Embed Size (px)

Citation preview

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 1/41

AdEx 2009European onlineadvertisingexpenditure

Published September 2010

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 2/41

Introduction 3About this report 4

Executive summary 5

Europe and the US 6

23 European markets in perspective 7

Europe retrospective 8

Update on ‘10 before 10’ 10

Search top of the formats in 2009 11

Search 12

Classifieds 15

Display 17

Regional and country detail

Western Europe 20

Central and Eastern Europe 23

Forecasting the European advertising market in 2009-2010 25

2010-2011 Forecast 25

Online TV advertising 27

Mobile advertising 29

Top 10 properties December 2009 30

Top 10 ad publisher sites by ad impressions 32

Internet penetration in Europe 34

Appendix i – Definition of formats 36

Appendix ii – Participating IABs 37

Appendix iii – Methodology and adjusted data 38

Appendix iv – Estimates and adjustments 39

Appendix v – Our research partners 40Special thanks 41

Contents

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 3/41

Introduction

One thing the digital advertising industry cannot be accused of iscomplacency: we devote a great deal of time, energy and money tocontinually challenging ourselves. As a young industry in a rapidlymoving environment, IAB Europe’s members know that if we don’tadapt, we won’t survive. This year’s AdEx Europe Benchmark reportshows that our self-examination is paying off: in extremely difficulteconomic times Europe’s online advertising market has continued togrow and - what’s more - it was the only advertising format thatdidn’t go backwards in 2009. The internet share of the totaladvertising market approached 20%, almost doubling its slice of the

market over two years.

Search advertising once again led the field recording a 10.8%increase on a like-for-like basis, a slowdown from the previous yearbut a notable achievement nonetheless. Display advertising was flatand even down in most mature markets. We took brand advertisingas our theme for this year’s Interact Congress in Barcelona,recognising the need to reinforce the message that brand advertisingoffers unique scope in creativity, innovation and engagement and it iscapable of delivering the enhanced measurement standards

advertisers seek to justify more investment in campaigns. Pressureon budgets had kept them relying on tried and tested formats, butthe good news is that display is already sprouting the green shoots ofrecovery in the first quarter of 2010. Video on digital platformscombined with social media is capable of delivering reach andefficiency measures to challenge any traditional media.

Growth in the most mature online ad markets UK, France, Germany,Netherlands, Spain and Italy - slowed to single digit rates, thoughSpain and Italy grew more as they started from a lower base. Growth

in Spain was remarkable when compared to the collapse of itstraditional advertising market at –23%. Only four markets posteddouble-digit growth in 2009: Greece, Austria, Poland and Turkeyagain starting from low bases.

Our reach this year has expanded with Russia, Switzerland, Bulgariaand Slovakia joining the AdEx Europe Benchmark – we welcome themwholeheartedly as members and celebrate the fresh perspectiveseach one brings to the report. In addition, we received figures fromIreland - one of our newest IABs - once the AdEx research had been

produced and released in June. We’re pleased to provide some Irishfigures in this report, but you won’t see the numbers in the totalfigures for 2010.

Alain HeureuxIAB Europe Presidentand CEO

My thanks to Catherine Borrel of IAB Europe and Vincent Létang Daniel Knapp of Screen Digest for presenting so clearly the data ananalysis of research covering 23 markets ranging from the maturemarkets of the Nordic nations and Western Europe to the emergingmarkets in Eastern and Southern Europe. In addition to auditing theAdEx data, Screen Digest’s analysts have provided some forwardlooking commentary and data that we hope you’ll find useful. I woalso like to thank our members InSites Consulting, comScore andNielsen Online for providing us with additional data for this report

As the fourth issue of this report, IAB Europe is proud toacknowledge that our annual report has become essential reading foeveryone connected to the digital advertising industry in marketsthroughout the world. We hope that once again you will find the dainsight and forecasts in this report useful for your business.

We look forward to the next chapter!

Regards

Alain Heureux

3IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 4/41

The sources of the online advertising spend data contained withinthis report are the annual industry benchmarking studies run by eacnational Interactive Advertising Bureau (IAB) in Europe. The natiobenchmarking studies represent the income of thousands of websiteand online advertising businesses.

The results reported are considered the closest measurement ofonline advertising revenues across Europe as the data is compileddirectly by local IABs based on information supplied by companiesselling advertising online. Only IABs that were able to provide 12

months of advertising expenditure data are included.

The data for this report is stated on the basis of actual gross incom(the monies actually paid by the advertiser, including any agencycommission). The report incorporated data from the following fouronline advertising sectors:

w Display advertisingw Search (pay per click fees)w Classifieds & Directoriesw Other

IAB Europe in partnership with Screen Digest collates and aggregathe data and makes the adjustments necessary to enable the data to bcomparable. More details of this process are provided in the Append

The result is comparable data based on actual revenues from acrossEurope. This is the fourth edition of the report, and therefore onceagain we are able to include year-on-year comparisons in the reportfor those countries that have participated for at least two years.

Screen Digest does not audit the information or the data from localIABs and provides no opinion or other form of assurance with respto the information. Only aggregate results are published andindividual company information is held in strict confidence by theaudit partners of local IAB studies.

The figures featured in this report include data from 23 IABs. Inaddition we have figures for the Irish market detailed in theAppendix, however these were not published in time to be included

the main report

4

About this report

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 5/41

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 6/41

EuropeUSA

Total online ad spend Europe vs USA2008 & 2009

0

5

10

15

20

2008 2009Source: IAB Europe/Screen Digest ©

B i l l i o

n E

u r o s

€ 16.3 € 16.8

€ 14.7

€ 13.2

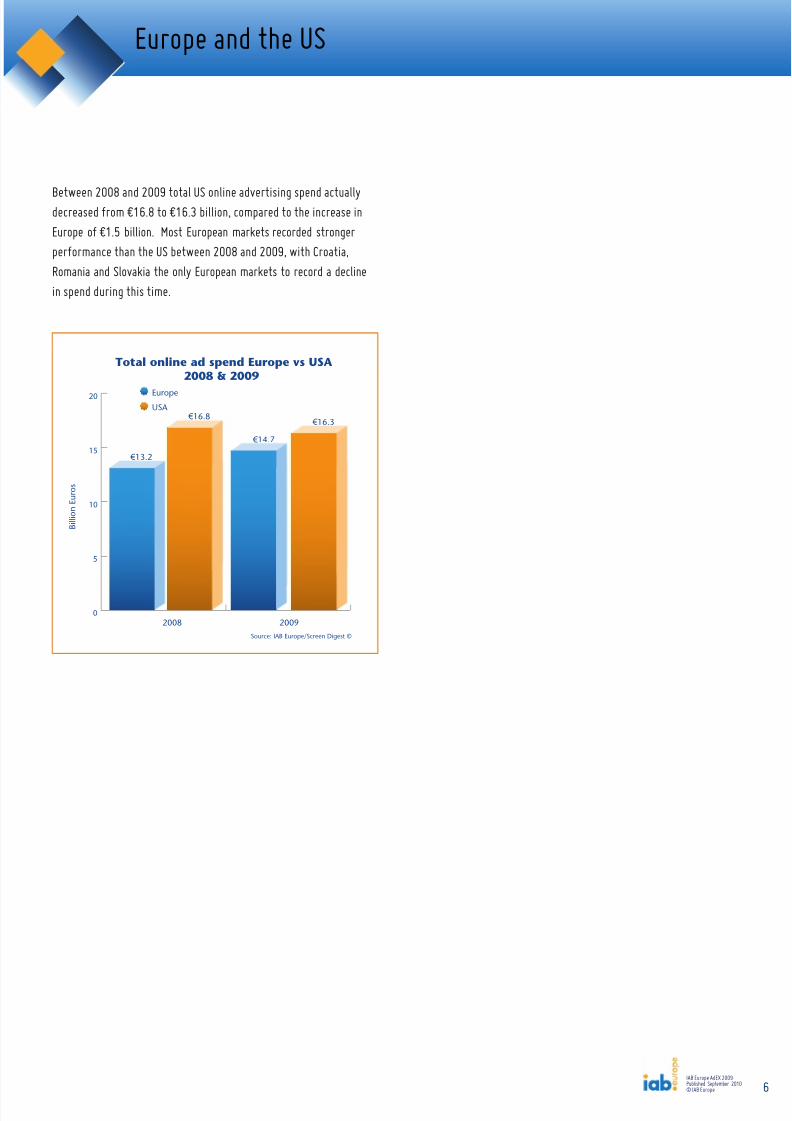

Between 2008 and 2009 total US online advertising spend actuallydecreased from €16.8 to €16.3 billion, compared to the increase inEurope of €1.5 billion. Most European markets recorded strongerperformance than the US between 2008 and 2009, with Croatia,Romania and Slovakia the only European markets to record a declinein spend during this time.

6

Europe and the US

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 7/41

Source: IAB Europe/Screen Digest ©

Total by country 2008 and 2009

Million Euros

0 1000 2000 3000 4000 5000

20092008

Romania

Croatia

Slovenia

Slovakia

Greece

HungaryTurkey

Finland

Austria

Belgium

Poland

Denmark

Norway

Sweden

Spain

Netherlands

Italy

France

GermanyUK

€ 3,834 € 4,011

€ 2,939

€ 1,731 € 3,092

€ 849 € 798

€ 1,760

€ 800 € 815

€ 635 € 683

€ 455 € 467

€ 374 € 401

€ 296 € 263

€ 384

€ 390

€ 280

€ 228

€ 293 € 200

€ 79 € 120 € 108

€ 182 € 174

€ 69 € 46

€ 85

€ 21 € 20 € 24 € 26

€ 14 € 13

€ 15 € 15

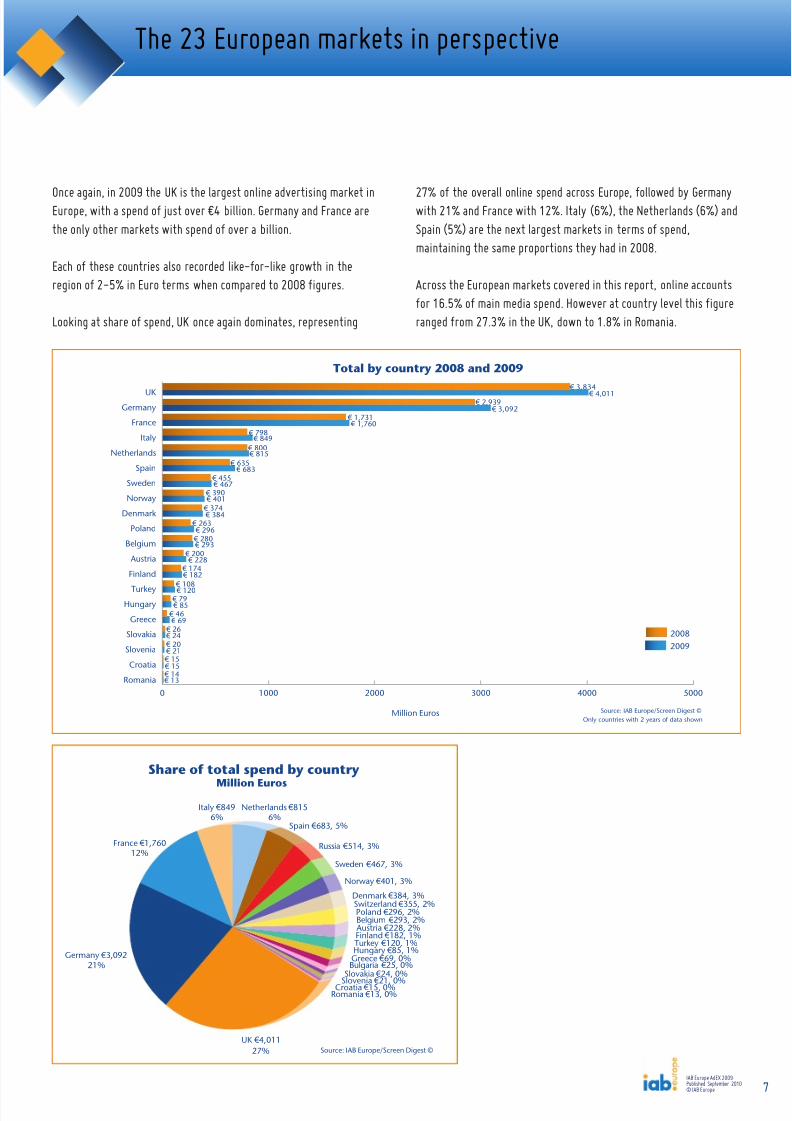

Once again, in 2009 the UK is the largest online advertising market inEurope, with a spend of just over €4 billion. Germany and France arethe only other markets with spend of over a billion.

Each of these countries also recorded like-for-like growth in theregion of 2-5% in Euro terms when compared to 2008 figures.

Looking at share of spend, UK once again dominates, representing

7

27% of the overall online spend across Europe, followed by Germawith 21% and France with 12%. Italy (6%), the Netherlands (6%) aSpain (5%) are the next largest markets in terms of spend,maintaining the same proportions they had in 2008.

Across the European markets covered in this report, online accountfor 16.5% of main media spend. However at country level this figuranged from 27.3% in the UK, down to 1.8% in Romania.

The 23 European markets in perspective

Share of total spend by countryMillion Euros

Source: IAB Europe/Screen Digest ©UK € 4,011

Germany € 3,09221%

France € 1,76012%

Netherlands € 8156%

Italy € 8496%

Spain € 683, 5%

Russia € 514, 3%

Sweden € 467, 3%

Norway € 401, 3%

Denmark € 384, 3%Switzerland € 355, 2%Poland € 296, 2%Belgium € 293, 2%

Austria € 228, 2%Finland € 182, 1%Turkey € 120, 1%Hungary € 85, 1%Greece € 69, 0%Bulgaria € 25, 0%

Slovakia € 24, 0%Slovenia € 21, 0%Croatia € 15, 0%

Romania € 13, 0%

27%

Only countries with 2 years of data shown

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 8/41

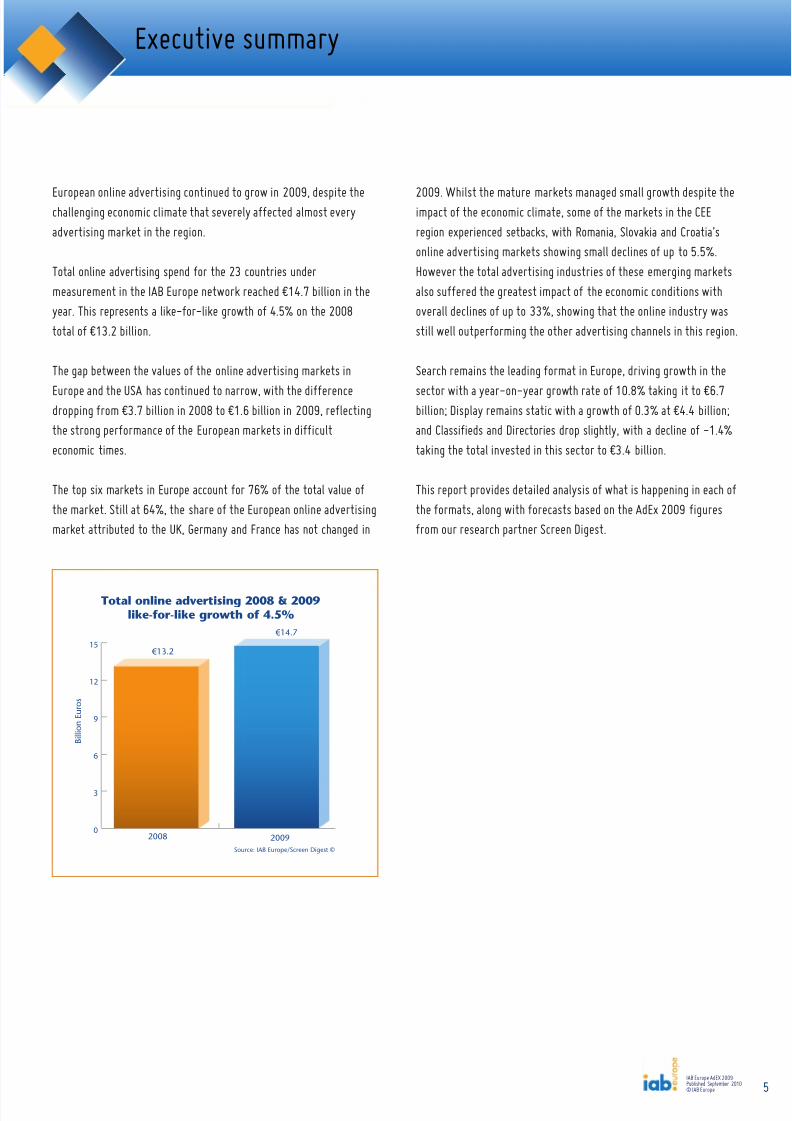

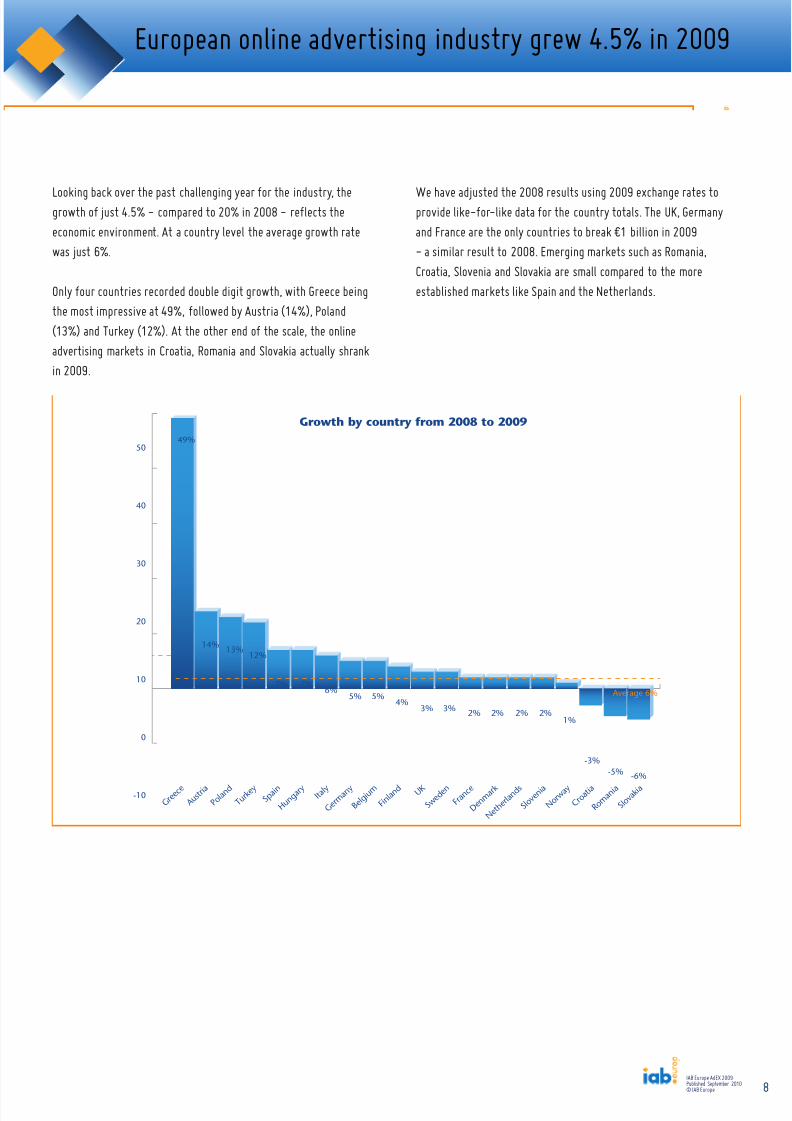

Looking back over the past challenging year for the industry, thegrowth of just 4.5% - compared to 20% in 2008 - reflects theeconomic environment. At a country level the average growth ratewas just 6%.

Only four countries recorded double digit growth, with Greece beingthe most impressive at 49%, followed by Austria (14%), Poland(13%) and Turkey (12%). At the other end of the scale, the onlineadvertising markets in Croatia, Romania and Slovakia actually shrankin 2009.

We have adjusted the 2008 results using 2009 exchange rates toprovide like-for-like data for the country totals. The UK, Germanyand France are the only countries to break €1 billion in 2009- a similar result to 2008. Emerging markets such as Romania,Croatia, Slovenia and Slovakia are small compared to the moreestablished markets like Spain and the Netherlands.

8

European online advertising industry grew 4.5% in 2009

Source: IAB Europe/Screen Digest ©

Growth by country from 2008 to 2009

G r e e c e

A u s t r i a

P o l a n d

T u r k e y S p a

i n H u

n g a r y I t a l y

G e r m

a n y B e l

g i u m F i n

l a n d U K S w

e d e n

F r a n c e

D e n m

a r k

N e t h e

r l a n d s

S l o v e n

i a N o

r w a y

C r o a t i a

R o m a n i a

S l o v a k

i a-10

0

10

20

30

40

50

Average 6%

49%

14% 13%12%

7% 7%6%

5% 5%4%

3% 3% 2% 2% 2% 2%1%

-3%-5% -6%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 9/419

European online advertising industry grew 4.5% in 2009

Source: IAB Europe/Screen Digest ©

0 1000 2000 3000 4000 5000

Romania € 13Croatia

SloveniaSlovakiaBulgariaGreece

HungaryTurkeyFinland Austria

BelgiumPoland

SwitzerlandDenmark

NorwaySweden

RussiaSpain

NetherlandsItaly

FranceGermany

UK

€ 15 € 21 € 24 € 25

€ 69 € 85 € 120

€ 182 €

228

€ 293 € 296

€ 355 € 384

€ 401 € 467 € 514

€ 683 € 815

€ 849 € 1760

€ 4011 € 3092

Online advertising spend by country 2009

Million Euros

IAB Europe AdEX 2009Published September 2010© IAB Europe

"Digital advertising is capable of delivering not double, but tripledigit growth if everyone can play their role to the best of theirability. In particular as an industry, we need to agree on our KeyPerformance Indicators, and to find a standardised way to measureonline branding"

Jef Vandecruys, Global Project Leader Digital Connection, Anheuser-Busch InBevIndustry growth -the advertiser’s perspective

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 10/4110IAB Europe AdEX 2009Published September 2010© IAB Europe

10 before 10 achieve d

In June 2008, Alain Heureux, President of IAB Europe predicted thatwe were well on the way to achieving a major online advertisingmilestone, where online advertising in 10 European countries wouldaccount for at least 10% of overall ad spend by 2010. In spite of thechallenging economic climate, in 2009 this target was surpassed with15 countries investing 10% or more of their main media spend ononline advertising. In 2008 nine countries met this benchmark, whilstin 2007 there were only seven.

These results highlight the growing importance of online as part ofthe advertising media mix. In fact in 2009 there are five countries -Netherlands, Sweden, Norway, Denmark and the UK - where onlinerepresents at least 20% of the main media spend. Only eight countrieshave an online advertising industry that constitutes less than 10% ofmain media spend.

WARC’s main media figures include spend on newspapers,magazines, TV, radio, cinema and outdoor advertising

UK 27.3%

Spending on online advertising as a proportion of main media spend in 2009

Source: IAB Europe/WARC ©

DenmarkNorwaySweden

Netherlands

GermanyFrance

Switzerland

FinlandPoland

SpainRussia

BelgiumItaly

HungaryTurkey

AustriaSloveniaBulgariaCroatia

GreeceRomania

25.5%23.4%

22.6%21.8%

17.8%15.3%

14.0%14.0%

13.4%

12.4%11.7%

10.6%10.3%

10.1%9.2%

7.5%

6.7%6.2%6.2%

4.1%1.8%

% of main media spend

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 11/41

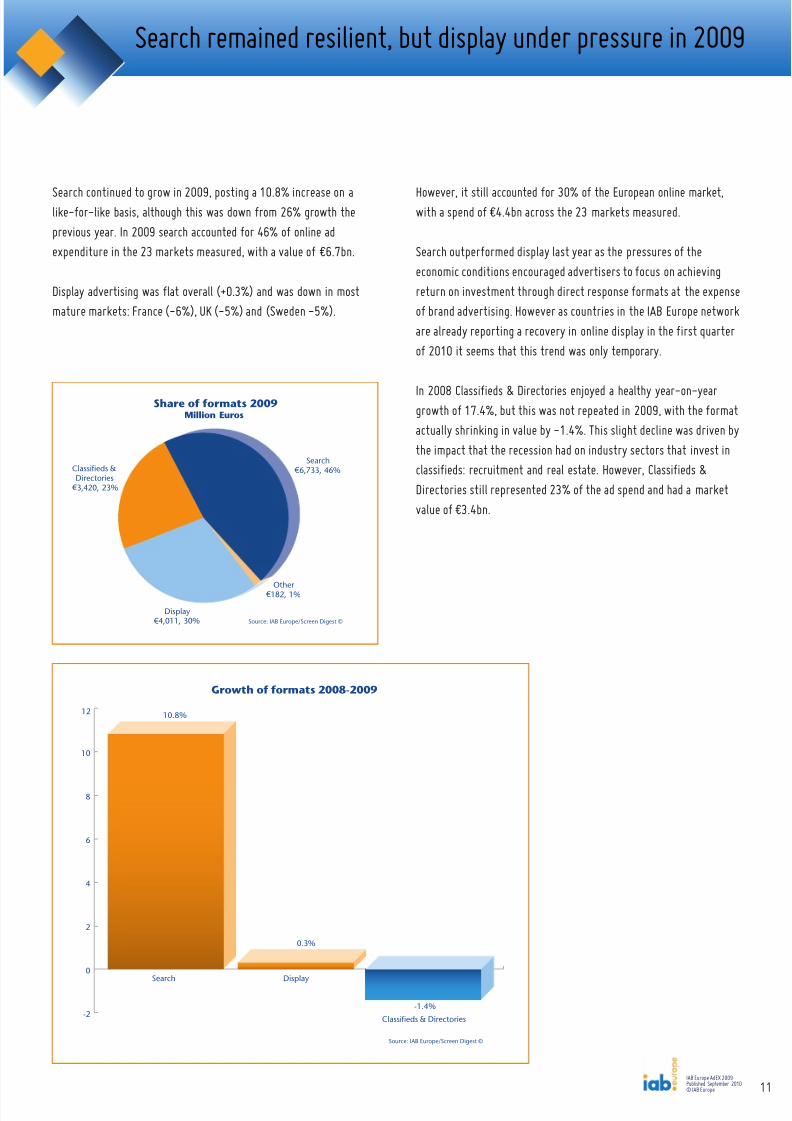

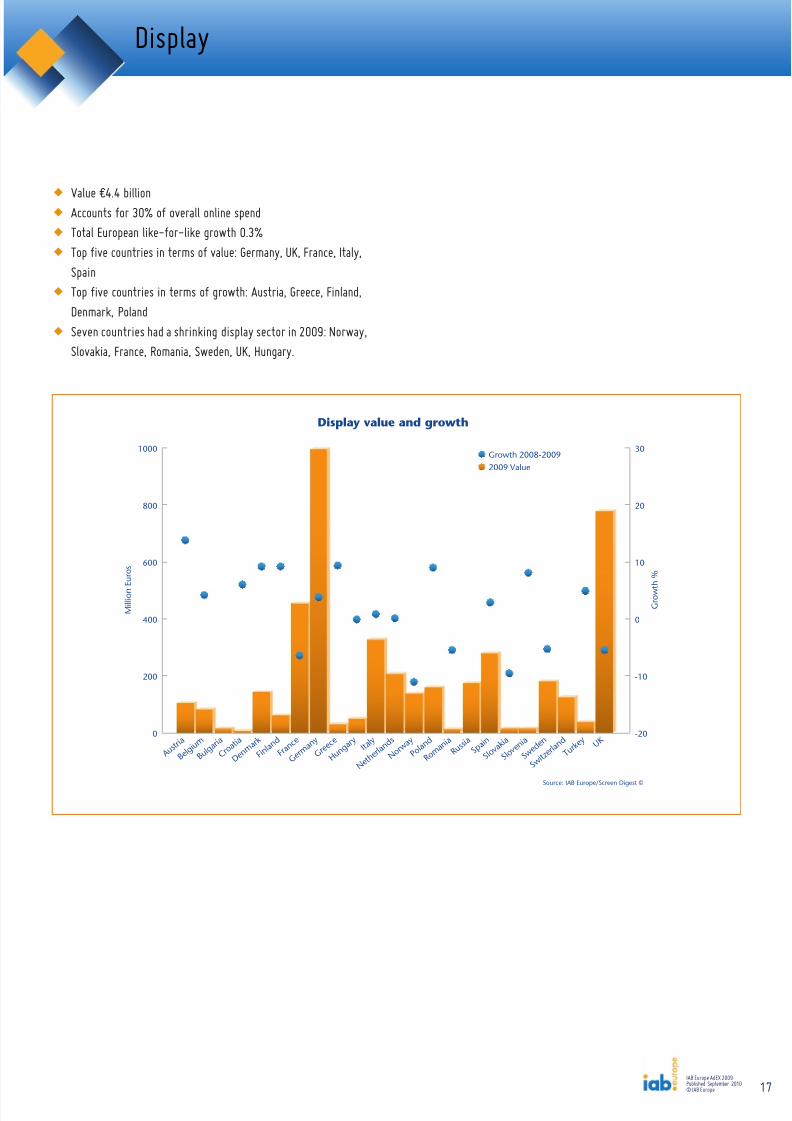

However, it still accounted for 30% of the European online market,with a spend of €4.4bn across the 23 markets measured.

Search outperformed display last year as the pressures of theeconomic conditions encouraged advertisers to focus on achievingreturn on investment through direct response formats at the expensof brand advertising. However as countries in the IAB Europe netware already reporting a recovery in online display in the first quarteof 2010 it seems that this trend was only temporary.

In 2008 Classifieds & Directories enjoyed a healthy year-on-yeargrowth of 17.4%, but this was not repeated in 2009, with the formaactually shrinking in value by -1.4%. This slight decline was driventhe impact that the recession had on industry sectors that invest inclassifieds: recruitment and real estate. However, Classifieds &Directories still represented 23% of the ad spend and had a marketvalue of €3.4bn.

Share of formats 2009Million Euros

Source: IAB Europe/Screen Digest ©

Classifieds &Directories

€ 3,420, 23%

Search € 6,733, 46%

Other € 182, 1%

Display € 4,011, 30%

Search continued to grow in 2009, posting a 10.8% increase on alike-for-like basis, although this was down from 26% growth theprevious year. In 2009 search accounted for 46% of online adexpenditure in the 23 markets measured, with a value of €6.7bn.

Display advertising was flat overall (+0.3%) and was down in mostmature markets: France (-6%), UK (-5%) and (Sweden -5%).

11

Search remained resilient, but display under pressure in 2009

Source: IAB Europe/Screen Digest ©

Growth of formats 2008-2009

-2

0

2

4

6

8

10

12

Classifieds & Directories

DisplaySearch

10.8%

0.3%

-1.4%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 12/41

Search value and growth

A u s t r i a

B e l g i u m B u l g a

r i a C r o a

t i a

D e n m a r k

F i n l a n d

F r a n c e

G e r m a n y

G r e e c e

H u n g a r y

I t a l y

N e t h e r l a n

d s

N o r w a y

P o l a n d

R o m a n i a

R u s s i a

S l o v a k i a

S l o v e n i a

S p a i n

S w e d e n

S w i t z e r l a

n d T u r k

e y U K

Source: IAB Europe/Screen Digest ©

0

500

1000

1500

2000

2500

Growth 2008-2009

2009 Value

M i l l i o n

E u r o s

G r o w

t h %

75

100

50

25

0

-25

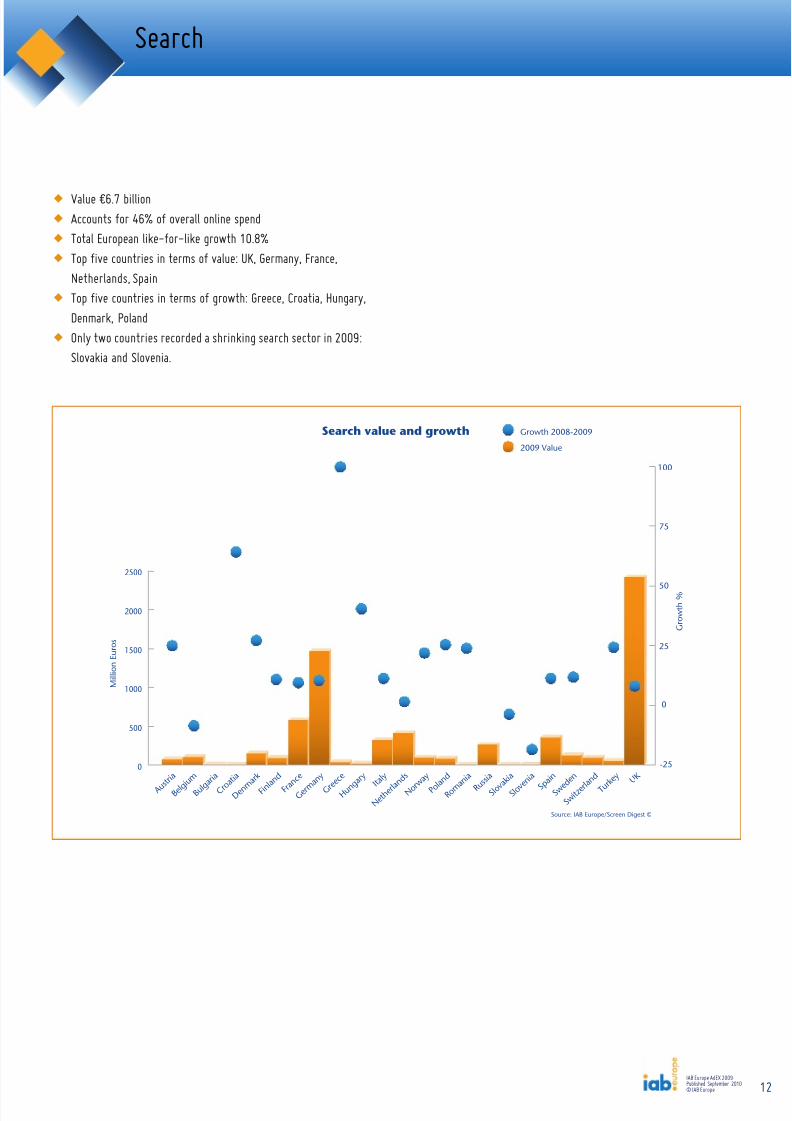

12

w Value €6.7 billionw Accounts for 46% of overall online spendw Total European like-for-like growth 10.8%w Top five countries in terms of value: UK, Germany, France,

Netherlands, Spainw Top five countries in terms of growth: Greece, Croatia, Hungary,

Denmark, Polandw Only two countries recorded a shrinking search sector in 2009:

Slovakia and Slovenia.

Search

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 13/4113

Search

2009

2008

Romania

Slovakia

Slovenia

Croatia

Bulgaria

Hungary

Greece

Turkey

Austria

Poland

Finland

Switzerland

Norway

Belgium

Sweden

Denmark

Russia

Italy

Spain

Netherlands

France

Germany

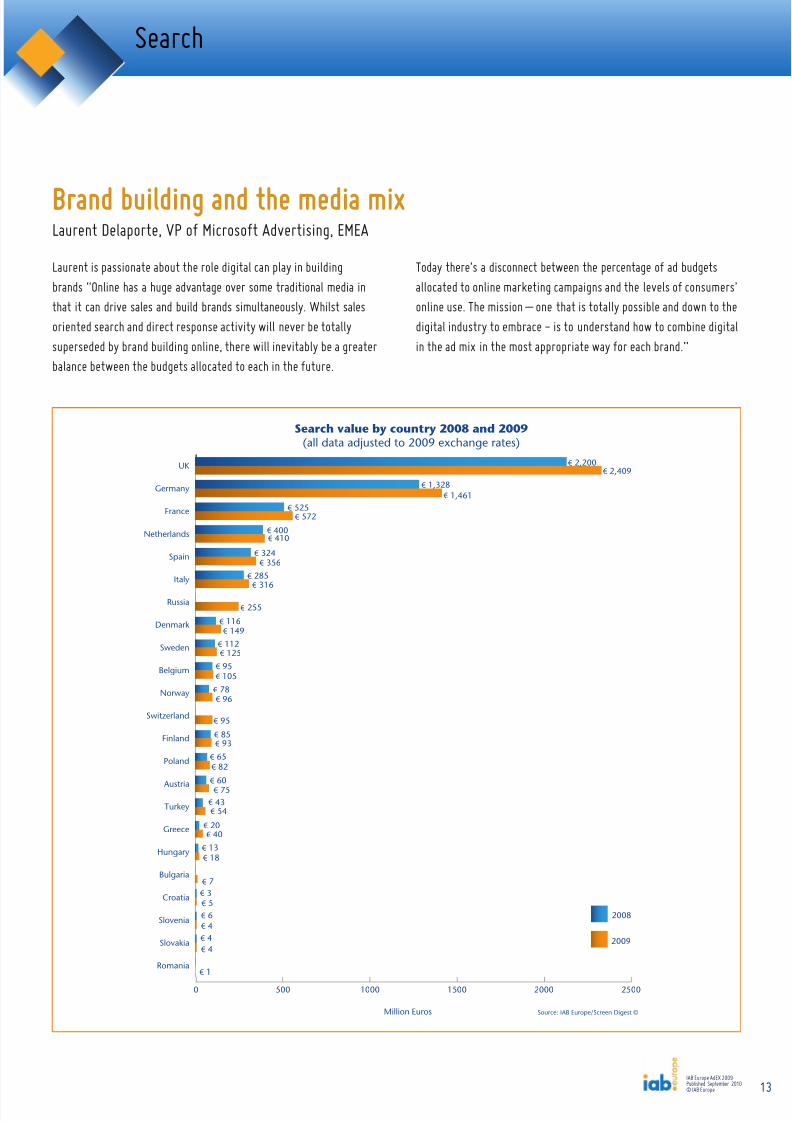

UK € 2,200€ 2,409

Search value by country 2008 and 2009(all data adjusted to 2009 exchange rates)

€ 1,328€ 1,461

€ 525€ 572

€ 400€ 410

€ 324€ 356

€ 285€

316€ 255

€ 116€ 149

€ 112€ 125

€ 95€ 105

€ 78€ 96

€ 95€ 85€ 93

€ 65€ 82

€ 60€ 75

€ 43€ 54

€ 20€ 40

€ 13€ 18

€ 7€ 3€ 5€ 6€ 4€ 4€ 4

€ 1

Source: IAB Europe/Screen Digest © Million Euros

0 500 1000 1500 2000 2500

IAB Europe AdEX 2009Published September 2010© IAB Europe

Laurent is passionate about the role digital can play in buildingbrands “Online has a huge advantage over some traditional media inthat it can drive sales and build brands simultaneously. Whilst salesoriented search and direct response activity will never be totallysuperseded by brand building online, there will inevitably be a greaterbalance between the budgets allocated to each in the future.

Laurent Delaporte, VP of Microsoft Advertising, EMEABrand building and the media mix

Today there’s a disconnect between the percentage of ad budgetsallocated to online marketing campaigns and the levels of consumeonline use. The mission – one that is totally possible and down to tdigital industry to embrace - is to understand how to combine digitin the ad mix in the most appropriate way for each brand.”

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 14/4114

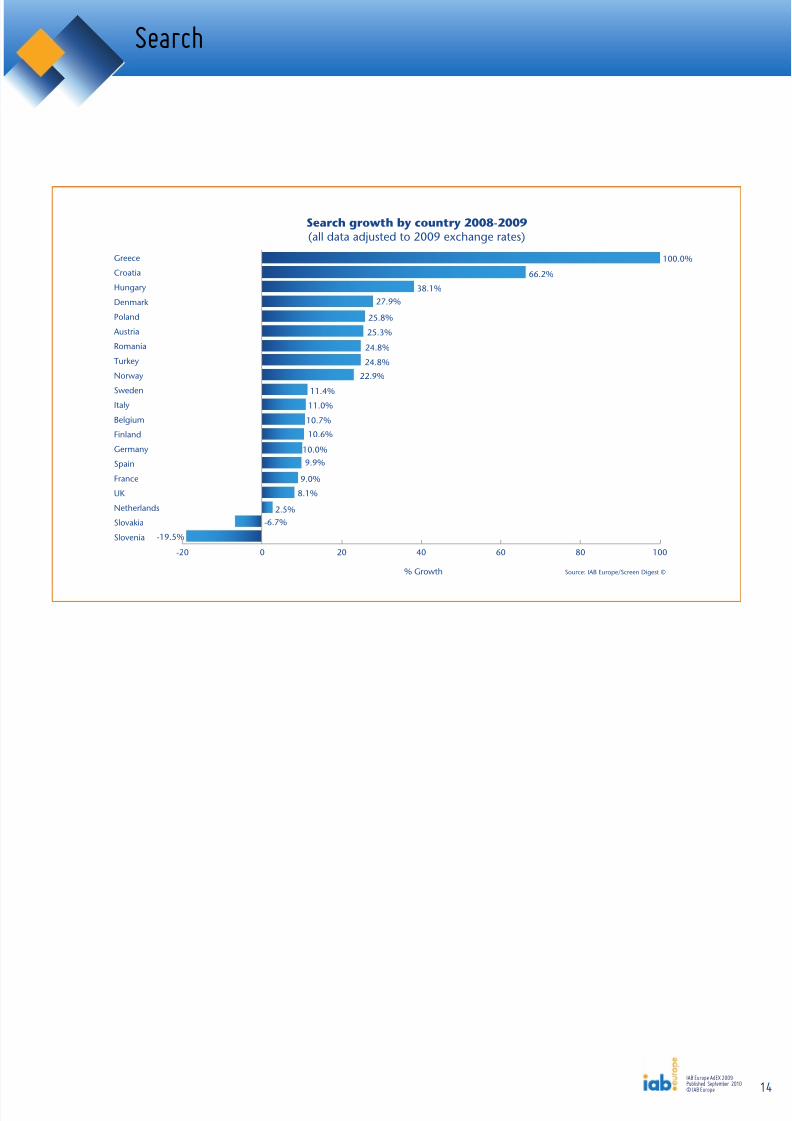

Search

-20 0 20 40 60 80 100

-19.5%

-6.7%2.5%

8.1%

9.0%

10.0%

10.6%

10.7%

11.0%

9.9%

11.4%

22.9%

24.8%

24.8%

25.3%

25.8%

27.9%38.1%

66.2%

100.0%Greece

Croatia

Hungary

Denmark

Poland

Austria

Romania

Turkey

Norway

SwedenItaly

Belgium

Finland

Germany

Spain

France

UK

Netherlands

Slovakia

Slovenia

Source: IAB Europe/Screen Digest ©

Search growth by country 2008-2009(all data adjusted to 2009 exchange rates)

% Growth

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 15/41

M i l l i o n

E u r o s

G r o w

t h %

Growth 2008-2009

2009 Value

Classifieds & directories value and growth

Source: IAB Europe/Screen Digest ©

0

100

200

300

400

500

600

-40

700

800

-30

-20

-10

0

10

20

30

40

A u s t r i a

B e l g i u m

B u l g a r

i a C r o

a t i a

D e n m

a r k F i n

l a n d F r a

n c e

G e r m

a n y G r e

e c e

H u n g a r

y I t a l

y

N e t h e

r l a n d s

N o r w a

y P o l

a n d

R o m a n i

a R u s

s i a S l o

v a k i a

S l o v e n

i a S p a

i n S w

e d e n

S w i t z e

r l a n d T u r

k e y U K

15

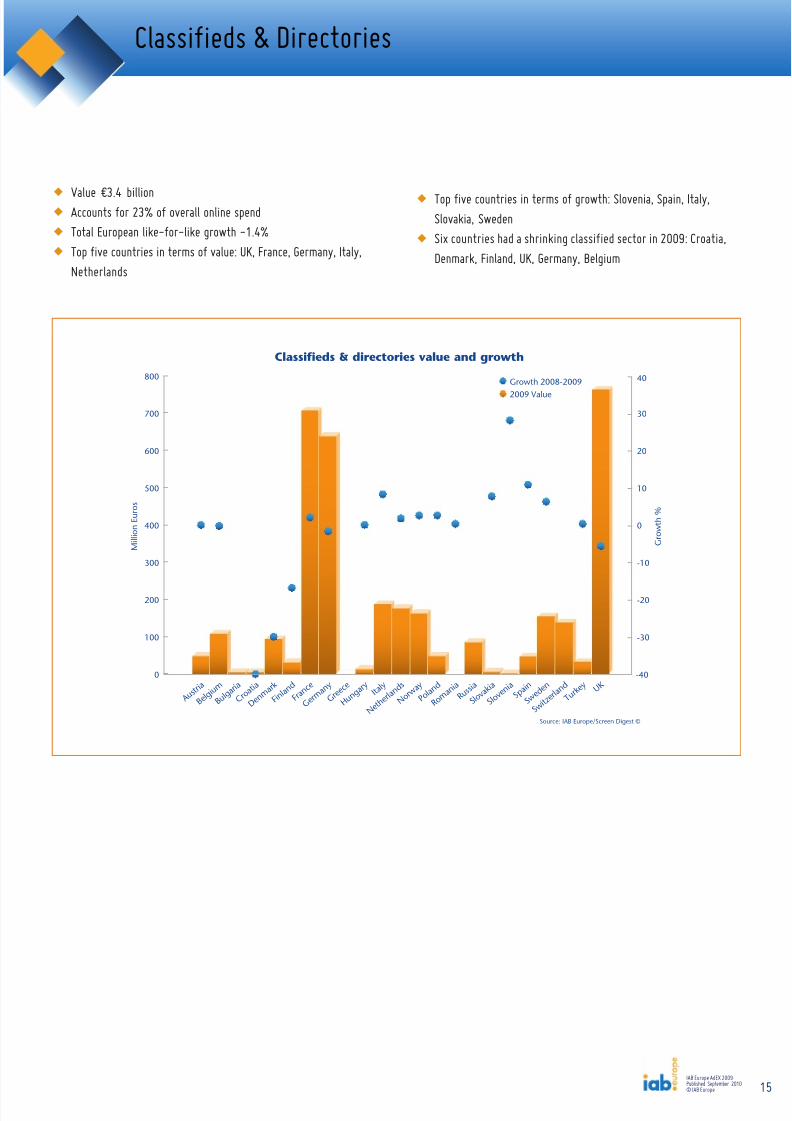

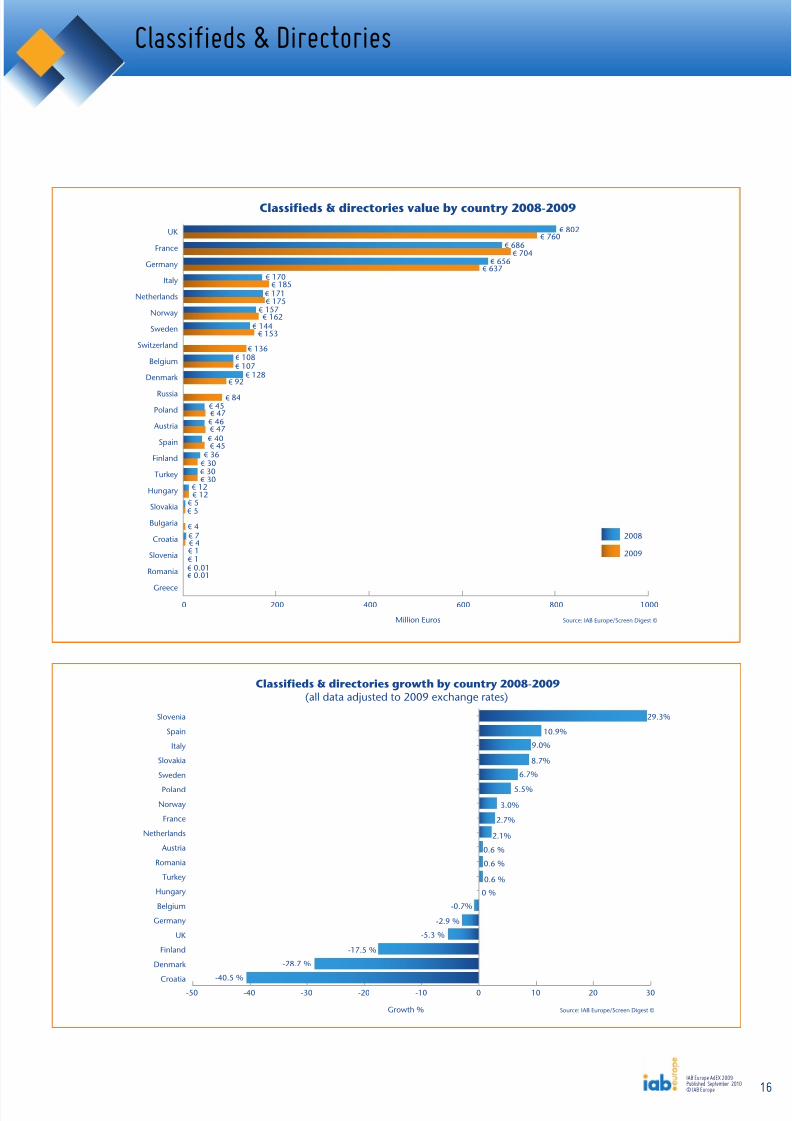

w Top five countries in terms of growth: Slovenia, Spain, Italy,Slovakia, Sweden

w Six countries had a shrinking classified sector in 2009: Croatia,Denmark, Finland, UK, Germany, Belgium

wValue €3.4 billion

w Accounts for 23% of overall online spendw Total European like-for-like growth -1.4%w Top five countries in terms of value: UK, France, Germany, Italy,

Netherlands

Classifieds& Directories

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 16/41

0 200 400 600 800 1000

2009

2008

Greece

Romania

Slovenia

Croatia

Bulgaria

Slovakia

Hungary

Turkey

Finland

Spain

Austria

Poland

Russia

Denmark

Belgium

Switzerland

Sweden

Norway

Netherlands

Italy

Germany

France

UK € 802€ 760

€ 686€ 704

€ 656€ 637

€ 170€ 185

€ 171€ 175

€ 157€ 162

€ 144€ 153

€ 136€ 108€ 107

€ 128€ 92

€ 84€ 45€ 47

€ 46€ 47

€ 40€ 45

€ 36€ 30€ 30€ 30

€ 12€ 12

€ 5€ 5

€ 4€ 7€ 4€ 1€ 1€ 0.01€ 0.01

Classifieds & directories value by country 2008-2009

Source: IAB Europe/Screen Digest © Million Euros

Classifieds& Directories

Source: IAB Europe/Screen Digest ©

Classifieds & directories growth by country 2008-2009(all data adjusted to 2009 exchange rates)

Growth %

-50 -40 -30 -20 -10 0 10 20 30Croatia

Denmark

Finland

UK

Germany

Belgium

Hungary

Turkey

Romania

Austria

Netherlands

France

Norway

Poland

Sweden

Slovakia

Italy

Spain

Slovenia 29.3%

10.9%

9.0%

8.7%

6.7%

5.5%

3.0%

2.7%

2.1%

0.6 %

0.6 %

0.6 %

0 %

-0.7%

-2.9 %

-5.3 %

-17.5 %

-28.7 %

-40.5 %

16IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 17/41

M i l l i o n E u r o s

G r o w

t h %

Growth 2008-20092009 Value

Display value and growth

Source: IAB Europe/Screen Digest ©

A u s t r i a

B e l g i u m

B u l g a r

i a C r o

a t i a

D e n m

a r k F i n

l a n d F r a

n c e

G e r m

a n y G r e

e c e

H u n g a r

y I t a l

y

N e t h e

r l a n d s

N o r w a

y P o l

a n d

R o m a n i

a R u s

s i a S p a

i n S l o

v a k i a

S l o v e n

i a S w

e d e n

S w i t z e

r l a n d T u r

k e y U K0

200

400

600

800

1000

-20

-10

0

10

20

30

17

w Value €4.4 billionw Accounts for 30% of overall online spendw Total European like-for-like growth 0.3%w Top five countries in terms of value: Germany, UK, France, Italy,

Spainw Top five countries in terms of growth: Austria, Greece, Finland,

Denmark, Polandw Seven countries had a shrinking display sector in 2009: Norway,

Slovakia, France, Romania, Sweden, UK, Hungary.

Display

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 18/41

0 200 400 600 800 1000

2009

2008

Croatia

Romania

Greece

Turkey

Hungary

Finland

Belgium

Austria

Switzerland

Norway

Denmark

Poland

Russia

Sweden

Netherlands

Italy

France

UK

Germany € 956€ 994

€ 821€ 777

€ 482€ 453

€ 323€ 326

€ 205€ 206

€ 190€ 180

€ 174€ 145€ 158

€ 129€ 141

€ 154€ 137

€ 124€ 91

€ 103€ 77

€ 81€ 54€ 59

€ 49€ 49

€ 35€ 37

€ 26€ 29

€ 270Spain € 278

Bulgaria

Slovakia € 15€ 17

€ 14Slovenia € 13

€ 14€ 13€ 12€ 5€ 6

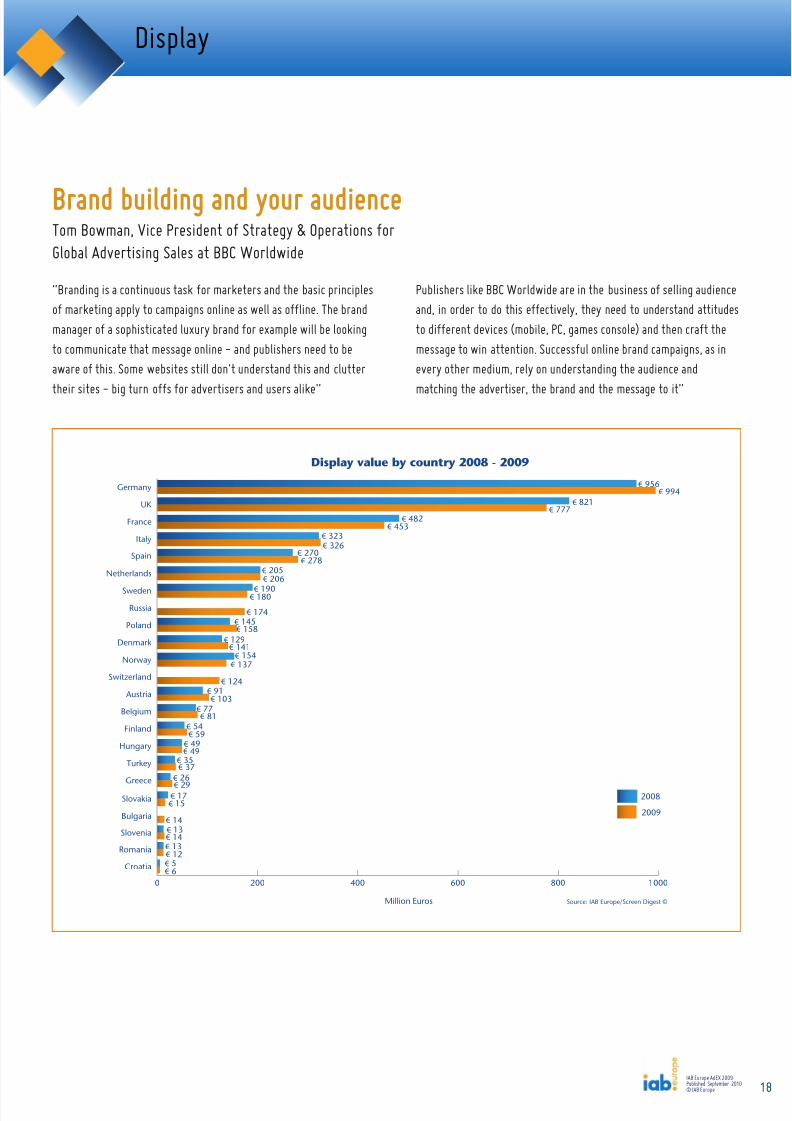

Display value by country 2008 - 2009

Source: IAB Europe/Screen Digest ©Million Euros

18

Display

IAB Europe AdEX 2009Published September 2010© IAB Europe

“Branding is a continuous task for marketers and the basic principlesof marketing apply to campaigns online as well as offline. The brandmanager of a sophisticated luxury brand for example will be lookingto communicate that message online - and publishers need to beaware of this. Some websites still don't understand this and clutter

their sites - big turn offs for advertisers and users alike”

Tom Bowman, Vice President of Strategy & Operations forGlobal Advertising Sales at BBC Worldwide

Brand building and your audience

Publishers like BBC Worldwide are in the business of selling audieand, in order to do this effectively, they need to understand attitudeto different devices (mobile, PC, games console) and then craft themessage to win attention. Successful online brand campaigns, as inevery other medium, rely on understanding the audience and

matching the advertiser, the brand and the message to it”

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 19/41

-12 -9 -6 -3 0 3 6 9 12 15

Norway

Slovakia

France

Romania

Sweden

UK

Hungary

Netherlands

Italy

Spain

Germany

Belgium

Turkey

Croatia

Slovenia

Poland

Denmark

Finland

Greece

Austria 13.4 %

9.6 %

9.4 %

9.4 %

8.9 %

8.6 %

6.2 %

-5.4 %

4.0 %

4.5 %

5.0 %

-5.3 %

-0.047 %

0.2 %

1.0 %

3.1 %

-11.1 %

-9.2 %

-6.0 %

-5.5 %

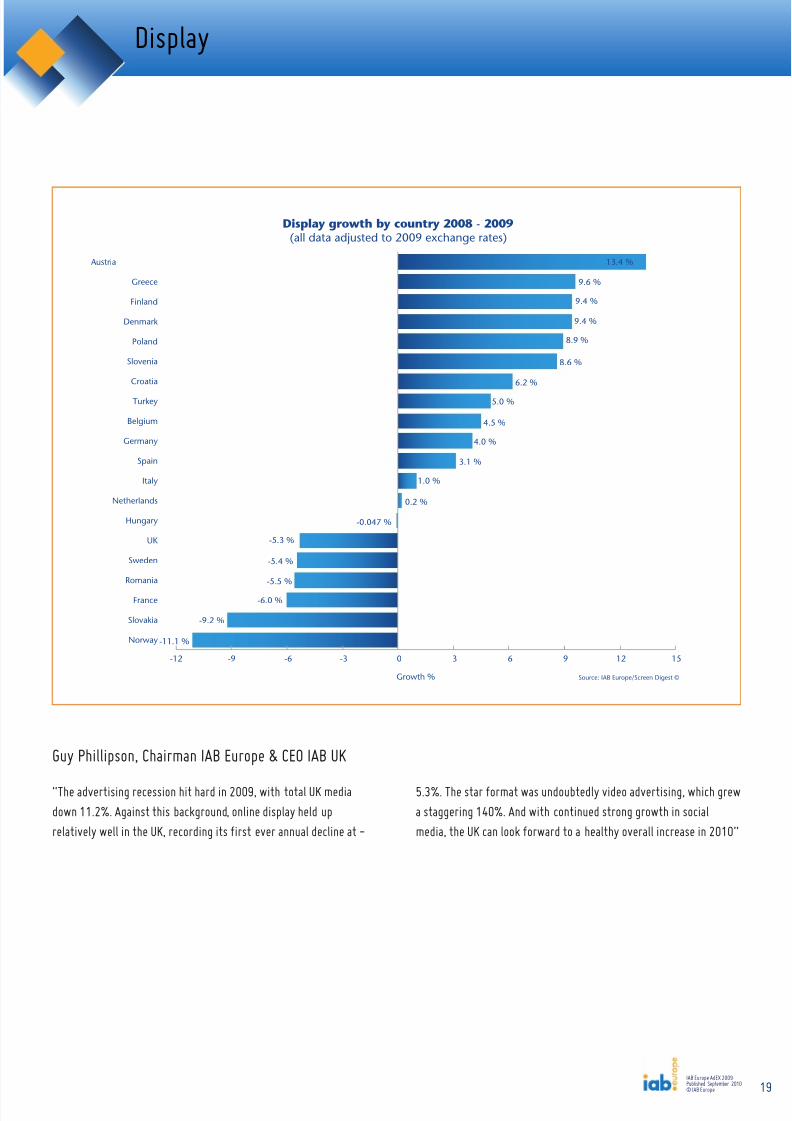

Display growth by country 2008 - 2009(all data adjusted to 2009 exchange rates)

Source: IAB Europe/Screen Digest ©Growth %

19

Display

IAB Europe AdEX 2009Published September 2010© IAB Europe

“The advertising recession hit hard in 2009, with total UK mediadown 11.2%. Against this background, online display held uprelatively well in the UK, recording its first ever annual decline at -

Guy Phillipson, Chairman IAB Europe & CEO IAB UK

5.3%. The star format was undoubtedly video advertising, which ga staggering 140%. And with continued strong growth in socialmedia, the UK can look forward to a healthy overall increase in 20

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 20/41

M i l l i o n

E u r o s

DisplayClassifieds & DirectoriesSearchOther

Spend by format and by country: Western Europe

U K

G e r m

a n y

F r a n c

e I t a l y

N e t h e

r l a n d s

S p a i n

S w e d

e n

N o r w

a y

D e n m

a r k

S w i t z e

r l a n d

B e l g i u m

A u s t r i a

F i n l a n d

Source: IAB Europe/Screen Digest ©

Other

Search

Classifieds

Display

€ 65.9

€ 2408.9

€ 759.7

€ 776.7

€ 1461.2

€ 636.5

€ 993.9

€ 30.8

€ 572.0

€ 704.4

€ 453.0

€ 21.6

€ 316.4

€ 185.3

€ 326.0

€ 24.5

€ 410.0

€ 175.0

€ 205.6

€ 3.9

€ 356.4

€ 44.7

€ 278.3

€ 9.1

€ 124.7

€ 153.4

€ 179.7

€ 6.1

€ 95.6

€ 161.7

€ 137.2

€ 2.5

€ 148.9

€ 91.5

€ 140.6

€ 95.1

€ 136.4

€ 123.9

€ 104.7

€ 107.4

€ 80.7

€ 3.2

€ 75.2

€ 46.6

€ 103.0

€ 93.5

€ 29.9

€ 58.7

0

1000

2000

3000

4000

5000

G r e e

c e

€ 40.0

€ 0.0

€ 28.5

20

GermanyAs was the case in 2008, Germany is the second largest marketoverall. Germany has the most valuable display sector - worth €994million, however in terms of proportional spend, this only accounts

for 32% of the overall online ad spend. Search is the dominantcategory, with 47% of overall online spend, with Classifieds &Directories at 21%. The German online advertising market alsomanaged a small growth despite the fact that the advertising markeas a whole saw a decline of -9.3%,

UKThe UK is the largest market by spend of the 23 countries covered inthis report, with a value of just over €4 billion in 2009. The UK alsorecorded the highest proportional spend for online - 27.3% of total

main media spend. Search is the dominant category in the UK,accounting for 60% of total online spend, and making the UK thecountry with the highest proportion of online ad spend in this category.The UK online advertising market managed a 3.2% like-for-like growthwhen the rest of the advertising market saw a decline of -11.5%

Regional and country detailWestern Europe

2009 Online Ad Spend €4,011 m2008-2009 online ad spend growth 3.2%2009 main media spend (WARC) €14,714 mOnline as a proportion of main media spend (WARC) 27.3%

2009 Online Ad Spend €3,092 m2008-2009 online ad spend growth 5.2%2009 main media spend (WARC) €17,391 mOnline as a proportion of main media spend (WARC) 17.8%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 21/4121

SpainSpain had the third highest proportional spend on Search in Europe,52%. Display is the second largest category at 41%, whilst Classifi& Directories account for only 7% of online spend. Growth was juabove average at 7.1% and achieved when the advertising market awhole saw a decline of -20%. As online still only accounts for 12.of main media spend there is still room for strong growth.

SwedenAt 22.6% Sweden has the third highest proportion of online spend part of the overall main media mix. Display accounts for 38% ofspend, followed by Classifieds & Directories (33%) and Search (27The modest growth of 2.7% in online advertising was achieved in ayear where the advertising market as a whole saw a decline of -13.4%

NorwayNorway has the second highest proportion of main media spenddevoted to online - 23.4%. The majority of spend, 40%, goes onClassifieds & Directories. This is the highest proportion in Europe,position shared with France where 40% of spend also goes towardsClassifieds & Directories. Display represents 34% of online spend Norway, while Search accounts for just 24%.

FranceFrance, along with Norway, has the largest classified market in termsof proportional spend (both 40%), and the second largest after theUK in terms of spend (€704m). Search is the second most popularcategory at 32%, followed by Display at 26%. The online advertisingmarket in France managed a small growth despite the fact that theadvertising market as a whole saw a decline of -12.5%

ItalyItaly is the fourth largest market in Europe, maintaining its positionfrom 2008. Display is the dominant sector, but only by 1% inproportional spend terms accounting for 38% of the spend comparedto Search on 37%. Classifieds & Directories come a distant third at22%. However as online still represents only 10.3% of main media

spend, considerably below many other Western European markets,there is still room for industry growth in the near future.

NetherlandsThe Netherlands is the fifth largest market in terms of spend. As oneof the most mature European markets, the Netherlands saw littlegrowth in online advertising spend in 2009 - just 1.8%. This wasachieved despite the advertising market as a whole declining by -13.1%in the same period. Search is the predominant category, accountingfor 50% of spend, followed by Display (25%) and Classifieds &Directories (21%). 21.8% of the Netherlands main media spend goestowards online, which is the fifth largest proportion in Europe.

Regional and country detailWestern Europe

2009 Online Ad Spend €1,760 m2008-2009 online ad spend growth 2.2%2009 main media spend (WARC) €11,525 mOnline as a proportion of main media spend (WARC) 15.3%

2009 Online Ad Spend €683 m2008-2009 online ad spend growth 7.1%2009 main media spend (WARC) €5,502 mOnline as a proportion of main media spend (WARC) 12.4%

2009 Online Ad Spend €849 m2008-2009 online ad spend growth 6.4%2009 main media spend (WARC) €8,259 mOnline as a proportion of main media spend (WARC) 10.3%

2009 Online Ad Spend €467 m2008-2009 online ad spend growth 2.7%2009 main media spend (WARC) €2,069 mOnline as a proportion of main media spend (WARC) 23%

2009 Online Ad Spend €401 m2008-2009 online ad spend growth 1.4%2009 main media spend (WARC) €1,714 mOnline as a proportion of main media spend (WARC) 23.4%

2009 Online Ad Spend €815 m2008-2009 online ad spend growth 1.8%2009 main media spend (WARC) €3,746 mOnline as a proportion of main media spend (WARC) 21.8%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 22/4122

FinlandThe Finnish online advertising market is worth €182 million in 200which represents14% of main media spend. Search represents 51%online spend, followed by Display (32%) and Classifieds & Directo(16%).

IrelandIreland is the second smallest market in Western Europe, worth€97.2 million in 2009. Search represents 46% of online spend,followed by Classifieds & Directories (27%) and Display (26%). Tthe first year that data from Ireland has been included in the AdExreport, so there is no growth data available. There is no WARC datavailable for Ireland. The data from Ireland was received after initipublication, and is therefore not included in the other calculations i

this report.

GreeceGreece was the fastest growing market in Europe in 2009 by aconsiderable margin, recording an increase of 48.9%, although theoverall market value is small, and online represents only 4.1% ofmain media spend. Greece is the only European market that recordno spend on Classifieds & Directories in 2009, instead spending 58on Search and 42% on Display advertising.

DenmarkOne quarter of Denmark's main media spend goes to online - thesecond highest proportion in Europe. Search accounts for 39% ofspend, closely followed by Display (37%), with Classifieds &Directories on 22%.

SwitzerlandSwitzerland is a new market for this report, so no growth figures areavailable. The Classifieds & Directories market accounts for 38% oftotal online spend, the second highest proportion in Europe. Displayaccounts for 35%, and search 27%.

BelgiumBelgium devotes 10.6% of main media spend to online. Classifieds &Directories account for 37%, Search 36% and Display 28%.

AustriaAlthough Austria recorded the best growth rate in Western Europe, andthe second highest growth rate overall (14%), online still only accountsfor 7.5% of main media spend. Display is the dominant format (40%),followed by Search (33%) and Classifieds & Directories (20%).

Regional and country detailWestern Europe

2009 Online Ad Spend €384 m2008-2009 online ad spend growth 2%2009 main media spend (WARC) €1,507Online as a proportion of main media spend (WARC) 25.5%

2009 Online Ad Spend €182 m2008-2009 online ad spend growth 4.4%2009 main media spend (WARC) €1,296 mOnline as a proportion of main media spend (WARC) 14%

2009 Online Ad Spend €355 m2009 main media spend (WARC) €2,531 mOnline as a proportion of main media spend (WARC) 14%

2009 Online Ad Spend €97.2 m

2009 Online Ad Spend €228 m2008-2009 online ad spend growth 14%2009 main media spend (WARC) €3,039 mOnline as a proportion of main media spend (WARC) 7.5%

2009 Online Ad Spend €293 m2008-2009 online ad spend growth 4.6%2009 main media spend (WARC) €2,753 mOnline as a proportion of main media spend (WARC) 10.6%

2009 Online Ad Spend €69 m2008-2009 online ad spend growth 48.9%2009 main media spend (WARC) €1,654Online as a proportion of main media spend (WARC) 4.1%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 23/4123

M i l l i o n

E u r o s

DisplayClassifieds & DirectoriesSearchOther

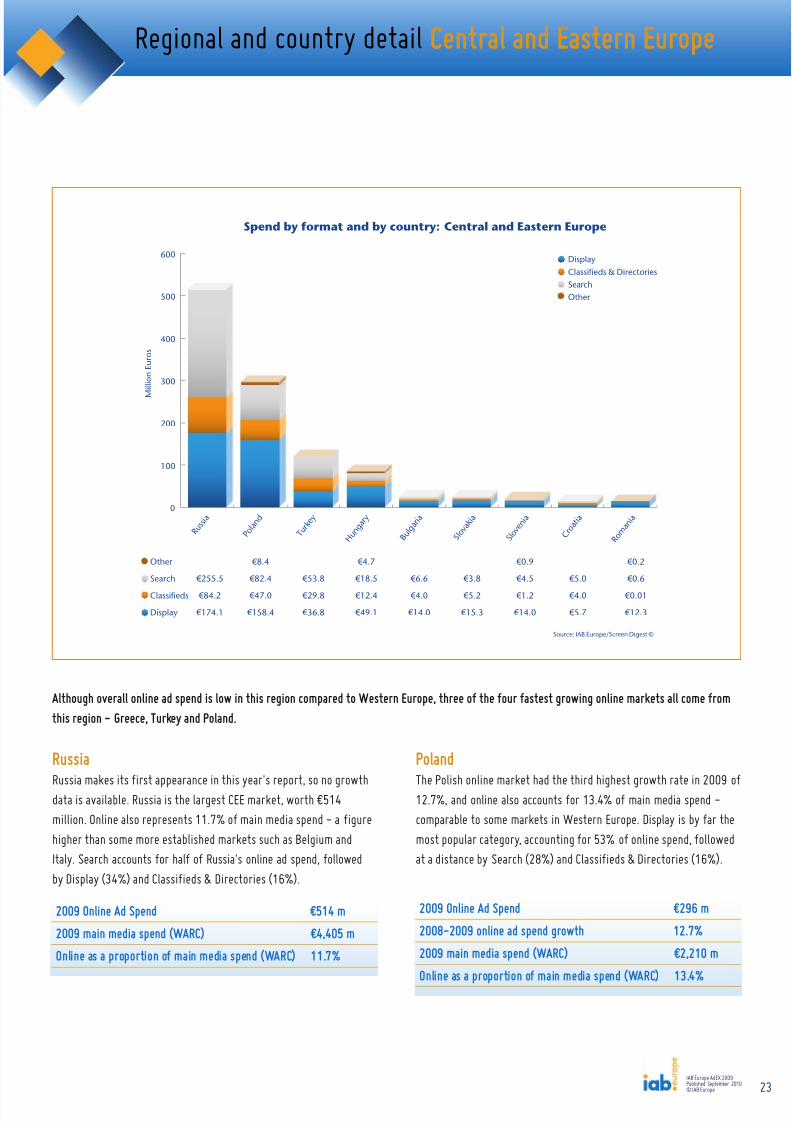

Spend by format and by country: Central and Eastern Europe

R u s s i a

P o l a n

d

T u r k e

y

H u n g a r y

B u l g a r i a

S l o v a k i a

S l o v e n i a

C r o a

t i a

R o m a

n i a

Source: IAB Europe/Screen Digest ©

Other

Search

Classifieds

Display

€ 255.5

€ 84.2

€ 174.1

€ 8.4

€ 82.4

€ 47.0

€ 158.4

€ 53.8

€ 29.8

€ 36.8

€ 4.7

€ 18.5

€ 12.4

€ 49.1

€ 6.6

€ 4.0

€ 14.0

€ 3.8

€ 5.2

€ 15.3

€ 0.9

€ 4.5

€ 1.2

€ 14.0

€ 5.0

€ 4.0

€ 5.7

€ 0.2

€ 0.6

€ 0.01

€ 12.3

0

100

200

300

400

500

600

Poland

The Polish online market had the third highest growth rate in 2009 12.7%, and online also accounts for 13.4% of main media spend -comparable to some markets in Western Europe. Display is by far tmost popular category, accounting for 53% of online spend, followat a distance by Search (28%) and Classifieds & Directories (16%)

Russia

Russia makes its first appearance in this year's report, so no growthdata is available. Russia is the largest CEE market, worth €514million. Online also represents 11.7% of main media spend - a figurehigher than some more established markets such as Belgium andItaly. Search accounts for half of Russia's online ad spend, followedby Display (34%) and Classifieds & Directories (16%).

Regional and country detailCentral and Eastern Europe

2009 Online Ad Spend €514 m2009 main media spend (WARC) €4,405 mOnline as a proportion of main media spend (WARC) 11.7%

2009 Online Ad Spend €296 m2008-2009 online ad spend growth 12.7%2009 main media spend (WARC) €2,210 m

Online as a proportion of main media spend (WARC) 13.4%

Although overall online ad spend is low in this region compared to Western Europe, three of the four fastest growing online marketthis region - Greece, Turkey and Poland.

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 24/4124

SloveniaSlovenia is the third smallest online advertising market in Europe,and the only one of these three markets to record growth, albeit onlof 1.6%. Proportionally it has the second largest Display market, at68% of online spend. Search accounts for 22% of spend, andClassifieds & Directories just 6%.

CroatiaThe value of the online advertising market in Croatia fell by 2.7% 2009, making it the second smallest market in Europe. However this a reasonable balance between formats with 39% spent on Display34% on Search and 29% on Classifieds & Directories.

RomaniaRomania is the smallest online advertising market in Europe, with just €13 million, representing a decline of 4.5% since 2008. It alsohas the smallest proportion of main media spend devoted to online, just 1.8%. Romania has the highest proportional spend on Display Europe, accounting for 94% of the total market. Search accounts fo4% and Classifieds & Directories just 0.1%.

TurkeyTurkey was the fourth fastest growing market in Europe in 2009,with a growth rate of 11.7%, and online already represents 9.2% ofmain media spend. Search accounts for 45% of online spend, followedby Display (31%) and Classifieds & Directories (25%).

HungaryAlthough the online advertising market in Hungary is one of thesmallest in Europe, the market value of €85 represents 10.1% of mainmedia spend. The market grew at just over the European average ratein 2009. 58% of online spend goes to Display advertising, followed atsome distance by Search (22%) and Classifieds & Directories (15%).

BulgariaThis is the first year Bulgaria has appeared in this report, so no trenddata is available. Online ad spend in Bulgaria accounts for just 6.2% ofmain media spend. Display is the dominant format, accounting for 57%of spend, followed by Search (27%) and Classifieds & Directories (16%).

Regional and country detailCentral and Eastern Europe

2009 Online Ad Spend €120 m2008-2009 online ad spend growth 11.7%2009 main media spend (WARC) €1,313 mOnline as a proportion of main media spend (WARC) 9.2%

2009 Online Ad Spend €25 m2009 main media spend (WARC) €395Online as a proportion of main media spend (WARC) 6.2%

2009 Online Ad Spend €85 m

2008-2009 online ad spend growth 6.8%2009 main media spend (WARC) €843 mOnline as a proportion of main media spend (WARC) 10.1%

2009 Online Ad Spend €24 m2008-2009 online ad spend growth -5.5%

2009 Online Ad Spend €21 m2008-2009 online ad spend growth 1.6%2009 main media spend (WARC) €305 mOnline as a proportion of main media spend (WARC) 6.7%

2009 Online Ad Spend €15 m2008-2009 online ad spend growth -2.7%2009 main media spend (WARC) €239 mOnline as a proportion of main media spend (WARC) 6.2%

IAB Europe AdEX 2009Published September 2010© IAB Europe

SlovakiaAt -5.5% Slovakia recorded the largest decline in online ad spend in2009. However, online still outperformed the advertising market as awhole, which declined by -32.7% in the same period. The majority of

online ad spend went towards Display (63%), followed by Classifieds& Directories (21%) and Search (15%).

2009 Online Ad Spend €13 m2008-2009 online ad spend growth -4.5%2009 main media spend (WARC) €710 mOnline as a proportion of main media spend (WARC) 1.8%

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 25/4125

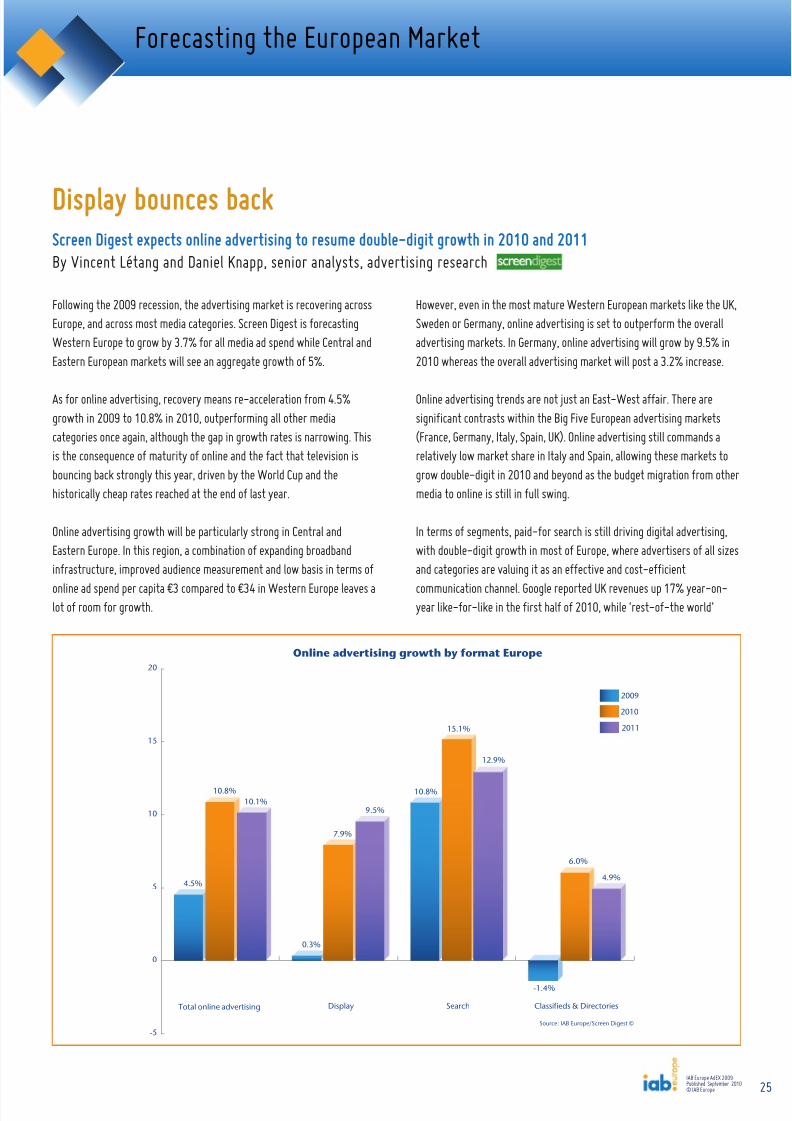

However, even in the most mature Western European markets like the USweden or Germany, online advertising is set to outperform the overalladvertising markets. In Germany, online advertising will grow by 9.5%2010 whereas the overall advertising market will post a 3.2% increase.

Online advertising trends are not just an East-West affair. There aresignificant contrasts within the Big Five European advertising markets(France, Germany, Italy, Spain, UK). Online advertising still commandrelatively low market share in Italy and Spain, allowing these markets tgrow double-digit in 2010 and beyond as the budget migration from otmedia to online is still in full swing.

In terms of segments, paid-for search is still driving digital advertising,with double-digit growth in most of Europe, where advertisers of all siand categories are valuing it as an effective and cost-efficient

communication channel. Google reported UK revenues up 17% year-oyear like-for-like in the first half of 2010, while ‘rest-of-the world’

Forecastingthe European Market

Screen Digest expects online advertising to resume double-digit growth in 2010 and 2011By Vincent Létang and Daniel Knapp, senior analysts, advertising research

Display bounces back

-5

0

5

10

15

20

2011

2010

2009

Classifieds & DirectoriesSearchDisplayTotal online advertising

Online advertising growth by format Europe

4.5%

10.8%10.1%

0.3%

7.9%

9.5%

10.8%

15.1%

12.9%

-1.4%

6.0%

4.9%

Source: IAB Europe/Screen Digest ©

IAB Europe AdEX 2009Published September 2010© IAB Europe

Following the 2009 recession, the advertising market is recovering acrossEurope, and across most media categories. Screen Digest is forecastingWestern Europe to grow by 3.7% for all media ad spend while Central andEastern European markets will see an aggregate growth of 5%.

As for online advertising, recovery means re-acceleration from 4.5%growth in 2009 to 10.8% in 2010, outperforming all other mediacategories once again, although the gap in growth rates is narrowing. Thisis the consequence of maturity of online and the fact that television isbouncing back strongly this year, driven by the World Cup and thehistorically cheap rates reached at the end of last year.

Online advertising growth will be particularly strong in Central andEastern Europe. In this region, a combination of expanding broadbandinfrastructure, improved audience measurement and low basis in terms of

online ad spend per capita €3 compared to €34 in Western Europe leaves alot of room for growth.

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 26/4126

Forecastingthe European Market

0

5

10

15

20

2011

2010

2009

UKSpainItalyGermanyFrance

2.2%

7.7%

12.0%

Total online advertising growth by country

7.5%

9.5%

5.2%

3.2%

13.6%

12.3%

7.1%

17.5%

11.5%

6.4%

9.5%

7.1%

Source: IAB Europe/Screen Digest ©

revenues were up 24%. Although we believe Google’s display formats andrevenues, non-European markets have grown even more strongly, ScreenDigest modelling suggests 2010 growth for paid-for search will bebetween 10% and 30% in continental Europe, and around 13% in the UK,despite the fact that the UK is one of the world’s most saturated searchmarket. Alongside Central and Eastern Europe, we expect Scandinaviancountries to experience the highest growth rates in search in the mid-term. In Scandinavia, strong online directories from the pre-Google erahave long hindered the rapid uptake of search advertising, but budgets areincreasingly migrating from directories to search.

However the main feature of internet advertising this year and next isprobably the perspective of renewed online display growth after a severeslowdown in 2009. This is part of a general return to brand advertising,also benefitting television and outdoor in particular, after almost twoyears of focusing on traffic and direct, ROI-oriented short termmarketing. Although CPMs and CPCs are flat or still going down in mostformat categories, many publishers are successful in limiting the erosionof ‘premium’ CPMs, while ‘remnant’ inventory is increasingly sold usingtargeting technologies that make it cost-efficient and attractive for somecategories of advertisers. Revenue growth is thus not generated by

increased prices in each format, but by the fact that the market’s centreof gravity is drifting towards higher-value formats like video, mobile,special high visibility banner formats and sponsorship. Networkconsolidation is also happening in most territories. It is welcomed by thbuying side, which likes to see fragmentation and transaction costs goindown and generating economies of scale in trading. Ad exchanges arecoming of age as the next step in display trading.

But traditional, CPM-based display still has room for growth, as manymainstream advertisers, for instance in FMCG who had delayed or slowdown their display uptake in 2009, are returning strongly this year. Theare further encouraged by the widespread availability of video inventormost notably catch-up pre-rolls which are often planned alongsidebroadcast TV, and the shift of video sharing sites towards professionalcontent consumption.

In 2010-2011, many mainstream global advertisers are also gearing uptheir use of social media, acknowledging user-friendly buying mechaniand the fact that 500 million Facebook users cannot be ignored by anyglobal brand. The 2010 FIFA World Cup was also the first time the inteplayed a massive role in global campaign alongside television.

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 27/4127

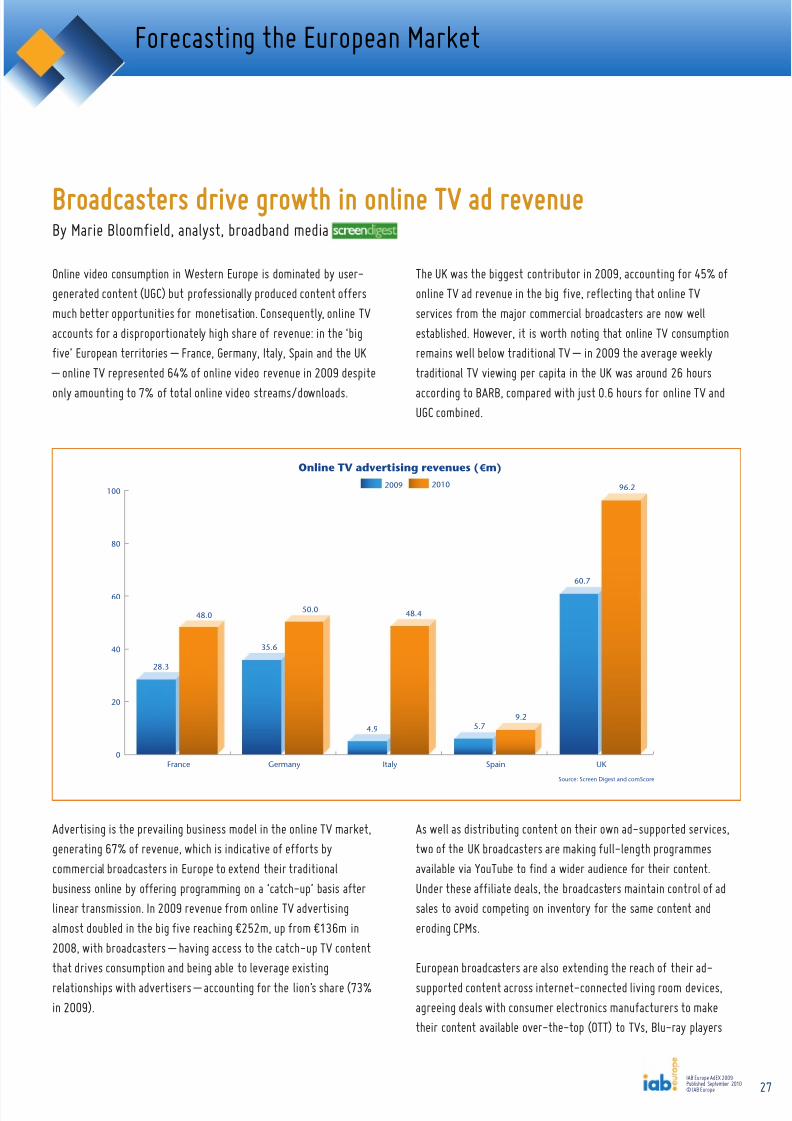

The UK was the biggest contributor in 2009, accounting for 45% oonline TV ad revenue in the big five, reflecting that online TVservices from the major commercial broadcasters are now wellestablished. However, it is worth noting that online TV consumptioremains well below traditional TV – in 2009 the average weeklytraditional TV viewing per capita in the UK was around 26 hours

according to BARB, compared with just 0.6 hours for online TV anUGC combined.

As well as distributing content on their own ad-supported services,two of the UK broadcasters are making full-length programmesavailable via YouTube to find a wider audience for their content.Under these affiliate deals, the broadcasters maintain control of adsales to avoid competing on inventory for the same content anderoding CPMs.

European broadcasters are also extending the reach of their ad-supported content across internet-connected living room devices,agreeing deals with consumer electronics manufacturers to maketheir content available over-the-top (OTT) to TVs, Blu-ray players

Online video consumption in Western Europe is dominated by user-generated content (UGC) but professionally produced content offersmuch better opportunities for monetisation. Consequently, online TVaccounts for a disproportionately high share of revenue: in the ‘bigfive’ European territories – France, Germany, Italy, Spain and the UK – online TV represented 64% of online video revenue in 2009 despite

only amounting to 7% of total online video streams/downloads.

Advertising is the prevailing business model in the online TV market,generating 67% of revenue, which is indicative of efforts bycommercial broadcasters in Europe to extend their traditionalbusiness online by offering programming on a ‘catch-up’ basis afterlinear transmission. In 2009 revenue from online TV advertisingalmost doubled in the big five reaching €252m, up from €136m in2008, with broadcasters – having access to the catch-up TV contentthat drives consumption and being able to leverage existingrelationships with advertisers – accounting for the lion’s share (73%in 2009).

Forecasting the European Market

By Marie Bloomfield, analyst, broadband mediaBroadcasters drive growth in online TV ad revenue

0

20

40

60

80

10020102009

UKSpainItalyGermanyFrance

28.3

48.0

35.6

50.0

4.9

48.4

5.79.2

60.7

96.2

Online TV advertising revenues ( € m)

Source: Screen Digest and comScore

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 28/41

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 29/4129

has trouble exiting the lucrative messaging ditch it carved for itselfLG and Samsung will play it safe with multiple operating systems;as for Microsoft and Palm/HP, 2010 is about restructuring an offerrather than a power demonstration.

Operator’s practices with data charging must also be kept in check avoid bill shock. Operators still have to deal with the schizophreniaoffering powerful advertising solutions and respecting the users’permissions/privacy/preferences. With search firmly within thegrasp of online incumbents and display following the same path,messaging remains a great opportunity for operators. However theyneed to work on allowing their inventories to open up, sinceadvertisers usually avoid dealing with operator fragmentation. In thlight, infrastructure vendors might have a substantial opportunity ifthey offer operators the right tools.

The year ahead promises more of the same consolidation, growth amaturation. We can expect operators and tech companies to keep onpreparing for the significant growth ahead, and mobile to integratefurther into advertisers’ digital advertising arsenal.

From a demand side perspective, the smartphone environment isbringing scale, creativity and usability. On top of being a great channfor CRM and social media and a return-channel for other media(typically TV), mobile advertising is now establishing itself in the

display and search environment. Some challenges remain however:fragmentation of standards and currencies; absence of independentthird-party ad-serving and reliance on operators for data and campaigreporting. In terms of audience measurement, the deal betweencomScore and GSMA to aggregate operators’ data on mobile internusage is a major breakthrough but it only applies in the UK so far.

The past 12 months have paved the way for a maturing period in mobile advertising. Can everyone win?

If there were any doubts last year about the strategic importance ofmobile in the future of advertising, they were most likely wiped clean

after the market events of the past 12 months.

After an important peak in funding in 2008, 2009 was more aboutventure exits and bigger players making their moves. Between July 2009and June 2010, mobile advertising saw at least 28 acquisition deals,twice the number of deals for the previous 12 months. If Google(AdMob) and Apple (Quattro Wireless) stood out, we should alsomention companies such as Orange (Unanimis), Nokia (Acuity Mobile) orVelti (Media Cannon) who were active and will likely continue to be so.

The consolidation in mobile advertising essentially underlines a pathtowards maturity for mobile advertising. Despite its small size (IABUK estimated mobile ad spend to be £38m i.e. around 1% of overalldigital media spend), mobile advertising seems to be taking off atlast in 2009: +32% year-on-year like-for-like in the UK in 2009.Now that formats and metrics have started to fall in place, now is thetime for scaling and increasing budgets. For advertisers, the keychallenge will become to cope with regional environments that mightprovide very different usages for the mobile device: for example,countries with a high smartphone penetration will be better suited for a

mobile app strategy, while emerging markets will still favour SMS.

Smartphone advertising in 2010-2011 will likely remain a two-horserace between Apple’s iAds and Google’s Android + AdMob combo.Nokia-backed Symbian doesn’t leverage its high shipment volumeseither from developer interest or user data consumption; BlackBerry

Forecastingthe European Market

By Julien Theys, senior analyst, mobile mediaMobile advertising comes of age

2008 2009 2010 2011 2012 2013 2014

Handset Shipments (m) 290 289.6 297.8 303.4 298.8 302.1 307.9Smartphone share of handset market 11.3% 14.8%19.8% 22.7% 26.2% 29.2% 32.5%

IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 30/4130

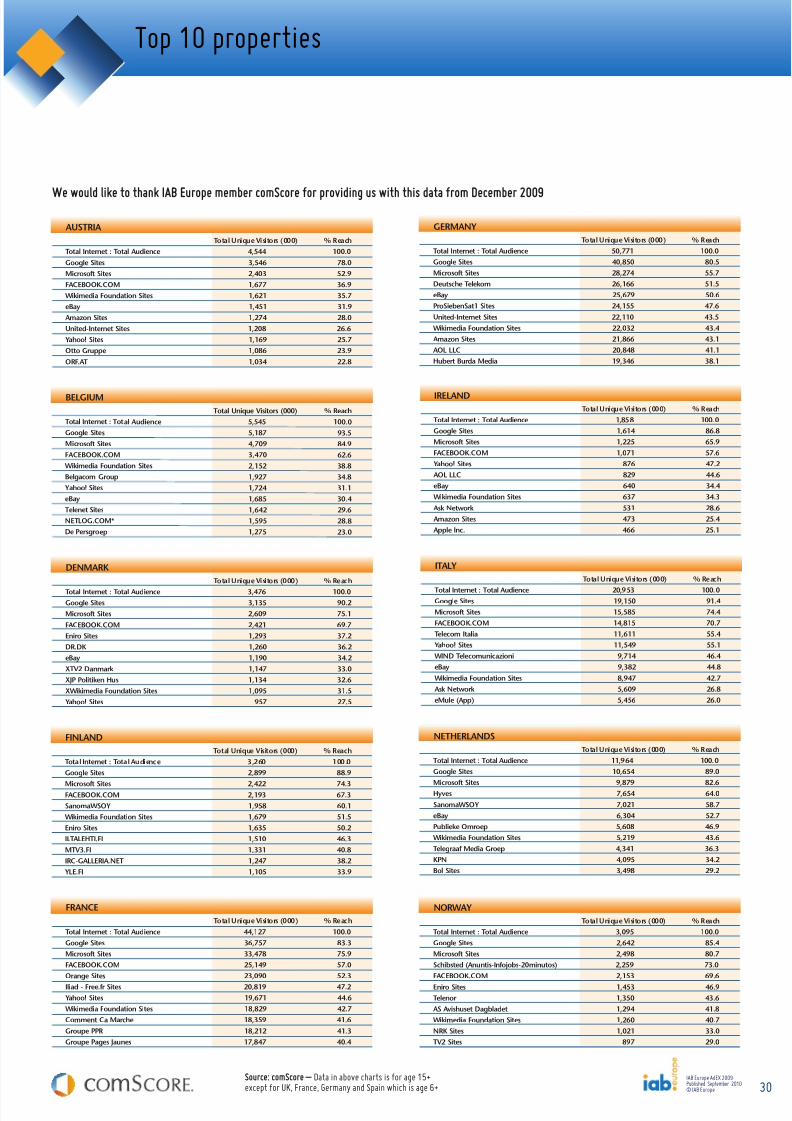

We would like to thank IAB Europe member comScore for providing us with this data from December 2009

Top 10 properties

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 4,544 100.0Google Sites 3,546 78.0Microsoft Sites 2,403 52.9FACEBOOK.COM 1,677 36.9Wikimedia Foundation Sites 1,621 35.7eBay 1,451 31.9Amazon Sites 1,274 28.0United-Internet Sites 1,208 26.6Yahoo! Sites 1,169 25.7Otto Gruppe 1,086 23.9ORF.AT 1,034 22.8

AUSTRIATotal Unique Visitors (000) % Reach

Total Internet : Total Audience 50,771 100.0Google Sites 40,850 80.5Microsoft Sites 28,274 55.7Deutsche Telekom 26,166 51.5eBay 25,679 50.6ProSiebenSat1 Sites 24,155 47.6United-Internet Sites 22,110 43.5Wikimedia Foundation Sites 22,032 43.4Amazon Sites 21,866 43.1AOL LLC 20,848 41.1Hubert Burda Media 19,346 38.1

GERMANY

Total Unique Visitors (000) % ReachTota l Internet : Tot al Audience 5,545 10 0.0Google Site s 5,187 93.5Microsoft Sites 4,709 84.9FACEBOOK.COM 3,470 62.6Wikimedia Foundation Sites 2,152 38.8Belgacom Group 1,927 34.8Yahoo! Sites 1,724 31.1eBay 1,685 30 .4Telenet Sites 1,642 29.6NETLOG.COM* 1,595 28 .8De Persgro ep 1,275 23.0

BELGIUM

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 1,858 100.0Google Sites 1,614 86.8Microsoft Sites 1,225 65.9FACEBOOK.COM 1,071 57.6Yahoo! Sites 876 47.2AOL LLC 829 44.6eBay 640 34.4Wikimedia Foundation Sites 637 34.3Ask Network 531 28.6Amazon Sites 473 25.4Apple Inc. 466 25.1

IRELAND

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 3,476 100.0Google Sites 3,135 90.2Microsoft Sites 2,609 75.1FACEBOOK.COM 2,421 69.7Eniro Sites 1,293 37.2DR.DK 1,260 36.2eBay 1,190 34.2XTV2 Danmark 1,147 33.0XJP Politiken Hus 1,134 32.6XWikimedia Foundation Sites 1,095 31.5Yahoo! Sites 957 27.5

DENMARKTotal Unique Visitors (000) % Reach

Total Internet : Total Audience 20,953 100.0Google Sites 19,150 91.4Microsoft Sites 15,585 74.4FACEBOOK.COM 14,815 70.7Telecom Italia 11,611 55.4Yahoo! Sites 11,549 55.1WIND Telecomunicazioni 9,714 46.4eBay 9,382 44.8Wikimedia Foundation Sites 8,947 42.7Ask Network 5,609 26.8eMule (App) 5,456 26.0

ITALY

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 3,260 100.0Google Sites 2,899 88.9

Microsoft Sites 2,422 74.3FACEBOOK.COM 2,193 67.3SanomaWSOY 1,958 60.1Wikimedia Foundation Sites 1,679 51.5Eniro Sites 1,635 50.2ILTALEHTI.FI 1,510 46.3MTV3.FI 1,331 40.8IRC-GALLERIA.NET 1,247 38.2YLE.FI 1,105 33.9

FINLAND

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 44,127 100.0Google Sites 36,757 83.3Microsoft Sites 33,478 75.9FACEBOOK.COM 25,149 57.0Orange Sites 23,090 52.3Iliad - Free.fr Sites 20,819 47.2Yahoo! Sites 19,671 44.6Wikimedia Foundation Sites 18,829 42.7Comment Ca Marche 18,359 41.6Groupe PPR 18,212 41.3Groupe Pages Jaunes 17,847 40.4

FRANCE

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 11,964 100.0Google Sites 10,654 89.0

Microsoft Sites 9,879 82.6Hyves 7,654 64.0SanomaWSOY 7,021 58.7eBay 6,304 52.7Publieke Omroep 5,608 46.9Wikimedia Foundation Sites 5,219 43.6Telegraaf Media Groep 4,341 36.3KPN 4,095 34.2Bol Sites 3,498 29.2

NETHERLANDS

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 3,095 100.0Google Sites 2,642 85.4Microsoft Sites 2,498 80.7Schibsted (Anuntis-Infojobs-20minutos) 2,259 73.0FACEBOOK.COM 2,153 69.6Eniro Sites 1,453 46.9Telenor 1,350 43.6AS Avishuset Dagbladet 1,294 41.8Wikimedia Foundation Sites 1,260 40.7NRK Sites 1,021 33.0TV2 Sites 897 29.0

NORWAY

IAB Europe AdEX 2009Published September 2010© IAB Europe

Source: comScore – Data in above charts is for age 15+except for UK, France, Germany and Spain which is age 6+

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 31/412531

Top 10 properties

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 21,637 100.0Google Sites 18,396 85.0

Microsoft Sites 17,082 78.9FACEBOOK.COM 10,671 49.3Yahoo! Sites 10,535 48.7Wikimedia Foundation Sites 8,934 41.3Grupo Prisa 8,635 39.9RCS Media Group 8,466 39.1Vocento 8,169 37.8Schibsted (Anuntis-Infojobs-20minutos) 7,949 36.7Terra - Telefonica 7,912 36.6

SPAIN

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 5,768 100.0Google Sites 5,302 91.9Microsoft Sites 4,951 85.8Schibsted (Anuntis-Infojobs-20minutos) 4,080 70.7FACEBOOK.COM 3,832 66.4Bonnierförlagen 3,074 53.3Eniro Sites 2,929 50.8Wikimedia Foundation Sites 2,327 40.3BLOGG.SE 2,229 38.6Swedbank 1,993 34.5Spotify 1,975 34.2

SWEDEN

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 4,519 100.0Google Sites 4,217 93.3Microsoft Sites 3,492 77.3FACEBOOK.COM 2,643 58.5Swisscom Sites 1,950 43.2Wikimedia Foundation Sites 1,891 41.8Yahoo! Sites 1,668 36.9Apple Inc. 1,504 33.3MIH Limited 1,337 29.6eBay 1,228 27.2Deutsche Telekom 1,189 26.3

SWITZERLAND

Total Unique Visitors (000) % Reach

Total Internet : Total Audience 20,579 100.0Google Sites 19,204 93.3Microsoft Sites 18,431 89.6FACEBOOK.COM 17,128 83.2Dogan Online 12,158 59.1Milliyet Group 9,213 44.8BLOGCU.COM 9,132 44.4Mynet A.S. 8,612 41.8Hurriyet Internet Group 8,193 39.8Nokta Internet Teknolojileri 7,723 37.5Wikimedia Foundation Sites 7,111 34.6

TURKEY

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 3,825 100.0Google Sites 3,572 93.4Microsoft Sites 3,428 89.6Portugal Telecom 2,385 62.3HI5.COM 2,252 58.9Yahoo! Sites 1,349 35.3UOL 1,320 34.5Wikimedia Foundation Sites 1,306 34.1Grupo Impresa 1,251 32.7iG Sites 1,202 31.4WordPress 1,154 30.2

PORTUGAL

Total Unique Visitors (000) % Reach

Total Internet : Total Audience 36,589 100.0Yandex 22,124 60.5Mail.Ru Sites 21,453 58.6Google Sites 19,451 53.2Vkontakte 17,127 46.8RosBusinessConsulting 16,023 43.8Rambler Media 13,875 37.9AOL LLC 13,714 37.5BitTorrent Network 10,651 29.1Microsoft Sites 10,309 28.2Wikimedia Foundation Sites 9,864 27.0

RUSSIA

Total Unique Visitors (000) % ReachTotal Internet : Total Audience 42,258 100.0Google Sites 38,944 92.2

Microsoft Sites 34,591 81.9FACEBOOK.COM 32,415 76.7Yahoo! Sites 25,650 60.7eBay 22,936 54.3BBC Sites 21,156 50.1Amazon Sites 19,101 45.2Wikimedia Foundation Sites 17,570 41.6Ask Network 16,993 40.2AOL LLC 15,739 37.2

UK

IAB Europe AdEX 2009Published September 2010© IAB Europe

Source: comScore – Data in above charts is for age 15+except for UK, France, Germany and Spain which is age 6+

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 32/412632

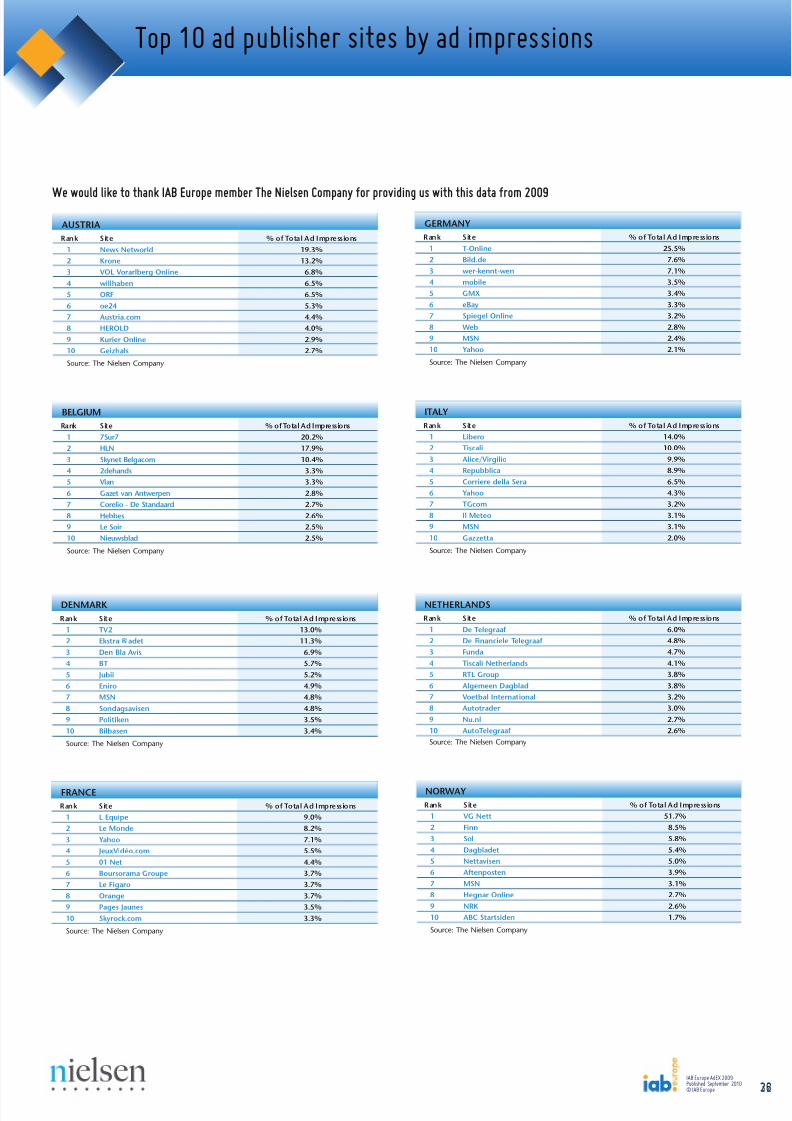

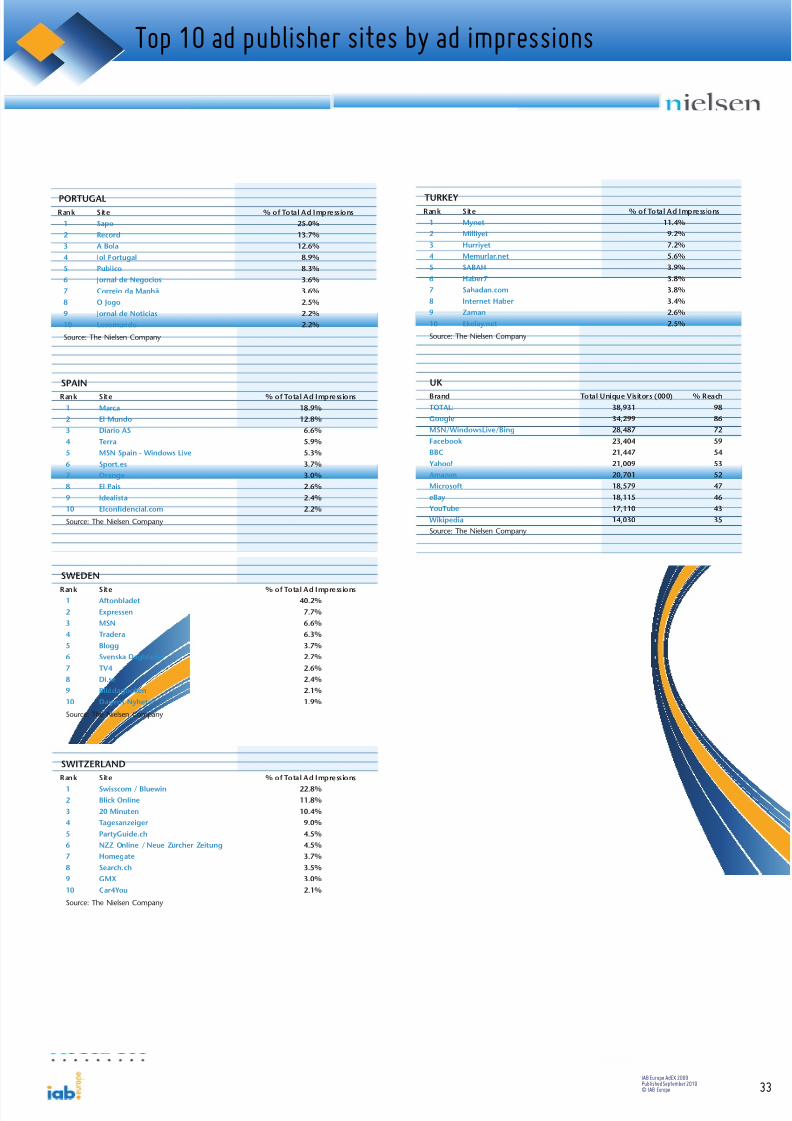

We would like to thank IAB Europe member The Nielsen Company for providing us with this data from 2009

Top 10 ad publisher sites by ad impressions

Rank Site % of Total Ad Impressions1 News Networld 19.3%2 Krone 13.2%3 VOL Vorarlberg Online 6.8%4 willhaben 6.5%5 ORF 6.5%6 oe24 5.3%7 Austria.com 4.4%8 HEROLD 4.0%9 Kurier Online 2.9%10 Geizhals 2.7%

Source: The Nielsen Company

AUSTRIARank Site % of Total Ad Impressions

1 T-Online 25.5%2 Bild.de 7.6%3 wer-kennt-wen 7.1%4 mobile 3.5%5 GMX 3.4%6 eBay 3.3%7 Spiegel Online 3.2%8 Web 2.8%9 MSN 2.4%10 Yahoo 2.1%

Source: The Nielsen Company

GERMANY

Rank Site % of Total Ad Impressions1 7Sur7 20.2%2 HLN 17.9%3 Skynet Belgacom 10.4%4 2dehands 3.3%5 Vlan 3.3%6 Gazet van Antwerpen 2.8%7 Corelio - De Standaard 2.7%8 Hebbes 2.6%9 Le Soir 2.5%10 Nieuwsblad 2.5%

Source: The Nielsen Company

BELGIUMRank Site % of Total Ad Impressions

1 Libero 14.0%2 Tiscali 10.0%3 Alice/Virgilio 9.9%4 Repubblica 8.9%5 Corriere della Sera 6.5%6 Yahoo 4.3%7 TGcom 3.2%8 Il Meteo 3.1%9 MSN 3.1%10 Gazzetta 2.0%

Source: The Nielsen Company

ITALY

Rank Site % of Total Ad Impressions1 TV2 13.0%2 Ekstra Bladet 11.3%3 Den Bla Avis 6.9%4 BT 5.7%5 Jubii 5.2%6 Eniro 4.9%7 MSN 4.8%8 Sondagsavisen 4.8%9 Politiken 3.5%10 Bilbasen 3.4%

Source: The Nielsen Company

DENMARKRank Site % of Total Ad Impressions

1 De Telegraaf 6.0%2 De Financiele Telegraaf 4.8%3 Funda 4.7%4 Tiscali Netherlands 4.1%5 RTL Group 3.8%6 Algemeen Dagblad 3.8%7 Voetbal International 3.2%8 Autotrader 3.0%9 Nu.nl 2.7%10 AutoTelegraaf 2.6%Source: The Nielsen Company

NETHERLANDS

Rank Site % of Total Ad Impressions1 L Equipe 9.0%2 Le Monde 8.2%3 Yahoo 7.1%4 JeuxVidéo.com 5.5%5 01 Net 4.4%6 Boursorama Groupe 3.7%7 Le Figaro 3.7%8 Orange 3.7%9 Pages Jaunes 3.5%10 Skyrock.com 3.3%

Source: The Nielsen Company

FRANCE

IAB Europe AdEX 2009Published September 2010© IAB Europe

Rank Site % of Total Ad Impressions1 VG Nett 51.7%2 Finn 8.5%3 Sol 5.8%4 Dagbladet 5.4%5 Nettavisen 5.0%6 Aftenposten 3.9%7 MSN 3.1%8 Hegnar Online 2.7%9 NRK 2.6%10 ABC Startsiden 1.7%

Source: The Nielsen Company

NORWAY

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 33/4133

Top 10 ad publisher sites by ad impressions

Rank Site % of Total Ad Impressions1 Mynet 11.4%2 Milliyet 9.2%3 Hurriyet 7.2%4 Memurlar.net 5.6%5 SABAH 3.9%6 Haber7 3.8%7 Sahadan.com 3.8%8 Internet Haber 3.4%9 Zaman 2.6%10 Ekolay.net 2.5%

Source: The Nielsen Company

TURKEYRank Site % of Total Ad Impressions

1 Sapo 25.0%2 Record 13.7%3 A Bola 12.6%4 Iol Portugal 8.9%5 Publico 8.3%6 Jornal de Negocios 3.6%7 Correio da Manhã 3.6%8 O Jogo 2.5%9 Jornal de Noticias 2.2%10 Losomundo 2.2%

Source: The Nielsen Company

PORTUGAL

Rank Site % of Total Ad Impressions1 Marca 18.9%2 El Mundo 12.8%3 Diario AS 6.6%4 Terra 5.9%5 MSN Spain - Windows Live 5.3%6 Sport.es 3.7%7 Orange 3.0%8 El Pais 2.6%9 Idealista 2.4%10 Elconfidencial.com 2.2%

Source: The Nielsen Company

SPAIN

Rank Site % of Total Ad Impressions1 Aftonbladet 40.2%2 Expressen 7.7%3 MSN 6.6%4 Tradera 6.3%5 Blogg 3.7%6 Svenska Dagbladet 2.7%7 TV4 2.6%8 Di.se 2.4%9 Bilddagboken 2.1%10 Dagens Nyheter 1.9%

Source: The Nielsen Company

SWEDEN

Rank Site % of Total Ad Impressions1 Swisscom / Bluewin 22.8%2 Blick Online 11.8%3 20 Minuten 10.4%4 Tagesanzeiger 9.0%5 PartyGuide.ch 4.5%6 NZZ Online / Neue Zürcher Zeitung 4.5%7 Homegate 3.7%8 Search.ch 3.5%9 GMX 3.0%10 Car4You 2.1%

Source: The Nielsen Company

SWITZERLAND

IAB Europe AdEX 2009Published September 2010© IAB Europe

Brand Total Unique Visitors (000) % ReachTOTAL: 38,931 98Google 34,299 86MSN/WindowsLive/Bing 28,487 72Facebook 23,404 59BBC 21,447 54Yahoo! 21,009 53Amazon 20,701 52Microsoft 18,579 47eBay 18,115 46YouTube 17,110 43Wikipedia 14,030 35Source: The Nielsen Company

UK

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 34/41

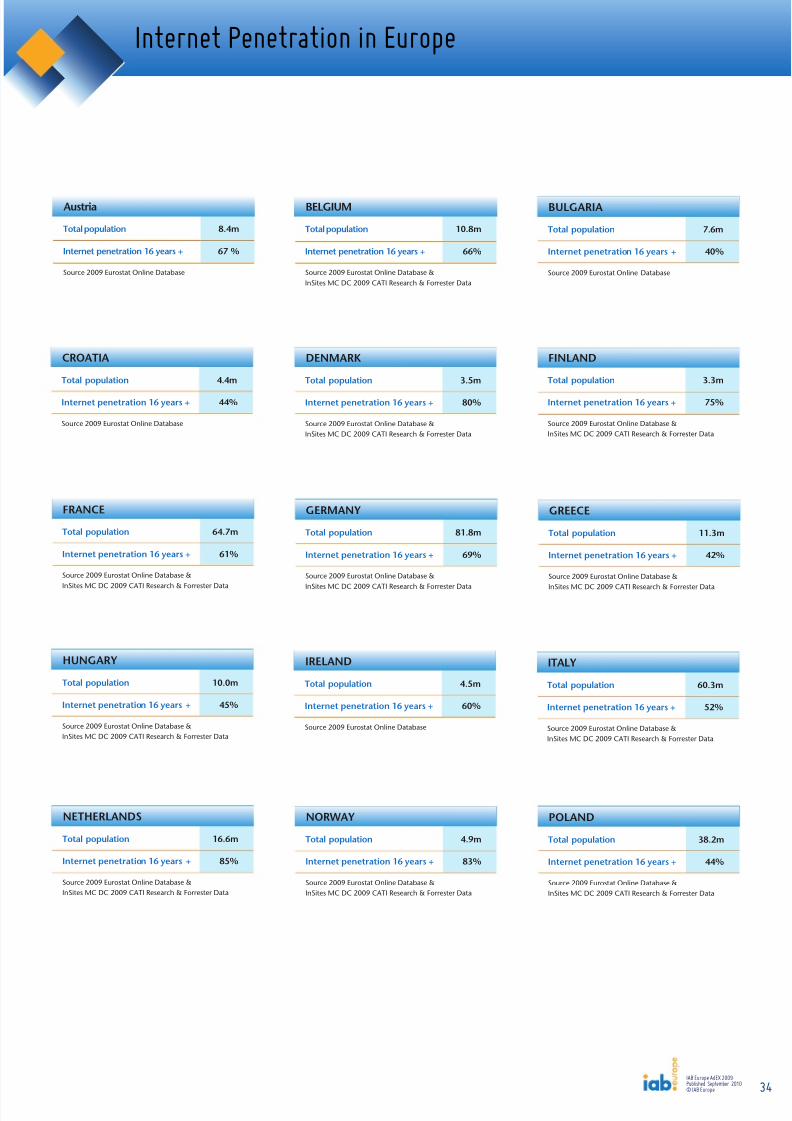

Internet Penetration in Europe

Total population 8.4m

Internet penetration 16 years + 67 %

Source 2009 Eurostat Online Database

Austria

Total population 10.8m

Internet penetration 16 years + 66%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

BELGIUM

Total population 7.6m

Internet penetration 16 years + 40%

Source 2009 Eurostat Online Database

BULGARIA

Total population 3.5m

Internet penetration 16 years + 80%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

DENMARK

Total population 3.3m

Internet penetration 16 years + 75%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

FINLAND

Total population 64.7m

Internet penetration 16 years + 61%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

FRANCE

Total population 81.8m

Internet penetration 16 years + 69%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

GERMANY

Total population 11.3m

Internet penetration 16 years + 42%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

GREECE

Total population 10.0m

Internet penetration 16 years + 45%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

HUNGARY

Total population 4.5m

Internet penetration 16 years + 60%

Source 2009 Eurostat Online Database

IRELAND

Total population 60.3m

Internet penetration 16 years + 52%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

ITALY

Total population 16.6m

Internet penetration 16 years + 85%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

NETHERLANDS

Total population 4.9m

Internet penetration 16 years + 83%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

NORWAY

Total population 38.2m

Internet penetration 16 years + 44%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

POLAND

34IAB Europe AdEX 2009Published September 2010© IAB Europe

Total population 4.4m

Internet penetration 16 years + 44%

Source 2009 Eurostat Online Database

CROATIA

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 35/41

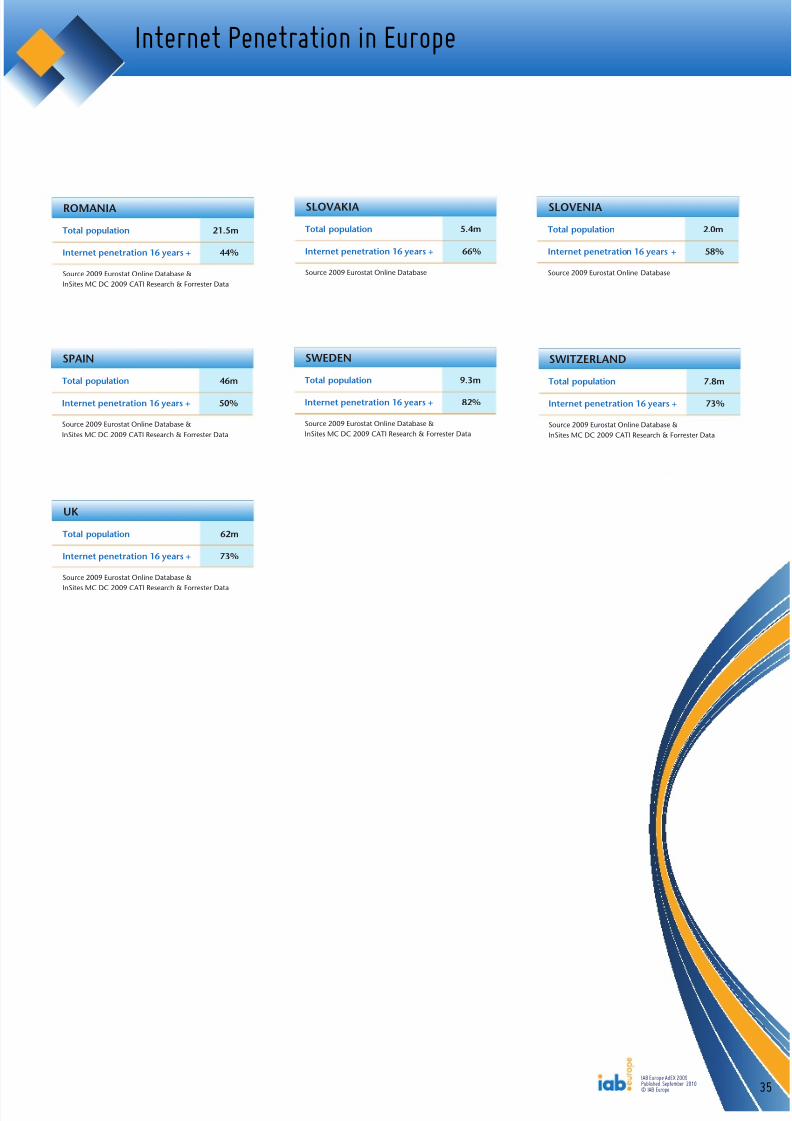

Internet Penetration in Europe

Total population 5.4m

Internet penetration 16 years + 66%

Source 2009 Eurostat Online Database

SLOVAKIA

Total population 2.0m

Internet penetration 16 years + 58%

Source 2009 Eurostat Online Database

SLOVENIA

Total population 46m

Internet penetration 16 years + 50%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

SPAIN

Total population 9.3m

Internet penetration 16 years + 82%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

SWEDEN

Total population 7.8m

Internet penetration 16 years + 73%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

SWITZERLAND

Total population 62m

Internet penetration 16 years + 73%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

UK

35IAB Europe AdEX 2009Published September 2010© IAB Europe

Total population 21.5m

Internet penetration 16 years + 44%

Source 2009 Eurostat Online Database &

InSites MC DC 2009 CATI Research & Forrester Data

ROMANIA

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 36/41

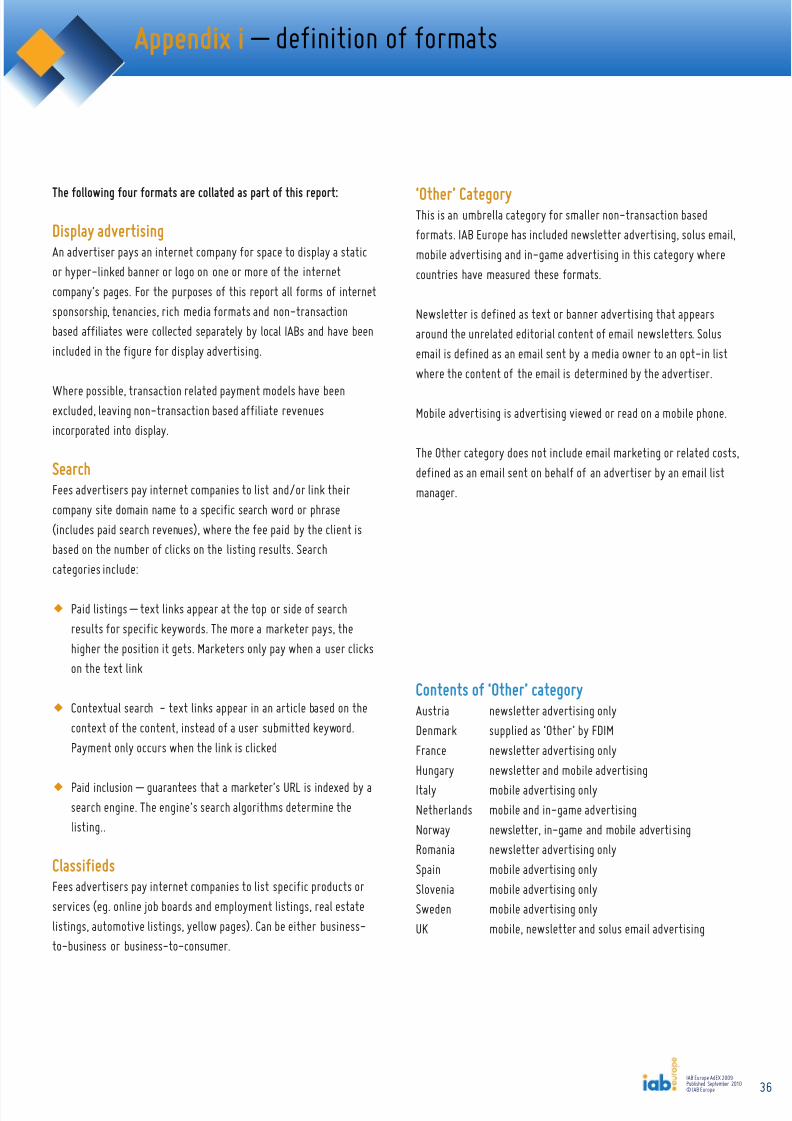

Appendix i – definition of formats

The following four formats are collated as part of this report:

Display advertisingAn advertiser pays an internet company for space to display a staticor hyper-linked banner or logo on one or more of the internetcompany’s pages. For the purposes of this report all forms of internetsponsorship, tenancies, rich media formats and non-transactionbased affiliates were collected separately by local IABs and have beenincluded in the figure for display advertising.

Where possible, transaction related payment models have beenexcluded, leaving non-transaction based affiliate revenuesincorporated into display.

SearchFees advertisers pay internet companies to list and/or link theircompany site domain name to a specific search word or phrase(includes paid search revenues), where the fee paid by the client isbased on the number of clicks on the listing results. Searchcategories include:

w Paid listings – text links appear at the top or side of searchresults for specific keywords. The more a marketer pays, thehigher the position it gets. Marketers only pay when a user clickson the text link

w Contextual search - text links appear in an article based on thecontext of the content, instead of a user submitted keyword.Payment only occurs when the link is clicked

w Paid inclusion – guarantees that a marketer’s URL is indexed by asearch engine. The engine’s search algorithms determine thelisting..

ClassifiedsFees advertisers pay internet companies to list specific products orservices (eg. online job boards and employment listings, real estatelistings, automotive listings, yellow pages). Can be either business-to-business or business-to-consumer.

‘Other’ CategoryThis is an umbrella category for smaller non-transaction basedformats. IAB Europe has included newsletter advertising, solus emmobile advertising and in-game advertising in this category wherecountries have measured these formats.

Newsletter is defined as text or banner advertising that appearsaround the unrelated editorial content of email newsletters. Solusemail is defined as an email sent by a media owner to an opt-in listwhere the content of the email is determined by the advertiser.

Mobile advertising is advertising viewed or read on a mobile phone

The Other category does not include email marketing or related cosdefined as an email sent on behalf of an advertiser by an email listmanager.

Contents of ‘Other’ categoryAustria newsletter advertising onlyDenmark supplied as ‘Other’ by FDIMFrance newsletter advertising onlyHungary newsletter and mobile advertisingItaly mobile advertising onlyNetherlands mobile and in-game advertisingNorway newsletter, in-game and mobile advertisingRomania newsletter advertising onlySpain mobile advertising onlySlovenia mobile advertising onlySweden mobile advertising onlyUK mobile, newsletter and solus email advertising

36IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 37/41

Appendix ii – The ParticipatingIABs

IAB Austriawww.iab-austria.atPartner: Focus MR

IAB Belgiumwww.iab-belgium.beSource: CIM

IAB Chapter in Bulgaria(Interactive Association)www.iabulgaria.bg

IAB Chapter in Croatia(INAMA)www.inama.hrSource: PricewaterhouseCoopers

IAB Chapter in Denmark(FDIM)www.fdim.dkPartner: Deloitte

IAB Finlandwww.iab.fi

Partner: TNS Gallup Oy Media Intelligence

IAB Francewww.iabfrance.comPartner: France Pub

IAB Chapter in Germany(OVK)www.bvdw.orgPartner: Nielsen Media Research

IAB Greecewww.iab.gr

IAB Hungarywww.iab.huPartner: PricewaterhouseCoopers

IAB Irelandwww.iabireland.iePartner: PricewaterhouseCoopers Ireland

IAB Italywww.iab.itPartner: Assointernet/Nielsen Media Research

IAB Netherlandswww.iab.nlPartner: Nielsen Media Research

IAB Chapter in Norwaywww. inma.noPartner: ANFA

IAB Polandwww.iabpolska.plPartner: PricewaterhouseCoopers Poland

IAB Romaniawww.iab-romania.roPartner: PricewaterhouseCoopers Romania

IAB Russiawww.iabrus.ruPartner: Russian Association of Communication Agencies

IAB Chapter in Slovakia(AIM)

www.aimsr.skSource: Mediana

IAB Sloveniawww.soz.si

IAB Spainwww.iabspain.netPartner: PricewaterhouseCoopers

IAB Swedenwww.iabsverige.seSource: IRM

IAB SwitzerlandSource: MediaFocus

IAB Turkeywww.iab-turkiye.orgPartner: Turkish Advertising Agencies Association

IAB UKwww.iabuk.netPartner: PricewaterhouseCoopers

37IAB Europe AdEX 2009Published September 2010© IAB Europe

8/8/2019 AdEx 2009 - European online advertising expenditure

http://slidepdf.com/reader/full/adex-2009-european-online-advertising-expenditure 38/41

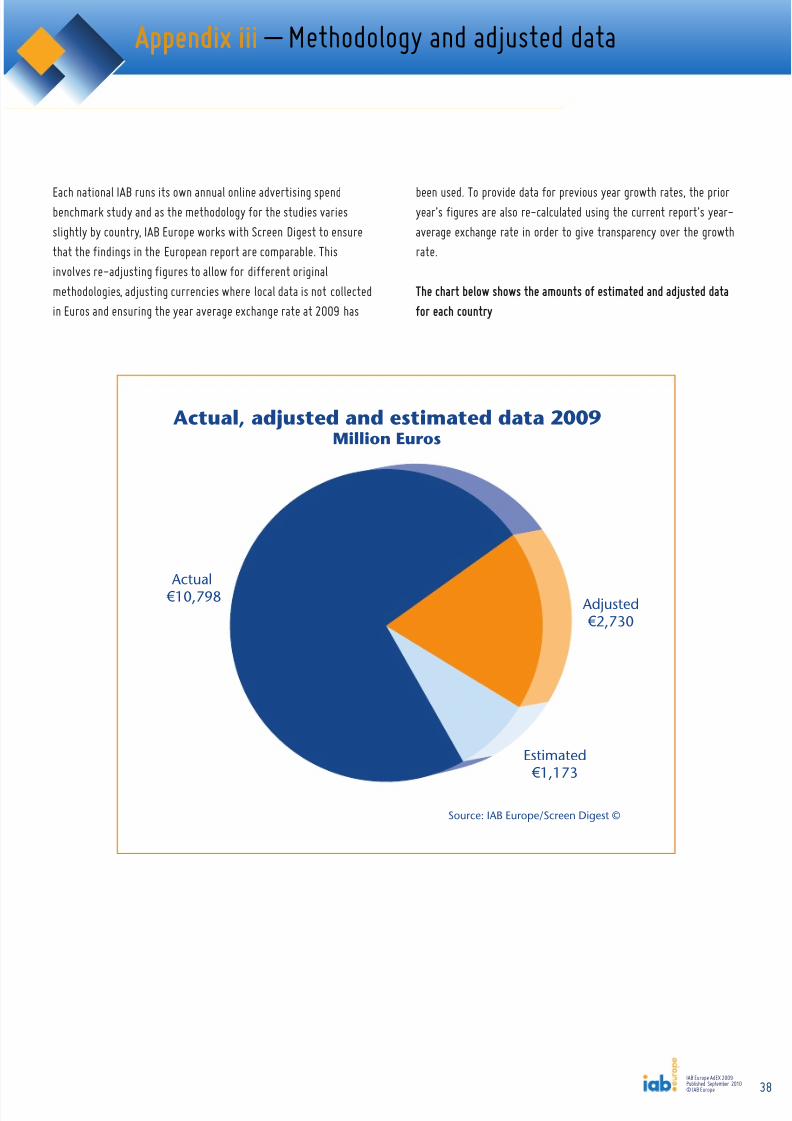

Appendix iii – Methodology and adjusted data