Embed Size (px)

Citation preview

1

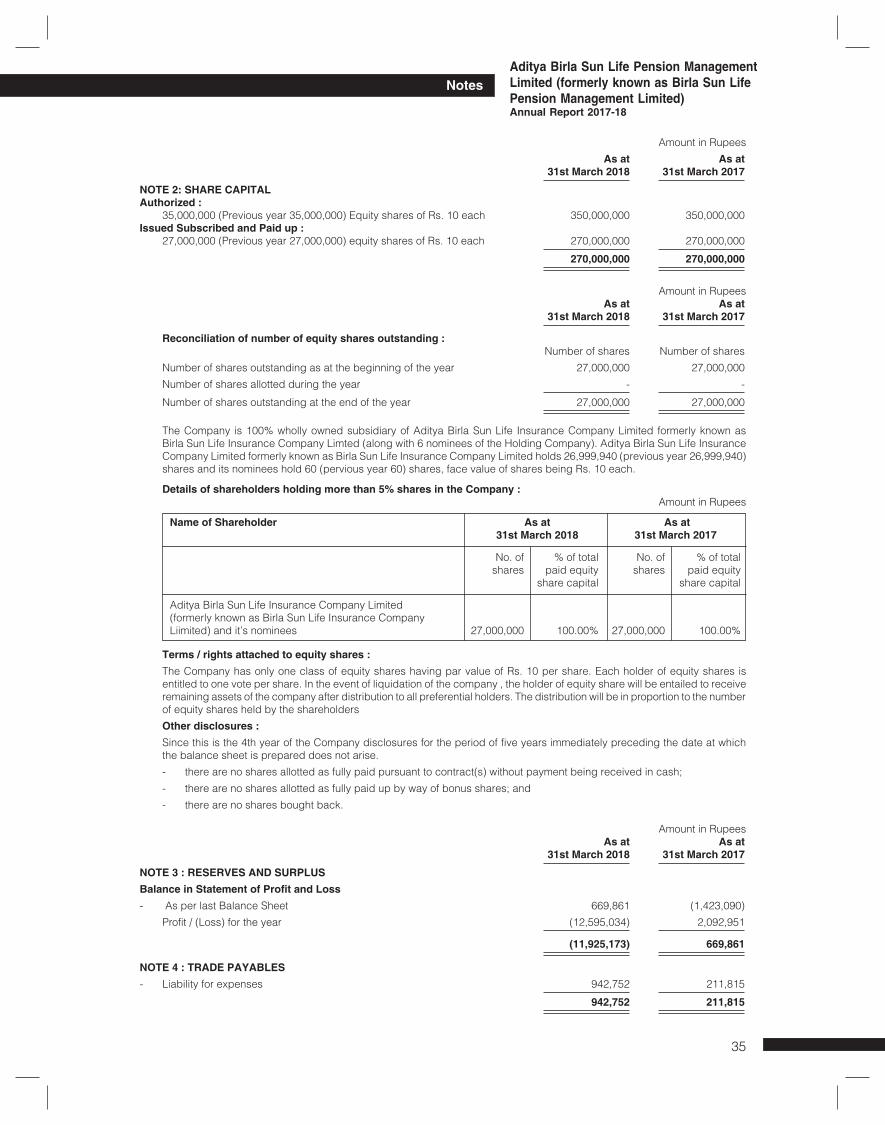

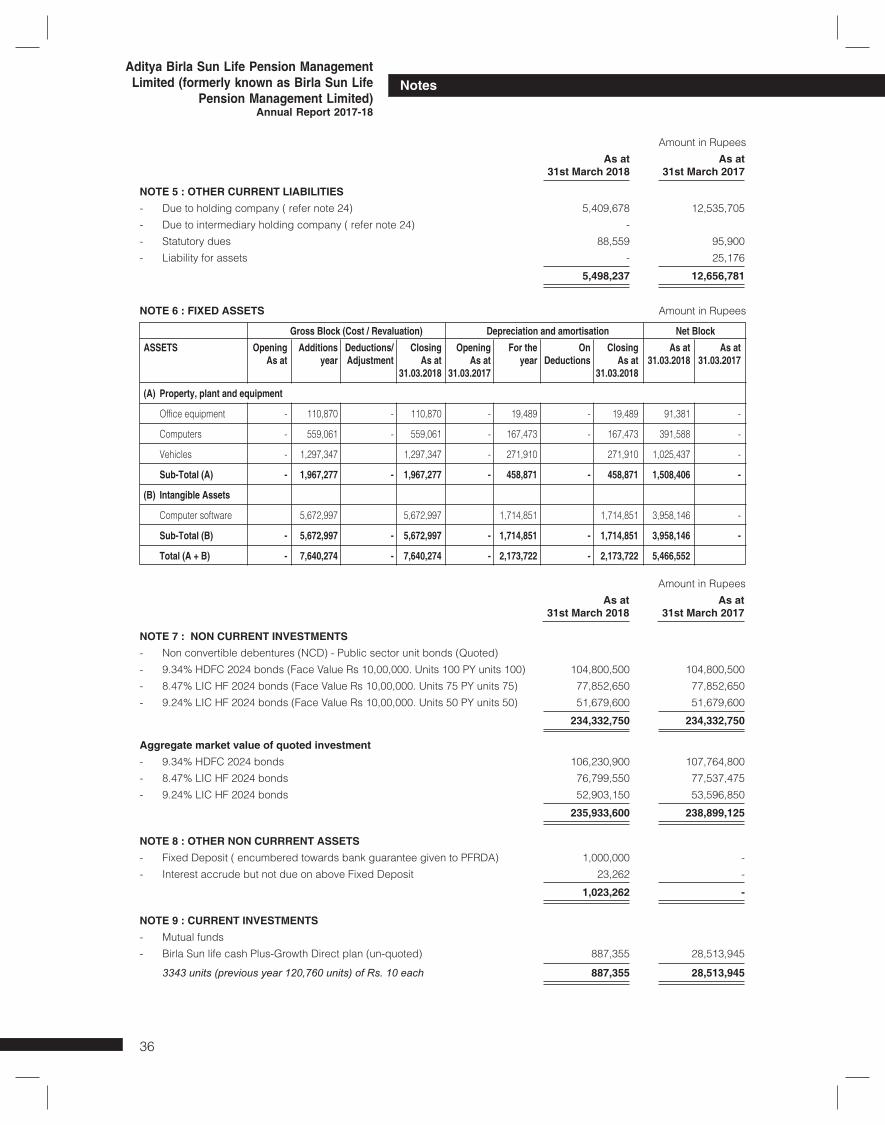

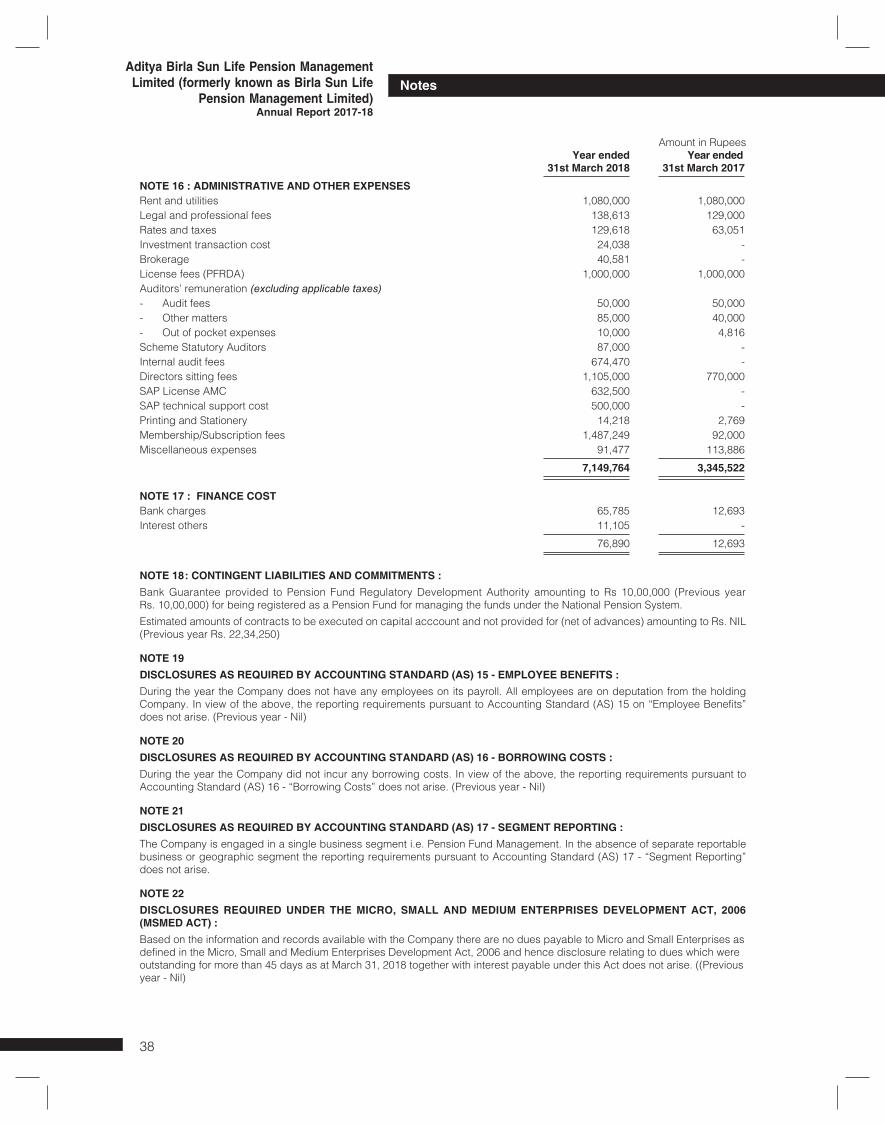

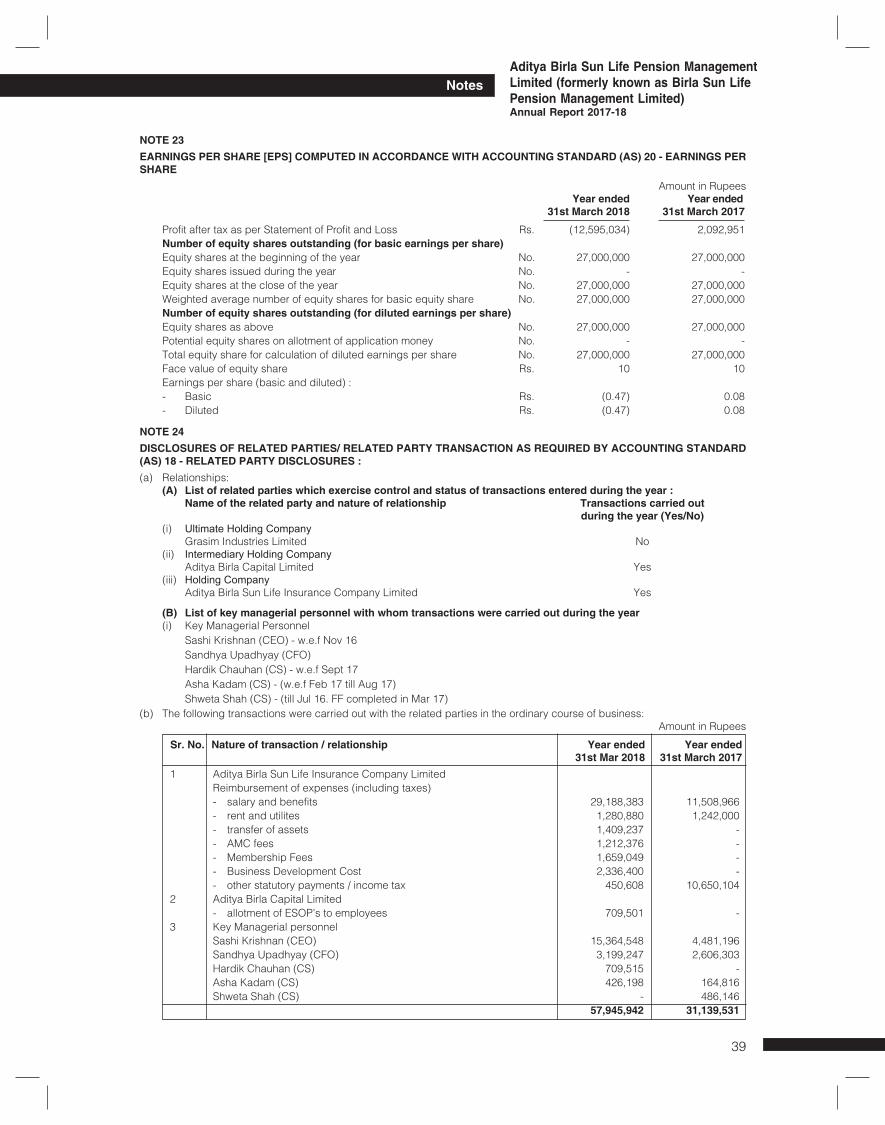

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

Board’s ReportDear Shareholders,The Board of Directors of Aditya Birla Sun Life Pension Management Limited (Formerly known as Birla Sun Life Pension Management Limited) (“your Company” or “the Company” or “ABSLPML”) are pleased to present the Fourth Annual Report and the audited financial statements of your Company for the financial year ended March 31, 2018.

OVERVIEW OF GLOBAL ECONOMYThe world economy gained momentum witnessing its strongest, most broad-based and synchronised growth uptick since the global financial crisis. Most regions of the world including major economies of US, Euro zone, China and Japan witnessed growth acceleration. Moreover, world trade also picked up smartly despite the growing fear of protectionism.

Despite the beginning of gradual withdrawal of extraordinary monetary accommodation by US Federal Reserve, other major central bankers continued to increase their already large asset holdings, which underpinned continuation of easy financial conditions. Business and consumer confidence remained strong, global PMIs rallied and there was a pick-up in investments.

Our baseline expectation is that the global economy will continue to show steady expansion in 2018-19 and grow at a rate closer to IMF’s forecast of 3.9%. The key risks to the global economy are sharp escalation in trade protectionism, geo-political tensions, sharp rise in global bond yield sand inflation.

The Indian economy started FY18 amidst challenges posed by balance sheet deleveraging, the impact of demonetisation, and GST. Growth in 1QFY18 was the lowest in 13 quarters at 5.7%. However, the economy picked up thereafter, growing steadily through the year and is expected to have grown at ~6.5% in FY18. Besides the headline numbers, the composition of growth was quite positive with pickup in manufacturing and capital formation, which reflect the beginning of revival in the investment cycle. A variety of data points like IIP, infrastructure index, PMI, auto sales, cement consumption, and non-oil non-gold imports attested to the broad based pickup in growth momentum. Indian equities reflected the growth uptick, rallying along with global equity markets.

Inflation remained well contained except for a brief uptick in food inflation in Nov-Jan period.

Board’s Report

Average inflation in FY18 was 3.6%, lower than RBI’s target of 4%, despite the statistical impact of pay commission HRA award on headline inflation. Core inflation remained well contained. However, there is an upside risk to inflation in FY19 owing to the likely impact of higher MSP, higher crude price, growth uptick and some weakness in INR. Bond yields started to rise from August owing to the uptick in growth, some fiscal slippage, and prospect of higher inflation down the line.

Indian external account was well funded with healthy BoP surplus, owing to strong foreign capital flows even as current account deficit witnessed some increase towards the second half of the fiscal. Forex reserves rose by US$54 bn and stood at US$424 bn, giving a healthy import cover of 10.5 month. INR appreciated to sub-64 levels against USD before moving to 65 levels towards the end of the fiscal.

We remain positive about growth prospects in FY19 and expect economic growth to rise to 7.25%. The last few years have been one of structural reforms (eg GST and Banking reforms) and macro-stabilisation (lower twin deficits and higher real rates) for Indian economy. This has laid the foundation for a sustained and durable growth recovery and made the economy much better positioned to withstand domestic and global shocks. We believe that the economy is now moving from stabilization to recovery phase, and is on course to a healthy cyclical recovery.

Market OutlookEquityThe NSE NIFTY gave a return of 10.25% in FY18, ending the year at a level of 10,114 after touching a peak of 11,130 on January 29th 2018. Equity market rallied in the first three quarters, as economic activity picked up and corporate earnings showed a healthy double digit growth. Markets corrected in the last quarter Q4FY18, on account global trade tensions and rising oil prices. We expect markets to be range bound for a large part of 2018-19 as the contraction of the price earning multiple will continue. A normal monsoon, resolution of the NPA problems plaguing banks and improving macros sans positives for the market. Uncertainty on account global trade tensions, rising oil prices and political rhetoric in the run up to the 2019 general elections may pose challenges.

2

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Fixed IncomeThe 10 year Indian Government Bond yield moved up 72 bps in the year, from 6.68% to 7.40% as on March 31, 2018. Interest rates hardened due to a number of factors including (i) the continuing stress in the banking sector (ii) fiscal slippage and (iii) hardening global interest rates. Interest rates across the world moved up in FY18, with the US Fed raising policy rates by 75bps in 2017 and 25bps in 2018 and a further rise of another 50 bps point more expected in 2018. CPI inflation in India has come down to 4.28% in March 2018, after touching a high of 5.21% in December 2017. RBI projects the CPI for the FY18-19 at around 4.5% and thus it looks unlikely that RBI will hike rates in 2018. We expect the 10year G-sec rate to remain in the 7.25%-7.60% range in the first half of 2018-19. The 10 year G-sec could probably trade higher in the second half, given that the risk of lower GST collections may result in higher second half borrowings and that global tightening may continue.

Financial PerformanceThe income generated by the Company during the year under review is from the management of the Pension Fund and Investments made of the Shareholders’ Fund. The Company’s financial performance for the year ended March 31, 2018 is summarized below:

(` in crore)

Particulars 2017-18 2016-17

Total Revenue 2.4 2.4

Total Expenses 3.7 1.3

Profit / (Loss) before tax -1.25 1.09

Tax Expense 0.01 0.88

Profit/(Loss) after tax -1.26 0.21

Transfer to General Reserve

0 0

Balance carried to Balance Sheet

-1.26 0.21

Earnings per share -0.47 0.08

Accounting MethodThe Company has prepared the financial statements as per I-GAAP (Indian Generally accepted accounting principles). Since, the accounts of the Company are consolidated with Grasim Industries Limited (GIL) the ultimate Holding Company, to which Ind-AS applies, the Company has also prepared and submitted to GIL the financial statements in Ind-AS format for FY18.

Key highlights of the Company:The Company closed the fiscal with AUM of ` 29.44/- crores and gained the lead position in scheme E & C Tier I in FYTD ranking. The Company also secured 2nd rank in scheme E & C Tier II in FYTD ranking.

ReservesYour directors do not propose any amount to be carried to Reserves.

DividendYour Directors do not recommend any dividend for the year ended March 31, 2018.

Change in the Name of the CompanyDuring the year, the name of the Company was changed from Birla Sun Life Pension Management Limited to Aditya Birla Sun Life Pension Management Limited vide Fresh Certificate of Incorporation pursuant to change of the name of Company dated August 3, 2017 issued by Registrar of Companies, Mumbai, Maharashtra.

Share CapitalThe Authorised Share Capital of the Company is ` 35 crore. The Issued, Subscribed and Paid up share Capital of the Company is ` 27 crore as on March 31, 2018.

Deposits During the year under review, the Company has not accepted any deposit from the public falling within the ambit of section 73 of the Companies Act, 2013 and The Companies (Acceptance of Deposits) Rules, 2014.

Particulars of Loans given, investment made, guarantees given or security provided under Section 186 of the Companies Act, 2013During the year under review, no Loans, Guarantees and Investments were made by the Company pursuant to Section 186 of the Companies Act, 2013.

Conservation of Energy & Technology Absorption The Company has no particulars to report as required under the provisions of Section 134(3) (m) of the Companies Act, 2013 in respect of conservation of energy and technology absorption considering the nature of activities undertaken by the Company during the year under review.

Board’s Report

3

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

Foreign Exchange earnings and expenditure during the year:There were no foreign exchange earnings and expenditure during the year.

Material Changes and Commitment affecting Financial Position of the CompanyThere are no material changes and commitments, affecting the financial position of the Company which has occurred between the end of the financial year of the Company i.e. March 31, 2018 and the date of this Board’s report.

Significant and material orders passed by the Regulators or Courts or TribunalsNo significant or material orders were passed by the Regulators or Courts or Tribunals which impact the going concern status and Company’s operations in future.

Change in Nature of Business During the year under review, there has been no change in the nature of business of the Company.

Employees Stock Option Scheme 2017The Aditya Birla Capital Limited Employee Stock Option Scheme (the “Scheme 2017”) has been formulated by the Nomination, Remuneration and Compensation Committee of the Board of Directors of Aditya Birla Capital Limited (ABCL), the Holding Company, with an aim to provide competitive remuneration opportunities to its employees and further by way of a separate special resolution, the shareholders of ABCL at their AGM held on July 19, 2017, extended the benefits and coverage of the Scheme 2017 to the employees of ABCL’s Subsidiary Companies.

The Nomination and Remuneration Committee and the Board of Directors of the Company had adopted the Scheme 2017 and had approved the extension of benefits of the Scheme 2017 to its permanent employees in the management cadre, including Managing and Whole-time Directors of the Company. The Scheme 2017 inter-alia involves the granting of employee stock options in the form of options (“Options”) and/or Restricted Stock Units (“RSUs”), which will be exercisable into equity shares of ¹ 10/- each of the Holding Company (the “Equity Shares”) in accordance with the terms of the Scheme 2017 and on such terms and conditions as may be fixed or determined by the Board and/or by Aditya Birla Capital Limited in accordance with the SEBI SBEB Regulations or other provisions of the law as may be prevailing at that time.

The approval for extension of benefits of Scheme 2017 as well as the payment of ESOP charge for the allocation of Options and RSU’s as applicable has also been approved by the shareholders of the Company at its EOGM held on August 10, 2017.

Consequently 61,920 Stock Options and 4,500 RSUs were granted in terms of the provisions of the Scheme 2017.

Holding and Subsidiaries During the year under review, a Composite Scheme of Arrangement (“Scheme”) was entered between Aditya Birla Nuvo Limited (“ABNL”), Grasim Industries Limited (“Grasim”) and Aditya Birla Capital Limited (formerly known as Aditya Birla Financial Services Limited) (“ABCL”), a subsidiary of ABNL.

The Scheme was approved by the National Company Law Tribunal bench at Ahmedabad on June 1, 2017. ABNL has been amalgamated with Grasim with effect from July 1, 2017 and accordingly, Grasim became the holding Company of ABCL. Consequently, the ultimate Holding Company of your Company has been changed from ABNL to Grasim with effect from July 1, 2017.

Further, in accordance with the Scheme of arrangement, the demerger of the Demerged Undertaking (‘the financial services business’) from the Demerged Company (“Grasim Industries Limited”) and subsequent transfer to the Resulting Company (“Aditya Birla Capital Limited”) (formerly known as Aditya Birla Financial Services Limited) comes into effect.

Aditya Birla Sun Life Insurance Company Limited (formerly known as Birla Sun Life Insurance Company Limited) continues to be the holding Company. Your Company does not have any subsidiary Company, joint venture or associate.

Risk Management FrameworkThe Company has put in place a Risk Management Policy (‘Policy’), which provides a base for the overall risk management framework of the Company. The Policy is reviewed by the Risk Management Committee and the Board of Directors on an Annual basis. A detailed Risk Management policy is attached as Annexure 1 to this report

Contracts and Arrangements with Related Party TransactionsThe Board has formulated and adopted a Related Party Transactions Policy (Policy) for the purpose of identification, monitoring and reporting of such transactions. The RPT Policy is available

Board’s Report

4

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

on the Company’s website at www.pensionfund.adityabirlacapital.com.

All Related Party Transactions (RPT) entered into by your Company during the FY18 were on arm’s length basis and in the ordinary course of business under the Related Party Transaction Policy framework. The particulars of such transactions with the related parties are reported by your Company in the prescribed form AOC 2 and annexed as Annexure 2. The details of all related party transactions also form part of the Annual Accounts.

Internal Financial ControlsThe Company has in place adequate internal financial controls with reference to financial statements.

Internal Audit Framework The Company has in place an adequate internal audit framework to monitor the efficacy of internal controls with the objective of providing to the Audit Committee and the Board of Directors, an independent, objective and reasonable assurance on the adequacy and effectiveness of the organization’s risk management, control and governance processes.

The framework is commensurate with the nature of the business and the size of its operations. Internal auditing at the Company involves the utilization of a systematic methodology for analyzing business processes or organizational problems and recommending solutions to add value and improve the organization’s operations.

The audit approach verifies compliance with the regulatory, operational and system related procedures and controls.

Directors’ Responsibility Statement Pursuant to Section 134(5) of the Companies Act 2013, the Directors, to the best of their knowledge and belief confirm that:

i) in the preparation of the annual accounts for the year ended March 31, 2018, the applicable accounting standards have been followed along with proper explanation relating to material departures;

ii) the Directors have selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the Company at the end of the financial year and of the profit and loss of the Company for that period;

iii) the Directors have taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of Companies Act, 2013 preventing and detecting fraud and other irregularities;

iv) the Directors have prepared the annual accounts on a going concern basis;

v) the Directors have devised proper systems to ensure compliance with the provisions of all applicable laws and that such systems were adequate and operating effectively.

Directors & Key Managerial Personnel Changes in composition of the Board Appointment of DirectorsAs on March 31, 2018, your Board of Directors comprises of 5 (Five) Directors, wherein there are 2 (two) Non-Executive Directors and 3 (three) Independent Directors.

Mr. Harish Engineer (DIN 01843009), Mr. Subhash Bhargava (DIN 00020021), Mr. Vijay Agarwal (DIN 00058548) were appointed as an Independent Directors on the Board of the Company for a period of 5 years with effect from August 14, 2015.

Resignation of DirectorsDuring the year under review, Mr. Ajay Srinivasan, Director on the Board has resigned from the Directorship of the Company w.e.f. 16th June, 2017. The Board places on record its sincere appreciation for the valuable guidance and contribution made by Mr. Ajay Srinivasan in the deliberations of the Board during their tenure on the Board of the Company.

Retirement by RotationFurther, the Independent Directors will not be liable to retire by rotation and therefore shall not be counted for determining the number of Directors liable to retire by rotation.

In accordance with the provisions of the Companies Act, 2013, Mr. Sandeep Ashthana (DIN:00401858), Director, is liable to retire by rotation at the forthcoming Annual General Meeting of the Company, and being eligible, offer himself for re-appointment.

Declaration by Independent DirectorThe Company has received requisite disclosures and undertakings from all the Directors in compliance with the provisions of the Companies Act, 2013. The Independent Directors have given the declaration and confirmed that they met the criteria of Independence as provided under Section 149(6) of the Companies Act, 2013.

Board’s Report

5

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

Key Managerial PersonnelPursuant to section 203 of the Companies Act, 2013, the following employees were holding the position of Key Managerial Personnel (‘KMP’)• Mr. SashiKrishnan (Chief ExecutiveOfficer

and Chief Investment Officer)• Ms. Sandhya Upadhyay (Chief Financial

Officer)• Mr. Asha Kadam (Company Secretary)

(Resigned w.e.f 31st Aug 2017)• Mr. HardikChauhan (Company Secretary)

(Appointed w.e.f 24th October, 2017)

Managerial Remuneration Remuneration (sitting fees) paid to Independent Directors and Elements of remuneration package (including incentives) of MD & CEO and Key Management Persons are disclosed in form MGT 9 and annexed as Annexure 3 which forms part of this Annual Report

Annual Performance EvaluationA formal evaluation mechanism has been adopted for evaluating the performance of the Board, Committees thereof, individual directors and the Chairman of the Board. The evaluation is based on criteria, which include, among others, providing strategic perspective, chairmanship of Board and Committees, attendance and preparedness for the meetings, contribution at meetings, effective decision making ability and role of the Committees.Pursuant to Companies Act, 2013, the annual performance evaluation of the Board, the Directors (Independent and others) individually, as well as applicable Committees of the Board were carried out for FY18. The outcome of the said performance evaluation was placed at the Board Meeting held on 24th April 24, 2018. The Committees and the Board as a whole are functioning very effectively.

Meetings of the BoardBoard The Board meets at regular intervals to discuss and decide on the Company’s policies and strategy. During the year under review, the Board of Directors met 5 (Five) times. The Meetings were held on

1. April 25, 2017

2. July 20, 2017

3. August, 09, 2017

4. October, 24, 2017

5. January, 23, 2018

The attendance of the Directors at the above Board meetings was as under:

Sr. No.

Name of the Directors

Number of Meetings

Attendance in the last

AGM dated June 15,

2017

Held: 5 Held : 1

Attended Attended

1 Mr. Ajay Srinivasan1 1 1

2 Mr. Pankaj Razdan 2 1

3 Mr. Sandeep Asthana 4 1

4 Mr. Subhash Chandra Bhargava

5 -

5 Mr. Harish Hansubhai Engineer

5 -

6 Mr. Vijay Gopal Krishna Agarwal

5 -

1. Resigned w.e.f. 16th June, 2017

Audit CommitteeThe Board has duly constituted an Audit Committee. The Company has a qualified and independent Audit Committee, and its composition is in line with the applicable provisions of Section 177 of the Companies Act, 2013. The Meetings were held on

1. April 25, 2017

2. July 20, 2017

3. August, 09, 2017

4. October, 24, 2017

5. January, 23, 2018The attendance of the Directors at the above Audit Committee meetings was as under:

Sr. No.

Name of the Directors

Designation/ Category

Number of Meetings

Held: 5

Attended

1 Mr. Ajay Srinivasan1 Non-Executive Director

1

2 Mr. Pankaj Razdan Non-Executive Director

1

3 Mr.Subhash Chandra Bhargava

Independent Director

5

4 Mr. Harish Hansubhai Engineer

Independent Director

5

1. Resigned w.e.f. 16th June, 2017

Board’s Report

6

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Nomination and Remuneration CommitteeThe Board has duly constituted a Nomination and Remuneration Committee consisting of following members

Mr. Harish Engineer (Independent Director)

Mr. Vijay Agarwal (Independent Director)

Mr. Sandeep Asthana (Non-Executive Director)

Mr. Pankaj Razdan (Non-Executive Director)

During the year one Meeting was held on August 10, 2017

The Executive Remuneration Phi losophy/ Policy of the Company is annexed herewith as Annexure 4.

Investment CommitteeThe Investment Committee is set up in line with the provisions of PFRDA (Pension Fund) Regulation, 2015.

The Meetings were held on

1. July 20, 2017

2. October, 24, 2017

3. January, 23, 2018

The attendance of the Directors at the above Investment Committee meetings was as under:

Sr. No.

Name of the Directors

Designation/ Category

Number of Meetings

Held: 3

Attended

1 Mr. Sandeep Asthana Non-Executive Director

3

2 Mr. Pankaj Razdan Non-Executive Director

1

3 Mr. Sashi Krishnan Chief Executive Officer

3

4 Mr. Niles Bharkhada1 Senior Manager Investments

1

1. Appointed w.e.f. November 6, 2017.

Risk Management CommitteeThe Risk Management Committee is set up in line with the provisions of PFRDA (Pension Fund) Regulation, 2015.

The Meetings were held on

1. July 20, 2017

2. October, 24, 2017

3. January, 23, 2018

The attendance of the Directors at the above Risk Management Committee meetings was as under:

Sr. No.

Name of the Directors

Designation/ Category

Number of Meetings

Held: 3

Attended

1 Mr. Harish Engineer Independent Director

3

2 Mr. Pankaj Razdan Non-Executive Director

1

3 Mr. Sashi Krishnan Chief Executive Officer

3

4 Mr. Niles Bharkhada1 Senior Manager Investments

1

5 Mr. Hardik Chauhan2 Company Secretary & Compliance Officer

1

1. Appointed w.e.f. November 6, 2017.2. Appointed w.e.f. October 24, 2017.

Corporate Social Responsibility The provisions relating to the constitution of the Corporate Social Responsibility (CSR) are not applicable to your Company.

Extract of Annual Return In accordance with the provisions of Section 134 (3) (a) of the Companies Act, 2013, the extract of the Annual Return for the financial year ended March 31, 2018 in form MGT 9 made under the provisions of 92(3) of the Act form part of the Board’s Report as Annexure 3

AuditorsStatutory Auditors, their Report and Notes to Financial StatementsPursuant to the provisions of Section 139 of the Act and the rules framed there under, M/s. Sharp & Tannan (Firm Registration no. 109982W), Chartered Accountants, were appointed as the statutory auditors of the Company from the conclusion of the First Annual General Meeting (AGM) of the Company till the conclusion of the Sixth AGM of the Company, subject to ratification of their appointment at every AGM. Accordingly, the Board of Directors recommends to the shareholders, the ratification of M/s. Sharp & Tannan, Chartered Accountants, as the Statutory Auditors of the Company.

Board’s Report

7

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

The observations, if any, made by the Statutory Auditors of the Company in their report read with relevant notes to the Accounts are self-explanatory and, therefore do not call for any further comments.

Secretarial Audit In terms of Section 204 of the Companies Act, 2013 and Rules made there under, Secretarial Audit is not applicable to your Company.

Internal Auditor Pursuant to the provision of the PFRDA (Appointment of Internal Auditor) Guidance Note – 2013 M/s. M. P. Chitale & Co., Chartered Accountants were appointed as Internal Auditor of the Company.

Whistle Blower Policy The Company has implemented a Whistle Blower Policy providing a mechanism to report any suspected or confirmed incident of fraud/misconduct through any of the determined reporting protocols. The Whistle Blower Policy also lay down the procedure for handling the complaint and the reporting method. During the year under review, there were no cases reported under this policy.

Policy on prevention of Sexual Harassment at WorkplaceYour Directors further state that during the year under review, there were no cases filed pursuant to the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013.

Human Resources Your Company believes that human resources will play a critical role in its future growth. With an unswerving focus on nurturing and retaining talent, your Company provides avenues for learning and development through functional, behavioral and leadership training programs, knowledge exchange conferences and providing communication channels for information sharing, to name a few of the initiatives.

Secretarial Standards of ICSIPursuant to the approval by the Central Government to the Secretarial Standards specified by the Institute of Company Secretaries of India on

10th April, 2015, the Secretarial Standards on Meetings of the Board of Directors (SS-1) and General Meetings (SS-2) came into effect from 1 July 2015. Thereafter, Secretarial Standards were revised. The Company is in compliance with the revised Secretarial Standards.

Other Disclosures :Your Directors state that no disclosure or reporting is required in respect of the following items as these items were not applicable during the year under review:1. Issue of shares (including sweat equity shares)

to employees of the Company under any scheme.

2. Issue of shares with differential rights.3. Provision of money for the purchase of its own

shares by employees or by trustees for the benefit of employees.

4. Report on fraud by the Auditors to the Audit Committee or the Board of Directors

5. Statement containing salient features of financial statements of subsidiaries

AcknowledgementsYour Directors thank Pension Fund and Regulatory Development Authority of India (PFRDA), National Pension Trust, other regulatory/government authorities, Bankers, Shareholders and all others for their support during the year and look forward to their continued support in the years ahead.

By order of the Board of Directors for Aditya Birla Sun Life Pension

Management Limited(formerly known as Birla Sun Life Pension

Management Limited) Pankaj Razdan Sandeep Ashthana Director Director (DIN – 00061240) (DIN – 00401858) Mumbai, April 24, 2018

Board’s Report

8

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

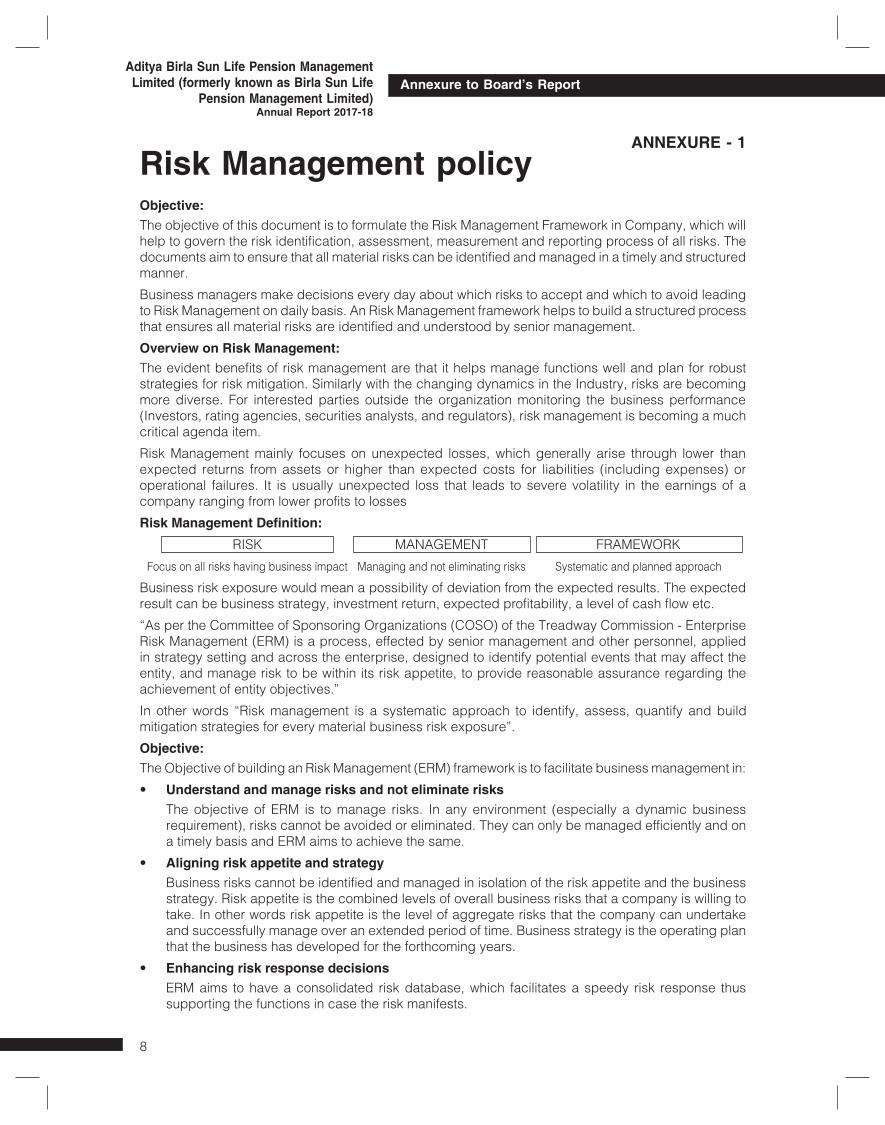

Objective:The objective of this document is to formulate the Risk Management Framework in Company, which will help to govern the risk identification, assessment, measurement and reporting process of all risks. The documents aim to ensure that all material risks can be identified and managed in a timely and structured manner.

Business managers make decisions every day about which risks to accept and which to avoid leading to Risk Management on daily basis. An Risk Management framework helps to build a structured process that ensures all material risks are identified and understood by senior management.

Overview on Risk Management:The evident benefits of risk management are that it helps manage functions well and plan for robust strategies for risk mitigation. Similarly with the changing dynamics in the Industry, risks are becoming more diverse. For interested parties outside the organization monitoring the business performance (Investors, rating agencies, securities analysts, and regulators), risk management is becoming a much critical agenda item.

Risk Management mainly focuses on unexpected losses, which generally arise through lower than expected returns from assets or higher than expected costs for liabilities (including expenses) or operational failures. It is usually unexpected loss that leads to severe volatility in the earnings of a company ranging from lower profits to losses

Risk Management Definition: RISK MANAGEMENT FRAMEWORK

Focus on all risks having business impact Managing and not eliminating risks Systematic and planned approach

Business risk exposure would mean a possibility of deviation from the expected results. The expected result can be business strategy, investment return, expected profitability, a level of cash flow etc.

“As per the Committee of Sponsoring Organizations (COSO) of the Treadway Commission - Enterprise Risk Management (ERM) is a process, effected by senior management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.”

In other words “Risk management is a systematic approach to identify, assess, quantify and build mitigation strategies for every material business risk exposure”.

Objective:The Objective of building an Risk Management (ERM) framework is to facilitate business management in:

• Understand and manage risks and not eliminate risks The objective of ERM is to manage risks. In any environment (especially a dynamic business

requirement), risks cannot be avoided or eliminated. They can only be managed efficiently and on a timely basis and ERM aims to achieve the same.

• Aligning risk appetite and strategy Business risks cannot be identified and managed in isolation of the risk appetite and the business

strategy. Risk appetite is the combined levels of overall business risks that a company is willing to take. In other words risk appetite is the level of aggregate risks that the company can undertake and successfully manage over an extended period of time. Business strategy is the operating plan that the business has developed for the forthcoming years.

• Enhancing risk response decisions ERM aims to have a consolidated risk database, which facilitates a speedy risk response thus

supporting the functions in case the risk manifests.

Risk Management policy

Annexure to Board’s Report

ANNEXURE - 1

9

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

• Reducing operational surprises and losses An effective ERM framework can assist business management to reduce the operational surprises

and losses by framing mitigation strategy for key business risks so that the same can be implemented in a timely and efficient manner

• Seizing new business opportunities ERM facilitates business management to evaluate new opportunities as a risk mitigation technique.

Through ERM, the management can evaluate new business proposal and products. For example, a risk management strategy to diversify business share would be evaluating and carrying research on new products across industry.

• Improving deployment of capital Obtaining robust risk information allows management to effectively assess overall capital needs and

enhance capital allocation.

Benefits of ERM:ERM can support and assist the business management in:

• Improved understanding of risks and their true costs to the organization ERM will provide an overall database of risks, their associated control cost and clarity on the risk

response. By risk measurement and assessment the true cost of the mitigating or avoiding the risks will be pertinent. ERM also ensures the ability to aggregate business unit risks across an enterprise enabling better understanding of risk across functions and business units.

• Enhancing Shareholders and Policyholders value Shareholders and policyholders expect business value and appreciation out of their investments.

ERM helps generate the business value through a management framework governed and assessed by senior management. ERM also helps build investor confidence.

• A company culture enhanced by a greater awareness of risks Senior management drives ERM. Hence the drive on managing business risks and creating a risk

culture efficiently is to be generated by senior management. This top down approach helps develop greater awareness of risk.

• Definition and application of risk appetite ERM helps in defining every risk as well as helps in assessing risk appetite of the company. This way

all senior management is aware and aligned on the overall risk appetite of the company, which helps them in the risk response decision. This approach helps management with informed decision-making.

• Efficient allocation of funds and management resources within the company ERM, through investment risk management ensures efficient allocation of funds for higher profitability.

ERM also provides and objective base for allocating resources.

• Improving capital efficiency and earning stability Risk management improves capital efficiency and costs savings through more effective management

of internal resources and capital as well as providing protection against earnings related surprises. Since the risk management framework focuses on avoiding surprises it also improves the stability of the earning.

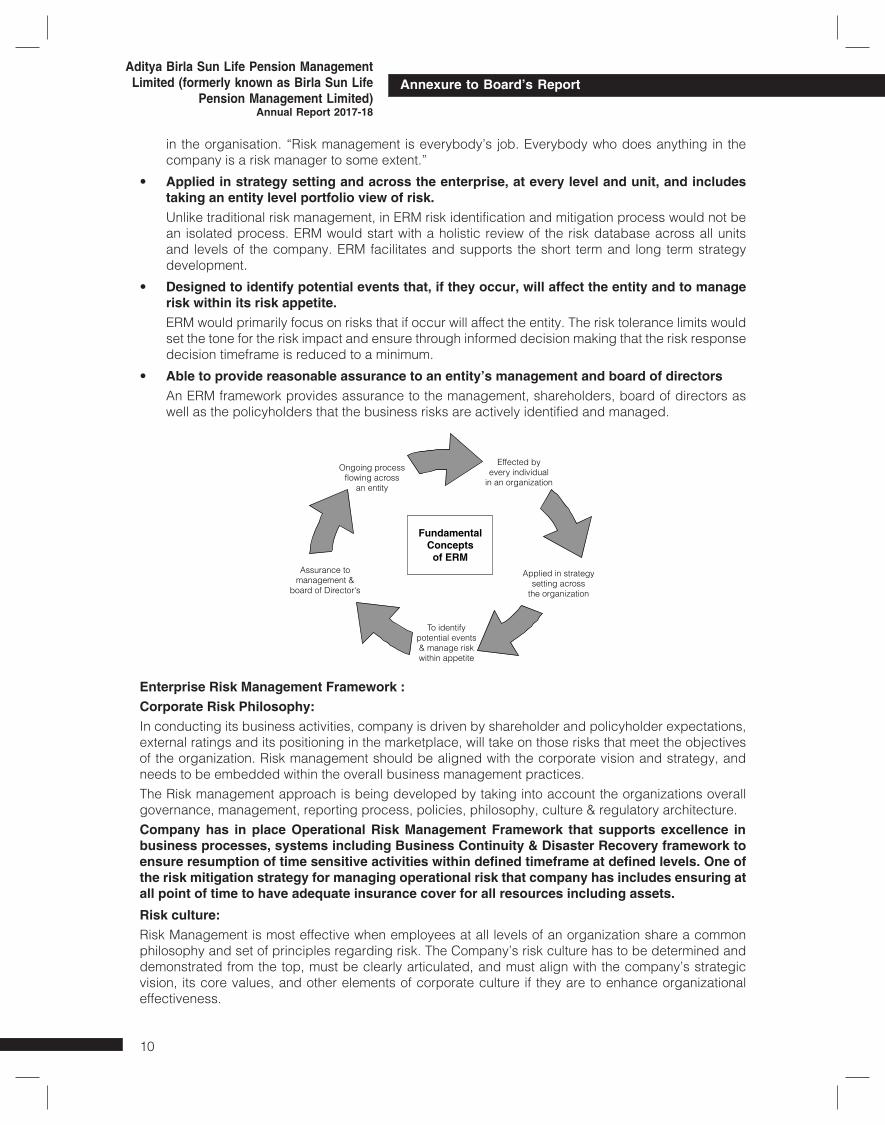

Fundamental concepts of ERM:The fundamental concepts of ERM are as follows:

• A process, ongoing and flowing across an entity. Unlike traditional risk management, ERM is not a one-time activity or a project. ERM is an ongoing

process within the organisation. All the elements especially the risk identification and assessment will have to be an ongoing process to manage the expected and unexpected risks efficiently.

• Effected by people at every level of an organization. ERM is not only a responsibility of the risk management team or senior management. Responsibility

to manage risk and driving the ERM forward is eventually to be effected by people at every level

Annexure to Board’s Report

10

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

in the organisation. “Risk management is everybody’s job. Everybody who does anything in the company is a risk manager to some extent.”

• Applied in strategy setting and across the enterprise, at every level and unit, and includes taking an entity level portfolio view of risk.

Unlike traditional risk management, in ERM risk identification and mitigation process would not be an isolated process. ERM would start with a holistic review of the risk database across all units and levels of the company. ERM facilitates and supports the short term and long term strategy development.

• Designed to identify potential events that, if they occur, will affect the entity and to manage risk within its risk appetite.

ERM would primarily focus on risks that if occur will affect the entity. The risk tolerance limits would set the tone for the risk impact and ensure through informed decision making that the risk response decision timeframe is reduced to a minimum.

• Able to provide reasonable assurance to an entity’s management and board of directors An ERM framework provides assurance to the management, shareholders, board of directors as

well as the policyholders that the business risks are actively identified and managed.

Enterprise Risk Management Framework :Corporate Risk Philosophy:In conducting its business activities, company is driven by shareholder and policyholder expectations, external ratings and its positioning in the marketplace, will take on those risks that meet the objectives of the organization. Risk management should be aligned with the corporate vision and strategy, and needs to be embedded within the overall business management practices.The Risk management approach is being developed by taking into account the organizations overall governance, management, reporting process, policies, philosophy, culture & regulatory architecture.Company has in place Operational Risk Management Framework that supports excellence in business processes, systems including Business Continuity & Disaster Recovery framework to ensure resumption of time sensitive activities within defined timeframe at defined levels. One of the risk mitigation strategy for managing operational risk that company has includes ensuring at all point of time to have adequate insurance cover for all resources including assets.Risk culture:Risk Management is most effective when employees at all levels of an organization share a common philosophy and set of principles regarding risk. The Company’s risk culture has to be determined and demonstrated from the top, must be clearly articulated, and must align with the company’s strategic vision, its core values, and other elements of corporate culture if they are to enhance organizational effectiveness.

Annexure to Board’s Report

11

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

Risk management enhances shareholder value. The company can more effectively compete and win through superior execution of the risk management function throughout all levels of the organization.

To ensure that the company achieves and maintains a strong risk culture, every employee must feel accountable for achieving the best results for his or her business unit and for the company as a whole. Business decisions are made at all levels of the organization, and every employee has a role in identifying exposures, communicating concerns, and escalating risk issues as appropriate.

The following fundamental principles are required in an effective risk management program:

– Acting with Integrity Acting with integrity is one of Company’s core values, and goes hand-in-hand with effective risk

management. This means that we make the right decisions for the right reasons, even when it is difficult to do so or may mean the loss of business.

– Customer Alignment The company accepts risk from and shares risks with customers. This requires that the company

proactively and clearly communicate to customers the nature of the risks that are being shared. It also means that the company must fully understand the risks it has acquired from customers, and understand the value of the management of those risks on behalf of the customer.

– Discipline This requires discipline through the development of sound business practices, attention to established

processes, a clear delineation of accountabilities, and adherence to company policies. Discipline is also achieved through commitment to a strong control environment to forge an appropriate balance between stewardship and entrepreneurship

– Embedding Risk Management Effective risk management requires that risk management be embedded into the business so that

individuals making business decisions do so with full awareness of the risks inherent in the products or activities being managed or considered. In order to make appropriate risk/reward tradeoffs, we must ensure that we have the capability throughout the organization to undertake rigorous, unbiased identification and assessment of risk. Investment must be made in risk management infrastructure to support this effort.

– Promotion of Full and Transparent Communication Effective risk management is a cross-disciplinary exercise involving employees throughout the

organization that relies upon clear channels of communication — up, down and across the organization. Emerging risk issues must be escalated to the appropriate levels of senior management. Transparency in our risk management program requires that we are able to communicate the risk profile of the organization to our stakeholders.

– Collaboration Collaboration creates value – that the whole is greater than the sum of its parts – and strives to share

and leverage our tools, processes and experience across the organization.

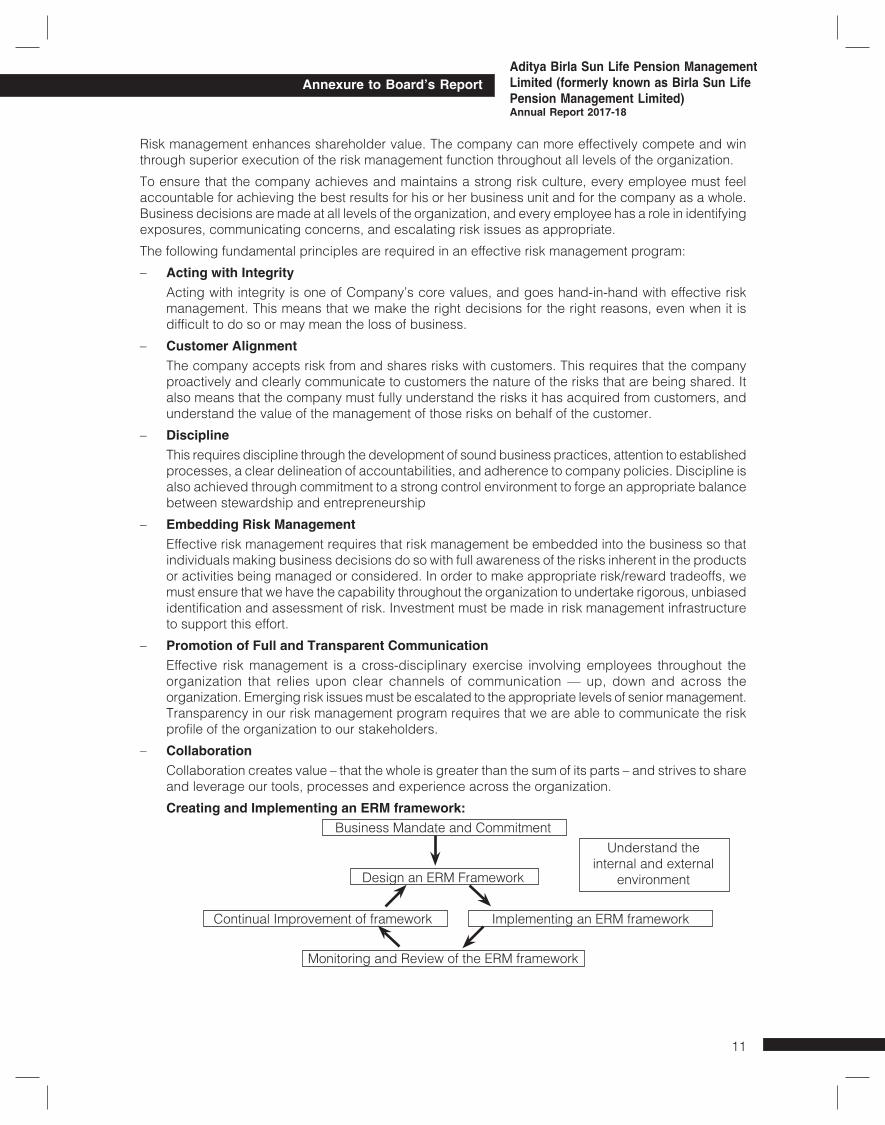

Creating and Implementing an ERM framework:Business Mandate and Commitment

Design an ERM Framework

Monitoring and Review of the ERM framework

Annexure to Board’s Report

Understand the internal and external

environment

Implementing an ERM frameworkContinual Improvement of framework

12

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Mandate and Commitment:Management should:

- Articulate and endorse the risk management policy

- Communicate the benefit of risk management to all stakeholders

- Ensure that necessary resources are allocated to risk management

Designing an ERM Framework:- Understand the organization and its environment

- Clear the framework objectives

- Integrate into organizational processes

- Specify accountability and resources

- Establish internal/external communication and reporting mechanisms.

Implementing an ERM Framework:- Developing a plan for implementation

- Implementing the framework (phased approach mentioned below)

Monitoring and review of the framework:- Periodically measure progress against risk management plan

- Continuous review of the framework

- Review effectiveness of risk management process.

Continual Improvement of framework- Based on the review of the framework, the framework should be updated to make the organizational

risk management process more robust.

Roles and responsibilities in an ERM framework:Everyone in an entity has responsibility towards risk management.

– The Chief Executive Officer is ultimately responsible and would assume ownership for an effective risk management framework.

– Leadership team members and Functional Heads usually have key support responsibilities in managing the overall ERM framework by guiding the risk management team in carrying out the ERM framework.

– The Risk management team is responsible to support the management in implementing the overall ERM framework.

– Functional managers support the entity’s risk management philosophy, promote compliance with its risk appetite, and manage risks within their spheres of responsibility consistent with risk appetite.

– Other entity personnel are responsible for executing enterprise risk management in accordance with established directives and protocols.

– The Risk Management Committee provides important oversight to enterprise risk management, and is aware of and concurs with the entity’s risk appetite. The Risk Management Committee composition and charter has been separately listed.

– A number of external parties, such as customers, vendors, business partners, external auditors, regulators, and financial analysts often provide information useful in effecting enterprise risk management, but they are not responsible for the effectiveness of, nor are they a part of, the entity’s enterprise risk management.

– Internal Audit will review the risk management practices within the department on a regular basis and report as appropriate on issues arising from these reviews.

– All employees will actively support and contribute to risk management initiatives and maintain an awareness of risks (current and potential) that relate to their area of responsibility

Annexure to Board’s Report

13

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

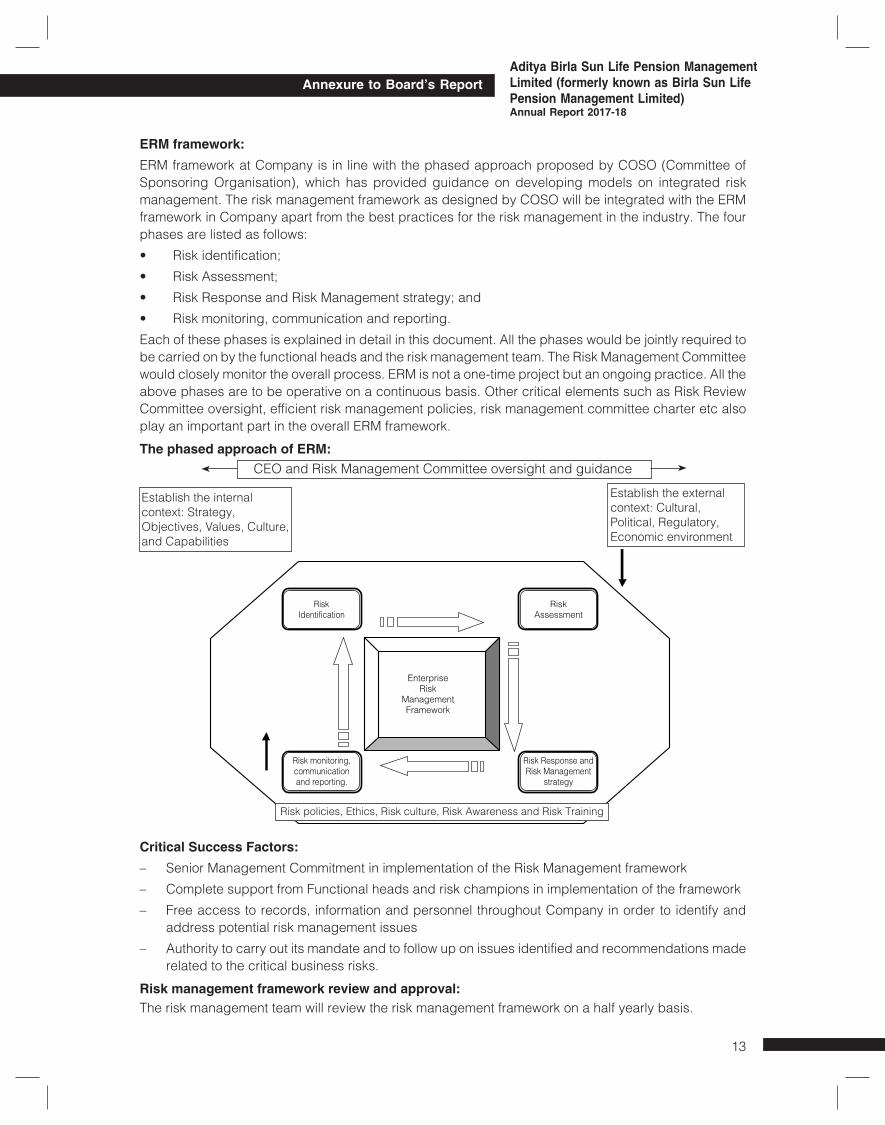

ERM framework:ERM framework at Company is in line with the phased approach proposed by COSO (Committee of Sponsoring Organisation), which has provided guidance on developing models on integrated risk management. The risk management framework as designed by COSO will be integrated with the ERM framework in Company apart from the best practices for the risk management in the industry. The four phases are listed as follows:

• Riskidentification;

• RiskAssessment;

• RiskResponseandRiskManagementstrategy;and

• Riskmonitoring,communicationandreporting.

Each of these phases is explained in detail in this document. All the phases would be jointly required to be carried on by the functional heads and the risk management team. The Risk Management Committee would closely monitor the overall process. ERM is not a one-time project but an ongoing practice. All the above phases are to be operative on a continuous basis. Other critical elements such as Risk Review Committee oversight, efficient risk management policies, risk management committee charter etc also play an important part in the overall ERM framework.

The phased approach of ERM:CEO and Risk Management Committee oversight and guidance

Critical Success Factors:– Senior Management Commitment in implementation of the Risk Management framework

– Complete support from Functional heads and risk champions in implementation of the framework

– Free access to records, information and personnel throughout Company in order to identify and address potential risk management issues

– Authority to carry out its mandate and to follow up on issues identified and recommendations made related to the critical business risks.

Risk management framework review and approval:The risk management team will review the risk management framework on a half yearly basis.

Annexure to Board’s Report

Establish the internal context: Strategy, Objectives, Values, Culture, and Capabilities

Establish the external context: Cultural, Political, Regulatory, Economic environment

Risk policies, Ethics, Risk culture, Risk Awareness and Risk Training

14

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Annexure A: Enterprise Risk Management framework – Process and Procedures:Risk Management frameworkThe Company has an Enterprise Risk Management (ERM) framework covering procedures to identify, assess and mitigate the key business risks. Aligned with the business planning process, the ERM framework covers all business risks including reputation risk, operational risks, regulatory risks, insurance risks, people risks and market risks.

Below are key points of framework:• RiskManagementteamconductsanexerciseannuallyforidentificationofkeybusinessrisksand

relevant mitigation strategies• ThefunctionalRSCAsandtheinternalauditreportswillalsogoverntheriskframeworkforCompany.• Identifiedriskswouldbesuitablycategorized• IdentificationofKeyRiskParametersandKeyRiskDrivers• KeyriskmetricswouldthenbepresentedtotheRiskManagementCommittee• RiskManagementwillseekperiodicalstatusupdatesforallTopbusinessrisksasidentifiedandreview

the risk metric as well.• ThekeyriskupdateswillbequarterlyupdatedtotheRiskManagementCommittee

Annexure B: Risk Category DefinitionIn order to facilitate discussions and identification of risks and exposures, the matrix of risk categories have been developed. Utilization of common risk categories and an understanding of the sources and consequences of risk events will allow for consistency in reporting, facilitation of aggregation and contribute to the enterprise risk management framework.

In addition, we need to understand all of the potential aspects of risks, which will help in risk assessment. In order to provide a framework for that understanding, we have developed a matrix of risk categorization, which is structured as follows:

• Risks Drivers In order to manage risk effectively, risks need to be specifically defined so that appropriate action

plans can be developed. This section provides further breakdown of risks within the main categories.

• Source This column identifies the key activities, which create an exposure to the company within the specific

risk categories.

• Exposure Triggers Exposure triggers are the actual events that need to occur before a risk manifests itself into a situation

that requires specific management actions and impacts the organization.

• Direct Consequences Consequences are both financial and non-financial impacts to the organization as a result of a risk

event.

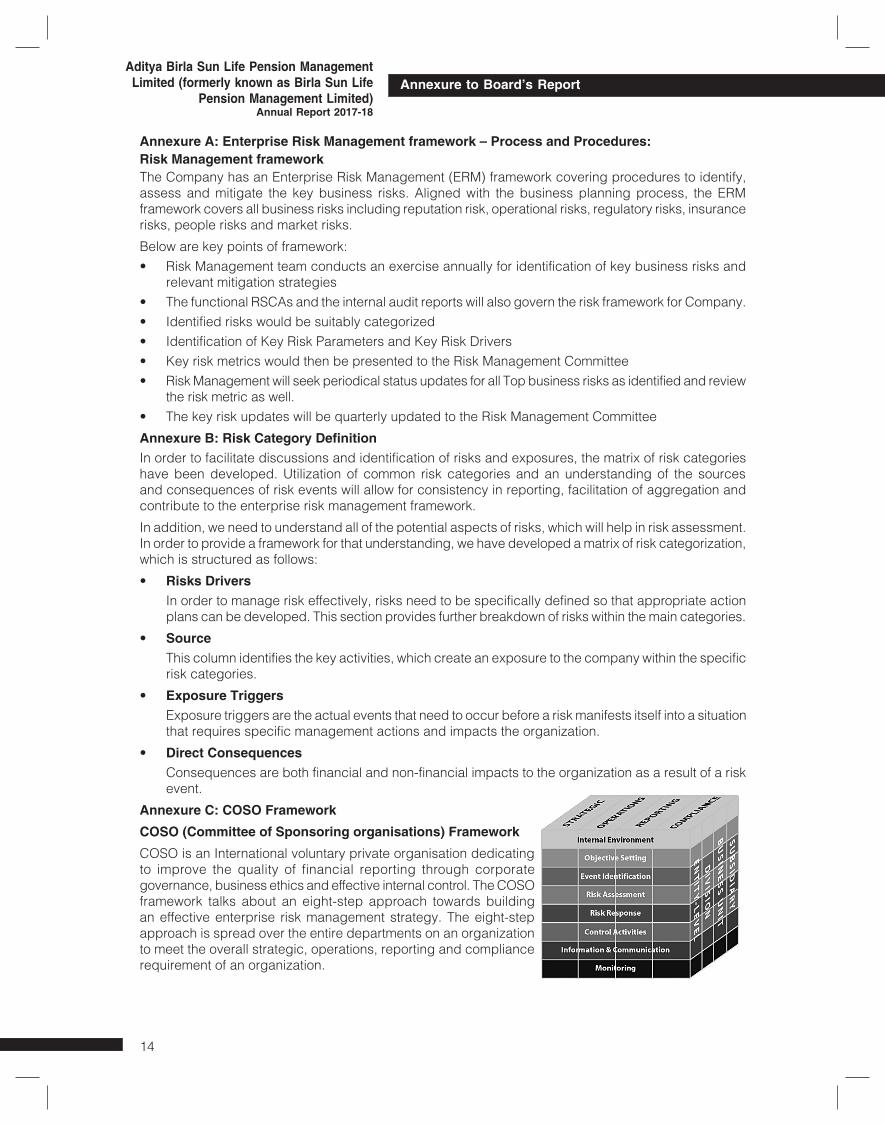

Annexure C: COSO FrameworkCOSO (Committee of Sponsoring organisations) FrameworkCOSO is an International voluntary private organisation dedicating to improve the quality of financial reporting through corporate governance, business ethics and effective internal control. The COSO framework talks about an eight-step approach towards building an effective enterprise risk management strategy. The eight-step approach is spread over the entire departments on an organization to meet the overall strategic, operations, reporting and compliance requirement of an organization.

Annexure to Board’s Report

15

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

ANNEXURE - 2FORM NO. AOC -2

(Pursuant to clause (h) of sub-section (3) of section 134 of the Act and Rule 8(2) of the Companies (Accounts) Rules, 2014.

Form for Disclosure of particulars of contracts/arrangements entered into by the company with related parties referred to in sub section (1) of section 188 of the Companies Act, 2013 including certain arms length transaction under third proviso thereto.1. Details of contracts or arrangements or transactions not at Arm’s length basis. - NIL

SL. No. Particulars Details

1. Name (s) of the related party & nature of relationship

2. Nature of contracts/arrangements/transaction

3. Duration of the contracts/arrangements/transaction

4. Salient terms of the contracts or arrangements or transaction including the value, if any

5. Justification for entering into such contracts or arrangements or transactions’

6. Date of approval by the Board

7. Amount paid as advances, if any

8. Date on which the special resolution was passed in General meeting as required under first proviso to section 188

2. Details of contracts or arrangements or transactions at Arm’s length basis.

SL. No. Particulars Details

1. Name (s) of the related party & nature of relationship

Aditya Birla Sun Life Insurance Company Limited (formerly known as Birla Sun Life Insurance Company Ltd.) – Holding Company

2. Nature of contracts/arrangements/transaction i) Reimbursement salary paid to Employees on secondment

ii) Workstation usage

3. Duration of the contracts/arrangements/transaction

i) 15 month

4. Salient terms of the contracts or arrangements or transaction including the value, if any

Entire expenses incurred by the Holding Company will be reimbursed to ABSPML

5. Date of approval by the Board N.A.

6. Amount paid as advances, if any Nil

By order of the Board of Directorsfor Aditya Birla Sun Life Pension Management Company Limited (formerly known as Birla Sun Life Pension Management Limited)

Pankaj Razdan Sandeep Asthana Director DirectorMumbai, April 24, 2018 (DIN – 00061240) (DIN – 00401858)

Annexure to Board’s Report

16

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

ANNEXURE - 3FORM NO. MGT 9

EXTRACT OF ANNUAL RETURNas on financial year ended on 31.03.2018Pursuant to Section 92 (3) of the Companies Act, 2013 and rule

12(1) of the Company (Management & Administration) Rules, 2014.

1 REGISTRATION & OTHER DETAILS:

CIN U66000MH2015PLC260801

Registration Date January 9, 2015

Name of the Company Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)

Category/Sub-category of the Company Public limited with share capital

Address of the Registered office & One Indiabulls Centre, Tower-1, 16th floor, Jupiter contact details Mill Compound, 841, S.B. Marg, Elphinstone Road, Mumbai 400 013. Telephone No. 022 67239100

Whether listed company No

Name, Address & contact details of the Registrar & Transfer Agent, if any. NA

2 PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY

All the business activities contributing 10% or more of the total turnover of the company shall be stated

Name and Descriptionof main NIC Code of the % to total turnover products /services Product/ service of the company

Management of Pension Funds 66302 The Company is yet to commence the business operations.

3 PARTICULARS OF HOLDING , SUBSIDIARY & ASSOCIATE COMPANIES

Name and Address of the Company CIN/GLN Holding/ % of Shares Applicable Subsidiary/ Held Section Associate

Aditya Birla Sun Life Insurance U99999MH2000PLC128110 Holding 100% 2(46) Company Limited (formerly known as Birla Sun Life Insurance Company Limited) One Indiabulls Centre, Tower-1, 16th floor, Jupiter Mill Compound, 841, S.B. Marg, Elphinstone Road, Mumbai 400 013

Annexure to Board’s Report

17

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

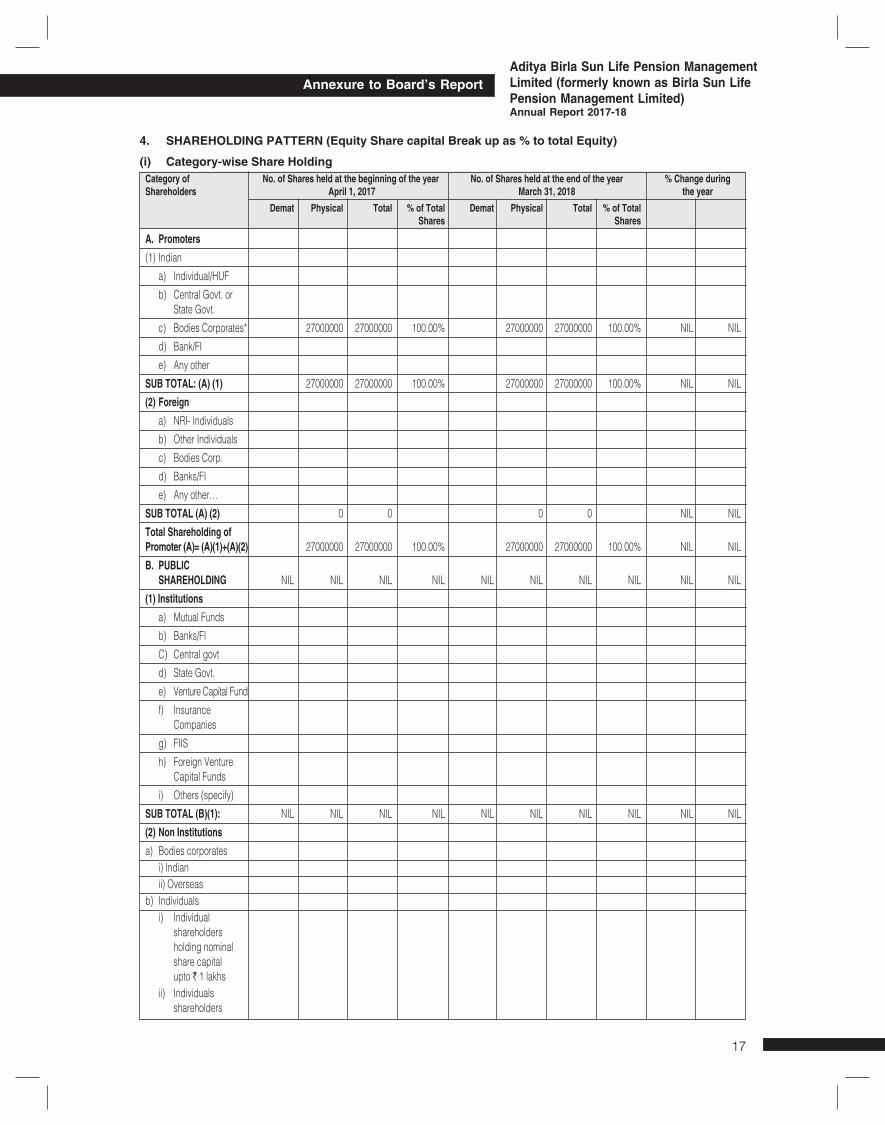

4. SHAREHOLDING PATTERN (Equity Share capital Break up as % to total Equity)

(i) Category-wise Share HoldingCategory of No. of Shares held at the beginning of the year No. of Shares held at the end of the year % Change during Shareholders April 1, 2017 March 31, 2018 the year Demat Physical Total % of Total Demat Physical Total % of Total Shares Shares

A. Promoters(1) Indian

a) Individual/HUF

b) Central Govt. or State Govt.

c) Bodies Corporates* 27000000 27000000 100.00% 27000000 27000000 100.00% NIL NIL

d) Bank/FI

e) Any other

SUB TOTAL: (A) (1) 27000000 27000000 100.00% 27000000 27000000 100.00% NIL NIL

(2) Foreign a) NRI- Individuals

b) Other Individuals

c) Bodies Corp.

d) Banks/FI

e) Any other…

SUB TOTAL (A) (2) 0 0 0 0 NIL NIL

Total Shareholding of Promoter (A)= (A)(1)+(A)(2) 27000000 27000000 100.00% 27000000 27000000 100.00% NIL NIL

B. PUBLIC SHAREHOLDING NIL NIL NIL NIL NIL NIL NIL NIL NIL NIL

(1) Institutions a) Mutual Funds

b) Banks/FI

C) Central govt

d) State Govt.

e) Venture Capital Fund

f) Insurance Companies

g) FIIS

h) Foreign Venture Capital Funds

i) Others (specify)

SUB TOTAL (B)(1): NIL NIL NIL NIL NIL NIL NIL NIL NIL NIL

(2) Non Institutionsa) Bodies corporates i) Indian ii) Overseasb) Individuals i) Individual shareholders holding nominal share capital upto ` 1 lakhs ii) Individuals shareholders

Annexure to Board’s Report

18

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

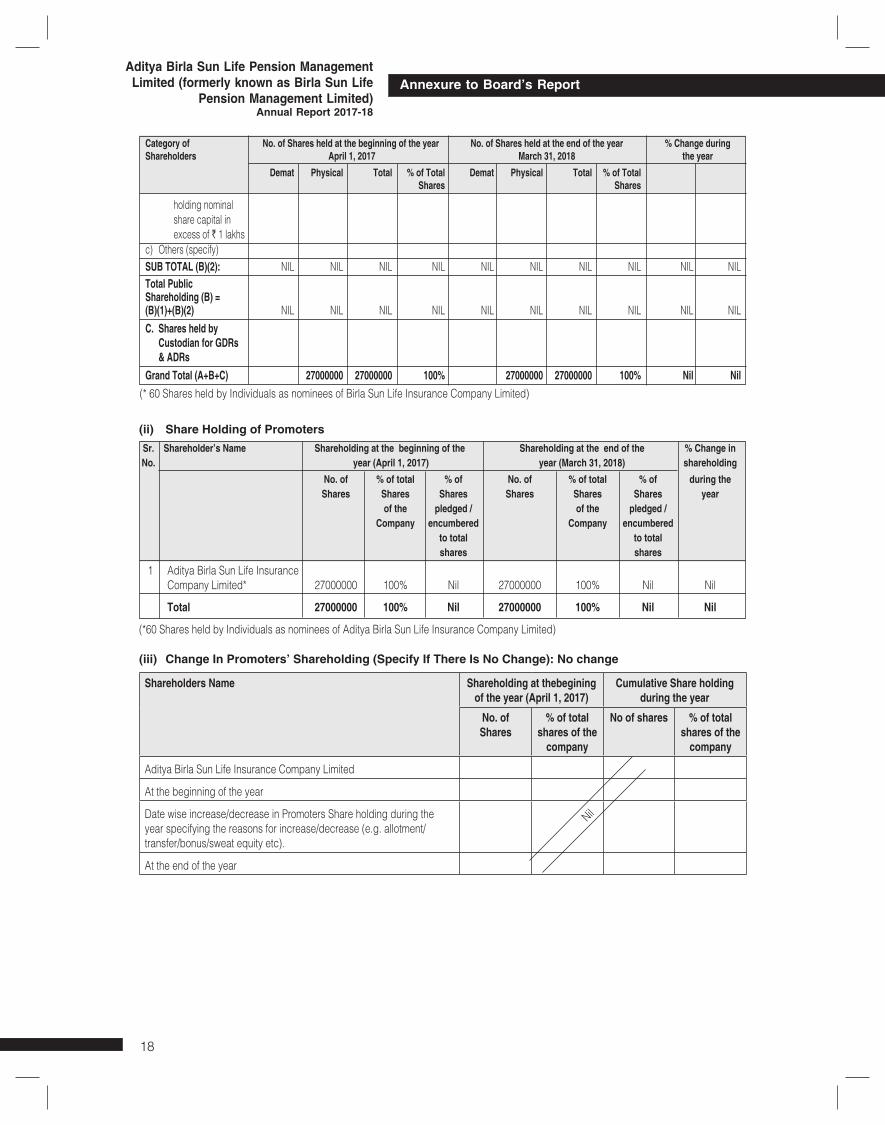

Category of No. of Shares held at the beginning of the year No. of Shares held at the end of the year % Change during Shareholders April 1, 2017 March 31, 2018 the year Demat Physical Total % of Total Demat Physical Total % of Total Shares Shares

holding nominal share capital in excess of ` 1 lakhsc) Others (specify)SUB TOTAL (B)(2): NIL NIL NIL NIL NIL NIL NIL NIL NIL NILTotal Public Shareholding (B) = (B)(1)+(B)(2) NIL NIL NIL NIL NIL NIL NIL NIL NIL NIL

C. Shares held by Custodian for GDRs & ADRsGrand Total (A+B+C) 27000000 27000000 100% 27000000 27000000 100% Nil Nil

(* 60 Shares held by Individuals as nominees of Birla Sun Life Insurance Company Limited)

(ii) Share Holding of Promoters Sr. Shareholder’s Name Shareholding at the beginning of the Shareholding at the end of the % Change in No. year (April 1, 2017) year (March 31, 2018) shareholding No. of % of total % of No. of % of total % of during the Shares Shares Shares Shares Shares Shares year of the pledged / of the pledged / Company encumbered Company encumbered to total to total shares shares

1 Aditya Birla Sun Life Insurance Company Limited* 27000000 100% Nil 27000000 100% Nil Nil

Total 27000000 100% Nil 27000000 100% Nil Nil

(*60 Shares held by Individuals as nominees of Aditya Birla Sun Life Insurance Company Limited)

(iii) Change In Promoters’ Shareholding (Specify If There Is No Change): No change

Shareholders Name Shareholding at thebegining of the year (April 1, 2017)

Cumulative Share holding during the year

No. of Shares

% of total shares of the

company

No of shares % of total shares of the

company

Aditya Birla Sun Life Insurance Company Limited

At the beginning of the year

Date wise increase/decrease in Promoters Share holding during the year specifying the reasons for increase/decrease (e.g. allotment/transfer/bonus/sweat equity etc).

At the end of the year

Nil

Annexure to Board’s Report

19

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

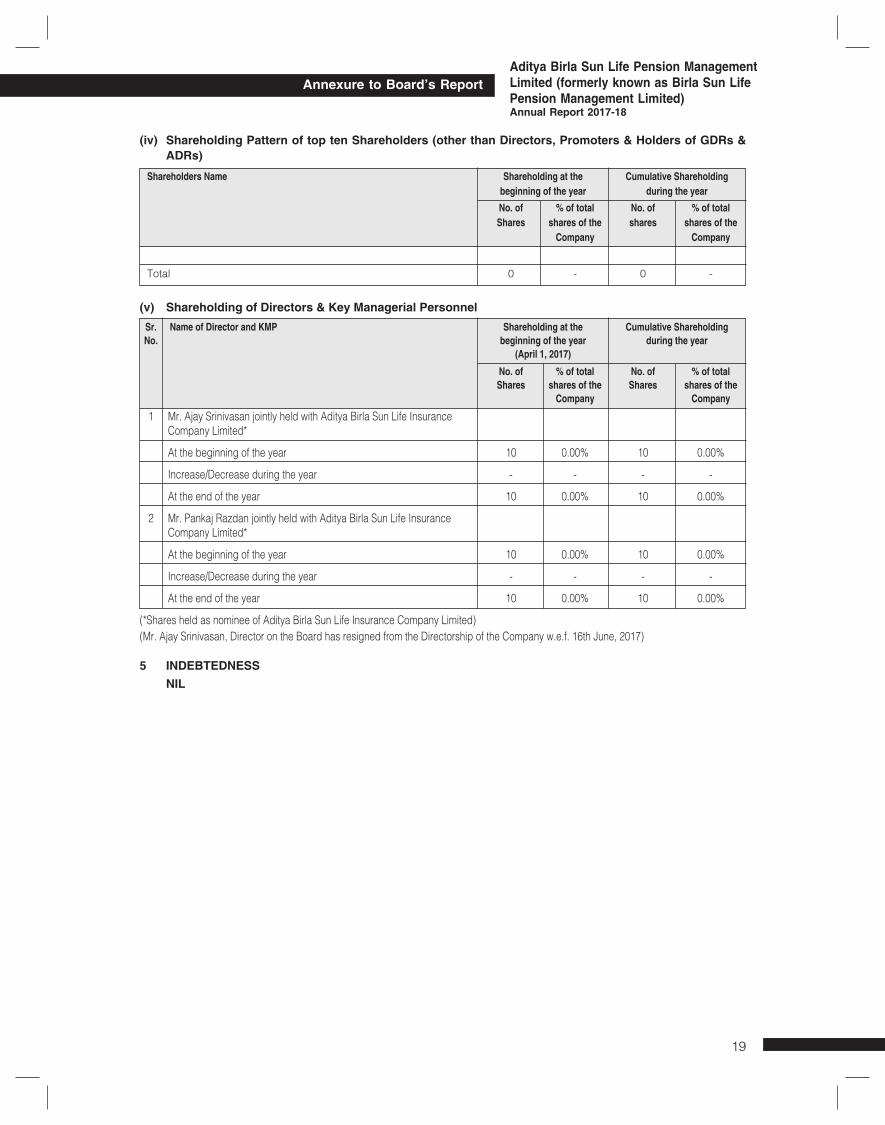

(iv) Shareholding Pattern of top ten Shareholders (other than Directors, Promoters & Holders of GDRs & ADRs)

Shareholders Name Shareholding at the Cumulative Shareholding beginning of the year during the year No. of % of total No. of % of total Shares shares of the shares shares of the Company Company

Total 0 - 0 -

(v) Shareholding of Directors & Key Managerial Personnel Sr. Name of Director and KMP Shareholding at the Cumulative Shareholding No. beginning of the year during the year (April 1, 2017) No. of % of total No. of % of total Shares shares of the Shares shares of the Company Company

1 Mr. Ajay Srinivasan jointly held with Aditya Birla Sun Life Insurance Company Limited*

At the beginning of the year 10 0.00% 10 0.00%

Increase/Decrease during the year - - - -

At the end of the year 10 0.00% 10 0.00%

2 Mr. Pankaj Razdan jointly held with Aditya Birla Sun Life Insurance Company Limited*

At the beginning of the year 10 0.00% 10 0.00%

Increase/Decrease during the year - - - -

At the end of the year 10 0.00% 10 0.00%

(*Shares held as nominee of Aditya Birla Sun Life Insurance Company Limited)(Mr. Ajay Srinivasan, Director on the Board has resigned from the Directorship of the Company w.e.f. 16th June, 2017)

5 INDEBTEDNESS NIL

Annexure to Board’s Report

20

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

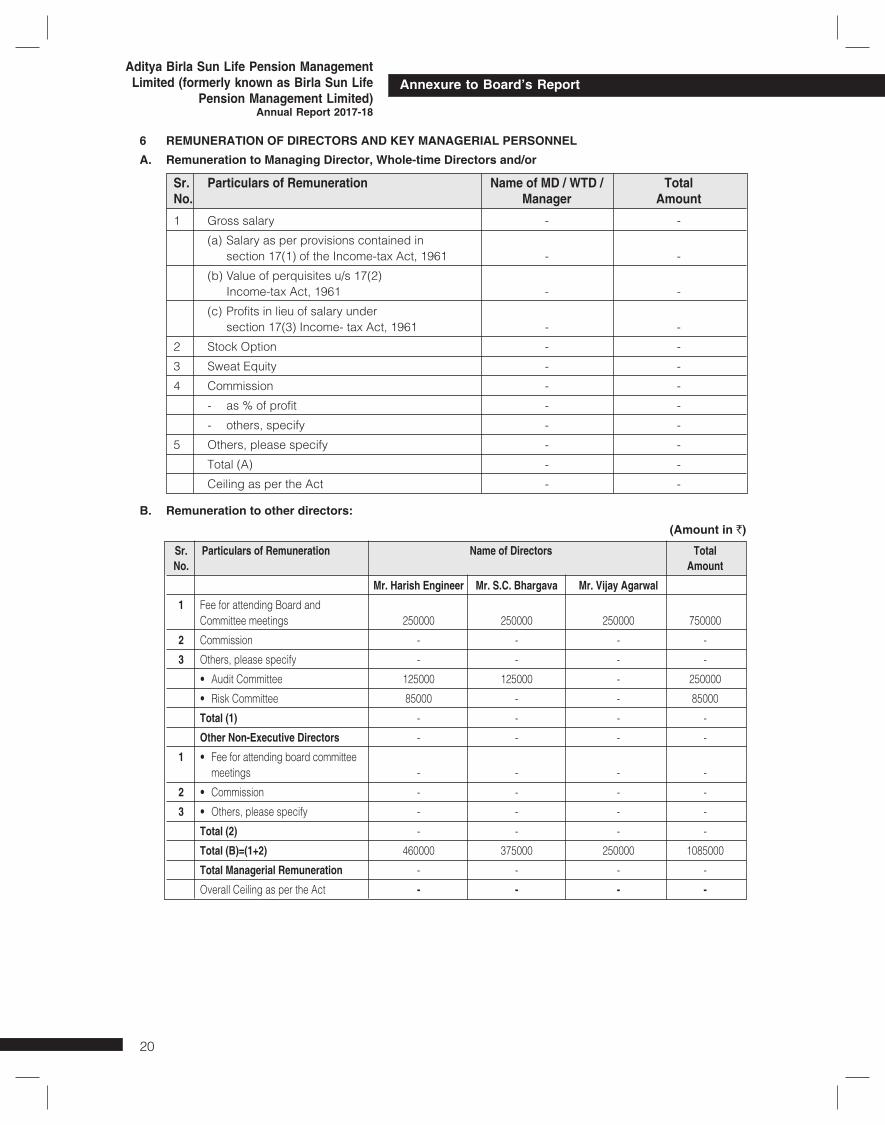

6 REMUNERATION OF DIRECTORS AND KEY MANAGERIAL PERSONNELA. Remuneration to Managing Director, Whole-time Directors and/or

Sr. Particulars of Remuneration Name of MD / WTD / Total No. Manager Amount 1 Gross salary - -

(a) Salary as per provisions contained in section 17(1) of the Income-tax Act, 1961 - -

(b) Value of perquisites u/s 17(2) Income-tax Act, 1961 - -

(c) Profits in lieu of salary under section 17(3) Income- tax Act, 1961 - -

2 Stock Option - -

3 Sweat Equity - -

4 Commission - -

- as % of profit - -

- others, specify - -

5 Others, please specify - -

Total (A) - -

Ceiling as per the Act - -

B. Remuneration to other directors:(Amount in `)

Sr. Particulars of Remuneration Name of Directors Total No. Amount Mr. Harish Engineer Mr. S.C. Bhargava Mr. Vijay Agarwal 1 Fee for attending Board and Committee meetings 250000 250000 250000 750000

2 Commission - - - -

3 Others, please specify - - - -

•AuditCommittee 125000 125000 - 250000

•RiskCommittee 85000 - - 85000

Total (1) - - - -

Other Non-Executive Directors - - - -

1 • Feeforattendingboardcommittee meetings - - - -

2 • Commission - - - -

3 • Others,pleasespecify - - - -

Total (2) - - - -

Total (B)=(1+2) 460000 375000 250000 1085000

Total Managerial Remuneration - - - -

Overall Ceiling as per the Act - - - -

Annexure to Board’s Report

21

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

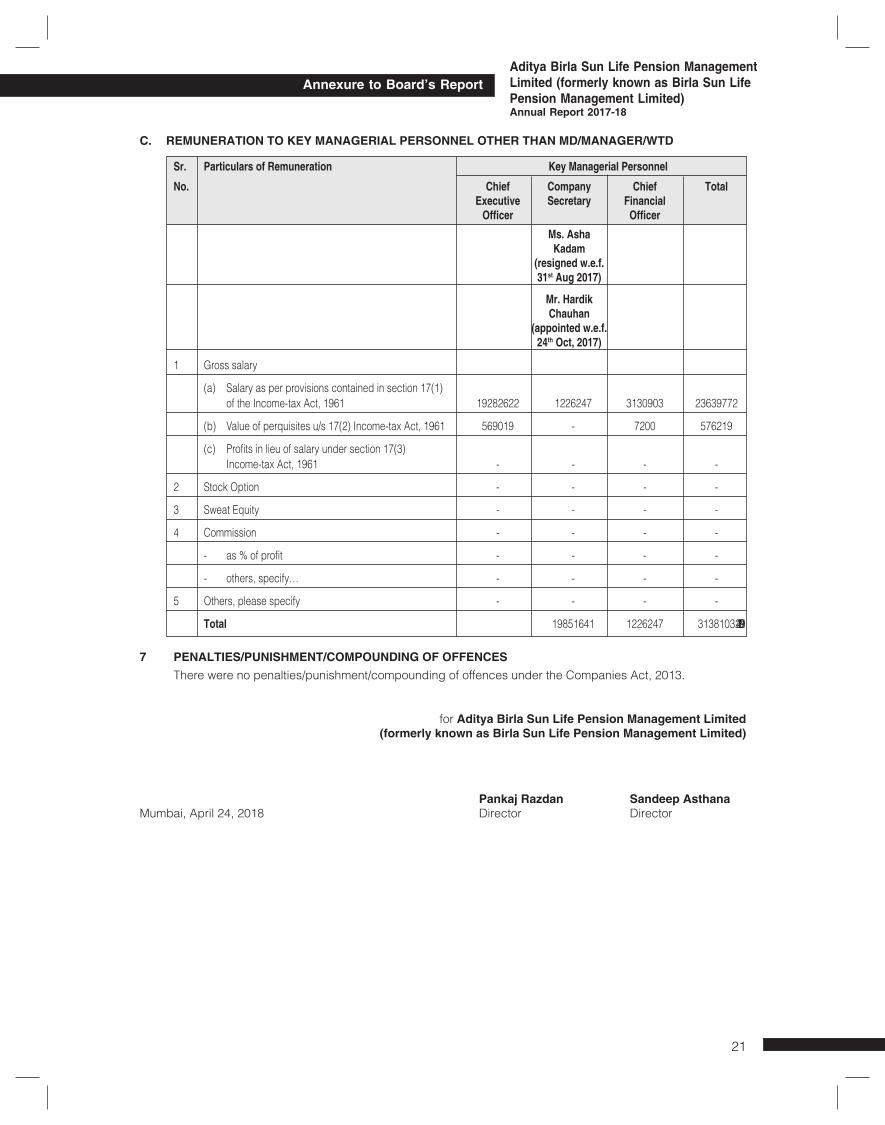

C. REMUNERATION TO KEY MANAGERIAL PERSONNEL OTHER THAN MD/MANAGER/WTD

Sr. Particulars of Remuneration Key Managerial Personnel

No. Chief Company Chief Total Executive Secretary Financial Officer Officer Ms. Asha Kadam (resigned w.e.f. 31st Aug 2017)

Mr. Hardik Chauhan (appointed w.e.f. 24th Oct, 2017)

1 Gross salary

(a) Salary as per provisions contained in section 17(1) of the Income-tax Act, 1961 19282622 1226247 3130903 23639772

(b) Value of perquisites u/s 17(2) Income-tax Act, 1961 569019 - 7200 576219

(c) Profits in lieu of salary under section 17(3) Income-tax Act, 1961 - - - -

2 Stock Option - - - -

3 Sweat Equity - - - -

4 Commission - - - -

- as % of profit - - - -

- others, specify… - - - -

5 Others, please specify - - - -

Total 19851641 1226247 3138103 24215991

7 PENALTIES/PUNISHMENT/COMPOUNDING OF OFFENCES There were no penalties/punishment/compounding of offences under the Companies Act, 2013.

for Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)

Pankaj Razdan Sandeep AsthanaMumbai, April 24, 2018 Director Director

Annexure to Board’s Report

22

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Aditya Birla Sun Life Pension Management Limited, (“the Company’), an Aditya Birla Group Company adopts/shall adopt this Executive Remuneration Philosophy/Policy as applicable across Group Companies. This philosophy/ policy is detailed below. Aditya Birla Group: Executive Remuneration Philosophy/Policy At the Aditya Birla Group, we expect our executive team to foster a culture of growth and entrepreneurial risk-taking. Our Executive Remuneration Philosophy/Policy supports the design of programs that align executive rewards – including incentive programs, retirement benefit programs, promotion and advancement opportunities – with the long-term success of our stakeholders. Our business and organizational modelOur Group is a conglomerate and organized in a manner such that there is sharing of resources and infrastructure. This results in uniformity of business processes and systems thereby promoting synergies and exemplary customer experiences.I. Objectives of the Executive Remuneration Program Our executive remuneration program is designed to attract, retain, and reward talented executives

who will contribute to our long-term success and thereby build value for our shareholders. Our executive remuneration program is intended to: 1. Provide for monetary and non-monetary remuneration elements to our executives on a holistic

basis 2. Emphasize “Pay for Performance” by aligning incentives with business strategies to reward

executives who achieve or exceed Group, business and individual goals.II. Covered Executives Our Executive Remuneration Philosophy/Policy applies to the following: 1. Directors of the Company: 2. Key Managerial Personnel: Chief Executive Officer and equivalent (eg: Deputy Managing

Director), Chief Financial Officer and Company Secretary. 3. Senior Management: III. Business and Talent Competitors We benchmark our executive pay practices and levels against peer companies in similar industries,

geographies and of similar size. In addition, we look at secondary reference (internal and external) benchmarks in order to ensure that pay policies and levels across the Group are broadly equitable and support the Group’s global mobility objectives for executive talent. Secondary reference points bring to the table, the executive pay practices and pay levels in other markets and industries, to appreciate the differences in levels and medium of pay and build in as appropriate for decision making.

IV. Executive Pay Positioning We aim to provide competitive remuneration opportunities to our executives by positioning target

total remuneration (including perks and benefits, annual incentive pay-outs, long term incentive pay-outs at target performance) and target total cash compensation (including annual incentive pay-outs) at target performance directionally between median and top quartile of the primary talent market. We recognize the size and scope of the role and the market standing, skills and experience of incumbents while positioning our executives.

We use secondary market data only as a reference point for determining the types and amount of remuneration while principally believing that target total remuneration packages should reflect the typical cost of comparable executive talent available in the sector.

V. Executive Pay-Mix Our executive pay-mix aims to strike the appropriate balance between key components: (i) Fixed

Cash compensation (Basic Salary + Allowances) (ii) Annual Incentive Plan (iii) Long-Term Incentives (iv)Perks and Benefits

ANNEXURE - 4Executive Remuneration policy

Annexure to Board’s Report

23

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

Annual Incentive Plan: We tie annual incentive plan pay-outs of our executives to relevant financial and operational metrics

achievement and their individual performance. We annually align the financial and operational metrics with priorities/ focus areas for the business.

Long-Term Incentive: Our Long-term incentive plans incentivize stretch performance, link executive remuneration to

sustained long term growth and act as a retention and reward tool. We use stock optionsas the primary long-term incentive vehicles for our executives as we believe

that they best align executive incentives with stockholder interests. We grant restricted stock units as a secondary long term incentive vehicles, to motivate and retain

our executives.VI. Performance Goal Setting We aim to ensure that for both annual incentive plans and long term incentive plans, the target

performance goals shall be achievable and realistic. Threshold performance (the point at which incentive plans are paid out at their minimum, but non-

zero, level) shall reflect a base-line level of performance, reflecting an estimated 90% probability of achievement.

Target performance is the expected level of performance at the beginning of the performance cycle, taking into account all known relevant facts likely to impact measured performance.

Maximum performance (the point at which the maximum plan payout is made) shall be based on an exceptional level of achievement, reflecting no more than an estimated 10% probability of achievement.

VII. Executive Benefits and Perquisites Our executives are eligible to participate in our broad-based retirement, health and welfare,

and other employee benefit plans. In addition to these broad-based plans, they are eligible for perquisites and benefits plans commensurate with their roles. These benefits are designed to encourage long-term careers with the Group.

Other Remuneration ElementsEach of our executives is subject to an employment agreement. Each such agreement generally provides for a total remuneration package for our executives including continuity of service across the Group Companies. We limit other remuneration elements, for e.g. Change in Control (CIC) agreements, severance agreements, to instances of compelling business need or competitive rationale and generally do not provide for any tax gross-ups for our executives.Risk and ComplianceWe aim to ensure that the Group’s remuneration programs do not encourage excessive risk taking. We review our remuneration programs for factors such as,remuneration mix overly weighted towards annual incentives, uncapped pay-outs, unreasonable goals or thresholds, steep pay-out cliffs at certain performance levels that may encourage short-term decisions to meet pay-out thresholds.Claw back Clause:In an incident of restatement of financial statements, due to fraud or non-compliance with any requirement of the Companies Act 2013 and the rules made thereafter, we shall recover from our executives, the remuneration received in excess, of what would be payable to him / her as per restatement of financial statements,pertaining to the relevant performance year. ImplementationThe Group and Business Centre of Expertise teams will assist the Nomination & Remuneration Committee in adopting, interpreting and implementing the Executive Remuneration Philosophy/Policy. These services will be established through “arm’s length”, agreements entered into as needs arise in the normal course of business.

Annexure to Board’s Report

24

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

Independent Auditor’s ReportTo the members of Aditya Birla Sun Life Pension Management Limited

Report on the Financial Statements

We have audited the accompanying financial statements of Aditya Birla Sun Life Pension Management Limited (‘the Company’), which comprise the Balance Sheet as at 31st March, 2018 , the Statement of Profit and Loss, the Cash Flow Statement for the year then ended, and a summary of the significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

The Company’s Board of Directors is responsible for the matters stated in Section 134(5) of the Companies Act, 2013 (“the Act”) with respect to the preparation of these financial statements that give a true and fair view of the financial position, financial performance and cash flows of the Company in accordance with the accounting principles generally accepted in India, including the Accounting Standards specified under Section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules, 2014. This responsibility also includes maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit.

We have taken into account the provisions of the Act, the accounting and auditing standards and matters which are required to be included in the audit report under the provisions of the Act and the Rules made thereunder.

We conducted our audit in accordance with the Standards on Auditing specified under Section 143(10) of the Act. Those Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and the disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal financial control relevant to the Company’s preparation of the financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of the accounting estimates made by the Company’s Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion on the financial statements.

Opinion

In our opinion and to the best of our information and according to the explanations given to us, the aforesaid financial statements give the information required by the Act in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at 31st March, 2018, and its loss and its cash flows for the year ended on that date.

Report on Other Legal and Regulatory Requirements

1. As required by the Companies (Auditors Report) Order, 2016 (“the Order”), issued by the Central Government in terms of sub-section (11) of Section 143 of the Act, we given in Annexure A, a statement on the matters specified in Paragraphs 3 and 4 of the Order.

2. As required by Section 143(3) of the Act, we report that:

Independent Auditor’s Report

25

Notes to Financial StatementsNotes to Financial StatementsAditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life Pension Management Limited)Annual Report 2017-18

a) we have sought and obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit;

b) in our opinion, proper books of account as required by law have been kept by the Company so far as it appears from our examination of those books;

c) the Balance Sheet, the Statement of Profit and Loss, and the Cash Flow Statement dealt with by this Report are in agreement with the books of account;

d) in our opinion, the aforesaid financial statements comply with the Accounting Standards specified under Section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules, 2014;

e) on the basis of the written representations received from the directors as on 31st March, 2018 taken on record by the Board of Directors, none of the directors is disqualified as on 31st March, 2018 from being appointed as a director in terms of Section 164(2) of the Act;

f) with respect to the adequacy of internal financial controls over financial reporting of the Company and the operating effectiveness of such controls, refer to our separate report in Annexure B; and

g) with respect to the other matters to be included in the Auditor’s Report in accordance with Rule 11 of the Companies (Audit and Auditors) Rules, 2014, in our opinion and to the best of our information and according to the explanations given to us:

i. The Company has disclosed the impact of pending litigations on its financial position in its financial statements – Refer Note 18 to the financial statements;

ii. The Company did not have any long-term contracts including derivative contracts for which there were any material foreseeable losses.

iii. There were no amounts which were required to be transferred to the Investor Education and Protection Fund by the Company.

For Sharp & TannanChartered Accountants

Firm’s Registration No. 109982W

Edwin P. AugustinePartner

(Membership No. 043385)

Mumbai, 24th April, 2018

Independent Auditor’s Report

26

Aditya Birla Sun Life Pension Management Limited (formerly known as Birla Sun Life

Pension Management Limited)Annual Report 2017-18

ANNEXURE ‘A’ TO THE INDEPENDENT AUDITOR’S REPORT(Referred to in paragraph 1 of our report of even date)

(i) (a) The Company is maintaining proper records showing full particulars, including quantitative details of fixed assets. However the identification number are yet to be updated.

(b) As explained to us, the Company has physically verified all its fixed assets during the year. No material discrepancies were noticed on such verification.

(c) According to the information and explanations given to us, and the records of the Company examined by us, the Company does not hold any immoveable property.

(ii) Since the Company is engaged in service activity, it does not hold any inventory and accordingly Paragraph 3(ii) of the Order is not applicable to the Company.