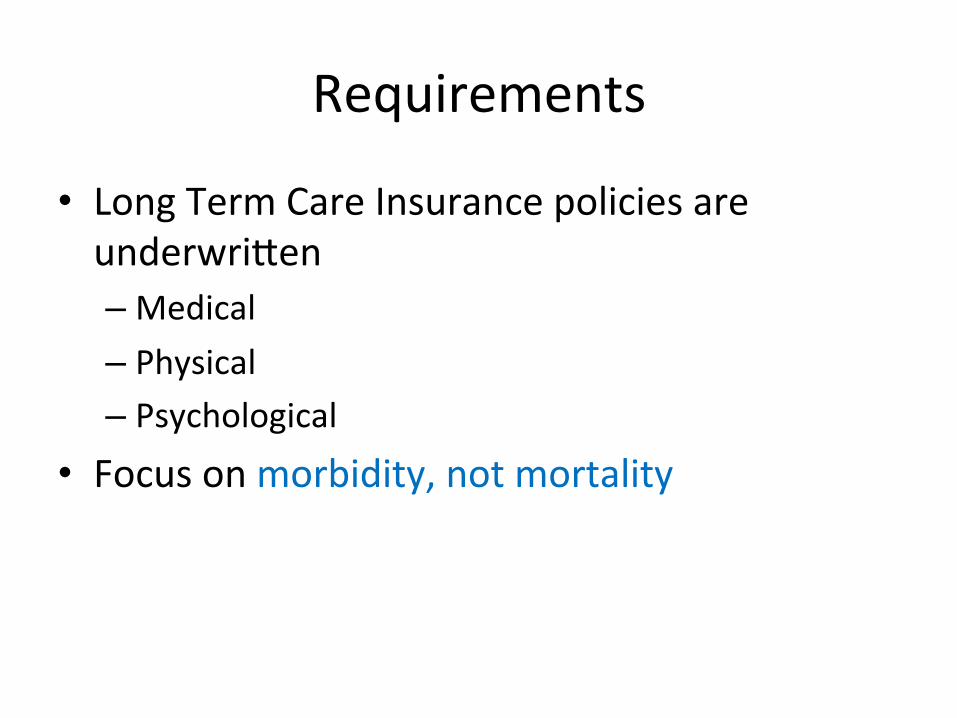

Requirements

• Long Term Care Insurance policies are underwrioen – Medical – Physical – Psychological

• Focus on morbidity, not mortality

Long-‐Term Care Insurance -‐-‐UnderwriEng

• Long Term Care Insurance is not like life insurance – Life Underwriters Worry about Mortality

• Things which are likely to kill you – Long-‐Term Care Underwriters Worry about Morbidity

• Things which are likely to make you sick, disabled, or leave you in need of assistance

Long-‐Term Care Insurance

• Common features of LTC policies include: – Daily benefits range from $50 -‐ $300 or more – Most policies are reimbursement policies, which reimburse for actual charges up to a daily limit

• Some policies reimburse on a per diem basis

– Many insurers offer policies with pooled benefits, which provide a total dollar amount that can be used to pay for the different types of long-‐term care services

Long-‐Term Care Insurance: Common Features

• An eliminaEon period is a waiEng period during which Eme benefits are not paid aeer meeEng qualificaEons – 0/30/60/90/100/180/360 days – Basically Self Insurance for Daily Rate for Specified Period of Time-‐-‐”DeducEble”

• i.e. 180 days x $125 daily benefit = $22,550 of benefit not received

Long-‐Term Care Insurance -‐-‐Common Features (cont)

• Benefit Period – 360/720/1240 etc. days of coverage

• Usually creates a pool of benefit – i.e. 720 days x $135 day = $97,200 benefits

– Unlimited • InflaEon ProtecEon

– None/Simple/Compound • Unlike DI, Usually Starts Right Away

– Be Prepared to JusEfy an ElecEon of “None”

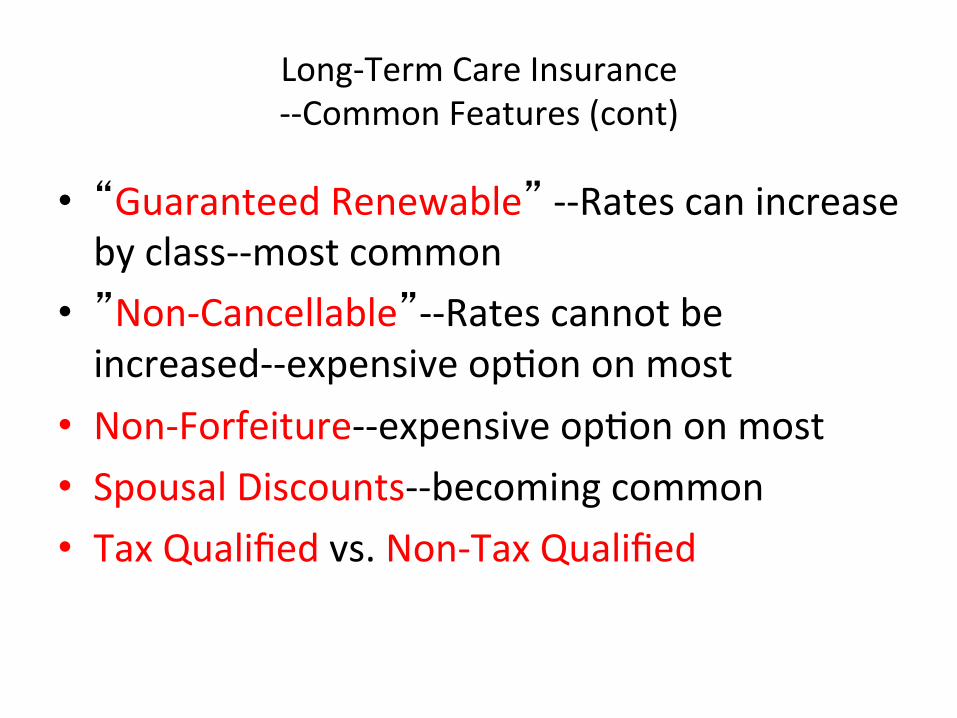

Long-‐Term Care Insurance -‐-‐Common Features (cont)

• “Guaranteed Renewable” -‐-‐Rates can increase by class-‐-‐most common

• ”Non-‐Cancellable”-‐-‐Rates cannot be increased-‐-‐expensive opEon on most

• Non-‐Forfeiture-‐-‐expensive opEon on most • Spousal Discounts-‐-‐becoming common • Tax Qualified vs. Non-‐Tax Qualified

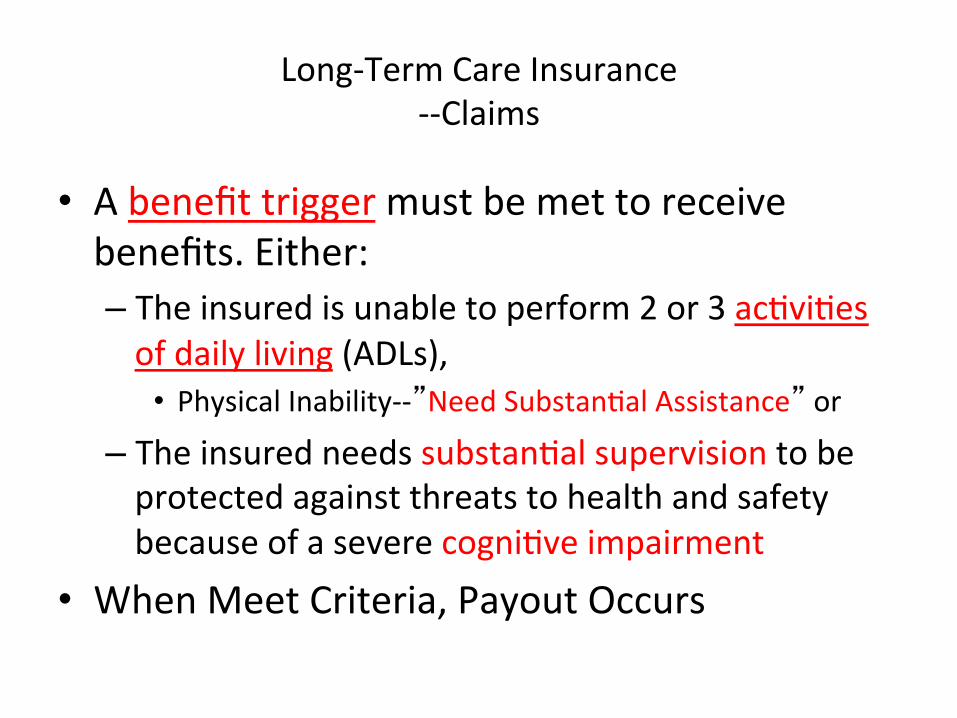

Long-‐Term Care Insurance -‐-‐Claims

• A benefit trigger must be met to receive benefits. Either: – The insured is unable to perform 2 or 3 acEviEes of daily living (ADLs),

• Physical Inability-‐-‐”Need SubstanEal Assistance” or – The insured needs substanEal supervision to be protected against threats to health and safety because of a severe cogniEve impairment

• When Meet Criteria, Payout Occurs

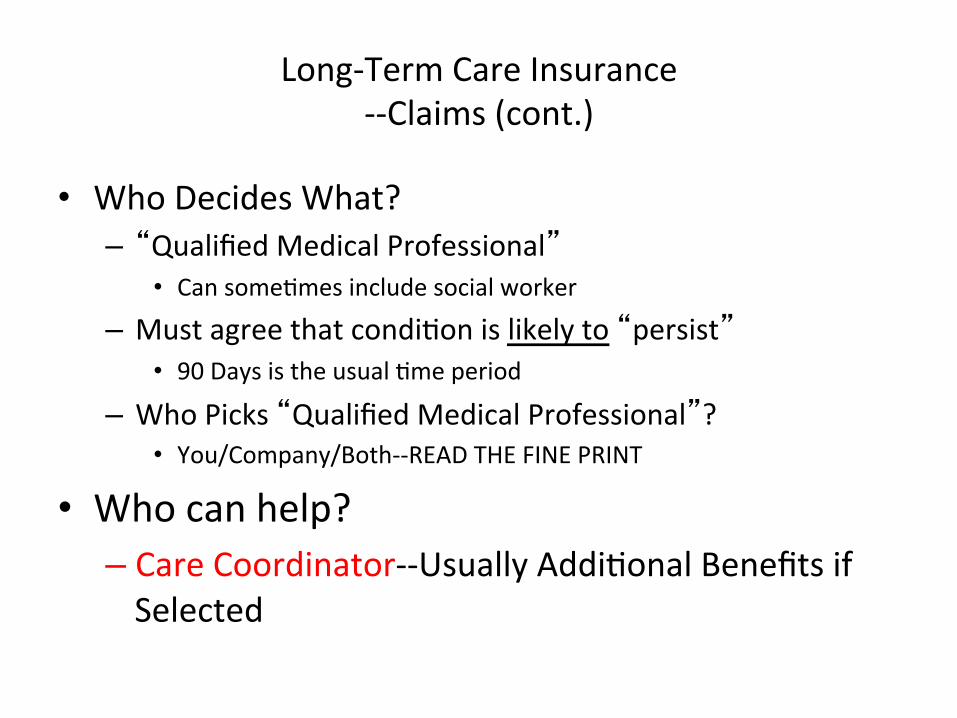

Long-‐Term Care Insurance -‐-‐Claims (cont.)

• Who Decides What? – “Qualified Medical Professional”

• Can someEmes include social worker

– Must agree that condiEon is likely to “persist” • 90 Days is the usual Eme period

– Who Picks “Qualified Medical Professional”? • You/Company/Both-‐-‐READ THE FINE PRINT

• Who can help? – Care Coordinator-‐-‐Usually AddiEonal Benefits if Selected

Long Term Care Insurance

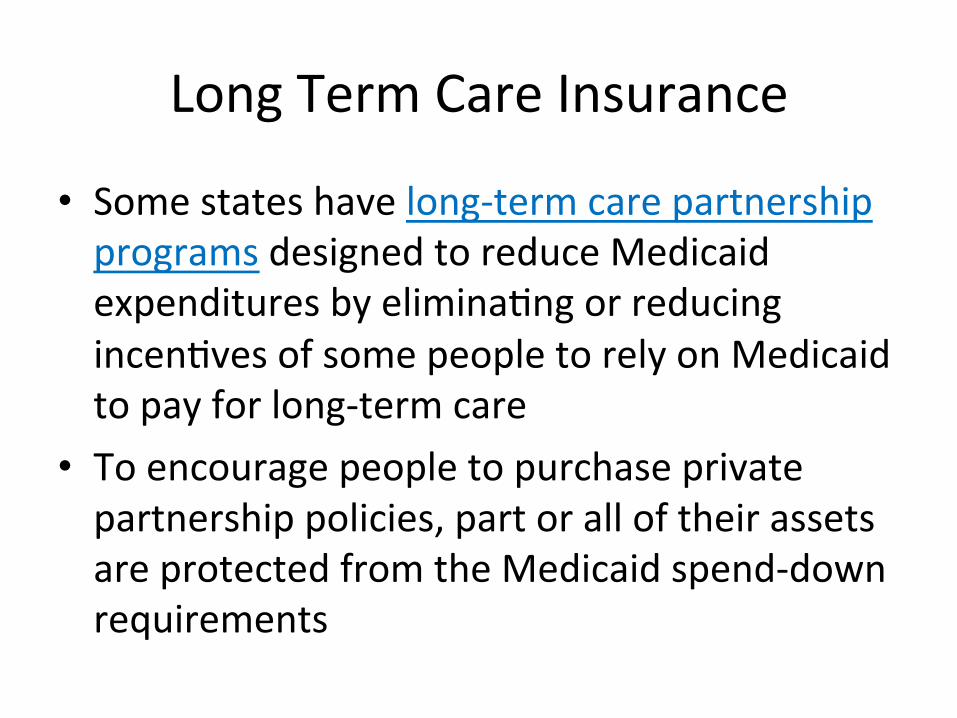

• Some states have long-‐term care partnership programs designed to reduce Medicaid expenditures by eliminaEng or reducing incenEves of some people to rely on Medicaid to pay for long-‐term care

• To encourage people to purchase private partnership policies, part or all of their assets are protected from the Medicaid spend-‐down requirements

What about ETF endorsed programs?

What about ETF endorsed programs?

AddiEonal Benefits to Consider

• Unused sick leave credits can be used to pay premiums

• Can convert Basic Group Life insurance coverage to pay for premiums

• Contact Employee Trust Funds for addiEonal informaEon

How should I think about Long Term Care Insurance?

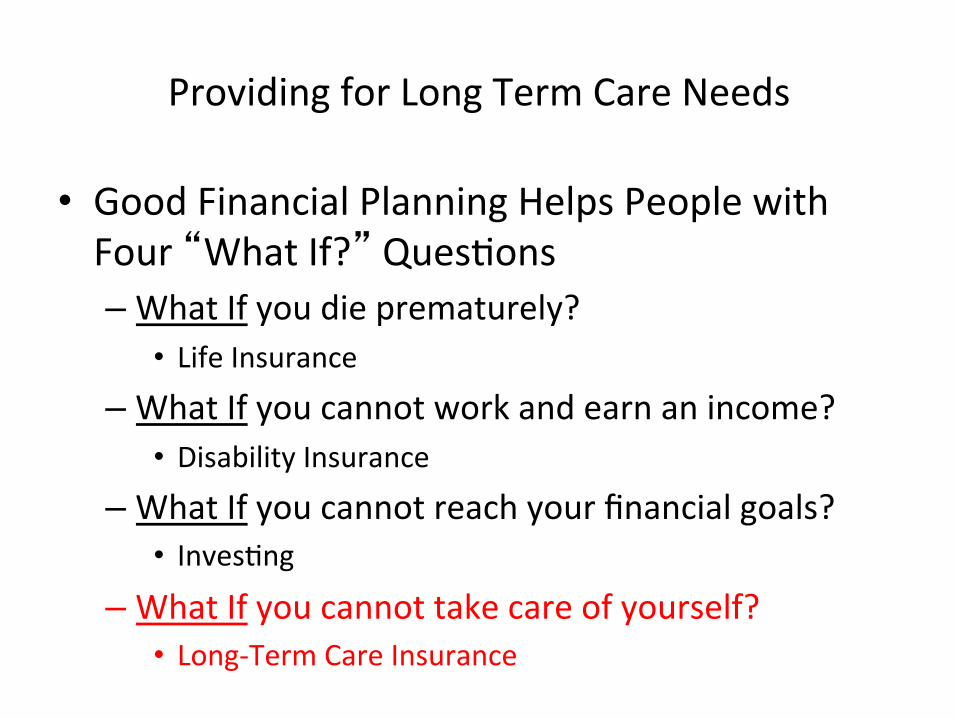

Providing for Long Term Care Needs

• Good Financial Planning Helps People with Four “What If?” QuesEons – What If you die prematurely?

• Life Insurance – What If you cannot work and earn an income?

• Disability Insurance – What If you cannot reach your financial goals?

• InvesEng – What If you cannot take care of yourself?

• Long-‐Term Care Insurance

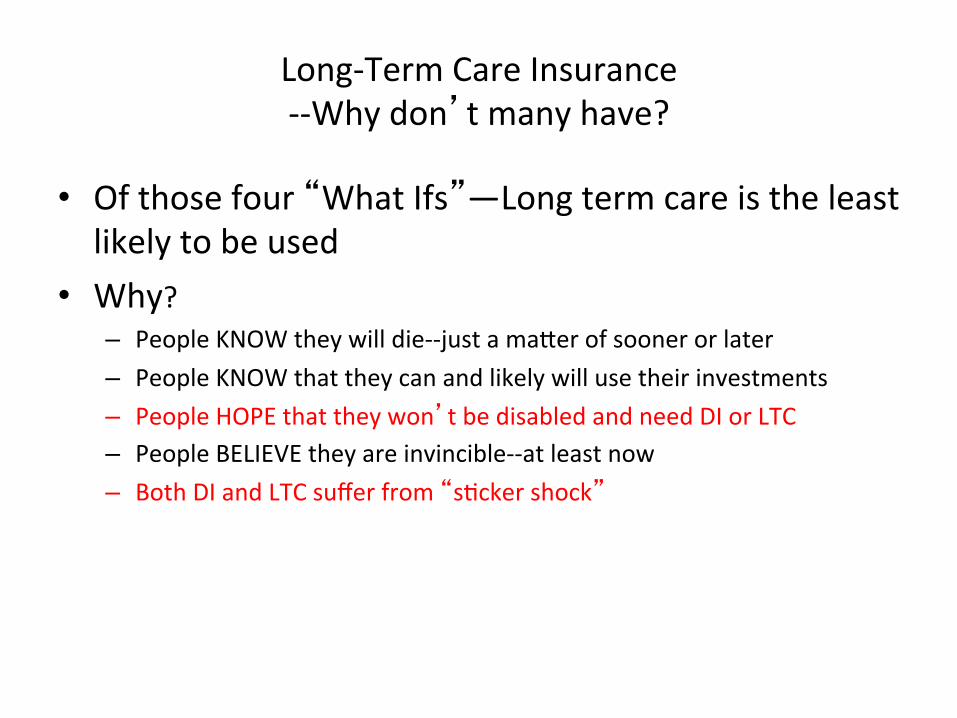

Long-‐Term Care Insurance -‐-‐Why don’t many have?

• Of those four “What Ifs”—Long term care is the least likely to be used

• Why? – People KNOW they will die-‐-‐just a maoer of sooner or later – People KNOW that they can and likely will use their investments – People HOPE that they won’t be disabled and need DI or LTC – People BELIEVE they are invincible-‐-‐at least now – Both DI and LTC suffer from “sEcker shock”

Long-‐Term Care Insurance -‐-‐Why Consider It?

• Preserve Independence, both financial and emoEonal

• Preserve/protect assets – For yourselves and for your heirs

• Avoid emoEonal, physical, and financial burdens on family-‐-‐spouse, children, grandchildren

• Avoid becoming financial liability • Assure that you can get good quality care

– Despite legal protecEons, Medicare/Medicaid paEents do not always get the best care or choices

Long-‐Term Care Insurance -‐-‐Obstacles

• Why Don’t People Buy? – ”I Don’t Need It” – “I’ll Get it Later” – ”It is Too Expensive” – ”Medicare Covers Me” – ”We’d Have Enough to Cover It” – “What If I Die and Don’t Use It?”

Long-‐Term Care Insurance -‐-‐Obstacles

• ”I Don’t Need It” – Review your assets and decide if you feel comfortable paying out a significant porEon to a nursing home or other providers-‐-‐review odds of needing care

– Do you have any plans for passing along assets? • Do you want to protect your inheritance plans?

• “I’ll Get it Later” – Like all age-‐based policies, it gets more expensive as you wait

– As you get older, the odds of something happening to affect your ability to qualify increase

Long-‐Term Care Insurance -‐-‐Obstacles

• ”It’s Too Expensive” – Compared to what? – Consider costs paid-‐in versus potenEal payout – Maybe it makes sense as “asset insurance” or “inheritance protecEon”

– Are mulEple coverage opEons

• “Medicare Covers Me” – Yes-‐but as we have discussed, only in very limited circumstances

Long-‐Term Care Insurance -‐-‐Obstacles

• “We’d Have Enough To Cover It” – Can one afford to self-‐insure? – Does it make sense to self-‐insure? – How many can afford to write a check for $100,000 or more?

– You may have enough to cover the cost-‐-‐but is that really how you want to spend that money?

• “What if I Die and Never Use This Insurance?” – Think about that for a minute….

When to buy? • If you buy a policy at age 75, the premium will generally be

two and a half Emes greater than if you had bought the policy at age 65.

• It will be six Emes higher than if you bought at age 55. • If you buy a policy with a large daily benefit or a longer

benefit period, it will also cost you more. • InflaEon protecEon can add 25% to 40% to the premium. • Nonforfeiture benefits can add 10% to 100% to the premium.

• NAIC Shoppers Guide

OK—that was a lot to digest…let’s wrap things up!

Review

• The potenEal costs of long term care are significant

• The odds of needing care are high…but whether you will need it is unknown

• There are many opEons to pay for this care…but none are aoracEve

• The choice of which opEon to select depends on your individual situaEon

QuesEons?

Thank-‐you!

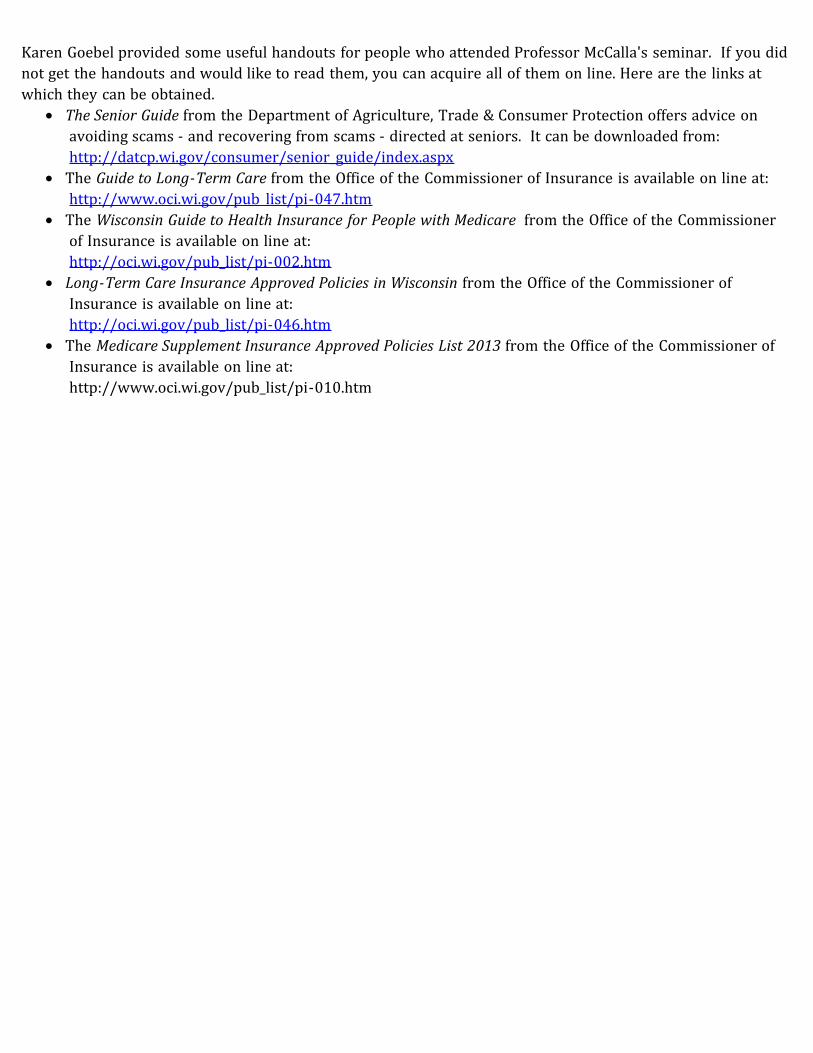

Karen Goebel provided some useful handouts for people who attended Professor McCalla's seminar. If you didnot get the handouts and would like to read them, you can acquire all of them on line. Here are the links atwhich they can be obtained.

· The Senior Guide from the Department of Agriculture, Trade & Consumer Protection offers advice onavoiding scams - and recovering from scams - directed at seniors. It can be downloaded from:http://datcp.wi.gov/consumer/senior_guide/index.aspx

· The Guide to Long-Term Care from the Office of the Commissioner of Insurance is available on line at:http://www.oci.wi.gov/pub_list/pi-047.htm

· The Wisconsin Guide to Health Insurance for People with Medicare from the Office of the Commissionerof Insurance is available on line at:http://oci.wi.gov/pub_list/pi-002.htm

· Long-Term Care Insurance Approved Policies in Wisconsin from the Office of the Commissioner ofInsurance is available on line at:http://oci.wi.gov/pub_list/pi-046.htm

· The Medicare Supplement Insurance Approved Policies List 2013 from the Office of the Commissioner ofInsurance is available on line at:http://www.oci.wi.gov/pub_list/pi-010.htm